mreit q4 2015 fs - morguard home reit... · title: mreit q4 2015 fs created date: 20160210115

TRANSCRIPT

MORGUARD REAL ESTATEINVESTMENT TRUST

DECEMBER 31, 2015

CONSOLIDATEDFINANCIAL STATEMENTS

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 2

INDEPENDENT AUDITORS' REPORT

TO THE UNITHOLDERS OF MORGUARD REAL ESTATE INVESTMENT TRUST

We have audited the accompanying consolidated financial statements of Morguard Real Estate Investment Trust, which comprise the consolidated balance sheets as at December 31, 2015 and 2014, and the consolidated statement of income and comprehensive income, unitholders’ equity and cash flows for the years then ended and a summary of significant accounting policies and other explanatory information.

MANAGEMENTS' RESPONSIBILITY FOR THE CONSOLIDATED FINANCIAL STATEMENTS

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

AUDITOR'S RESPONSIBILITY

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

OPINION

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Morguard Real Estate Investment Trust as at December 31, 2015 and 2014, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards.

“Ernst & Young LLP”

Chartered Professional AccountantsLicensed Public AccountantsToronto, CanadaFebruary 17, 2016

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 3

BALANCE SHEETSIn thousands of Canadian dollars

As at December 31 Notes 2015 2014

ASSETSNon-current assetsReal estate properties 5 $2,847,398 $2,866,235Equity-accounted investments 6 32,509 30,770

2,879,907 2,897,005Current assetsAmounts receivable 12(b),(e) 13,011 42,635Prepaid expenses and other assets 955 1,054Cash and cash equivalents 26,282 12,612

40,248 56,301Real estate properties held for sale 20 — 63,190Total assets $2,920,155 $3,016,496

LIABILITIES AND UNITHOLDERS’ EQUITYNon-current liabilitiesMortgages payable 8 $1,082,799 $1,111,360Convertible debentures payable 9 147,698 146,541Other liabilities 3,517 4,111

1,234,014 1,262,012Current liabilitiesMortgages payable 8 89,536 71,096Accounts payable and accrued liabilities 12(a) 40,465 41,650Bank indebtedness 10 — 4,927

130,001 117,673Mortgages payable on real estate properties held for sale 20 — 29,730

Total liabilities 1,364,015 1,409,415Unitholders' equity 14 1,556,140 1,607,081

$2,920,155 $3,016,496Commitments and contingencies 17

See accompanying notes to the consolidated financial statements.

On behalf of the Trustees:

David King, Paul Cobb,Chairman of the Board of Trustees Trustee

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 4

STATEMENT OF INCOME AND COMPREHENSIVE INCOMEIn thousands of Canadian dollars, except per unit amounts

For the year ended December 31 Notes 2015 2014

Revenue from real estate properties $290,982 $298,461Property operating expenses 13(a) 115,646 119,139Property management fees 12(a) 9,406 9,583Net operating income 165,930 169,739

Interest expense 11 58,981 62,000General and administrative 13(b) 4,367 5,414Other income (571) (375)Income before fair value (losses)/gains, loss on sale of real estateproperties and net income/(loss) from equity-accounted investments 103,153 102,700

Fair value (losses)/gains on real estate properties 5 (78,977) 11,239Loss on sale of real estate properties — (37)Net income/(loss) from equity-accounted investments 6 2,441 (20)Net income for the year 26,617 113,882

OTHER COMPREHENSIVE INCOMEItems to be reclassified to profit or loss in subsequent periods:

Amortization – cash flow hedges 935 1,010Comprehensive income $27,552 $114,892

NET INCOME PER UNIT 14(d)Basic $0.43 $1.83Diluted (1) $0.43 $1.72

(1) The calculation of diluted net income per unit excludes the impact of the convertible debentures for the year ended December 31, 2015, as their inclusion would be anti-dilutive.

See accompanying notes to the consolidated financial statements.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 5

STATEMENT OF UNITHOLDERS' EQUITYIn thousands of Canadian dollars, except number of units

Numberof Units

Issueof Units

RetainedEarnings

Equity Component

of ConvertibleDebentures

ContributedSurplus

Accumulated Other

ComprehensiveLoss

TotalUnitholders’

Equity

Balance, at January 1, 2014 62,221,836 $625,824 $927,184 $1,526 $338 ($2,134) $1,552,738

Repurchase of units (100,000) (1,006) (667) — — — (1,673)

Debentures converted 609 15 — — — — 15

Net income for the year — — 113,882 — — — 113,882

Distributions to unitholders — — (58,891) — — — (58,891)

Issue of units – DRIP 45,209 791 (791) — — — —

Amortization – cash flow hedges — — — — — 1,010 1,010

Balance, at December 31, 2014 62,167,654 625,624 980,717 1,526 338 (1,124) 1,607,081

Repurchase of units (1,328,022) (13,368) (6,673) — — — (20,041)

Net income for the year — — 26,617 — — — 26,617

Distributions to unitholders — — (58,452) — — — (58,452)

Issue of units – DRIP 52,022 788 (788) — — — —

Amortization – cash flow hedges — — — — — 935 935

Balance, at December 31, 2015 60,891,654 $613,044 $941,421 $1,526 $338 ($189) $1,556,140

See accompanying notes to the consolidated financial statements.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 6

STATEMENT OF CASH FLOWIn thousands of Canadian dollars

For the year ended December 31 Notes 2015 2014

OPERATING ACTIVITIESNet income for the year $26,617 $113,882

Items not affecting operating cash 15(a) 76,678 (10,567)Distributions from equity-accounted investments 6 702 2,518Deferred leasing cost additions (3,586) (3,892)Tenant incentive additions (398) (114)Net change in non-cash operating assets and liabilities 15(b) (2,056) 2,790Cash provided by operating activities 97,957 104,617

FINANCING ACTIVITIESProceeds from new mortgages 56,155 269,177Repayment of principal

Repayments on maturity (36,925) (219,157)Repayment due to early extinguishment of mortgage (6,125) (13,747)Principal instalment repayments (35,644) (33,677)Amortization of fair value adjustments (10) (131)

Financing cost on new mortgages (278) (890)Decrease in bank indebtedness 10 (4,927) (73)Issue of loan payable 12(b) — 60,000Repayment of loan payable 12(b) — (60,000)Distributions to unitholders (58,452) (58,891)Units repurchased for cancellation (20,041) (1,673)Cash used in financing activities (106,247) (59,062)

INVESTING ACTIVITIESAcquisition of loan receivable 12(b) (36,000) (30,000)Settlement of loan receivable 12(b) 66,000 —Capital expenditures on real estate properties (42,327) (40,671)Acquisition of real estate properties (1,474) (16,354)Net proceeds from sale of real estate properties 15(b) 35,761 41,005Cash provided by/(used in) investing activities 21,960 (46,020)

Net change in cash and cash equivalents during the year 13,670 (465)Cash and cash equivalents, beginning of year 12,612 13,077Cash and cash equivalents, end of year $26,282 $12,612

See accompanying notes to the consolidated financial statements.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 7

NOTESFor the year ended December 31, 2015In thousands of Canadian dollars, except units, per unit amounts and where otherwise noted

NOTE 1NATURE AND DESCRIPTION OF THE TRUSTMorguard Real Estate Investment Trust (“the Trust”) is a “closed-end” real estate investment trust established on June 18, 1997, under the laws of the Province of Ontario. The Trust commenced active operations on October 14, 1997. The Trust owns a diverse portfolio of retail, office and industrial properties located in six Canadian provinces. The Trust’s head office is located at 55 City Centre Drive, Suite 1000, Mississauga, Ontario, L5B 1M3.

The Trust has a property management agreement with Morguard Investments Limited (“MIL”), a subsidiary of Morguard Corporation (“Morguard”). Morguard is the parent company of the Trust, owning 50.41% of the outstanding units, as at December 31, 2015. Morguard is a real estate company, which owns a diversified portfolio of multi-unit residential, retail, hotel, office and industrial properties. Morguard also provides advisory and management services to institutional and other investors.

NOTE 2STATEMENT OF COMPLIANCE AND SIGNIFICANT ACCOUNTING POLICIESThe consolidated financial statements of the Trust have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board.

The consolidated financial statements were approved and authorized for issue by the Board of Trustees on February 17, 2016.

Basis of PresentationThe Trust's consolidated financial statements are prepared on a going-concern basis and have been presented in Canadian dollars rounded to the nearest thousand unless otherwise indicated. The consolidated financial statements are prepared on a historical cost basis, except for real estate properties and certain financial instruments that are measured at fair value. The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements unless otherwise indicated.

Basis of ConsolidationThe consolidated financial statements include the financial statements of the Trust, as well as the entities that are controlled by the Trust ("subsidiaries"). The Trust controls an entity when the Trust is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully consolidated from the date of acquisition or the date on which the Trust obtains control and are deconsolidated from the date that control ceases. Inter-company transactions, balances, unrealized losses and unrealized gains on transactions between the Trust and its subsidiaries are eliminated.

Real Estate PropertiesIncome Producing PropertiesIncome producing properties include retail, office and industrial properties held to earn rental income and for capital appreciation.

Income producing properties, where not acquired in a business combination, are measured initially at cost including transaction costs. Transaction costs include transfer taxes and professional fees for legal and other services.

Subsequent to initial recognition, income producing properties are recorded at fair value, determined based on available market evidence, at the consolidated balance sheet date. The changes in fair value during each reporting period are recorded in the consolidated statements of income and comprehensive income. In order to avoid double counting, the carrying value of income producing properties includes straight-line rent receivable, tenant improvements, tenant incentives and direct leasing costs since these amounts are incorporated in the appraised values of real estate properties.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 8

Tenant improvements include costs incurred to meet the Trust’s lease obligations and are classified as either tenant improvements owned by the landlord or tenant incentives. When the obligation is determined to be an improvement that benefits the landlord and is owned by the landlord, the improvement is accounted for as a capital expenditure and included in the carrying amount of income producing properties on the consolidated balance sheets.

Tenant incentives are inducements given to prospective tenants to move into the Trust's properties or to existing tenants to extend the lease term. Tenant incentive receivables are included in the carrying value of real estate properties and are deducted from rental revenue on a straight-line basis over the term of the tenant’s lease.

Properties Under DevelopmentThe cost of properties under development includes all expenditures incurred in connection with the acquisition, including all direct development costs, realty taxes and other costs of the building to prepare it for its productive use, the applicable portion of general and administrative expenses and borrowing costs directly attributable to the development. Borrowing costs associated with direct expenditures on properties under development or redevelopment are capitalized. Borrowing costs are also capitalized on the purchase cost of a site or property acquired specifically for redevelopment in the short term if the activities necessary to prepare the asset for development or redevelopment are in progress. The amount of borrowing costs capitalized is determined by reference to interest incurred on debt specific to the development project. Borrowing costs are capitalized from the commencement of the development until the date of practical completion. The capitalization of borrowing costs is suspended if there are prolonged periods when development activity is interrupted. The Trust considers practical completion to have occurred when the property is capable of operating in the manner intended by management. Generally, this consideration occurs upon completion of construction and receipt of all necessary occupancy and other material permits. Where the Trust has pre-leased space as at, or prior to, the start of the development and the lease requires the Trust to construct tenant improvements that enhance the value of the property, practical completion is considered to occur on completion of such improvements.

Properties under development are measured at fair value with changes in fair value being recognized in the consolidated statements of income and comprehensive income.

Interests in Joint ArrangementsThe Trust views its interests in joint arrangements and those for which the Trust is entitled to only the net assets as joint ventures, which are accounted for using the equity method of accounting. Those joint arrangements in which the Trust is entitled to its share of the assets and liabilities are accounted for as joint operations, and the Trust recognizes its rights to and obligations for the assets, liabilities, revenue and expenses of the joint operation.

Cash and Cash EquivalentsCash and cash equivalents include cash on hand, balances with banks and short-term deposits with remaining maturities at the time of acquisition of three months or less. Bank borrowings are considered to be financing activities.

ProvisionsA provision is a liability of uncertain timing or amount. Provisions are recognized when the Trust has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation and the amount can be reliably estimated. Provisions are measured at the present value for the expenditures expected to be required to settle the obligation using a discount rate that reflects current market assessment of the time value of money and the risks specific to the obligation. Provisions are remeasured at each consolidated balance sheet date using the current discount rate. The increase in the provision due to passage of time is recognized as interest expense.

Revenue RecognitionThe Trust has retained substantially all of the risks and benefits of ownership of its real estate properties and, therefore, accounts for leases with its tenants as operating leases. Revenue from properties includes rents from tenants under leases, percentage participation rents, property tax and operating cost recoveries, lease cancellation fees, leasing concessions, parking income and incidental income. Percentage participation rents are accrued based on sales estimates submitted by tenants if the tenant anticipates attaining the minimum sales level stipulated in the tenant lease. All other rental revenue is recognized in accordance with each lease.

Revenue from real estate properties recorded in the consolidated statements of income and comprehensive income during free rent periods represents future cash receipts and is reflected in the consolidated balance sheets in the carrying value of real estate properties and recognized in the consolidated statements of income and comprehensive income on a straight-

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 9

line basis over the initial term of the lease. The Trust accounts for stepped rents on a straight-line basis, which are reflected in the consolidated balance sheets in the carrying value of real estate properties and recognized in the consolidated statements of income and comprehensive income over the initial term of the lease. Rents recorded in advance of cash received are included in amounts receivable.

Revenue from properties under development is recognized upon substantial completion of the development project andwhen the property is capable of operating in the manner intended by management, which generally occurs uponcompletion of construction and receipt of all necessary occupancy and other material permits.

Assets Held for SaleReal estate properties held for sale are assets that the Trust intends to sell rather than hold on a long-term basis and meet the criteria established in IFRS 5 for separate classification. Non-current assets and groups of assets and liabilities, that comprise disposal groups, are categorized as assets held for sale where the asset or disposal group is available for immediate sale in its present condition and the sale is highly probable.

Comprehensive IncomeComprehensive income is defined as the change in equity from transactions and other events from non-owner sources. Other comprehensive income ("OCI") refers to items recognized in comprehensive income that are excluded from net income. Accordingly, the Trust prepares consolidated statements of comprehensive income and includes accumulated other comprehensive income as a component of unitholders’ equity within the consolidated balance sheets.

Per Unit CalculationBasic net income per unit is calculated by dividing net income by the weighted average number of units outstanding for the year. The dilutive effect of the convertible debentures is determined by considering both the holders' option to convert these debentures into units and the issuer’s option to redeem these debentures by issuing units. The diluted net income per unit calculation considers both of these options and discloses the more dilutive of the two options.

Stock-Based CompensationMorguard has granted certain officers of the Trust stock appreciation rights (“SARs”), which entitle these officers to receive a cash payment equal to the excess of the market price of Morguard’s common shares at the time of exercise over the exercise price of the right. The SARs granted generally vest over 10 years. The Trust accounts for the SARs plan using the fair value method. Under this method, compensation expense for the SARs plan is measured at fair value at the grant date using the Black-Scholes option pricing model and recognized over the vesting period. The liability is measured at each reporting period at fair value with changes in fair value recorded in the consolidated statements of income and comprehensive income.

Financial InstrumentsRecognition and Measurement of Financial InstrumentsFinancial assets must be classified into one of the following categories: held to maturity, loans and receivables, fair value through profit or loss ("FVTPL") or available-for-sale assets. Financial liabilities, including FVTPL, are classified as other financial liabilities. All financial instruments, including derivatives, are measured in the consolidated balance sheets at fair value except for held-to-maturity loans and receivables and other financial liabilities that are measured at amortized cost using the effective interest rate method.

The Trust classifies its cash and cash equivalents and amounts receivable as loans and receivables, which are measured at amortized cost. Bank indebtedness, accounts payable and accrued liabilities and mortgages payable and convertible debentures are classified as other financial liabilities, which are measured at amortized cost.

Derivatives and Embedded DerivativesAll derivative instruments, including embedded derivatives, are recorded in the consolidated balance sheets at fair value unless exempted from derivative treatment as a normal purchase and sale. All changes in their fair value are recorded in income unless cash flow hedge accounting is used, in which case changes in fair value are recorded in OCI to the extent of hedge effectiveness. Financial guarantees are recorded at their inception date fair value and reversed as the Trust is relieved of its guarantee obligations.

HedgesDerivative financial instruments are utilized to reduce interest rate risk on the Trust’s debt. Interest rate swap agreements are used to manage the fixed and floating interest rate mix of the Trust’s total debt portfolio and related overall cost of

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 10

borrowing. Such instruments are designated, and are effective, as hedges of certain of the Trust’s interest rate risk exposures. The interest rate swap agreements involve the periodic exchange of payments without the exchange of the notional principal amount upon which the payments are based. The net receipt or payment of interest will be recorded as an adjustment to interest expense in each period.

Gains and losses on termination of interest rate swap agreements that were designated, and were effective, as hedges of certain interest rate risk exposures are included in accumulated other comprehensive income and are amortized in interest expense over the remaining term of the original contract life of the terminated swap agreement. Interest expense on the related debt obligation together with this amortization reflects the overall costs of such borrowing.

Transaction CostsDirect and indirect financing costs that are attributable to the issue of financial liabilities are presented as a reduction from the carrying amount of the related debt and are amortized using the effective interest rate method over the terms of the related debt. These costs include interest, amortization of discounts or premiums relating to borrowings, fees and commissions paid to lenders, agents, brokers and advisers, and transfer taxes and duties that are incurred in connection with the arrangement of borrowings.

Fair ValueThe fair value of a financial instrument is the consideration that could be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability takes place either (i) in the principal market for the asset or liability or (ii) in the absence of a principal market, in the most advantageous market for the asset or liability.

Fair value measurements recognized in the consolidated balance sheets are categorized using a fair value hierarchy that reflects the significance of inputs used in determining the fair values:

Level 1: Quoted prices in active markets for identical assets or liabilities.Level 2: Quoted prices in active markets for similar assets or liabilities or valuation techniques where significant inputs are

based on observable market data.Level 3: Valuation techniques for which any significant input is not based on observable market data.

Each type of fair value is categorized based on the lowest-level input that is significant to the fair value measurement in its entirety.

Critical Judgments in Applying Accounting PoliciesThe following are the critical judgments that have been made in applying the Trust’s accounting policies and that have the most significant effect on the amounts in the consolidated financial statements:

Real Estate PropertiesThe Trust’s accounting policies relating to real estate properties are described above. In applying these policies, judgment has been applied in determining whether certain costs are additions to the carrying amount of the property, in distinguishing between tenant incentives and tenant improvements and, for properties under development, identifying the point at which practical completion of the property occurs and identifying the directly attributable borrowing costs to be included in the carrying value of the development property. Judgment is also applied in determining the extent and frequency of independent appraisals. The key assumptions are further described in Note 5.

LeasesThe Trust makes judgments in determining whether certain leases, in particular those leases with long contractual terms where the lessee is the sole tenant in a property and long-term ground leases where the Trust is the lessee, are operating or finance leases. The Trust has determined that all of its tenant leases and long-term ground leases are operating leases.

Critical Accounting Estimates and AssumptionsThe preparation of the consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as at the date of the consolidated financial statements and reported amounts of revenue and expenses during the reporting periods. In determining estimates of fair market value for its real estate assets, the assumptions underlying estimated values are limited

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 11

by the availability of comparable data and the uncertainty of predictions concerning future events. Should the underlying assumptions change, actual results could differ from the estimated amounts. In addition, the computation of cost reimbursements from tenants for realty taxes, insurance and common area maintenance charges is complex and involves a number of estimates, including the interpretation of terms and other tenant lease provisions. Tenant leases are not consistent in dealing with such cost reimbursements, and variations in computations can exist. Adjustments are made throughout the year to these cost recovery revenues based upon the Trust’s best estimate of the final amounts to be billed and collected.

NOTE 3ADOPTION OF ACCOUNTING STANDARDS

IAS 40, “Investment Property” (“IAS 40”)On January 1, 2015, the Trust adopted an amendment with respect to the description of ancillary services in IAS 40, which differentiates between investment property and owner-occupied property (i.e., property, plant and equipment). The amendment is applied prospectively and clarifies that IFRS 3, Business Combinations, and not the description of ancillary services in IAS 40, is used to determine if the transaction is the purchase of an asset or a business combination. This amendment did not result in a material impact to the consolidated financial statements.

IFRS 8, “Operating Segments” (“IFRS 8”)On January 1, 2015, the Trust adopted the amendments to IFRS 8. The amendments are applied retrospectively and clarify that:

• An entity must disclose the judgments made by management in applying the aggregation criteria in paragraph 12 of IFRS 8, including a brief description of operating segments that have been aggregated and the economic characteristics (e.g., sales and gross margins) used to assess whether the segments are similar.

• The reconciliation of segment assets to total assets is required to be disclosed only if the reconciliation is reported to the chief operating decision-maker, similar to the required disclosure for segment liabilities.

These amendments did not result in a material impact to the consolidated financial statements.

NOTE 4FUTURE ACCOUNTING POLICY CHANGE

Amendments to IFRS 11, “Joint Arrangements” (“IFRS 11”): Accounting for Acquisitions of InterestsThe amendments to IFRS 11 require that a joint operator accounting for the acquisition of an interest in a joint operation, in which the activity of the joint operation constitutes a business, must apply the relevant IFRS 3 principles for business combinations accounting. The amendments also clarify that a previously held interest in a joint operation is not remeasured on the acquisition of an additional interest in the same joint operation while joint control is retained. In addition, a scope exclusion has been added to IFRS 11 to specify that the amendments do not apply when the parties sharing joint control, including the reporting entity, are under common control of the same ultimate controlling party.

The amendments apply to both the acquisition of the initial interest in a joint operation and the acquisition of any additional interests in the same joint operation and are prospectively effective for annual periods beginning on or after January 1, 2016, with early adoption permitted. These amendments are not expected to have any impact on the Trust.

Amendments to IAS 1, “Presentation of Financial Statements” (“IAS 1”): Disclosure InitiativeThe amendments to IAS 1 clarify rather than significantly change existing IAS 1 requirements. The amendments clarify:

• The materiality requirements in IAS 1;• That specific line items in the statement(s) of profit or loss and OCI and the statement of financial position may be

disaggregated;• That entities have flexibility as to the order in which they present the notes to financial statements; and• That the share of OCI of associates and joint ventures accounted for using the equity method must be presented in

aggregate as a single line item and classified between those items that will or will not be subsequently reclassified to profit or loss.

Furthermore, the amendments clarify the requirements that apply when additional subtotals are presented in the statement of financial position and the statement(s) of profit or loss and OCI. These amendments are effective for annual periods

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 12

beginning on or after January 1, 2016, with early adoption permitted. These amendments are not expected to have any impact on the Trust.

IFRS 15, “Revenue from Contracts with Customers” (“IFRS 15”)In May 2014, the IASB issued IFRS 15, a single comprehensive model to account for revenue arising from contracts with customers. The objective of IFRS 15 is to establish the principles that an entity shall apply to report useful information to users of financial statements about the nature, amount, timing and uncertainty of revenue and cash flows arising from a contract with a customer. The core principle of the standard is that an entity will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects consideration to which the entity expects to be entitled in exchange for those goods and services. The standard has a mandatory effective date for annual periods beginning on or after January 1, 2018, with earlier application permitted. The Trust is currently assessing the impact of IFRS 15 on its consolidated financial statements.

IFRS 9 (2014), “Financial Instruments” (“IFRS 9”)The final version of IFRS 9 was issued by the IASB in July 2014 and will replace IAS 39, “Financial Instruments: Recognition and Measurement” (“IAS 39”). IFRS 9 addresses the classification and measurement of all financial assets and liabilities within the scope of the current IAS 39 and a new expected loss impairment model that will require more timely recognition of expected credit losses and a substantially reformed model for hedge accounting. Included also are the requirements to measure debt-based financial assets at either amortized cost or fair value through profit or loss and to measure equity-based financial assets either as held for trading or as fair value through other comprehensive income ("FVTOCI"). No amounts are reclassified out of OCI if the FVTOCI option is elected. Additionally, embedded derivatives in financial assets would no longer be bifurcated and accounted for separately under IFRS 9. The standard has a mandatory effective date for annual periods beginning on or after January 1, 2018, with earlier application permitted. The Trust is currently assessing the impact of IFRS 9 on its consolidated financial statements.

IFRS 16, “Leases”In January 2016, the IASB issued IFRS 16, "Leases". The new standard requires that for most leases, lessees must initially recognize a lease liability for the obligation to make lease payments and a corresponding right-of-use asset for the right to use the underlying asset for the lease term. Lessor accounting, however, remains largely unchanged, and the distinction between operating and finance leases is retained. This standard will be effective for annual periods beginning after January 1, 2019, with early adoption permitted so long as IFRS 15 has been adopted. The Trust is currently assessing the impact this new standard will have on its consolidated financial statements.

NOTE 5REAL ESTATE PROPERTIESReal estate properties consist of the following:

As at December 31 2015 2014Income producing properties $2,816,124 $2,822,074Properties under development 2,524 16,511Land held for development 28,750 27,650

$2,847,398 $2,866,235

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 13

Reconciliations of the carrying amounts for real estate properties at the beginning and end of the current financial period are set out below:

As at December 31, 2015

IncomeProducingProperties

PropertiesUnder

Development

Land Held for

Development

Total Real Estate Properties

Balance as at December 31, 2014 $2,822,074 $16,511 $27,650 $2,866,235Additions:

Acquisitions and investments 1,474 — — 1,474Capital expenditures/capitalized costs 17,210 14,748 367 32,325Tenant improvements, tenant incentives and commissions 13,925 — — 13,925

Reclassifications 28,735 (28,735) — —Reclassification from properties held for sale 9,450 — — 9,450Fair value (losses)/gains (79,513) — 733 (78,780)Other changes 2,769 — — 2,769Balance as at December 31, 2015 $2,816,124 $2,524 $28,750 $2,847,398

As at December 31, 2014

IncomeProducingProperties

PropertiesUnder

Development

Land Held for

Development

Total Real Estate

PropertiesBalance as at December 31, 2013 $2,831,269 $20,839 $17,250 $2,869,358Additions:

Acquisitions and investments 23,935 — — 23,935Capital expenditures/capitalized costs 15,228 17,937 — 33,165Tenant improvements, tenant incentives and commissions 11,512 — — 11,512

Reclassifications (6,520) (3,610) 10,130 —Reclassification to properties held for sale (48,540) (14,650) — (63,190)Reclassification from equity-accounted investments 19,000 — — 19,000Disposition (41,042) — — (41,042)Fair value gains/(losses) 14,974 (4,005) 270 11,239Other changes 2,258 — — 2,258Balance as at December 31, 2014 $2,822,074 $16,511 $27,650 $2,866,235

Morguard Investments Limited (Note 12) provides appraisal services to the Trust. MIL’s valuation team consists of Appraisal Institute of Canada (“AIC”) designated Accredited Appraiser Canadian Institute (“AACI”) members who are qualified to offer valuation and consulting services and expertise for all types of real property, all of whom are knowledgeable and have recent experience in the fair value techniques for investment properties. AACI designated members must adhere to AIC’s Canadian Uniform Standards of Professional Appraisal Practice (CUSPAP) and undertake on-going professional development. Management reviews both the valuation processes and results at least once every quarter, in line with the Trust's quarterly reporting dates.

Generally, the Trust’s real estate properties are appraised using a number of approaches that typically include a discounted cash flow analysis, a direct capitalization approach and a direct comparison approach. The primary method of valuation used by the Trust is discounted cash flows. This approach involves determining the fair value of each income producing property based on, among other things, rental income from current leases and assumptions about rental income from future leases reflecting market conditions at the applicable consolidated balance sheet dates, less future cash outflows pertaining to the respective leases. Fair values are primarily determined by discounting the expected future cash flows, generally over a term of 10 years and including a terminal value based on the application of a capitalization rate to estimated year 11 net operating income.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 14

The table below provides further details of the average discount rate and terminal cap rate by business segments:

December 31, 2015 December 31, 2014

Maximum MinimumWeighted

Average Maximum MinimumWeightedAverage

RETAILDiscount rate 8.3% 6.0% 6.8% 8.5% 6.0% 6.8%Terminal cap rate 7.8% 5.3% 6.0% 7.8% 5.3% 6.0%Stabilized occupancy 100.0% 90.0% —% 100.0% 90.0% —%

OFFICEDiscount rate 8.0% 6.0% 6.7% 7.8% 6.0% 6.8%Terminal cap rate 7.5% 5.0% 5.9% 7.5% 5.3% 6.0%Stabilized occupancy 100.0% 94.3% —% 100.0% 94.3% —%

INDUSTRIALDiscount rate 7.5% 7.0% 7.2% 7.5% 7.0% 7.4%Terminal cap rate 7.0% 6.5% 6.8% 7.3% 6.5% 6.9%Stabilized occupancy 100.0% 95.0% —% 100.0% 95.0% —%

Using the direct capitalization income approach to corroborate the discounted cash flow method, the properties were valued using capitalization rates in the range of 5.0% to 7.5% applied to a stabilized net operating income (2014 – 5.0% to 7.5%), resulting in an overall weighted average capitalization rate of 5.8% (2014 – 5.8%). The total stabilized annual net operating income as at December 31, 2015, was $161,118 (2014 – $165,736). Values are most sensitive to changes in discount rates, capitalization rates and timing or variability of cash flow.

Excluded from the above analysis is a retail property located in British Columbia where the highest and best use is a redevelopment to mixed residential and commercial use. As at December 31, 2015, the value of the property is in the underlying land value with minimal holding income, and it has been valued using recent comparable land sales.

Fair values are most sensitive to changes in discount rates, capitalization rates and stabilized or forecasted net operating income. Generally an increase in net operating income will result in an increase in the fair value of the income producing properties, and an increase in capitalization rates will result in a decrease in the fair value of the properties. The capitalization rate magnifies the effect of a change in net operating income, with a lower capitalization rate resulting in a greater impact to the fair value of the property than a higher capitalization rate. If the weighted average stabilized capitalization rate were to increase or decrease by 25 basis points, the value of the income producing properties as at December 31, 2015, would decrease by $114,789 or increase by $125,131, respectively.

DispositionsThe following table provides details of dispositions completed by the Trust during the reporting period:

NetDate Property Sale Mortgage Operating

Property Name Sold Type GLA Price Payable Income20-24 Lesmill, ON May 15, 2015 Industrial 27,577 $6,350 $— $127

5591-5631 Finch, ON April 1, 2015 Industrial 210,123 $10,000 $6,125 $177

350 Sparks/361 Queen, ON February 17, 2015 Office/Hotel 86,372 $37,692 $17,835 $150

Cedar Pointe Business Park, ON July 2, 2014 Industrial 350,797 $41,900 $13,747 $1,218

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 15

AcquisitionsOn June 4, 2014, the Trust and a major Canadian pension fund each acquired a 50% interest in a 35,000 square foot office building located in Ottawa, Ontario, for a total purchase price of $4,037 plus other acquisition costs of $128. The Trust accounted for the purchase as an asset acquisition.

The allocation of the total cost for the Trust’s 50% acquisition is as follows:

Total acquisition costs:Purchase price – cash $4,037Transaction costs 128Total purchase price $4,165

On July 25, 2014, the Trust acquired the remaining 50% interest in a limited partnership that owns and operates a 78,000 square foot Class A office complex located in Calgary, Alberta, for a total purchase price of $19,000 plus other costs of $77. The Trust accounted for the purchase as a business combination.

The allocation of the total cost for the Trust’s acquisition is as follows:

Total acquisition costs:Purchase price – cash $11,549Purchase price – assumed working capital 7,451Other costs 77Total purchase price $19,077

NOTE 6EQUITY-ACCOUNTED INVESTMENTS On December 22, 2011, the Trust and a major Canadian pension fund each acquired a 50% interest in a limited partnership that owns and operates a 304,000 square foot Class A office complex located in downtown Edmonton, Alberta, in which the Trust has a total original net investment of $28,008. The Trust has joint control over the limited partnership and accounts for its investment using the equity method.

On December 22, 2011, the Trust and a major Canadian pension fund each acquired a 50% interest in a limited partnership that owns and operates a 78,000 square foot Class A office complex located in Calgary, Alberta, in which the Trust had a total original net investment of $8,666. The Trust had joint control over the limited partnership and accounted for its investment using the equity method. The Trust acquired the remaining 50% interest in this limited partnership on July 25, 2014, and consolidates its 100% interest.

As at December 31 2015 2014Balance, beginning of year $30,770 $44,857

Equity income/(loss) 2,441 (20)Distributions to partners (2,360) (2,518)Contributions from partners 1,658 —Reclassification adjustments on purchase:

Real estate properties — (19,000)Mortgages payable — 7,581Other working capital — (130)

Balance, end of year $32,509 $30,770

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 16

The following details the Trust’s share of the limited partnerships' aggregated assets, liabilities and results of operations accounted for under the equity method for the following periods:

As at December 31 2015 2014Real estate properties $61,950 $62,750Current assets 1,392 294Total assets $63,342 $63,044

Non-current liabilities $28,306 $29,225Current liabilities 2,527 3,049Total liabilities $30,833 $32,274

For the year ended December 31 2015 2014Revenue from real estate properties $6,561 $7,759Property operating expenses 2,172 2,613Net operating income 4,389 5,146

Other expenses (1,157) (1,330)Fair value losses on real estate properties (791) (3,836)Net income/(loss) for the year $2,441 ($20)

The real estate properties included above in the Trust's equity-accounted investments are appraised using a number of approaches that typically include a discounted cash flow analysis, a direct capitalization approach and a direct comparison approach. As at December 31, 2015, the property was valued using a discount rate of 7.0% (2014 – 7.0%), a terminal cap rate of 6.3% (2014 – 6.3%) and a stabilized cap rate of 7.0% (2014 – 6.8%). The stabilized annual net operating income as at December 31, 2015, was $4,337 (2014 – $4,236).

NOTE 7CO-OWNERSHIP INTERESTS The Trust is a co-owner in several properties, listed below, that are subject to joint control based on the Trust's decision-making authority with regards to the relevant activities of the properties. These co-ownerships have been classified as joint operations and, accordingly, the Trust recognizes its rights to and obligations for the assets, liabilities, revenue andexpenses of these co-ownerships in the respective lines in the consolidated financial statements.

Property Trust's Ownership ShareJointly-Controlled Operations Location Type 2015 2014505 Third Street Calgary, AB Office 50% 50%Scotia Place Edmonton, AB Office 20% 20%Prairie Mall Grande Prairie, AB Retail 50% 50%Heritage Place Ottawa, ON Office 50% 50%Standard Life Centre Ottawa, ON Office 50% 50%77 Bloor Toronto, ON Office 50% 50%Woodbridge Square Woodbridge, ON Retail 50% 50%825 Des Erables Salaberry-de-Valleyfield, QC Industrial 50% 50%Place Innovation St. Laurent, QC Office 50% 50%

Dispositions (see Notes 5 and 20)350 Sparks Ottawa, ON Office — 50%361 Queen Ottawa, ON Hotel — 50%

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 17

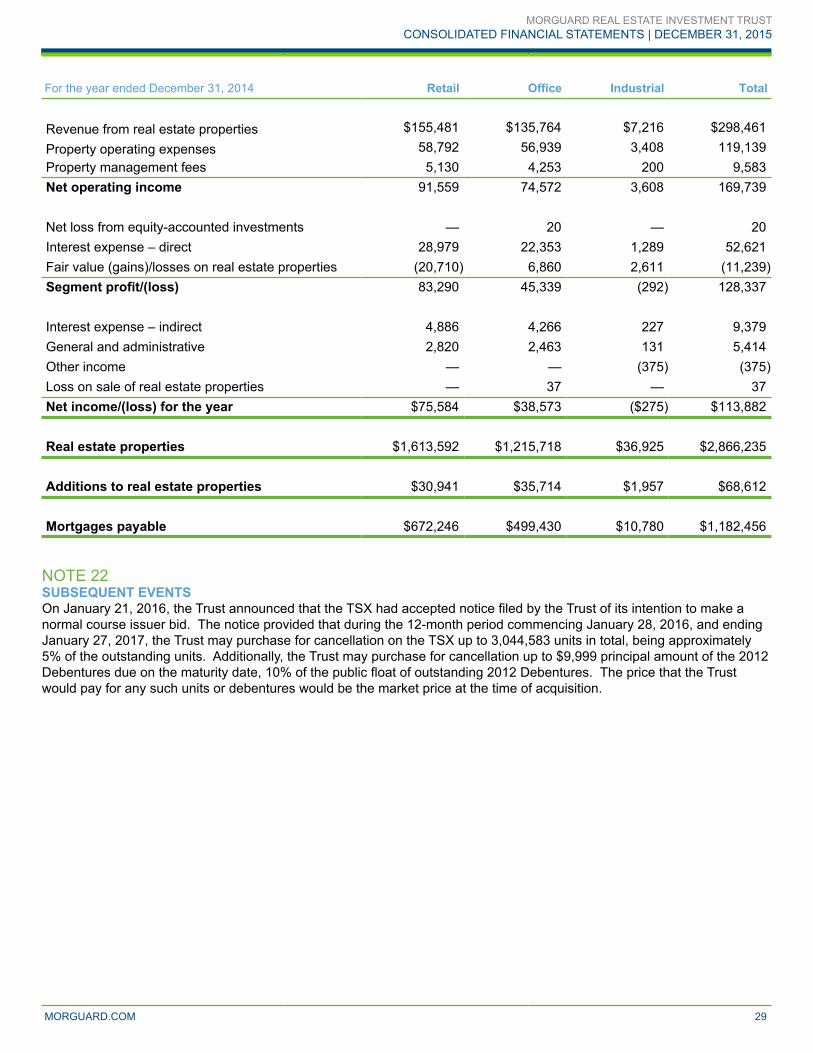

The following amounts, included in these consolidated financial statements, represent the Trust’s proportionate share of the assets and liabilities of the nine co-ownerships as at December 31, 2015, and the 11 co-ownerships as at December 31, 2014, and the results of operations for the years ended December 31, 2015, and 2014:

As at December 31 2015 2014Assets $490,910 $483,792Assets – properties held for sale — 38,531Liabilities 198,149 199,192Liabilities – properties held for sale — 18,803

For the year ended December 31 2015 2014Revenue $55,270 $57,151Expenses 34,223 35,924Income before fair value adjustments 21,047 21,227Fair value losses on real estate properties (3,749) (10,434)Net income for the year $17,298 $10,793

NOTE 8MORTGAGES PAYABLEMortgages payable consist of the following:

As at December 31 2015 2014Mortgages payable before deferred financing costs $1,175,880 $1,186,480Premium on acquired debt 1 11Deferred financing costs (3,546) (4,035)Mortgages payable $1,172,335 $1,182,456

Mortgages payable – non-current $1,082,799 $1,111,360Mortgages payable – current 89,536 71,096Mortgages payable $1,172,335 $1,182,456

The aggregate principal repayments and balances maturing on the mortgages payable as at December 31, 2015, together with the weighted average contractual rate on debt maturing in the year indicated, are as follows:

Principal Instalment

RepaymentsBalances Maturing Total

Weighted AverageContractual Rate on

Balance Maturing2016 $34,454 $55,786 $90,240 4.1%2017 34,121 50,289 84,410 4.5%2018 32,155 55,464 87,619 4.4%2019 26,724 162,122 188,846 3.6%2020 25,627 114,493 140,120 4.6%Thereafter 49,656 534,989 584,645 4.1%

$202,737 $973,143 $1,175,880 4.1%

Substantially all of the Trust’s rental properties and related rental revenues have been pledged as collateral for the mortgages payable.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 18

NOTE 9CONVERTIBLE DEBENTURES PAYABLE2012 Debentures On October 31, 2012, the Trust issued a $150,000 principal amount of 4.85% convertible unsecured subordinated Debentures (“2012 Debentures”) maturing on October 31, 2017 (the “Maturity Date”), of which a $50,000 principal amount was purchased by Morguard at the offering price.

Interest is payable semi-annually, not in advance, on April 30 and October 31 of each year, commencing on April 30, 2013.

The Trust’s convertible debentures, with the exception of the value assigned to the holders’ conversion option, have been recorded as debt on the consolidated balance sheets. The following table summarizes the allocation of the principal amount and related issue costs of the debentures at the date of original issue. The portion of issue costs attributable to the liability of $4,182 has been capitalized and will be amortized over the term to maturity, while the remaining amount of $46 has been charged to equity.

PrincipalAmount Issued Liability Equity

Transaction date – October 31, 2012 $150,000 $148,428 $1,572Issue costs (4,228) (4,182) (46)

$145,772 $144,246 $1,526

Each 2012 Debenture is convertible into freely tradable units of the Trust at the option of the holder, exercisable at any time prior to the close of business on the last business day preceding the maturity date at a conversion price of $24.60 (the “Conversion Price”) per unit being a rate of approximately 40.6504 units per thousand principal amount of 2012 Debentures, subject to adjustment.

As at December 31, 2015, $15 (2014 – $15) of the 2012 Debentures had been converted into 609 (2014 – 609) units. The liability and equity component of these debentures has been included in unitholders’ equity under issue of units.

As at December 31, 2015, the 2012 Debentures payable consist of the following:

As at December 31 2015 2014Convertible debentures payable – liability $148,428 $148,428Convertible debentures payable – accretion 946 630Debentures converted (15) (15)Convertible debentures payable before issue costs 149,359 149,043Issue costs (1,661) (2,502)Convertible debentures payable $147,698 $146,541

Interest and principal payments on the 2012 Debentures are as follows:

Interest Principal Total2016 $7,274 $— $7,2742017 7,274 149,985 157,259

$14,548 $149,985 $164,533

Redemption RightsEach 2012 Debenture is redeemable any time from November 1, 2015, to the close of business on October 31, 2016, in whole or in part, on at least 30 days' prior notice at a redemption price equal to par plus accrued and unpaid interest, at the Trust’s sole option provided that the weighted average trading price of the units on the Toronto Stock Exchange ("TSX") for the 20 consecutive trading days ending five trading days prior to the date on which the notice of redemption is given is not less than 125% of the conversion price.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 19

From November 1, 2016, to the close of business on October 31, 2017, the 2012 Debentures are redeemable, in whole or in part, at par plus accrued and unpaid interest, at the Trust’s sole option.

Repayment OptionsPayment Upon Redemption or MaturityThe Trust may satisfy its obligation to repay the principal amounts of the 2012 Debentures, in whole or in part, by delivering units of the Trust. In the event that the Trust elects to satisfy its obligation to repay principal with units of the Trust, the number of units issued is obtained by dividing the principal amount of the 2012 Debentures by 95% of the weighted average trading price of the units on the TSX for the 20 consecutive trading days ending five trading days prior to the date fixed for redemption or the maturity date, as applicable.

Interest Payment ElectionThe Trust may elect, subject to applicable regulatory approval, to issue and deliver units of the Trust to the Debenture Trustee in order to raise funds to pay interest on the 2012 Debentures, in which event the holders of the 2012 Debentures will be entitled to receive a cash payment equal to the interest payable from the proceeds of the sale of such units.

NOTE 10 BANK INDEBTEDNESS The Trust has credit facilities and operating lines of credit totalling $70,000 (2014 – $70,000), that renew annually and are secured by fixed charges on specific properties owned by the Trust.

As at December 31, 2015, the Trust had borrowed $nil (2014 – $4,927) and issued letters of credit in the amount of $286 (2014 – $290) related to these facilities.

The bank credit agreements include certain restrictive covenants and undertakings by the Trust. As at December 31, 2015, and 2014, the Trust was in compliance with all covenants and undertakings. As the bank indebtedness is current and at prevailing market rates, the carrying value of the debt as at December 31, 2015, approximates fair value.

NOTE 11INTEREST EXPENSEThe components of interest expense are as follows:

For the year ended December 31 2015 2014

Interest on mortgages payable $49,262 $51,178Amortization – deferred financing costs – mortgages 811 767Amortization – premium on acquired debt (10) (131)Interest on mortgages payable 50,063 51,814

Interest on convertible debentures payable 7,274 7,275Accretion on convertible debentures payable, net 316 299Amortization – deferred financing costs – convertible debentures 841 797Interest on convertible debentures payable 8,431 8,371

Interest on bank indebtedness 32 134

Amortization – cash flow hedges 935 1,010Interest on loan payable and other 155 878Capitalized interest (635) (207)Interest on loans payable and other 455 1,681

$58,981 $62,000

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 20

NOTE 12RELATED PARTY TRANSACTIONSWith the exception of Note 20, all related party transactions are summarized as follows:

(a) Agreement With Morguard Investments LimitedUnder the property management agreement, the Trust pays MIL fees for property management services, capital expenditure administration, information system support activities and risk management administration. Property management fees average approximately 3.3% of gross revenue from the income producing properties owned by the Trust. The management agreement is renewed annually to ensure fees paid reflect fair value for the services provided. Under a leasing services arrangement, the Trust may, at its option, use MIL for leasing services. Leasing fees range from 2% to 6% of the total minimum rent of new leases. Fees for the renewal of a lease are half of the fees for a new lease. Leasing services include lease documentation.

The Trust has employed the services of MIL for the acquisition of properties on a case-by-case basis. Fees are generally based on the acquisition price of the properties and are capitalized in the case of an asset acquisition. MIL is a tenant at three of the Trust’s properties. The Trust has employed the services of MIL for the appraisal of its real estate properties as required for IFRS reporting purposes. Fees are generally based on the size and complexity of each property and are expensed as part of the Trust’s professional and compliance fees.

During the year, the Trust incurred/(earned) the following:

For the year ended December 31 2015 2014Property management fees $9,522 $9,713Acquisition fees — 85Disposition fees 97 240Appraisal/valuation fees 370 388Information services 220 220Leasing fees 2,880 3,274Project administration fees 1,087 1,060Project management fees 491 596Risk management fees 282 283Internal audit fees 110 149Off-site administrative charges 1,761 1,837Rental revenue (230) (338)

$16,590 $17,507

The following amounts relating to MIL are included in the consolidated balance sheets:

December 31, December 31,

As at December 31 2015 2014Accounts payable and accrued liabilities, net $898 $1,149

(b) Revolving Loan With MorguardThe Trust has a revolving loan agreement with Morguard that provides for borrowings or advances of up to $50,000. The promissory notes are interest-bearing at the lender’s borrowing rate and are due on demand subject to available funds. On December 10, 2013, the revolving loan agreement was temporarily amended for a period of 60 days for either party to borrow up to $90,000 at the same interest rate terms. The temporary amendment expired on February 10, 2014.

Loan Payable to MorguardDuring the year ended December 31, 2015, there were no advances or repayments, and as at December 31, 2015 and 2014, there was no loan payable owing to Morguard. During the year ended December 31, 2015, the Trust did not incur interest expense on loans payable to Morguard (2014 – $764).

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 21

Loan Receivable From MorguardDuring the year ended December 31, 2015, a gross amount of $36,000 was advanced to Morguard, and $66,000 was repaid. As at December 31, 2015, the total amount receivable from Morguard was $nil (2014 – $30,000). For the year ended December 31, 2015, interest income amounted to $568 (2014 – $353), at an interest rate of 2.19% (2014 – 2.44%).

(c) Sublease With Morguard (Excluding MIL)The Trust subleases office space from Morguard. For the year ended December 31, 2015, the Trust incurred rent expense in the amount of $195 (2014 – $181). (d) Stock-Based Compensation With MorguardMorguard has granted certain officers of the Trust SARs, which entitle such officers to receive a cash payment equal to the excess of the market price of Morguard’s common shares at the time of exercise over the exercise price of the right. The SARs granted generally vest over 10 years. The fair values of these SARs are charged to the Trust by Morguard and are recorded as compensation expense by the Trust over their respective vesting periods. On March 20, 2008, 30,000 SARs were granted at an exercise price of $30.74. As at December 31, 2015, no further SARs have been granted.

As at December 31, 2015 and 2014, there were no SARs payable outstanding. For the year ended December 31, 2015, the compensation expense amounted to $nil (2014 – $397).

(e) Amounts Receivable From and Accounts Payable to Morguard (Excluding MIL)Other than the revolving loan, the following additional amounts relating to Morguard are included in the consolidated balance sheets:

As at December 31 2015 2014Amounts receivable $271 $—Accounts payable and accrued liabilities $4 $8

(f) Rental Revenue From Morguard (Excluding MIL)Morguard is a tenant in one of the Trust’s properties. For the year ended December 31, 2015, the Trust earned rental revenue in the amount of $109 (2014 – $104).

NOTE 13EXPENSES (a) Property Operating Expenses Property operating expenses consist of the following:

For the year ended December 31 2015 2014Property taxes $53,157 $52,813Repairs and maintenance 28,078 28,700Utilities 15,354 17,027Other operating expenses 19,057 20,599

$115,646 $119,139

(b) General and AdministrativeGeneral and administrative expenses consist of the following:

For the year ended December 31 2015 2014Trustees’ fees and expenses $268 $289Professional and compliance fees 1,518 1,716Other administrative expenses 2,581 3,409

$4,367 $5,414

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 22

NOTE 14UNITHOLDERS' EQUITY(a) Units OutstandingThe Trust is authorized to issue an unlimited number of units. The following table summarizes the changes in units for the period from January 1, 2014, to December 31, 2015:

As at December 31 2015 2014Balance, beginning of year 62,167,654 62,221,836Distribution Reinvestment Plan 52,022 45,209Debentures converted — 609Repurchase of units (1,328,022) (100,000)Balance, end of year 60,891,654 62,167,654

Total distributions recorded, accrued and paid during the year ended December 31, 2015, amounted to $58,452 (2014 – $58,891). On January 15, 2016, the Trust declared a distribution in the amount of $0.08 per unit for the month of January 2016. This distribution was paid to unitholders on February 16, 2016, prior to the date the consolidated financial statements were authorized for issue by the Board of Trustees of the Trust. On February 16, 2016, the Trust declared a distribution of $0.08 per unit payable on March 15, 2016.

(b) Normal Course Issuer BidsOn January 22, 2015, the Trust announced that the TSX had accepted notice filed by the Trust of its intention to make a normal course issuer bid. The notice provided that during the 12-month period commencing January 28, 2015, and ending January 27, 2016, the Trust may purchase for cancellation on the TSX up to 3,247,282 units in total, being approximately 10% of the public float of outstanding units. Additionally, the Trust may purchase for cancellation up to $9,999 principal amount of the 2012 Debentures due on the maturity date, 10% of the public float of outstanding 2012 Debentures. The price that the Trust would pay for any such units or debentures would be the market price at the time of acquisition.

During the year ended December 31, 2015, the Trust purchased for cancellation 1,328,022 units (2014 –100,000 units) for cash consideration of $20,041 (2014 – $1,673). The excess of the purchase price of the units over the average carrying value was $6,673 (2014 – $667).

(c) Distribution Reinvestment PlanUnder the Trust’s Distribution Reinvestment Plan (the “DRIP”), unitholders can elect to reinvest cash distributions into additional units at a weighted average trading price of the units on the TSX for the 20 trading days immediately preceding the applicable date of distribution. During the year ended December 31, 2015, the Trust issued 52,022 units under the DRIP (2014 – 45,209 units).

(d) Net Income Per UnitThe following table sets forth the computation of basic and diluted net income per unit:

For the year ended December 31 2015 2014

Net income – basic $26,617 $113,882Net income – diluted $26,617 $122,253

Weighted average number of units outstanding – basic 61,779 62,168Weighted average number of units outstanding – diluted 61,779 71,093

Net income per unit – basic $0.43 $1.83Net income per unit – diluted $0.43 $1.72

To calculate net income for the calculation of diluted income per unit, interest, accretion and the amortization of financing costs on convertible debentures outstanding that were expensed during the year are added back to net income. The calculation of diluted net income per unit excludes the impact of the convertible debentures for the year ended December 31, 2015, as their inclusion would be anti-dilutive. The weighted average number of units outstanding for the

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 23

calculation of diluted income per unit is calculated as if all convertible debentures outstanding as at December 31, 2014, had been converted into units of the Trust at the beginning of the period.

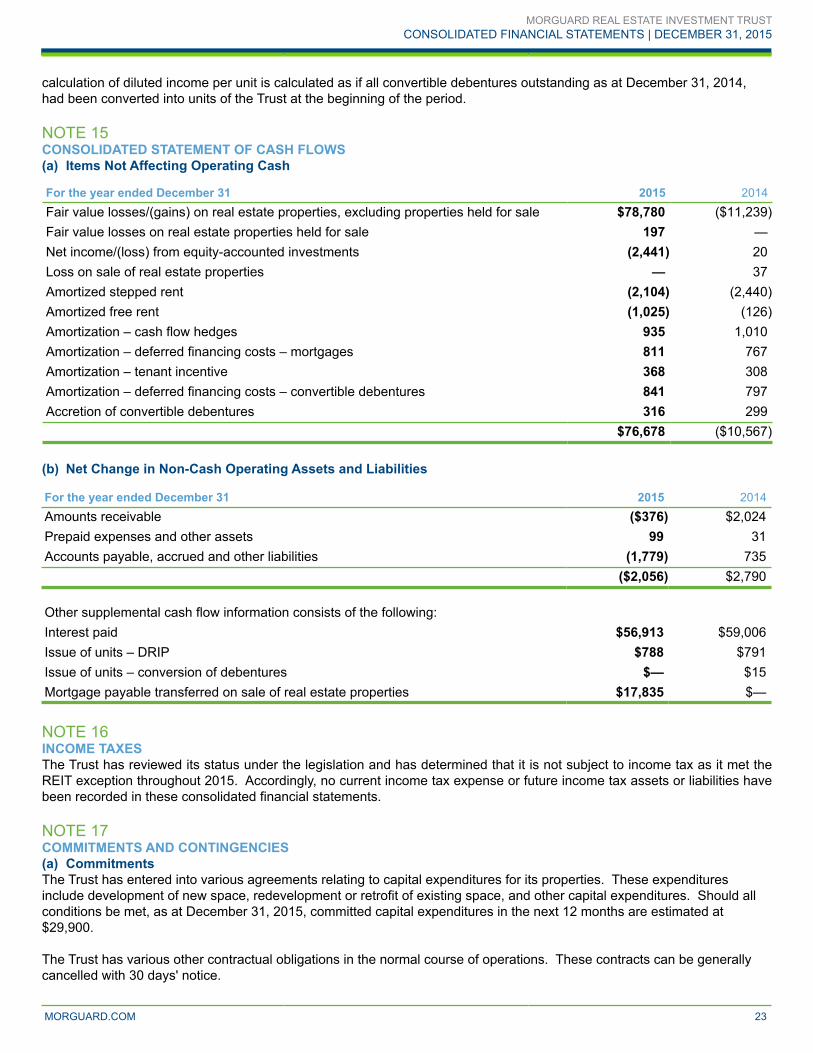

NOTE 15CONSOLIDATED STATEMENT OF CASH FLOWS (a) Items Not Affecting Operating Cash

For the year ended December 31 2015 2014Fair value losses/(gains) on real estate properties, excluding properties held for sale $78,780 ($11,239)Fair value losses on real estate properties held for sale 197 —Net income/(loss) from equity-accounted investments (2,441) 20Loss on sale of real estate properties — 37Amortized stepped rent (2,104) (2,440)Amortized free rent (1,025) (126)Amortization – cash flow hedges 935 1,010Amortization – deferred financing costs – mortgages 811 767Amortization – tenant incentive 368 308Amortization – deferred financing costs – convertible debentures 841 797Accretion of convertible debentures 316 299

$76,678 ($10,567)

(b) Net Change in Non-Cash Operating Assets and Liabilities

For the year ended December 31 2015 2014Amounts receivable ($376) $2,024Prepaid expenses and other assets 99 31Accounts payable, accrued and other liabilities (1,779) 735

($2,056) $2,790

Other supplemental cash flow information consists of the following:Interest paid $56,913 $59,006Issue of units – DRIP $788 $791Issue of units – conversion of debentures $— $15Mortgage payable transferred on sale of real estate properties $17,835 $—

NOTE 16INCOME TAXESThe Trust has reviewed its status under the legislation and has determined that it is not subject to income tax as it met the REIT exception throughout 2015. Accordingly, no current income tax expense or future income tax assets or liabilities have been recorded in these consolidated financial statements.

NOTE 17COMMITMENTS AND CONTINGENCIES(a) CommitmentsThe Trust has entered into various agreements relating to capital expenditures for its properties. These expenditures include development of new space, redevelopment or retrofit of existing space, and other capital expenditures. Should all conditions be met, as at December 31, 2015, committed capital expenditures in the next 12 months are estimated at $29,900.

The Trust has various other contractual obligations in the normal course of operations. These contracts can be generally cancelled with 30 days' notice.

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 24

The Trust is committed to making the following annual payments under a ground lease to the year 2065 for the land upon which one of the properties is situated:

March 1, 2011, to February 28, 2021 $714Subsequent to February 28, 2021 Fair market value of land in February 2021 multiplied by 8.5% per annum

Effective November 17, 2013, the Trust entered into an operating sublease agreement with Morguard, expiring on November 15, 2023. Annual rent agreement amounts to approximately $193.

In addition to the above-mentioned contractual obligations, the Trust has entered into equipment operating leases with terms ranging to 2020. The remaining payments for the leases are as follows:

2016 $1152017 422018 232019 222020 9

(b) ContingenciesThe Trust is contingently liable with respect to litigation, claims and environmental matters that arise from time to time, including those that could result in mandatory damages or other relief, which could result in significant expenditures. While the outcome of these matters cannot be predicted with certainty, in the opinion of management, any liability that may arise from such contingencies would not have a material adverse effect on the financial position or results of operations of the Trust. Any expected settlement of claims in excess of amounts recorded will be charged to operations as and when such determination is made.

NOTE 18MANAGEMENT OF CAPITALThe Trust defines capital that it manages as the aggregate of its unitholders’ equity and interest-bearing debt less cash and cash equivalents and interest-bearing receivables. The Trust’s objective when managing capital is to ensure that the Trust will continue as a going concern so that it can sustain daily operations and provide adequate returns to its unitholders.

The Trust is subject to risks associated with debt financing, including the possibility that existing mortgages may not be refinanced or may not be refinanced on as favourable terms or with interest rates as favourable as those of the existing debt. The Trust mitigates these risks by its continued efforts to stagger the maturity profile of its long-term debt, to enhance the value of its real estate properties and to maintain high occupancy levels. The Trust manages its capital structure and makes adjustments to it in light of changes in economic conditions and the risk characteristics of the underlying assets.

The total managed capital for the Trust is summarized below:

As at December 31 Note 2015 2014Total mortgages payable (including held for sale) $1,172,335 $1,212,186Convertible debentures payable 147,698 146,541Bank indebtedness — 4,927Cash and cash equivalents (26,282) (12,612)Loan receivable 12(b) — (30,000)Unitholders’ equity 1,556,140 1,607,081

$2,849,891 $2,928,123

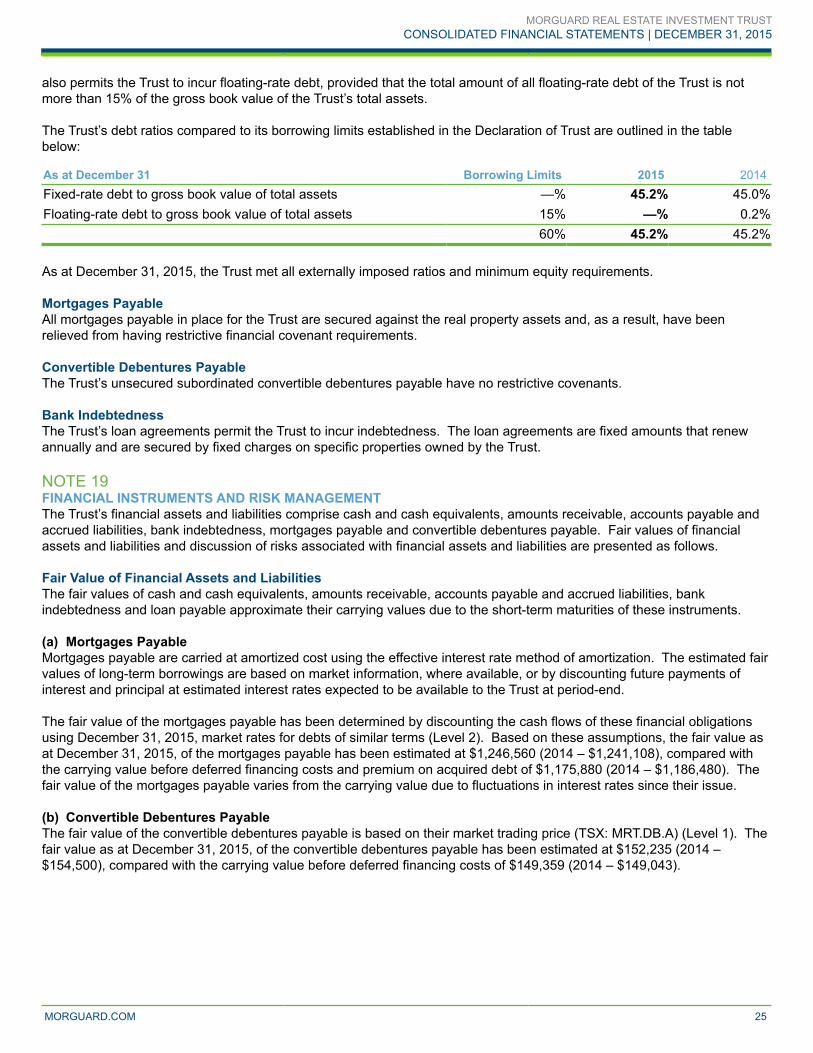

The Trust’s Declaration of Trust permits the Trust to incur indebtedness, provided that after giving effect to incurring or assuming any indebtedness (as defined in the Declaration of Trust), the amount of all indebtedness of the Trust is not more than 60% of the gross book value of the Trust’s total assets as defined in the Declaration of Trust. The Declaration of Trust

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 25

also permits the Trust to incur floating-rate debt, provided that the total amount of all floating-rate debt of the Trust is not more than 15% of the gross book value of the Trust’s total assets.

The Trust’s debt ratios compared to its borrowing limits established in the Declaration of Trust are outlined in the table below:

As at December 31 Borrowing Limits 2015 2014Fixed-rate debt to gross book value of total assets —% 45.2% 45.0%Floating-rate debt to gross book value of total assets 15% —% 0.2%

60% 45.2% 45.2%

As at December 31, 2015, the Trust met all externally imposed ratios and minimum equity requirements.

Mortgages PayableAll mortgages payable in place for the Trust are secured against the real property assets and, as a result, have been relieved from having restrictive financial covenant requirements.

Convertible Debentures PayableThe Trust’s unsecured subordinated convertible debentures payable have no restrictive covenants.

Bank IndebtednessThe Trust’s loan agreements permit the Trust to incur indebtedness. The loan agreements are fixed amounts that renew annually and are secured by fixed charges on specific properties owned by the Trust.

NOTE 19FINANCIAL INSTRUMENTS AND RISK MANAGEMENTThe Trust’s financial assets and liabilities comprise cash and cash equivalents, amounts receivable, accounts payable and accrued liabilities, bank indebtedness, mortgages payable and convertible debentures payable. Fair values of financial assets and liabilities and discussion of risks associated with financial assets and liabilities are presented as follows.

Fair Value of Financial Assets and LiabilitiesThe fair values of cash and cash equivalents, amounts receivable, accounts payable and accrued liabilities, bank indebtedness and loan payable approximate their carrying values due to the short-term maturities of these instruments.

(a) Mortgages PayableMortgages payable are carried at amortized cost using the effective interest rate method of amortization. The estimated fair values of long-term borrowings are based on market information, where available, or by discounting future payments of interest and principal at estimated interest rates expected to be available to the Trust at period-end.

The fair value of the mortgages payable has been determined by discounting the cash flows of these financial obligations using December 31, 2015, market rates for debts of similar terms (Level 2). Based on these assumptions, the fair value as at December 31, 2015, of the mortgages payable has been estimated at $1,246,560 (2014 – $1,241,108), compared with the carrying value before deferred financing costs and premium on acquired debt of $1,175,880 (2014 – $1,186,480). The fair value of the mortgages payable varies from the carrying value due to fluctuations in interest rates since their issue.

(b) Convertible Debentures PayableThe fair value of the convertible debentures payable is based on their market trading price (TSX: MRT.DB.A) (Level 1). The fair value as at December 31, 2015, of the convertible debentures payable has been estimated at $152,235 (2014 – $154,500), compared with the carrying value before deferred financing costs of $149,359 (2014 – $149,043).

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 26

(c) Fair Value Hierarchy of Real Estate PropertiesThe fair value hierarchy of income producing properties, properties under development and land held for development measured at fair value in the consolidated balance sheets is as follows:

As atDecember 31, 2015 December 31, 2014

Level 1 Level 2 Level 3 Level 1 Level 2 Level 3ASSETS:

Income producing properties $— $— $2,816,124 $— $— $2,822,074Properties under development $— $— $2,524 $— $— $16,511Land held for development $— $— $28,750 $— $— $27,650

Risks Associated With Financial Assets and LiabilitiesThe Trust is exposed to financial risks arising from its financial assets and liabilities. The financial risks include interest rate risk, credit risk and liquidity risk. The Trust’s overall risk management program focuses on establishing policies to identify and analyze the risks faced by the Trust, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Trust’s activities. The Trust aims to develop a disciplined control environment in which all employees understand their roles and obligations.

Market RiskMarket risk, the risk that the fair value or future cash flows of financial assets or liabilities will fluctuate due to movements in market prices, comprises the following:

(i) Interest Rate RiskThe Trust is subject to the risks associated with debt financing, including the risk that mortgages and credit facilities will not be able to be refinanced on terms as favourable as those of the existing indebtedness. Interest on the Trust's bank indebtedness is subject to floating interest rates. The Trust mitigates these risks by its continued efforts to enhance the value of its real estate properties, to maintain high occupancy levels to meet its debt obligations and to foster excellent relations with its lenders. For the year ended December 31, 2015, the average increase or decrease in net income for each 1% change in interest rates paid on floating debt amounts to $nil.

The Trusts objective in managing interest rate risk is to minimize the volatility of the Trust's earnings. As at December 31, 2015, interest rate risk has been minimized because all long-term debt is financed at fixed interest rates with maturities scheduled over a number of years.

(ii) Credit RiskCredit risk arises from the possibility that tenants and/or debtors may experience financial difficulty and be unable or unwilling to fulfill their lease commitments. The Trust mitigates the risk of loss by investing in well-located properties in urban markets that attract quality tenants, by ensuring that its tenant mix is diversified and by limiting its exposure to any one tenant. A tenant's success over the term of its lease and its ability to fulfill its obligations are subject to many factors. There can be no assurance that a tenant will be able to fulfill all of its existing commitments and leases up to the expiry date.

The Trust's commercial leases typically have a lease term between five and 10 years, and may include clauses to enable periodic upward revision of the rental rates, and contractual extensions at the option of the lessee.

Future minimum annual rental receipts on non-cancellable tenant operating leases are as follows:

For the year ended December 31 2015 2014Not later than one year $155,298 $161,903Later than 1 year and not later than 5 years 493,959 498,862Later than 5 years 354,582 402,139

$1,003,839 $1,062,904

The objective in managing credit risk is to mitigate exposure through the use of approved policies governing the Trust's

MORGUARD REAL ESTATE INVESTMENT TRUSTCONSOLIDATED FINANCIAL STATEMENTS | DECEMBER 31, 2015

MORGUARD.COM 27

credit practices that limit transactions according to counterparties' credit quality.

The carrying value of amounts receivable is reduced through the use of an allowance account, and the amount of the loss is recognized in the consolidated statement of income within property operating expenses. When a receivable balance is considered uncollectible, it is written off against the allowance for doubtful accounts. Subsequent recoveries of amounts previously written off are credited against operating expenses in the consolidated statement of income.

The following table sets forth details of amounts receivable and related allowance for doubtful accounts:

As at December 31 2015 2014

AMOUNTS RECEIVABLE:Trade receivables $13,784 $13,377Less: Allowance for doubtful accounts (773) (742)Trade receivables, net $13,011 $12,635Loans receivable — 30,000Total amounts receivable, net $13,011 $42,635

(iii) Liquidity RiskLiquidity risk is the risk that the Trust will encounter difficulties in meeting its financial obligations. The Trust will be subject to the risks associated with debt financing, including the risk that mortgages, convertible debentures and credit facilities will not be able to be refinanced. The Trust's objectives in minimizing liquidity risk are to maintain appropriate levels of leverage of its real estate assets and to stagger its debt maturity profile. As at December 31, 2015, the Trust was holding cash and cash equivalents in the amount of $26,282 (2014 – $12,612). The Trust also had undrawn lines of credit available in the amount of $69,714 (2014 – $64,783).