nrg’s huntley plant and a just transition risks facing coal-fired generators in 2014 and coming...

TRANSCRIPT

NRG’s Huntley Plant and a Just Transition

Risks Facing Coal-Fired Generators in 2014 and Coming Years

David Schlissel

Director of Resource Planning Analysis

June 7, 2014

Background (1)

2

• Before late 1990s – rates and services of electric utilities were regulated by state public service or public utility commissions.• e.g., the New York State Public Service Commission.

• Utilities were vertically integrated.• Owned generating facilities, transmission lines and

distribution system and allowed to recover costs from their ratepayers - Niagara Mohawk Power Corporation.

• Then markets were “restructured.” • Competitive wholesale power markets established.

• Independent system operators created to operate high voltage transmission lines and to administer and monitor competitive wholesale power markets.

• Many power plants sold to unregulated merchant power generator companies like NRG.

©2014 Institute for Energy Economics & Financial Analysis

Background (2)

3©2014 Institute for Energy Economics & Financial Analysis

Background (3)

4

• Competitive markets now exist for both capacity (megawatts – MW) and energy (megawatt hours – MWh).

• Power plants now owned by 3 different types of owners.

• Regulated utilities in some states – • reduced risks for investors.

• protected by state regulatory commissions

• can pass through increased costs to ratepayers.

• Merchant owners - like NRG – the risks of competitive markets are borne by investors.

• Plants also are owned by public power utilities & Co-ops.

©2014 Institute for Energy Economics & Financial Analysis

NYISO Zones

5©2014 Institute for Energy Economics & Financial Analysis

Risks of Investing in Coal

6

• Low natural gas prices.

• Flat or slow sales growth due to slow economic recovery and energy efficiency.

• Increased use of renewable resources (mainly wind and solar).

• Uncertain, and often low, capacity market prices

• Need for upgrades to meet new environmental rules and requirements.

• Increasing coal prices in some areas.

• Potential for comprehensive system to reduce greenhouse gas (CO2) emissions.

• Aging of nation’s fleet of coal plants.

©2014 Institute for Energy Economics & Financial Analysis

Natural Gas Prices Collapsed in 2009

7

• This led to:

Lower energy market prices that, in turn, have led to less net revenue per MWh.

Increased generation at gas-fired units and lower generation at coal-fired units.

Pre-tax earnings for coal plant owners that have “fallen off a cliff.”

Coal plant owners concerned about difference between market prices at which they can sell output and the variable costs of generation.

Caught between lower operating revenues and increasing costs.

©2014 Institute for Energy Economics & Financial Analysis

8

Natural Gas Price Collapse in 2009 led to Lower Power Market Prices

©2014 Institute for Energy Economics & Financial Analysis

©2014 Institute for Energy Economics & Financial Analysis 9

Lower Nat Gas Prices Have Led to Reduced Coal Plant and Increased Gas Plant Generation

©2014 Institute for Energy Economics & Financial Analysis 10

Spread Between Power Market Prices and Costs of Generation at Coal Units Decreased Precipitously

No Growth in Peak Summer Demand for Power in NYS Between 2005 & 2012

©2014 Institute for Energy Economics & Financial Analysis 11

No Growth in Energy Sales in NYS Between 2005 and 2012

©2014 Institute for Energy Economics & Financial Analysis 12

Increased National Competition from Renewable Resources – Solar Photovoltaics

©2014 Institute for Energy Economics & Financial Analysis 13

Increased National Competition from Renewable Resources – Wind

©2014 Institute for Energy Economics & Financial Analysis 14

Capacity Market Prices Have Been Up and Down – Example PJM

©2014 Institute for Energy Economics & Financial Analysis 15

Rising Coal Prices Have Also Reduced Plant Owner Profits

16

• Coal prices have increased over the past decade due to:

Higher costs of production (mining) as lower cost reserves are used up.

Higher transportation costs as more plants burn coal from the Powder River Basin in Wyoming.

Some plants have used expensive coal from overseas to avoid having to make large investments in new pollution control equipment.

©2014 Institute for Energy Economics & Financial Analysis

Coal Plant Owner Profits Declined After 2009 – Example Brayton Point Coal Plant in Mass.

©2014 Institute for Energy Economics & Financial Analysis 17

$345

$229

$73

$24

$0

$50

$100

$150

$200

$250

$300

$350

$400

2009 2010 2011 2012

Mill

ions

of D

olla

rs

Risks for Coal Plant Owners Unlikely to Go Away Anytime Soon

18

• Natural gas prices and energy market prices expected to remain relatively low except in peak summer and/or winter months.

• Uncertainty about future capacity market prices.

• Little growth projected in demand for power plus increased competition from energy efficiency and renewables.

• Coal mining production costs will continue to rise as easier-to-mine reserves continue to be depleted.

• Need for environmental upgrades at many plants.

• Potential for higher prices for CO2 emissions.

• Uncertainty about plant operating performance and operating costs as they age.

©2014 Institute for Energy Economics & Financial Analysis

©2014 Institute for Energy Economics & Financial Analysis

Natural Gas Prices Expected to Remain Low for Foreseeable Future

19

©2014 Institute for Energy Economics & Financial Analysis

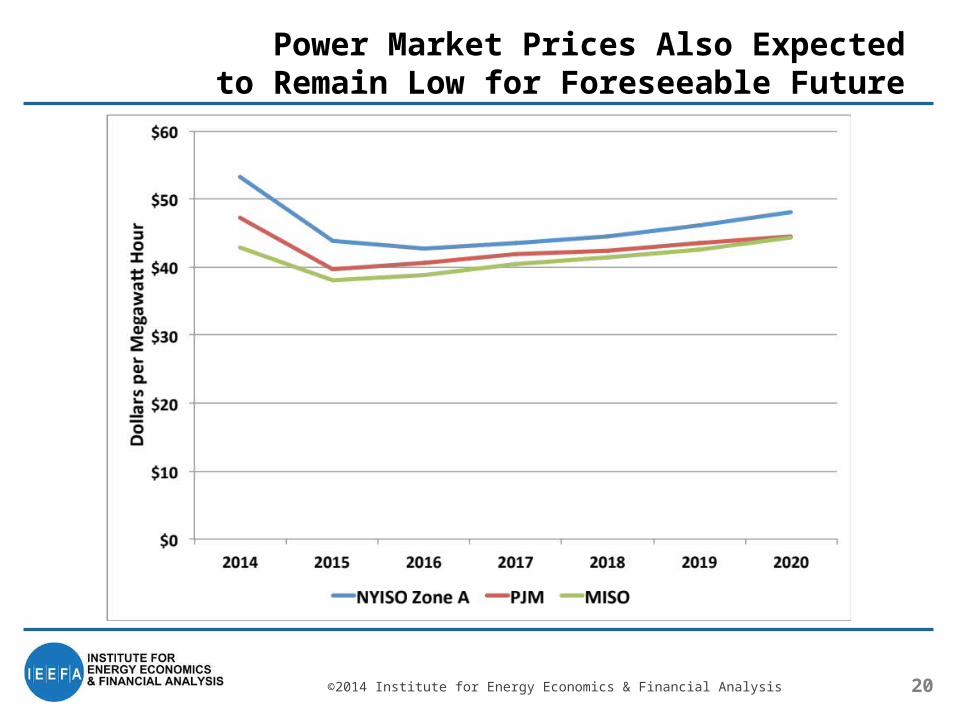

Power Market Prices Also Expected to Remain Low for Foreseeable Future

20

©2014 Institute for Energy Economics & Financial Analysis

Except for Peak Summer and Winter Months – Example NYISO Zone A

21

Proposed New EPA Rules Will Impact the Cost of Continuing to Operate Existing Coal Plants

22

• Cross-State Air Pollution Rule (CSAPR).

• Mercury and Air Toxics Rule (MATS).

• CO2 emissions.

• Coal ash disposal.

• Cooling water intake and emission rules.

• New Ozone and SO2 standards.

©2014 Institute for Energy Economics & Financial Analysis

Some Examples of Recent Coal Plant Retirements Without Significant Advance Notice

23

• Hatfields Ferry and Mitchell (First Energy) – announced in July 2013, closed in December 2013.

• Albright, Rivesville and Willow Island (First Energy) – announced in February 2012, closed in September 2012.

• Hutsonville (Ameren) – announced in October 2011, closed in December 2011.

• Tanners Creek (AEP) – announced September 2013 for mid-2015.

©2014 Institute for Energy Economics & Financial Analysis

The Winter of 2014 and the Displaced Polar Vortex

24

• A number of circumstances led to a southern displacement of the polar vortex which usually keeps the extremely cold weather up north in Canada.

• This displacement of the polar vortex began in January 2014 & brought extremely cold temperatures down to the middle, southern and eastern sections of the U.S. for extended periods.• Natural gas usage for home heating soared, as did its

price.

• As a result, power prices skyrocketed for portions of January and February, and much more power was generated from coal.

• Key Questions:

©2014 Institute for Energy Economics & Financial Analysis

The January 2014 Polar Vortex Event

25©2014 Institute for Energy Economics & Financial Analysis

Normal Early January

Early January 2014

What Does the 2014 Displaced Polar Vortex Event Mean for the Future of Coal (1)

26

Key Questions:

1. Was the displacement of the polar vortex caused or made worse by climate change? Unclear.

2. Was the displacement a one-time event or a sign of futures to come? Unknown.

3. Will natural gas and power prices spike as high in future peak winter months as they did in January 2014? Unknown but less likely as new natural gas transmission projects are completed.

©2014 Institute for Energy Economics & Financial Analysis

What Does the 2014 Displaced Polar Vortex Event Mean for the Future of Coal (2)

27

4. Can anything other than continuing to operate aging and polluting coal plants be done to protect consumers from the potential for spiking natural gas and power prices in peak winter or summer months?

Yes. More aggressive investments in economical renewable resources (wind & solar) and energy efficiency and encouragement of more demand response can make consumers less dependent on natural gas and coal and reduce the likelihood of price spikes like those experienced this past winter.

©2014 Institute for Energy Economics & Financial Analysis