new priorities in asset management · ©2015 new priorities in asset management christopher w....

TRANSCRIPT

©2015

NEW PRIORITIES IN ASSET MANAGEMENT

CHRISTOPHER W. ROSCOEDIRECTOR AND RETAIL SECTOR HEAD

CLARION PARTNERS

©2015

mobile.icsc.org

©2015

INTRODUCTIONS

©2015

MARKET OUTLOOK

©2015

Key Market Trends

• Demand

– Steady growth forecast: GDP expanding at 2.5% - 3.0%

– Expanding labor markets and consumer spending

– Shifting real estate demand based on socioeconomic trends

• Supply

– New supply lagging historic levels

– Obsolescence of growing percentage of existing space

• Capital Markets

– Increased demand for core real estate driven by strong US and foreign capital flows

– Strong yields compared to core pricing, resulting in attractive risk-adjusted returns

©2015

A Backdrop of Steady Growth Sets the Stage for Increased Demand

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Annaul Job Growth (Millions)

Annual Real GDP Growth

Employment (right)

GDP (left)

©2015

Strong Sectors Drive Shift in Demand

©2015

New Supply Remains Well Below Historic AveragesObsolescence of existing space further increases demand for well-located, modern functional space

©2015

Rental Increases Following Occupancy Recovery

Source: CBRE-EA, Reis, Clarion Partners Investment Research, November 2014. Note: The forecasted data was provided by Clarion Partners Investment Research, dated November 2014.

Please see important information regarding forecasts and projections at the beginning of this presentation.

©2015

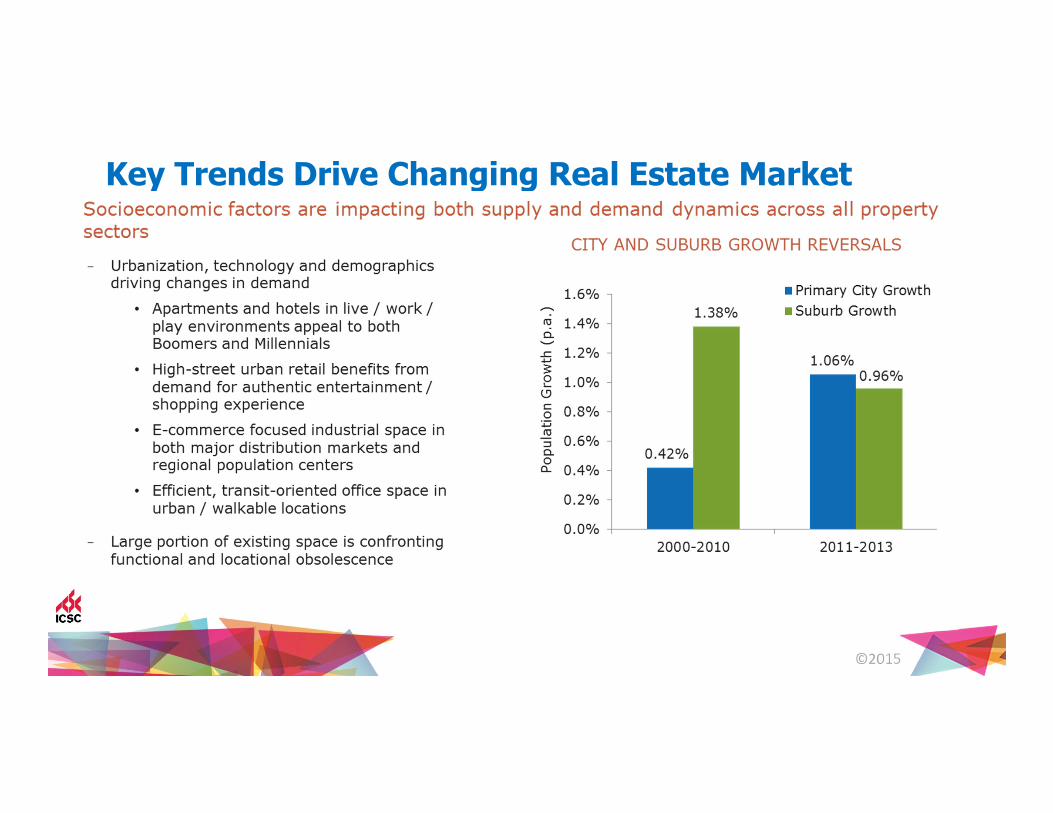

Key Trends Drive Changing Real Estate Market

©2015

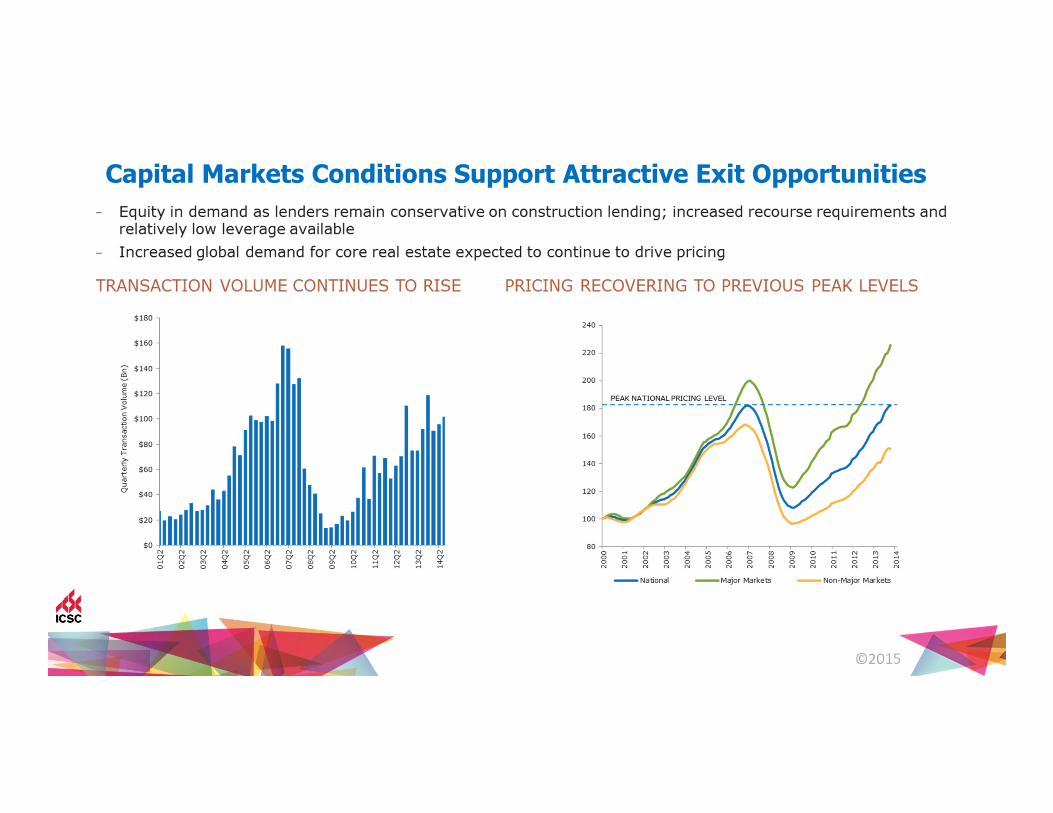

Capital Markets Conditions Support Attractive Exit Opportunities

©2015

RETAIL MARKET OUTLOOK

©2015

U.S. Retail Market Outlook

©2015

Retail: Highest Risk-Adjusted Total Return

©2015

Total Retail Sales Are Now 17% Above the Prior Peak, Driven By Strong Job Gains

©2015

While Income and Wealth Inequality Are Reflected in Bifurcation in Retail Demand, Declining Fuel Prices Benefit All Consumers

©2015

E-commerce Expanding Rapidly at 16% Year-Over-Year And Now Accounts for 8.5% of Core Retail Sales

©2015

Store Formats Shrinking While Major Retailers Are Taking Less Space And Focusing on More Profitable Stores and Locations

©2015

Retail Growth Moderating With Growing Divergence Between Top and Bottom Retailers

©2015

Retail Fundamentals Strengthening Supported by the Lowest New Supply in 25 Years

©2015

Clarion’s Focus: High-Street Retail, Market-Dominant Necessity/Value-Oriented Retail and Neighborhood and Power Centers

©2015

ECONOMIC CONCLUSIONS / SUMMARY

©2015

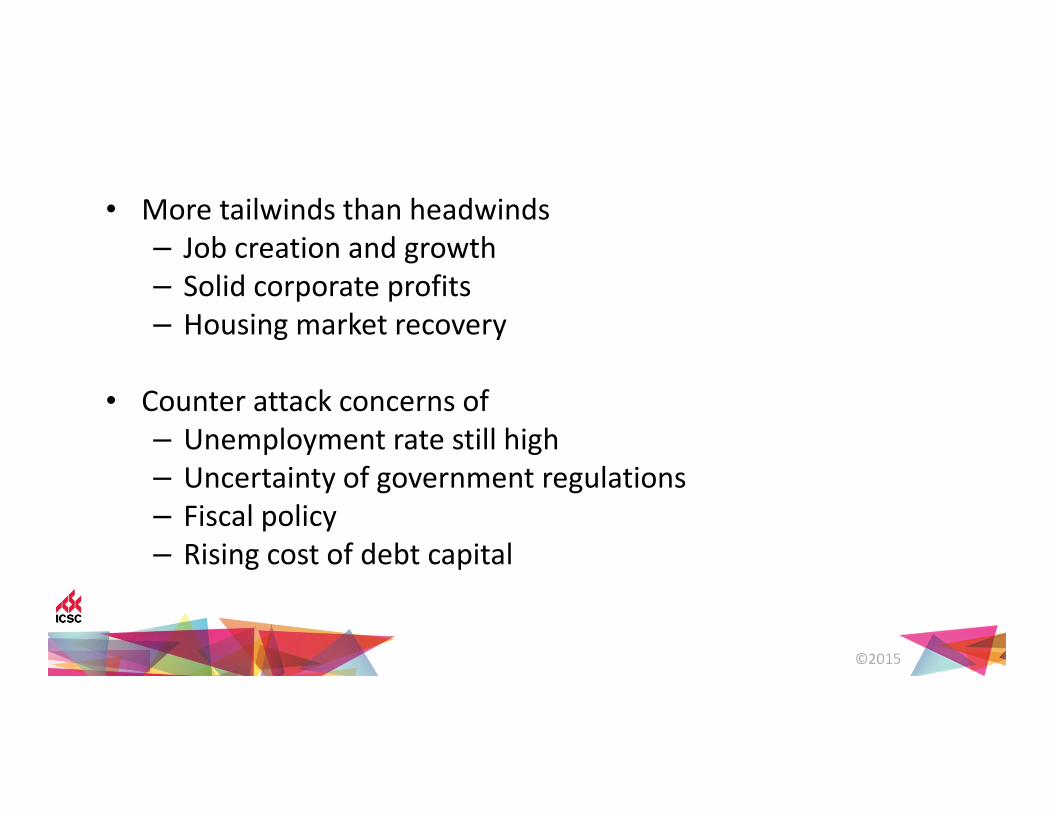

• More tailwinds than headwinds

– Job creation and growth

– Solid corporate profits

– Housing market recovery

• Counter attack concerns of

– Unemployment rate still high

– Uncertainty of government regulations

– Fiscal policy

– Rising cost of debt capital

©2015

• Back to Fundamentals – this transition from cap rate compression to fundamental performance will increase the emphasis on asset management to enhance returns.

• This marks a significant shift from a dependence on cap rate compression for appreciation growth that has become ingrained in investment strategies across all property types.

• Availability of debt and equity capital is on the rise in 2015. Sources of capital all becoming more comfortable with improving market conditions.

• As space is continued to be absorbed with very little new supply, rents will start to push making development proformas begin to make sense.

©2015

• The real estate recovery will gain momentum through 2015.

• Commercial real estate is reaching an inflection point where valuations will no longer be driven by capital markets.

• With cap rate compression beginning to wane, the focus is

more on property fundamentals.

• The search for returns through cap rate compression will become the search for returns through improving property fundamentals and/or operational improvements.

©2015

NEW PRIORITIES IN ASSET MANAGEMENT

©2015

NEW PRIORITIES IN ASSET MANAGEMENT

When we underwrite assets, we look at a lot of property

and market information. There are 3 key pieces that will

have a measurable affect on defining our asset

management strategy:

� Bundle of Rights

� Health Ratio Analysis

� Lease Expiration Schedule

©2015

BUNDLE OF RIGHTS

©2015

BUNDLE OF RIGHTS

• REA’s/CCR’s/Master Plan Communities

• Co-Tenancies

• Kick-Outs-Landlord/Tenant

• Anchor Tenant Zone of Control

• Easements

• Entitlements

©2015

BUNDLE OF RIGHTS (continued)

• Pads

• Zoning

• Go Dark Clauses

• Debt-Lender Approval

• ROFO’s/ROFR’s

©2015

HEALTH RATIO ANALYSIS

©2015

Lease All-In Gross Sales Health

TENANT Sq. Ft % Expiration Rent Sales PSF Ratio

1 TRADER JOHN'S 13,530 13.15% 12/31/19 36.00$ 10,000,000$ 739.10$ 4.87%

2 JERSEY MARK'S 1,609 1.56% 06/30/15 72.00$ 1,750,000$ 1,087.63$ 6.62%

3 WALGOLD'S 12,489 12.14% 10/31/16 39.00$ 4,750,000$ 380.33$ 10.25%

4 PARTY COUNTY 7,500 7.29% 12/31/15 42.00$ 1,250,000$ 166.67$ 25.20%

5 BANK OF VEGAS 4,075 3.96% 03/31/18 42.00$ 2,250,000$ 552.15$ 7.61%

6 LOCAL PIZZA GUY 1,429 1.39% 03/31/18 45.00$ 425,000$ 297.41$ 15.13%

7 SALLY'S SALON 5,490 5.33% 04/30/17 40.00$ 2,000,000$ 364.30$ 10.98%

8 CHRIS'S TACOS 1,623 1.58% 01/31/16 51.00$ 1,200,000$ 739.37$ 6.90%

9 MIKE'S MEAT PIES 1,661 1.61% 04/30/20 60.00$ 500,000$ 301.02$ 19.93%

10 BETTER BUY 35,000 34.01% 07/31/16 30.00$ 6,000,000$ 171.43$ 17.50%

11 SUBURBAN OUTFITTER 15,000 14.58% 09/30/17 35.00$ 8,000,000$ 533.33$ 6.56%

12 VICTOR'S SECRET 3,500 3.40% 03/31/16 45.00$ 1,000,000$ 285.71$ 15.75%

TOTAL 102,906 100.00% 38,125,000$ 370.48$ 8.21%

ROSCOE'S RETAIL EMPORIUM

©2015

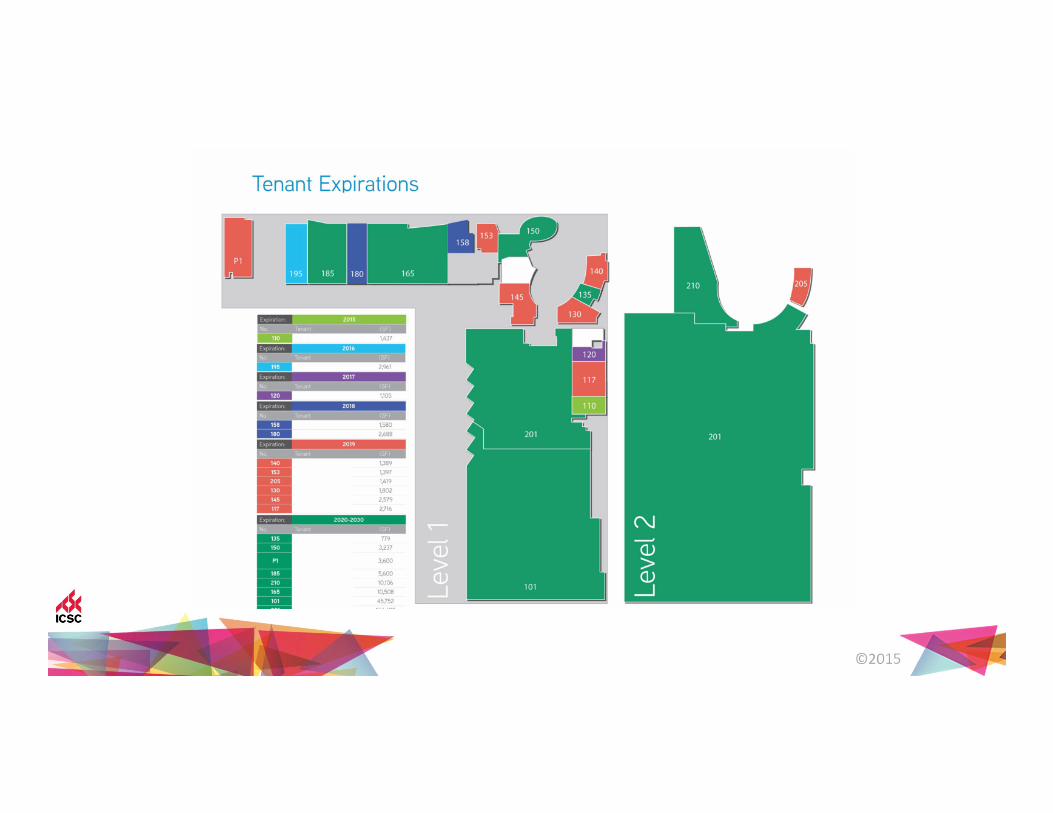

LEASE EXPIRATION SCHEDULE

©2015

0

0.2

0.4

0.6

0.8

1

0 sf

20,000 sf

40,000 sf

60,000 sf

80,000 sf

'15 '16 '17 '18 '19 '20 '21 '22 '23 '24

Annual Area Expiration

Annual Area Expiration Cumulative % Expiration

©2015

0

0.2

0.4

0.6

0.8

1

$-

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

'15 '16 '17 '18 '19 '20 '21 '22 '23 '24

Annual Base Rent Expiration

Annual Base Rent Expiration Cumulative % Expiration

©2015

©2015

VALUE CREATION

©2015

INVESTMENT CYCLE

• Acquire Asset

• Develop strategy to maximize value over a defined “hold period”.

• Hire capable property managers and leasing agents to assist with carrying out this strategy.

• Review and adjust strategy as necessary

– Property conditions

– Market conditions

– Capital Market conditions

• Sell and hopefully meet or exceed your client’s return objectives.

©2015

PROPERTY VALUES IMPACTED BY…

External Sources

• Capital Markets

• Competition

• Changing Demographics

• Public Transportation

©2015

VALUE CREATION DRIVERS

• Tenant Mix

• Redevelopments

• Quantifiable vs Unquantifiable Value

• Additional Value Creation Methods

©2015

IMPORTANCE OF TENANT MIX

Getting it right

� Demographics review

� Balancing act

� Local/Regional/National

� Small Shops/Sub-Anchors/Anchors

� Analyzing health ratios

©2015

IMPORTANCE OF TENANT MIX

Getting it right

� Maximizing sales

� Maximizing rents

� Maximizing value

©2015

REDEVELOPMENTS

Reasons for Redevelopement:

• Secure market position

• Meet consumer demand

• Update project

©2015

COMPONENTS OF A PRO FORMA

• Projected sales impact

• Projected market share changes

• Leasing assumptions

• Impact of new tenants/anchors

• Return on cost analysis – incremental rent versus cost

• Cap rate impact

• Discounted cash flow analysis

©2015

PAD DEVELOPMENT EXAMPLE

Assume the Following:

• Land 16,000 s.f.• Original Cost $ 3.00/s.f.• Market Value $12.00/s.f.• Tenant Restaurant• Term 10 Years• Square Footage 6,000 s.f.• Rent $20.00/s.f.• Percentage 6%• Expenses NNN• TI’s $12.00/s.f.• Leasing Commission $ 4.00/s.f.

©2015

QUANTIFIABLE VALUE-ADD

©2015

ANALYSIS “A” (MARKET RETURN)

This analysis outlines a typical developer construction proforma and is a quick check to a market driven return:

• Soft Costs (10%) $ 62,400

• Hard Costs ($60.00/s.f.) $360,000

• T.I. Contribution ($12.00/s.f.) $ 72,000

• Land (Market Value @ $12.00/s.f.) $192,000

• Construction Financing

• (Land & Building @ 10% for 10 months) $ 52,000

• Leasing commission $4.00/s.f. $ 24,000

• Total Project Costs: $762,400

• Restaurant Rent: $120,000

• Return on cost $120,000 / $762,400 = 15.74%

©2015

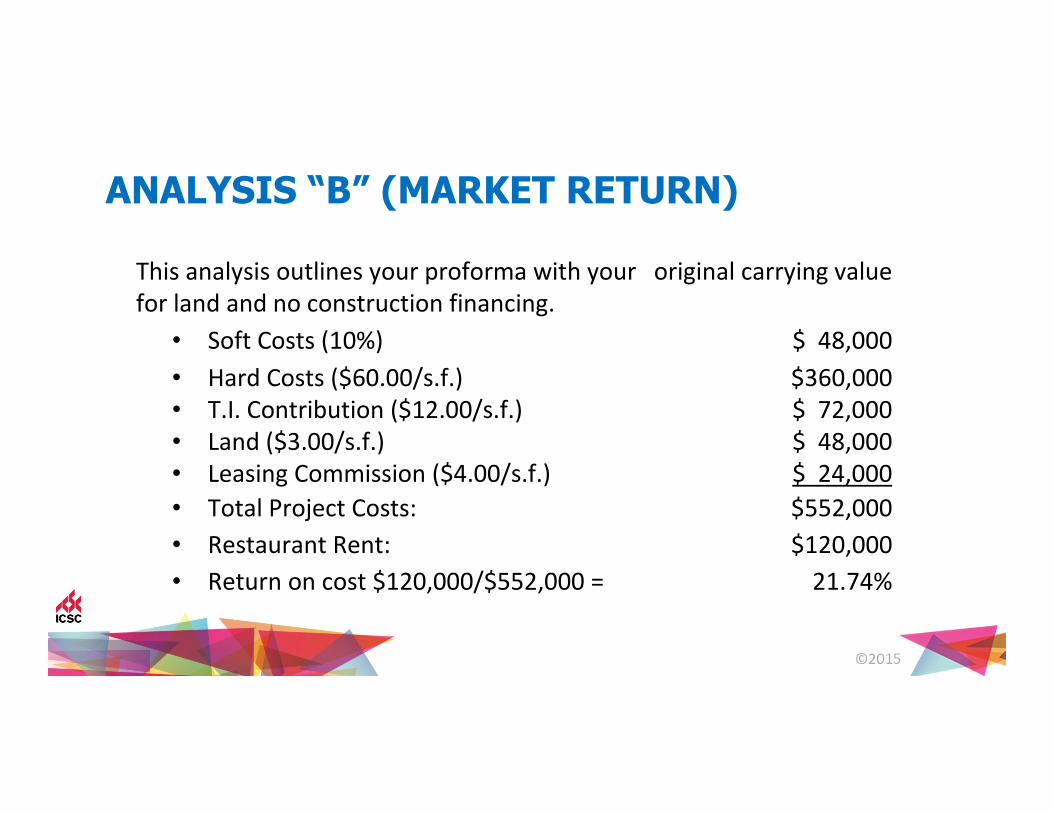

ANALYSIS “B” (MARKET RETURN)

This analysis outlines your proforma with your original carrying value

for land and no construction financing.

• Soft Costs (10%) $ 48,000

• Hard Costs ($60.00/s.f.) $360,000

• T.I. Contribution ($12.00/s.f.) $ 72,000

• Land ($3.00/s.f.) $ 48,000

• Leasing Commission ($4.00/s.f.) $ 24,000

• Total Project Costs: $552,000

• Restaurant Rent: $120,000

• Return on cost $120,000/$552,000 = 21.74%

©2015

UNQUANTIFIABLE VALUE-ADD

©2015

NON-ECONOMIC EXAMPLE

Assume the Following:

• Regional Mall: 1,350,000 square feet

• $18.15/s.f. NNN expenses (CAM, Tax, Ins)

• Annual Sales of $440.00/s.f. (Non-Anchor)

• You have a 4,500 Vacancy:

• Budgeted Rent: $45.00/s.f. NNN

• Budgeted TI: $15.00/s.f.

• Net Effective Rent: $42.60/s.f. NNN

• Proposed Rent: $55.00/s.f. gross

• Proposed TI: $45.00/s.f.

• Net Effective Rent: $31.33/s.f. NNN

©2015

ANALYSIS “A” (NET EFFECTIVE RENT)

Rent/PSF

Free Rent /

Downtime

(Months)

Adjusted

Rent/PSF

Leasing

Commission

TI Allowance &

LL Cost Rent/PSF

Free Rent /

Downtime

(Months)

Adjusted

Rent/PSF

Leasing

Commission

TI Allowance &

LL Cost

Year 1 36.85$ 4 24.57$ 77,112.00$ 202,500.00$ 45.00$ 3 33.75$ 94,162.50$ 67,500.00$

Year 2 36.85$ - 36.85$ 45.00$ - 45.00$

Year 3 36.85$ - 36.85$ 45.00$ - 45.00$

Year 4 36.85$ - 36.85$ 45.00$ - 45.00$

Year 5 36.85$ - 36.85$ 45.00$ - 45.00$

Year 6 40.54$ - 40.54$ 49.50$ - 49.50$

Year 7 40.54$ - 40.54$ 49.50$ - 49.50$

Year 8 40.54$ - 40.54$ 49.50$ - 49.50$

Year 9 40.54$ - 40.54$ 49.50$ - 49.50$

Year 10 40.54$ - 40.54$ 49.50$ - 49.50$

37.47$ 46.13$

31.25$ 42.53$

(169,062.00)$ 1,406,388.00$

(9,787.50)$ 1,913,962.50$

(159,274.50)$ (507,574.50)$

Proposed Deal Budgeted Deal

Average Rent Average Rent

Effective Rent Effective Rent

Proposed Year 1 Revenue

Budgeted Year 1 Revenue

Variance

Proposed Total Revenue

Forecasted Total Revenue

Variance

©2015

VALUE BENEFIT

• Net effective rent decreased by: $11.28

• Year 1 income decreased by: $159,275

• Total income decreased by: $507,575

Where is the value?

• Gross sales prior = $440.00/s.f.

• Gross sales 4 years after = $600.00/s.f.

Increase of $160/s.f. in gross sales in 4 years!

Over $100M additional spent at your center!

©2015

ADDITIONAL VALUE CREATION METHODS

• Land Assemblage

• Marketing/Events

• Security and Cleanliness

©2015

HOLD/SELL DISCUSSION

� Comment on short-term, medium-term, and long-term

hold strategies.

� Supplement short-term, medium-term, and long-term

hold strategies with a financial analysis (discounted cash

flow).

� Review major events with respect to the property and

market within the short-term, medium-term, and long-

term strategies.

©2015

Opportunities• Outlet centers

• A malls –capital partner with operator

• Mixed use

• Urban in-fill city center opportunities

• Suburban in-fill city center opportunities

• High street

• Dominant traditional grocery anchored neighborhood/community centers

• Redevelopment opportunities

• Newer power centers that are right sized

• Ethnic market opportunities

©2015

� Menswear

� Fast Fashion

� E-Commerce/On-Line/Internet…Electronic Sales

� Big Food

� Square Footage Formats

� Lack of Development Supply

� Traditional Grocery Stores

� “Made in the USA”

� Activewear apparel

� Outlets/Factory Stores

� Non-Traditional Uses

� Urban Retail

A few thoughts on trends going forward…

©2015

COMPLETE YOUR SHOW EXPERIENCEMORE THAN 30 SESSIONS CAPTURED LIVE DURING RECON!

• Recording Package $150 usd

• Extend Your Own Education

• Share Sessions with Colleagues

• Compatible with Mobile Devices

icsc.sclivelearningcenter.com

©2015

Course Evaluation

Please Complete Your Evaluation Now.

1. Take Out Your Smartphone or Tablet

2. Go to survey.icsc.org/2015RECON

3. Select this course: New Priorities in Asset Management