investor presentation nordex ag 2 disclaimer this document is made by nordex ag solely for use at...

TRANSCRIPT

Investor PresentationNordex AG

May 2006

Page 2

Disclaimer

This document is made by Nordex AG solely for use at the presentation held to you by Nordex AG in April/May, 2006. It is furnished toyou solely for your information, should not be treated as giving investment advice and may not be copied, distributed or otherwise madeavailable to any other person by any recipient.

The facts and information contained herein are as up to date as is reasonably possible and is subject to revision in the future. NeitherNordex AG nor any of its directors, officers, employees or advisors nor any other person makes any representation or warranty, express orimplied, as to the accuracy or completeness of the information contained in this presentation. Neither Nordex AG nor any of its directors,officers, employees and advisors nor any other person shall have any liability whatsoever for loss howsoever arising, directly or indirectly,from any use of this presentation.

Whilst all reasonable care has been taken to ensure the facts stated herein are accurate and that the opinions contained herein are fairand reasonable, this document is selective in nature and is intended to provide an introduction to, and overview of, the business of NordexAG. Any opinions expressed in this document are subject to change without notice and neither Nordex AG nor any other person is underany obligation to update or keep current the information contained herein. Where any information and statistics are quoted from anyexternal source, such information or statistics should not be interpreted as having been adopted or endorsed by Nordex AG as beingaccurate.

This presentation contains forward-looking statements, which involve risks and uncertainties. These statements may be identified bywords such as “expectation” or “target” or “forecast” and similar expressions, or by their context. These statements are made on the basisof current knowledge and assumptions. Various factors could cause actual future results, performance or events to differ materially fromthose described in these statements. No obligation is assumed to update any forward-looking statements. This presentation does notconstitute an offer or invitation to subscribe for, or purchase, any shares of Nordex AG and neither this document nor anything containedherein shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever.

This document is not an offer for sale of securities. Securities may not be offered or sold in the United States absent registration or anexemption from registration under the U.S. Securities Act of 1933, as amended. Nordex AG does not intend to register any securities inthe United States or to conduct any public offering of securities in the United States.

Page 3

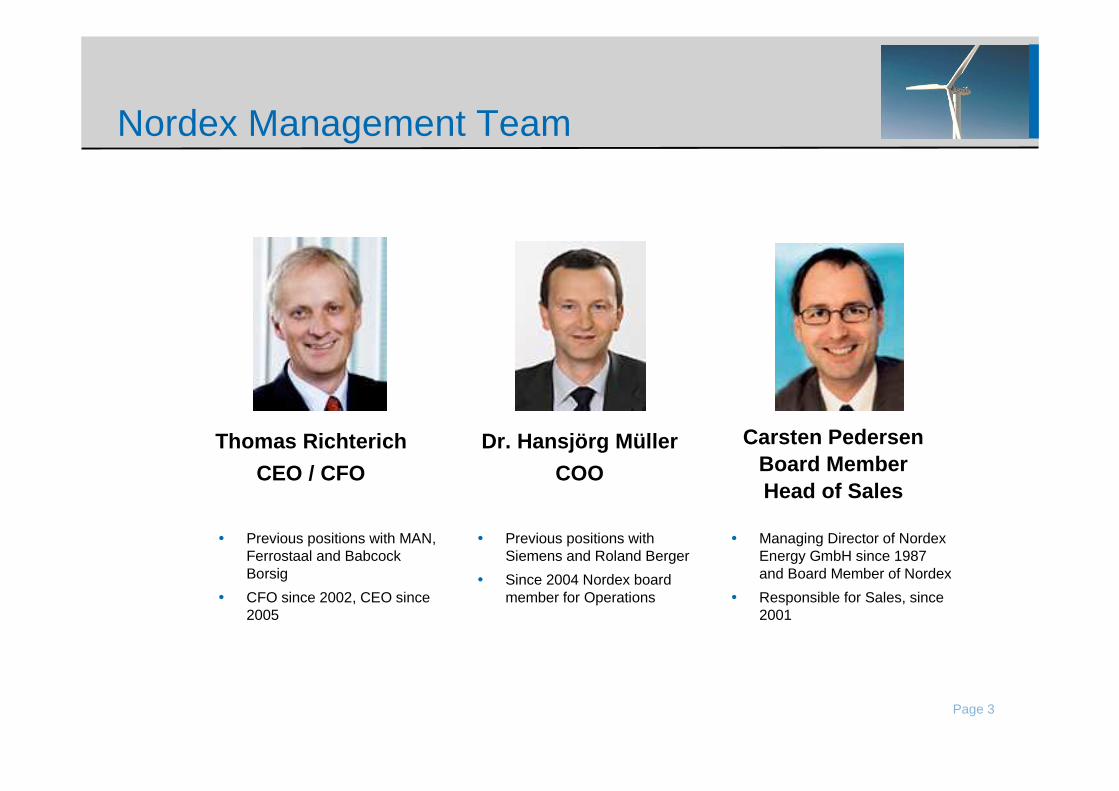

Nordex Management Team

Thomas Richterich

CEO / CFO

Carsten PedersenBoard MemberHead of Sales

Dr. Hansjörg Müller

COO

� Previous positions with MAN,Ferrostaal and BabcockBorsig

� CFO since 2002, CEO since2005

� Managing Director of NordexEnergy GmbH since 1987and Board Member of Nordex

� Responsible for Sales, since2001

� Previous positions withSiemens and Roland Berger

� Since 2004 Nordex boardmember for Operations

Page 4

Nordex at a Glance

� Headquarter: Norderstedt, Germany

� Founded in 1985 in Denmark

� Establishment of production operationsin Germany (1992) and China (1998)

� IPO in 2001

� Global manufacturer of wind energysystems with a focus on turbines in the“MW class”

� 2005 Sales of €309m

� 721 employees

� Main production sites in Rostock (Germany)and Baoding (China)

Installed Base by Geography

Installed Base by Segment

Germany44%

Asia 20%

Africa 4%

America 2%

Other Europe30%

Mainstream(0.75-1.5MW)

51%

“MW Class”(1.5-2.5MW)

43%

Small WTG (<750 kW)6%

Total Base (as of Mar-2006): 2,738

Page 5

Investment Highlights

� Attractive fast growing end-markets

� Well positioned for strong growth

� Technology leader

� Well-positioned across the value chain

� Positioned in high-growth product segments

� International expansion

� Successful completion of turnaround

� Momentum generation & further upside potential

� Strong management team with proven track record

Page 6

Attractive Fast Growing End-Markets:Growing Importance of Wind Energy

4.8 6.1 7.6 10.2 13.9 18.424.9

32.040.3

47.959.3

72.687.6

104.2

124.4

148.8

170.4

193.9

219.5

246.9

276.6

0.1% 0.1% 0.2% 0.2% 0.3% 0.3% 0.4% 0.5% 0.6% 0.7%0.9%

1.1%1.2%

1.4%1.6%

1.9%2.1%

2.4%2.7%

2.9%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Tot

al In

stal

led

GW

Europe The Americas Asia-Pacific RoW Wind Powers' Share of Total Power Market

CAGR 1995-2005: 28.6%CAGR 2006E – 2015E: 15.8%

12.012.513.213.814.619.619.419.020.722.423.718.925.828.535.132.437.233.025.827.0% Increase

CAGR

‘05 – ‘10 ‘10 – ‘15

53% 17%

29% 17%

24% 16%

16% 11%

13%20%

Source: BTM

Page 7

Attractive Fast Growing End-Markets:Key Growth Drivers

GrowingEnergy

Consumption

RisingEnergyCosts

FavourableRegulatory

Environment

� World demand for primary energy increased byover 4% in 2004, world petrol demand by 1.5% in2005

� Economic growth in 2006 expected to support oildemand further (+2.2% vs. 2005 in volumeterms)

� IEA estimates worldwide energy demand maydouble from 2002 to 2030

� Oil price more than tripled since 2001, reachingall-time high in spring 2006 with in excess ofUS$70/barrel

� Market forward curve for oil swaps implies pricesat a level of US$70-75 for next three years

� Kyoto protocol supports renewable energy tohelp countries achieve their targets

� Regulatory outlook worldwide positive:

� PTC in US extended until end of 2007; widelyexpected to be extended again

� Supportive new renewable energy law inChina

� European Parliament reiterates position onrenewable energy targets (20% by 2020)

Source: Goldman Sachs Commodity Research, Bundesverband Wind Energie, Merrill Lynch Commodities Research

Demand for wind energy driven by renewables regulat ions, pricecompetitiveness of wind energy and strong worldwide energy demand

Generation Cost in €/MWh

0 50 100 150 200 250

Advanced Nuclear

Conv. Hydro

Geothermal

IGCC - Coal

Wind

Advanced Gas/Oil CC

Biomass

Conv. Gas/Oil CC

Solar Thermal

Photovoltaic

€/MWh

Page 8

Well Positioned for Strong Growth:Technology Leader

Nordex track record of technological innovation

Production ofthe world’s

largest serieswind turbine

(250 kW)

Constructionof the world’s

first seriesMW windturbine

Completion ofthe world’s firstseries of 80mclass 2.5 MWwind turbine

Installation of1st Nordexoffshoreturbine

Launch of serialproduction of90m class 2.5

MW windturbine

Current R&D Initiatives

� New drive train concept withdifferential gearbox(N90/2500)

� Upgrade yaw system

� Upgrade pitch system

� New platform generation

� Modular tower concept incl.standardized mounting parts(S70 & N90)

� Advanced control system(reduced-load operation)

� Redesign of rotor blade NR45(until maturity phase)

� Adoption to international gridcodes

� Development of 100m classturbine

1987 1995 2000 2003 2005

Page 9

Well Positioned for Strong Growth:Well Positioned Across the Value Chain

Wind farm systemplanning

Technicalrealisation

Wind farmoperation

Service andmaintenance

Projectdevelopment

marketingfinancing

� Micrositing of 100%of signed projectsto review customerlayout

� Supportingcustomers (co-development) toreceive necessaryapprovals and tooptimize the parklayout

� Core business:WTG assembly,production ofselected

components, installation on

site, initial operation

� 2200 turbines arecurrently underNordex service

� Full servicecontract offering upto 9+3 yearsduration

� Market leader inFrance (highmargin potential)

� Development offirst commerciallyfinanced project inChina

� Additional serviceoffering:

increasing demanddue to newwind farm investors, which

are only interested in stablecash flow

Page 10

Well Positioned for Strong Growth:Positioned in High-Growth Product Segments

MW-Class (1500 – 2500 kW) is by far the fastest gro wing segment and will bethe market mainstream in the next 5 years

Newly installed MW p.a.11,203

8,1538,3057,417

7,057

0

2,000

4,000

6,000

8,000

10,000

12,000

2001A 2002A 2003A 2004A 2005A

< 750 750 - 1500 1500 - 2500 > 2500

CAGR: 12.2%

CAGR ‘01-’05 by MW class

NM

+39.9%

+13.6%

(35.2)%

Nordex is growing faster than the market and has es tablished a proven technological position in theMW turbine class

Page 11

Nordex Has Grown Faster Than the MarketLeading to Recovery of Market Share

0%

9%

12%

15%

17%

24%

60%

117%

120%

30%

Gamesa

Mitsubishi

Ecotécnia

Vestas

Enercon

Siemens

Repower

Nordex

Suzlon

GE

Market Growth in 2005 Nordex’ World Market Share Recovery in 2005

70

230

500

250

190

300

2002 2003 2004 2005

7% 3% 2% 3% MarketShare

2H

1HWorld Market

Growth40%

Source: BTM 2006

60%

Nor

dex’

New

ly In

stal

led

Cap

acity

in M

W

Page 12

Well Positioned for Strong Growth:International Expansion

China: � Foundation of rotor blade production (4,000 sqm) for N60/1,300 kW in spring 2005

� Foundation of production JV for S70/77 (1,500 kW) in spring 2006

� Foundation of rotor blade production for S70/77 planned for 2006

� Market re-entry in 2006/7

� Upgrading capacities for project development

� 17 new projects developed, construction expected in 2006/7 (total capacity: ~240MW)

� Successful re-entry achieved in 2006 (first major orders signed)

� Successful entry achieved in 2006 (first major order signed)

Country Activity

As of Mar-2006 Nordex has installed 1,543 turbines outside Germany (56% of total installed base)and is further expanding its international operatio ns.

UK:

USA:

France:

Italy:

Page 13

Successful Completion of TurnaroundMonthly Performance Since 2005

(0.9) (0.9)

(1.6) (1.5)

3.1

1.3

1.9

3.1

7.0

1.7

2.6

(0.9)

2.3

0.2

2.2

5.0%5.1%6.1%

11.2%

8.8%6.1%4.8%

(6.3)%

(15.8)%

(6.3)%

(10.5)%

(6.6)%

7.4%1.0%

7.9%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

EBITDA Margin

Revenues (in €m) EBITDA (in €m)

12.4 12.410.1

14.3 13.7

41.9

19.5

27.023.9

35.9 35.2

62.7

27.8

44.9

52.1

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

May-2005Financial

RestructuringCompleted

2005 2006 2005 2006

May-2005Financial

RestructuringCompleted

Page 14

0

50

100

150

200

250

300

350

400

450

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Momentum Generation: ContinuouslyIncreasing Order Intake

Order Intake Above Budget in 2005 and 1Q 2006

Q1:€35m

Q1-2:€158m

Q1-3:€280m

Q1-4:€395m

Q1/2006:€263m

20052006

+67%

Germany16%

Order Intake byRegion in 1Q-2006

Rest ofEurope

83%

Asia 1%

Total: €263m

Order Intake byProduct in 1Q-2006

Total: €263m

N80/N9084%

N60/N62 4% Sub-MW 0%

S70/S7712%

2004

Page 15

Further Upside PotentialEBIT Improvement Plan

2%

2%

~10%

1.5-2%

2-3%

1.5-2%

Pos

tR

estr

uctu

ring

Ser

vice

Per

form

ance

Pro

cure

men

t&

Log

istic

s

Tec

hnol

ogy

Oth

ers

Tar

get

EBIT Improvement Plan TargetsEBIT Improvement Plan

� Operative restructuring completed in Mar-2005

� Subsequently EBIT Improvement Planlaunched with a focus on

� Service Performance

� Procurement & Logistics

� Technology

� Aim of the plan is to enable Nordex to achievean attractive sustainable level of profitability inorder to reduce the exposure to externalinfluences, e.g. change of market demand,supply situation, raw material pricing etc.

Page 16

Increase of EBIT Margin Expected Due toImplementation of Improvement Plan

22.8

12.17.7

3.0

70.0

38.6

May

-200

5

Sep

-200

5

Dec

-200

5

Mar

-200

6

Dec

-200

6E

Dec

-200

7E

Examples of Measures

� Development of lighter tower for weak windsites� Steps of implementation:

– Specification– Prototyping– Certification– Implementation in series production

� Duration: approx. 18 months� New supplier for casting parts in China

� Steps of implementation:– Pre-selection– Qualification– Certification– Audit

� Duration: approx. 18 months

Proven track record in implementation of extensive plans

Cumulative Sustainable Cost Savings(in €m)

Page 17

Further Upside Potential:Enhanced Outlook 2006

� Projected revenues secured by order volume:

� 100% of 2006 revenues secured by unconditional orde rs

� Unconditional and conditional orders (> €1bn) secur e workload until end of 2007

� Mid-term annual growth target of 50%

2006E (old) 2006E (new)

Order Intake >€450m ≥€600m

(Y-on-Y) +14% +50%

Revenues >€400m ≥€460m

(Y-on-Y) 30% +50%

EBIT Margin 2.5% ≥3.0%

Page 18

Opportunities for and Limitations of GrowthBeyond Plan

1. Markets � Recovery of market share,target > 5%

� New set-up in 1-2 markets p.a.

� Cautious towards offshore

2. Core components � International supply

� 2-3 supplier strategy

� Production capacity gear boxesand blades

3. Product development capabilities

� Solid 2.5 MW technology

� Scaling up to 4.0 MW

� Above 4.0 MW completelynew design required

4. Production capacities

� Europe: expandable to750 (turbines) / 400 (blades) MW

� Asia: expandable to250 (turbines) / 300 (blades) MW

� North America

� Further investments in Europe andAsia

5. Management & organisation

� Restructuring completed

� Basis for furtherimprovements

� Max. growth path +50% p.a.

6. Financial capabilities

� Set-up for businessvolume with a target of €500-600m

� Working capital requirements

� Investment requirements

LimitationsOpportunities

Page 19

Investment Highlights

� Attractive fast growing end-markets

� Well positioned for strong growth

� Technology leader

� Well-positioned across the value chain

� Positioned in high-growth product segments

� International expansion

� Successful completion of turnaround

� Momentum generation & further upside potential

� Strong management team with proven track record

Page 20

Appendix

Page 21

in %

Source: ARA, WTI, Datastream

Increasing prices of fossil fuels have made wind mo re competitive

Price Development of Fossil Fuels

50

100

150

200

250

Q1/2004 Q2/2004 Q3/2004 Q4/2004 Q1/2005 Q2/2005 Q3/2005 Q4/2005 Q1/2006

Steam Coal ARA $/MT Natural Gas $/MMBTU Crude Oil WTI Spot U$/BBL

Page 22

Market power price was considerably in excess of th e EEG tariff

Spot Market Price in 2005 (EEX)

Jan-2005 Feb-2005 Mar-2005 Apr-2005 May-2005 Jun-2005 Jul-2005 Aug-2005 Sep-2005 Oct-2005 Nov-2005 Dec-2005

Peakload

Baseload

Euro/MWh

EEG max. remuneration (85.9 EUR/MWh)

EEG basic remuneration (53.9 EUR/MWh)

Source: EEX

Page 23

The Nordex Group’s Restructuring Conceptwas based on Five Core Elements

Elements ofrestructuring atNordex Group

Focus on attractive core markets� Concentration on foreign growth

markets

� Improved marketing efficiency

Regaining technical position inupper market segment� Elimination of existing deficiencies

and lowering production costs

� Priority: N80/N90

Elimination of previous organizationalshortcomings� Pragmatic approach to optimize business

processes with immediate activities

� Avoidance of inventory losses andguarantee expenditure

Radical cost-cutting by means ofoperative and structural measures� Creation of a reasonable cost

structure to regain competitiveness

Harnessing liquidity potential byreducing working capital� Creation of a reasonable cost

structure to regain competitiveness

1 2

3

4

5

Page 24

2005 Recapitalisation and CurrentShareholder Structure of Nordex

• Reduction in bank liabilities of €28m

• Issue of 12m new shares

Debt-to-Equity Swap

• Renewal for a further four years in theexisting credit facilities

• €60 million in additional credit facilities

CreditFacilities

• €41.6m

• Capital increase with pre-emptive rightsfor existing shareholders

• All shares from rights not taken up byexisting shareholders purchased byCMP and Goldman Sachs

Cash CapitalIncrease

• Reverse split 10 : 1ShareCapital

CMP35.2%

GoldmanSachs23.1%HypoVereinsbank

5.7%

HSH Nordbank5.0%

Morgan Stanley4.8%

Nordvest4.8%

Freefloat21.4%

Recapitalisation Completed in May 2005 Current Shareholder Structure

Page 25

Product Overview

Nordex N60 1,300kW stall GL1/GL2

Nordex S70/77 1,500kW pitch GL2/IEC 3a

Nordex N80 2,500kW pitch IEC 1a

Nordex N90 2,300kW pitch GL2

Nordex N90 2,500kW pitch IEC 1b (HS)

IEC 2a (LS)

Type Capacity Regulation Certification

Page 26

Production Facilities

8-10 WTG MW-class/week

2 WTG 600 kW-class/week

99 blades/yearYinchuan:S70/77 JV

NR-34/37 120 blades/year

NR-40/45 180 blades/year

Page 27

Income Statement (IFRS)

01-Oct-2003-30-Sep-2004€m

Sales

Total Revenues

Cost of materialsas a percentage of total revenues

Personnel costsas a percentage of total revenues

Depreciation/amortisationas a percentage of total revenues

Other operating income/expensesas a percentage of total revenues

EBIT (operational)

One-off items

Financial result

Tax

Net income/loss

221.6

218.8

(173.3) 79.2%

(34.5)15.8%

(12.1) 5.5%

(24.0)11.0%

(25.5)

(2.5)

(5.1)

0.4

(33.5)

01-Jan-2005-31-Dec-2005

309.0

319.4

(251.3) 78.6%

(34.1) 10.7%

(11.7) 3.7%

(22.1) 6.9%

0.3

(5.4)

(3.0)

0.1

(8.2)

∆∆∆∆

39.4%

46.0%

45.0%

(1.3)%

(3.3)%

(7.9)%

101.2%

(116.0)%

41.4%

75.4%

87.4

100.6

78.0

(0.4)

(0.4)

(1.9)

25.8

(2.9)

2.1

0.3

25.3

Page 28

Balance Sheet (IFRS)

€m 31-Dec-2004 31-Dec-2005 31-Dec-2004 31-Dec-2005

Fixed assets

Current assets

Net inventories

Receivablesand other assets

Liquid funds

Other assets

Total Assets

54.2

106.1

47.5

49.2

9.4

26.1

186.4

Shareholder‘s equity

Provisions

Liabilities

Banks

Trade payables

Other liabilities

Others

Total liabilitiesand equity

2.5

62.1

115.3

37.6

39.8

37.9

6.5

186.4

55.4

150.0

71.1

59.4

19.5

26.0

231.4

63.5

55.8

105.2

7.1

64.1

34.0

6.9

231.4

Page 29

Cash Flow Statement (IFRS)

01-Oct-2003-30-Sep-2004

Net income/loss

Depreciation

Change in provisions

Change in inventories

Change in trade receivables and other assets

Change in trade payables and other liabilities

Other changes from operating activities

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

Change in liquidity

01-Jan-2005-31-Dec-2005

(8.2)

11.7

(6.3)

(23.5)

(12.6)

18.6

(0.3)

(20.6)

(8.6)

39.0

9.9

(33.5)

12.2

(4.6)

41.8

(6.6)

(8.6)

0.1

0.8

(3.3)

(0.4)

(2.9)

€m

Page 30

Contact

Ralf Peters

Head of Corporate Communication/ InvestorRelations

Phone: +49 (0)40/500 98 522

Fax: +49 (0)40/500 98 333

eMail: [email protected]

Nordex AG

Bornbarch 2

22848 Norderstedt

Germany

www.nordex-online.com

Page 31

Financial Calendar

� Annual general meeting in Rostock May 15, 2006

� Report on the first quarter of 2006 May 30, 2006

� Report on the first half of 2006 August 25, 2006

� Report on the third quarter of 2006 November 23, 2006

� Report on fiscal 2006 April 26, 2007