ndic quarterly quartely sept dec 2007.pdf · global depository receipts by nigerian banks to raise...

TRANSCRIPT

1

NDIC QUARTERLY

Volume 17 September/December Nos 3/4 TABLE OF CONTENTS Content Page Review of Developments in Banking and Finance in the Third and Fourth Quarters of 2007 By Research Department The nation’s economy, particularly the financial services industry and the banking sub-sector, witnessed series of developments during the third and fourth quarters of 2007. Following the inauguration of a new government in May29, 2007, a new economic agenda to be pursued by government was announced during the period under review. Secondly, a post-consolidation merger between IBTC Chartered Bank Plc and Stanbic Bank (Nigeria) Limited was completed during the period under review. At the regulatory level, the Central Bank of Nigeria (CBN) issued new guidelines to further liberalize the foreign exchange market and the use of Global Depository Receipts by Nigerian banks to raise funds from the international financial market. Details of these developments and others including the report on interest rates on major financial instruments, the naira exchange rate as well as the average performance of quoted banks’ shares on the Nigerian Stock Exchange (NSE) as at the end of 2007, are presented below. Financial Condition and Performance of Insured Banks in the Third and Fourth Quarters of 2007 By Research & Off-Site Supervision Departments The conditions of the insured banks were generally sound whilst the industry witnessed positive performance in the period under review. Total assets of the banks increased. However, asset quality deteriorated as the proportion of non-performing loans to total credit increased. In terms of earnings and profitability, the industry performed creditably well as profit before tax increased significantly by more than 114.72 percent. Details of these and other indicators are contained in this paper.

2

Proactive Measures to Guard against Fraud/Cash Theft in The Banking Industry And In Organisations BY G. A. Ogunleye, OFR Managing Director/Chief Executive The paper examines the modus operandi of fraudsters in perpetrating fraud in our environment with a view to creating a high level of awareness amongst the citizenry. Also discussed in the paper are the causes, the nature and various types of frauds. Finally, the author identifies the needed measures to be taken in order to deter, prevent and detect fraud in a timely and effective manner Bank Directors and Related Party Transactions By Professor Peter N. Umoh, FCIB Executive Director (Operations) The paper first examines the laws and regulations governing directors’ transactions with their banks. That is followed by the lessons of such business experience in Nigeria. From lessons of experience, the author concludes that in spite of the provisions of the law and the regulators’ guidelines on such relationship, some directors found ways to evade the laws/regulations and exploit the relationship for selfish ends. However, he opines that the recent banking consolidation which has produced relatively stronger banks with better corporate governance ethos would promote a healthy business relationship between banks and their directors The Northern Rock Crisis By Research Department The paper critically examines the Northern Rock Crisis in the United Kingdom. In that respect, the paper discusses the causes of the crisis. It also reviews the reactions of regulators and depositors as well as possible lessons which could be learnt from the U.K. experience.

3

MAJOR DEVELOPMENTS IN THE BANKING SECTOR

DURING THE THIRD AND FOURTH QUARTERS 2007

By

Research Department

1.0 Introduction

The nation’s economy, particularly the financial services industry and the

banking sub-sector, witnessed series of developments during the third and

fourth quarters of 2007. First, the Minister of Finance announced a new

economic agenda to be pursued by government. Secondly, IBTC Chartered

Bank Plc and Stanbic Bank (Nigeria) Limited completed their merger

arrangement. Thirdly, the apex regulatory body, the Central Bank of Nigeria

(CBN) issued new guidelines during the period under review and amongst

the notable ones were those related to further liberalization of the foreign

exchange market and the use of Global Depository Receipts by Nigerian

banks to raise funds from the international financial market. Other notable

developments during the period included the federal government

announcement of N2.45 trillion budget for 2008. Details of these

developments and the report on interest rates on major financial instruments,

the naira exchange rate as well as the average performance of quoted banks’

shares on the Nigerian Stock Exchange (NSE) as at the end of 2007, are

presented below.

4

2.0 Listing of Guaranty Trust Bank (GT Bank) Plc’s Global Depository

Receipt (GDR) on the London Stock Exchange (LSE)

During the period under review, Guaranty Trust Bank (GT Bank) Plc Global

Depository Receipt (GDR) was listed on the London Stock Exchange. The listing

of the GT Bank Plc on Thursday, July 26, 2007 was the first international listing on

the London Stock Exchange (LSE) by a company quoted on the Nigerian Stock

Exchange and indeed the first African bank.

Global Depository Receipt (GDR) is a dollar-denominated instrument issued in

international financial markets through a registered depository bank. It is a

negotiable certificate, which represents ownership of a certain equity securities that

are issued and traded in a local market as well as ownership of a certain number of

shares of a company. It can be listed/traded independently from the equity

securities. GDRs are typically used by companies from emerging markets to raise

capital and access investors in international markets.

3.0 Announcement of New Economic Agenda by Government

During the period under review, the Honourable Minister of Finance, outlined the

new economic agenda of the government. According to the Minister, the new

agenda was designed to present a working roadmap towards accelerating the

economic transformation by sustaining and improving on the relative

macroeconomic stability. He emphasized that the key values that will underpin the

framework were:

· Upholding the constitution and the rule of law

· Respect for due process and

5

· Integrity, Accountability and Transparency

The Minister enumerated the major areas of focus in the new reform process to

include:

i. Accelerating Institutional Reforms.

The need to broaden and intensify the institutional reform carried out

under the pilot scheme of the first phase of the public sector reforms was

emphasized. That would encompass both in-house cleansing within the

Ministry and in a number of its agencies where there was a fundamental

lack of focus.

ii. Budget and Debt Management.

While acknowledging the commendable role and achievement of the

Debt Management Office (DMO) in the recent exit of Nigeria from the

Paris and London club debts as well as the restructuring of the country’s

internal debt, the Minister announced the Federal Governments intention

to take the reforms to a higher level with some specific measures. Some

of the measures included:

a) Raising the required funding for key infrastructural projects, such as

roads and railways from both the Bond and Capital Markets,

b) Encouraging states to initiate and pass their own Fiscal Responsibility

laws.

c) Setting up of a standard IT platform for effective and timely linkage

with all the relevant agencies on the Federal, States and Local

Government loans.

6

d) Ensuring earlier submission of proposed budget and greater

consultation with the stakeholders in the earlier, critical, planning

stages of the Budget.

e) The Ministry of Finance was to ensure full compliance with current

regulations that require Ministries, Departments and Agencies to

prepare and submit their final accounts to the Office of the Auditor

General of the Federation (OAGF) not later than March 31st,

following the end of each financial year. This along with other

periodic (quarterly) reporting would ensure greater accountability in

Government accounts and assist the office of the Auditor General of

the Federation in performing its audit function better and reporting to

the National Assembly.

(iii) Tax Reform

Part of the reform announced by the Minister was tax reform. These would involve

the review of existing legislation or enacting new ones, where such legislation is

non- existent. In addition, steps would be taken to improve the coordination

between the Federal Inland Revenue Service (FIRS) and the relevant Departments

of the Ministry, most especially the Revenue and Fiscal Departments so as to

ensure that they do not work at cross purposes.

(iv) Capital Market

Some of the specific measures that would be put in place to strengthen the nation’s

capital market as explained by the Minister during the press briefing would

include:

7

a) Broadening and deepening the market through the introduction of additional

financial instruments. In that regard SEC and the DMO would be expected

to work closely in the development of the bond market and its greater use by

the Federal, States and Local Governments, as well as by corporate bodies.

b) Developing stronger mechanisms to check insider dealings and other forms

of market abuse.

c) Creating greater public awareness and utilization, of the capital market,

especially the Abuja Commodities and Securities Exchange and

d) Reducing the cost of doing business in the Nigerian capital market.

(v) Economic Management Team (EMT)

The Minister announced the new membership of the Economic Management Team

(EMT) which was recently reconstituted by the President. The Membership of the

EMT was as follows:

1. Minister of Finance - Chairman

2. Minister of National Planning - Vice Chairman

3. Minister of State, Finance - Member

4. Minister of State, Petroleum - Member

5. Hon Strategic Adviser to the President on Energy-Member

6. Economic Adviser to the President - Member

7. Deputy Governor (Economic Policy, CBN) -Member

8. Special Asst to the President (Power) - Member

9. Special Asst to the President (Petroleum)-Member

10. Chairman FIRS - Member

8

11. Director of Research & Statistics (CBN) - Member

Technical Support was to be provided by the following:

1. Group Managing Director, NNPC

2. Director-General, DMO

3. Accountant-General of the Federation

In addition, representatives of the Nigeria Economic Summit Group and the

Nigerian Economic Society were to serve in the Committee.

4.0 IBTC Chartered Bank Plc and Stanbic Bank (Nigeria) Limited

Completed Merger Arrangement

During the period under review, the merger arrangement between IBTC Chartered

Bank Plc and Stanbic Bank (Nigeria) Limited, which had previously received the

approvals of the shareholders of both banks, the Securities & Exchange

Commission (SEC), the South African Reserve Bank and the Central Bank of

Nigeria, was approved by the Federal High Court on Monday, September, 24 2007.

With the merger which became unconditional and effective from that date, IBTC

Chartered Bank Plc had now acquired all the assets, liabilities and undertakings of

Stanbic (Nigeria) bank and Stanbic (Nigeria) bank had been dissolved without

being wound up. The new bank that emerged from the merger was named Stanbic

IBTC Bank PLC. That development reduced the total number of deposit money

banks in the system to 24 as at the end of December, 2007.

9

5.0 The Central Bank of Nigeria (CBN) Circular on Further Liberalization

of the Foreign Exchange Market

During the period under review, the CBN further liberalized the foreign exchange

market through the review of rules and regulations guiding transactions in the

market. The amendments/reviews included the following:

i. National Youth Service Corps (N.Y.S.C) discharge certificate or

certificate of exemption where applicable was no longer part of

documentation requirements for remittance of school fees for Post

graduate studies abroad.

ii. Where an applicant is proceeding on a business trip duly authorized

by a corporate body where the applicant is an employee, the latter

(employee) would be eligible to purchase Personal Travel Allowance

(PTA), in addition to the normal Business Travel Allowance (BTA)

subject to relevant documentation.

iii. Authorized Dealers that had huge cash deposits from Ordinary

Domiciliary Account holders as indicated in Circular could avail such

for their BDC window and its equivalent from WDAS winnings

transferred to their Nostro Account. Accordingly, any Authorized

Dealer that wants to avail itself to the arrangement should inform the

CBN a day to the Auction date.

Authorized Dealers, Bureau de Change operators and indeed the general public

were reminded that it was a very serious offence (for which offenders could be

liable to prosecution) to use fictitious/spurious documents to purchase foreign

exchange in the Foreign exchange Market (FEM).

10

6.0 Ecobank Nigeria Plc to Run Non-resident Naira Settlement Accounts

During the period, the Central Bank of Nigeria approved Ecobank Nigeria Plc’s

bid to run non-resident Naira Settlement Accounts for African educational

institutions. The approval was to ease the payment process for Nigerian students

studying in other African countries. This followed a high demand and requests by

several African educational institutions. These institutions were said to have

requested that Ecobank act as their collection bank for school fees and other

administrative charges for their increasing number of Nigerian students. By this

development, Nigerian students and their parents can now pay tuition fees and

expenses in Naira through Ecobank directly into the account of their educational

institutions with Ecobank affiliates.

Ecobank, the Pan African Bank, currently has an integrated retail network of over

200 locations in Nigeria and with subsidiaries in 19 other countries is seen by

many as the gateway to West, Central and Eastern African markets, being one of

the few banks that undertake transactions in popular currencies used on the

continent such as the Cedi and CFA.

7.0 The Federal Government Announced A N2.45 Trillion Budget For 2008

The Federal Government, during the period under review, announced a budget of

N2.45 trillion for fiscal year 2008. The budget proposal showed that Security and

the Niger Delta got a lion share of N444.6 billion, which is about 20 percent of the

entire budget, as against 6.5 percent in the previous year. Education got N210

billion; Energy, excluding National Integrated Power Projects billed to be

implemented through alternative funding was given N139.78 billion. Agriculture

and Water Resources got N121.19 billion. A total of N38.17 billion was allocated

to the Health Sector, while N73 billion was budgeted for Transportation.

11

Described by the President as a “Budget for the Common man”, the fiscal plan

sought to make life more comfortable for the average man on the street through

employment generation and access to micro credit facility among others. The

budget proposal was based on an exchange rate of N117 per dollar.

8.0 New Guidelines On Bank Mergers And Acquisitions

The Central Bank of Nigeria (CBN) issued new guidelines for mergers and

acquisitions by banks in the country in order to streamline such transactions in the

post-consolidation period. Under the new arrangement, any bank wishing to

acquire or merge with another bank must initiate preliminary discussions with the

target bank at the highest level, that is, the Board of Directors/key shareholders of

the institutions. Thereafter, the bank involved must notify it in writing and obtain a

“no objection” response before proceeding with further discussions or negotiations.

All the banks involved were expected to continue to provide the CBN with regular

updates on the progress made in the discussions. The CBN stated further that banks

must at all times comply strictly with all the relevant laws and regulations

including the provisions of the Banks and Other Financial Institutions Act – 1991

(as amended); Investment and Securities Act 1999; and the Companies and Allied

Matters Act 1990, in the conduct of the transaction.

9.0 Access Bank Commenced Operations in Sierra Leone

Access Bank PLC, during the period under review, opened a subsidiary bank in

Sierra Leone. The new bank is known as Access Bank Sierra Leone Limited. The

bank commenced operations after receiving necessary approvals from the Bank of

Sierra Leone and the Central Bank of Nigeria.

12

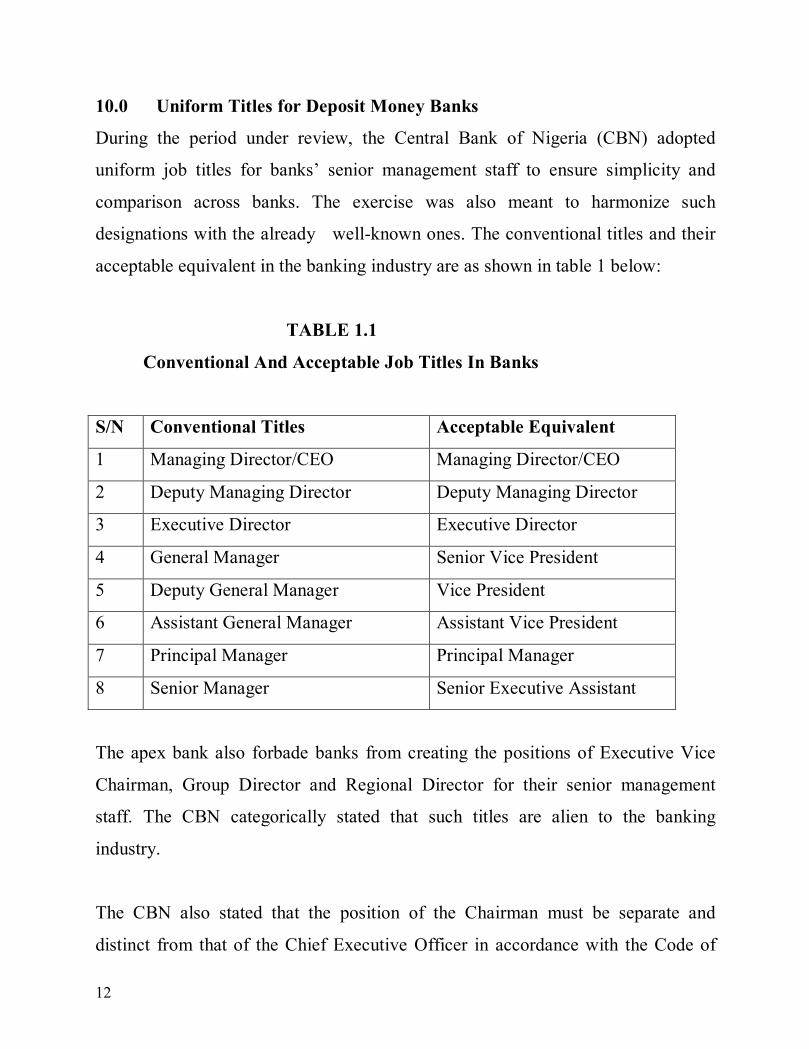

10.0 Uniform Titles for Deposit Money Banks

During the period under review, the Central Bank of Nigeria (CBN) adopted

uniform job titles for banks’ senior management staff to ensure simplicity and

comparison across banks. The exercise was also meant to harmonize such

designations with the already well-known ones. The conventional titles and their

acceptable equivalent in the banking industry are as shown in table 1 below:

TABLE 1.1

Conventional And Acceptable Job Titles In Banks

S/N Conventional Titles Acceptable Equivalent

1 Managing Director/CEO Managing Director/CEO

2 Deputy Managing Director Deputy Managing Director

3 Executive Director Executive Director

4 General Manager Senior Vice President

5 Deputy General Manager Vice President

6 Assistant General Manager Assistant Vice President

7 Principal Manager Principal Manager

8 Senior Manager Senior Executive Assistant

The apex bank also forbade banks from creating the positions of Executive Vice

Chairman, Group Director and Regional Director for their senior management

staff. The CBN categorically stated that such titles are alien to the banking

industry.

The CBN also stated that the position of the Chairman must be separate and

distinct from that of the Chief Executive Officer in accordance with the Code of

13

Corporate Governance. The directive took immediate effect.

11.0 New Rules On Global Depository Receipts (GDRs)

The Central Bank of Nigeria (CBN) issued new guidelines to regulate the issuance

of Global Depository Receipts (GDRs) by banks selling their shares to

international investors. The new regulatory framework mandated banks selling

GDRs to furnish the apex bank with details of the beneficial investors on a copy of

the Certificate of Capital Importation issued in favour of such banks. The

Guidelines became necessary, according to the CBN, in view of the resort of banks

to GDRs with the principal aim of raising capital and selling shares, and the need

to align the new development with the requirements of CCI issuance to foreign

investors as well as build their confidence in the GDRs. It would be recalled that

during the period under review, not fewer than five banks raised funds through the

GDRs.

12.0 145 Community Banks Closed Shop

During the period under review, the Central Bank of Nigeria (CBN) disclosed that

a total of 145 Community Banks (CBs) closed shop due to their inability to beef up

their share capital to N20 million as prescribed by the apex bank. This was

disclosed in a Circular dated December 21, 2007 addressed to all the Chairmen,

Directors, and other stakeholders of the affected banks.

13.0 All Federal Government Bonds Re-Classified As Liquid Assets

The Central Bank of Nigeria (CBN), during the period under review, classified all

Federal Government Bonds that are actively traded on the secondary market as

liquid assets for banks. This is irrespective of the tenor of such bonds. Prior to the

decision by the CBN, only Federal Government bonds with three years maturity or

less were considered as liquid assets of banks.

14

According to the CBN, the decision was taken to deepen the financial market and

enhance the information content of the yield curve for effective price discovery as

well as bench mark international best practices. By the new decision, only FGN

bonds actively traded on the secondary market shall qualify as eligible instruments

for the computation of liquidity ratio of the banks. In addition such FGN bonds

would serve as collateral for lending/repo at the CBN window.

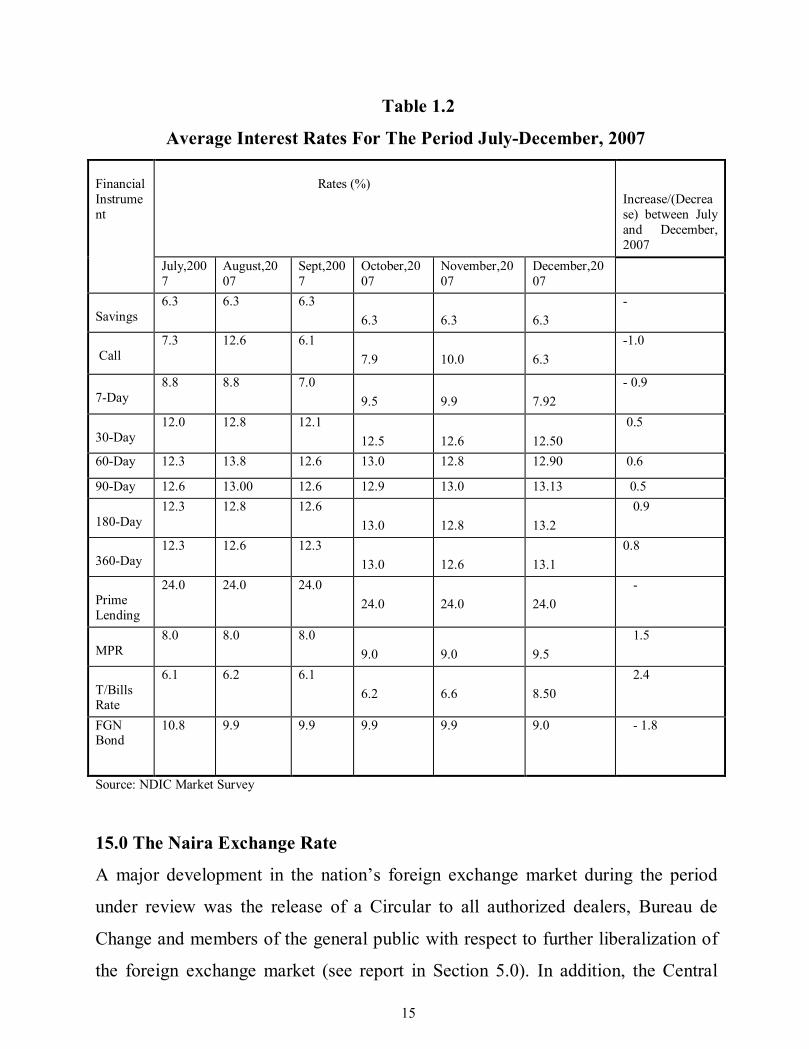

14.0 Interest Rates

The interest rates for major financial instruments during the second half of 2007

are presented in Table 1.2. As revealed in the table, the Prime Lending and

Savings deposit rates as at end of the year remained the same at 24.0 and 6.3 per

cent respectively when compared to those obtainable as at July, 2007, the

beginning of the review period. Rates on Call and 7-Day money decreased, as at

the end of December 2007, by 1.0 and 0.9 percentage points respectively, during

the period under review whereas rates on other deposit instruments with varied

maturities witnessed some slight appreciation. For instance, whilst rate on 90-day

grew by 0.5 percentage point during the period, rate on one-year deposits attracted

an increase of 0.8 percentage point. Rates depicting the stance and direction of

monetary policy enjoyed the highest increase during the period: MPR increased by

1.5 percentage points during the period under review while Treasury Bills rate

grew by 2.4 percentage points during the same period. The FGN Bond Rates, as

evidenced in Table 1.2, decreased by 1.8 percentage points from 10.8 percent in

July to 9.0 percent in December, 2007.

15

Table 1.2

Average Interest Rates For The Period July-December, 2007 Financial Instrument

Rates (%)

Increase/(Decrease) between July and December, 2007

July,2007

August,2007

Sept,2007

October,2007

November,2007

December,2007

Savings

6.3 6.3 6.3 6.3

6.3

6.3

-

Call

7.3 12.6 6.1 7.9

10.0

6.3

-1.0

7-Day

8.8 8.8 7.0 9.5

9.9

7.92

- 0.9

30-Day

12.0 12.8 12.1 12.5

12.6

12.50

0.5

60-Day 12.3 13.8 12.6 13.0 12.8 12.90 0.6

90-Day 12.6 13.00 12.6 12.9 13.0 13.13 0.5 180-Day

12.3 12.8 12.6 13.0

12.8

13.2

0.9

360-Day

12.3 12.6 12.3 13.0

12.6

13.1

0.8

Prime Lending

24.0 24.0 24.0 24.0

24.0

24.0

-

MPR

8.0 8.0 8.0 9.0

9.0

9.5

1.5

T/Bills Rate

6.1 6.2 6.1 6.2

6.6

8.50

2.4

FGN Bond

10.8 9.9 9.9 9.9

9.9 9.0 - 1.8

Source: NDIC Market Survey

15.0 The Naira Exchange Rate

A major development in the nation’s foreign exchange market during the period

under review was the release of a Circular to all authorized dealers, Bureau de

Change and members of the general public with respect to further liberalization of

the foreign exchange market (see report in Section 5.0). In addition, the Central

16

Bank offered 25billion Naira ($209.81 million) worth of one-year treasury bonds

on Wednesday the 7th November 2007, which attracted substantial interest from

foreign investors. Aside the inflow from foreign investors, the market was mostly

driven by speculative transactions among dealers. The massive inflows coupled

with the dollar’s decline in the international market led to a steady appreciation of

the Naira against the US dollar during the period under review.

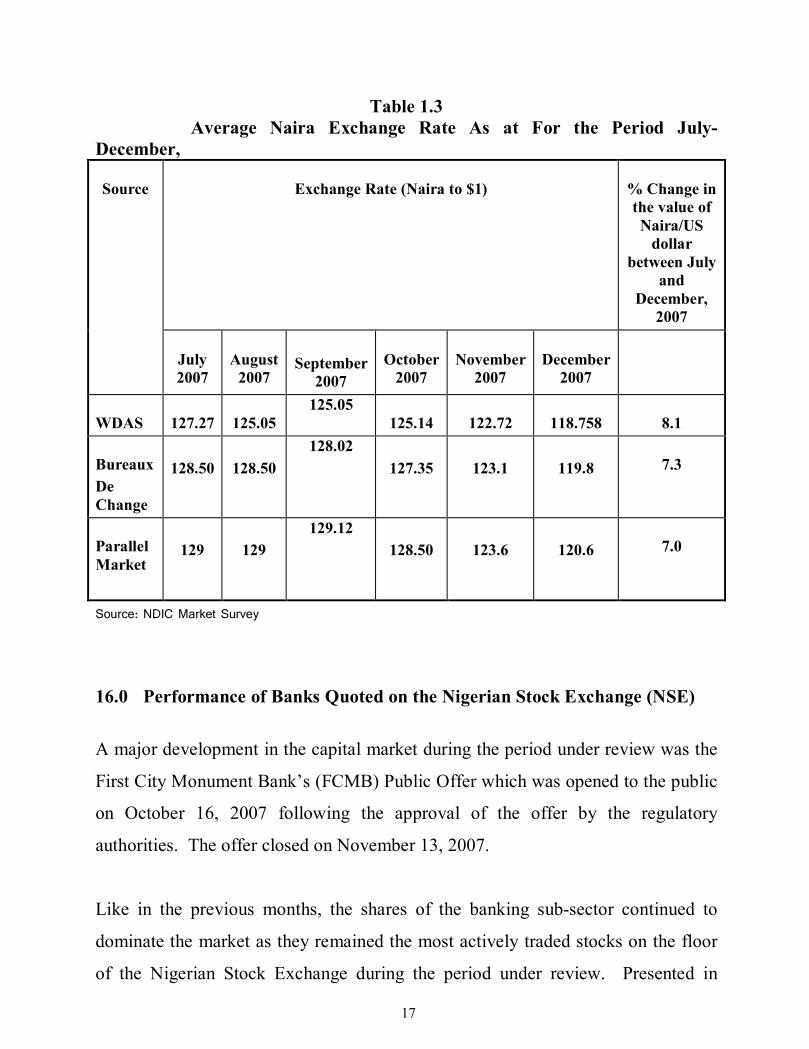

The average Naira exchange rate against the US Dollar for the second half, 2007

is presented in Table 1.3 with the comparative changes in rates between the months

of July and December, 2007. As evidenced in the table, the Naira appreciated in

the three segments of the market, namely Wholesale Dutch Auction System

(WDAS), Bureau De Change (BDCs) and Parallel market. The Naira exchange

rate was N1178.76 to a US dollar in December, 2007 as against N127.27 in July,

2007 at the WDAS depicting an appreciation of 8.1 percent of the Naira. In the

Bureau De Change, the Naira exchanged for N119.8 for a US dollar in December

as against N128.5 in July, 2007. In the parallel market from our survey, the Naira

appreciated by about 7 percent against the US dollar as shown in the table.

17

Table 1.3 Average Naira Exchange Rate As at For the Period July-December,

Source

Exchange Rate (Naira to $1)

% Change in the value of Naira/US

dollar between July

and December,

2007

July 2007

August

2007

September

2007

October

2007

November

2007

December

2007

WDAS

127.27

125.05

125.05 125.14

122.72

118.758

8.1

Bureaux De Change

128.50

128.50

128.02 127.35

123.1

119.8

7.3

Parallel Market

129

129

129.12 128.50

123.6

120.6

7.0

Source: NDIC Market Survey

16.0 Performance of Banks Quoted on the Nigerian Stock Exchange (NSE)

A major development in the capital market during the period under review was the

First City Monument Bank’s (FCMB) Public Offer which was opened to the public

on October 16, 2007 following the approval of the offer by the regulatory

authorities. The offer closed on November 13, 2007.

Like in the previous months, the shares of the banking sub-sector continued to

dominate the market as they remained the most actively traded stocks on the floor

of the Nigerian Stock Exchange during the period under review. Presented in

18

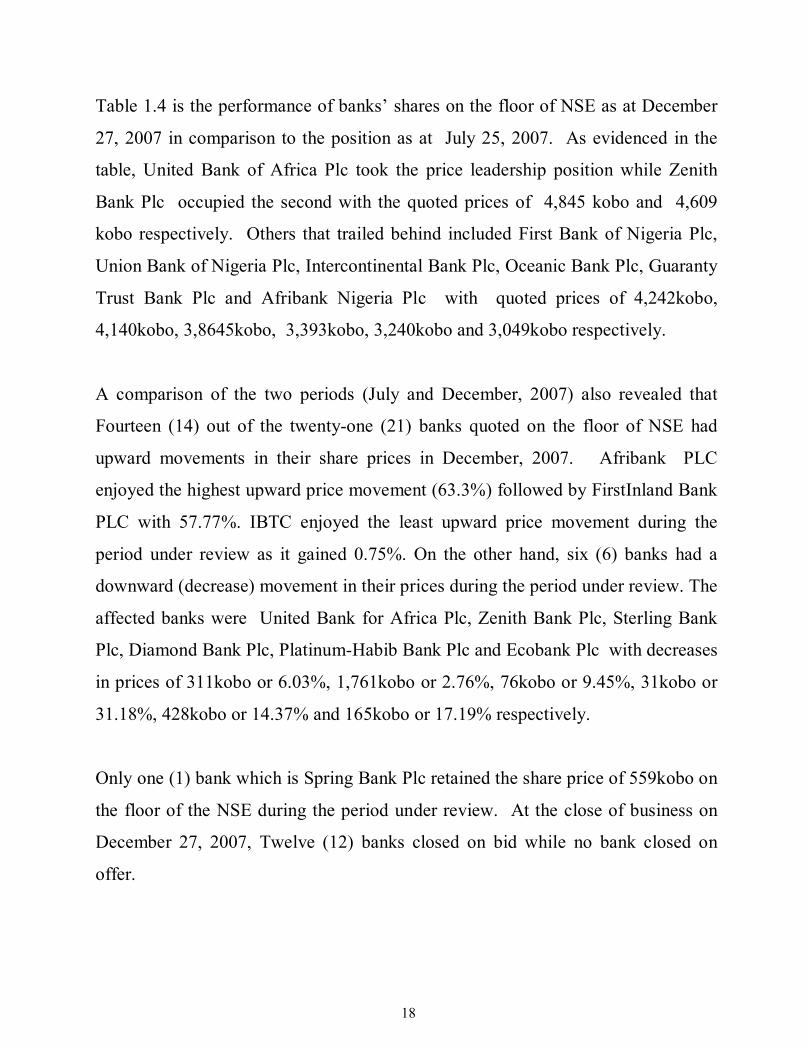

Table 1.4 is the performance of banks’ shares on the floor of NSE as at December

27, 2007 in comparison to the position as at July 25, 2007. As evidenced in the

table, United Bank of Africa Plc took the price leadership position while Zenith

Bank Plc occupied the second with the quoted prices of 4,845 kobo and 4,609

kobo respectively. Others that trailed behind included First Bank of Nigeria Plc,

Union Bank of Nigeria Plc, Intercontinental Bank Plc, Oceanic Bank Plc, Guaranty

Trust Bank Plc and Afribank Nigeria Plc with quoted prices of 4,242kobo,

4,140kobo, 3,8645kobo, 3,393kobo, 3,240kobo and 3,049kobo respectively.

A comparison of the two periods (July and December, 2007) also revealed that

Fourteen (14) out of the twenty-one (21) banks quoted on the floor of NSE had

upward movements in their share prices in December, 2007. Afribank PLC

enjoyed the highest upward price movement (63.3%) followed by FirstInland Bank

PLC with 57.77%. IBTC enjoyed the least upward price movement during the

period under review as it gained 0.75%. On the other hand, six (6) banks had a

downward (decrease) movement in their prices during the period under review. The

affected banks were United Bank for Africa Plc, Zenith Bank Plc, Sterling Bank

Plc, Diamond Bank Plc, Platinum-Habib Bank Plc and Ecobank Plc with decreases

in prices of 311kobo or 6.03%, 1,761kobo or 2.76%, 76kobo or 9.45%, 31kobo or

31.18%, 428kobo or 14.37% and 165kobo or 17.19% respectively.

Only one (1) bank which is Spring Bank Plc retained the share price of 559kobo on

the floor of the NSE during the period under review. At the close of business on

December 27, 2007, Twelve (12) banks closed on bid while no bank closed on

offer.

19

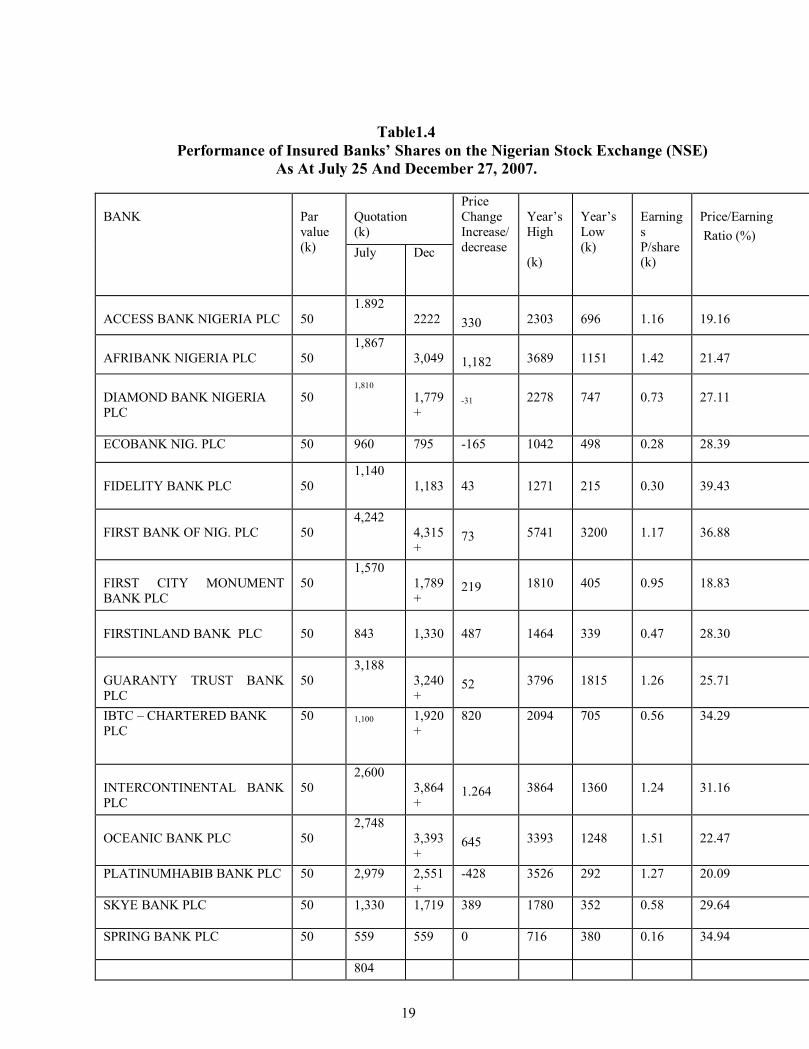

Table1.4 Performance of Insured Banks’ Shares on the Nigerian Stock Exchange (NSE)

As At July 25 And December 27, 2007.

BANK

Par value (k)

Quotation (k)

Price Change Increase/decrease

Year’s High (k)

Year’s Low (k)

Earnings P/share (k)

Price/Earning Ratio (%)

July Dec

ACCESS BANK NIGERIA PLC

50

1.892 2222

330

2303

696

1.16

19.16

AFRIBANK NIGERIA PLC

50

1,867 3,049

1,182

3689

1151

1.42

21.47

DIAMOND BANK NIGERIA PLC

50

1,810 1,779+

-31

2278

747

0.73

27.11

ECOBANK NIG. PLC 50 960 795 -165 1042 498 0.28 28.39

FIDELITY BANK PLC

50

1,140 1,183

43

1271

215

0.30

39.43

FIRST BANK OF NIG. PLC

50

4,242 4,315 +

73

5741

3200

1.17

36.88

FIRST CITY MONUMENT BANK PLC

50

1,570 1,789+

219

1810

405

0.95

18.83

FIRSTINLAND BANK PLC

50

843

1,330

487

1464

339

0.47

28.30

GUARANTY TRUST BANK PLC

50

3,188 3,240 +

52

3796

1815

1.26

25.71

IBTC – CHARTERED BANK PLC

50 1,100 1,920 +

820

2094 705 0.56 34.29

INTERCONTINENTAL BANK PLC

50

2,600 3,864 +

1.264

3864

1360

1.24

31.16

OCEANIC BANK PLC

50

2,748 3,393 +

645

3393

1248

1.51

22.47

PLATINUMHABIB BANK PLC 50 2,979 2,551 +

-428 3526 292 1.27 20.09

SKYE BANK PLC 50 1,330 1,719 389 1780 352 0.58 29.64

SPRING BANK PLC

50 559 559 0 716 380 0.16 34.94

804

20

BANK

Par value (k)

Quotation (k)

Price Change Increase/decrease

Year’s High (k)

Year’s Low (k)

Earnings P/share (k)

Price/Earning Ratio (%)

July Dec

STERLING BANK PLC 50 728 -76 1010 300 0.20 36.40 UBA PLC

50

5,156 4,845+

-311

5775

2531

1.90

25.50

UNION BANK NIG. PLC

50

3,980 4,140 +

168

5033

2291

1.63

25.40

UNITY BANK PLC 50 620 850+ 238 889 250 0.00 0.00

WEMA BANK PLC

50

1,099 1,500 +

481

1500

318

0.55

27.27

ZENITH BANK PLC

50

6,370

4,609 +

-1,761

6897

2440

1.90

24.26

Source: The Nigerian Stock Exchange, Lagos Key: - = Supply (Offer) + = Demand (Bid)

21

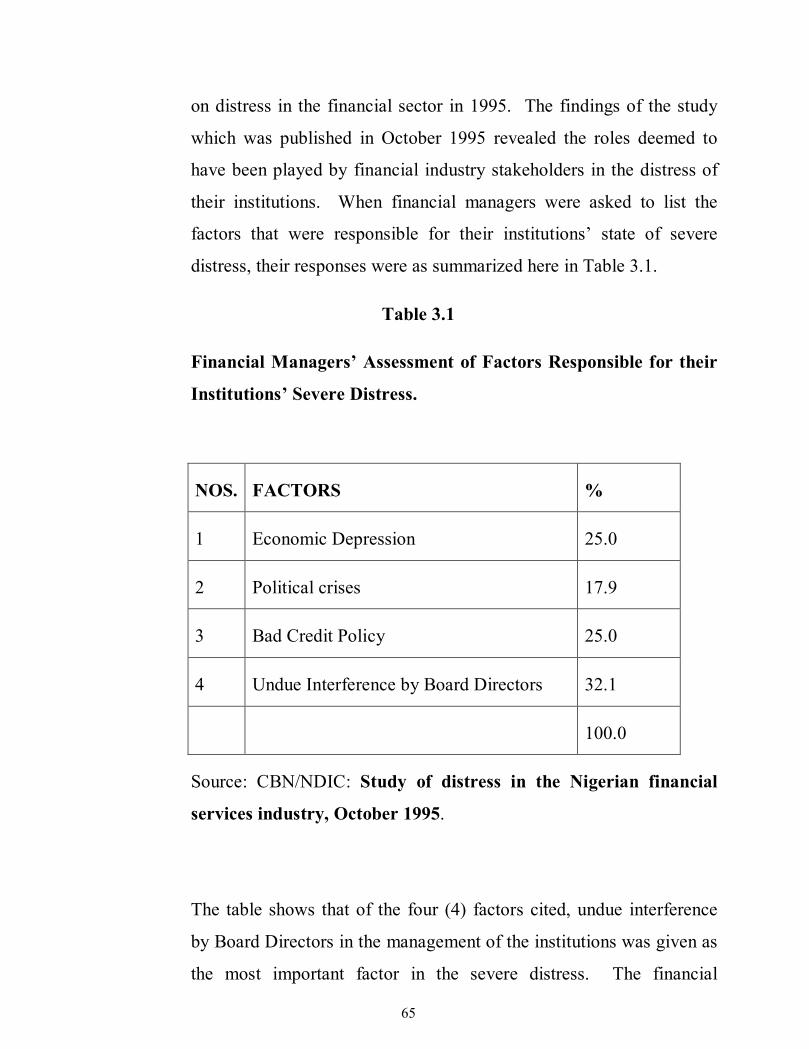

FINANCIAL CONDITION AND PERFORMANCE OF INSURED BANKS IN THE THIRD AND FOURTH QUARTERS OF 2007 BY RESEARCH & OFF-SITE SUPERVISION DEPARTMENTS 1.0 INTRODUCTION The conditions of the insured banks were generally sound whilst the industry

witnessed positive performance in the period under review. Total assets of the

banks increased by 4.3% during the period under review: from N10.00 trillion as at

the end of the third quarter of 2007 to N10.43 trillion as at the end of the fourth

quarter of 2007. On a similar note, the industry’s total loans and advances

increased by 13.22 percent, from N3.36 trillion as at the end of September, 2007 to

N3.80 trillion as at the end of December, 2007. However, asset quality deteriorated

as the proportion of non-performing loans to total credit increased from 7.09

percent as at the end of the third quarter to 7.39 percent as at the end of the last

quarter of 2007. Profit before tax (PBT) which amounted to N184.31 billion as at

the end of the third quarter increased significantly by 114.72 percent to N395.75

billion as at the end of the fourth quarter. Also capital to risk-weighted asset ratio

increased slightly by 0.31 percentage points from 20.78 percent at the end of

September 2007 to 21.09 percent at the end of December 2007. The industry

average liquidity ratio also increased significantly by 6.28 percentage points from

55.72 percent as at the end of September 2007 to 61.98 percent as at the end of

December 2007.

The rest of the paper is divided into three sections. Section 2 presents the structure

of assets and liabilities of the banking industry, while section 3 examines the

22

financial condition of insured banks. Section 4 concludes the paper.

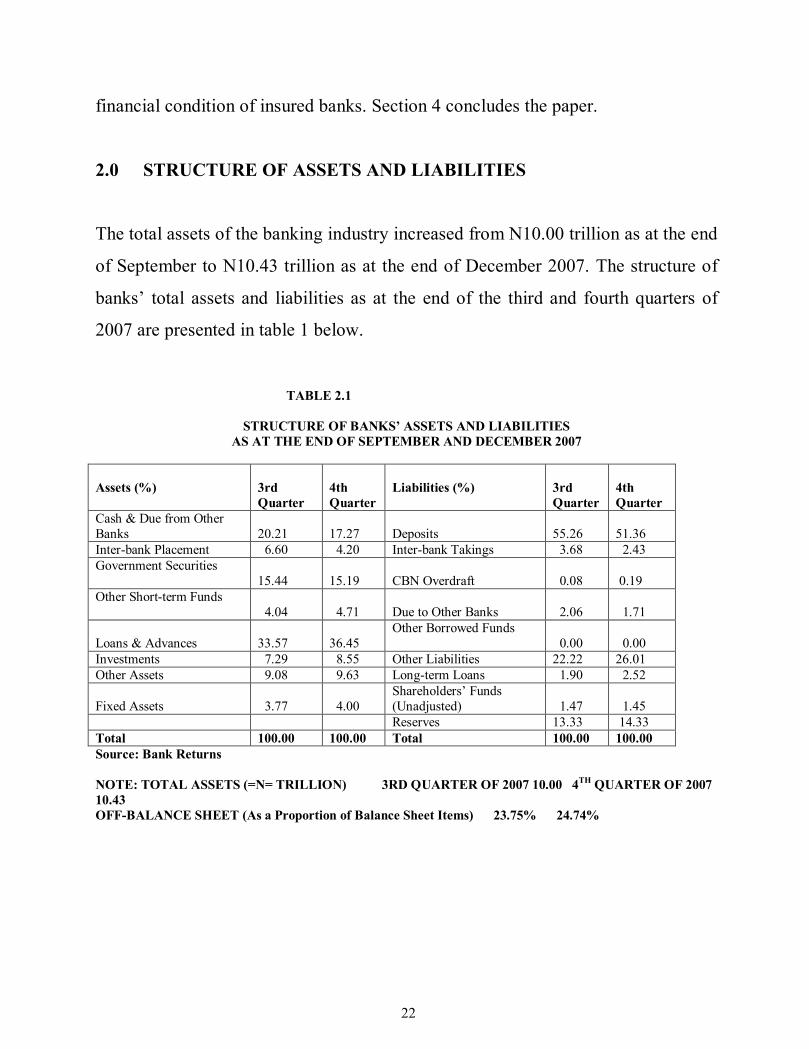

2.0 STRUCTURE OF ASSETS AND LIABILITIES

The total assets of the banking industry increased from N10.00 trillion as at the end

of September to N10.43 trillion as at the end of December 2007. The structure of

banks’ total assets and liabilities as at the end of the third and fourth quarters of

2007 are presented in table 1 below.

TABLE 2.1

STRUCTURE OF BANKS’ ASSETS AND LIABILITIES AS AT THE END OF SEPTEMBER AND DECEMBER 2007

Assets (%)

3rd Quarter

4th Quarter

Liabilities (%)

3rd Quarter

4th Quarter

Cash & Due from Other Banks

20.21

17.27

Deposits

55.26

51.36

Inter-bank Placement 6.60 4.20 Inter-bank Takings 3.68 2.43 Government Securities

15.44 15.19

CBN Overdraft

0.08

0.19

Other Short-term Funds 4.04

4.71

Due to Other Banks

2.06

1.71

Loans & Advances

33.57

36.45

Other Borrowed Funds 0.00

0.00

Investments 7.29 8.55 Other Liabilities 22.22 26.01 Other Assets 9.08 9.63 Long-term Loans 1.90 2.52 Fixed Assets

3.77

4.00

Shareholders’ Funds (Unadjusted)

1.47

1.45

Reserves 13.33 14.33 Total 100.00 100.00 Total 100.00 100.00 Source: Bank Returns NOTE: TOTAL ASSETS (=N= TRILLION) 3RD QUARTER OF 2007 10.00 4TH QUARTER OF 2007 10.43 OFF-BALANCE SHEET (As a Proportion of Balance Sheet Items) 23.75% 24.74%

23

05

10152025303540

3rd Quarter 4th Quarter

CHART 1 A: STRUCTURE OF BANKS' ASSETS FOR THE 3RD AND 4TH QUARTERS OF 2007

Cash & Due from Other Banks Interbank Placements

Government Securities Other Short-term Funds

Loans & Advances/Leases Investments

Other Assets Fixed Assets

24

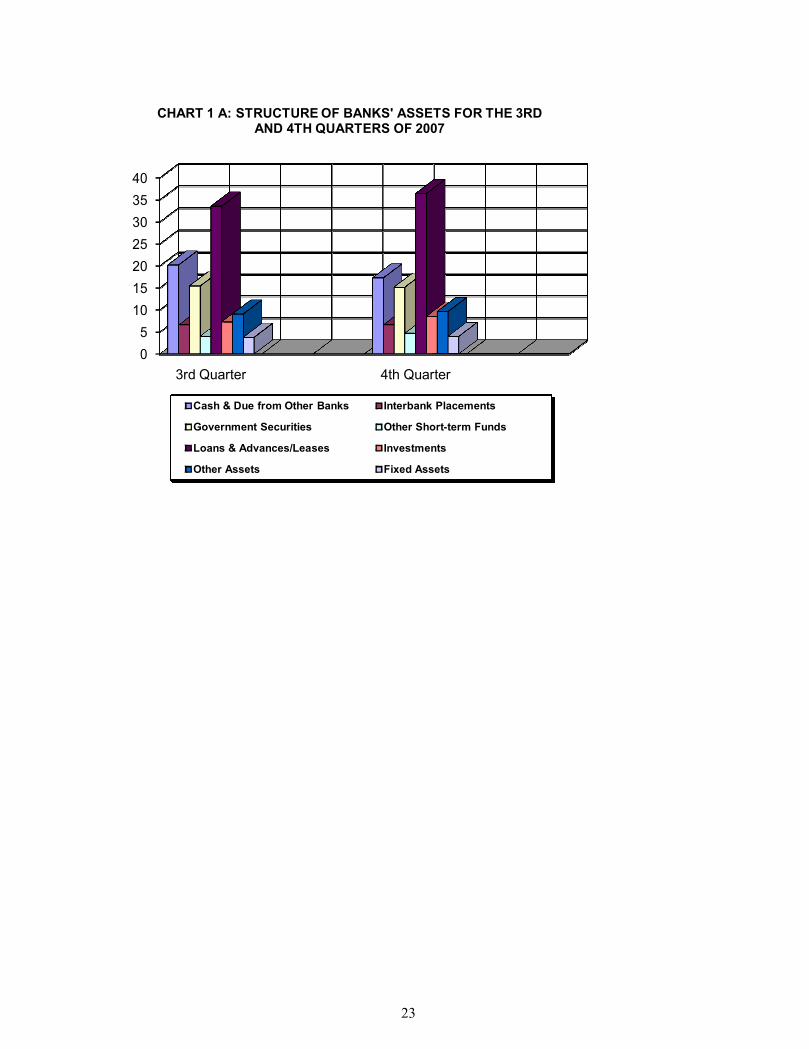

As usual, the largest proportion of total assets during the third quarter of 2007 was

Loans & Advances, which accounted for 33.57 percent. This item increased

slightly by 2.88 percentage points to 36.45 percent as at the end of the fourth

quarter. The relative share of Cash & Due from Other Banks declined from 20.21

percent as at the end of September 2007 to 17.27 percent as at the end of December

2007, which represents a decline of 2.94 percentage points though it retained its

position as the second largest component of total assets. Government Securities

which constituted 15.44 percent of total assets in the third quarter of 2007

maintained its third position on the log. However, its relative contribution declined

0

10

20

30

40

50

60

3rd Quarter 4th Quarter

CHART 1 B: STRUCTURE OF BANKS' LIABILITIES FOR 3RD AND 4TH QUARTERS OF 2007

Total Deposits Interbank Takings CBN Overdrafts

Due to Other Banks Other Borrowed Funds Other Liabilities

Long-term Loans Shareholders' Funds (Unadjusted) Reserves

25

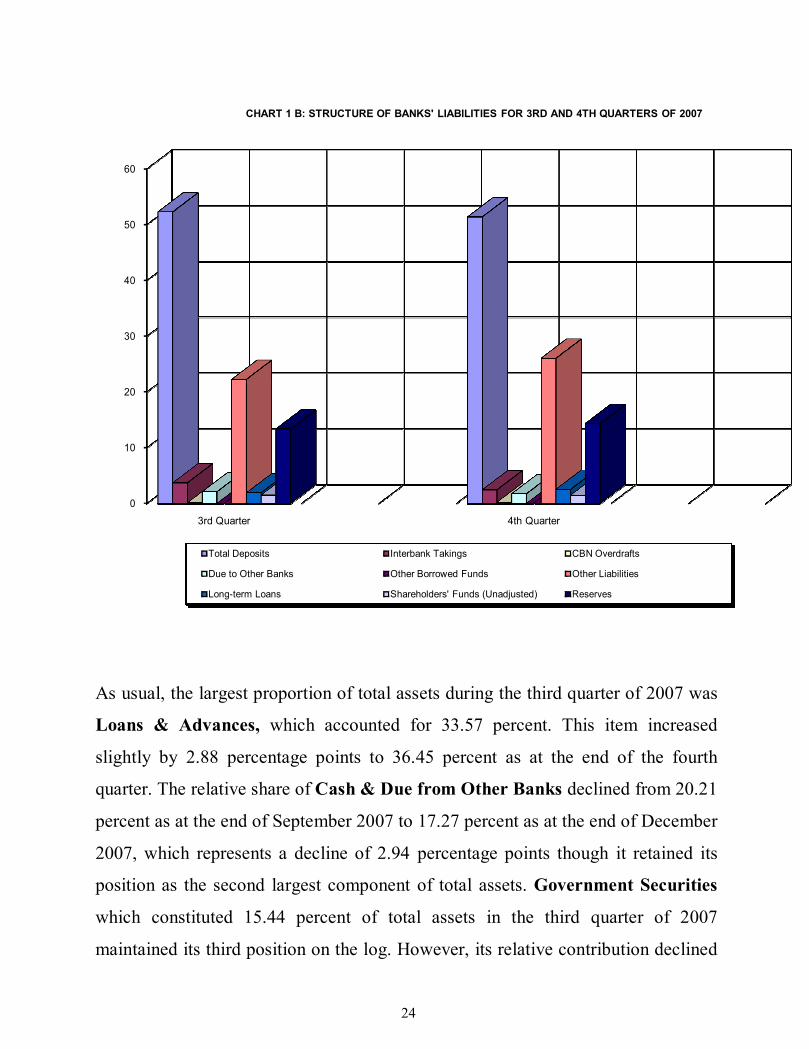

slightly by 0.28 percentage points to 15.18 percent in the fourth quarter but still

maintained its position as the third largest component of total assets. Other

components of the banking industry’s assets whose relative contributions increased

in the fourth quarter of 2007 compared to the situation in the third quarter of 2007

were Other Short-term Funds, Investments, Other Assets and Fixed Assets

which increased by 0.67, 1.26, 0.61, and 0.23 percentage points respectively.

On the liabilities side of the balance sheet, Deposits accounted for 51.36 percent of

the total as at the end of December 2007 but this was lower than its contribution in

the third quarter by 0.90 percentage points. The second largest liability of the

banking industry as at the end of the fourth quarter of 2007 was Other Liabilities

which accounted for 26.01 percent. That was 3.79 percentage points higher than its

contribution in the third quarter. Other sources of funding in the industry during the

fourth quarter of 2007 included the following: Inter-bank Takings (2.43%); Due

to Other Banks (1.71%); Long-term Loans (2.52%); Shareholders’ Funds

(1.45%); and Reserves (14.33%).

3.0 ASSESSMENT OF THE FINANCIAL CONDITION OF INSURED

BANKS

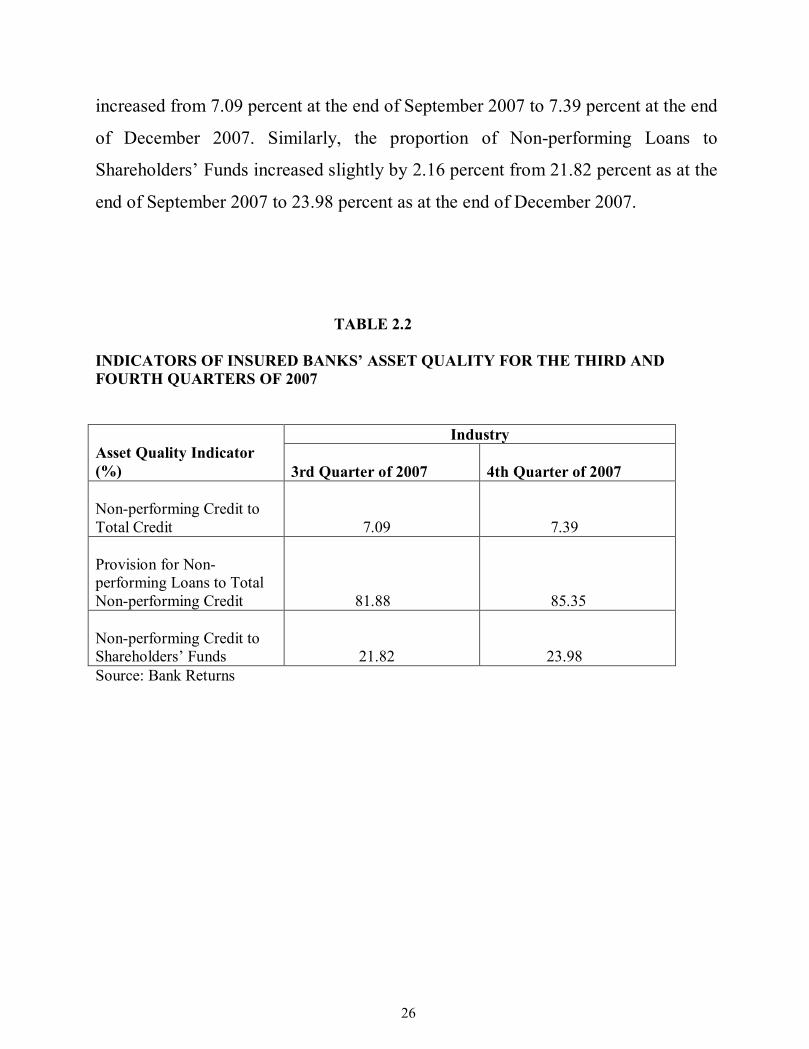

3.1 Asset Quality

The industry’s total loans and advances increased by 13.19 percent from N3.36

trillion as at the end of September 2007 to N3.80 trillion as at the end of December

2007. However, the quality of those assets deteriorated during the same period.

Table 2.2 and Chart 2 present the indicators of insured banks’ asset quality for the

third and fourth quarters of 2007. Non-performing Loans increased by 22.36

percent from N317.07 billion in the third quarter to N388.00 billion in the fourth

quarter of 2007. Thus, the proportion of Non-performing Credit to Total Credit also

26

increased from 7.09 percent at the end of September 2007 to 7.39 percent at the end

of December 2007. Similarly, the proportion of Non-performing Loans to

Shareholders’ Funds increased slightly by 2.16 percent from 21.82 percent as at the

end of September 2007 to 23.98 percent as at the end of December 2007.

TABLE 2.2 INDICATORS OF INSURED BANKS’ ASSET QUALITY FOR THE THIRD AND FOURTH QUARTERS OF 2007 Asset Quality Indicator (%)

Industry 3rd Quarter of 2007

4th Quarter of 2007

Non-performing Credit to Total Credit

7.09

7.39

Provision for Non-performing Loans to Total Non-performing Credit

81.88

85.35

Non-performing Credit to Shareholders’ Funds

21.82

23.98

Source: Bank Returns

27

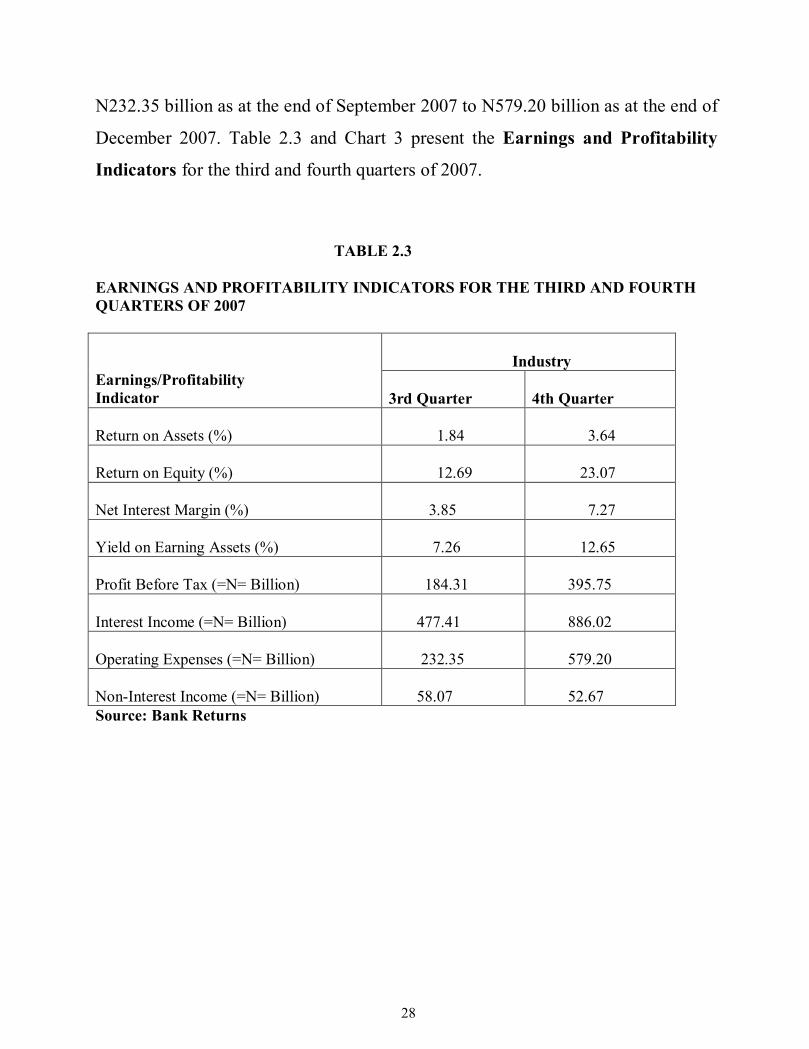

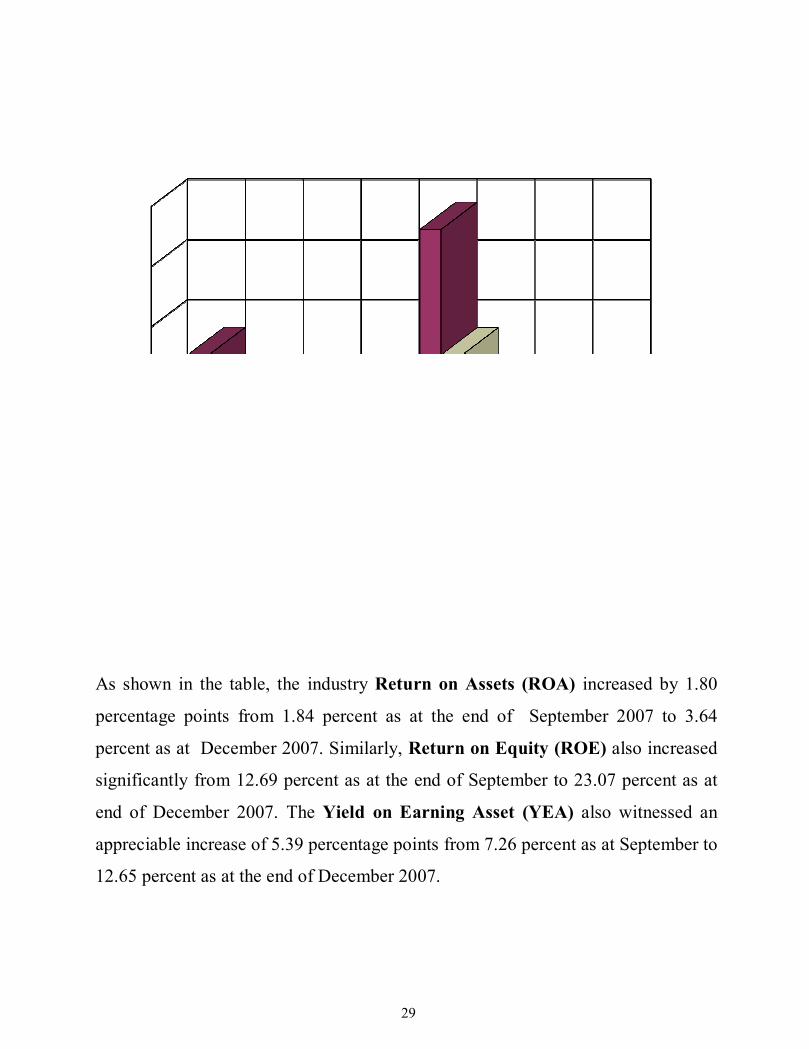

3.2 Earnings and Profitability

The banking industry recorded an 85.59 percent increase in Interest Income from

N477.41 billion in the third quarter to N886.02 billion in the fourth quarter of 2007.

Similarly, Non-Interest Income increased appreciably from N153.20 billion in the

third quarter to N408.97 billion in the fourth quarter of 2007. Thus, total Profit

Before Tax (PBT) of the banking industry increased significantly by 105.49

percent from N184.31 billion as at September to N379.75 billion as at December of

the same year. Following the same trend, Operating Expenses also increased from

0

10

20

30

40

50

60

70

80

90

3rd Quarter 4th Quarter

CHART 2: INSURED BANKS' ASSET QUALITY FOR THE 3RD AND 4TH QUARTERS OF 2007

Non-performing Credit to total Credit

Provision for Non-performing Loans to non-performing Credit

Non-performing Credit to Shareholders' Funds

28

N232.35 billion as at the end of September 2007 to N579.20 billion as at the end of

December 2007. Table 2.3 and Chart 3 present the Earnings and Profitability

Indicators for the third and fourth quarters of 2007.

TABLE 2.3 EARNINGS AND PROFITABILITY INDICATORS FOR THE THIRD AND FOURTH QUARTERS OF 2007 Earnings/Profitability Indicator

Industry 3rd Quarter

4th Quarter

Return on Assets (%)

1.84

3.64

Return on Equity (%)

12.69

23.07

Net Interest Margin (%)

3.85

7.27

Yield on Earning Assets (%)

7.26

12.65

Profit Before Tax (=N= Billion)

184.31

395.75

Interest Income (=N= Billion)

477.41

886.02

Operating Expenses (=N= Billion)

232.35

579.20

Non-Interest Income (=N= Billion)

58.07

52.67

Source: Bank Returns

30

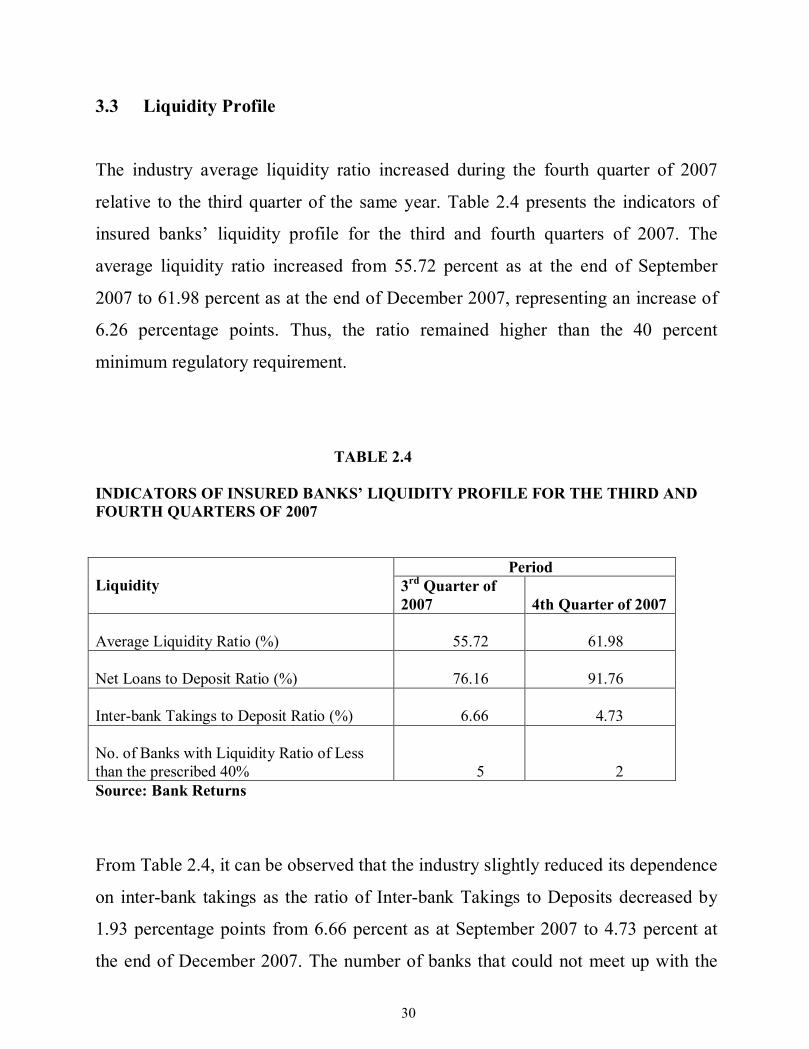

3.3 Liquidity Profile

The industry average liquidity ratio increased during the fourth quarter of 2007

relative to the third quarter of the same year. Table 2.4 presents the indicators of

insured banks’ liquidity profile for the third and fourth quarters of 2007. The

average liquidity ratio increased from 55.72 percent as at the end of September

2007 to 61.98 percent as at the end of December 2007, representing an increase of

6.26 percentage points. Thus, the ratio remained higher than the 40 percent

minimum regulatory requirement.

TABLE 2.4 INDICATORS OF INSURED BANKS’ LIQUIDITY PROFILE FOR THE THIRD AND FOURTH QUARTERS OF 2007 Liquidity

Period 3rd Quarter of 2007

4th Quarter of 2007

Average Liquidity Ratio (%)

55.72

61.98

Net Loans to Deposit Ratio (%)

76.16

91.76

Inter-bank Takings to Deposit Ratio (%)

6.66

4.73

No. of Banks with Liquidity Ratio of Less than the prescribed 40%

5

2

Source: Bank Returns From Table 2.4, it can be observed that the industry slightly reduced its dependence

on inter-bank takings as the ratio of Inter-bank Takings to Deposits decreased by

1.93 percentage points from 6.66 percent as at September 2007 to 4.73 percent at

the end of December 2007. The number of banks that could not meet up with the

31

liquidity ratio of 40 percent prescribed by the regulatory authorities also declined

from 5 in the third quarter to 2 at the end of December 2007.

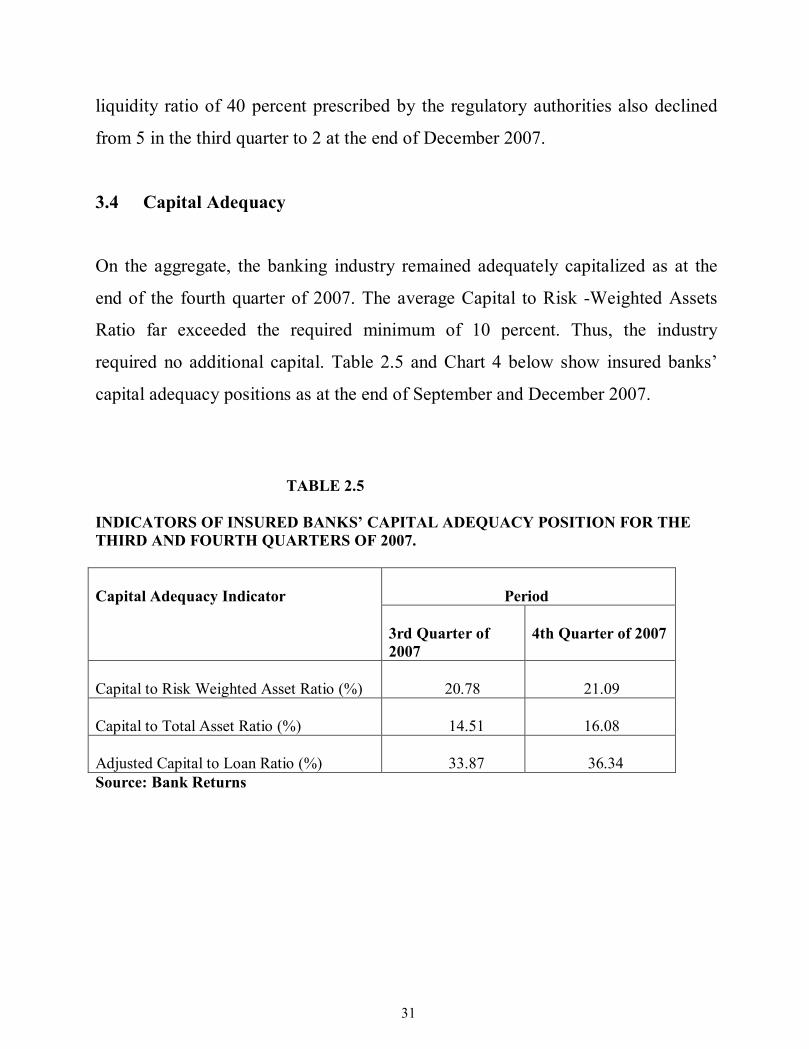

3.4 Capital Adequacy

On the aggregate, the banking industry remained adequately capitalized as at the

end of the fourth quarter of 2007. The average Capital to Risk -Weighted Assets

Ratio far exceeded the required minimum of 10 percent. Thus, the industry

required no additional capital. Table 2.5 and Chart 4 below show insured banks’

capital adequacy positions as at the end of September and December 2007.

TABLE 2.5

INDICATORS OF INSURED BANKS’ CAPITAL ADEQUACY POSITION FOR THE THIRD AND FOURTH QUARTERS OF 2007. Capital Adequacy Indicator

Period 3rd Quarter of 2007

4th Quarter of 2007

Capital to Risk Weighted Asset Ratio (%)

20.78

21.09

Capital to Total Asset Ratio (%)

14.51

16.08

Adjusted Capital to Loan Ratio (%)

33.87

36.34

Source: Bank Returns

32

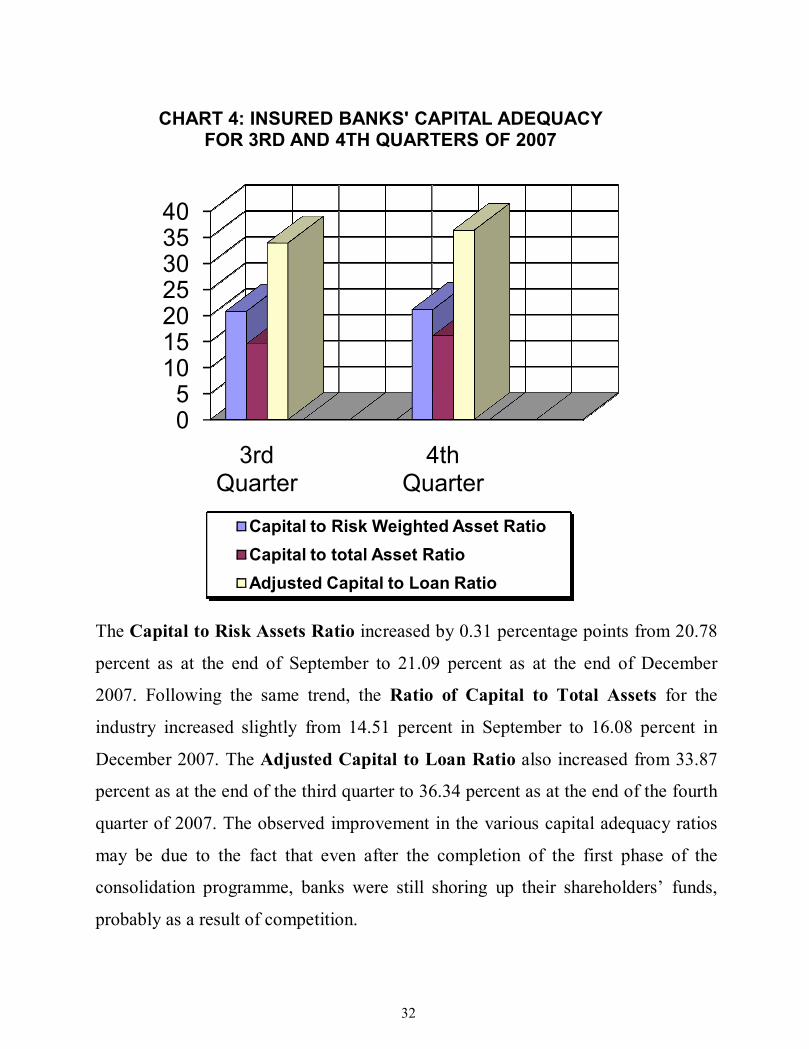

The Capital to Risk Assets Ratio increased by 0.31 percentage points from 20.78

percent as at the end of September to 21.09 percent as at the end of December

2007. Following the same trend, the Ratio of Capital to Total Assets for the

industry increased slightly from 14.51 percent in September to 16.08 percent in

December 2007. The Adjusted Capital to Loan Ratio also increased from 33.87

percent as at the end of the third quarter to 36.34 percent as at the end of the fourth

quarter of 2007. The observed improvement in the various capital adequacy ratios

may be due to the fact that even after the completion of the first phase of the

consolidation programme, banks were still shoring up their shareholders’ funds,

probably as a result of competition.

05

10152025303540

3rd Quarter

4th Quarter

CHART 4: INSURED BANKS' CAPITAL ADEQUACY FOR 3RD AND 4TH QUARTERS OF 2007

Capital to Risk Weighted Asset RatioCapital to total Asset RatioAdjusted Capital to Loan Ratio

33

4.0 CONCLUSION

The overall financial condition and performance of the insured banks during the

fourth quarter of 2007 were better relative to the third quarter. The total assets of

the industry increased during the period under review. On the other hand, there was

a slight increase in the ratio of non-performing credit to total credit during the

period in question. In terms of earnings and profitability, the industry performed

creditably well as profit before tax increased significantly by more than 114.72

percent.

34

PROACTIVE MEASURES TO GUARD AGAINST FRAUD/CASH THEFT IN THE BANKING INDUSTRY AND IN ORGANISATIONS1

BY

G. A. OGUNLEYE, OFR

Managing Director/Chief Executive

1.0 INTRODUCTION

Fraud is recognized as a significant threat facing Governments, Businesses and

Individuals all over the world. In our own environment, fraud appears to have

assumed a tragedy of epic dimension. Fraudsters are not only becoming more

sophisticated, innovative and refined in the planning and execution of their

nefarious act, but are becoming daring as well. Our everyday living experiences

are awash with stories of fraudulent acts being committed in our businesses and on

individuals

Fraud losses impact every business and every household. It results in huge

financial losses to banks and other organizations, their shareholders and customers.

In particular, fraud leads to loss of confidence in business, insolvency or winding

up of businesses, bankruptcy, failure of creditors’ business with attendant loss of

employment, revenue to the government, lenders and investors. The costs of fraud

are always passed on to society in the form of increased customer inconvenience,

opportunity costs, unnecessary high prices for goods and services, and criminal

activities funded by the fraudulent gains. It was established that fraud was one of

the main causes of distress in our banking system that led to the closure of many

banks in the 1990s. As a matter of fact, some recent bank failures were caused by

fraud. 1 Original Paper was delivered at a One-Day Security Enlightenment Forum organized by Police Community Relations Committee, Garki Division, Garki, Abuja, F.C.T

35

The subject of fraud is of great concern to an organization like the Nigerian

Deposit Insurance Corporation ( NDIC) that is saddled with the responsibility of

protecting depositors of banks and other financial institutions. Section 35 and 36

of NDIC Act No. 16 of 2006 require all insured banks in Nigeria to render to the

Corporation, returns on frauds and forgeries or outright theft occurring in their

organizations and also report on any staff dismissed, terminated or advised to retire

on the grounds of fraud. The purpose of obtaining these information is not only for

statistic, but to assist the Corporation in understanding the tricks, antics and tactics

employed by fraudsters to perpetrate their nefarious acts with a view to devising

counter measures that will checkmate and frustrate their efforts. The information is

to also assist in ensuring that fraudsters are not allowed to circulate in our financial

system.

What is fraud? There is no precise legal definition of fraud just as there is no single

offence that can be called fraud. Nevertheless, it is usually taken to have elements

including an intentional and unlawful misrepresentation which causes prejudice,

most often misappropriation, which is the removal of cash, or asset to which the

fraudsters is not entitles as well as false accounting in which records and numbers

reported are falsified to give and create false impression. Black’s Law Dictionary

defines fraud as |an intentional perversion of truth for the purpose of inducing

another in reliance upon it to part with some valuable thing belonging to him or

surrender a legal right”. Fraud is therefore a false representation intending to

mislead, whether by word, conduct that deceives and is intended to deceive another

so that he shall act upon it to legal injury. From the definition, it is obvious that the

subject matter of fraud is very wide ranging from the simple theft or petty cash or

cheques fraud to a major one. Fraud can be committee by employees, customers or

other operating independently or in conspiracy with others inside or outside the

36

organisation.

The purpose of this paper is to examine the modus operandi of fraudsters in

perpetrating fraud in our environment with a view to creating a high level of

awareness and a sense of urgency in order to stem its tide in our businesses by way

of developing and implementing proactive measures. The Second Part of this

paper therefore examines the causes of fraud in our environment while Part Three

looks at the nature and various types of frauds. The paper in Part Four identifies

the needed measures to be taken in order to deter, prevent and detect fraud in a

timely and effective manner. The conclusion is given in Part Five.

2.0 FACTORS CAUSING FRAUD AND ITS EXTENT

There are many factors that cause fraud in Nigeria and these can be classified into

three main groups, namely: institutional, social and individual.

2.1 Institutional Factors

Many institutions unconsciously create conditions that allow fraud to flourish. In

such institutions a lot of loopholes are allowed to exist which fraudsters easily

identify and exploit to commit their acts. The common institutional causes of fraud

are highlighted hereunder.

2.1.1. Inadequate Internal Control

Internal control has long been prescribed as an antidote to fraud. As such, poor

internal control creates incentive and fertile grounds for fraud to thrive.

Weaknesses occur where the controls designed to prevent people using the system,

for an improper or unauthorized purpose, do not operate effectively and efficiently.

The simplest example would be a failure in access controls that allow unauthorized

individuals into the premises or sensitive areas of business, for instance computer

network. Ineffective internal audit, poor staff supervision, absence of segregation

37

of duties and lack of dual control over sensitive documents and keys are all

manifestations of inadequate internal control which aid fraud.

2.1.2. Inexperience of Staff/Inadequate Staff Training

In instances where organization recruit and place their staff in positions far beyond

their capabilities and competence for reasons ranging from political patronage to

family connection, fraud becomes easy to perpetrate through such staff. Because

of their lack of experience and knowledge fraud easily pass through them without

being detected.

Lack of adequate training and re-training of staff on their job schedules result in

poor performance which breeds fraud. Failure to give staff on-the-job training as

well as sending them to relevant courses also lead to unsatisfactory performance

which eventually creates room for fraud.

2.1.3. Employment Disaffection

The motive for fraud is often due to staff disaffection, based on being passed over

for promotion, inadequate pay reward, or a feeling of carrying more than a fair

workload. The number of employees who see themselves threatened and therefore

could turn into potential malefactors has been on the increase mainly due to

management practices that are considered negative and inbibitive. Management

practices bordering on reorganization, restructuring, reengineering and downsizing

or rightsizing have resulted in employee lay-offs. In fact, restructuring in some

organizations seem to have become a way of life with its attendant loss of jobs.

This creates job insecurity in the minds of the generality of employees which in

turn increases the population of potential fraudsters and breeds fraudulent practices

as well.

38

2.1.4. Poor Management

It is the responsibility of board and management to ensure the security and integrity

of the business assets by putting in place appropriate control and procedures.

Where a management is ineffective, incompetent or self-serving, the tendency is

for the controls not to be in place or to be overridden and compromised thereby

allowing fraud to flourish. In such organizations, managements are not only

facilitators but active collaborations in perpetrating fraud. It is therefore not

surprising that those organizations record higher incidence of fraud than those with

effective management.

Management style is also known to be a factor in committing fraud. An autocratic,

aggressive or domineering management facilitates overriding of controls and

prevents questioning by others. This style may end up permeating the whole

organization thereby creating a closed environment where corporate policies and

culture yield to individual’s whims and caprices, and fraud in this circumstance can

go unchallenged. Where performance goals set by management appear overly

aggressive given conditions in the marketplace, for instance the unrealistic deposit

targets being given by banks to their staff, breeds all sorts of fraud.

2.1.5. Negligence of Staff/Customers

Staff negligence is found to be a cause of fraud in many instances. Negligence

itself is a product of several factors, including poor supervision, lack of technical

knowledge, apathy, workload, pressure, etc.

Similar, negligence of customers is also a great factor in perpetrating fraud.

Customers who fail to adequately secure documents and other assets related to their

business transactions, e.g. cheque books, stock records, company seals, etc, create

conductive environment for fraud. Failure to also carry out accounts reconciliation

39

assists in facilitating fraud.

2.1.6. Automation and Computerization

Computerization and automation of business processes are known to facilitate

fraud especially where there is no proper project planning and execution including

adequate training of people to use the system. Computers have become powerful

instruments and ready tools in the hands of fraudsters for perpetrating fraud

because of ease in usage and difficulty in tracing trail.

2.2 Social Factors

2.2.1. Societal Values

The value system in our society today is such that reputation, respect, honour and

other social status are conferred on people mainly on the basis of their material

wealth. Access to political power, chieftaincy titles, religious positions and

influence are seen to be for money bags. People are no longer respected for

honesty, integrity and wisdom. Instead, recognition is accorded to materialism.

People are therefore driven to commit fraud as a means of easy acquisition of

money and properly which in our today’s world translate into recognition and

power.

2.2.2. Poor Economy

It is being argued that the poor state of our economy has been a contributory factor

to fraud perpetration. The level of unemployment and poverty in the polity due to

recession has been a major cause for concern to all and sundry. Hash economic

conditions can drive people to commit fraud. The individual must necessarily

satisfy the basic needs of food, cloth and shelter otherwise he will readily succumb

to fraud if opportunity presents itself.

40

2.2.3. Slow and Tortuous Legal Process

The law enforcement and judicial process of bringing fraudsters to justice has been

extremely slow and tortuous. Cases of fraud reported to the police take a long time

to investigate and prosecute. Many other cases are not investigated to prosecution

to serve as deterrent. The delay in investigation and prosecution can perhaps be

explained because the police and courts are poorly equipped and remunerated.

However, the understanding that our laws are weak in promptly bringing fraudsters

to justice send wrong signals that people can commit fraud and get away with it.

2.3 Individual Factors

These are factors that pertain to the person, that is, those that are peculiar to the

individual who may encourage him to live a fraudulent life. These factors include;

i) Biological make-up – e.g. Kleptomania

ii) Poor moral upbringing

iii) Criminal background, and

iv) Weak mind

The above factors are identifies to cause fraud in many instances.

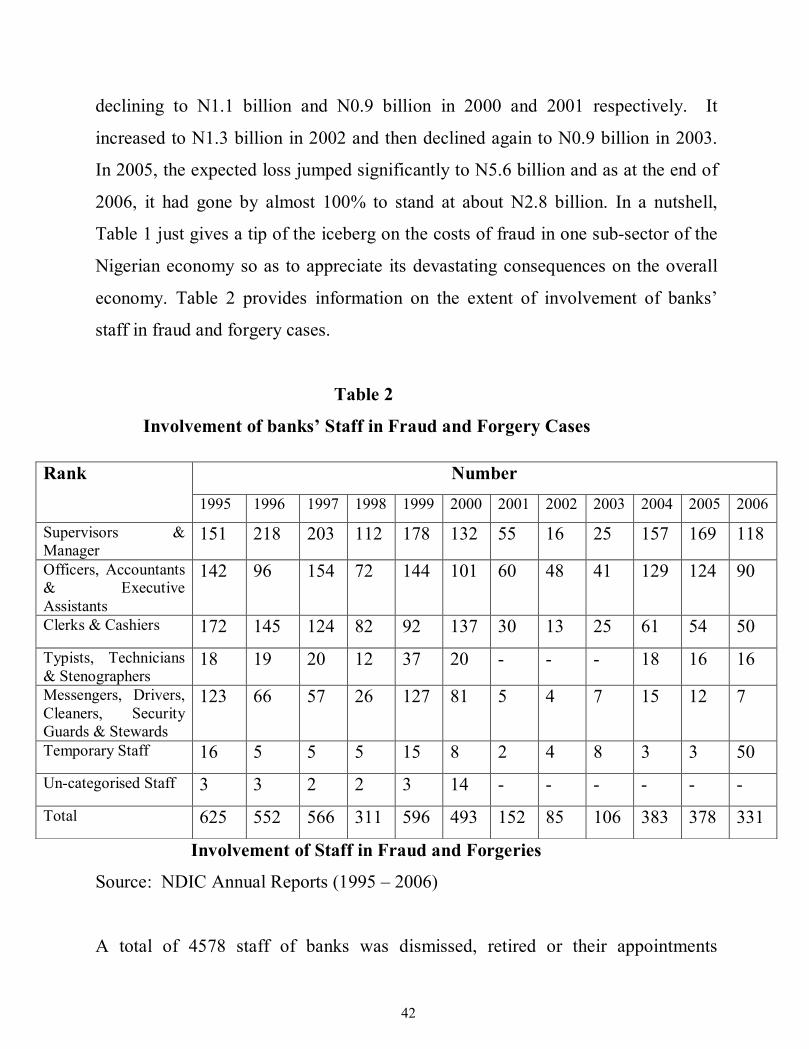

2.4 Extent of Fraud in the Economy

The extent of the havoc that fraud wrecks on the Nigerian economy is difficult to

determine for reason of lack of comprehensive and reliable data. However, if the

information available from the banking industry can be regarded as a good

representation, it is obvious that the damage to the economy by means of fraud is

colossal. It can be said to be the most costly of all criminal activities in the

country. Table 1 gives the total number of fraud cases, total amount involved and

total expected loss in the banking industry for the years 1995 to 2003.

41

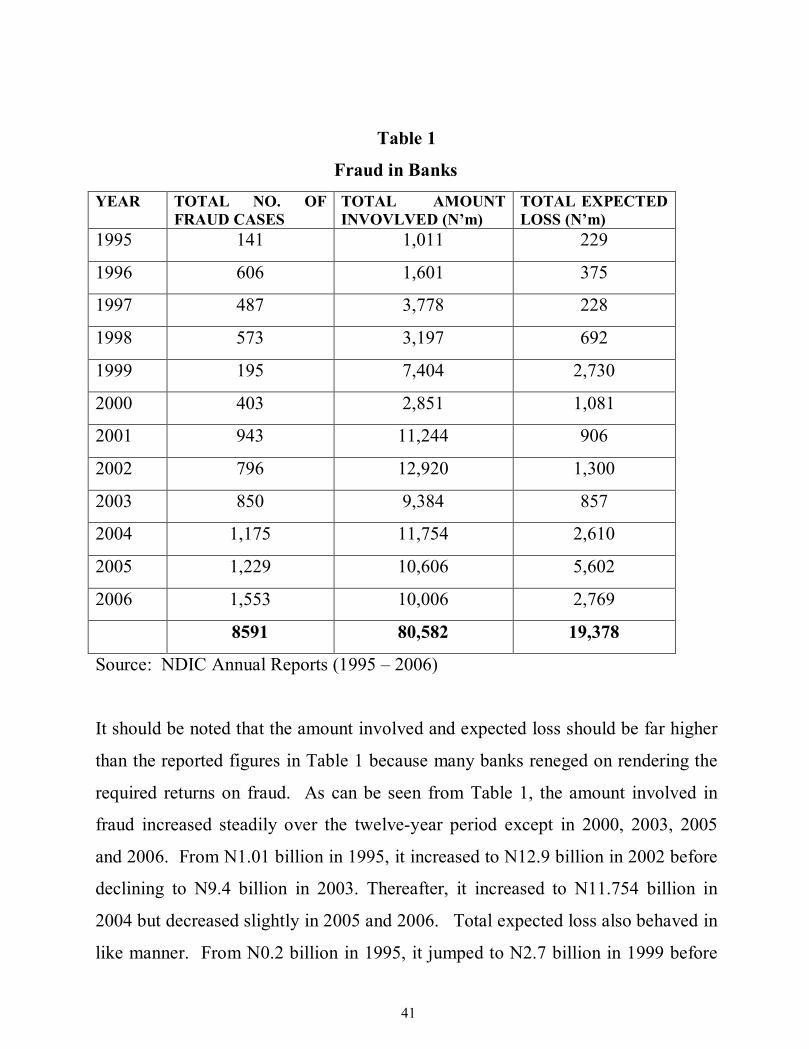

Table 1

Fraud in Banks

YEAR TOTAL NO. OF FRAUD CASES

TOTAL AMOUNT INVOVLVED (N’m)

TOTAL EXPECTED LOSS (N’m)

1995 141 1,011 229

1996 606 1,601 375

1997 487 3,778 228

1998 573 3,197 692

1999 195 7,404 2,730

2000 403 2,851 1,081

2001 943 11,244 906

2002 796 12,920 1,300

2003 850 9,384 857

2004 1,175 11,754 2,610

2005 1,229 10,606 5,602

2006 1,553 10,006 2,769

8591 80,582 19,378

Source: NDIC Annual Reports (1995 – 2006)

It should be noted that the amount involved and expected loss should be far higher

than the reported figures in Table 1 because many banks reneged on rendering the

required returns on fraud. As can be seen from Table 1, the amount involved in

fraud increased steadily over the twelve-year period except in 2000, 2003, 2005

and 2006. From N1.01 billion in 1995, it increased to N12.9 billion in 2002 before

declining to N9.4 billion in 2003. Thereafter, it increased to N11.754 billion in

2004 but decreased slightly in 2005 and 2006. Total expected loss also behaved in

like manner. From N0.2 billion in 1995, it jumped to N2.7 billion in 1999 before

42

declining to N1.1 billion and N0.9 billion in 2000 and 2001 respectively. It

increased to N1.3 billion in 2002 and then declined again to N0.9 billion in 2003.

In 2005, the expected loss jumped significantly to N5.6 billion and as at the end of

2006, it had gone by almost 100% to stand at about N2.8 billion. In a nutshell,

Table 1 just gives a tip of the iceberg on the costs of fraud in one sub-sector of the

Nigerian economy so as to appreciate its devastating consequences on the overall

economy. Table 2 provides information on the extent of involvement of banks’

staff in fraud and forgery cases.

Table 2

Involvement of banks’ Staff in Fraud and Forgery Cases

Involvement of Staff in Fraud and Forgeries

Source: NDIC Annual Reports (1995 – 2006)

A total of 4578 staff of banks was dismissed, retired or their appointments

Rank Number 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Supervisors & Manager

151 218 203 112 178 132 55 16 25 157 169 118

Officers, Accountants & Executive Assistants

142 96 154 72 144 101 60 48 41 129 124 90

Clerks & Cashiers 172 145 124 82 92 137 30 13 25 61 54 50

Typists, Technicians & Stenographers

18 19 20 12 37 20 - - - 18 16 16

Messengers, Drivers, Cleaners, Security Guards & Stewards

123 66 57 26 127 81 5 4 7 15 12 7

Temporary Staff 16 5 5 5 15 8 2 4 8 3 3 50 Un-categorised Staff 3 3 2 2 3 14 - - - - - -

Total 625 552 566 311 596 493 152 85 106 383 378 331

43

terminated because of their involvement in fraudulent activities during 1995 to

2006 as can be seen from Table 2. In 1995, 625 members of staff of banks were

involved in fraud. That number reduced to 311 by the end of 1998 only to increase

substantially to 596 in 1999. In 2002, only 85 staff of different grades were

involved in fraud or the other, the least during the twelve-year period. Only 383,

378 and 331 staff were involved in fraud in 2004, 2005 and 2006. As can be

observed from table, banks’ staff involvement n fraud and forgeries did not follow

any pattern. However, the noticeable decrease in the number of banks’ staff

involved in fraud in some of the years could be partly attributed to the failure of

banks to render the required return. The decrease notwithstanding, the amount

involved in fraud in some of the years was astronomical when compared with other

years when Table 1 and 2 are compared.

3.0 NATURE AND TYPES OF FRAUD

It is of importance to understand the nature and types of fraud as that will be of

great assistance to organizations in checkmating and combating it. Generally,

fraud is categorized on the basis of its perpetrators. This way, it could be internal,

external or mixed. Internal perpetrators of fraud are staff under the employment of

the organization either as directors, management staff, officers, supervisors or other

employees while the external ones are those outside the organization. Mixed

perpetrators are those involving members of staff of an organization colluding with

outsiders to carry out their fraudulent activities. Another way of classifying fraud

is on the basis of methods employed in perpetrating it. Given the sophistication,

inventiveness and ingenuity of fraudsters in devising ways to carry out their trade,

it will be practically impossible to list and discuss all of them. However, the most

important and common ones are highlighted hereunder.

44

3.1. Theft

Theft involves the removal of cash or assets to which fraudster is not entitled. Any

business asset can be stolen by staff or their parties. The nature of theft may vary

according to the asset being misappropriated and the identity of the perpetrator.

The most common types of theft in our system are:

i) Direct theft of cash or any asset of the business, e.g. stock, computer

equipment, stationary, intellectual property, price lists or customer lists,

etc.

ii) False expense claim which can be anything from claiming for private

entertainment expenses to large scale projects.

iii) Payroll fraud involving the diversion of ex-employees or fictitious

employee payments to the benefits of perpetrators.

iv) Rolling debtors’ receipts that is misappropriating debtors’ receipts and

substituting subsequent receipts.

v) Payments against fictitious jobs or supplies.

vi) Inflation of contracts.

3.2. False Accounting

The main aim of false accounting is to present the results and affairs of an

organization in a better light than the reality. Frequently, there are commercial

pressures to report an unrealistic level of earnings. Whatever the purpose, the

features that are common to all cases of false accounting are the falsification of

records, alteration of figures, and perhaps the keeping of two or more sets of books.

The reasons for all these include:

i) to obtain more financing from banks and creditors;

ii) to manipulate share prices;

iii) to improve results over the year-end and generate performance related

remuneration to which the perpetrator would not otherwise be entitled;

45

iv) to cover up a theft;

v) to attract customers by appearing to be more successful than in reality;

and

vi) to prevent or delay intervention by supervisors/regulators.

This is a typical “corporate fraud” and the amount involved which is colossal, is

hardly reported. The management is usually the architect of this type of fraud.

3.3. Advance Fee Fraud (“419”)

This is a very popular type of fraud in our environment. It is internationally

referred to as Nigerian scam. A method of perpetrating this type of fraud is for

numerous letters to be sent to unsuspecting individuals by fraudsters soliciting for

assistance to transfer large sum of money belonging to them but which is being

held by government. The assistance requested will be in the form of advance fee

which will be uses to settle perceived government officials and the details of the

off-shore foreign accounts of such individuals.

3.4. Computer Fraud

Computer fraud refers to fraud being committed using computer rather than

traditional method of paper and pen. This type of fraud includes:

i) Disguising the true nature of a transaction by manipulating input and or

data including tampering with programme.

ii) Hacking into an organisation’s computer system to steal or manipulate

information.

iii) Unauthorised electronic transfer.

iv) Posing as a legitimate business on the internet using it to defraud the

public.

46

v) Theft of intellectual property, e.g. engineering drawings, trade secrets, e-

books, music, etc.

3.5. Foreign Exchange (FX) Fraud

Foreign exchange transactions have been veritable source of fraud as a result of

sharp practices involving banks and other parties. The most common types

include:

i) Round Tripping – This arise in a situation where banks obtain FX through

official sources at a regulated exchange rate for qualified transaction and

simply sell to autonomous users at a black market exchange rate.

ii) Documentary credit fraud – This can be quite varied and will involve

forgery of FX documents, e.g. import duty receipts, shipping documents,

Clean Report of Inspection and attested invoices. It can be carried out

with the objective of transferring FX for non-existent transaction or by

way of over invoicing.

iii) Travelers’ Cheque (TC) Fraud – This is done by illegal purchase of TCs

which are then uploaded in the black market.

3.6. Loan Fraud

Loans and other forms of credit extensions to business and individual scustomers

constitute the main function of financial institutions. In the process of credit

extension, fraud may occur at any stage, from the first interaction between the

customer and the bank to the final payment of the credit. Loan fraud which is a

typical type of”corporate fraud” in banks occurs when credit is extended without

following the credit policy, law, rules and regulations. Inadequate or absence of

collaterals for loans which by law or policy should be fully collateralized and

diversion of loan for other uses different from which it is given constitute fraud.

Advanced perpetrations of credit fraud go to the extent of applying credit facility

47

approved for one customer to the credit of another who is often unrelated to the

first customer. That is to say, a credit facility for a customer “A” yet to be drawn

down is diverted fro a customer “B”. Failure to make provision in accordance with

Prudential Guidelines also constitutes fraud. The amount involved in loan fraud is

gargantuan.

3.7. Cheque Fraud

The use of cheques as a means of paying for financial obligations is an essential

feature of modern economy. Cheque fraud is now common involving millions of

naira annually. Common types of cheque are personal, business, government,

travelers’ certified, draft and counter cheques, with each having its own

characteristics and vulnerabilities or fraudulent use. The most common cheque

fraud involves that are stolen, forged, counterfeited, altered or cloned.

3.8. Money Laundering Fraud

This is a means to conceal the existence, source or use of illegally-obtained money

by concerting the cash into untraceable transactions. The cash is disguised to make

the income appear legitimate. Fraudsters are known to employ various means in

order to launder their money. These include depositing laundered funds with

banks, using illegally-obtained money to purchase stocks in the capital market,

investing funds of questionable source in real assets, etc.

3.9. Manufacturers Fraud

Manufacturers in the country have been discovered to disregard adherences to

stipulated standards, with the result that more quantity or less quality of the same

product is unleashed into the market for unjust gain.

3.10. Identity Fraud

48

This type of fraud is committed by individuals who assume names and identities of

others living or dead with a view to gaining employment, using their stolen credit

or value cards to secure some monetary benefits like pension or other payments.

3.11. Insurance Fraud

In this type of fraud, insurance agents sell policies to clients and refuse to deliver

premium collected to the insurance companies, or state-manage accidents in order

to replace old or defective vehicles, or “causing firs to come from heaven” to burn

houses after previously removing choice items of value for the purpose of making

undue claims from the insurance companies.

4.0 MEASURES TO GUARD AGAINST FRAUD

The best defenses against the risk of fraud in any organization are proactive

measures. For an organization to create a corporate environement that prevents,

deters and timely detects fraud, it needs to understand why fraud occur, types and

methods of perpetration as well as identify its business areas that are at risk and

implementing appropriate procedures to address them. It is a well established fact

that before fraud can take place there must be:

i) an item worth stealing;

ii) a potential perpetrator willing to steal; and

iii) an opportunity for the crime to take place.

It follows therefore that successful prevention of fraud in an organization lies in

the isolation of the perpetrators from the assets and from the opportunity and

knowledge required for access. In other words, walls of policies, procedures,

devices and controls need to be erected to surround and isolate each factor in the

equation to combat fraud. It is for this reason that the system of internal control

is identified as very critical in minimizing the incidence of fraud in any business

49

organization. Internal control can be defined as the whole system of controls,

financial and otherwise, established by the management to carry on the business

of the enterprise in an orderly and efficient manner, ensure adherence to

management polices, safeguard the assets and secure as far as possible the

completeness and accuracy of the records.

Management has overall responsibility for ensuring the security and integrity of

the assets of a business by putting in place appropriate controls and review

procedures. However, it needs to be emphasized that the controls required for

each business will be specific to that business, depending on the way in which

departments or processes function, the systems in place, the number of

personnel and so on. That is to say, every organization needs to assess and

determine the area in which fraud could occur and implement the controls that

are considered necessary to mitigate it. Some of the direct controls that need to

be considered include:

i) Timely and periodic reconciliation of bank accounts, cash in hand,

inventory and other items of value.

ii) Dual signatories and authorization limits.

iii) Segregation of duties.

iv) Management review.

4.1. Other Organisational Measures

Other measures that should be adopted in the fight against fraud are those

relating to the attitude and culture of the organization and the way in which it

deals with fraud. These are indirect controls which convey the message that

fraud will be detected, that action will be taken and that the repercussions could

be severe. Some of these measures include:

50

4.1.1. Physical Security/Access Controls

Operating effective access controls is essential, be it within the premises

themselves, particular departments or offices, computer systems, database, bank

accounts or other areas critical to the business. The role of security tags, which

allow someone’s progress around the building to be monitored, CCTC cameras

or other surveillance equipment, should not be underestimated. Particular

attention should be paid to access controls over computer systems, which should

include the rigorous use of passwords, firewalls and/or other measures to

prevent or detect hacking into the system.

4.1.2. Effective Internal Audit

An effective internal control function is very critical in managing fraud risk in

any organization. For maximum effectiveness, ensure that your internal audit

department has enough resources to carryout its functions, that it is focusing on

the most important risk area of your business, that it is independent and free to

establish the scope of its activities without let or hindrances by management,

and that it is reporting fully and directly to the highest authority, ideally the

board of directors or its audit committee. Internal auditors should be given

comprehensive training in fraud prevention, deterrence and detection.

4.1.3. Pre-employment Screening

The fight against fraud should start even before a new employee joins the

organization. You must have an effective recruitment policy which ensures that

employees are recruited based on their capabilities, competence and integrity

rather than exterior motives. References must be sought and checked

thoroughly, while temporary staff should be vetted just like permanent ones.

Background checks should be conducted on employees to assure of their

integrity.

51

4.1.4. Conducive Working Environment

The motive for internal fraud is often employee dissatisfaction, personal

financial problem, and gambling, drugs or drink problems. Create a favourable

working environment to ensure that employees are not placed under undue

duress to reach impossible goals and that they are not intimidated by supervisors

or superior officers that they are afraid to challenge instructions to commit

fraud. Let there be procedures that give them the opportunity to air their

grievances and discuss aspirations and concerns. Also ensure that your

organization has an “employee assistance program” which the staff trust to be

confidential and can help them deal with their personal problems. In effect,

create a culture of openness, transparency and trust as against that of secrecy,

mistrust and autocracy.

4.1.5. Fraud Policy

There should be fraud policy in organizations. Fraud policy is a formal, written

statement recording the organisation’s attitude to fraud. It may be part of

general ethics statement or code of conduct that records the way in which the

organization deals with its customers, suppliers and staff. In particular, the

policy should make it clear that fraud is unacceptable and that all instances of

suspected fraud will be treated seriously and with dispatch.

4.1.6. Make It Known How You Deal With Fraud

When fraud occurs, resolve it promptly and effectively. Then communicate to

employees how it was resolved. While care should be taken to avoid

defamation, communication of the outcome reinforces in employees the

organisation’s commitment to the issue of fraud and gives them practical

example to help make appropriate decisions in the future and to deter

52

recurrence.

4.1.7. Fraud Training

Promote fraud training in your organizations. All new employees should be

provided with the organisation’s fraud policy statement. Fraud deterrence,

prevention and detection programs that deal with practical issues should be

included in your induction and continuous career training.

4.1.8. Whistle-blowing Policy

Employees and third parties should be encouraged to report their suspicions of

fraud or other irregular activity without fear or reprisal. To encourage

reporting, whether anonymous or not, an E-mail or telephone fraud hotline can

be implemented. The existence of such facilities should be well publicized and

their roles in deterring or detecting fraud should be made known to all.

Information should be treated on a confidential basis to reassured reporters, and

management should be seen to be fair and just in handling such confidential

information.

4.1.9. Contingency Plan

It is important that every company has in place a contingency plan, which sets

out the steps that should be taken in the even that fraud is suspected. The

existence of the plan, and the fact that it will make clear to prospective

fraudsters that the company will take swift, decisive action and involve the

police or appropriate authorities, should serve as an effective deterrent.

4.1.10. Controls over the IT environment

Significant amounts of information are now held in database and other formats

to aid communication within companies. If improperly managed, however, this

53

concentration of information provides an increased risk. Sensitive data could be

compromised and end up in the hands of unauthorized individuals. Necessary

physical and logical access control over the computer system should be

provided.

4.1.11. Insurance policy

In addition to taking measures to minimize the risk of fraud, management