mortality regimes and pricing samuel h. cox university of manitoba yijia lin university of nebraska...

TRANSCRIPT

Mortality Regimes and PricingSamuel H. Cox

University of Manitoba

Yijia LinUniversity of Nebraska - Lincoln

Andreas MilidonisUniversity of Cyprus

& University of Manchester

Presented at Fifth International Longevity Risk and Capital Markets Solutions Conference

New York City, NY

September 26, 20091

Figure 1. US population mortality index from 1901 to 2005

Mortality Regimes and Pricing 2

Mortality Regimes - Motivation

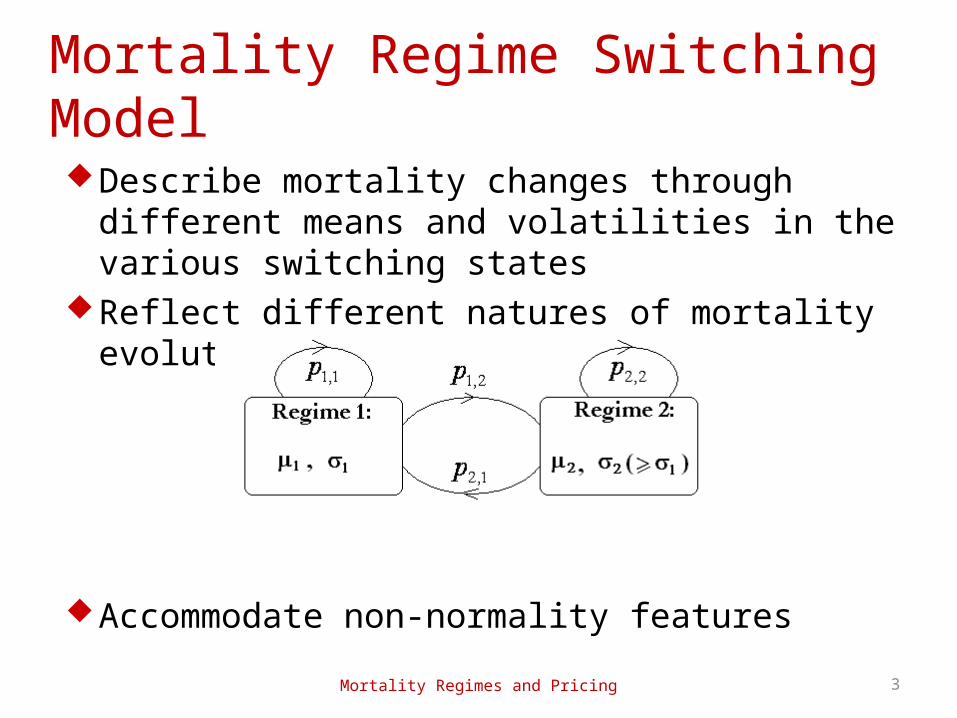

Describe mortality changes through different means and volatilities in the various switching states

Reflect different natures of mortality evolutions

Accommodate non-normality features

Mortality Regimes and Pricing 3

Mortality Regime Switching Model

Regime Switching models have been constructed to: Model dynamics in population mortality indices Extend the Lee-Carter (1992) model

Results of proposed Regime Switching models have been benchmarked to existing models

Price mortality/longevity security to show the economic significance of modeling different mortality regimes through Changes in market price of risk Changes in call option premiums

Mortality Regimes and Pricing 4

Outline

Mortality log change rate Markov process with two regimes:

Markovian probability transition matrix

where , j = 1 or 2; k = 1 or 2.

Mortality Regimes and Pricing 5

RS-GBM model for Modeling US Population Mortality Index

1log ttt qqY

11 1

22 2

1.

2t t

t

t t

Y t W ifY

Y t W if

2221

1211

pp

ppP

.2,1t

jkp ttjk |Pr 1

Figure 2

Conditional Probability of US Population Mortality Index Classified in High Volatility Regime

Mortality Regimes and Pricing 6

Geometric Brownian motion

Lin and Cox (2008) Model

where

Mortality Regimes and Pricing 7

Competing Models for US Population Mortality Index

tttt Wqtqq ddd

.1yprobabilitwith

yprobabilitwith

pq

pRqq

t

ttt

.21 tVrrt eR

Table 2

Maximum Likelihood Parameter Estimates of Competing Models

Mortality Regimes and Pricing 8

Mortality Regimes and Pricing 9

Is Modeling Changes in Mortality Regimes Important?

Mortality Regimes and Pricing 10

Is Modeling Changes in Mortality Regimes Important? (Cont’)

Wang transform

]))(([)( 1* ii LFGLF

Lee-Carter (1992) model

where

We model as RS-normal

where and

Mortality Regimes and Pricing 11

Improving the Lee-Carter Model with Regime Switching Model

txtxxtx kbaq ,,ln

ttt egkk 1

).,0(~ 2Net

te

, 2

12

1

tt

ttt

ife

ifegk

tt Wte 111 .22

2tt Wte

Figure 4

Conditional Probability of Error Term Classified in Low Volatility Regime

Mortality Regimes and Pricing 12

te

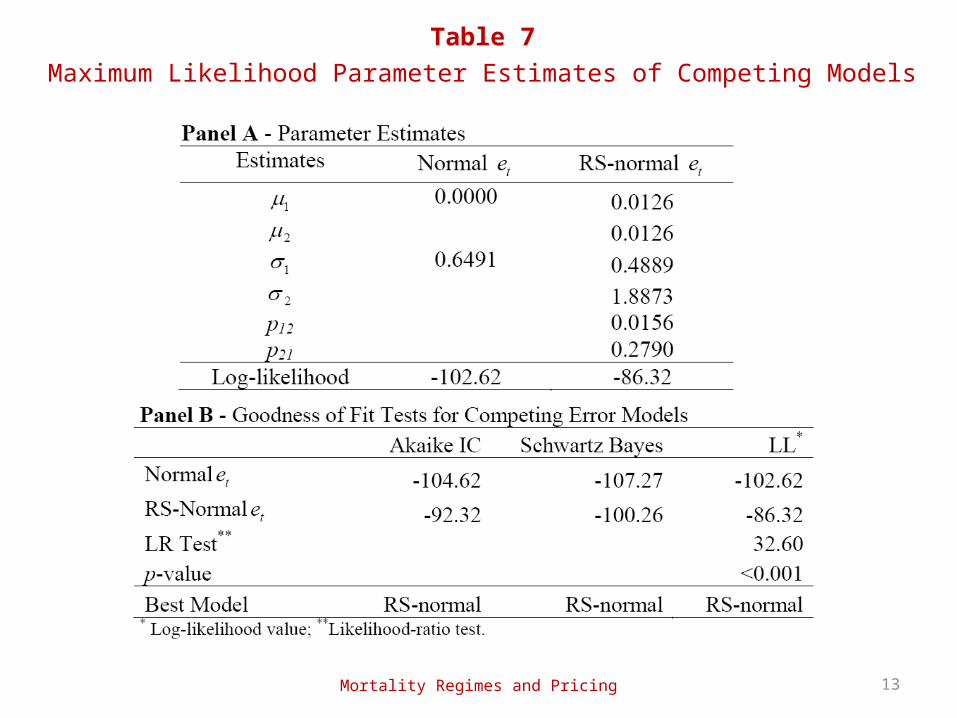

Table 7

Maximum Likelihood Parameter Estimates of Competing Models

Mortality Regimes and Pricing 13

Longevity Call Option

Esscher Transform

Mortality Regimes and Pricing 14

Pricing Longevity Securities with RS Models

.0

NA,

xtxt

xtxtxtxttx ppif

ppifppV

.][E

])([E

][E

])([E)(E 0 cX

cX

cX

cXr

Qr

Xe

eXVx

e

eXVeXVe ff

Mortality Regimes and Pricing 15

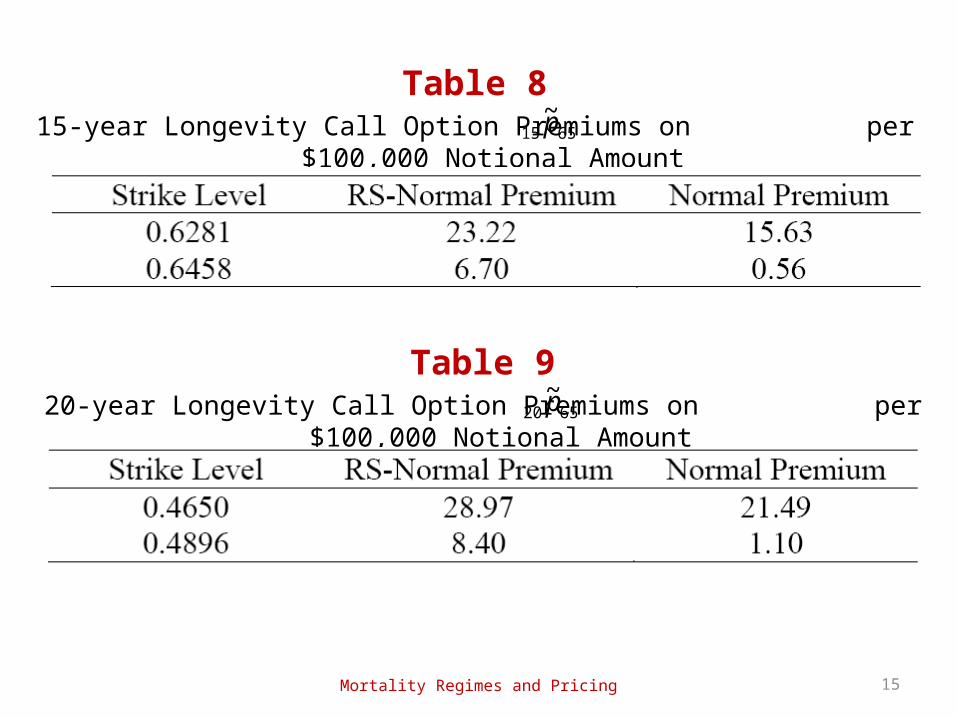

Table 815-year Longevity Call Option Premiums on per $100,000 Notional Amount6515

~p

Table 920-year Longevity Call Option Premiums on per $100,000 Notional Amount6520

~p

We propose two regime switching models in the mortality context Model the dynamics of the population mortality index Extend the Lee-Carter (1992) model

We find the statistical improvement provided by our proposed regime switching models relative to some existing mortality stochastic models.

We show how to apply mortality regime switching models to price longevity securities.

Mortality Regimes and Pricing 16

Conclusions