naic blanks (e) working group · insurance and banking affiliation: ... add a question to the...

TRANSCRIPT

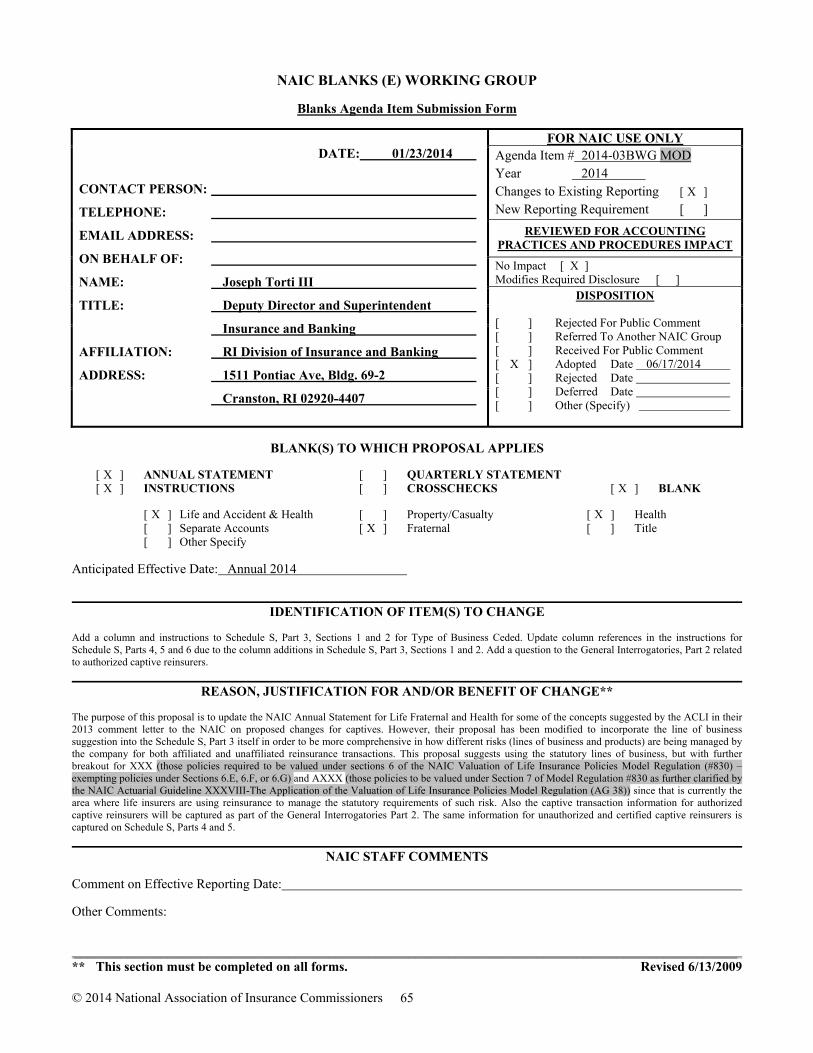

© 2014 National Association of Insurance Commissioners 65

NAIC BLANKS (E) WORKING GROUP

Blanks Agenda Item Submission Form

DATE: 01/23/2014

CONTACT PERSON:

TELEPHONE:

EMAIL ADDRESS:

ON BEHALF OF:

NAME: Joseph Torti III

TITLE: Deputy Director and Superintendent

Insurance and Banking

AFFILIATION: RI Division of Insurance and Banking

ADDRESS: 1511 Pontiac Ave, Bldg. 69-2

Cranston, RI 02920-4407

FOR NAIC USE ONLY Agenda Item # 2014-03BWG MOD Year 2014 Changes to Existing Reporting [ X ] New Reporting Requirement [ ]

REVIEWED FOR ACCOUNTING PRACTICES AND PROCEDURES IMPACT

No Impact [ X ] Modifies Required Disclosure [ ]

DISPOSITION [ ] Rejected For Public Comment [ ] Referred To Another NAIC Group [ ] Received For Public Comment [ X ] Adopted Date 06/17/2014 [ ] Rejected Date [ ] Deferred Date [ ] Other (Specify)

BLANK(S) TO WHICH PROPOSAL APPLIES

[ X ] ANNUAL STATEMENT [ ] QUARTERLY STATEMENT [ X ] INSTRUCTIONS [ ] CROSSCHECKS [ X ] BLANK

[ X ] Life and Accident & Health [ ] Property/Casualty [ X ] Health [ ] Separate Accounts [ X ] Fraternal [ ] Title [ ] Other Specify

Anticipated Effective Date: Annual 2014

IDENTIFICATION OF ITEM(S) TO CHANGE

Add a column and instructions to Schedule S, Part 3, Sections 1 and 2 for Type of Business Ceded. Update column references in the instructions for Schedule S, Parts 4, 5 and 6 due to the column additions in Schedule S, Part 3, Sections 1 and 2. Add a question to the General Interrogatories, Part 2 related to authorized captive reinsurers.

REASON, JUSTIFICATION FOR AND/OR BENEFIT OF CHANGE**

The purpose of this proposal is to update the NAIC Annual Statement for Life Fraternal and Health for some of the concepts suggested by the ACLI in their 2013 comment letter to the NAIC on proposed changes for captives. However, their proposal has been modified to incorporate the line of business suggestion into the Schedule S, Part 3 itself in order to be more comprehensive in how different risks (lines of business and products) are being managed by the company for both affiliated and unaffiliated reinsurance transactions. This proposal suggests using the statutory lines of business, but with further breakout for XXX (those policies required to be valued under sections 6 of the NAIC Valuation of Life Insurance Policies Model Regulation (#830) – exempting policies under Sections 6.E, 6.F, or 6.G) and AXXX (those policies to be valued under Section 7 of Model Regulation #830 as further clarified by the NAIC Actuarial Guideline XXXVIII-The Application of the Valuation of Life Insurance Policies Model Regulation (AG 38)) since that is currently the area where life insurers are using reinsurance to manage the statutory requirements of such risk. Also the captive transaction information for authorized captive reinsurers will be captured as part of the General Interrogatories Part 2. The same information for unauthorized and certified captive reinsurers is captured on Schedule S, Parts 4 and 5.

NAIC STAFF COMMENTS

Comment on Effective Reporting Date:

Other Comments:

___________________________________________________________________________________________________ ** This section must be completed on all forms. Revised 6/13/2009

© 2014 National Association of Insurance Commissioners 66

ANNUAL STATEMENT INSTRUCTIONS – LIFE

SCHEDULE S − PART 3 − SECTION 1

REINSURANCE CEDED LIFE INSURANCE, ANNUITIES, DEPOSIT FUNDS AND OTHER LIABILITIES WITHOUT LIFE OR DISABILITY CONTINGENCIES, AND RELATED BENEFITS LISTED BY REINSURING

COMPANY AS OF DECEMBER 31, CURRENT YEAR

NOTE: This schedule is to include Exhibit 7 cessions. Include actual reinsurance ceded on group cases but exclude jointly underwritten group contracts.

If a reporting entity has any detail lines reported for any of the following required groups, categories, or subcategories, it shall report the subtotal amount of the corresponding group, category, or subcategory, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 5 – Domiciliary Jurisdiction

Report the two-character postal code abbreviation for the domiciliary jurisdiction for U.S. states, territories and possessions. A comprehensive listing of three-character abbreviations for foreign countries is available in the appendix of these instructions. For abbreviations of foreign countries not found in the appendix, use the three-character abbreviations found at:

www.nationsonline.org/oneworld/countrycodes.htm

If a reinsurer has merged with another entity, report the domiciliary jurisdiction of the surviving entity.

Column 6 – Type of Reinsurance Ceded

Use the following abbreviations to identify the plan and type of reinsurance. For example, group coinsurance with funds withheld should be identified as COFW/G. (If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line.) NOTE: The type should be entered in all capital letters, and ALL reinsurance types must be followed by /G (for Group) or /I (for Individual).

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES CO Coinsurance ACO Annuity coinsurance

COFW Coinsurance with funds

withheld ACOFW Annuity coinsurance with

funds withheld

MCO Modified coinsurance

AMCO Annuity modified

coinsurance

© 2014 National Association of Insurance Commissioners 67

MCOFW Modified coinsurance with funds withheld

AMCOFW Annuity modified coinsurance with funds withheld

COMB Combination coinsurance/modified coinsurance

ACOMB Annuity combination coinsurance/modified coinsurance

COMBW Combination coinsurance/modified coinsurance with funds withheld

ACOMBW Annuity combination coinsurance/modified coinsurance with funds withheld

YRT Yearly renewable term

GMDB Guaranteed minimum

death benefit

CAT Catastrophe

GMDBFW Guaranteed minimum death benefit funds withheld

OTH Other reinsurance ADB Accidental death benefit DIS Disability benefits NOTE: The insurance type should be entered in all capital letters.

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

IL INDUSTRIAL LIFE FL FIXED ANNUITIES XXXL XXX LIFE IA INDEXED ANNUITIES AXXX AXXX LIFE VGAA VARIABLE GENERAL ACCOUNT

ANNUITIES CL CREDIT LIFE VSAA VARIABLE SEPARATE ACCOUNT

ANNUITIES SC SUPPLEMENTARY

CONTRACTS OA OTHER ANNUITIES

OL OTHER LIFE

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Analysis of Operations by Lines of Business and the Analysis of Annuity Operations by Lines of Business except as noted below:

XXX Life: Used to describe the actuarial reserves required to be held under Section 6

(exempting policies under 6.E, 6.F, or 6.G) of the NAIC Valuation of Life Insurance Policies Model Regulation (#830) which is commonly referred to as Regulation XXX (or, more simply, XXX).

AXXX Life: Used to describe the actuarial reserves required to be held under Section 7 of

Regulation XXX as further clarified by the NAIC Actuarial Guideline Guidance XXXVIII—The Application of the Valuation of Life Insurance Policies Model Regulation (AG 38), which is more commonly referred to as AXXX.

For year-end 2014 reporting only, those non-captive treaties that are not able to completely identify the type of business ceded can report wholly under "OL - Other Life". Detail reporting for type of business ceded will be required for year-end 2015 reporting.

© 2014 National Association of Insurance Commissioners 68

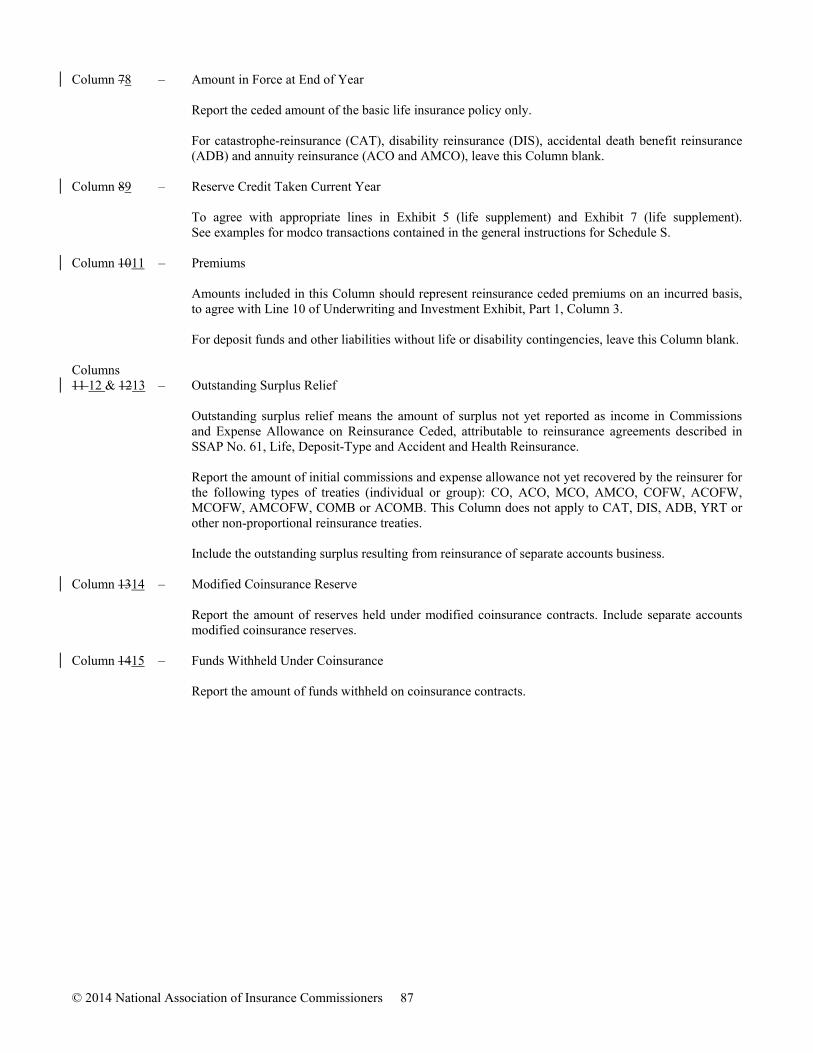

Column 78 – Amount in Force at End of Year

Report the ceded amount of the basic life insurance policy only, to agree with Line 22 of the Exhibit of Life Insurance x 1000.

For catastrophe-reinsurance (CAT), disability reinsurance (DIS), accidental death benefit reinsurance (ADB) and annuity reinsurance (ACO and AMCO), leave this column blank.

Column 89 – Reserve Credit Taken Current Year

To agree with appropriate lines in Exhibit 5 and Exhibit 7. See examples for modco transactions contained in the general instructions for Schedule S.

Column 1011 – Premiums

Amounts included in this column should represent reinsurance ceded premiums on an incurred basis, to agree with Line 20.3 of Exhibit 1, Part 1, Column 1 less Columns 8, 9 and 10.

For deposit funds and other liabilities without life or disability contingencies, leave this column blank.

Columns 11 12 & 1213 – Outstanding Surplus Relief

Outstanding surplus relief means the amount of surplus not yet reported as income in Commissions and Expense Allowance on Reinsurance Ceded, in the Summary of Operations, attributable to reinsurance agreements described in SSAP No. 61, Life, Deposit-Type and Accident and Health Reinsurance.

Report the amount of initial commissions and expense allowance not yet recovered by the reinsurer for the following types of treaties (individual or group): CO, ACO, MCO, AMCO, COFW, ACOFW, MCOFW, AMCOFW, COMB, ACOMB, ACOMBW AND COMBW. This column does not apply to CAT, DIS, ADB, YRT or other non-proportional reinsurance treaties.

Include the outstanding surplus resulting from reinsurance of separate accounts business.

Column 1314 – Modified Coinsurance Reserve

Report the amount of reserves held under modified coinsurance contracts. Include separate accounts modified coinsurance reserves. The General Account total for Column 13 14 must agree with the sum of the parenthetical amounts on Page 3, Lines 1 and 3.

Column 1415 – Funds Withheld Under Coinsurance

Report the amount of funds withheld on coinsurance contracts.

© 2014 National Association of Insurance Commissioners 69

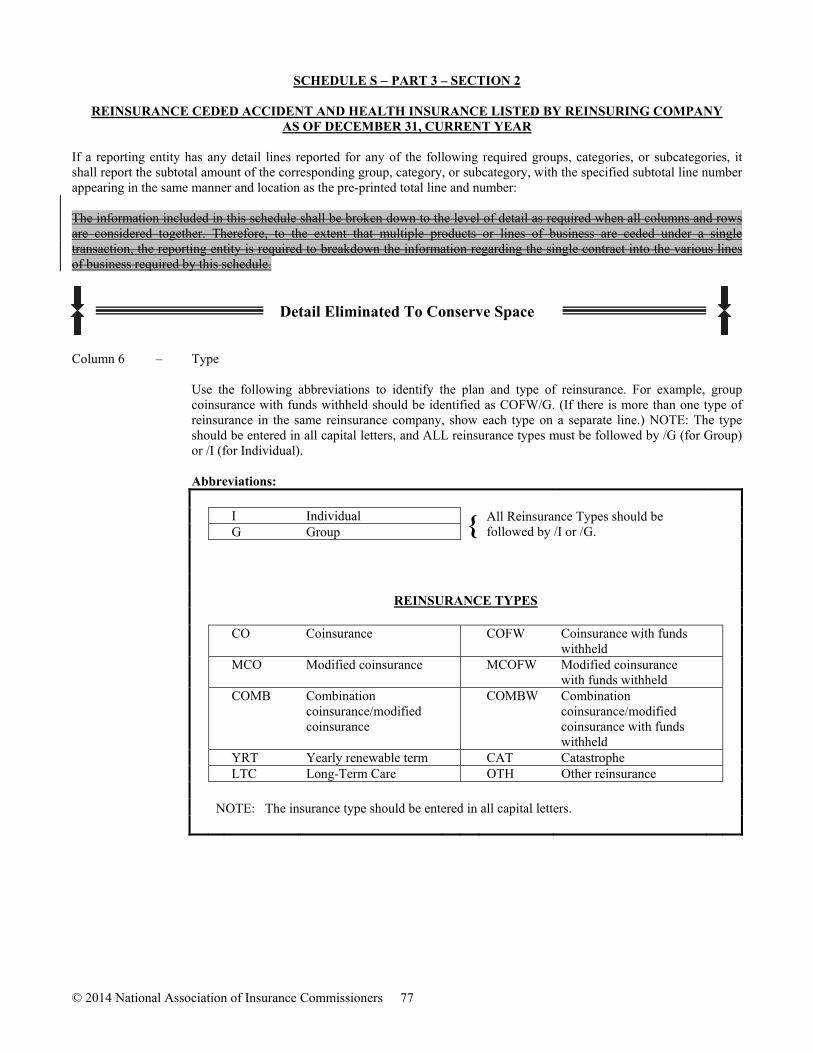

SCHEDULE S − PART 3 − SECTION 2

REINSURANCE CEDED ACCIDENT AND HEALTH INSURANCE LISTED BY REINSURING COMPANY AS OF DECEMBER 31, CURRENT YEAR

Include actual reinsurance ceded on group cases but exclude jointly underwritten group contracts. If a reporting entity has any detail lines reported for any of the following required groups, categories, or subcategories it shall report the subtotal amount of the corresponding group, category, or subcategory, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 6 – Type

Use the following abbreviations to identify the plan and type of reinsurance. For example, group coinsurance with funds withheld should be identified as COFW/G. (If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line.) NOTE: The type should be entered in all capital letters, and ALL reinsurance types must be followed by /G (for Group) or /I (for Individual).

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES

CO Coinsurance

COFW Coinsurance with funds

withheld

MCO Modified coinsurance

MCOFW Modified coinsurance

with funds withheld

COMB Combination coinsurance/modified coinsurance

COMBW Combination coinsurance/modified coinsurance with funds withheld

YRT Yearly renewable term CAT Catastrophe LTC Long-Term Care OTH Other reinsurance NOTE: The insurance type should be entered in all capital letters.

© 2014 National Association of Insurance Commissioners 70

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

CMM COMPREHENSIVE MAJOR MEDICAL STM SHORT-TERM MEDICAL

OM OTHER MEDICAL (NON=COMPREHENSIVE)

LB LIMITED BENEFIT

SD SPECIFIED/NAMED DISEASE S STUDENT A ACCIDENT ONLY OR AD&D LTC LONG-TERM CARE STDI DISABILITY INCOME – SHORT-TERM D DENTAL LTDI DISABILITY INCOME – LONG-TERM MR MEDICARE MS MEDICARE SUPPLEMENT (MEDIGAP) MDMC MEDICAID MD MEDICARE PART D – STAND-ALONE TRI TRICARE FEHBP FEDERAL EMPLOYEES HEALTH BENEFIT

PLAN CAH CREDIT A&H

SCHIP STATE CHILDREN’S HEALTH INSURANCE PROGRAM

OH OTHER HEALTH

SLEL STOP LOSS/EXCESS LOSS

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Accident and Health Policy Experience Exhibit.

Column 78 – Premiums

Amounts included in this column should represent reinsurance ceded premiums on an incurred basis and agree with Exhibit 1, Part 1, Line 20.3, Columns 8, 9 and 10.

Column 89 – Unearned Premiums (Estimated)

Amounts represent, by company, the ceded part of the unearned premium reserve included in the Active Life Reserve in Exhibit 6, Line 8.

Column 910 – Reserve Credit Taken Other Than For Unearned Premiums

This column represents the reinsurance ceded portion of the remaining Active Life Reserve (excluding unearned premiums) and the Claim Reserve reported in Exhibit 6. The sum of the totals for Columns 8 and 9 must agree with the sum of the appropriate Lines in Exhibit 6, (Line 8, Column 1 and Line 15, Column 1).

Columns 10 11 and 1112 – Outstanding Surplus Relief

Outstanding surplus relief means the amount of surplus not yet reported as income in Line 6, commissions and expense allowance on reinsurance ceded, of the Summary of Operations, attributable to reinsurance agreements described in SSAP No. 61, Life, Deposit-Type and Accident and Health Reinsurance.

Report the amount of initial commissions and expense allowance not yet recovered by the reinsurer for the following types of treaties (individual or group): CO, MCO, COFW, MCOFW, COMB or COMBW. This column does not apply to YRT or other nonproportional reinsurance treaties.

Column 1213 – Modified Coinsurance Reserve

Report the amount of reserves held under modified coinsurance contracts. The sum of the total for Column 12 13 must agree with the parenthetical amount on Page 3, Line 2.

Column 1314 – Funds Withheld Under Coinsurance

Report the amount of funds withheld on coinsurance contracts.

© 2014 National Association of Insurance Commissioners 71

SCHEDULE S − PART 4

REINSURANCE CEDED TO UNAUTHORIZED COMPANIES

Detail Eliminated To Conserve Space

Column 5 – Reserve Credit Taken

Report the amount by which the aggregate reserve for life contracts (Exhibit 5), deposit-type contracts (Exhibit 7), and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with unauthorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S, Part 3, Section 1, Column 8 9 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

SCHEDULE S − PART 5

REINSURANCE CEDED TO CERTIFIED REINSURERS

Detail Eliminated To Conserve Space

Column 9 – Reserve Credit Taken

Report the amount by which the aggregate reserve for life contracts (Exhibit 5), deposit-type contracts (Exhibit 7) and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with certified reinsurers. The amounts by company should be the same as those shown for life reinsurance ceded in Schedule S, Part 3, Section 1, Column 8 9 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

© 2014 National Association of Insurance Commissioners 72

SCHEDULE S − PART 6

FIVE-YEAR EXHIBIT OF REINSURANCE CEDED BUSINESS A. Operations Items:

Line 1 – Premiums and Annuity Considerations for Life and Accident and Health Contracts

Exhibit 1, Part 1, Line 20.3.

Detail Eliminated To Conserve Space

Line 7 – Increase in Aggregate Reserves for Life and Accident and Health Contracts

Schedule S, Part 3, Section 2, Column 89, Current Year,,

(+) Schedule S, Part 3, Section 2, Column 910, Current Year,

(–) Schedule S, Part 3, Section 2, Column 8, Prior Year,

(–) Schedule S, Part 3, Section 2, Column 9, Prior Year,

(–) Prior Year (from prior year’s statement),

(+) Schedule S, Part 3, Section 1, Column 89,

(–) Schedule S, Part 3, Section 1, Column 910,

(–) Reinsurance ceded portion of Exhibit 5A, Lines 0199999 and 0299999, Column 4. B. Balance Sheet Items:

Line 8 – Premiums and Annuity Considerations for Life and Accident and Health Contracts Deferred and Uncollected

Exhibit 1, Part 1, Lines 3.3 plus 13.3.

Line 9 – Aggregate Reserves for Life and Accident and Health Contracts

Exhibit 5, Life Insurance and Annuities, Lines 0199998 and 02999998, Column 2

(+) Exhibit 5, Lines, 0399998, 0499998, 0599998, 0699998 and 0799998, Column 2

(+) Exhibit 6, Line 8, Column 1,

(+) Exhibit 6, Line 15, Column 1.

OR

Schedule S, Part 3 Section 2, Column 89,

(+) Schedule S, Part 3 Section 2, Column 910, (+) Schedule S, Part 3 Section 1, Column 89.

Line 11 – Contract Claims Unpaid

Exhibit 8, Part 1, Line 4.3.

Detail Eliminated To Conserve Space

© 2014 National Association of Insurance Commissioners 73

PART 2 – LIFE INTERROGATORIES

Detail Eliminated To Conserve Space

10.1 Disclose the amount of reserves carried by the reporting entity because it has sold annuities with a claimant as payee

and to the extent to which the reporting entity is liable for such amounts. Include only annuities for which the property and casualty insurer obtained a release of liability from the claimant as a result of the purchase of an annuity from the reporting entity.

10.2 Disclose the name and location of the insurance company (i.e., legal entity and not group) that purchased the annuities during the current year and the aggregate statement value of annuities purchased, to the extent that the aggregate value of those annuities equals or exceeds $250,000. Include only annuities for which the property and casualty insurer obtained a release of liability from the claimant as a result of the purchase of an annuity from the reporting entity.

12.2 If the response to 12.1 is “YES”, provide for the captive affiliate the company name, NAIC company code,

domiciliary jurisdiction, reserve credit amount and the amounts supporting the reserve credit (letters of credit, trust agreements and other).

Reserve Credit: Report the amount by which the aggregate reserve for life contracts (Exhibit 5),

deposit-type contracts (Exhibit 7), and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with authorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S, Part 3, Section 1, Column 9 and 13 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 9, 10 and 12.

© 2014 National Association of Insurance Commissioners 74

ANNUAL STATEMENT INSTRUCTIONS – FRATERNAL

SCHEDULE S − PART 3 – SECTION 1

REINSURANCE CEDED LIFE INSURANCE, ANNUITIES, DEPOSIT FUNDS AND OTHER LIABILITIES WITHOUT LIFE OR DISABILITY CONTINGENCIES, AND RELATED BENEFITS LISTED BY REINSURING

COMPANY AS OF DECEMBER 31, CURRENT YEAR NOTE: This schedule is to include Exhibit 7 cessions. If a reporting entity has any detail lines reported for any of the following required groups, categories, or subcategories, it shall report the subtotal amount of the corresponding group, category, or subcategory, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 5 – Domiciliary Jurisdiction

Report the two-character U.S. postal code abbreviation for the domiciliary jurisdiction for U.S. states, territories and possessions. A comprehensive listing of three-character abbreviations for foreign countries is available in the appendix of these instructions. For abbreviations of foreign countries not found in the appendix, use the three-character abbreviations found at:

www.nationsonline.org/oneworld/countrycodes.htm

If a reinsurer has merged with another entity, report the domiciliary jurisdiction of the surviving entity.

Column 6 – Type of Reinsurance Ceded

Use the following abbreviations to identify the plan and type of reinsurance. For example, group coinsurance with funds withheld should be identified as COFW/G. (If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line.) NOTE: The type should be entered in all capital letters, and ALL reinsurance types must be followed by /G (for Group) or /I (for Individual).

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES CO Coinsurance ACO Annuity coinsurance

COFW Coinsurance with funds

withheld ACOFW Annuity coinsurance with

funds withheld

MCO Modified coinsurance

AMCO Annuity modified

coinsurance

© 2014 National Association of Insurance Commissioners 75

MCOFW Modified coinsurance with funds withheld

AMCOFW Annuity modified coinsurance with funds withheld

COMB Combination coinsurance/modified coinsurance

ACOMB Annuity combination coinsurance/modified coinsurance

COMBW Combination coinsurance/modified coinsurance with funds withheld

ACOMBW Annuity combination coinsurance/modified coinsurance with funds withheld

YRT Yearly renewable term

GMDB Guaranteed minimum

death benefit

CAT Catastrophe

GMDBFW Guaranteed minimum death benefit funds withheld

OTH Other reinsurance ADB Accidental death benefit DIS Disability benefits NOTE: The insurance type should be entered in all capital letters.

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

IL INDUSTRIAL LIFE FL FIXED ANNUITIES XXXL XXX LIFE IA INDEXED ANNUITIES AXXX AXXX LIFE VAAA VARIABLE GENERAL ACCOUNT

ANNUITIES CL CREDIT LIFE VSAA VARIABLE SEPARATE ACCOUNT

ANNUITIES SC SUPPLEMENTARY

CONTRACTS OA OTHER ANNUITIES

OL OTHER LIFE

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Analysis of Operations by Lines of Business and the Analysis of Annuity Operations by Lines of Business except as noted below:

XXX Life: Used to describe the actuarial reserves required to be held under Section 6

(exempting policies under 6.E, 6.F, or 6.G) of the NAIC Valuation of Life Insurance Policies Model Regulation (#830) which is commonly referred to as Regulation XXX (or, more simply, XXX).

AXXX Life: Used to describe the actuarial reserves required to be held under Section 7 of

Regulation XXX as further clarified by the NAIC Actuarial Guideline Guidance XXXVIII—The Application of the Valuation of Life Insurance Policies Model Regulation (AG 38), which is more commonly referred to as AXXX.

For year-end 2014 reporting only, those non-captive treaties that are not able to completely identify the type of business ceded can report wholly under "OL - Other Life". Detail reporting for type of business ceded will be required for year-end 2015 reporting.

© 2014 National Association of Insurance Commissioners 76

Column 78 – Amount in Force at End of Year

Report the ceded amount of the basic life insurance certificate only.

Total Line 2299999 should agree with Line 22 of the Exhibit of Life Insurance x 1000.

For catastrophe reinsurance (CAT), disability reinsurance (DIS), accidental death benefit reinsurance (ADB), and annuity reinsurance leave this column blank.

Column 89 – Reserve Credit Taken – Current Year

Amounts to agree with appropriate lines in Exhibit 5 and Exhibit 7. See examples for MODCO transactions contained in the general instructions for Schedule S.

Column 1011 – Premiums

Amounts included in this column should represent reinsurance ceded premiums on an incurred basis to agree with Line 20.3 of Exhibit 1, Part 1, Column 1 less Column 4.

For deposit funds and other liabilities without life or disability contingencies, leave this column blank.

Columns 11 12 & 1213 – Outstanding Surplus Relief

Outstanding surplus relief means the amount of surplus not yet reported as income on the “Commissions and expense allowance on reinsurance ceded” line, of the Summary of Operations, attributable to reinsurance agreements described in SSAP No. 61, Life, Deposit-Type and Accident and Health Reinsurance.

Report the amount of initial commissions and expense allowance not yet recovered by the reinsurer for the following types of treaties: CO, ACO, MCO, AMCO, COFW, ACOFW, MCOFW, AMCOFW, COMB, ACOMB, ACOMBW and COMBW. This column does not apply to CAT, DIS, ADB, YRT or other nonproportional reinsurance treaties.

Include: Outstanding surplus resulting from reinsurance of separate accounts business.

Column 1314 – Modified Coinsurance Reserve

Report the amount of reserves held under modified coinsurance contracts. Include separate accounts modified coinsurance reserves. The General Account total for Column 13 must agree with the parenthetical amount on Page 3, Line 1.

Column 1415 – Funds Withheld Under Coinsurance

Report the amount of funds withheld on coinsurance contracts.

© 2014 National Association of Insurance Commissioners 77

SCHEDULE S − PART 3 – SECTION 2

REINSURANCE CEDED ACCIDENT AND HEALTH INSURANCE LISTED BY REINSURING COMPANY AS OF DECEMBER 31, CURRENT YEAR

If a reporting entity has any detail lines reported for any of the following required groups, categories, or subcategories, it shall report the subtotal amount of the corresponding group, category, or subcategory, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 6 – Type

Use the following abbreviations to identify the plan and type of reinsurance. For example, group coinsurance with funds withheld should be identified as COFW/G. (If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line.) NOTE: The type should be entered in all capital letters, and ALL reinsurance types must be followed by /G (for Group) or /I (for Individual).

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES

CO Coinsurance

COFW Coinsurance with funds

withheld

MCO Modified coinsurance

MCOFW Modified coinsurance

with funds withheld

COMB Combination coinsurance/modified coinsurance

COMBW Combination coinsurance/modified coinsurance with funds withheld

YRT Yearly renewable term CAT Catastrophe LTC Long-Term Care OTH Other reinsurance NOTE: The insurance type should be entered in all capital letters.

© 2014 National Association of Insurance Commissioners 78

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

CMM COMPREHENSIVE MAJOR MEDICAL STM SHORT-TERM MEDICAL

OM OTHER MEDICAL (NON=COMPREHENSIVE)

LB LIMITED BENEFIT

SD SPECIFIED/NAMED DISEASE S STUDENT A ACCIDENT ONLY OR AD&D LTC LONG-TERM CARE STDI DISABILITY INCOME – SHORT-TERM D DENTAL LTDI DISABILITY INCOME – LONG-TERM MR MEDICARE MS MEDICARE SUPPLEMENT (MEDIGAP) MDMC MEDICAID MD MEDICARE PART D – STAND-ALONE TRI TRICARE FEHBP FEDERAL EMPLOYEES HEALTH BENEFIT

PLAN CAH CREDIT A&H

SCHIP STATE CHILDREN’S HEALTH INSURANCE PROGRAM

OH OTHER HEALTH

SLEL STOP LOSS/EXCESS LOSS

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Accident and Health Policy Experience Exhibit.

Column 78 – Premiums

Amounts included in this column should represent reinsurance ceded premiums on an incurred basis. Total Line 2299999 should agree with Exhibit 1, Part 1, Line 20.3, Column 4.

Column 89 – Unearned Premiums (Estimated)

Amounts represent, by company, the ceded part of the unearned premium reserve included in the Active Life Reserve in Exhibit 6, Line 7.

Column 910 – Reserve Credit Taken Other Than For Unearned Premiums

This column represents the reinsurance ceded portion of the remaining Active Life Reserve (excluding unearned premiums) and the Claim Reserve reported in Exhibit 6. The sum of the totals for Columns 8 and 9 must agree with the sum of the appropriate lines in Exhibit 6, (Line 7, Column 1 and Line 14, Column 1).

Columns 10 11 & 1112 – Outstanding Surplus Relief

Outstanding surplus relief means the amount of surplus not yet reported as income in Line 6, commissions and expense allowance on reinsurance ceded, of the Summary of Operations, attributable to reinsurance agreements described in SSAP No. 61, Life, Deposit-Type and Accident and Health Reinsurance.

Report the amount of initial commissions and expense allowance not yet recovered by the reinsurer for the following types of treaties: CO, MCO, COFW, MCOFW, COMB or COMBW. This column does not apply to YRT or other nonproportional reinsurance treaties.

Column 1213 – Modified Coinsurance Reserve

Report the amount of reserves held under modified coinsurance contracts. The sum of the total for Column 12 13 must agree with the parenthetical amount on Page 3, Line 2.

Column 1314 – Funds Withheld Under Coinsurance

Report the amount of funds withheld on coinsurance contracts.

© 2014 National Association of Insurance Commissioners 79

SCHEDULE S − PART 4

REINSURANCE CEDED TO UNAUTHORIZED COMPANIES

Detail Eliminated To Conserve Space

Column 5 – Reserve Credit Taken

Report the amount by which the aggregate reserve for Life certificates and contracts (Exhibit 5), deposit funds and other liabilities without life or disability contingencies (Exhibit 7), and Accident and Health certificates (Exhibit 6) has been reduced on account of reinsurance with unauthorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S – Part 3 Section 1, Column 8 9 and for Accident and Health reinsurance ceded in Schedule S – Part 3 Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

SCHEDULE S − PART 5

REINSURANCE CEDED TO CERTIFIED REINSURERS

Detail Eliminated To Conserve Space

Column 9 – Reserve Credit Taken

Report the amount by which the aggregate reserve for life contracts (Exhibit 5), deposit-type contracts (Exhibit 7) and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with certified reinsurers. The amounts by company should be the same as those shown for life reinsurance ceded in Schedule S, Part 3, Section 1, Column 8 9 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

© 2014 National Association of Insurance Commissioners 80

SCHEDULE S − PART 6

FIVE-YEAR EXHIBIT OF REINSURANCE CEDED BUSINESS A. Operations Items:

Line 1 – Premiums and Annuity Considerations for Life and Accident and Health Contracts

Exhibit 1, Part 1, Line 20.3.

Detail Eliminated To Conserve Space

Line 7 – Increase in Aggregate Reserves for Life and Accident and Health Contracts

Schedule S, Part 3, Section 2, Column 8 9

(+) Schedule S, Part 3, Section 2, Column 910, Current Year.

(–) Schedule S, Part 3, Section 2, Column 8, Prior Year,

(–) Schedule S, Part 3, Section 2, Column 9, Prior Year,

(–) Prior year (from prior year’s statement),

(+) Schedule S, Part 3, Section 1, Column 89,

(–) Schedule S, Part 3, Section 1, Column 910,

(–) Reinsurance ceded portion of Exhibit 5A, Lines 0199999 and 0299999, Column 4. B. Balance Sheet Items:

Line 8 – Premiums and Annuity Considerations for Life and Accident and Health Contracts Deferred and Uncollected

Exhibit 1, Part 1, Lines 3.3 plus 13.3.

Line 9 – Aggregate Reserves for Life and Accident and Health Contracts

Exhibit 5, life Insurance and Annuities, Lines 0199998 and 0299998, Column 2

(+) Exhibit 5, Lines 0399998, 0499998, 0599998, 0699998 and 0799998, Column 2,

(+) Exhibit 6, Line 7, Column 1,

(+) Exhibit 6, Line 14, Column 1.

OR

Schedule S, Part 3 Section 2, Column 89

(+) Schedule S, Part 3, Section 2, Column 910,

(+) Schedule S, Part 3 Section 1, Column 89.

Line 11 – Contract Claims Unpaid

Exhibit 8, Part 1, Line 4.3.

Detail Eliminated To Conserve Space

© 2014 National Association of Insurance Commissioners 81

PART 2 – FRATERNAL INTERROGATORIES

Detail Eliminated To Conserve Space

25.1 Disclose the amount of reserves carried by the reporting entity because it has sold annuities with a claimant as payee

and to the extent to which the reporting entity is liable for such amounts. Include only annuities for which the property and casualty insurer obtained a release of liability from the claimant as a result of the purchase of an annuity from the reporting entity.

25.2 Disclose the name and location of the insurance company (i.e., legal entity and not group) that purchased the

annuities during the current year and the aggregate statement value of annuities purchased, to the extent that the aggregate value of those annuities equals or exceeds $250,000. Include only annuities for which the property and casualty insurer obtained a release of liability from the claimant as a result of the purchase of an annuity from the reporting entity.

27.2 If there are multiple liens, they should be listed individually. 28.2 If the response to 28.1 is “YES”, provide for the captive affiliate the company name, NAIC company code,

domiciliary jurisdiction, reserve credit amount and the amounts supporting the reserve credit (letters of credit, trust agreements and other).

Reserve Credit: Report the amount by which the aggregate reserve for life contracts (Exhibit 5),

deposit-type contracts (Exhibit 7), and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with authorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S, Part 3, Section 1, Column 9 and 13 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 9, 10 and 12.

© 2014 National Association of Insurance Commissioners 82

ANNUAL STATEMENT INSTRUCTIONS – HEALTH

SCHEDULE S – PART 3 – SECTION 2

REINSURANCE CEDED ACCIDENT AND HEALTH INSURANCE LISTED BY REINSURING COMPANY AS OF DECEMBER 31, CURRENT YEAR

Include actual reinsurance ceded on group cases but exclude jointly underwritten group contracts. If a reporting entity has any detail lines reported for any of the following required groups, categories, or sub-categories it shall report the subtotal amount of the corresponding group, category, or sub-category, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 6 – Type

Use the following abbreviations to identify the plan and type of reinsurance. If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line. Note: The type should be entered in all capital letters, and ALL reinsurance types must be followed by /G (for Group) or /I (for Individual). For example, group specific stop loss for hospital only should be identified as SSL/L/G.

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES L Hospital Only ASL Aggregate Stop Loss A All Medical Combined SSL Specific Stop Loss QA Quota Share LRSL Loss Ratio Stop Loss SS Surplus Share LTC Long-Term Care OTH Other Reinsurance NOTE: The insurance type should be entered in all capital letters.

© 2014 National Association of Insurance Commissioners 83

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

CMM COMPREHENSIVE MAJOR MEDICAL STM SHORT-TERM MEDICAL

OM OTHER MEDICAL (NON=COMPREHENSIVE)

LB LIMITED BENEFIT

SD SPECIFIED/NAMED DISEASE S STUDENT A ACCIDENT ONLY OR AD&D LTC LONG-TERM CARE STDI DISABILITY INCOME – SHORT-TERM D DENTAL LTDI DISABILITY INCOME – LONG-TERM MR MEDICARE MS MEDICARE SUPPLEMENT (MEDIGAP) MDMC MEDICAID MD MEDICARE PART D – STAND-ALONE TRI TRICARE FEHBP FEDERAL EMPLOYEES HEALTH BENEFIT

PLAN CAH CREDIT A&H

SCHIP STATE CHILDREN’S HEALTH INSURANCE PROGRAM

OH OTHER HEALTH

SLEL STOP LOSS/EXCESS LOSS

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Accident and Health Policy Experience Exhibit.

Column 78 – Premiums

This represents reinsurance premiums ceded to the companies assuming risk and agrees with the Underwriting and Investment Exhibit, Part 1, Column 3, Line 9.

Column 89 – Unearned Premiums (Estimated)

This represents the portion of the unearned premium reserve that is transferred to the company assuming the risk.

Column 910 – Reserve Credit Taken Other Than For Unearned Premiums

This column represents the reinsurance ceded portion of the claim reserve. Columns 1011 and 1112 – Outstanding Surplus Relief

Not Applicable. Column 1213 – Modified Coinsurance Reserve

Not Applicable. Column 1314 – Funds Withheld Under Coinsurance

Not Applicable.

© 2014 National Association of Insurance Commissioners 84

SCHEDULE S – PART 4

REINSURANCE CEDED TO UNAUTHORIZED COMPANIES

Detail Eliminated To Conserve Space

Column 5 – Reserve Credit Taken

Report the amount by which the aggregate reserve for life contracts (Exhibit 5 – life supplement), deposit-type contracts (Exhibit 7 – life supplement), and accident and health contracts (Underwriting and Investment Exhibit, Part 2D) has been reduced on account of reinsurance with unauthorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S – Part 3 Section 1, Column 8 9 and for accident and health reinsurance ceded in Schedule S – Part 3 Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

SCHEDULE S − PART 5

REINSURANCE CEDED TO CERTIFIED REINSURERS

Detail Eliminated To Conserve Space

Column 9 – Reserve Credit Taken

Report the amount by which the aggregate reserve for life contracts (Exhibit 5 – life supplement), deposit-type contracts (Exhibit 7 – life supplement) and accident and health contracts (Underwriting and Investment Exhibit, Part 2D) has been reduced on account of reinsurance with certified reinsurers. The amounts by company should be the same as those shown for life reinsurance ceded in Schedule S, Part 3, Section 1, Column 8 9 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 8 9 and 910.

Detail Eliminated To Conserve Space

© 2014 National Association of Insurance Commissioners 85

ANNUAL STATEMENT INSTRUCTIONS – HEALTH (LIFE SUPPLEMENT)

SCHEDULE S − PART 3 − SECTION 1 REINSURANCE CEDED LIFE INSURANCE, ANNUITIES, DEPOSIT FUNDS AND OTHER LIABILITIES WITHOUT LIFE OR DISABILITY CONTINGENCIES, AND RELATED BENEFITS LISTED BY REINSURING COMPANY AS OF

DECEMBER 31, CURRENT YEAR To be filed on or before March 1. NOTE: This schedule is to include Exhibit 7 (life supplement) cessions. Include actual reinsurance ceded on group cases but

exclude jointly underwritten group contracts. If a reporting entity has any detail lines reported for any of the following required groups, categories, or subcategories, it shall report the subtotal amount of the corresponding group, category, or subcategory, with the specified subtotal line number appearing in the same manner and location as the pre-printed total line and number: The information included in this schedule shall be broken down to the level of detail as required when all columns and rows are considered together. Therefore, to the extent that multiple products or lines of business are ceded under a single transaction, the reporting entity is required to breakdown the information regarding the single contract into the various lines of business required by this schedule.

Detail Eliminated To Conserve Space

Column 5 – Domiciliary Jurisdiction

Report the two-character U.S. postal code abbreviation for the domiciliary jurisdiction for U.S. states, territories and possessions. A comprehensive listing of three-character abbreviations for foreign countries is available in the appendix of these instructions. For abbreviations of foreign countries not found in the appendix, use the three-character abbreviations found at:

www.nationsonline.org/oneworld/countrycodes.htm

If a reinsurer has merged with another entity, report the domiciliary jurisdiction of the surviving entity.

Column 6 – Type of Reinsurance Ceded

Use the following abbreviations to identify the plan and type of reinsurance. For example, group coinsurance with funds withheld should be identified as COFW/G. (If there is more than one type of reinsurance in the same reinsurance company, show each type on a separate line.)

Abbreviations:

I Individual { All Reinsurance Types should be

followed by /I or /G.

G Group REINSURANCE TYPES CO Coinsurance ACO Annuity coinsurance

COFW Coinsurance with funds

withheld ACOFW Annuity coinsurance with

funds withheld

MCO Modified coinsurance

AMCO Annuity modified

coinsurance

© 2014 National Association of Insurance Commissioners 86

MCOFW Modified coinsurance with funds withheld

AMCOFW Annuity modified coinsurance with funds withheld

COMB Combination coinsurance/modified coinsurance

ACOMB Annuity combination coinsurance/modified coinsurance

COMBW Combination coinsurance/modified coinsurance with funds withheld

ACOMBW Annuity combination coinsurance/modified coinsurance with funds withheld

YRT Yearly renewable term

GMDB Guaranteed minimum

death benefit

CAT Catastrophe

GMDBFW Guaranteed minimum death benefit funds withheld

OTH Other reinsurance ADB Accidental death benefit DIS Disability benefits NOTE: The insurance type should be entered in all capital letters.

Column 7 – Type of Business Ceded

Use the following codes to identify the type of business ceded. If there is more than one type of business ceded to the same reinsurance company, show each type.Enter one of the following for Type of Business Ceded

IL INDUSTRIAL LIFE FL FIXED ANNUITIES XXXL XXX LIFE IA INDEXED ANNUITIES AXXX AXXX LIFE VAAA VARIABLE GENERAL ACCOUNT

ANNUITIES CL CREDIT LIFE VSAA VARIABLE SEPARATE ACCOUNT

ANNUITIES SC SUPPLEMENTARY

CONTRACTS OA OTHER ANNUITIES

OL OTHER LIFE

NOTE: The Type of Business Ceded code should be entered in all capital letters.

All types of business shown above are as reported in the Analysis of Operations by Lines of Business and the Analysis of Annuity Operations by Lines of Business except as noted below:

XXX Life: Used to describe the actuarial reserves required to be held under Section 6

(exempting policies under 6.E, 6.F, or 6.G) of the NAIC Valuation of Life Insurance Policies Model Regulation (#830) which is commonly referred to as Regulation XXX (or, more simply, XXX).

AXXX Life: Used to describe the actuarial reserves required to be held under Section 7 of

Regulation XXX as further clarified by the NAIC Actuarial Guideline Guidance XXXVIII—The Application of the Valuation of Life Insurance Policies Model Regulation (AG 38), which is more commonly referred to as AXXX.

For year-end 2014 reporting only, those non-captive treaties that are not able to completely identify the type of business ceded can report wholly under "OL - Other Life". Detail reporting for type of business ceded will be required for year-end 2015 reporting.

© 2014 National Association of Insurance Commissioners 87

Column 78 – Amount in Force at End of Year

Report the ceded amount of the basic life insurance policy only.

For catastrophe-reinsurance (CAT), disability reinsurance (DIS), accidental death benefit reinsurance (ADB) and annuity reinsurance (ACO and AMCO), leave this Column blank.

Column 89 – Reserve Credit Taken Current Year

To agree with appropriate lines in Exhibit 5 (life supplement) and Exhibit 7 (life supplement). See examples for modco transactions contained in the general instructions for Schedule S.

Column 1011 – Premiums

Amounts included in this Column should represent reinsurance ceded premiums on an incurred basis, to agree with Line 10 of Underwriting and Investment Exhibit, Part 1, Column 3.

For deposit funds and other liabilities without life or disability contingencies, leave this Column blank.

Columns 11 12 & 1213 – Outstanding Surplus Relief

Outstanding surplus relief means the amount of surplus not yet reported as income in Commissions and Expense Allowance on Reinsurance Ceded, attributable to reinsurance agreements described in SSAP No. 61, Life, Deposit-Type and Accident and Health Reinsurance.

Report the amount of initial commissions and expense allowance not yet recovered by the reinsurer for the following types of treaties (individual or group): CO, ACO, MCO, AMCO, COFW, ACOFW, MCOFW, AMCOFW, COMB or ACOMB. This Column does not apply to CAT, DIS, ADB, YRT or other non-proportional reinsurance treaties.

Include the outstanding surplus resulting from reinsurance of separate accounts business.

Column 1314 – Modified Coinsurance Reserve

Report the amount of reserves held under modified coinsurance contracts. Include separate accounts modified coinsurance reserves.

Column 1415 – Funds Withheld Under Coinsurance

Report the amount of funds withheld on coinsurance contracts.

© 2014 National Association of Insurance Commissioners 88

ANNUAL STATEMENT INSTRUCTIONS – HEALTH

PART 2 – HEALTH INTERROGATORIES

Detail Eliminated To Conserve Space

11. If the Plans’ minimum net worth requirement is based upon a contingency reserve for Minimum Net Worth that is

other than a flat dollar amount, the calculation must be shown. An example of the disclosure of a calculation based upon 2% of the net capitation revenue from risk contracts is:

Net earned subscription revenue $ 33,103,906 2% Addition to Reserve 662,078 Reserve Balance Beginning of Year 353,689 Reserve Balance End of Year 1,025,767

Item 11.4 should equal Column 1, Line 3 of the Five Year History Page.

14.2 If the response to 14.1 is “YES”, provide for the captive affiliate the company name, NAIC company code,

domiciliary jurisdiction, reserve credit amount and the amounts supporting the reserve credit (letters of credit, trust agreements and other).

Reserve Credit: Report the amount by which the aggregate reserve for life contracts (Exhibit 5),

deposit-type contracts (Exhibit 7), and accident and health contracts (Exhibit 6) has been reduced on account of reinsurance with authorized companies. The amounts by company should be the same as those shown for Life reinsurance ceded in Schedule S, Part 3, Section 1, Column 9 and 13 and for accident and health reinsurance ceded in Schedule S, Part 3, Section 2, Columns 9, 10 and 12.

© 2

014

Nat

iona

l Ass

ocia

tion

of I

nsur

ance

Com

mis

sion

ers

89

AN

NU

AL

ST

AT

EM

EN

T B

LA

NK

– L

IFE

, HE

AL

TH

(L

IFE

SU

PP

LE

ME

NT

) A

ND

FR

AT

ER

NA

L

S

CH

ED

UL

E S

– P

AR

T 3

– S

EC

TIO

N 1

R

eins

uran

ce C

eded

Lif

e In

sura

nce,

Ann

uiti

es, D

epos

it F

unds

and

Oth

er L

iabi

liti

es

Wit

hout

Lif

e or

Dis

abil

ity

Con

ting

enci

es, a

nd R

elat

ed B

enef

its

Lis

ted

by R

eins

urin

g C

ompa

ny a

s of

Dec

embe

r 31

, Cur

rent

Yea

r

1 N

AIC

C

ompa

ny C

ode

2 ID

Num

ber

3 E

ffec

tive

D

ate

4 N

ame

of C

ompa

ny

5 D

omic

ilia

ry

Juri

sdic

tion

6 T

ype

of

Rei

nsur

ance

C

eded

7 78

R

eser

ve C

redi

t Tak

en

1011

O

utst

andi

ng S

urpl

us R

elie

f 13

14

Mod

ifie

d C

oins

uran

ce

Res

erve

1415

Fu

nds

Wit

hhel

d U

nder

C

oins

uran

ce

T

ype

of B

usin

ess

Ced

ed

A

mou

nt in

For

ce

at E

nd o

f Y

ear

89

Cur

rent

Yea

r

910

Pri

or Y

ear

P

rem

ium

s

1112

Cur

rent

Yea

r

1213

Pri

or Y

ear

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

......

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

.....

......

......

......

..

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

......

......

......

. ...

......

......

....

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

..

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

......

......

......

......

......

......

... ..

......

......

......

......

......

......

......

......

......

......

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

..

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

.....

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

......

......

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

..

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

.....

......

......

...

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

......

......

......

..

.....

......

......

...

.....

......

......

...