new players new models march 2019 pb - oxfordenergy.org · • the equity/cost model seeks to move...

TRANSCRIPT

NewPlayers,NewModelsAresearchthinkpiece

March2019

NATURALGASPROGRAMME

2DAVIDLEDESMA&MIKEFULWOOD NATURALGASPROGRAMME

AuthorsDavidLedesma,SeniorResearchFellowMikeFulwood,SeniorResearchFellow

Note:• Thecontentsofthispaperaretheauthorssoleresponsibility.Theydonotnecessarily

representtheviewsoftheOxfordInstituteforEnergyStudiesoranyofitsmembers• Sourcesaredetailedinthelastslidewithnumberreferencesintheslides

3DAVIDLEDESMA&MIKEFULWOOD NATURALGASPROGRAMME

MARKETCHANGE

Firm long-term supply contracts were needed to underpin LNG supply security

Low cost US shale growth and subsequent development of US liquefaction capacity gave an alternative supply and contract choice

Middle East LNG supply growth globalised the LNG business

2011 Fukushima disaster and subsequent Japanese fiscal deficits drove the need for market change

Market driven change led to new ways of contracting • China and SE Asia

market growth • Price & volume

sensitive market growth

• Liberalisation of the Japanese market

The‘oldmodel’haschangedThechangeshaveledtoincreaseduncertaintyandtheneedforgreater

contractualflexibility

4DAVIDLEDESMA&MIKEFULWOOD

• TheLNGbusinesshasevolvedfromitsoriginalsecurityofsupplybased‘EstablishedModel’thatwasbasedonfixedlinksbetweentheLNGsupplierandtheLNGbuyer

• NewplayersandchangesinthestructureoftheLNGmarkethavedriventheLNGvaluechainmodeltoonewherenewandexistingplayerscanintroduceanadaptiveLNGchainwheredifferentlinkagescanoperatemoreindependentlyofeachother

• Thishasbeenmadepossiblebythepresenceofhighcredit(AAAorAA)intermediariesunderpinningofftakeagreements

– SeenmostrecentlyintheUSmodelandFLNGstructures• Willtheseaggregators/portfoliocompanies/intermediarieshavethefinancialand

commercialcapacitytounderpinthenextwaveofLNGliquefactioncapacity?• Inresponsetothisuncertaintynewplayersarecreatingnewmodels.Thequestionis

–willthesemodelswork?

Hypothesis

NATURALGASPROGRAMME

5DAVIDLEDESMA&MIKEFULWOOD

Thepathtoatrulytraded/merchantmodelfromtheestablishedliquefactionmodelhasseveralsteps

NATURALGASPROGRAMME

EstablishedModel

Market Change

CheniereModel

Equity/CostModel

Trading/MerchantModel

6DAVIDLEDESMA&MIKEFULWOOD

Thepathtoatrulytraded/merchantfromtheestablishedliquefactionmodelhasseveralsteps

NATURALGASPROGRAMME

• FourModels• The‘EstablishedModel’usedintheliquefactionplantdevelopmentsofthe1980-1990swas

basedaroundfixedlinkageswithintheLNGchain.Themovetotollingagreementsinthe2000s*gavethefirststepstowardscargooptimisationandtrading

• TheinnovationoftheChenieretollingmodeltotheUSmarket,basedonlowcostofUSfeedgas,sawUShubpricedLNGwithgreateroperationalflexibilityofLNGcargoes,butthestructureisstillbasedaroundlong-termcontracts

• Theequity/costmodelseekstomovefurthertowardsamerchantmodel,butstillrequireslargeequityinvestmentstobemade,whichinthemselvesmeanonlylargecompanieswithlargeportfoliosareabletobeinvolved.Thisstructurealsorequiresmediumtolongtermcontractstounderpinthelargeinvestments

• InatrulytradedmarkettheabilityofthemarkettoactasahomeforLNGcargoes,atthemarketprice,meansthatthechaincanfullydisaggregate,contractscanbeflexible,andnewliquefactionplantscanbefinancedwithoutanyvolumerisk.Allfinanceisbasedonmarketbasedprices

• Thispapercomparesthedifferentmodelsonthewaytothisfullytradedmarketandchallengeshow,intheintermediateperiodbeforewereachthismarket,newliquefactioncapacitycanbedeveloped

* Indonesia did use tolling structures before this but still based around the fixed point-point LNG supply structure

7DAVIDLEDESMA&MIKEFULWOOD

The‘EstablishedModel’hadacleardelineationofactivities

Transfer pricing project structure Integrated project structure

NATURALGASPROGRAMME

Source: OIES, ’LNG Markets in Transition, The Great Reconfiguration’5, Chapter 3, Ledesma

8DAVIDLEDESMA&MIKEFULWOOD

The‘EstablishedModel’hadacleardelineationofactivitiesthatsupportedinvestmentbutlimitedflexibility

NATURALGASPROGRAMME

• Theestablishedmodelusedintegratedandtransferpricingstructures(withafewusingthetollingstructure).Longtermsupplycontractsbetweensellersandbuyersunderpinnedthedevelopmentofcapitalintensiveupstreamgasreservesandliquefactionplants

• ProjectstructuringusuallyincludedafewcompaniesinvolvedfromwellheadtoLNGdeliveryattheLNGbuyersfacility

• Projectswereonshore,largescale,withincreasinglybiggerLNGtrains• Buyerswereoftenend-userutilitiesorgascompanieswhosoldgasintoregulated

marketswheretheenergycostswerepassedthroughtotheendbuyer• LNGsalesweremainlymadeonadeliveryex-ship(DES)basis• Limitedcontractflexibilitywithlimited,ifany,cargodiversions• LNGwaspricedonanoilrelatedbasis,basedontheJapanCrudeCocktail(JCC)oilprice.

Theformulawasfairlystandard:JCCx14.85(theslope,where17.1representoil/gasparity)plusaconstantusuallyrepresentingtheshippingcost

• Projectsstructuredwithjointventurecompaniesassellersusinglimited/nonrecourseprojectfinancingthatallocatedrisktomaximisefinancingandoftenoptimizethefinancecapacityofthegassupplyingcountry

9DAVIDLEDESMA&MIKEFULWOOD

The‘CheniereModel’tookthetollingmodelandadapteditfortheNorthAmericangasmarket

Cheniere’s modified transfer pricing structure The established tolling structure

NATURALGASPROGRAMME

Source: OIES, ‘LNG Markets in Transition, The Great Reconfiguration’5, Chapter 3, Ledesma

10DAVIDLEDESMA&MIKEFULWOOD NATURALGASPROGRAMME

• TheestablishedtollingmodelallowedforthesamecompanytooperateintheupstreamandLNGsalespartsofthechainwithathirdpartyowningandoperatingtheliquefactionplant

• Longtermtollingcontractssecureddedicatedgasreservesfromupstreamcompaniestousetheliquefactionplantcapacity

• Thesecontracts,withhighcreditratedcompanies,underpinnedtheplantfinancing

• LNGwassoldbytheupstreamcompanies,thattolledthroughtheliquefactionplant,notthejointventurecompany.InEgypt,thisenabledthedevelopmentof’BrandedLNG’whereLNGissoldinthenameofthesellercompany

• BuyerswouldbuyLNGfromtheupstreamcompanies.LargeIOCsorcompanieswithmultiplesupplycontractscouldofferLNGfromtheirportfolioratherthanaspecificsupplysource.ThiswasthestartofaggregatorLNGandrealcargodiversions

• LNGsalescouldbeonvaryingcontractsandunderdifferentpricingmechanisms• LNGwassourcedFOBforcargoflexibility.

• The‘CheniereModel’adaptedthetollingmodelfurthertosourcefeedgasfromthelargelowcostUSgasmarket(notdedicatedreserves),selltollingcapacitywithfeedgassupplyandpipelinesupplycapacityatcost,separatedfromthetolling.

• Theunbundledmodelremoveddestinationrestrictionsandgavevolumeflexibility

The‘CheniereModel’tookthetollingmodelandadapteditfortheNorthAmericangasmarket

11DAVIDLEDESMA&MIKEFULWOOD

The‘Equity/Cost’modelseekstosecureequityinvestorstofundnewliquefactionandsupplyequityLNG

NATURALGASPROGRAMME

Investor1

Investor2

Investor1

Investor1

Investor2

Investor1

Projectdevelopmentcompany(investmentinLNGchain/liquefaction)

CorporateLenders

Equity ownership

Equity LNG offtake

ProjectFinanceLenders

Alternatively equity holders may decide to finance at a project level on non-recourse basis

Equity holders may finance through corporate financing – debt or equity

12DAVIDLEDESMA&MIKEFULWOOD NATURALGASPROGRAMME

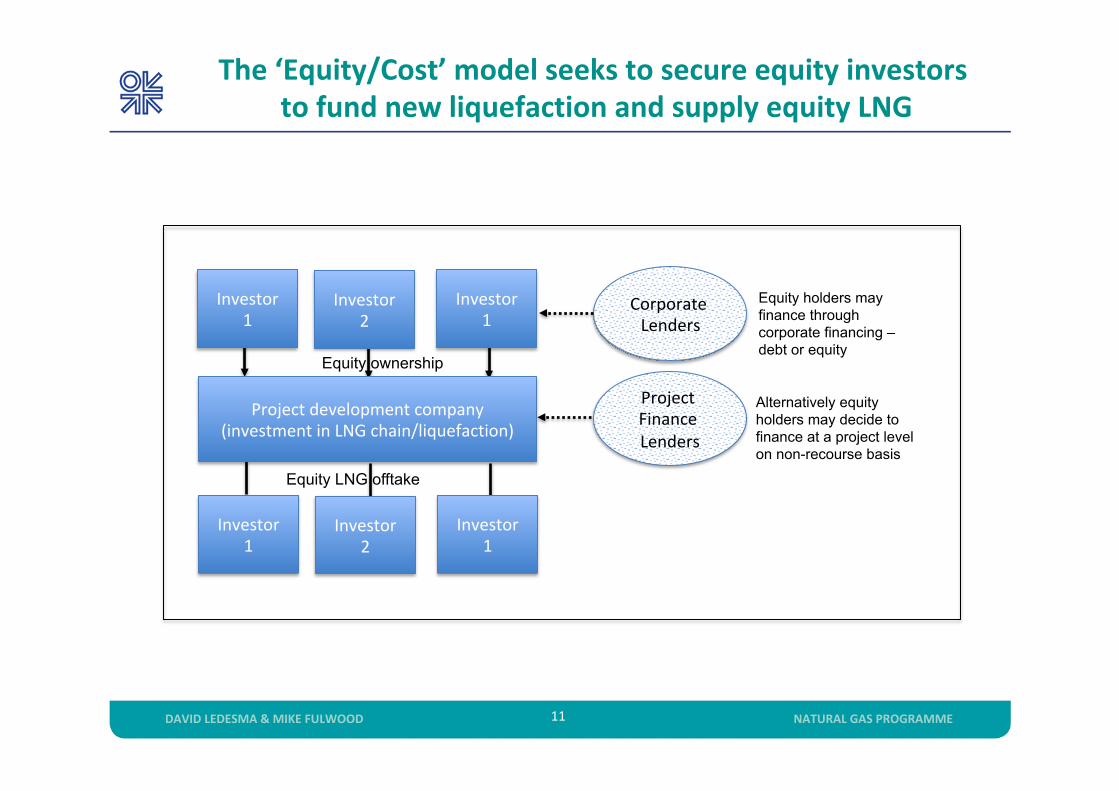

• Projectcompanyshareholdersfundtheliquefactionplant(andpotentiallytheupstream)throughtheirownequity.LNGofftakeisbasedonequityshares-allLNGisdestinationfreeandcompletelyflexible

– Equityholdersareresponsibleforsourcingtheirowngasandsecuringpipelinecapacitytomovegastotheliquefactionplant

– TheinvestorreceivesequityLNGatshiploadingflangeoftheliquefactionplantatcost• ProjectequityholderstaketheLNGintotheirownportfoliosandmanagethe

marketingrisk– LNGmaybesoldfromtheprojectcompanytotheequityholdersownLNGmarketing

company– LNGon-soldundercontractsofvaryinglengthsanddifferentcontractpricesandterms

• LNGCanadatookFIDwiththisprojectstructureinOctober2018• Tellurian’sDriftwoodLNGprojecthasadaptedthismodelfurthertoofferequityin

theproject(whileprojectfinancingisaround66%).LNGbuyersbuyequityandreceiveLNGinproportionofthatequityamount

– Theprojectismanagedandoperatedbyaprovendeveloperandoperator.Anycost-overrunswillbebornbytheequityholders.Projectfinancecompanieswilllikelyneedsecurityofofftakeandsomeformofconstructioncompletionguarantees

The‘Equity/Cost’modelseekstosecureequityinvestorstofundnewliquefactionandsupplyequityLNG

13DAVIDLEDESMA&MIKEFULWOOD

Theendgame‘Trading/Merchant’modelwillnegatetheneedforlong-termcontractsandenablefullmarketflexibility

Globally traded LNG market

NATURALGASPROGRAMME

PLUS MULTIPLE RESALES

LiquidMarket

AvailableLNG

Vessels

Seller

Buyer

14DAVIDLEDESMA&MIKEFULWOOD NATURALGASPROGRAMME

• AtrulymerchantmarketwillmeanmultipleLNGsellers,buyers,tradersandindependentscanfreelytradeLNGonthebasisofglobalorregionalLNGpriceindiceswith‘basisdifferentials’betweentheseindicesequaltosupply/demandLNG

– Tradeoncommoncontracts– BuyersareconfidentthattherewillalwaysbeLNGcargoesavailabletomeettheirdemand

thusensuringsecurityofLNGsupply– Volumeriskhasdisappearedandriskhastotallybeentransferredtotheprice(i.e.takeor

payis100%asthebuyerknowsthatitcanalwaysplacethecargoonthemarket)

• AllLNGisflexible,nolong-termcontracts(thoughsomebuyersmaysecure1-5yearsforeaseofoperations).Volumeofftakeriskisremovedbymarketliquidity

• Lendersarehappytolend,andinvestorstoinvest,onthebasisoftheeconomicsofaprojectandtheLNGpricelevel,notvolumerisk(long-termcontractsmaynotberequiredtounderpintheirinvestments)

• EquityinvestorswillseektomaximizeleverageandeachsegmentoftheLNGchaincanbefinancedindependently

Theendgame‘Trading/Merchant’modelwillnegatetheneedforlong-termcontractsandenablefullmarketflexibility

15DAVIDLEDESMA&MIKEFULWOOD

ButtheLNGmarketisintransitionbetweenastructuredandfullyflexible/liquidstructure.Operatinginthegreytransitionperiod

betweentheseendstatescreatesuncertainty

NATURALGASPROGRAMME

1970-1990structuredLNGmarket

Merchant/tradedmarket

(expectedtobe43-50%by2020)3

Movingto

Greyfuzzyareaoftransition

Question:Whenisthe‘tipping

point’

Source:Authorresearch

In2018~32%LNGtradedwasin‘pure’spottrades(in2015itwas15%)4

16DAVIDLEDESMA&MIKEFULWOOD

• Whenthemarketisfullymerchantandliquid,thenLNGcanbetradedundershort-term/spotcontractsconfidentthatthereisamarketthatcannotbemanipulated.Lenderscanlendmoneywithouttherequirementforlong-termofftake/capacityagreementswithoutimpactingongearinglevels

• ThepathtowardsafullytradedLNGmarketisunstoppable,thequestioniswhenwillthe‘TippingPoint’be(i.e.whenacargocanbedeliveredintomultipleliquidtradingmarketswithoutlimit)

• IncreasedvolumesofLNGareavailablewithoutcontractualdestinationrestrictions• ThevolumeofPureSpotTradesincreasedto32%LNGin20184• By2020,70cargoes/monthwillbesuppliedfromtheUSwith24differentlifterscreating

realFOB

• ThevolumeofLNGtradedbyaggregatorsandtradersisincreasing• IncreasingvolumesofLNGarebeingsoldfromtermbuyersandsellersusingtheLNG

spot/short-termmarkettocoverdisposalandsourcingofshort-termvolumes• End-userbuyersaresourcingLNGthroughaportfoliooflong,medium,short-term

andspotcargoestomanagegasofftakerisksandpriceexposure

Asthemarketchangestowardsafullyliquidbusiness,thewaythatLNGistradedischanging

NATURALGASPROGRAMME

17DAVIDLEDESMA&MIKEFULWOOD

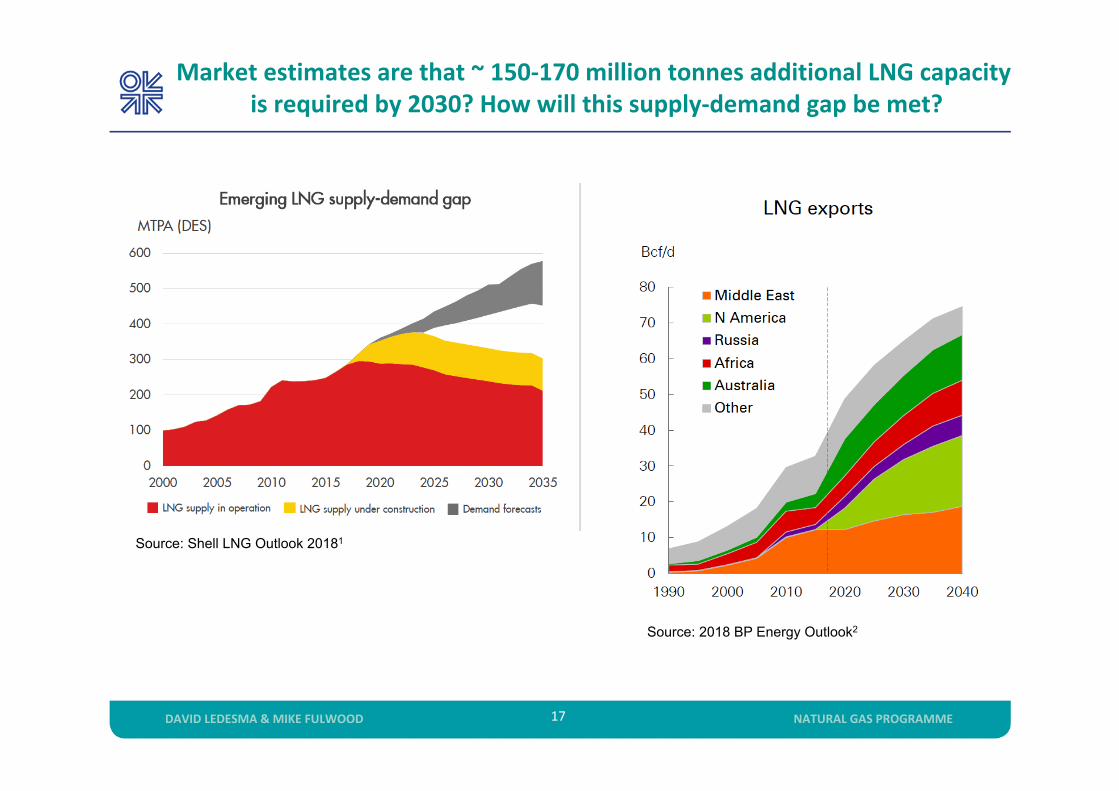

Marketestimatesarethat~150-170milliontonnesadditionalLNGcapacityisrequiredby2030?Howwillthissupply-demandgapbemet?

NATURALGASPROGRAMME

Source: 2018 BP Energy Outlook2

Source: Shell LNG Outlook 20181

18DAVIDLEDESMA&MIKEFULWOOD

• Anadditional150-170mtpaLNGcapacityisrequiredby2030whichmeansthatanestimated$150bninvestmentisneededbetween2019-2025inliquefaction,associatedfacilitiesandships*.(assumingacostof$600/MT+associatedinfrastructurecostsandships).Over6yearsthisequatesto$25billion/year

• Inordertosecurefinancing,andsupportthislevelofinvestment,projectdeveloperswillneedtosecureofftakeagreementstounderpintheinvestments

~150milliontonnesadditionalLNGcapacityisrequiredby2030?Whatisthecapitalcost?WhatisthevalueoftherequiredLNGinvestment?

CompanieswillbeexpectedtounderpinthisinvestmentandLNGofftake

NATURALGASPROGRAMME

* 150 million mt @ 52 Tr Btu/million mt LNG = 7800 Tr Btu @ $6/MMBtu = Cost LNG of $46.8 billion/annum

• AssuminganLNGpriceof$6/MMBtu,thiscontractualcommitmentisequivalentto~$46billion/year.AtanLNGpriceof$8/MMBtuthisrisesto$62billion/year*

• $108bninvestmentinliquefactionandassociatedfacilitiesequatesto$18billion/year

• Assuminggearingof67%then~$12bn.debtrequiredeachyear

Estimatedcapitalinvestmentrequired150 millionmtnewcapacityrequired

Cost:600 Capex$/MT newcapacity90 $billion Totalinvestmentinliquefaction18 20% associatedcostsforinfrastructure108 $billion Totalshorecosts(excludingupstream)

214 Nonewships [email protected] $billion @$200million/ship

151 $billion TOTALnewinvestmentrequired

NOTE:Theamountonevesselcancarry/year:cargo:62000mt,30daysroundtrip=11.7voyages/year(@350days)=0.723millionmt

19DAVIDLEDESMA&MIKEFULWOOD

0

5

10

15

20

25

30

35

20042005200620072008200920102011201220132014201520162017

US$billion

Thirdpartydebtraisedforliquefactionplantfinancings2004-2017

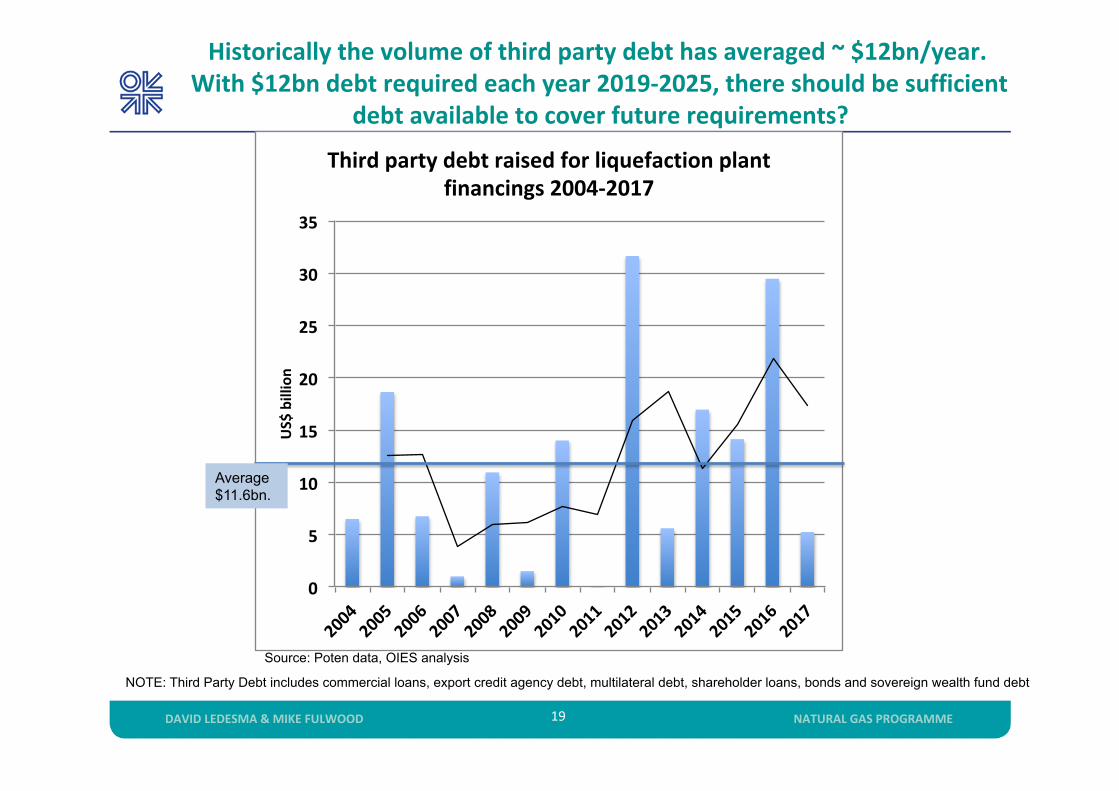

Historicallythevolumeofthirdpartydebthasaveraged~$12bn/year.With$12bndebtrequiredeachyear2019-2025,thereshouldbesufficient

debtavailabletocoverfuturerequirements?

NATURALGASPROGRAMME

Source: Poten data, OIES analysis

Average $11.6bn.

NOTE: Third Party Debt includes commercial loans, export credit agency debt, multilateral debt, shareholder loans, bonds and sovereign wealth fund debt

20DAVIDLEDESMA&MIKEFULWOOD

Bankssaythattheyareflexibletochangingcontractualstructuresbutarethey?• Lendersseeklong-termstablerevenueflow.Projectfinancetodatehasreliedonlong-

termtakeorpaycontractsfromA+buyers(oftenwithgovernmentsupport)– Withoutasuitablefinancingpackagetherewillberecoursetoshareholdersandthislimits

thenumberandfinancialqualityofcompanieswhichcandevelopprojects– ImmaturityofthespotLNGmarketstillmeansthatlong-termcommitmentsareneeded–thoughbankssaythatperiodof‘long-term’hasreduced

• Ittendstobethesmallerplayerswhoareofferingcontractualflexibilitytosmaller,lowercreditratedbuyers.Lendersseethisasincreasingprojectrevenueuncertainties

• Aggregatorscanbundlebuyersofdifferentcreditratings– Riskslicingbuyersofdifferentcreditratingscanoptimisefinancinglevels– Aggregatorscanalsooffertodevelopdomesticinfrastructure

• Lendersmustgetcomfortablewiththeriskstooptimisedebtpackagesandthatspot&short-termcargoescanbesoldata‘marketlevel’but...theyneedaliquidmarket

• Accesstonewcapitalsourcesisonlypossibleifrisksareclearlydefined– Shorter-termcontractsareOKinmatureeconomiesthathavealiquiddebtmarket– Newsourcesoffundsstillneedclearriskallocation– Equityinvestmentisthemostexpensivesourceoffunds

ThefinancingcommitmentforthenextwaveofLNGcouldbe$150bn.Istheresufficientfinancingcapacityavailabletosupportsuchalarge

investmentrequirement?

NATURALGASPROGRAMME

21DAVIDLEDESMA&MIKEFULWOOD

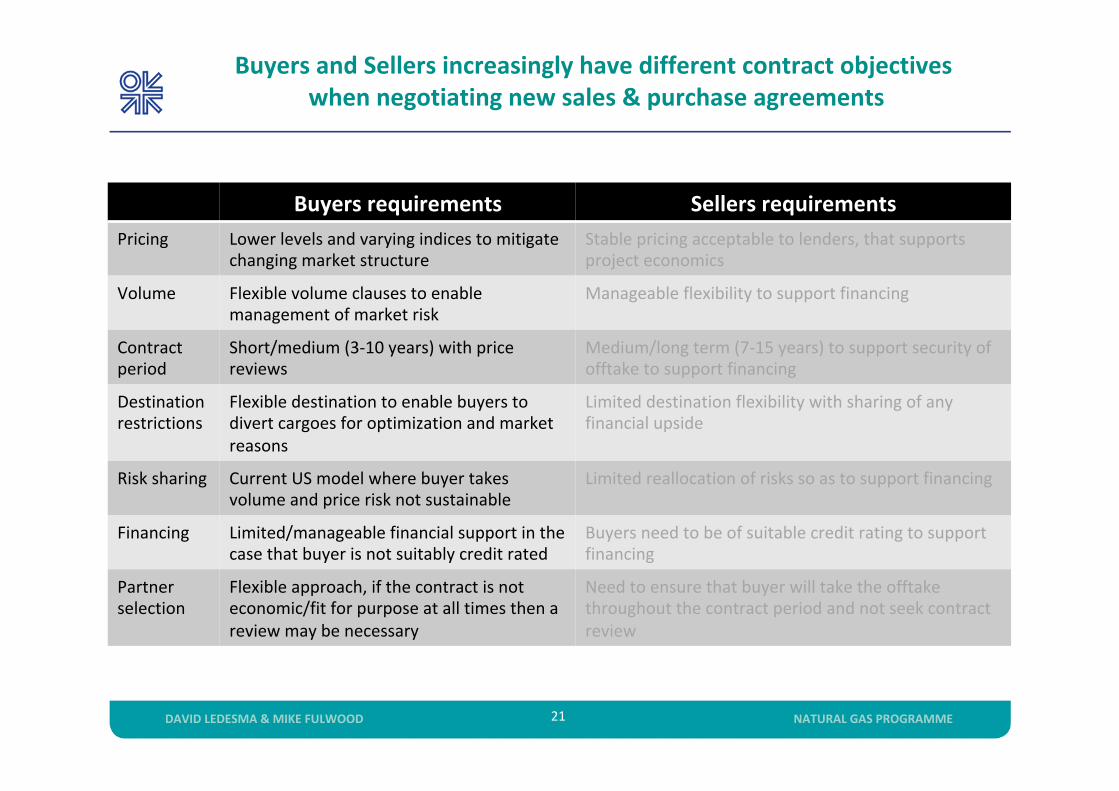

BuyersandSellersincreasinglyhavedifferentcontractobjectiveswhennegotiatingnewsales&purchaseagreements

NATURALGASPROGRAMME

Buyersrequirements SellersrequirementsPricing Lowerlevelsandvaryingindicestomitigate

changingmarketstructureStablepricingacceptabletolenders,thatsupportsprojecteconomics

Volume Flexiblevolumeclausestoenablemanagementofmarketrisk

Manageableflexibilitytosupportfinancing

Contractperiod

Short/medium(3-10years)withpricereviews

Medium/longterm(7-15years)tosupportsecurityofofftaketosupportfinancing

Destinationrestrictions

Flexibledestinationtoenablebuyerstodivertcargoesforoptimizationandmarketreasons

Limiteddestinationflexibilitywithsharingofanyfinancialupside

Risksharing CurrentUSmodelwherebuyertakesvolumeandpricerisknotsustainable

Limitedreallocationofriskssoastosupportfinancing

Financing Limited/manageablefinancialsupportinthecasethatbuyerisnotsuitablycreditrated

Buyersneedtobeofsuitablecreditratingtosupportfinancing

Partnerselection

Flexibleapproach,ifthecontractisnoteconomic/fitforpurposeatalltimesthenareviewmaybenecessary

Needtoensurethatbuyerwilltaketheofftakethroughoutthecontractperiodandnotseekcontractreview

22DAVIDLEDESMA&MIKEFULWOOD

ButthereisanimpassebetweenLNGbuyersandsellers.Buyersareseekinggreatercontractualflexibilityinordertomeettheirdomestic

gasdemanduncertainties

NATURALGASPROGRAMME

• Price-buyersarelookingfordifferentpricingindicestomitigatetheirrisks– ReportsthatsomesmallerbuyersarelookingtobuyLNGusingaformulalinkedtofertiliser

prices,steelpricesandfocusingonshort-termrequirementsratherthanlong-termmarketswhicharesouncertain(itisviewedthatsellersareunlikelytoagreetothis)

• Volume-marketliberalisationandtheneedtobecompetitiveintheirchangingmarketshasledtodomesticgasdemanduncertaintyandLNGbuyersseekingsmallercontractamounts,greatervolumetolerances,shortercontractperiodsandcargodestinationfreedomsotheycandivertcargoesincasetheyarenotrequiredintheirhomemarket

• Thethreatofpricedisputes/arbitrationmeansthatsellersfeelatriskthattheircontractsmaybechallengedinthefuturedespitecontractualprovisions.Thisremovesthetraditional‘markettrust’andcommoditizestheLNGmarket.

• TheUSmodelthathasbeenusedforLNGexportprojectstodatepassespriceandvolumerisktothebuyer–thismodelisnotsustainableforthenextroundofLNGFIDsasbuyersarebeingaskedtotakeontoomuchrisk

• Thisleadstothequestion-whatarethepossibleevolutionarypathsforLNGpricingandcontractsthatcanmatchtherequirementsofbothLNGbuyersandsellers?

Source: Input from Heren 30/3/17

23DAVIDLEDESMA&MIKEFULWOOD

BuyersandSellersincreasinglyhavedifferentcontractobjectiveswhennegotiatingnewsales&purchaseagreements

NATURALGASPROGRAMME

Buyersrequirements SellersrequirementsPricing Lowerlevelsandvaryingindicestomitigate

changingmarketstructureStablepricingacceptabletolenders,thatsupportsprojecteconomics

Volume Flexiblevolumeclausestoenablemanagementofmarketrisk

Manageableflexibilitytosupportfinancing

Contractperiod

Short/medium(3-10years)withpricereviews

Medium/longterm(7-15years)tosupportsecurityofofftaketosupportfinancing

Destinationrestrictions

Flexibledestinationtoenablebuyerstodivertcargoesforoptimizationandmarketreasons

Limiteddestinationflexibilitywithsharingofanyfinancialupside

Risksharing CurrentUSmodelwherebuyertakesvolumeandpricerisknotsustainable

Limitedreallocationofriskssoastosupportfinancing

Financing Limited/manageablefinancialsupportinthecasethatbuyerisnotsuitablycreditrated

Buyersneedtobeofsuitablecreditratingtosupportfinancing

Partnerselection

Flexibleapproach,ifthecontractisnoteconomic/fitforpurposeatalltimesthenareviewmaybenecessary

Needtoensurethatbuyerwilltaketheofftakethroughoutthecontractperiodandnotseekcontractreview

24DAVIDLEDESMA&MIKEFULWOOD

• LNGliquefactionprojectcostsarefallingbuteconomicsdictatethattheymayneedtofallfurtherinordertosupportthelowpricelevelsthatbuyersseek

• Thisiscompoundedbythelowmarketgaspricesandbuyerpriceformulaaspirationsthattogetherchallengeoverallprojecteconomics

• Buyer’swishforshort-termofftakeorcapacitycontractsgivesconcernstolendersandsponsorsthatrevenuesmaynotbeashighasrequiredtosupporttherequiredeconomics.ThisriskisexacerbatedastheLNGmarketisnotfullyliquid

• ThenewermarketsthatareunderpinningLNGdemandgrowthoftenhaveapoorcreditrating.ThischallengesthevalueandreliabilityofLNGsalesrevenuesthatarerequiredtounderpinfinancing

• Projectsrequirelargeupfrontinfrastructurerequirements,thequestionis–whopays?Theeconomicsofnewgreenfieldprojectsmaynotsupportsuchlargeexpenditureandsomegovernmentsarenotabletopayorgivethenecessarytaxincentivestosupporttheinvestment

• SellersandlendershaveconcernsthatiftheycommittosellLNGlong-termandthemarketmovestobemoremerchant/traded,thebuyermayseekareviewoutsidethetermsofthecontractbecausethey‘have’to.Partnerandbuyerselectionisbecomingevenmorekey

ButthereisanimpassebetweenLNGbuyersandsellers.Sellersneedsecurityofofftake/revenuesthatarefoundinastructuredmarketbut

arenotinamarketintransition

NATURALGASPROGRAMME

25DAVIDLEDESMA&MIKEFULWOOD

Economiclowcostproject

Lowtechnical&operating

risk

Guaranteedcreditworthy

offtake

Acceptablefinance

structure&terms

• Costiskey• Newmarketsneedlowerprices

• Reductionsincapitalcostsrequired• Projectneedstostart-upontime• Reliableoperations

• Priortomarketreachingits‘tippingpoint’buyertakeorpayrequired

• Lowcostprojectsgivesomestructuringflexibility

ThechallengefacingtheindustryissecuringFIDsforadditionalLNGcapacity.Whatfactorsareneededtoenablecommitmentstobemade?

• Suitablesecuritypackageisrequiredtosupportfinancing• Lendersneedtogivegreaterflexibilityasthemarketchanges• Newfinancestructuresneedtofitnewmarketrealities

26DAVIDLEDESMA&MIKEFULWOOD

• Aneconomic,lowcostLNGsupplyproject– Costiskey,lowcostfeedgas,liquefaction,shippingandliquidscreditifpossible– Tollingfeesarecomingunderpressure,the‘olddays’of$3-3.50/MMBtuforUSLNGprojects

havegone,$2-2.25/MMBtutollingfeesarewhatnewcapacityofftakersareseeking– LNGmustbeabletobedeliveredtoAsiafor~$6/MMBtuifnewmarketsaretobeopened8

– Equityinvestmentmodelsreducetherequirementtoraiseprojectdebt

• Lowtechnicalandoperationalrisk– Tomitigateprojectconstruction,infrastructureconstructionandfinancingrisk

• ReliableLNGofftakeorcapacitycommitmentfromacreditworthybuyer– Needtomanagethematuringofthemarketasitgoesthroughthedifferentdevelopment

stepsfromilliquidtowhenitreachesits‘tippingpoint’(refslide16)andissufficientlyliquid– Suitablecontractstosupportfinancing,butthefinanciersneedtoincreaseflexibility– ThelinkingoflowcostLNGmeansalternativepricingformulascanbeoffered

• Lenderswhofinanceataneconomiccostunderacceptableterms–stillrequired– Onlylendmoneyifthesecuritypackagesupportsthelevelofdebt– WithgreaterflexibilityofLNGcontracts,lenderswillhavetoadapttheirdebtpackagesto

acceptanincreasedamountofrisk(seeback-upslide)– Developfinancingpackagesthatbalancethedifferentrisksofdifferentofftakers

NATURALGASPROGRAMME

ThechallengefacingtheindustryissecuringFIDsforadditionalLNGcapacity.Whatfactorsareneededtoenablecommitmentstobemade?

27DAVIDLEDESMA&MIKEFULWOOD

Stagestoatraded/merchantmodel–BusinessStructure

NATURALGASPROGRAMME

BusinessStructure EstablishedModel CheniereModel Equity/CostTrading/Merchant

Model

Buyer EnduserutilitiesIntermediarieswith

someendusersVaried Varies

SellerNOCorNOC/IOC

sponsoredjoint

ventures(SPV)

ProjectdeveloperVaried,equitylifting,

'brandedLNG'Varies

FinancingFinancewholechainor

liquefactionportion

Financeofliquefaction

&somemidstream

pipelines

Varied(underpinned

bysomeLTsecurityor

higherequity)

Novolumerisk,

projectsfinanced

basedonmarket

EquityMinimisedas

structuresoftenSPVs

Minimiseddueto

maximumleverage

strategy

Dependsonsponsor

financialpositionbut

likelymax.leverage

Dependsonsponsor

financialpositionbut

likelymax.leverage

Projectscale OnshorelargetrainsBrownfieldand

Greenfield

Brownfield,greenfield,

smallertrainsand

FLNG

Brownfieldand

Greenfield

GaschainInvolvedineverything

uptobuyerflangeLiquefactiononly

Combination/

unbundledLiquefactiononly

ProjectDeveloperIOC/NOCwith

upstreaminterests

Independent

developers,no

upstreaminvestment

Independent

developers,no

upstreaminvestment

Independent

developers,no

upstreaminvestment

Gassupplysource DedicatedgasreservesNodedicatedgas,but

fromthemarket

Nodedicatedgas,but

fromthemarket

Nodedicatedgas,but

fromthemarket

28DAVIDLEDESMA&MIKEFULWOOD

• AstheLNGmarketliberalises,thebusinessstructureschange– Thechaingetsincreasinglyflexible– Gasresourcescanbeflexibleratherthanfromaspecificfield(especiallyinNorth

America)

• Differentcompaniesoperateunderdifferentbusinessstructures– Greaterrangeofbuyerandseller– Differentcompaniesoperatealongthewholedisaggregatedchain

• Projectscalecandeterminecompanyinvestment– Smallerscaleliquefactionopportunitieslowerthebarrierstoentrytosmallerinvestors

• Financingstructuresvary– Separatepartsofthechainarefinancedseparately– Changingstructureofthemarketmeanslenderscanrelyonthemarketforguaranteed

offtakeratherthanspecificbuyers– Disaggregatedmarketenablesinnovativefinancingstructures

NATURALGASPROGRAMME

Stagestoatraded/merchantmodel–BusinessStructure

29DAVIDLEDESMA&MIKEFULWOOD

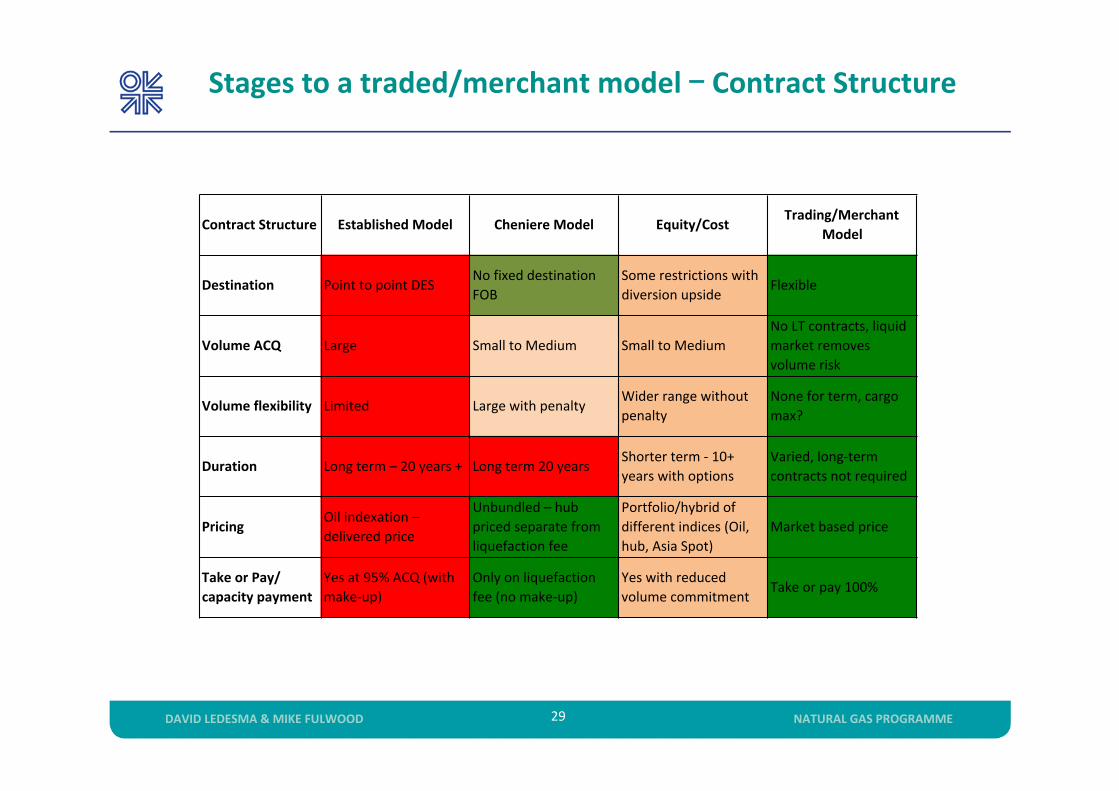

Stagestoatraded/merchantmodel–ContractStructure

NATURALGASPROGRAMME

ContractStructure EstablishedModel CheniereModel Equity/CostTrading/Merchant

Model

Destination PointtopointDESNofixeddestination

FOB

Somerestrictionswith

diversionupsideFlexible

VolumeACQ Large SmalltoMedium SmalltoMedium

NoLTcontracts,liquid

marketremoves

volumerisk

Volumeflexibility Limited LargewithpenaltyWiderrangewithout

penalty

Noneforterm,cargo

max?

Duration Longterm–20years+ Longterm20yearsShorterterm-10+

yearswithoptions

Varied,long-term

contractsnotrequired

PricingOilindexation–

deliveredprice

Unbundled–hub

pricedseparatefrom

liquefactionfee

Portfolio/hybridof

differentindices(Oil,

hub,AsiaSpot)

Marketbasedprice

TakeorPay/capacitypayment

Yesat95%ACQ(with

make-up)

Onlyonliquefaction

fee(nomake-up)

Yeswithreduced

volumecommitmentTakeorpay100%

30DAVIDLEDESMA&MIKEFULWOOD

• AstheLNGmarketliberalises,contractstructureswillchange– Contractsbecomeincreasinglyflexible,passingthroughahybridstageuntiltheybecome

merchanttypeagreements– Contractdurationreduces,ultimatelytonolong-termcontractsoncethemarketisfully

merchant– Inamerchantmarketnotake-orpayisrequiredassecuritycomesfromthemarket

• Differentcompaniesoperatedifferently,buteventuallyamerchantmarketresultsinallplayersoperatingonalevelplayingfield

– Movetowardsmarketpricingandcommonalityofcontracts• Financingstructuresrelyonthemarket

– Marketgivessufficientsecurityofofftake,theprimaryriskispricelevelnotvolume

NATURALGASPROGRAMME

Stagestoatraded/merchantmodel– ContractStructure

31DAVIDLEDESMA&MIKEFULWOOD

• Compromisebetweenbuyersandsellersoncontracttermssuchthatbuyersagreetotermsthatsupportsellersprojecteconomicsandsellersgiveflexibilitytomanagebuyersmarketuncertainties

• LendersmustdevelopfundingpackagesthatsupportchangesintheLNGmarketstructure

– Projectsmusthavecrediblefinanceablebuyers/capacityholderstounderpinofftake/capacitycontracts

– SufficientfinancialcapacitymustbeavailabletomeetLNGfundingrequirements– Projectsmustbestructuredcorrectly

• Acceptancethatmedium/long-termcontractsarerequired(untilLNGmarkethassufficientliquiditysuchthatLNGcanbetradedwithoutperiodsofextremevolatilityandthatcargoescanalwaysbeboughtorsoldinthemarket).Couldthisbepost2020when~40-45%LNGsoldgloballywillbeunderflexiblecontractterms5?

• Managingmarketuncertainties-BuyerswilllikelypurchasenewLNGonaportfoliobasisonavarietyofpricingindiceswithdifferentcontracttermsasameanstomanagerisk

• Marketliquidityandtrustedpricingindices-Weareonthepathtoamerchant/tradedLNGmarket,butthereisstillalongwaytogo.AmajorblockeristheavailabilityofanindependentLNGpricingindices.

Conclusion1WhataretheissuesthatneedtoberesolvedtoenableFIDstohappen?

NATURALGASPROGRAMME

32DAVIDLEDESMA&MIKEFULWOOD

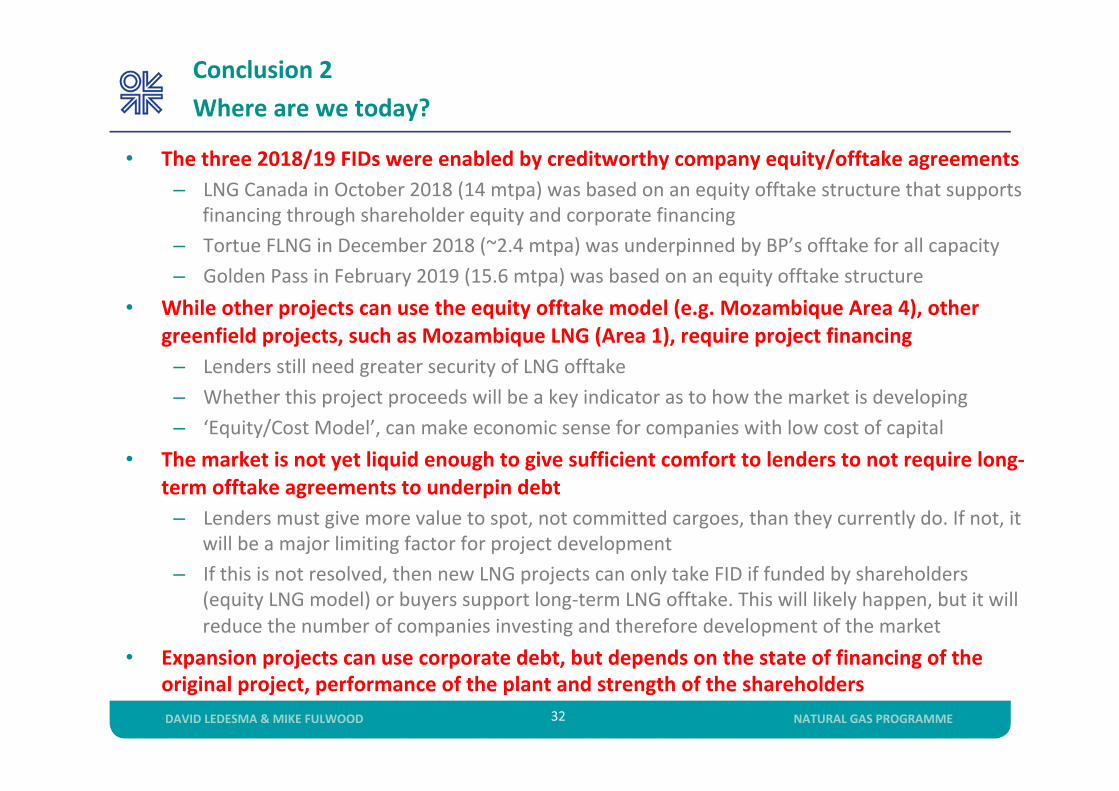

• Thethree2018/19FIDswereenabledbycreditworthycompanyequity/offtakeagreements– LNGCanadainOctober2018(14mtpa)wasbasedonanequityofftakestructurethatsupports

financingthroughshareholderequityandcorporatefinancing– TortueFLNGinDecember2018(~2.4mtpa)wasunderpinnedbyBP’sofftakeforallcapacity– GoldenPassinFebruary2019(15.6mtpa)wasbasedonanequityofftakestructure

• Whileotherprojectscanusetheequityofftakemodel(e.g.MozambiqueArea4),othergreenfieldprojects,suchasMozambiqueLNG(Area1),requireprojectfinancing

– LendersstillneedgreatersecurityofLNGofftake– Whetherthisprojectproceedswillbeakeyindicatorastohowthemarketisdeveloping– ‘Equity/CostModel’,canmakeeconomicsenseforcompanieswithlowcostofcapital

• Themarketisnotyetliquidenoughtogivesufficientcomforttolenderstonotrequirelong-termofftakeagreementstounderpindebt

– Lendersmustgivemorevaluetospot,notcommittedcargoes,thantheycurrentlydo.Ifnot,itwillbeamajorlimitingfactorforprojectdevelopment

– Ifthisisnotresolved,thennewLNGprojectscanonlytakeFIDiffundedbyshareholders(equityLNGmodel)orbuyerssupportlong-termLNGofftake.Thiswilllikelyhappen,butitwillreducethenumberofcompaniesinvestingandthereforedevelopmentofthemarket

• Expansionprojectscanusecorporatedebt,butdependsonthestateoffinancingoftheoriginalproject,performanceoftheplantandstrengthoftheshareholders

Conclusion2Wherearewetoday?

NATURALGASPROGRAMME

33DAVIDLEDESMA&MIKEFULWOOD

1. ShellLNGOutlook2018,https://www.shell.com/energy-and-innovation/natural-gas/liquefied-natural-gas-lng/lng-outlook.html2. 2018BPEnergyOutlook,https://www.bp.com/en/global/corporate/energy-economics/energy-outlook.html3. “LNGMarketsinTransition,OIES,2016estimates43%&Cheniereconferencepresentationsestimate50%4. “TheLNGIndustryGIIGNLAnnualReport2019”,GIIGNL,March2019.“Pure”spottrades(PST)arecargoesdeliveredwithin3

monthsofthetransactiondate.5. ‘LNGMarketsinTransition:TheGreatConfiguration’,Ed.Anne-SophieCorbeauandDavidLedesma,p574,OIES2016,OUP,

https://www.oxfordenergy.org/shop/lng-markets-in-transition-the-great-reconfiguration/6. ICISGlobalLNGMarkets,8thMarch2018“Shelltopsupafurther1mtpawithUSVentureGlobal”7. Japan'sJERAintalksforLNGcontractwithnodestinationlimits”,Reuters11thOctober2017,

https://www.reuters.com/article/us-commodities-summit-jera/japans-jera-in-talks-for-lng-contract-with-no-destination-limits-idUSKBN1CG0SR

8. Stern,J(2017).‘ChallengestotheFutureofGas:unburnableorunaffordable?’,OIESNG125,https://www.oxfordenergy.org/publications/challenges-future-gas-unburnable-unaffordable/

9. LedesmapresentationtoOIESNaturalGasProgrammeSponsors,25thApril2017,‘LongtermLNGsupply–thechallengesofinvestingfor2025’

10. Reuters14thMarch2018,‘TokyoGastorenewMalaysiaLNGpurchasesfromPetronasunit”,https://af.reuters.com/article/commoditiesNews/idAFL3N1QW2GH

11. TellurianCorporatePresentation,1stOctoberhttps://ir.tellurianinc.com/presentations12. http://www.cheniere.com/terminals/corpus-christi-project/liquefaction-facilities-midscale-trains/13. https://www.macrobusiness.com.au/2018/03/energy-crisis-deepens-gas-reserves-evaporate/14. www.ventureglobalng.comand

https://www.federalregister.gov/documents/2017/12/05/2017-26139/venture-global-calcasieu-pass-llc-transcameron-pipeline-llc-notice-of-schedule-for-environmental

15. ThePrincipleofProjectFinance,RodMorrison,GowerPublishing2012,Chapter16ProjectFinancingLNGProjects,DavidLedesma

Bibliography/Sources

NATURALGASPROGRAMME

34DAVIDLEDESMA&MIKEFULWOOD

1. Thesecuritypackagecanincludetheequityinvestmentofsponsorsmadepriortoloandisbursement,engineering,procurementandconstructioncontracts,sponsorcompletionguarantees,availabilityofstart-upworkingcapital,implementationofatrusteerevenueaccountoffshore(i.e.escrowaccount),prioritisationofinsuranceproceeds,anyliensoverproperty,sovereignassurances(ifapplicable)andprioritisationoffundallocation(thecash‘Waterfall’)

2. ‘TippingPoint’asdefinedinthispaper-thepointinthemarketatwhichacargoofLNGcanbeboughtandsoldandcanbedeliveredintomultipleliquidtradingmarketswithoutlimitandhavingamajorimpactonthemarketprice

3. DefinitionsJV–JointVentureLT–Long-TermSPV–SpecialPurposeVehicleIOC–InternationalOilCompanyNOC–NationalOilCompanyHighcredit(AAAorAA)–highestcreditratedcompaniesthatcantradeusuallywithoutbankorparentcompanyguarantees

Glossary/Definitions

NATURALGASPROGRAMME