mortgagor/grantee’s audit guide · virginia housing development authority (vhda) to meet its...

TRANSCRIPT

VIRGINIA HOUSING DEVELOPMENT AUTHORITY

MULTIFAMILY PROGRAMS

MORTGAGOR/GRANTEE’S AUDIT GUIDE

Effective: 10/86 Revised: 10/97, 05/01, 11/04, 11/06, 11/07, 11/08, 12/09, 12/10, 12/11, 12/13, 12/15, 12/16, 12/17, 12/18, 12/19Revised: 11/4/19 for Fiscal Years Ending On or After 12/31/19

i

TABLE OF CONTENTS

TABLE OF CONTENTS i

FOREWORD iii

MORTGAGOR / GRANTEE’S AUDIT GUIDE Control and Management of the Development 1 Organizational Relationships 1 Reference Material 3 Submission 6 Audit Scope and Approach 7 Definitions 9 Contents of Annual Financial Statements 12

APPENDICES

APPENDIX A SAMPLE AUDITED FINANCIAL STATEMENTS A-1

Appendix A, A-1a MORTGAGOR / GRANTEE CERTIFICATION A-2

Appendix A, A-1b MANAGEMENT AGENT CERTIFICATION A-3

Appendix A, A-2 REPORT ON AUDITED FINANCIAL STATEMENTS AND OTHER VHDA INFORMATION

A-4

Appendix A, A-3 BALANCE SHEET A-6

Appendix A, A-4 STATEMENT OF PROFIT AND LOSS A-9

Appendix A, A-5 STATEMENT OF CHANGES IN OWNER EQUITY A-12

Appendix A, A-6 STATEMENT OF CASH FLOWS A-13

Appendix A, A-7 NOTES TO FINANCIAL STATEMENTS Organization Summary of Significant Accounting Policies Notes Payable and Due To Mortgagor / Grantee Entity Risks and Uncertainties Identity-of-Interest/Related Party Transactions Master Tenant Master Lease(s) & Commercial Space(s)

A-16

Appendix A, A-8 OTHER VHDA INFORMATION Accrued Expenses A-18Accounts and Notes Receivable (Other Than From Tenants) A-19Delinquent Tenant Accounts Receivable A-20

ii

Appendix A, A-8 OTHER VHDA INFORMATION (Continued) Mortgage Reserve Funds (Schedule) Reserve for Replacements Mortgage Reserve Funds (Schedule) Operating Reserve

A-21 A-22

Mortgage Reserve Funds (Schedule) Miscellaneous Reserve A-23 Mortgage Reserve Funds (Schedule) Development-Held Reserve A-24 Schedule of Funds in Financial Institutions A-25 Changes in Fixed Asset Accounts A-26 Accounts Payable (Other Than Trade Creditors & Trade Creditors) A-27 Statement of Surplus Cash / Residual Receipts and Distributions A-28 Instructions for Statement of Surplus Cash / Residual Receipts and

Distributions A-29

Ownership Entity Identification of Engagement Auditor Audit Compliance and Internal Control Questionnaire

A-31 A-32 A-33

Appendix A, A-9

CORRECTIVE ACTION PLAN

A-37

APPENDIX B VHDA CHART OF ACCOUNTS B-1

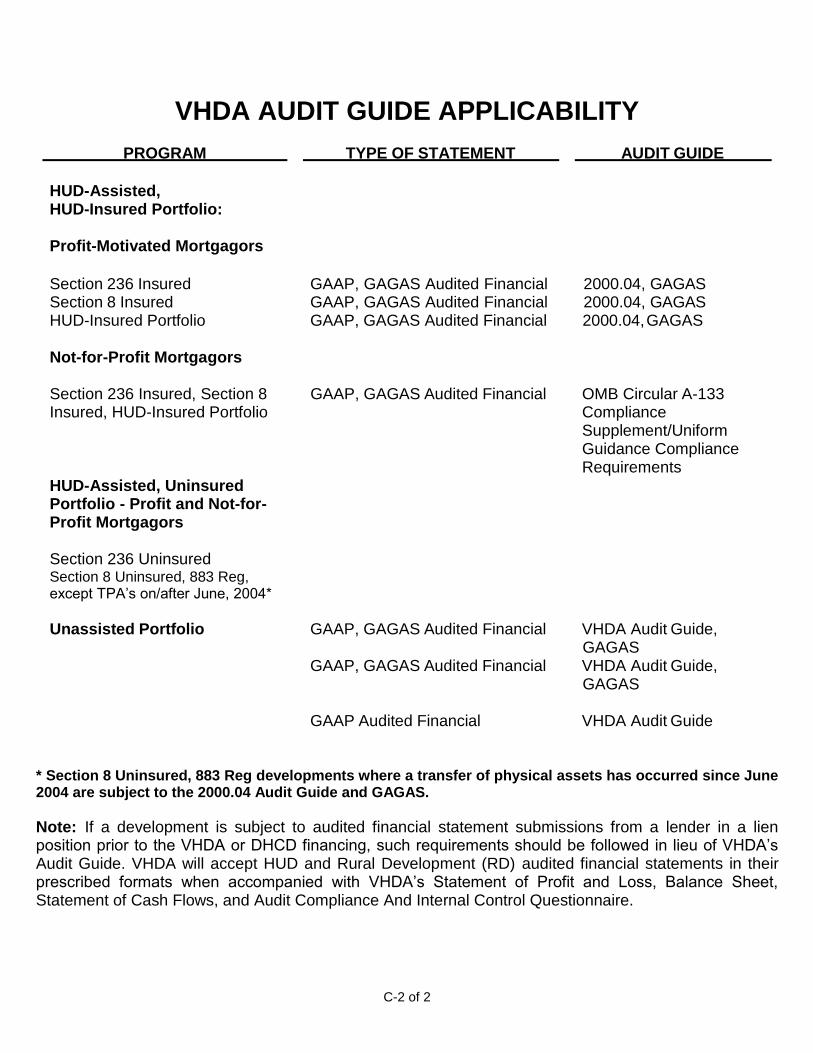

APPENDIX C VHDA AUDIT GUIDE APPLICABILITY C-1

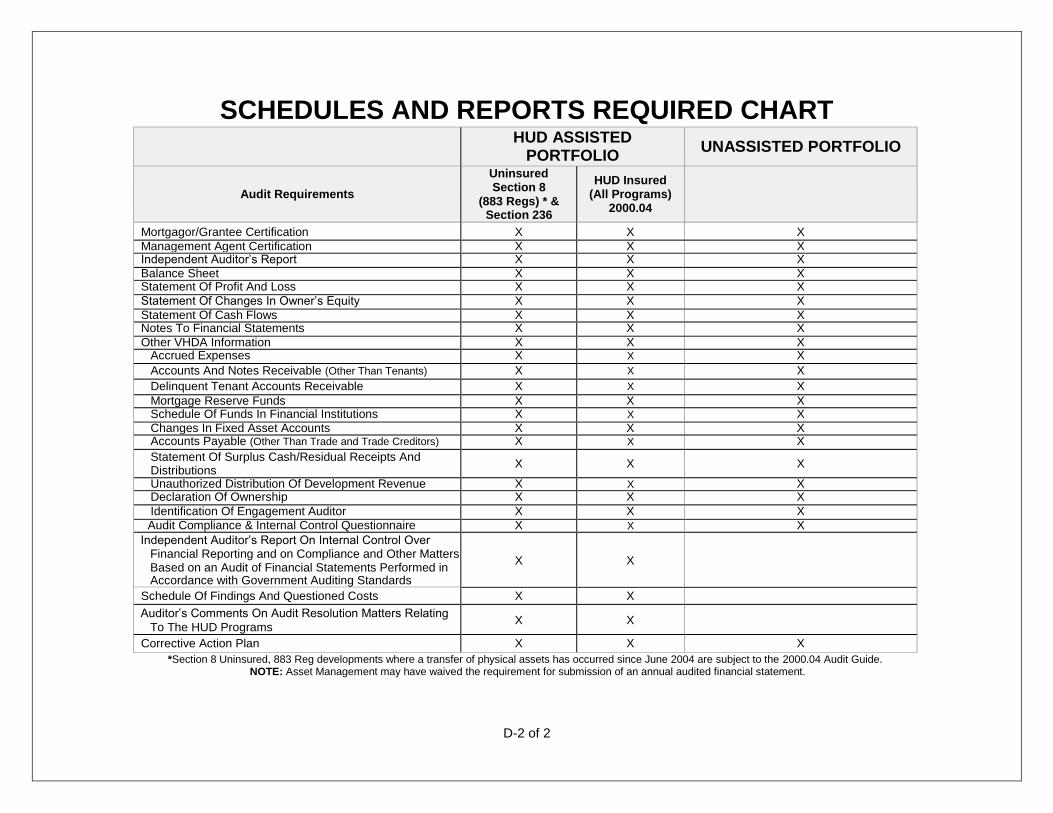

APPENDIX D SCHEDULES AND REPORTS REQUIRED D-1

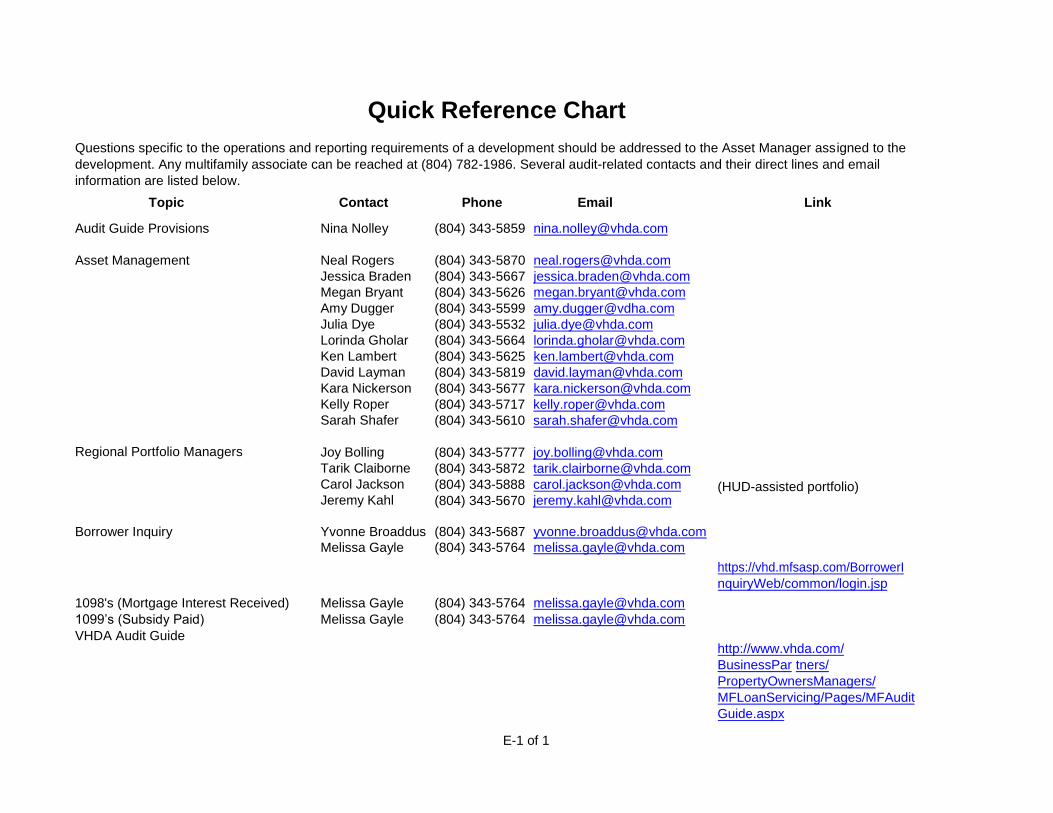

APPENDIX E QUICK REFERENCE CHART E-1

iii

FOREWORD

Audited financial statements are one of the primary tools used by the Virginia Housing Development Authority (VHDA) to meet its fiduciary responsibility in overseeing housing programs and assuring the integrity of its financed multifamily portfolio. Asset Managers, as appropriate, will address the areas of noncompliance and internal control weaknesses noted in these statements.

The VHDA Mortgagor/Grantee’s Audit Guide (VHDA Audit Guide) is

neither intended to be a complete manual of procedures, nor is it intended to supplant the auditor’s judgment of audit work required. Suggested formats and requested levels of detail contained herein may not cover all circumstances or conditions encountered in an audit. The auditor should use professional judgment to add supplemental information and to determine the extent of testing necessary to support the opinion in the financial statements. The auditor must address all applicable compliance requirements in the VHDA Audit Guide.

Any substantial deviation from VHDA’s Audit Guide, including formatting changes to schedules and reports, must receive prior written approval of VHDA. Note: The Balance Sheet, Statement of Profit and Loss, and Statement of Cash Flows are required in the VHDA formats. In addition to submission in the audited financial statements, the Balance Sheet and Statement of Profit and Loss must be submitted electronically using the form and associated instructions found at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServi cing/Pages/MFAuditGuide.aspx.

The auditor should contact the Multifamily Servicing or Asset Management staffs of Virginia Housing at (804) 782-1986 if technical assistance is needed pertaining to programs, regulations or operations of VHDA, DHCD, HUD or any other organization with contractual relationships. Appendix E provides a quick reference list to assist in directing calls. In addition the most current version of VHDA’s Audit Guide is available, with all forms in an interactive format, at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServi cing/Pages/MFAuditGuide.aspx. Future updates will be posted on this site.

1 of 22

VIRGINIA HOUSING DEVELOPMENT AUTHORITY MULTIFAMILY PROGRAMS

MORTGAGOR/GRANTEE’S AUDIT GUIDE

Control and Management of the Development

As an inducement to the Virginia Housing Development Authority (VHDA) or the Department of Housing and Community Development (DHCD) to provide financing for a housing development, the Mortgagor/Grantee agrees to be regulated in the manner set forth in a Deed of Trust, Regulatory Agreement, Grant Agreement and/or other regulatory documents. These documents are incorporated in and made a part of the mortgage/grant security. In addition, the Mortgagor/Grantee and the Management Agent agree to conduct the operation and management of the development in accordance with the provisions of the regulatory documents.

Organizational Relationships

VHDA has formal relationships with several federal and state agencies that affect the monitoring of those loans/grants with which these agencies are affiliated and the regulations that are imposed. Often there is more than one type of funding or agency involvement in VHDA loans. Generally, the most stringent requirements for each program are used for compliance purposes.

It is important that auditors determine the nature of the financing and the relationship VHDA has with any other agency involved in the financings of the development(s) of the Mortgagor/Grantee being audited. This will enable the auditor to determine which agency’s rules take precedence not only in program requirements but also for audit purposes. Some basic information on VHDA financing and affiliated agencies follows.

Virginia Housing Development Authority (VHDA) - VHDA provides direct financing of multifamily developments through various programs and financing sources.

Department of Housing and Community Development (DHCD) - VHDA services loan and grant programs for the Commonwealth Priority Housing Fund (CPHF), the HOME program, and the Virginia Housing Trust Fund in coordination with the Department of Housing and Community Development. VHDA has also assisted with the Virginia Housing Partnership Revolving Fund (VHPRF). The VHPRF financed the Affordable Housing Production Program, as well as several individual programs including the Multifamily Rehabilitation, Multifamily Production, SHARE Energy, SHARE Expansion, and Congregate programs. VHDA monitors compliance with DHCD program guidelines, including rent and occupancy restrictions, services the mortgages and

2 of 22

grants, and analyzes financial data (monthly and/or annually). All findings are reported directly to DHCD.

Department of Housing and Urban Development (HUD) - VHDA is the mortgagee for HUD-insured and uninsured loans under several programs.

VHDA has a number of HUD-insured loans in its portfolio. For the majority of

these developments, HUD approves rents, authorizes reserve releases, determines audit procedures, and contracts subsidy administration to a third party vendor. The servicing of HUD-insured loans is either handled directly by VHDA or through a servicing company approved by VHDA. VHDA performs asset management reviews and monitors the financial performance of these developments in its role as a mortgagee.

VHDA is also the mortgagee of Section 236 and Section 8 uninsured loans that were financed through the Housing Finance Agency Set-Aside program. Virginia Housing conducts all servicing of these mortgages/grants in-house. VHDA also serves as the contract administrator for many of its Section 236 and Section 8 uninsured loan portfolio. As mortgagee and contract administrator, VHDA authorizes rent increases and reserve releases, monitors compliance with program requirements, and monitors compliance with the terms of the regulatory documents. The Asset Management staff performs asset management reviews and financial monitoring of the developments. When VHDA is the contract administrator, VHDA pays Housing Assistance Payments (HAP) to the Section 8 developments based on data supplied through the TRACS automated system.

VHDA also administers through administrative agents the Section 8 Mod Rehab and Housing Choice Voucher programs for many localities throughout the Commonwealth of Virginia. The Housing Choice Voucher staff of Virginia Housing handles these programs.

Internal Revenue Service - Section 42 Tax Credits - VHDA is the housing credit agency for Virginia and issues Federal Low-Income Housing Tax Credits under Section 42 of the IRS code. After allocation of tax credits to a development, VHDA staff conducts record and physical inspections to ensure compliance with the IRS monitoring regulations. Discrepancies are reported directly to the IRS.

Department of Behavioral Health and Developmental Services (DBHDS) (formerly DMHMRSAS) - VHDA offers various programs for special needs populations. For these programs, funding is provided in conjunction with Memoranda of Understanding that provide for financial commitments by that agency to ensure the continued viability of the loan. These programs include both assisted and unassisted financing.

3 of 22

Reference Material

The following documents and subsequent addenda, where applicable, are necessary in order to conduct the audit and should be obtained from the Mortgagor/Grantee and/or Management Agent prior to starting the examination.

1. Regulatory Agreement.

2. Deed(s) of Trust.

3. Deed of Trust Note(s) and Note Agreement, if applicable.

4. Housing Management Agreement.

5. Grant Agreement(s).

6. Extended Use Agreement (EUA).

7. Any subsidy contracts (and amendments thereto) in force at the development(s), including, where applicable, Housing Assistance Payments Contract, Rental Assistance Payments Contract, Interest Reduction Payments Contract, etc.

8. Rent schedule(s) in effect during the audited year. For HUD- assisted developments, the signed HUD 92458, Rent Schedule must be obtained. The Management Agent should provide schedules for unassisted developments.

9. Fair Market Rents (FMR’s) and Income Limits applicable to the

audited development(s). FMR’s and Income Limits are available from HUD User at http://www.huduser.org.

10. Final Closing Determinations (CD: 1500) or other closing settlement statements.

11. Notices of default, acceleration, or other regulatory non- compliance.

12. Any mortgage or grant instruments including modification, forbearance, pre-workout, and workout agreements and arrangements.

13. Any contracts for services or supplies executed on behalf of the development(s).

4 of 22

14. Confirmation of loan, escrow and reserve balances, principal, interest, escrows, and reserves paid, etc. (VHDA Account Summary Status and Reserve History Report(s)). These reports are available online from VHDA’s Borrower Inquiry application at https://vhd.mfsasp.com/BorrowerInquiryWeb/common/login.jsp. Inquiries regarding access to the application should be directed to (804) 343-5687.

15. Any correspondence related to the latest asset management review and occupancy audit reports (Report of Occupancy Audit Findings, Occupancy Review, and Conclusion) issued by VHDA’s staff. On HUD assisted developments, a copy of the latest HUD- 9834, Management Review for Multifamily Housing Projects, commonly called the MOR (Management Occupancy Review), must be obtained. The Management Agent’s response and supplemental follow-up to any of these reports, if any, must be obtained.

16. On HUD assisted developments, a copy of the Inspection Summary Report, from the most recent physical inspection using the REAC protocol. Attention should be given to the final REAC score, located on the first page of the report, particularly to those scores below 60. Any correspondence related to the inspection or subsequent follow-up or appeal should be obtained.

17. Any applicable HUD Handbooks (and all subsequent updates), including but not limited to HUD 4350.1, Multifamily Asset Management and Project Servicing, HUD 4350.3, Occupancy Requirements of Subsidized Multifamily Housing Programs, HUD 4370.1, Reviewing Annual and Monthly Financial Statements, HUD 4370.2, Financial Operations and Accounting Procedures for Insured Multifamily Projects, HUD 4381.5, The Management Agent Handbook, and HUD Section 8 Renewal Policy Guidebook. Note: Directives, including handbooks, notices, interim notices, and special instructions should be downloaded as needed from several Internet sites, including http://www.gpo.gov, http://www.huduser.org, or http://www.hud.gov. In addition, VHDA instructions for implementing occupancy changes are available at each development. Questions should be addressed to VHDA’s Regional Portfolio Manager contacts in Appendix E.

18. Additional program information, including HUD policy, procedures, and notices are available at HUD Internet sites including http://www.hud.gov and http://www.hud.gov/reac. OMB circulars, forms and compliance supplements can be located on the Internet

5 of 22

at http://www.whitehouse.gov/omb. HUD reference material may be ordered from HUD’s direct distribution system by calling (800) 767-7468, by addressing a letter to: HUD, Customer Service Center, Room B-100, 451 Seventh Street, SW, Washington DC 20410, or by fax at (202) 708-2313.

19. Information on tax credit topics can be found at http://www.huduser.org and http://www.vhda.com.

20. The most current version of any applicable auditing directives and standards, including but not limited to the VHDA Mortgagor/Grantee’s Audit Guide (VHDA Audit Guide), located at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/ MFLoanServicing/Pages/MFAuditGuide.aspx, the U. S. Inspector General’s (U. S. Department of Housing & Urban Development) Audit Guide (Handbook 2000.04 Consolidated Audit Guide for Audits of HUD Programs) available at http://www.hudoig.gov/reports-publications/audit- guides/consolidated-audit-guides, Government Auditing Standards (the Yellow Book) available at http://www.gao.gov/govaud/ybk01.htm, and OMB circulars and subsequent compliance supplements available at http://www.whitehouse.gov/omb.REAC’s Summary of Financial Reporting and Auditing Guidance for HUD Multifamily Program Participants and Independent Auditors (FRAG) is available at https://www.hud.gov/sites/documents/DOC_26323.PDF. Note: Applicability of IG’s Consolidated Audit Guide is referenced in Appendix C.

HUD strongly encourages agencies, owners, accountants, and industry organizations to subscribe to its Multifamily RHIIP listserv email system. The system provides email notification of reference guide revisions and updates as well as important industry announcements. HUD has been recently been relying on listserv to provide information to multifamily owners in lieu of official notification.

21. Virginia Residential Landlord Tenant Act, available at http://www.landlord.com/landlord_law_virginia.htm.

22. All other agreements or correspondence considered pertinent. Particular attention should be given to any correspondence affecting the terms of the Regulatory Agreement or loan documents.

6 of 22

Submission

All audits must be conducted in accordance with generally accepted accounting principles (GAAP) and generally accepted auditing standards (GAAS). VHDA will allow departures from GAAP only for the treatment of depreciation, amortization, and syndication costs. Note: Any such departure must be indicated in the Auditor’s Opinion letter. Virginia Housing will not accept income tax basis audits. Appendices C and D address Audit Guide applicability and reporting requirements of the various programs in VHDA’s portfolio.

VHDA requires that financial statements be prepared and certified by an

independent Certified Public Accountant, unless otherwise excepted by specific programs. The CPA must have no business relationship with the Mortgagor/Grantee except for the performance of the audit, accounting systems work, and tax preparation. An individual who performs manual or automated bookkeeping services and/or maintains the official accounting records is prohibited from performing the audit of a Mortgagor/Grantee. Where Government Auditing Standards apply, the auditor must meet the auditor qualifications of Government Auditing Standards, including the qualifications relating to independence and continuing professional education. Additionally, the audit organization must meet the quality control standards of Government Auditing Standards.

The audit engagement letter or arrangements for the audit between the auditor and Mortgagor/Grantee must allow duly authorized agents of VHDA to examine the auditor’s working papers supporting the audit report. One copy of the complete annual financial statements, including the signed Mortgagor/Grantee and Management Agent Certifications, must be emailed or submitted to the Asset Manager assigned to the development(s) at the following address:

Virginia Housing Development Authority Compliance & Asset Management Department

601 South Belvidere Street Richmond, Virginia 23220

Additionally, the Balance Sheet and Statement of Profit and Loss must be submitted electronically to the asset manager assigned to the development(s). These forms that must be sent to VHDA by email and their associated instructions may be found at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Pa ges/MFAuditGuide.aspx.

Submission is required within ninety (90) days after the end of each fiscal year. Extensions must specify extenuating circumstances and must be requested by the Mortgagor/Grantee, in writing, from the assigned Asset Manager. Note: Financial statements for HUD-insured, HUD-decoupled 236 developments, and most Section 8 properties that have gone through an assumption (transfer of physical assets) must be submitted electronically to HUD within the filing deadlines established by HUD. Detailed requirements for transmitting financial statements electronically to HUD are available at http://www.hud.gov/reac. Any questions regarding REAC and their Financial

7 of 22

Assessment Subsystem (FASS) should be referred to REAC’s technical assistance center at (888) 245-4860. Note: A paper or electronic copy of the audit must be submitted to VHDA within ninety (90) days after the end of the fiscal year.

On developments with construction financing provided by VHDA or DHCD, the initial audit period should cover the date of initial occupancy through the end of the fiscal year of the development(s). On acquisition, bond refunding and rehab financings, the initial audit period should cover from the date of construction (initial) closing (permanent closing if no construction closing) through the end of the fiscal year of the development(s). Typically, the initial audit submission reflects the fiscal year end when the permanent closing occurred. A multi-year audit (i.e., less than 24 months) is acceptable to VHDA. If a multi-year audit is presented, two Statements of Profit and Loss and Statements of Cash Flows must be included (one the partial year; the other a full fiscalyear).

Audit Scope and Approach

The primary purpose of the audit is to report to the Mortgagor/Grantee and VHDA on the financial aspects of the operations of the development(s). The auditor must also report on any failure to comply with VHDA’s and other regulatory requirements. VHDA is interested in the financial solvency of the Mortgagor/Grantee, its ability to meet operating expenses and debt service requirements, and, ultimately, to avoid mortgage default. If there is a master tenant, schedules must be provided to allow VHDA to assess the financial aspects of the development’s operations. Should the auditor during the course of the review have concerns about the solvency of the mortgagor trading as the development(s), such concerns and an evaluation of the extent of the credit risk must be reported in the audit report.

The objectives of the audit are to determine:

1. Whether the financial statements fairly present the financial position of the Mortgagor/Grantee trading as the development(s) and the results of its operations;and

2. Whether operating practices and controls comply with the HUD or VHDA requirements contained in Appendix A, A-8, Other VHDA Information, pages A-18 through A-32, Audit Compliance and Internal Control Questionnaire (Appendix A, A-8, Other VHDA Information, pages A-33 through A-36) and Government Auditing Standards, where applicable.

The audit must be sufficiently comprehensive in scope to permit the expression of an opinion on the financial statements and other VHDA information in the report, and it must be performed in accordance with generally accepted accounting principles and Government Auditing Standards, where applicable, in addition to audit requirements set forth in the VHDA Audit Guide. "Expression of Opinion" includes an unmodified opinion or

8 of 22

a modified opinion. If anything other than an unmodified opinion is given, the reasons for such must be stated and explained in detail.

The opinion must state whether the basic financial statements present fairly the

financial position of the Mortgagor/Grantee trading as the development(s) as of the audit date, and the results of its operations, its cash flows, and its changes in owners’ equity for the period then ended in accordance with generally accepted accounting principles. In addition, the opinion must state that the other VHDA information has been subjected to the audit procedures applied in the audit of the basic financial statements, and whether it is fairly stated in all material respects in relationship to the financial statements taken as a whole. Note: For VHDA purposes, no amounts are considered immaterial.

The auditor must assess the risk of material misstatement of the financial

statements due to fraud and must consider such in designing the audit procedures to be performed. The auditor should consider fraud risk factors contained in the Statement on Auditing Standards (SAS) No. 99, “Consideration of Fraud in a Financial Statement Audit.” If the auditor becomes aware of illegal acts or fraud that have occurred, the auditor must prepare a separate written report and include all questioned costs. The report must be submitted in accordance with Government Auditing Standards, if applicable. A copy of the report must be provided to the VHDA Asset Manager assigned to the development(s).

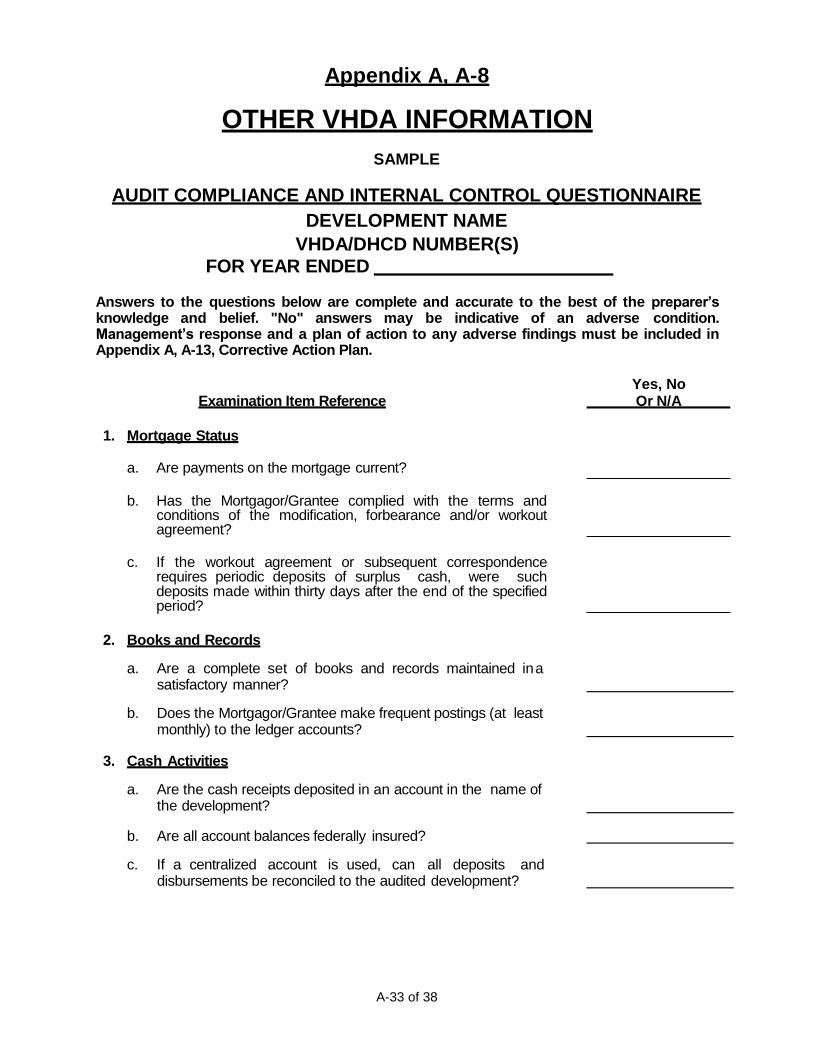

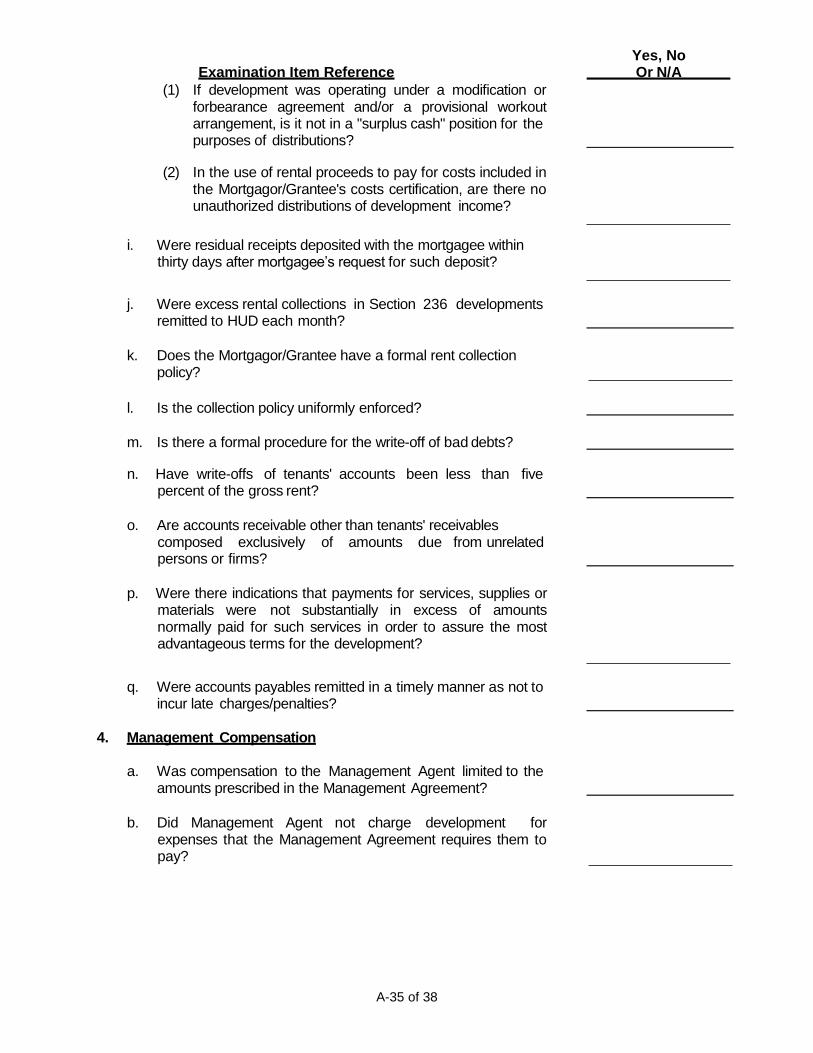

Where applicable, the auditor is required: 1) to perform tests of controls to evaluate the effectiveness of the design and operation of internal control policy and procedures; 2) to test, review, evaluate and comment on the adequacy of the accounting records and procedures as well as the system of internal controls maintained, including the handling of funds; and 3) to test and report on the Mortgagor/Grantee's compliance with certain specific provisions of the Regulatory Agreement, Housing Management Agreement, and VHDA, DHCD, and HUD regulations and procedures applicable to the operation of the development(s) in order to comply with Government Auditing Standards. Note: The VHDA Audit Compliance and Internal Control Questionnaire is required to be included in all financial statements.

Internal control and compliance reporting is required as specified in Appendix D. Where applicable, compliance reporting in adherence with Government Auditing Standards is required. Compliance requirements and suggested audit procedures detailed in HUD’s audit guide should be used as guidance in performing internal control and compliance reporting. Further, in order that the Mortgagor/Grantee and VHDA may be assured of the effectiveness of the development(s) in meeting its program objectives, an Audit Compliance and Internal Control Questionnaire is provided to guide the auditor in the review of compliance and internal control matters that are of particular interest to VHDA. The auditing firm should examine the following areas: mortgage status, books and records, cash activities, management activities, rents and occupancy, and subsidy payments. The Questionnaire has been designed so that "No" answers may be indicative of an adverse condition that must be described in the audit report. Appendix A, A-9 provides a sample format to be used to respond to all “No” answers. The auditor must also cite alternative conditions that mitigate weaknesses as disclosed by the

9 of 22

Questionnaire. The Audit Compliance and Internal Control Questionnaire must be submitted to VHDA with all financial statements. Note: The mortgagor and auditor determine who will complete the Questionnaire.

Definitions

1. Total Rental Income Potential at 100% Occupancy - The total rent potential shown on the rent roll prior to adjustments for concessions or additional charges such as pet fees, washer/dryers, carports, etc. Rent potential should not exceed the rents for all units based on full occupancy and should exclude any “unrealized potential” such as “loss to old leases” and “street rent” vs. actual rent per lease agreement. Rent potential should delineate residential income from other sources such as commercial spaces.

2. Concessions - Money uncollected because of marketing discounts, promotions, or incentives, including the state tax credit program. Note: Non-income-producing units should be expensed under the appropriate category.

3. Distribution - Any withdrawal or taking of cash or other assets of

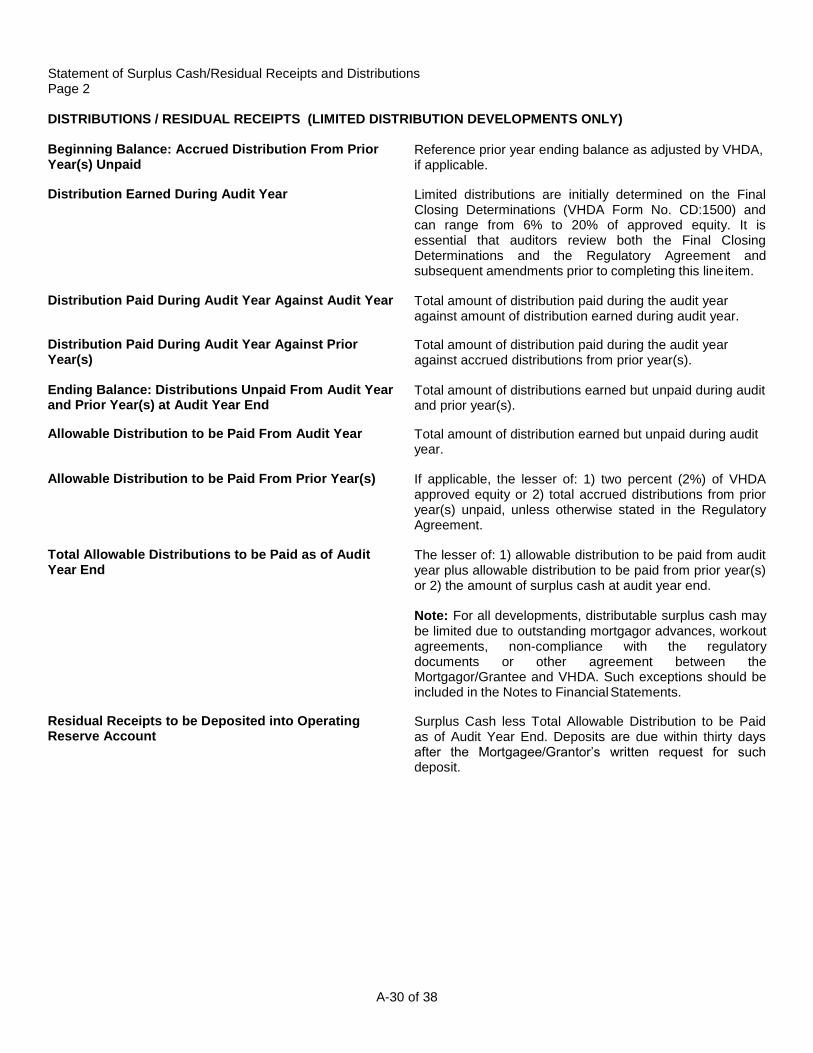

the development(s), excluding payment for reasonable expenses necessary and essential to the operation and maintenance of the development(s) (including repayment of owner advances). Distributions include cash or assets segregated for subsequent withdrawal (including funds transferred to mortgagor entity-held accounts), asset management fees, incentive management fees, development fees, or other corporate or mortgagor entity expenses. Distributions are subject to the terms of the Regulatory Agreement or other governing documents. Distribution earnings (return on equity investment) commence upon the permanent (final) closing of the loan, unless otherwise specified in the regulatory documents. The amount of equity investment and the maximum allowable return thereon are initially determined at permanent (final) closing. The maximum allowable distribution may be amended during the term of the mortgage. The auditor must verify any changes to the initial equity determination with the assigned Asset Manager.

Distributions should not be made: 1) from borrowed funds, 2) prior to permanent (final) closing of the mortgage loan/grant, 3) when the development(s) is not in good repair or condition based on VHDA’s or other regulatory entity’s physical inspection or asset management review and subsequent notification by VHDA or its representatives, 4) when the development(s) is in a non-

10 of 22

surplus cash position as defined hereunder, 5) when restricted by a modification agreement, 6) when there is any default under the Regulatory Agreement, Deed of Trust Note and/or other regulatory documents, or 7) when there are any notices of non- compliance issued by VHDA or its representatives. Note: The requirement of a development(s) to be in a surplus cash position prior to making a distribution may have been modified by separate written correspondence from VHDA.

4. Surplus Cash - Cash remaining as of the last day of the fiscal year of the development(s) after all reasonable expenses necessary and essential to the operation of the development(s) have been paid or funds have been set aside for such payment and all reserve requirements have been met. Note: Mortgagor entity cash and obligations must be excluded from the calculation. It includes all funds received by the Mortgagor/Grantee in connection with the operation of the development(s) and remaining after:

a. The payment of:

(1) All sums due under the terms of the Note(s), Deed(s) of Trust, Regulatory Agreement, or other regulatory documents as of the last day of the fiscal year of the development(s);

(2) All amounts required to be deposited in the

Replacement, Miscellaneous and/or Operating Reserves as of the last day of the fiscal year of the development(s); and

(3) All other obligations of the development(s) except to the extent that funds for payment of any such obligations are set aside or deferment of payment has been approved by an Authorized Officer of VHDA; and

b. The segregation of:

(1) An amount equal to the aggregate of all special funds required to be maintained by or with respect to the development(s); and

(2) Resident security deposit liability, including

accrued interest as of the last day of the fiscal year of the development(s).

11 of 22

The surplus cash calculation is specified on the Statement of Surplus Cash/Residual Receipts and Distributions, Appendix A, A-8, page A-28.

5. Identity-of-Interest – Includes a Management Agent and other parties having business relationships with a development(s) owner or any officer, director, partner, member or manager of the Mortgagor/Grantee. Transactions with identity-of-interest relationships occur when there are common controlling equity interests and/or management control between the entities. Such a relationship should be construed to exist when the owner and the Management Agent are not the same person but 1) the development owner; or 2) any officer or director of the development owner; or 3) any person who directly or indirectly controls 10 percent or more of the development owner’s voting rights or directly or indirectly owns 10 percent or more of the development owner; is also 1) an officer or director of the Management Agent; or 2) a person who directly or indirectly controls 10 percent or more of the Management Agent’s voting rights or directly or indirectly owns 10 percent or more of the Management Agent. For purposes of this definition, the term “person” includes any individual, member of the Board of Directors, partnership, corporation, or other business entity. Any ownership, control or interest held or possessed by a person’s spouse, parent, child, grandchild, brother or sister is attributed to that person.

6. Essential, Necessary and Reasonable Expenses - Limited to those obligations specifically incurred directly by the operations and maintenance of the development(s). The auditor will have to make a judgment as to the propriety of development(s) disbursements. However, some expenditures, such as for expenses incurred by the mortgagor entity, the fee for the preparation of a partner's, shareholder's or individual's federal, state or local income tax returns, or the payment for advice to an owner on the tax consequences of foreclosure, clearly are not expenses essential, necessary and reasonable to the operations of the development(s) and, therefore, constitute distributions of development(s) income. Also not allowed as a development(s) expense is the cost of a fidelity bond (other than for on-site staff) or letter of credit required of the agent or Mortgagor/Grantee. The fee for preparation of the federal, state or local income tax returns of the mortgagor entity or corporation is an expense necessary and reasonable to the operations of the development(s).

12 of 22

7. Tenant Eligibility - Each program contains specific eligibility requirements based on income, family size and similar criteria. The criteria, for the most part, are contained on the application forms for tenant eligibility maintained at the development and/or managing agent’s office. The auditor should also have access to the applicable HUD, DHCD, VHDA, and/or other contractual organization handbooks and directives. The auditor should also be familiar with the Fair Market Rents (FMR’s) and Income Limits applicable on the audited development(s). Any tenant eligibility questions that cannot be resolved through these resources should be directed to VHDA’s Occupancy and Program Compliance contacts in Exhibit E.

8. Exit Conference - At the conclusion of the audit, an exit conference is to be held with the Mortgagor/Grantee to discuss the audit findings and obtain comments from the Mortgagor/Grantee on: 1) the accuracy and completeness of the facts presented and whether they agree with the audit conclusions; and 2) any action the Mortgagor/Grantee plans to take or reasons for not taking action. A Corrective Action Plan, if applicable, is required to be submitted by the Mortgagor/Grantee with the financial statements (Appendix A, A-9, pages A-37 and A-38).

Contents of Annual Financial Statements

Please pay particular attention to the requirements for submitting the Statement of Profit And Loss and Balance Sheet. In addition to submission in the audited financial statements, the Balance Sheet and Statement of Profit and Loss must be submitted electronically using the form and associated instructions found at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Page s/MFAuditGuide.aspx. The audited financial statements delivered to VHDA must conform to the contents of the VHDA Audit Guide and must include all schedules and reports as specified in Appendix D. These reports and schedules are defined below and illustrative examples are shown in Appendix A. These examples exhibit preferred formats and requested levels of detail in the presentations. The sample statements presented in the VHDA Audit Guide are designed for a profit-motivated mortgagor/grantee entity. Note: Financial statements for not-for-profit mortgagors/grantees subject to the IG’s Consolidated Audit Guide should follow OMB Circular A-133 Compliance Supplement/Uniform Guidance Compliance Requirements. Financial statements on not- for-profit mortgagors/grantees not subject to IG’s Consolidated Audit Guide must follow the VHDA Audit Guide. Financial Statements on all mortgagors/grantees (profit-motivated and not-for-profit) are required to be in accordance with GAAP.

13 of 22

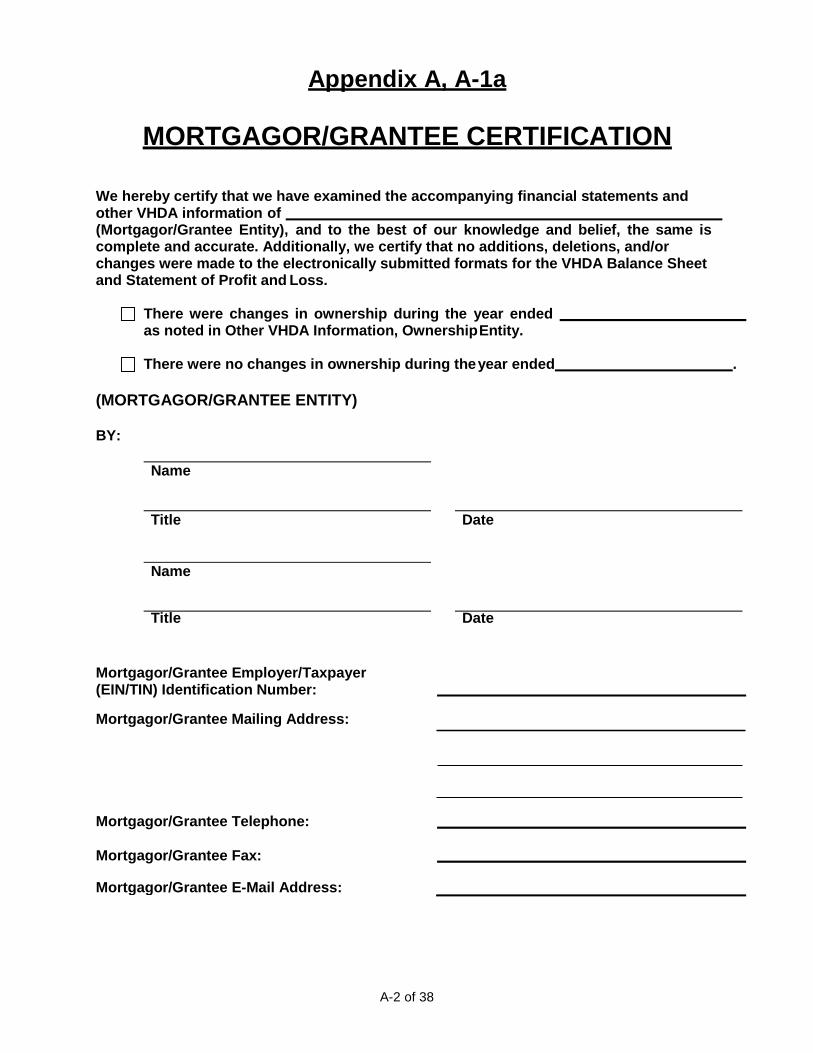

1. Mortgagor/Grantee Certification. The report must include a certification signed by an authorized official of the Mortgagor/Grantee entity as to the completeness and accuracy of the financial statements and other VHDA information. The official must also 1) indicate whether or not there have been changes in the ownership during the reported year and 2) certify that no additions, deletions and/or changes were made to the electronically submitted formats for the VHDA Balance Sheet and Statement of Profit and Loss. (Appendix A, A-1a, page A-2).

2. Management Agent Certification. The report must include a certification signed by an authorized official of the Management Agent as to the completeness and accuracy of the financial statements and other VHDA information. (Appendix A, A-1b, page A-3).

3. Report On Audited Financial Statements And Other VHDA Information (Independent Auditor’s Report). Appendix A, A-2, pages A-4 and A-5 includes a sample format to be included in the statement. The auditor’s opinion (see pages 7 - 8 of this Audit Guide) must be included in the report.

4. Balance Sheet. This form must be submitted electronically using the form and associated instructions found at http://www.vhda.com/BusinessPartners/PropertyOwnersManag ers/MFLoanServicing/Pages/MFAuditGuide.aspx. The Balance Sheet must reflect all prepaid and deferred items. The security deposit asset must reflect the reconciled cash balance held, and the liability should include accrued interest. A separate Balance Sheet should be included for a master tenant, if appropriate. The VHDA Balance Sheet is required (Appendix A, A-3, pages A-7 and A-8). Note: Mortgagor/Grantee entity related entries must be detailed separately from those of the development(s). (Appendix A, A-3, pages A-7 and A-8).

5. Statement of Profit And Loss. This form must be submitted

electronically using the form and instructions found at http://www.vhda.com/BusinessPartners/PropertyOwnersManag ers/MFLoanServicing/Pages/MFAuditGuide.aspx. A separate Statement of Profit and Loss should be included for a master tenant, if appropriate. The VHDA Statement of Profit and Loss is required (Appendix A, A-4, pages A-10 through A-11). Note: Statement of Profit and Loss account numbers and titles must not be altered.

14 of 22

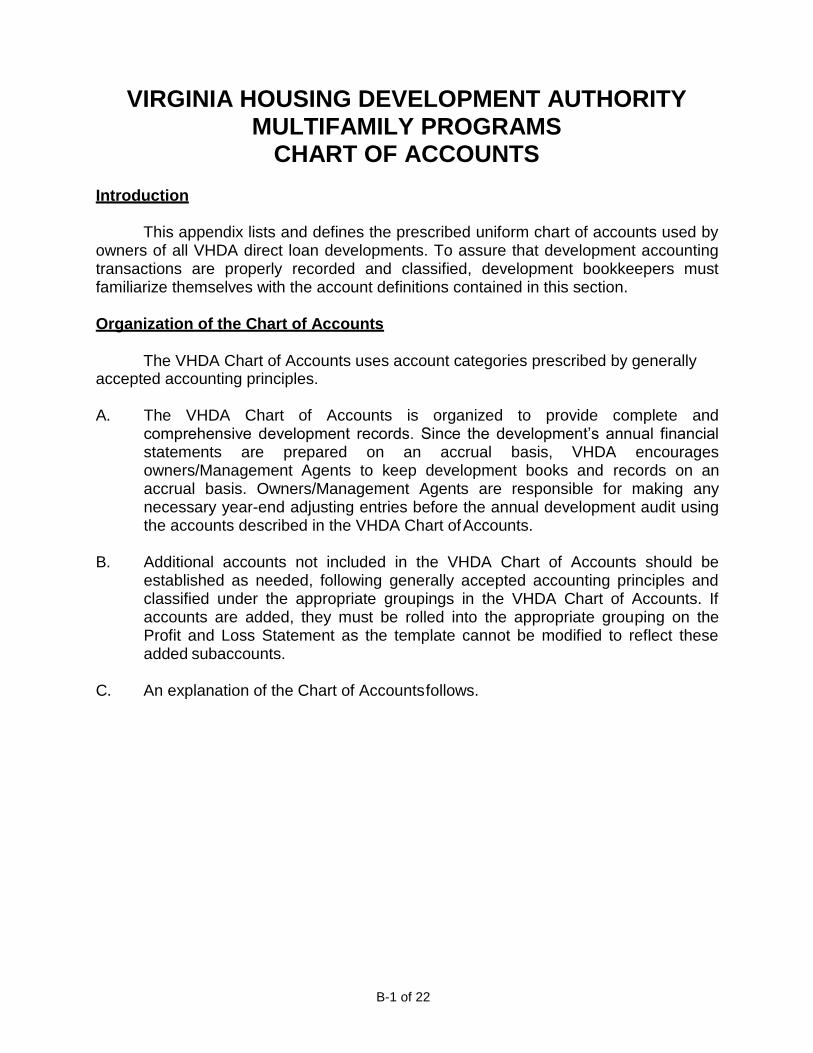

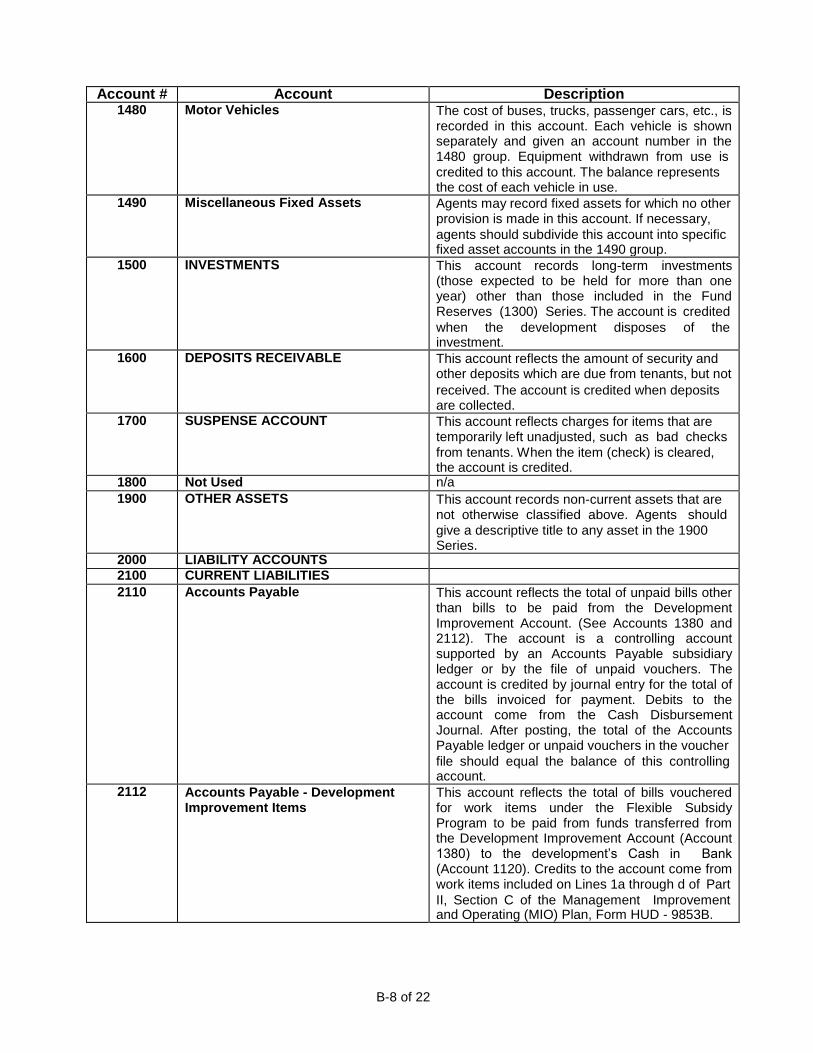

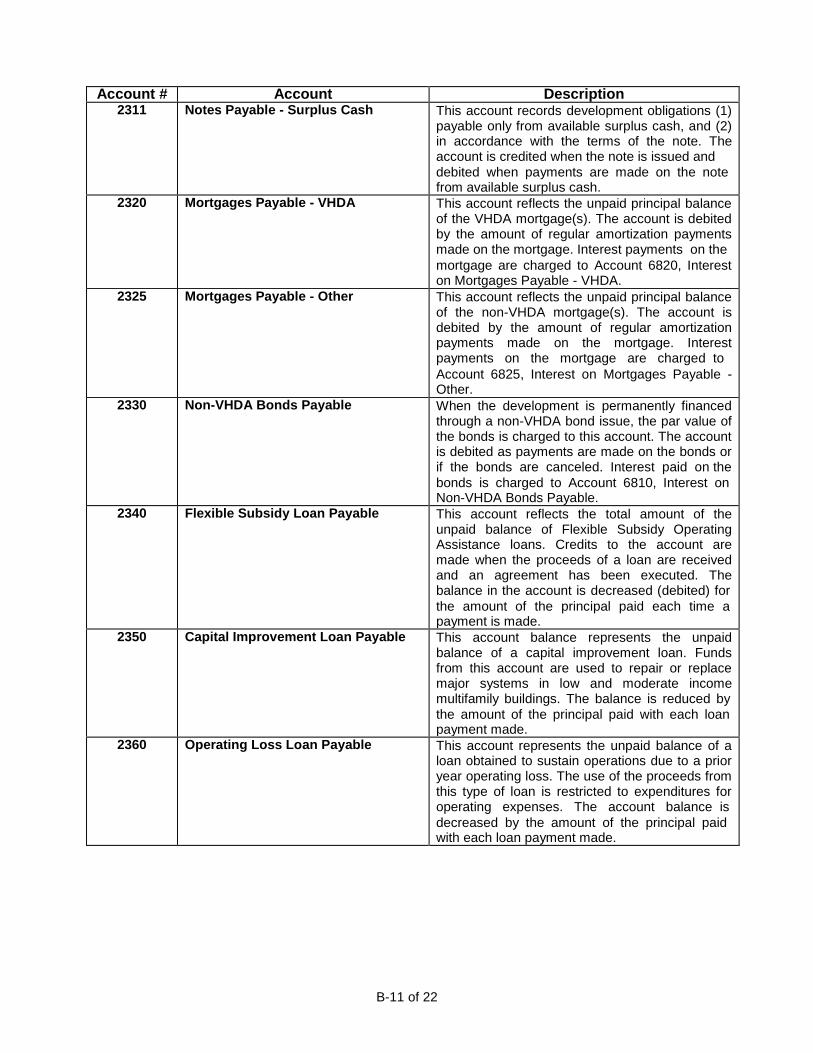

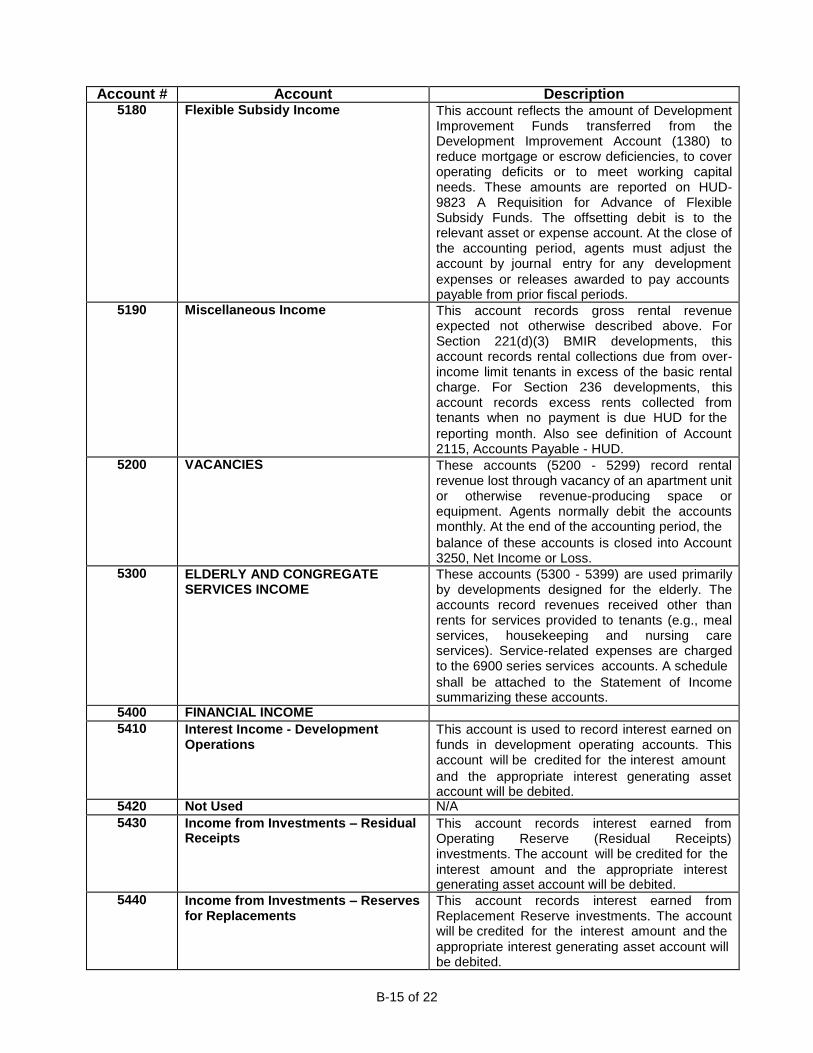

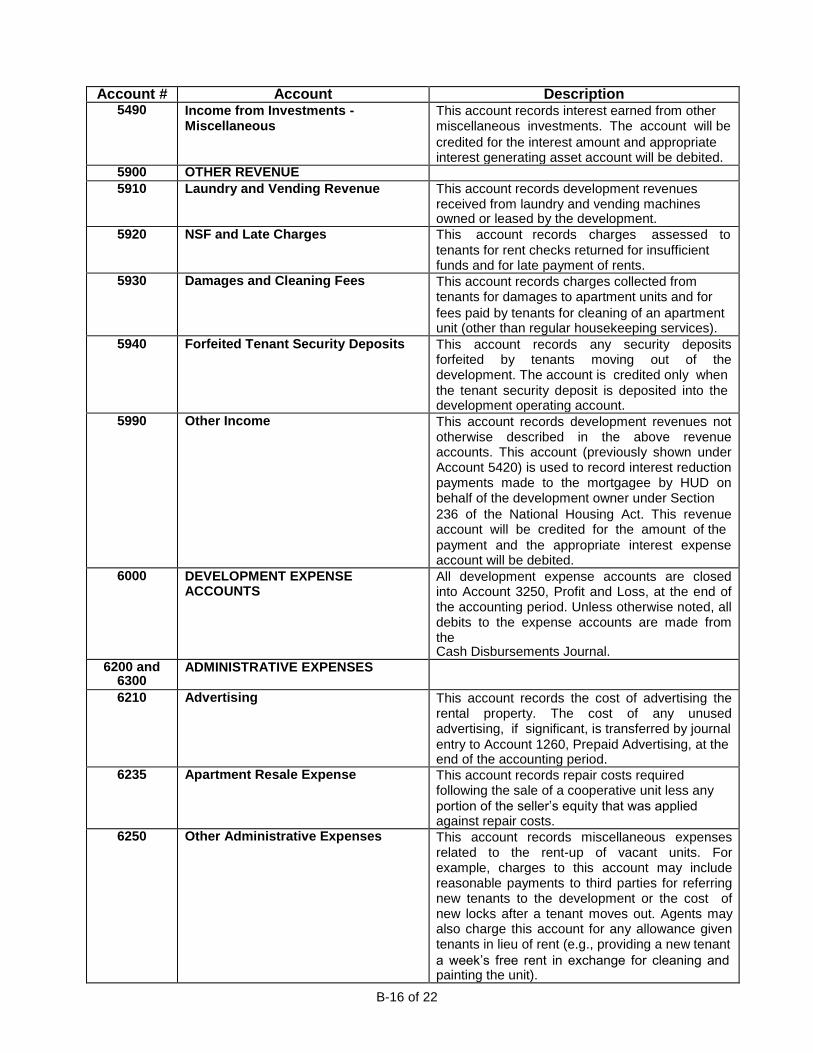

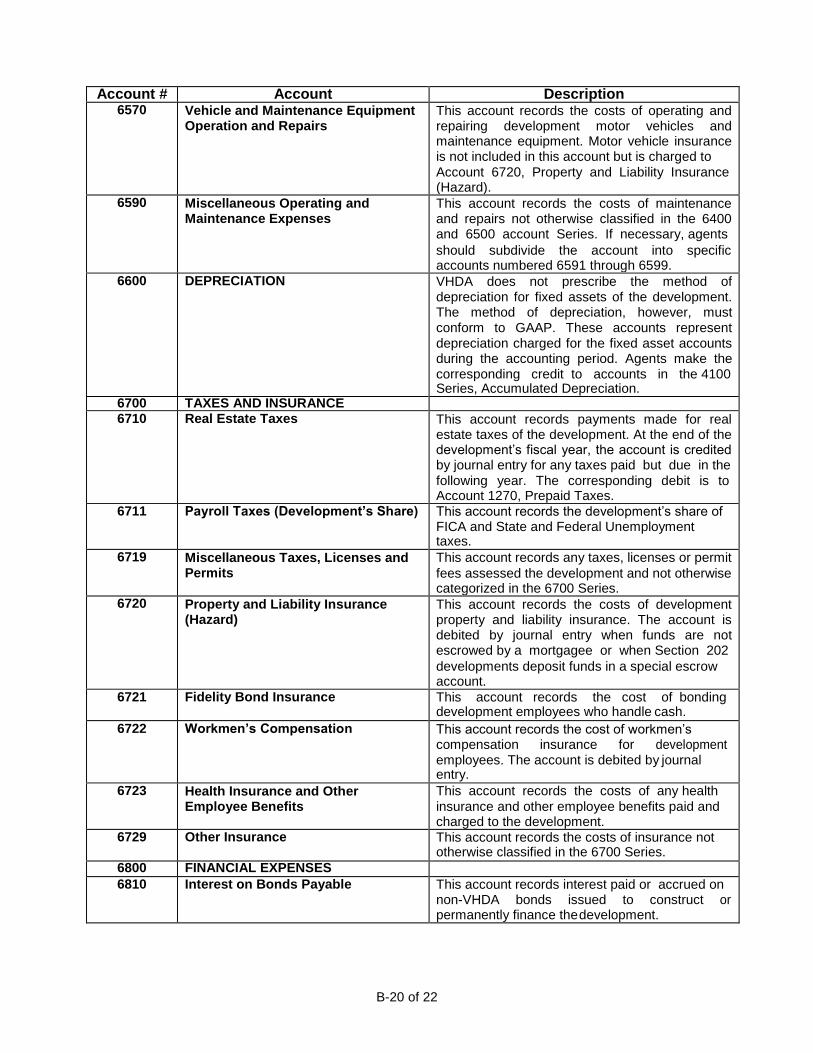

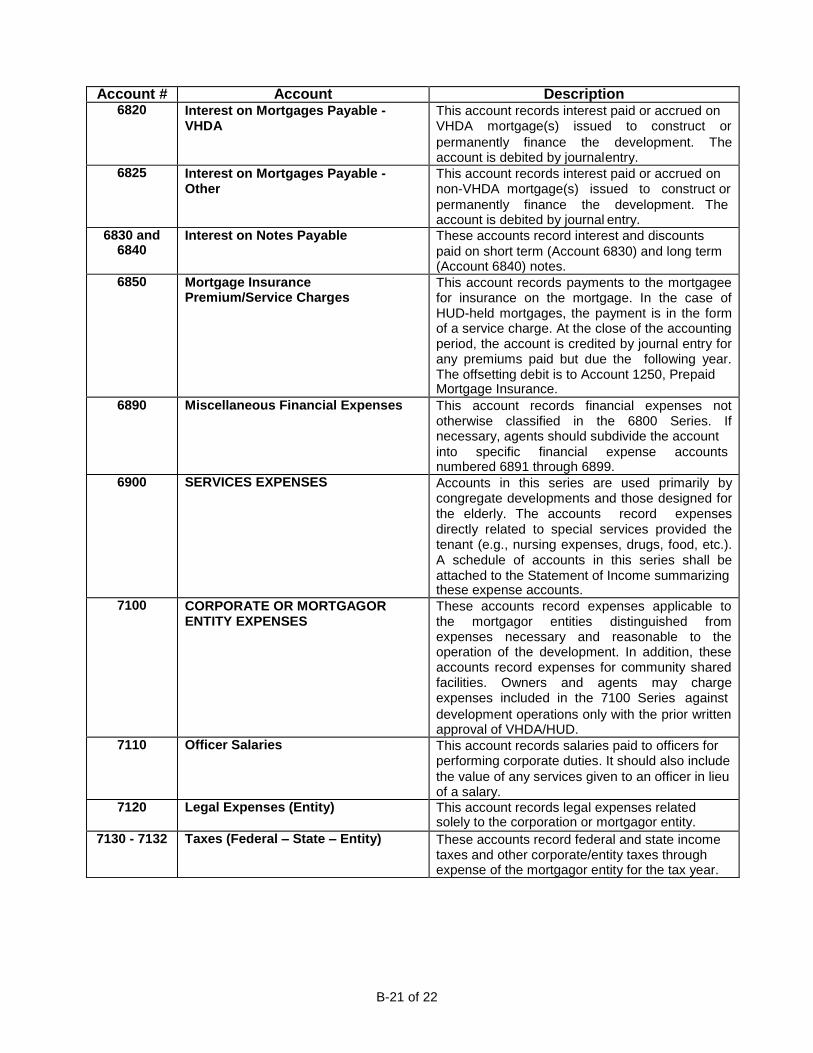

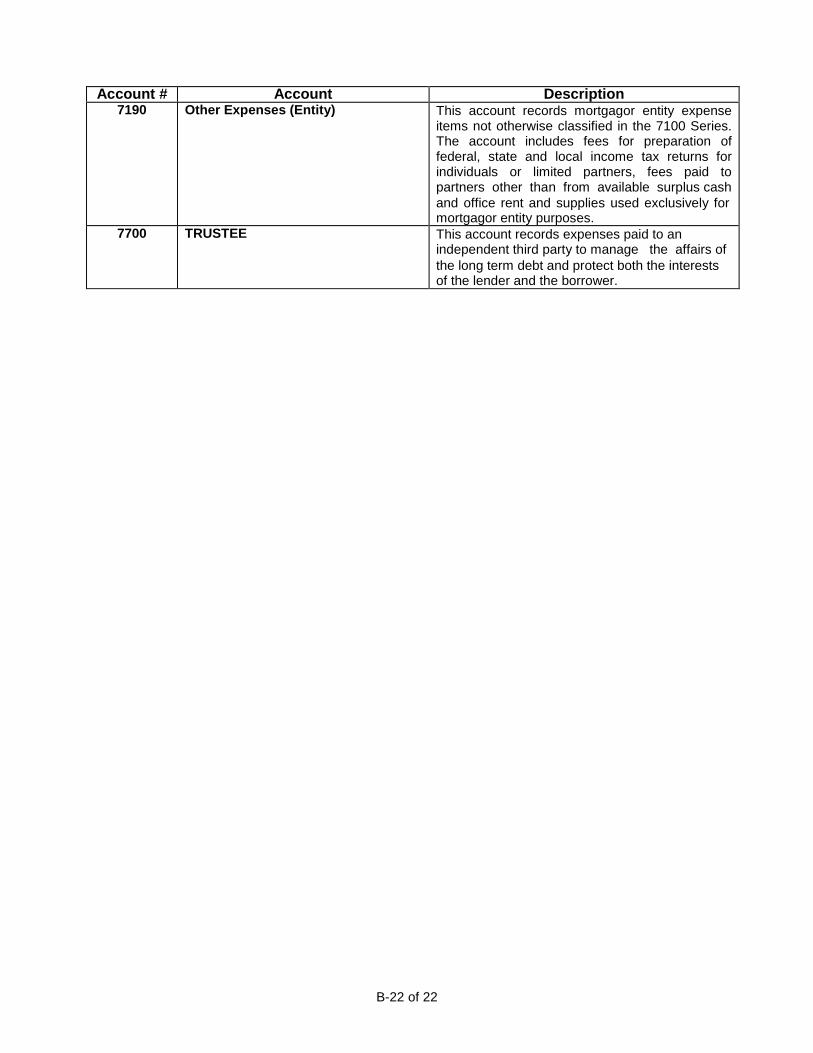

Appendix B provides descriptive information on VHDA’s prescribed chart of accounts. Note: VHDA has not adopted the revised HUD Chart of Accounts.

The Statement of Profit and Loss must conform to the following requirements:

a. It must be on an accrual basis.

b. It must show total rent revenue potential less vacancies and concessions for both residential units and commercial space(s) to arrive at a net rental income. Net rental income should not include “loss to old leases” or “street rent” vs. actual rent per lease agreement. On Section 8 developments, vacancy loss should be net of vacancy payments made by VHDA. Utility allowances received from VHDA must not be reflected as either an income or expense on the Statement of Profit and Loss. All other income (Account 5990) items must be identified as to type or source if they exceed the account groupings by 10% or more.

c. Any apartments or commercial space occupied but not

producing income must be shown as an expense under the applicable expense classification. Supporting information that identifies such occupants and their connection with the development(s) should be included in the Notes or Other VHDA Information. If no such expense applies, it should be so indicated on the statement.

d. Concessions must be reflected in Account 5280.

e. Any expenses reported as salaries or other compensa- tion to supervisory or administrative employees, officers, directors or stockholders of the Mortgagor/Grantee or Management Agent must be supported by a schedule showing duties and salaries paid.

f. Any receipts from charges for facilities or services other than reimbursement for breakage or damage by tenants must be scheduled if they exceed the account groupings by 10% or more.

15 of 22

g. Amortization expenses related to organizational costs, including loan fees, organizational expenses, etc. must be reflected in Account 6600 rather than Account 6890.

h. All monthly payments required to the Replacement, Operating, and/or Miscellaneous reserves should be shown on Part II, 2. Residual Receipts deposits should be excluded.

i. As the Statement of Profit and Loss is prepared on an accrual basis, items expensed on Part II, 3 should be for those incurred during the year covered by the financial statement. Reimbursements for prior periods (even if paid during the audit year) should be excluded.

j. If a multi-year audit is presented, two Statements of Profit and Loss must be included.

k. Mortgagor/Grantee entity related items can only be

reflected in the 7100 accounts on the Statement of Profit and Loss.

6. Statement Of Changes In Owner's Equity. This should include an explanation of changes in the account other than profit or loss for the operating period. (Appendix A, A-5, page A-12).

7. Statement Of Cash Flows. This statement must be presented using the direct method and must include the reconciled cash at the beginning and the end of the year. Changes in cash flows must differentiate between operating and Mortgagor/Grantee- related activities. Beginning and ending balances for operating and mortgagor entity accounts must be detailed in the Cash and Cash Equivalents portion of the statement. A separate Statement of Cash Flows should be included for a master tenant, if appropriate. The VHDA Statement of Cash Flows is required (include two if multi-year audit) (Appendix A, A-6, pages A-14 and A-15). If a facsimile format is used, it must be identical to the VHDA template. Note: Mortgagor entity distributions and/or contributions must be reflected in the Cash Flows from Financing Activities section on the Statement of Cash Flows. (Appendix A, A-6, pages A-14 and A-15).

8. Notes To Financial Statements. A suggested format is given in the sample report (Appendix A, A-7, pages A-16 and A-17). The notes must address the development(s), program(s), number of units, DHCD/HUD/VHDA relationship, all identity of

16 of 22

interest/related party transactions, maximum distribution, surplus cash, undistributed amount and cumulative distributable to date, handling of depreciation, and loan costs. Funds moved from operating to mortgagor entity accounts are considered distributions and should be reflected in the notes. All notes payable should be covered, including those to VHDA/DHCD (the mortgagee/grantor), to other mortgagees, if any, to the Mortgagor/Grantee entity and to the management company and the method of repayment. A distinction must be made between obligations incurred against syndication proceeds/mortgagor entity advances and those due from development(s) operating funds. The auditor must consider the effect of risks and uncertainties on the financial statement presentation in the notes.

A list should be included of all related parties and/or identity-of- interest companies (per definition cited on page 11 of the VHDA Audit Guide) that have provided, during the last year, labor, materials or services to the development(s). The schedule should include the related firm, the amount paid under contract, and the nature of the contracted business.

Identification of and details relating to a Master Tenant must be specified. Sufficient documentation must be provided to allow an assessment of the financial aspects of the development’s operations.

A list should be included of all commercial tenants and master leases. The tenant, the service provided, and the lease term should be specified for master leases.

The Mortgagor/Grantee and Management Agent have agreed to obtain contract materials, supplies and services at the best possible cost and on the terms most advantageous to the development(s) and to secure and credit to the development(s) all discounts, rebates or commissions obtainable with respect to purchases, service contracts and other transactions on behalf of the development(s). The Mortgagor/Grantee and the Management Agent have agreed that all goods and services purchased from individuals or companies having a related party and/or an identity-of-interest with the Agent, Mortgagor/Grantee or Management Agent should be purchased at costs not in excess of those that would be incurred in making arms-length purchases on the open market.

When required by the loan documents, the Management Agent should have solicited written cost estimates (i.e., bids) from at

17 of 22

least three contractors or suppliers for any work and/or contract, ongoing supply or service arrangement in accordance with the provisions of the Management Agreement. The Management Agent agreed to accept the bid that represented the best price, taking into consideration the bidder's reputation for quality of workmanship or materials and timely performance, and the time frame within which the goods or service was needed. For any contract, ongoing supply or service arrangement obtainable from more than one source, the Management Agent should have solicited oral or written cost estimates, as necessary to assure that the development(s) was obtaining services, supplies and purchases at the best possible cost in accordance with the provisions of the Management Agreement. The Management Agent must have a written record of any oral estimate obtained.

Copies of all required bids and documentation of all other written or oral cost comparisons made by the Management Agent should have been made part of the records of the development(s) and should be retained for three years from the date the work was completed. This documentation is subject to inspection by VHDA, and the Management Agent has agreed to submit such documentation upon request

9. Other VHDA Information. Other VHDA information in the form of explanatory comments or appropriate schedules (Appendix A, A-8, pages A-18 through A-36) must include the following:

a. Accrued Expenses - A statement should be

attached supporting any accrued expenses shown, including description, date(s) due, and amount(s) accrued (separated by development(s) and mortgagor entity). (Appendix A, A-8, Other VHDA Information, page A-18).

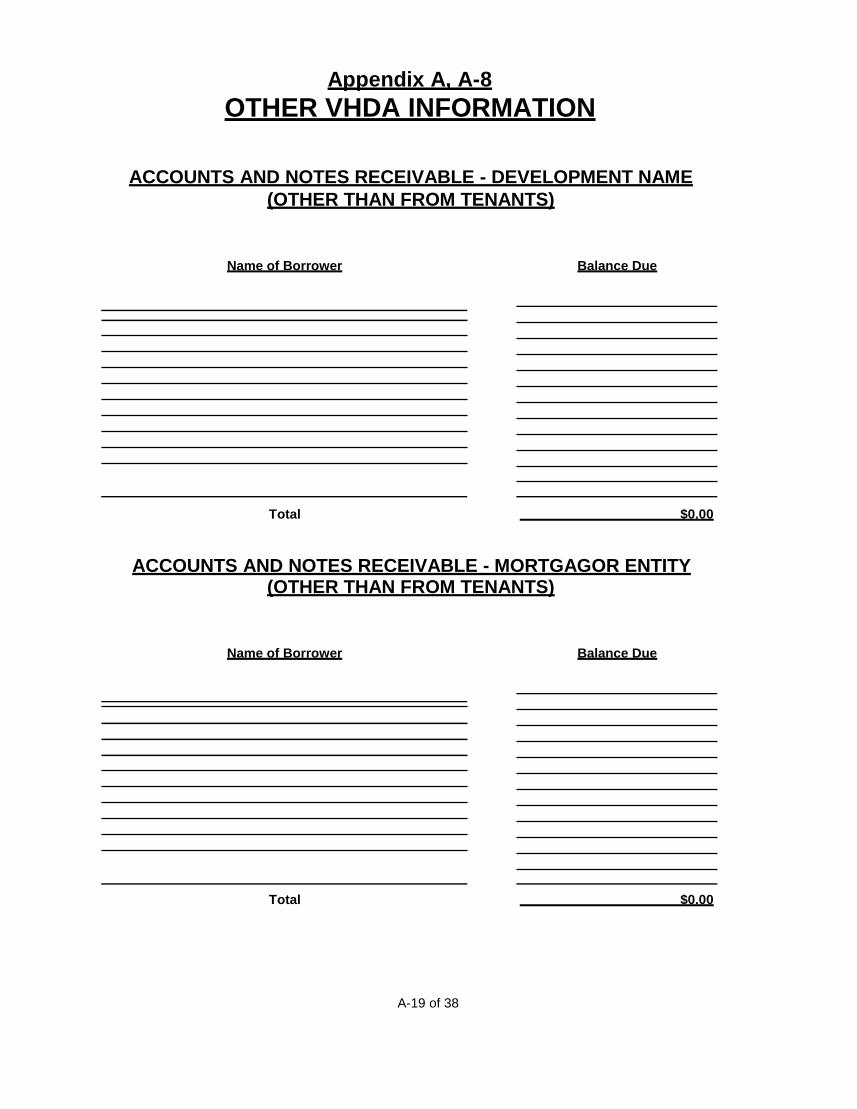

b. Accounts And Notes Receivable (Other Than From Tenants) - A complete detailed analysis should be included of any accounts or notes receivable other than tenant accounts, including name of borrower and balance due. Receivables due to the development(s) must be separate from those due to the mortgagor/grantee. (Appendix A, A-8, Other VHDA Information, page A-19).

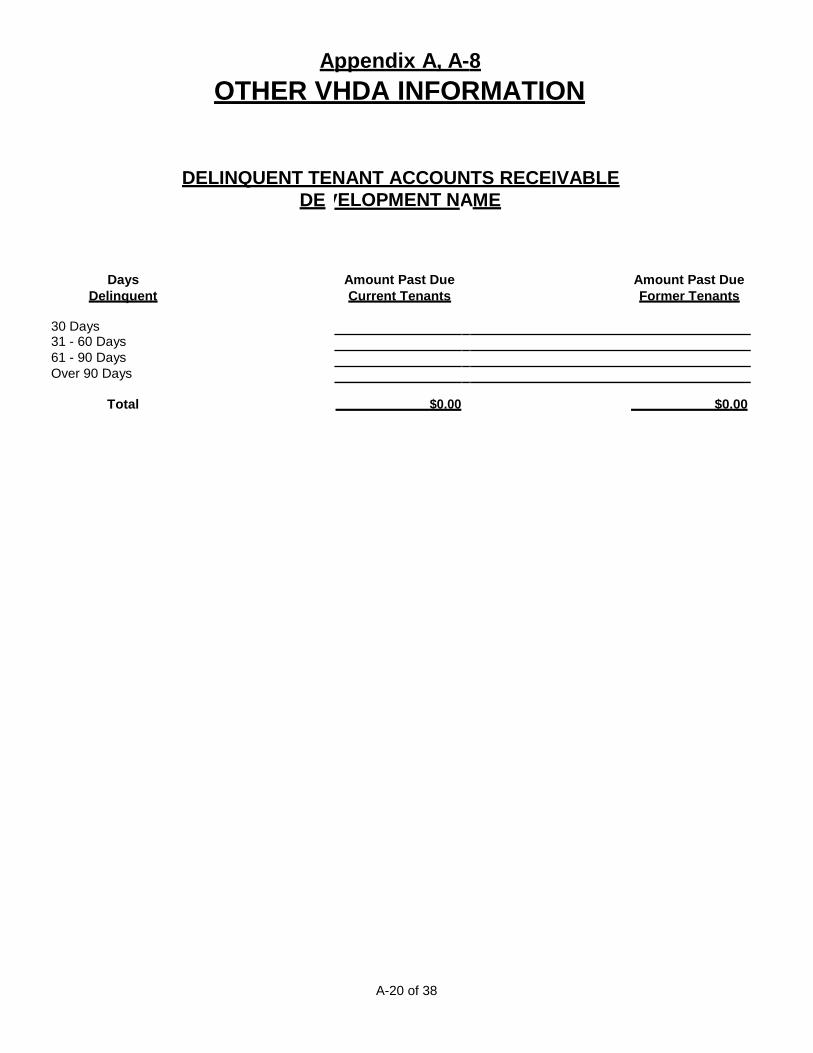

c. Delinquent Tenant Accounts Receivable - A summary analysis should be made of delinquent tenant accounts, segregated by current and former

18 of 22

tenants. This should include the amounts delinquent for 30 days, 31-60 days, 61-90 days and over 90 days. (Appendix A, A-8, Other VHDA Information, page A-20).

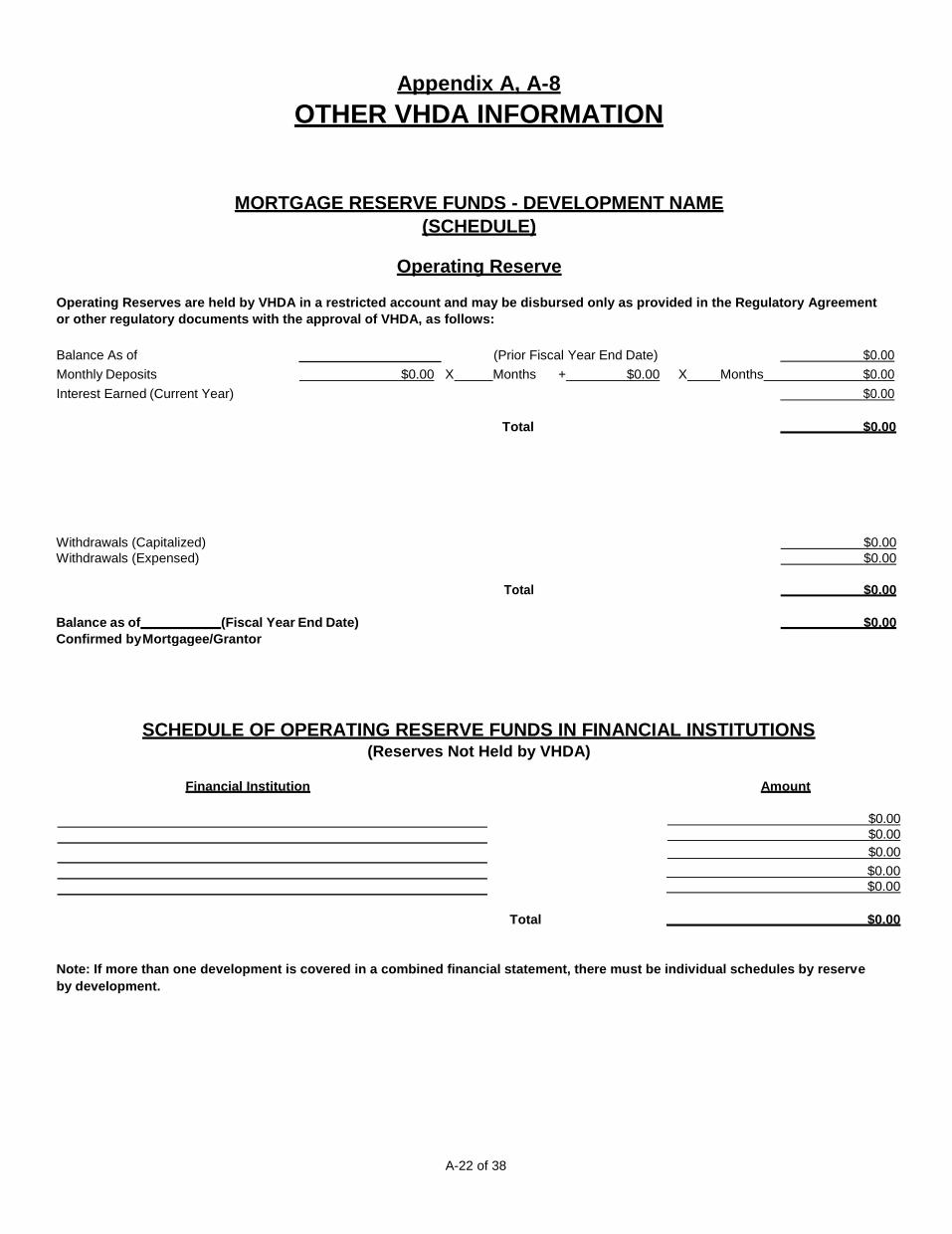

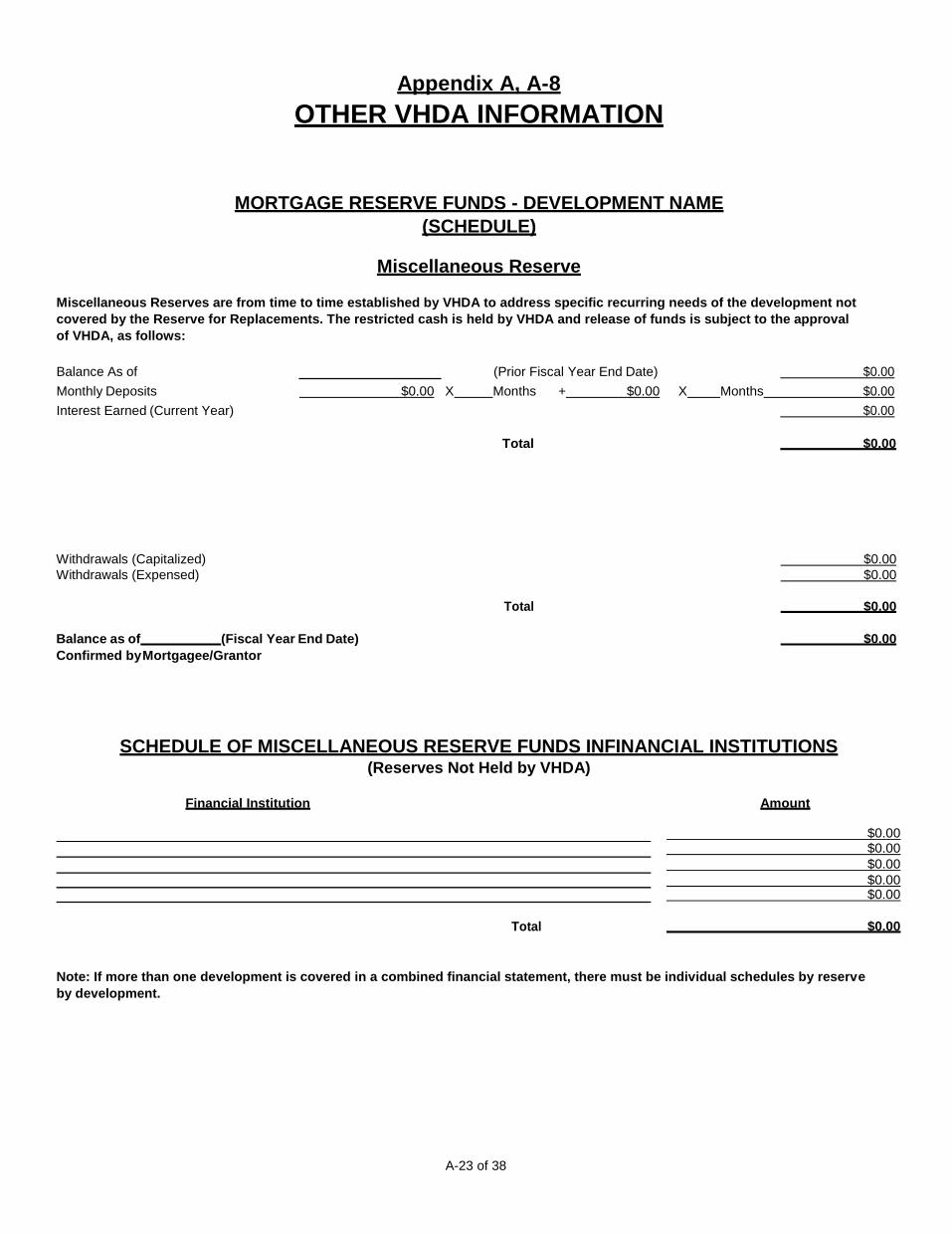

d. Mortgage Reserve Funds Schedules (Replacement, Operating, Miscellaneous and Development-Held) - An analysis (Appendix A, A-8, Other VHDA Information, pages A-21 through A-24) should be made of all required reserve funds including the following:

(1) A statement as to any payments required to the account. If establishment of more than one fund is required, a separate statement must be submitted for each fund. If more than one development is covered in a combined financial statement, there must be individual schedules by reserve per development;

(2) A statement as to interest earned on the reserve during the audit year;

(3) A statement of total withdrawals per

reserve account during the year. The withdrawals must be grouped by those capitalized (as shown on the Changes in Fixed Asset Accounts Report, Appendix A, A-8, Other VHDA Information, page A-26), and those expensed; and

(4) Investment details on reserves not maintained by VHDA must be scheduled including depository and amount. The investment schedule is not required for funds held by VHDA. Confirmation of balances and account activity for reserve funds held by VHDA are available to multifamily customers from VHDA’s online Borrower Inquiry application at https://vhd.mfsasp.com/BorrowerInquiry Web/common/login.jsp.

e. Schedule Of Funds In Financial Institutions - A schedule specifying the financial institution name and account balance must be included in the statement.

19 of 22

Operating and mortgagor entity accounts must be segregated and detailed separately. The year end balance(s) must be the reconciled amount(s). Note: Do not include escrow and reserve funds maintained by VHDA. (Appendix A, A-8, Other VHDA Information, page A-25).

f. Changes In Fixed Asset Accounts - A schedule should be included showing full details and explanations of any changes in fixed asset accounts. (Appendix A, A-8, Other VHDA Information, page A- 26).

g. Accounts Payable (Other Than Trade Creditors & Trade Creditors) - A list of other than trade accounts payable, segregated by those payable within 30 days and more than 30 days must be included. The list should segregate those due to the Mortgagor/Grantee entity, Management Agent, and Others. The amount of accounts payable at least 30 days past due should be specified. Accrued expenses should be shown separately from accounts payable. (Appendix A, A-8, Other VHDA Information, page A-27).

A list of trade accounts payable, segregated by those payable within 30 days and more than 30 days must be included. The amount of accounts payable at least 30 days past due should be specified. Accrued expenses should be shown separately from accounts payable. The list should segregate those payables incurred by the development(s) from those of the Mortgagor/Grantee entity. Note: Any trade creditors that have an identity-of-interest with the Mortgagor/Grantee and/or Management Agent must be identified in the Notes. (Appendix A, A-8, Other VHDA Information, page A-27).

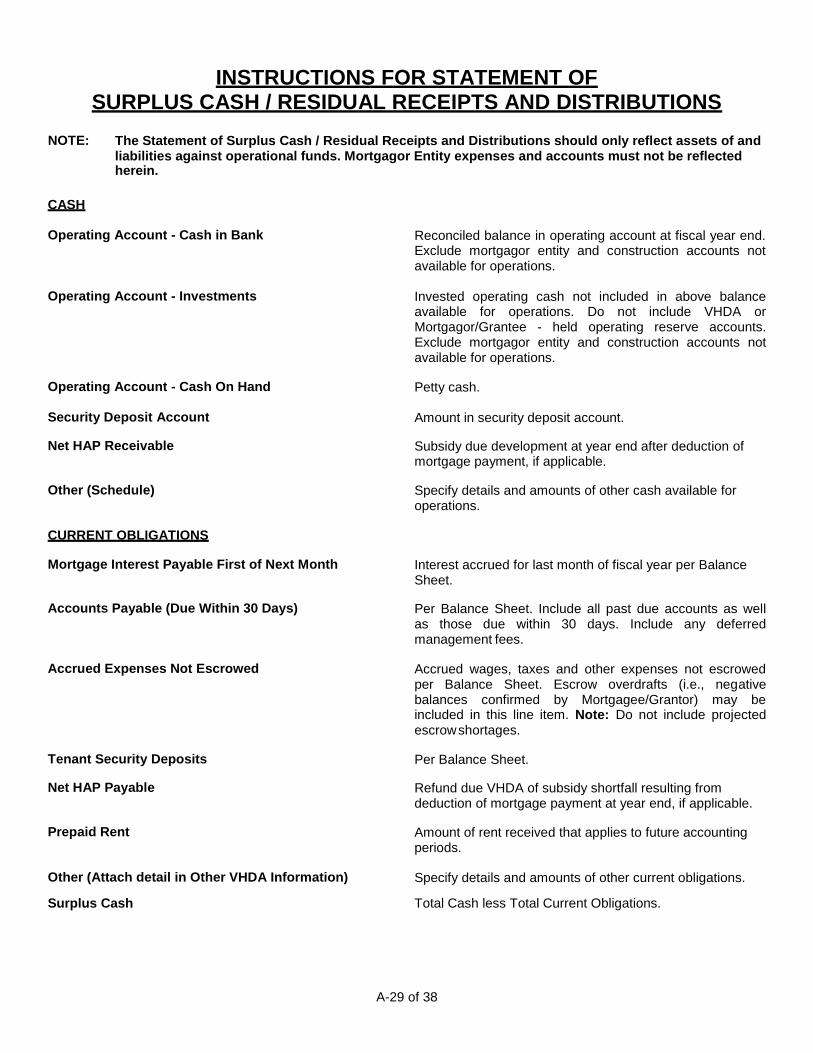

h. Statement Of Surplus Cash / Residual Receipts

and Distributions - A computation in the format shown in the sample statement (Appendix A, A-8, Other VHDA Information, page A-28) showing the amount of surplus cash at the end of the fiscal year, a tabulation of limited distribution payments paid and unpaid, distributions allowed per the regulatory documents and any remaining funds (i.e., Residual Receipts) to be deposited to the Operating Reserve

20 of 22

account, if applicable, is required. Note: Residual Receipts deposits should not be included with the financial statements submission. Deposits are due to VHDA within thirty days after the mortgagee’s written request for such deposit.

Note: Statement of Surplus Cash / Residual Receipts and Distributions (Appendix A, A-8, Other VHDA Information, page A-28) must be used. Instructions (Appendix A, A-8. Other VHDA Information, pages A- 29 and A-30) are attached to the sample form. Do not use HUD Form 93486, Computation of Surplus Cash, Distributions and Residual Receipts, unless the development(s) is HUD-Insured.

i. Unauthorized Distribution Of Development Revenue - If any unauthorized distribution of development(s) revenue is revealed during the audit, a separate schedule must be prepared detailing the amounts involved, date of distributions, and any other relevant information.

j. Ownership Entity - Full details should be included in the initial report concerning the issuance of all stock and/or investments including names of stockholders or investors, proportionate interest of each and whatever consideration is received by corporate or non-corporate developments (considerations should be itemized to show amount of cash, land, services, etc.). Initially, a list should be furnished by the mortgagor/grantee entity consisting of officers, directors and individuals having a financial interest in the development(s). Thereafter, as required by the Regulatory Agreement and/or other loan/grant documents, details should be furnished of any changes in ownership interests and/or positions occurring during the year. Generally, changes in ownership interests would involve any sale, transfer, assignment or substitution of limited partnership interests which in any twelve month period constitute in the aggregate 50% or more of the partnership interests in the Mortgagor/Grantee (the foregoing shall include any sale, transfer, assignment or substitution of ownership interests in any limited partner in the Mortgagor which in any twelve month period constitute in the aggregate 50%

21 of 22

or more of the ownership interests in such limited partner). Note: If no changes have occurred, it should be so noted. (Appendix A, A-8, Other VHDA Information, page A-31).

k. Identification Of Engagement Auditor - A statement specifying the name, mailing address, telephone and fax numbers, and email address of the lead auditor on the engagement must be included in the statements. This contact should be the individual to whom questions on the report can be addressed. (Appendix A, A-8, Other VHDA Information, page A-32).

l. Audit Compliance And Internal Control Questionnaire - The questionnaire shown in Appendix A, A-8, Other VHDA Information, pages A- 33 through A-36, must be completed and must be included in all financial statements submitted to VHDA. The decision who will complete the document is left to the mortgagor/grantee and his/her auditor. If completed by the agent, Management must certify to the completeness and accuracy of the questionnaire in the Management Agent Certification, Appendix A, A-1b. As “no” responses in the questionnaire may be indicative of an adverse condition, management’s plan of action to address such conditions must be included in the Corrective Action Plan, Appendix A, A- 9, pages 37 – 38. Note: Language used in the questionnaire must not be altered.

m. Other - Comments on, and explanations of, all other

Balance Sheet items not fully explained by the title of the account should be a part of the report.

10. Internal Control and Compliance. See pages 8 and 9 of the VHDA Audit Guide. In order to comply with Government Auditing Standards, reports in addition to those specified in this Audit Guide may be required. In addition, a recommended format for use by the Mortgagor/Grantee in completing a Corrective Action Plan, if necessary, is included in Appendix A, A-9, pages A-37 and A-38. Auditors should exercise professional judgment in tailoring their reports to the circumstances of individual audits. VHDA’s Compliance and Internal Control Questionnaire (Appendix A, A-8, Other VHDA Information, pages A-33 through A-36) must be included with all audited financial statements submitted to VHDA.

22 of 22

11. Auditor's Certification. The auditor may be requested by VHDA to justify any material departure from the language in Appendix A, A-2, Independent Auditor’s Report.

APPENDICES

APPENDIX A SAMPLE AUDITED FINANCIAL STATEMENTS

A-1 of 38

MORTGAGOR/GRANTEE ENTITY

t/a DEVELOPMENT NAME(S)

VHDA / DHCD NUMBER(S)

FINANCIAL STATEMENTS

DATE

XYZ and Company

Certified Public Accountants

A-2 of 38

Appendix A, A-1a

MORTGAGOR/GRANTEE CERTIFICATION

We hereby certify that we have examined the accompanying financial statements and other VHDA information of (Mortgagor/Grantee Entity), and to the best of our knowledge and belief, the same is complete and accurate. Additionally, we certify that no additions, deletions, and/or changes were made to the electronically submitted formats for the VHDA Balance Sheet and Statement of Profit and Loss.

There were changes in ownership during the year ended as noted in Other VHDA Information, Ownership Entity.

There were no changes in ownership during the year ended .

(MORTGAGOR/GRANTEE ENTITY)

BY:

Name

Title Date

Name

Title Date

Mortgagor/Grantee Employer/Taxpayer (EIN/TIN) Identification Number:

Mortgagor/Grantee Mailing Address:

Mortgagor/Grantee Telephone:

Mortgagor/Grantee Fax:

Mortgagor/Grantee E-Mail Address:

A-3 of 38

Appendix A, A-1b

MANAGEMENT AGENT CERTIFICATION

We hereby certify that we have examined the accompanying financial statements and other VHDA information of (Mortgagor/Grantee Entity), and to the best of our knowledge and belief, the same is complete and accurate. Additionally, any “No” answers on the Audit Compliance and Internal Control Questionnaire are detailed in the Corrective Action Plan.

(MANAGEMENT AGENT)

BY:

Name

Title Date

Management Agent Employer/Taxpayer (EIN/TIN) Identification Number:

Management Agent Mailing Address:

Management Agent Telephone:

Management Agent Fax:

Management Agent E-Mail Address:

A-4 of 38

Appendix A, A-2

REPORT ON AUDITED FINANCIAL STATEMENTS AND OTHER VHDA INFORMATION

Independent Auditor’s Report

To the Mortgagor/Grantee Entity Mortgagor/Grantee Address Anytown, USA

Virginia Housing Development Authority 601 South Belvidere Street Richmond, VA 23220

Report on the Financial Statements

We have audited the accompanying financial statements of (Mortgagor/Grantee Entity), VHDA / DHCD No(s). , which comprise the balance sheet as of (date), and the related statements of profit and loss, cash flows, and changes in owner’s equity for the year then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial

statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America, the standards applicable to financial audits contained in Government Auditing Standards (if applicable), issued by the Comptroller General of the United States, and the Virginia Housing Development Authority’s Mortgagor/Grantee’s Audit Guide (Guide). Those standards and the Guide require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence that we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

A-5 of 38

Report on Audited Financial Statements and Other VHDA Information

Page 2

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of (Mortgagor/Grantee Entity) as of (date), and the results of its operations, its cash flows, and its changes in owners’ equity for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Report on Other VHDA Information

Our audit was conducted for the purpose of forming an opinion on the financial statements as

a whole. The accompanying other information shown on pages to is presented for purposes of additional analysis as required by the Guide and the Consolidated Audit Guide for Audits of HUD Programs, issued by the U. S. Department of Housing and Urban Development, Office of the Inspector General (the Guides) and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole.

Report Issued in Accordance with Government Auditing Standards.

In accordance with Government Auditing Standards (if applicable), we have also issued a report(s) dated (date) on our consideration of (Mortgagor/Grantee Entity’s) internal control over financial reporting and on our test of its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. Also, in accordance with Government Auditing Standards (if applicable) and the Guides, we have also issued a report dated , on (Mortgagor/Grantee Entity’s) internal control over compliance and an opinion on its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters that could have a direct and material effect on a major HUD-assisted program (if applicable). Those reports are an integral part of an audit performed in accordance with Government Auditing Standards (if applicable) and the Guides in considering the entity’s internal control over financial reporting and compliance.

XYZ and Company Certified Public Accountants

Anytown, USA Date

A-6 of 38

Appendix A, A-3

BALANCE SHEET

Note: The VHDA Balance Sheet is accessible at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Pa ges/MFAuditGuide.aspx and is required to be emailed to the assigned Asset Manager. A paper copy must be included in the financial statements submission.

The template is available at: http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Pa

ges/MFAuditGuide.aspx

A-7 of 38 Form updated 03/25/2011 See Notes to Financial Statements

Appendix A, A-3

BALANCE SHEET

DEVELOPMENT NAME VHDA / DHCD NUMBER(S)

AS OF

A S S E T S

CURRENT ASSETS

Cash on Hand $ -

Cash in Bank $ -

Cash - Investments $ -

Cash - Mortgagor Entity $ -

Accounts Receivable - Tenant $ -

Accounts Receivable - Net HAP $ -

Accounts Receivable - Other $ -

Prepaid Expenses

Property Insurance $ -

Mortgage Insurance $ -

Taxes $ -

Miscellaneous (Attach detail in Other VHDA Information) $ - $ -

DEPOSITS HELD IN TRUST - FUNDED

Tenant Security Deposits $ -

Other Deposits $ - $ -

RESTRICTED DEPOSITS & FUNDED RESERVES

Mortgage Escrow Deposits (Attach detail in Other VHDA Information) $ -

Replacement Reserve $ -

Miscellaneous Reserve $ -

Operating/Residual Receipts Reserve $ -

Development-Held Reserve $ - $ -

FIXED ASSETS

Net Book Value

Land $ -

Land Improvements $ -

Buildings $ -

Equipment $ -

Furniture and Fixtures $ -

Other $ - $ -

OTHER ASSETS

(Attach detail in Other VHDA Information) $ - $ -

TOTAL ASSETS

$ -

A-8 of 38 Form updated 03/25/2011 See Notes to Financial Statements

Balance Sheet

Page 2

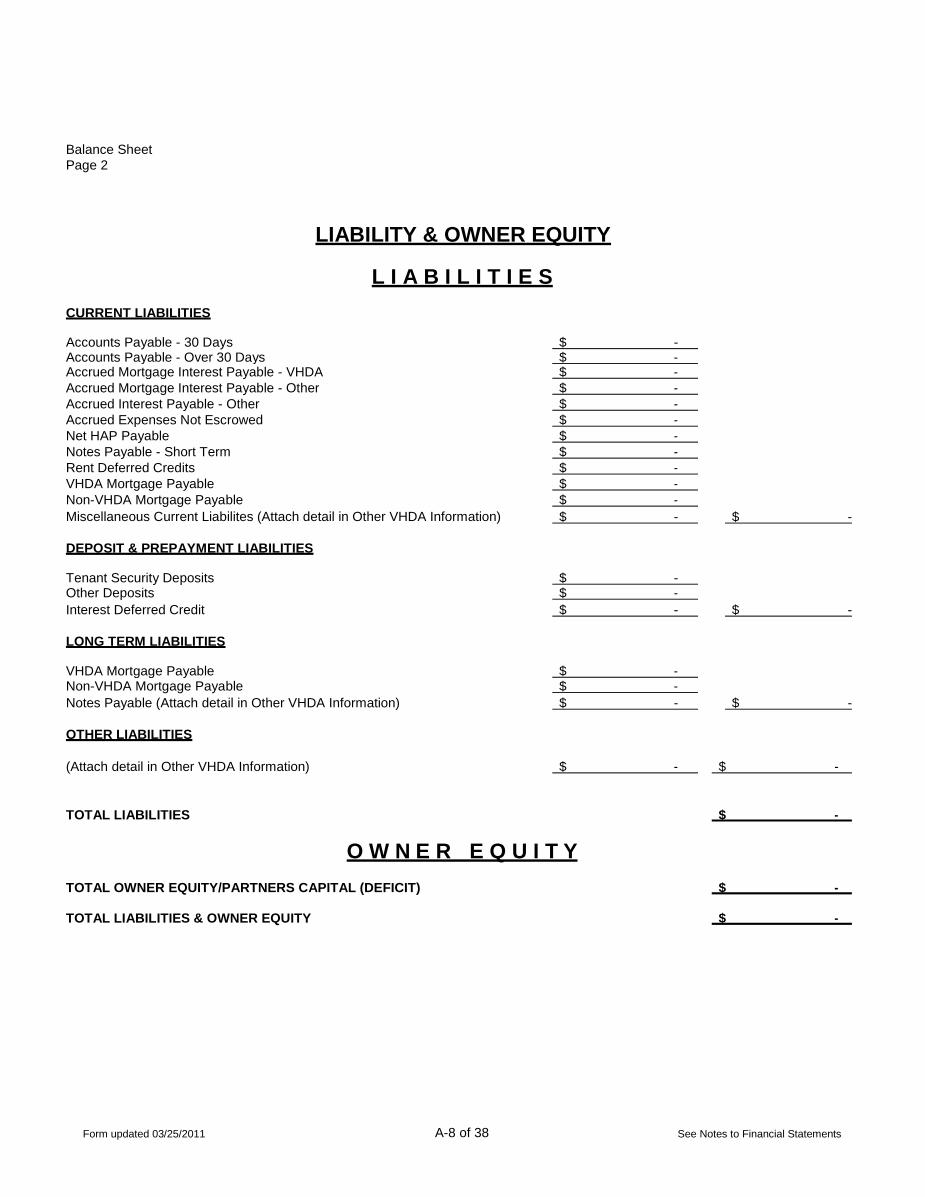

LIABILITY & OWNER EQUITY

L I A B I L I T I E S

CURRENT LIABILITIES

Accounts Payable - 30 Days $ -

Accounts Payable - Over 30 Days $ -

Accrued Mortgage Interest Payable - VHDA $ -

Accrued Mortgage Interest Payable - Other $ -

Accrued Interest Payable - Other $ -

Accrued Expenses Not Escrowed $ -

Net HAP Payable $ -

Notes Payable - Short Term $ -

Rent Deferred Credits $ -

VHDA Mortgage Payable $ -

Non-VHDA Mortgage Payable $ -

Miscellaneous Current Liabilites (Attach detail in Other VHDA Information) $ - $ -

DEPOSIT & PREPAYMENT LIABILITIES

Tenant Security Deposits $ -

Other Deposits $ -

Interest Deferred Credit $ - $ -

LONG TERM LIABILITIES

VHDA Mortgage Payable $ -

Non-VHDA Mortgage Payable $ -

Notes Payable (Attach detail in Other VHDA Information) $ - $ -

OTHER LIABILITIES

(Attach detail in Other VHDA Information) $ - $ -

TOTAL LIABILITIES

$ -

O W N E R E Q U I T Y

TOTAL OWNER EQUITY/PARTNERS CAPITAL (DEFICIT)

$ -

TOTAL LIABILITIES & OWNER EQUITY

$ -

Appendix A, A-4

STATEMENT OF PROFIT AND LOSS

Note: The VHDA Statement of Profit and Loss is accessible at http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Pa ges/MFAuditGuide.aspx and is required to be emailed to the assigned Asset Manager. A paper copy must be included in the financial statements submission.

The template is available at: http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServicing/Pa

ges/MFAuditGuide.aspx

A-9 of 38

A-10 of 38

Month/Period

VIRGINIA HOUSING DEVELOPMENT AUTHORITY

STATEMENT OF PROFIT AND LOSS

Beginning: Ending:

Development Name

VHDA/DHCD Numbers:

Part I Description of Account Acct. No. Amount

Apartments 5120 $ -

Tenant Assistance Payments 5121 $ -

Rental Furniture and Equipment 5130 $ -

Income Stores and Commercial 5140 $ -

5100 Garage and Parking Spaces 5170 $ -

Flexible Subsidy Income 5180 $ - Miscellaneous Income (attach detail in Other VHDA Information) 5190 $ -

Total Rental Income Potential at 100% Occupancy $ -

Apartments 5220 $ -

Furniture and Equipment 5230 $ -

Vacancies Stores and Commercial 5240 $ -

5200 Garage and Parking Spaces 5270 $ - Concessions 5280 $ -

Miscellaneous (attach detail in Other VHDA Information) 5290 $ -

Total Vacancies $ -

Net Rental Income - Rental Income Less Vacancies $ -

Elderly and Congregate Services Income -- 5300

5300

$ -

$ - Total Service Income (attach detail in Other VHDA Information)

Interest Income--Development Operations 5410 $ -

Financial Income from Investments--Residual Receipts 5430 $ -

Income Income from Investments--Reserve for Replacements 5440 $ -

5400 Income from Investments--Miscellaneous 5490 $ - Total Financial Income $ -

Laundry and Vending 5910 $ -

NSF and Late Charges 5920 $ -

Other Damages and Cleaning Fees 5930 $ -

Income Forfeited Tenant Security Deposits 5940 $ -

5900 Other Income (attach detail in Other VHDA Information) 5990 $ - Total Other Income $ -

Total Income $ -

Advertising 6210 $ -

Other Administrative Expenses 6250 $ -

Office Salaries 6310 $ -

Office Supplies 6311 $ - Office or Model Apartment Rent 6312 $ -

Administrative Management Fee 6320 $ -

Expenses Manager's or Superintendent's Salaries 6330 $ -

6200/6300 Manager's or Superintendent's Rent Free Unit 6331 $ -

Legal Expenses (Development) 6340 $ -

Auditing Expenses (Development) 6350 $ - Bookkeeping Fees/Accounting Services 6351 $ -

Telephone and Answering Service 6360 $ -

Bad Debts 6370 $ - Miscellaneous Administrative Expenses (attach detail in Other VHDA Information) 6390 $ -

Total Administrative Expenses $ -

Fuel Oil/Coal 6420 $ -

Utilities Electricity (Light and Miscellaneous Power) 6450 $ -

Expense Water 6451 $ -

6400 Gas 6452 $ - Sewer 6453 $ -

Total Utilities Expense $ -

A-11 of 38

Janitor and Cleaning Payroll 6510 $ -

Janitor and Cleaning Supplies 6515 $ -

Janitor and Cleaning Contract 6517 $ - Exterminating Payroll/Contract 6519 $ -

Exterminating Supplies 6520 $ -

Operating and Garbage and Trash Removal 6525 $ -

Maintenance Security Payroll/Contract 6530 $ -

Expenses Grounds Payroll 6535 $ -

6500 Grounds Supplies 6536 $ - Grounds Contract 6537 $ -

Repairs Payroll 6540 $ -

Repairs Materials 6541 $ - Repairs Contract 6542 $ -

Elevator Maintenance/Contract 6545 $ -

Heating/Cooling Repairs and Maintenance 6546 $ - Swimming Pool Maintenance/Contract 6547 $ -

Snow Removal 6548 $ -

Decorating Payroll/Contract 6560 $ - Decorating Supplies 6561 $ -

Vehicle and Maintenance Equipment Operation and Repairs 6570 $ -

Miscellaneous Operating and Maintenance Expenses 6590 $ - Total Operating and Maintenance Expenses $ -

Real Estate Taxes 6710 $ -

Payroll Taxes (Development's Share) 6711 $ - Miscellaneous Taxes, Licenses and Permits 6719 $ -

Taxes Property and Liability Insurance (Hazard) 6720 $ -

and Fidelity Bond Insurance 6721 $ -

Insurance Workmen's Compensation 6722 $ -

6700 Health Insurance and Other Employee Benefits 6723 $ -

Other Insurance (attach detail in Other VHDA Information) 6729 $ - Total Taxes and Insurance $ -

Interest on Bonds Payable 6810 $ -

Interest on Mortgages Payable - VHDA 6820 $ - Interest on Mortgages Payable - Other 6825 $ -

Financial Interest on Notes Payable (Short -Term) 6830 $ -

Expenses Interest on Notes Payable (Long -Term) 6840 $ -

6800 Mortgage Insurance Premium/Service Charges 6850 $ -

Miscellaneous Financial Expenses 6890 $ -

Total Financial Expenses $ -

Services Total Services Expenses (attach detail in Other VHDA Information) 6900 $ - $ -

Expenses Total Cost of Operations Before Depreciation $ -

6900 Profit (Loss) Before Depreciation $ -

Depreciation Depreciation (Total)---6600 6600 $ - $ -

6600 Operating Profit or (Loss) $ -

Officer Salaries 7110 $ -

Corporate or Legal Expenses (Entity) 7120 $ -

Mortgagor Taxes (Federal - State - Entity) 7130-32 $ -

Entity Other Expenses (Entity) 7190 $ -

Expenses Total Corporate Expenses $ -

7100 Net Profit or (Loss) $ -

Miscellaneous or Other Income and Expense Sub-account Groups. If Miscellaneous or Other Income and/or Expense Sub-accounts (5190, 5290, 5490, 5990,

6390, 6590, 6729, 6890 and 7190) exceed the Account Groupings by 10% or more, attach Other VHDA Information describing or explaining the Miscellaneous

Income or Expense.

Part II

1a. Total principal payments required under the VHDA mortgage(s), even if payments under a Workout Agreement are $ -

less or more than those required under the mortgage(s).

1b. Total principal payments required under non-VHDA mortgage(s), even if payments under a Workout Agreement are $ -

less or more than those required under the mortgage(s).

2. Replacement, Miscellaneous and Operating Reserve deposits required by the Regulatory Agreement or Amendments $ -

thereto, even if payments may be temporarily suspended or waived.

3. Replacement, Miscellaneous or Operating Reserve releases included as expense items on this Profit and Loss Statement. $ -

4. Development Improvement Reserve Releases under the Flexible Subsidy Program that are included as expense items on $ -

this Profit and Loss Statement.

Appendix A, A-5

STATEMENT OF CHANGES IN OWNER'S EQUITY

DEVELOPMENT NAME VHDA / DHCD NUMBER(S)

AS OF

Beginning of Year

$0.00

Add:

Net Income $0.00

Contributions $0.00

Other $0.00 $0.00

Deduct:

Distributions $0.00

End of Year

$0.00

See Notes to Financial Statements

A-12 of 38

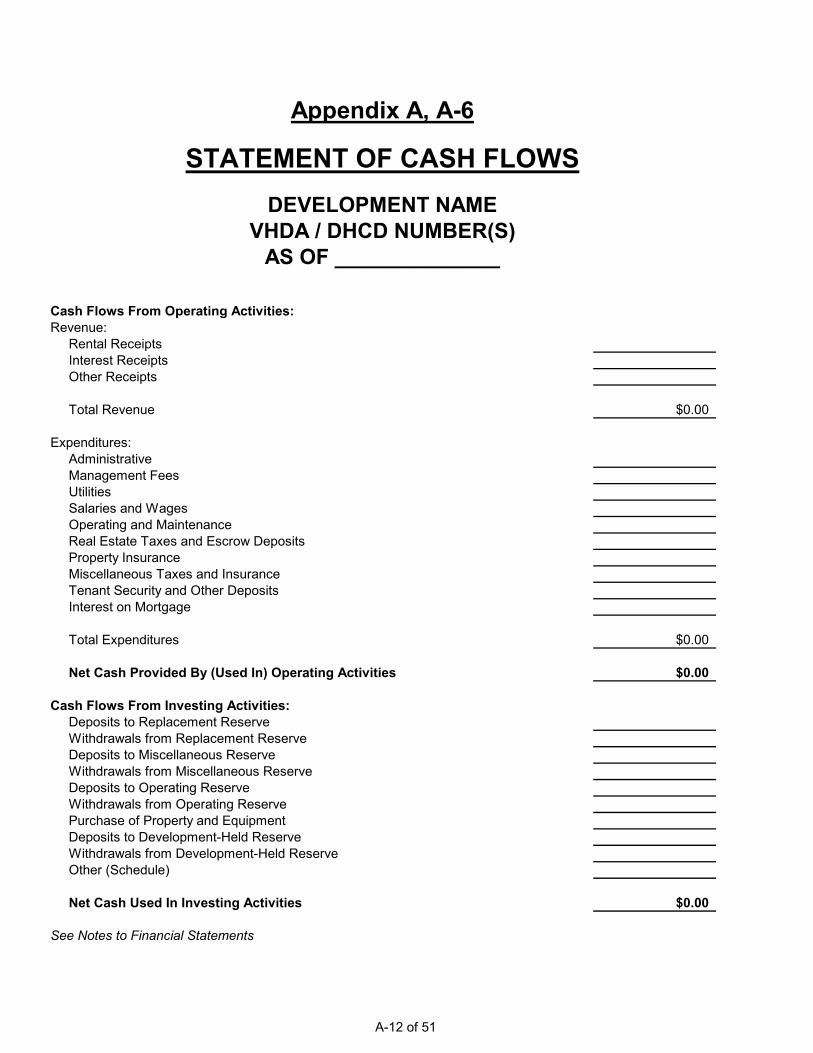

Appendix A, A-6

STATEMENT OF CASH FLOWS

Note: An identical facsimile format of the following document is required to be included in the audited financial statements.

The template is available at

http://www.vhda.com/BusinessPartners/PropertyOwnersManagers/MFLoanServi cing/Pages/MFAuditGuide.aspx

A-13 of 38

A-12 of 51

Appendix A, A-6

STATEMENT OF CASH FLOWSDEVELOPMENT NAME

VHDA / DHCD NUMBER(S)AS OF ______________

Cash Flows From Operating Activities:Revenue: Rental Receipts Interest Receipts Other Receipts

Total Revenue $0.00

Expenditures: Administrative Management Fees Utilities Salaries and Wages Operating and Maintenance Real Estate Taxes and Escrow Deposits Property Insurance Miscellaneous Taxes and Insurance Tenant Security and Other Deposits Interest on Mortgage

Total Expenditures $0.00

Net Cash Provided By (Used In) Operating Activities $0.00

Cash Flows From Investing Activities: Deposits to Replacement Reserve Withdrawals from Replacement Reserve Deposits to Miscellaneous Reserve Withdrawals from Miscellaneous Reserve Deposits to Operating Reserve Withdrawals from Operating Reserve Purchase of Property and Equipment Deposits to Development-Held Reserve Withdrawals from Development-Held Reserve Other (Schedule)

Net Cash Used In Investing Activities $0.00

See Notes to Financial Statements

A-13 of 51

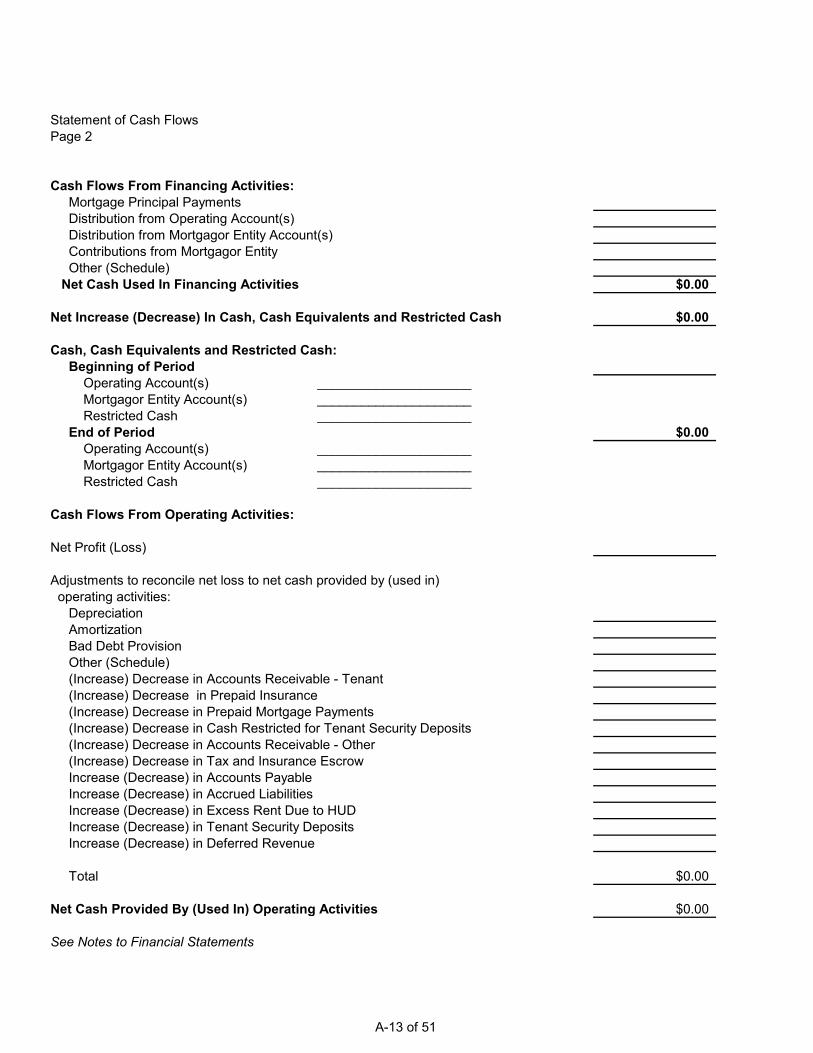

Statement of Cash FlowsPage 2

Cash Flows From Financing Activities: Mortgage Principal Payments Distribution from Operating Account(s) Distribution from Mortgagor Entity Account(s) Contributions from Mortgagor Entity Other (Schedule) Net Cash Used In Financing Activities $0.00

Net Increase (Decrease) In Cash, Cash Equivalents and Restricted Cash $0.00

Cash, Cash Equivalents and Restricted Cash: Beginning of Period Operating Account(s) _____________________ Mortgagor Entity Account(s) _____________________ Restricted Cash _____________________ End of Period $0.00 Operating Account(s) _____________________ Mortgagor Entity Account(s) _____________________ Restricted Cash _____________________

Cash Flows From Operating Activities:

Net Profit (Loss)

Adjustments to reconcile net loss to net cash provided by (used in) operating activities: Depreciation Amortization Bad Debt Provision Other (Schedule) (Increase) Decrease in Accounts Receivable - Tenant (Increase) Decrease in Prepaid Insurance (Increase) Decrease in Prepaid Mortgage Payments (Increase) Decrease in Cash Restricted for Tenant Security Deposits (Increase) Decrease in Accounts Receivable - Other (Increase) Decrease in Tax and Insurance Escrow Increase (Decrease) in Accounts Payable Increase (Decrease) in Accrued Liabilities Increase (Decrease) in Excess Rent Due to HUD Increase (Decrease) in Tenant Security Deposits Increase (Decrease) in Deferred Revenue

Total $0.00

Net Cash Provided By (Used In) Operating Activities $0.00

See Notes to Financial Statements

A-16 of 38

Appendix A, A-7

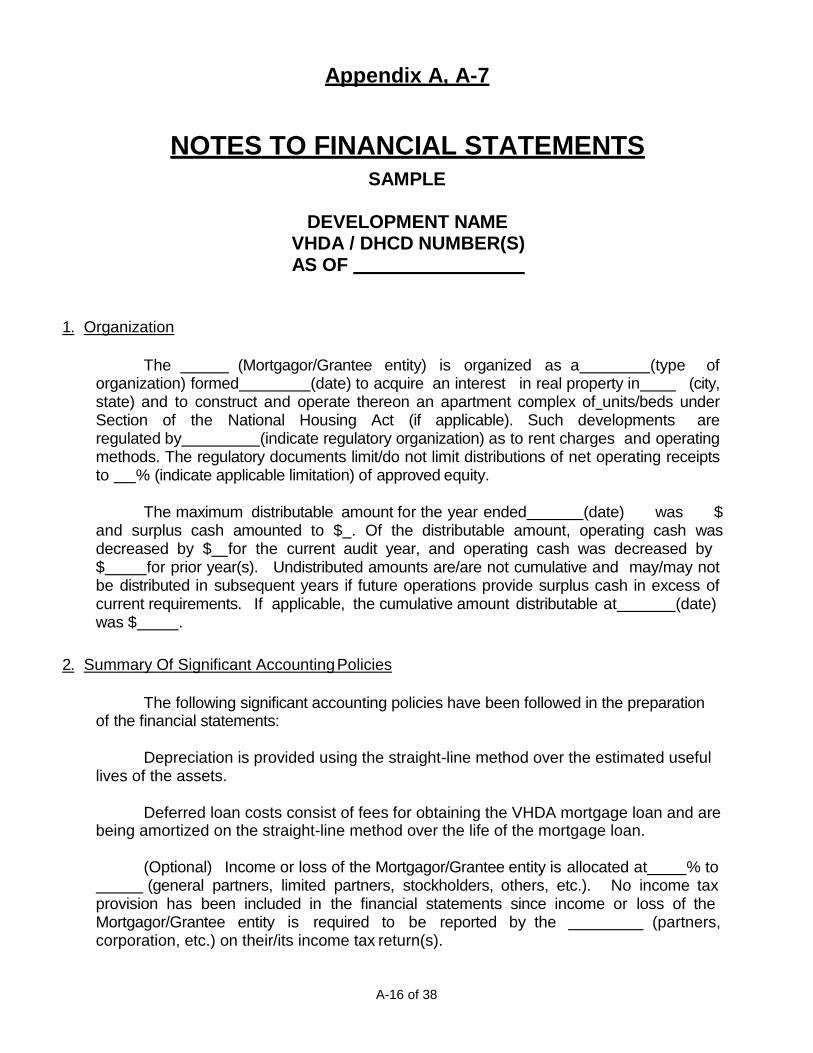

NOTES TO FINANCIAL STATEMENTS SAMPLE

DEVELOPMENT NAME VHDA / DHCD NUMBER(S) AS OF

1. Organization

The (Mortgagor/Grantee entity) is organized as a (type of organization) formed (date) to acquire an interest in real property in (city, state) and to construct and operate thereon an apartment complex of units/beds under Section of the National Housing Act (if applicable). Such developments are regulated by (indicate regulatory organization) as to rent charges and operating methods. The regulatory documents limit/do not limit distributions of net operating receipts to % (indicate applicable limitation) of approved equity.

The maximum distributable amount for the year ended (date) was $ and surplus cash amounted to $ . Of the distributable amount, operating cash was decreased by $ for the current audit year, and operating cash was decreased by $ for prior year(s). Undistributed amounts are/are not cumulative and may/may not be distributed in subsequent years if future operations provide surplus cash in excess of current requirements. If applicable, the cumulative amount distributable at (date) was $ .

2. Summary Of Significant Accounting Policies

The following significant accounting policies have been followed in the preparation of the financial statements:

Depreciation is provided using the straight-line method over the estimated useful lives of the assets.

Deferred loan costs consist of fees for obtaining the VHDA mortgage loan and are being amortized on the straight-line method over the life of the mortgage loan.

(Optional) Income or loss of the Mortgagor/Grantee entity is allocated at % to (general partners, limited partners, stockholders, others, etc.). No income tax

provision has been included in the financial statements since income or loss of the Mortgagor/Grantee entity is required to be reported by the corporation, etc.) on their/its income tax return(s).

(partners,

A-17 of 38

Notes To Financial Statements Page 2

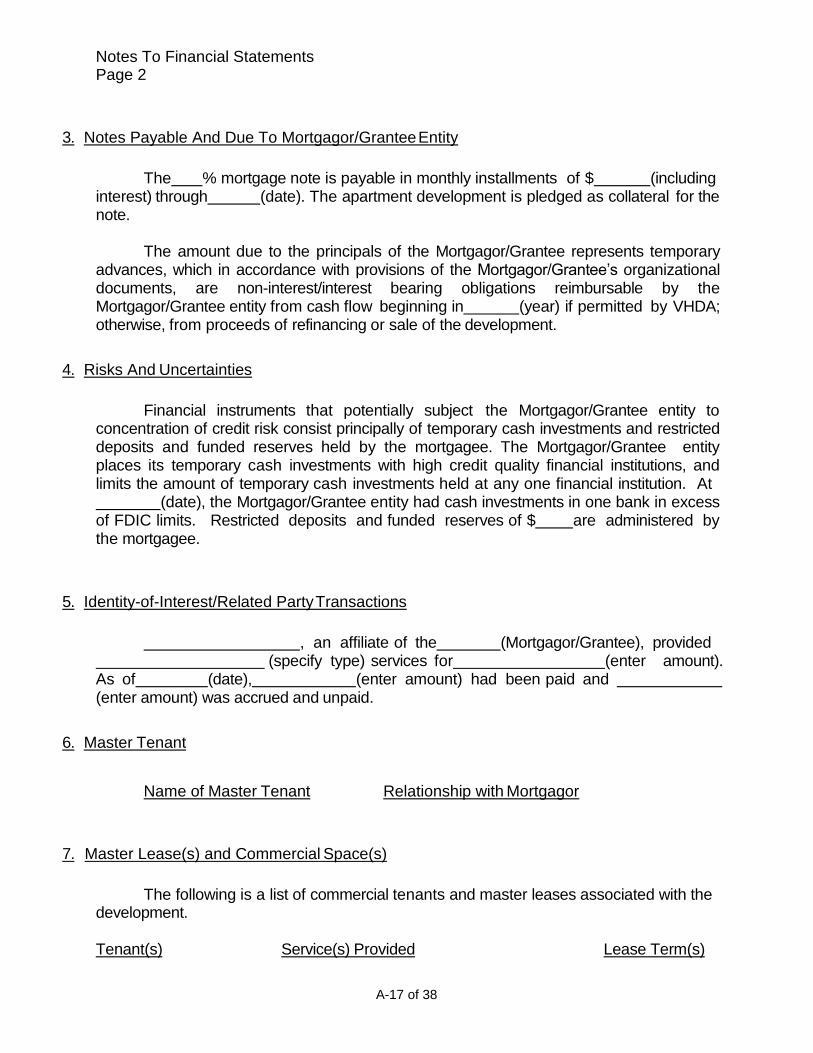

3. Notes Payable And Due To Mortgagor/Grantee Entity

The % mortgage note is payable in monthly installments of $ (including interest) through (date). The apartment development is pledged as collateral for the note.

The amount due to the principals of the Mortgagor/Grantee represents temporary advances, which in accordance with provisions of the Mortgagor/Grantee’s organizational documents, are non-interest/interest bearing obligations reimbursable by the Mortgagor/Grantee entity from cash flow beginning in (year) if permitted by VHDA; otherwise, from proceeds of refinancing or sale of the development.

4. Risks And Uncertainties

Financial instruments that potentially subject the Mortgagor/Grantee entity to concentration of credit risk consist principally of temporary cash investments and restricted deposits and funded reserves held by the mortgagee. The Mortgagor/Grantee entity places its temporary cash investments with high credit quality financial institutions, and limits the amount of temporary cash investments held at any one financial institution. At

(date), the Mortgagor/Grantee entity had cash investments in one bank in excess of FDIC limits. Restricted deposits and funded reserves of $ are administered by the mortgagee.

5. Identity-of-Interest/Related Party Transactions

, an affiliate of the (Mortgagor/Grantee), provided (specify type) services for (enter amount).

As of (date), (enter amount) had been paid and (enter amount) was accrued and unpaid.

6. Master Tenant

Name of Master Tenant Relationship with Mortgagor

7. Master Lease(s) and Commercial Space(s)

The following is a list of commercial tenants and master leases associated with the development.

Tenant(s) Service(s) Provided Lease Term(s)

A-18 of 38

Appendix A, A-8

OTHER VHDA INFORMATION

ACCRUED EXPENSES - DEVELOPMENT NAME

Description Date Due Amount Accrued

Total $0.00

ACCRUED EXPENSES - MORTGAGOR ENTITY

Description Date Due Amount Accrued

Total $0.00

Appendix A, A-8

OTHER VHDA INFORMATION

ACCOUNTS AND NOTES RECEIVABLE - DEVELOPMENT NAME

(OTHER THAN FROM TENANTS)