newfound’s dynamic momentum - cranbergercommunity.cranberger.com/sites/default/files/... ·...

TRANSCRIPT

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

1

Newfound Research White Paper

Newfound’s Dynamic Momentum

An Introduction to MomentumMomentum, also known as trend-following or relative-strength, is one of the oldest investment strategies and most well-researched phenomena in the marketplace. The strategy is the core of two of Wall Street’s oldest adages: “cut your losses [short] and let your profits run” (a quote frequently attributed to British economist David Ricardo) and Marty Zweig’s “the trend is your friend.”

Momentum indicators are reactive -- security price behavior is translated into strength / weakness signals that are agnostic to fundamental valuation and economic circumstance. Momentum strategies are therefore opportunistic, seeking to invest in securities that have exhibited recent outperformance and avoid those that have exhibited recent underperformance.

The existence of momentum is a market anomaly which financial theory struggles to explain. An increase in asset prices, in and of itself, should not warrant further increase according to the efficient market hypothesis. Such an increase is warranted only by changes in demand and supply or by new information. Even Eugene Fama and Kenneth French (1996) have found the momentum anomaly to be the largest discrepancy to their own Fama-French model, remaining unexplained by standard market, size and value risk factors.

“The premier [market] anomaly is momentum.” Eugene Fama & Kenneth French (2007)

2

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

Momentum Exists in Most PortfoliosFor nearly two decades, momentum has generally been accepted in academia as a distinct driver of return premiums, although the root cause of the anomaly is still highly debated. The inefficiency is most commonly explained as being due to investor’s behavioral biases, such as:

• Herding (also known as the “bandwagon” effect)• The over- or under-reaction to new information• Confirmation bias (ignoring information contradictory to your beliefs)• The asymmetric response of investors to gains and losses

The majority of investors already utilize a momentum core in their strategic investments without necessarily realizing it. Market-capitalization weighted indices are one of the most efficient ways to implement a momentum strategy. Market capitalization is the price of security multiplied by the number of shares outstanding. Therefore, as the price of a security increases, so does its market capitalization, and therefore it receives greater weight in a market capitalization weighted index. Similarly, as the price of a security falls, so does its market capitalization, and therefore it receives less weight in a market capitalization weighted index.

Absolute & Relative MomentumMomentum has historically been attractive as an active strategy because of its durability and robustness across asset classes and in different time periods.

The goal of absolute momentum is to identify those periods when bearing market risk makes the most sense. Faber (2007), extending the work of Jeremy Siegel in his book “Stocks for the Long Run,” utilized a simple 10-month moving-average technique as an absolute momentum screen across a variety of asset classes, reporting results that had “equity-like returns with bond-like volatility and drawdown.”

Relative momentum measures are generally based on relative total returns between securities. Frequently, near-term months are skipped due to short-term mean-reversion exhibited by many asset classes. For example, AQR’s momentum indices rank stocks based on their previous 12 month returns minus the most recent month’s return, and the top 33% of equities are selected.

When the Trend is Not Your FriendInvestments do not exhibit momentum over all time horizons. Evidence shows that momentum is a driving factor over a variety of asset classes over 3 to 12 month measurement periods, after which the advantage begins to fade. Berger, Ronen, and Moskowitz (2009) explain that securities which out-perform over longer periods of time actually become relatively expensive and tend to under-perform their peers.

When no trend exists, momentum strategies can suffer from whipsaw (the consistent mis-timing in the purchase and sale of securities) and excessive costs from high turnover. In the worst case scenario, a portfolio might suffer a “death from a thousand paper cuts” before a trend re-emerges. It is critical, therefore, to employ a process that is as robust as possible to these risks.

Introducing Newfound’s Dynamic MomentumWhether relative or absolute, the consistent theme shared by almost all momentum investors is the reliance on a fixed time-horizon to identify momentum. At Newfound Research, we believe that this methodology ignores the critical fact that while returns are measured over time, valuations change relative to the flow of new information into the marketplace.

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

3

Our process begins by looking at momentum over a dynamic time-horizon instead of a fixed time-horizon window. Three measures are utilized in constructing the dynamic window:

• A security’s total return

• A security’s volatility

• A security’s volatility-of-volatility (“vol-of-vol”)

These factors are utilized to attempt to identify which security movements can be dismissed as noise and which represent significant trend movements. Our thesis is that when significant information moves into the market, a security’s price should react beyond what can be explained as day-to-day market noise. As significant information flows into the market more frequently, the dynamic window will shrink, becoming more adaptive to short-term changes. As more time elapses between significant information, the dynamic window expands, becoming more robust to short-term fluctuations.

A Dynamic EngineTo explore how a dynamic window can drive a model, consider the graph below which displays the price of the S&P 500 ETF SPY, its 50-day moving average, its 200-day moving average, and a moving average built upon a dynamic time-horizon window.

By comparing the behavior of the dynamic moving average to the fixed-length moving averages, we can see that size of the dynamic window changes depending on the market environment. In 2005, the

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

4

dynamic moving-average behaved very similarly to the 200-day moving average, as directional movement in SPY is slow and small relative to the size of volatility, corresponding to what many traders would call a “slow” market. In 2008, however, the dynamic moving average behaved like the 50-day moving average, as directional movement has become fast and large relative to volatility, corresponding to what traders might call a “fast” market.

Our ModelsAt Newfound Research, our proprietary dynamic window technology powers two models that seek to identify and capture momentum opportunities: our Absolute Exposure (A.E.) model and our Relative Exposure (R.E.) model.

The Absolute Exposure model is utilized to identify absolute momentum opportunities, providing a binary “in or out” decision on a given security. The Relative Exposure model is utilized to identify relative momentum opportunities between securities, identifying which of two securities is exhibiting the greater momentum opportunity.

Benefits of a Dynamic ProcessIn our research paper “Seeking Timeless Momentum,” we compare a fixed window momentum model to our dynamic window momentum process. For each security in the S&P 500, we create two “switching” strategies -- one driven by the fixed window model and one by the dynamic window model. The switching strategy allocates fully either to the security or the S&P 500 at a given time, depending on which is exhibiting greater momentum.

Figure 1: Relative percentage of trades in fixed-window model versus dynamic-window model

Figure 2: The “smile” of the fixed-window model strategies; a plot of strategy returns versus benchmark returns

Figure 3: The “smile” of the dynamic-window model strategies; a plot of strategy returns versus benchmark

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

5

Figure 1 plots the distribution of the relative number of trades in the dynamic window strategies relative to their fixed window counter-parts. On average, we find that the strategies driven by the dynamic window process trade 60% less frequently than their fixed-window counter-parts, reducing both turn-over and whipsaw costs.

Figures 2 and 3 exhibit the momentum “smiles” for the fixed window and dynamic window strategies. The smile occurs when strategy returns are plotted against benchmark returns, highlighting the fact that momentum strategies tend to perform better when the underlying securities exhibit more extreme returns. Comparing the two smiles, we see that the dynamic window smile is steeper, indicating a more efficient momentum capture. Furthermore, we see more points above the 0% horizontal line, indicating that fewer strategies resulted in negative returns due to whipsaw and trading costs.

The Role of Momentum in Your PortfolioMany researchers have discovered benefits in combining value and momentum strategies, finding that their diversified approaches can lead to increased annualized returns, lower volatility, reduced maximum drawdown, and increased stability in returns. The negative correlation of these two strategies can be intuitively understood: securities with strong momentum tend to have risen in price and offer less value, while securities with strong value have often fallen in price and have poor momentum. Therefore, a portfolio built from a combination of these strategies captures the power of diversification.

The following chart demonstrates that active returns of equity value strategies applied across varying geographic regions exhibit little to no diversification opportunities (active returns are measured as monthly return differences between the portfolio and a market-capitalization weighted benchmark; index data from MSCI®).

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

6

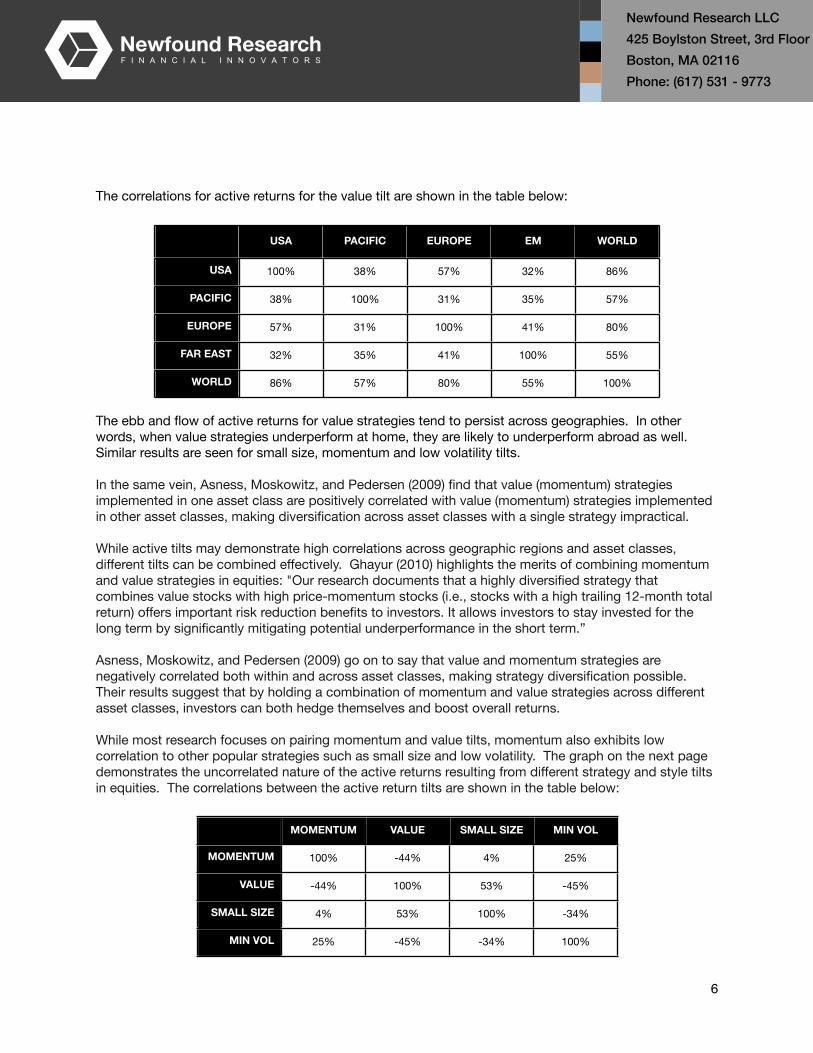

The correlations for active returns for the value tilt are shown in the table below:

USA PACIFIC EUROPE EM WORLD

USA 100% 38% 57% 32% 86%

PACIFIC 38% 100% 31% 35% 57%

EUROPE 57% 31% 100% 41% 80%

FAR EAST 32% 35% 41% 100% 55%

WORLD 86% 57% 80% 55% 100%

The ebb and flow of active returns for value strategies tend to persist across geographies. In other words, when value strategies underperform at home, they are likely to underperform abroad as well. Similar results are seen for small size, momentum and low volatility tilts.

In the same vein, Asness, Moskowitz, and Pedersen (2009) find that value (momentum) strategies implemented in one asset class are positively correlated with value (momentum) strategies implemented in other asset classes, making diversification across asset classes with a single strategy impractical.

While active tilts may demonstrate high correlations across geographic regions and asset classes, different tilts can be combined effectively. Ghayur (2010) highlights the merits of combining momentum and value strategies in equities: "Our research documents that a highly diversified strategy that combines value stocks with high price-momentum stocks (i.e., stocks with a high trailing 12-month total return) offers important risk reduction benefits to investors. It allows investors to stay invested for the long term by significantly mitigating potential underperformance in the short term.”

Asness, Moskowitz, and Pedersen (2009) go on to say that value and momentum strategies are negatively correlated both within and across asset classes, making strategy diversification possible. Their results suggest that by holding a combination of momentum and value strategies across different asset classes, investors can both hedge themselves and boost overall returns.

While most research focuses on pairing momentum and value tilts, momentum also exhibits low correlation to other popular strategies such as small size and low volatility. The graph on the next page demonstrates the uncorrelated nature of the active returns resulting from different strategy and style tilts in equities. The correlations between the active return tilts are shown in the table below:

MOMENTUM VALUE SMALL SIZE MIN VOL

MOMENTUM 100% -44% 4% 25%

VALUE -44% 100% 53% -45%

SMALL SIZE 4% 53% 100% -34%

MIN VOL 25% -45% -34% 100%

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

7

By diversifying a portfolio across strategy and style tilts, a smoother active return curve is achieved:

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

8

ConclusionMomentum is a powerful investment style. Few market anomalies exhibit the robustness to academic critiques and market competition factors that momentum does.

Traditional methods of identifying momentum opportunities utilize a fixed-length measurement period. We believe that by utilizing a dynamic window we can increase our opportunity set. Our initial studies show that a dynamic process can improve upon a standard momentum model’s return results, both before and after fees, while reducing costs typically associated with momentum such as whipsaw and high turnover.

We believe such a process will enable investors to enhance portfolio diversification and increase expected risk-adjusted returns through more efficient momentum capture.

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

9

References

Antonacci, Gary, Risk Premia Harvesting Through Dual Momentum (January 28, 2013). Available at SSRN: http://ssrn.com/abstract=2042750 or http://dx.doi.org/10.2139/ssrn.2042750

Asness, Clifford S., Moskowitz, Tobias J. and Pedersen, Lasse Heje, Value and Momentum Everywhere (March 6, 2009). AFA 2010 Atlanta Meetings Paper. Available at SSRN: http://ssrn.com/abstract=1363476 or http://dx.doi.org/10.2139/ssrn.1363476

Berger, Adam L., Israel, Ronen and Moskowitz, Tobias J. (2009) The Case for Momentum Investing. Available through: AQRIndex http://www.aqrindex.com/resources/docs/PDF/News/News_Case_for_Momentum.pdf [Accessed: 17th March 2013].

Faber, Mebane T., A Quantitative Approach to Tactical Asset Allocation (February 17, 2009). Journal of Wealth Management, Spring 2007. Available at SSRN: http://ssrn.com/abstract=962461

Faber, Mebane T., Relative Strength Strategies for Investing (April 1, 2010). Available at SSRN: http://ssrn.com/abstract=1585517 or http://dx.doi.org/10.2139/ssrn.1585517

Fama, Eugene F. and French, Kenneth R., Dissecting Anomalies (June 2007). CRSP Working Paper No. 610. Available at SSRN: http://ssrn.com/abstract=911960 or http://dx.doi.org/10.2139/ssrn.911960

Fama, E. and French, K. (1996) Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance, 51 (1), p.55-84. Available at: http://faculty.chicagobooth.edu/john.cochrane/teaching/35904_Asset_Pricing/Fama_French_multifactor_explanations.pdf [Accessed: 17th March 2013].

Ghayur, Khalid (2010) Using momentum to help mitigate risk. [online] Available at: http://systematicrelativestrength.com/2010/09/07/using-momentum-to-help-mitigate-risk/ [Accessed: 17 Mar 2013].

Hurst, Brian, Ooi, Yao H. and Pedersen, Lasse H. (2012) A Centure of Evidence on Trend-Following Investing. [online] Available through: http://gallery.mailchimp.com/6750faf5c6091bc898da154ff/files/A_Century_of_Evidence_on_Trend_Following.pdf [Accessed: 17th March 2013].

Jegadeesh, N. and Titman, S. (1993) Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48 (1), p.65-91. Available at: http://www.jstor.org/discover/10.2307/2328882?uid=2&uid=4&sid=21101783565343 [Accessed: 17th March 2013].

Shaik, Rasool (2011) Risk-Adjusted Momentum: A Superior Approach to Momentum Investing. [online]. Available at: http://dorseywrightmm.com/downloads/hrs_research/Momentum%20White%20Paper%202011%20Fall.pdf [Accessed: 17 Mar 2013].

Newfound Research LLC

425 Boylston Street, 3rd Floor

Boston, MA 02116

Phone: (617) 531 - 9773

10

For more information about Newfound Research call us at + 1-617-531-9773 or visit us at www.thinknewfound.comor email us at [email protected]

• These materials are proprietary to Newfound Research LLC and may not be reproduced, modified, transmitted, transferred or distributed in any form without the prior written consent of Newfound Research LLC.

• These materials are subject to confidentiality obligations that the recipient owes to Newfound Research LLC. Any disclosure of these materials without Newfound Research LLC’s prior written consent is strictly prohibited and in violation of ongoing contractual restrictions. The recipient of these materials agrees to keep them and all contents confidential.

• These materials represent an assessment of the market environment at specific points in time and are intended neither to be a guarantee of future events nor as a primary basis for investment decisions. The performance results should not be construed as advice meeting the particular needs of any investor. Neither the information presented nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any security. Past performance is not indicative of future performance and investments in equity securities do present risk of loss. Newfound Research LLC’s results are historical and their ability to repeat could be effected by material market or economic conditions, among other things.

Copyright © Newfound Research LLCAll rights reserved.