naresh mefa jntuh.ppt

DESCRIPTION

JNTU MEFA SLIDESTRANSCRIPT

Managerial Economics Managerial Economics &&

Financial AnalysisFinancial Analysis

bybyGUDURU NARESHGUDURU NARESH

Asst.Prof of ManagememtAsst.Prof of Managememt

BALAJI INSTITUTE OF BALAJI INSTITUTE OF ENGINEERING & SCIENCESENGINEERING & SCIENCES

WHAT IS THISWHAT IS THIS

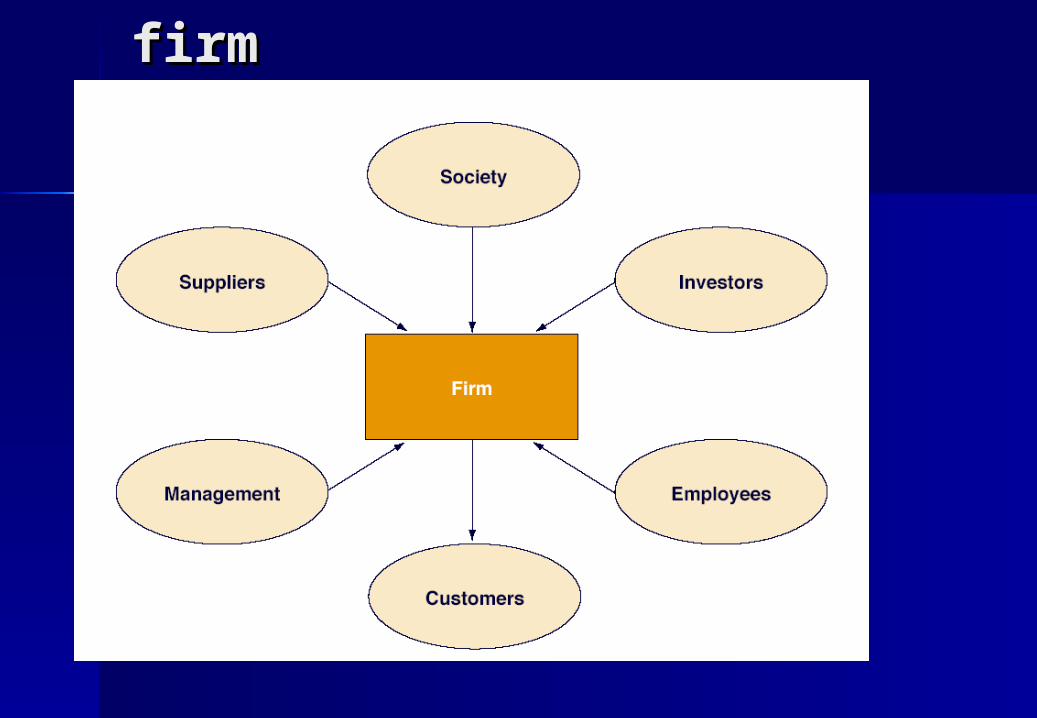

firmfirm

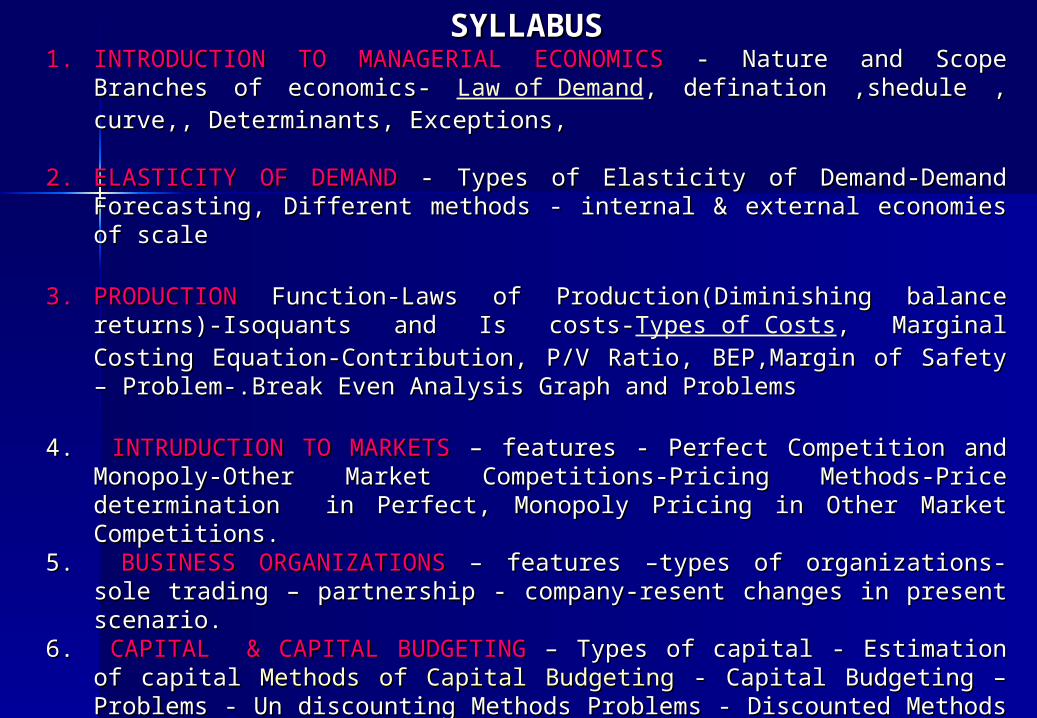

SYLLABUSSYLLABUS1.1. INTRODUCTION TO MANAGERIAL ECONOMICSINTRODUCTION TO MANAGERIAL ECONOMICS - Nature and Scope Branches of - Nature and Scope Branches of

economics- economics- Law of Demand, defination ,shedule , curve,, Determinants, Exceptions, , defination ,shedule , curve,, Determinants, Exceptions,

2.2. ELASTICITY OF DEMANDELASTICITY OF DEMAND - Types of Elasticity of Demand-Demand Forecasting, - Types of Elasticity of Demand-Demand Forecasting, Different methods - internal & external economies of scaleDifferent methods - internal & external economies of scale

3.3. PRODUCTIONPRODUCTION Function-Laws of Production(Diminishing balance returns)-Isoquants Function-Laws of Production(Diminishing balance returns)-Isoquants and Is costs-and Is costs-Types of Costs, Marginal Costing Equation-Contribution, P/V Ratio, , Marginal Costing Equation-Contribution, P/V Ratio, BEP,Margin of Safety – Problem-.Break Even Analysis Graph and ProblemsBEP,Margin of Safety – Problem-.Break Even Analysis Graph and Problems

4. 4. INTRUDUCTION TO MARKETSINTRUDUCTION TO MARKETS – features - Perfect Competition and Monopoly-Other – features - Perfect Competition and Monopoly-Other Market Competitions-Pricing Methods-Price determination in Perfect, Monopoly Market Competitions-Pricing Methods-Price determination in Perfect, Monopoly Pricing in Other Market Competitions.Pricing in Other Market Competitions.

5. 5. BUSINESS ORGANIZATIONSBUSINESS ORGANIZATIONS – features –types of organizations- sole trading – – features –types of organizations- sole trading – partnership - company-resent changes in present scenario.partnership - company-resent changes in present scenario.

6. 6. CAPITAL & CAPITAL BUDGETINGCAPITAL & CAPITAL BUDGETING – Types of capital - Estimation of capital – Types of capital - Estimation of capital Methods Methods of Capital Budgetingof Capital Budgeting - Capital Budgeting – Problems - Un discounting Methods - Capital Budgeting – Problems - Un discounting Methods Problems - Discounted Methods ProblemsProblems - Discounted Methods Problems

7. 7. Introduction to Accounting-Introduction to Accounting- Concepts and Book keeping - Rules of Accounting – Concepts and Book keeping - Rules of Accounting – Journal – Ledger - Cash Book – Types of Cash Books - Trial balance - Trading Journal – Ledger - Cash Book – Types of Cash Books - Trial balance - Trading Account - Profit and Loss Account - Balance Sheet-ProblemAccount - Profit and Loss Account - Balance Sheet-Problem

8. 8. Introduction to Ratio AnalysisIntroduction to Ratio Analysis – Importance Of Ratio’s - Merits and Demerits of Ratios- – Importance Of Ratio’s - Merits and Demerits of Ratios- calculation of ratios- problems 51.Revisioncalculation of ratios- problems 51.Revision

UNIT - IUNIT - I

MANAGERIAL MANAGERIAL ECONOMICSECONOMICS

The word economics is derived The word economics is derived from a Greek term “from a Greek term “ocio nomosocio nomos” which means ” which means house management it explains how different house management it explains how different individuals behave while managing their individuals behave while managing their economics activities.economics activities.

Economics teaches us how a person tries Economics teaches us how a person tries to satisfy his unlimited desires with the limited to satisfy his unlimited desires with the limited resources at his disposal. In other word it resources at his disposal. In other word it teaches us how to use the available scares teaches us how to use the available scares resources to meet our unlimited desires .hear resources to meet our unlimited desires .hear the question of choice comes in the need for the question of choice comes in the need for choice arises in the context of” Scarcity”.choice arises in the context of” Scarcity”.Hence economics is the study of the allocation Hence economics is the study of the allocation of scarce resources among alterative and of scarce resources among alterative and competing ends.competing ends.

ECONOMICSECONOMICS

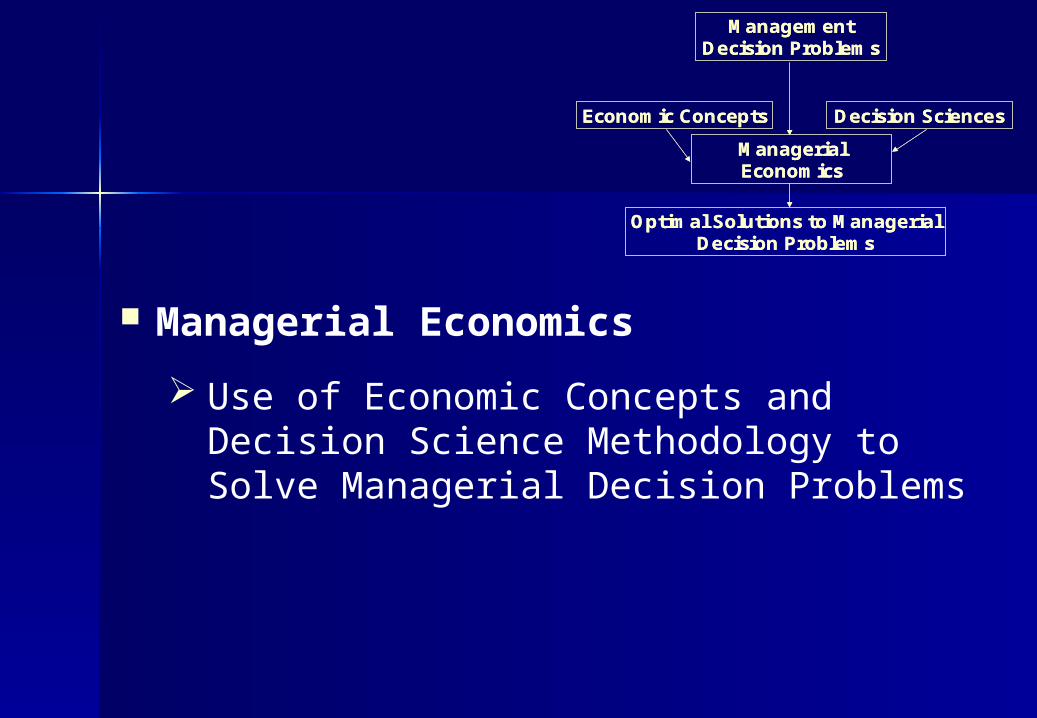

Managerial Economics

Use of Economic Concepts and Decision Science Methodology to Solve Managerial Decision Problems

Management Decision Problems

Economic Concepts

Managerial Economics

Optimal Solutions to Managerial Decision Problems

Decision Sciences

Management Decision Problems

Economic Concepts

Managerial Economics

Optimal Solutions to Managerial Decision Problems

Decision Sciences

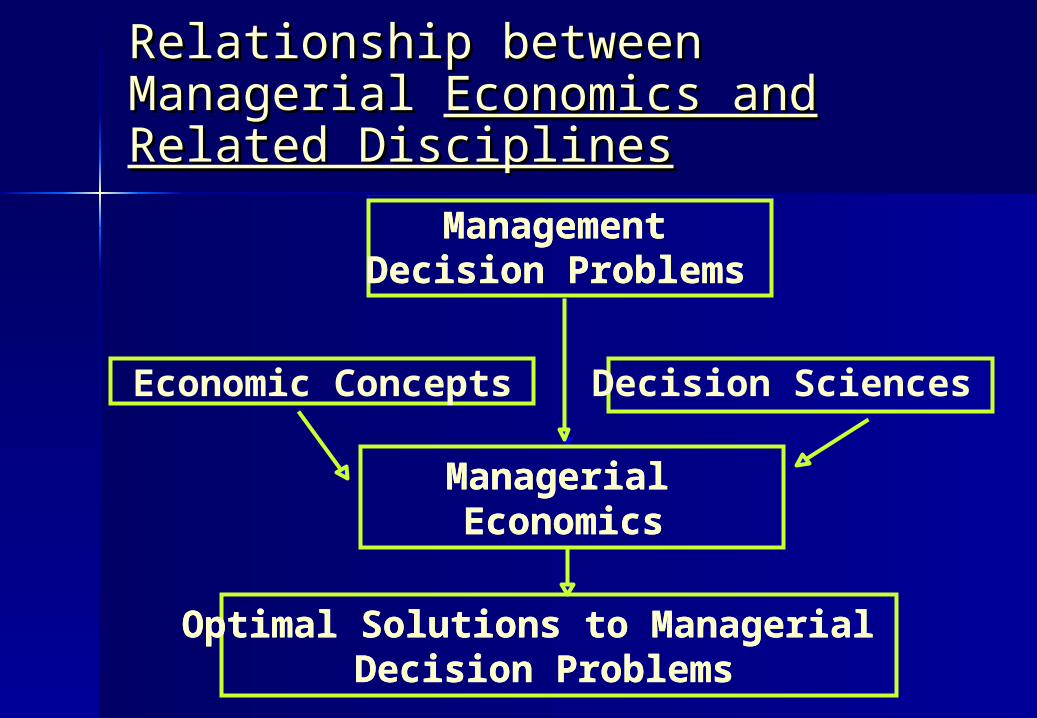

Relationship between Managerial Relationship between Managerial Economics and Related DisciplinesEconomics and Related Disciplines

Management Decision Problems

Economic Concepts

Managerial Economics

Optimal Solutions to Managerial Decision Problems

Management Decision Problems

Managerial Economics

Optimal Solutions to Managerial Decision Problems

Decision Sciences

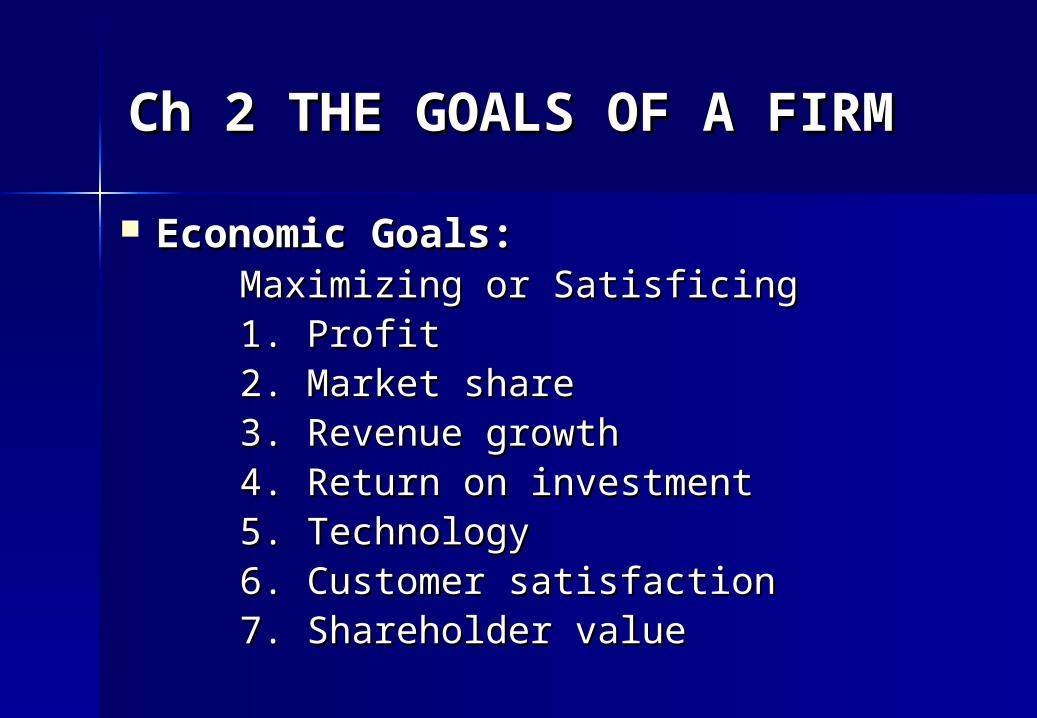

Ch 2 THE GOALS OF A FIRMCh 2 THE GOALS OF A FIRM

Economic Goals:Economic Goals:Maximizing or SatisficingMaximizing or Satisficing1. Profit1. Profit2. Market share2. Market share3. Revenue growth3. Revenue growth4. Return on investment4. Return on investment5. Technology5. Technology6. Customer satisfaction6. Customer satisfaction7. Shareholder value7. Shareholder value

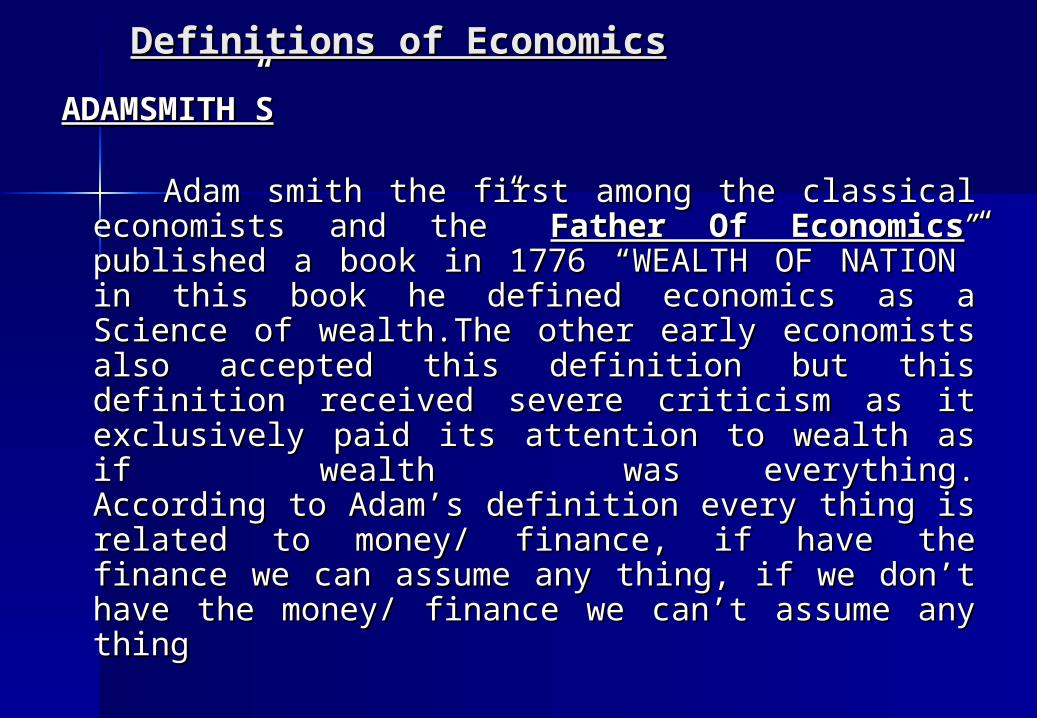

Definitions of EconomicsDefinitions of Economics

ADAMSMITH”SADAMSMITH”S

Adam smith the first among the classical Adam smith the first among the classical economists and the” economists and the” Father Of EconomicsFather Of Economics”” published a book in 1776 “WEALTH OF NATION” published a book in 1776 “WEALTH OF NATION” in this book he defined economics as a Science in this book he defined economics as a Science of wealth.The other early economists also of wealth.The other early economists also accepted this definition but this definition accepted this definition but this definition received severe criticism as it exclusively paid received severe criticism as it exclusively paid its attention to wealth as if wealth wasits attention to wealth as if wealth waseverything.everything.According to Adam’s definition every thing is According to Adam’s definition every thing is related to money/ finance, if have the finance related to money/ finance, if have the finance we can assume any thing, if we don’t have the we can assume any thing, if we don’t have the money/ finance we can’t assume any thingmoney/ finance we can’t assume any thing

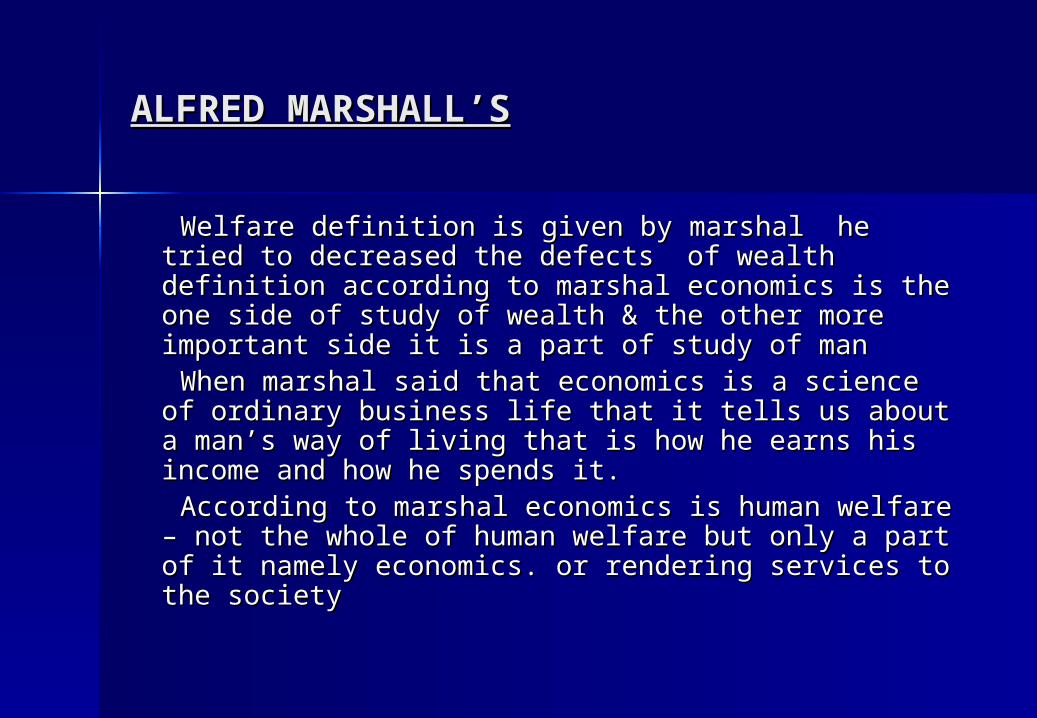

ALFRED MARSHALL’SALFRED MARSHALL’S

Welfare definition is given by marshal he tried to Welfare definition is given by marshal he tried to decreased the defects of wealth definition according decreased the defects of wealth definition according to marshal economics is the one side of study of to marshal economics is the one side of study of wealth & the other more important side it is a part of wealth & the other more important side it is a part of study of manstudy of man

When marshal said that economics is a science of When marshal said that economics is a science of ordinary business life that it tells us about a man’s ordinary business life that it tells us about a man’s way of living that is how he earns his income and way of living that is how he earns his income and how he spends it.how he spends it.

According to marshal economics is human welfare – According to marshal economics is human welfare – not the whole of human welfare but only a part of it not the whole of human welfare but only a part of it namely economics. or rendering services to the namely economics. or rendering services to the society society

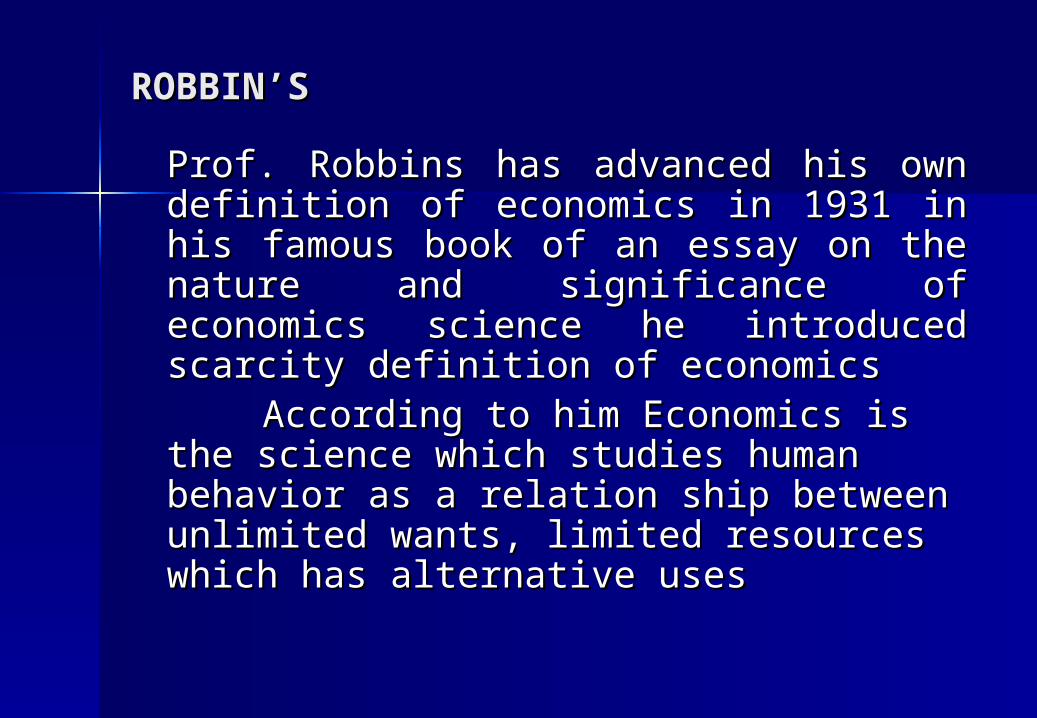

ROBBIN’S ROBBIN’S

Prof. Robbins has advanced his own Prof. Robbins has advanced his own definition of economics in 1931 in his definition of economics in 1931 in his famous book of an essay on the nature famous book of an essay on the nature and significance of economics science he and significance of economics science he introduced scarcity definition of introduced scarcity definition of economics economics

According to him Economics is the According to him Economics is the science which studies human behavior as science which studies human behavior as a relation ship between unlimited wants, a relation ship between unlimited wants, limited resources which has alternative limited resources which has alternative uses uses

Scope of Managerial EconomicsScope of Managerial Economics

The main focus in managerial economics The main focus in managerial economics is to find an optimal solution to a given is to find an optimal solution to a given managerial problem. The problem may managerial problem. The problem may relate to production, reduction or relate to production, reduction or control of costs determination of price control of costs determination of price of a given product or service make or of a given product or service make or buy decision inventory decision. Capital buy decision inventory decision. Capital management investment decision or management investment decision or human resource management.human resource management.

The economist is concerned with analysis The economist is concerned with analysis of the economy as a whole where as of the economy as a whole where as the managerial economist is essentially the managerial economist is essentially concerned with making decision in the concerned with making decision in the context of a single firm. context of a single firm.

The main areas of managerial The main areas of managerial economicseconomics

Demand analysisDemand analysis Cost analysis Cost analysis Pricing decisionsPricing decisions Profit managementProfit management Investment decisionInvestment decision Capital managementCapital management

BRANCHES OF ECONOMICSBRANCHES OF ECONOMICS

The total economic is divided in to two The total economic is divided in to two branchesbranches

Micro EconomicsMicro Economics

Macro EconomicsMacro Economics

MICRO ECONOMICSMICRO ECONOMICS:-:-

The word micro means a” millionth” part or The word micro means a” millionth” part or very small the study of individual units are very small the study of individual units are called micro economics. It deals with called micro economics. It deals with individuals or single units. The micro individuals or single units. The micro economics is called as a economics is called as a priceprice theory theory

MACRO ECONOMICSMACRO ECONOMICS

Macro economics is the study of economic system Macro economics is the study of economic system as a whole it studies not the individual as a whole it studies not the individual economics units like consumer but whole economics units like consumer but whole economic system “MACRO” means big it is well economic system “MACRO” means big it is well developed by J.M.KEYNES. The macro economics developed by J.M.KEYNES. The macro economics is called as a is called as a income and employmentincome and employment theory. theory. This theory deals with aggregates and average of This theory deals with aggregates and average of the entire economy for example national income, the entire economy for example national income, aggregates demand, aggregates savings, aggregates demand, aggregates savings, aggregates investment etc.aggregates investment etc.

DEMAND ANALYSISDEMAND ANALYSIS In ordinary language demand means desires. but in In ordinary language demand means desires. but in

economics demand has a separate meaning which is economics demand has a separate meaning which is quite differ from above meaning a person has a desire quite differ from above meaning a person has a desire it can’t became demand in economics. A desire which it can’t became demand in economics. A desire which is backed up by is backed up by having want, Ability to buy & having want, Ability to buy & willingness to pay willingness to pay at the price is called demand.at the price is called demand.

““Thus the quantity of commodity purchased at a given Thus the quantity of commodity purchased at a given price at a given time in a given market is called price at a given time in a given market is called demand”.demand”.

Demand functionDemand function:-:- The demand function explain the relationship between The demand function explain the relationship between

the demand for a commodity and its various the demand for a commodity and its various determinants may be express mathematically is determinants may be express mathematically is called “Demand function” called “Demand function”

Mathematical EquationMathematical Equation:-:-Dn = f { P1,P2,I,T,H……….n}Dn = f { P1,P2,I,T,H……….n}

LAW OF THE DEMANDLAW OF THE DEMAND The law of the demand thus it started as where the The law of the demand thus it started as where the

remaining all are constant the higher price leads remaining all are constant the higher price leads to lower demand for the goods and lower price to lower demand for the goods and lower price leads higher demand for the goods (or) where the leads higher demand for the goods (or) where the remaining all are constant there is inverse relation remaining all are constant there is inverse relation between price and demand .it explains the between price and demand .it explains the consumer should purchase high at lower price and consumer should purchase high at lower price and low quantity at higher price. low quantity at higher price.

In other wordsIn other words “ “When price increase demand will decrease”When price increase demand will decrease” “ “When price decreases demand will When price decreases demand will

increase” increase” This is called This is called inverse relationinverse relation between price and between price and

demand because of inverse relation demand demand because of inverse relation demand curve moves to left to right down forwardcurve moves to left to right down forward

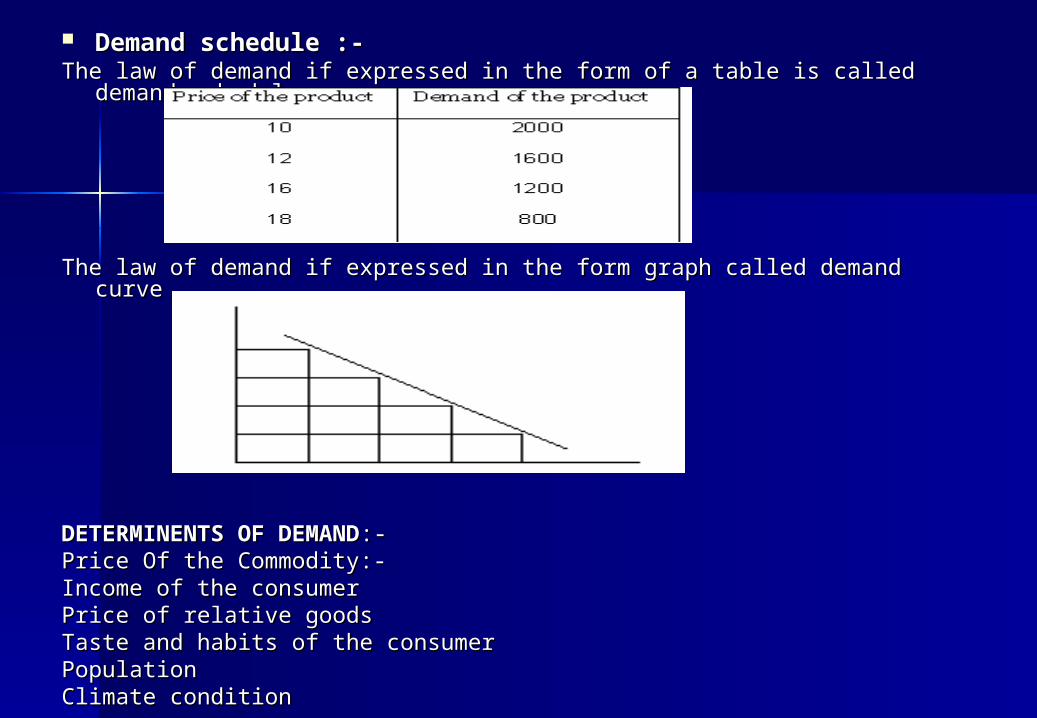

Demand schedule :-Demand schedule :-The law of demand if expressed in the form of a table is called demand The law of demand if expressed in the form of a table is called demand

schedule.schedule.

The law of demand if expressed in the form graph called demand curveThe law of demand if expressed in the form graph called demand curve

DETERMINENTS OF DEMANDDETERMINENTS OF DEMAND:-:-Price Of the Commodity:-Price Of the Commodity:-Income of the consumerIncome of the consumerPrice of relative goodsPrice of relative goodsTaste and habits of the consumerTaste and habits of the consumerPopulationPopulationClimate conditionClimate condition

EXCEPTION OF THE DEMANDEXCEPTION OF THE DEMAND:-:-The law of the demand may not be The law of the demand may not be

applicable in all cases.applicable in all cases. In such cases if the price is increasing In such cases if the price is increasing

demand also increases, if the price demand also increases, if the price decreases demand also decreases such decreases demand also decreases such cases are called exception of the cases are called exception of the demand.demand.

Giffen paradoxGiffen paradox Veblan goodsVeblan goods PopulationPopulation Seasonal businessSeasonal business

UNIT - IIUNIT - II

ELASTICITY OF DEMANDELASTICITY OF DEMAND

Elasticity of demand primarily refers to the Elasticity of demand primarily refers to the demand-price relation.demand-price relation.

Demand elasticity is the percent increase in the Demand elasticity is the percent increase in the sales that accompanies one percent increase in sales that accompanies one percent increase in any demand determined.any demand determined.The important demand elasticity’s are:The important demand elasticity’s are:

1. Price elasticity1. Price elasticity2. Income elasticity2. Income elasticity3. Cross elasticity3. Cross elasticity PRICE ELASTICITYPRICE ELASTICITY:-:- Price elasticity demand: it is also called Price elasticity demand: it is also called

demand elasticity. It is defined as the percentage demand elasticity. It is defined as the percentage change of demand and percentage change of change of demand and percentage change of price.price.

Ep= Ep= Percentage change in quantity demandPercentage change in quantity demandPercentage change in pricePercentage change in price

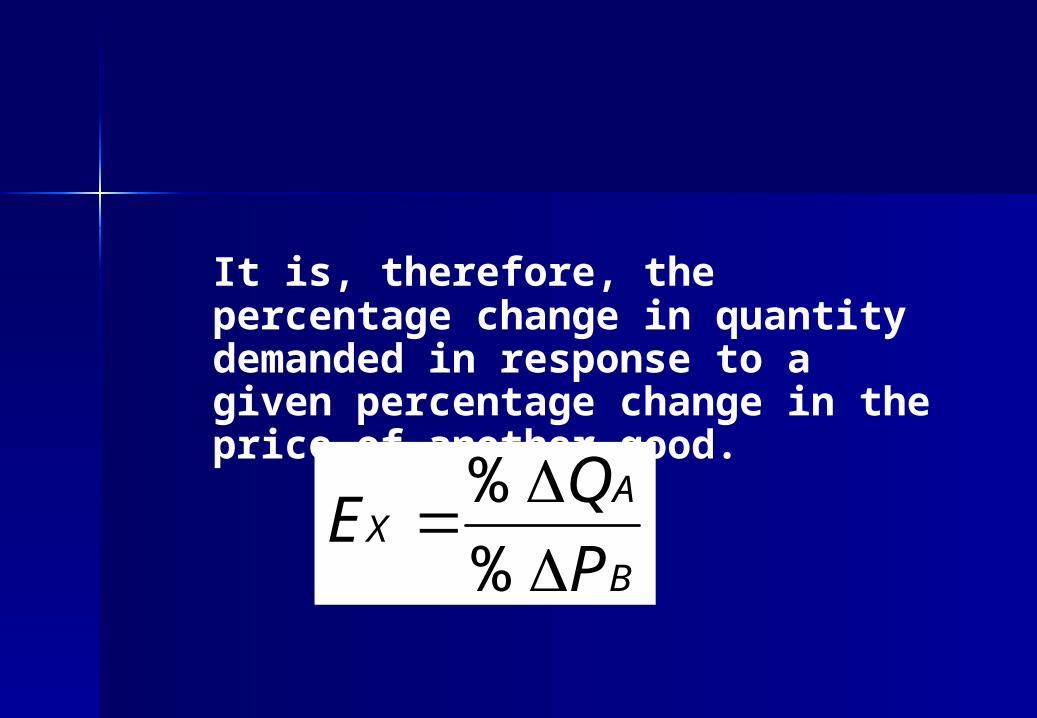

It is, therefore, the percentage change in quantity demanded in response to a given percentage change in the price of another good.

B

AX

P

QE

%

%

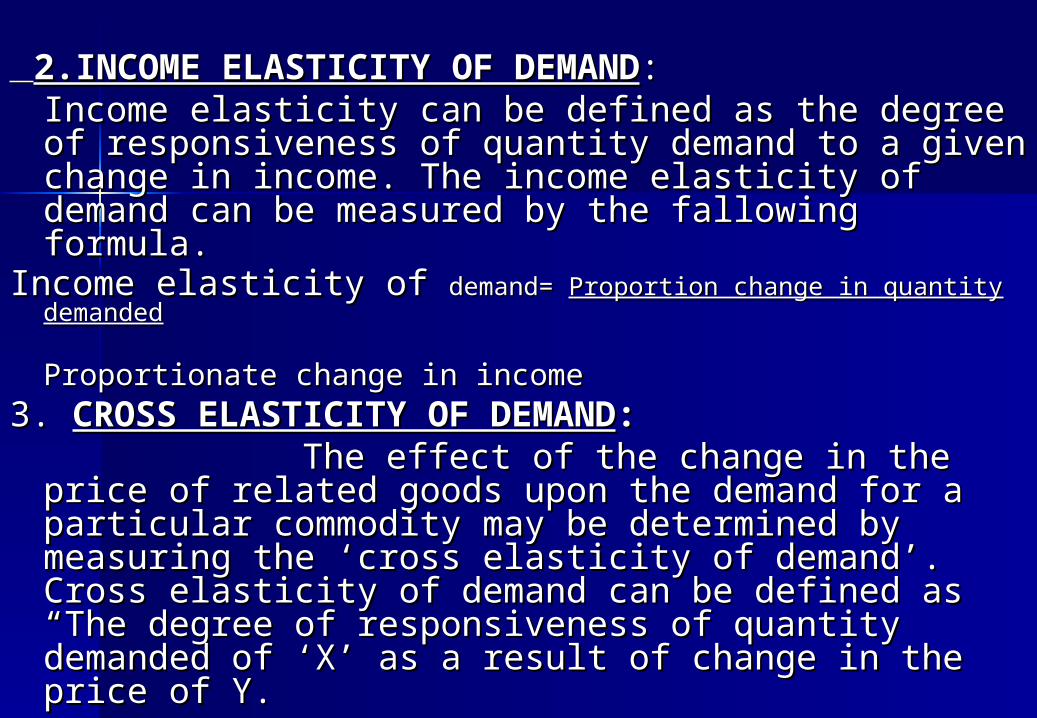

2.INCOME ELASTICITY OF DEMAND2.INCOME ELASTICITY OF DEMAND::Income elasticity can be defined as the degree of Income elasticity can be defined as the degree of responsiveness of quantity demand to a given responsiveness of quantity demand to a given change in income. The income elasticity of demand change in income. The income elasticity of demand can be measured by the fallowing formula.can be measured by the fallowing formula.

Income elasticity of Income elasticity of demand= demand= Proportion change in quantity Proportion change in quantity demandeddemanded

Proportionate change in incomeProportionate change in income3. 3. CROSS ELASTICITY OF DEMANDCROSS ELASTICITY OF DEMAND:: The effect of the change in the price of The effect of the change in the price of

related goods upon the demand for a particular related goods upon the demand for a particular commodity may be determined by measuring the commodity may be determined by measuring the ‘cross elasticity of demand’. Cross elasticity of ‘cross elasticity of demand’. Cross elasticity of demand can be defined as “The degree of demand can be defined as “The degree of responsiveness of quantity demanded of ‘X’ as a responsiveness of quantity demanded of ‘X’ as a result of change in the price of Y. result of change in the price of Y.

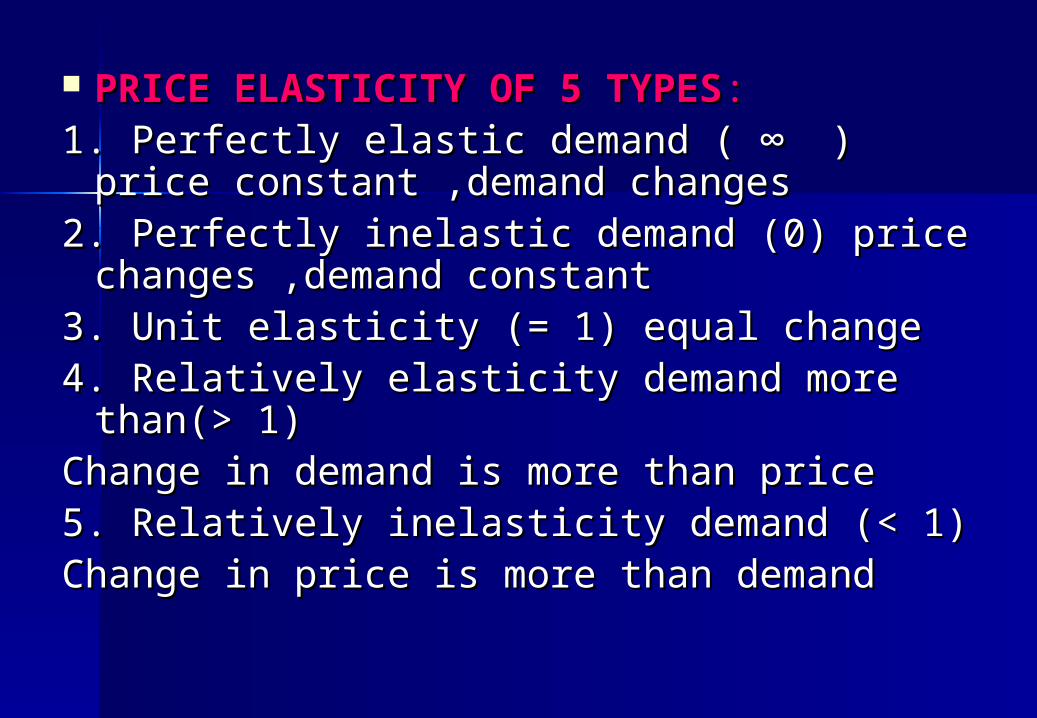

PRICE ELASTICITY OF 5 TYPESPRICE ELASTICITY OF 5 TYPES: : 1. Perfectly elastic demand ( 1. Perfectly elastic demand ( ∞∞ ) price ) price

constant ,demand changesconstant ,demand changes2. Perfectly inelastic demand (0) price 2. Perfectly inelastic demand (0) price

changes ,demand constantchanges ,demand constant3. Unit elasticity (= 1) equal change3. Unit elasticity (= 1) equal change4. Relatively elasticity demand more 4. Relatively elasticity demand more

than(> 1)than(> 1)Change in demand is more than priceChange in demand is more than price5. Relatively inelasticity demand (< 1)5. Relatively inelasticity demand (< 1)Change in price is more than demandChange in price is more than demand

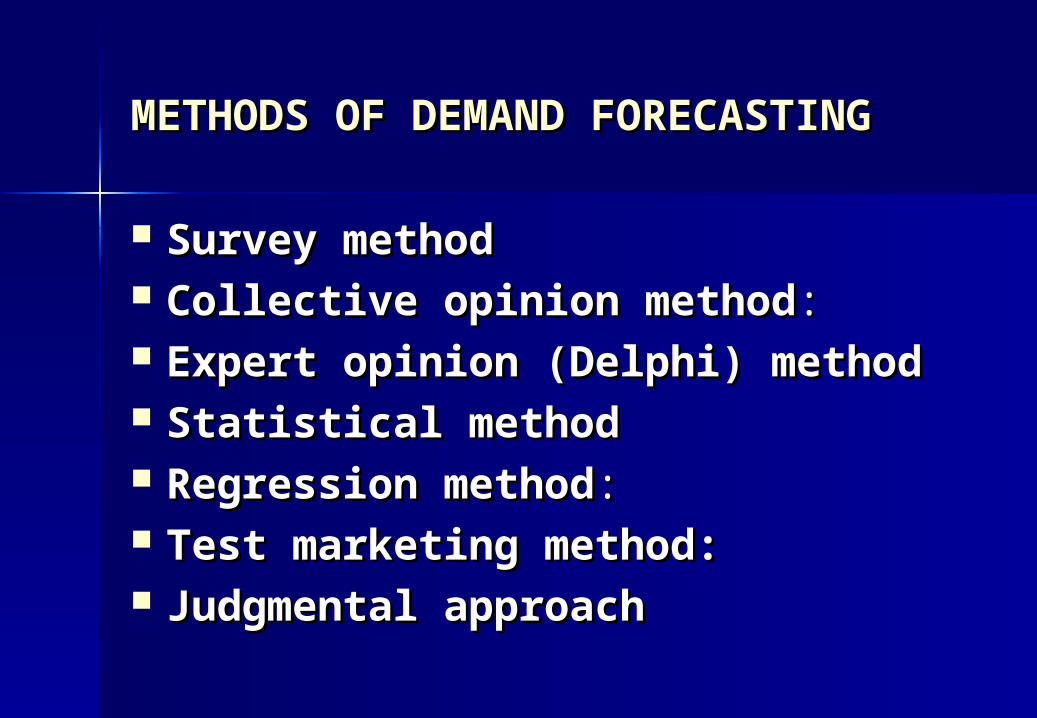

METHODS OF DEMAND METHODS OF DEMAND

FORECASTINGFORECASTING

Survey methodSurvey method Collective opinion methodCollective opinion method:: Expert opinion (Delphi) methodExpert opinion (Delphi) method Statistical methodStatistical method Regression methodRegression method:: Test marketing method:Test marketing method: Judgmental approachJudgmental approach

The Effect of a Price Ceiling on Supply and Demand

0

P1

P0

P2

P

Q1 Q0 Q2 Q

D

S

The Use of Price Supports

Surplus Surplus (Q(Q22-Q-Q11)) bought bought Production quota Production quota QQ33 by the governmentby the government introduced by the introduced by the

governmentgovernment

Q0

P0

P1

P

Q1 Q2

D

S

Q0

P1

P

Q1 Q3

D

a) b)

UNIT- IIIUNIT- III

PRODUCTIONPRODUCTION

&&

COST ANALYSISCOST ANALYSIS

ProductionProduction

Meaning -The Production is the process of Meaning -The Production is the process of transforming the various inputs land, transforming the various inputs land, labour, capital & organisation into output labour, capital & organisation into output

Production theory studies the Production theory studies the relationship between various possible relationship between various possible input and output combinations. The input and output combinations. The factors of production nothing but inputs of factors of production nothing but inputs of production. Factor of production mean production. Factor of production mean Land, Labour, Capital & Organisation. Land, Labour, Capital & Organisation.

PRODUCTION FUNCTION PRODUCTION FUNCTION

The technological relationship between The technological relationship between physical out put and physical quantities of physical out put and physical quantities of inputs is referred to as production function. inputs is referred to as production function. It shows the relation between quantity of It shows the relation between quantity of output and the quantity of various inputs output and the quantity of various inputs used in production used in production An improved technology helps to produce a An improved technology helps to produce a given out put with a less or quantity of given out put with a less or quantity of inputs.inputs.In algebraic from the production function In algebraic from the production function may be stated as:may be stated as:- - P = F{X1 X2 X 3 X4 ……….. n}P = F{X1 X2 X 3 X4 ……….. n}

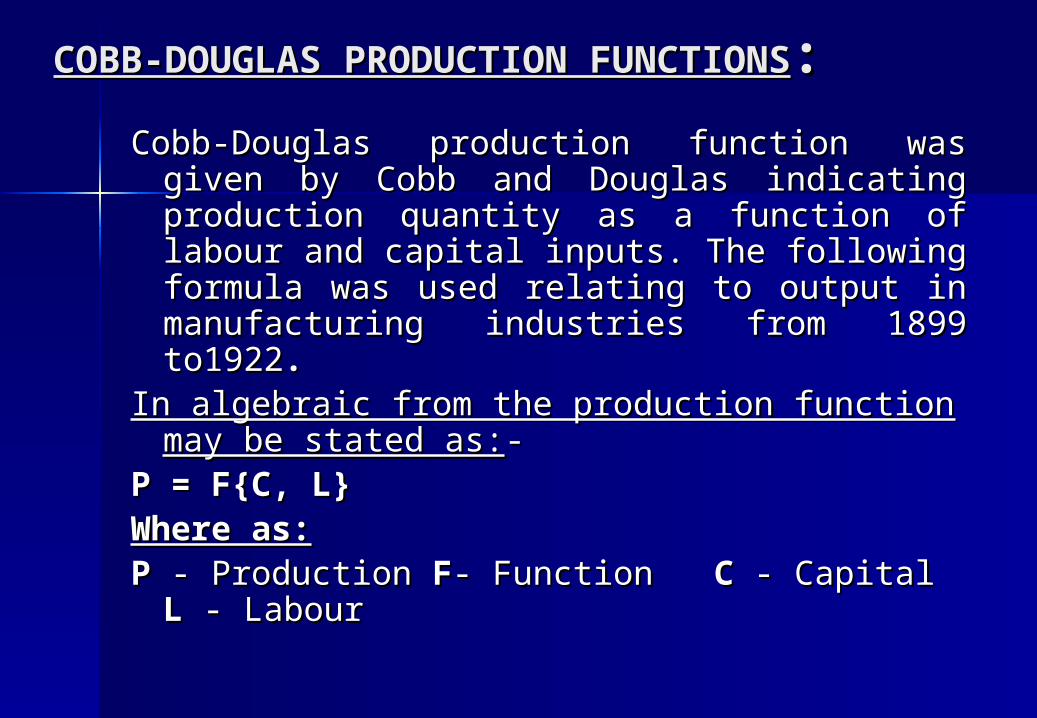

COBB-DOUGLAS PRODUCTION FUNCTIONSCOBB-DOUGLAS PRODUCTION FUNCTIONS::

Cobb-Douglas production function was given Cobb-Douglas production function was given by Cobb and Douglas indicating production by Cobb and Douglas indicating production quantity as a function of labour and capital quantity as a function of labour and capital inputs. The following formula was used inputs. The following formula was used relating to output in manufacturing relating to output in manufacturing industries from 1899 to1922industries from 1899 to1922..

In algebraic from the production function may In algebraic from the production function may be stated as:be stated as:- -

P = F{C, L}P = F{C, L}Where as:Where as:PP - Production - Production FF- Function - Function CC - Capital - Capital LL - -

LabourLabour

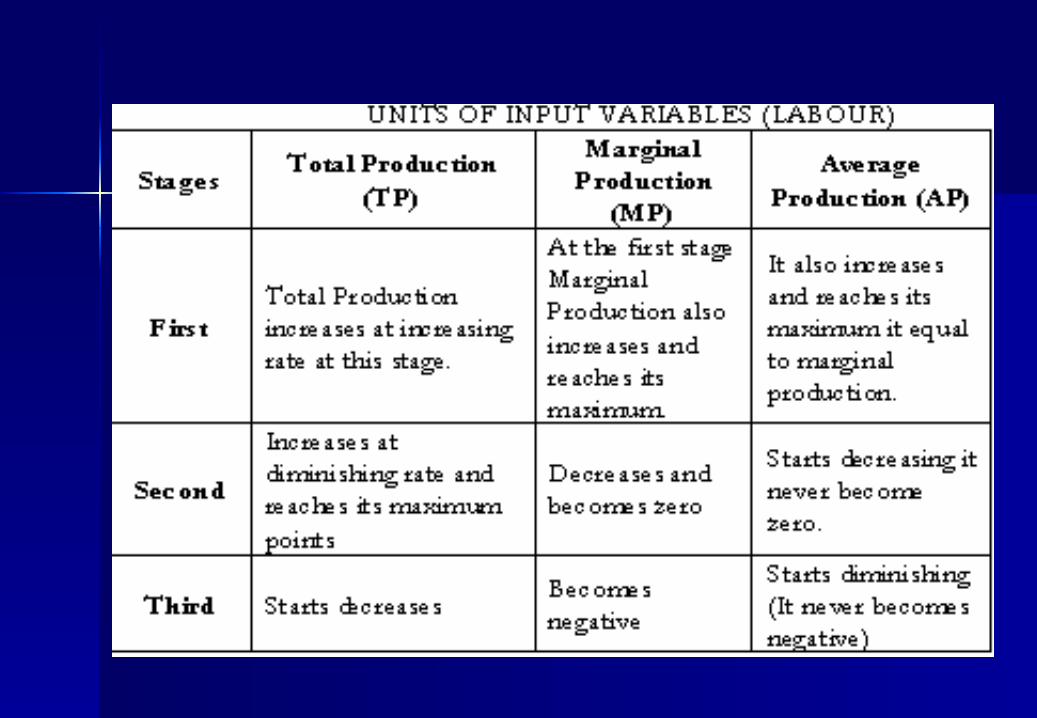

LAW OF PRODUCTION (OR) LAW OF LAW OF PRODUCTION (OR) LAW OF RETURNS:-RETURNS:-

While production function specifies the While production function specifies the relation ship between a given quantity of relation ship between a given quantity of output and certain given quantities of output and certain given quantities of inputs. Laws of production state the inputs. Laws of production state the relational out put. The laws which explain relational out put. The laws which explain input output .input output .

The law of variable proportions also The law of variable proportions also known as laws of returns is associated with known as laws of returns is associated with short-term production functionshort-term production function

AssumptionsAssumptions:-:- one factor is fixed and others are one factor is fixed and others are

variablevariable methods of production remain un methods of production remain un

changedchanged There is no change in production There is no change in production

techniquestechniques The variable factors are homogeneous The variable factors are homogeneous

and identical in amounts quality.and identical in amounts quality.

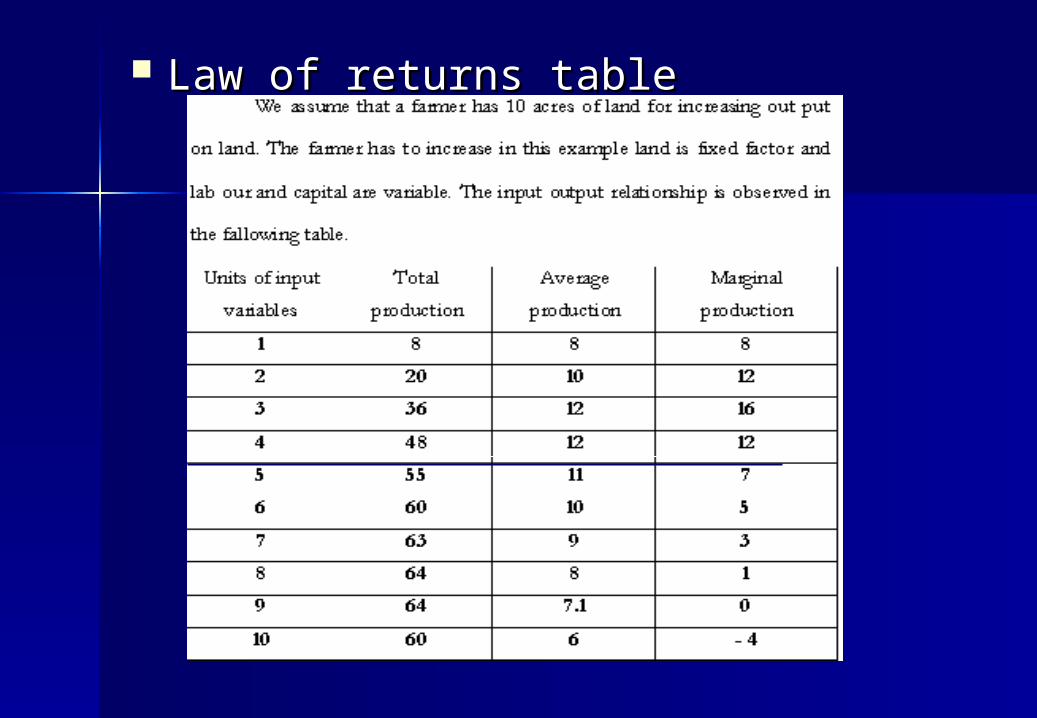

Law of returns tableLaw of returns table

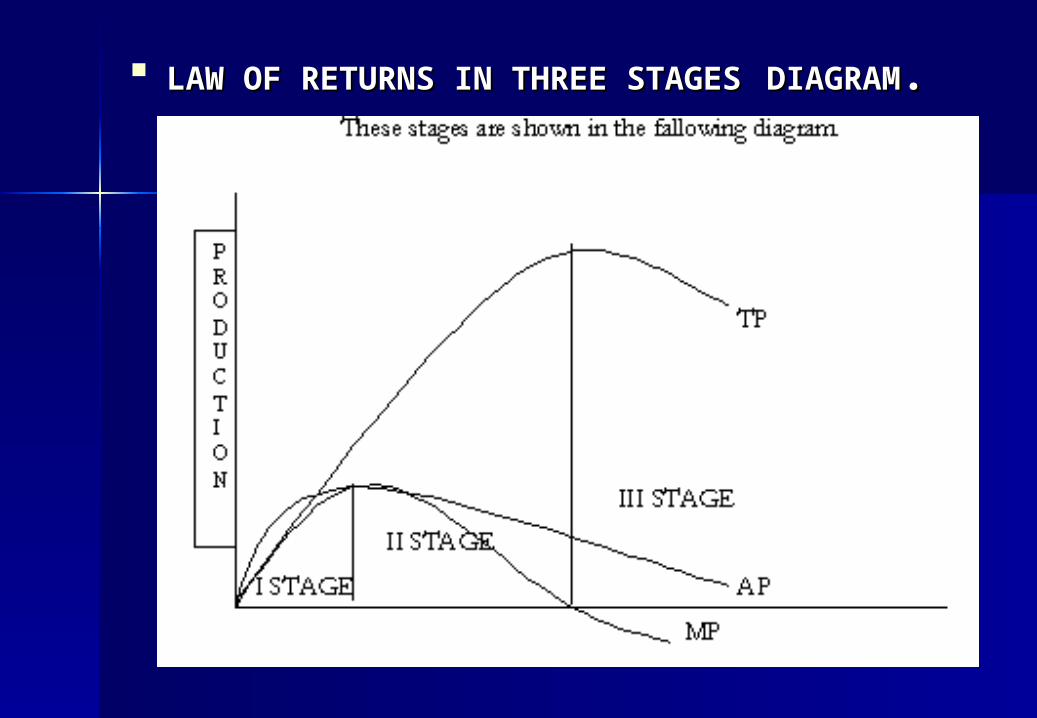

LAW OF RETURNS IN THREE STAGESLAW OF RETURNS IN THREE STAGES DIAGRAMDIAGRAM..

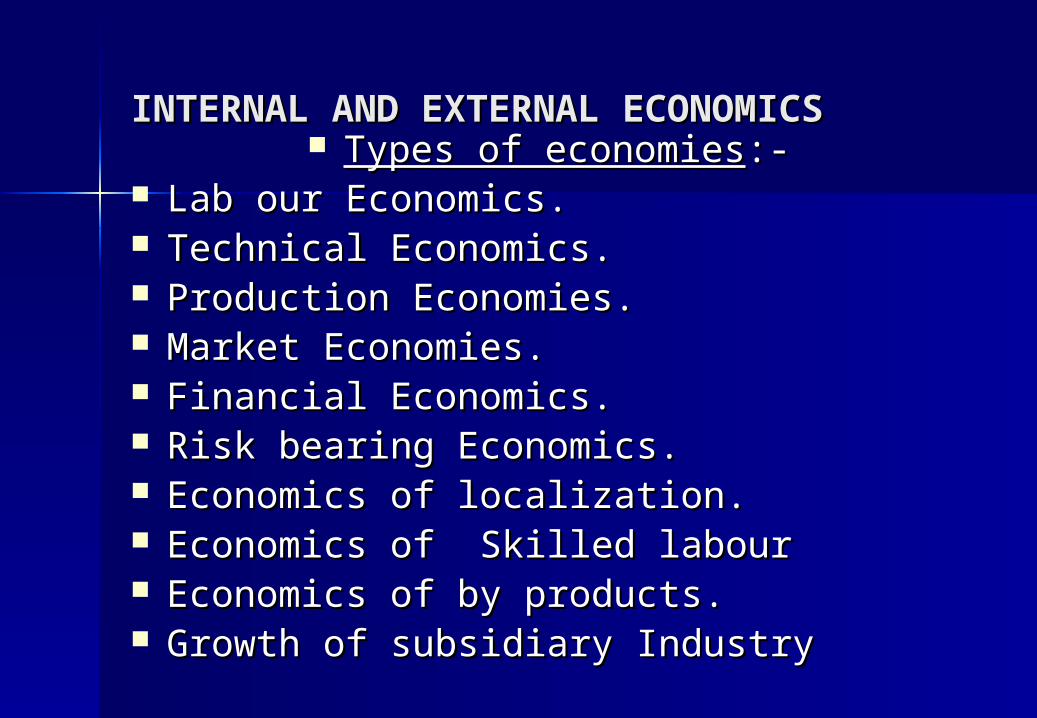

INTERNAL AND EXTERNAL ECONOMICS INTERNAL AND EXTERNAL ECONOMICS Types of economiesTypes of economies:-:-

Lab our Economics.Lab our Economics. Technical Economics.Technical Economics. Production Economies.Production Economies. Market Economies.Market Economies. Financial Economics.Financial Economics. Risk bearing Economics.Risk bearing Economics. Economics of localization.Economics of localization. Economics of Skilled labourEconomics of Skilled labour Economics of by products.Economics of by products. Growth of subsidiary Industry Growth of subsidiary Industry

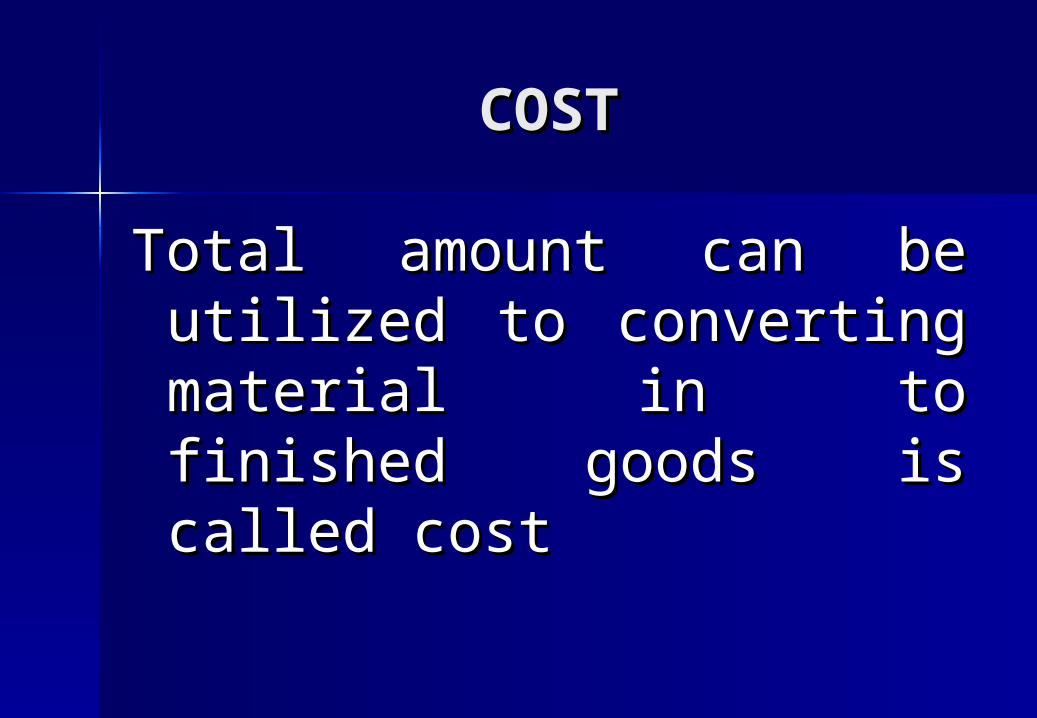

COST ANALYSISCOST ANALYSIS

COSTCOST

Total amount can be Total amount can be utilized to converting utilized to converting material in to finished material in to finished goods is called costgoods is called cost

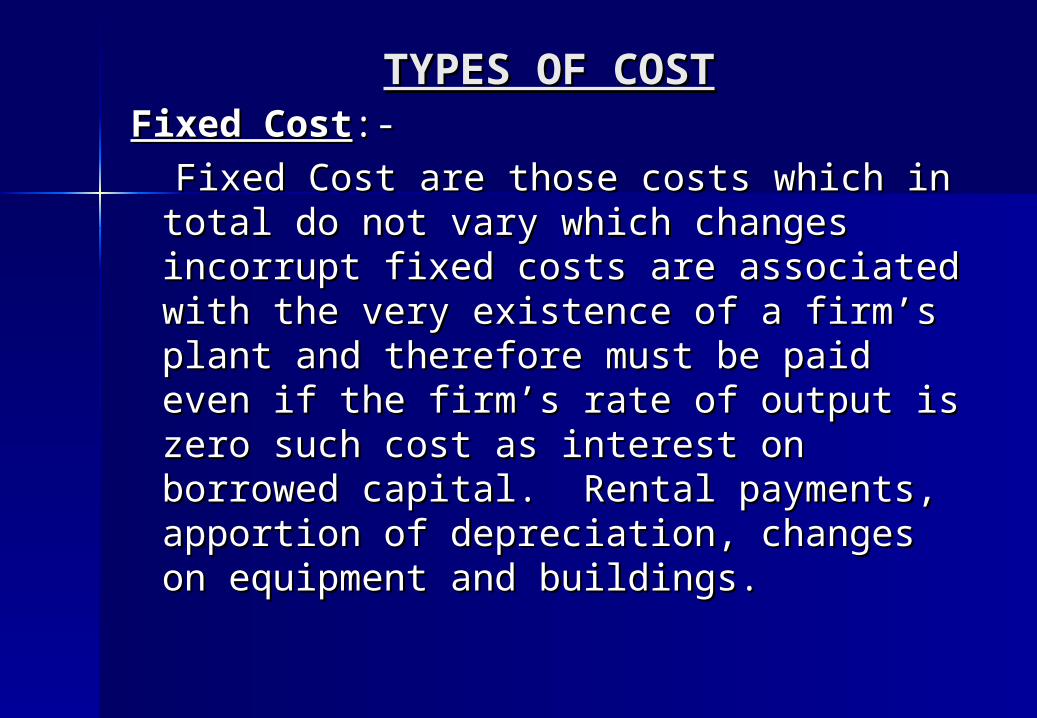

TYPES OF COSTTYPES OF COSTFixed CostFixed Cost:- :-

Fixed Cost are those costs which in Fixed Cost are those costs which in total do not vary which changes total do not vary which changes incorrupt fixed costs are associated incorrupt fixed costs are associated with the very existence of a firm’s with the very existence of a firm’s plant and therefore must be paid even plant and therefore must be paid even if the firm’s rate of output is zero such if the firm’s rate of output is zero such cost as interest on borrowed capital. cost as interest on borrowed capital. Rental payments, apportion of Rental payments, apportion of depreciation, changes on equipment depreciation, changes on equipment and buildings.and buildings.

Variable CostVariable Cost::

On the other hand variable costs On the other hand variable costs are those costs which increase with are those costs which increase with the level of output. They include the level of output. They include payments for raw materials. Changes payments for raw materials. Changes as fuel, and electricity. Wages and as fuel, and electricity. Wages and salaries of temporary staff, salaries of temporary staff, depreciation charges, based upon the depreciation charges, based upon the production. Production is increases production. Production is increases the cost also increases, if production the cost also increases, if production decreases cost also decreases.decreases cost also decreases.

Explicit Costs (or) Out of Pocket CostsExplicit Costs (or) Out of Pocket Costs:: - -

Payment made for the Payment made for the purchases of factors of production, purchases of factors of production, goods and services from other firms for goods and services from other firms for the production of the commodity is the production of the commodity is known as explicit cost. There costs are known as explicit cost. There costs are also known as out of pocket cost. For also known as out of pocket cost. For ex: - Wages, Pay for raw material, Rent ex: - Wages, Pay for raw material, Rent

Implicit Costs (or) Book CostsImplicit Costs (or) Book Costs: -: - Producer uses his own factors, Producer uses his own factors,

also in the process of production; also in the process of production; producers generally do not take into producers generally do not take into account the cost of their own factors. account the cost of their own factors. While calculating the expenditures, of While calculating the expenditures, of the firm, but they should definitely be the firm, but they should definitely be included. Their cost should be included. Their cost should be calculated on the market rate and that calculated on the market rate and that should be included. There are called should be included. There are called implicit costs, because producers do implicit costs, because producers do not make payments to others for not make payments to others for them. Ex: - Rent to own land. them. Ex: - Rent to own land.

Opportunity CostsOpportunity Costs: -: - Opportunity Cost refers, to Opportunity Cost refers, to

Sacrificing the next best alternative in order Sacrificing the next best alternative in order to attain that alternative. This is nothing but to attain that alternative. This is nothing but the revenue that is lost in not utilizing the the revenue that is lost in not utilizing the best alternative.best alternative.

In other words. The foregone In other words. The foregone Opportunity is considered as cost and it Opportunity is considered as cost and it termed opportunity cost. “Opportunity cost termed opportunity cost. “Opportunity cost of a particular product that resources, used in of a particular product that resources, used in its production could have produced. its production could have produced.

Sunk Costs:Sunk Costs: Sunk cost refers to those cost which is Sunk cost refers to those cost which is

not affected by change in level of business not affected by change in level of business activity. There costs remains same at all activity. There costs remains same at all levels of business activity. Ex: - Preliminary levels of business activity. Ex: - Preliminary expenses. expenses.

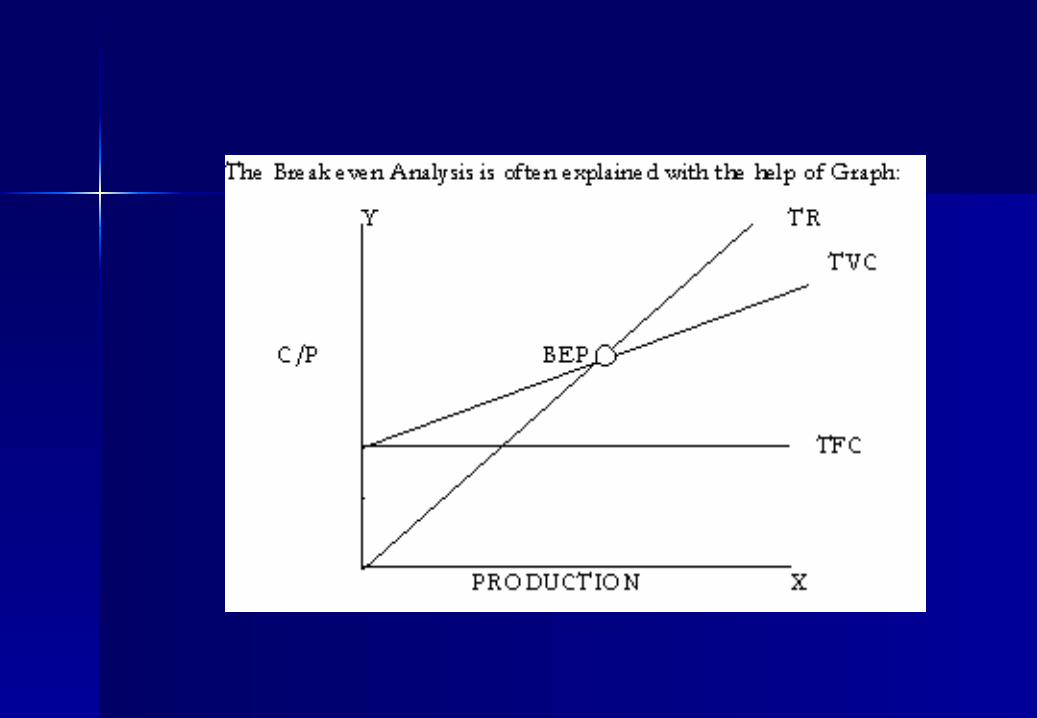

BREAK EVEN ANALYSISBREAK EVEN ANALYSISBreak even Analysis is a technique of Break even Analysis is a technique of profit planning. It is essentially a device profit planning. It is essentially a device for integrating costs. Revenues and for integrating costs. Revenues and output of the firm in order to illustrate output of the firm in order to illustrate the probable effects of alternative the probable effects of alternative courses of action upon net profits.courses of action upon net profits.The Break even point is defined as the The Break even point is defined as the one where profit is equal to zero total one where profit is equal to zero total revenue equals total cost. “No profit No revenue equals total cost. “No profit No loss zone is BEP”loss zone is BEP”

AssumptionsAssumptions

The behavior of costs and revenues of The behavior of costs and revenues of the firm remain linear.Sale prices the firm remain linear.Sale prices remain constant.remain constant.

Cost of production remains unchanged.Cost of production remains unchanged. Volume of output is the only relevant Volume of output is the only relevant

factor affecting cost.factor affecting cost. Cost can be divided into fixed and Cost can be divided into fixed and

variablevariable

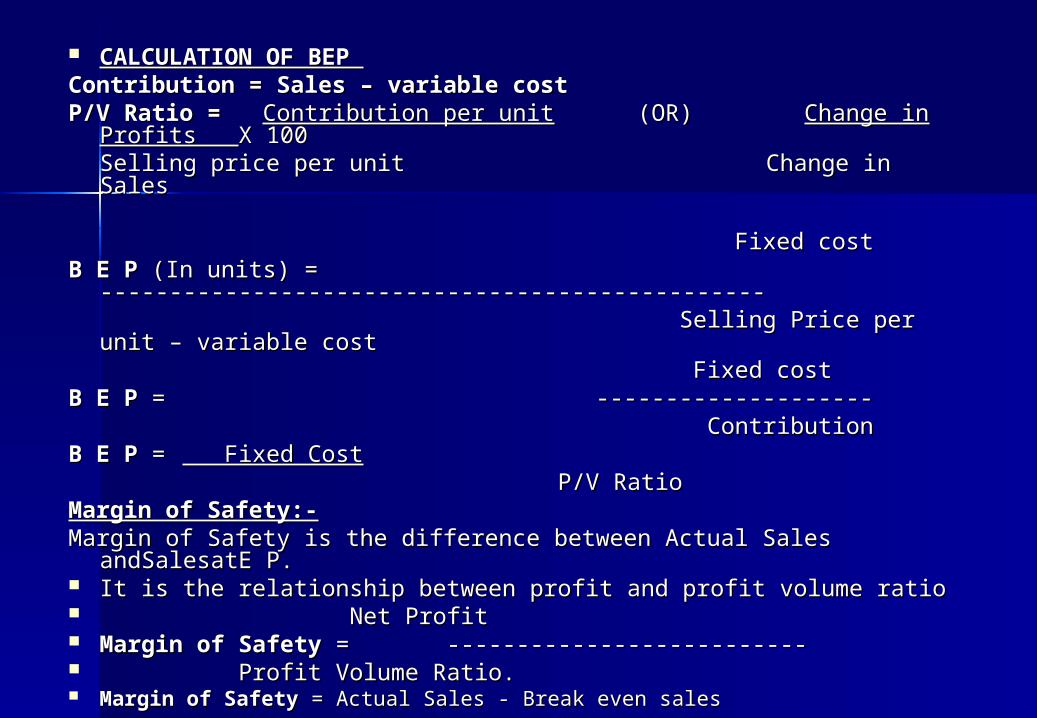

CALCULATION OF BEP CALCULATION OF BEP Contribution = Sales – variable costContribution = Sales – variable costP/V Ratio = P/V Ratio = Contribution per unitContribution per unit (OR) (OR) Change in Profits Change in Profits

X 100X 100Selling price per unitSelling price per unit Change in Sales Change in Sales

Fixed costFixed costB E PB E P (In units) = ------------------------------------------------ (In units) = ------------------------------------------------ Selling Price per unit – variable costSelling Price per unit – variable cost Fixed costFixed costB E PB E P = -------------------- = -------------------- ContributionContributionB E PB E P = = Fixed Cost Fixed Cost P/V RatioP/V RatioMargin of Safety:-Margin of Safety:-Margin of Safety is the difference between Actual Sales Margin of Safety is the difference between Actual Sales

andSalesatE P.andSalesatE P. It is the relationship between profit and profit volume ratioIt is the relationship between profit and profit volume ratio Net ProfitNet Profit Margin of SafetyMargin of Safety = -------------------------- = -------------------------- Profit Volume Ratio.Profit Volume Ratio. Margin of SafetyMargin of Safety = Actual Sales - Break even sales = Actual Sales - Break even sales

UNIT – IV UNIT – IV

MARKETSMARKETS

MarketMarket Introduction:Introduction:

A Market is understood as a place where A Market is understood as a place where commodities are bought and sold at retails or commodities are bought and sold at retails or wholesale prices a market place is thought is a wholesale prices a market place is thought is a place consisting of a number of bi and small shops place consisting of a number of bi and small shops stalls and even hawkers selling various types of stalls and even hawkers selling various types of goods.goods.

In economics however the term ‘Market’ In economics however the term ‘Market’ does not refers to a particular place as such but it does not refers to a particular place as such but it refers to a market for commodity or commodities. refers to a market for commodity or commodities. These economists speak of say a wheat market, a These economists speak of say a wheat market, a tea market, a gold market are so on.tea market, a gold market are so on.

DefinitionDefinitionAn arrangement whereby buyers and sellers come An arrangement whereby buyers and sellers come in close contact with each other directly or in close contact with each other directly or indirectly to sell and buy goods is described as indirectly to sell and buy goods is described as market.market.

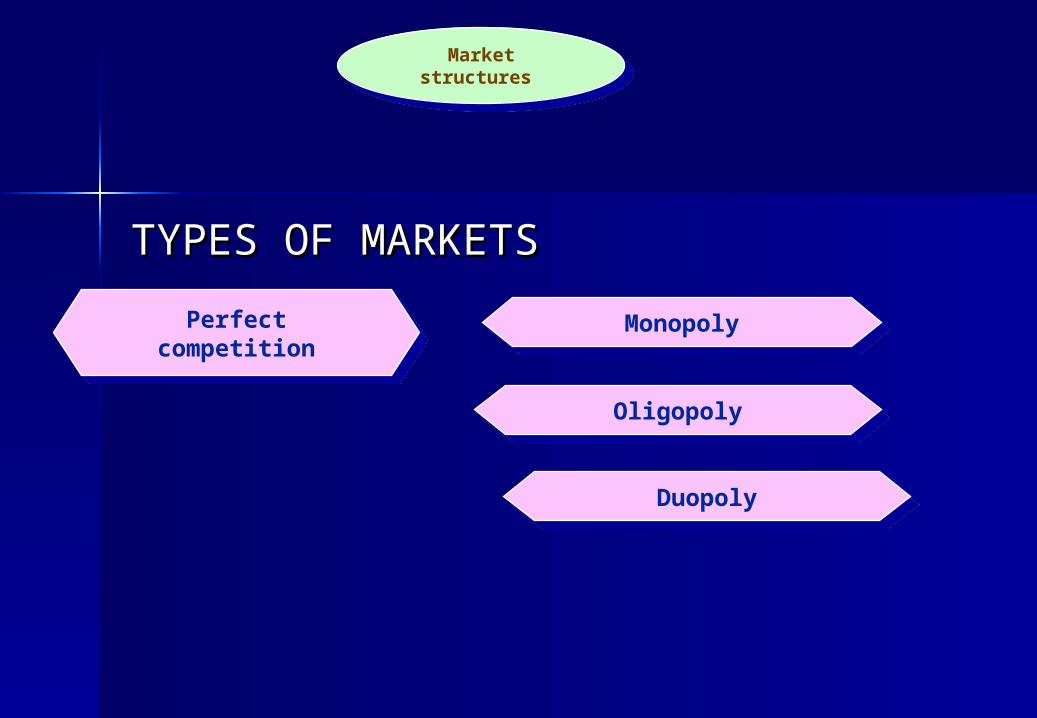

Market structures Market structures

Perfect competition

Perfect competition

OligopolyOligopoly

MonopolyMonopoly

DuopolyDuopoly

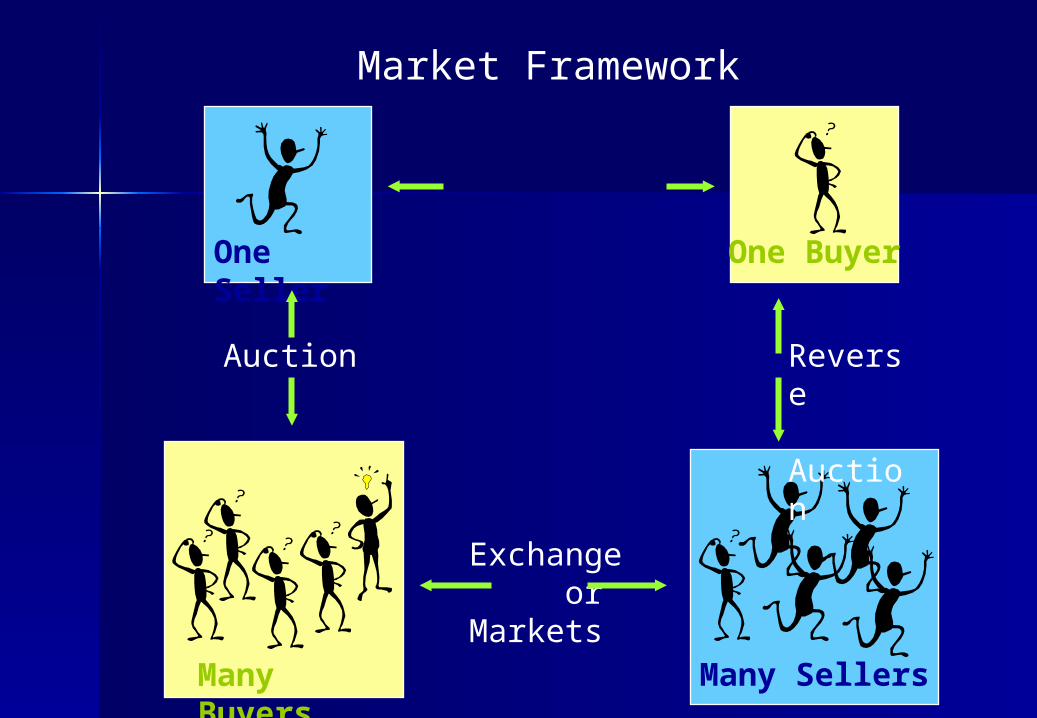

TYPES OF MARKETSTYPES OF MARKETS

One BuyerOne Seller

Many Buyers

Auction

Many Sellers

Reverse Auction

Exchange orMarkets

Market Framework

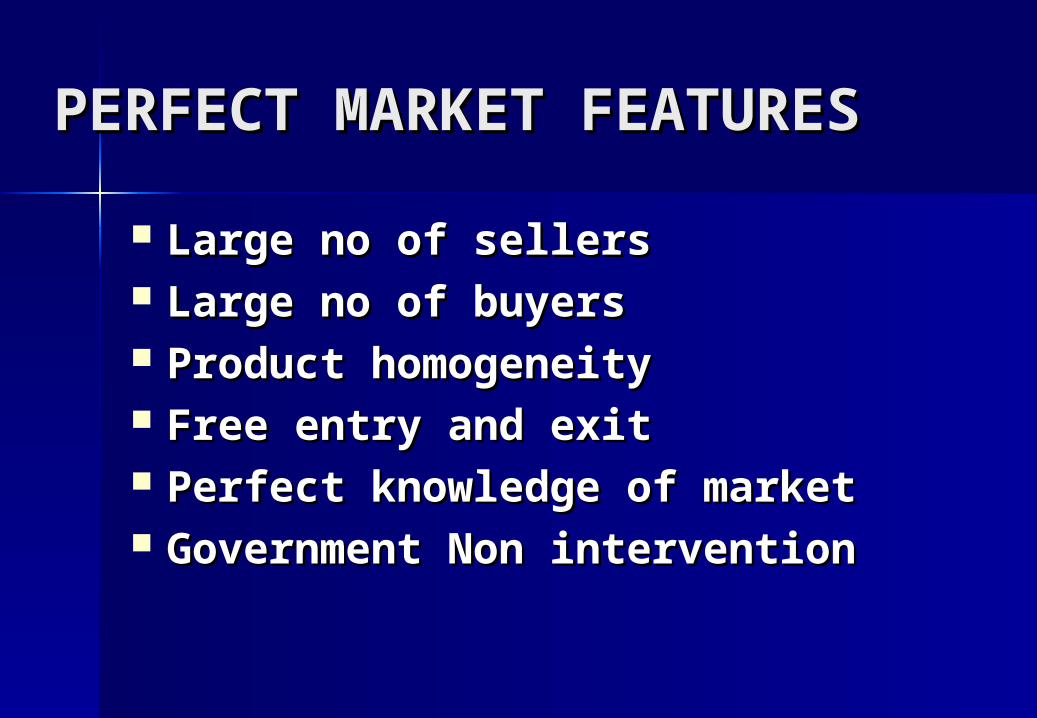

PERFECT MARKET PERFECT MARKET FEATURESFEATURES

Large no of sellersLarge no of sellers Large no of buyersLarge no of buyers Product homogeneityProduct homogeneity Free entry and exitFree entry and exit Perfect knowledge of marketPerfect knowledge of market Government Non interventionGovernment Non intervention

PRICE DETEMINATION PRICE DETEMINATION UNDERUNDER

MARKETMARKET

PRICE DETERMINATION UNDER PERFECT PRICE DETERMINATION UNDER PERFECT

MARKETMARKET It characterized by a large number of It characterized by a large number of

buyers and sellers of an essentially identical buyers and sellers of an essentially identical product each member of the market, whether product each member of the market, whether buyer or seller is so small in relation to the total buyer or seller is so small in relation to the total industry volume that he is unable to influence industry volume that he is unable to influence the price of the product individual buyers and the price of the product individual buyers and sellers are essentially price takers. It requires sellers are essentially price takers. It requires that all the buyers and sellers must posses’ that all the buyers and sellers must posses’ perfect knowledge about the existing market perfect knowledge about the existing market conditions especially regarding the market price, conditions especially regarding the market price, quantities and source of supplyquantities and source of supply

AssumptionsAssumptions:: More no of sellers & buyersMore no of sellers & buyers Price was fixed for a product Price was fixed for a product Average revenue equal to the marginal revenue Average revenue equal to the marginal revenue The buyers and sellers must posses’ perfect The buyers and sellers must posses’ perfect

knowledgeknowledge

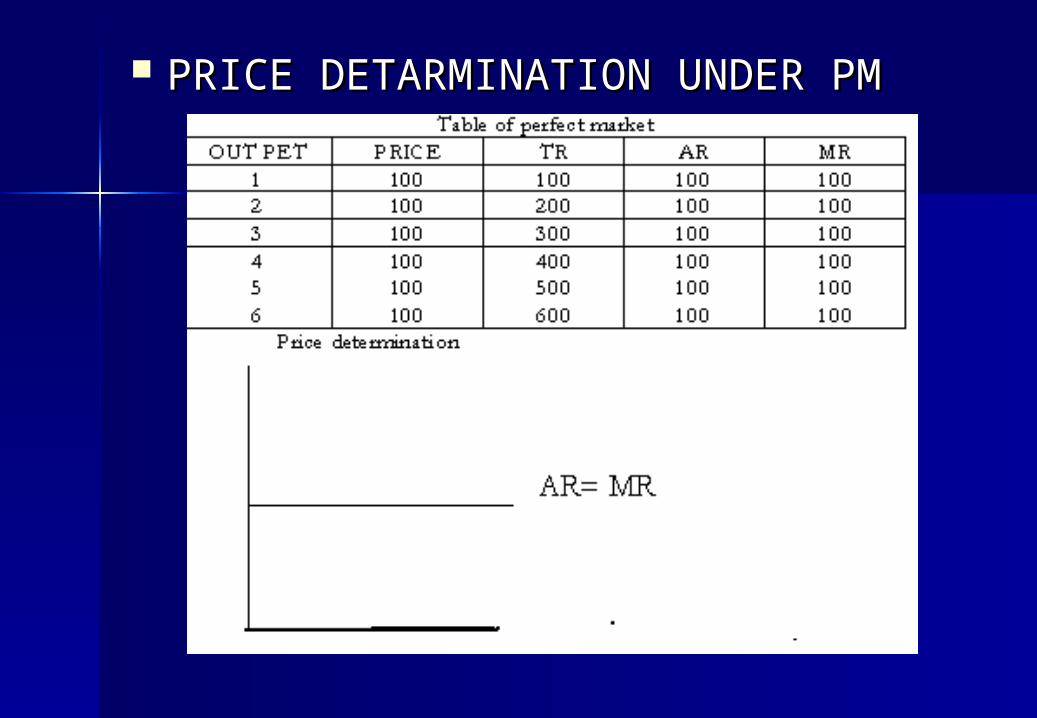

PRICE DETARMINATION UNDER PMPRICE DETARMINATION UNDER PM

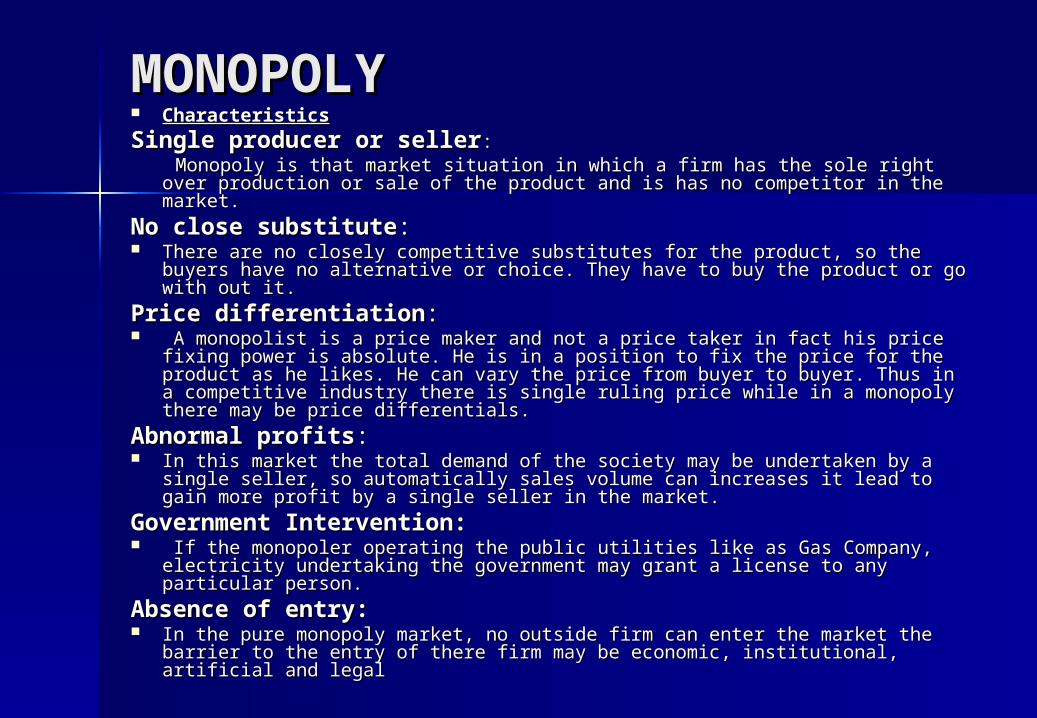

MONOPOLYMONOPOLY CharacteristicsCharacteristics

Single producer or sellerSingle producer or seller:: Monopoly is that market situation in which a firm has the sole right over Monopoly is that market situation in which a firm has the sole right over

production or sale of the product and is has no competitor in the market.production or sale of the product and is has no competitor in the market.

No close substituteNo close substitute: : There are no closely competitive substitutes for the product, so the buyers There are no closely competitive substitutes for the product, so the buyers

have no alternative or choice. They have to buy the product or go with out it. have no alternative or choice. They have to buy the product or go with out it.

Price differentiationPrice differentiation:: A monopolist is a price maker and not a price taker in fact his price fixing A monopolist is a price maker and not a price taker in fact his price fixing

power is absolute. He is in a position to fix the price for the product as he power is absolute. He is in a position to fix the price for the product as he likes. He can vary the price from buyer to buyer. Thus in a competitive likes. He can vary the price from buyer to buyer. Thus in a competitive industry there is single ruling price while in a monopoly there may be price industry there is single ruling price while in a monopoly there may be price differentials.differentials.

Abnormal profitsAbnormal profits:: In this market the total demand of the society may be undertaken by a In this market the total demand of the society may be undertaken by a

single seller, so automatically sales volume can increases it lead to gain single seller, so automatically sales volume can increases it lead to gain more profit by a single seller in the market.more profit by a single seller in the market.

Government Intervention: Government Intervention: If the monopoler operating the public utilities like as Gas Company, If the monopoler operating the public utilities like as Gas Company,

electricity undertaking the government may grant a license to any particular electricity undertaking the government may grant a license to any particular person.person.

Absence of entry:Absence of entry: In the pure monopoly market, no outside firm can enter the market the In the pure monopoly market, no outside firm can enter the market the

barrier to the entry of there firm may be economic, institutional, artificial and barrier to the entry of there firm may be economic, institutional, artificial and legallegal

PRICE DETERMINATION UNDERPRICE DETERMINATION UNDER MONOPOLYMONOPOLY

In this market just one producer of a In this market just one producer of a product the firm has substantial control product the firm has substantial control over the price. further if product is over the price. further if product is differentiated and if there are no threats of differentiated and if there are no threats of new firms entering the same business a new firms entering the same business a monopoly firm can manage to earn monopoly firm can manage to earn excessive profits aver a long period if excessive profits aver a long period if doesn’t requires knowledge about the doesn’t requires knowledge about the existing market conditions existing market conditions The Monopolistic firm attains equilibrium The Monopolistic firm attains equilibrium when its marginal cost becomes equal to when its marginal cost becomes equal to the marginal revenues. The monopolist the marginal revenues. The monopolist always desires to make maximum profits. always desires to make maximum profits. He makes maximum profit when MC=MR He makes maximum profit when MC=MR

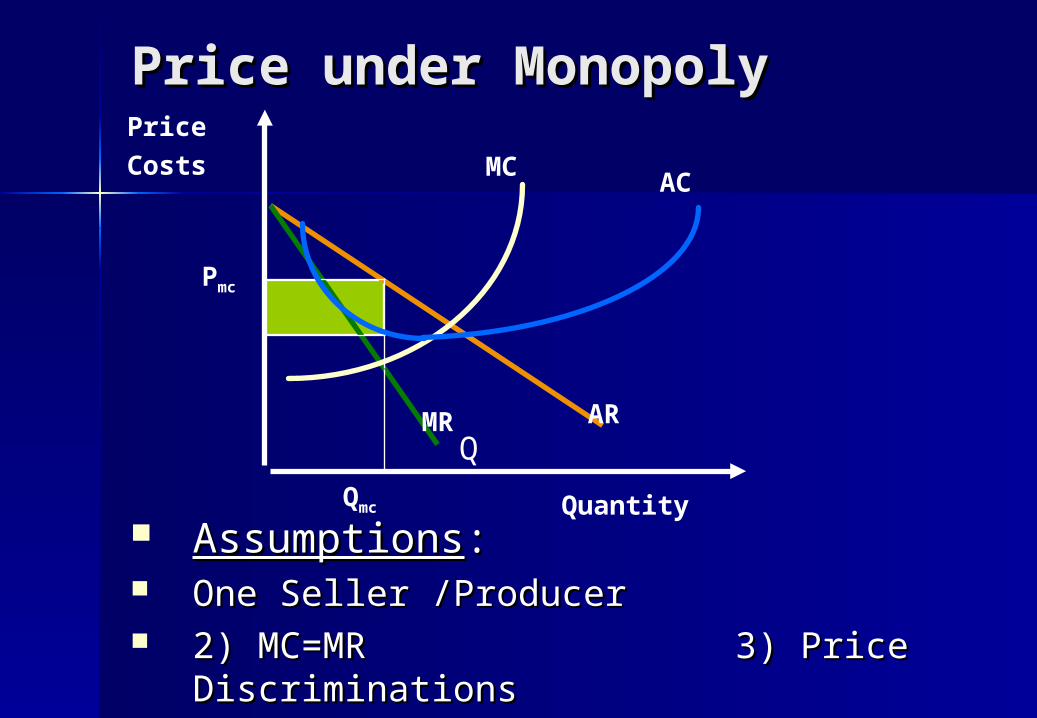

Price under MonopolyPrice under Monopoly

AssumptionsAssumptions:: One Seller /Producer One Seller /Producer 2) MC=MR 3) Price 2) MC=MR 3) Price

Discriminations Discriminations

Q

Price

Costs

Quantity

MR AR

MCAC

Qmc

Pmc

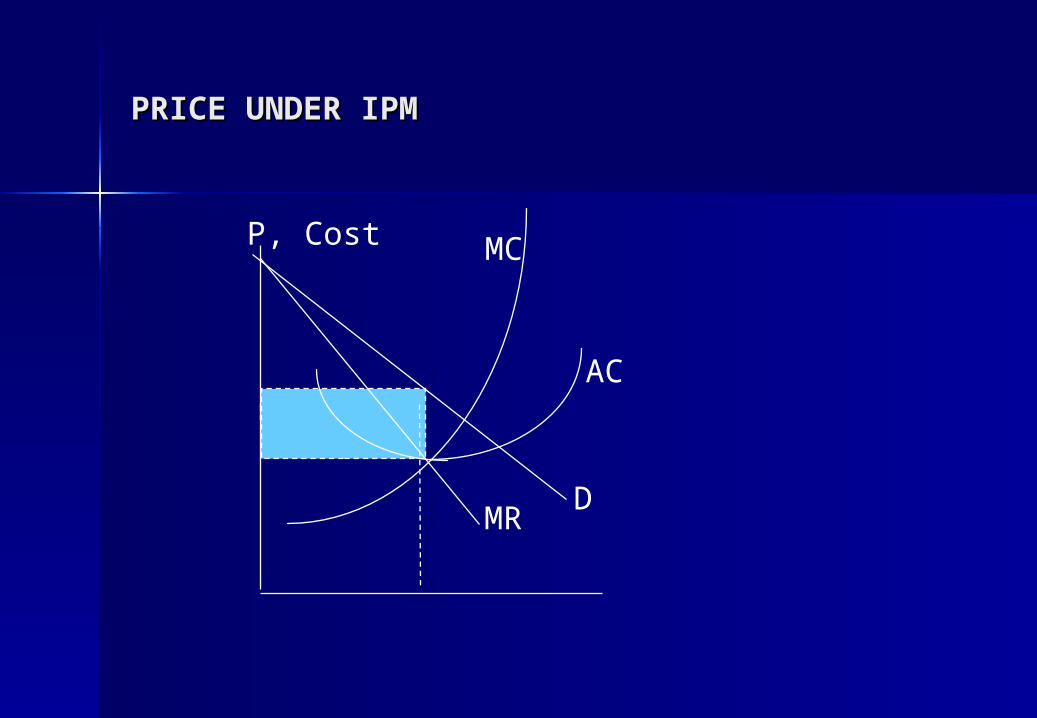

PRICE UNDER IPMPRICE UNDER IPM

DMR

AC

MCP, Cost

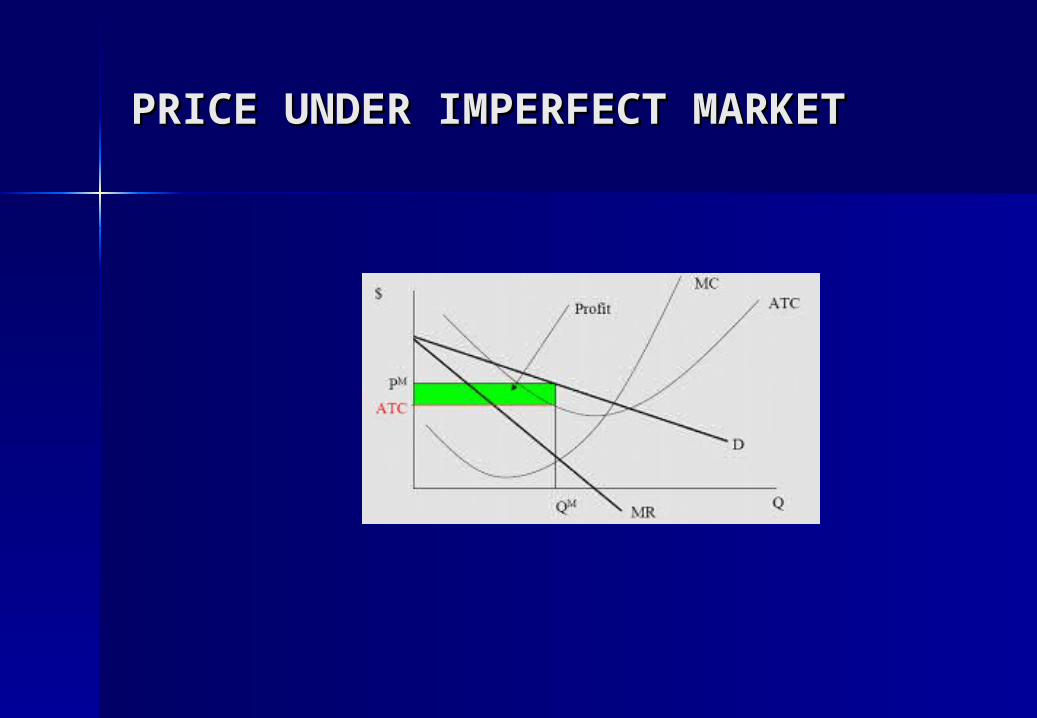

PRICE UNDER IMPERFECT MARKETPRICE UNDER IMPERFECT MARKET

METHODS OF PRICING:METHODS OF PRICING: COST BASED PRICING -COST PLUS PRICING:COST BASED PRICING -COST PLUS PRICING: This is also called full cost or markup pricing here This is also called full cost or markup pricing here

the average cost at normal capacity of output is the average cost at normal capacity of output is ascertained and then a conventional margin of ascertained and then a conventional margin of profit is added to the cost to arrive at the price. In profit is added to the cost to arrive at the price. In other words find out the product units total cost other words find out the product units total cost and add a percentage of profit to arrive at the and add a percentage of profit to arrive at the selling priceselling price

MARGINAL COST PRICINGMARGINAL COST PRICING:: In marginal cost pricing selling price is fixed In marginal cost pricing selling price is fixed

in such away that it covers fully the variable or in such away that it covers fully the variable or marginal cost and contributed towards recovery of marginal cost and contributed towards recovery of fixed cost fully or partially depending upon the fixed cost fully or partially depending upon the market situations in times of stiff competition market situations in times of stiff competition marginal cost offers a guide tome to how far the marginal cost offers a guide tome to how far the selling price can be loweredselling price can be lowered

COMPETITION BASED PRICING --COMPETITION BASED PRICING --SEALED BID PRICING:SEALED BID PRICING:

This method is more popular in tenders and This method is more popular in tenders and contracts. Each contracting from quotes its contracts. Each contracting from quotes its price in a sealed cover called ‘tender’ all price in a sealed cover called ‘tender’ all the tenders are opened on a scheduled date the tenders are opened on a scheduled date and the person who quotes the lowest price and the person who quotes the lowest price other things remaining the same is awarded other things remaining the same is awarded the contract. the contract.

GOING RATE PRICING:GOING RATE PRICING: Here the price charged by the firm by Here the price charged by the firm by

based upon the cost of the production (or) based upon the cost of the production (or) the total cost of the industry where costs the total cost of the industry where costs are particularly difficult to measure this are particularly difficult to measure this may seem to be the logical first step in may seem to be the logical first step in rational pricing policy.rational pricing policy.

STRATEGY BASED PRICING - MARKET STRATEGY BASED PRICING - MARKET SKIMMING:SKIMMING:

When the product is introduced for the first time in When the product is introduced for the first time in the market company follows this method under this the market company follows this method under this method the company fixes a very high price for the method the company fixes a very high price for the product the main idea is to charge the customer product the main idea is to charge the customer maximum possible. In this situation all cannot afford maximum possible. In this situation all cannot afford except a very few. As the time passes by the price except a very few. As the time passes by the price comes down and more people can afford to buy. comes down and more people can afford to buy.

MARKET PENERATION:MARKET PENERATION: This is exactly opposite to the market This is exactly opposite to the market

skimming method. Here the price of the product is skimming method. Here the price of the product is fixed so low that the company an increase its fixed so low that the company an increase its market share the company attains profits with market share the company attains profits with increasing volumes and increase in the market increasing volumes and increase in the market share. More often the companies believe that it is share. More often the companies believe that it is necessary to dominate the market in the long-run necessary to dominate the market in the long-run the making profits in the short-run the making profits in the short-run

UNIT – V UNIT – V

BUSINESS BUSINESS ORGANISATIONORGANISATION

““Business may be defined as the regular Business may be defined as the regular production or purchase and sale of goods production or purchase and sale of goods with the object of earning profits and with the object of earning profits and acquiring wealth through satisfaction of acquiring wealth through satisfaction of human wants” human wants”

In the words of Petersen and plowman, In the words of Petersen and plowman, “Business may be defined as activities is “Business may be defined as activities is which different person exchange something which different person exchange something of value whether goods or services for of value whether goods or services for mutual gain or profit”mutual gain or profit”

Characteristics of BusinessCharacteristics of Business:-:- From the above definitions, Business will have the following From the above definitions, Business will have the following

characteristics.characteristics. ExchangeExchange: - Business involves exchange of goods and : - Business involves exchange of goods and

services for money or money’s worth. On way transactions such services for money or money’s worth. On way transactions such as gift given by one person to another do not constitute business.as gift given by one person to another do not constitute business.

Continuity of OperationContinuity of Operation: -: - Business pre supposes Business pre supposes continuity of operations these should be a regular sequence of continuity of operations these should be a regular sequence of dealing isolated transaction such as sale of house do not dealing isolated transaction such as sale of house do not constitute business.constitute business.

Profit MotiveProfit Motive: - Business activity is motivated by desire to : - Business activity is motivated by desire to earn profit business has other objectives apart from. But profit is earn profit business has other objectives apart from. But profit is desired as a fair compensation for the efforts of the businessman.desired as a fair compensation for the efforts of the businessman.

RiskRisk: - Every business involves some element of uncertainty in : - Every business involves some element of uncertainty in the operating environment. For ex; one may not be able to sell all the operating environment. For ex; one may not be able to sell all the goods produced or purchased, amount due from credit sales the goods produced or purchased, amount due from credit sales may not be collected etc. Risk is an inherent part of businessmay not be collected etc. Risk is an inherent part of business

Organized ActivityOrganized Activity: - Business needs to be properly : - Business needs to be properly organized to be succeeful. There is a need for clear definition of organized to be succeeful. There is a need for clear definition of roles and responsibilities of various people. Systems are designed roles and responsibilities of various people. Systems are designed and implemented so that there is co-ordination between the and implemented so that there is co-ordination between the various activities.various activities.

CLASIFICATION OF CLASIFICATION OF BUSINESSBUSINESS

1) Sole trader or Proprietorship1) Sole trader or Proprietorship 2) Partnership2) Partnership 3) Joint Stock Company3) Joint Stock Company

Sole trader or ProprietorshipSole trader or Proprietorship

Sole trading business is the simplest and oldest and Sole trading business is the simplest and oldest and natural from of business organization. It is also natural from of business organization. It is also called sole proprietorship “called sole proprietorship “solesole” means ” means oneone. Sole . Sole tradertrader impels that there is only one trader who is impels that there is only one trader who is the owner of the business. Such person introduces the owner of the business. Such person introduces his own capital or borrows from others. uses his his own capital or borrows from others. uses his own skills or employs people working under his own skills or employs people working under his direction, is in personal touch with the routing of direction, is in personal touch with the routing of the business, takes all the decisions concerning the the business, takes all the decisions concerning the business and is completely responsible for the business and is completely responsible for the profits made or losses incurred by the business .the profits made or losses incurred by the business .the person is called a sole trader.person is called a sole trader.

PARTNERSHIP PARTNERSHIP

According to the Oxford Dictionary for the According to the Oxford Dictionary for the Business World. “Partner is a person who Business World. “Partner is a person who shares or takes part in activities of another shares or takes part in activities of another person. person.

Partnership is an association of two or Partnership is an association of two or more people formed for the purpose of more people formed for the purpose of carrying on a business”.carrying on a business”.

According to According to Indian partnership act Indian partnership act 19321932””TheThe business which is organized by two business which is organized by two are more than the two persons for the purpose are more than the two persons for the purpose of distribution of profit and losses equally” of distribution of profit and losses equally”

CompanyCompany

““An artificial personAn artificial person (being an association of (being an association of natural persons) natural persons) recognized by lawrecognized by law, with a , with a distinctive name, a distinctive name, a common seal,common seal, a common a common capital comprising of transferable shares of fixed capital comprising of transferable shares of fixed value carrying limited liability, and having a value carrying limited liability, and having a perpetual (continuous uninterrupted) succession”- perpetual (continuous uninterrupted) succession”-

““A company having permanent paid up or A company having permanent paid up or nominal share capital of fixed amount nominal share capital of fixed amount divided into shares, also of fixed amount, divided into shares, also of fixed amount, held and transferable as stock and formed held and transferable as stock and formed on the principles of having in its members on the principles of having in its members only the holders of those shares or stocks only the holders of those shares or stocks and no other persons” – and no other persons” – Indian Indian Companies Act, 1956Companies Act, 1956..

PUBLIC ENTERPRISESPUBLIC ENTERPRISES Public enterprises as a form of business Public enterprises as a form of business

organization have gained importance only in organization have gained importance only in recent times. Industrial revolution helped all recent times. Industrial revolution helped all – round growth of industries. Private – round growth of industries. Private entrepreneurs started working only for profit entrepreneurs started working only for profit motive. The exploitation of consumers and motive. The exploitation of consumers and workers by private entrepreneur become the workers by private entrepreneur become the order of the day. The industrial resolutions order of the day. The industrial resolutions of 1948 and 1956 have clearly defined the of 1948 and 1956 have clearly defined the role of public and private sectors.role of public and private sectors.

Enterprise is and undertaking owned Enterprise is and undertaking owned and controlled by local or state or and controlled by local or state or central government. Whole of the central government. Whole of the investment is done by the investment is done by the government.government.

Objectives of Public enterprisesObjectives of Public enterprises

Helping all-round industrialization.Helping all-round industrialization. Establishing enterprises, requiring heavy Establishing enterprises, requiring heavy

investment.investment. To provide necessities.To provide necessities. To have balanced economic growth.To have balanced economic growth. To avoid concentration of economic powerTo avoid concentration of economic power To establish socialistic pattern of society.To establish socialistic pattern of society. To run monopoly sector. To run monopoly sector. To exploit natural resources.To exploit natural resources. Helping in implementing government Helping in implementing government

plans.plans. To increase government resourcesTo increase government resources

UNIT- VIUNIT- VI

CAPITALCAPITAL

&&

CAPITAL BUDGETINGCAPITAL BUDGETING

CAPITALCAPITAL

Capital refers amount needed to starts the Capital refers amount needed to starts the business. The initial amount invested in the business. The initial amount invested in the business is called as capital to start business we business is called as capital to start business we need fixed capital. Without fixed capital one need fixed capital. Without fixed capital one cannot start any business for any type of business cannot start any business for any type of business fixed capital is required. The fixed capital can be fixed capital is required. The fixed capital can be used to purchase fixed assets of the business like. used to purchase fixed assets of the business like. Land .building, machinery and furniture etc.Land .building, machinery and furniture etc.

To run any type of business activity we need To run any type of business activity we need working capital. Working capital refers to the working capital. Working capital refers to the amount needed to run day-to-day expenses of the amount needed to run day-to-day expenses of the business.business.

“ “Capital does not include money only but it includes Capital does not include money only but it includes money worth also”. money worth also”.

NEED OF CAPITALNEED OF CAPITAL

To promote a businessTo promote a business To conduct business operations smoothly.To conduct business operations smoothly. To establishment of the organizationTo establishment of the organization To pay taxes like income tax & sales tax.To pay taxes like income tax & sales tax. To pay dividends and interests.To pay dividends and interests. Support the workers welfare programmers Support the workers welfare programmers At the time of winding up the company may need funds to At the time of winding up the company may need funds to

meet the liquidation expanses.meet the liquidation expanses. ExpansionExpansion DiversificationDiversification Research and developmentResearch and development Replacement & modernizationReplacement & modernization MiscellaneousMiscellaneous

TYPES OF CAPITALTYPES OF CAPITALCapital can be classified into two types:-Capital can be classified into two types:- Fixed capital (or)Block capitalFixed capital (or)Block capital Working capitalWorking capital FIXED CAPITALFIXED CAPITAL:: To start business we need fixed capital. To start business we need fixed capital.

Without fixed capital one cannot start any business for Without fixed capital one cannot start any business for any type of business fixed capital is required. The fixed any type of business fixed capital is required. The fixed capital can be used to purchase fixed assets of the capital can be used to purchase fixed assets of the business like. Land .building, machinery and furniture etcbusiness like. Land .building, machinery and furniture etc

WORKING CAPITAL:WORKING CAPITAL: To run any type of business activity we need To run any type of business activity we need

working capital. Working capital refers to the amount working capital. Working capital refers to the amount needed to run day-to-day expenses of the business.needed to run day-to-day expenses of the business.

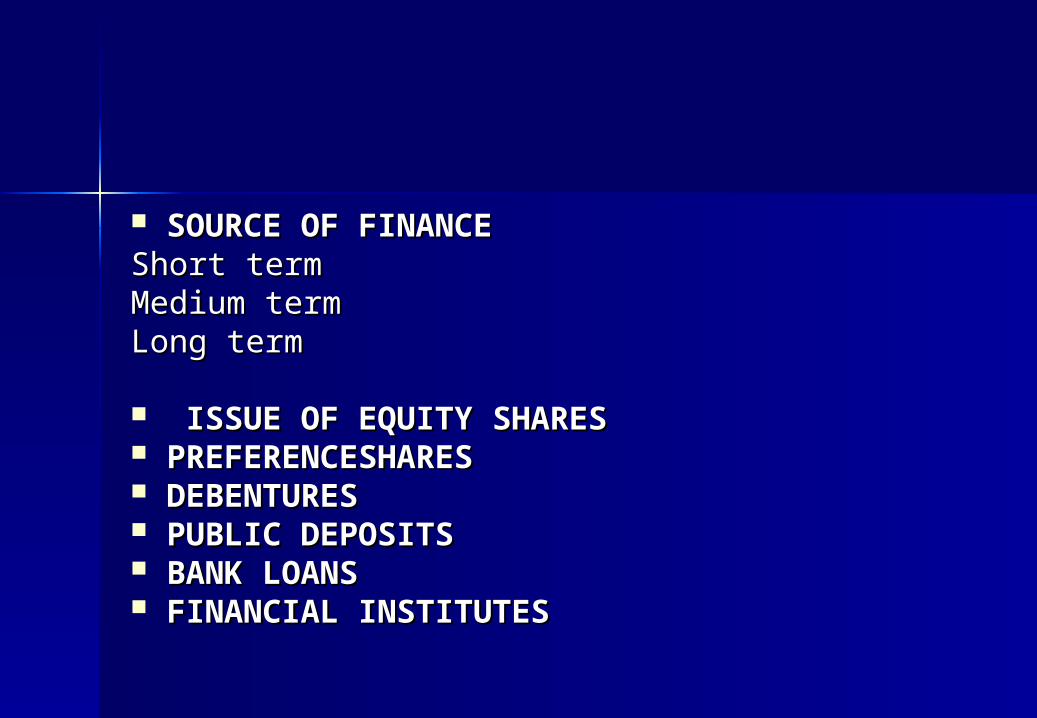

SOURCE OF FINANCESOURCE OF FINANCEShort term Short term Medium termMedium termLong term Long term ISSUE OF EQUITY SHARESISSUE OF EQUITY SHARES PREFERENCESHARESPREFERENCESHARES DEBENTURES DEBENTURES PUBLIC DEPOSITSPUBLIC DEPOSITS BANK LOANSBANK LOANS FINANCIAL INSTITUTESFINANCIAL INSTITUTES

CAPITAL BUDGETINGCAPITAL BUDGETING

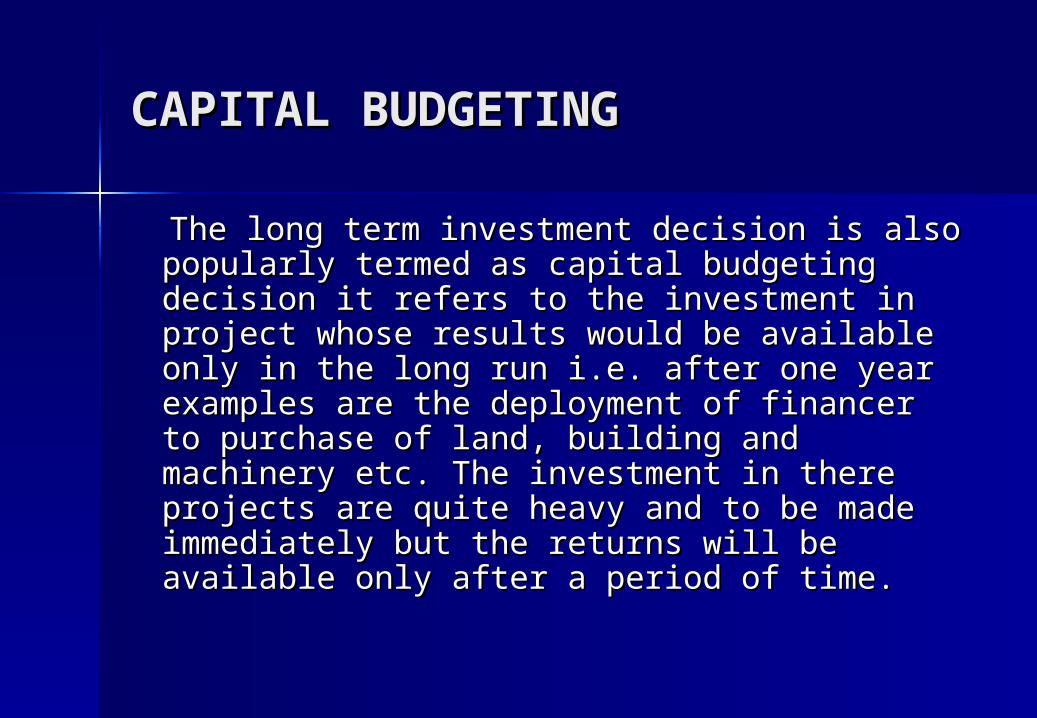

The long term investment decision is also The long term investment decision is also popularly termed as capital budgeting popularly termed as capital budgeting decision it refers to the investment in decision it refers to the investment in project whose results would be available project whose results would be available only in the long run i.e. after one year only in the long run i.e. after one year examples are the deployment of financer examples are the deployment of financer to purchase of land, building and to purchase of land, building and machinery etc. The investment in there machinery etc. The investment in there projects are quite heavy and to be made projects are quite heavy and to be made immediately but the returns will be immediately but the returns will be available only after a period of time. available only after a period of time.

CAPITAL BUDGETING METHODSCAPITAL BUDGETING METHODS

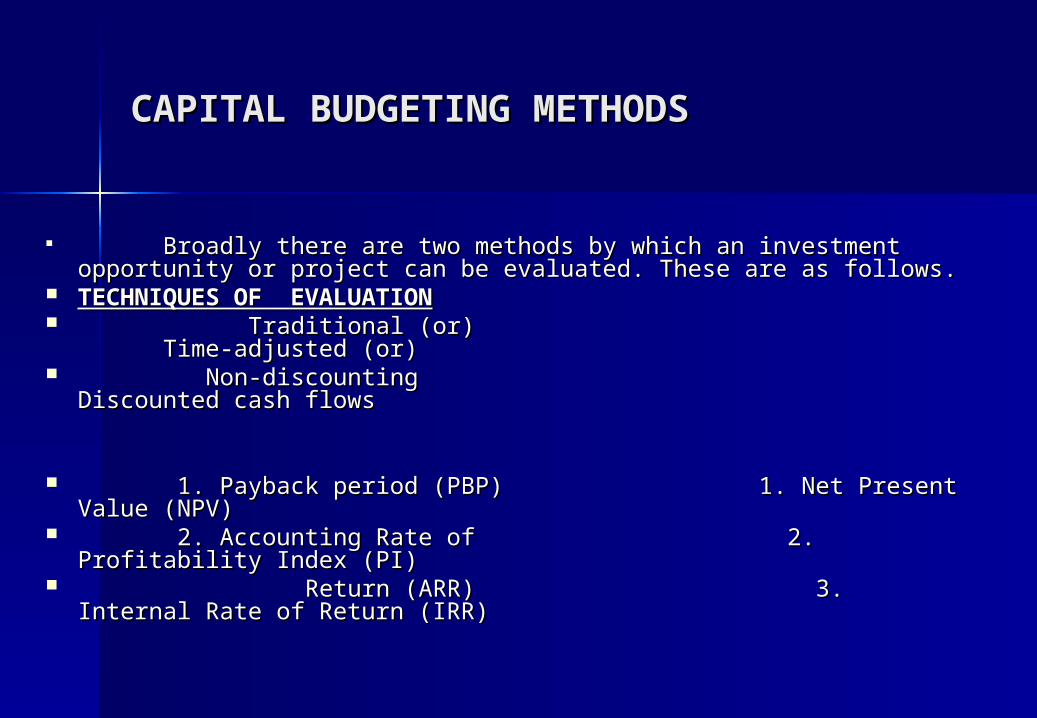

Broadly there are two methods by which an investment Broadly there are two methods by which an investment opportunity or project can be evaluated. These are as follows.opportunity or project can be evaluated. These are as follows.

TECHNIQUES OF EVALUATIONTECHNIQUES OF EVALUATION Traditional (or) Time-adjusted Traditional (or) Time-adjusted

(or)(or) Non-discounting Discounted cash flowsNon-discounting Discounted cash flows 1. Payback period (PBP) 1. Net Present Value 1. Payback period (PBP) 1. Net Present Value

(NPV)(NPV) 2. Accounting Rate of 2. Profitability Index (PI)2. Accounting Rate of 2. Profitability Index (PI) Return (ARR) 3. Internal Rate of Return Return (ARR) 3. Internal Rate of Return

(IRR)(IRR)

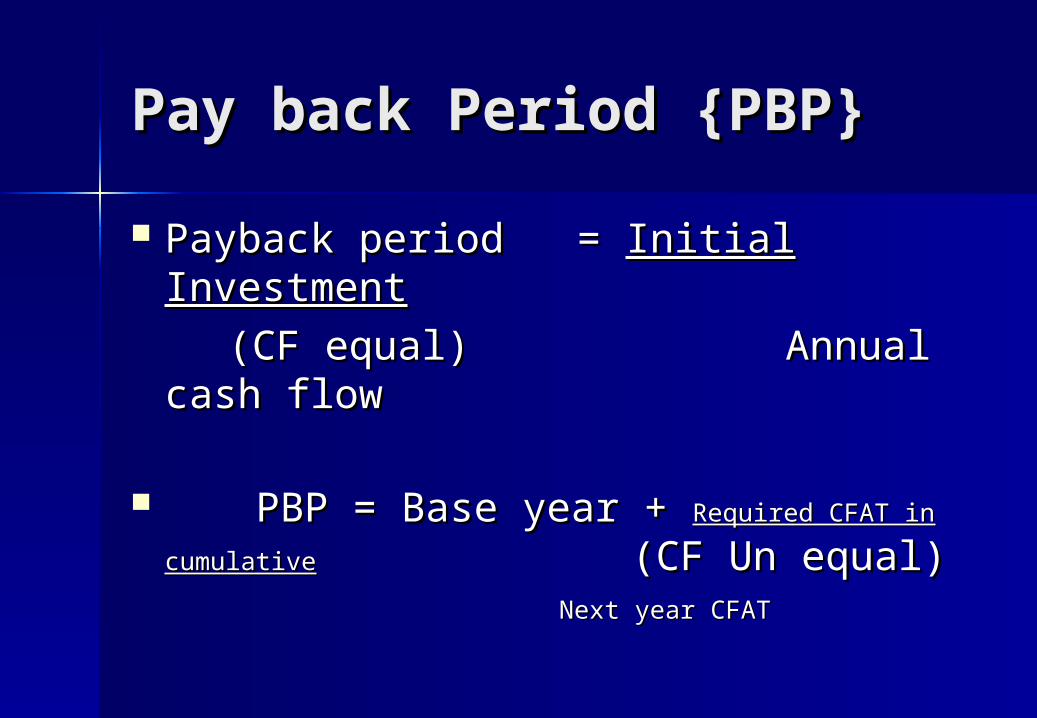

Pay back Period {PBP}Pay back Period {PBP}

Payback period = Payback period = Initial InvestmentInitial Investment

(CF equal) Annual cash flow(CF equal) Annual cash flow

PBP = Base year + PBP = Base year + Required CFAT in Required CFAT in

cumulativecumulative (CF Un equal) (CF Un equal) Next year CFATNext year CFAT

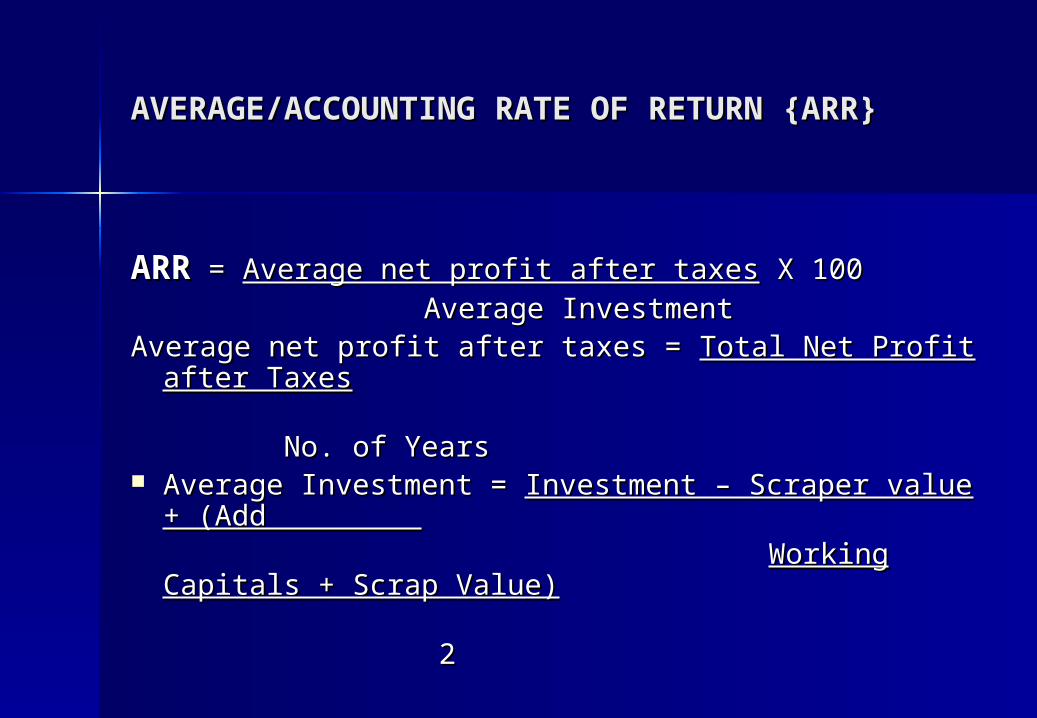

AVERAGE/ACCOUNTING RATE OF RETURN AVERAGE/ACCOUNTING RATE OF RETURN {ARR}{ARR}

ARRARR = = Average net profit after taxesAverage net profit after taxes X 100 X 100 Average InvestmentAverage InvestmentAverage net profit after taxes = Average net profit after taxes = Total Net Profit after Total Net Profit after

TaxesTaxes No. of YearsNo. of Years Average Investment = Average Investment = Investment – Scraper value Investment – Scraper value

+ (Add + (Add Working Capitals + Scrap Working Capitals + Scrap

Value)Value) 2 2

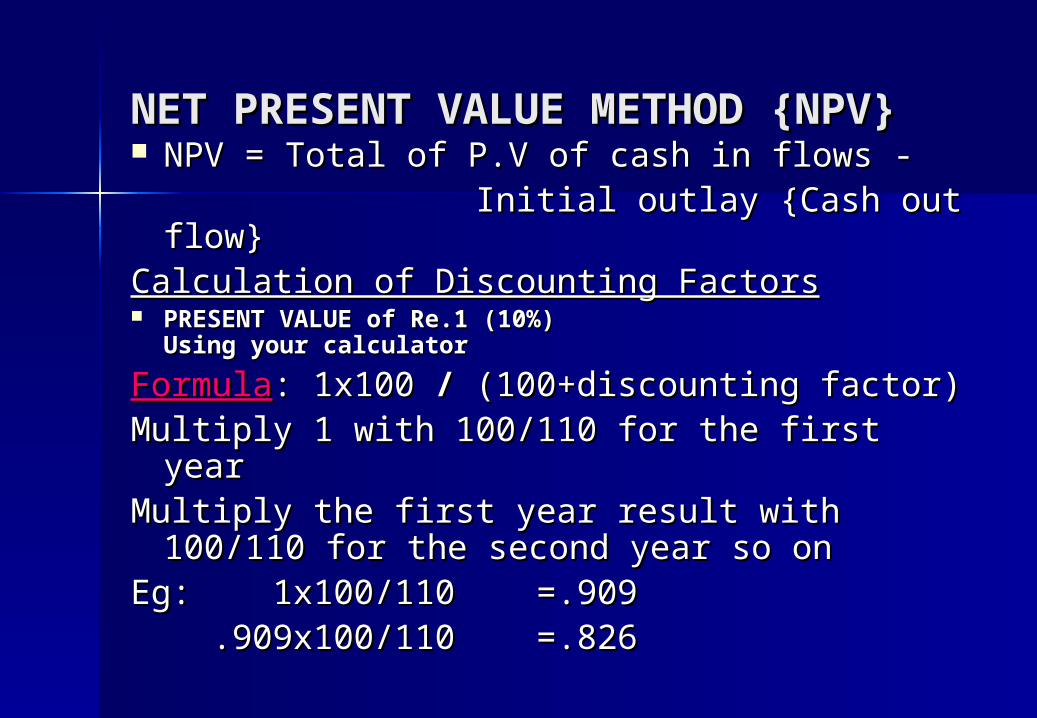

NET PRESENT VALUE METHOD NET PRESENT VALUE METHOD {NPV}{NPV} NPV = Total of P.V of cash in flows -NPV = Total of P.V of cash in flows - Initial outlay {Cash out flow}Initial outlay {Cash out flow}Calculation of Discounting FactorsCalculation of Discounting Factors PRESENT VALUE of Re.1 (10%)PRESENT VALUE of Re.1 (10%)

Using your calculatorUsing your calculator

FormulaFormula: 1x100 : 1x100 / / (100+discounting factor)(100+discounting factor)Multiply 1 with 100/110 for the first yearMultiply 1 with 100/110 for the first yearMultiply the first year result with 100/110 Multiply the first year result with 100/110

for the second year so on for the second year so on Eg: 1x100/110 =.909Eg: 1x100/110 =.909 .909x100/110 =.826.909x100/110 =.826

UNIT – VIIUNIT – VII

FINANCIAL ACCOUNTINGFINANCIAL ACCOUNTING

DefinationsDefinations AccountingAccounting is an art as well as sciences of is an art as well as sciences of

identifying, analyzing, recording, classifying and identifying, analyzing, recording, classifying and summarizing of business transactions which are summarizing of business transactions which are of a financial character and are expressed in of a financial character and are expressed in terms of money. It also includes interpretation terms of money. It also includes interpretation aspect of the recorded information.aspect of the recorded information.

Book-keepingBook-keeping is the art of recording all is the art of recording all business transactions in the books of account business transactions in the books of account maintained by businessman for that purpose. maintained by businessman for that purpose.

Keeping a separate book to recording all the Keeping a separate book to recording all the business transaction by using principle of business transaction by using principle of accounting is also called Book-keeping.accounting is also called Book-keeping.

Objectives of Book keeping & Objectives of Book keeping & Accountancy:-Accountancy:-

To ascertainment of financial position of the To ascertainment of financial position of the business organization. To determine the profit business organization. To determine the profit and loss of organizationand loss of organization

To knowing the information about capital To knowing the information about capital employed in the business.employed in the business.

To know the value of asset of the organizationTo know the value of asset of the organization Calculation of amounts due to and due by others.Calculation of amounts due to and due by others. To know how much tax to pay to the government To know how much tax to pay to the government To comparison between the current year and the To comparison between the current year and the

previous years records.previous years records. To plan the organizationTo plan the organization

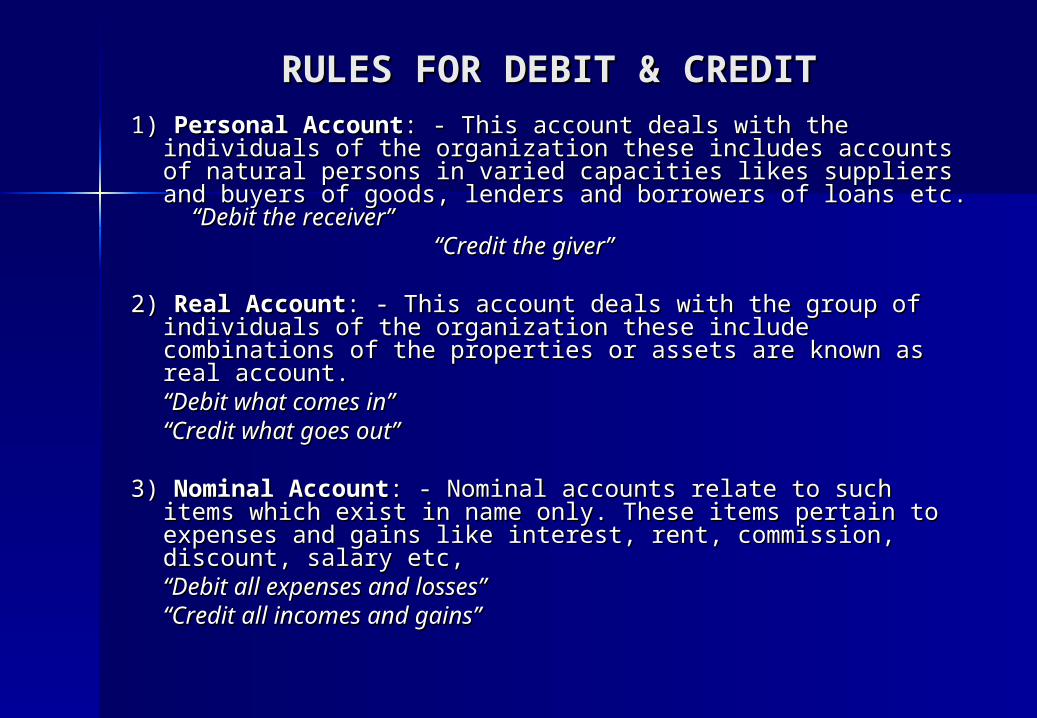

RULES FOR DEBIT & CREDITRULES FOR DEBIT & CREDIT1)1) Personal Account Personal Account: - This account deals with the individuals : - This account deals with the individuals

of the organization these includes accounts of natural of the organization these includes accounts of natural persons in varied capacities likes suppliers and buyers of persons in varied capacities likes suppliers and buyers of goods, lenders and borrowers of loans etc.goods, lenders and borrowers of loans etc. “Debit the “Debit the receiver” receiver”

“ “Credit the giver”Credit the giver”

2) 2) Real AccountReal Account: - This account deals with the group of : - This account deals with the group of individuals of the organization these include combinations of individuals of the organization these include combinations of the properties or assets are known as real account.the properties or assets are known as real account.

““Debit what comes in”Debit what comes in”““Credit what goes out”Credit what goes out”

3) 3) Nominal AccountNominal Account: - Nominal accounts relate to such items : - Nominal accounts relate to such items which exist in name only. These items pertain to expenses which exist in name only. These items pertain to expenses and gains like interest, rent, commission, discount, salary and gains like interest, rent, commission, discount, salary etc,etc,

““Debit all expenses and losses”Debit all expenses and losses”““Credit all incomes and gains”Credit all incomes and gains”

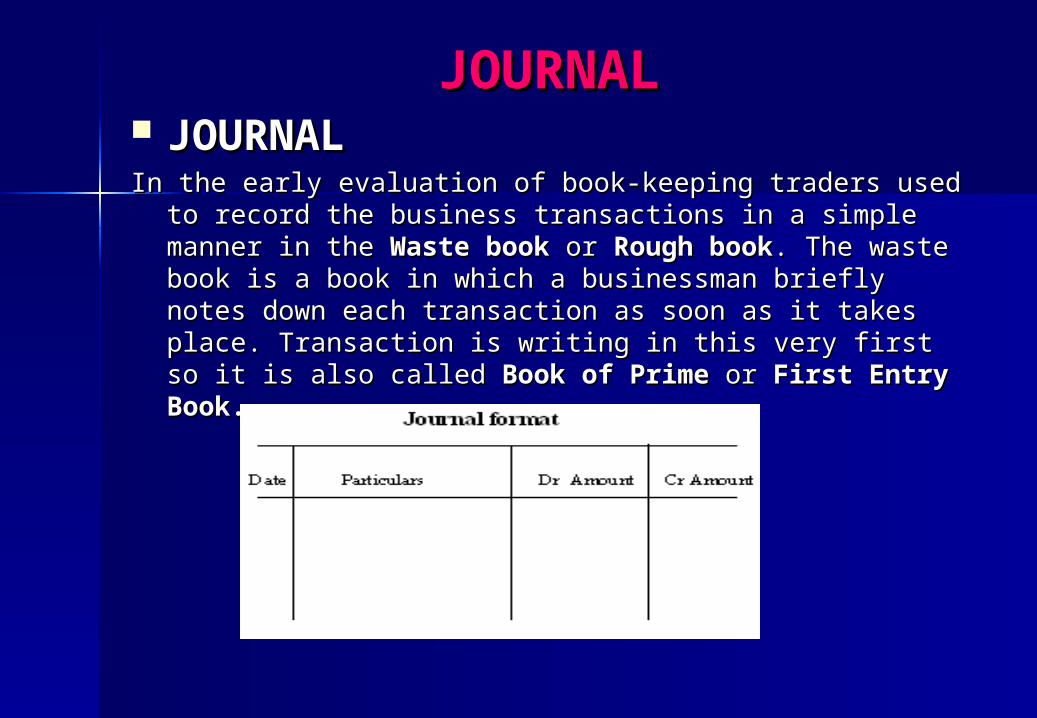

JOURNALJOURNAL JOURNALJOURNALIn the early evaluation of book-keeping traders used to record In the early evaluation of book-keeping traders used to record

the business transactions in a simple manner in the the business transactions in a simple manner in the Waste Waste bookbook or or Rough bookRough book. The waste book is a book in which a . The waste book is a book in which a businessman briefly notes down each transaction as soon businessman briefly notes down each transaction as soon as it takes place. Transaction is writing in this very first so as it takes place. Transaction is writing in this very first so it is also called it is also called Book of PrimeBook of Prime or or First Entry Book.First Entry Book.

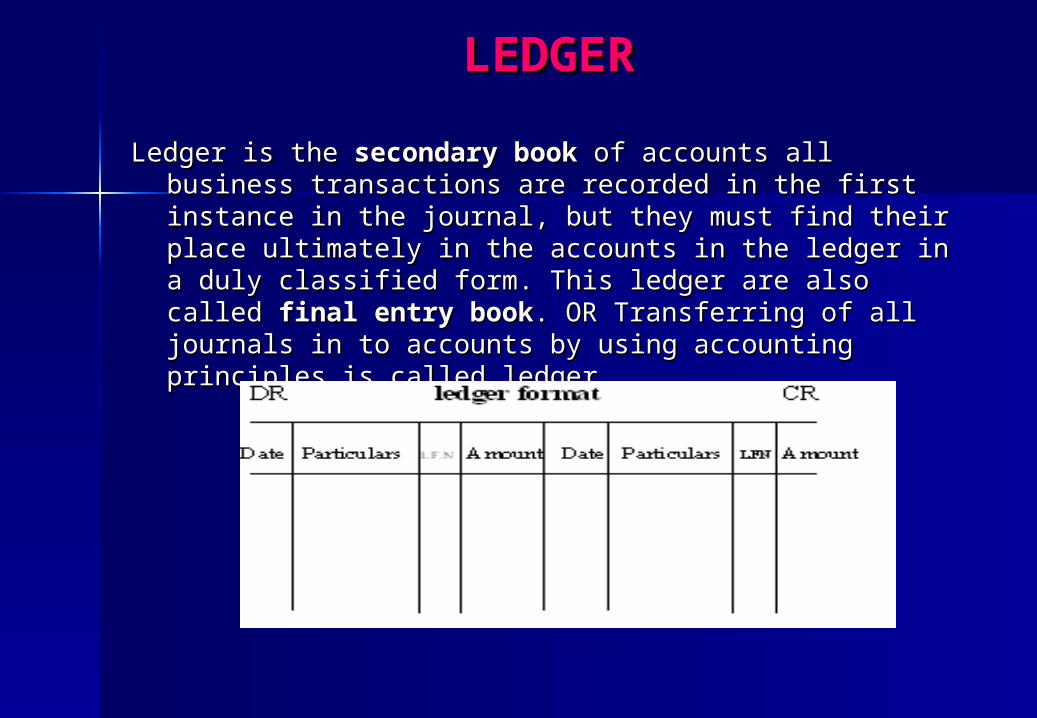

LEDGERLEDGER

Ledger is the Ledger is the secondary booksecondary book of accounts all business of accounts all business transactions are recorded in the first instance in the transactions are recorded in the first instance in the journal, but they must find their place ultimately in the journal, but they must find their place ultimately in the accounts in the ledger in a duly classified form. This ledger accounts in the ledger in a duly classified form. This ledger are also called are also called final entry bookfinal entry book. OR Transferring of all . OR Transferring of all journals in to accounts by using accounting principles is journals in to accounts by using accounting principles is called ledger.called ledger.

CASH BOOKCASH BOOK Every businessman receives cash and pays cash Every businessman receives cash and pays cash

practically every day. All the receipts and practically every day. All the receipts and payments of cash are recorded in a separate payments of cash are recorded in a separate book called the “Cash book” in modern times book called the “Cash book” in modern times cash includes not only legal tender money like cash includes not only legal tender money like notes and coins but also other forms of money notes and coins but also other forms of money like cheque bank, drafts. Etc.like cheque bank, drafts. Etc.

KINDS OF CASH BOOKSKINDS OF CASH BOOKSThe following are the most common cash booksThe following are the most common cash books

Simple or single column cash bookSimple or single column cash book Two or Double column cash bookTwo or Double column cash book Three or Triple column cash bookThree or Triple column cash book

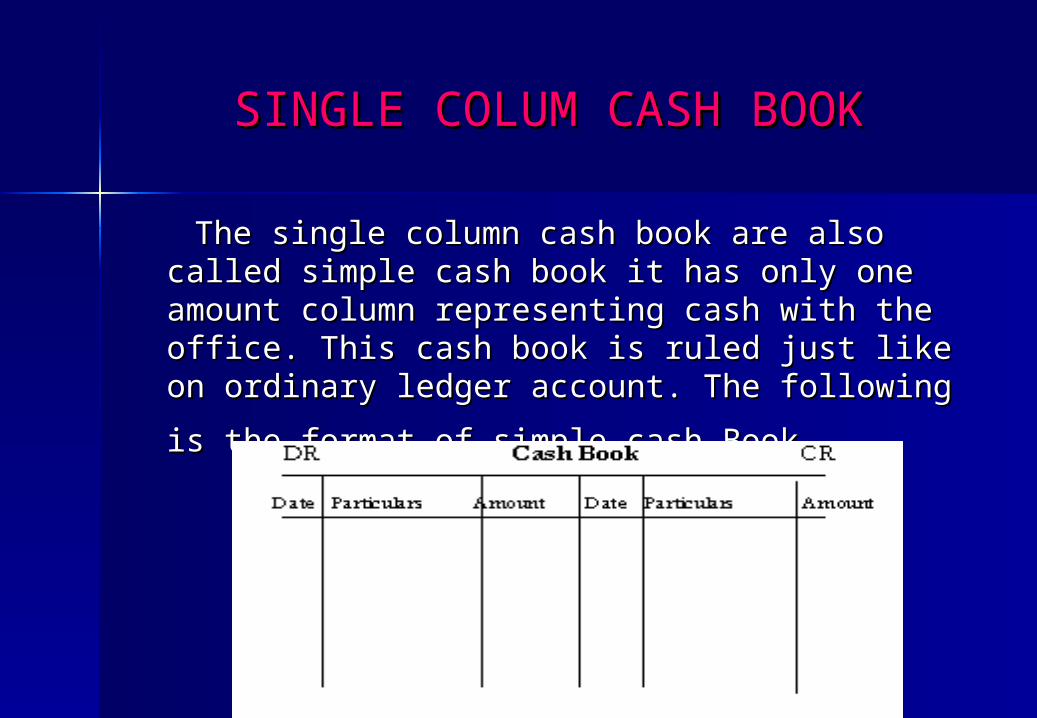

SINGLE COLUM CASH BOOKSINGLE COLUM CASH BOOK

The single column cash book are also called The single column cash book are also called simple cash book it has only one amount column simple cash book it has only one amount column representing cash with the office. This cash book representing cash with the office. This cash book is ruled just like on ordinary ledger account. The is ruled just like on ordinary ledger account. The

following is the format of simple cash Book.following is the format of simple cash Book.

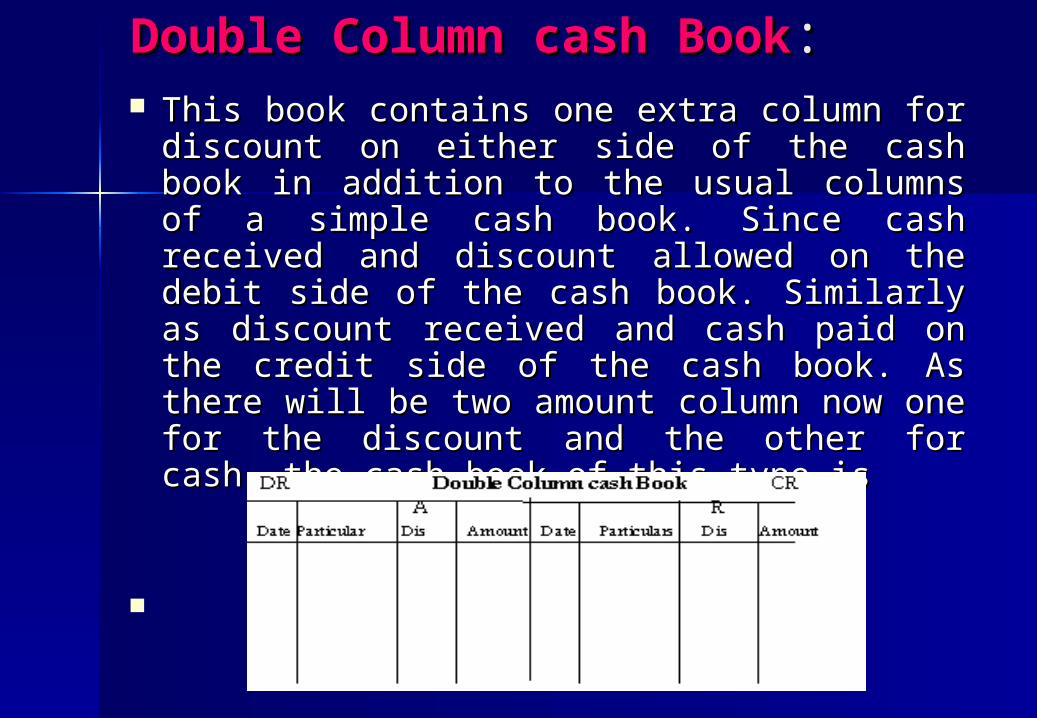

Double Column cash BookDouble Column cash Book:: This book contains one extra column for This book contains one extra column for

discount on either side of the cash book in discount on either side of the cash book in addition to the usual columns of a simple addition to the usual columns of a simple cash book. Since cash received and cash book. Since cash received and discount allowed on the debit side of the discount allowed on the debit side of the cash book. Similarly as discount received cash book. Similarly as discount received and cash paid on the credit side of the cash and cash paid on the credit side of the cash book. As there will be two amount column book. As there will be two amount column now one for the discount and the other for now one for the discount and the other for cash, the cash book of this type iscash, the cash book of this type is

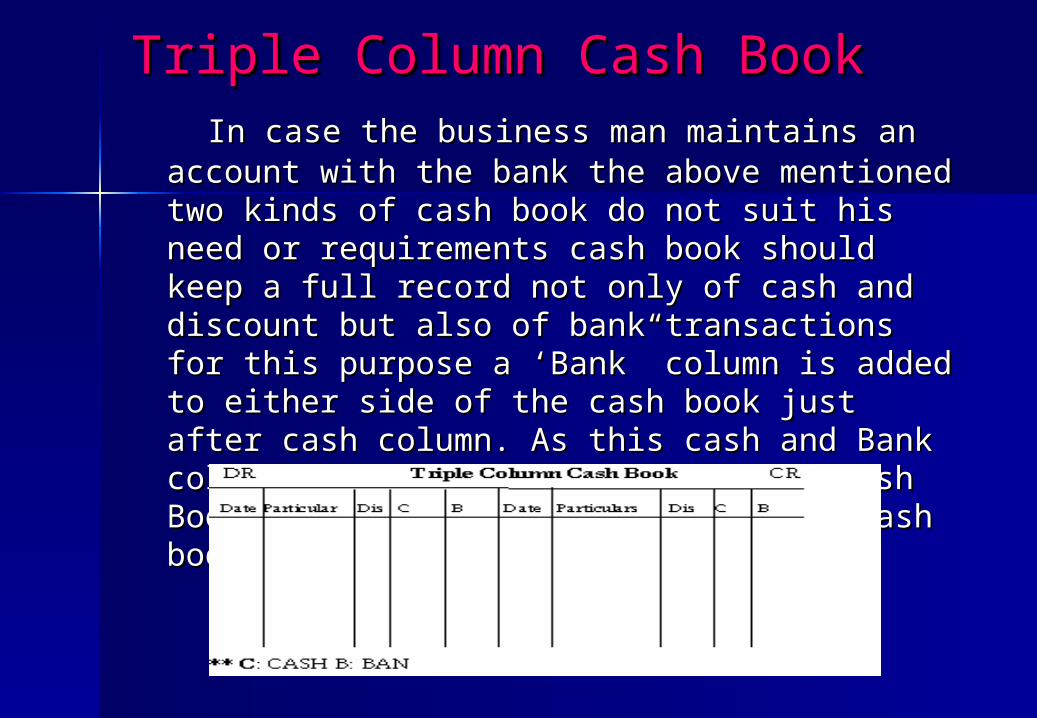

Triple Column Cash BookTriple Column Cash Book In case the business man maintains an account In case the business man maintains an account

with the bank the above mentioned two kinds of with the bank the above mentioned two kinds of cash book do not suit his need or requirements cash book do not suit his need or requirements cash book should keep a full record not only of cash book should keep a full record not only of cash and discount but also of bank transactions cash and discount but also of bank transactions for this purpose a ‘Bank” column is added to for this purpose a ‘Bank” column is added to either side of the cash book just after cash either side of the cash book just after cash column. As this cash and Bank column it is called column. As this cash and Bank column it is called three columns “Cash Book”. The format of a three columns “Cash Book”. The format of a three column cash book is given below.three column cash book is given below.

TRIAL BALANCETRIAL BALANCE

Trail balance is a statement Trail balance is a statement containing closing balances of the containing closing balances of the ledger accounts. It is prepared to ledger accounts. It is prepared to verify the arithmetical accuracy verify the arithmetical accuracy whether the totals of the debit whether the totals of the debit column and the credit column are column and the credit column are equal or not.equal or not.

Final AccountsFinal Accounts ONE OF THE MAIN OBJECTS OF MAINTAINING ONE OF THE MAIN OBJECTS OF MAINTAINING

ACCOUNTS IS TO FIND OUT THE PROFIT OR LOSS MADE BY ACCOUNTS IS TO FIND OUT THE PROFIT OR LOSS MADE BY THE BUSINESS DURING A PERIOD AND TO ASCERTAIN THE THE BUSINESS DURING A PERIOD AND TO ASCERTAIN THE FINANCIAL POSITION OF THE BUSINESS AS A GIVEN DATE. IN FINANCIAL POSITION OF THE BUSINESS AS A GIVEN DATE. IN ORDER TO KNOW THE PROFIT OR LOSS MADE BY THE ORDER TO KNOW THE PROFIT OR LOSS MADE BY THE BUSINESS, TRADING AND PROFIT AND LOSS ACCOUNT IS BUSINESS, TRADING AND PROFIT AND LOSS ACCOUNT IS PREPARED. THE POSITION OF THE BUSINESS ON THE LAST PREPARED. THE POSITION OF THE BUSINESS ON THE LAST DATE OF THE FINANCIAL YEAR WILL BE REVEALED BY THE DATE OF THE FINANCIAL YEAR WILL BE REVEALED BY THE BALANCE SHEET. THE TRADING AND PROFIT AND LOSS BALANCE SHEET. THE TRADING AND PROFIT AND LOSS ACCOUNT AND BALANCE SHEET PREPARED BY THE ACCOUNT AND BALANCE SHEET PREPARED BY THE BUSINESSMAN AT THE END OF THE TRADING PERIOD ARE BUSINESSMAN AT THE END OF THE TRADING PERIOD ARE CALLED FINAL ACCOUNTS.CALLED FINAL ACCOUNTS.

IN ORDER TO ASCERTAIN ITS INCOME AND ALSO TO IN ORDER TO ASCERTAIN ITS INCOME AND ALSO TO ASSESS THE POSITION OF ASSETS AND LIABILITIES ASSESS THE POSITION OF ASSETS AND LIABILITIES STATEMENTS ARE PREPARED ARE KNOW AS FINANCIAL STATEMENTS ARE PREPARED ARE KNOW AS FINANCIAL STATEMENT. THESE STATEMENTS ARE ALSO CALLED WITH STATEMENT. THESE STATEMENTS ARE ALSO CALLED WITH THEIR TRADITIONAL NAME AS FINAL ACCOUNTSTHEIR TRADITIONAL NAME AS FINAL ACCOUNTS

FINAL STATEMENTS ARE DIVIDED IN TWO PARTS. I.E., FINAL STATEMENTS ARE DIVIDED IN TWO PARTS. I.E., INCOME STATEMENTS AND POSITION STATEMENTS. THE INCOME STATEMENTS AND POSITION STATEMENTS. THE TERM INCOME STATEMENT IS TRADITIONALLY KNOWN AS TERM INCOME STATEMENT IS TRADITIONALLY KNOWN AS TRADING AND PROFIT AND LOSS ACCOUNT AND POSITION TRADING AND PROFIT AND LOSS ACCOUNT AND POSITION STATEMENTS ARE KNOWN AS BALANCE SHEET.STATEMENTS ARE KNOWN AS BALANCE SHEET.

Preparation of Final AccountsPreparation of Final Accounts:: THERE ARE THREE FOLLOWING STAGES OF THERE ARE THREE FOLLOWING STAGES OF

PREPARING FINAL ACCOUNTS OF A TRADING PREPARING FINAL ACCOUNTS OF A TRADING CONCERN.CONCERN.

TRADING ACCOUNTTRADING ACCOUNTPROFIT AND LOSS ACCOUNTPROFIT AND LOSS ACCOUNTBALANCE SHEETBALANCE SHEET TRADING ACCOUNT:-TRADING ACCOUNT:-

TTrading account is prepared mainly to rading account is prepared mainly to know the “profitability” of the goods brought and know the “profitability” of the goods brought and sold by the businessman. It show the result of sold by the businessman. It show the result of trading i.E. Buying and selling of goods called trading i.E. Buying and selling of goods called ““gross profit or gross lossgross profit or gross loss””

“ “THE DIFFERENCE BETWEEN THE SALES AND THE DIFFERENCE BETWEEN THE SALES AND

COST OF GOODS SOLD IS GROSS PROFIT OR COST OF GOODS SOLD IS GROSS PROFIT OR GROSS LOSS”GROSS LOSS”

PROFIT AND LOSS ACCOUNT:-PROFIT AND LOSS ACCOUNT:- TTHE PROFIT AND LOSS ACCOUNT IS AN HE PROFIT AND LOSS ACCOUNT IS AN

ACCOUNT, WHICH SHOWS THE NET PROFIT OR ACCOUNT, WHICH SHOWS THE NET PROFIT OR NET LOSS OF A BUSINESS FOR A PARTICULAR NET LOSS OF A BUSINESS FOR A PARTICULAR PERIOD. ALL INDIRECT EXPENSES SUCH AS PERIOD. ALL INDIRECT EXPENSES SUCH AS ADMINISTRATIVE OR MANAGEMENT EXPENSES, ADMINISTRATIVE OR MANAGEMENT EXPENSES, SELLING AND DISTRIBUTION EXPENSES. SELLING AND DISTRIBUTION EXPENSES. FINANCIAL EXPENSES AND OTHER ITEMS SUCH FINANCIAL EXPENSES AND OTHER ITEMS SUCH AS DEPRECIATION, ETC ARE TAKEN DEBIT SIDE. AS DEPRECIATION, ETC ARE TAKEN DEBIT SIDE. GROSS PROFIT AND ALL OTHER INCOME ITEMS GROSS PROFIT AND ALL OTHER INCOME ITEMS ARE TAKEN CREDIT SIDE. SUCH AS INTEREST ARE TAKEN CREDIT SIDE. SUCH AS INTEREST RECEIVED, DISCOUNT RECEIVED, ECT. THE RECEIVED, DISCOUNT RECEIVED, ECT. THE DIFFERENCE BETWEEN TWO SIDES IS EITHER DIFFERENCE BETWEEN TWO SIDES IS EITHER NET NET PROFIT OR NET LOSSPROFIT OR NET LOSS, WHICH IS TRANSFERRED , WHICH IS TRANSFERRED TO CAPITAL ACCOUNT.TO CAPITAL ACCOUNT.

BALANCE SHEET: -BALANCE SHEET: - BALANCE SHEET IS PREPARED TO KNOW BALANCE SHEET IS PREPARED TO KNOW

THE FINANCIAL POSITION OF A BUSINESS THE FINANCIAL POSITION OF A BUSINESS ON A PARTICULAR DATE. IT IS A ON A PARTICULAR DATE. IT IS A STATEMENT, WHICH SHOWS THE ASSETS STATEMENT, WHICH SHOWS THE ASSETS AND LIABILITIES OF A BUSINESS AS ON A AND LIABILITIES OF A BUSINESS AS ON A PARTICULAR DATE. IT SHOWS” WHAT A PARTICULAR DATE. IT SHOWS” WHAT A BUSINESS OWNS AND WHAT IT OWES” BUSINESS OWNS AND WHAT IT OWES” BALANCE SHEET IS A STATEMENT AND NOT BALANCE SHEET IS A STATEMENT AND NOT AN ACCOUNT IT DOES NOT HAVE DEBIT AN ACCOUNT IT DOES NOT HAVE DEBIT AND CREDIT SIDES. IT IS DIVIDED IN TO AND CREDIT SIDES. IT IS DIVIDED IN TO TWO SIDES LEFT SIDE AND RIGHT SIDE. TWO SIDES LEFT SIDE AND RIGHT SIDE. THE LEFT SIDE IS CALLED THE LIABILITIES THE LEFT SIDE IS CALLED THE LIABILITIES SIDE AND THE RIGHT SIDE IS CALLED THE SIDE AND THE RIGHT SIDE IS CALLED THE ASSETS SIDE.ASSETS SIDE.

ADJUSTMENTSADJUSTMENTS

An adjustment is a transaction which has An adjustment is a transaction which has not been taken into consideration while not been taken into consideration while preparing the trial balance. But now preparing the trial balance. But now considered for the purpose of preparing considered for the purpose of preparing final accountsfinal accounts

If any item of adjustment appears outside If any item of adjustment appears outside the trial balance. it will e shown at two the trial balance. it will e shown at two places in the final accounts. The places in the final accounts. The treatment of such item has been shown as treatment of such item has been shown as follows. follows.

Treating of AdjustmentsTreating of Adjustments

The treatment of such main items is as followsThe treatment of such main items is as follows1) 1) CLOSING STOCKCLOSING STOCK

– IN THE TRADING ACCOUNT CR SIDEIN THE TRADING ACCOUNT CR SIDE– IN THE BALANCE SHEET ASSET SIDEIN THE BALANCE SHEET ASSET SIDE

2) 2) OUTSTANDING WAGESOUTSTANDING WAGES– IN THE TRADING ACCOUNT ADD TO WAGESIN THE TRADING ACCOUNT ADD TO WAGES– IN THE BALANCE SHEET LIABILITIES IN THE BALANCE SHEET LIABILITIES

3) 3) OUTSTANDING SALARIESOUTSTANDING SALARIES– IN THE TRADING ACCOUNT ADD TO SALARIESIN THE TRADING ACCOUNT ADD TO SALARIES– IN THE BALANCE SHEET LIABILITIES SIDEIN THE BALANCE SHEET LIABILITIES SIDE

4) 4) PREPAID INSURANCEPREPAID INSURANCE IN THE P & L A/C LESS FROM INSURANCE IN THE P & L A/C LESS FROM INSURANCE IN THE BALANCE SHEET ASSETS SIDEIN THE BALANCE SHEET ASSETS SIDE 5) 5) INTEREST ON CAPITALINTEREST ON CAPITAL IN THE P & L A/C DR SIDEIN THE P & L A/C DR SIDE IN THE BALANCE SHEET ADD TO CAPITALIN THE BALANCE SHEET ADD TO CAPITAL

UNIT - VIIIUNIT - VIII

RATIO ANALYSISRATIO ANALYSIS

A ratio is a simple mathematical A ratio is a simple mathematical expression. It is a number expressed expression. It is a number expressed in terms of another number expressing in terms of another number expressing the quantitative relationship between the quantitative relationship between the two. Ratio analysis is the the two. Ratio analysis is the technique of inter petition of financial technique of inter petition of financial statements with the help of various statements with the help of various meaningful ratio’s.meaningful ratio’s.

Importance /AdvantagesImportance /Advantages

1.1. Comparison of past dataComparison of past data2.2. Comparison of one firm with another firmComparison of one firm with another firm3.3. Comparison of one firm with the industryComparison of one firm with the industry4.4. Comparison of an achieved performance with pre-determined Comparison of an achieved performance with pre-determined

standards.standards.5.5. Comparison of one department of a concern with other Comparison of one department of a concern with other

departments. departments. 6.6. ““The Ratios can be expressed as percentage or properties or times The Ratios can be expressed as percentage or properties or times

based on the nature of ratio.”based on the nature of ratio.”7.7. Ratio analysis simplifies the understanding of financial statements. Ratio analysis simplifies the understanding of financial statements. 8.8. Ratios serve as effective control tools.Ratios serve as effective control tools.9.9. Ratio facilitate inter firm and intra firm comparisons.Ratio facilitate inter firm and intra firm comparisons.10.10. Ratio contributes significantly towards effective planning and Ratio contributes significantly towards effective planning and

forecasting. forecasting. 11.11. Ratio brings out the inter-relationship among various financial Ratio brings out the inter-relationship among various financial

figures and brings to light their financial significance and it is a figures and brings to light their financial significance and it is a device to analyses and interprets the financial health of the device to analyses and interprets the financial health of the enterprise.enterprise.

12.12. Useful in locating the weak spots of the business.Useful in locating the weak spots of the business.13.13. Useful in comparison of performance.Useful in comparison of performance.14.14. Useful in simplifying accounting figures.Useful in simplifying accounting figures.

LIMITATION OF RATIOLIMITATION OF RATIO1.1. False results it based on incorrect accounting data.False results it based on incorrect accounting data.2.2. No idea of probable happenings in future.No idea of probable happenings in future.3.3. Ratio analysis suffers from lack of consistency.Ratio analysis suffers from lack of consistency.4.4. Ratio is volatile and can be influenced by a single Ratio is volatile and can be influenced by a single

transaction with extreme value.transaction with extreme value.5.5. Ratio is based on past data and hence cannot be reliable Ratio is based on past data and hence cannot be reliable

guide to future performance.guide to future performance.6.6. Ratio is only indicators they need a proper analysis by a Ratio is only indicators they need a proper analysis by a

capable management. They are only the means. And not capable management. They are only the means. And not an end in the interpretation of financial statements.an end in the interpretation of financial statements.

7.7. Ratio can be calculated only on the basis on the data. If Ratio can be calculated only on the basis on the data. If the original data is not reliable then ratio will be the original data is not reliable then ratio will be misleading.misleading.

8.8. Ratios fail to reflect the impact of price level change and Ratios fail to reflect the impact of price level change and hence can be misleading.hence can be misleading.

TYPES OF RATIOSTYPES OF RATIOS

CURRENT RATIOCURRENT RATIO QUICK RATIOQUICK RATIO GROSS PROFIT RATIOGROSS PROFIT RATIO NETPROFIT RATIONETPROFIT RATIO DEBITOR RATIODEBITOR RATIO DEBT EQUITY RATIODEBT EQUITY RATIO INVENTORY RATIOINVENTORY RATIO

THANK” QTHANK” Q

ALL THE BEST FOR YOUR EXAMSALL THE BEST FOR YOUR EXAMS