oil india investor presentation – h1 fy2010€¦ · oil india investor presentation – h1 fy2010...

TRANSCRIPT

OIL INDIA LIMITED

Investor Presentation

November 2009

Oil India Investor Presentation – H1 FY2010

2

Disclaimer

This presentation contains certain forward looking statements concerning OIL India’s future business prospects and business

profitability, which are subject to a number of risks and uncertainties and the actual results could materially differ from those in

such forward looking statements. The risks and uncertainties relating to these statements include, but not limited to, risks and

uncertainties, regarding fluctuations in earnings, our ability to manage growth, competition (both domestic and international),

economic growth in India, ability to attract and retain highly skilled professionals, time and cost over runs on projects, our ability to

manage our international operations, government policies and actions with respect to investments, fiscal deficits, regulations, etc.,

interest and other fiscal costs generally prevailing in the economy. The company does not undertake to make any announcement

in case any of these forward looking statements become materially incorrect in future or update any forward looking statements

made from time to time by or on behalf of the company.

Oil India Investor Presentation – H1 FY2009Oil India Investor Presentation – H1 FY2010

Sector outlook and opportunities

OIL India – An overview

Business structure, performance and strategy

Financial performance

Oil India Investor Presentation – H1 FY2009Oil India Investor Presentation – H1 FY2010

Sector outlook and opportunities

OIL India – An overview

Business structure, performance and strategy

Financial performance

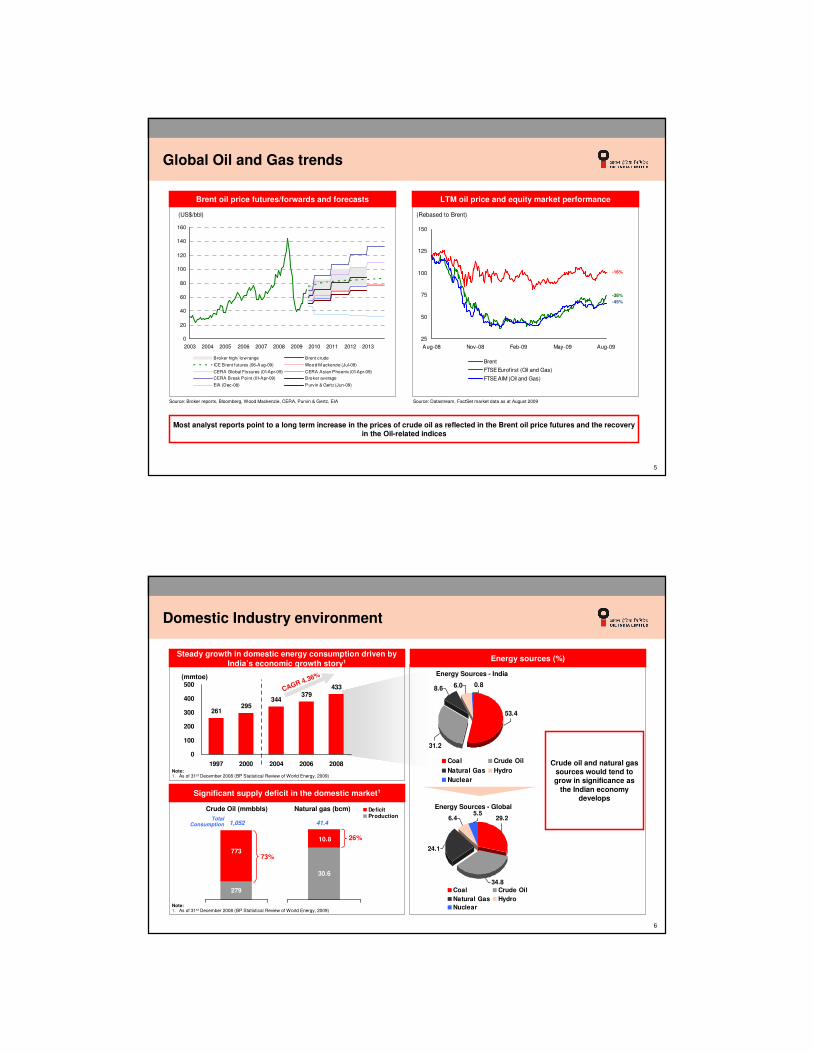

5

Global Oil and Gas trends

Source: Broker reports, Bloomberg, Wood Mackenzie, CERA, Purvin & Gertz, EIA

(Rebased to Brent)

25

50

75

100

125

150

Aug-08 Nov-08 Feb-09 May-09 Aug-09

Brent

FTSE Eurof irst (Oil and Gas)

FTSE AIM (Oil and Gas)

-16%

-45%

-38%

(US$/bbl)

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Broker high/ low range Brent crude

ICE Brent futures (06-Aug-09) Wood M ackenzie (Jul-09)

CERA Global Fissures (01-Apr-09) CERA Asian Phoenix (01-Apr-09)

CERA Break Point (01-Apr-09) Broker average

EIA (Dec-08) Purvin & Gertz (Jun-09)

Source: Datastream, FactSet market data as at August 2009

Most analyst reports point to a long term increase in the prices of crude oil as reflected in the Brent oil price futures and the recovery in the Oil-related indices

Brent oil price futures/forwards and forecasts LTM oil price and equity market performance

6

31.2

0.8

53.4

8.6 6.0

Coal Crude Oil

Natural Gas Hydro

Nuclear

CAGR 4.36%

Note:1. As of 31st December 2008 (BP Statistical Review of World Energy, 2009)

279

773

1,052

73%

30.6

10.8

41.4

26%

Crude Oil (mmbbls) Natural gas (bcm) DeficitProduction

TotalConsumption

Note:1. As of 31st December 2008 (BP Statistical Review of World Energy, 2009)

(mmtoe) Energy Sources - India

Domestic Industry environment

Steady growth in domestic energy consumption driven by India’s economic growth story1

261295

344379

433

0

100

200

300

400

500

1997 2000 2004 2006 2008

Significant supply deficit in the domestic market1

34.8

5.529.2

24.1

6.4

Coal Crude Oil

Natural Gas Hydro

Nuclear

Energy Sources - Global

Energy sources (%)

Crude oil and natural gas sources would tend to grow in significance as

the Indian economy develops

7

India: Energy scenario

Primary Energy Consumption (MTOE) Crude Oil Consumption (MTOE)

• 53% of primary energy consumed by 5 countries• India is the 5th largest consumer of Primary Energy

− India CAGR (1998-2008): 4.8% vs. Global CAGR: 2.4%

• World oil consumption (2008): 3,928 MTOE• India is the 4th largest consumer of Oil comprising 3.4% of total

− India CAGR (1998-2008): 3.9% vs. Global CAGR: 1.3%

Note: (1) Annualized crude oil production rate of 26.24 mmboe in Q2 FY2010(2) Annualized crude oil delivery rate of 26.90 mmboe in Q2 FY2010

Note: (1) 1 BCM of Natural Gas = 6.2898 MMBOE

2,299

2,003

685

508

330

311

258

240

212

433

0 500 1,000 1,500 2,000 2,500

USA

China

Russia

Japan

India

Canada

Germany

France

South Korea

UK

3.8% of total 3.4% of total

885

376

222

118

103

102

135

130

0 200 400 600 800 1,000

USA

China

Japan

India

Russia

Germany

S. Korea

Canada

8

OIL at a glance

India’s premier Oil & Gas company engaged in the exploration, development, production and transportation of crude oil and natural gas in India

Professionally managed company with experienced management with a proven track recordManagement

ICRA has assigned an A1+ (A one plus) rating to Rs. 5 billion short-term debt programme of OIL

indicating highest safetyCredit rating

Revenue: USD 1,677 m (FY09) and USD 929 m (1H2010)PAT : USD 460m (FY 09) and USD 301m (1H2010)Market cap : USD 5,852 mn2

Size

A corporate citizen committed towards corporate social responsibility, environment protection, implementation of safety measures & conservation of natural resources

Est. independent proved plus probable crude oil reserves: 575 mmboe

Est. independent proved plus probable natural gas reserves: 399 mmboeReserves

Domestic acreage: 117,6221 square kilometers; International acreage: 41,273 square kilometersAcreage

Note:1. Excluding blocks provisionally awarded in NELP VIII2. As of 29rd October 2009

Oil India Investor Presentation – H1 FY2009Oil India Investor Presentation – H1 FY2010

Sector outlook and opportunities

OIL India – An overview

Business structure, performance and strategy

Financial performance

10

Rich heritage of building a company

• Independent India’s first commercial oil discoveries were made

by Assam Oil Company

– Nahorkatiya, Assam – 1953

– Moran, Assam – 1956

• Incorporated as Joint Sector Company on 18 February, 1959

– 2/3rd Owned by Assam Oil Company / Burmah Oil Company

– 1/3rd Owned by Government of India

• Became a Public Sector Undertaking, GOI on 14 October, 1981

• Five decades of experience in Exploration & Production

• Second largest national oil and gas company in India

• Achieved overwhelming response in its maiden public issue on

30 September 2009

11

Select highlights for H1 FY2010

OIL’s shares listed on September 2009 at a 8% premium to its issue price on the NSE and

continues to trade above issue price

Highest ever crude oil production at 3.58 mtpa - a 2.2 % increase over Q2, 2008-09

Highest ever crude oil delivery at 3.67 mtpa - a 3.9 % increase over Q2, 2008-09

1 hydrocarbon discovery in August, 2009 in Well, Umatara -1 in Barail formation adjacent

to Sapkaint structure in Dibrugarh district in Q2

Achieved a cumulative increase in drilling activity upto 1H FY2010 by over 24%

Drilling commenced in Libya on 31st October,2009

OIL as Operator spuds the first well, LOC: AMG-1, in NELP-VI Block: AA-ONN-2004/1,

Amguri, under NEF Project on 25th October'2009

12

Shareholding pattern

78.4%

2.4%3.2%

4.0%

11.6%

0.3%

Promoters (GOI) Bodies Corporate

Public & Others FII

MF FI / Banks

2.23%Hindustan Petroleum Corporation

1.35%ICICI Prudential Life Insurance

0.41%SBI Life Insurance

2.23%Bharat Petroleum Corporation

0.27%HDFC Standard Life Insurance

0.34%Prudential India Equity (FII)

4.45%Indian Oil Corporation

% ShareholdingKey shareholders

• Listing: Listed on the BSE and NSE on 30th Sept 2009

• Number of shares outstanding: 240.45 mn

• Dividend: FY09 dividend per share of Rs. 305

• Share price as on 29th Oct 2009: Rs. 1,132 (NSE/BSE)

Oil India Investor Presentation – H1 FY2009Oil India Investor Presentation – H1 FY2010

Sector outlook and opportunities

OIL India – An overview

Business structure, performance and strategy

Financial performance

14

Key lines of business

• Domestic: 23 exploration blocks through NELP1

• International: Egypt, Gabon, Iran, Libya, Nigeria, Timor Leste and Yemen2

• Reserves (2P): Total reserves – est. 974 mmboe; Crude Oil – est. 575 mmboe3; Natural Gas – est. 399 mmboe4

• Discoveries: 11 Small to Medium5 size discoveries from Fiscal 2007 to Fiscal 2009 and three-month period ending 30th June 2009

• Refining and marketing petroleum products: 26% equity stake in NRL1

• Gas cracker project: 10% equity stake in BCPL2

• Acquiring, transporting and distributing natural gas -23% equity stake in DNPL3

• City gas business - Signed MOU with GAIL, IOCL and BPCL

• 50 years of experience in Oil & Gas production

• Crude oil: 40 installations and est. 1,315 km of internal crude oil pipelines grid; H1 FY10 production of 13.1 mmboe

• Natural gas: 29 installations and est. 571 km of internal gas network pipelines grid; H1 FY10 production of 7.6 mmboe

• Advanced Recovery Techniques - Artificial Lifting, Enhanced Oil Recovery and horizontal drilling

Exploration DownstreamProduction Transportation

• Crude Oil: 1,157 km crude oil pipeline with an annual capacity of over 44 mn barrels

• Multi-Product: 660 km pipeline from NRL1 to Siliguriwith an estimated capacity of 2.13 million kiloliters of refined petroleum products

• Overseas pipeline: 10% equity stake in a 741 km pipeline in Sudan

• Natural Gas: 23% stake in the 192 km DNPL3, which proposes to lay a 192 km pipeline project to transport natural gas from Duliajan to Numaligarh

Note:1. NRL – Numaligarh Refinery Limited2. BCPL – Brahmaputra Cracker and Polymer

Limited3. DNPL – Duliajan-Numaligarh Pipeline Limited

Note:1. 27 blocks acquired in 7 rounds of NELP and 4 relinquished. 9 blocks have been provisionally awarded under NELP VIII.2. Participating interests in exploration and development blocks3. Oil Reserves exclude participatory interest in Kharsang; Based on our unaudited independent proved plus probable crude oil reserves as of 31st March 2009; Include

certain reserves attributable to condensate from non-associated gas reservoirs4. Based on our unaudited independent proved plus probable natural gas reserves as of 31st March 2009; Includes certain reserves attributable to fuel gas consumption5. Small to Medium size discoveries: Estimated proved plus probable reserves size of less than 30 million barrels of oil and oil equivalent gas6. MMBOE – Million Barrels of Oil Equivalent

15

1,542

1,511

1,471

1,450

1,500

1,550

2007 2008 2009

Reserves Overview (3P)

Total Reserves (mmboe)

1,5421,5111,471Overall (O+OEG)

543472471Natural Gas

9991,0391,000Crude Oil

200920082007Total reserves (mmboe)

Reserv

es CAGR: 2

.4%

Note:1. OEG – Oil Equivalent Gas

16

Note:NO – Non-operatorPI – Participatory Interests1. Includes a 40% PI in the Kharsang fields of area 11 sq. km.

Strong presence in prospective East Coast

RJ-ONN

KG-DWN

KG-DWNMN-DWN

AA-ONN

AA-ONN

AA-ONN

AA-ONN

AA-ONN

AAP-ON

MZ-ONN

KG-DWN

AN-DWN

�

�

�

�

�

�

�

�

AA-ONN

AA-ONN

�

CY-DWN

WB-ONN

RJ-ONN

RJ-ONN

30%

90%

85%

16%

15%

10%

75%

25%

10%

RJ-ONN60%

75%

60%

60%

10%

20%

15%20%

KG-DWN 10%

20%

85%

20%

15%

20%

�KG-ONN 90%

GK-OSJ-3 MN-OSN

Exploration Blocks : National Presence

Total Area – 158,895 Sq. Km

Summary of Acreage (sq. km.)

1

OIL as Operator

NELP I-VII

Nomination ML(s)/PEL(s)

JVC Blocks

�

Map Not to Scale

2

4,811

41,273

82,175

5,368

6,041

19,227

PEL Nomination PML Nomination

JV/PSC (NO) NELP (Operator)

NELP (NO) Overseas (PI)

RJ-ONN� 60%

�

ASSAM +AP

17

3,735

616 460

Assam Arunachal

Pradesh

Rajasthan

4,852

516

Assam Arunachal

Pradesh

15 2 2 11 5

PML Areas 19 4,811 Pre-NELP – JV/PSC (Non Operator) 3 6,041

305

5,725

11

Assam & AP Kutch

Offshore

Kharsang

1 1 1

Operator Blocks (NELP) 11 19,227

899

8,885

275

7,650

1,518

II IV V VI VII

1 1 12 6

Non-Operator Blocks (NELP) 12 82,175

4,970

37,066

110 1,060

22,829

16,140

I II III IV VI VII

1 1 24 1 3

All Onshore 4 Onshore, 1 Offshore & 7 Deepwater

Block category Blocks Area (Sq.km.)

Petro. Mining License (PML) Petro. Exploration License (PEL) JV/Production Sharing Contract (PSC)

Area (Sq.km.)

Blocks

PEL Areas 16 5,368

1

Map Not to Scale

Exploration Acreages

18

NELP VIII: Blocks provisionally awarded

APGIC-10%

NTPC-10%

ONGC-50%

30835Shallow OffshoreKrishna-Godavari BasinONGCKG-OSN-2009/4

GAIL-10%

ONGC-60%304,040Deep WaterAndaman BasinONGCAN-DWN-2009/18

ONGC-60%403,992Deep WaterAndaman BasinONGC & OIL (Joint)

AN-DWN-2009/3

ONGC-60%403,995Deep WaterAndaman BasinONGCAN-DWN-2009/2

ONGC-70%304,981Deep WaterAndaman BasinONGCAN-DWN-2009/1

APGIC-10%

ONGC-45%

BGEPIL-30%

151,800Deep WaterKrishna-Godavari BasinBGEPILKG-DWN-2009/1

ONGC-50%5084OnlandAssamONGCAA-ONN-2009/3

ONGC-50%501,621Shallow OffshoreCauvery BasinOILCY-OSN-2009/2

ONGC-50%5084OnlandAssamOILAA-ONN-2009/4

Consortium Partners (PI)

OIL’sP. I. (%)

Area (sq. km.)TypeAreaOperatorName of the Block

�

�

�

OIL as Operator�

19

Overseas Exploration and Development Blocks

Area – 41,273 sq.km.17 Blocks1

Total

OIL also holds a 10% equity stake in 741 km crude oil pipeline in Sudan

Note:1. Participating Interest in exploration and development blocks

* Government approval is awaited

Operator

Area (Sq. Km)

OIL’s Participating Interest (%)

LIBYAArea 86Area 102/4Area 95/96

GABON Shakti

NIGERIA OPL 205

TIMOR LESTE*Block K

YEMENBlock 82 Block 83

EGYPT*Block 3Block 4

IRAN Farsi Offshore

3,500 20 (OVL)

8,2872,600

25 (GSPC)

2,09417.5

(Suntera)

3,76145

1,857364

15 (Medco)

2,38412.5

(Reliance)

7,0872,7106,629

50 50 25

(Sonatrach)

20

Exploration and Development Growth Mapping (Acreage)

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Nomination Including Pre-NELP JVs (Till 1998)

Very limited Scope for Growth

NELP (1999 onwards)

+Overseas

(2005 onwards)

Competition Level Playing Field

Operation Area – NE, RJ, UP, Uttarakhand Operation Area – Pan India + Overseas

Acreage (Sq. Km)

Growth

~ 11 Times Growth1

Current Acreage

Domestic = 117,622 sq.km

Overseas = 41,273 sq.km

21

Proved Proved & Probable Proved, Probable & Possible

Crude Oil and Natural Gas Reserves

Crude Oil Reserves (mmboe) Natural Gas Reserves (mmboe)

283 296 285

540588 575

1,0001,039

999

0

300

600

900

1,200

1,500

1,800

2007 2008 2009

169233 247

289345

399471 472

543

0

300

600

900

1,200

1,500

1,800

2007 2008 2009

Overall Reserves (mmboe)

452529 532

829

933974

1,4711,511 1,542

0

300

600

900

1,200

1,500

1,800

2007 2008 2009

Has improved the overall reserves available consistently over the past 3 years through enhanced oil recovery methods and aggressive exploration

22

22.17 22.38

24.95

12.92 13.16

0

5

10

15

20

25

30

2006-07 2007-08 2008-09 H1 2008-

09

H1 2009-

10

14.24 14.72 14.27

7.27 7.59

0

5

10

15

20

25

30

2006-07 2007-08 2008-09 H1 2008-

09

H1 2009-

10

Crude Oil and Natural Gas Production

Crude Oil Production (mmboe) Natural Gas Production (mmboe)

• Crude oil production in H1 FY2010 increased by 1.9% over H1 FY2009 to 13.16 mmboe1

• Natural gas production in H1 FY2010 increased by 4.4% over H1 FY2009

Note: (1) 1 BCM of Natural Gas = 6.2898 MMBOE

23

6.576.25 6.22 6.38

6.79

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

2.86 2.792.53

2.96 2.89

0

1

2

3

4

5

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

Crude Oil and Natural Gas Sales

Crude Oil Quarter on quarter sales (mmboe) Natural Gas Sales (mmboe)

24

5.23

4.80

7.10

6.81

0 2 4 6 8

FY2006

FY2007

FY2008

FY2009

1.80

1.81

1.83

2.99

0 1 2 3 4

FY2006

FY2007

FY2008

FY2009

Low Lifting and Finding costs

Lifting Costs (US$/boe) Finding Costs (US$/boe)

Note: (1) BOE: Barrels of Oil Equivalent

Production Cost NG (US$/MMBTU)

0.96

0.77

1.11

1.17

0.00 0.20 0.40 0.60 0.80 1.00 1.20 1.40

FY2006

FY2007

FY2008

FY2009

25

Healthy reserve replacement ratio

176

159

204

204

169

0 50 100 150 200 250

FY2005

FY2006

FY2007

FY2008

FY2009

Crude Oil and Natural Gas (O+OEG)

Adequate reserve replenishment

26

64.96

83.22 81.69

117.74

62.6

45.68

58.13 55.56

73.51

56.32

29.55

38.47 41.22

53.46

40.11

0

20

40

60

80

100

120

140

FY2007 FY2008 FY2009 HI FY2009 H1 FY2010

Gross Realized Price Realized Price after Subsidy/Discount Net Realized Price

CAGR (FY07 – 09) = 13.0%

1

Realized Price

Realized Price ($/barrel)

Current subsidy burden only on auto fuels

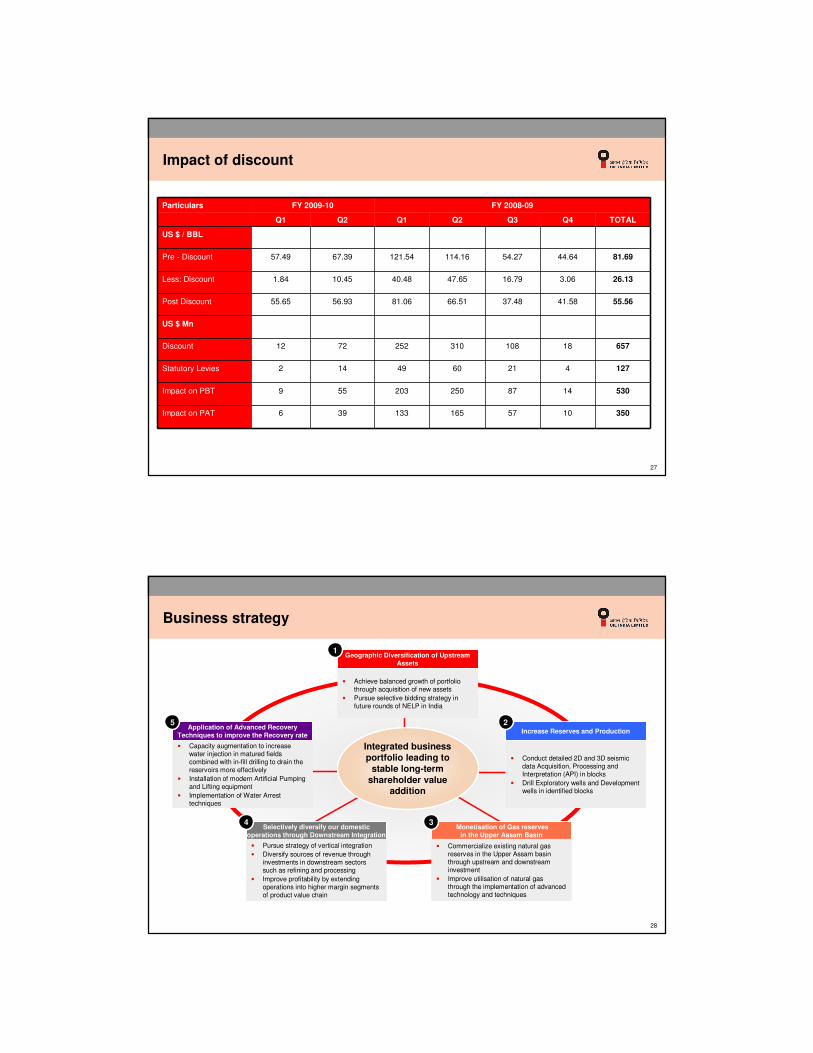

27

Impact of discount

Particulars FY 2009-10 FY 2008-09

Q1 Q2 Q1 Q2 Q3 Q4 TOTAL

US $ / BBL

Pre - Discount 57.49 67.39 121.54 114.16 54.27 44.64 81.69

Less: Discount 1.84 10.45 40.48 47.65 16.79 3.06 26.13

Post Discount 55.65 56.93 81.06 66.51 37.48 41.58 55.56

US $ Mn

Discount 12 72 252 310 108 18 657

Statutory Levies 2 14 49 60 21 4 127

Impact on PBT 9 55 203 250 87 14 530

Impact on PAT 6 39 133 165 57 10 350

28

Business strategy

Geographic Diversification of Upstream Assets

Integrated business portfolio leading to

stable long-term shareholder value

addition

• Achieve balanced growth of portfolio through acquisition of new assets

• Pursue selective bidding strategy in future rounds of NELP in India

1

Increase Reserves and Production

• Conduct detailed 2D and 3D seismic data Acquisition, Processing and Interpretation (API) in blocks

• Drill Exploratory wells and Development wells in identified blocks

2

Monetisation of Gas reserves in the Upper Assam Basin

• Commercialize existing natural gas reserves in the Upper Assam basin through upstream and downstream investment

• Improve utilisation of natural gas through the implementation of advanced technology and techniques

3Selectively diversify our domestic

operations through Downstream Integration

• Pursue strategy of vertical integration

• Diversify sources of revenue through investments in downstream sectors such as refining and processing

• Improve profitability by extending operations into higher margin segments of product value chain

4

Application of Advanced Recovery Techniques to improve the Recovery rate

• Capacity augmentation to increase water injection in matured fields combined with in-fill drilling to drain the reservoirs more effectively

• Installation of modern Artificial Pumping and Lifting equipment

• Implementation of Water Arrest techniques

5

Oil India Investor Presentation – H1 FY2009Oil India Investor Presentation – H1 FY2010

Sector outlook and opportunities

OIL India – An overview

Business structure, performance and strategy

Financial performance

30

Revenue and profitability analysis (USD mn)

Revenue CAGR: 10.5%

Revenue and profitability

1,242 1,239

1,401

1,677

1155

929

379317

367460

353301

0

400

800

1,200

1,600

2,000

FY2006 FY2007 FY2008 FY2009 H1 FY2009 H1 FY2010

Income PAT

Note: Exchange rate 1 USD = 48.52 INR used for figures upto FY2009; for H1FY2009 and H1FY2010, actual exchange rates have been used.

31

1,220

1,406

1,629

1,935 1,992

12.8

9.39.0

7.66.65.7

0

500

1,000

1,500

2,000

2,500

FY2006 FY2007 FY2008 FY2009 H1 FY2009 H1 FY2010

0

5

10

15

20

Networth (LHS)Book Value (RHS)

Networth and Book Value

Networth (USD mn) and Book Value Analysis (USD)

Networth CAGR: 16.6%2,788

32

Cash Flow (USD mn) EBITDA (USD mn) and EBITDA MARGIN (%)

Consistent and Attractive Cash Flow EBITDA EBITDA MARGIN

Cash Flow and EBITDA Margin

275

344

391

353

269

0

50

100

150

200

250

300

350

400

450

FY2007 FY2008 FY2009 H1FY0809 H1FY0910

533586

734

550501

44%

53% 54%

43% 42%

0

100

200

300

400

500

600

700

800

FY2007 FY2008 FY2009 H1FY0809 H1FY0910

0%

10%

20%

30%

40%

50%

60%

33

33.5633.93

32.9

30.19

305

275

265260

28

29

30

31

32

33

34

35

FY2006 FY2007 FY2008 FY2009

220

240

260

280

300

320

Dividend Payout (%) - LHS Dividends (%) - RHS

Dividends distribution Earnings per share and Debt-Equity ratio

The dividend per share has shown a consistent uptrend Steady increase in EPS and minimal debt on the balance sheet

86

72

83

104

67

0.004x0.006x

0.02x

0.06x

0.12x

0

20

40

60

80

100

120

FY2006 FY2007 FY2008 FY2009 H1 FY2010

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Earnings per share (INR) Debt/Equity

Dividends distribution and Earnings per share highlights

34

Investment PlansIN

R M

illi

on

24638131066584US$ Million

110821365794796426278Grand Total INR Million

24507270225631673Acquisition & Diversification

8285387819032504Overseas Projects

78029324312349822101Total INR Million

10286342326934170Capital Equipments & Facilities

20344988855274929Development Activities

47400191201527813002Exploration & appraisal activities

Total2011-122010-112009-10

35

THANK YOUTHANK YOU