nielsen - evolving markets and consumer e-book purchasing behavior

DESCRIPTION

David Walter (Nielsen) shows some numbers about US, Europe and Italy.TRANSCRIPT

David Walter 19 March 2013

EVOLVING MARKETS AND CONSUMER E-BOOK PURCHASING BEHAVIOUR

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

• Context

• Consumer Confidence and International Print Book Markets

• Connected devices adoption

• US and Italy e-reader and tablet penetration

• Manufacturer market share

• The UK e-book market

• E-book penetration and the rate of change

• The value of the e-book and print book market

• E-book pricing and the consequence for print book prices

CONTEXT

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

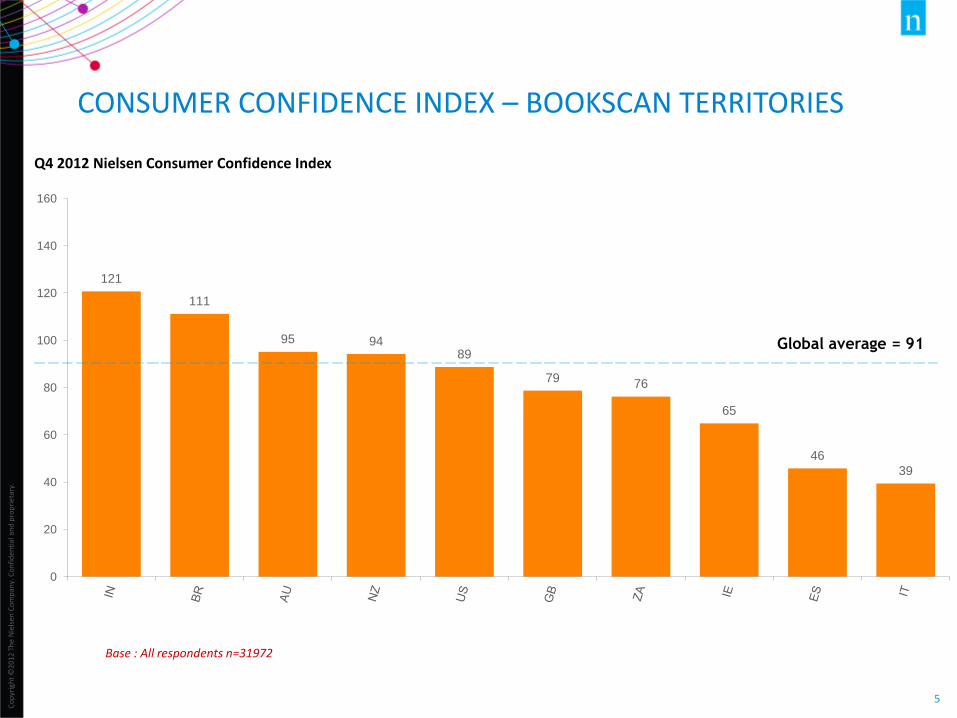

GLOBAL CONSUMER CONFIDENCE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

121

111

95 94 89

79 76

65

46

39

0

20

40

60

80

100

120

140

160

Global average = 91

Q4 2012 Nielsen Consumer Confidence Index

CONSUMER CONFIDENCE INDEX – BOOKSCAN TERRITORIES

Base : All respondents n=31972

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

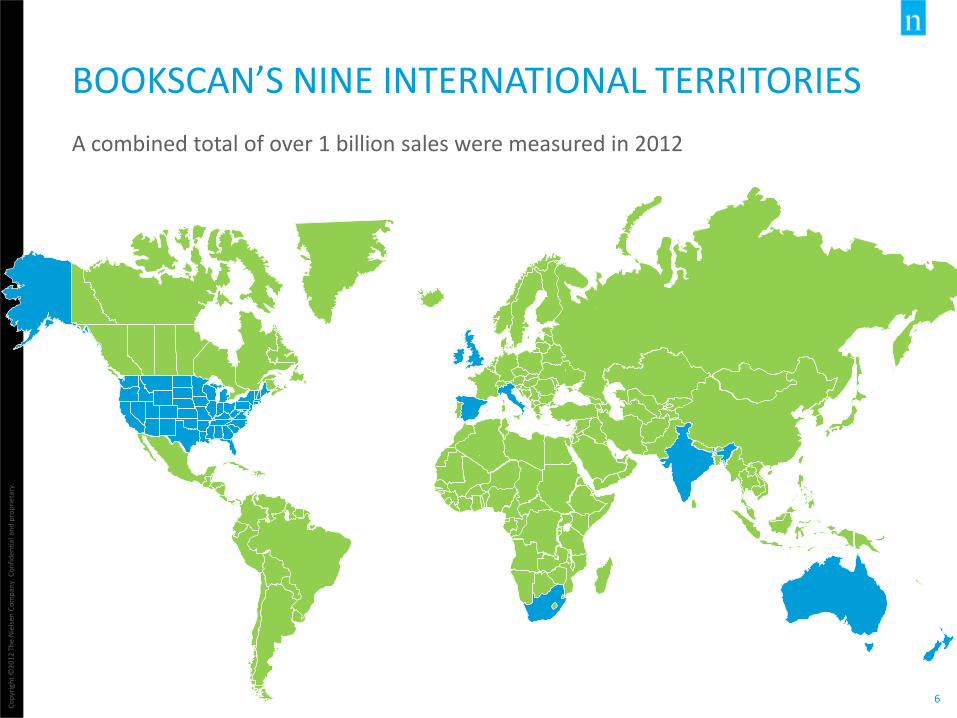

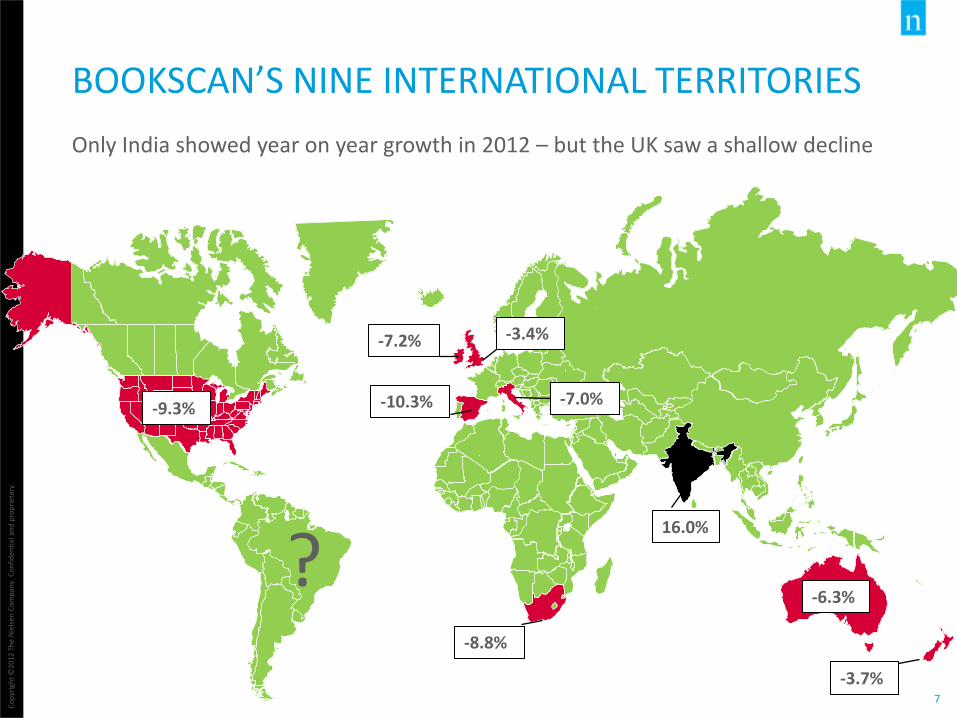

BOOKSCAN’S NINE INTERNATIONAL TERRITORIES

A combined total of over 1 billion sales were measured in 2012

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

-7.2% -3.4%

-7.0% -10.3%

-8.8%

-6.3%

-9.3%

16.0%

-3.7%

BOOKSCAN’S NINE INTERNATIONAL TERRITORIES

Only India showed year on year growth in 2012 – but the UK saw a shallow decline

?

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

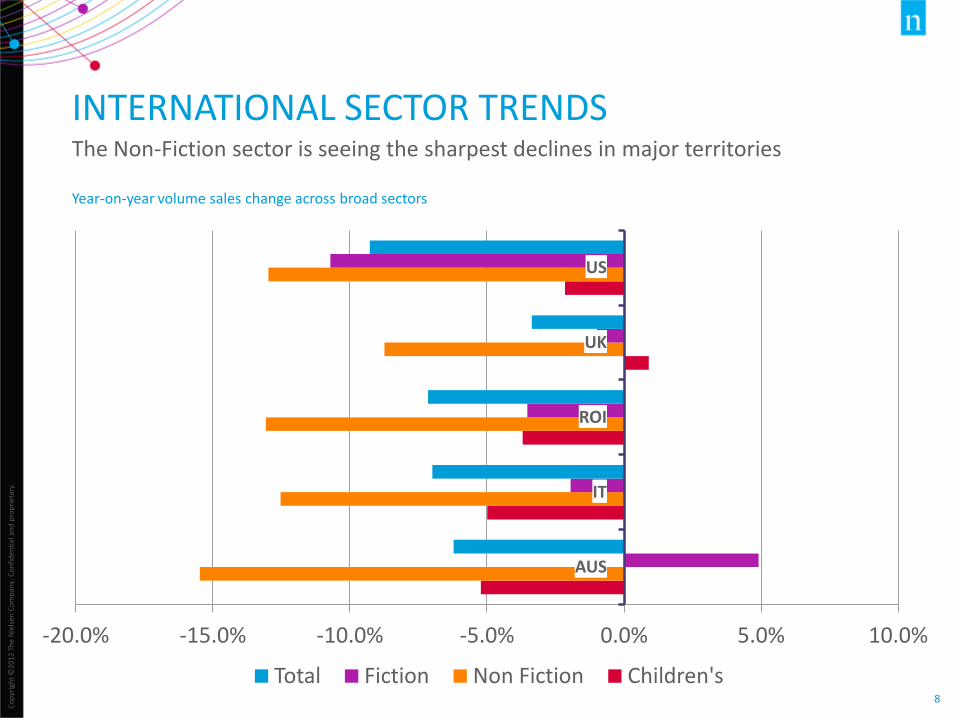

Year-on-year volume sales change across broad sectors

-20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0%

AUS

IT

ROI

UK

US

Total Fiction Non Fiction Children's

INTERNATIONAL SECTOR TRENDS The Non-Fiction sector is seeing the sharpest declines in major territories

THE UK E-BOOK MARKET

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

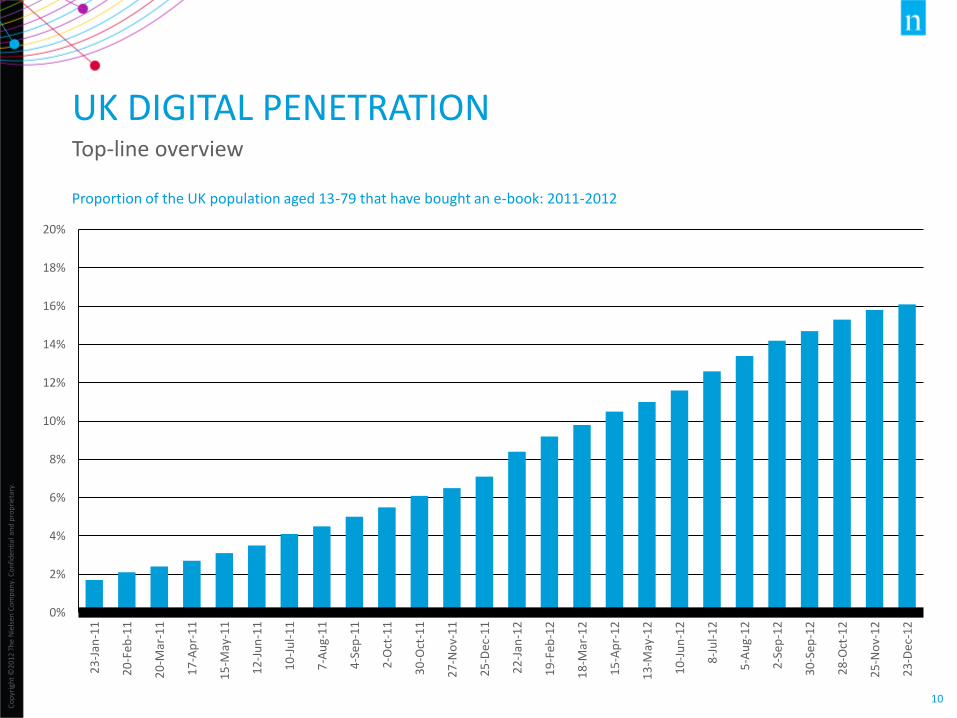

Proportion of the UK population aged 13-79 that have bought an e-book: 2011-2012

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

23

-Jan

-11

20

-Feb

-11

20

-Mar

-11

17

-Ap

r-1

1

15

-May

-11

12

-Ju

n-1

1

10

-Ju

l-1

1

7-A

ug-

11

4-S

ep-1

1

2-O

ct-1

1

30

-Oct

-11

27

-No

v-1

1

25

-Dec

-11

22

-Jan

-12

19

-Feb

-12

18

-Mar

-12

15

-Ap

r-1

2

13

-May

-12

10

-Ju

n-1

2

8-J

ul-

12

5-A

ug-

12

2-S

ep-1

2

30

-Sep

-12

28

-Oct

-12

25

-No

v-1

2

23

-Dec

-12

UK DIGITAL PENETRATION Top-line overview

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

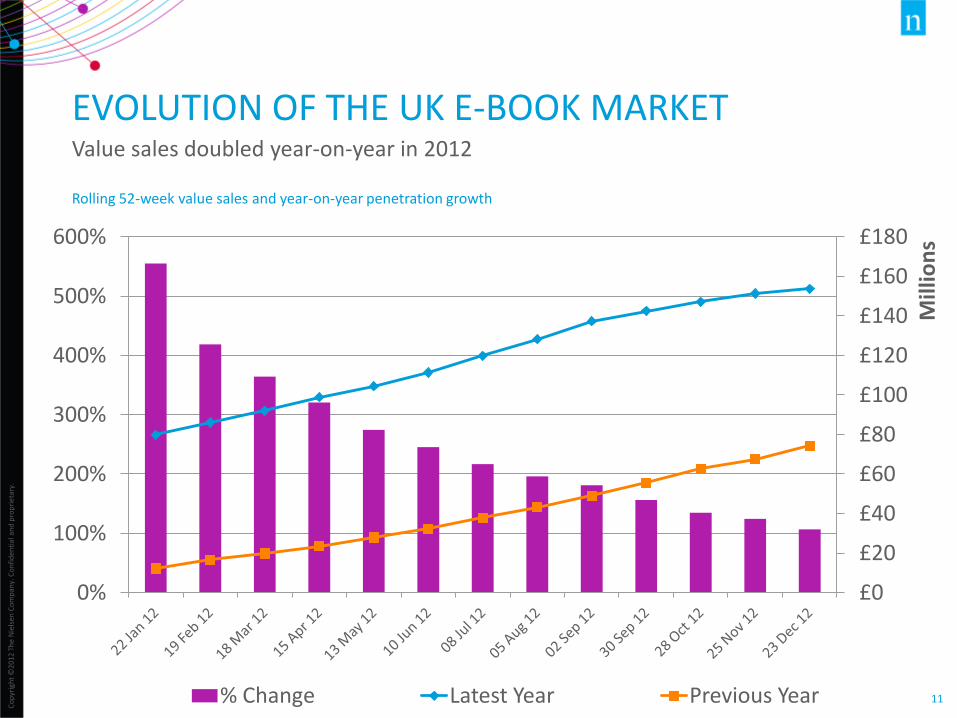

Rolling 52-week value sales and year-on-year penetration growth

£0

£20

£40

£60

£80

£100

£120

£140

£160

£180

0%

100%

200%

300%

400%

500%

600%

Mill

ion

s

% Change Latest Year Previous Year

EVOLUTION OF THE UK E-BOOK MARKET Value sales doubled year-on-year in 2012

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

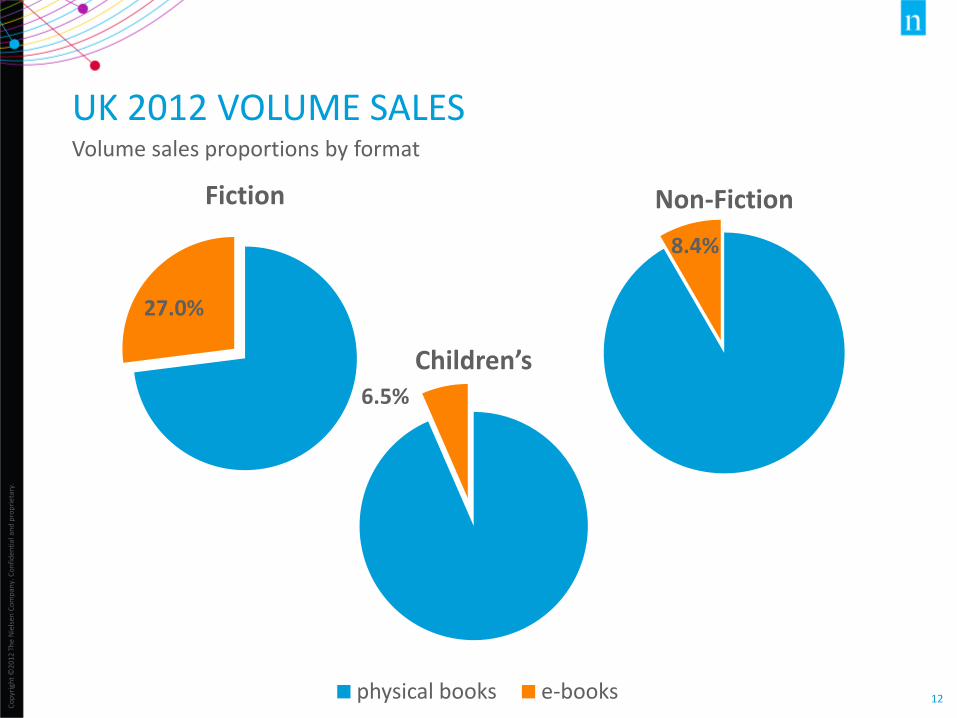

27.0%

Fiction

UK 2012 VOLUME SALES Volume sales proportions by format

8.4%

Non-Fiction

6.5%

Children’s

physical books e-books

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

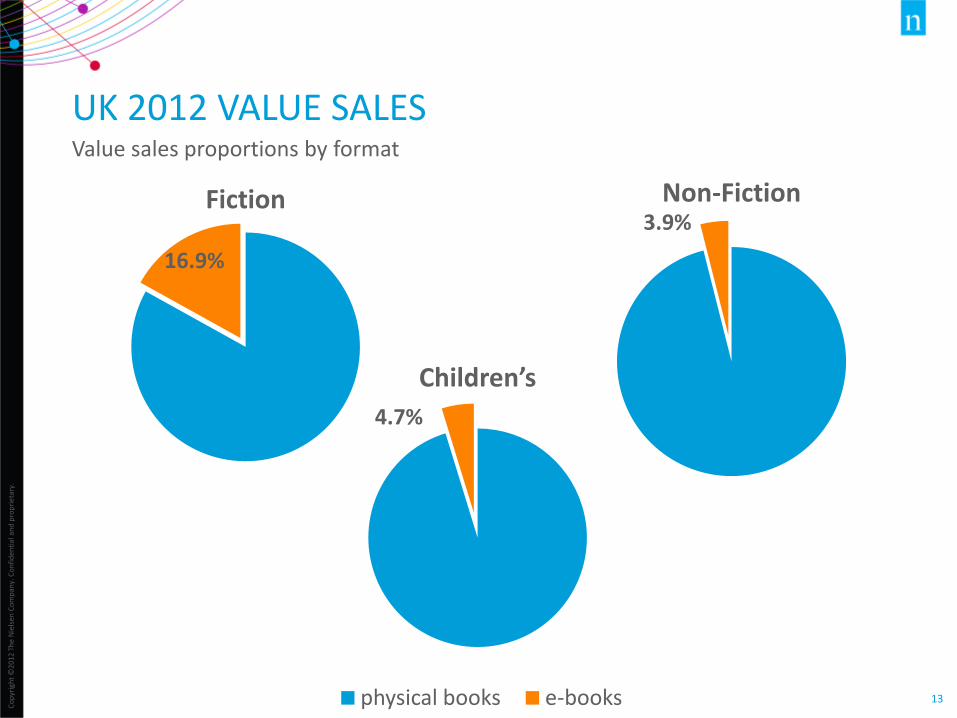

16.9%

Fiction

UK 2012 VALUE SALES Value sales proportions by format

3.9% Non-Fiction

4.7%

Children’s

physical books e-books

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

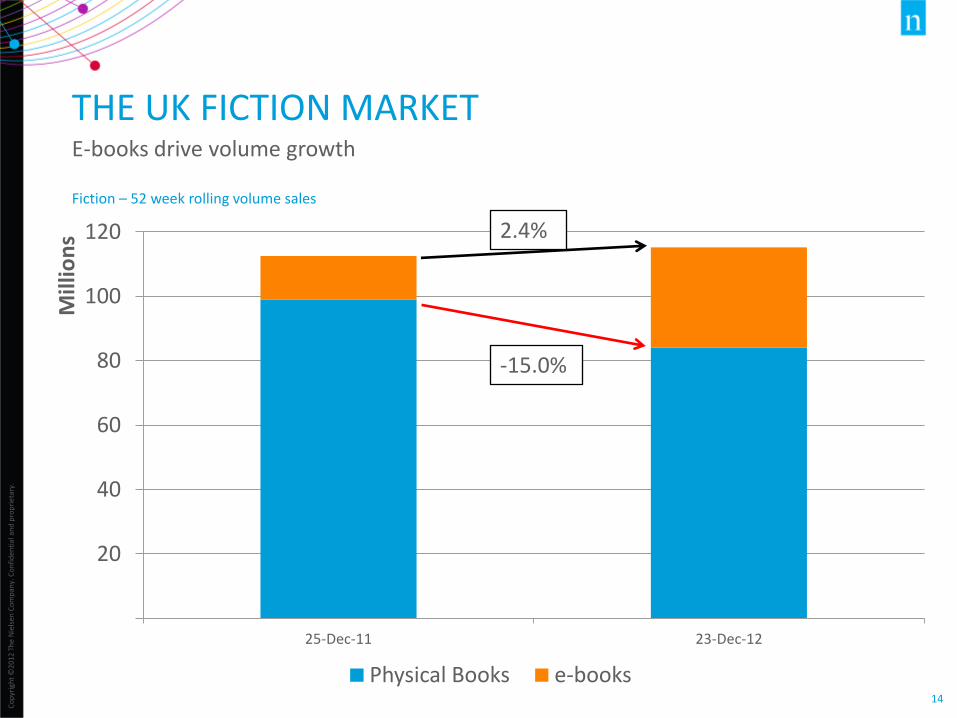

Fiction – 52 week rolling volume sales

THE UK FICTION MARKET E-books drive volume growth

20

40

60

80

100

120

25-Dec-11 23-Dec-12

Mill

ion

s

Physical Books e-books

-15.0%

2.4%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

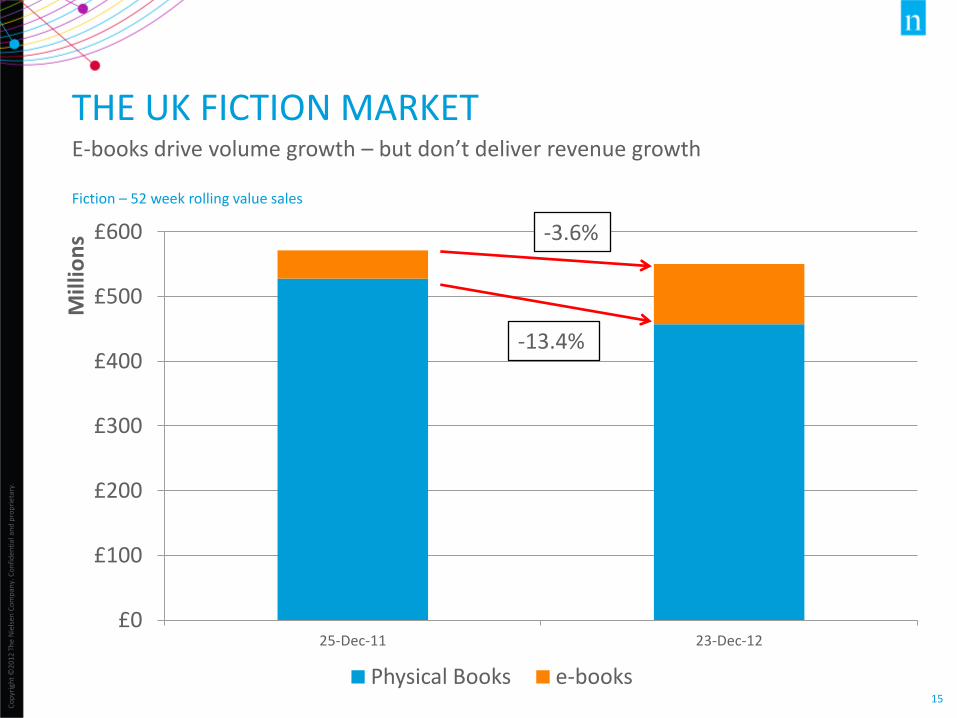

15

£0

£100

£200

£300

£400

£500

£600

25-Dec-11 23-Dec-12

Mill

ion

s

Physical Books e-books

-13.4%

-3.6%

THE UK FICTION MARKET E-books drive volume growth – but don’t deliver revenue growth

Fiction – 52 week rolling value sales

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

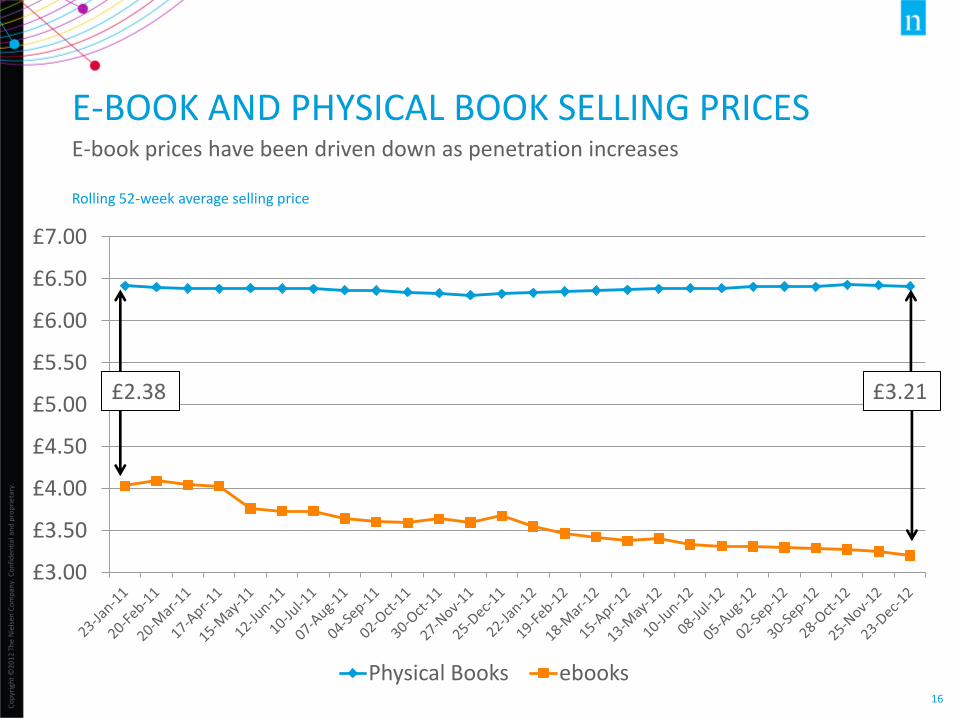

Rolling 52-week average selling price

£3.00

£3.50

£4.00

£4.50

£5.00

£5.50

£6.00

£6.50

£7.00

Physical Books ebooks

E-BOOK AND PHYSICAL BOOK SELLING PRICES E-book prices have been driven down as penetration increases

£2.38 £3.21

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

KEY FINDINGS From our international markets, including the US, Italy and the UK

• Print book markets worldwide continue to see decline

• E-book sales data is not yet broadly available – consumer data helps to bridge this gap

• US e-reader adoption is skewed towards an older, female demographic

• Italian e-reader adoption is stronger among a younger, male demographic

• In the UK e-books have rapidly taken a substantial proportion of the Fiction market, delivering volume growth – but this is not matched by revenue growth

• Whilst e-books become increasingly significant for the Fiction market, the Non-Fiction and Children’s sectors have not kept up

• E-book pricing is not only lower then physical books - it has been driven down as penetration has increased

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

KEY CHALLENGES In the developing digital space

• How can publishers maintain (and grow) revenue as the migration to digital brings a new pressure to deliver low prices?

• How can publishers develop compelling digital content for the Non-Fiction and Children’s markets?