navigating the “promised land”

TRANSCRIPT

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

Navigating the “Promised Land”Barry KublinChief Executive Officer, Benefit Plans Administrative Services, Inc.

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

2

WELCOME and THANK YOU• Attendees• Sponsors – conf and industry• Guest Speakers• BPAS Staff

– Developing and Supporting Advisor Relationships— Developing Program Content— Marketing the Program— Logistics

• Success Agency• BTI Travel

2016 BPAS Partner Conference

3

AGENDA – Navigating the “Promised Land”

• BPAS Firm Profile• Navigating the “Promised Land”• Global Pension Index – rankings – Adequacy– Sustainability– Integrity

• Re-setting the “Promise”

2016 BPAS Partner Conference

4

AGENDA – Navigating the “Promised Land”

• Government Solutions– State-run IRA– State-run MEP– Fiduciary Regs

• Private Sector Solutions– VEBA/HRA, HSA– MEP/MET– Universal Availability/Auto Plans– Reducing Leakage

2016 BPAS Partner Conference

5

AGENDA – Navigating the “Promised Land”

• Government/Private Solutions– It is Possible!– Top Heavy– MEP Regs– Terminated Participants– Public Sector Plans– CBO Scoring

• Delivering on Tomorrow’s “Promise” – Moving Forward

2016 BPAS Partner Conference

6

Firm Profile

• NY (Rochester, Syracuse, Utica, New York City)

• NJ (East Hanover)• PA (Philadelphia, Pittsburgh)• TX (Houston)• PR (San Juan)• 4 staff members in Seattle/Portland

2016 BPAS Partner Conference

$19 billion assets under custody

4,000 engagements

400,000 plan participants

10 Offices

275 professionals

7

BPAS Lines of Business

• Plan Administration & Recordkeeping Services— Bundled administration, recordkeeping and custody services for

defined contribution-type plans and IRAs• TPA Services

— Unbundled retirement plan services in support of balance forward and third-party recordkeeping plans

• Actuarial & Pension Services— Actuarial services for traditional defined benefit, cash balance,

executive supplemental retirement and other post-retirement benefit plans, including retiree medical

2016 BPAS Partner Conference

8

BPAS Lines of Business• Healthcare Consulting Services– Plan design, actuarial consulting, RFP and analysis, and

contracting with service providers in select markets.

• VEBA & HRA/HSA Services—Bundled administration for VEBA/HRA retiree medical

plans, FSA and Transit plans, and HSA accounts• Fiduciary Services

— ERISA 3(21) and 3(38) services for retirement and VEBA plans, in support of brokers and directed trustees

2016 BPAS Partner Conference

9

BPAS Lines of Business

• AutoRollovers and MyPlanLoan Services— Service bureaus supporting EGTRAA IRA services and non-payroll-

deduction loan administration• BPAS Trust Company of Puerto Rico

— Directed Trustee services for PR 1081 plans• Hand Benefits & Trust, a BPAS Company

— Institutional Trust services, including Collective Investment Fund administration

2016 BPAS Partner Conference

10

BPAS Premier Services

2016 BPAS Partner Conference

One Company. One Call.• DC Auto Enroll/Escalation Plans• DC Plans with Employer Securities• Multiple Employer Plans/Multiple Employer Trusts• VEBA/HRA• PR 1081 Plans• Cash Balance Plans• Collective Investment Fund Administration

11

Falling Short on the “Promise” – Municipal Bankruptcies

2016 BPAS Partner Conference

Cities, towns, and countries are shown in red. Utility authorities and other municipalities are displayed in black. Multiple municipalities have filed for bankruptcy in some cities, such as Omaha, NE, so not all markers are visible without zooming in on the map.

12

Falling Short on the “Promise” – Unfunded Liabilities

2016 BPAS Partner Conference

State level unfunded OPEB liabilities .85 trillionState level net pension liabilities 3.1 trillionFederal net OPEB and pension liabilities 6.0 trillionMedicare net liabilities 35.0 trillionSocial Security net liabilities 13.55 trillion$58.5 trillion amounts to $175,000 per person (plus fed/state/muni debt)

Sources: Gabriel, Roeder, Smith & Company. The Social Security and Medicare Boards of Trustees' 2014 report

13

Global Pension Index

• Annual report issued by the Australian Centre for Financial Studies, in partnership with Mercer — Report issued October 2015

• A comparison of retirement income systems in 25 countries ranked by “Adequacy, Sustainability and Integrity”

2016 BPAS Partner Conference

14

Global Pension Index

Adequacy (40%)• Is there favorable tax treatment of voluntary

retirement savings?• Is there a minimum access age to receive benefits

from the private plans (leakage)?• Portability and continuation of benefits for

employees who change their employment• Proportion of private retirement benefit that must be

taken as an income stream• Percentage of investments held in growth assets

2016 BPAS Partner Conference

15

Global Pension Index

Sustainability (35%)• Contribution rates (level of advance funding)• Coverage and participation rates• Level of government debt, given the key role of public

pensions• Labor force participation rates amongst older workers• Ratio of workers to retirees

2016 BPAS Partner Conference

16

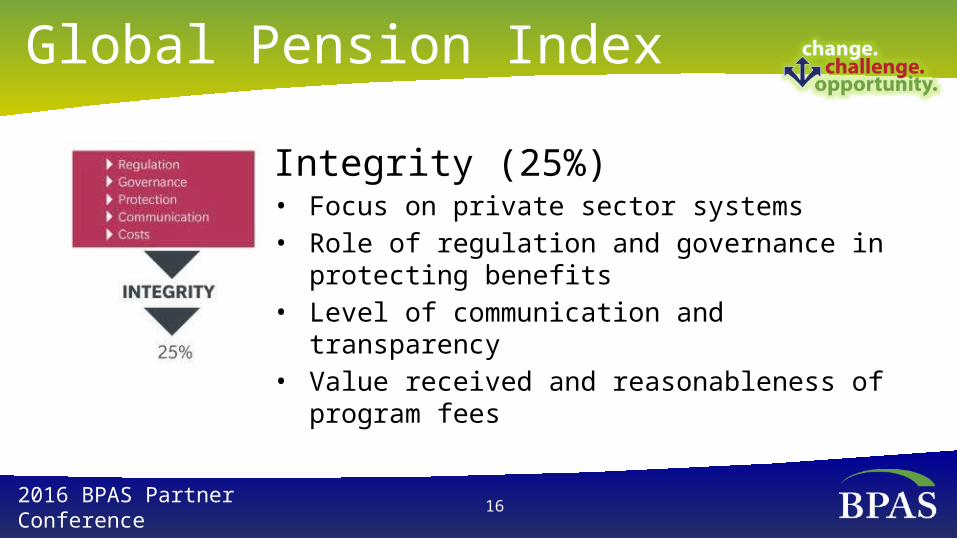

Global Pension Index

Integrity (25%)• Focus on private sector systems• Role of regulation and governance in protecting

benefits• Level of communication and transparency• Value received and reasonableness of program fees

2016 BPAS Partner Conference

17

Global Pension Index

Overall Adequacy Sustainability Integrity

1st Denmark Australia Denmark Finland

2nd Netherlands Netherlands Netherlands Netherlands

3rd Sweden Canada Sweden Australia

U.S. 14th 20th 10th 20th

23rd Japan S. Korea Japan China

24th S. Korea Indonesia Austria S. Korea

25th India India Italy Mexico

2016 BPAS Partner Conference

18

Relevance of Global Comparisons on U.S. Retirement Policy?

• Presented to Parliament by the Secretary of State for Work and Pensions by Command of Her Majesty, March 2014.

• As of April 2015:– a 0.75 percent default fund charge cap on funds under

management, excluding transaction costs, for all qualifying schemes. Any commission must not take member-borne charges above this level.

2016 BPAS Partner Conference

19

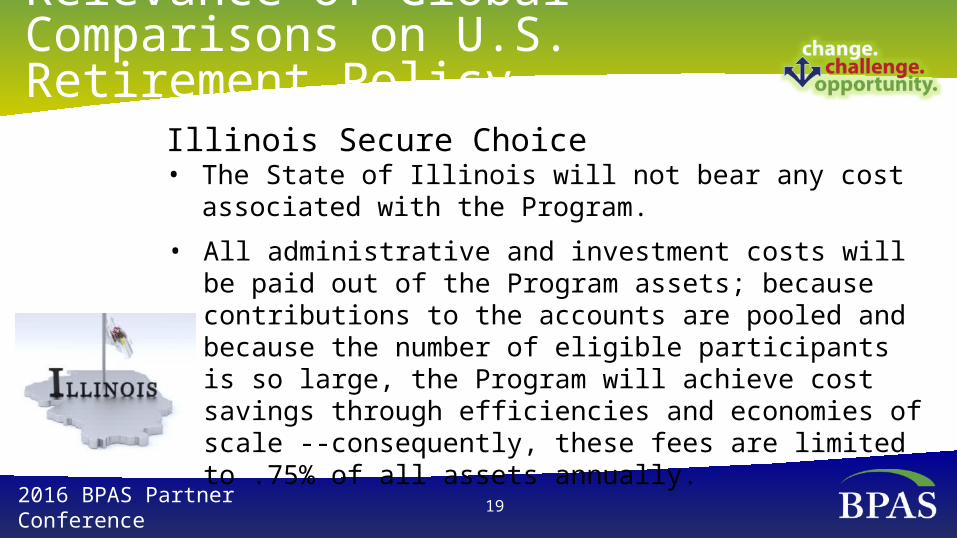

Relevance of Global Comparisons on U.S. Retirement Policy

Illinois Secure Choice• The State of Illinois will not bear any cost associated with the

Program.

2016 BPAS Partner Conference

• All administrative and investment costs will be paid out of the Program assets; because contributions to the accounts are pooled and because the number of eligible participants is so large, the Program will achieve cost savings through efficiencies and economies of scale --consequently, these fees are limited to .75% of all assets annually.

20

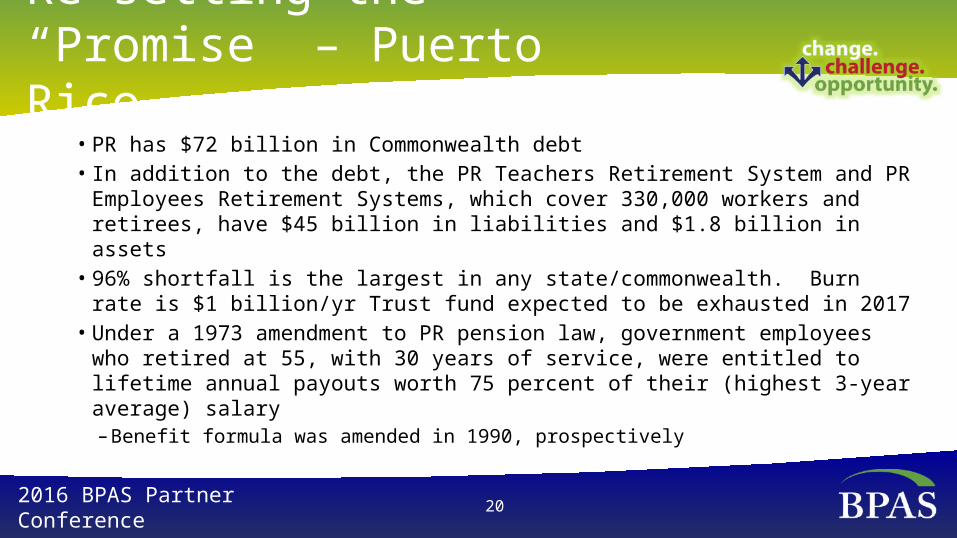

Re-setting the “Promise” – Puerto Rico

• PR has $72 billion in Commonwealth debt• In addition to the debt, the PR Teachers Retirement System and PR

Employees Retirement Systems, which cover 330,000 workers and retirees, have $45 billion in liabilities and $1.8 billion in assets

• 96% shortfall is the largest in any state/commonwealth. Burn rate is $1 billion/yr Trust fund expected to be exhausted in 2017

• Under a 1973 amendment to PR pension law, government employees who retired at 55, with 30 years of service, were entitled to lifetime annual payouts worth 75 percent of their (highest 3-year average) salary– Benefit formula was amended in 1990, prospectively

2016 BPAS Partner Conference

21

Re-setting the “Promise” – Puerto Rico

• Aggressive sale of pension obligation bonds to “fund” pension trusts

• “Behind every quasi-insolvent public entity stands a poorly run public employee retirement plan” – Forbes

• The Puerto Rico Oversight, Management, and Economic Stability Act (PROMESA) establishes a Control Board with the authority to make binding decisions on debt and pension issues.

• Legislation applies to U.S. territories, not U.S. states

2016 BPAS Partner Conference

22

Re-setting the “Promise”

• Stockton, CA eliminated its retiree medical benefit under bankruptcy proceedings - $544 million benefit

• The Multiemployer Pension Reform Act of 2014 (PBGC)– Provides for the cut back of benefits before the trust is exhausted– Targets participants in plans where the employer withdrew without contributing their

withdrawal liability

• Detroit– Pre-65-year-old retirees, with household incomes under $75,000 to receive monthly

stipend of $175 toward individual policy– Medicare-eligible retiree to receive supplemental prescription drug benefits– $6 billion OPEB reduced to $2 billion

2016 BPAS Partner Conference

23

A view of the “Promised Land”

2016 BPAS Partner Conference

“Everything looks okay from here”

“Same from here”

24

Government Solutions – To Date

2016 BPAS Partner Conference

Re-negotiate the “promises”

Coverage

Moving the dial on Global Scoring

Means-Testing

Investing in Government Securities (?)

• myRA• State-run payroll deduct IRA Plans• State-run 401(a) MEP Plans• Fee Transparency – 408(b)

(2) / 404(a)(5)• Eligibility (?)• Fiduciary Regulations

• myRA, money market reform, State-run plans, State escheat initiatives

25

Government Solutions - IRA

2016 BPAS Partner Conference

26

Elements of State Run Plans

• No required employer contribution, no employer administrative fees• Exempt from ERISA• Illinois Secure Choice Savings Program

– 25+ employees, $250 fine per employer per year for non-compliance– Auto-enroll at 3%, non-ERISA plan– Roth IRA contribution limit ($5,500/$6,500)– Participant directed– Expense ratio not to exceed 75 bps– State Board to create vendor website to assist employers

in identifying provider

2016 BPAS Partner Conference

27

Government Solutions: MEP

• A state-sponsored MEP is a single plan under ERISA, according to the bulletin. While the state is the named ERISA fiduciary, it may require participating employers to assume limited fiduciary responsibilities. In addition, the employer has a fiduciary duty to prudently select the arrangement and to monitor plan operations.

2016 BPAS Partner Conference

28

Government Solutions: MEP

• According to the DOL, ERISA does not permit an “open MEP”– If participating employers have nothing in common other than participation, the

arrangement creates separate plans rather than a single MEP for ERISA purposes.

– However, the bulletin provides that a state-sponsored MEP is distinguishable from business enterprises that underwrite benefits or provide administrative services to several unrelated employers, because “a state has a unique representational interest in the health and welfare of its citizens that connects it to the in-state employers that choose to participate in the state MEP and their employees, such that the state should be considered to act indirectly in the interest of the participating employers.”

2016 BPAS Partner Conference

29

Government Solutions: Closing the Global Scoring GAP• Factors Affecting U.S. Rankings

– Increase coverage and participation rates to include part-time employees– Adjust the level of mandatory contributions (minimum funding requirements,

automatic enrollment/escalation plan design)– Reduce pre-retirement leakage by limiting access before retirement– Introduce a requirement that part of the retirement benefit must be taken as

an income stream– Increase labor force participation and decrease the retiree dependency ratio

with workplace policies and government incentives– Drive retirement assets into larger pools, improve governance with respect to

fiduciary stands and fee transparency

2016 BPAS Partner Conference

30

US Retirement SystemGlobal Standards

Expand Availability/Eligibili

tyMEP Enhance Fiduciary

Standards

Holistic Financial Planning

Manage Decumulation

(longevity insurance regs)

Auto Features

Government Solutions: Closing the Global Scoring GAP

31

“Today, one out of three workers does not have access to a retirement savings plan, including half of workers at firms with fewer than 50 employees and more than three-quarters of part-time workers.”

2016 BPAS Partner Conference

Jeff Zients, Director of Obama’s National Economic Council

Government Solutions: Closing the Global Scoring GAP

32

Women’s Pension Protection Act of 2015• Recent GAO report: 68 % of the lowest income workers and 81% of part-time

workers would participate in a plan if they had access• New standards would require employers to allow employees to participate in a

plan when they reach the earlier of the current minimum participation standards (age 21 or the completion of one year of service, which is generally 1,000 hours of service during a 12-month period), or once they have completed at least 500 hours of service for three consecutive years

• Under current law, one spouse could take a distribution or a loan from the plan without the other spouse’s knowledge or consent--could have a devastating effect on the unknowing spouse and family. WPPA would extend the spousal protections currently available for DB plans to DC plans like a 401(k)

2016 BPAS Partner Conference

Government Solutions: Closing the Global Scoring GAP

Government Solutions – Fiduciary Regs

Dept. of Labor Conflict of Interest Rules• Four (4) Categories of Advice Covered

1. Investment Recommendations2. Distribution / Rollover Recommendations3. Recommendations to use the services of a particular advisor4. Recommendations about the type of account (fee-based or brokerage)

33

Government Solutions – Fiduciary Regs

Dept. of Labor Conflict of Interest Rules• The following are deemed NOT to involve a

“Recommendation”1. Providing a platform available to a plan fiduciary (ERISA Plans, only)2. General communications regarding investment features, costs,

performance, etc.3. Investment education

34

Government Solutions – Fiduciary Regs

Dept. of Labor Conflict of Interest Rules• The following are deemed to involve a “Recommendation”

1. A one-time discussion between an individual and a financial professional regarding whether to rollover that individual’s assets from an employer plan to an IRA

2. Responding to an RFP by providing a sample K investment menu, unless the sample menu is based on client provided IPS criteria or other non subjective criteria

35

Government Solutions – Fiduciary Regs

• If you give advice, you are a fiduciary• If you are a fiduciary, you must subscribe to a level

fee arrangement, unless– You satisfy the “Best Interest Contract Exemption”

2016 BPAS Partner Conference 36

Government Solutions – Fiduciary Regs

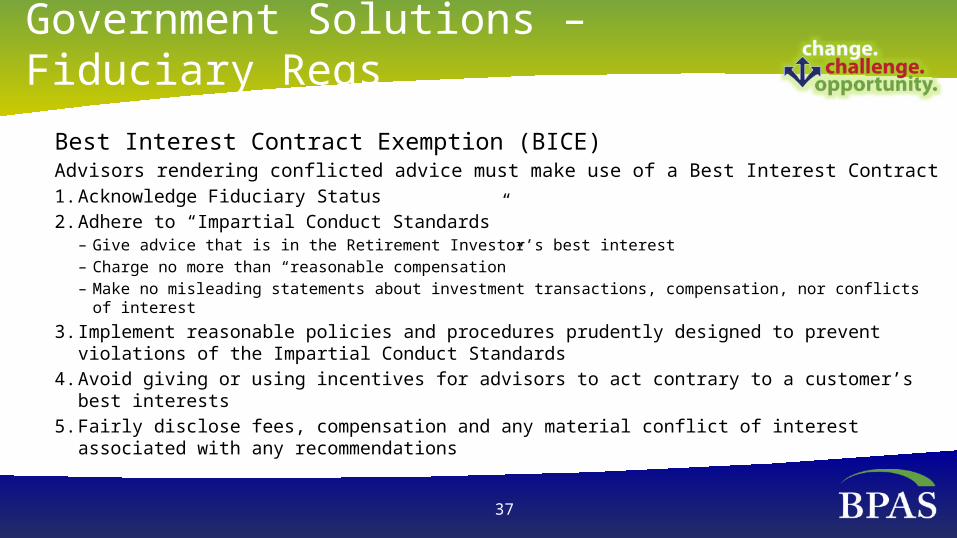

Best Interest Contract Exemption (BICE)Advisors rendering conflicted advice must make use of a Best Interest Contract1. Acknowledge Fiduciary Status2. Adhere to “Impartial Conduct Standards”

– Give advice that is in the Retirement Investor’s best interest– Charge no more than “reasonable compensation”– Make no misleading statements about investment transactions, compensation, nor conflicts of interest

3. Implement reasonable policies and procedures prudently designed to prevent violations of the Impartial Conduct Standards

4. Avoid giving or using incentives for advisors to act contrary to a customer’s best interests5. Fairly disclose fees, compensation and any material conflict of interest associated with any

recommendations

37

Government Solutions – Fiduciary Regs

How do we deal with the new Regs?Level Fee or Best Interest Contract Exemption (BICE)?

BIC light or BIC

38

Government Solutions – Fiduciary Regs

BICE LiteFor advisors that only receive level fees with regard to advice they provide1. No contract Requirement2. Other BICE requirements still apply (Acknowledge fiduciary status, Comply

with standards of Impartial Conduct, etc.)3. Appropriate consideration must be made and documented to ensure

that certain recommendations are in the customer’s best interest4. Level fee requirement extends to all affiliates

39

Government Solutions – Fiduciary Regs

Considerations?Level Fee arrangementsDirected TrusteesUse of commissionable product (limit menu to funds that all pay (x) bps?)Offering Asset Allocation Models Soliciting for Rollover/IRA businessRollovers/transfers: Plan-to-IRA, IRA-to-Plan, Plan-to-Plan, IRA-to-IRA, commission to fee based, fee-based to commission

40

41

Private-Sector Solutions:Fiduciary Standards

• The fiduciary responsibility and liability regarding the reasonableness of administrative and investment fees has been the responsibility of the plan sponsor

• The new fiduciary regulations expand upon that responsibility and liability to all fiduciaries associated with an ERISA plan

• Accordingly, Benchmark type reports become more relevant to the interests of service providers

2016 BPAS Partner Conference

42

Private-Sector Solutions:Fiduciary Standards

• Insurance-based advisors, typically commission-based and non-fiduciary, have declined from 25% of all advisors in 2011 to 12% in 2015 (RRI, 2015)

• Channel Affiliation– Growing: Ind BD, RIA, Bank Trust– Declining: Insurance, Wirehouse

• Plans served by non-fiduciary generalists may be “orphaned” and in play for fiduciary specialists

2016 BPAS Partner Conference

43

• Significant opportunities for fiduciary advisor servicing non-contributory profit sharing plans

• Many plans provide for transaction based fee income• Opportunity:

– Daily valuation trustee directed– Daily valuation, non-participant directed, aged-based investments– Daily valuation, participant directed– PR Keogh marketplace

2016 BPAS Partner Conference

Private-Sector Solutions:Fiduciary Standards

BPAS Fiduciary Regs Working Group

• Invitation to Bank Partners and Unaffiliated RIAs• A working group, facilitated to BPAS to retain counsel and

develop a “Best Interest Toolkit”– Model written contract applicable to IRA clients– Model disclosures applicable to ERISA plan clients– Model transaction disclosures and Web page disclosures– Model compliance policies and procedures to mitigate conflicts

2016 BPAS Partner Conference 44

BPAS Fiduciary Regs Working Group

• Tailored analysis of proposed changes to compensation structures and payout grids for individual advisors in order to limit the effect of differential compensation in compromising advice

• Tailored analysis to proposed system to ensure specific compensation figures will be available on demand

• Training with regard to new fiduciary standard, BIC Exemption and the firm’s compliance policy

2016 BPAS Partner Conference 45

BPAS Fiduciary Regs Working Group

• Projected as a 4 month project• Estimated at $75,000 for core services• 10 firms? - $7,500 per firm• Expression of interest sign up sheet at the

registration table

2016 BPAS Partner Conference 46

47

Private Sector Solutions: MEP

Corporate Market Retirement Plan Penetration 2014 (RRI, 2015)

# Employees # Firms % w/DC Plan

< 10 4,600,000 5.5%

10-50 985,000 23.9%

51-100 121,000 51.6%

2016 BPAS Partner Conference

Private Sector Solutions: MEP

• MEP Legislative Initiatives– Senate-S 266, House-HR 506; bi-partisan sponsorship– Hatch Safe Act

• Amend ERISA to allow for MEP without nexus• Direct Treasury to address “one-bad apple rule”• Hatch establishes a “designated service provider” registered

with the IRS, to be the focal point of audit and compliance

2016 BPAS Partner Conference 48

49

Private Sector Solutions: Auto Features

• Plans with Auto Features by Plan Size – 2013

• Plans with Auto Features, of those with Escalation

Plan Size 1-49 50-199 200-999 1,000-4,999

5,000+ Total

19% 45% 54% 64% 67% 50%

2005 2007 2009 2013

w/auto 17% 36% 38% 50%

Of those w/escalation

15% 33% 40% 35%

2016 BPAS Partner Conference

50

Reasons Cited for Not Using Auto FeaturesReason 1-49 50-199 200-999 1,000-

4,9995,000+ Total

Satisfied w/participation rate

73.1% 56.1% 22.0% 19.0% 13.8% 43.7%

Philosophy 19.2% 43.9% 36.6% 40.5% 34.5% 32.5%

Cost 3.8% 2.4% 17.1% 35.7% 41.4% 16.5%

Added work 10.3% 19.5% 14.6% 11.9% 3.4% 12.1%

2016 BPAS Partner Conference

Private Sector Solutions: Auto Features

2013 Report

Private Sector Solutions: Auto Features

• First generation of 3,4,5,6 is not sufficient to close the GAP– Employee turnover, assuming they move from auto-plan to auto-

plan, keeps too many people from saving at a sustained high level

– Consider 4,6,8 or substantially higher initial default rate– Applying auto to new employees only is a reverse grandfather

that negatively affects employees who serve the longest

2016 BPAS Partner Conference 51

Private Sector Solutions: Auto Features

• If we believe passionately in auto features, then the issue with the sponsor is more when than if

• If then it becomes a timing issue, more plans should be placed with administration firms that have robust auto enroll / escalation administrative capabilities

• Otherwise, the adoption of auto features involves a conversion, which constitutes a potential roadblock

2016 BPAS Partner Conference 52

53

Private Sector Solutions: Eligibility

• Employees who have not satisfied the age 21, one year and 1,000 hour requirements may be excluded from discrimination tests and employer contributions, except– They are included in the top-heavy test; employer contribution

requirements related thereto• Such employees may be excluded from auto sweep transactions• Plan administration fees with larger explicit monthly fees and lower

basis points will lessen the issue of average account balance• Theoretical issue of excludable employees in qualified plans enrolled

in state-run IRA plans

2016 BPAS Partner Conference

54

Private Sector Solutions: HSAs

Medical Premiums – Income Related Monthly Adjustment Amount (IRMAA)Single Filer Part B Part D Total

Up to $85k 121.80 per Plan premium $1,462

$85,001 to 107k 170.50 per Plus $12.70 per $2,198

$107,001 to $160k

243.60 per Plus $32.80 per $3,317

$160,001 to 214k

316.70 per Plus $52.80 per $$4,434

Above $214k 389.80 per Plus 72.90 per $5,552

2016 BPAS Partner Conference

55

• Fidelity's Retirement Health Care Cost Estimate reveals: a couple, both aged 65 and retiring this year, can expect to spend an estimated $245,000 on health care throughout retirement, up from $220,000 last year.

2016 BPAS Partner Conference

Private Sector Solutions: HSAs

• Estimate assumes enrollment in Medicare health coverage, but doesn’t include added expenses of nursing home or long-term care

56

“The sticker shock of $245,000 hopefully reinforces for many people that they need to act now, regardless of their age. For people offered a high-deductible health plan with a health savings account at work, choosing this option can really help them prepare, especially for Millennials who have a long time to save."

2016 BPAS Partner Conference

Private Sector Solutions: HSAs

—Brad Kimler, Executive Vice President of Fidelity's Benefits Consulting Services

57

Private Sector Solutions: HSAs

• 20 million people covered by high deductible health plans in 2015, up from 10 million in 2010

• HSA assets are projected to grow each year: – 3.5 billion in 2014 – 11.5 billion in 2017 – 40 billion in 2020

2016 BPAS Partner Conference

• Average interest rate credit offered by banks is 10bp

• With an investment platform, Stable Value of 200 bp plus open architecture

• HSAs are a form of IRA, thus subject to the fiduciary regulations

• HSA investment education— Role of the insurance broker vs. the

licensed financial advisor

58

Private Sector Solutions: HSAs• Means tested Medicare

– Where possible, stay below a threshold– Implications for 401k/403b-Roth contributions for

high income earners– Cash balance plus Roth 401k?– Implications for HSA utilization for high income

earners– Implications for pre-65 Roth conversions

• Medicare premiums deducted from Social Security benefits

2016 BPAS Partner Conference

59

Private Sector Solutions: HSAs

• Increase in Basic Premium is tied to increase in Social Security benefit (%)

• Increase in IRMAA is tied to medical inflation rate– Compounded differential increase in IRMAA could significantly

impact SS benefit

2016 BPAS Partner Conference

• Thresholds – will they trickle down?• Increase in the social security wage

base? Cash Balance!

60

Private Sector Solutions – HSAs

• HSA may not be a profitable service offering on a stand-alone basis

• Can be coupled with an RIA capacity on the retirement plan and incorporated into the participant education model

• RIA for HSA, with a similar IPS, fund lineup and recordkeeping platform, should constitute a value-add and differentiator in the current marketplace

2016 BPAS Partner Conference

61

Private Sector Solutions: Reducing Leakage

—Optimizing Social Security benefits — MedicareWills and Trusts — Decumulation strategies — Long term care expenses

2016 BPAS Partner Conference

Reducing Leakage and Retaining Assets Post Termination of Employment – 401k for Life

Assets Retained in the Plan

• Installment and ad hoc payment plan provisions• Loan plan provisions (limits and continuity)• Lifetime income products• Longevity insurance• Participant Education

62

Govt. / Private Solutions

• MEP for terminated participants– Consolidate disparate service model– Employer to adopt second plan, subject to fiduciary

standards– Participant given a 5th option under 402(f) notice• Plan to plan transfer with enhanced features and

advice supported by premium pricing

2016 BPAS Partner Conference

63

Govt. / Private Solutions• Advocacy List

– Top Heavy, eliminate elective deferrals from calculation; discriminates against small business and discourages eligibility for part-time employees

– MEP, open MEP legislation with relief from 100 life audit and bad apple issues

– CBO Scoring, should not be applied to retirement savings policies• Cannot increase savings and increase short term tax

revenue at the same time

2016 BPAS Partner Conference

64

Govt. / Private Solutions

• Advocacy List– 403b and 457b, best practice regulations from Consumer Financial

Protection Bureau • Auto enrollment provisions – currently ERISA preemption• Fee disclosures – DOL Reg• Fiduciary standards – DOL Reg• Selling fiduciary practices into the 403b/457 market represents

an opportunity for RIAs

2016 BPAS Partner Conference

65

Govt. / Private Solutions: It’s Possible

• In Rev. Proc. 2015-28, issued April 2, the IRS provided new safe harbor correction methods for errors relating to automatic contribution features, including automatic enrollment and automatic escalation of elective deferrals in 401(k) and 403(b) plans

2016 BPAS Partner Conference

• ASPPA was a primary instigator of these changes, and the final safe harbor largely mirrors the recommendations submitted to the Treasury Department by ASPPA and the Council of Independent 401(k) Recordkeepers (CIkR) in 2012

66

• In January 2016, the IRS issued proposed regulations modifying a number of provisions in the existing nondiscrimination regulations to address situations and plan designs, including benefit formulas for individual employees or groups without a reasonable business purpose.

• In April, the IRS has announced it will withdraw certain provisions included in recently released proposed regulations relating to nondiscrimination requirements applicable to qualified retirement plans under Code Sec. 401(a)(4).

2016 BPAS Partner Conference

Govt. / Private Solutions: It’s Possible

67

Summary• We, as a professional society, must increase the percentage of

working Americans who are retirement income ready• Many of the tools to accomplish such are available; we need to

deploy more cost effective ways to serve the non-covered constituency

• Playing “musical chairs” with existing plans while ignoring systemic issues of coverage and eligibility will lead to more aggressive government “solutions”

• If we focus more on “PUM”, AUM will follow

2016 BPAS Partner Conference

68

Summary• We need to save more

– VEBA for employer related retiree medical obligations– HSA for non-employer provided retiree medical expenses– DB / Cash Balance – More aggressive auto enroll / escalation

• We need to reduce leakage– Distributable events– More effective management of decumulation

2016 BPAS Partner Conference

Summary

• From Byron Wien: Strategist at Blackstone Group, age 83

“Don’t try to be better than your competition; try to be different”

2016 BPAS Partner Conference 69

70

Barry S. Kublin, Chief Executive Officer

Benefit Plans Administrative Services, Inc.

Questions?

B P A S P A R T N E R C O N F E R E N C E 2 0 1 6

BPAS PARTNER CONFERENCE 2016

#BPASPC