murray & roberts retirement fund … statistics as at 31 december 2011 may 2012 pensioner...

TRANSCRIPT

May 2012May 2012

MURRAY & ROBERTSMURRAY & ROBERTSRETIREMENT FUNDRETIREMENT FUND

Pensioner Pensioner RoadshowRoadshowPensioner Pensioner RoadshowRoadshow20122012

Globalising Murray & Roberts

A G E N D AA G E N D A May 2012May 2012

Welcome and Introduction GM

Pensioner Statistics

S li t F t AMC Salient Features AMC

Murray & Roberts Retirement Fund - Overview

Pension Review

General

Ex Gratia GM Ex Gratia GM

Medical Aid update KJ

Globalising Murray & Roberts

Market OverviewMay 2012May 2012

Market Overview US d fi i US deficits

Can Southern European nations pay their debts?

Shaky position of US’s consumer

Direction of interest rates

Vacillations in various currencies

Iran – nuclear capabilities

Syria – revolution

Will US emerge from “recession”g

Will Fed provide further stimulants

Globalising Murray & Roberts

MURRAY & ROBERTS PENSIONERSMay 2012May 2012

STATISTICAL OVERVIEW - PRINCIPAL MEMBERS

AGE NEAREST BIRTHDAY NUMBER OF PENSIONERS ANNUAL PENSION

PENSIONERS R’000

Up to 52 6 268

53 – 62 26 3 624

63 – 72 367 33 484

73 – 82 722 42 134

83 – 87 216 13 754

88 – and older 119 6 996

TOTAL 1 456 100 260

Globalising Murray & Roberts

MURRAY & ROBERTS PENSIONERS STATISTICAL OVERVIEW - SPOUSES May 2012May 2012

AND CHILDREN PENSIONERSAGE NEAREST BIRTHDAY NUMBER OF PENSIONERS ANNUAL PENSION R’000

SPOUSES

Up to 52 86 4 612

53 – 62 220 12 170

63 – 72 369 21 338

73 – 82 508 33 894

83 – 87 158 10 852

88 and older 85 6 232

SUB TOTAL 1 426 89 098

DEFERRED PENSIONERS 14 857

CHILDREN 170 3 925

Globalising Murray & RobertsTOTAL 1 610 93 880

MURRAY & ROBERTS PENSIONERSMay 2012May 2012

ADDITIONAL STATISTICS

Currently 137 pensioners between 88 – 91 yearsCurrently 137 pensioners between 88 – 91 years

57 between 92 – 95 years

8 between 96 – 99 years

2 1002 over 100 years

Globalising Murray & Roberts

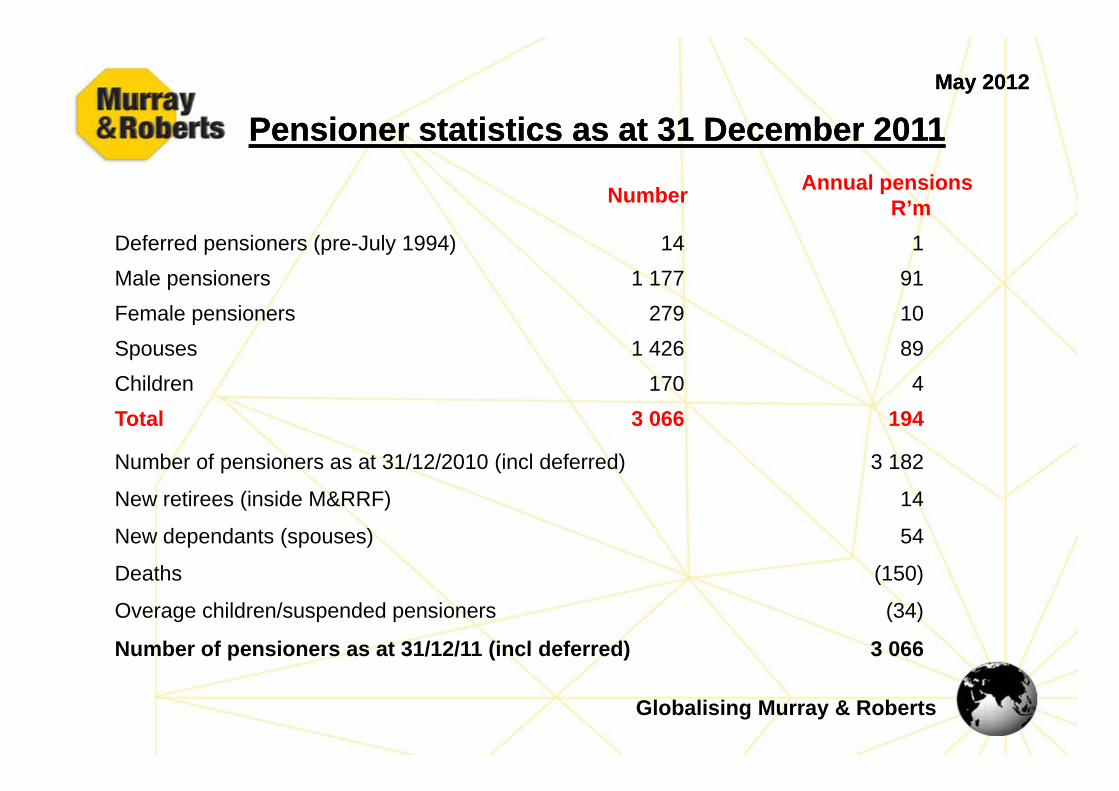

Pensioner statistics as at 31 December 2011Pensioner statistics as at 31 December 2011May 2012May 2012

Pensioner statistics as at 31 December 2011Pensioner statistics as at 31 December 2011

Number Annual pensionsR’m

Deferred pensioners (pre-July 1994) 14 1Male pensioners 1 177 91F l i 279 10Female pensioners 279 10Spouses 1 426 89Children 170 4Total 3 066 194

Number of pensioners as at 31/12/2010 (incl deferred) 3 182

New retirees (inside M&RRF) 14

New dependants (spouses) 54

Deaths (150)Deaths (150)

Overage children/suspended pensioners (34)

Number of pensioners as at 31/12/11 (incl deferred) 3 066

Globalising Murray & Roberts

May 2012May 2012

Globalising Murray & Roberts

Salient Features of 2011Salient Features of 2011May 2012May 2012

South African All Share Index (ALSI) up 2,6%

Salient Features of 2011Salient Features of 2011

SA All Bond Index (ALBI) up by 8,8%

MSCI ( l b l iti ) i d 15 9% i R d t d d 5% MSCI (global equities) index up 15,9% in Rand terms and down 5%measured in US Dollar terms

Rand in US dollar terms depreciated by 22%

Net Return : Pensioner Portfolio : 8,5%,

Y-o-Y CPI as at 31/12/11 : 6,1%

Pension Increase with effect from 1 March 2012 : 4,6%

Fund in a sound financial positionGlobalising Murray & Roberts

Fund in a sound financial position

TRUSTEES OF THETRUSTEES OF THEMay 2012May 2012

MURRAY & ROBERTS RETIREMENT FUNDMURRAY & ROBERTS RETIREMENT FUND

C L W k Ch iC L van Wyk Chairman

I G Appleton Appointed by Murray & Roberts

*R A G Skudder Appointed by Murray & Roberts

L J Lindsay Appointed by Murray & Roberts

D L Orton Elected by Pensioners

A M van der Colff Elected by Pensionersy

C Lerumo Elected by Members

T Wakefield Elected by MembersT Wakefield Elected by Members

*RAG Skudder replaced A Langham

Globalising Murray & RobertsTrustee Elections - 2012

Murray & Roberts Retirement FundMurray & Roberts Retirement Fund May 2012May 2012

StructureStructure

Investments as at 31/12/2011: Approximately R4 3 billionInvestments as at 31/12/2011: Approximately R4.3 billion

Mature fund3 066 Pensioners3 771 Employees3 771 Employees

Investment portfolios of employees and pensioners were split and ring-fenced effective from 1 January 2000.

Administrators: ABSA Consultants & Actuaries

Christina van der BreggenInvestment Consultants:

ggTowers Watson (formally Fifth Quadrant Actuaries and Consultants)

F d A t Jeanine SchubachFund Actuary: Jeanine SchubachNMG Consultants and Actuaries

Auditors: Deloitte & Touche

Globalising Murray & Roberts

Statement of Investment PrinciplesStatement of Investment PrinciplesMay 2012May 2012

Statement of Investment PrinciplesStatement of Investment PrinciplesThe Trustees have adopted a statement of investment e ustees a e adopted a state e t o est e tprinciples which includes the following-:

Asset Liability ModellingAsset Liability Modelling

Strategic Asset Allocation

Active Management of Asset Classes by 3rd party investment managers

Specialist MandatesSpecialist Mandates

Absolute Mandates

P f f I t t i ti l it dPerformance of Investment managers is continuously monitored and evaluated

Globalising Murray & Roberts

May 2012May 2012

PERFORMANCE OF INVESTMENT MANAGERS

Th t bl b l i th f i R d t f th i di id l

12 MONTH 12 MONTH 12 MONTH

The table below summarises the gross performance in Rand terms of the individual managers over the 12 months ended 31 December 2011

MANAGER12 MONTH

PERFORMANCE12 MONTH

BENCHMARK12 MONTH

ALPHASA Equity : Investec 3,1% 3,0% 0,1%SA Equity : Coronation 3 7% 3 0% 0 7%SA Equity : Coronation 3,7% 3,0% 0,7%SA Equity : Allan Gray 9,8% 3,0% 6,8%SA Equity : Domestic Absolute : RE:CM 3,1% 4,2% (1,1%)SA Bonds : Sanlam 9 7% 8 8% 0 9%SA Bonds : Sanlam 9,7% 8,8% 0,9%SA Bonds : Investec 8,9% 8,8% 0,1%SA Credit Income 8,5% 5,5% 3,0%International Equity : Brandes 14,6% 15,9% (1,3%)International Equity : Brandes 14,6% 15,9% (1,3%)International Equity : Orbis 12,5% 15,9% (3,4%)

Globalising Murray & Roberts

May 2012May 2012

PERFORMANCE OF INVESTMENT MANAGERSThe table below shows the annualised gross performance in Rand terms of the investment

managers over the 3-years period to 31 December 2011

MANAGER

3-YEARPERFORMANCE

(P.A.)

3-YEARBENCHMARK

(P.A.)

3-YEARALPHA(P.A.)

SA Equity : Investec 18,1% 17,7% 0,4%SA Equity : Coronation 21,1% 17,7% 3,3%SA Equity : Allan Gray 18,2% 17,7% 0,56%SA Equity : Domestic Absolute : RE:CM 16,6% 18,1% (1,5%)SA Bonds : Sanlam 8,4% 7,4% 1,0%SA Bonds : Investec 8,3% 7,4% 0,9%International Equity : Brandes 2 6% 6 8% (4 2%)International Equity : Brandes 2,6% 6,8% (4,2%)International Equity : Orbis 7,0% 6,8% 0,2%

Globalising Murray & Roberts

May 2012May 2012

INVESTMENT MANAGER PERFORMANCE FOR THE PERIOD SINCE APPOINTMENT TO 31 DECEMBER 2011

Allan Gray has been the best performer, out-performing the benchmark by 7.7% p.a.The only manager under-performing their benchmark over a period of longer than 3years since appointment is Brandes on the international equity front.

All performance numbers shown below are in Rand terms and annualised.

SA Equities SA Bonds International Equities

Manager Allan Gray Coronation Investec Sanlam Investec Brandes OrbisMeasurement period 11 years 11 years 11 years 11 years 9 years 107

months 56 months

Actual return 24,5% 18,7% 18,3% 12,1% 11,3% 4,2% 1,8%

Benchmark return 16,8% 15,8% 15,8% 11,4% 10,2% 7,0% (0,5%)

Alpha 7,7% 2,9% 2,5% 0,7% 1,1% (2,8%) 2,3%

Globalising Murray & Roberts

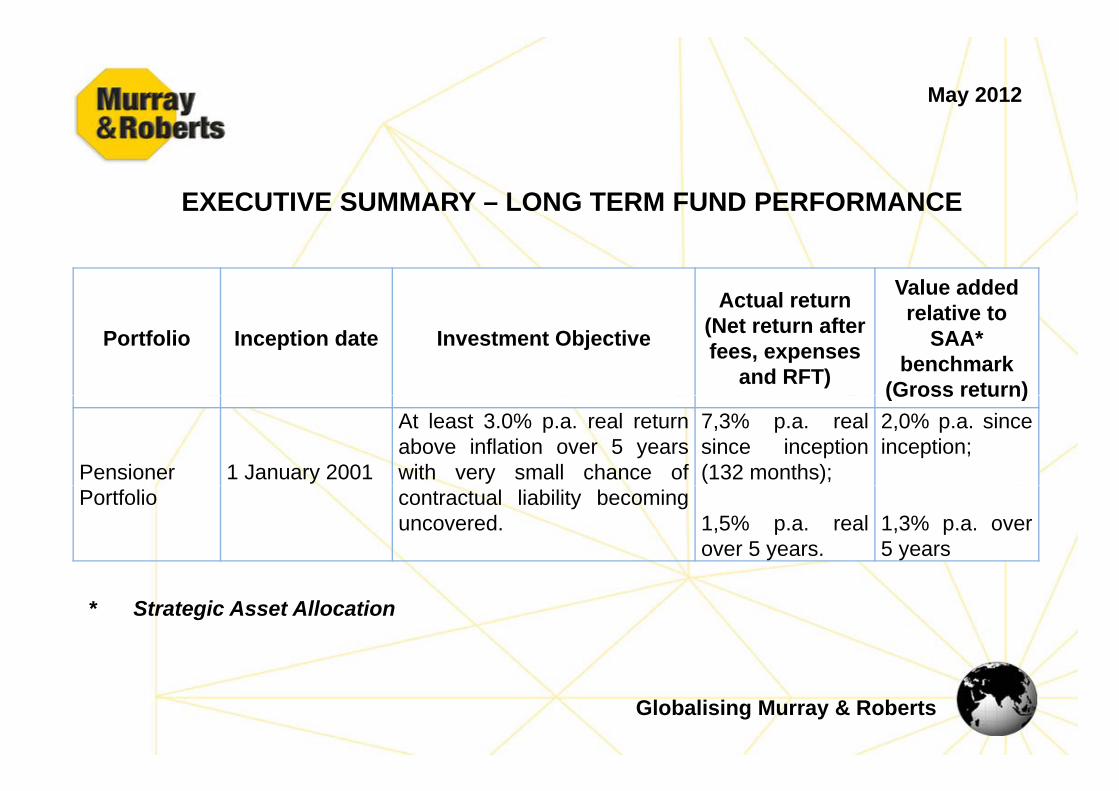

May 2012

EXECUTIVE SUMMARY – LONG TERM FUND PERFORMANCE

Actual return Value added l ti t

Portfolio Inception date Investment Objective

Actual return (Net return after fees, expenses

and RFT)

relative to SAA*

benchmark (Gross return)(Gross return)

Pensioner 1 January 2001

At least 3.0% p.a. real returnabove inflation over 5 yearswith very small chance of

7,3% p.a. realsince inception(132 months);

2,0% p.a. sinceinception;

Portfolio contractual liability becominguncovered. 1,5% p.a. real

over 5 years.1,3% p.a. over5 years

* Strategic Asset Allocation

Globalising Murray & Roberts

May 2012May 2012

260280300320

Cumulative Investment Portfolio Performance (net of fees)

160180200220240

80100120140

-04

-04

-04

-04

-04

-04

-05

-05

-05

-05

-05

-05

-06

-06

-06

-06

-06

-06

-07

-07

-07

-07

-07

-07

-08

-08

-08

-08

-08

-08

-09

-09

-09

-09

-09

-09

-10

-10

-10

-10

-10

-10

-11

-11

-11

-11

-11

-11

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Jan-

Mar

-M

ay-

Jul-

Sep

-N

ov-

Balanced Pensioner Capital Secure Money Market CPI

Graph shows the illustrative value on 31 December 2011 of R100 invested ineach of the Funds Portfolios on 1 January 2004 compared to inflation.

Globalising Murray & Roberts

Market Values at Market Values at 31/12/201131/12/2011((PensionerPensioner PortfolioPortfolio))

May 2012May 2012

((PensionerPensioner PortfolioPortfolio))Manager Asset class R’millions

Investec SA Equity 330Investec SA Equity 330Coronation SA Equity 334Allan Gray SA Equity 247*RE:CM SA Equity 99Investec Bonds & Cash 201Sanlam Bonds & Cash 259Investec Credit opportunity fund 70Investec Credit income fund 450Investec Credit income fund 450Investec Inflation linked bonds 238International Equity 392Cash Cash 15Total 2 635

* RE CM d t ithd i J 2012Globalising Murray & Roberts

* RE:CM mandate withdrawn in January 2012

Strategic Asset AllocationStrategic Asset Allocation ––May 2012May 2012

Strategic Asset Allocation Strategic Asset Allocation Pensioner Portfolio 31/12/2011Pensioner Portfolio 31/12/2011

PensionersSAA ACTUALSAA ACTUAL

SA Equity 20,0% 21,1%SA Nominal Bonds & Cash 34,5% 37,0%International Equity 14,0% 15,0%ySA Inflation Linked Bonds 11,5% 9,1%Absolute (Multi Class) 20 0% 17 8%Absolute (Multi Class) 20,0% 17,8%

Globalising Murray & Roberts

Market Indicators over last 3 yearsMarket Indicators over last 3 yearsMarket Indicators over last 3 yearsMarket Indicators over last 3 years

2009 2010 2011

R/$ -20,3% -10,2% 22,0%Global Equities ® 4,2% 0,9% 15,9%ALSI 32 1% 19 0% 2 6%ALSI 32,1% 19,0% 2,6%Global Bonds ® -18,8% -4,4% 30.8%SA Bonds -1,0% 15,0% 8,8%CPI 6,3% 3,5% 6,1%

Globalising Murray & Roberts

Murray & Roberts Retirement Fund Murray & Roberts Retirement Fund May 2012May 2012

Pensioner & Employee PortfolioPensioner & Employee Portfolio

31/12/2010 31/12/2011Total Fund Size R’000 R’000

Employees 1 297 108 1 640 853

Pensioner Liability 2 074 691 2 178 643

% of total fund 67% 67%

Pensioner Reserves ** 508 809508 809 452 251452 251

Funding LevelFunding Level 24,5%24,5% 20,8%20,8%

TotalTotal 3 880 6083 880 608 4 271 7474 271 747

* The Pensioner Reserves belong to the Pensioner Portfolio* The Pensioner Reserves belong to the Pensioner Portfolio

Globalising Murray & Roberts

Market Indicators 2012 (1Market Indicators 2012 (1stst QuarterQuarter))(( QQ ))

INDICATORS

R/$ -4,9%Global Equities® 6,2%ALSI 6,0%Global Bonds® -5,8%Global Bonds 5,8%ALBI 2,4%CPI 2,3%

2012 P i P tf li R t

January 2,04% 2,04%February 0,73% 2,80%

2012 Pensioner Portfolio ReturnsMONTHLY YTD

March 1,05% 3,90%April 0,93% 4,80%

Return 1st Quarter 3,9%

Globalising Murray & Roberts

PENSIONPENSION

REVIEWREVIEW

Globalising Murray & Roberts

FSB INTERPRETATION NOTE 1 OF 2012FSB INTERPRETATION NOTE 1 OF 2012

Board must establish and implement a pension increaseBoard must establish and implement a pension increasepolicy.

Fund’s pension increase policy must be communicated toFund s pension increase policy must be communicated topensioners.

C i ti t di l t i h t iCommunication must disclose to pensioners when certaincircumstances would result in Fund being unable toprovide increases in line with pension increase policy.provide increases in line with pension increase policy.

Valuator must use a market related valuation basis.

This is a change from the 3% PRI valuation basis used

Globalising Murray & Roberts

May 2012May 2012

PENSION INCREASE POLICYPENSION INCREASE POLICYRevised with effect 1 March 2005Revised with effect 1 March 2005

CURRENT POLICYCURRENT POLICY :

“The Trustees will consider the awarding of pensionincreases each year. The Trustees aim to award pensionincreases each year. The Trustees aim to award pensionincreases at a level of 75 % of the increase in the headlineconsumer price index over the financial year precedingthe pension increase date. When considering theawarding of any pension increase, the Trustees will belimited by affordability and guided by historical pastlimited by affordability and guided by historical pastpractice.”

Globalising Murray & Roberts

May 2012May 2012

PENSION INCREASE POLICYPENSION INCREASE POLICY

Every year the Trustees consider the following :-

Net Investment performance.

Long term government Bond yield and Inflation environment.

Are assets backing the pensioner liability sufficient for thepension increase.

Constraints of the Valuation Basis.

Required level of Reserves.

The recommendation by the Actuary

Globalising Murray & Roberts

May 2012May 2012

PENSION INCREASE POLICYPENSION INCREASE POLICY (cont)(cont)

Important :

If assets considered insufficient to provide for pensionsp pin payment, then the employer will be called upon tomake such contributions to the Fund as may be

i d id f f i h irequired to provide for payment of pensions at theirthen current levels.

In such an event no pension increases will be granted.

Globalising Murray & Roberts

VALUATION METHODOLOGY May 2012May 2012

Fund holds reserves as protection against possible future poor

investment experience.investment experience.

Previously recognised liabilities using a 3.00% PRI.

2010 Solvency Reserve level of 15,5%.

Market movements in long term real interest rates have meant thatMarket movements in long term real interest rates have meant that

more conservative assumptions are required.

The future inflation expectation has increased from 5,6% to 6,2%

Globalising Murray & Roberts

VALUATION METHODOLOGY(cont) May 2012May 2012

( )

Decrease in real interest rates has increased pensioner liabilities.

Solvency Reserve level has reduced to 5,9%, as a result of

i d li bilitiincreased liabilities.

Globalising Murray & Roberts

May 2012May 2012

VALUATION METHODOLOGY

Impact of Interpretation Note 1 of 2012

Valuation basis set according to Pension Increase Policy.

Funding level allows for expected increases of 75% of CPI going

forwardforward.31 December 2010 funding level 124.5%31 December 2011 funding level 120 8%31 December 2011 funding level 120.8%

Higher assets need to be held to cover the same expected future

iincrease.

Globalising Murray & Roberts

CPI CATCH UPMay 2012May 2012

CPI CATCH UP

Pension Funds Act requires Fund to calculate CPIincreases for all pensioners since retiringincreases for all pensioners since retiring.

At the time of Fund Statutory Valuation and subject toff d bilit i l i 100% f CPI t baffordability, any pensioner lagging 100% of CPI to be

adjusted.

CPI catch up completed for 86 pensioners at the end of2010

Process carried out every 3 years (statutory valuation) andentering first year of a three year cycle.

Globalising Murray & Roberts

May 2012May 2012

STRENGTHENING OF MORTALITY BASISSTRENGTHENING OF MORTALITY BASIS

At this stage the mortality basis will remain unchanged.g y g

The Actuary is satisfied the present mortality basisaddresses the improving longevity of pensioners.addresses the improving longevity of pensioners.

The actuary will continue to monitor the situation andmake adjustments when necessarymake adjustments when necessary.

Globalising Murray & Roberts

May 2012May 2012

PENSION INCREASEPENSION INCREASEPENSION INCREASEPENSION INCREASE

4,6% (w.e.f. 1/3/2012), ( )

CPI : 6,1%

P i I P li 75% f CPI (4 6%) Pension Increase Policy : 75% of CPI (4,6%)

Globalising Murray & Roberts

May 2012May 2012

PENSIONER RESERVING LEVELSPENSIONER RESERVING LEVELS

As at 31/12/11 :

Funding Level (Liability based on 75% ofFunding Level (Liability based on 75% ofCPI ) - 20,8%

Solvency Reserve (Liability based on 100%of CPI) - 5,9%

Considering current state of marketvolatility and uncertainty the Trusteesvolatility and uncertainty the Trusteesbelieve the Reserving levels areappropriate

Globalising Murray & Roberts

appropriate.

Pension Increases DeclaredPension Increases Declared May 2012May 2012

Period ended Pension 75% of (1)31 March 2012 Increases (p.a.) CPI

( )Year-on-Year CPI (p.a.)

1 year (p.a.) 4,6% 4,6% 6,1%

3 years (p.a) 7,0% 4,0% 5,3%

5 years (p.a.) 5,8% 5,1% 6,8%5 years (p.a.) 5,8% 5,1% 6,8%

10 years (p.a.) 5,3% 4,5% 5,9%

(1) “Year-on-Year” inflation rate is defined as the annual change in the CPIof the relevant month of the current year compared with the CPI of thesame month in the previous year expressed as a percentagesame month in the previous year, expressed as a percentage.

(2) NB : Please note the pension increase table above does not include the

Globalising Murray & Robertsspecial bonuses or once off payments.

MURRAY & ROBERTS RETIREMENT FUNDMURRAY & ROBERTS RETIREMENT FUND

May 2012May 2012

MURRAY & ROBERTS RETIREMENT FUNDMURRAY & ROBERTS RETIREMENT FUND

FUND RULESFUND RULES

Rule Amendments 5 & 7 were approved by the FSB in 2011.

In view of upcoming Trustee Elections a summary of Rule Amendment 7 is asIn view of upcoming Trustee Elections, a summary of Rule Amendment 7 is asfollows :-

RULE AMENDMENT NO.7

Makes allowance for voting for a single employee member trustee and pensioner elected trustee.

Allows for continuity amongst Trustees to provide that both the employeemember trustees or both the pensioner trustees do not vacate office at the same time and to also increase the period of office for trustees fromthree to four years.

Globalising Murray & Roberts

May 2012May 2012

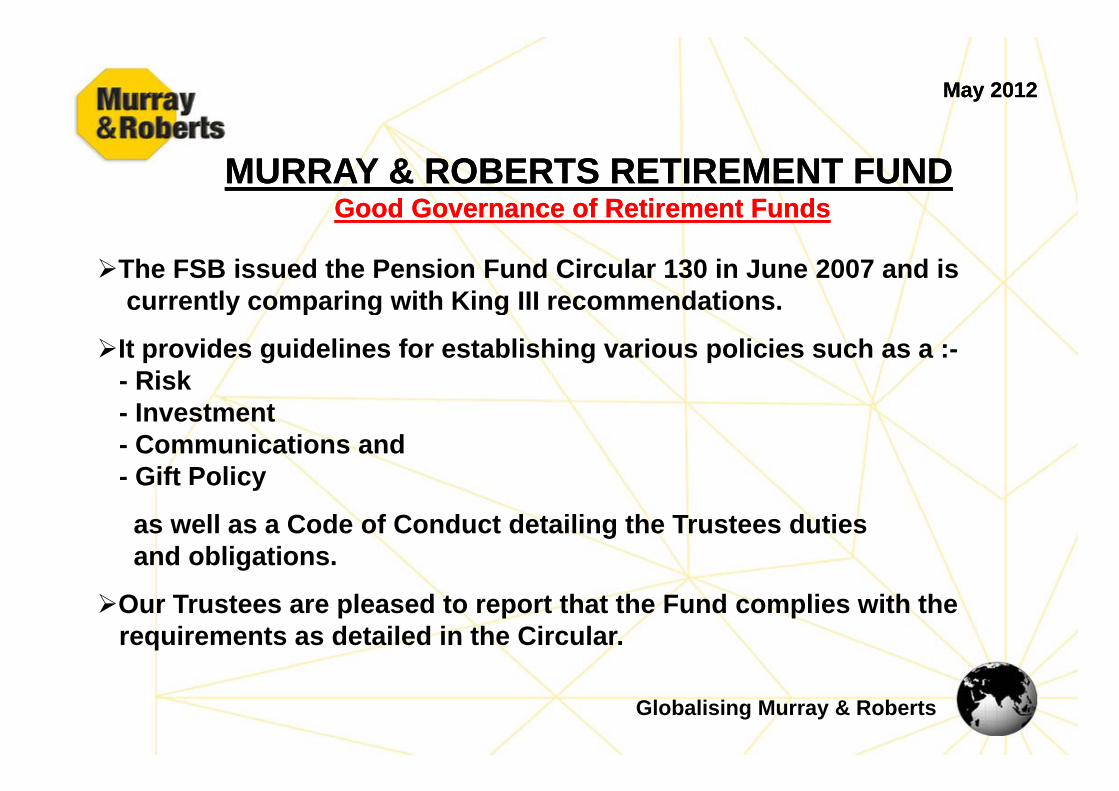

MURRAY & ROBERTS RETIREMENT FUNDMURRAY & ROBERTS RETIREMENT FUNDGood Governance of Retirement FundsGood Governance of Retirement FundsGood Governance of Retirement FundsGood Governance of Retirement Funds

The FSB issued the Pension Fund Circular 130 in June 2007 and iscurrently comparing with King III recommendationscurrently comparing with King III recommendations.

It provides guidelines for establishing various policies such as a :-- Risk- Investment- Communications and- Gift PolicyG t o cy

as well as a Code of Conduct detailing the Trustees dutiesand obligations.

Our Trustees are pleased to report that the Fund complies with therequirements as detailed in the Circular.

Globalising Murray & Roberts

May 2012May 2012

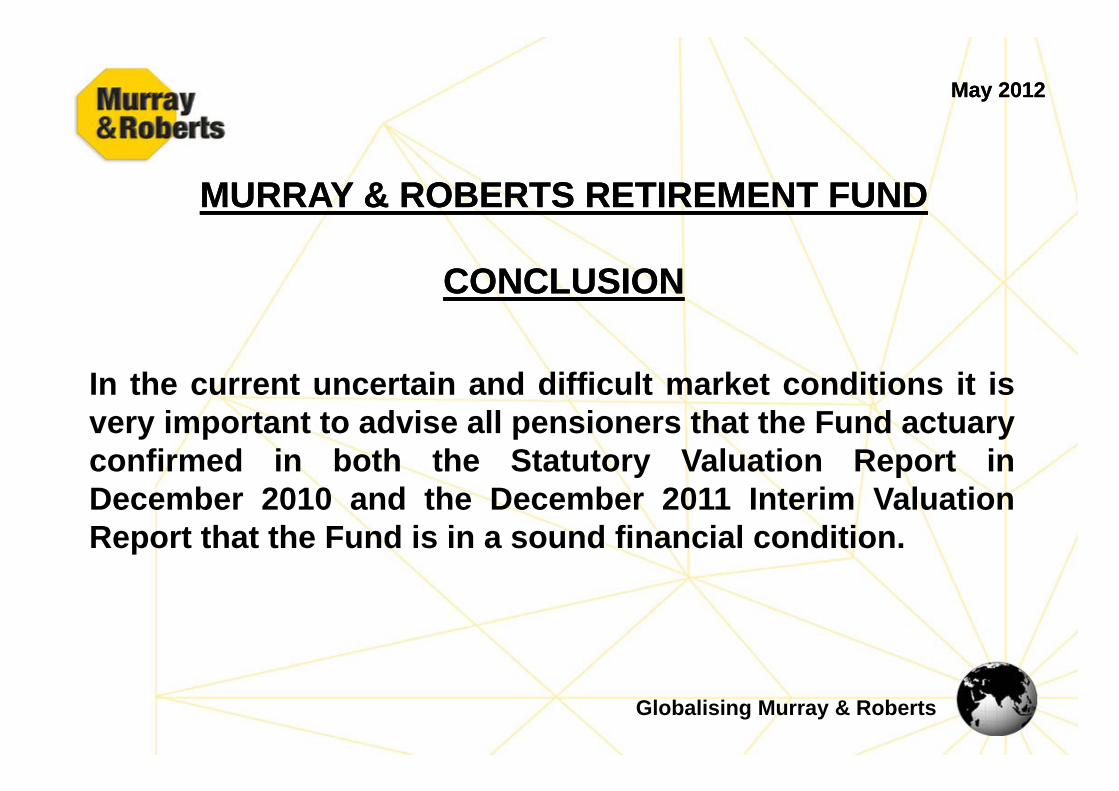

MURRAY & ROBERTS RETIREMENT FUNDMURRAY & ROBERTS RETIREMENT FUND

CONCLUSIONCONCLUSION

In the current uncertain and difficult market conditions it isvery important to advise all pensioners that the Fund actuaryconfirmed in both the Statutory Valuation Report inDecember 2010 and the December 2011 Interim ValuationReport that the Fund is in a sound financial condition.

Globalising Murray & Roberts

May 2012May 2012

GENERALGENERAL

Trustee Reports.

Benefit Statements.

Nomination of dependants form update Nomination of dependants form – update when circumstances change.

IRP 5’s

Website addressWebsite address www.pensioners.murrob.com

Globalising Murray & Roberts

May 2012May 2012

We make a living by what we get g y gbut we make a life by what we give

Winston Churchill

Globalising Murray & Roberts

QUESTIONSQUESTIONSQUESTIONSQUESTIONS

??

THANK YOU FOR LISTENINGTHANK YOU FOR LISTENING

Globalising Murray & Roberts

May 2012May 2012

EX GRATIAEX GRATIA

Discovery does not provide ex-gratia assistance.Discovery does not provide ex gratia assistance.

Exceptional life threatening cases would be lookedat by the Benefits Trust.

Th f Th B fit T tThe money for The Benefits Trust wasmade available by the D G Murray Trust andMurray & Roberts.

Globalising Murray & Roberts

EX GRATIA (Cont)EX GRATIA (Cont) May 2012May 2012EX GRATIA (Cont)EX GRATIA (Cont)

Written request should be submitted to E/Gcommitteecommittee.

Application forms available from Murray &Roberts,Group Benefits.

Li it d i t ld b i t itLimited assistance would be given to merit cases.

Funding secured for a five (5) year period.g ( ) y p

Globalising Murray & Roberts

South African economyM d t th

May 2012May 2012

Moderate growth South African GDP

GDP averages 2.5 - 3 per cent in 2012 and 3.5 per cent in 2013

Rand

Fair value estimated at USDZAR 8.40

CPI probably peaked at 6.3 per cent in Jan 2012 and is anticipated to gradually increaseincrease .

By end 2013 CPI inflation expected to slow

SARB repo ratep

The historic long-term real interest rate suggests SARBs repo rate should be 150bp-200bp higher

H i th i li ith t ti l d i fl ti th SARB ld However, given growth in line with potential and inflation the SARB could remain on hold through 2012

Globalising Murray & Roberts

May 2012May 2012

Moderate global growth expected in 2012

US economy, while not robust, has surprised on the upside of consensus– Continued jobs growth– Credit conditions have thawedCredit conditions have thawed

• Consumer and large business credit have recorded improvements

J ’ h i d f i h k l i 1H11 Japan’s economy has improved from its post-earthquake lows in 1H11

Also, China’s PMI manufacturing, while softer continues to point to industrial g pproduction growth– Monetary policy loosening on the back of slowing headline inflation is expected

to be supportive of China and EM generally, given exceptionspp g y, g p We expect the global economic recovery to continue into 2012 with emerging

market economies outperforming developed economies.– But growth seems likely to remain below trend

Globalising Murray & Roberts

– But, growth seems likely to remain below trend

Market OverviewMay 2012May 2012

Market Overview US d fi i US deficits

Can Southern European nations pay their debts?

Shaky position of US’s consumer

Direction of interest rates

Vacillations in various fiat currencies

Iran – nuclear capabilities

Syria – revolution

Will US emerge from “recession”g

Will Fed provide further stimulants

Globalising Murray & Roberts

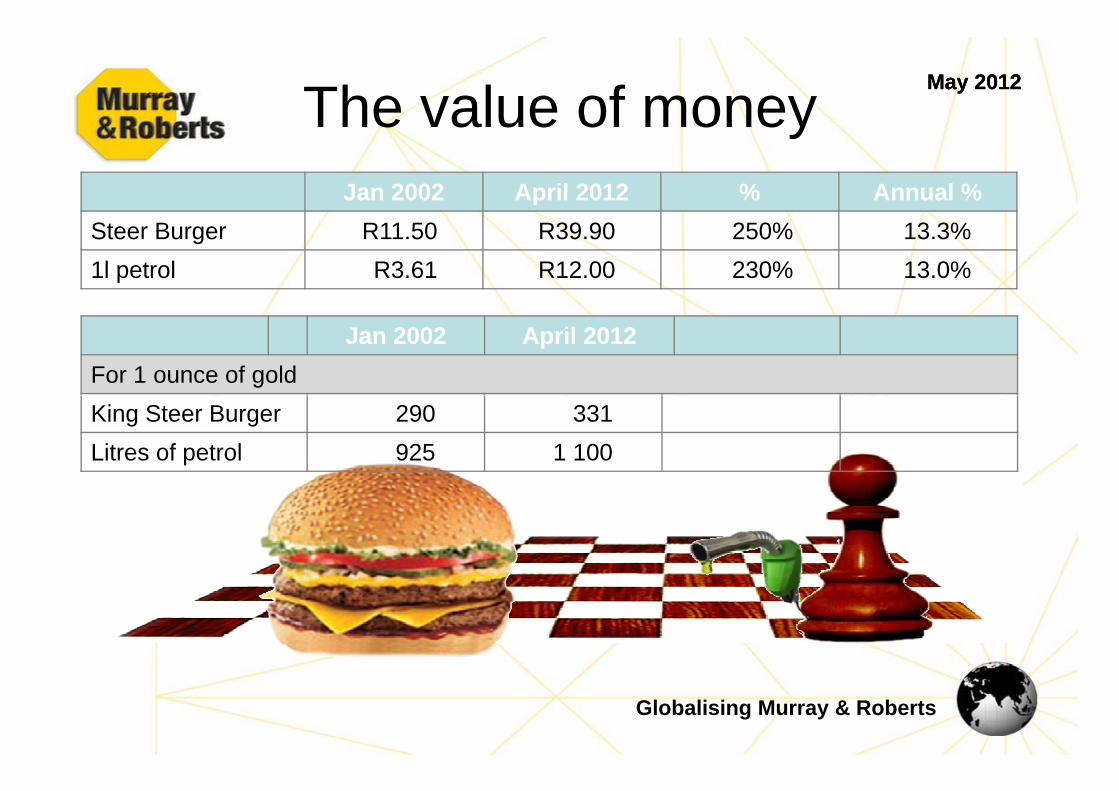

The value of money May 2012May 2012The value of moneyJan 2002 April 2012 % Annual %

Steer Burger R11.50 R39.90 250% 13.3%1l petrol R3.61 R12.00 230% 13.0%

Jan 2002 April 2012For 1 ounce of goldKing Steer Burger 290 331Litres of petrol 925 1 100

Globalising Murray & Roberts

May 2012May 2012

Moderate global growth expected in 2012

• US economy, while not robust, has surprised on the upside of consensus– Continued jobs growth– Credit conditions have thawedCredit conditions have thawed

• Consumer and large business credit have recorded improvements

J ’ h i d f i h k l i 1H11• Japan’s economy has improved from its post-earthquake lows in 1H11

• Also, China’s PMI manufacturing, while softer continues to point to industrial g pproduction growth– Monetary policy loosening on the back of slowing headline inflation is expected

to be supportive of China and EM generally, given exceptionspp g y, g p• We expect the global economic recovery to continue into 2012 with emerging

market economies outperforming developed economies.– But growth seems likely to remain below trend

Globalising Murray & Roberts

– But, growth seems likely to remain below trend

South African economyM d t th

May 2012May 2012

Moderate growth South African GDP

GDP averages 2.5 - 3 per cent in 2012 and 3.5 per cent in 2013

Rand

Fair value estimated at USDZAR 8.40

CPI probably peaked at 6.3 per cent in Jan 2012 and is anticipated to gradually increaseincrease .

By end 2013 CPI inflation expected to slow

SARB repo ratep

The historic long-term real interest rate suggests SARBs repo rate should be 150bp-200bp higher

H i th i li ith t ti l d i fl ti th SARB ld However, given growth in line with potential and inflation the SARB could remain on hold through 2012

Globalising Murray & Roberts

The value of money May 2012May 2012The value of moneyJan 2002 April 2012 % Annual %

Steer Burger R11.50 R39.90 250% 13.3%1l petrol R3.61 R12.00 230% 13.0%

Jan 2002 April 2012For 1 ounce of goldKing Steer Burger 290 331Litres of petrol 925 1 100

Globalising Murray & Roberts

Annual advance in CPIMay 2012May 2012

• Although the inflation data may be mixed in the next couple of months, it appears as though

– Core inflation still expected to drift higher

– Oil prices pose some near-term upside risk

– But, food price inflation likely to slow markedly into 2013

Currency stability should assist in slowing inflation into next year barring• Currency stability should assist in slowing inflation into next year – barring additional spikes in oil prices

Globalising Murray & Roberts