h1 09 presentation final

TRANSCRIPT

1

Datatec GroupUnaudited results for the six months ended 31 August 2008

2

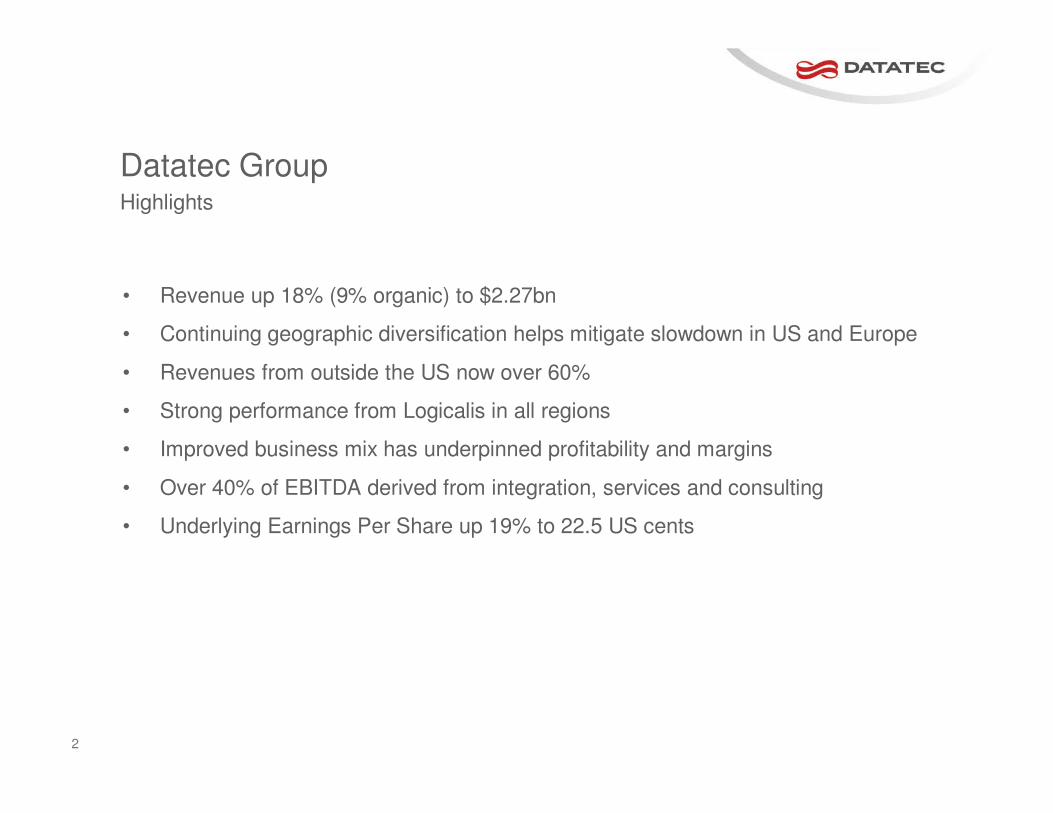

Datatec Group

• Revenue up 18% (9% organic) to $2.27bn

• Continuing geographic diversification helps mitigate slowdown in US and Europe

• Revenues from outside the US now over 60%

• Strong performance from Logicalis in all regions

• Improved business mix has underpinned profitability and margins

• Over 40% of EBITDA derived from integration, services and consulting

• Underlying Earnings Per Share up 19% to 22.5 US cents

Highlights

3

Datatec Group

• Financial crisis has created a deterioration in confidence

• Challenging conditions in US and Europe

• South America, the Middle East and Asia are less impacted

• Growth segments are SMB, managed services, virtualization & security

• Consolidation opportunities are growing as weaker competitors fair worse

Market conditions

4

Datatec Group

• Revenue growth of 18% (9% organic) to $2.27 billion

• Gross margin percentage improved to 13.4% from 12.9%

• Underlying* EBITDA up 25% to $76 million

• Underlying* earnings per share up 19% to 22,5 US cents

• $66 million cash generated from operations (2007: $3 million)

Financial performance summary

* excluding goodwill impairment, amortisation of intangible fixed assets, profit or loss on sale of assets and businesses, fair value movements on put/call arrangements and unrealised foreign exchange movements

5

Datatec GroupBusiness stream analysis

Distribution

ICT Solutions

Consulting & Prof Services

H1 2009 H1 2009

Revenues grew by 18% (9% organic)

Revenue Gross profit

Gross profit grew by 22%

$471m

21%

$145m

6%

$1,650m

73%

$90m

30%$48m

16%

$165m

54%

6

Datatec GroupRevenue % by geography

Increase in non-US and non-European revenues

43

42

6

7 2

North America

Europe

Asia Pac

Africa Middle East

South America

35

42

6

8

9

H1 2008 H1 2009

7

Datatec GroupGross profit contribution % by geography

Increased gross profit contribution from South America

43

5

7 2

43

North America

Europe

Asia Pac

Africa Middle East

South America

40

6

7

13

34

H1 2008 H1 2009

8

Datatec GroupFinancial performance

($m) H1 2007 H1 2008 H1 2009

Sales 1,520.3 1,921.7 2,266.0

Gross margin 191.0 247.8 303.4

Gross margin % 12.6% 12.9% 13.4%

Operating costs 138.9 187.4 232.0

Operating cost margin % 9.1% 9.7% 10.2%

EBITDA 52.0 60.4 71.4

EBITDA% 3.4% 3.1% 3.2%

Depreciation 7.1 7.5 8.3

Amortisation of acquired intangible assets 1.7 4.5 8.8

Operating profit 43.3 48.5 54.3

Operating profit % 2.8 2.5% 2.4%

+26 %

+30 %

+16 %

+18 %

+18 %

+22 %

9

Datatec GroupFinancial performance (continued)

173163147Weighted average number of shares (million)

175169147Issued number of shares (million)

($m) H1 2007 H1 2008 H1 2009

Operating profit 43.3 48.5 54.3

Net finance costs 4.7 8.0 7.4

Profit before tax 38.5 40.5 47.2

Underlying * EPS (US cents) 14.0 18.9 21.4

HEPS (US cents) 15.6 16.8 17.6

* excluding goodwill impairment, amortisation of intangible fixed assets, profit or loss on sale of assets and businesses, fair value movements on put/call arrangements and unrealised foreign exchange movements

+12 % +12 %

+35 % +19 %

10

Datatec GroupCash flow ($m)

H1 2008 H1 2009

EBITDA 60.4 71.4

Working capital changes (58.3) (0.6)

Non-cash items 0.6 (4.5)

Cash generated from operations 2.7 66.3

Net finance costs paid (8.0) (7.4)

Taxation paid (16.6) (19.4)

Net cash inflow / (outflow) from operating activities (21.9) 39.5

Net cash outflow from investing in subsidiaries (153.8) (49.5)

Net cash outflow from other investing activities (7.1) (7.8)

Net cash inflow from financing activities 76.1 20.9

Capital distribution to shareholders (16.8) (20.5)

Decrease in cash and cash equivalents (123.5) (17.4)

Translation difference on opening cash position 4.6 5.5 Cash and cash equivalents at beginning of period 141.4 34.2

Cash and cash equivalents at end of period 22.6 22.3

11

Datatec GroupBalance sheet summary ($m)

FY 2008 H1 2009

Equity and Liabilities

Shareholders funds 654.7 632.4

Outside shareholders 23.6 54.6

Long term liabilities 83.3 95.0

Amounts due to vendors 2.0 78.9

Current liabilities 1,120.8 1,229.3

1,884.3 2,090.1

Assets

Non current assets

Goodwill 284.3 354.5

Other intangible assets 55.0 82.9

Other non-current assets 81.8 80.1

Current assets 1,463.2 1,572.6

1,884.3 2,090.1

12

Westcon Group

13

Westcon GroupHighlights

• H1 revenues increase 9% to $1.5 billion

• Revenue increases in Europe and Asia Pacific offset by static revenues in Americas

• Gross margin increases to 10.1% with increases in the Americas and Asia Pacific

• Effective working capital management drives 26% reduction in interest expense

• New COO, Dean Douglas, joined in July

14

Westcon GroupFinancial performance summary

($m) H1 2008 H1 2009 Growth %

Sales 1,385,2 1,509,6 9%

Gross margin 136.4 151.9 11%

Gross margin % 9.8% 10.1%

Operating costs 88.7 107.8 21%

Operating cost margin % 6.4% 7.1%

EBITDA 47.7 44.1 (7%)

EBITDA% 3.4% 2.9%

Operating profit 41.2 36.9 (11%)

As a % of revenue 3.0% 2.4%

Net interest 9.2 6.8 (26%)

Pre-tax income 32.0 30.3

15

Westcon GroupRevenue % by geography

Americas

Europe

Asia Pac

46

45

9

Growth in European business

41

49

10

H1 2008 H1 2009

16

Westcon GroupRevenue % by vendor

57

11

10

8

14

Reduced reliance on Cisco; growth in Security

55

10

10

15

10

Cisco

Nortel

Avaya

Security

Other

H1 2008 H1 2009

17

Westcon GroupRevenue % by customer Reseller

System Integrator

Service Provider

65

27

9

Customer groups remain constant

66

21

13

H1 2008 H1 2009

18

Westcon GroupGross Margin %

9.310.1

10.9

9.89.610.2

11.6

10.1

0

2

4

6

8

10

12

14

Americas Europe Asia Pac Total

H1 2008

H1 2009

19

Westcon GroupEBITDA ($ millions)

Note: Central costs include infrastructure, systems and other non-operating group costs

H1 2008

H1 2009

35

17

6

48

31

16

8

44

-11 -12

-20

-10

0

10

20

30

40

50

60

Americas Europe Asia Pac Central

Costs

Total

20

Westcon GroupConsolidated balance sheet – working capital – US GAAP

Note: Amounts are stated before intercompany elimination and ratios based on trailing 90 day averages

1,6911,6341,556Total Headcount

179192177Net Debt (including Datatec loan)

1.3

65

514

9.3x

311

66

581

H1 2009($m) H1 2008 FY 2008

Accounts receivable 504 567

DSO (days) 61 69

Inventory 262 279

Inventory turns 10.4x 9.7x

Accounts payable 436 484

DPO (days) 59 66

Current ratio 1.3 1.3

21

Westcon GroupNet cash / debt trend ($m)

Note: Including Datatec loan

Mar

-

02

Jul

-

02

Nov

-

02

Mar

-

03

Jul

-

03

Nov

-

03

Mar

-

04

Jul

-

04

Nov

-

04

Mar

-

05

Jul

-

05

Nov

-

05

Mar

-

06

Jul

-

06

Nov

-

06

Mar

-

07

Jul

-

07

Nov

-

07

Mar

-

08

Jul

-

08

-$350

-$300

-$250

-$200

-$150

-$100

-$50

$0

$50

Mar-

02

Jul-02

No

v-0

2

Mar-

03

Jul-03

No

v-0

3

Mar-

04

Jul-04

No

v-0

4

Mar-

05

Jul-05

No

v-0

5

Mar-

06

Jul-06

No

v-0

6

Mar-

07

Jul-07

No

v-0

7

Mar-

08

Jul-08

Net Cash

22

Westcon GroupFuture outlook

• Economic outlook uncertain

• Weakness in US market extends to Europe

• Cost cutting initiatives underway to reduce operating expenses

• Leverage international reach and global scale for vendors and customers

• Consolidation opportunities in mature markets

• Improved cash generation

23

Logicalis Group

24

Logicalis Group

• Revenues up 39% to $550.7 million (11% organic)

• Annuity service revenues up 36%

• Strong Cisco growth

• All regions produced top and bottom line growth with operating costs well managed

• Significant improvement in EBITDA to $32.0 million (H1 08: $8.1 million)

• Gross margins expand to 22% and EBITDA margins to 5.8%

• Continued improvement in US profitability post last year’s restructuring

• Very strong performance by Brazil acquisition (completed 2 May 2008)

Highlights

25

Logicalis GroupFinancial performance summary

($m) H1 2008 H1 2009 Growth %

Sales 395.5 550.7 39%

Gross margin 85.3 121.3 42%

Gross margin % 21.6% 22.0%

Operating costs 77.2 89.2 16%

Operating cost % 19.5% 16.2%

EBITDA 8.1 32.0 295%

EBITDA% 2.0% 5.8%

Operating profit 3.3 23.2 608%

As a % of revenue 0.8% 4.2%

26

Logicalis GroupRevenue % geographic split North America

South America

UK

Germany

50

6

43

1

41

25

33

1

H1 2008 H1 2009

Improved geographic mix

27

Logicalis GroupRevenue segmental split

81

9

10

81

8

11

Product

Professional Services

Maintenance & Managed Services

H1 2008 H1 2009

Sales mix remained steady

28

Logicalis GroupRevenue product vendor mix %

39

26

24

92

27

44

18

92

IBM

Cisco

HP

Others

EMC

H1 2008 H1 2009

Cisco largest vendor partner

29

Logicalis GroupGross margin %

21.2

25.9

21.523.6

21.6

28.5

22.021.823.1

20.7

0

5

10

15

20

25

30

UK Germany North

America

South

America

Total

H1 2008

H1 2009

Overall margin up 0.4%

30

Logicalis GroupEBITDA ($m)

7.8

-0.5

3.21.4

-3.8

8.19.8

-0.5

11.9

16.1

-5.3

32.0

-10

-5

0

5

10

15

20

25

30

35

UK Germany North

America

South

America

Central

Costs

Total

H1 2008

H1 2009

Continued recovery in US profitability and strong Brazil performance

31

Logicalis GroupKey financial measures

44.3

72

116.5

44

133.9

18

28.0

19.3

FY2008($m) H1 2008 H1 2009

Deferred revenue 20.1 20.7

Inventory 12.3 51.7

Inventory days (excluding spares stock) 6 23

Accounts receivable 145.8 184.8

DSO days 48 40

Accounts payable 100.2 171.1

DPO days 69 58

Net cash 7.6 67.0

Significant cash generation

32

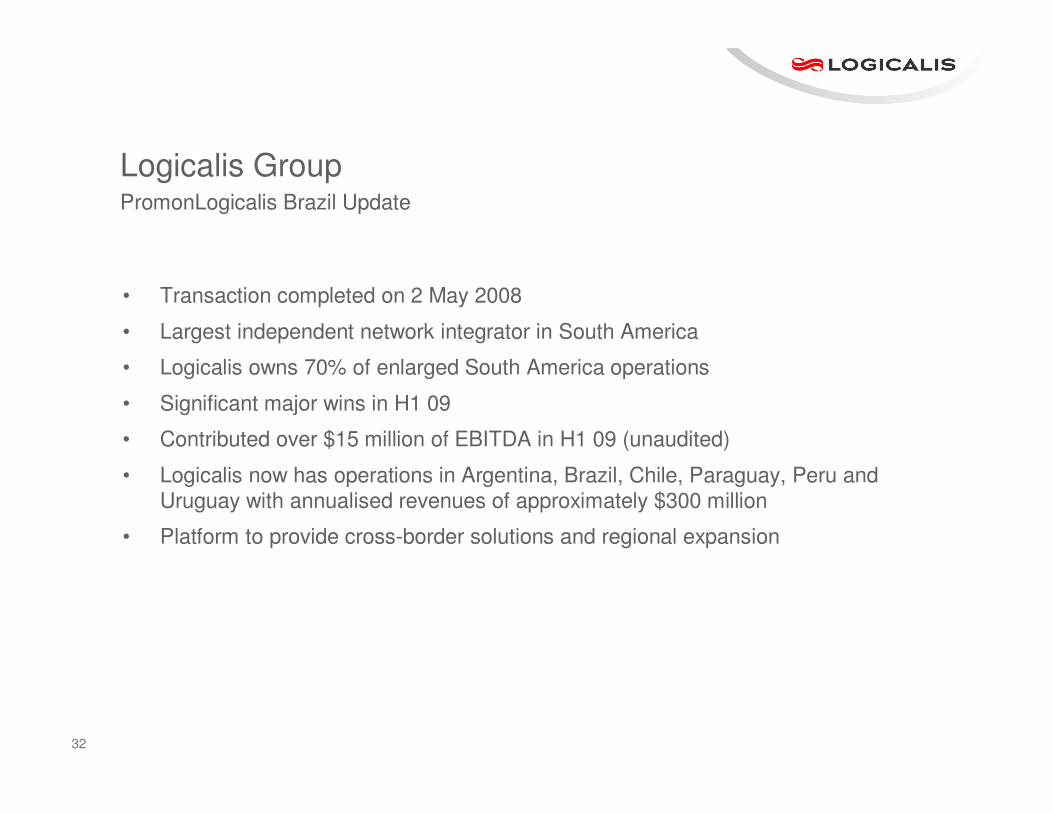

Logicalis GroupPromonLogicalis Brazil Update

• Transaction completed on 2 May 2008

• Largest independent network integrator in South America

• Logicalis owns 70% of enlarged South America operations

• Significant major wins in H1 09

• Contributed over $15 million of EBITDA in H1 09 (unaudited)

• Logicalis now has operations in Argentina, Brazil, Chile, Paraguay, Peru and Uruguay with annualised revenues of approximately $300 million

• Platform to provide cross-border solutions and regional expansion

33

Logicalis GroupFuture outlook

• Step change in the scale, business mix and positioning of the group

• Solid financial performance in tough market conditions

• Annuity based services revenues will continue to grow in proportion

• Macroeconomic conditions have deteriorated everywhere

• Continuing to rein in operating expenses

• Opportunities to exploit consolidation

34

Analysys Mason

35

Analysys Mason Highlights

• Revenues decline modestly on back of dollar strength

• Non-UK client base now generates 61% of total revenues (50% in H1 08)

• Strong start after opening of Dubai office for MENA region

• Completed the acquisition of Boston based OSS Observer on 26th June 2008

• Strategy business now represents 53% of total revenues (up 8% over H1 08)

• Research revenues have grown 22% year over year

• Move to a single brand Analysys Mason, completed in April 2008

• Steps taken to reduce fixed cost base in response to slowing market conditions

36

Analysys MasonFinancial performance summary

($ millions) H1 2008 H1 2009 Growth %

Revenue 31.5 30.4 (3.5%)

Gross margin 12.3 11.2 (9.0%)

Gross margin % 39.2% 36.8%

Operating costs 9.3 8.9 (4.3%)

Operating cost margin % 29.5% 29.3%

EBITDA 3.0 2.4 (23.3%)

EBITDA% 9.6% 7.9%

Operating profit 2.7 1.9 (29.6%)

As a % of revenue 8.9% 5.6%

37

Analysys MasonRevenue % geographical split

50

17

21

111

39

22

26

94

UK

Europe

MENA

Asia

USA

H1 2008 H1 2009

38

• Deepening our client relationships by increasing our support for operational activities

• Internationalising existing propositions

• Investing in our intellectual capital, high-profile and behind-the-scenes successes

• Managing our fixed cost base

Analysys MasonStrategy

39

• Mobile user growth in Emerging Markets

• Content delivery over broadband wireless (HSPA)

• Government and regulator engagements in next generation digital broadcast

• Exploiting broader ICT market

• Focused on improving diversification to drive growth

• Expecting to remain relatively defensive in downturn

Analysys MasonFuture Outlook

40

Other Emerging Market Operations

41

Other Emerging Market OperationsHighlights

• Revenue growth across all regions

• Profitability impacted by start-up costs in Pan-Africa operations

• Acquisition of Inflow India expected to contribute profitably in 2nd half

• Creation of Westcon Emerging Markets Sub-Group

• Good growth and profitability in African Legend Indigo (SA IT services group)

42

Other Emerging Market OperationsFinancial performance summary

($m) H1 2008 H1 2009 Growth

Sales 109.5 175.3 60%

Gross margin 13.8 19.1 38%

Gross margin % 12.6% 10.9%

Operating costs 11.4 17.5 54%

Operating cost margin % 10.4% 10.0%

EBITDA 2.4 1.5 (38%)

EBITDA% 2.2% 0.9%

Operating profit 2.1 0.9 (56%)

As a % of revenue 1.9% 0.5%

Net interest 0.4 1.6 321%

Pre-tax income 1.7 (0.7) (139%)

43

Other Emerging Market OperationsRevenue % by geography

5727

16

38

26

36

South Africa

Middle East & North Africa

Sub Saharan Africa

H1 2008 H1 2009

44

Other Emerging Market OperationsStrategic focus and outlook

• Drive synergies and operating leverage with Westcon Emerging Markets group

• India transaction offers excellent platform to grow rapidly and profitably

• Other untapped markets under review

• Aiming for $400 million + revenues and improving profitability for next year

45

Datatec Group

46

Datatec GroupMarket outlook

• US and European weakness likely to spread to the rest of the world

• Financial crisis likely to impact global growth for some time

• Wall Street and London financial firms will be hard hit and need to downsize

• Advancing user base in emerging markets should still relatively out perform

• Certain technologies will be vital for future productivity and growth

47

Datatec GroupStrategy

• Remain lightly exposed to the financial sector

• Accelerate activities in more dynamic and growth potential markets

• Focus on essential product and services segments

• Lower operating costs in all areas

• Increase cash flow and reduce debt

48

Datatec GroupCurrent trading and prospects

• Despite the recent financial crisis we continue to trade in line with our expectations

• US remains soft and similarly Europe

• Impact in the rest of the world unclear, Middle East and Asia still holding up

• Recent expansion in Brazil and now India is expected to contribute strongly

• Expect 2nd half to be similar to or beat 1st half financial performance

• Focused on controlling operating costs and generating cash

• Opportunistic acquisition consolidation targets may become available

49

Questions