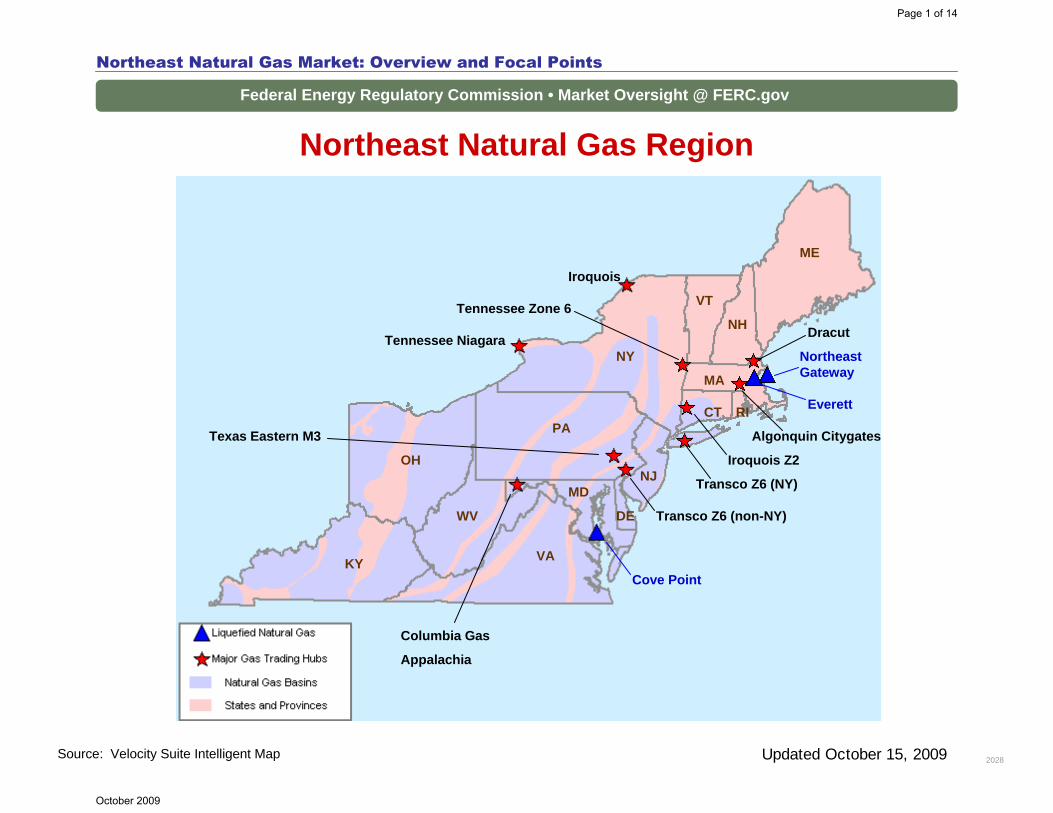

northeast natural gas region · northeast natural gas region ... texas eastern m3, transco zone 6...

TRANSCRIPT

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeast Natural Gas Region

Northeast Natural Gas Market: Overview and Focal Points

Source: Velocity Suite Intelligent Map Updated October 15, 2009 2028

NY

NH

ME

VT

MA

RICT

DE

NJMD

PA

KY

OH

VA

WV

Dracut

Iroquois Z2

Iroquois

Northeast Gateway

Tennessee Zone 6

Algonquin CitygatesTexas Eastern M3

Transco Z6 (non-NY)

Columbia Gas

Appalachia

Tennessee Niagara

Transco Z6 (NY)

Everett

Cove Point

Page 1 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeast Natural Gas Market: Overview and Focal Points

2028

Overview:

Market DescriptionNatural gas use is increasingly important to the Northeast. Though traditionally the Northeast has been a winter peaking region, increased reliance on natural-gas fired generation has evened out annual gas use. Increased dual requirements for natural gas as a space heat fuel and utilization of gas-fired plants has imposed greater challenges on the Northeast, compared to other regions, in aligning commercial and operating conditions between the gas and power industries. The Northeast has little indigenous production (mainly in the Appalachian basin) and none in New England although this trend could begin to change with the successful exploitation of the Marcellus Shale play located in the heart of Appalachia.

Beginning in 2009 the Rockies Express Pipeline began service to the Northeast opening up less expensive Rockies gas to the market. To take advantage of the additional supply pipeline operators added over 3 Billion Cubic Feet per day of additional capacity to the market between 2008 and quarter one 2009, the most in over a decade. Despite increased gas use for power generation, pipeline utilization remains highly seasonal; major regional pipelines often operate at high load factors during the winter resulting in basis differentials to upstream liquid trading points that may greatly exceed firm transportation tariff levels. Rockies and Marcellus Shale supply to the Northeast will becomeincreasingly competitive with traditional supply from the Gulf. The influx of natural gas supply could help moderate the severe basis spikes that traditionally occur during winter peak demand days. The Northeast relies upon conventional and LNG storage to meet peak-day gas needs. LNG plays a critical role in the overall supply mix and at times accounts for up to 30 percent of peak-day gas needs in New England. Market participants in the Northeast can draw upon the nation’s most extensive portfolio of dual, gas-oil fired power plants to flexibly respond to market price and load changes.

GeographyStates covered: Connecticut, Delaware Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, West Virginia, and Vermont.

Updated September 30, 2009

Page 2 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeast Natural Gas Market: Overview and Focal Points

2028

Major Trading HubsAlgonquin Citygates, Columbia Gas Appalachia, Dominion South Point, Dracut, Iroquois Zone 2, Niagara, Texas Eastern M3, Transco Zone 6 NY, and, Transco Zone 6 Non-NY.

Pipeline Flows

Average Daily Southern Zones Deliveries to the Northeast2005: 6.9 Bcf/d2006: 6.6 Bcf/d2007: 7.3 Bcf/d2008: 7.7 Bcf/d2009: 8.2 Bcf/d (Jan-June)

Major Pipelines: Transco, Tennessee, Texas Eastern and Columbia carry a significant amount of gas from the Gulf coast to the Northeast.

Average Daily Mid-Continent Deliveries to the Northeast2005: 1.6 Bcf/d2006: 1.6 Bcf/d2007: 1.5 Bcf/d2008: 1.5 Bcf/d2009: 1.3 Bcf/d (Jan-June)

Major Pipelines: Columbia, Texas Eastern and Dominion move gas from the Midwest to the Northeast

Updated September 30, 2009

Page 3 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeast Natural Gas Market: Overview and Focal Points

2028

Imports and Exports

Average Daily Imports from Canada into the Northeast2005: 2.8 Bcf/d2006: 2.7 Bcf/d2007: 2.7 Bcf/d2008: 2.5 Bcf/d2009: 2.0 Bcf/d (Jan-June)

Major Importers Maritimes and Northeast pipeline, Tennessee Gas Pipeline and Iroquois Gas Transmission System flow the majority of the gas from Canada to the Northeast. In 2009 the Brunswick Pipeline began service delivering LNG from the Canaport LNG terminal into New England. Together, they represent the following percentages of pipeline gas imports:

2005: 83%2006: 85%2007: 88%2008: 89%2009: 84% (Jan-June)

Updated September 30, 2009

Page 4 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeast Natural Gas Market: Overview and Focal Points

2028Updated September 30, 2009

Average Daily LNG Send out: 2005: 0.3 Bcf/d2006: 0.3 Bcf/d2007: 0.5 Bcf/d2008: 0.2 Bcf/d2009: 0.3 Bcf/d (Jan-June)

Note: Represents daily receipts from Everett to Tennessee and Algonquin. 2009 numbers also represent the addition of Northeast Gateway Terminal deliveries to Algonquin. Excludes volumes delivered via truck, consumed at Mystic or other distribution.

Contact InformationFor specific issues regarding the Northeast Natural Gas Region please contact the following Analysts:

Ryan Jett – [email protected]

Page 5 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Annual Average Spot Hub Prices

Northeast Natural Gas Market: Yearly Hub Prices

2026Source: Derived from Platts data. Updated January 23, 2009

Annual Average Day Ahead Prices ($/MMBtu)2004 2005 2006 2007 2008 5-Year Avg

Algonquin Citygates $6.86 $9.75 $7.40 $8.18 $10.06 $8.45Transco Z6 NY $6.82 $10.03 $7.37 $8.46 $10.13 $8.56Transco Z6 non-NY $6.55 $9.63 $7.30 $7.77 $9.85 $8.22Columbia-Appalachia $6.14 $9.18 $6.97 $7.20 $9.18 $7.73Niagara $6.20 $8.88 $6.96 $7.32 $9.25 $7.72

Page 6 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeastern Spot Prices and Basis

Source: Derived from Platts data.

Northeast Natural Gas Market: Spot Prices and Basis

2030Updated October 7, 2009

-$5

$0

$5

$10

$15

$20

$25

$30

$35

$40

Nov-

07De

c-07

Jan-

08Fe

b-08

Mar

-08

Apr-0

8M

ay-0

8Ju

n-08

Jul-0

8Au

g-08

Sep-

08O

ct-08

Nov-

08De

c-08

Jan-

09Fe

b-09

Mar

-09

Apr-0

9M

ay-0

9Ju

n-09

Jul-0

9Au

g-09

Sep-

09

-$20

$0

$20

$40

$60

$80

$100

$120

$140

$160

ALGONQUIN CITYGATESTRANSCO ZONE 6 NON-NYCOLUMBIA GAS APPALACHIATRANSCO ZONE 6 NY

30 Day Rolling Average

$0

$5

$10

$15

$20

$25

2003 2004 2005 2006 2007 2008 2009

Spot

Basis

Spo

t Pric

es ($

/MM

Btu

)

Bas

is P

rices

($/M

MB

tu)

Page 7 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Northeastern Monthly Average Basis Value to Henry Hub

Source: Derived from Platts data.

Northeast Natural Gas Market: Average Basis to Henry Hub

2031

$0

$1

$2

$3

$4

$5

$6

Nov-07

Dec-07

Jan-0

8Feb

-08Mar-

08Apr-

08May

-08Ju

n-08

Jul-0

8Aug

-08Sep

-08Oct-

08Nov

-08Dec

-08Ja

n-09

Feb-09

Mar-09

Apr-09

May-09

Jun-0

9Ju

l-09

Aug-09

Sep-09

ALGONQUIN CITYGATESCOLUMBIA GAS APPALACHIADAWN ONTARIODRACUTTRANSCO ZONE 6 NON-NY

Pric

e D

iffer

ence

($/

MM

Btu)

Updated October 7, 2009

Page 8 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

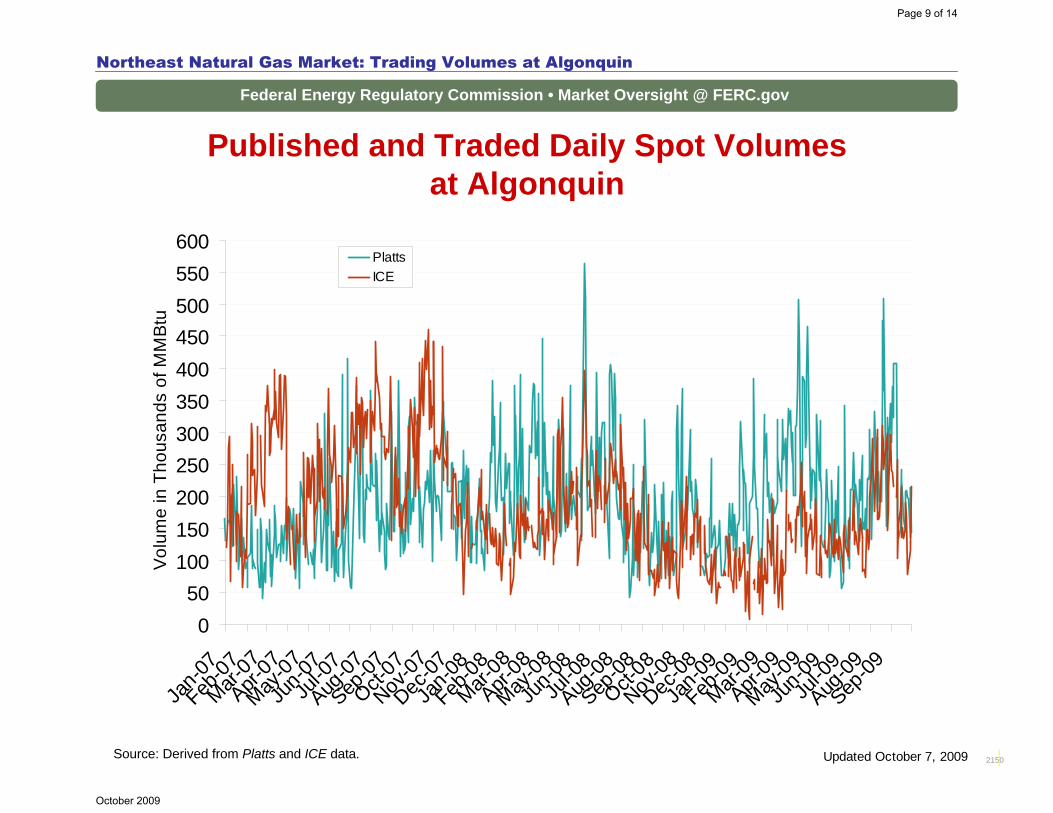

Published and Traded Daily Spot Volumesat Algonquin

Source: Derived from Platts and ICE data.

Northeast Natural Gas Market: Trading Volumes at Algonquin

2150

050

100150200250300350400450500550600

Jan-0

7Feb

-07Mar-

07Apr-

07May

-07Ju

n-07

Jul-0

7Aug

-07Sep

-07Oct-

07Nov

-07Dec

-07Ja

n-08

Feb-08

Mar-08

Apr-08

May-08

Jun-0

8Ju

l-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-0

9Feb

-09Mar-

09Apr-

09May

-09Ju

n-09

Jul-0

9Aug

-09Sep

-09

PlattsICE

Vol

ume

in T

hous

ands

of M

MBt

u

Updated October 7, 2009

Page 9 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Published and Traded Daily Spot Volumesat Transco Zone 6

Source: Derived from Platts and ICE data.

Northeast Natural Gas Market: Trading Volumes at Transco Zone 6

2150

0

200

400

600

800

1,000

1,200

Jan-0

7Mar-

07May

-07Ju

l-07

Sep-07

Nov-07

Jan-0

8Mar-

08May

-08Ju

l-08

Sep-08

Nov-08

Jan-0

9Mar-

09May

-09Ju

l-09

Sep-09

Platts

ICE

Vol

ume

in T

hous

ands

of M

MB

tu

Updated October 7, 2009

Page 10 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Maritimes Pipeline Flows

Northeast Natural Gas Market : Maritimes Pipeline Flows

22054Source: Derived from Bentek data. Updated October 9, 2009

050

100150200250300350400450500550600650700750800850900

5/15

/09

5/29

/09

6/12

/09

6/26

/09

7/10

/09

7/24

/09

8/7/

098/

21/0

99/

4/09

9/18

/09

10/2

/09

MM

cfd

Nova Scotia DemandM&N Power Plant Deliveries

050

100150200250300350400450500550600650700750800850900

5/15

/09

5/29

/09

6/12

/09

6/26

/09

7/10

/09

7/24

/09

8/7/

098/

21/0

99/

4/09

9/18

/09

10/2

/09

Supply from Canaport

Supply from Sable Island

Page 11 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

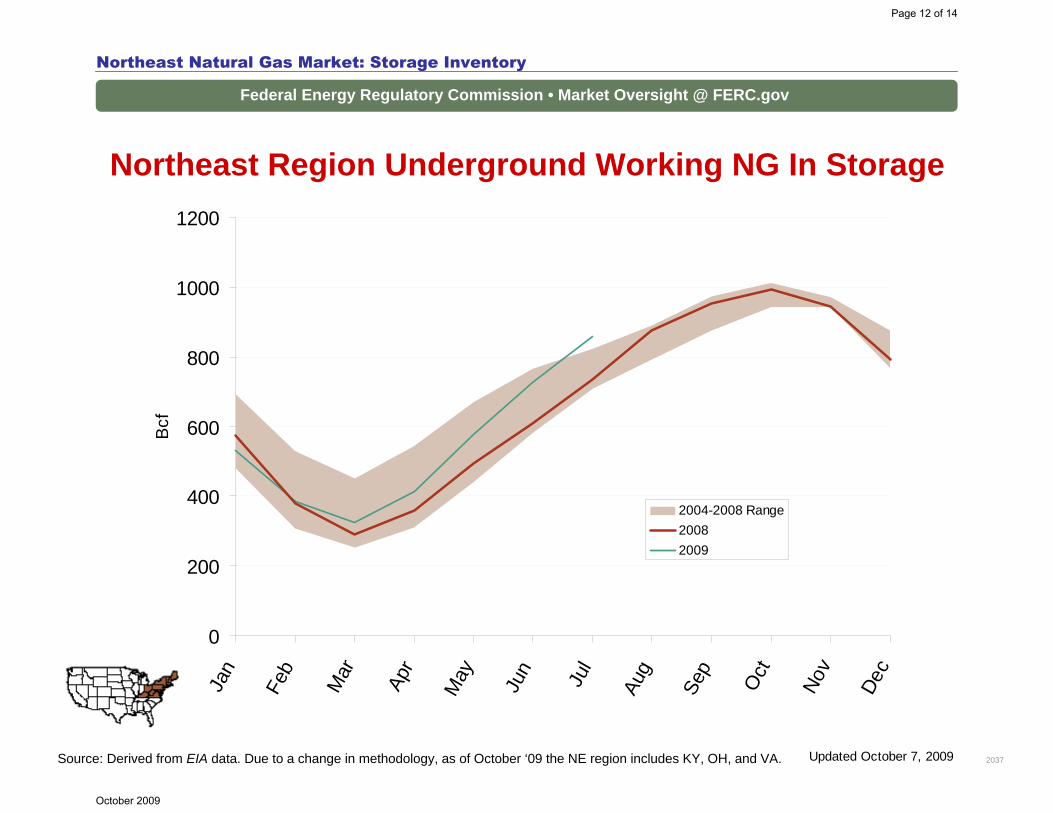

Northeast Region Underground Working NG In Storage

Source: Derived from EIA data. Due to a change in methodology, as of October ‘09 the NE region includes KY, OH, and VA.

Northeast Natural Gas Market: Storage Inventory

2037Updated October 7, 2009

0

200

400

600

800

1000

1200Ja

n

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec

Bcf

2004-2008 Range20082009

Page 12 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

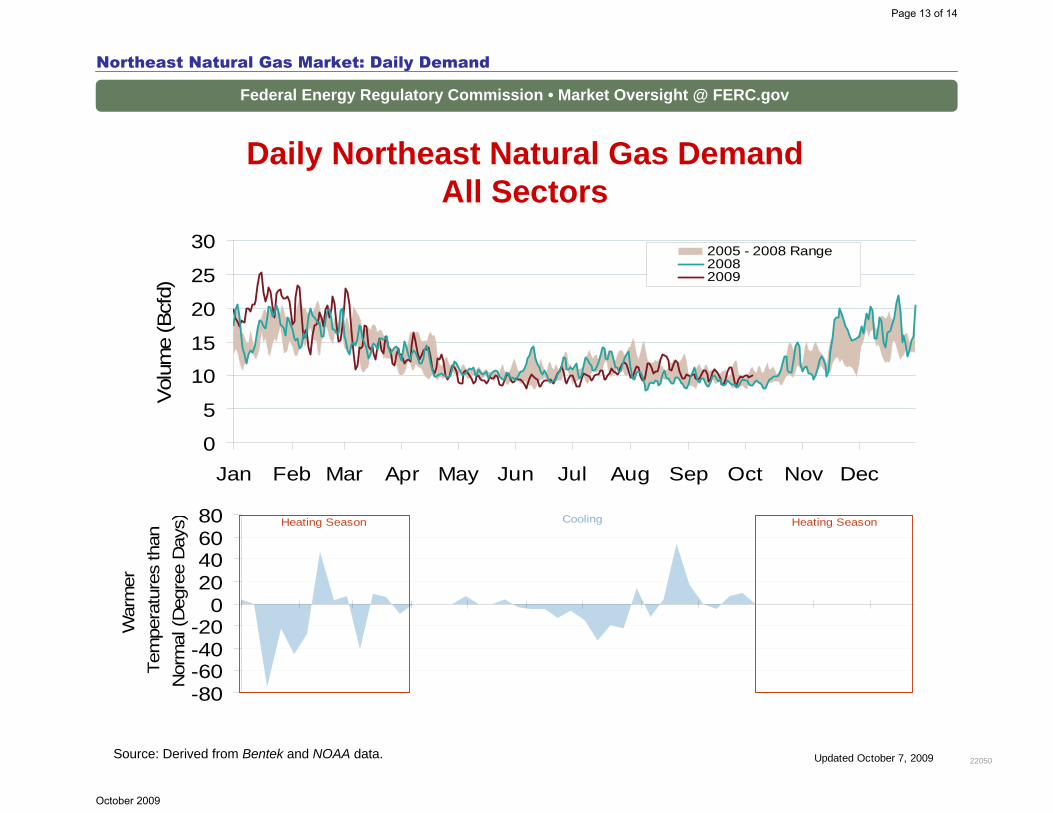

Daily Northeast Natural Gas DemandAll Sectors

Source: Derived from Bentek and NOAA data.

Northeast Natural Gas Market: Daily Demand

22050Updated October 7, 2009

0

5

10

15

20

25

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Vol

ume

(Bcf

d)

2005 - 2008 Range20082009

-80-60-40-20

020406080

War

mer

Tem

pera

ture

s th

anN

orm

al (D

egre

e D

ays ) Heating SeasonCooling Heating Season

Page 13 of 14

October 2009

Federal Energy Regulatory Commission • Market Oversight @ FERC.gov

Natural Gas Infrastructure Additions

Northeast Natural Gas Market : Northeast Infrastructure Additions

22051Source: Derived from Bentek data. Updated October 15, 2009

1 32

4

56

78

9

PipeLNG

Rockies Gas

Gulf S

upply

LNG

LNG

PROJECT IN SERVICE

MAX CAPACITY

1) REX (Clarington) Nov-09 1.800 Bcfd2) DTI Hub Dec-09 0.200 Bcfd3) TETCO Northern Bridge Nov-09 0.150 Bcfd4) VNG Hampton Roads Dec-09 0.100 Bcfd5) Transco Sentinel Phase II Nov-09 0.102 Bcfd6) Iroquois 09/09 Phase III Nov-09 0.025 Bcfd7) AGT J-2 Loop Sep-09 0.140 Bcfd8) Neptune Offshore LNG Sep-09 0.400 Bcfd9) Canaport LNG Jun-09 1.000 Bcfd

Page 14 of 14

October 2009