notes on the financial statements - hong kong … airport authority hong kong annual report 2004/05...

TRANSCRIPT

72 Airport Authority Hong Kong Annual Report 2004/05

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

1. Establishment of the AuthorityThe Airport Authority (“Authority”) is a statutory corporation wholly owned by the Government of the Hong Kong

Special Administrative Region (“the Government”). It was formally established on 1 December 1995 when the

Airport Authority Ordinance (“the Ordinance”) was brought into effect as a continuation of the Provisional Airport

Authority which had been set up in 1990.

The Authority’s statutory purpose is to provide, operate, develop and maintain Hong Kong’s airport at Chek Lap

Kok, in order to maintain Hong Kong’s status as a centre of international and regional aviation. Pursuant to these

purposes, the Authority may also engage in airport-related activities in trade, commerce or industry at Chek Lap

Kok and is permitted to engage in or carry out airport-related activities at any place in or outside Hong Kong. The

Authority is required under the Ordinance to conduct its business according to commercial principles.

Under the Land Grant signed on 1 December 1995, the Government has granted to the Authority up to the year

2047 the legal rights to the entire airport site at Chek Lap Kok together with the rights necessary to develop such

site for the purposes of its business.

2. Principal Activities of the Authority

The Authority’s principal activities are the management, operation, planning and development of the Hong Kong

International Airport at Chek Lap Kok. It also engages in airport-related commercial and industrial activities at

Chek Lap Kok.

The Authority’s subsidiaries, Aviation Security Company Limited and HKIA Information Services Limited are

engaged in the provision of aviation security services at the airport and the provision of airline ticketing

information services respectively.

3. Significant Accounting Policies(a) Statement of compliance

The financial statements have been prepared in accordance with all applicable Statements of Standard

Accounting Practice (“SSAP”) and Interpretations issued by the Hong Kong Institute of Certified Public

Accountants (“HKICPA”), accounting principles generally accepted in Hong Kong and so as to comply with

the disclosure provisions of the Hong Kong Companies Ordinance. A summary of the significant accounting

policies adopted is set out below.

(b) Basis of preparation

The measurement basis used in the preparation of the financial statements is historical cost modified by the

revaluation of other investments as explained in the relevant accounting policy.

The group’s financial statements include the financial statements of the Authority and its subsidiaries made up to

the balance sheet date. All material intercompany transactions and balances are eliminated on consolidation.

(c) Interests in subsidiaries

A subsidiary is a company in which the Authority, directly or indirectly, holds more than half of the issued share

capital, or controls more than half of the voting power, or controls the composition of the board of directors.

Interests in subsidiaries in the Authority’s balance sheet is stated at cost less any impairment loss.

Minority interests represent the interests of outside shareholders in the operating results and net assets

of subsidiaries.

73Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(d) Other investments

Investments held on a continuing basis for an identified long term purpose are classified as other

investments. Other investments are accounted for in the consolidated financial statements at their fair

values. A gain or loss on valuation on such investments is recognised directly in equity, until they are

disposed of or until they are determined to be impaired, at which time the cumulative gain or loss is included

in the income statement for the period.

(e) Fixed assets

(i) Fixed assets are stated at cost less accumulated depreciation and impairment losses (note 3(g)).

(ii) Subsequent expenditure relating to a fixed asset that has already been recognised is added to the

carrying amount of the asset when it is probable that future economic benefits, in excess of the

originally assessed standard of performance of the existing asset, will flow to the group.

Repairs and maintenance expenditure to restore or maintain the originally assessed standard of

performance of fixed assets is charged to the income statement as and when incurred.

(iii) Gains or losses arising from the retirement or disposal of a fixed asset are determined as the difference

between the net disposal proceeds and the carrying amount of the asset and are recognised as

income or expense in the income statement on the date of retirement or disposal.

(iv) Leases of assets under which the group assumes substantially all the risks and benefits of ownership

are classified as finance leases and treated as if the group owned the assets outright. Leases of

assets under which the group has not been transferred all the risk and benefits of ownership are

classified as operating leases.

When the group leases out assets under operating leases, the assets are included in the balance sheet

according to their nature and, where applicable, are depreciated in accordance with the group’s

depreciation policies set out in note 3(f) below. Revenue arising from operating leases is recognised

in accordance with the group’s revenue recognition policies set out in note 3(h) below.

(v) Construction in progress

Assets under construction and capital works for the operating airport are stated at cost. Costs

comprise direct costs of construction, such as materials, staff costs and overheads, as well as net

borrowing costs (note 3(k)) capitalised during the period of construction or installation and testing.

Capitalisation of these costs ceases and the asset concerned is transferred to fixed assets when

substantially all the activities necessary to prepare the asset for its intended use are completed, at

which time it commences to be depreciated in accordance with the policy detailed in note 3(f).

(f) Depreciation

Fixed assets are depreciated on a straight-line basis so as to write off the cost of the assets over their

estimated useful lives.

Following a review undertaken during the year, the estimated useful lives of certain fixed assets were revised

with effect from 1 April 2004, resulting in a net increase in the Authority’s annual depreciation charge of

approximately $106 million.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

74 Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(f) Depreciation (continued)

The estimated useful lives are:

Leasehold land 100 years

Airfields:

Runways, taxiways, aprons and tunnels 10 – 75 years

Lighting and other airfield facilities 10 – 50 years

Terminal complexes:

Building structure 50 – 75 years

Building services and fit-outs 25 years

Access, utilities, other buildings and support facilities:

Roads and bridges 75 years

Other building and support facilities 50 years

Utility supply equipment 25 years

Systems, installations, plant and equipment 5 – 20 years

Furniture, fixtures and equipment 5 – 10 years

The above useful lives assume that the Land Grant referred to in note 9(c) on the financial statements will be

renewed upon its expiry on 30 June 2047 for a period of at least 50 years (note 3(s)(i)).

(g) Impairment of assets

The carrying amount of fixed assets is reviewed annually in order to determine whether there is any

indication of impairment. If any such indication exists, the recoverable amount is estimated. An impairment

loss is recognised whenever the carrying amount exceeds the recoverable amount. Impairment losses are

recognised as an expense in the income statement.

The recoverable amount of an asset is the greater of its net selling price and value in use.

An impairment loss is reversed if there has been a change in the estimates used to determine the

recoverable amount. A reversal of impairment loss is limited to the assets’ carrying amount that would have

been determined had no impairment loss been recognised in prior years. Reversals of impairment losses are

credited to the income statement in the year in which the reversals are recognised.

(h) Revenue recognition

Provided it is probable that the economic benefits will flow to the group and the revenue and costs, if

applicable, can be measured reliably, revenue is recognised in the income statement as follows:

(i) Airport charges, representing landing charges, parking charges and terminal building charges are

recognised when the airport facilities are utilised.

(ii) Security charges in respect of aviation security services to passengers are recognised when the airport

facilities are utilised.

(iii) Aviation security services revenue from the provision of security services to airlines, franchisees and

licensees is recognised when the services are rendered.

75Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(h) Revenue recognition (continued)

(iv) Franchise revenue from awarded airside support services, retail revenue from awarded retail

licences, other terminal commercial revenue from leasing of check-in counters and airline office

rental and other service revenue and recoveries, are recognised on an accruals basis in accordance

with the related agreements.

(v) Real estate revenue arising from sub-leases of land or property is recognised in the income statement

on a straight-line basis over the periods of the leases. Amounts received in advance in respect of sub-

leases of land granted are accounted for as deferred income and are recognised in the income

statement on a straight line basis over the periods of the respective sub-leases.

(vi) Amounts received in advance in respect of lease-out/lease-back and franchise facility payment

agreements are accounted for as deferred income and are recognised in the income statement over

the period of the respective agreements.

(vii) Interest income is recognised on a time-apportioned basis by reference to the principal outstanding

and at the rate applicable.

(i) Defeasance of long-term lease payments

Where commitments to make long-term lease payments have been defeased by the placement of security

deposits, those commitments and deposits (and income and charges arising therefrom) have been netted

off, in order to reflect the overall commercial substance of the arrangement. Such netting-off has been

effected where the group has the ability to insist on net settlement of the commitments and the deposits.

(j) Stores and spares

Stores and spares are stated at cost, computed on a weighted average basis, less provision for

obsolescence. When stores and spares are consumed, the carrying amount of these stores and spares is

recognised as an expense in the year in which the consumption occurs. Any obsolete and damaged stores

and spares are written off to the income statement.

(k) Interest-bearing borrowings and borrowing costs

Notes issued by the Authority are stated in the balance sheet at their face values. Premiums and discounts

arising from their issuance are amortised to the income statement over the term of the respective notes.

Borrowing costs are expensed in the income statement in the period in which they are incurred except to

the extent that they are capitalised as being directly attributable to the acquisition, construction or

production of an asset which necessarily takes a substantial period of time to get ready for its intended use.

Borrowing costs include interest and finance charges on borrowing, amortisation of discounts net of

premiums relating to borrowing and differences in amounts paid and received on interest rate swap

agreements entered into for hedging purposes.

(l) Translation of foreign currencies

Foreign currency transactions during the year are translated into Hong Kong dollars at the exchange rates

ruling at the transaction dates. Monetary assets and liabilities in foreign currencies are translated into Hong

Kong dollars at the market rates of exchange ruling at the balance sheet date. Exchange gains and losses

are dealt with in the income statement.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

76 Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(m) Off-balance sheet financial instruments

Where non-speculative forward exchange contracts are used as hedges of monetary assets or liabilities, the

gains or losses on the contracts are taken to the income statement and the discounts or premiums are

amortised over the periods of the contracts.

Gains or losses arising on interest rate derivatives, which are used as hedges of risks associated with the

interest on floating/fixed rate borrowings are recognised in the income statement over the periods of the

respective instruments.

(n) Provisions and contingent liabilities

Provisions are recognised for liabilities of uncertain timing or amount when there is a legal or constructive

obligation arising as result of a past event, and it is probable that an outflow of economic benefits will be

required to settle the obligations and a reliable estimate can be made. Where the time value of money is

material, provisions are stated at the present value of the expenditure expected to settle the obligation.

Where it is not probable that an outflow of economic benefits will be required, or the amount cannot be

estimated reliably, the obligation is disclosed as a contingent liability, unless the probability of outflow of

economic benefits is remote.

(o) Employee benefits

(i) Salaries, performance awards, paid annual leave and the cost to the group of non-monetary benefits

are accrued in the year in which the associated services are rendered by employees of the group.

(ii) Contributions to defined contribution schemes, such as Mandatory Provident Funds as required under

the Hong Kong Mandatory Provident Fund Schemes Ordinance, are recognised as an expense in the

income statement as incurred.

(iii) The group’s net obligation in respect of defined benefit retirement plans is calculated by estimating the

amount of future benefit that employees have earned in return for their service in the current and prior

periods; that benefit is discounted to determine the present value, and the fair value of any plan assets

is deducted. The discount rate is the yield at the balance sheet date on high quality corporate bonds

that have maturity dates approximating the terms of the group’s obligations. If there is no deep market

in such bonds, the market yield in government bonds would be used. The calculation is performed by

a qualified actuary using the projected unit credit method.

When the benefits of a plan are improved, the portion of the increased benefit relating to past service

by employees is recognised as an expense in the income statement on a straight-line basis over the

average period over which the benefits are vested. To the extent that the benefits vest immediately,

the expense is recognised immediately in the income statement.

In calculating the group’s obligation in respect of a plan, to the extent that any cumulative

unrecognised actuarial gain or loss exceeds ten percent of the greater of the present value of the

defined benefit obligation and the fair value of plan assets, that portion is recognised in the income

statement over the expected average remaining working lives of the employees participating in the

plan. Otherwise, the actuarial gain or loss is not recognised.

77Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(o) Employee benefits (continued)

(iii) (continued)

Where the calculation of the group’s net obligation results in a negative amount, the asset recognised is

limited to the net amount of the present value of any future refunds from the plan or reductions in future

contributions to the plan less any cumulative unrecognised net actuarial losses and past service costs.

(p) Income tax

(i) Income tax for the year comprises current tax and movements in deferred tax assets and liabilities.

Current tax and movements in deferred tax assets and liabilities are recognised in the income

statement except to the extent that they relate to items recognised directly in equity, in which case

they are recognised in equity.

(ii) Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or

substantively enacted at the balance sheet date, and any adjustment to tax payable in respect of

previous years.

(iii) Deferred tax assets and liabilities arise from deductible and taxable temporary differences

respectively, being the differences between the carrying amounts of assets and liabilities for financial

reporting purposes and their tax bases. Deferred tax assets also arise from unused tax losses and

unused tax credits.

Apart from certain limited exceptions, all deferred tax liabilities, and all deferred tax assets to the extent

that it is probable that future taxable profits will be available against which the asset can be utilised,

are recognised.

The amount of deferred tax recognised is measured based on the expected manner of realisation or

settlement of the carrying amount of the assets and liabilities, using tax rates enacted or substantively

enacted at the balance sheet date. Deferred tax assets and liabilities are not discounted.

The carrying amount of a deferred tax asset is reviewed at the balance sheet date and is reduced to

the extent that it is no longer probable that sufficient taxable profit will be available to allow the related

tax benefit to be utilised. Any such reduction is reversed to the extent that it become probable that

sufficient taxable profit will be available.

Current tax balances and deferred tax balances, and movements therein, are presented separately

from each other and are not offset. Current tax assets are offset against current tax liabilities, and

deferred tax assets against deferred tax liabilities if, and only if, the company or the group has the

legally enforceable right to set off current tax assets against current tax liabilities and the following

additional conditions are met:

– in the case of current tax assets and liabilities, the Authority or the group intends either to settle

on a net basis, or to realise the asset and settle the liability simultaneously; or

– in the case of deferred tax assets and liabilities, if they relate to income taxes levied by the same

taxation authority on the same taxable entity or different taxable entities, which, in each future

period in which significant amounts of deferred tax liabilities or assets are expected to be settled

or recovered, intend to realise the current tax assets and settle the current tax liabilities on a net

basis or realise and settle simultaneously.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

78 Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(q) Related parties

For the purposes of these financial statements, parties are considered to be related to the group if the group

has the ability, directly or indirectly, to control the party or exercise significant influence over the party in

making financial and operating decisions, or vice versa, or where the group and the party are subject to

common control or common significant influence. Related parties may be individuals or other entities.

(r) Cash equivalents

Cash equivalents are short-term, highly liquid investments which are readily convertible into known amounts

of cash without notice and which were within three months of maturity when acquired. For the purposes of

the cash flow statement, cash equivalents also includes overdrafts and advances from banks which are

repayable on demand and form an integral part of the group’s cash management.

(s) Recently issued accounting standards

The HKICPA has issued a number of new and revised Hong Kong Financial Reporting Standards and Hong

Kong Accounting Standards (“new HKFRSs”) which are effective for accounting periods beginning on or

after 1 January 2005. The group has not early adopted these new HKFRSs in its financial statements for the

year ended 31 March 2005. However, the group has been carrying out an assessment of the impact of

these new HKFRSs and so far considers that the adoption of the revised standards may have a significant

impact to its financial statements as described below:

(i) Hong Kong Accounting Standard 17 (“HKAS 17”) on leases

The adoption of HKAS 17 would require operating leasehold land to be classified as leasehold land

and the lease premium for land to be recognised as an expense on a straight-line basis or other

systemic basis over the lease term.

Draft Interpretation 25 on “Leases-Determination of the Length of Lease Term in respect of Hong Kong

Land Leases” issued for consultation on 17 March 2005 by the HKICPA provides guidance on the

determination of the length of lease term of a Hong Kong land lease for the purpose of applying the

depreciation requirements under HKAS 16 on “Property, plant and equipment” and HKAS 17. The

Draft Interpretation does not allow lessees to take the assumption that Hong Kong land leases will be

extended for another 50 years, or any other period, upon expiry, while the Government retains the sole

discretion as to whether to renew.

If the Draft Interpretation is adopted by the HKICPA in its current form, the Authority’s current practice

of assuming the Land Grant will be renewed upon its expiry on 30 June 2047 for a period of at least 50

years will not be permitted. Accordingly, the current depreciation policy of 100 years for leasehold

land and 75 years for certain building, airfield and access assets would require to be revised. The

potential effect of this change would be an annual increase in depreciation of approximately $200

million commencing 2005/06.

The Authority is currently in discussion with the Government with regard to the Land Grant and the

arrangements upon its expiry.

79Airport Authority Hong Kong Annual Report 2004/05

3. Significant Accounting Policies (continued)

(s) Recently issued accounting standards (continued)

(ii) Hong Kong Accounting Standards 32 & 39 (“HKASs 32 & 39”) on financial instruments

The adoption of HKASs 32 and 39 would require all financial instruments which the group is using to

hedge the interest rate and currency risks of its borrowings to be marked to market, with change in

their fair values recognised in the income statement directly. The standard allows the application of

hedge accounting, that is, to use the change in fair value of the underlying hedged items to offset this

impact. Should there be inefficiency in the hedging relationship to the extent that the opposing

impacts do not cancel each other out, there will be a net residual impact to the income statement.

Given that hedge efficiency is affected by a number of factors including the nature of the hedging

relationship, direction of interest rates and changes in foreign exchange rates, it is difficult to forecast

and control this residual impact.

It should be noted, however, that these accounting changes are non-cash items and hence do not affect

cashflow.

The group will continue to assess the impact of other new HKFRSs and other changes may be identified as

a result. However, it is not currently expected that these will have a significant impact on the group’s

financial statements.

4. Operating Profit Before Interest and Finance ChargesOperating profit before interest and finance charges of the group and the Authority are after charging:

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Auditors’ remuneration 2 2 2 2

Stores and spares expensed 53 65 53 65

Loss on disposal of fixed assets 124 91 124 91

Auditors’ remuneration includes charges for audit services only. Auditors’ remuneration with respect to non audit

services is immaterial for 2004 and 2005.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

80 Airport Authority Hong Kong Annual Report 2004/05

5. Members of the Board and Executive Directors’ Remuneration(a) The remuneration of the Members of the Board and the Executive Directors are as

follows:

2005 2004$ million $ million

Fees paid to non-executive Members of the Board 1 1

Remuneration of Chief Executive Officer and Executive Directors

– base salaries, allowances and other benefits in kind 17 18

– performance-related compensation paid 3 4

– retirement scheme contributions 1 1

– gratuities in lieu of retirement scheme contributions 1 1

22 24

(i) The fees disclosed include those payable in respect of Members who are public officers which are

paid directly to the Government rather than to the individuals concerned.

(ii) For purposes of meaningful comparison, gratuities in lieu of retirement scheme contributions are

disclosed on an accruals basis, notwithstanding the contractual entitlement and date of payment.

(b) The remuneration of the Members of the Board and Executive Directors are within thefollowing bands:

2005 2004Number Number

$0 – $250,000 12 13

$1,000,001 – $1,500,000 1 –

$2,500,001 – $3,000,000 1 1

$3,000,001 – $3,500,000 – 2

$3,500,001 – $4,000,000 3 2

$6,500,001 – $7,000,000 1 –

$7,000,001 – $7,500,000 – 1

18 19

The information shown in the above table includes the five highest paid employees. Remuneration paid to

non-executive Members of the Board is included in the first remuneration band.

81Airport Authority Hong Kong Annual Report 2004/05

5. Members of the Board and Executive Directors’ Remuneration (continued)

(c) The remuneration details of the Chief Executive Officer and Executive Directors areshown below:

Base salaries, Retirementallowances Performance- contributions/

and benefits related gratuitiesin kind compensation in lieu Total

$ million $ million $ million $ million

2005

Chief Executive Officer 4.7 1.5 0.6 6.8

Commercial Director 3.0 0.4 0.3 3.7

Finance Director 3.0 0.4 0.3 3.7

Airport Management Director 2.9 0.4 0.3 3.6

Human Resources and

Administration Director* 1.0 0.4 0.1 1.5

Legal Director and Secretary 2.3 0.2 0.2 2.7

16.9 3.3 1.8 22.0

2004

Chief Executive Officer 4.7 1.9 0.5 7.1

Commercial Director 3.0 0.4 0.3 3.7

Finance Director 3.0 0.4 0.3 3.7

Airport Management Director 2.7 0.4 0.3 3.4

Human Resources and

Administration Director 2.6 0.5 0.2 3.3

Legal Director 2.3 0.2 0.2 2.7

18.3 3.8 1.8 23.9

* Left office in August 2004 and not replaced.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

82 Airport Authority Hong Kong Annual Report 2004/05

6. Staff Costs and Related Expenses

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Costs for defined contribution plan 28 26 10 9

Costs for defined benefit plan (note 12(a)) 30 29 30 29

Retirement costs 58 55 40 38

Salaries, wages and other benefits 868 848 482 463

926 903 522 501

7. Finance Costs

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Interest on bank loans repayable within five years 16 20 16 20

Interest on notes issued 266 229 266 229

Other borrowing costs 12 6 12 6

294 255 294 255

Less: Borrowing costs capitalised into

construction in progress (8) – (8) –

286 255 286 255

The borrowing costs have been capitalised at the average cost of funds to the group calculated on a monthly

basis. The average interest rate for the year was 2.3% per annum.

8. Taxation(a) Taxation in the consolidated income statement represents:

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Current tax – Provision for Hong Kong

profits tax for the year (note 8(c)) 2 – – –

Deferred taxation (note 8(d))

– Net increase in temporary differences 320 102 320 102

322 102 320 102

83Airport Authority Hong Kong Annual Report 2004/05

8. Taxation (continued)

(b) Reconciliation between tax expense and accounting profit at applicable tax rate:

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Profit before tax 1,736 488 1,732 490

Notional tax on profit before tax 304 86 303 86Tax effect of non-deductible expenses 18 17 17 17Tax effect of non-taxable revenue – (1) – (1)

Actual tax expense 322 102 320 102

(c) Taxation in the balance sheets represents:

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Provision for Hong Kong profits taxfor the year (note 8(a)) 2 – – –

Provisional profits tax paid (1) – – –

1 – – –

No provision for Hong Kong profits tax has been made in the financial statements in respect of the Authority

as the current year taxable income has been offset against carried forward tax losses. Provision for Hong

Kong profits tax is in respect of a subsidiary calculated at 17.5% of its estimated assessable profits.

(d) Deferred tax assets and liabilities recognised:

The components of deferred tax (assets)/liabilities of the Authority and the group recognised in the balance

sheet and the movements during the year are as follows:

Depreciationallowances

in excessof related Deferred Estimated

depreciation income tax losses Total$ million $ million $ million $ million

Deferred tax arising from:At 1 April 2003 2,796 (463) (2,210) 123Charged/(credited) to consolidated

income statement 415 (233) (80) 102

At 31 March 2004 3,211 (696) (2,290) 225

At 1 April 2004 3,211 (696) (2,290) 225Charged/(credited) to consolidated

income statement (21) (13) 354 320

At 31 March 2005 3,190 (709) (1,936) 545

There is no significant deferred taxation not provided for at the balance sheet date.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

84 Airport Authority Hong Kong Annual Report 2004/05

9. Fixed Assets(a) The group

Access,Utilities,

Other Systems,Buildings Installations, Furniture,

Leasehold Terminal & Support Plant & Fixtures & ConstructionLand Airfields Complexes Facilities Equipment Equipment in Progress Total

$ million $ million $ million $ million $ million $ million $ million $ million

Cost

At 1 April 2004 11,571 6,726 20,376 11,790 6,810 1,142 236 58,651

Additions – 213 136 47 178 30 687 1,291

Disposals – (8) (66) (44) (74) (83) – (275)

At 31 March

2005 11,571 6,931 20,446 11,793 6,914 1,089 923 59,667

Depreciation

At 1 April 2004 731 643 2,909 1,705 3,502 764 – 10,254

Charge for

the year 116 215 544 297 400 113 – 1,685

Written back

on disposal – (1) (16) (9) (43) (81) – (150)

At 31 March

2005 847 857 3,437 1,993 3,859 796 – 11,789

Net Book

Value

At 31 March

2005 10,724 6,074 17,009 9,800 3,055 293 923 47,878

At 31 March

2004 10,840 6,083 17,467 10,085 3,308 378 236 48,397

85Airport Authority Hong Kong Annual Report 2004/05

9. Fixed Assets (continued)

(b) The Authority

Access,Utilities,

Other Systems,Buildings Installations, Furniture,

Leasehold Terminal & Support Plant & Fixtures & ConstructionLand Airfields Complexes Facilities Equipment Equipment in Progress Total

$ million $ million $ million $ million $ million $ million $ million $ million

Cost

At 1 April

2004 11,571 6,726 20,376 11,783 6,798 1,126 236 58,616

Additions – 213 136 47 176 28 687 1,287

Disposals – (8) (66) (43) (73) (83) – (273)

At 31 March

2005 11,571 6,931 20,446 11,787 6,901 1,071 923 59,630

Depreciation

At 1 April 2004 731 643 2,909 1,699 3,494 753 – 10,229

Charge for

the year 116 215 544 297 396 112 – 1,680

Written back

on disposal – (1) (16) (9) (40) (81) – (147)

At 31 March

2005 847 857 3,437 1,987 3,850 784 – 11,762

Net Book

Value

At 31 March

2005 10,724 6,074 17,009 9,800 3,051 287 923 47,868

At 31 March

2004 10,840 6,083 17,467 10,084 3,304 373 236 48,387

(c) On 1 December 1995, the Authority was granted legal rights to the entire airport site at Chek Lap Kok for a

nominal land premium and nominal annual rent under a Private Treaty Land Grant issued by the Government for

the period from 1 December 1995 to 30 June 2047. It is assumed that the Land Grant will be renewed for a

period of at least 50 years and that the operation of the airport will continue after 2047 (note 3(s)(i)). In

addition, leasehold land also comprises land formation costs.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

86 Airport Authority Hong Kong Annual Report 2004/05

9. Fixed Assets (continued)

(d) Pursuant to a franchise agreement, the Authority has exercised an option to acquire the aviation fuel service

system in July 2003 at a price of $3,539 million according to the terms of the franchise agreement. After the

acquisition of the aviation fuel service system, the Authority is entitled to receive monthly facility payments

over the remaining franchise period of 15 years as stipulated in the franchise agreement. In January 2004,

the Authority entered into an agreement with a third party under which the third party is entitled to 25% of

the future facility payments of the aviation fuel service system. The Authority received an up-front payment

of $1,388 million in December 2003, net of related expenses in this regard. The amount has been recorded

as deferred income and is being amortised over the remaining term of the franchise agreement.

(e) The cost less accumulated depreciation of the fixed assets held for use under operating leases at 31 March

2005 was $7,240 million (2004: $7,952 million) and depreciation for the year amounted to $204 million

(2004: $182 million).

(f) The Authority leases out part of its terminal complexes under operating leases for periods ranging from two

to five years. Generally, lease payments may be varied periodically to reflect prevailing market indices and

passenger flow and contain fixed and contingent rental elements.

The Authority has granted sub-leases of part of its land for airport related development. Generally, these are

for periods ranging from 20 to 49 years and payments are made lump sum in advance.

The Authority has entered into franchise agreements for the provision of airside support services. Generally, these

are for periods ranging from 5 to 30 years. Under these agreements, the franchisees are granted sub-leases of

land for the periods of the respective franchises. Lease payments contain fixed and variable elements.

During the year $3,135 million (2004: $2,475 million), including contingent rentals of $510 million (2004:

$514 million), was recognised as income in the income statement in respect of operating leases.

(g) The total future minimum lease payments under non-cancellable operating leases receivable by the Authority

and the group are as follows:

2005 2004$ million $ million

Within one year 2,317 2,225

After one but within five years 5,891 6,727

After five years 2,676 3,183

10,884 12,135

87Airport Authority Hong Kong Annual Report 2004/05

9. Fixed Assets (continued)

(h) In December 2001, the Authority entered into a lease-out/lease-back agreement for its baggage handling

system and related security screening equipment. Since the Authority retains title to these assets and no

restrictions are placed on its ability to utilise them, no adjustment is made to fixed assets. The total cost of

the system and related equipment at 31 March 2005 amounted to $1,361 million (2004: $1,319 million) and

net book value of $769 million (2004: $809 million). Under this lease arrangement, the Authority received

cash of $1,229 million in April 2002 and committed to make long-term lease payments with a total estimated

net present value of $1,120 million which are defeased by payments of deposits totalling $1,120 million. The

net cash amount received in April 2002, less related transaction expenses, of $90 million in respect of this

transaction was recorded as deferred income, and is being amortised over the lease term.

10. Interests in Subsidiaries

2005 2004$ million $ million

Unlisted shares, at cost 5 5

Details of principal subsidiaries are as follows:

Place of Particulars ofincorporation issued and Percentage

Name of company and operation paid up capital of shareholding Principal activity

Aviation Security Hong Kong 10,000,000 shares of 51% Provision of aviation

Company Limited $1 each security services

(“AVSECO”)

HKIA Information Hong Kong 2 shares of $10 each 100% Provision of airline

Services Limited ticketing information

services

HKIA Logistics Limited Hong Kong 2 shares of $1 each 100% Investment holding

(formerly known as company

HKIA Exhibition

Limited)

On 17 February 1998, the Authority signed a Financing Agreement with AVSECO under which the Authority

agreed to provide a term facility of $50 million and a revolving credit facility of $80 million to AVSECO. These

facilities will expire in June 2006 and were not utilised at the balance sheet date.

All of these are controlled subsidiaries as defined under note 3(c) and have been consolidated into the group

financial statements.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

88 Airport Authority Hong Kong Annual Report 2004/05

11. Other Investments

2005 2004$ million $ million

Unlisted shares 261 50

Other investments represent the Authority’s 11.6% equity interest in IEC Holdings Limited, a company set up by

the Authority and the Government, which holds an equity interest of 86.5% in a joint venture company set up to

procure the development of the AsiaWorld-Expo exhibition centre. The remaining 13.5% of the equity interest in

the joint venture company is held by a third party consortium. As consideration for the shares in IEC Holdings

Limited, the Authority has granted a sub-lease of land to IEC Holdings Limited to 2047. IEC Holdings Limited has

granted an under-lease of the land to 2031 to the joint venture company which will construct and operate the

exhibition centre over the period, at the end of which the land and the exhibition facilities will revert to IEC

Holdings Limited. The Authority’s investment in IEC Holdings Limited is stated at its estimated fair value.

12. Employee Retirement Benefits(a) Defined benefit retirement schemes

The Authority makes contributions to a defined benefit retirement scheme which covers 19% of the group’s

employees. The scheme is administered by independent trustees with its assets held separately from those

of the Authority.

The scheme is funded by contributions from the Authority in accordance with an independent actuary’s

recommendation based on actuarial valuations. The latest independent actuarial valuation of the scheme

was at 31 March 2003 and was prepared by qualified staff of Watson Wyatt (Hong Kong) Limited using the

projected unit credit method. The actuarial valuation indicates that the Authority’s obligations under this

defined benefit retirement scheme are fully covered by the plan assets held by the trustees.

(i) The amounts recognised in the Authority and group balance sheet are as follows:

2005 2004$ million $ million

Present value of wholly funded obligations (287) (258)

Fair value of plan assets 366 331

Net unrecognised actuarial loss 1 7

Net asset 80 80

A portion of the above asset is expected to be settled after more than one year. However, it is not

practicable to segregate this amount from the amounts recoverable in the next twelve months, as

future contributions will also relate to future services rendered and future changes in actuarial

assumptions and market conditions.

89Airport Authority Hong Kong Annual Report 2004/05

12. Employee Retirement Benefits (continued)

(a) Defined benefit retirement schemes (continued)

(ii) Movements in the net asset recognised in the Authority and group balance sheet are as follows:

2005 2004$ million $ million

At 1 April 80 78

Contributions paid to scheme 30 31

Expense recognised in the income statement (30) (29)

At 31 March 80 80

(iii) Expense recognised in the Authority and group income statement is as follows:

2005 2004$ million $ million

Current service cost 38 34

Interest cost 13 11

Expected return on plan assets (21) (16)

30 29

The expense is recognised in the staff costs and related expenses in the income statement. The actual

gain on plan assets for the year is $20 million (2004: gain of $48 million).

(iv) The principal actuarial assumptions used (expressed as weighted averages) are as follows:

2005 2004

Discount rate 5.0% 5.0%

Expected rate of return on plan assets 6.0% 6.0%

Future long term salary increases 4.0% 4.0%

(b) Defined contribution retirement plan

The group also operates Mandatory Provident Fund Schemes (“MPF”) under the Hong Kong Mandatory

Provident Fund Schemes Ordinance for employees employed under the jurisdiction of the Hong Kong

Employment Ordinance and not previously covered by the defined benefit retirement scheme. The MPF

schemes are defined contribution retirement schemes administered by independent trustees. Under the

MPF schemes, employers are required to make contributions to the schemes at 5% of the employees’

relevant income, subject to a cap of monthly relevant income of $20,000. Contributions to the schemes by

the group ranging from 5% to 15% of employees’ relevant income are charged to the income statement.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

90 Airport Authority Hong Kong Annual Report 2004/05

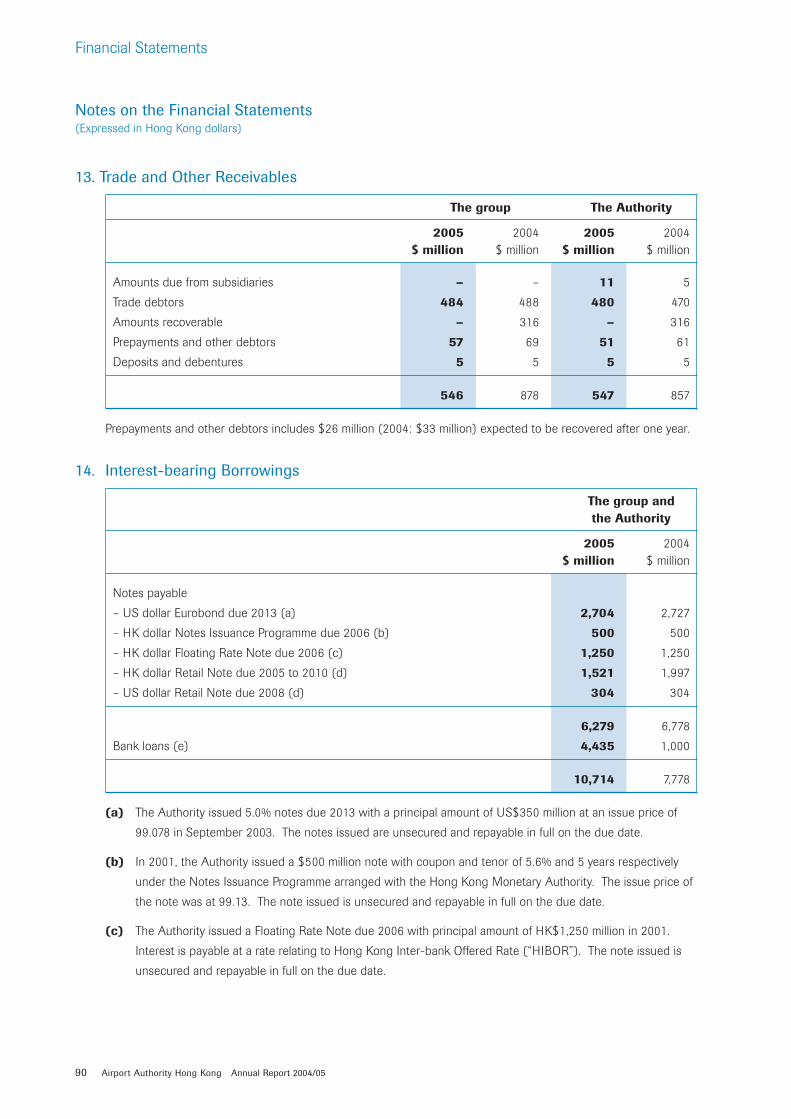

13. Trade and Other Receivables

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Amounts due from subsidiaries – – 11 5

Trade debtors 484 488 480 470

Amounts recoverable – 316 – 316

Prepayments and other debtors 57 69 51 61

Deposits and debentures 5 5 5 5

546 878 547 857

Prepayments and other debtors includes $26 million (2004: $33 million) expected to be recovered after one year.

14. Interest-bearing Borrowings

The group andthe Authority

2005 2004$ million $ million

Notes payable

– US dollar Eurobond due 2013 (a) 2,704 2,727

– HK dollar Notes Issuance Programme due 2006 (b) 500 500

– HK dollar Floating Rate Note due 2006 (c) 1,250 1,250

– HK dollar Retail Note due 2005 to 2010 (d) 1,521 1,997

– US dollar Retail Note due 2008 (d) 304 304

6,279 6,778

Bank loans (e) 4,435 1,000

10,714 7,778

(a) The Authority issued 5.0% notes due 2013 with a principal amount of US$350 million at an issue price of

99.078 in September 2003. The notes issued are unsecured and repayable in full on the due date.

(b) In 2001, the Authority issued a $500 million note with coupon and tenor of 5.6% and 5 years respectively

under the Notes Issuance Programme arranged with the Hong Kong Monetary Authority. The issue price of

the note was at 99.13. The note issued is unsecured and repayable in full on the due date.

(c) The Authority issued a Floating Rate Note due 2006 with principal amount of HK$1,250 million in 2001.

Interest is payable at a rate relating to Hong Kong Inter-bank Offered Rate (“HIBOR”). The note issued is

unsecured and repayable in full on the due date.

91Airport Authority Hong Kong Annual Report 2004/05

14. Interest-bearing Borrowings (continued)

(d) In 2002 and 2003, the Authority issued four fixed rate Retail Notes totalling $1,858 million. Their coupons

and tenors range from 2.3% to 4.5% and 2 years to 7 years. In 2003, the Authority also issued two tranches

of Retail Notes with principal amounts of HK$139 million and US$39 million with coupons of 2.7% and

2.95% and maturities of 2 and 3 years with a 2 year extension option. The issue price of these Retail Notes

ranges from 98.12 to 99.62. The notes are unsecured and repayable in full on the respective due dates.

One Retail Note amounting to $476 million matured and was repaid during the year.

(e) The Authority signed a credit agreement with certain banks for a $3,000 million unsecured club credit facility

in August 2001. The facility consists of a 3-year revolving credit tranche, a 3-year and a 5-year term credit

tranche of $1,000 million each. Interest is payable on amounts drawn down at a rate relating to HIBOR.

The $1,000 million 3-year term credit facility was voluntarily repaid and cancelled in 2002 and the $1,000

million 3-year revolving credit tranche expired during the year.

In October 2004, the Authority signed a credit agreement for a $6,000 million unsecured syndicated bank

loan. The facility consists of a 3-year revolving credit tranche and a 5-year term/revolving credit tranche of

$3,000 million each with repayment commencing from the end of the third anniversary of the credit

agreement. Interest is payable on amounts drawn down at a rate relating to HIBOR. During the year a total

of $3,200 million was drawn down under the facilities.

During the year, the Authority also drew down an amount of $235 million under uncommitted money market

line facilities totalling $2,490 million. Interest is payable on amounts drawn down at a rate relating to HIBOR

and the loan is payable in 2005.

(f) At 31 March 2005, the interest-bearing borrowings were repayable as follows:

Notes Bank

payable Loans Total Total

2005 2005 2005 2004

$ million $ million $ million $ million

Within one year 2,179 235 2,414 476

After one year but within two years 639 1,000 1,639 2,179

After two years but within five years 757 3,200 3,957 1,943

After five years 2,704 – 2,704 3,180

6,279 4,435 10,714 7,778

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

92 Airport Authority Hong Kong Annual Report 2004/05

14. Interest-bearing Borrowings (continued)

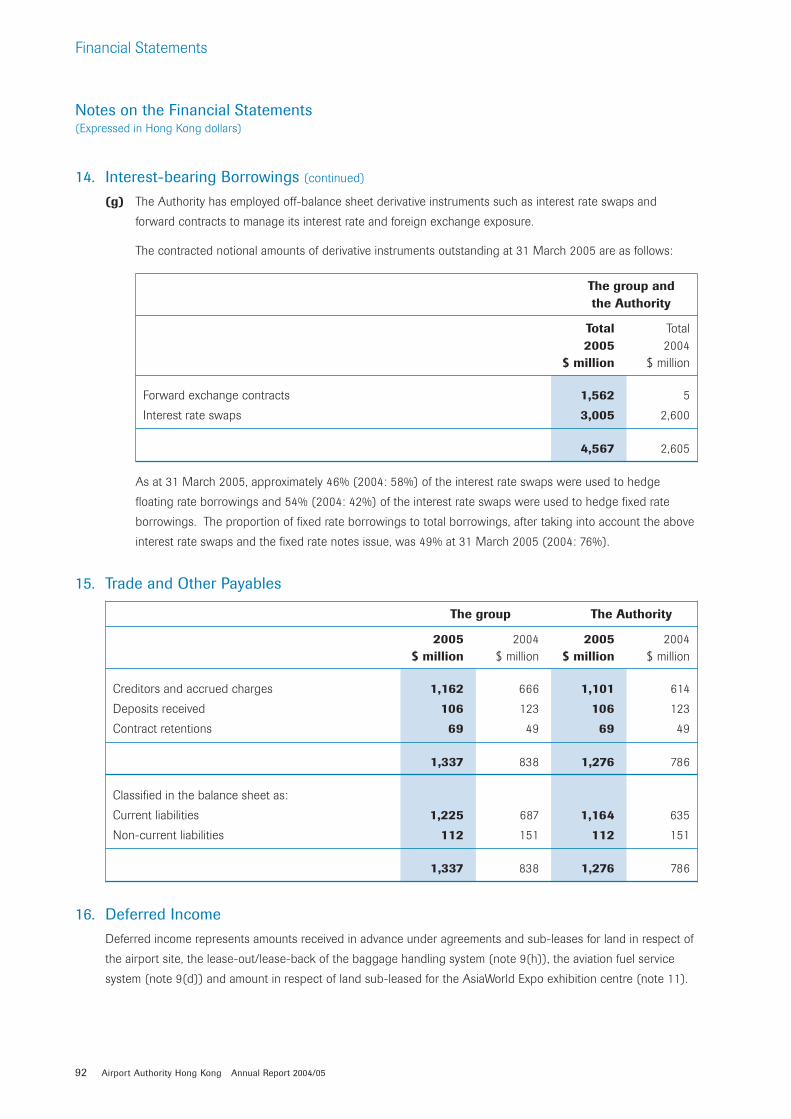

(g) The Authority has employed off-balance sheet derivative instruments such as interest rate swaps and

forward contracts to manage its interest rate and foreign exchange exposure.

The contracted notional amounts of derivative instruments outstanding at 31 March 2005 are as follows:

The group andthe Authority

Total Total2005 2004

$ million $ million

Forward exchange contracts 1,562 5

Interest rate swaps 3,005 2,600

4,567 2,605

As at 31 March 2005, approximately 46% (2004: 58%) of the interest rate swaps were used to hedge

floating rate borrowings and 54% (2004: 42%) of the interest rate swaps were used to hedge fixed rate

borrowings. The proportion of fixed rate borrowings to total borrowings, after taking into account the above

interest rate swaps and the fixed rate notes issue, was 49% at 31 March 2005 (2004: 76%).

15. Trade and Other Payables

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Creditors and accrued charges 1,162 666 1,101 614

Deposits received 106 123 106 123

Contract retentions 69 49 69 49

1,337 838 1,276 786

Classified in the balance sheet as:

Current liabilities 1,225 687 1,164 635

Non-current liabilities 112 151 112 151

1,337 838 1,276 786

16. Deferred IncomeDeferred income represents amounts received in advance under agreements and sub-leases for land in respect of

the airport site, the lease-out/lease-back of the baggage handling system (note 9(h)), the aviation fuel service

system (note 9(d)) and amount in respect of land sub-leased for the AsiaWorld Expo exhibition centre (note 11).

93Airport Authority Hong Kong Annual Report 2004/05

17. Share Capital

2005 2004$ million $ million

Authorised, issued, allotted and fully paid:

366,480 shares of $100,000 each 36,648 36,648

Less: cancellation of 60,000 shares of $100,000

each during the year (note 21(f)) (6,000) –

30,648 36,648

18. Reserves

The group The Authority

2005 2004 2005 2004$ million $ million $ million $ million

Retained earnings at 1 April 716 330 696 308

Profit for the year 1,410 386 1,412 388

Dividend declared and paid during the year (note 19) (380) – (380) –

Retained earnings at 31 March 1,746 716 1,728 696

19. Dividends

2005 2004$ million $ million

Dividend declared and paid during the year 380 –

Dividend declared by the Authority after the balance sheet date of

$3,262.85 per share (2004: $1,036.89 per share) 1,000 380

The dividend declared after the balance sheet date has not been recognised as a liability at the balance sheet date.

Financial Statements

Notes on the Financial Statements(Expressed in Hong Kong dollars)

94 Airport Authority Hong Kong Annual Report 2004/05

20. Outstanding Commitments

2005 2004$ million $ million

Commitments outstanding for the group and the Authority

in respect of capital expenditure not provided for in the

accounts are as follows:

Authorised and contracted for: 1,575 220

Authorised but not contracted for: 3,169 2,097

21. Material Related Party TransactionsThe Authority is wholly-owned by the Government. Transactions between the Authority and Government

departments, agencies or Government controlled entities, other than those transactions such as the payment of

fees, taxes, leases and rates, etc. that arise in the normal dealings between the Government and the Authority, are

considered to be related party transactions pursuant to SSAP 20 “Related Party Disclosures” and are identified

separately in these financial statements.

Members of the Board and the Executive Directors, and parties related to them, are also considered to be related

parties of the Authority. Material transactions with these parties are separately disclosed in the financial statements.

During the year, the Authority has had the following material related party transactions:

(a) In connection with the construction of the airport, MTR Corporation entered into entrustment agreement

with the Authority for the construction of various infrastructure works that were reimbursable according to

actual costs certified. The amount charged as reimbursable from MTR Corporation in respect of the

entrustment works amounted to $ nil (2004: $4 million) for the year ended 31 March 2005. As at 31 March

2005, the amount due from MTR Corporation relating to the entrustment works amounted to $ nil (2004:

$316 million).

(b) The Authority has entered into service agreements with the Government under which the Government is to

provide aviation meteorological and air traffic control services and aircraft rescue and fire fighting services at

the airport. The amounts incurred for the year amounted to $697 million (2004: $694 million) and the

amounts due to the Government as at 31 March 2005 with respect to the above services amounted to $ nil

(2004: $ nil).

(c) In addition, the Authority has also entered into agreements with the Government under which the Government

provides electrical and mechanical maintenance services at the airport. The amounts incurred for these

services for the year amounted to $90 million (2004: $74 million). As at 31 March 2005, the amount due to

the Government with respect to the above services amounted to $32 million (2004: $15 million).

(d) The Authority has entered into an agreement with AVSECO, a subsidiary in which the Government is the

other shareholder, for the provision of airport related security services to the Authority on a cost

reimbursement basis. The amount incurred by the Authority for these services for the year amounted to

$302 million (2004: $281 million). In addition, the Authority licensed certain areas to AVSECO for a total fee

of $8 million (2004: $8 million) during the year.

95Airport Authority Hong Kong Annual Report 2004/05

21. Material Related Party Transactions (continued)

(e) Pursuant to a shareholders agreement dated 21 August 2003, the Authority and the Government have

formed a company, IEC Holdings Limited, in which the Authority holds an 11.6% equity interest, to

participate and co-operate with a third party consortium in the development, funding and operation of the

AsiaWorld-Expo exhibition centre. The Authority has sub-leased to IEC Holdings Limited to 2047 the land

on which the exhibition centre will be built.

(f) Subsequent to the approval in June 2004 by Legislative Council for an amendment to the Airport Authority

Ordinance to permit a reduction of share capital of the Authority, the Authority repaid an amount of $6,000

million to the Government and cancelled 60,000 shares of $100,000 each in relation thereto.

22. Subsequent eventOn 15 April 2005, the Authority signed an agreement with Hangzhou Xiaoshan International Airport Co. Ltd

(HXIACO), owner of the Hangzhou Xiaoshan International Airport at Hangzhou, China (HXIA) to jointly operate and

manage HXIA. Under the agreement, HXIACO will be converted into a limited liability Chinese-foreign joint venture

(HXIAJV). The original shareholders of HXIACO, being the Zhejiang Provincial, Hangzhou Municipal and Hsaushan

Township Government, will hold a 65% equity interest in HXIAJV, and the Authority will make a cash capital

contribution of approximately HK$1.9 billion in exchange for a 35% equity interest in HXIAJV. The finalisation of the

transaction is subject to the negotiation and completion of the relevant Articles of Association and the Joint Venture

contract, and the approval of The State Owned Assets Supervision and Administration Commission of the Zhejiang

Provincial Government, the National Development and Reform Commission, the Zhejiang Foreign Trade & Economic

Cooperation Bureau and the Ministry of Commerce of the People’s Republic of China.