nest presentation 2015

TRANSCRIPT

Alzheimer ScotlandYour Retirement and Life Assurance Provision

19 May 2015

Agenda

Retirement

Life Assurance

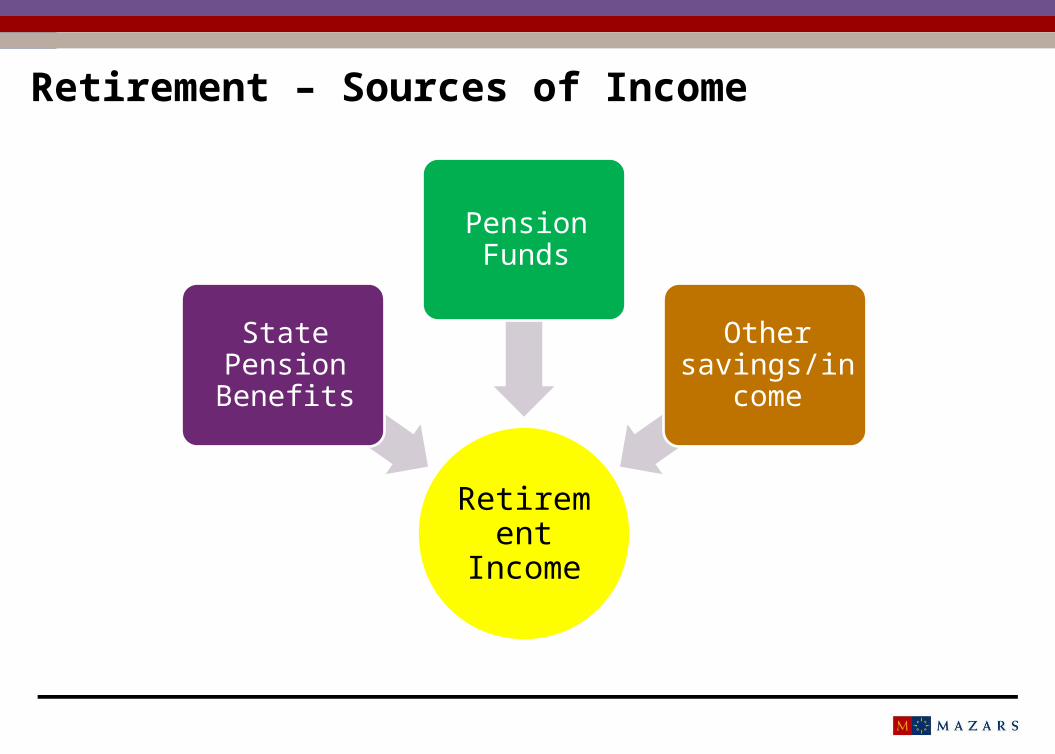

Retirement – Sources of Income

Retirement Income

State Pension Benefits

Pension Funds

Other savings/income

Saving for retirement – essential questions

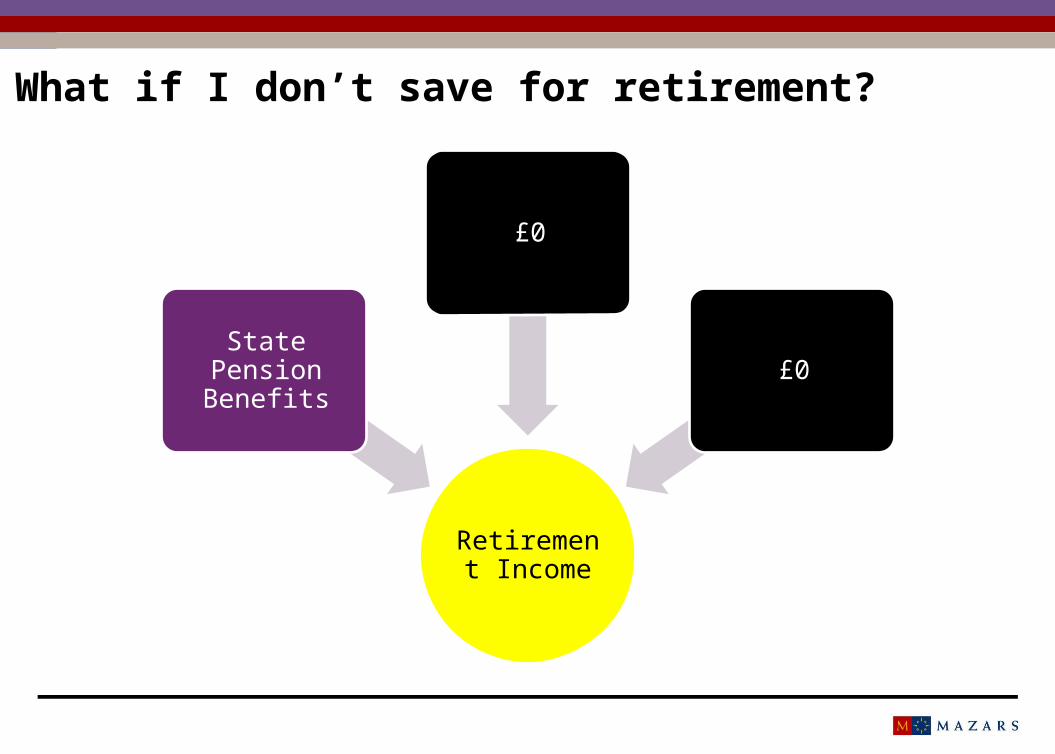

1. What if I don’t save for retirement?

2. When do I want to retire?

3. How do I want to live in retirement?

4. Will I be able to retire?

5. Can I, and do I want to save for retirement?

What if I don’t save for retirement?

Retirement Income

State Pension Benefits

£0

£0

When? Male or female When were you born No earlier than State Pension Age

How much? Number of years you have paid National Insurance Contributions

(NIC)

www.gov.uk/calculate-state-pension

Key questions and where to get the answersState Pension Benefits

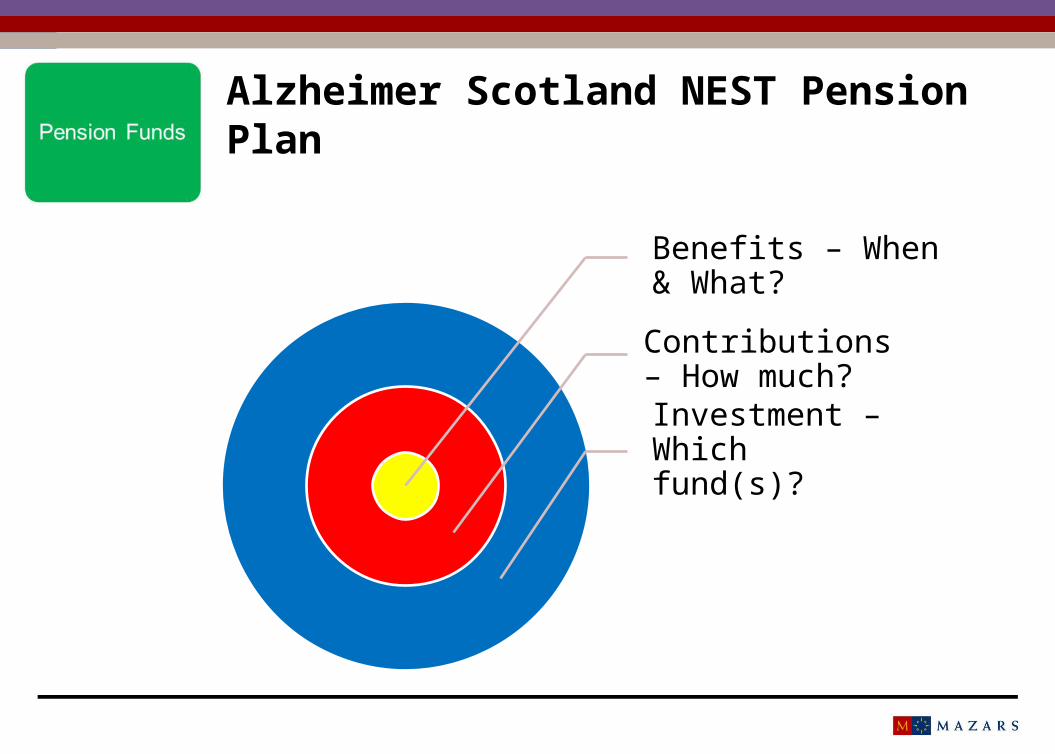

Alzheimer Scotland NEST Pension Plan

Benefits – When & What?

Contributions – How much?

Investment – Which fund(s)?

Benefits - When?

Earliest date you can take your Alzheimer Scotland Pension Plan benefits:

Currently age 55 Increasing to 57 from 2028 Thereafter, no earlier than 10 years before State Pension Age

Selected Retirement Date You choose – if not, default dare is your State Pension Age Annual Plan statement benefits projection Sets date for Retirement Date Fund investments

8

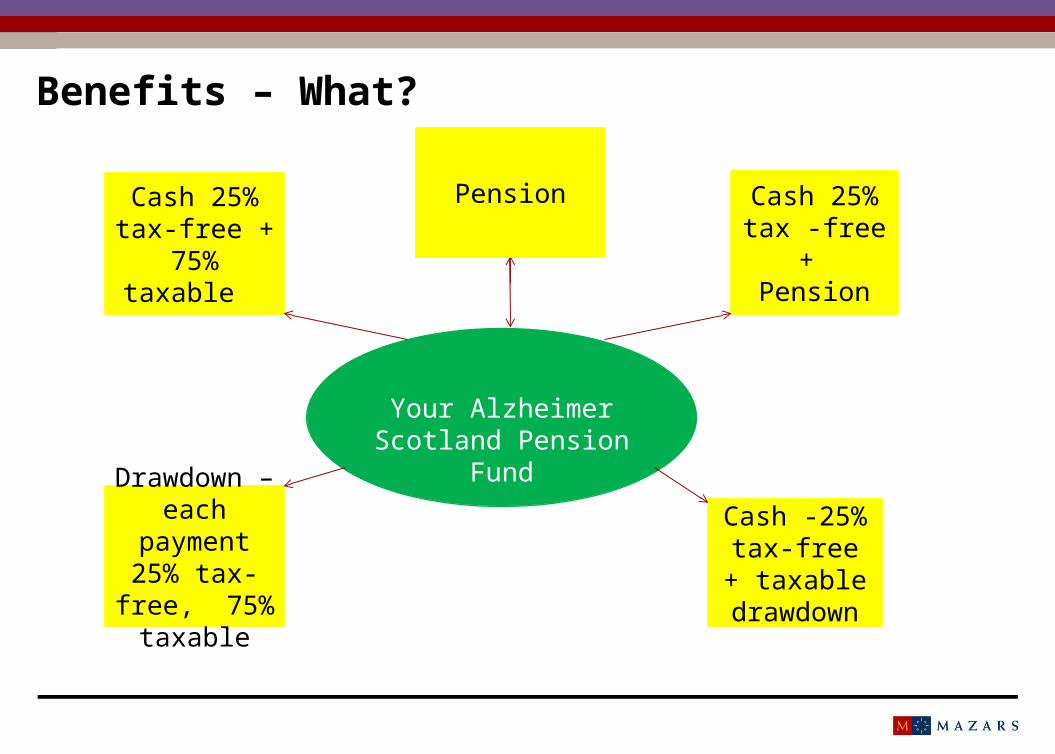

Benefits – What?

Your Alzheimer Scotland Pension Fund

Cash 25% tax -free

+ Pension

Cash 25% tax-free + 75%

taxable

Drawdown – each payment 25% tax-free, 75% taxable

Pension

Cash -25% tax-free +

taxable drawdown

Benefits – What?

Contributions Investment Returns

Your Alzheimer Scotland

Pension Fund

Contributions - How it works?

NEST

Employer Contribution

Employee Contributions

(x80%)

Tax Relief (20%)

Contribution Structure

Employer Contribution

Employee Contributions

(x80%)

Tax Relief (20%)

Dates Employer Contribution (% of qualifying

earnings)Your Minimum

Contribution (% of qualifying earnings)

Enrolment date to 30 September 2017 1% 1%

1 October 2017 – 30 September 2018 2% 3%

1 October 2018 onwards 3% 5%

Qualifying Earnings - All monthly earnings between £486 and £3,532 (2015/16 tax year)

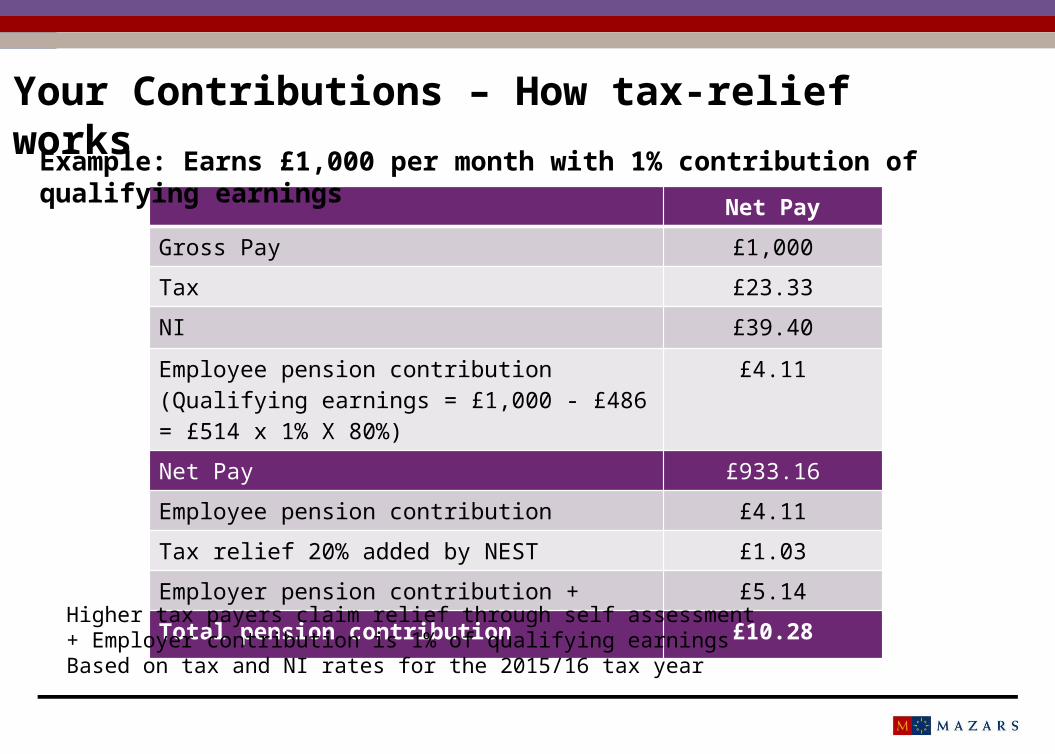

Your Contributions – How tax-relief works

Net Pay

Gross Pay £1,000Tax £23.33NI £39.40

Employee pension contribution (Qualifying earnings = £1,000 - £486 = £514 x 1% X 80%)

£4.11

Net Pay £933.16Employee pension contribution £4.11Tax relief 20% added by NEST £1.03Employer pension contribution + £5.14

Total pension contribution £10.28

Example: Earns £1,000 per month with 1% contribution of qualifying earnings

Higher tax payers claim relief through self assessment + Employer contribution is 1% of qualifying earningsBased on tax and NI rates for the 2015/16 tax year

Key questions and planning support

1. When - Am I saving enough?

2. Lifestyle - Am I saving enough?

3. Ability - Am I saving enough?

4. Capability – Can I/will I save enough?

Investment - Options

1. Default Investment Option NEST Retirement Date Fund. Based on your State Pension Age (or your selected NEST retirement date)

2. Select your own funds Five alternative funds available from NEST

Investment – Plan Default OptionThe Retirement Date funds work in three phases:

Phase Objectives Years to Selected Retirement Age (approximate)

Foundation • Preserve fund value and keep pace with inflation• Reduce likelihood of extreme investment shocks• Target long-term volatility average of 7%

>40

Growth • Target investment returns of inflation + 3%, net of charges

• Take sufficient investment risks whilst reducing likelihood of extreme investment shocks

• Target long-term volatility average of 10-12%

<40 >10

Consolidation • Gradual move to annuity-tracking and cash like investments

• Reduce likelihood of investment shocks• Reduce volatility

<10

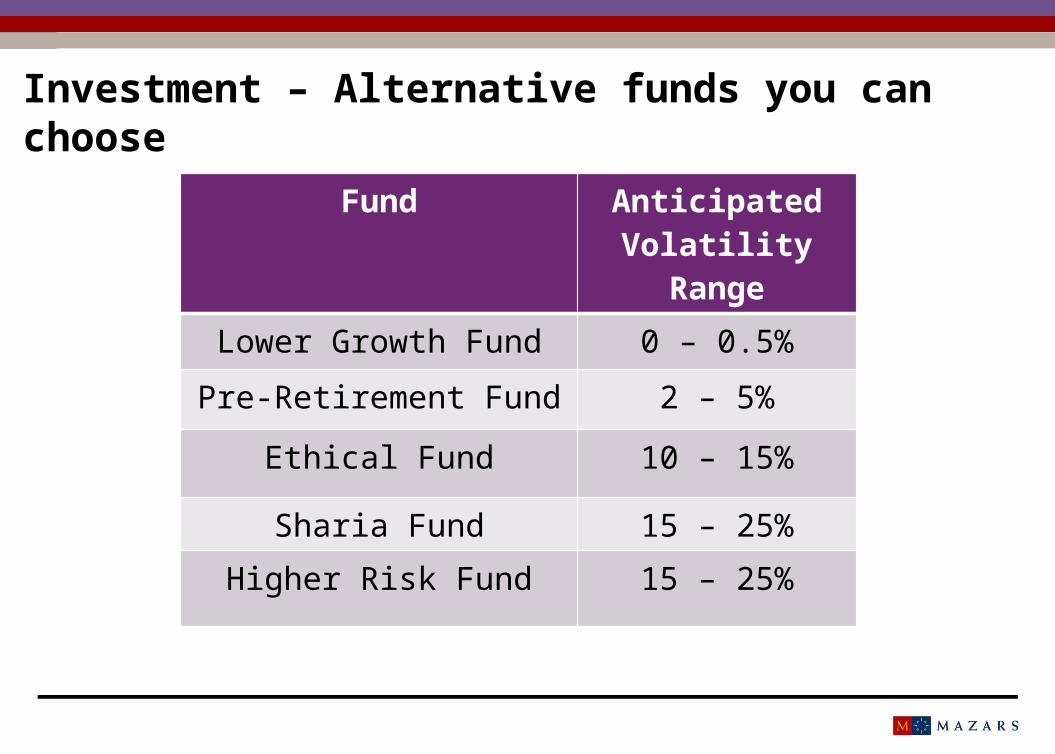

Investment – Alternative funds you can choose

Fund Anticipated Volatility Range

Lower Growth Fund 0 – 0.5%

Pre-Retirement Fund 2 – 5%

Ethical Fund 10 – 15%

Sharia Fund 15 – 25%

Higher Risk Fund 15 – 25%

Plan Charges

Annual Fund Management Charge

– 0.30%

Contribution Charge – 1.80%

Investment & Administration – NEST Online Services

Access individual account details and update View contributions Valuation of your policy Switch funds Update nominated beneficiaries

Registration process:

https://www.nestpensions.org.uk/schemeweb/NestWeb/faces/secure/USER_REG/pages/activateYourAccount.xhtml

Follow online instructions

19

Planning For Your Retirement – Summary Considerations

www.gov.uk/calculate-state-pension

Individual annual benefit statement

Previous employers pension schemes or individual pension policies www.pensiontracingservice.com

Other savings and/or income available on retirement ?

20

State Pension Benefits

Your Alzheimer Scotland

Pension Fund

Other Pension Funds

Other Savings/Income

What happens if….I die before taking my retirement benefits?

Your fund returned to your nominated beneficiary(ies) as a tax free lump sum

Update nominated beneficiary via NEST online access, or complete the return nomination form included in Welcome Pack from NEST

No completed nomination – NEST normally pay your fund to person looking after your financial affairs on death

Change of personal circumstances/nomination - Inform NEST to ensure your funds are distributed in line with your wishes.

21

What happens if….I leave Alzheimer Scotland?

Options available:

1. Continue to make personal contributions to the Plan (minimum £10 each time)

2. Suspend contributions and restart later

3. Make no further contributions and leave funds invested until you take benefits

You will not be entitled to a refund of contributions if you leave the Plan. You are currently unable to transfer your fund elsewhere unless aged 55 or over (to be removed 1 April 2017).

22

Life Assurance Insurer AvivaWhen am I eligible? All permanent employees aged 16 – 75When can I join? On commencement of employmentHow do I join? Automatically includedWhat do I pay? Nothing, full cost met by Alzheimer ScotlandBenefit Lump sum = 3 x your earnings (before salary exchange) subject

to a minimum of £5,000Contract workers – annual basic salarySeasonal – total earnings declared in tax year before death

When is it paid? In the event of your death as a permanent employee of Alzheimer Scotland

Who is this paid to? Your nominated beneficiaries, at Trustees discretion

Is this a taxable benefit? No, exempt from Inheritance Tax

When does cover cease? Earlier of employment ceasing with Alzheimer Scotland or attainment of age 75

Life Assurance – Nominating Your Beneficiaries

Trustees – Alzheimer Scotland

Trustees discretion to whom benefit payable = exempt from Inheritance Tax

Nomination Form available from Trustees

Completion supports payment of benefits with minimum delays

Complete updated form if circumstances/wishes change

24

Questions

?

Disclaimer

The contents of this presentation are confidential and not for onward distribution. Disclosure to third parties cannot be made without the prior written consent of Mazars Employee Benefits Limited.

The information presented does not constitute advice.

It is based on our current interpretation of UK legislation and HMRC practice at the date of production. This may be subject to change in the future and any tax rates or reliefs may be altered. Professional advice should be sought prior to making any decision and Mazars Employee Benefits Limited will not accept responsibility for decisions taken solely on the basis of the information presented. Some services offered by Mazars Employee Benefits Limited are not regulated by the Financial Conduct Authority.

Mazars Employee Benefits Limited is an Appointed Representative of Mazars Financial Planning Limited which is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 03893679 with its registered office at Tower Bridge House, St Katharine’s Way, London, E1W 1DD.

Mazars Employee Benefits Limited and Mazars Financial Planning Limited are both wholly owned subsidiaries of Mazars LLP, the UK firm of Mazars, an integrated international advisory and accountancy organisation