nordex se investor presentation july 2015 · subsidiary established france market share 2014: 10%...

TRANSCRIPT

Hamburg

September, 2015

Nordex SE Investor Presentation

1. Intro and corporate strategy

2. Markets and market success

3. Products and R&D

4. Financials 2014 & outlook

5. Appendix (shareholder structure)

AGENDA

2 Investor Presentation | Nordex SE | September 2015

1. COMPANY PROFILE NORDEX SE

Nordex at a glance Installed capacity (12.1 GW)

Investor Presentation | Nordex SE | September 2015 3

Global manufacturer of wind energy systems

with a focus on turbines in the 2-3 MW class

Most extensive and consistent use of

platform technology in the industry; variants

for different wind and climate conditions

leveraging shared components

Production sites in Germany (Rostock –

blades and nacelles)

Headquartered in Germany (Hamburg) and

USA (Chicago); subsidiaries in more than 20

other countries

Listed company in the German TecDax

Main shareholder Skion/momentum (22.8%),

rest is freefloat

Revenues 2014: EUR 1.74 bn

~3,000 employees as of H1/2015

Track record as of H1/2015:

>6,600 turbines and >12,000 MW in 41

countries worldwide

By region

Germany 23%

Other Europe 60%

Asia 8%

America 7%

Africa 2%

By segment

MMW Class (2.3-3.3 MW)

74%

Mainstream (1.3/1.5 MW) 20%

Small (<1.0 MW) 6%

1. MANAGEMENT STRUCUTURE

4

New structure to increase operational and strategic responsibility of top managers

Lars Bondo Krogsgaard

Bernard Schäferbarthold Board

Executive Committee

Supervisory Board

Board + 7 top managers with ~70

years of experience in wind

Investor Presentation | Nordex SE | September 2015

1. INTRODUCTION TO STRATEGY

5

Strategy implementation: Nearly all targets reached one year earlier

Turnaround (Phase I) successfully managed – “delivered as promised”

Start of Phase II:

Stronger focus on margin improvement

Underlying measures for all main functions defined and partly initiated

Main financial targets 2017:

EBIT 7-8% Positive FCF

Investor Presentation | Nordex SE | September 2015

Phase 1: Reaching critical top-line (Revenues in bn EUR)

Phase 2: Margin improvement (EBIT margin in %)

6

1. CHANGE OF PRIORITIES: FROM STRONG TOP-LINE GROWTH TO FOCUS ON PROFITABILITY

0,9

2012 2014 2011

1.1

1.4

2013

1.7

2015 2017E 2014 2016

1.7

4-5%

7-8% 0.9

Investor Presentation | Nordex SE | September 2015

7

Key strategy areas identified in 2012

Focused sales and service strategy

Improved operational excellence

Reductions in cost of materials

Development of excellent products and launch of Generation Delta

Finalize restructuring

Financial stability

Main Financial targets

CMD 2013

CMD 2014

Current Guidance

Timeframe 2015 2017 2015

Order Intake EUR 1.5bn n/a EUR 2.1 – 2.3bn

Sales EUR 1.5bn EUR 2.0bn EUR 2.0 – 2.2bn

Gross margin 25% 25% 22%-23%

EBIT margin 5% 7-8% 5-6%

CAPEX EUR 60-70m

EUR 50-60m

EUR 60 -65m

W/C ratio <10% <5% <5%

FCF neutral FCF positive FCF positive

1. PHASE I (2012 -2014): OVERVIEW

Investor Presentation | Nordex SE | September 2015

1. MAIN FOCUS AREAS OF THE NEW STRATEGY (PHASE 2)

8

PROFITABLE GROWTH

HIGH VALUE PRODUCTS

PROJECT DRIVEN COMPANY

BUSINESS MODEL EXPANSION

Investor Presentation | Nordex SE | September 2015

1. Corporate Strategy

2. Markets and market success

3. Products and R&D

4. Financials 2014 & outlook

5. Appendix (Shareholder structure)

AGENDA

Investor Presentation | Nordex SE | September 2015 9

2. DIFFERENTIATION PAYS OFF

Doing Things Differently

Broad global market approach

Strong focus on utilities/big IPPs

Onshore and offshore

Narrow scope

Low complexity

Different WTG platforms

~20 focus markets

Strong focus on small/midsized customers

Onshore only

Broad scope

Accept complexity

One competitive product for each wind class

Competitor´s developments

Investor Presentation | Nordex SE | September 2015 10

2. FOCUSED SALES APPROACH LEAD TO DOUBLE DIGIT MARKET SHARES IN MANY FOCUS MARKETS

Currently focused on ~20 countries – onshore market position 2014

Pakistan Market share 2014: 66%

South Africa Market share 2014: 20%

Qualified for 111 MW round 3 Uruguay Market share 2014: 14% Major order of 142 MW

received

Turkey Market share 2014: 20%

Order intake: +67%

Germany Market share 2014: 9%

Order intake:+ 28%

Sweden Market share 2014: 10%

UK Market share 2014: 10%

Order intake: +58%

Ireland Market share 2014: 47%

Chile Subsidiary established

France Market share 2014: 10%

Order intake: +200%

Finland Market share 2014: 40%

Order intake: +52%

EUROPE Market share 2014: 10%

10% 10% GLOBAL Market share 2014: 3%

Order intake: + 17%

Investor Presentation | Nordex SE | September 2015 11

2. ORDER INTAKE

Order intake H1/15 vs. H1/14

(in EUR mn) Order intake by areas H1/15

12

Generation Delta accounts for ~20% of new orders; bestselling WTG N117/2400 (~ 40%)

One third of the OI stems from emerging markets like South Africa, Uruguay and Pakistan

>90% contracted in EUR or USD, rest of projects hedged (natural, forwards/ derivatives)

Investor Presentation | Nordex SE | September 2015

GER

RSA FR

TRK

FIN 909

H1 2015

1,354

H1 2014

+49%

8%

RoW other

25%

6%

Germany

30%

France

EMEA other

Americas

19%

Turkey

12%

2. GROWTH IN NORDEX MARKETS EXPECTED

Order intake 2013 and 2014 by markets (in EUR)

13

Germany Turkey France UK/IRL Finland Lithuania

+28%

+67% +200% +61% +52%

>100%

Highly competitive N117/2400 for low-wind sites

– turbine of the year Focus on small and medium-sized customers;

comprehensive sales and service support Focus on increasing sales in Germany

Past Success Factors

N131/3000 (and N131/3300 for German market) next stage of evolution – turbine of the year

Expand business with existing (loyal) customer base Exploit opportunities with big IPPs / utilities Ability to serve new markets profitably

Future Success Factors

2013

2014

Investor Presentation | Nordex SE | September 2015

2. ORDER BOOK

Development of the firm order book* 2013 – H1 2015 (in EUR mn)

14

EMEA currently accounts for 78% of the firm order book, Americas 15% and Asia 7%

Book-to-bill ratio* improvement to 1.34 (H1 2014: 1.17)

Conditional order back-log at EUR 664 mn (H1 2014: EUR 720 mn; -7.7%)

Investor Presentation | Nordex SE | September 2015

* Turbine business, excluding service

1.769

1.462

1.259

+16%

+21%

H1 2015 FY 2014 FY 2013

1.13 1.17

1.34

Book-to-bill ratio*

4. A CLOSER LOOK AT FRANCE AND GERMANY

Installations France H1:

524 MW onshore

Installations Germany H1:

~1,200 MW onshore

Investor Presentation | Nordex SE | September 2015 15

French market picking up – on the way back to a solid GW market

Market leadership with 28 % in H1 2015 (based on grid-connections; FY 2015: 9.1%)

Strong development pipeline

Gains in market share: 11.8 % (H1 2014: 8.1%; FY 2014: 8.4 %)

German market intact for 2015-17; EEG amendment and details on tender regime expected for late summer

Current focus on selling N131/3000 – ongoing modification of WTG

28%

Nordex

18%

OEM 1

26% OEM 2

6% 6%

OEM 3

OEM 4

16%

OEM 5

12%

Nordex

Others (not discolsed)

88%

Sources: FEE, VDMA

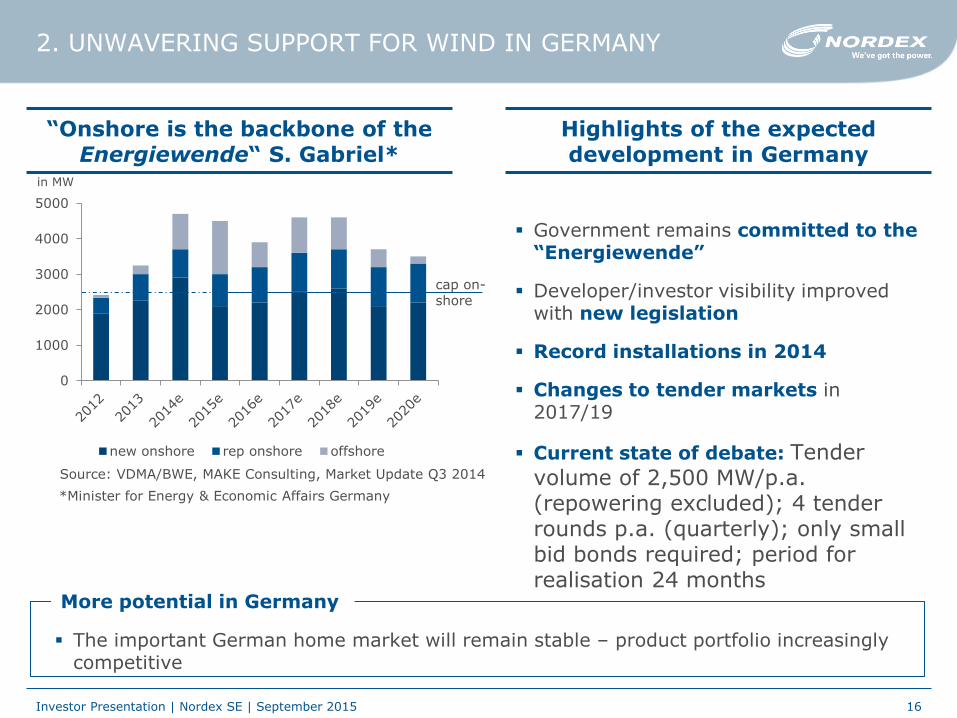

Government remains committed to the “Energiewende”

Developer/investor visibility improved with new legislation

Record installations in 2014

Changes to tender markets in 2017/19

Current state of debate: Tender volume of 2,500 MW/p.a. (repowering excluded); 4 tender rounds p.a. (quarterly); only small bid bonds required; period for realisation 24 months

“Onshore is the backbone of the Energiewende“ S. Gabriel*

Highlights of the expected development in Germany

2. UNWAVERING SUPPORT FOR WIND IN GERMANY

0

1000

2000

3000

4000

5000

new onshore rep onshore offshore

Source: VDMA/BWE, MAKE Consulting, Market Update Q3 2014

More potential in Germany

The important German home market will remain stable – product portfolio increasingly competitive

*Minister for Energy & Economic Affairs Germany

in MW

cap on-shore

Investor Presentation | Nordex SE | September 2015 16

4. DEMAND OUTLOOK IN GW PER REGION

17

Source: MAKE Q3 outlook as of 9/2015

Investor Presentation | Nordex SE | September 2015

2015/2016:

Global onshore growth of ~16 %

expected in 2015. Clean energy

spending still at a high level

2016 dip mainly caused by China

and the US

Through 2020:

Germany: continues on a high level

(~3 GW p.a.)

Northern Europe: Nordex core

markets provide stable foundation

for our business - gains in market

share targeted in various focus

markets

Southern Europe: High demand

for volume in Turkey and France

Eastern Europe: Some recovery in

EMEA East due to new regulations in

Poland

Emerging Markets: Ongoing

growth opportunities in Africa (RSA,

Egypt), Latin America (URU, Chile)

and smaller markets in Asia (PAK

etc.)

611

24

2825

27 28 27

26

11

14

138

9 10

1113

12

12 1313 14

14

544

58

62

2018e

57

2020e

52

2017e

55

52

2016e 2019e

Offshore 2 2

50

EMEA

APAC

2014 2015e

Americas

+4%

1. Corporate Strategy

2. Markets and market success

3. Products and R&D

4. Financials 2014 & Outlook

5. Appendix (Shareholder structure)

AGENDA

18 Investor Presentation | Nordex SE | September 2015

3. HIGHLY COMPETITIVE PRODUCT PORTFOLIO FOR ALL WIND CLASSES

117 m

100 m

90 m

6,0 6,5 7,0 7,5 8,0 8,5 9,0 9,5 10,0

Wind speed [m/s]

IEC 3a IEC 2a IEC 1a

N117/3000

N100/3300

N117/2400

N100/2500

N90/2500

N131/3000*

Rotor-diameter

131 m

Investor Presentation | Nordex SE | September 2015 19

*Introduction of N131/3300 (for German market) on HUSUM Wind fair

3. STATUS N131/3000

20

Update

Installation of the first turbine completed in Janneby, Germany

30 WTGs on order for 2015 projects in Germany and Finland

Successful completion of IEC design evaluation conformity statements (DECS) and DIBt type approvals

Awarded Windpower Monthly‘s „Turbine of the Year“ Award in 3MW+ segment

Hollich Sellen

Wettringen I & II

Kooninkallio-Kankaanpää

Myllykangas II

Janneby

Investor Presentation | Nordex SE | September 2015

1. Corporate Strategy

2. Markets and market success

3. Products and R&D

4. Financials 2014 & Outlook

5. Appendix (Shareholder structure)

AGENDA

21 Investor Presentation | Nordex SE | September 2015

4. HIGHLIGHTS ON FY 2014 …

22

2014 was a very good year

Strong demand in focus markets

Sales + 21%, EBIT + 1.4 ppt to 4.5%, free cash flow of EUR 89m

Order intake + 17%

Successful market launch of the new Generation Delta N131/3000

Implementation of medium-term strategy going according to plan

2015 has started well, positive order momentum continues

2017 sales target may be achieved earlier than previously expected

Investor Presentation | Nordex SE | September 2015

4. ... AND ON H1 2015

23

Nordex in good shape

Good H1 results

Strong increase in revenues and order intake

EBIT margin up to 5.6%

Positive free cash flow

Largest single order in Nordex history so far (Pampa, Uruguay)

Strategic projects on track

Guidance for FY 2015 raised for sales and order intake

Update on strategy and medium-term targets during Capital Markets Day

on 15 October

Investor Presentation | Nordex SE | September 2015

4. BUSINESS PERFORMANCE ALONG THE VALUE CHAIN

Production – Installations - Service

24

Turbine assembly: 1.013 MW (+ 75% yoy) – assembly of turbines for installations in H2

Blade production: 165 blades (- 29% yoy) – extension of facility in Rostock, ramp-up of NR 65.5

Installations: 611.2 MW (-8% yoy) – phasing of projects with a focus in H2

235 turbines installed in 12 countries – main markets Germany, Turkey and France

Service sales: EUR 92 mn (+24% yoy)

Renewal rate: 87% (-10 ppt)

Investor Presentation | Nordex SE | September 2015

4. GROUP INCOME STATEMENT H1 2015

25

In EUR millions

H1 2015 H1 2014 ∆ in %

Sales 1,100.3 815.4 34.9

Total revenues 1,083.8 774.5 39.9

Cost of materials (847.9) (597.7) 41.9

Gross profit 235.9 176.8 33.4

Personnel costs (93.4) (81.0) 15.3

Other operating (expenses)/income (54.6) (40.0) 36.5

EBITDA 87.9 55.8 57.5

Depreciation (26.4) (18.7) 41.2

EBIT 61.5 37.1 65.8

Net financial result (10.3) (12.9) (20.2)

EBT 51.3 24.2 >100

Tax (14.4) (7.7) 87.0

Net profit 36.9 16.5 >100

Sales increase reflects high order backlog and order intake as well as sales of large projects and increased production volume

Net profit increase by 123 % due to higher volume and as a result of lower structural costs, relative to total revenues and optimized financial result

H1 EBIT margin of 5.6 % well in the target range; EBIT margin in Q2 at 6.1 %

Investor Presentation | Nordex SE | September 2015

4. DEVELOPMENT OF GROSS MARGIN AND PRODUCTIVITY

Development of gross margin

Q1 2014 – H1 2015 (in %) Gross profit per employee (in TEUR)

26

Some volatility of gross margin during the year, with 22 – 23 % expected for the full year

Value added measured as gross profit/employee above last year

Investor Presentation | Nordex SE | September 2015

H1 2015

21.8

Q4 2014

27.2

Q3 2014

20.4

Q2 2014

19.8

Q1 2014

24.0

21.5

Q1 2015

Q2 2015

22.8 8481

H1 2015

+5%

H1 2014

Based on sales

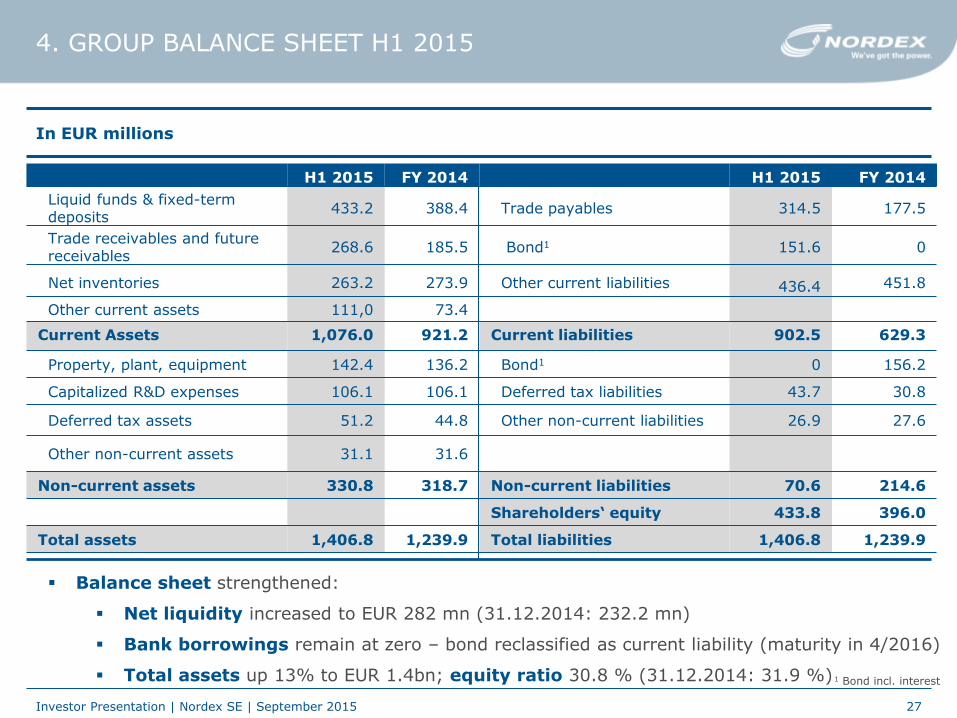

4. GROUP BALANCE SHEET H1 2015

In EUR millions

27

H1 2015 FY 2014 H1 2015 FY 2014

Liquid funds & fixed-term deposits

433.2 388.4 Trade payables 314.5 177.5

Trade receivables and future receivables

268.6 185.5 Bond1 151.6 0

Net inventories 263.2 273.9 Other current liabilities 436.4 451.8

Other current assets 111,0 73.4

Current Assets 1,076.0 921.2 Current liabilities 902.5 629.3

Property, plant, equipment 142.4 136.2 Bond1 0 156.2

Capitalized R&D expenses 106.1 106.1 Deferred tax liabilities 43.7 30.8

Deferred tax assets 51.2 44.8 Other non-current liabilities 26.9 27.6

Other non-current assets 31.1 31.6

Non-current assets 330.8 318.7 Non-current liabilities 70.6 214.6

Shareholders‘ equity 433.8 396.0

Total assets 1,406.8 1,239.9 Total liabilities 1,406.8 1,239.9

Balance sheet strengthened:

Net liquidity increased to EUR 282 mn (31.12.2014: 232.2 mn)

Bank borrowings remain at zero – bond reclassified as current liability (maturity in 4/2016)

Total assets up 13% to EUR 1.4bn; equity ratio 30.8 % (31.12.2014: 31.9 %)

1 Bond incl. interest

Investor Presentation | Nordex SE | September 2015

4. WORKING CAPITAL

Development of working capital 2013 – H1 2015

28

Working capital ratio well below the target (<5%)

Volatility reflects production and installation activity

Continuing stringent working capital management with:

Optimised turnaround and order times

High customer prepayments

Investor Presentation | Nordex SE | September 2015

-2,1

2,2

-4,8

1,0

-3,4 -2,3

-100

-80

-60

-40

-20

0

20

40

-5

-4

-3

-2

-1

0

1

2

3

H1 2015

FY 2013 Q1 2014 H1 2014 Q1 2015 Q3 2014

-1,4

FY 2014

W/C (EUR mn)

W/C ratio

4. OPERATING CASH FLOW AND FREE CASH FLOW

Key figures cash flow statement H1 2015 Key figures cash flow statement H1 2014

Investor Presentation | Nordex SE | September 2015 29

Decreased operating cash flow because of higher operational performance and corresponding increase in trade payables/receivables

Investing activities in H1 2015 mainly for capitalized product development and expansion of the blade center in Rostock – project almost completed

Cash flow from financing activities results from investment in fixed-term deposits

in EUR mn

Cash flow from operating activities

73.4

Cash flow from investing activities

(31.5)

Free cash flow 41.9

Cash flow from financing activities

(-35.0)

in EUR mn

Cash flow from operating activities

91.2

Cash flow from investing activities

(21.2)

Free cash flow 70.0

Cash flow from financing activities

(-152.2)

2014A 2015 old 2015 update

Order intake EUR 1.75 bn EUR 1.8 – 2.0 bn EUR 2.1 – 2.3 bn

Sales EUR 1.73 bn EUR 1.9 – 2.1 bn EUR 2.0 – 2.2 bn

EBIT margin 4.5 % 5 – 6 % 5 – 6 %

Working capital ratio

- 2.3% < 5% <5 %

Investment EUR 76.3 m ~ EUR 50 - 60 m ~EUR 60 – 65 m

4. GUIDANCE 2015

30 Investor Presentation | Nordex SE | September 2015

Guidance update triggered by strong order momentum and increase in activity level

Large installation volume in H2

4. MEDIUM-TERM DIRECTION 2017

31 Investor Presentation | Nordex SE | September 2015

Strong demand

Positive momentum

Solid order book for Nordex

Measures to improve operating efficiency

High growth brings its own challenges

Implementation of operational improvement according to plan, impact not

yet fully reflected in financial results

Strong product pipeline and focused sales strategy to secure future development

1. Corporate Strategy

2. Markets and market success

3. Products and R&D

4. Financials 2014 & outlook

5. Appendix (Shareholder structure)

AGENDA

32 Investor Presentation | Nordex SE | September 2015

5. APPENDIX: SHAREHOLDER STRUCTURE NORDEX SE

33

Based on 80.882.447 shares, as of September 2015

Free float 64.13%

SKion/momentum capital 22.79 %

Investor Presentation | Nordex SE | September 2015

DWS 5,04 %

JPMorgan 5.02 %

Old Mutual 3.02 %

5. APPENDIX: FINANCIAL CALENDAR 2015 AS OF SEPTEMBER 2015

Investor Presentation | Nordex SE | September 2015 34

Date Event

10 September Commerzbank Sector Conference (Frankfurt)

21-22 September Goldman Sachs & Berenberg German Corporate Conference (Munich)

15 October Capital Markets Day (Frankfurt)

31 October Börsentag (retail investors; Hamburg)

12 November Q3 2015 results and analyst call

17-20 November EWEA fair (Paris)

23 November Goldman Sachs Renewables Conference (London)

3 December HSBC Luxembourg Conference

5. DISCLAIMER

35 Investor Presentation | Nordex SE | September 2015

This presentation was produced in August 2015 by Nordex SE solely for use as a source of general information regarding the economic circumstances and status of Nordex SE. It does not constitute an offer for the sale of securities or an invitation to buy or otherwise acquire securities in the Federal Republic of Germany or any other jurisdiction. In particular it is not intended to be an offer, an investment recommendation or a solicitation of an offer to anyone in the U.S., Canada, Japan and Australia or any other jurisdiction. This presentation is confidential. Any reproduction or distribution of this presentation, in whole or in part, without Nordex SE’s prior written consent is expressly prohibited. This presentation contains certain forward-looking statements relating to the business, financial performance and results of Nordex SE and/or the industry in which Nordex SE operates, these statements are generally identified by using phrases such “aim”, “anticipate”, “believe”, “estimate”, “expect”, “forecast”, “guidance”, “intend”, “objective”, “plan”, “predict”, “project”, and “will be” and similar expressions. Although we believe the expectations reflected in such forward-looking statements are based upon reliable assumptions, they are prepared as up-to-date and are subject to revision in the future. We undertake no responsibility to update any forward-looking statement. There is no assurance that our expectations will be attained or that any deviations may not be material. No representation or warranty can be given that the estimates, opinions or assumptions made in, or referenced by, this presentation will prove to be accurate.

THANK YOU FOR YOUR ATTENTION.

36

Nordex SE

Ralf Peters Head of Corporate Communications

Oliver Kayser Senior Manager Investor Relations

Langenhorner Chaussee 600, 22419 Hamburg, Germany

Phone: +49 (0)40 30030 1000

Fax: +49 (0)40 30030 1333

eMail: [email protected]

NDX1

ISIN: DE000A0D6554

WKN: A0D655

www.nordex-online.com

Investor Presentation | Nordex SE | September 2015