novartis ag investor relations · 2018-05-22 · 16.2% 17.0% 18.5% 17.1% 20.2% 2017 2018 1,2 core...

TRANSCRIPT

Meet Novartis ManagementInvestor Presentation

May 16, 2018

Novartis AG

Investor Relations

Disclaimer

This presentation contains forward-looking statements that can be identified by terminology such as such as “potential,” “expected,” “will,” “planned,” “pipeline,” “outlook,” or similar

expressions, or by express or implied discussions regarding potential new products, potential new indications for existing products, or regarding potential future revenues from any

such products; or regarding potential future sales or earnings of Novartis; or regarding the potential outcome of the strategic review being undertaken to maximize shareholder value

of the Alcon Division; or regarding the potential financial or other impact of the significant acquisitions and reorganizations of recent years; or regarding potential future sales or

earnings of the Novartis Group or any of its divisions or potential shareholder returns; or by discussions of strategy, plans, expectations or intentions. You should not place undue

reliance on these statements. Such forward looking statements are based on our current beliefs and expectations regarding future events, and are subject to significant known and

unknown risks and uncertainties. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially

from those set forth in the forward looking statements. There can be no guarantee that any new products will be approved for sale in any market, or that any new indications will be

approved for any existing products in any market, or that any approvals which are obtained will be obtained at any particular time, or that any such products will achieve any particular

revenue levels. Neither can there be any guarantee that the strategic review being undertaken to maximize shareholder value of the Alcon Division will reach any particular results, or

at any particular time, or that the result of the strategic review will in fact maximize shareholder value. Neither can there be any guarantee that Novartis will be able to realize any of

the potential strategic benefits, synergies or opportunities as a result of the significant acquisitions and reorganizations of recent years. Neither can there be any guarantee that

shareholders will achieve any particular level of shareholder returns. Nor can there be any guarantee that the Group, or any of its divisions, will be commercially successful in the

future, or achieve any particular credit rating or financial results. In particular, our expectations could be affected by, among other things: global trends toward health care cost

containment, including government, payor and general public pricing and reimbursement pressures and requirements for increased pricing transparency; regulatory actions or delays

or government regulation generally, including potential regulatory actions or delays with respect to the development of the products described in this release; the potential that the

strategic benefits, synergies or opportunities expected from the proposed acquisition of AveXis, Inc. may not be realized or may take longer to realize than expected; the successful

integration of AveXis into the Novartis Group subsequent to the closing of the transaction and the timing of such integration; potential adverse reactions to the proposed transaction

by customers, suppliers or strategic partners; dependence on key AveXis personnel and customers; the potential that the strategic benefits, synergies or opportunities expected from

the significant acquisitions and reorganizations of recent years may not be realized or may take longer to realize than expected; the inherent uncertainties involved in predicting

shareholder returns; the uncertainties inherent in the research and development of new healthcare products, including clinical trial results and additional analysis of existing clinical

data; our ability to obtain or maintain proprietary intellectual property protection, including the ultimate extent of the impact on Novartis of the loss of patent protection and exclusivity

on key products which commenced in prior years and will continue this year; safety, quality or manufacturing issues; uncertainties regarding actual or potential legal proceedings,

including, among others, actual or potential product liability litigation, litigation and investigations regarding sales and marketing practices, intellectual property disputes and

government investigations generally; uncertainties involved in the development or adoption of potentially transformational technologies and business models; general political and

economic conditions, including uncertainties regarding the effects of ongoing instability in various parts of the world; uncertainties regarding future global exchange rates;

uncertainties regarding future demand for our products; and uncertainties regarding potential significant breaches of data security or data privacy, or disruptions of our information

technology systems; and other risks and factors referred to in Novartis AG’s current Form 20-F on file with the US Securities and Exchange Commission. Novartis is providing the

information in this presentation as of this date and does not undertake any obligation to update any forward-looking statements as a result of new information, future events or

otherwise.

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation2

Agenda

1 Focusing as a medicines company

2 Positioned for growth

3 Driving margin expansion

4 Leading innovation power

5 Alcon update

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation3

We outlined a clear strategy in January 2018

1 Operational Execution

2 Breakthrough Innovation

3 Data / Digital Leadership

4 Trust & Reputation

5 Culture Transformation

Pursue 5 priorities to drive growth

1920 - 1996 1996 - 2009 2009 - 2017 2018+

Medicinal

chemistry and

industrials

Portfolio

transformation

Diversified

healthcare

group

Focused medicines

company powered

by data / digital

Focus the company and our capital

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation4

1. GSK shareholders approved the transaction on May 3, 2018. Divestment is subject to customary closing conditions.

We have started the journey to focus our company and our capital

2018

January February March April

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation5

Acquired AAA

Licensing agreement

with Spark for

Luxturna® ex-US

Agreement with GSK

to divest OTC JV1

Collaboration with

Pear Therapeutics

Agreement to acquire

AveXis

Liz BarrettCEO, Novartis

Oncology

Bertrand

BodsonChief Digital Officer

Shannon

KlingerGeneral Counsel

Steffen LangGlobal Head,

Novartis Technical

Operations (NTO)

John TsaiHead of Global

Drug Development

(GDD) & Chief

Medical Officer

Robert

WeltevredenGlobal Head,

Novartis Business

Services (NBS)

Natacha

TheytazGlobal Head,

Internal Audit1

Prior companies:

Our reshaped executive team is now in place 2018 appointments

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation6

All trademarks are the property of their respective owners 1. Not a member of the Novartis Executive Committee (ECN), but a permanent attendee of ECN meetings. All other executives on this slide are members of the ECN.

To lead, we have to be realistic about our strengths and weaknesses

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation7

Researching new science, and

developing innovative medicines

Marketing and selling our

products to specialist

physicians

Manufacturing complex drugs

and biologics at high quality

Sustainably managing broad

diversification

Cost leadership to aggressively

take cost out year-on-year

What we do well What we don't do so well

Integrating innovative medicine

acquisitions (e.g., GSK portfolio)

Integrating non-innovative

medicine acquisitions

(e.g. Alcon, generic integrations)

Fast paced, continuous

incremental R&D

Engaged, high

quality people

In Innovative Medicines, we have the key ingredients to lead and are actively addressing our gaps

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation8

Plan to drive margin

expansion

Global scale with

leadership ex-US1

Credible strong

management team

Established growth

drivers in key

therapeutic areas

13 potential

blockbuster launches

in next 3 years

Increasing pipeline

focus on first-in-class

medicines

Disruptive technology

platforms to drive

innovation

1. Source: Novartis peer group (as outlined on page 123 of the 2017 Novartis Annual Report) analysis of peers’ FY 2017 press releases; Novartis ranks #2 in ex-US sales.

Alcon is returning to a position of strength as the world leader in eye care devices

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation

Alcon net sales growthvs. PY, % cc

9

includes OTC

excludes OTC

Strong market positionVariances in cc

% of total sales Americas EMEA Asia/JP

SurgicalFY 2017 sales: USD 3.7bn

51% 25% 24%

Share position4 #1 #1 #1

Vision Care3

FY 2017 sales: USD 3.0bn50% 32% 18%

Share position4 #1 #1 #4

3%1%

7%6%1

Q1

7%1

Q4Q1 Q2 Q3

Core margin %

excl. OTC

16.2% 17.0% 18.5% 17.1% 20.2%

2017 2018

1,2

Core margin %

incl. OTC

13.2% 13.9% 15.6% 14.1%

1. Alcon sales growth benefitted from stock in trade movements, approx. 2% (cc) in Q3 2017, 1% (cc) in Q4 2017, and 1% (cc) in Q1 2018. 2. Alcon Division Q1 2018 growth rates and core margin include the Ophthalmic OTC products and a

small portfolio of surgical diagnostic products, transferred from the Innovative Medicines Division effective January 1, 2018, and are compared against the Q1 2017 updated financials including the aforementioned product transfer. 3. Includes

Ophthalmic OTC products 4. Based on revenues; source: company filings

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation10

In Sandoz, we are evolving our strategy based on macro trends and our core competencies

US:

• Impacted by industry-wide pricing pressure and

customer consolidation

• Limited market uptake of biosimilars so far

US:

• Optimizing our portfolio through targeted pruning/

divestment of low-margin products

• Pivoting to differentiated segments for profitability

and growth, and learning from recent setbacks

Ex-US:

• Stable growth in Europe with strong adoption of

biosimilars

• Increasing demand for high-quality medicines in

largely out-of-pocket driven emerging markets

Ex-US:

• Continuous growth across regions from biosimilars

and generics, market leader in Europe1

• Focus on branded generics, as well as continuously

optimizing geographic and product mix

1. Source: IQVIA MIDAS, FY 2017

Macro trends Sandoz position

M&A BD&L

Strengthen Oncology pipeline

Strengthen Pharma TAs

Cell and gene therapies

Digital and data science

Our capital allocation priorities support our strategy to become a focused medicines company

1. Includes M&A and BD&L

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation11

Capital allocation priorities M&A / BD&L priorities

Investments in

organic business

Growing annual

dividend in CHF

Value-creating

bolt-ons1

Share buybacks

1

2

3

4

Across our five strategic priorities, we are reshaping Novartis for the future

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation12

Breakthrough

Innovation

Operational

Execution

Culture

Transformation

Trust &

Reputation

Data / Digital

Leadership

Mix of me-too’s and

first/best-in-class

Mixed launch performance

Expanding costs

Hierarchical, bureaucratic

Mixed reputation

Pilot data/digital projects

Focus on first or transformative in class

New therapeutic platforms

Consistent launches

Productivity excellence

Inspired, empowered

Respected leader

Data/Digital at scale company-wide

From: To:

Beginning our journey to rebuild trust with society

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation13

Select ongoing issues Strong actions being undertaken,

multi-year effortTrust &

Reputation

Let me be absolutely clear: I never want Novartis to achieve our financial performance or objectives

because we compromised on our ethical standards or our values – we must always choose our values.“

“

Vas Narasimhan

New integrated risk function; Chief Ethics, Compliance

and Risk Officer elevated to ECN

New Head of Internal Audit

New Professional Practices policy rolling out globally

Independent Ethics Board in place for managed access /

patient issues

Tightened controls on IIT, Phase 4 and grants activities

Planning deployment of big data analytics system for

compliance monitoring

Southern District of New York /

speaker programs

Alcon Asia

Greece

Korea

Essential Consultants

Agenda

1 Focusing as a medicines company

2 Positioned for growth

3 Driving margin expansion

4 Leading innovation power

5 Alcon update

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation14

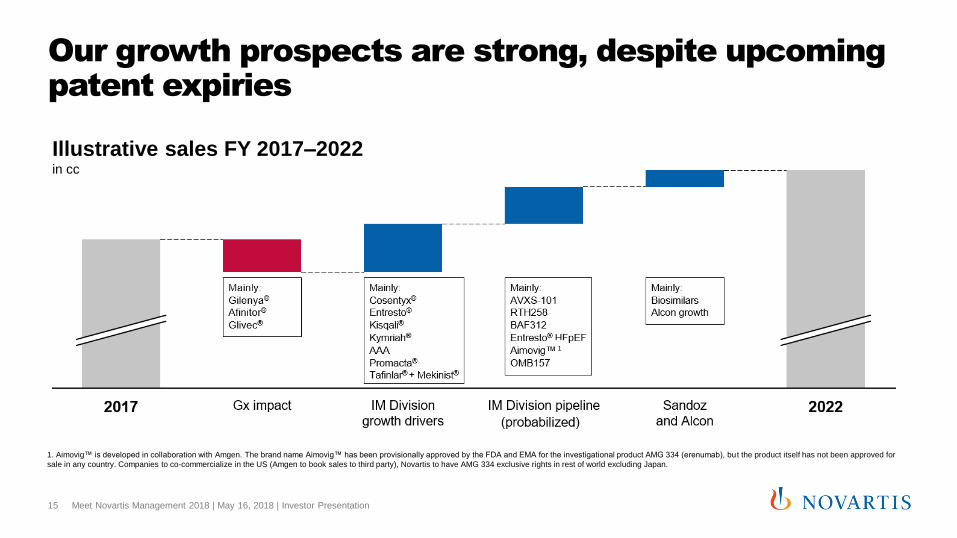

Our growth prospects are strong, despite upcoming patent expiries

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation15

1. Aimovig™ is developed in collaboration with Amgen. The brand name Aimovig™ has been provisionally approved by the FDA and EMA for the investigational product AMG 334 (erenumab), bu t the product itself has not been approved for

sale in any country. Companies to co-commercialize in the US (Amgen to book sales to third party), Novartis to have AMG 334 exclusive rights in rest of world excluding Japan.

Illustrative sales FY 2017–2022 in cc

1

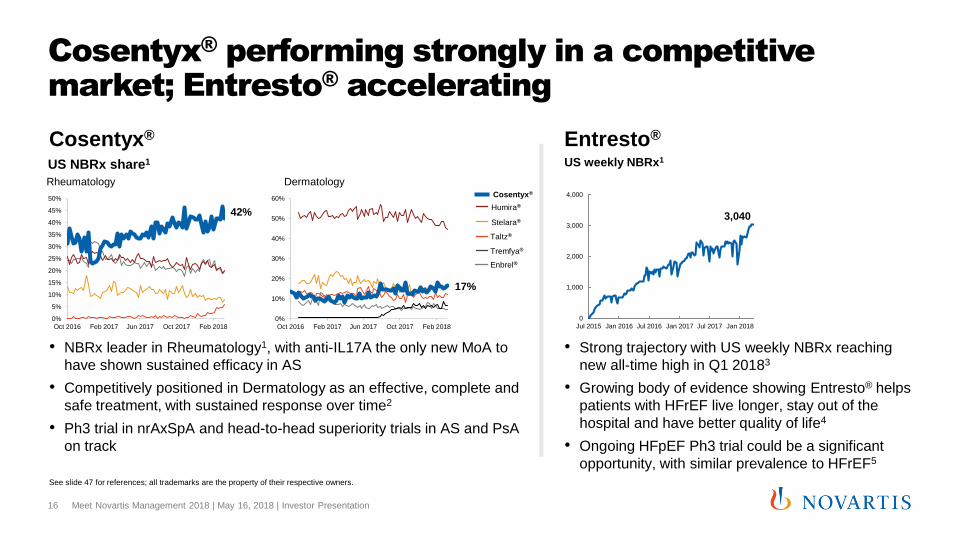

Cosentyx® performing strongly in a competitive market; Entresto® accelerating

• NBRx leader in Rheumatology1, with anti-IL17A the only new MoA to

have shown sustained efficacy in AS

• Competitively positioned in Dermatology as an effective, complete and

safe treatment, with sustained response over time2

• Ph3 trial in nrAxSpA and head-to-head superiority trials in AS and PsA

on track

• Strong trajectory with US weekly NBRx reaching

new all-time high in Q1 20183

• Growing body of evidence showing Entresto® helps

patients with HFrEF live longer, stay out of the

hospital and have better quality of life4

• Ongoing HFpEF Ph3 trial could be a significant

opportunity, with similar prevalence to HFrEF5

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation16

See slide 47 for references; all trademarks are the property of their respective owners.

Rheumatology Dermatology

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Oct 2016 Feb 2017 Jun 2017 Oct 2017 Feb 2018

42%

0%

10%

20%

30%

40%

50%

60%

Oct 2016Jan 2017Apr 2017Jul 2017Oct 2017Jan 2018

17%

0%

10%

20%

30%

40%

50%

60%

Oct 2016 Feb 2017 Jun 2017 Oct 2017 Feb 2018

Cosentyx® Entresto®

US NBRx share1

3,040

0

1,000

2,000

3,000

4,000

Jul 2015 Jan 2016 Jul 2016 Jan 2017 Jul 2017 Jan 2018

US weekly NBRx1

Stelara®

Tremfya®

Humira®

Cosentyx®

Taltz®

Enbrel®

124 162234

131

175

257150

187

267

Q1 2016 Q1 2017 Q1 2018

Tafinlar® + Mekinist®

13k+ BRAF+ melanoma patients p.a. in G7

Market leader in melanoma targeted therapy (>70%+ patient share in G7)1

Approved for adjuvant melanoma in US and filed in EU, potentially increasing eligible patients by 50%

Added to NCCN guidelines for 1L treatment in BRAF+ lung (~2% of lung patients)

Ph3 study with PDR001 progressing

Strong momentum behind Oncology growth drivers

Jakavi®

~30k MF patients in EU

Market leader in MF across EU with 50%+ patient share1 supported by long-term safety and

survival data

PV indication similar in size, ~20% share in EU and growing

Ph3 studies in GVHD expected filing in 2020 (~5k new cases per year)

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation17

Promacta®/Revolade®

300k+ ITP patients diagnosed globally p.a.

Promacta® gaining share on strength of data, convenient administration & broad label

EXTEND publication confirms long-term efficacy and safety data

FDA Breakthrough Therapy designation in SAA (1.4k+ newly diagnosed patients in US/EU5 p.a.)

Net salesUSD million

0.4bn

0.5bn

0.8bn

1. Novartis estimated share based on weighted average volumes in 2017

Executing against recent Oncology launches in complex and competitive environments

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation18

Lutathera®

Progression free survival (PFS)

Rapid acceptance as best second line option for

NET patients after somatostatin analogues

Already showing strong uptake in the US

EU approved in Sep. 2017, reimbursement

underway

Kisqali®

EU countries launched

Positioned well to grow in Europe, with

reimbursement in UK, ES, DE

Rolling out refined messages and targeting

in the US

MONALEESA 3 & 7 submissions planned in

2018

Kymriah®

US centers on-line

Over 40 centers ready to prescribe

Kymriah® across two indications (r/r

pediatric & young adult ALL, r/r DLBCL) in

the US

Patients able to achieve and maintain a

durable response

EU filed for r/r pediatric & young adult ALL

and r/r DLBCL in Nov. 2017; also filed in

Australia, Switzerland, Canada and Japan

Full pipeline of late-stage assets with blockbuster potential

1. Exact launches and timing depends on filing date, HAs decisions and timelines. 2. Aimovig™ is developed in collaboration with Amgen. The brand name Aimovig™ has been provisionally approved by the FDA and EMA for the investigational

product AMG 334 (erenumab), but the product itself has not been approved for sale in any country.

6

3ACZ885

CV risk reduction

BAF312

SPMS

RTH258

nAMD

Aimovig™2

Migraine

Kymriah®

DLBCL

Lutathera®

GEP-NET

OMB157

Relapsing MS

QVM149

Asthma

Entresto®

HFpEF

Cosentyx®

nrAxSpA

SEG101

Sickle cell disease

20181 20191 20201

Expected

launches

QAW039

Asthma

AVXS-101

SMA

4

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation19

Positive pivotal readout

Launched

Potentially first in class or indication

Leveraging differentiated data to support upcoming launches in competitive settings

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation20

EXPAND study demonstrated 21% reduction with siponimod in 3 month

confirmed disability progression vs. placebo in an SPMS population3

US submission planned in H1 2018, EU submission planned in H2 2018

BAF312 (siponimod)

Efficacy in SPMS creates opportunity

to address an unmet need

New unique LIBERTY2 data showed nearly 3x higher odds of having

migraine days cut by half or more with Aimovig™ (vs. placebo) in patients

who failed multiple treatments

FDA action expected May 2018, EMA action expected Q3 2018

AimovigTM1 (erenumab)

Potentially the first monoclonal

antibody targeting the CGRP receptor

• Met primary endpoint of non-inferiority to aflibercept in BCVA, with >50% of

patients maintained on q12w dosing at 1 year4,6

• Superiority was shown in three key secondary endpoints; central subfield

retinal thickness, retinal fluid and disease activity5

• US submission targeted for Q4 2018, EU in first half 2019

RTH258 (brolucizumab)

Comparable vision gains, less fluid and

less disease activity vs. aflibercept4,5

See slide 47 for references

China emerging as a key growth opportunity

China pharmaceutical market growth trend1

USD bn, hospital purchase price

6.9%

6.4%

0

1

2

2

2

4

3

6

7

7

Roche

Bayer

AstraZeneca

BMS

Lilly

Sanofi

Xi’an Janssen

Pfizer

MSD

NOVARTIS

Number of products listed

in 2017 NRDL2

1

1

1

1

2

2

3

6

6

Sanofi

Pfizer

GSK

Roche

AbbVie

Bayer

AstraZeneca

J&J

NOVARTIS4

... and up to 11 more NDA approvals expected (2018-20) for Novartis

2017 approvals3

177167

157148

139130122116

107100

2015 2023e2022e2020e 2021e2014 20172016 2018e 2019e

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation21

See slide 47 for references

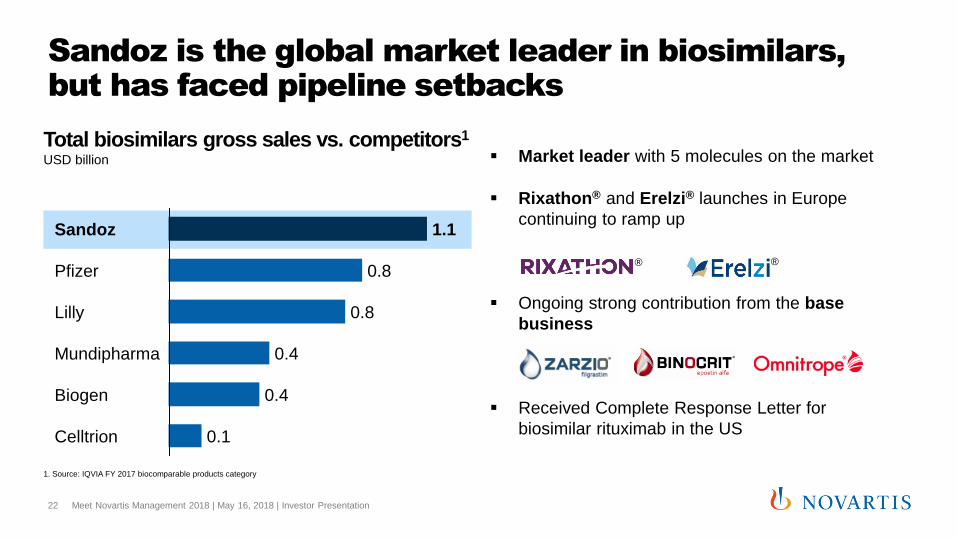

Sandoz is the global market leader in biosimilars, but has faced pipeline setbacks

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation22

Market leader with 5 molecules on the market

Rixathon® and Erelzi® launches in Europe

continuing to ramp up

Ongoing strong contribution from the base

business

Received Complete Response Letter for

biosimilar rituximab in the US

1. Source: IQVIA FY 2017 biocomparable products category

Total biosimilars gross sales vs. competitors1

USD billion

1.1Sandoz

Biogen

Pfizer

0.1

0.4

0.4

0.8

0.8

Mundipharma

Lilly

Celltrion

® ®

Agenda

1 Focusing as a medicines company

2 Positioned for growth

3 Driving margin expansion

4 Leading innovation power

5 Alcon update

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation23

Key drivers of our margin expansion

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation24

31

Mid 30’s

IM Division

2017

Large Pharma

average1

Innovative MedicinesCore margin (%)

1. Source: Novartis analysis of average 2016 core margins of Large Pharma peer companies

+ Sales momentum

+ Product mix

+ Resource allocation and productivity

programs in commercial units

+ Cross-divisional synergies: technical

operations (NTO), business services

(NBS) and drug development (GDD)

− Generics (mainly Gilenya®, Afinitor®,

and tail end of Glivec®)

− Launch investments for potential

future blockbusters

Oncology

Oncology

Pharmaceuticals

Immunology Hepatology

Dermatology

Cardio-Metabolic Ophthalmology Respiratory Neuroscience

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation25

Expected launches leverage existing infrastructure1

TH

ER

AP

EU

TIC

AR

EA

DE

PT

H

OMB157

Relapsing MS

BAF312

SPMS

Aimovig™1

Migraine

Lutathera®

GEP-NET

SEG101

Sickle cell disease

Kymriah®

DLBCL

Cosentyx®

nrAxSpA

AVXS-101

SMA

1. Aimovig™ is developed in collaboration with Amgen. The brand name Aimovig™ has been provisionally approved by the FDA and EMA for the investigational product AMG 334 (erenumab), but the product itself has not been approved for

sale in any country.

Entresto®

HFpEF

ACZ885

CV risk reduction

RTH258

nAMD

QVM149

Asthma

QAW039

Asthma

Luxturna®

RPE65 mutations

Major cost savings efforts ongoing

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation26

Novartis Technical

Operations (NTO)

Novartis Business

Services (NBS)

Procurement

Strategy

Stage IOn track to deliver on

USD 1bn savings plan1 by

2020

Operational go-live in

January 2015 with the

objective to keep costs flat

as sales grew

Evolved from a multi-division

approach to coordinated

sourcing with the creation of

NBS

Stage IIEffort ongoing to develop

predictive capabilities to

reduce inventory and

increase efficiency and

automation

New mandate to reduce

costs through location

strategy and lean

processes

Developing plan to

accelerate savings and

radically simplify supplier

base

1. NTO responsible for ~85% of the savings plan announced in January 2016; the rest comes from Global Drug Development and other functions. Novartis is on track to deliver the full USD 1 billion in savings by 2020.

Agenda

1 Focusing as a medicines company

2 Positioned for growth

3 Driving margin expansion

4 Leading innovation power

5 Alcon update

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation27

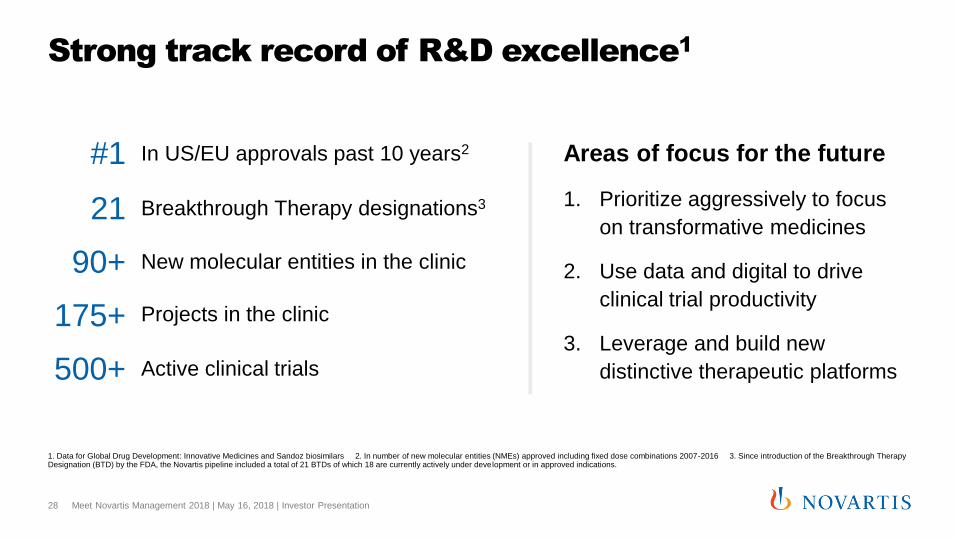

Strong track record of R&D excellence1

1. Data for Global Drug Development: Innovative Medicines and Sandoz biosimilars 2. In number of new molecular entities (NMEs) approved including fixed dose combinations 2007-2016 3. Since introduction of the Breakthrough Therapy Designation (BTD) by the FDA, the Novartis pipeline included a total of 21 BTDs of which 18 are currently actively under development or in approved indications.

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation28

Areas of focus for the future

1. Prioritize aggressively to focus

on transformative medicines

2. Use data and digital to drive

clinical trial productivity

3. Leverage and build new

distinctive therapeutic platforms

#1 In US/EU approvals past 10 years2

21 Breakthrough Therapy designations3

90+ New molecular entities in the clinic

175+ Projects in the clinic

500+ Active clinical trials

Emerging assets reflect therapeutic area focus

1. Selected assets not including the near-term potential blockbuster launches on slide 19 2. Novartis has an option to license APO(a)-LRx from Ionis Pharmaceuticals, Inc. and its affiliate Akcea Therapeutics, Inc.

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation29

Oncology

Oncology

Pharmaceuticals

Immunology Hepatology

Dermatology

Cardio-Metabolic Ophthalmology Respiratory Neuroscience

TH

ER

AP

EU

TIC

AR

EA

DE

PT

H

ABL001 (CML)

ACZ885 (NSCLC)

BYL719 (Breast)

CAR-T (Multiple)

EGF816 (EGFRmut NSCLC)

INC280 (NSCLC)

LJN452 (NASH)

QGE031 (CSU)

CFZ533 (Sjogren’s)

VAY785 (Liver disease)

ZPL389 (Atopic dermatitis)

APO(a)-LRx2

(Atherosclerosis)

CLR325 (Cardiac failure)

Entresto® (Post-MI)

LHW090 (rtHypertension)

LTW980

(Hypertriglyceridaemia)

ECF843 (Dry eye)

SAF312 (Ocular pain)

UNR844 (Presbyopia)

CSJ117 (Asthma)

QBW251 (COPD)

QCC374 (PAH)

VAY736 (IPF)

AVXS-101 (SMA label

expansion)

BYM338 (Hip fracture,

sarcopenia)

CNP520 (Alzheimer’s)

EMA401 (Pain)

Select Early Phase 3 & Phase 2 Programs1

EU US

EU US

Starting 2018

Starting 2018

Starting 2018

Starting 2018

Started

Started

Starting 2018

Started

CAR-T type Indication Ph 1 Ph 2/Pivotal Ph 3 Submitted Approved

CD19 CAR-T Ped. r/r ALL

CD19 CAR-T r/r DLBCL

CD19 CAR-T DLBCL in 1st relapse

CD19 CAR-T r/r FL

CD19 CAR-T r/r DLBCL in combination

with pembrolizumab

CD19 CAR-T Adult r/r ALL

CD19 CAR-T CLL

CAR-T-BCMA r/r M/M

CAR-T-EGFRvIII Recurrent GBM

CAR-T-Meso Adv. ovarian cancer,

mesothelioma

Approaching immuno-oncology (IO) with a focus on CAR-T and only selected differentiated IO assets

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation30

CAR-T Other IO assets

Optimizing manufacturing

Advancing multiple indications beyond pediatric & young adult ALL

and r/r DLBCL:

Taking a rigorous approach to prioritizing

IO assets for development

Looking for single agent activity, or

synergistic combinations with appropriate

control arms

Selected IO studies:

Asset Indication Status

ACZ885 NSCLC, adjuvant Ph 3 ongoing

ACZ885 NSCLC, 1st line Initiating Ph 3

ACZ885 NSCLC, 2nd line Initiating Ph 3

PDR001+Tafinlar+Mekinist Melanoma Ph 3 ongoing

PDR001+INC280 NSCLC Initiating Ph 2

LAG525+PDR001 TNBC Initiating Ph 2

Building new platform capabilities in therapeutics and advanced therapies...

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation31

CAR-T

mRNA

CRISPR

Novel IO Rx Delivery

AAV

Targeted Protein

Degradation

Covalent Binders

Cancer cell

T-cell

Radiopharmaceuticals

All trademarks are the property of their respective owners.

... and leveraging M&A to build and accelerate our pipeline

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation32

Radiopharmaceutical theragnostics Gene therapies

Selected assets Indication Status

AVXS-101 (AAV9) SMA Pivotal studies

CGF166 (AAV5) Hearing loss Phase 1b

CPK850 (AAV8) Retinitis pigmentosa Phase 1b

AVXS-201 RTT Rett Syndrome Preclinical

AVXS-301 SOD1 Inherited ALS-SOD1 Preclinical

Homology

Medicines

collaboration

Ophthalmology

& hematology

Preclinical

Gene therapy A Undisclosed Preclinical

Gene therapy B Undisclosed Preclinical

1. USAN lutetium Lu 177 dotatate / INN: lutetium (177Lu) oxodotreotide

1

0

20

40

60

80

100

0 3 6 9 12 15 18 21 24

AVXS-101: Additional 2 years data1 indicate strong efficacy across survival, nutrition, respiratory and motor endpoints

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation33

Long-

term

follow-up

Ev

en

t-fr

ee s

urv

ival (%

)3

Month

• CL-101 study: Efficacy maintained, no new safety signals at 2 years

• Long-term follow-up (n=11):

• 4 patients achieved 5 new motor milestones beyond 2 years, 3 of

whom not treated with other agents

• Longest total follow-up – 40.6 months

• Additional studies in SMA:

1. STR1VE: Type 1 (n=15-20); first 6 patients followed for >1 month

show improvements in CHOP scores similar to CL-101

2. STR1VE EU: Type 1 (n=30); to start H1 2018

3. STRONG: Type 2, i.t. dose selection (n=27); first 4 patients dosed

4. SPRINT: Type 1-3, pre-symptomatic (n=44); first patient dosed

5. REACH: Type 1-3 (n=50); planned to start H2 2018/H1 2019

• Pre-BLA meeting planned for Q2 2018, BLA submission planned

for H2 2018; EU and Japan submissions planned for 2019

AVXS-101-CL-101 study (n=15)

1. AAN Annual Meeting April 25, 2018 2. N Engl J Med 2017;377:1713-22 3. Event = Death or permanent ventilatory support , defined as ≥16 hrs/day of respiratory assistance continuously for ≥14 days in the absence of an acute, reversible

illness or perioperative state

2 1

Significant unmet need in SMA affecting 23,500 patients

worldwide1, 2

Potential for newborn

screening to transform

SMA patient care

All available treatments work

better when started earlier, lost

function unlikely to be regained

Type 1/2/3 categorization

expected to be replaced by SMN2

gene copy assessment and

genetic diagnosis of early-onset

or late-onset SMA

Clear progress in US newborn

screening for SMA; EU and other

countries also evaluating

34

Strong market opportunity for AVXS-101

Type 1 Type 2 Type 3 Type 4

SMN2 copy number 2 35 3 or 4 4 to 8

Onset Before 6 months 6-18 months Early childhood to early

adulthood (juvenile)

Adulthood (20s-30s),

usually after 30

Incidence split ~60% ~27% ~13% Uncommon/limited information available

Prevalence split3 ~14% ~51% ~35% Uncommon/limited information available

Est WW prevalent

population

~3,300 ~12,000 ~8200 Uncommon/limited information available

Development

milestones

Will never be able to sit

without support

Difficulty breathing/

swallowing

Cannot crawl/will never

walk

Will never be able to walk

without support

Most will never stand

without support

Stand unassisted and

walk independently, but

may lose ability to walk

over time

Stand alone and walk

but may lose ability to

walk in 30s-40s

Survival Over 90% die or have

significant critical event4 by

age 2

32% die before age 25 Normal Normal

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation

See slide 47 for references

Agenda

1 Focusing as a medicines company

2 Positioned for growth

3 Driving margin expansion

4 Leading innovation power

5 Alcon update

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation35

Alcon is the world leader in eye care devices today

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation36

SurgicalUSD 8 billion market growing +4% p.a.1

3.7

1.0

1.0

0.7

Revenue by eye care segmentFY 2017, USD billion

3.0

3.0

1.7

1.3

1. Based on Novartis analysis, company filings; Vision Care includes Ophthalmic OTC products. 2. J&J FY 2017 represents partial year reporting after AMO acquisition.

Vision CareUSD 12 billion market growing +4% p.a.1

2 2

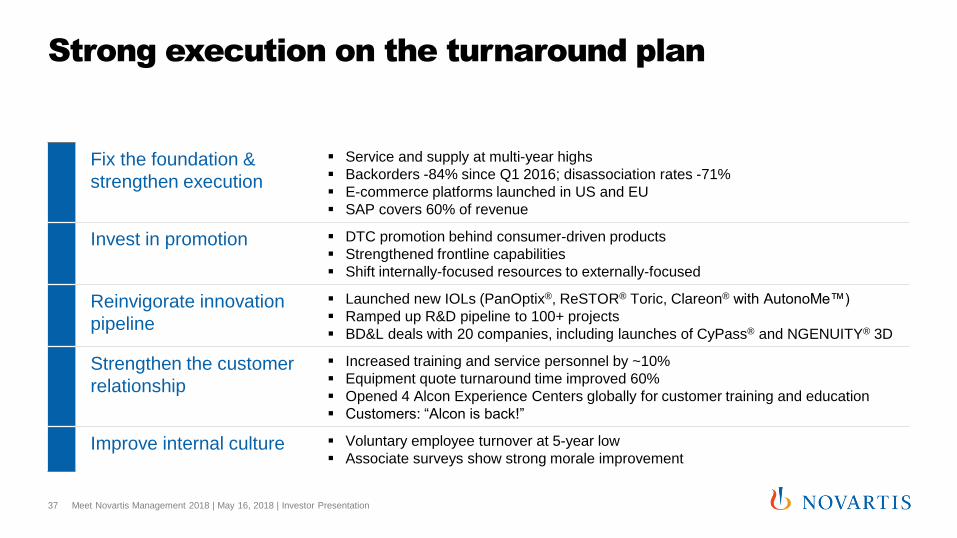

Strong execution on the turnaround plan

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation37

Fix the foundation &

strengthen execution

Service and supply at multi-year highs

Backorders -84% since Q1 2016; disassociation rates -71%

E-commerce platforms launched in US and EU

SAP covers 60% of revenue

Invest in promotion DTC promotion behind consumer-driven products

Strengthened frontline capabilities

Shift internally-focused resources to externally-focused

Reinvigorate innovation

pipeline

Launched new IOLs (PanOptix®, ReSTOR® Toric, Clareon® with AutonoMe™)

Ramped up R&D pipeline to 100+ projects

BD&L deals with 20 companies, including launches of CyPass® and NGENUITY® 3D

Strengthen the customer

relationship

Increased training and service personnel by ~10%

Equipment quote turnaround time improved 60%

Opened 4 Alcon Experience Centers globally for customer training and education

Customers: “Alcon is back!”

Improve internal culture Voluntary employee turnover at 5-year low

Associate surveys show strong morale improvement

Resulting in a return to growth in 2017

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation

Net sales growthvs. PY, % cc

38

Core margin %

excl. OTC

16.2% 17.0% 18.5% 17.1% 20.2%Core margin %

incl. OTC

13.2% 13.9% 15.6% 14.1%

1. Alcon sales growth benefitted from stock in trade movements, approx. 2% (cc) in Q3 2017, 1% (cc) in Q4 2017, and 1% (cc) in Q1 2018. 2. Alcon Division Q1 2018 growth rates and core margin include the Ophthalmic OTC products and a

small portfolio of surgical diagnostic products, transferred from the Innovative Medicines Division effective January 1, 2018, and are compared against the Q1 2017 updated financials including the aforementioned product transfer.

1,2

1%

3%

7%6%

7%

Q1 Q2 Q3 Q4 Q1

11

2017 2018

includes OTC

excludes OTC

We expect margins to be in line with the medical device industry average by 2022

Core margin evolution%, incl. OTC

Expected key drivers:

Top-line growth

New opportunities in high-

potential markets

Operational efficiencies

Long-term expect

mid-20’s core margin

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation39

17.3%20.2%

FY 2017 Q1 2018 2022

Low- to mid-20’s

Alcon has built a robust pipeline to fuel growth into the future

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation40

Surgical

Vision

Care

Recent launches 2018 – 2020 planned launches 2020+ planned launches

Clareon® with AutonoMe™ – EU

UltraSert™ – US/OUS

PanOptix® Trifocal – OUS

ReSTOR® Toric with

ACTIVEFOCUSTM – US

NGENUITY® 3D – US/OUS

Non-diffractive extended depth of focus

IOL – OUS

PanOptix® Trifocal – US

Clareon® with AutonoMe™ – US

ORA™ System with VerifEye™ Lynk –

US/OUS

4 major new IOL platforms

(e.g. accommodating)

Next generation cataract and

vitreoretinal technology platforms

Integrative technologies to connect

the clinic to the operating room

AIR OPTIX® plus HydraGlyde®

Dailies Total1® Multifocal

Clear Care® plus HydraGlyde®

AIR OPTIX® plus HydraGlyde®

(Toric and Multifocal lenses)

AIR OPTIX® Colors – 3 new colors

FRESHLOOK® – 5 new limbal lenses

Systane® Complete

New daily disposable lens

2 innovative new contact lens

platforms

Accommodating contact lens

Systane® Ultra

Systane® Hydration

Alcon summary

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation41

1 Alcon is the global leader in eye care devices, with leading positions in Surgical and Vision Care

2 The eye care industry is underpinned by favorable megatrends, including aging demographics,

expanding wealth, and significant market expansion opportunities

3 Alcon has a global footprint with significant sales and brand presence in all key markets

4 Alcon is differentiated by the strength of its customer relationships, breadth of portfolio and

powerful brands

5 Alcon continues to build on the momentum of a successful turnaround

6 Alcon expects to achieve a core margin in the mid-20% range in the long-term, driven by top-line

growth, operational efficiencies and new market expansion opportunities

Concluding thoughts

We have taken steps to focus the company and our

capital in areas where we have the key ingredients to lead

We are positioned to deliver sales growth and margin

expansion through 2022

We have pipeline depth in our key therapeutic areas, and

are building new, distinctive platform capabilities

Alcon is returning to a position of strength as the world’s

leading eye care devices company

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation42

Appendix

2018 pipeline milestones

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation44

H1 2018 H2 2018

Regulatory

decisions and

opinions

Kymriah® DLBCL (US) ✓ Aimovig™1 Migraine (EU) =

Tafinlar® + Mekinist® Adjuvant melanoma (US) ✓ Kymriah® Pediatric and young adult r/r ALL (EU) =

Lutathera® NET (US) ✓ Kymriah® DLBCL (EU) =

Gx Advair®2 Asthma, COPD (US) ✕ Tafinlar® + Mekinist® Adjuvant melanoma (EU) + ATC (US) (✓7)

Aimovig™1 Migraine (US) = Gilenya® Pediatric MS (US) ✓

Glatopa® 40mg Relapsing MS (US) ✓ GP2017 Adalimumab BS (EU) =

LA-EP2006 Peg-filgrastim BS (EU) =

GP1111 Infliximab BS (EU) =

GP20136 Rituximab BS (US) ✕

Submissions ACZ885 CV risk reduction (US/EU) ✓ BAF312 MS (EU) =

BAF312 MS (US) ✓ RTH258 nAMD (US/EU) =

Kisqali® Advanced BC (US/EU)3 = BYL719 HR+ BC (US/EU) =

Cosentyx® AS (JP) =

CTL019 Pediatric ALL + DLBCL (JP) =

Promacta® 1st line SAA (US/EU) =

Major trial

readouts

Kisqali® Advanced BC (MONALEESA-3) ✓ BYL719 HR+ BC =

LJN452 NASH = INC280 ALK- cMET amplified NSCLC =

Entresto® HFpEF (interim analysis) =

✓ Achieved ✕ Missed = On track

1. Aimovig™ is developed in collaboration with Amgen. The brand name Aimovig™ has been provisionally approved by the FDA and EMA for the investigational product AMG 334 (erenumab), bu t the product itself has not been approved for

sale in any country 2. Complete Response Letter received from FDA after Q4 2017 results; Advair® is a registered trademark of Glaxo Group Ltd. 3. Indication expansion based on MONALEESA-3 & 7 results

4. Positive CHMP opinion received 5. Data to be presented at ASCO 6. Complete Response Letter received from FDA after Q1 2018 results 7. US approval in ATC received; EU approval in adj. melanoma still outstanding

5

4

1. Secondary prevention of cardiovascular events

2. Diffuse large B-cell lymphoma

3. Severe aplastic anemia

4. Chronic myeloid leukemia

5. Long-acting release

6. Non-small cell lung cancer

7. Neovascular age-related macular degeneration

8. Multi-drug resistant

9. Breast cancer

10. Retinopathy of prematurity

11. Indolent Non-Hodgkin’s lymphoma

12. Non-radiographic axial spondyloarthritis

13. Preserved ejection fraction

14. Graft-versus-host disease

15. Neuroendocrine tumors

16. Chronic spontaneous urticaria / chronic idiopathic urticaria

17. Psoriatic arthritis head-to-head study versus adalimumab

18. Non-alcoholic steatohepatitis

19. Ankylosing spondylitis head-to-head study versus adalimumab

20. Acute myeloid leukemia

21. Chronic Obstructive Pulmonary Disease

22. Chronic Lymphocytic Leukemia

23. Exact language of indication pending regulatory interactions

Planned filings 2018 to 2022

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation45

2022202020192018 2021

a) EU filing, approved in US.

b) US filing, approved in EU.

c) US filing, submitted in EU.

d) Lubris LLC transaction announced in April 2017.

e) Conatus transaction for exclusive global license for

emricasan announced in May 2017.

Combination abbreviations:

fulv fulvestrant

tmx tamoxifen

gsn goserelin

NSAI Non-steroidal aromatase inhibitor

Taf Tafinlar® (dabrafenib)

Mek Mekinist® (trametinib)

LCI699Cushing’s disease

BAF312SPMS22

BYL719 + fulvHR+, HER2 (-) postmenopausal

adv. BC9 2nd line

RTH258nAMD7

LAM320MDR8 tuberculosis

Lucentis®

ROP10

Kisqali® + fulvHR+, HER2 (-) postmenopausal

adv. BC9 1st/2nd line

Kisqali® + tmx + gsn/or NSAI + gsnHR+, HER2 (-) premenopausal

adv. BC9 1st line

Promacta®/Revolade®

SAA3 1st line

BYM338Sarcopenia

VAY736Primary Sjoegren’s syndrome

QBW251COPD21

Kisqali®HR+, HER2 (-) BC9 (adjuvant)

Cosentyx®

AS H2H19

Rydapt®AML20 (FLT3 wild type)

INC280NSCLC6 (EGFRm)

VAY785e

NASH18

VAY736Autoimmune Hepatitis

CTL019 (Kymriah® US)+ pembrolizumab - r/r DLBCL

ACZ885Adjuvant NSCLC

ACZ8851st Line NSCLC

ABL001CML4 1st line

CTL019 (Kymriah® US)r/r DLBCL in 1st relapse

Entresto®

Heart failure (PEF)13

INC280 NSCLC6

Cosentyx®

nrAxSpA12

OMB157Relapsing multiple sclerosis

SEG101Sickle cell disease

LA-EP2006 (pegfilgrastim, US)Chemotherapy-induced neutropenia

and others (same as originator)

PDR001 + Tafinlar ® + Mekinist ®

Metastatic BRAF V600+ melanoma

QVM149Asthma

QMF149Asthma

QGE031CSU/CIU16

ZPL389Atopic dermatitis

UNR844Presbyopia

LMI070Spinal muscular atrophy

ACZ8852nd Line NSCLC

CTL019 (Kymriah® US)CLL22

PDR001Metastatic Melanoma

MTV273Multiple myeloma

ABL001CML4 3rd line

Entresto®

Post-acute myocardial infarction

RTH258Diabetic macular edema

QAW039Asthma

Arzerra®

iNHL11 (refractory)

Jakavi®Acute GVHD14

Cosentyx®

PsA H2H17

Jakavi®Chronic GVHD14

XolairNasal Polyps

CTL019 (Kymriah® US)r/r Follicular Lymphoma

EGF816 NSCLC2

MAA868Stroke prevention in atrial fibrillation

KAE609Malaria

EMA401Peripheral neuropathic pain

CNP520Alzheimer’s disease

BYM338Hip fracture recovery

KAF156 Malaria

LJN452NASH18

ECF843d

Dry eye

CAD106Alzheimer’s disease

LHW090Resistant hypertension

HDM201Acute myeloid leukemia

LOU064Chronic spontaneous urticaria

CFZ533Solid Organ Transplant

New molecule

New indication

New formulation

Biosimilars

AVXS-101Spinal muscular atrophy23

Key definitions and trademarks

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation46

This presentation contains several important words or phrases that we define as below:AAA: Advanced Accelerator Applications

ADHF: Acute decompensated heart failure

AE: Adverse Event

ALK: Anaplastic lymphoma kinase

ALL: Acute lymphatic leukemia

AMD: Age-Related Macular Degeneration

AMI: Acute myocardial infection

AML: Acute myeloid leukemia

Approval: In Pharmaceuticals and Alcon in US and EU; each indication and regulator combination counts as

approval; excludes label updates, CHMP opinions alone and minor approvals

aRCC: advanced renal cell cancer

ARNI: Antiogensin receptor neprilysin inhibitor

AS: Ankylosing Spondylitis

ASM: Aggressive systemic mastocytosis

ATC: Anaplastic thyroid cancer

BC: Breast cancer

BCMA: B-cell maturation antigen

BCVA: best corrected visual acuity

BS: Biosimilars

BTD: Breakthrough therapy designation

CGRP: Calcitonin gene-related peptide

CLL: Chronic lymphocytic leukemia

cITP: Chronic immune thrombocytopenia

CM: Chronic migraine

CML: Chronic myeloid leukemia

COPD: Chronic Obstructive Pulmonary Disease

CR: complete remission

CRC: Colorectal Cancer

CRi: Complete remission with incomplete blood count recovery

CSU / CIU: Chronic spontaneous urticaria / Chronic idiopathic urticaria

CVRR: Cardiovascular risk reduction

DLBCL: Diffuse large B-cell lymphoma

DMC: Data monitoring committee

EDSS: Expanded Disability Status Scale

EF: ejection fraction

EM: Episodic migraine

FL: Follicular lymphoma

FPFV: First patient first visit

GBM: Glioblastoma multiforme

GvHD: graft vs. host disease

HbA1C: Glycated hemoglobin

HCC: Hepatocellular carcinoma

HF: Heart failure

HF-pEF: Heart failure with preserved ejection fraction

HFrEF: Heart failure with reduced ejection fraction

HR+/HER2- mBC:Hormone Receptor positive / Human Epidermal growth factor receptor 2 negative metastatic

breast cancer

ITP: Immune thrombocytopenia

LoE: Loss of exclusivity

MF: Myelofibrosis

M/M: Multiple myeloma

MI: Myocardial infarction

MS: Multiple sclerosis

NASH: Non-Alcoholic Steatohepatitis

NET: Neuroendocrine tumor

New assets: Assets acquired in the GSK transaction which closed on March 2, 2015

NSAI: Nonsteroidal aromatase inhibitor

NSCLC: Non-small cell lung cancer

NTD: New Therapeutic Drug

ORR: Overall response rate

OS: Overall survival

PA: Prior authorization

PASI 90: 90% reduction in Psoriasis Area Severity Index from baseline

PFS: Progression free survival

PsA: Psoriatic arthritis

PsO: Psoriasis

PV: Polycythemia vera

PY: Prior year

QoL: Quality of Life

RCC: Renal cell cancer

ROP: Retinopathy of prematurity

r/r ALL: relapsed/refractory acute lymphoblastic leukemia

RRMS: relapsing-remitting multiple sclerosis

SAA: Severe aplastic anemia

scFv: Single chain variable fragment

SCPC: Sickle cell pain crisis

SpA: Spondyloarthropathy

SPMS: Secondary progressive multiple sclerosis

TFR: Treatment-free Remission

TNBC: Triple negative breast cancer

Trademarks

Eylea® is a registered trademark of Regeneron Pharmaceuticals, Inc.

Enbrel®, Epogen® and Neulasta® are a registered trademark of Amgen Inc.

Humira® is a registered trademark of AbbVie Ltd.

MabThera® is a registered trademark of Roche, Ltd.

Procrit® is a registered trademark of Janssen Products, LP.

Remicade® and Stelara® are registered trademarks of Janssen Biotech, Inc.

Rituxan® is a registered trademark of Biogen Inc

References

Meet Novartis Management 2018 | May 16, 2018 | Investor Presentation47

1. NBRx Share in Rheum / Derm specialty, IMS NBRx allocated using SHS APLD Factors where only PsO/PsA/AS uses are carved in for TNFs. IMS NPA restated as of week ending August 11, 2017 to

include Cosentyx® free drug access program. Data as of week ending March 30, 2018. Market definition includes Cosentyx®, Enbrel®, Humira®, Taltz®, Stelara®, Tremfya®, Siliq® (Includes Cimzia® and

Simponi® for Rheumatology). All trademarks are the property of their respective owners. 2. Secukinumab USPI, Secukinumab SmPC, Bissonnette R, et al. JEADV 2018;doi: 10.1111/jdv.14878 (e-pub

ahead of print), Reich K, et al. PGC 2017;Poster 021; Bagel J, et al. JAAD 2017;77:667, Gottlieb AB, et al. PGC 217;Poster 026, McInnes IB, et al. Rheumatol 2017;56:1993 3. US data, NBRx and TRx

across specialties from week ending July 10, 2015 to March 30, 2018 (Source: IMS) 4. Chandra, A et al. The Effects of Sacubitril/Valsartan on Physical and Social Activity Limitations in Heart Failure

Patients: The PARADIGM-HF Trial. JAMA Cardiol. 2018. 5. Benjamin E. J et al. Heart disease and stroke statistics 2017 update: a report from the American Heart Association. Circulation 135, e146–

e603 2017

Slide 16: Cosentyx® & Entresto®

1. Aimovig™ is developed in collaboration with Amgen. The brand name Aimovig™ has been provisionally approved by the FDA and EMA for the investigational product AMG 334 (erenumab), but the

product itself has not been approved for sale in any country 2. Reuter, et al. Presented at: American Academy of Neurology Annual Meeting; April 21–27, 2018; Los Angeles CA, USA. Oral Presentation

P009. 3. Kappos L, et al. Lancet Neurology 2018; 391: 1263-1273 4. Primary Endpoint. Dugel PU, et al. AAO 2017 [Oral presentation]. 5. Prespecified secondary endpoint in both HAWK and

HARRIER with confirmatory analysis in HAWK (brolucizumab 6 mg vs aflibercept 2 mg 6. Prespecified secondary endpoint in both HAWK and HARRIER with confirmatory analysis in HAWK

(brolucizumab 6 mg vs aflibercept 2 mg).

Slide 20: Upcoming launches

1. Established markets estimate: US, Japan, EU15, Australia, Canada, Turkey 2. Estimated incidence of SMA is 1 out of 6,000 births; there were 3.95 million births in the US in 2016 (per CDC Center

for Health Statistics) 3. Spinal Muscular Atrophy: Introduction to SMA families: SMA Foundation 4. Event = Death or >= 16 hr/day ventilation continuously for >=2 weeks, in the absence of acute

reversible illness 5. 100% have 3 copies (PNCR)

Slide 34: AVXS-101

1. IMS Market Prognosis China Q3 2017, Novartis analysis, FX is 6.86. As IMS MIDAS database has low coverage of retail channel, actual China pharmaceutical market sales exceed figures shown above. Total Chinese Pharma market sales are projected to exceed USD 200 bn by 2020 2. NRDL – China’s National Reimbursement Drug List; Negotiation products are not included in this chart; Lucentis and Afinitor have entered China negotiation list for high value drugs 3. Source: GBI report. China CFDA/CDE website. Refer to only new molecular entities and indication expansion is not included 4. For Novartis 6 new molecular entities approvals: Entresto, Xolair, Ultibro, Jakavi, Votrient, Revolade

Slide 21: China