nonprofitfinancefund.org ©2010 nonprofit finance fund ® nonprofit finance fund ® new financing...

TRANSCRIPT

nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Nonprofit Finance Fund®

New Financing Structures for Nonprofits

March 20, 2012

Presented to: Grant Managers Network

Presented by:

Dione AlexanderVice President

2nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

2

Foundation Perspective: Investment Tools

Endowment Investments

GrantsProgram Related

Investments

Financial Returns

Programmatic Returns

3nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

The Bottom Lines:

1. Single Bottom Line=Mission Success: General Operating Support Program Grants In-kind support Scholarships Capital campaign funding

2. Double Bottom Line= 1+ return of principal and interest

3. Triple Bottom Line=2+ premium/dividend

4nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

PRI vs. Grant

Grant– Affordability gap vs. financing gap– Extremely high risk level– Smaller $ amounts (<$100,000)– No repayment source, 100% negative return– Project or program funding vs. enterprise-level funding

Program-Related Investment (PRI) – True financing gap– Reasonable risk level– Larger $ amount– Obvious and reliable repayment source– Enterprise-level funding that addresses growth or change in business

model or revenue production

4

5nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

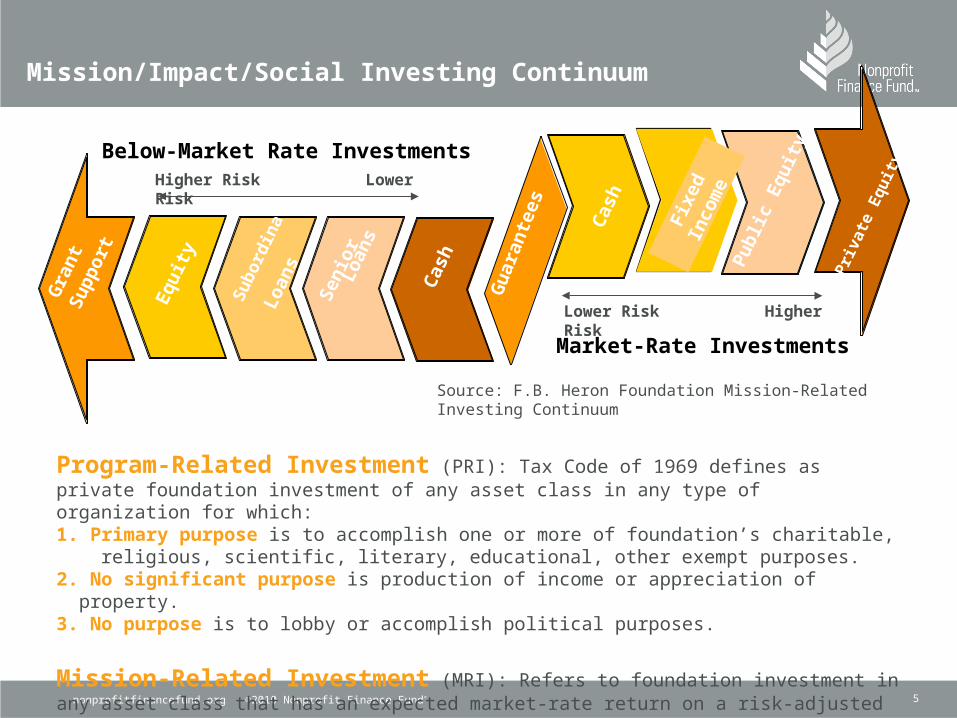

Mission/Impact/Social Investing Continuum

Source: F.B. Heron Foundation Mission-Related Investing Continuum

Market-Rate Investments

Below-Market Rate Investments

Cas

h Pub

lic E

quity

Fixe

d In

com

e

Cas

h

Pri

vate

Equ

ity

Gu

aran

tees

Sen

ior

Loan

s

Sub

ordi

nate

dLo

ans

Gra

ntS

uppo

rt

Equ

ity

Lower Risk Higher Risk

Higher Risk Lower Risk

Program-Related Investment (PRI): Tax Code of 1969 defines as private foundation investment of any asset class in any type of organization for which:1. Primary purpose is to accomplish one or more of foundation’s charitable, religious, scientific, literary, educational, other exempt purposes.2. No significant purpose is production of income or appreciation of property.3. No purpose is to lobby or accomplish political purposes.

Mission-Related Investment (MRI): Refers to foundation investment in any asset class that has an expected market-rate return on a risk-adjusted basis

6nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

6

Impact Investing Lessons

Past practices can constrain: Lack of investment discipline Search for excellence Over concentration on start-ups/new enterprises Must differentiate capital (grants, PRI, MDI)

Need both program and investment staff involvement

Distinctive opportunity and responsibility

Every investor has a different entry point

Every investor has different definition of mission-related

Education and capacity building for staff, partners

Link to program/mission critical

Not every idea/organization appropriate for an investment

Deals can take time to develop, unique skills and staffing may be required Grant support sometimes necessary to do deal

7nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

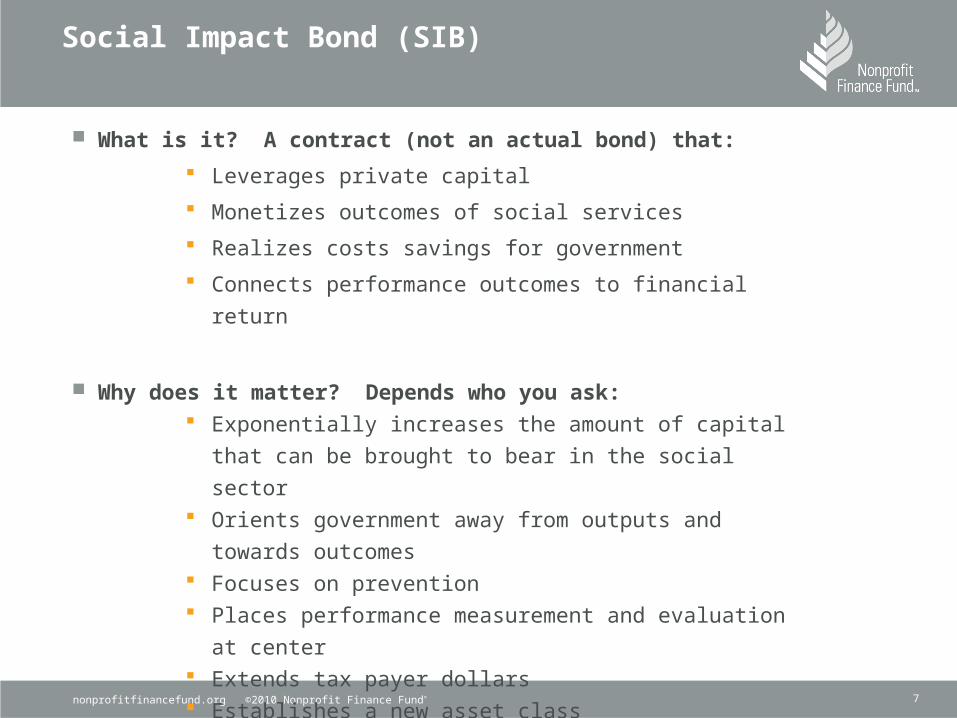

Social Impact Bond (SIB)

What is it? A contract (not an actual bond) that:

Leverages private capital

Monetizes outcomes of social services

Realizes costs savings for government

Connects performance outcomes to financial return

Why does it matter? Depends who you ask: Exponentially increases the amount of capital that can

be brought to bear in the social sector Orients government away from outputs and towards

outcomes Focuses on prevention Places performance measurement and evaluation at

center Extends tax payer dollars Establishes a new asset class

8nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

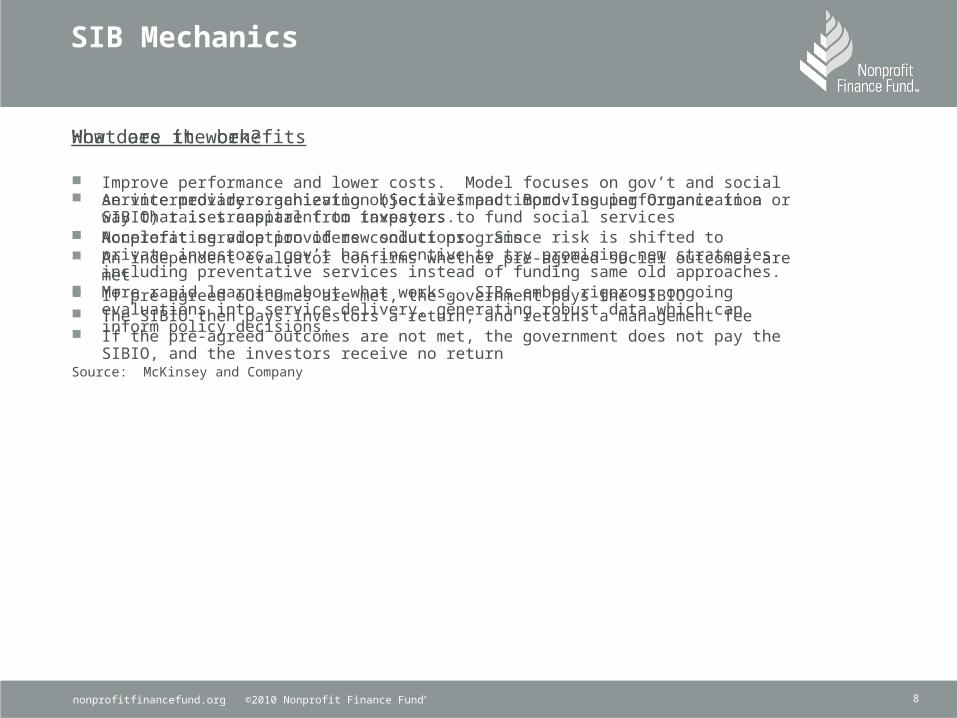

SIB Mechanics

How does it work?

An intermediary organization (Social Impact Bond-Issuing Organization or SIBIO) raises capital from investors to fund social services

Nonprofit service providers conduct programs An independent evaluator confirms whether pre-agreed social outcomes are met If pre-agreed outcomes are met, the government pays the SIBIO The SIBIO then pays investors a return, and retains a management fee If the pre-agreed outcomes are not met, the government does not pay the SIBIO, and

the investors receive no returnSource: McKinsey and Company

What are the benefits

Improve performance and lower costs. Model focuses on gov’t and social service providers achieving objectives and improving performance in a way that is transparent to taxpayers.

Accelerating adoption of new solutions. Since risk is shifted to private investors, gov’t has incentive to try promising new strategies including preventative services instead of funding same old approaches.

More rapid learning about what works. SIBs embed rigorous ongoing evaluations into service delivery, generating robust data which can inform policy decisions.

9nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Continuum of Structures: Some Examples

UK Model “Guaranty” Model

Govt Bond Model

Issuing Organization

• Delivery Agent• SIBIO

• SIBIO• Nonprofit Provider

• State or local government

Investor Type

• Philanthropic • Philanthropic• Impact investors

• Market investors• Impact investors

Risk Carry 100% risk to investors

Shared risk between all parties, depending on structure

• Majority of risk carried by provider

• Some govt risk

Drivers • Private equity structure• Repayment tied to outcomes

• Guaranty structure• % of guaranteed principal, plus outcome- driven repayments

• Broad market access

• Improved performance (providers and govt)

10nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Social Impact Bond Learning Hub(nffsib.org or payforsuccess.org)

11nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Low-profit Limited Liability Company (L3C)

The low-profit, limited liability company, or L3C, is a hybrid of a nonprofit and for-profit organization. More specifically, it is a new type of limited liability company (LLC) designed to attract private investments and philanthropic capital in ventures designed to provide a social benefit. Unlike a standard LLC, the L3C has an explicit primary charitable mission and only a secondary profit concern. But unlike a charity, the L3C is free to distribute the profits, after taxes, to owners or investors.

A principal advantage of the L3C is its qualification as a program related investment (PRI), an investment with a socially beneficial purpose that is consistent with and furthers a foundation’s mission.

Sources: Nonprofit Law Blog, Attys. Takagi and Chan

12nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

New Market Tax Credits (NMTC)

Enacted in 2000, the NMTC is administered by the US Treasury Department’s Community Development Financial Institution (CDFI) Fund, and is intended to bring private investments to low-income communities

NMTCs are allocated annually by the CDFI Fund through a competitive application process

Since the program’s inception, the CDFI Fund has awarded a total of $29.5 billion in tax credit authority to CDEs

Originally approved for five rounds (2003-2007), the program has received extensions through 2011

13nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

NMTC Background: Structure

NFF New Markets Fund, LLCSub-CDE

0.01% Managing Member: NFF99.99% Member: Investment Fund

QALICB100% Member: Nonprofit Sponsor

Investment Fund100% Member: NMTC InvestorLeverage Lender NMTC Investor

NFF

Nonprofit Sponsor

Qualified Equity Investment(QEI)

Distributions

Qualified Low-Income Community Investments (QLICI)

Debt Service

Fees

NMTC

Equity

Loan

Debt Service

Lease Payments

14nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

NMTC Background: The Credit

NMTC is claimed over seven years starting on the date the investment is made in the CDE and each subsequent anniversary

o 5.0 percent credit of the investment in Years 1 to 3; ando 6.0 percent credit in Years 4 to 7

39 percent credit (total) on investment (QEI) in the CDE

IRS Revenue Ruling 2003-20o A partnership/LLC can borrow non-recourse debt and

invest as equity into a CDEo 100 percent of the investment is recognized as a QEIo The ruling was made to aid in the deployment of NMTC in

response to the current tax credit investment community desire to “buy” tax credits more akin to the Low Income Housing Tax Credit

15nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

NMTC Lessons Learned

Some things to consider………

Not all grants can be used in NMTC structures The unwinding of a transaction after compliance period is

based on an option; it cannot be certain True debt analysis It is not “free” money – the compliance period is 7 years

long and involves significant reporting and accounting requirements, and sometimes limitations on business

The transaction costs are going to be significant Get a consultant

16nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Creating Efficient Social Capital Markets

Innovation:Greater/DifferentReal/Perceived Risk:“But for” ~ “Impact”

SubsidyReturn

Scale

Guarantees / Credit Enhancement

Demand for Social Capital

Foundation / Government

Grants

Bank CRA Lending

Foundation PRIs

CDFIs / Intermediaries

DBL/TBL Equity Funds

Public Goods

Private Equity

Bond Market:: Affordable Housing, Charter Schools, SBA loans, health centers, CD loans

Private Equity Funds:

Clean Tech, Sustainable

Timber, LOHAS

Tax Credits

Supply of Social Capitalmeets risk-return demand ofPublic Capital Markets

Faith-Based

Investors

Credit Enhancement

Source: GPS Capital Partners

17nonprofitfinancefund.org ©2010 Nonprofit Finance Fund®

Learn More nonprofitfinancefund.org

Twitter twitter.com/nff_news

Facebook facebook.com/nonprofitfinancefund

Our Blog philanthropy.com/blogs/money-and-mission

Sign Up nonprofitfinancefund.org/sign-up

RSS nonprofitfinancefund.org/news/feed

Get in Touch!

Dione Alexander, Vice President313.965.9145 ext. [email protected]

nonprofitfinancefund.org

Thank You!To Stay Connected…

17