nepal public debt sustainability analysis · nepal public debt sustainability analysis ... finish...

TRANSCRIPT

NRM Working Paper No. 5

NEPALPUBLIC DEBT SUSTAINABILITY ANALYSIS

Mohiuddin Alamgir and Sungsup Ra

October 2005

Mohiuddin Alamgir is an Asian Development Bank Staff Consultant, and Sungsup Ra is Head,Macroeconomic, Finance, Governance, Regional and External Relations and Senior CountryPrograms Specialist in the Nepal Resident Mission.

Copyright: Asian Development Bank 2005

All rights reserved.

The views expressed in this book are those of the authors and do not necessarily reflect the viewsand policies of the Asian Development Bank, or its Board of Governors or the governments theyrepresent.

The Asian Development Bank does not guarantee the accuracy of the data included in thispublication an accepts no responsibility for any consequence of their use.

Use of the term “country” does not imply any judgement by the authors or the Asian DevelopmentBank as to the legal or other status of any territorial entity.

ISSN 1816-3416

Published and printed by the Asian Development Bank, 2005.

ii

PREFACE

In Nepal, public debt, both domestic and foreign, has played an important role in financingoverall budget deficit and public development expenditure. Hindered by the escalating insurgencythat has directly contributed to a slowdown in tourism and other economic activities throughout thenation, economic growth has been significantly lower than envisaged by the Ninth Five Year Plan(FY1997–FY2002) and the Tenth Five Year Plan (FY2003–FY2007). This could exacerbate thealready narrow base for domestic resource mobilization. It is therefore imperative to continuouslymonitor the sustainability of public debt of Nepal.

The study on Nepal Public Debt Sustainability Analysis was undertaken by the AsianDevelopment Bank (ADB) in 2001 to analyze the public debt sustainability of Nepal. The outcomeof the study was intended to improve debt management by the Government of Nepal and to provideinputs for the Tenth Five Year Plan and other long-term perspective plans. It was also intended toassist the ADB to articulate its lending policy for Nepal based on country risk analysis.

Although a few years have elapsed since the study was completed, the findings are stillrelevant as Nepal reviews its eligibility for Highly Indebted Poor Countries (HIPC) initiatives.

The study was carried out by Mohiuddin Alamgir, ADB Staff Consultant and Sungsup Ra,Head, Macroeconomics, Finance, Governance, Regional, and External Relations, and SeniorCountry Programs Specialist, Nepal Resident Mission (NRM). The editorial assistance of Arun S.Rana is appreciated, and thanks are due to Kavita Sherchan, External Relations and Civil SocietyLiaison Officer, NRM for finalizing the report.

Sultan Hafeez RahmanCountry DirectorNepal Resident MissionAsian Development Bank

iii

CURRENCY EQUIVALENTS

(as of 31 October 2001)

Currency Unit = Nepalese Rupees (NRe/NRs)Nre 1.00 = $0.1315$1.00 = NRs76.05

(i) The Nepalese rupee is pegged to the Indian rupee (Re) at NRs1.60 to Re 1.00 andis fully convertible on all current account transactions.

(ii) The exchange rate used to determine the dollar equivalent of Nepalese rupee valuesin the text is the end of the period rate.

ABBREVIATIONS

ADB – Asian Development BankAPP – Agriculture Perspective planASYCUDA – Automatic System of Customs DataAUG – Auditor General’s OfficeBOP – balance of paymentsCS-DRMS – Commonwealth Secretariat Debt Recording and Management

SystemDFID – Department for International Development, United KingdomDMU – Debt Management UnitDOD – disbursed outstanding debtDPMU – Debt Policy Management UnitEEC – European Economic CommunityEKPF – EksportfinanceFCGO – Financial Comptroller General’s OfficeFDI – foreign direct investmentFEC – Finish Export Credit LimitedFMP – Financial Management ProjectGDP – gross domestic productGNP – gross national productHIPC – heavily indebted poor countriesICOR – Incremental capital output ratioIDA – International Development AssociationIFAD – International Fund for Agricultural DevelopmentIFC – International Finance CorporationIMF – International Monetary FundIPRSP – Interim Poverty Reduction Strategy PaperKFAD – Kuwait Fund for Arab Economic Development

iv

M1 – Narrow MoneyM2 – Broad MoneyMFCL – Mitsui Fudosan Company LimitedMOF – Ministry of FinanceMTBF – Medium Term Budget Framework ProjectNADC – Norwegian Agency for Development CooperationNDF – Nordic Development FundNPC – National Planning CommissionNPV – net present valueNRB – Nepal Rastra BankOPEC Fund – OPEC Fund for International DevelopmentPDD – Public Debt DepartmentPRSP – Poverty Reduction Strategy PaperSAFD – Saudi Fund for DevelopmentSDR – special drawing rightsUNCD – United Nations Capital Development Fund

NOTES

(i) The fiscal year (FY) of the Government ends on 15 July. FY before a calendar yeardenotes the year in which the fiscal year ends, e.g., FY2002 ends on 15 July 2002.

(ii) In this report, “$” refers to US dollars.

v

CONTENTS

Page

EXECUTIVE SUMMARY i

I. EXTERNAL DEBT 1

A. Review of Current External Debt Position 1B. External Debt Sustainability Analysis 33

II. PUBLIC DEBT 51

A. Review of Current Public Debt Position 51B. Public Debt Sustainability Analysis 63

III. THE COMMONWEALTH SECRETARIAT DEBT RECORDINGAND MANAGEMENT SYSTEM (CS-DRMS) 68

A. Current Status 68B. Options for the Future 69

IV. POLICY IMPLICATIONS 72

A. Policy Recommendatyions for the Government 72B. Policy Implications for ADB Operation 73

V. CONCLUSIONS 74

Appendix 78

BIBLIOGRAPHY 81

vi

EXECUTIVE SUMMARY

Public debt, domestic and foreign has played an important role in financing overall budgetdeficit and public development expenditures. Of the two, foreign financing has been predominant.Foreign financing has also been crucial to financing balance of payments deficit. Given the lacklusterperformance of the economy over the first four years of the Ninth Five Year Plan, covering fiscalyear (FY)1997–FY2002, a significantly higher level of effort will be required to mobilize and efficientlyutilize domestic and foreign resources in order to achieve the Ninth Plan (FY1997–FY2002) targetof an average annual growth rate of real gross domestic product (GDP) of 6% and maintain themomentum over the Tenth Five Year Plan (FY2003–FY2008). Given the narrow base for domesticresource mobilization and exports, it is important to continuously monitor the sustainability of publicdebt of Nepal—that is, the country’s ability to meet its medium and long-term debt obligations.

In Nepal, debt management is the responsibility of the Ministry of Finance (MOF) and NepalRastra Bank (NRB). A Debt Management Unit (DMU) under the Foreign Aid Coordination Divisionof the MOF is responsible for recording loan details and monitoring payments. The FinancialComptroller General’s Office (FCGO) records actual disbursements and authorizes payment onloans. External funds are received and foreign payments are made through NRB which recordsand monitors private sector loans and domestic debt instruments. The DMU received technicalassistance grant support from the Department for International Development (DFID) of the UnitedKingdom.

The Commonwealth Secretariat Debt Recording and Management System (CS-DRMS)was installed at the DMU. The CS-DRMS is a comprehensive database management system,which can carry out useful debt analysis and provide a wide rage of reports. After the completion ofDFID supported technical assistance the DMU and the CS-DRMS were confronted with certaininstitutional and logistic problems, which needed to be addressed. Debt data had not been inputtedup since March 2000. The equipment had not been maintained properly, trained personnel of theDMU had been withdrawn to their parent units in other ministries, there was apparent lack ofdemand for debt reports from relevant ministries and donor agencies, and the proposed extensionsto FCGO and NRB had not been implemented neither was a decision to transfer the server toFCGO had been followed through.

Against this backdrop, an Asian Development Bank (ADB) staff consultant undertook ananalysis of public debt sustainability of Nepal in order to improve debt management by theGovernment of Nepal, provide inputs for the Tenth Plan (FY2003–FY2007) and assist ADB toarticulate its lending policy for Nepal based on country risk analysis. More specifically, objectivesof debt sustainability analysis would include the following: (i) provide inputs regarding requirementsfor borrowing, domestic and foreign for the Tenth Plan (FY2003–FY2007); (ii) improve public debtmanagement including, public domestic debt; (iii) make recommendations for Governmentborrowing policies; (iv) link debt management policies to macroeconomic policies; (v) assess theCS-DRMS and make recommendations for its sustainability; and (vi) improve country riskmanagement for ADB operation in Nepal. All of these have been accomplished. In particular, thesystem is now up and running. Debt data has been inputted up to end September 2001 and it iscontinuing on a regular basis. The server has been installed in FCGO with connections to MOFand NRB through dedicated telephone line. A plan for upgrading the system is under considerationof the Government.

vii

of Nepal. The Government is now keen to ensure that this integrated debt data base managementsystem is maintained properly and reports are generated to provide inputs policy and strategyarticulation regarding debt management including foreign loan negotiations, annual budget andannual development plan exercises and Government domestic borrowing.

Nepal is one of the poorest countries of the region with an estimated gross national product(GNP) per capita of $250 in FY2000. It is estimated that in 1996, 42% of the population lived belowthe poverty line of $77 per capita per annum. The Ninth Plan (FY1997–FY2002) envisioned anaverage annual growth rate of real GDP of 6% but this goal remained elusive as it was reachedonly in FY2000. The performance over the first four years was mixed (3.3% in FY1998, 4.4% inFY1999 and 6.4% in FY2000 and estimated to have dropped to 5.7% in FY2001). FY2002 is shapingup to be a difficult year in the aftermath of the Maoist insurrection, slow down of the global economyand the impact of the September 11, 2001 attack on the World Trade Center in New York, adverselyaffecting Nepal’s income from tourism, industrial production, revenue collection and traditionalexports like garments, carpet and handicrafts.

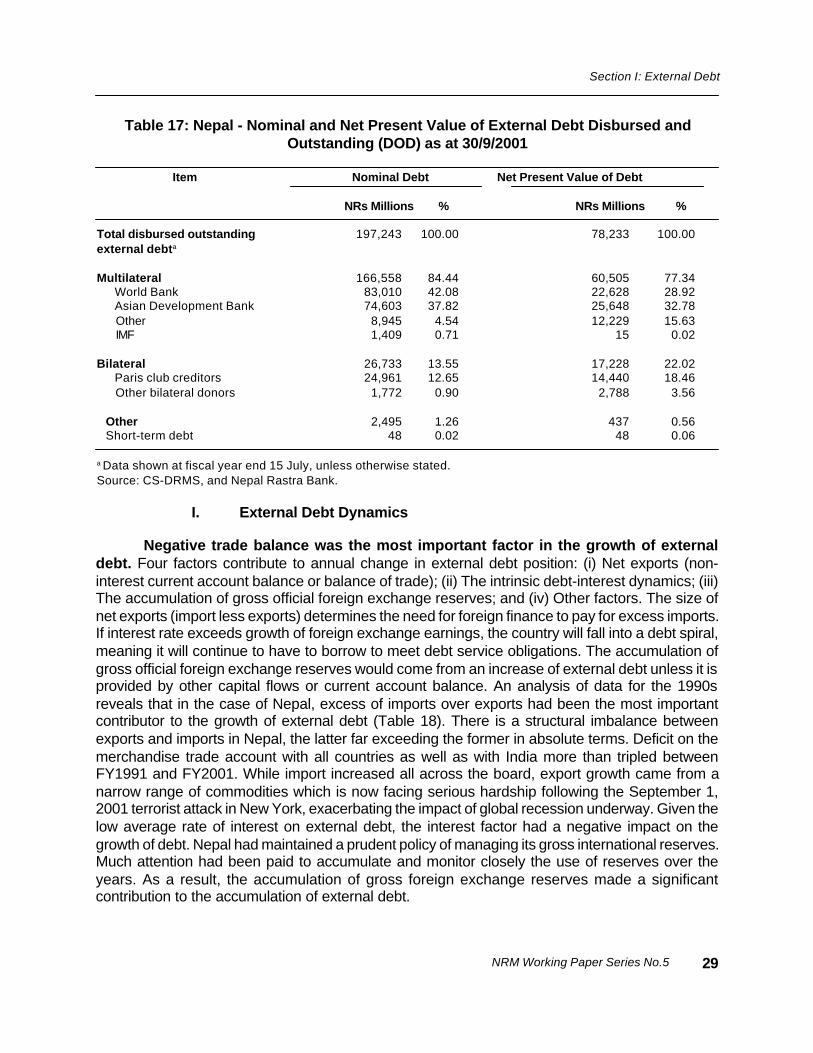

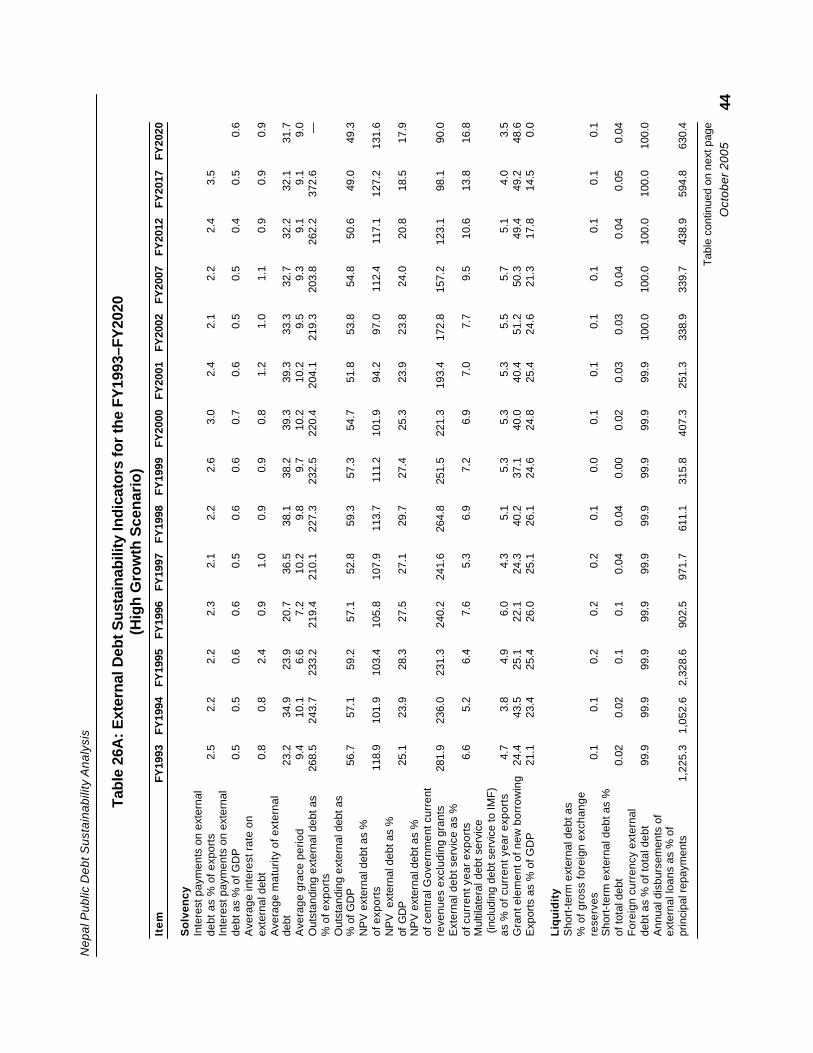

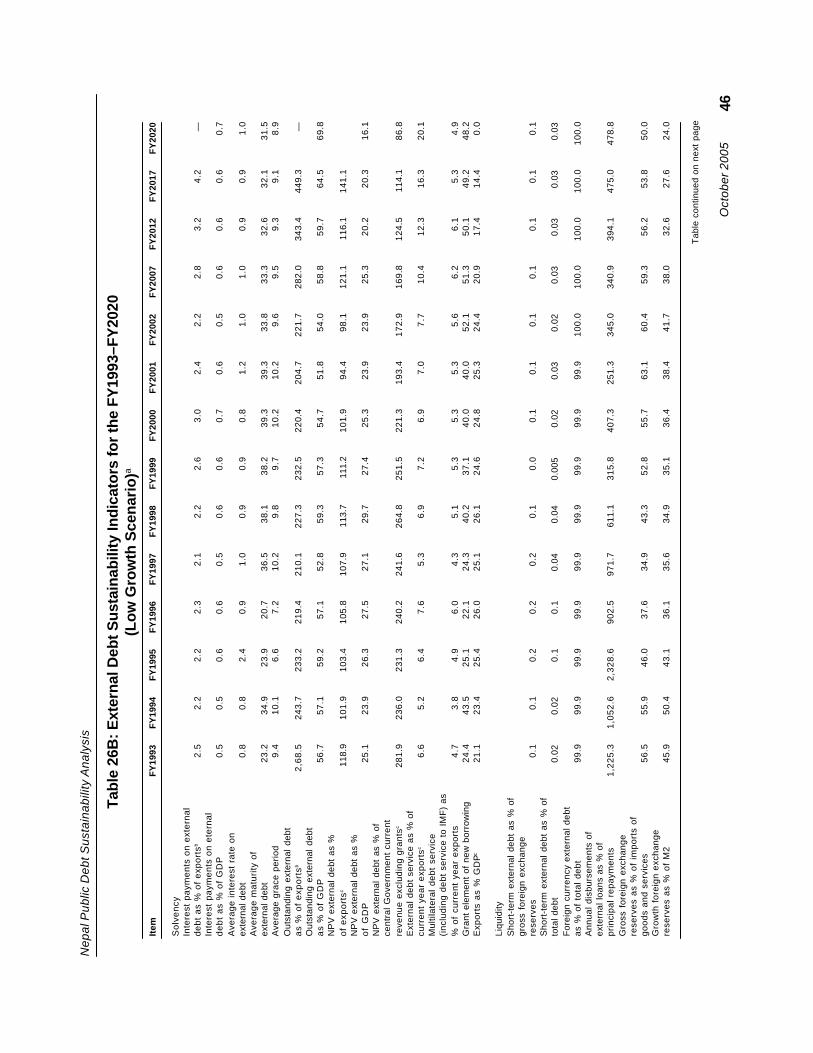

The level of external debt and debt service burden have remained reasonable throughoutthe period—total disbursed outstanding debt (DOD) was 51.8% of GDP and debt service remained7.0% of exports in FY2001—the only concern being matching foreign debt repayment obligationsin foreign currency with foreign exchange receipts given a large share of export receipts in Indianrupees. However, the fiscal burden of debt service, domestic and foreign is high—total serviceburden 47.0% of current revenue in FY2001.

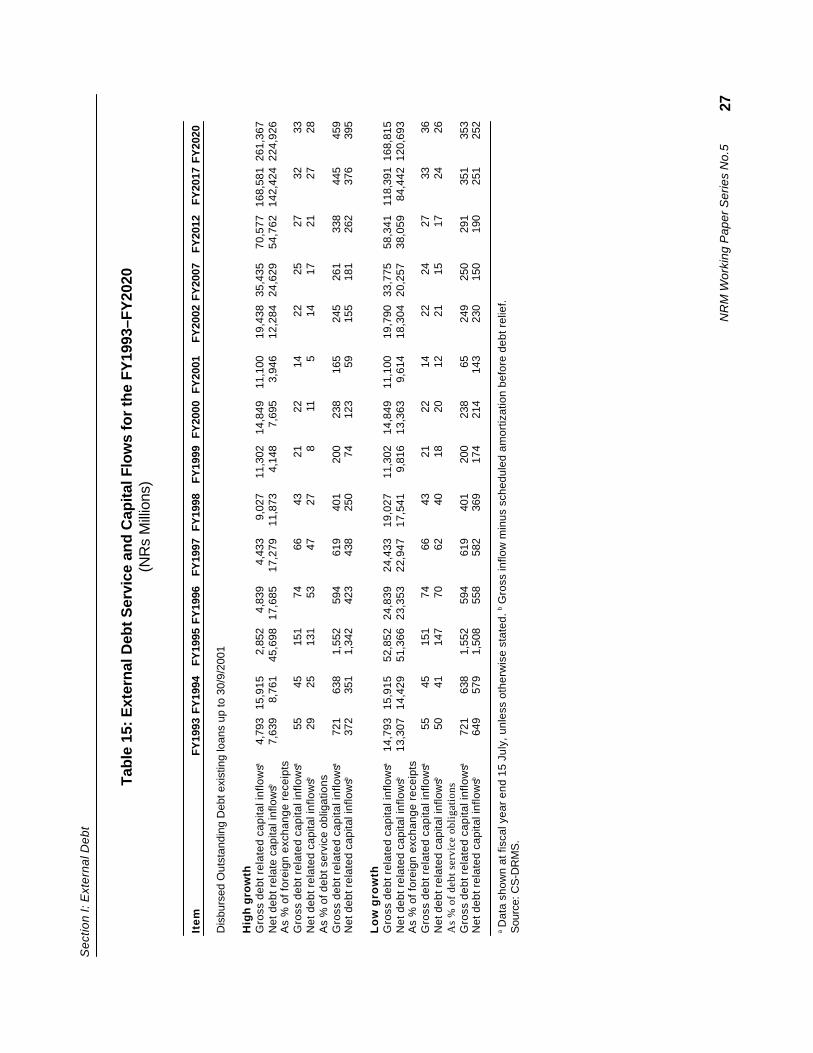

Nepal’s external debt stood at NRs197,195 million (approximately $2.6 billion at the exchangerate of end October 2001) as at 30 September 2001. The net present value (NPV) of external debtwas estimated at NRs78,233 million. The nominal debt stock represented a 115% increase overthe level of FY1993. However, total debt as percentage GDP and exports declined over this period,from 57% to 52% and from 269% to 204% respectively. Annual gross disbursement averagedabout NRs17,592 million ($231 million at the exchange rate end October 2001) and net disbursementNRs10,438 million ($137 million). Most external borrowing is done by the central Government.Private share was less than 2%. Loans contracted are primarily long-term. Short-term debt playsa small part in the total. Long-term debts are held by public authorities or are guaranteed by them.

Over past years, the share of multilateral creditors remained in excess of 80%. Bilateralshare was on the decline. The World Bank and the ADB accounted for over three fourth of multilaterallending to Nepal. Among bilateral creditors, major players included the Governments of Japan andFrance. Most debts were contracted on concessional terms (grant element less than 35%).However, 119 loans out of 323 reviewed were contracted on non-concessional terms. Loans werealmost all in foreign currency, of which special drawing rights (SDR) accounted for about 70%.The most important push factor in increase of external debt was large negative net exports followedby accumulation of foreign exchange reserve in most years. In Nepal’s case, the interest factor—excess of interest rate over growth of foreign exchange earnings—was actually a negative pushfactor. According to the most widely used debt sustainability indicators like net present vlaue (NPV)as percentage of exports (three year average) or debt service as percentage of current year exports,Nepal is well below critical levels. In terms of debt sustainability indicators, Nepal compares favorablywith other selected developing countries of Asia and Africa. The World Bank classifies Nepal as aless indebted country.

viii

Foreign loans were contracted for a wide range of activities across many sectors. Implicitprioritization seems to have had favored agriculture and rural development (including irrigation)and electricity. Broadly defined, the share of agriculture in total external debt increased from 27%in FY1992 to 36% in FY2002, the change being explained entirely by a significant shift of emphasistowards irrigation in accordance with the 20-year Agriculture Perspective Plan (APP).

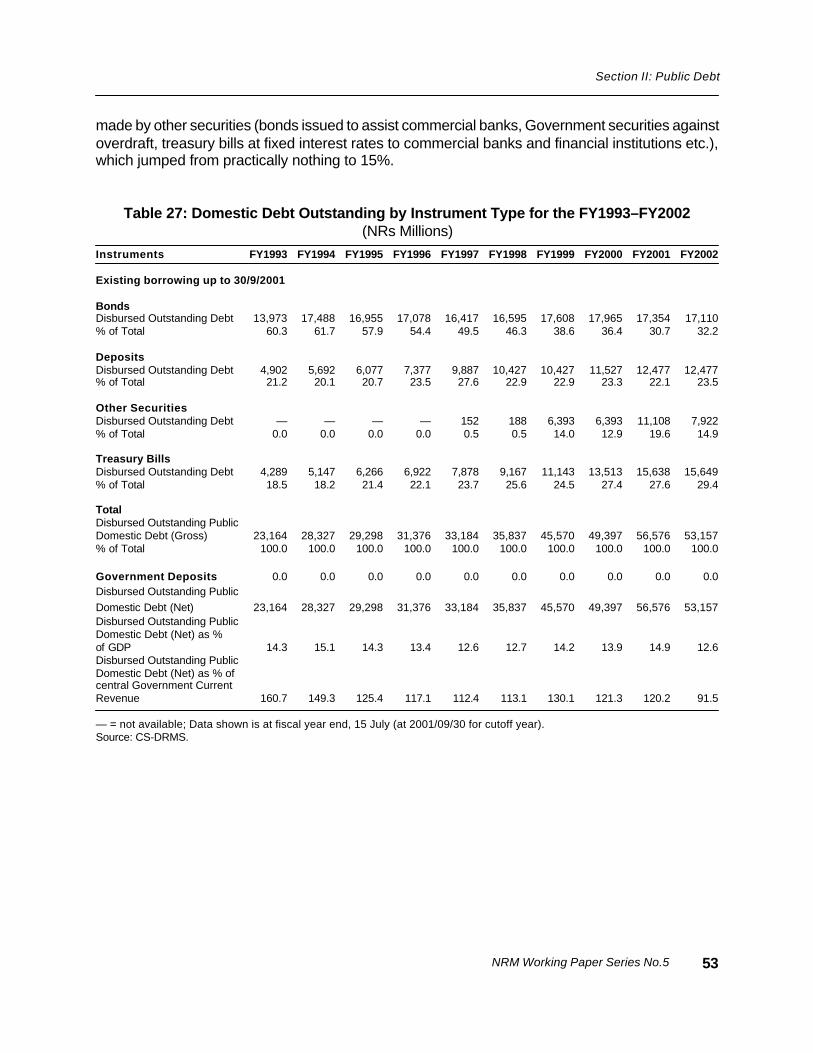

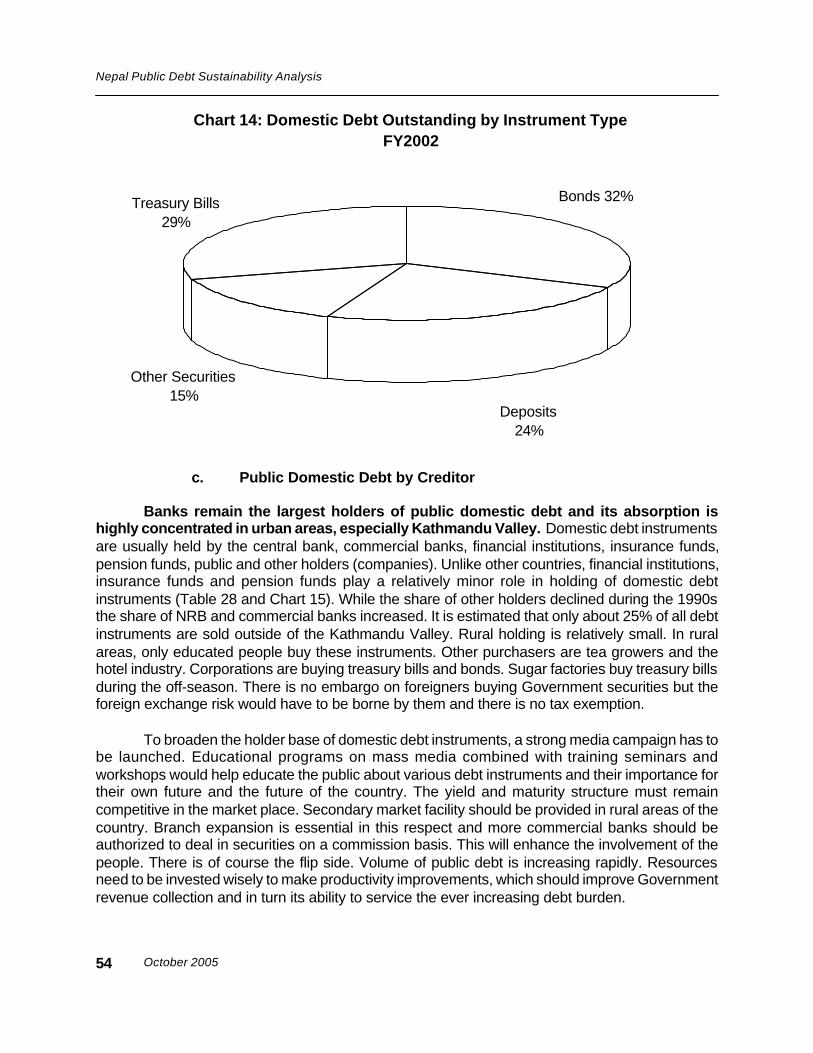

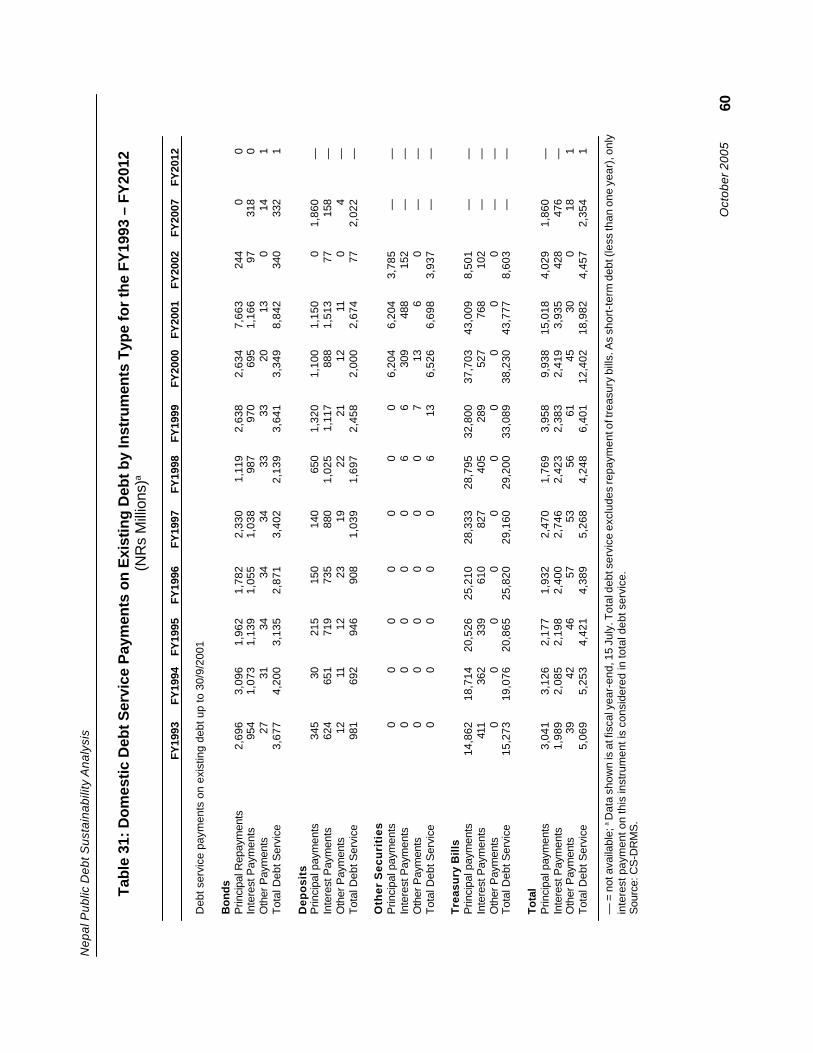

As for domestic debt, total DOD stood at NRs56,576 million as at end FY2001. BetweenFY1993 and FY2001, domestic DOD as percentage of GDP remained unchanged at 14%, but aspercentage of central Government current revenue it declined from 161% to 120%. Bonds accountedfor 32.2% of total domestic DOD in FY2001, deposits 23.5%, treasury bills 14.9% and other securities29.4%. Among holders of domestic debt instruments, the share of the central bank was 16.0%, ofwhich commercial banks held 23.0%, public 1.2%, and others 58.0%. Domestic debt serviceburden was high at 3–4% throughout the 1990s and at 33–35% of central Government currentrevenue. Debt and debt service burden turns out to be heavier if one looks together at both domesticand external debt although there was a marked improvement between FY1992 and FY2001. Atend FY2001, total public debt stood at NRs248,313 million. The most important push factorcontributing to increase of public debt was the primary deficits, especially discretionary primarybalance. Other push factors included were interest payment and exchange rate valuation adjustmentof the foreign currency denominated debt. The growth factor was a pull factor. Total public debt aspercentage of GDP declined from 71% in FY1992 to 65% in FY2001, and as percentage of revenuefrom 794% to 527%. During the 1990s, total public debt service burden was estimated at 4–6% ofGDP and 47–49% of central Government current revenue.

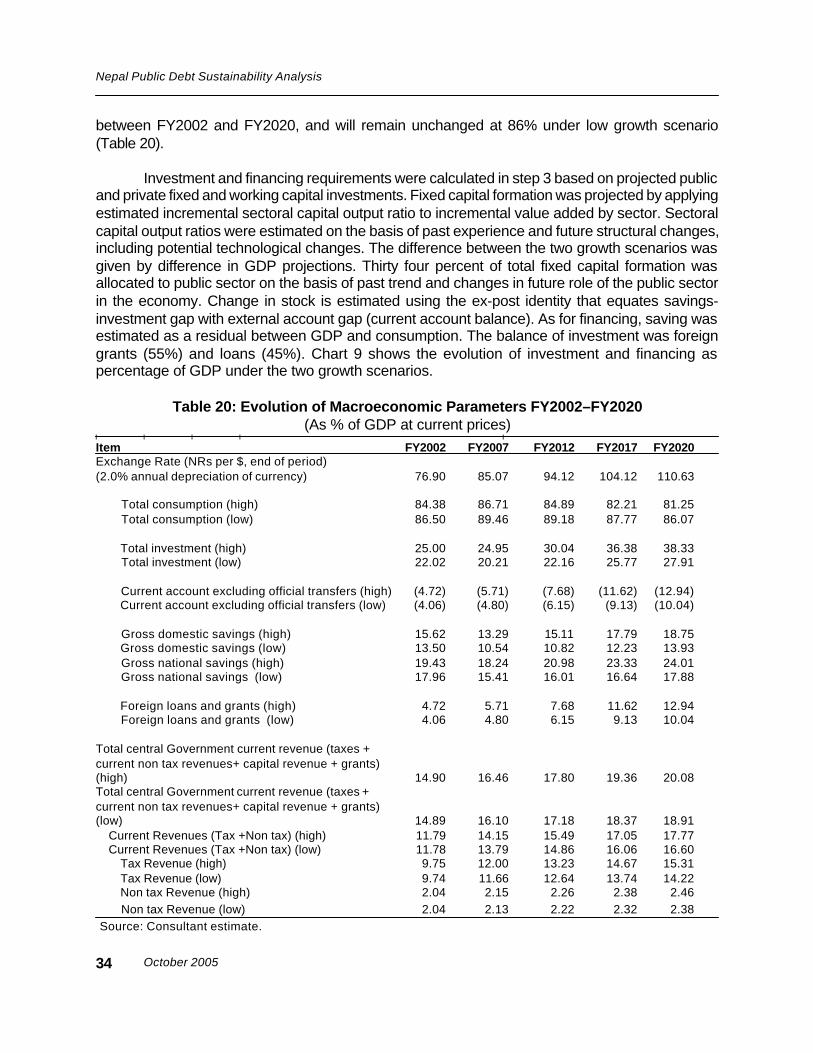

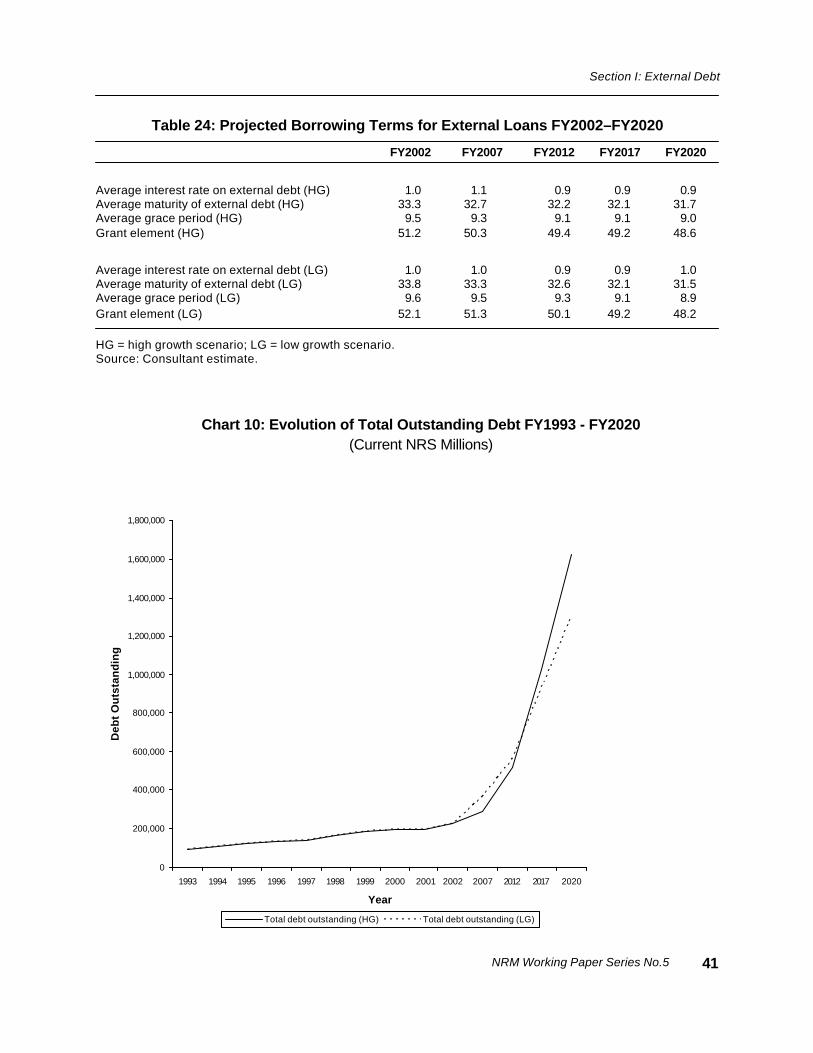

Projections for the future have been made based on two alternative growth assumptions,one high growth scenario and the other, low growth scenario. The high growth is a relatively optimisticscenario based on the assumption of rapid recovery from the aftermath of world economicslowdown and September 11, 2001 terrorist attack in New York. The agriculture sector growth isassumed to follow projections under the APP although there will be structural shift in favor oftourism and service sectors. The Government of Nepal is expected to pursue policies consistentwith continued macroeconomic stability, low inflation (3% per annum), increased share of revenuein GDP (from 12% in 2002 to 18% in FY2020), pruning of public expenditure to reflect efficiencyand effectiveness of public investments, and money supply growth reflecting growth of production,monetization, and capacity utilization. Both gross domestic savings and total investment rates areprojected to grow substantially from their current modest levels—from 16% of GDP in FY2002 to19% in FY2020, and from 25% to 38%, respectively. For foreign grants and loans, the Governmentof Nepal will aggressively seek to obtain at least 45% in grants and loans on concessional terms(grant element > 35%). In financing of the budget deficit, it is assumed that the share of internalborrowing will be retained at 35% mostly through medium term instruments. An enabling policyenvironment will be kept in place to ensure growing participation of the private sector includingforeign private investments in the economy. The role of the public sector will be limited to areas ofcomparative advantage away from direct production and distribution. The low growth scenario, onthe other hand, assumes lingering hangover of the global economic slowdown and the impact ofthe events of September 11, 2001. It is assumed in general that the negative impact on tourism,industrial production, revenue collection and traditional exports like garments, carpet and handicraftswill persist and the economy will at best recover to follow the past trend. Under the high growth

ix

scenario, average annual rate of growth of GDP in constant 1985 prices is projected to increasefrom 5.6% during the Tenth Plan (FY2003–FY2007) period to 8.5% during FY2017–FY2020 period.The corresponding rates under the low growth scenario are 5.6% and 5.9%. What are theimplications of alternative growth scenarios for public debt sustainability and country riskmanagement?

Requirements for external and domestic borrowing will differ significantly depending ongrowth assumptions. Under the high growth scenario, the nominal value of total public debt isprojected to increase from NRs248,313 million in FY2001 to NRs1,677,188 million in FY2020. Ofthis, external debt is projected to go up to NRs1,576,970 million from NRs1,919,737, and domesticdebt to NRs100,219 million from NRs56,576 million. Total public debt/GDP ratio declines slightlyfrom 65% to 63%, domestic from 15% to 4%, but external debt ratio increases from 50% to 60%.As percentage of central Government current revenue, total public debt declines from 527% to319% between FY2001 and FY2020. The corresponding ratios for domestic and external debt areprojected to be 121% and 19% and 407% and 300%, respectively. All the ratios are lower for thelow growth scenario. The external debt burden will clearly be increasing substantially if the countrywere to realize the high growth assumptions. A good part of the external borrowing is to fill thebalance of payments deficit, which is likely to increase from 4% of GDP to 13% of GDP. Much ofthe country risk is linked to this aspect of macroeconomic vulnerability.

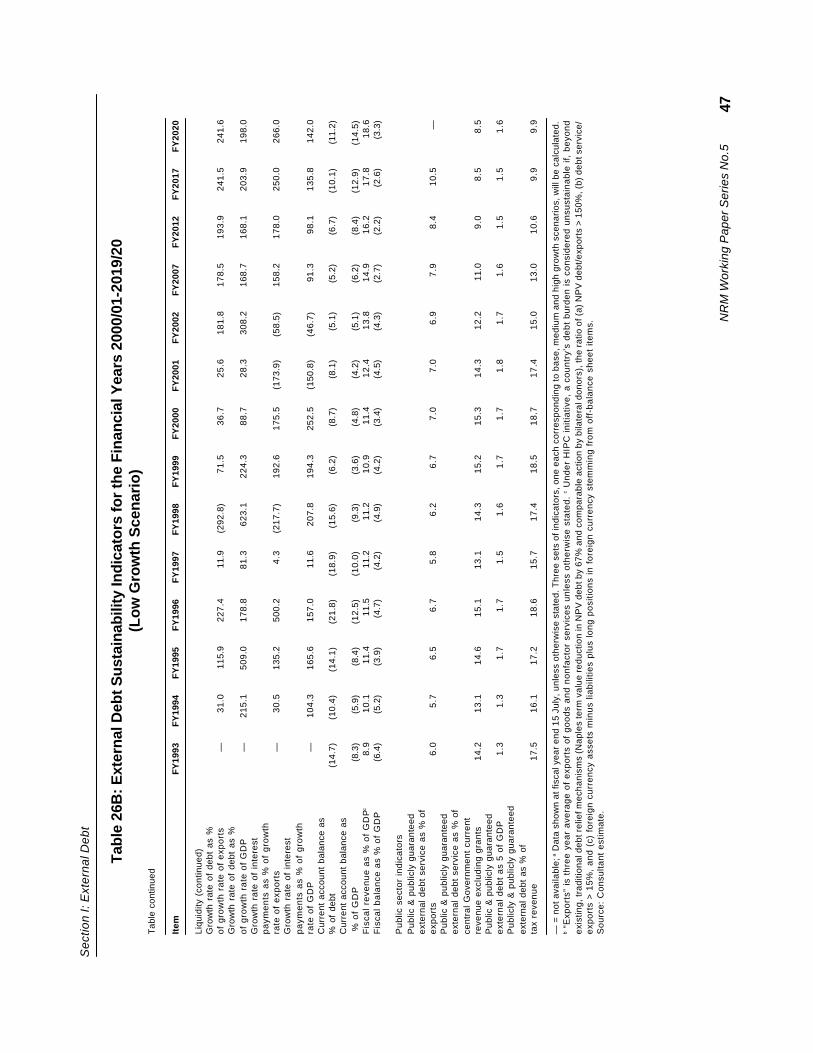

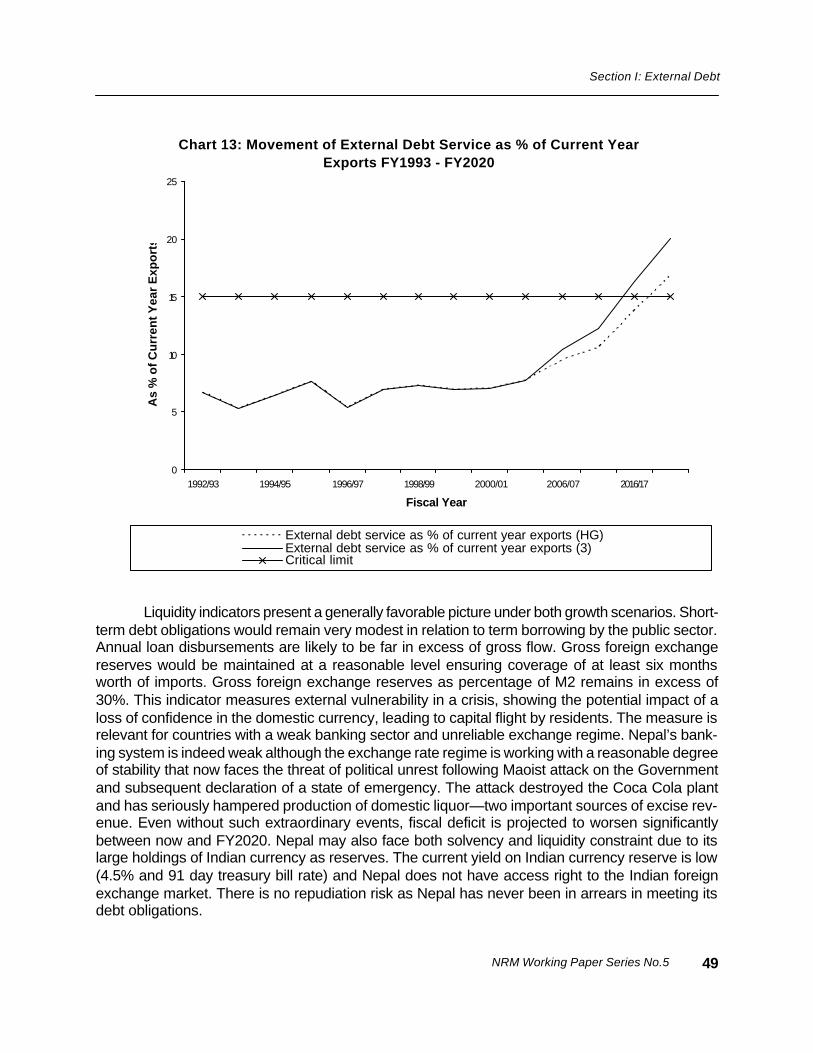

Public debt service burden is projected to decline slightly from 5.3% of GDP and 38.0% ofcentral Government current revenue in FY2002 to 5.1% and 26.0%, respectively, in FY 2020 underthe high growth scenario. In case Nepal is trapped along the low growth path the end year debtratios will be much lower, 3.7% and 20.0%, respectively. The patterns for external and domesticdebt ratios are similar. NPV of total national debt, on the other hand, is projected to increase fromNRs103,584 million in FY2001 to NRs491,189 million in FY2020 under high growth, and NRs318,555under low growth scenario. NPV of both domestic external debts is projected to grow almost fivetimes by FY2020 under high growth scenario, the increase as expected being lower for low growthscenario. Under both scenarios, the projected NPV of external debt as percentage of exportsremain well below the critical level of 150% as defined by the World Bank/International MonetaryFund as the cut off threshold for Heavily Indebted Poor Countries (HIPC). However, the secondrelevant indicator in this context, external debt service as percentage of current year exports isprojected to exceed the cut off value of 15% in FY2020 under both scenarios. Hence, there iscause for concern, caution and surveillance.

Relevant indicators suggest that in the foreseeable future, there is no solvency risk withregard to the external debt burden of Nepal although as mentioned earlier, close monitoring of thedebt service burden in relation to exports would be in order beyond FY2012. The current accountdeficit as percentage of GDP is projected to triple between FY2001 and FY2020 to reach a level of15% under both scenarios. Nepal may also face both solvency and liquidity constraint due to itslarge holdings of Indian currency as reserves. The current yield on Indian currency reserve is low(4.5% and 91 day treasury bill rate), and Nepal does not have access right to the Indian foreignexchange market. There is no repudiation risk as Nepal has never been in arrears in meeting itsdebt obligations. The projected evolution of the fiscal balance of the Government raises seriousquestion about future macroeconomic stability as fiscal deficit worsens as percentage of GDPfrom 4.5% in FY2001 to 7.6% in FY2020 under the high growth scenario. The situation appears

x

more manageable under the low growth scenario as the ratio remains around 3.0% by the endperiod of projection. Total public debt would continue to impose some burden on the Nepaleseeconomy under both scenarios although projections suggest an improvement over time in allrelevant indicators. One area of particular concern is the loan delinquent status of public enterprises.As on July 15, 2001, the total amount of outstanding external loans on-lent to selected publicenterprises was estimated at NRs48,924 million and that on internal loans at NRs502 million.

A number of policy recommendations are made for consideration of the Government ofNepal and ADB: (i) broadly speaking, Nepal should closely monitor the evolution of debt stock, debtservice burden and the development of fiscal and external repayment capacity; (ii) the debt strategyshould seek coordination with monetary and fiscal policies, and adhere to the principles oftransparency, public disclosure, and accountability; (iii) the Government should seek grant andconcessional loans with grant element greater than 35%; (iv) a careful review of non-concessionalloans is in order to determine which could be eliminated or for which a softer term could berenegotiated; (v) Government of Nepal should soon enter into a dialogue with the Government ofIndia to yield and convertibility of its Indian currency reserves; (vi) Nepal should continue to pursuestrong policies to preserve the current macroeconomic stability; (vii) a concerted effort needs to bemade to improve revenue generation so as to generate primary surplus; (viii) public expenditurereview should be an ongoing exercise with special emphasis on the fiscal, foreign exchange, andpoverty impact of all investments; (ix) new external debt should be contracted only if it is consistentwith the Tenth Plan (FY2003–FY2007), the medium term expenditure framework (MTEF), and alonger term perspective plan; (x) export diversification in terms of both commodity composition anddestination (away from India) should be at the top of Government agenda; (xi) existing constraintsto increases in foreign direct investment should be carefully analyzed and countervailing measuresbe put into operation; (xii) the private sector should be promoted and the Government shouldguarantee private sector loans after careful scrutiny of proposed activities; (xiii) the Governmentshould move forward with structural reforms (e.g., the recently legislated land reform), and sectorreforms, especially financial sector reform and good governance; (xiv) in light of the specialrelationship, Nepal should harmonize its own monetary policies with India in order to ensure stabilityof its foreign exchange regime; and (xv) maturity on domestic debt should be increased.

In addition to the above, a number of specific recommendations are made regarding debtmanagement including the CS-DRMS. It is recommended that debt management and debtinformation system management be made the joint responsibility of the MOF, FCGO and the NRB.This would be critical to guarantee the sustainability of the system. MOF will be responsible foroverall strategy and policy articulation, coordination, and implementation, FCGO for external andpublic enterprise debt information system management and timely debt repayment, and NRB formanagement of domestic debt operations, information on domestic debt, private external loans,and foreign exchange rates. The DMU could be renamed as the Debt Policy Management Unit(DPMU) with revised terms of reference. The DPMU will be responsible for assisting MOF ininitiation, articulation, and implementation of future borrowing (domestic and external) policies,and debt management strategies in conjunction with other divisions of MOF, FCGO, NRB andother relevant agencies of the Government of Nepal. It will liaise, in collaboration with FCGO, otherrelevant sections of MOF and NRB, and with the National Planning Commission (NPC) to facilitatepreparation and evaluation of five-year and long-term perspective plans, especially with regard tofinancing development expenditures through domestic and foreign borrowing. The DPMU will alsoassist in assessing debt-financing requirement underlying annual development plans and annual

xi

budgets. Another responsibility of the unit would be preparation and dissemination of reports,electronic and otherwise, and in this context, developing, maintaining, and updating of a CS-DRMSwebsite in collaboration with FCGO.

It is expected that the Government will allocate necessary budgetary resources for thepurpose. The Government of Nepal should mobilize technical and financial assistance of externaldonors, which need to be used for upgrading and enhancement of the system, including local andwider area networking, website development, system security, integration of different databasemanagement systems, and staff development. Alternatives to the current system of networkingthrough dedicated telephone lines should be revisited at an appropriate time to effect changeoverto a more efficient, speedy, and reliable networking system. It is paramount to avoid data duplicationin the future thereby allowing the maintenance of a secure and unique set of data on domestic andexternal debt. Steps need to be taken to (i) assign specific staff to CS-DRMS; (ii) ensure regularinputting of data; (iii) ensure compatibility of hardware and software configuration in different locations;(iv) homogenize logistic support; (v) induce demand for outputs of the system and online use; (vi)follow a specific timeline for implementation of all steps agreed upon; (vii) promote staff development;(viii) as given below, ensure (ix) complete system security including eliminating the risk of datamanipulation by unauthorized persons; (x) inculcate a sense of ownership among all principalactors, especially MOF, FCGO and NRB; and finally, (xi) maintain only two data entry points, namely,FCGO (external debt), and NRB (domestic debt, foreign exchange rates and private loans).

FCGO should be the focal point for (i) coordination and management of the debt informationmanagement system; (ii) inputting, editing, validation, and reconciliation of data on external andpublic enterprise debt; (iii) reconciliation of external debt data with records of lenders; (iv)reconciliation of public enterprise debt data with records of these enterprises; (v) databasemanagement; (vi) linking up of CS-DRMS with the Financial Management Project, Medium-TermBudget Framework Project, and the domestic debt database of NRB, to allow interactive dialoguebetween systems; (vii) provision of guidance to and coordination of data integration and systemcompatibility; (viii) CS-DRMS network, hardware and software system maintenance, upgrading,backup and security which will include procurement, testing and operationalization of new releasesof CS-DRMS software, other software and new equipment; (ix) staff development; and (x)preparation and dissemination of periodic reports as appropriate.

NRB, on the other hand, should be responsible for (i) management of information ondomestic debt, private external debt and foreign exchange rates; (ii) inputting, editing, validation,and reconciliation of data on public domestic debt; (iii) management of domestic debt database ofthe CS-DRMS; (iv) monitoring of domestic debt situation; (v) formulation and operationalization ofpublic domestic debt strategies and policies, and advising MOF on internal borrowing; and (vi)preparation and dissemination of periodic reports on public domestic debt.

The implications for ADB operations are the following: (i) Given its large portfolio, ADBshould carefully review its future exposure; (ii) Greater emphasis should be given to capacitybuilding and improvement of governance, transparency, and accountability at all levels; (iii) Theperformance of the portfolios need to be closely monitored with regard to impact on productivity,export growth and diversification, and alleviation of poverty; (iv) Internally, ADB should strengthenits country economic work, particularly macroeconomic modeling; (v) ADB should consider extending

xii

technical assistance to the Government of Nepal for institution building regarding debt policymanagement and debt information system management; (vi) Related to (iv) and (v), ADB shouldconsider support for analytic work linked to the development of a consistent macroeconomicframework, bringing together Financial Management Project, medium term expenditure framework,five-year plans, perspective plans, the budget exercise, as well as debt; (vii) ADB should assist theborrower to improve disbursement and maintain positive net aid flow; (viii) ADB should review itsmix of lending instruments in order to develop packages consistent with the long term repaymentcapacity of member developing countries; (ix) Requests for additional financing should be consideredfavorably if the situation warrants it; (x) ADB should support the development of the capital market,especially the secondary market, for domestic debt instruments; (xi) ADB should continue itssupport for financial sector reform, public enterprise reform, governance reform, and the TenthPlan (FY2003–FY2007); (xii) Commensurate with its status as the lead donor institution in thecountry, ADB should take the lead at donor coordination relating to resource management, database management, and all related analytic work; (xiii) ADB needs to improve its disbursementstatement formats sent to borrowers; and finally, (xiv) The currency composition of loan,disbursement and repayment should be carefully orchestrated to provide maximum flexibility tothe borrower to meet debt obligations without unnecessary stress.

xiii

I. EXTERNAL DEBT

A. Review of Current External Debt Situation

1. Introduction

Nepal has launched preparatory work on the Tenth Five Year Plan, covering fiscal year(FY)2003–FY2007 with technical assistance from the Asian Development Bank (ADB).ADB plan fielded an inception mission for the Tenth Plan exercise during 23 September–3

November 2001. Public debt, domestic and foreign, has played an important role in financingoverall budget deficit and public development expenditures. Of the two, foreign financing has beenpredominant. Foreign financing has also been crucial in financing balance of payments deficit.Given the lackluster performance of the economy over the first four years of the Ninth Five YearPlan (FY1997–FY2002), a significantly higher level of effort will be required to mobilize and efficientlyutilize domestic and foreign resources in order to achieve the Ninth Plan (FY1997–FY2002) targetof an average annual growth rate of real gross domestic product (GDP) of 6% and maintain themomentum over the Tenth Plan (FY2003–FY2007).

Given the narrow base for domestic resource mobilization and exports, it is important tocontinuously monitor the sustainability of public debt of Nepal—that is, the country’s ability to meetits medium and long-term debt obligations. The three key determinants of long-term debtsustainability are (i) the existing stock of debt and its repayment terms; (ii) the development offiscal and external repayment capacity which is linked to economic growth, exports, and fiscalrevenues; and (iii) the availability and concessionality of new external financing (growth, mix ofgrants and loans, and terms). Debt sustainability depends on formulation and implementation of acomprehensive set of macroeconomic and sectoral policies geared towards efficient mobilizationand utilization of resources including borrowed resources (domestic and external), achievingsustainable economic growth with poverty reduction, and sound debt management. The latterwould require periodic analysis of the debt situation, finance for development (access to adequateconcessional flows), and the state of debt sustainability, together with an efficient organization fordebt management and an effective debt information system.

In Nepal, debt management is the responsibility of the Ministry of Finance (MOF) and NepalRastra Bank (NRB). A Debt Management Unit (DMU) under the Foreign Aid Coordination Divisionof the MOF is responsible for recording loan details and monitoring payments. The FinancialComptroller General’s Office (FCGO) records actual disbursements and authorizes payment onloans. External funds are received and foreign payments are made through NRB which recordsand monitors private sector loans and domestic debt instruments. The DMU received technicalassistance grant support from the Department for International Development (DFID) of the UnitedKingdom. The Commonwealth Secretariat Debt Recording and Management System (CS-DRMS)was installed at the DMU with proposed extensions to FCGO and NRB. The CS-DRMS is acomprehensive database management system, which can carry out useful debt analysis andprovide a wide rage of reports. The challenge is how to ensure sustainability of the system interms of maintenance and updating of hardware and software and debt data. At present,

October 2005

Nepal Public Debt Sustainability Analysis

debt data has been inputted up to March 2000. The data has to be updated continuously to makeanalysis meaningful and to articulate sound debt management strategies and policies. The DMUand the CS-DRMS are confronted with certain institutional and logistic problems, which need to beaddressed. Otherwise, data updating, analysis, report production and policy formulation will beproblematic. The actual task of inputting new debt information since March 2000 will have to beaccomplished within the context of the proposed study.

Against this backdrop, Dr. Mohiuddin Alamgir, an ADB staff consultant and Sungsup Ra,Economist, Programs West 1, undertook an analysis of public debt sustainability of Nepal in orderto improve debt management by the Government of Nepal, provide inputs for the Tenth Plan(FY2003–FY2007) and assist ADB articulate its lending policy for Nepal based on country riskanalysis. More specifically, objectives of debt sustainability analysis include (i) providing inputsregarding requirements for borrowing, domestic and foreign, for the Tenth Plan; (ii) improvingpublic debt management, including public domestic debt; (iii) making recommendations forGovernment borrowing policies; (iv) linking debt management policies to macroeconomic policies;(v) assessing the CS-DRMS and making recommendations for its sustainability; and (vi) improvingcountry risk management for ADB operation in Nepal.

2. Recent Economic Performance and Trends

Nepal is one of the poorest countries of the region with an estimated gross national product(GNP) per capita of $250 in FY2000. It is estimated that in 1996, 42% of the population lived belowthe poverty line of $77 per capita per annum. The Ninth Plan (FY1997–FY2002) envisioned anaverage annual growth rate of GDP of 6.0%, but this goal remained elusive as it was reached onlyin FY2000. The performance over the first four years was mixed (3.3% in FY1998, 4.4% in FY1999and 6.4% in FY2000 and estimated to have dropped to 5.7% in FY2001). FY2002 is shaping up tobe a difficult year in the aftermath of the Maoist insurrection, slow down of the global economy andthe impact of the September 11, 2001 attack on the World Trade Center in New York, adverselyaffecting Nepal’s income from tourism, industrial production, revenue collection, and traditionalexports like garments, carpet, and handicrafts. The relatively poor performance of the economyover the Ninth Plan period was a major reason for non-attainment of the poverty reduction objectiveof the plan, from 42% to 32%. On the contrary, according to some estimates, the percentage ofpopulation living below the poverty line has increased to 51% during the first three years of theNinth Plan period (FY1997–FY2002). Nepal would have to raise real GDP growth rate substantiallyover coming years, thus creating a solid foundation for the forthcoming Tenth Plan (FY2003–FY2007), and the subsequent plans. This in turn can only happen if the rate of investment is raisedwell above the recent trend of 22% of GDP at market prices. With domestic savings stagnantaround 16% of GDP in late 1990s—gross national saving is higher by 1–3% of GDP—the futuregrowth and poverty reduction prospect depends heavily on mobilization and efficient utilization ofboth domestic and external resources.

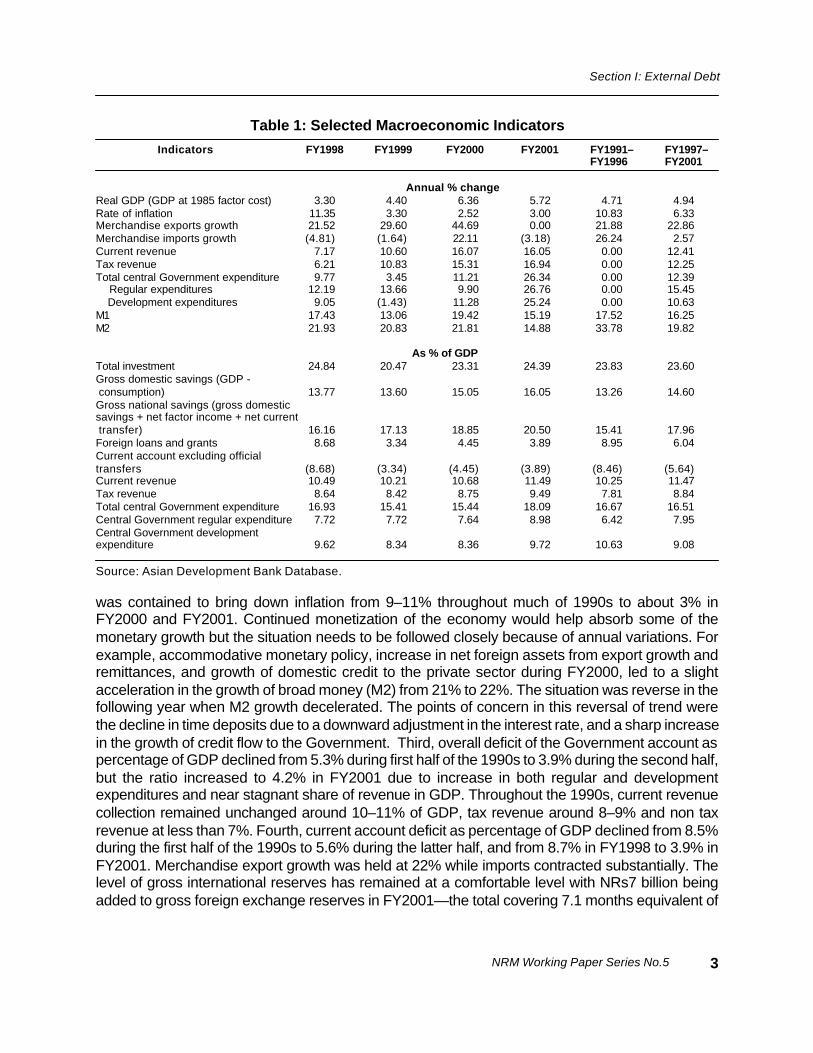

Other aspects of macroeconomic management raise several issues, both positive andnegative (Table 1). First, many macroeconomic variables and parameters showed stability orimprovement between FY1992–FY1996 and FY1997–FY2001 periods, but there were some negativesigns over the past two years. Second, growth of monetary aggregatesand the overall budget

2

NRM Working Paper Series No.5

Section I: External Debt

was contained to bring down inflation from 9–11% throughout much of 1990s to about 3% inFY2000 and FY2001. Continued monetization of the economy would help absorb some of themonetary growth but the situation needs to be followed closely because of annual variations. Forexample, accommodative monetary policy, increase in net foreign assets from export growth andremittances, and growth of domestic credit to the private sector during FY2000, led to a slightacceleration in the growth of broad money (M2) from 21% to 22%. The situation was reverse in thefollowing year when M2 growth decelerated. The points of concern in this reversal of trend werethe decline in time deposits due to a downward adjustment in the interest rate, and a sharp increasein the growth of credit flow to the Government. Third, overall deficit of the Government account aspercentage of GDP declined from 5.3% during first half of the 1990s to 3.9% during the second half,but the ratio increased to 4.2% in FY2001 due to increase in both regular and developmentexpenditures and near stagnant share of revenue in GDP. Throughout the 1990s, current revenuecollection remained unchanged around 10–11% of GDP, tax revenue around 8–9% and non taxrevenue at less than 7%. Fourth, current account deficit as percentage of GDP declined from 8.5%during the first half of the 1990s to 5.6% during the latter half, and from 8.7% in FY1998 to 3.9% inFY2001. Merchandise export growth was held at 22% while imports contracted substantially. Thelevel of gross international reserves has remained at a comfortable level with NRs7 billion beingadded to gross foreign exchange reserves in FY2001—the total covering 7.1 months equivalent of

Table 1: Selected Macroeconomic Indicators

Indicators FY1998 FY1999 FY2000 FY2001 FY1991– FY1997– FY1996 FY2001

Annual % changeReal GDP (GDP at 1985 factor cost) 3.30 4.40 6.36 5.72 4.71 4.94Rate of inflation 11.35 3.30 2.52 3.00 10.83 6.33Merchandise exports growth 21.52 29.60 44.69 0.00 21.88 22.86Merchandise imports growth (4.81) (1.64) 22.11 (3.18) 26.24 2.57Current revenue 7.17 10.60 16.07 16.05 0.00 12.41Tax revenue 6.21 10.83 15.31 16.94 0.00 12.25Total central Government expenditure 9.77 3.45 11.21 26.34 0.00 12.39 Regular expenditures 12.19 13.66 9.90 26.76 0.00 15.45 Development expenditures 9.05 (1.43) 11.28 25.24 0.00 10.63M1 17.43 13.06 19.42 15.19 17.52 16.25M2 21.93 20.83 21.81 14.88 33.78 19.82

As % of GDPTotal investment 24.84 20.47 23.31 24.39 23.83 23.60Gross domestic savings (GDP - consumption) 13.77 13.60 15.05 16.05 13.26 14.60Gross national savings (gross domesticsavings + net factor income + net current transfer) 16.16 17.13 18.85 20.50 15.41 17.96Foreign loans and grants 8.68 3.34 4.45 3.89 8.95 6.04Current account excluding officialtransfers (8.68) (3.34) (4.45) (3.89) (8.46) (5.64)Current revenue 10.49 10.21 10.68 11.49 10.25 11.47Tax revenue 8.64 8.42 8.75 9.49 7.81 8.84Total central Government expenditure 16.93 15.41 15.44 18.09 16.67 16.51Central Government regular expenditure 7.72 7.72 7.64 8.98 6.42 7.95Central Government developmentexpenditure 9.62 8.34 8.36 9.72 10.63 9.08

Source: Asian Development Bank Database.

3

October 2005

Nepal Public Debt Sustainability Analysis

imports. However, there are signs of weakening of commodity exports, and income from tourismand remittances, the latter due to movement of some Nepalese overseas workers from the Gulfcountries to Malaysia, which is a relatively lower wage country. Fifth, the level of external debt anddebt service burden have remained reasonable throughout the period—disbursed outstanding debt(DOD) 51.8% of GDP, and debt service 7.0 % of exports in FY2001—the only concern being matchingforeign debt repayment obligations in foreign currency with foreign exchange receipts given a largeshare of export receipts in Indian rupees. However, the fiscal burden of debt service, domestic andforeign is high (total service burden 47.0% of current revenue in FY2001).

3. Overview of External Debt Position

Nepal’s external debt and external debt burden is manageable. According to a World Bankclassification, Nepal is a less indebted country.1 The size of DOD increased more than two foldbetween FY1993 and FY2001. Annual gross disbursement averaged about NRs17,592 million($231 million at the exchange rate end October 2001) and net disbursement NRs10,438 million($137 million). Most external borrowing is done by the central Government. Private share was lessthan 2%. Loans contracted are primarily long-term. Short-term debt plays a small part in the total.Long-term debts are held by public authorities or are guaranteed by them. In Nepal, public enterprisescan receive external loans only through an on-lending arrangement with the Government underwhich the external creditor offer the loan credit to the Government which in turn lends it to publicenterprises. The contractual agreement for external debt servicing is between the Governmentand the creditor.

Over past years, the share of multilateral creditors remained in excess of 80% while thebilateral share declined. The World Bank and the ADB accounted for over three fourth of multilaterallending to Nepal. Among bilateral creditors, major players included the Governments of Japan andFrance. Most debts were contracted on concessional terms (grant element less than 35%).However, 119 loans out of 323 reviewed were contracted on non-concessional terms. Loans werealmost all in foreign currency, of which special drawing rights (SDR) accounted for about 70%.According to the most widely used debt sustainability indicators like net present value (NPV) aspercentage of exports (three year average), or debt service as percentage of current year exports,Nepal is well below critical levels.

4. Nepal’s External Debt during the 1990s

a. Level of External Debt

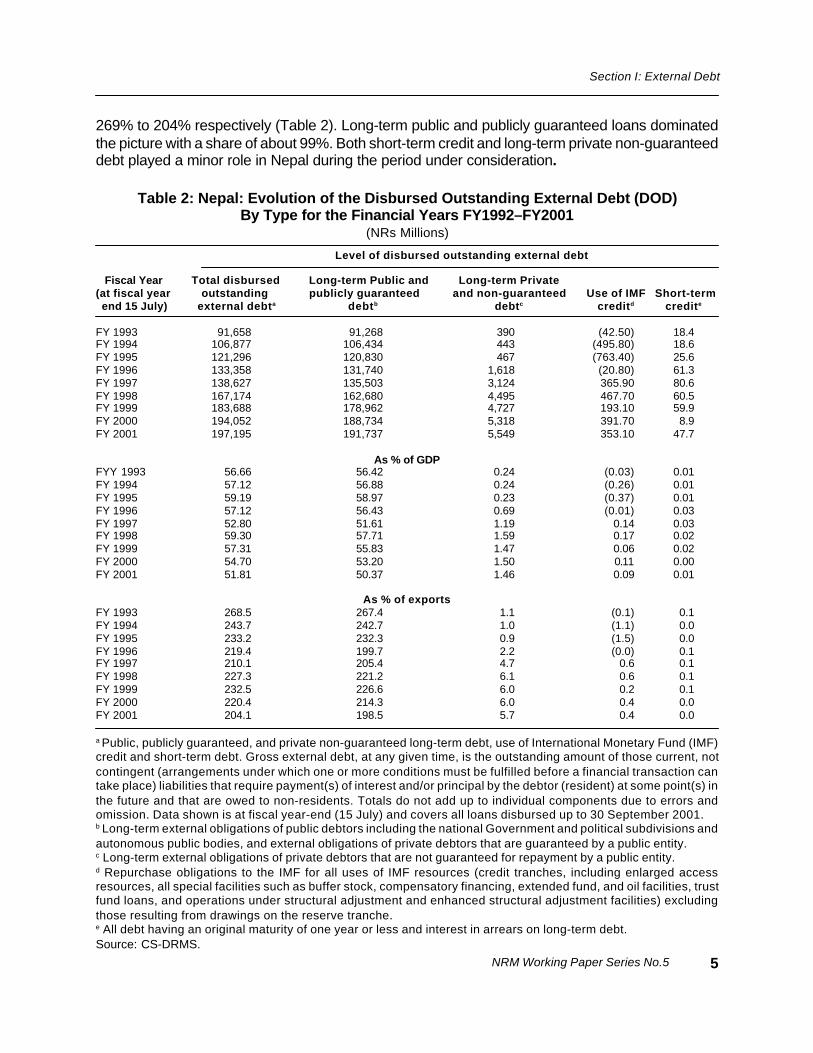

The level of external debt was modest and critical ratios improved. Nepal’s external debtstood at NRs197,195 million (approximately $2.6 billion at the exchange rate of end October 2001)as at 30 September 2001. This represented a 115% increase over the level of FY1993. However,total debt as percentage GDP and exports declined over this period, from 57% to 52% and from

1 According to the World Bank’s World Development Indicators 2001, in 1999, countries with a present value of debtservice greater than 220% of exports or 80% of gross national income were classified as severely indebted (S);countries that were not severely indebted but whose present value of debt service exceeded 132% of exports or48% of gross national income were classified as moderately indebted (M); and countries that did not fall into theabove two groups were classified as less indebted (L).

4

NRM Working Paper Series No.5

Section I: External Debt

269% to 204% respectively (Table 2). Long-term public and publicly guaranteed loans dominatedthe picture with a share of about 99%. Both short-term credit and long-term private non-guaranteeddebt played a minor role in Nepal during the period under consideration.

5

a Public, publicly guaranteed, and private non-guaranteed long-term debt, use of International Monetary Fund (IMF)credit and short-term debt. Gross external debt, at any given time, is the outstanding amount of those current, notcontingent (arrangements under which one or more conditions must be fulfilled before a financial transaction cantake place) liabilities that require payment(s) of interest and/or principal by the debtor (resident) at some point(s) inthe future and that are owed to non-residents. Totals do not add up to individual components due to errors andomission. Data shown is at fiscal year-end (15 July) and covers all loans disbursed up to 30 September 2001.b Long-term external obligations of public debtors including the national Government and political subdivisions andautonomous public bodies, and external obligations of private debtors that are guaranteed by a public entity.c Long-term external obligations of private debtors that are not guaranteed for repayment by a public entity.d Repurchase obligations to the IMF for all uses of IMF resources (credit tranches, including enlarged accessresources, all special facilities such as buffer stock, compensatory financing, extended fund, and oil facilities, trustfund loans, and operations under structural adjustment and enhanced structural adjustment facilities) excludingthose resulting from drawings on the reserve tranche.e All debt having an original maturity of one year or less and interest in arrears on long-term debt.Source: CS-DRMS.

Table 2: Nepal: Evolution of the Disbursed Outstanding External Debt (DOD)By Type for the Financial Years FY1992–FY2001

(NRs Millions)

Level of disbursed outstanding external debt

Fiscal Year Total disbursed Long-term Public and Long-term Private(at fiscal year outstanding publicly guaranteed and non-guaranteed Use of IMF Short-term end 15 July) external debta debtb debtc creditd credite

FY 1993 91,658 91,268 390 (42.50) 18.4FY 1994 106,877 106,434 443 (495.80) 18.6FY 1995 121,296 120,830 467 (763.40) 25.6FY 1996 133,358 131,740 1,618 (20.80) 61.3FY 1997 138,627 135,503 3,124 365.90 80.6FY 1998 167,174 162,680 4,495 467.70 60.5FY 1999 183,688 178,962 4,727 193.10 59.9FY 2000 194,052 188,734 5,318 391.70 8.9FY 2001 197,195 191,737 5,549 353.10 47.7

As % of GDPFYY 1993 56.66 56.42 0.24 (0.03) 0.01FY 1994 57.12 56.88 0.24 (0.26) 0.01FY 1995 59.19 58.97 0.23 (0.37) 0.01FY 1996 57.12 56.43 0.69 (0.01) 0.03FY 1997 52.80 51.61 1.19 0.14 0.03FY 1998 59.30 57.71 1.59 0.17 0.02FY 1999 57.31 55.83 1.47 0.06 0.02FY 2000 54.70 53.20 1.50 0.11 0.00FY 2001 51.81 50.37 1.46 0.09 0.01

As % of exportsFY 1993 268.5 267.4 1.1 (0.1) 0.1FY 1994 243.7 242.7 1.0 (1.1) 0.0FY 1995 233.2 232.3 0.9 (1.5) 0.0FY 1996 219.4 199.7 2.2 (0.0) 0.1FY 1997 210.1 205.4 4.7 0.6 0.1FY 1998 227.3 221.2 6.1 0.6 0.1FY 1999 232.5 226.6 6.0 0.2 0.1FY 2000 220.4 214.3 6.0 0.4 0.0FY 2001 204.1 198.5 5.7 0.4 0.0

October 2005

Nepal Public Debt Sustainability Analysis

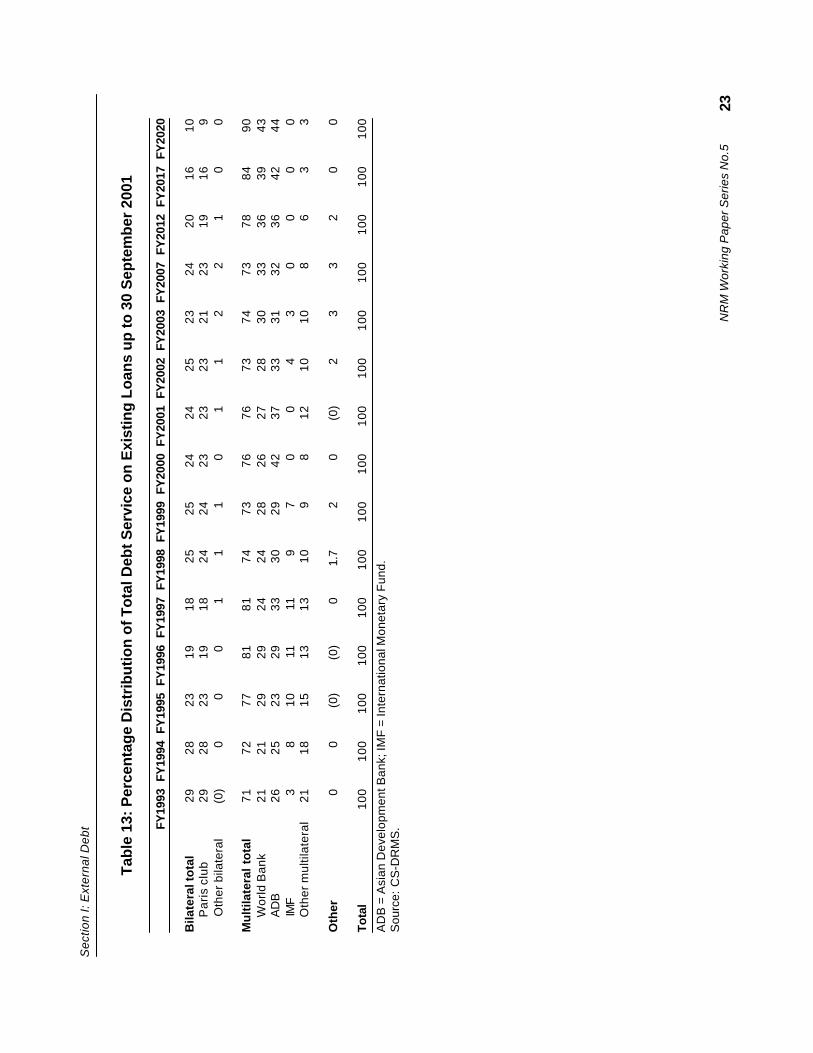

b. Creditor Composition of External Debt

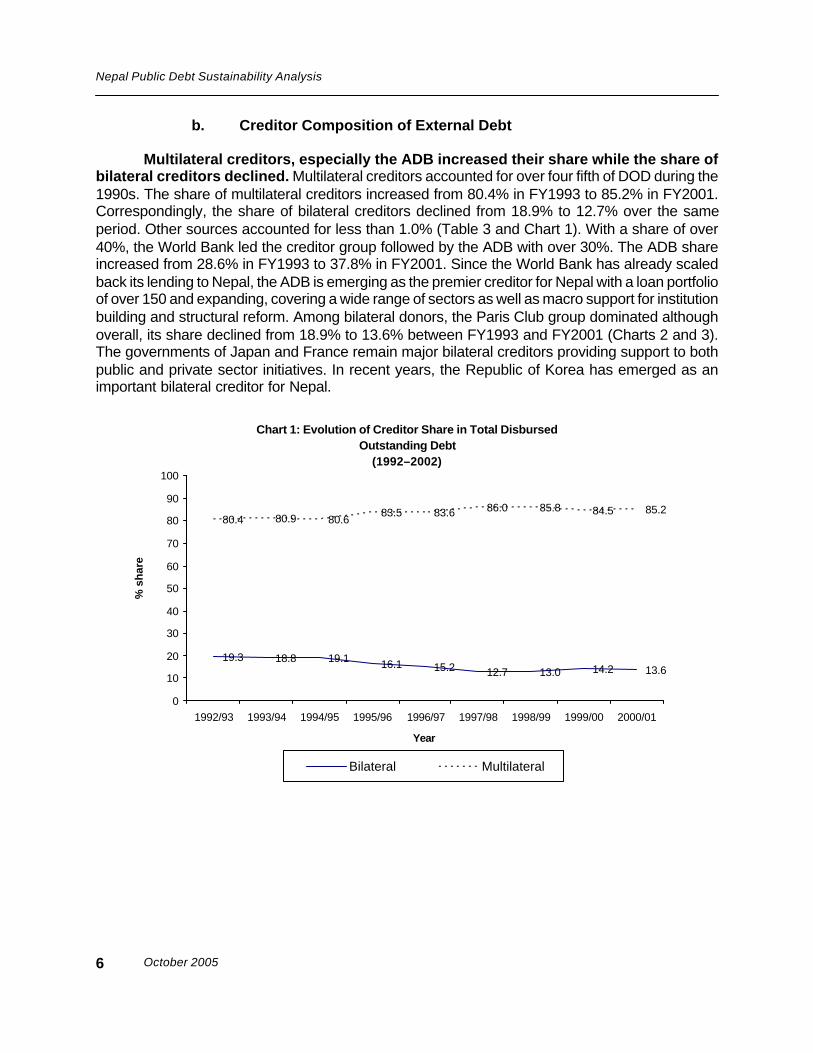

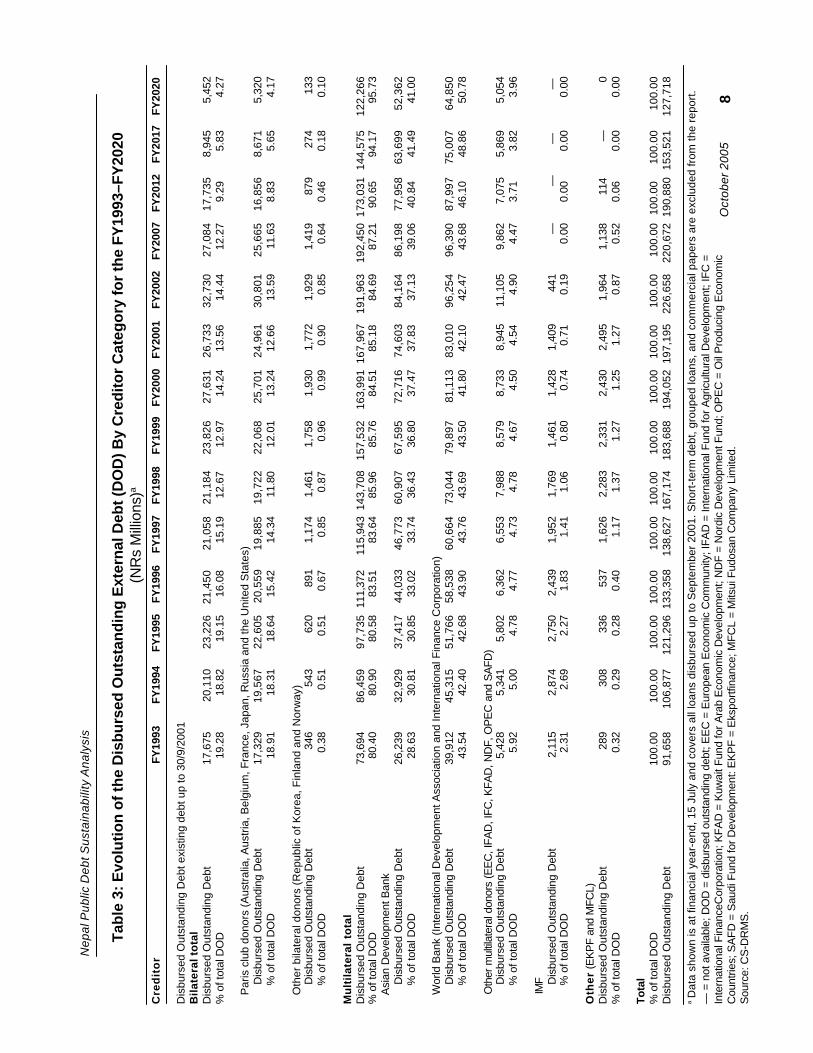

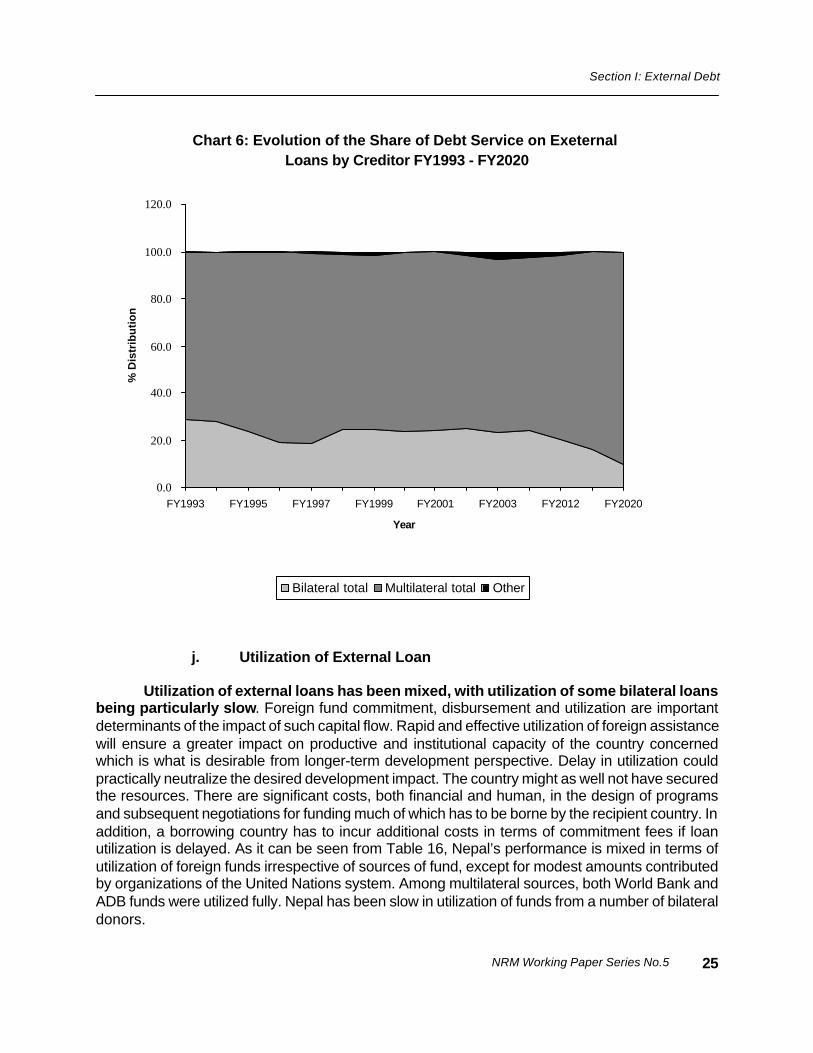

Multilateral creditors, especially the ADB increased their share while the share ofbilateral creditors declined. Multilateral creditors accounted for over four fifth of DOD during the1990s. The share of multilateral creditors increased from 80.4% in FY1993 to 85.2% in FY2001.Correspondingly, the share of bilateral creditors declined from 18.9% to 12.7% over the sameperiod. Other sources accounted for less than 1.0% (Table 3 and Chart 1). With a share of over40%, the World Bank led the creditor group followed by the ADB with over 30%. The ADB shareincreased from 28.6% in FY1993 to 37.8% in FY2001. Since the World Bank has already scaledback its lending to Nepal, the ADB is emerging as the premier creditor for Nepal with a loan portfolioof over 150 and expanding, covering a wide range of sectors as well as macro support for institutionbuilding and structural reform. Among bilateral donors, the Paris Club group dominated althoughoverall, its share declined from 18.9% to 13.6% between FY1993 and FY2001 (Charts 2 and 3).The governments of Japan and France remain major bilateral creditors providing support to bothpublic and private sector initiatives. In recent years, the Republic of Korea has emerged as animportant bilateral creditor for Nepal.

Chart 1: Evolution of Creditor Share in Total Disbursed Outstanding Debt

(1992–2002)

19.3 18.8 19.1 16.1 15.2 12.7 13.0 14.2 13.6

80.4 80.9 80.683.5 83.6 86.0 85.8 84.5 85.2

0

10

20

30

40

50

60

70

80

90

100

1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01

Year

% s

har

e

Bilateral Multilateral

6

NRM Working Paper Series No.5

Section I: External Debt

Chart 2: Percentage Share of Individual Creditors in Total Disbursed OutstandingDebt (1993)

7

Chart 3: Percentage Distribution of Creditor Share in Total Disbursed OutstandingExternal Loans

World Bank, 44%

Asian Development Bank, 29%

Paris Club, 19%

International Monetary Fund,

2%

Other Multilateral, 6%

Other Bilateral, 0%

World Bank41%

Other multilateral5%

ADB 38%

Other bilateral1%

Paris club13%Other 1%

IMF 1%

Oct

ober

200

5

Nep

al P

ublic

Deb

t Sus

tain

abili

ty A

naly

sis

Cre

dit

or

FY19

93FY

1994

FY19

95FY

1996

FY19

97FY

1998

FY19

99FY

2000

FY20

01FY

2002

FY20

07FY

2012

FY20

17FY

2020

Dis

burs

ed O

utst

andi

ng D

ebt e

xist

ing

debt

up

to 3

0/9/

2001

Bila

tera

l to

tal

Dis

burs

ed O

utst

andi

ng D

ebt

17,

675

20,1

1023

,226

21,4

5021

,058

2

1,18

4

23,

826

2

7,63

1

26,7

33

32,

730

2

7,08

4

17,7

35

8,

945

5,45

2%

of t

otal

DO

D19

.28

18.8

219

.15

16.0

815

.19

12.6

712

.97

14.2

413

.56

14.4

412

.27

9.29

5.83

4.27

P

aris

clu

b do

nors

(A

ustr

alia

, Aus

tria

, Bel

gium

, Fra

nce,

Jap

an, R

ussi

a an

d th

e U

nite

d S

tate

s)

D

isbu

rsed

Out

stan

ding

Deb

t

1

7,32

9

19,

567

2

2,60

5

20,5

59

19,

885

19

,722

2

2,06

8

25,

701

24

,961

3

0,80

1

25,

665

16

,856

8,67

1

5,

320

% o

f tot

al D

OD

18.9

118

.31

18.6

415

.42

14.3

411

.80

12.0

113

.24

12.6

613

.59

11.6

38.

835.

654.

17

O

ther

bila

tera

l don

ors

(Rep

ublic

of K

orea

, Fin

land

and

Nor

way

)

D

isbu

rsed

Out

stan

ding

Deb

t

34

6

543

62

0

8

91

1,

174

1

,461

1,75

8

1,

930

1

,772

1,92

9

1,

419

879

27

4

133

% o

f tot

al D

OD

0.38

0.51

0.51

0.67

0.85

0.87

0.96

0.99

0.90

0.85

0.64

0.46

0.18

0.10

Mu

ltil

ater

al t

ota

lD

isbu

rsed

Out

stan

ding

Deb

t

7

3,69

4

86,

459

9

7,73

5 1

11,3

72 1

15,9

43 1

43,7

08 1

57,5

32 1

63,9

91 1

67,9

67 1

91,9

63 1

92,4

50 1

73,0

31 1

44,5

75 1

22,2

66%

of t

otal

DO

D80

.40

80.9

080

.58

83.5

183

.64

85.9

685

.76

84.5

185

.18

84.6

987

.21

90.6

594

.17

95.7

3

Asi

an D

evel

opm

ent B

ank

Dis

burs

ed O

utst

andi

ng D

ebt

26,

239

3

2,92

9

37,

417

44

,033

4

6,77

3

60,9

07

67,

595

7

2,71

6

74,6

03

84,

164

8

6,19

8

77,9

58

63,

699

5

2,36

2

%

of t

otal

DO

D28

.63

30.8

130

.85

33.0

233

.74

36.4

336

.80

37.4

737

.83

37.1

339

.06

40.8

441

.49

41.0

0

W

orld

Ban

k (In

tern

atio

nal D

evel

opm

ent A

ssoc

iatio

n an

d In

tern

atio

nal F

inan

ce C

orpo

ratio

n)

D

isbu

rsed

Out

stan

ding

Deb

t

3

9,91

2

45,

315

5

1,76

6

58,5

38

60,

664

73

,044

7

9,89

7

81,

113

83

,010

9

6,25

4

96,

390

87

,997

7

5,00

7

64,

850

% o

f tot

al D

OD

43.5

442

.40

42.6

843

.90

43.7

643

.69

43.5

041

.80

42.1

042

.47

43.6

846

.10

48.8

650

.78

O

ther

mul

tilat

eral

don

ors

(EE

C, I

FAD

, IFC

, KFA

D, N

DF,

OP

EC

and

SA

FD)

Dis

burs

ed O

utst

andi

ng D

ebt

5,

428

5,34

1

5,

802

6

,362

6,55

3

7,9

88

8,

579

8,73

3

8,9

45

11,

105

9,86

2

7,0

75

5,

869

5,05

4

%

of t

otal

DO

D5.

925.

004.

784.

774.

734.

784.

674.

504.

544.

904.

473.

713.

823.

96

IM

F

D

isbu

rsed

Out

stan

ding

Deb

t

2,11

5

2,

874

2,75

0

2,4

39

1,

952

1

,769

1,46

1

1,

428

1

,409

44

1

—

—

—

—

% o

f tot

al D

OD

2.31

2.69

2.27

1.83

1.41

1.06

0.80

0.74

0.71

0.19

0.00

0.00

0.00

0.00

Oth

er (E

KP

F an

d M

FCL)

Dis

burs

ed O

utst

andi

ng D

ebt

289

30

8

336

537

1,62

6

2,2

83

2,

331

2,43

0

2,4

95

1,

964

1,13

8

1

14

—

0%

of t

otal

DO

D0.

320.

290.

280.

401.

171.

371.

271.

251.

270.

870.

520.

060.

000.

00

Tota

l%

of t

otal

DO

D10

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

00D

isbu

rsed

Out

stan

ding

Deb

t91

,658

106

,877

121

,296

133

,358

138

,627

167

,174

183

,688

194

,052

197

,195

226

,658

220

,672

190

,880

153

,521

127

,718

a Dat

a sh

own

is a

t fin

anci

al y

ear-

end,

15

July

and

cov

ers

all l

oans

dis

burs

ed u

p to

Sep

tem

ber

2001

. Sho

rt-t

erm

deb

t, gr

oupe

d lo

ans,

and

com

mer

cial

pap

ers

are

excl

uded

from

the

repo

rt.

Tab

le 3

: Evo

luti

on

of t

he

Dis

bu

rsed

Ou

tsta

nd

ing

Ext

ern

al D

ebt (

DO

D) B

y C

red

ito

r C

ateg

ory

for

the

FY

1993

–FY

2020

(NR

s M

illio

ns)a

— =

not

ava

ilabl

e; D

OD

= d

isbu

rsed

out

stan

ding

deb

t; E

EC

= E

urop

ean

Eco

nom

ic C

omm

unity

; IFA

D =

Inte

rnat

iona

l Fun

d fo

r Agr

icul

tura

l Dev

elop

men

t; IF

C =

Inte

rnat

iona

l Fin

ance

Cor

pora

tion;

KFA

D =

Kuw

ait F

und

for A

rab

Eco

nom

ic D

evel

opm

ent;

ND

F =

Nor

dic

Dev

elop

men

t Fun

d; O

PE

C =

Oil

Pro

duci

ng E

cono

mic

Cou

ntrie

s; S

AFD

= S

audi

Fun

d fo

r Dev

elop

men

t: E

KP

F =

Eks

portf

inan

ce; M

FCL

= M

itsui

Fud

osan

Com

pany

Lim

ited.

Sou

rce:

CS

-DR

MS

.

8

NRM Working Paper Series No.5

Section I: External Debt

c. The Debtor Composition of External Debt

The central Government dominated the borrower category but the private sectorincreased its share from a very modest level. The central Government is the principal borroweraccounting for over 95% of DOD. There had been a slight shift in favor of the private sector. Thecentral Government share in total DOD declined from 99.0% in FY1993 to 97.8% in FY2003 whileprivate borrowing increased from less than 1% to close to 3% (Table 4). Private sector borrowinghad been influenced by growth of hotel and other industries, Government’s economic liberalizationpolicy, and willingness of some lenders to provide suppliers/export credit without Governmentguarantee. However, the amount involved is still small to make much of an impact on foreigncapital flow or to have a measurable economic impact. Emerging economic difficulties would slowdown external capital flow to the private sector.

d. External Debt by Guarantee Status

The bulk of foreign loans are guaranteed by the central Government. In FY1993,99% of all loans were guaranteed by the central Government. The guaranteed loans were primarilycontracted by the central Government itself. The amount of private loans guaranteed by theGovernment was very modest and over time such guarantee declined sharply. On the other handprivate borrowing without Government increased between FY1993 and FY2001 from 0.4% to 2.8%though the absolute amount was modest (Table 5). Thus there was some opening of the internationalcapital market to Nepalese entrepreneurs. The future trend will depend on the pace and effectivenessof implementation of economic reform and liberalization process and on the availability of profitableinvestment opportunities in the country.

e. Currency Composition of External Debt

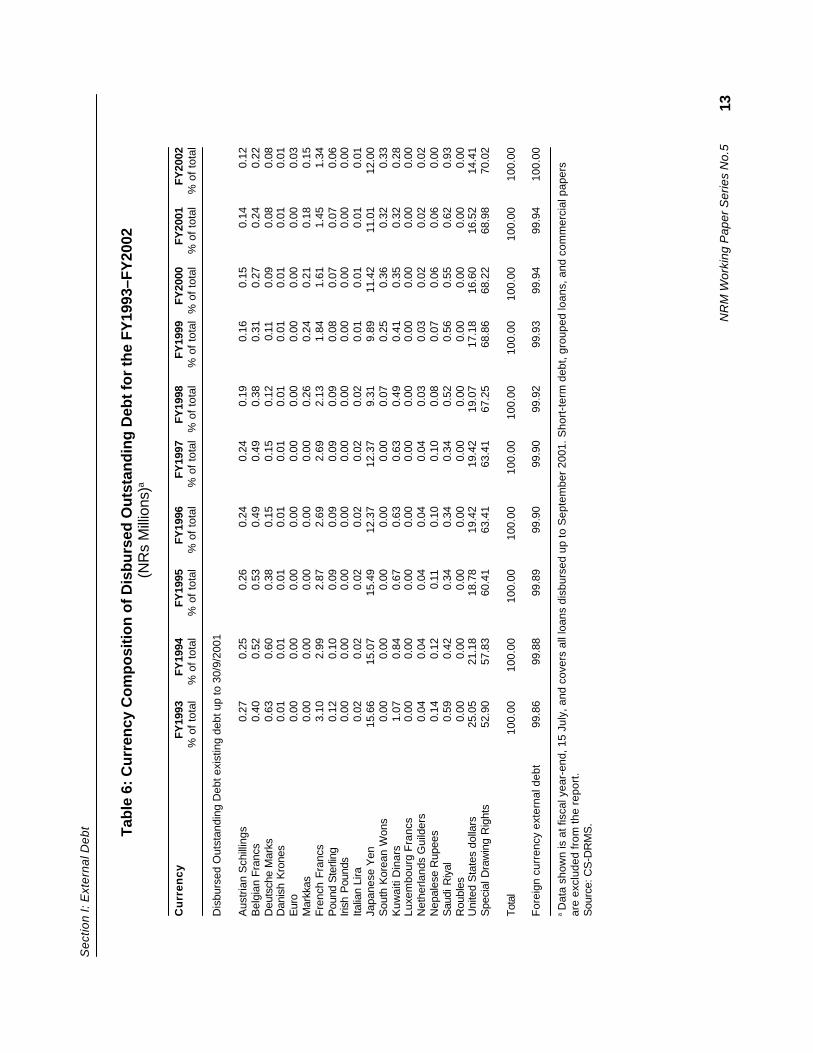

The currency composition of Nepal’s debt service obligation has moved in favor ofSDR. The currency in which an external loan is denominated may differ from the currency in whichdisbursement is made as well as the currency in which repayment has to be made. It is the latterthat is of interest to a debtor country since it must match its foreign exchange resources with thecurrency composition of repayment obligation. This is where part of the vulnerability of Nepal’sespecial situation vis-à-vis Indian currency arises. Of the total foreign exchange reserves,nonconvertible currencies (including Indian currency) accounted for about 23% in FY2001. Thethree dominant currencies in external debt repayment obligations are the SDR, US dollar, andJapanese Yen. The share of SDR increased from 53% in FY1993 to 70% in FY2002 (Table 6 andCharts 3 and 4). In contrast, the share of US dollar declined by about half and that of Japanese Yenby about 20%.

f. Terms of External Debt

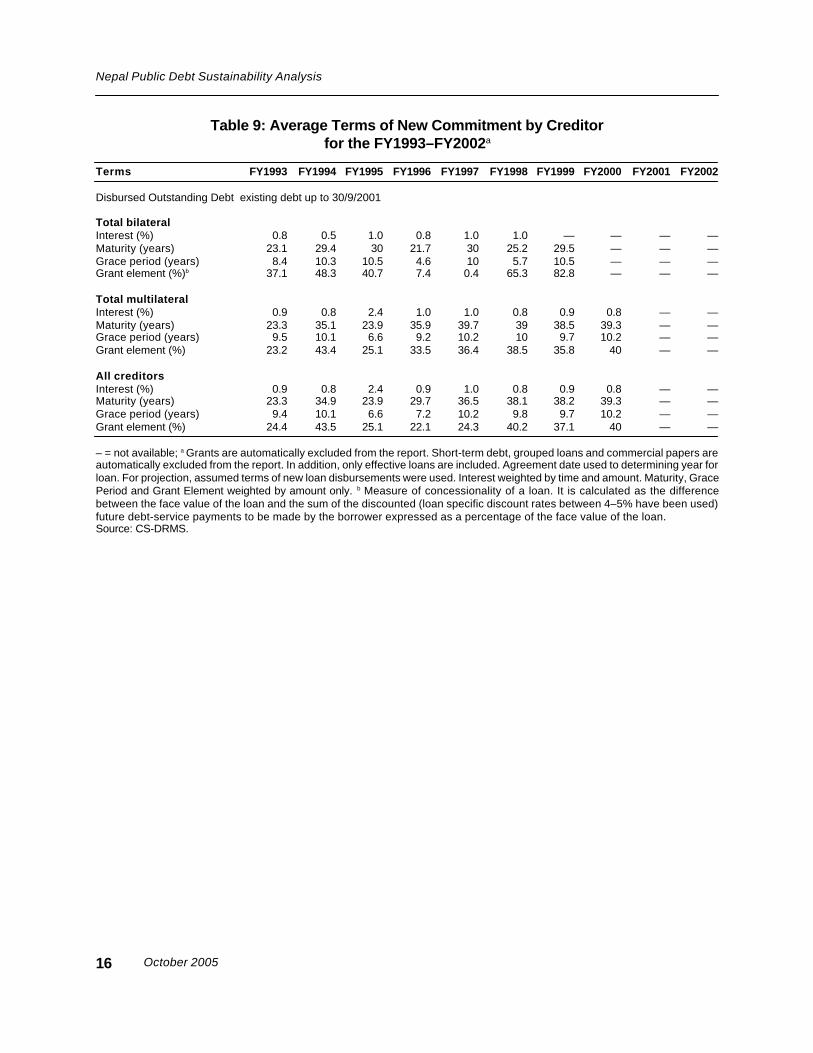

The majority of loans and loan amount was contracted on concessional terms, yet asignificant number was contracted on non-concessional terms. There was a significant shiftin the distribution of external debt in terms of original maturity from a mixed package of loans ofvarying maturity in the early 1990s to an exclusive focus on loans with maturity over 15 years inFY2002. The share of the latter increased from 76% in FY1993 to 99% in FY2002 (Table 7). As for

9

October 2005

Nepal Public Debt Sustainability Analysis

terms, central Government loans were contracted mostly at interest rates 1% or less, with averagematurity period increasing from 23 years in FY1992 to 39 years in FY2000 and grace period remainingstable at 10 years. Average grant element increased from 24% in FY1993 to 40% in FY2000 (Table8). Private sector loans were contracted at much more unfavorable terms, so much as to yieldnegative grant element, implying that interest rates charged were higher than the market referencerate. The term structure and grant element of total debt was similar to that of central Governmentdebt. What comes out clearly is that in some years (e.g., FY1993, FY1995 and FY1996), averageborrowing terms yielded a grant element well below the threshold for concessional loans (35%). Insome years, bilateral terms were more favorable than multilateral, while in others the reverse wastrue (Table 9). However, a more in-depth investigation of 323 loans revealed that as of 30 September2001, 119 were contracted at non-concessional terms, 22 yielding negative grant element (Table10). The bulk of these loans were contracted between 1985 and 1990. In terms of loan volume, theGovernment of Japan was one major source of non-concessional loans (77%). Future loannegotiations should keep these findings in perspective.

10

NR

M W

orki

ng P

aper

Ser

ies

No.

5

Sec

tion

I: E

xter

nal D

ebt

Tab

le 4

: Ext

ern

al D

ebt O

uts

tan

din

g b

y B

orr

ow

er C

ateg

ory

for

the

FY

1993

–FY

2020

(NR

s M

illio

ns)a

B

orr

ow

er

FY19

93FY

1994

FY19

95FY

1996

FY19

97FY

1998

FY19

99FY

2000

FY20

01FY

2002

FY20

07FY

2012

FY20

17FY

2020

Dis

burs

ed O

utst

andi

ng D

ebt e

xist

ing

debt

up

to 3

0/9/

2001

Cen

tral

Go

vern

men

tb

Dis

burs

ed O

utst

andi

ng D

ebt

90,8

3110

5,94

612

1,65

313

3,51

613

8,12

616

5,88

018

2,40

419

2,09

919

5,05

822

5,13

922

1,07

219

3,86

215

5,96

712

9,69

3%

of t

otal

99.0

799

.11

99.3

698

.76

97.7

597

.33

97.4

497

.27

97.2

597

.70

98.4

799

.74

99.8

099

.80

Pri

vate

sec

torc

Dis

burs

ed O

utst

andi

ng D

ebt

851

956

784

1,67

43,

178

4,55

64,

792

5,38

25,

521

5,29

33,

435

513

315

254

% o

f tot

al0.

930.

890.

641.

242.

252.

672.

562.

732.

752.

301.

530.

260.

200.

20

Tota

l

Dis

burs

ed O

utst

andi

ng D

ebt

91,6

8210

6,90

212

2,43

713

5,19

114

1,30

417

0,43

718

7,19

619

7,48

120

0,57

923

0,43

222

4,50

719

4,37

415

6,28

112

9,94

8%

of t

otal

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

a Dat

a sh

own

is a

t fis

cal y

ear-

end,

15

July

and

cov

ers

all l

oans

dis

burs

ed u

p to

Sep

tem

ber

2001

. Sho

rt-t

erm

deb

t, gr

oupe

d lo

ans,

and

com

mer

cial

pap

ers

are

excl

uded

from

the

repo

rt. b I

nclu

des

all p

ublic

sec

tor e

xter

nal d

ebt,

that

is, d

ebt o

f gen

eral

Gov

ernm

ent (

Gov

ernm

ent u

nits

at c

entr

al, s

tate

and

loca

l lev

el, s

ocia

l sec

urity

fund

s, n

onm

arke

t non

prof

itin

stitu

tions

con

trol

led

by th

e G

over

nmen

t, m

onet

ary

auth

oriti

es (c

entr

al b

ank

and

cent

ral b

ank

oper

atio

ns c

arrie

d ou

t by

othe

r Gov

ernm

ent i

nstit

utio

ns a

nd c

omm

erci

al b

anks

), a

ndpu

blic

ent

erpr

ises

. In

Nep

al, p

ublic

ent

erpr

ises

can

rece

ive

exte

rnal

loan

s on

ly th

roug

h an

on

lend

ing

arra

ngem

ent w

ith th

e G

over

nmen

t und

er w

hich

the

exte

rnal

cre

dito

r offe

r the

loan

cre

dit t

o th

e go

vern

emen

t whi

ch in

turn

lend

s it

to p

ublic

ent

erpr

ises

. The

con

trac

tual

agr

eem

ent f

or e

xter

nal d

ebt s

ervi

cing

is b

etw

een

the

Gov

ernm

ent a

nd th

e cr

edito

r.c I

nclu

des

publ

icly

gua

rant

eed

and

non-

guar

ante

ed d

ebt o

f the

ban

king

sec

tor (

com

mer

cial

ban

ks, s

avin

gs b

anks

, sav

ings

and

loan

ass

ocia

tions

, cre

dit u

nion

s an

d co

oper

ativ

es,

and

build

ing

soci

etie

s), n

onba

nk fi

nanc

ial c

orpo

ratio

ns (

insu

ranc

e co

rpor

atio

ns a

nd p

ensi

on fu

nds,

oth

er n

onba

nk fi

nanc

ial i

ntem

edia

ries,

and

fina

ncia

l aux

iliar

ies)

, non

finan

cial

corp

orat

ions

, hou

seho

lds

and

nonp

rofit

inst

itutio

ns s

ervi

ng h

ouse

hold

s, a

nd o

ther

sec

tors

.S

ourc

e: C

S-D

RM

S.

11

Oct

ober

200

5

Nep

al P

ublic

Deb

t Sus

tain

abili

ty A

naly

sis

Tab

le 5

: Ext

ern

al D

ebt O

uts

tan

din

g b

y G

uar

ante

e fo

r th

e F

Y19

93–F

Y20

20(N

Rs

Mill

ions

)a

Bo

rro

wer

an

d g

uar

ante

eFY

1993

FY19

94FY

1995

FY19

96FY

1997

FY19

98FY

1999

FY20

00FY

2001

Dis

burs

ed O

utst

andi

ng D

ebt e

xist

ing

debt

up

to 3

0/9/

2001

1. C

entr

al G

over

nmen

t (ex

istin

g lo

ans)

Dis

burs

ed O

utst

andi

ng D

ebt

90,

831

105

,946

120

,539

131

,712

135

,476

162

,649

178

,929

188

,702

191

,706

% o

f tot

al99

.10

99.1

399

.38

98.7

797

.73

97.2

997

.41

97.2

497

.22

2. P

ublic

cor

pora

tions

(ex

istin

g lo

ans)

Dis

burs

ed O

utst

andi

ng D

ebt

00

00

00

00

0%

of t

otal

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

3. P

rivat

e se

ctor

with

Gov

ernm

ent g

uara

ntee

(exi

stin

g lo

ans)

Dis

burs

ed O

utst

andi

ng D

ebt

437

489

291

2827

3133

3232

% o

f tot

al0.

480.

460.

240.

020.

020.

020.

020.

020.

02

Pub

lic a

nd p

ublic

ly g

uara

ntee

d de

bt (

exis

ting

loan

s)(T

otal

=1+2

+3)

Dis

burs

ed O

utst

andi

ng D

ebt

91

,268

106

,435

120

,830

131

,740

135

,503

162

,680

178

,962

188

,734

191

,738

% o

f tot

al99

.57

99.5

999

.62

98.7

997

.75

97.3

197

.43

97.2

697

.23

4. P

rivat

e se

ctor

with

out G

over

nmen

t gua

rant

ee(e

xist

ing

loan

s)D

isbu

rsed

Out

stan

ding

Deb

t

3

90

443

46

7

1,

618

3,12

4

4,

495

4,72

7

5,

318

5,45

8%

of t

otal

0.43

0.41

0.38

1.21

2.25

2.69

2.57

2.74

2.77

5. T

otal

=(1+

2+3+

4) (e

xist

ing

loan

s)

Dis

burs

ed O

utst

andi

ng D

ebt

91

,658

106

,878

121

,297

133

,358

138

,627

167

,175

183

,689

194

,052

197

,196

% o

f tot

al10

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

100.

0010

0.00

a Dat

a sh

own

is a

t fis

cal y

ear-

end,

15

July

. Sho

rt-t

erm

deb

t, gr

oupe

d lo

ans,

and

com

mer

cial

pap

ers

are

excl

uded

from

the

repo

rt fo

r F

Y19

92–F

Y20

01 p

erio

d.S

ourc

e: C

S-D

RM

S.

12

NR

M W

orki

ng P

aper

Ser

ies

No.

5

Sec

tion

I: E

xter

nal D

ebt Tab

le 6

: Cu

rren

cy C

om

po

sitio

n o

f Dis

bu

rsed

Ou

tsta

nd

ing

Deb

t fo

r th

e F

Y19

93–F

Y20

02 (N

Rs

Mill

ions

)a

Cu

rren

cyFY

1993

FY19

94FY

1995

FY19

96FY

1997

FY19

98FY

1999

FY20

00FY

2001

FY20

02%

of t

otal

% o

f tot

al%

of t

otal

% o

f tot

al%

of t

otal

% o

f tot

al%

of t

otal

% o

f tot

al%

of t

otal

% o

f tot

al

Dis

burs

ed O

utst

andi

ng D

ebt e

xist

ing

debt

up

to 3

0/9/

2001

Aus

tria

n S

chill

ings

0.27

0.25

0.26

0.24

0.24

0.19

0.16

0.15

0.14

0.12

Bel

gian

Fra

ncs

0.40

0.52

0.53

0.49

0.49

0.38

0.31

0.27

0.24

0.22

Deu

tsch

e M

arks

0.63

0.60

0.38

0.15

0.15

0.12

0.11

0.09

0.08

0.08

Dan

ish

Kro

nes

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

0.01

Eur

o0.

000.

000.

000.

000.

000.

000.

000.

000.

000.

03M

arkk

as0.

000.

000.

000.

000.

000.

260.

240.

210.

180.

15F

renc

h F

ranc

s3.

102.

992.

872.

692.

692.

131.

841.

611.

451.

34P

ound

Ste

rling

0.12

0.10

0.09

0.09

0.09

0.09

0.08

0.07

0.07

0.06

Irish

Pou

nds

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

0.00

Italia

n Li

ra0.

020.

020.

020.

020.

020.

020.

010.

010.

010.

01Ja

pane

se Y

en15

.66

15.0

715

.49

12.3

712

.37

9.31

9.89

11.4

211

.01

12.0

0S

outh

Kor

ean

Won

s0.

000.

000.

000.

000.

000.

070.

250.

360.

320.

33K

uwai

ti D

inar

s1.

070.

840.

670.

630.

630.

490.

410.

350.

320.

28Lu

xem

bour

g F

ranc

s0.

000.

000.

000.

000.

000.

000.

000.

000.

000.

00N

ethe