confidential & proprietary copyright © 2007 the nielsen company private label report plma a...

TRANSCRIPT

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Private Label Report PLMA

A review of Private Label purchasing behaviour by Australian Grocery Shoppers

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Opening Quiz• When was Australia’s last recession ?– Around 1990– Around 2000– When Warnie retired– Before I was born

• 1990/1991• But 2000/2001 was awfully close to the popular definition

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Opening Quiz• What % is Petrol of total HH consumption?– 0-10%– 10-20%– 20-30%– 100%

• 3%

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

What we’ll review…

• High level review of the Australian Economic Story– Economic benchmarks and implications

• How Consumers Have Changed– Their mood & how they are spending their money

• Key Stories for 2009 – Private Label growth and implications

• The 2008 Private Label Report– Share development by Retailer Chain– Category Highlights

• Private Label Report Q1 09– Key drivers and Implications

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Nielsen Consumer Assets Employed

• Nielsen Homescan– Data through to December 2008, Australia’s demographically and trade

balanced longitudinal consumer panel.• Nielsen ScanTrack

– Data through to December 2008. Retail sales sourced from over 50 retailers. Includes Homescan-fused data for ALDI – Australia’s fastest growing grocer.

• Nielsen Global Confidence Survey– 2008 Bi-Annual 40 country survey of consumer sentiment and outlook

• Nielsen Shopper Trends Report– 2008 Annual study of drivers of consumer retailer choices and

shopping repertoires• Nielsen Retail Barometer

– January 2009 online survey of FMCG Industry executives• Partner Support : Macquarie Bank Economic Team– Inclusive of Australian Bureau of Statistics Data

– Data to dates as specified.

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

The Private Label ReportApril 2009

The Australian Economic Story

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Outlook

• Declining GDP Outlook for 09/10– 1-2% appears to enjoy good consensus among economists– Important development is forecast declines in the commodity-

driven growth states of QLD and WA

• Rising Unemployment– From close to historic lows– Atypically led by professional labour groups rather than blue-

collar

• Inflation declines overall– Food CPI still strong however - in part due to fresh prices

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

What We’ve Learnt

• Economic Outlook is challenging– However retail, and food retail in particular is less likely to feel the effects as

other parts of the markets

• Consumers are Changing their Shopping Habits– More stores, more private label, more cooking at home and more focus on

stretching their budget by shrewd buying.

• FMCG environment has opportunity– CPI increases are encouraging, if you can pass your price rises on

• Your Route to Market is broader– Independent supermarkets and ALDI are performing well. If ALDI is not a

customer, your route to market is smaller

• Private Label is now entrenched in more FMCG categories, with over 2 dozen categories now in transition– Last 12 months figures are your strongest call to action yet to generate

consumer-based insights on your brands role in your retailer• Specialist fresh stores are under pressure as the economy drives

consumers back to a one stop shopping

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

What are the implications?

• There are some reassuring signs for business forecasts– CPI increases helps drive growth – Supermarket retailing offers some insulation from broader

economic malaise

• Growth states of QLD and WA will slow– This may force a review of state growth forecasts for suppliers

• The success of independent and ALDI supermarkets means that route to market opportunities exist– Mass, Convenience and online also potential plays

• Branded product will be tested (again) in 2009– Consumer-led retailer relevance and promotional execution will be

critical for profit protection and growth• Opportunities for fresh, and potentially packaged or

frozen alternatives in supermarkets if you play in this space

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

How Consumers Have ChangedTheir mood & how they are spending their money

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

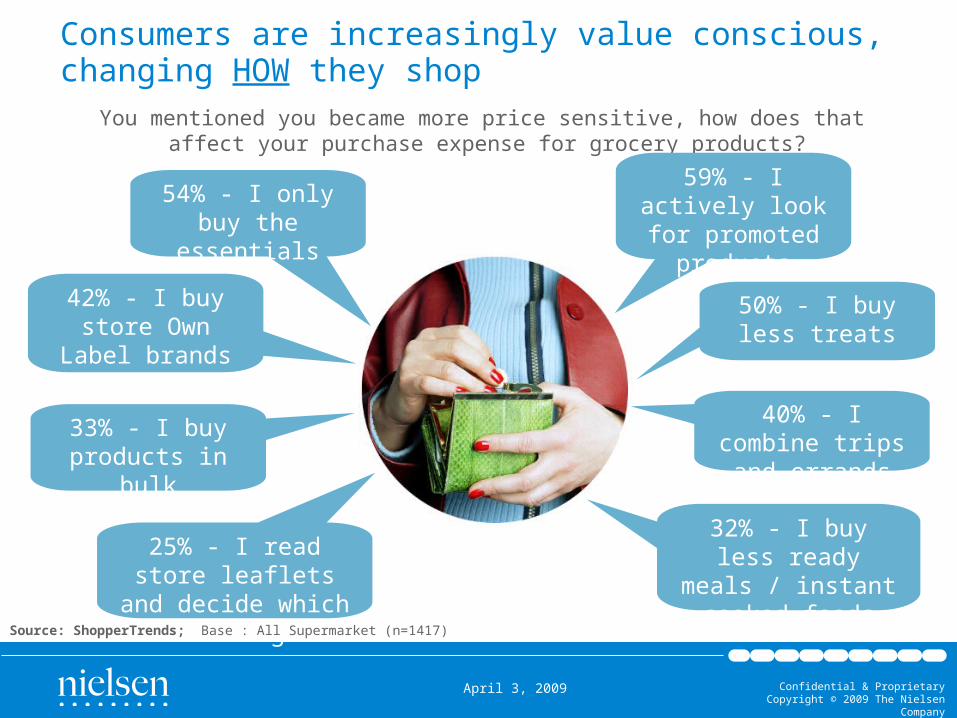

Consumers are increasingly value conscious, changing HOW they shop

You mentioned you became more price sensitive, how does that affect your purchase expense for grocery products?

59% - I actively look for promoted

products

50% - I buy less treats

32% - I buy less ready meals / instant

cooked foods

40% - I combine trips and errands

54% - I only buy the essentials

42% - I buy store Own Label brands

33% - I buy products in bulk

25% - I read store leaflets and decide

which stores to go toSource: ShopperTrends; Base : All Supermarket (n=1417)

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

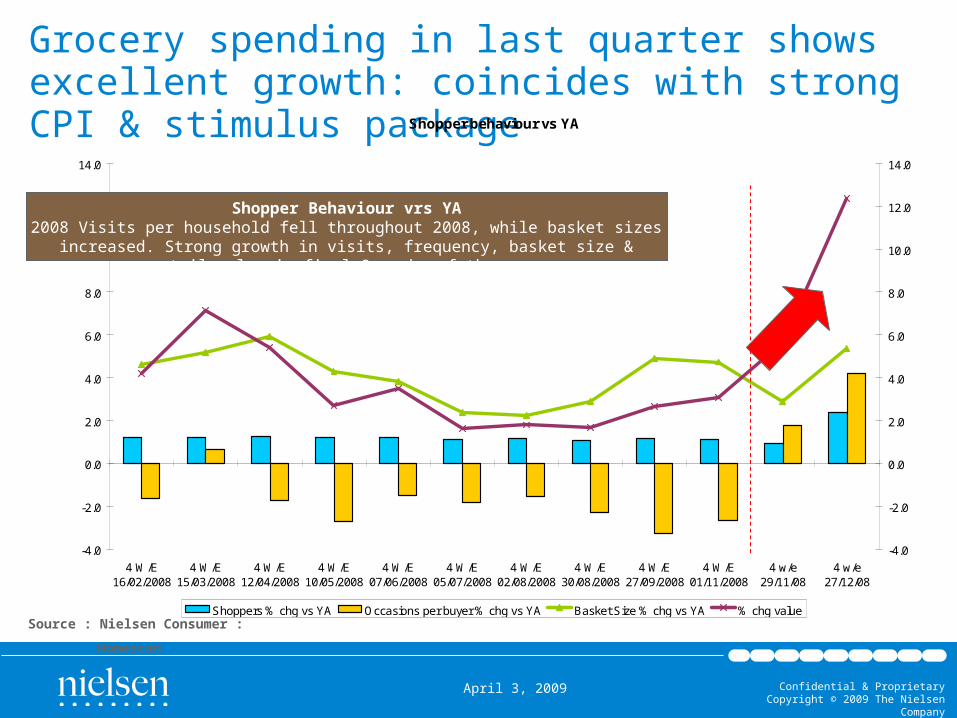

Grocery spending in last quarter shows excellent growth: coincides with strong CPI & stimulus package

Shopper behaviour vs YA

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

4 W/E16/02/2008

4 W/E15/03/2008

4 W/E12/04/2008

4 W/E10/05/2008

4 W/E07/06/2008

4 W/E05/07/2008

4 W/E02/08/2008

4 W/E30/08/2008

4 W/E27/09/2008

4 W/E01/11/2008

4 w/e29/11/08

4 w/e27/12/08

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Shoppers % chg vs YA Occasions per buyer % chg vs YA Basket Size % chg vs YA % chg value

Source : Nielsen Consumer : Homescan

Shopper Behaviour vrs YA2008 Visits per household fell throughout 2008, while basket sizes increased.

Strong growth in visits, frequency, basket size & retail value in final 8 weeks of the year

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

ALDI now accounts for nearly 6% of total grocery sales in Australia & 10% on the Eastern Seaboard

Source: Nielsen Consumer : Homescan

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

14

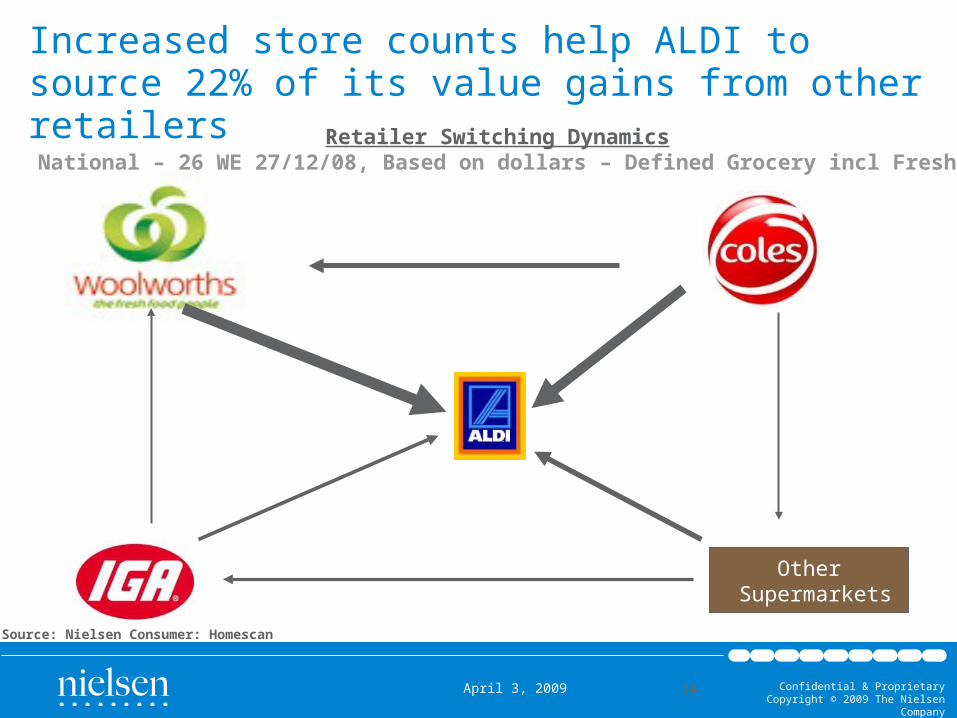

Increased store counts help ALDI to source 22% of its value gains from other retailers

Retailer Switching DynamicsNational – 26 WE 27/12/08, Based on dollars – Defined Grocery incl Fresh

Other Supermarkets

Source: Nielsen Consumer: Homescan

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Why do Australians love ALDI?Low Prices and Value for Money

1. Store is cheaper (55%)

2. Food & Groceries are Good Value

for money (53%)

3. Prices have increased: CPI impact

(23%)

4. Provides their own brands of

groceries which are a good

alternative to the main brand (37%)

5. Convenient to get to (30%)

Why are you spending more than you were 6 months ago at ALDI? Top 5 Reasons

Source: Homescan March Survey 2009 n=446 Based on those consumers who stated that they were spending more in-store in the latest 6 months

14% of panellists cited Quality of Fresh Food as the driver for increased spend in

ALDI

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Key Stories for 2009 Private Label growth and implications

Key Stories for 2009 and 2010•Private Label Growth & Response

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

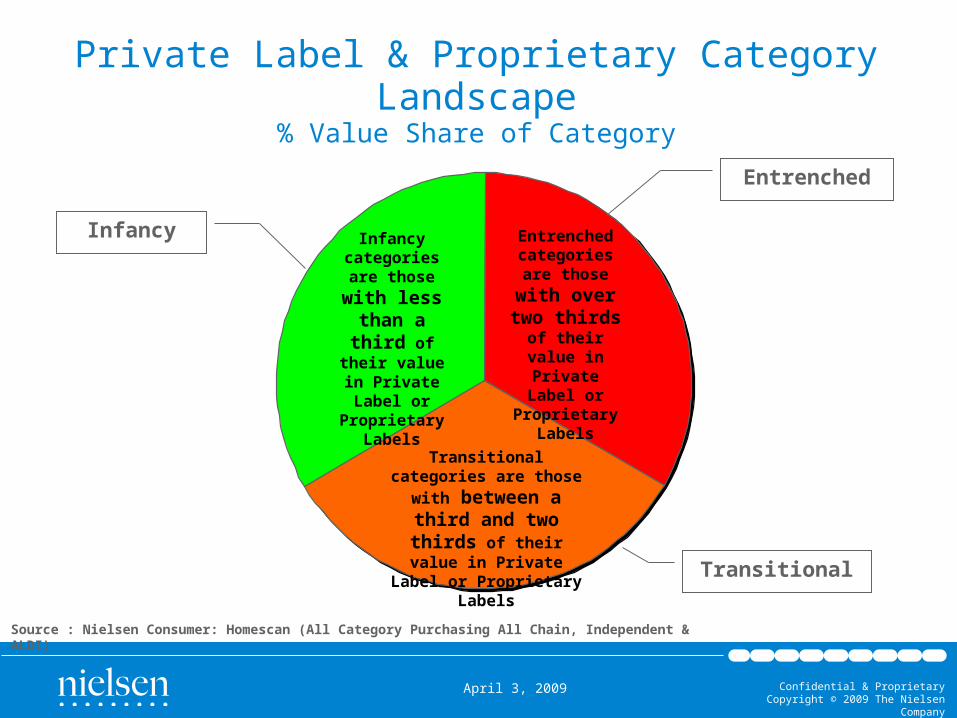

Private Label & Proprietary Category Landscape% Value Share of Category

Entrenched

Transitional

Infancy

Source : Nielsen Consumer: Homescan (All Category Purchasing All Chain, Independent & ALDI)

Infancy categories are

those with less than a third of their

value in Private Label or

Proprietary Labels

Entrenched categories are

those with over two

thirds of their value in Private

Label or Proprietary

Labels

Transitional categories are those with between a

third and two thirds of their value in Private Label

or Proprietary Labels

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Entrenched

Transitional

Infancy

Packaged Cakes

Eggs

Party & Picnic WareMilk

Packaged Bread

Seasonal Confectionary

Oil, Canned Fruit, Packaged Smallgoods, Cooking Needs

Pet Food & Care

Snack Food, Rice

Confectionery, Biscuits

Private Label & Proprietary Category Landscape% Value Share of Category

Source : Nielsen Consumer: Homescan (All Category Purchasing All Chain, Independent & ALDI)

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Entrenched

Transitional

Infancy

Canned Fruit 2008

Private Label & Proprietary Category Landscape% Value Share of Category 07-08

Canned Fruit 2007 4.4 point shift in 12 months

Source : Nielsen Consumer: Homescan (All Category Purchasing All Chain, Independent & ALDI)

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Entrenched

Transitional

Target

Seasonal Confectionary 2008

Private Label & Proprietary Category Landscape% Value Share of Category 07-08

Seasonal Confectionary 2007

19 point shift in 12 months

Source : Nielsen Consumer: Homescan (All Category Purchasing All Chain, Independent & ALDI)

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

•The 2008 Private Label ReportShare development by Retailer ChainCategory Highlights

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

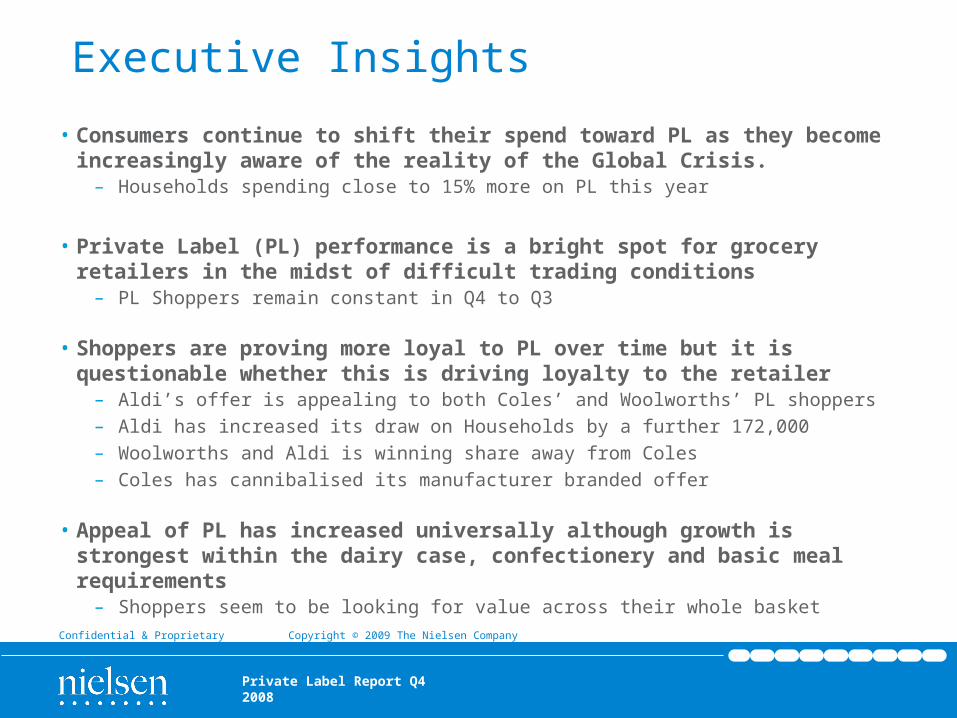

Executive Insights

• Consumers continue to shift their spend toward PL as they become increasingly aware of the reality of the Global Crisis.– Households spending close to 15% more on PL this year

• Private Label (PL) performance is a bright spot for grocery retailers in the midst of difficult trading conditions– PL Shoppers remain constant in Q4 to Q3

• Shoppers are proving more loyal to PL over time but it is questionable whether this is driving loyalty to the retailer– Aldi’s offer is appealing to both Coles’ and Woolworths’ PL shoppers– Aldi has increased its draw on Households by a further 172,000– Woolworths and Aldi is winning share away from Coles– Coles has cannibalised its manufacturer branded offer

• Appeal of PL has increased universally although growth is strongest within the dairy case, confectionery and basic meal requirements– Shoppers seem to be looking for value across their whole basket

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

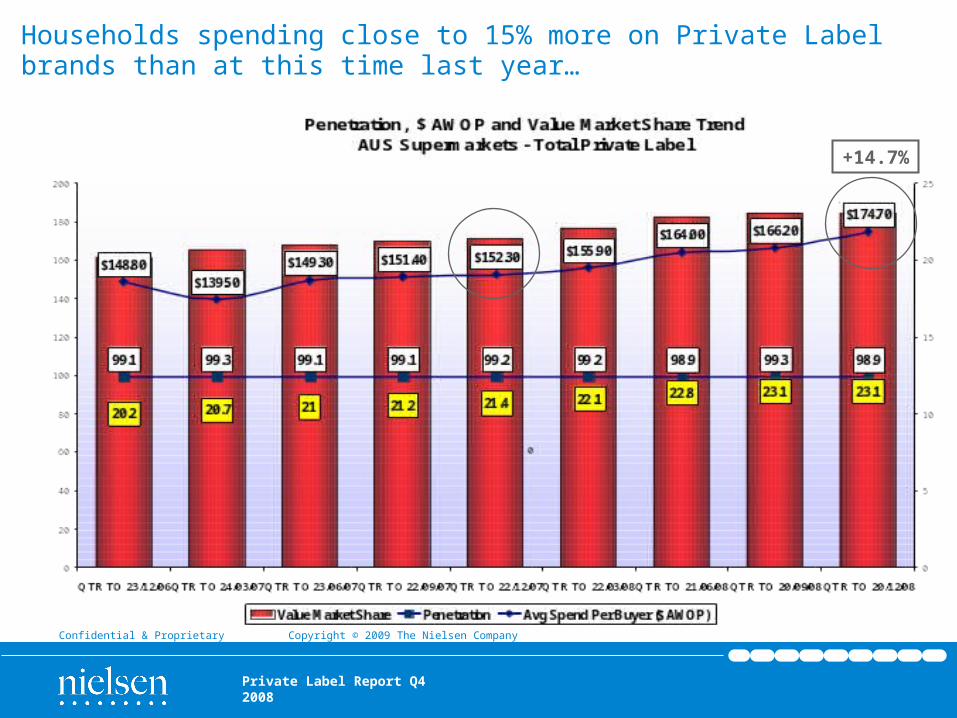

Households spending close to 15% more on Private Label brands than at this time last year…

+14.7%

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

ALDI - Contributing strongly to PL growth. Avg Household spend up 10% in Q4 vs YA, and new store openings bringing over 300k+ more Australian households through the doors

141 146 152 153 163 165 172

Aldi Store numbers reported for final month of quarter

200+

Read as: 93.4% of ALDI sales is PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Aldi’s growth continues to be dominated by customers’ switching their spend from other retailers

Even existing ALDI PL buyers are spending

more in-store

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

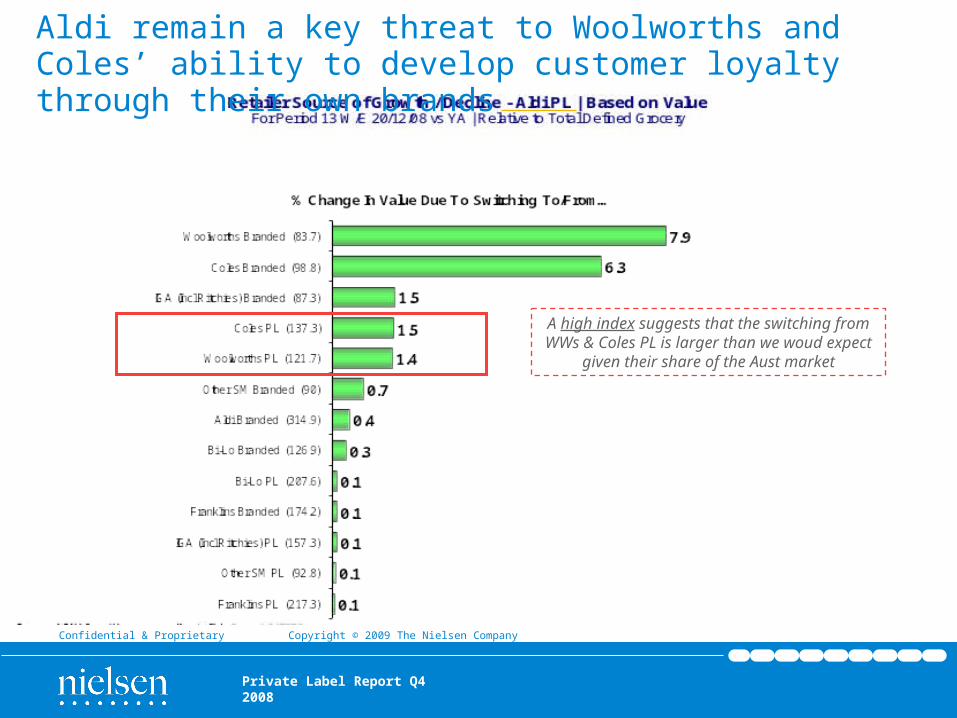

Aldi remain a key threat to Woolworths and Coles’ ability to develop customer loyalty through their own brands

A high index suggests that the switching from WWs & Coles PL is larger than we woud

expect given their share of the Aust market

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Woolworths – Similarly, Avg household spend up 10% on YA, helping to lift PL sales, however buyer numbers are down slightly

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

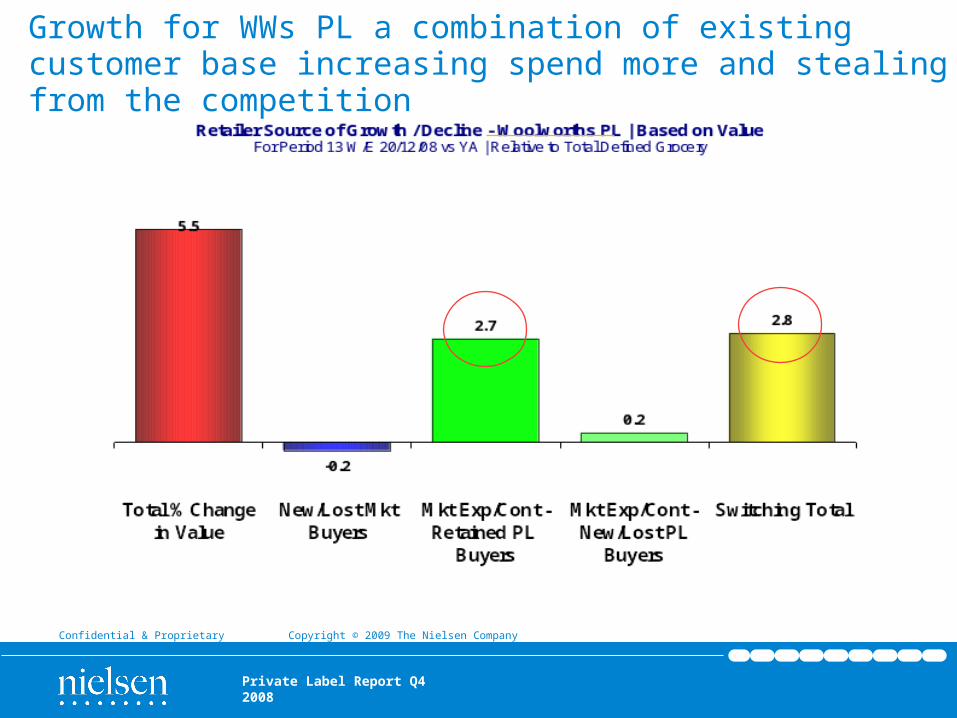

Growth for WWs PL a combination of existing customer base increasing spend more and stealing from the competition

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

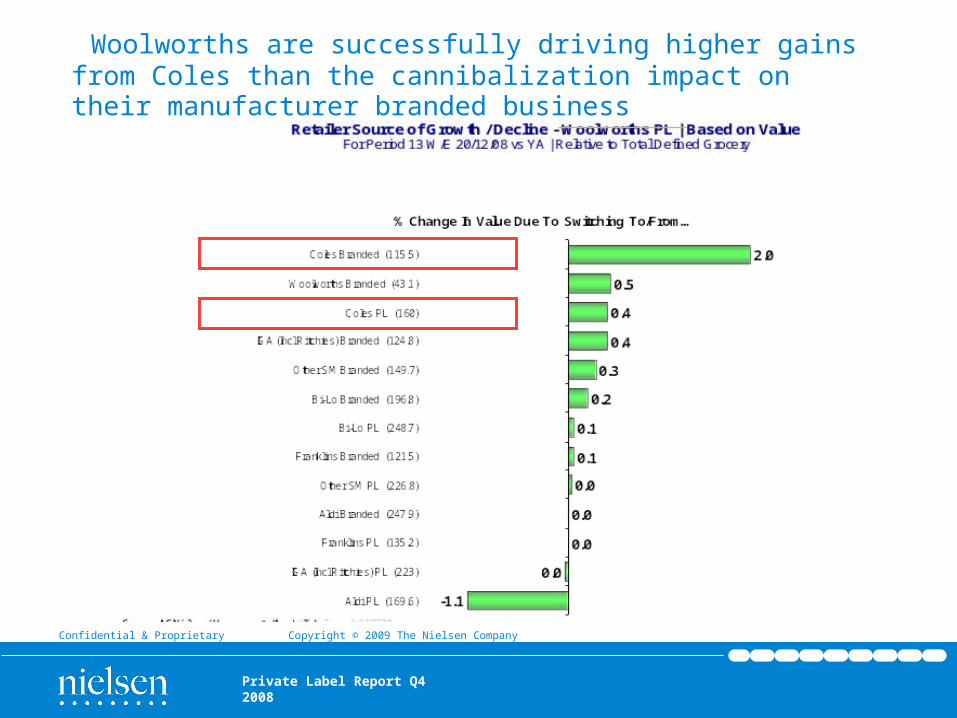

Woolworths are successfully driving higher gains from Coles than the cannibalization impact on their manufacturer branded business

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Coles – Despite buyer numbers flat, average spend up 12.4% on LY, resulting in 1pt share increase for Coles PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Coles growth coming primarily from existing shoppers spending more, whilst some growth being off-set by shoppers switching (mainly) to ALDI

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

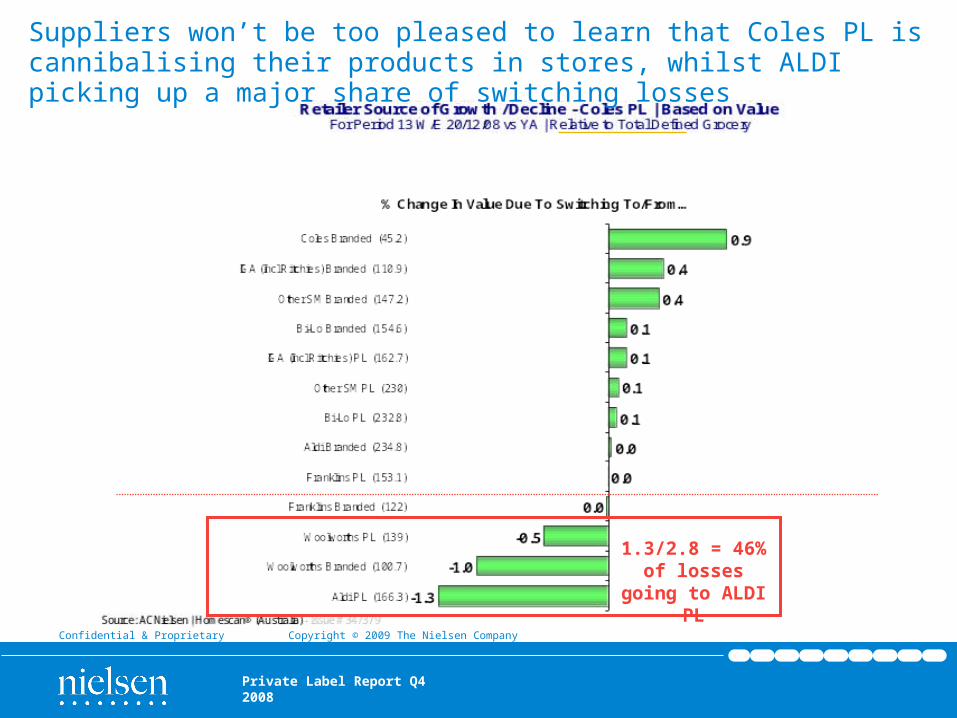

Suppliers won’t be too pleased to learn that Coles PL is cannibalising their products in stores, whilst ALDI picking up a major share of switching losses

1.3/2.8 = 46% of losses going to

ALDI PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

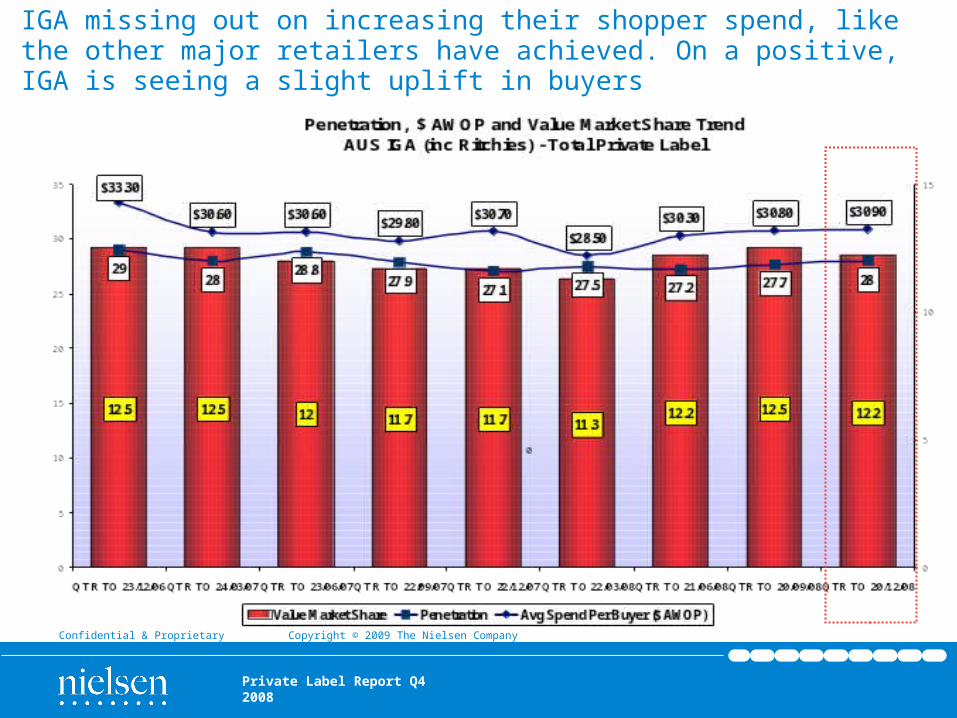

IGA missing out on increasing their shopper spend, like the other major retailers have achieved. On a positive, IGA is seeing a slight uplift in buyers

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Increased penetration accounting for 50% of IGA PL growth. Remaining coming from existing buyers

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

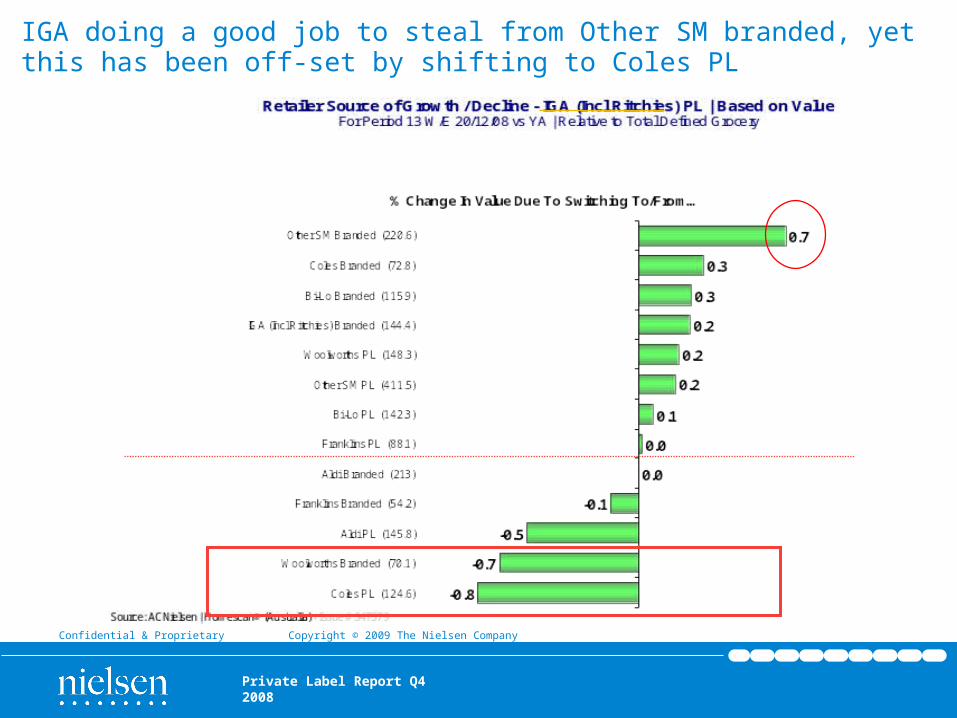

IGA doing a good job to steal from Other SM branded, yet this has been off-set by shifting to Coles PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Conclusions

•Despite Woolworths PL penetration falling in Q4 they continue to build steadily TY on LY. They are successfully winning custom from Coles (both PL and branded).

•With the PL penetration getting stronger Coles have managed to increase the average spend by 12.4% Q4.Despite having bigger losses in Q4 than Q3 to Woolworths and Aldi.

• Amongst the smaller chains PL market share has remained constant in Q4.

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Private Label Report Q1 09

Homescan Date to 21/03/2009

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Household PL spending is up 7.7% on this time last year. While Penetration is down slightly by .2% on LY

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

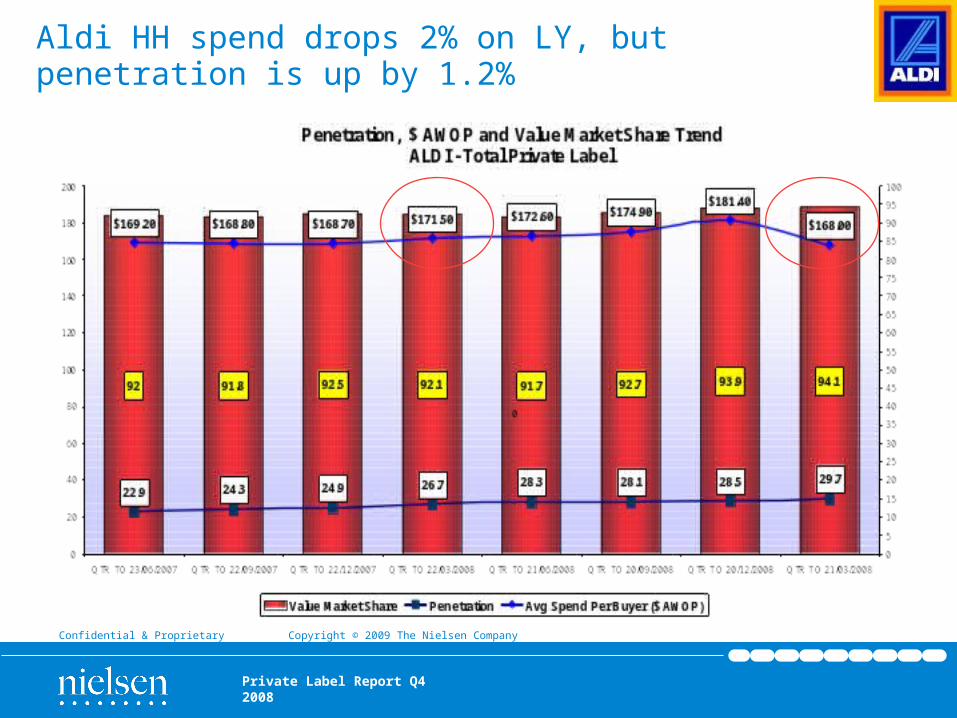

Aldi HH spend drops 2% on LY, but penetration is up by 1.2%

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

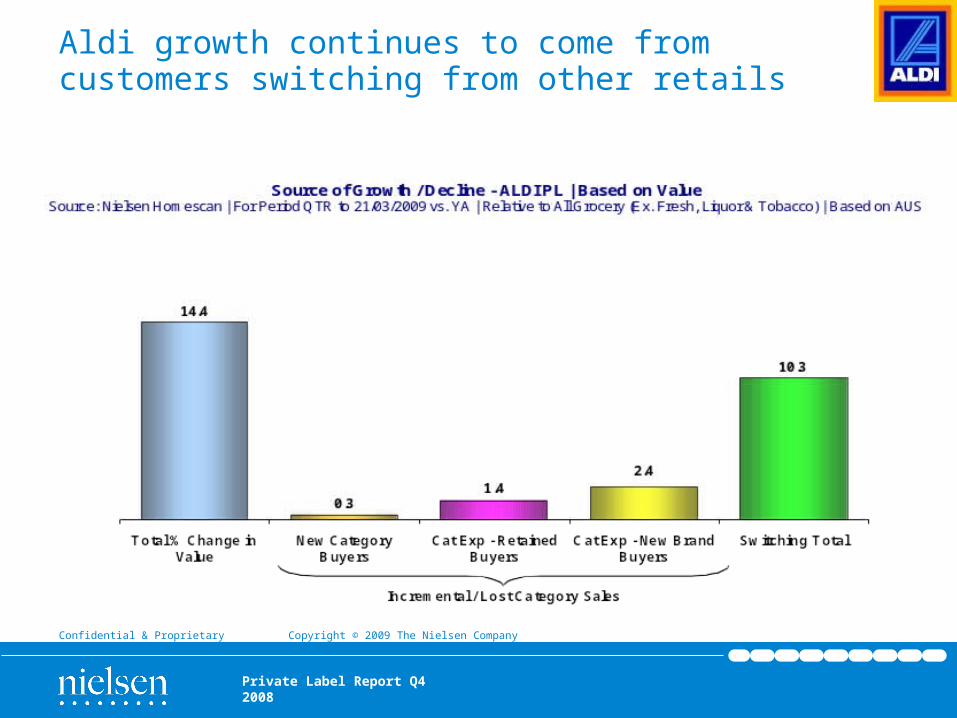

Aldi growth continues to come from customers switching from other retails

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

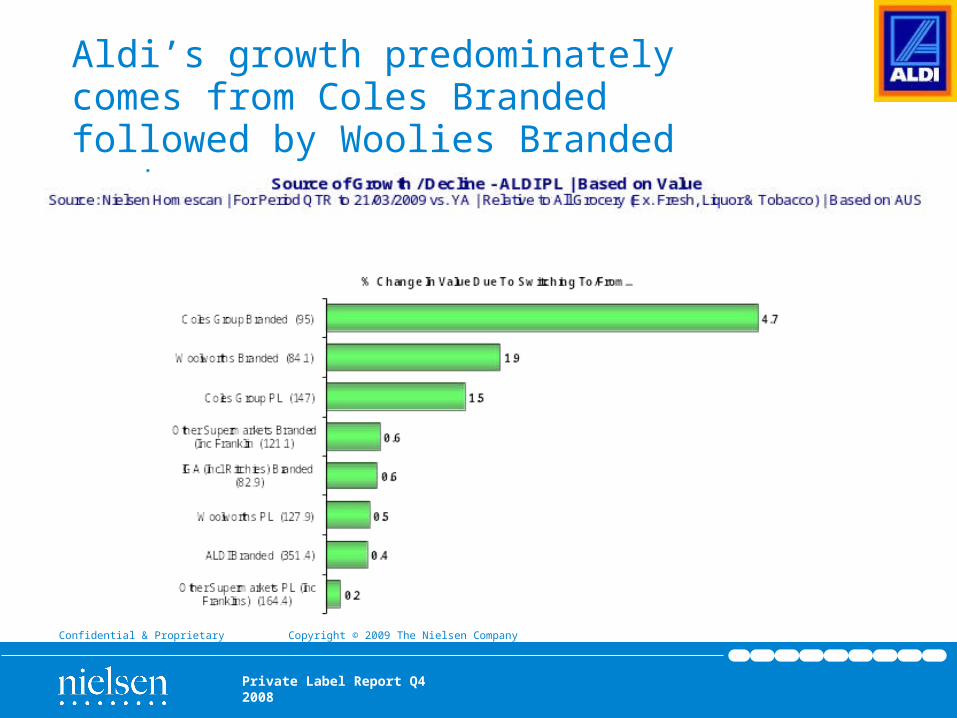

Aldi’s growth predominately comes from Coles Branded followed by Woolies Branded customers

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Woolworths HH Spend is up by 6% on this time last year while penetration is by 1.1%

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

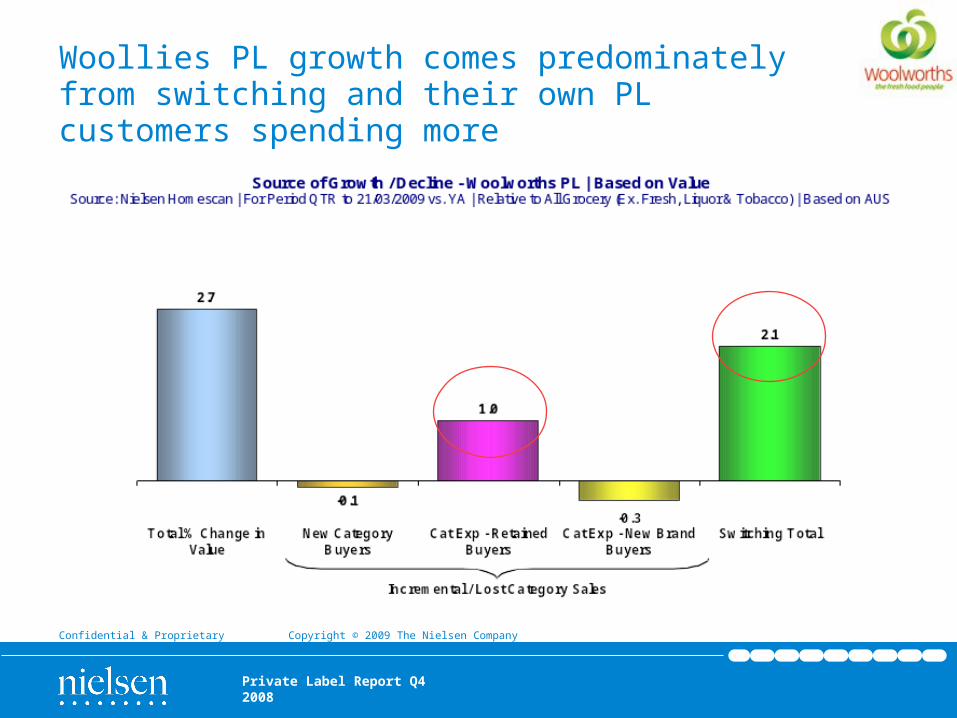

Woollies PL growth comes predominately from switching and their own PL customers spending more

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Woollies switching growth comes from Coles Branded and PL while they lose they still lose customers to Aldi

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

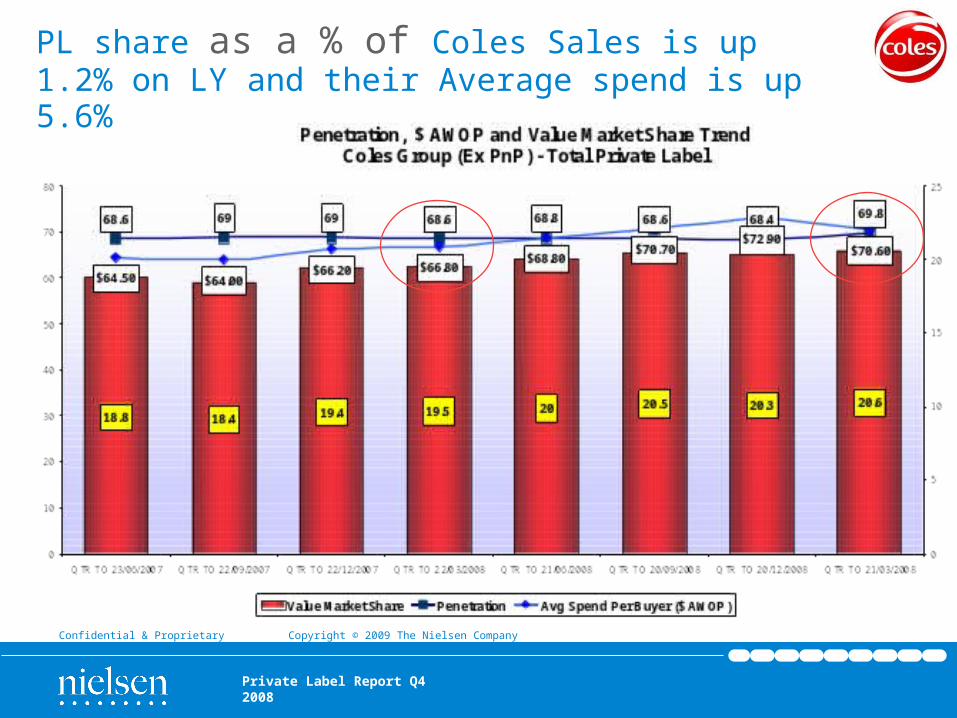

PL share as a % of Coles Sales is up 1.2% on LY and their Average spend is up 5.6%

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

…….But over all Coles are losing PL sales with switching, yet they are managing to convert their existing PL customers to spend more.

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Coles PL customers are switching to Woolworths branded, Aldi PL and gaining from Coles Branded

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

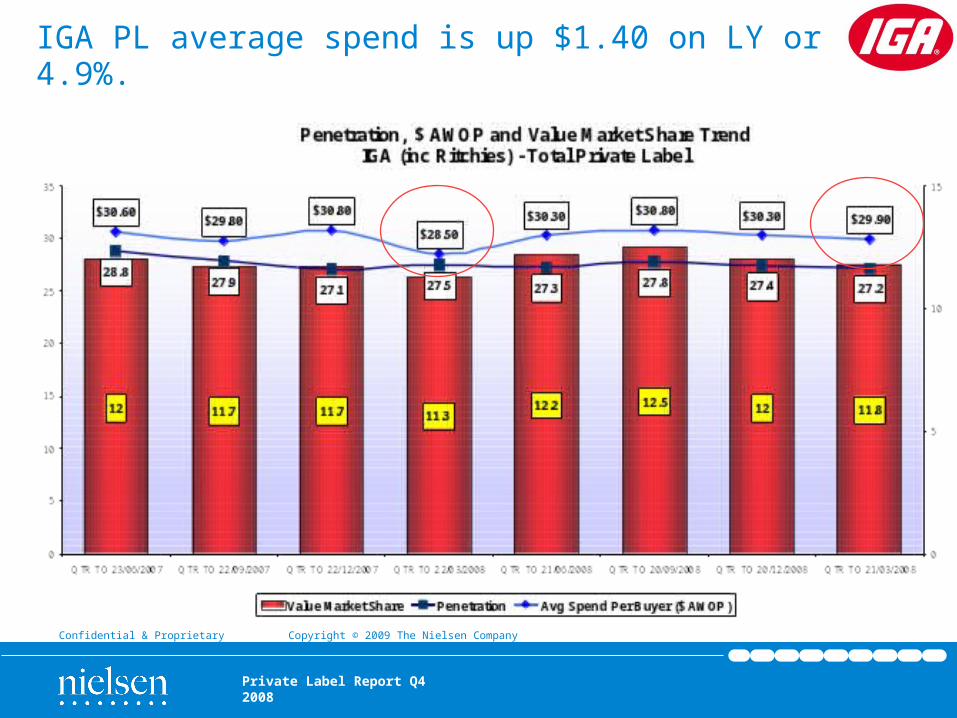

IGA PL average spend is up $1.40 on LY or 4.9%.

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

IGA Pl growth is coming from .8% customers switching to IGA PL and 1.7% growth in their own PL customers spending more.

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

IGA is gaining PL sales from their own branded but some gain is offset to Woolworths Branded and PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

PL Highlights

• Aldi is stealing sales from both Coles and Woolworths Branded customers.

•Woolworths is gaining sales from Coles Branded and PL customers

•Coles is not only losing sales to Aldi and Woolworths but is successfully switching their own branded customers to PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

52

Who’s getting Who’s Customers?

Retailer Switching DynamicsNational – 26 WE 27/12/08, Based on dollars – Defined Grocery incl Fresh

Other Supermarkets

Source: Nielsen Consumer: Homescan

Confidential & Proprietary Copyright © 2007 The Nielsen Company

Private Label Report

Customers attitudes toward PL

Confidential & Proprietary Copyright © 2007 The Nielsen Company

•In the last month have you bought any Woolworth Select, You'll Love Coles or any other store branded products?

–Yes 81%–No 16%

•.Compared to one year ago, would you say that you have bought more or less store branded products in the last month?

–The same 50%–More 37%

What are Customers attitudes toward PL

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Perceptions of Private Label overall have not changed significantly over the years, generally consumer believe they are as good as branded

House brand/generic products (those made specifically for a certain store) are generally as good as other branded products in a category.

Homescan PanelViews Australia

8% 6% 6% 7%

41%41% 43% 43%

35% 36% 32%33%

14% 14%16%

14%

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

2005 2006 2007 2008

% H

ou

seh

old

s

Strongly disagree

Disagree

Neither agree nordisagree

Agree

Strongly agree

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

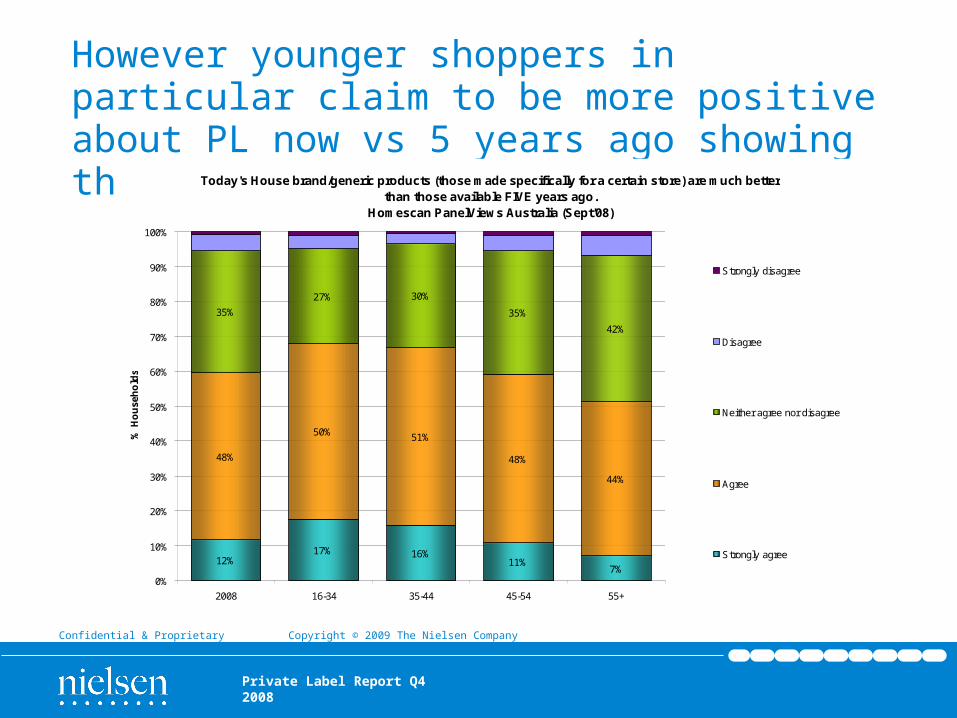

However younger shoppers in particular claim to be more positive about PL now vs 5 years ago showing that PL has kept pace with brands

Today's House brand/generic products (those made specifically for a certain store) are much better than those available FIVE years ago.

Homescan PanelViews Australia (Sept'08)

12%17% 16%

11%7%

48%

50% 51%

48%

44%

35%

27% 30%

35%

42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 16-34 35-44 45-54 55+

% H

ou

seh

old

s

Strongly disagree

Disagree

Neither agree nor disagree

Agree

Strongly agree

Confidential & ProprietaryCopyright © 2009 The Nielsen Company

45

45

47

50

52

52

55

55

55

61

61

63

66

69

74

77

86

87

SafewayFranklins

Soul PattinsonAldi

Coles $mart BuysChemists Own

IGAWoolworths Fresh

Terry WhiteYou'll Love Coles

AmcalBi-Lo

PricelineNo Frills

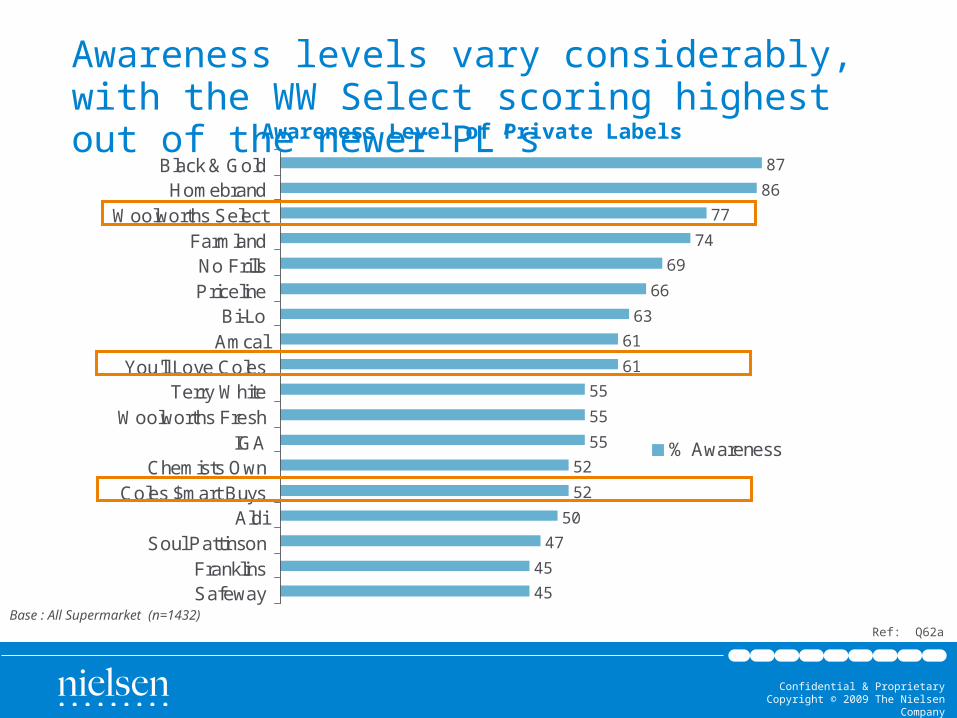

FarmlandWoolworths Select

HomebrandBlack & Gold

% Awareness

Ref: Q62aBase : All Supermarket (n=1432)

Awareness Level of Private Labels

Awareness levels vary considerably, with the WW Select scoring highest out of the newer PL’s

Confidential & ProprietaryCopyright © 2009 The Nielsen Company

1

1

8

12

12

14

15

16

19

19

26

26

27

29

33

36

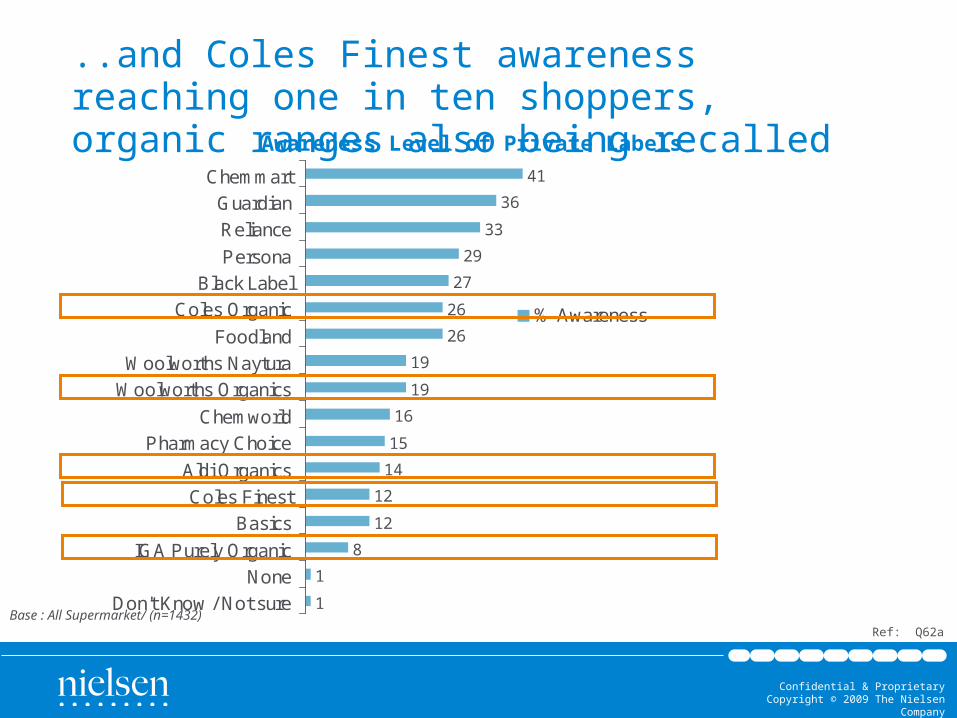

41

Don't Know / Not sure

None

IGA Purely Organic

Basics

Coles Finest

Aldi Organics

Pharmacy Choice

Chemworld

Woolworths Organics

Woolworths Naytura

Foodland

Coles Organic

Black Label

Persona

Reliance

Guardian

Chemmart

% Awareness

Awareness Level of Private Labels

Ref: Q62aBase : All Supermarket/ (n=1432)

..and Coles Finest awareness reaching one in ten shoppers, organic ranges also being recalled

Confidential & Proprietary Copyright © 2007 The Nielsen Company

•If you have bought more PL than a year ago why you have bought more?

Cheaper Price–71.9%

Improved Quality–40.7%

Increased PL Choice–18.3%

# %

Respondents 526

Price/ Cheaper 378 71.9

Improved Quality 214 40.7

Increased PL Choice 96 18.3

Increased PL Availability 11 2.1

Stores replacing with PL 31 5.9

Better packaging/ appearance 14 2.7

What are Customers attitudes toward PL

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Implications for You

•Question: How are you responding to the changes in private label?

•Need for a tailored response by category…

•What’s your “something special”?

April 3, 2009 Confidential & ProprietaryCopyright © 2009 The Nielsen Company

Implications for You

• Critical to develop internal understanding of the role of your categories within each retailer – Defined by consumer needs and engagement

• Opportunity – Fresh Foods – In Home Solutions– to promote entertainment/eating at home solutions– Including cook from scratch solutions– Imperative is to locate key communication moments pre-store and

instore by category by occasion

Private Label Report Q4 2008

Confidential & Proprietary Copyright © 2009 The Nielsen Company

Thank you

Confidential & Proprietary Copyright © 2007 The Nielsen Company