monetary and fiscal developments - bnm

TRANSCRIPT

Monetary and Fiscal Developments2Monetary Developments

Monetary developments in 1998 were influencedby the policy measures implemented during theyear as well as developments in the domesticcorporate and banking sectors. Monetary growthslowed down significantly in 1998 in a period ofsevere economic contraction. Growth in moneysupply decelerated sharply as credit growth sloweddown rapidly in an environment of sluggisheconomic activity; weak business prospects; lowerprivate consumption; as well as more cautiouslending policies of banking institutions amidst risingnon-performing loans (NPLs). Against thisbackground, monetary policy evolved according tothe changing conditions during the course of theyear to address emerging risks and challenges,with the aim of maintaining overall macroeconomic

stability. In achieving this objective, Bank NegaraMalaysia (BNM) relied on a combination of interestrate, and prudential and structural measures. Whilein the early part of the year the focus of policywas on ensuring stability and efficiency of thefinancial markets which is an important preconditionto achieve the longer term policy objectives, thelatter part of the year was focused on supportingeconomic recovery.

The annual growth rates of broad monetaryaggregates - M2 and M3 - moderated significantlyduring the year, while narrow money or M1 declinedfor the first time in 1998. By end-1998, the annualgrowth of M2 and M3 decelerated to 1.5% and2.7% respectively (22.7% and 18.5% respectivelyat end-1997), while M1 contracted by 14.6% (+4.6%at end-1997). On the whole, the deceleration ofmonetary growth during the year had been moresevere than anticipated, with M2 and M3 expandingby only RM4.2 billion and RM10.6 billion respectively(+RM54 billion and RM61.1 billion respectively in1997), while M1 contracted by RM9.2 billion(+RM2.8 bil l ion in 1997). M3 had trendeddownwards since February and contracted duringthe months of April to July (–RM7 billion or–1.8%). However, since August money supply turnedaround to record a moderate expansion in responseto the easing of monetary policy as well as theimproved performance in the external sector. Incomparison, the rate of deceleration in the growthof M3 during the previous recession experienced inthe mid-1980s was more gradual. During that period,the annual growth of M3 slowed down from apeak of 16.3% at end-March 1985, to 8.8% atend-1986 and further to a trough of 3.9% at end-January 1988. The more rapid slowdown in M3during the current economic downturn reflectedmainly the larger GDP contraction as well asstructural changes in the economy in which a moredeveloped equity market exerted a relatively moresignificant negative wealth effect on the economy.

Reflecting the contraction in economic activity,the demand for transaction balances (currencyholdings and demand deposits of the private sector)

Graph 2.1Money Supply

1994 1995 1996 1997 1998-10

-5

0

5

10

15

20

25

30

-10

-5

0

5

10

15

20

25

30

-25

-20

-15

-10

-5

0

5

10

15

20

25

-25

-20

-15

-10

-5

0

5

10

15

20

25

M1

M3

M2

Annual growth

Jan July Dec July Dec1997 1998

Contribution to M3 growth% contribution

%

Private sector credit Net externalassets

M3 growth

%

M3 growth (%)

declined by RM8.9 billion in 1998. Demand depositsrecorded a substantial decline of RM5.7 billion whilecurrency in circulation contracted by RM3.2 billion.Except for January, June, September, Novemberand December, the demand for transaction balancesdisplayed a declining trend during the year. Thegenerally weak business activity and poor businesssentiments resulted in lower holdings of demanddeposits by the corporate sector (–RM4.8 billion).Meanwhile, lower private sector consumptionreduced households’ requirements to hold morecurrency in their daily transactions, leading to adecline in the currency in circulation. In addition,the decline also reflected the return of currency tothe banking sector following the announcement ofthe demonetisation exercise of the RM500 andRM1,000 denominations. It was announced on 12September 1998 that the RM500 and RM1,000notes will cease to be legal tender, effective 1 July1999. In response to the announcement, aboutRM3.9 billion worth of RM500 and RM1,000 noteswere returned to BNM between September andDecember 1998. The bulk of these currency noteswas placed mostly in the form of deposits withbanking institutions.

Broad quasi-money (private sector holdings offixed and savings deposits, negotiable instrumentsof deposit (NIDs) and repurchase agreements(repos) with the banking system (excluding interbanktransactions), expanded moderately by RM19.6 billionor 6% in 1998, compared with RM58.7 billion or21.8% in 1997. The sharp deceleration in thegrowth of broad quasi-money reflected mainly lowerincome with the contraction in GDP. Depositplacement by individuals in savings andfixed deposits expanded by RM17.7 billion,compared with the increase of RM22.8 billion in1997. For the corporate sector, a combination ofweak business activities as well as relatively higherlending rates, particularly in the first half-yearadversely affected their liquidity and cash flowposition. As a result, total deposits placement bybusiness enterprises in interest-bearing instrumentswith banking institutions declined, with a netwithdrawal in fixed deposits (–RM4.9 billion) andNIDs (–RM425 million).

In terms of instruments, the moderate expansionin the broad quasi-money reflected the increase infixed deposits (RM14.9 billion); foreign currencydeposits (RM1.4 billion); savings deposits (RM1.3billion); repos (RM1.1 billion) and NIDs (RM974million). The large differential between savings and

fixed deposits interest rates, in particular during thefirst half of the year, led to the increase in fixeddeposits during the year. It also reflected the shiftin preference among institutional and retail investorsof the Kuala Lumpur Stock Exchange (KLSE) toless risky portfolios following the sluggish stockmarket performance.

In terms of determinants, the main impetus tothe expansion in money supply emanated fromexternal operations. Reflecting the surplus in thecurrent account of the balance of payments ofRM36.1 billion, as well as the impact from theintroduction of selective exchange control measuresin September, net external assets of BNM and thebanking system expanded by RM51.2 billion. Duringthe year, external reserves of BNM increased byRM40.3 billion, a turnaround from the decline ofRM10.9 billion in 1997. However, it should be notedthat effective 15 September 1998, following thefixing of the exchange rate of the ringgit againstthe United States dollar at US$1=RM3.80, all foreigncurrency assets and liabilities of BNM have beenrevalued into ringgit at rates of exchange prevailingon the reporting date. Hence, part of the increasein the external assets during the year reflected theexchange revaluation gains. This, however, had aneutral impact on money supply since therevaluation gains were offset by increases in theitem "other influences", which also recorded adecline of RM32.4 billion during the year. In additionto the significant accumulation of reserves by BNM,the higher net external assets position was alsodue to the marked decline in the external liabilitiesof the banking system. In 1998, net externalliabilities of the banking system declined byRM10.9 billion. This was largely attributed to therepayment of foreign loans by the bankinginstitutions. Following the improved liquidity situation,especially in the second half of 1998, local bankinginstitutions did not roll over the bulk of theirmaturing loans from abroad. The domestic bankinginstitutions also reduced a large portion of theirforeign interbank borrowings, especially those withshorter-term maturity.

Claims on the private sector, which had beenthe main expansionary factor in previous years,exerted a marginal impact on monetary growth in1998, contributing about 1.1% to M3 growthcompared with 27.3% in 1997. During the year,claims on the private sector expanded by onlyRM4.2 billion or 0.9%, compared with the significantexpansion of RM90.4 billion or 25.3% in the

previous year. The expansion in credit was duewholly to the higher holdings of private debtsecurities by the banking institutions of RM14.1billion, partly reflecting subscriptions to Danamodaland Danaharta bonds. In the last quarter of 1998,Danamodal Nasional Berhad (Danamodal) issuedzero-coupon bonds with a face value of RM11billion, while Pengurusan Danaharta Nasional Berhad(Danaharta) issued two series of zero-coupon bondswith a total face value of RM2.6 billion in exchangefor the banking institutions’ NPLs. In contrast, loansand advances extended by the banking institutions(as defined under M3 determinants) declined byRM9.9 billion or 2.4%, compared with a substantialexpansion of RM82.1 billion or 25.3% in 1997.

Total loans of the banking system (comprisingcommercial banks, finance companies and merchantbanks) declined by RM7.6 billion or 1.8% in 1998.However, if the NPLs that were purchased byDanaharta during the year were included, total loansin 1998 would have increased by RM5.5 billion or1.3%. By institutions, commercial banks continuedto record a moderate increase in loans (+3.3%).Loans extended by finance companies and merchantbanks, however, declined by 15% and 3.7%respectively. The ongoing merger exercise amongthe finance companies had affected their loangrowth. The poor performance of the affectedfinance companies also contributed to the declinein loans extended to the private sector. On thewhole, the decline in loans extended by the bankingsystem in 1998 was attributed to both demand andsupply factors. On the demand side, the relativelyhigher interest rates, particularly during the first half-year, as well as the contraction in economic activity

were the main reasons that led to the lowerdemand for loans by the private sector. The declinein loans also reflected the higher repayments inresponse to higher interest rates in the first half-year and the postponement of expansion plans asthe crisis became more severe. Furthermore, asinventory levels increased and capacity utilisationwas lower, the demand for loans for newinvestments fell, leading to a decline in the overallfinancing needs of the economy. On the supplyside, the decline in the extension of loans by thebanking institutions was attributed to the tightliquidity conditions in early 1998 and more cautiouslending policies by banking institutions. With theactual NPL ratio on a net basis increasing from4.1% of total loans as at end-1997 to 9% of totalloans as at the end of 1998, and the ensuingerosion of capital, banking institutions became morecautious in their lending activities during the yearas they adjusted to strengthen their balance sheet.

Total loans extended by the banking system weregenerally on a declining trend during the periodFebruary to September before reverting to an increasein October and November. Sales of gross NPLs toDanaharta amounting to RM13 billion in December,caused total loans to decline during the month. Forthe year as a whole, the decline in total loans wasdue to lower lending for consumption credit, purchaseof securities, purchase of transport vehicles andcommunity, social and personal services andmanufacturing sectors, which more than offset thehigher loans to the broad property; transport, storageand communication; electricity, gas and water; andfinance, insurance and business services sectors.The bulk of the loans continued to be channelledto the broad property sector (+RM6.2 billion or 4.4%).By the end of 1998, total credit extended to thebroad property sector represented 35.3% of totalloans (33.2% in 1997). Nevertheless, the higherexposure to the broad property sector did not reflectnew risks, as the increases in loans were mainlyfor the purchase of residential property (RM5.5 billion).Given the slowdown in the implementation of existinginfrastructure and non-residential projects as well asthe deferment of selected new projects, loans extendedto the construction sector and for the purchase ofnon-residential property increased by only RM582million and RM1.5 billion respectively. At the sametime, loans for transport, storage and communication,as well as for finance, insurance and businessservices sectors continued to receive adequatefinancing with increases of RM1.9 billion or 14.9%and RM907 million or 2.5% respectively.Meanwhile, in line with the lower economic activity

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

Graph 2.2Banking System: Direction of Lending

% of total loans

Manufacturing Wholesale,retail,

restaurants& hotels

Purchase ofsecurities

Finance,insurance &

businessservices

15.0 15.3

8.3 8.5

33.235.3

8.6 9.0

13.711.9

1997

1998

Broadproperty

9.27.8

Consumption credit

% of total loans

and contraction in disposable income, loans extendedfor consumption credit, including for purchase ofpassenger cars, recorded a net repayment of RM8.4billion. Consequently, the share of outstanding loansdeclined to 11.9% at end-1998. Similarly, loans forthe purchase of securities declined by RM6.5 billionor 16.7%. Loans to the manufacturing sector recordeda decline of RM110 million or 0.2%, reflecting lowermanufacturing activities as well as large loanrepayments. Meanwhile, loan approvals improvedsubstantially in the second half of 1998 (RM38.2billion compared with RM24 billion in the first half-year). For the year as a whole, the bulk of theapprovals were for the manufacturing sector, thepurchase of residential properties and the finance,insurance and business services sector. A total ofRM10.5 billion of new loans had been approved forthe manufacturing sector, which accounted for 16.9%of total loans approved. Loans approved for thepurchase of residential property and the finance,insurance and business sector amounted to RM9.3billion and RM8.1 billion respectively, accounting

for 14.9% and 13.1% of total new approvals duringthe year.

In response to the slowdown in loans, severalmeasures were implemented to promote creditexpansion and to avoid a credit crunch in order toensure that the banking sector is better able tosupport economic recovery. With the improvementin the medium-term inflation prospects, interest rateswere lowered in stages during the second half ofthe year. Consequently, the average BLR ofcommercial banks declined steadily from a peak of12.27% at end-June to 8.04% at end-1998. Inaddition, with effect from 14 September 1998, allbanking institutions were also required to reducethe maximum margin over the quoted BLR from 4percentage points previously, to 2.5 percentagepoints. These measures effectively reduced theborrowing cost to the borrowers and eased theburden in servicing interest payments. To ensurethat there were sufficient funds to finance the

Table 2.1Banking System: Loans by Sector

As at end Change Share of total

1997 1998 1998 1998

RM million %

Agriculture, hunting, forestry and fishing 7,637.8 7,717.8 80.0 1.9Mining and quarrying 1,348.5 1,673.6 325.1 0.4Manufacturing 63,310.4 63,200.4 –110.0 15.3Electricity, gas and water 4,461.1 5,879.2 1,418.1 1.4Wholesale, retail, restaurants and hotels 34,940.7 35,111.4 170.7 8.5

Wholesale trade 19,926.8 18,725.0 –1,201.8 4.5Retail trade 10,531.4 10,240.0 –291.4 2.5Restaurants and hotels 4,482.5 6,146.4 1,663.9 1.5

Broad property sector 139,922.4 146,148.4 6,226.0 35.3Construction 42,615.9 43,198.4 582.5 10.4Purchase of residential property 50,843.9 56,386.7 5,542.8 13.6Purchase of non-residential property 28,440.2 29,967.0 1,526.8 7.2Real estate 18,022.4 16,596.3 –1,426.1 4.0

Transport, storage and communication 13,040.6 14,983.1 1,942.5 3.6Finance, insurance and business services 36,209.4 37,116.8 907.4 9.0

Financial services 26,617.3 28,375.0 1,757.7 6.9Insurance 131.6 249.0 117.4 0.1Business services 9,460.5 8,492.8 –967.7 2.1

Consumption credit 57,836.0 49,418.5 –8,417.5 11.9Personal uses 14,924.8 13,446.9 –1,477.9 3.3Credit cards 4,586.4 4,313.0 –273.4 1.0Purchase of consumer durables 1,717.0 826.9 –890.1 0.2Purchase of passenger cars 36,607.8 30,831.7 –5,776.1 7.5

Purchase of securities 38,951.2 32,460.0 –6,491.2 7.9Purchase of transport vehicles 5,687.3 4,504.8 –1,182.5 1.1Community, social and personal services 6,872.0 6,671.4 –200.6 1.6Others 10,985.1 8,752.8 –2,232.3 2.1

Total loans 421,202.5 413,638.2 –7,564.3 100.0

Adjusted total loans 421,202.5 426,677.3 5,474.8(Including NPLs sold to Danaharta)

economic recovery process, banking institutions withthe capacity to lend were encouraged to expandtheir loan base and achieve a minimum loangrowth of 8%. In addition, the SRR and liquidityratios were also reduced to improve theliquidity conditions.

These measures have produced encouragingresults. Even though the actual loans disbursed inthe second half-year remained slow, the amount ofloans approved by the banking system increasedsubstantially in the latter half of 1998. Otherinitiatives that had been taken to improve thefinancial intermediation process and expand creditincluded the establishment of Danaharta to purchaseNPLs from the banking institutions so that bankinginstitutions can focus more on their core activity ofproviding credit. Similarly, Danamodal was set upto recapitalise the banking system. Thisrecapitalisation process by Danamodal was alsoaccompanied by a restructuring of the bankinginstitutions. A Corporate Debt RestructuringCommittee had also been established to assistborrowers and creditors to discuss solutions for debtrestructuring.

During the year, the expansionary impact fromthe external operations and claims on the privatesector were partially offset by the contractionaryinfluences of other determinants. Net lending to the

Government contracted by RM12.3 billion primarilydue to the higher accumulation of deposits duringthe year. By end-year, total Government depositsplaced with BNM and the banking institutionsamounted to RM46.2 billion, an increase of RM17.5billion from the previous year. The large increasein deposits was mainly attributed to the proceedsfrom domestic borrowing as well as disbursementof external loans, particularly during the last quarterof the year to finance the fiscal stimulus programme.As such, the accumulation of Government depositsduring the period was expected to be temporaryand would eventually be drawn down in stages tofinance the Government’s expenditure. In additionto Government operations, net other influences alsoexerted a contractionary impact on money supply.During the year, net other influences contracted byRM32.4 billion reflecting the exchange revaluationgains on external reserves holdings of BNM, thehigher provisions for bad and doubtful debts aswell as the capital injection by Danamodal toselective banking institutions.

In 1998, the movement of interest rates wasprimarily influenced by the level of liquidity, whichwas in turn affected by financial marketexpectations, as well as the shift in the monetarypolicy stance. On the whole, interest ratesdevelopments can be divided into three periods.Prior to February 1998, interest rates were on anupward trend. Between February and July 1998,interest rates were stable, while thereafter, interestrates were on a downward trend.

In the first two months of the year, interestrates continued its upward trend as a policy ofmonetary restraint was adopted since September1997 to contain inflationary pressures arising fromthe ringgit depreciation as well as to discouragecapital outflows. The 3-month interbank rate, whichis BNM’s policy rate, had been raised in severalsteps from 7.55% in mid-September 1997 to 8.7%at end-1997. It was raised twice again in January1998 to 10% and again in February to 11%.Reflecting the tight liquidity situation and the unevendistribution of liquidity among banking institutionsduring this period, the average 1-month interbankrate rose above the average 3-month rate fromOctober 1997 onwards, while the 1-week andovernight rates began to follow suit since December1997. As a result, the term structure of interestrates was inverted during this period. The highshorter-term interest rates reflected the tight liquidityconditions faced especially by smaller financial

Table 2.2Changes to BNM Intervention Rate & SRR Ratio

Intervention SRRRate Ratio

End-97 8.70 13.5

Jan-Feb Tightening 9 Jan 9.0020 Jan 10.00

6 Feb 11.00

Mid-Feb 16 Feb 10-Jul

1 Jul 8

3 Aug 10.5010 Aug 10.0027 Aug 9.50

1 Sep 63 Sep 8.00

16 Sep 4

5 Oct 7.50

9 Nov 7.00

Liquidity Date1998

EasingAug-Dec

Stable

institutions. Furthermore, with increased uncertaintiesin the financial market, there was a flight to qualityof retail deposits placed with these smallerinstitutions towards the end of 1997 and in early1998. During this period, these institutions facedconsiderable difficulties in obtaining interbank fundsdue to selective lending practices by the largerinstitutions. The consequent aggressive bidding bythe smaller institutions at the short end of themoney market led to sharply higher short-end rates,with the 1-week rate peaking at 15.04% in January1998 (see Graph 2.3: Interbank Rates). Theresulting inverted term structure of interest rates,therefore, reflected the exceptionally tight liquiditysituation of a few institutions rather than that ofthe banking system as a whole. The higher costof funds incurred by these institutions led to arapid increase in lending rates for loans priced ona cost plus basis.

Faced with this scenario, BNM injected liquiditythrough direct lending to banking institutions. Torationalise the term structure of interest rates aswell as to improve liquidity flows in the system,BNM raised the intervention rate to 11% on 6February as well as reduced the SRR from 13.5%to 10% on 16 February 1998. Consequently, theterm structure of interest rates flattened from itsinverted position. The purpose of the SRR reductionwas not to add further liquidity but to improve thedistribution of liquidity that had already been injectedinto the banking system as well as to reduce thecost of funds for banking institutions given thatbanks do not earn interest on SRR. The SRR wasagain lowered without causing a net injection on 1July. This time around, the main objective was toreduce the cost of funds to banking institutions so

as to enable them to lower the lending rates totheir customers. On both occasions of the SRRreduction, the liquidity for the system as a wholewas unchanged, resulting in the 3-month interbankrates remaining firm at around 11%.

In the subsequent months, the ringgit ratesbecame more stable following the monetarymeasures undertaken between February and July1998. There were also emerging signs thatinflationary pressures had moderated. Thesedevelopments enabled BNM to ease monetary policyto complement fiscal policy to revive the economy.In August, the 3-month intervention rate wasadjusted downwards in three steps to 9.50%. SinceSeptember when selective exchange controls wereintroduced, further monetary easing was pursued.The intervention rate was reduced to 7% over threesuccessive reductions, while the SRR was reducedin two steps to 4%. Consequently, the interbankrates fell below the BNM intervention rates as a

2

4

6

8

10

12

14

16

18

20

2

4

6

8

10

12

14

16

18

20

% per annum % per annum

Graph 2.3Interbank Rates

3-Mth Intervention 3-Mth 1-Mth 1-Wk O/nite

Period 1Liquidity

Tightening

Period 2LiquidityStable

Period 3LiquidityEasing

Jan Apr Jul Oct97 97 97 97

Jan Apr Jul Oct98 98 98 98

2

4

6

8

10

12

14

16

18

20

2

4

6

8

10

12

14

16

18

20

Dec Feb Apr Jun Aug Oct Dec96 97 97 97 97 97 97

Feb Apr Jun Aug Oct Dec98 98 98 98 98 98

Period 3LiquidityEasing

Feb Apr Jun Aug Oct Dec98 98 98 98 98 98

Graph 2.4Interest Rates of Financial Institutions

Commercial Banks (average rates at end-month)

Average lending rate Base lending rate (BLR)Fixed deposit 1-month Fixed deposit 3-monthFixed deposit 12-month Savings deposit

2

4

6

8

10

12

14

16

18

20

2

4

6

8

10

12

14

16

18

20

Dec Feb Apr Jun Aug Oct Dec96 97 97 97 97 97 97

Period 2LiquidityStable

Period 3LiquidityEasing

Average lending rate Base lending rate (BLR)Fixed deposit 1-month Fixed deposit 3-monthFixed deposit 12-month Savings deposit

Finance Companies (average rates at end-month)

% per annum

% per annum

% per annum

% per annum

Period 1Liquidity

Tightening

Period 1Liquidity

Tightening

Period 2LiquidityStable

result of the significant increase in liquidity in anenvironment of continued weak loan growth.

Reflecting the movements in the interbank moneymarket rates, interest rates of financial institutionsalso increased up to June and subsequentlyadjusted downwards (see Table 2.3: Interest Ratesof Financial Institutions). As these rates tend to lagbehind interbank rates, the rates peaked in June.In the case of fixed deposit rates, the financecompanies’ fixed deposit (FD) rates adjusted morerapidly in response to the increases in interbankrates, whereas commercial banks’ rates had alonger lagged response. As a result, the averagespread offered by finance companies overcommercial banks’ FD rates increased from 0.2%before the crisis in June 1997 to as high as 1.5%in January 1998, before declining to 0.6% by end-1998. The greater responsiveness of financecompanies’ FD rates reflected the more aggressivecompetition for funds following their tighter liquiditysituation compared with commercial banks.Meanwhile, savings deposit rates for both typesof institutions were more stable, moving within anarrower range of only 0.6–0.8% during the year(the corresponding range for FD rates was 4.4–4.5%). A similar trend was also evident for thebase lending rates (BLRs), which was linked tothe 3-month interbank rate under the BLRframework. These BLRs are also linked to the SRRand as such, the reductions of the SRR inFebruary, July and twice in September allcontributed to a decline in the BLR. With thereduction in both the 3-month interbank rate andthe SRR, the BLR for commercial banks adjusteddownwards by 4.23 percentage points from a peakof 12.27% at end-June to 8.04% by mid-November.It remained unchanged thereafter until the end ofthe year.

Meanwhile, the interest margins or interestspreads of financial institutions also narrowed during

1998. The smaller margin was due to the fasterreduction in the average lending rate (ALR)compared with the average cost of funds (ACFs)during the year. The spread, however, widenedtowards mid-year in the case of commercial banksbut narrowed in the case of finance companies,before reversing trends in each case towards year-end. This asymmetry reflected the differentrelationships of these institutions’ ALR and ACF tochanges in liquidity and the general level of interestrates (see Table 2.4). Essentially, despite the sharpincrease in the BLRs of finance companies at end-1997 and early 1998, their ALRs were relativelystable. The bulk of finance companies’ loans wasin the form of fixed rate hire purchase loans ratherthan BLR-plus loans. As a result of the relativestability or “stickiness” of the ALR of the financecompanies, the rates were lower than their BLRsfor the 10 months between November 1997 andAugust 1998. In contrast, the ALR of commercialbanks moved in tandem with their BLR. On theother hand, the ACFs of finance companies weremore sensitive to changes in liquidity and interestrates and had, therefore, increased significantlywhen there was a flight to quality in late 1997 andearly 1998. Meanwhile, the ACFs of commercialbanks increased more marginally. As a result ofthe stickiness of the ALR and the greaterresponsiveness of cost of funds to monetarydevelopments, the margins of finance companieswere squeezed in times of rising interest rates,while in contrast, the margins of commercial banksincreased during periods of tight liquidity.

Interest rate differentials with other countriesalso changed significantly during the year. The realinterest rates (nominal interest rates adjusted forinflation) in Malaysia have moderated and are nowlower than the real interest rates in the UnitedStates and Singapore. The trend reflects the moresignificant decline in Malaysia’s nominal rates andthe relatively higher Consumer Price Index vis-a-vis

Table 2.3Interest Rates of Financial Institutions

3-Month FD 9.06 10.19 5.83Savings Deposit 4.23 4.51 3.87Base Lending Rate 10.33 12.27 8.04

3-Month FD 10.32 10.97 6.43Savings Deposit 5.49 5.56 5.01Base Lending Rate 12.22 14.70 9.50

CommercialBanks

End-97 End-98June 98

FinanceCompanies

Table 2.4Interest Margins of Financial Institutions

Avg. Lending Rate (ALR)11.51 13.51 9.72Less Avg. Cost of

Funds (ACF) 7.62 8.60 6.17Interest Margin 3.89 4.91 3.55

Avg. Lending Rate (ALR)12.16 13.35 11.76Less Avg. Cost of

Funds (ACF) 8.47 11.67 7.68Interest Margin 3.69 1.68 4.08

CommercialBanks

End-97 End-98June 98

FinanceCompanies

Monetary Measures in 1998

Adjustment and Stabilisation Measures(January - July 1998)

Monetary measures implemented in the firstseven months were aimed at enhancing theefficiency of the money market to allow interestrates to reflect underlying liquidity conditions.The measures were also aimed at reinforcingthe fundamental thrust of policy to achieve theobjectives of monetary and financial stability whilesupporting economic recovery. The measureswere as follows:

● On 26 January, banking institutions wereallowed to continue to provide bridging financeto housing developers to start new projectsfor residential properties costing RM150,000and below as long as the project wasdeemed viable.

● On 6 February, Bank Negara Malaysia (BNM)announced the streamlining of the interestrate structure to better reflect liquidityconditions in the market. Arising fromdevelopments in late 1997 and early 1998,the term structure of the interbank and lendingrates was not reflective of the prevailingmarket conditions. The shorter-endinterbank rates mainly reflected theexceptionally tight liquidity situation of a smallnumber of banking institutions. Followinguncertainties during the period, there was atendency for lending rates to be based onthese short-term rates on a cost-plus basis.To improve the flow of liquidity in the system,and to streamline the term structure of interestrates that would better reflect the liquidity inthe financial system, the 3-month BNMintervention rate was adjusted upwards to 11%from 10%.

● With effect from 16 February, the statutoryreserve requirement (SRR) for allcommercial banks, finance companies andmerchant banks was reduced from 13.5% to10% of their eligible liabilities. This was aimedat enhancing the efficiency of theintermediation process rather than to provide

additional liquidity to the system. BNMfurther reduced the SRR to 8% on1 July so as to reduce the cost of fundsto the banking institutions and improvethe liquidity distribution among thebanking institutions.

● Effective 1 May, the band for thepermissible daily variation in the averagebalance that is required to meet theSRR was widened to ±2% of theprescribed SRR rate from the previous bandof ±0.5%. The widening of the SRR bandwould accord banking institutionsgreater flexibility in managing their dailyliquidity operations.

Economic Recovery Plan (fromAugust 1998)

Beginning early August, monetary measuresreflected easing of monetary policy to supporteconomic recovery. The measures were alsoaimed at strengthening the financial system.These measures were as follows:

● In early August, with the improvement in themedium-term inflation prospects, BNMreduced its 3-month intervention rate inthree steps from 11% to 10.5% on 3 August,to 10% on 10 August and further to 9.5%on 27 August. Following the introduction ofthe new exchange control measures, the 3-month intervention rate was further reducedto 8% on 3 September, to 7.5% on 5October and to 7% on 9 November.

● On 1 September , the Governmentintroduced selective exchange controls toinsulate the Malaysian economy from theprospects of further deterioration in theworld economic and financial environmentand to regain monetary independence.On 2 September, BNM announced thatthe exchange rate for the ringgit wasfixed at RM3.80 against the UnitedStates dollar.

● Meanwhile, to ease liquidity in the bankingsystem and make available more loanablefunds to borrowers at a lower rate, theSRR was reduced from 8% to 6% on1 September and further to 4% on16 September.

● As of 3 September, commercial banks wereno longer required to maintain vostrobalances of foreign banking institutionswith BNM.

● The base lending rate (BLR) framework wasrevised on 1 September to ensure a morerapid transmission of changes in monetarypolicy on interest rate levels into the BLR ofbanking institutions. The calculation of theBLR is now based on the BNM 3-monthintervention rate instead of the KLIBOR. Inaddition, to ensure that borrowers benefit fromthe higher level of operational efficiency withinthe banking industry, the flat administrativemargin of 2.5 percentage points was reducedby 25 basis points to 2.25 percentage points.The maximum margin over the quoted BLRwas also reduced from 4 percentage pointsto 2.5 percentage points.

● To ensure that there was sufficient fundsto finance the economic recoveryprocess, banking institutions with the capacityto lend were encouraged to achieve aminimum annual loan growth of 8%.

● In an effort to assist the construction sectorthat had been severely affected by theeconomic crisis, some relaxation to theearlier ceilings on the broad propertysector were implemented on 7 September.Lending for the construction or purchase ofresidential properties costing up to RM250,000were exempted from the 20% limit onlending to the broad property sector. Inaddition, effective 5 October, the 60%maximum margin of financing was abolishedfor the purchase of non-owner occupiedresidential properties costing RM150,000 andabove; the purchase of shophouses costingRM300,000 and above which are not for theconduct of own business; and the purchaseof land lots.

● The ceiling on loans for the purchaseof shares and unit trust funds was also

raised from 15% to 20% of totaloutstanding loans for commercial banks andfinance companies on 23 September. Thelimit for merchant banks remained at 30%.The increase in the limit was aimed atpromoting long-term investments in thestock market.

● The margin of financing for all passengercars was raised from 70% to 85% on23 April and the restriction on themaximum repayment period was removed on28 July. The margin of financing of 85%was abolished on 21 November, and bankswere free to determine the percentage offinancing based on their credit assessment ofthe borrower.

● Effective 5 December, BNM reduced themaximum lending rate under the Fund forSmall and Medium Industries and theSpecial Scheme for Low and Medium CostHouses from 10% per annum to 8.5% perannum and the funding rate from 8% perannum to 6% per annum.

● Effective 20 November, the minimummonthly repayment on credit cards wasreduced from 15% to 5% of theoutstanding credit card balances in order toease the cash flow burden of creditcard holders. To ensure that the chargesimposed on the credit card holders werereasonable, banking institutions thatissue credit cards were required from30 December to impose a maximum financecharge of not more than 1.5% per monthor 18% per annum and that the late paymentcharges should not be more than 1% of theamount in default. However, bankinginstitutions were allowed to charge a minimumpenalty of RM5.

● In view of the need to clear thecurrent backlog of properties, effective5 January 1999, banks were not allowed tofinance the development of new residentialproperties and shophouses where theindividual unit costs more than RM250,000each. In addition, banking institutionswere not allowed to provide financingto develop hotels, resorts, office buildings,golf courses, clubs and shoppingcomplexes.

the United States and Singapore. The low realrates in the region of 1% at end-1998 waspreviously experienced in 1994 in Malaysia, duringthe period of massive capital inflows, and in 1988,during the recovery years after the recession ofthe mid-1980s.

Monetary Policy in 1998

As the Asian financial crisis became more severein 1998, the formulation of monetary policy wasgoverned by the need to address the increasingvolatility in the financial markets, the irrational marketbehavior, the deterioration in the financial position ofthe banking and corporate sectors, the existence ofimbalances in the economy and the contraction ineconomic activities. In this context, monetary policywas pursued as part of a comprehensive set ofpolicies to maintain macroeconomic and financialstability with the ultimate objective of stabilising andreviving the economy. While price stability remainedthe primary objective of monetary policy, it wasnecessary that monetary policy was also implemented

to create a conducive environment to achievesustainable long-term growth. Given the severeadverse effects of too tight a monetary policy onthe economies of countries in the region, Malaysiaadopted a different approach. It was recognisedthat high interest rates would not stabilise theexchange rate due to the strong external factors. Itwas more important to ensure that monetary policywould promote domestic macroeconomic stability andconfidence and contain the severity of externaldevelopments on economic growth.

-8

-6

-4

-2

0

2

4

6

8

10

-40

-30

-20

-10

0

10

20

30

40

50

M1, M3 (%) GDP, Inflation (%)

Graph 2.6

Money supply, GDP & inflation

M1

M3

GDP

Inflation

1992 1993 1994 1995 1996 1997 19980

1

2

3

4

5

6Interest rate differential (%) Exchange rate

Interest rate differentials & exchange rate (end-period)

Malaysia-Singapore

Malaysia-US

RM/US$

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

1992 1993 1994 1995 1996 1997 1998-1

0

1

2

3

4

5

6

7

8

9

10

11

% per annum Annual growth (%)

Interest rates & loan growth (end-period)

BLR of commercial banks

3-month interbank

Banking system loans

-5

0

5

10

15

20

25

30

35

40

45

50

55

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

Real rates in Malaysia Real rates in the United States

Graph 2.5Real Interest Rate Differentials

Dec-97 Feb-98 Apr-98 Jun-98 Aug-98 Oct-98 Dec-98

Dec-97 Feb-98 Apr-98 Jun-98 Aug-98 Oct-98 Dec-98

differentials (-ve)

-2.57

-1.64

-2.03+0.61 +1.69

+0.85

+1.220.00

-1.70

-2.31

differentials (-ve)

5.80

6.60

5.47

5.00

3.90

3.903.46 3.47

1.76

1.16

5.80

5.19

6.60

4.91

5.47

4.62

6.64

5.00

3.90

5.93

4.33

1.76

3.13

1.16

3.95 4.04 4.093.78

-1.97

Real rates in Malaysia Real rates in Singapore

Malaysia versus United States

Malaysia versus Singapore

+1.85 +2.56 +1.38

% per annum % per annum

% per annum % per annum

In a rapidly changing environment and a globalenvironment of uncertainty, monetary managementneeds to be appropriately sequenced. The timingof policy is important. While several issues mayneed to be addressed, it is important to prioritisethese policy responses to minimise disruptions inthe system. Monetary policy, therefore, evolved atdifferent stages of the economic crisis to adapt tochanging domestic and external developments aswell as to address new risks and challenges.Nevertheless, throughout the crisis period, thefundamental objective of policy remained unchanged.

At the start of the year, the tight monetary policythat was pursued before the onset of the crisisaimed to address the rising inflationary pressuresassociated with the depreciation of the ringgit andthe consequent outflow of short-term funds. Towardsmid-1998, it was evident that inflationary pressureswere contained and the external balance turnedaround from a deficit to a surplus position. However,this contributed to reinforce the effects of aworsening external environment on domestic activity.Consequently, in response to early indicators of aweaker-than-expected growth and lower inflation inJuly, monetary policy was eased in early August.The policy aimed to complement the fiscal stimulusto create an environment in which the prospectsfor economic recovery would be enhanced. It wasalso recognised that growth could only recover andbe sustained in an environment of stability andinvestor confidence. Given the build-up in risks thatemerged in the regional and global financial marketsduring August-September, Malaysia acted decisivelyto stabilise the economy. On 1 September, selectiveexchange control measures were introduced andthe ringgit was fixed against the United States dollaron the following day. This, together with an easingof monetary policy and an expansionary fiscal policy,had a positive effect on the economy. Keymacroeconomic indicators as well as financialaggregates at the end of 1998 and in early 1999suggested that the economy is emerging from thecountry’s worst economic turbulence.

An integral part of financial policy has been thepromotion of a sound financial system that is ableto carry out its intermediation function efficiently.As Malaysia had entered the crisis with a relativelystrong and well-regulated financial sector, thepayments system and loan intermediation processremained relatively intact. However, the behaviourof markets caused distortions. Throughout the crisisperiod, Bank Negara Malaysia (BNM) had focused

on improving the intermediation process andensuring that sufficient funds were available atreasonable cost for productive activities. Thisbecame critical when credit growth slowed downfaster than envisaged in the Credit Plan for 1998.During this period, the prolonged contraction ledto a deterioration in the asset quality of thebanking system. Besides taking pre-emptive stepsto address the latter concern, a comprehensive four-pronged strategy was also initiated to strengthenthe banking system.

Against this backdrop, monetary policy in 1998can be classified into three phases, namely theadjustment phase from the outbreak of the crisisto early 1998; followed by the stabilisation phaseup to the period in July; and subsequently, therecovery phase.

The start of 1998 witnessed a sharp increase inthe volatility in both the foreign exchange and stockmarkets. Inflation also began to edge upwards asthe effects of the depreciation filtered through tothe real economy. During this period, the ringgitdepreciated further following the depreciation of theKorean won in December 1997 and the nearcollapse of the Indonesian rupiah in early 1998.Meanwhile, loans which had still been expandingrapidly up to the end of 1997 began to experiencea significant slowdown. The outflow of foreign short-term funds during this period contributed to aprogressive tightening of liquidity in the bankingsystem. Inefficiencies in the intermediation processalso emerged as the sharper depreciation of theringgit raised concerns on the banking system,particularly on the smaller institutions. This led toa shift of deposits from the smaller to the largerbanking institutions. During this period, a smallnumber of banking institutions faced significantliquidity problems due to the flight to quality ofdeposits. The competition for funds by theseinstitutions contributed to the sharp increases inmoney market interest rates which resulted in higherinterest rates for the industry as a whole. In suchan environment, monetary policy focused onaddressing this distortion. The most importantobjective of policy during this period was to improveliquidity distribution and remove distortions in theintermediation process, thereby enabling the bankinginstitutions to reduce their lending rates.

To address these problems, BNM lowered thestatutory reserve requirement (SRR) from 13.5% to

10% on 16 February, followed by another reductionto 8% on 1 July. Prior to this, BNM had placedRM34 billion in the banking system to provideliquidity to the system. The funds released by thereduction in the SRR was therefore offset by thenon-rollover of funds previously lent by BNM tofinancial institutions. The purpose of the SRRreduction was aimed at improving the distributionof liquidity that had already been injected into thebanking system and to reduce the cost of fundsfor the banking institutions given that banks earnedzero interest on the SRR. As a result of thesemeasures, the money market rates declined, leadingto a corresponding reduction in the lending rates,which fell from 21.5% in early February to 16.3%at the end of February.

During this period, there was little leeway toreduce the money market intervention rate. In theinitial stages of the crisis in July 1997, interestrates were spiked up briefly for about a week.Interest rates were subsequently reduced to thepre-crisis level from mid-August until September1997. As the crisis became more prolonged, it wasviewed that higher interest rates would have anadverse effect on the real sector, but by itselfwould not contribute to restore stability in the foreignexchange markets (see article on Monetary Policyin 1997 in the 1997 BNM Annual Report). However,when the Indonesian rupiah experienced a nearcollapse in January 1998, the ringgit depreciated toits weakest level to touch US$1=RM4.88 on 7January. Under these conditions, concerns over thepotential outflows of funds and rising inflationarypressures prompted increases in interest rates.Interest rates were then allowed to edge up to11% to ensure that depositors continued to receivepositive real rates of interest. This move containedfurther capital outflows and ringgit rates stabilisedin the region of US$1=RM3.84–3.98 in the firstand second quarters of 1998. Although interest rateswere raised to the level of 11%, it was to asignificantly lesser extent than that recommendedby the International Monetary Fund (IMF) andexpected by the market. The Bank’s view was thatsuch high interest rates would dampen economicactivity and cause strains on the banking system,resulting in further pressure on the ringgit, therebymaking economic recovery more difficult to achieve.

The Bank also undertook a number of otherinitiatives to ensure the efficient management ofliquidity and increase the efficiency of loanintermediation. Procedures were introduced on 30

April to make money market operations moretransparent and to promote efficient liquiditymanagement. Under the new procedures, BNMundertook to provide daily forecasts of the cashflows of the financial system, as well as informationon the major factors that were expected to influenceliquidity, including details of BNM’s money marketactivities. With effect from 1 May 1998, the bandfor the daily variation in the average balancerequired to meet the SRR was widened from ±0.5%to ±2%. In addition, a new framework for liquiditymanagement was introduced to enable bankinginstitutions to manage their liquidity positions withgreater flexibility without compromising prudentialstandards. The new framework was set on a six-month trial run starting July 1998. On 3 September1998, the liquid asset requirement of the commercialbanks was reduced from 17% to 15% of totaleligible liabilities. The Bank also undertook measuresto increase the efficiency of monetary policy. Thebase lending rate (BLR) framework was revamped.Under the previous BLR computation based on the3-month average weighted interbank rate of thepreceding month, the retail interest rates respondedto changes in monetary policy with a lag of severalweeks. To rectify this, with effect from 1 September1998, the calculation of the BLR was based onBNM’s 3-month intervention rate rather than theKLIBOR. The banking institutions were required toadjust their BLRs within a week of a change inBNM’s intervention rate, leading to a more rapidtransmission of changes in monetary policy. Theadministrative margin included in the BLR was alsoreduced from 2.50% to 2.25%. These measuresresulted in a downward adjustment in lending ratesand contributed to increases in the efficiency ofthe banking institutions given that they providedthe banking institutions with greater flexibility in themanagement of existing liquidity. The measuresalso resulted in a lower cost of funds. At the endof July, the BLR had declined to 12.07% from12.27% at end-June 1998.

Apart from efforts to lower the cost offunds to banks, the Government also recognisedthe adverse implications high interest rates wouldhave on small businesses. A number of funds wereestablished and existing funds expanded so thatbanking institutions could provide credit to prioritysectors at reasonable lending rates. These fundsincluded the Fund for Food (RM1 billion); PettyTraders and Hawkers Fund (RM500 million);Fund for Small and Medium Industries (RM1.5billion); Export Credit Refinancing Facility (RM3billion); Special Scheme for Low and Medium Cost

Houses (RM2 billion); Suppliers, Buyers andOverseas Investment Credit (RM1 billion); NewEntrepreneurs Fund (RM1.25 bill ion) andRehabilitation Fund for Small and Medium Industries(RM750 million).

The worsening of the regional crisis followingthe IMF intervention in Korea and Indonesia tookthe region into a phase of severe economiccontraction with its consequent effect on the financialsector. Lower aggregate demand in the regionamidst the exchange rate instability and uncertaintyand the negative wealth effect from declining assetmarkets contributed to the contraction in domesticactivity. By July 1998, it was evident that theeconomy had undergone a sharper correction thanearlier anticipated. Indications were that the economywould contract for the second consecutive quarter,indicating that the country was technically in aneconomic recession. The annual loan growth haddecelerated sharply from 26.5% at the end of 1997to 8.9% at the end of July 1998. Similarly, thegrowth rate of the broad monetary aggregate (M3)had also decelerated from 18.5% to 5.9% over thesame period. Other macroeconomic indicatorsshowed that there was a sharp contraction in carsales and collections of sales tax, indicating a sharpslowing down of economic activity. To revive theeconomy, an adjustment in macroeconomic policieswas necessary.

The deceleration in the inflation rate and anabsence of demand pressures enabled BNM toundertake an easing of monetary policy beginningin early August to complement fiscal policy tocontain the contraction and promote recovery ofthe economy. The 3-month intervention rate of BNMwas reduced in three successive steps, from 11%to 9.5% during the month of August. A cautiousand gradual easing of monetary policy wasnecessary given the threat of volatility in the foreignexchange markets and the risk of capital outflows.Of special concern was the high rates being offeredto attract ringgit funds in Singapore and the build-up of offshore ringgit balances to fund speculativeactivity on the ringgit. During this period, externalrisks in the regional and global markets had alsoworsened since end-August. The crisis had spreadto Russia and Latin America. In this environment,BNM introduced selective exchange controls on1 September, while the exchange rate was fixed atRM3.80 to the United States dollar on 2 September.The new measures were aimed at ensuring thatMalaysia could gain greater independence in the

conduct of domestic monetary policy as well asinsulate the economy from the potential risks andvulnerabilities of external developments in theinternational financial markets. Other considerationsincluded preserving the gains that had been madeto stabilise the domestic economy; ensuring stabilityin prices and the ringgit exchange rate; as well aspromoting a stable environment for restoring investorand consumer confidence to revive the economy.Hence, the exchange control regulations werecarefully designed to contain speculation on theringgit and minimise the impact of short-termcapital flows on the domestic economy. Theseregulations did not affect trade and investment ineconomic activity. Full convertibility remained forcurrent account transactions.

The new measures provided the Bank with theability to further ease monetary policy to supportthe domestic economic recovery process given theabsence of inflationary pressures. Following theintroduction of the exchange control measures andthe fixed exchange rate, additional monetarymeasures were introduced to improve the liquidityflows in the banking system to generate lendingactivities, as well as to ensure that viablebusinesses continued to receive financing at lowercost. Consequently, the SRR was reduced to 6%on 1 September, and then again to 4% on 16September. Similarly, the 3-month intervention ratewas reduced from 9.5% to 8% on 3 September,to 7.5% on 5 October, and to 7% on 9 November.As a result of the easing of monetary policy, theaverage BLR of the commercial banks and financecompanies declined further from 11.70% and 14.17%respectively in August 1998, to 8.04% and 9.50%by November.

The period of stability that followed was fullyutilised to expedite reform of the financial sectorthrough the institutional framework that was alreadyestablished. Targets set for Danamodal NasionalBerhad (Danamodal) and Pengurusan DanahartaNasional Berhad (Danaharta) were brought forward.As at 15 March 1999, Danaharta, the assetmanagement company, has acquired and ismanaging gross non-performing loans (NPLs) fromthe banking system amounting to RM15.1 billion.Danamodal, the special purpose vehicle torecapitalise the banking system, injected RM6.15billion in capital into 10 banking institutions andadditional injections are in the pipeline. TheCorporate Debt Restructuring Committee (CDRC)has received 48 applications involving debt totalling

RM22.7 billion. In the case of the small andmedium industries (SMIs), a rehabilitation fund wasalso set up in 1998, with an initial allocation ofRM750 million to provide financial assistance toSMIs which are viable but have temporary cashflow problems and NPLs. Amongst others, bankinginstitutions can utilise 30% of the total loansapproved under this Fund to replace and restructureproblem loans.

Throughout the crisis period, the Bank recognisedthe importance of ensuring the efficient functioningof the intermediation role of the banking institutions.However, given the protracted financial crisis andrising NPLs, the banking institutions placed greateremphasis on balance sheet considerations. Withrising NPLs and the erosion of capital, bankinginstitutions had become excessively cautious in theirlending decisions. A sharp slowdown in creditensued. A credit crunch, if allowed to develop,would deepen the economic recession, thuscompounding the financial difficulties of soundcompanies and subsequently affecting the health ofthe financial system. Hence, additional measureswere undertaken to encourage banking institutionsto continue to lend for productive purposes. Witheffect from 9 September 1998, banking institutionswith capacity were encouraged to achieve aminimum annual loan growth of 8% for 1998. Themotivation for the 8% credit floor was to free thebanking institutions from the self-imposed creditfreeze. The introduction of the credit growth target,however, did not sacrifice prudential consideration.Banking institutions were required to continueexercising financial discipline in providing creditand making their decisions withoutcompromising prudential standards to ensure thatthe balance sheets of the banking institutions donot deteriorate further. Nevertheless, bankinginstitutions should not unnecessarily complicate thecredit process, making it difficult for borrowers toobtain credit.

Other measures adopted to revive economicactivities of identified sectors included therelaxation of the earlier ceilings on the broadproperty sector and the share markets. Earlier rulesrestricting consumption credit imposed during theperiod of high credit growth were also relaxed.

On the whole, although there has been atendency to generalise the problems confronting theEast Asian region, there are important differences

in these economies that require alternative policyapproaches in dealing with the crisis. It is importantto recognise that there is no standard prescription.The approach adopted in Malaysia has differed fromthat of its neighbours in response to differencesthat exist in its financial and macroeconomicenvironment. Malaysia went into the crisis from aposition of favourable economic and financialfundamentals of a high savings rate, fullemployment, low external debt, a strong fiscalposition, and a strong and well-capitalised bankingsystem. These favourable initial conditions gaveMalaysia greater flexibility in its policy responseto the crisis and enabled the country to formulatea series of pre-emptive monetary and financialpolicy initiatives.

Fiscal Operations and Policy

The 1998 Budget was formulated in October 1997when Malaysia was in the initial phase of theregional crisis and was still experiencing robustgrowth. Fiscal policy during this period focused onstrengthening macroeconomic stability and restoringinvestor confidence. The policy aimed to addressthe key areas of vulnerabilities, including containinginflationary pressures arising from the ringgitdepreciation and addressing the current accountdeficit in the balance of payments. The fiscal policystance was therefore one of prudence and restraint.In line with these objectives, the Governmentbudgeted for a fiscal surplus of 2.7% of GNP inthe 1998 Budget. This was effected through restrainton consumption spending, the rightsizing of thepublic sector and the privatisation of Governmentactivities. Less critical projects were also deferredto narrow the resource gap. The Government,however, continued to provide essential expenditureto address supply constraints, raise productivity andenhance potential output. Priority was also accordedto poverty eradication programmes and upgradingthe quality of life.

In the wake of continued regional instability andits adverse impact on Federal revenue, theGovernment announced in December 1997, furtherfiscal austerity measures involving a reduction of10% across the board and 8% on a selective basis,of both operating and development expenditureallocations in the 1998 Budget. The cutback, washowever, implemented without affecting essentialpublic services, poverty eradication programmes andkey infrastructure development. As the crisis becamemore prolonged, this tight fiscal policy became

unsustainable. On 24 March 1998, the Governmentreversed the earlier policy and reduced the targetedbudget surplus to 0.5% of GNP as the contractionin the economy became evident in the first quarter.An additional expenditure of RM1 billion was alsoprovided for socio-economic projects to protect themore vulnerable segments of society.

The adjustment measures taken in terms ofrestrained fiscal and monetary policies in the earlypart of the crisis contributed towards improving thecurrent account of the balance of payments andcontaining price pressures. However, the publicsector expenditure cutbacks aggravated the declinein investor and consumer demand, causing a severedeflationary impact on the domestic economy. Giventhe change in economic conditions, the Governmentadopted counter-cyclical measures to revitalise thedomestic economy. The policy change aimed tominimise the severity of the economic downturn. InJuly 1998, the Government announced a fiscalstimulus package involving an additional allocationof RM7 billion for implementing projects with stronglinkages within the domestic economy; minimumleakage in terms of imports; short gestation period;and expenditures to meet socio-economic objectives.In this regard, the projects that were given priorityincluded those related to housing, education, health,and rural and infrastructure development. In addition,an Infrastructure Development Fund, with an initialallocation of RM5 billion was established to assistthe financing of infrastructure projects and largepublic facilities so that their implementation couldproceed. The projects identified included the mass-transit transportation system, ports, highways, watersupply and waste disposal as well as sewerageprojects. The Government also established orexpanded special funds to ensure continued accessto credit at reasonable costs for priority sectors.With the change in the fiscal policy stance, thefiscal account was estimated to have recorded adeficit of 3.7% of GNP in 1998.

After five years of fiscal surpluses, the 1999Budget, announced in October 1998, maintained afiscal deficit of 3.7% of GNP for 1998 and targetedfor an increase to 6.1% of GNP for 1999. Theexpansionary fiscal policy was designed to supporteconomic activities to promote economic recovery,to strengthen the nation’s resil ience andcompetitiveness, to restructure the financial sectorand to ensure social well-being. Although the thrustof budgetary operations was expansionary, fiscalprudence and discipline was being maintained to

contain the fiscal deficit at a manageable level soas not to jeopardise long-term growth. Theseobjectives are being achieved through budgetarycontrol on non-essential and non-productivespending, whilst according priority to infrastructureand socio-economic projects that could generateeconomic activities, promote efficiency, improvecompetitiveness and long-term productivity, but whichare low in import content. Emphasis was also beingplaced on an adequate programme to protect thelower income group and the poor from the adverseeffects of the crisis. Hence, a large share of the1999 Budget allocation was for public utilities,education and skills training and health and medicalservices. Emphasis was also being placed onagriculture and rural development and specialassistance schemes to assist the low-income group,petty traders and small businesses.

Given the prospect of weak revenue performancein 1999, the comprehensive plan to revitalise andrestructure the economy was carefully framed toensure that sufficient resources are available andthat the private sector would not be crowded out.The total financing requirement has been initiallyestimated at RM62 billion for 1998-99, to financethe recovery package including the fiscal deficit,restructuring of banking institutions and developmentof infrastructure. In view of the smaller overall fiscaldeficit of RM5 billion for 1998 (–RM9.6 billionestimated in the 1999 Budget), the total financingrequirement is now estimated to be lower at RM58billion for 1998-99. The financing requirement wouldbe raised from non-inflationary domestic sourcesand, to a lesser extent, from selective externalfinancing. In 1998, funding was largely met fromdomestic sources. For 1999, the bulk of the financingwould continue to be met from domestic sources.Besides new funds from the provident, pension andinsurance funds, there is sufficient liquidity in thebanking system. Additional liquidity would begenerated from the large current account surplusin the balance of payments recorded in 1998 andestimated for 1999. In order to avoid crowding outthe funding for the private sector, approximatelyone-third of the funding requirements would be metfrom external sources. The latter would comprisemainly loans from bilateral and multilateral sources.The Government would continue to ensure prudencein its recourse to external borrowing so as tomaintain the external debt at a manageable leveland to ensure favourable international credit ratings.The Government would continue to maintain a policyof containing the overall debt service ratio of thenation at a low level.

Throughout the crisis period, the Government haspersevered with its programme to reform andsimplify the tax system, provide a conduciveenvironment for investment, and enhancecompetitiveness and productivity. Tax measures thatwere implemented in 1998 and announced in the1999 Budget included the two percentage pointreduction in both the corporate and petroleumincome tax rates to 28% and 38% respectively,aimed at reducing the cost of doing business andproviding tax incentives to boost exports. Wide-ranging tax incentives and exemptions were alsointroduced to expedite the shift to higher value-added and technology-intensive industries, especiallyfor exports. These included tax exemption on theincrease in the export value. There was also areview of the reinvestment allowance to encourageindustries to move up the industrial ladder and anextension of research and development incentivesto accelerate the development of indigenoustechnology capability. In addition, incentives werealso introduced to promote the services sector toaddress the persistent services deficit in the balanceof payments. Comprehensive measures wereintroduced to strengthen the banking system andimprove transparency, while ensuring stability in thefinancial markets to facilitate trade and commerce.The measures included the introduction of severalprudential measures; the change in the tax treatmenton actuarial surplus; tax exemption (50%) forinterest-in-suspense; as well as the exemption ofstamp duty and real property gains tax on mergersof financial institutions. Meanwhile, the 1999 Budgetalso announced several changes in the taxadministration system to enhance its efficiency andresponsiveness in the collection of income tax. Mostimportant was the change in the tax assessment,which would now be based on income received inthe current year instead of the previous year basis,with effect from year 2000.

Consolidated Public Sector

The financial position of the consolidated publicsector weakened in 1998 largely attributable to thedeterioration in the revenue performance of theFederal Government and the increase inexpenditure, particularly by the non-financial publicenterprises (NFPEs). The consolidated public sectoraccount recorded an overall deficit compared withsignificant surpluses in 1996 and 1997. This largelyreflected the significant deterioration in the overallfinancial performance of the NFPEs as well as thegeneral government, in particular the FederalGovernment. In aggregate, the overall account of

the consolidated public sector recorded a deficit ofRM4.7 billion or 1.8% of GNP compared with alarge surplus of RM17.3 billion or 6.6% of GNP in1997. This is the first deficit recorded since 1993.The increase in development expenditure of thegeneral government was mainly to finance thestimulus package as well as for providing facilitiesand social amenities to the poor. The bulk of theexpenditure was mainly for education, health,housing, rural development and infrastructure.

The general government, comprising the FederalGovernment, 13 state governments, statutory bodiesand local governments continued to record a currentaccount surplus, albeit a much lower surplus ofRM19.5 billion or 7.4% of GNP (11.4% of GNP in1997). The lower surplus was mainly attributableto the decline in aggregate revenue collection(–12.4%), as operating expenditure remained virtuallyunchanged. Increased outlays were recorded mainlyfor debt servicing, the expansion of severaleducation funds and Fund for Food, as well asreactivating the Sinking Fund. However, theseoutlays were offset by the decline inother expenditures.

As in previous years, the surplus was mainlygenerated by the Federal Government and the state

Table 2.5Consolidated Public Sector Finance

1997 1998p 1999r

RM million

General government 1

Revenue 81,528 71,392 64,581Operating expenditure 51,884 51,896 54,852

Current surplus of general government 29,644 19,496 9,729

Current surplus of NFPEs 2 27,680 23,046 23,971

Public sector current surplus 57,324 42,542 33,700(% of GNP) 22.0 16.2 12.5

Net development expenditure 39,992 47,219 48,559General government 18,651 21,442 23,768NFPEs 2 21,341 25,777 24,791

Overall balance 17,332 –4,677 –14,859(% of GNP) 6.6 –1.8 –5.5

1Comprises Federal Government, state governments, statutory authoritiesand local governments.

2Refers to 28 NFPEs in 1997 and 1998 respectively.

p Preliminaryr Revised

Source: Ministry of Finance, state governments and non-financial publicenterprises

governments, while statutory bodies remained indeficit due to their narrow revenue base. Severalmajor public enterprises also experienced lessfavourable performances due mainly to higher costof operations and debt servicing arising from ringgitdepreciation during the year. As a result, theoperating surplus of the NFPEs was also reducedto RM23 billion or 8.8% of GNP (10.6% of GNPin 1997). Consequently, the consolidated publicsector current account recorded a reduced surplusof RM42.5 billion or 16.2% of GNP in 1998 (22%of GNP in 1997).

The public sector development expenditureincreased by 18.1% to RM47.2 billion in 1998(29.8% in 1997) due to the substantial increase incapital spending by the NFPEs (20.8%; 37.6% in1997), while the development outlays of the generalgovernment moderated to 15% (21.9% in 1997).Increases in development expenditure were recordedby several major NFPEs, including the PetroliamNasional Berhad (PETRONAS) and MalaysianInternational Shipping Corporation Berhad (MISC),mainly on project expansion and modernisationprogramme. A sizeable proportion of the capitalspending was also for the acquisition of companiesrelated to their core business, including investmentoverseas. However, due to the adverse economicdevelopments, several other NFPEs consolidatedtheir positions and deferred or scaled downdevelopment projects during the year.

Federal Government Finance

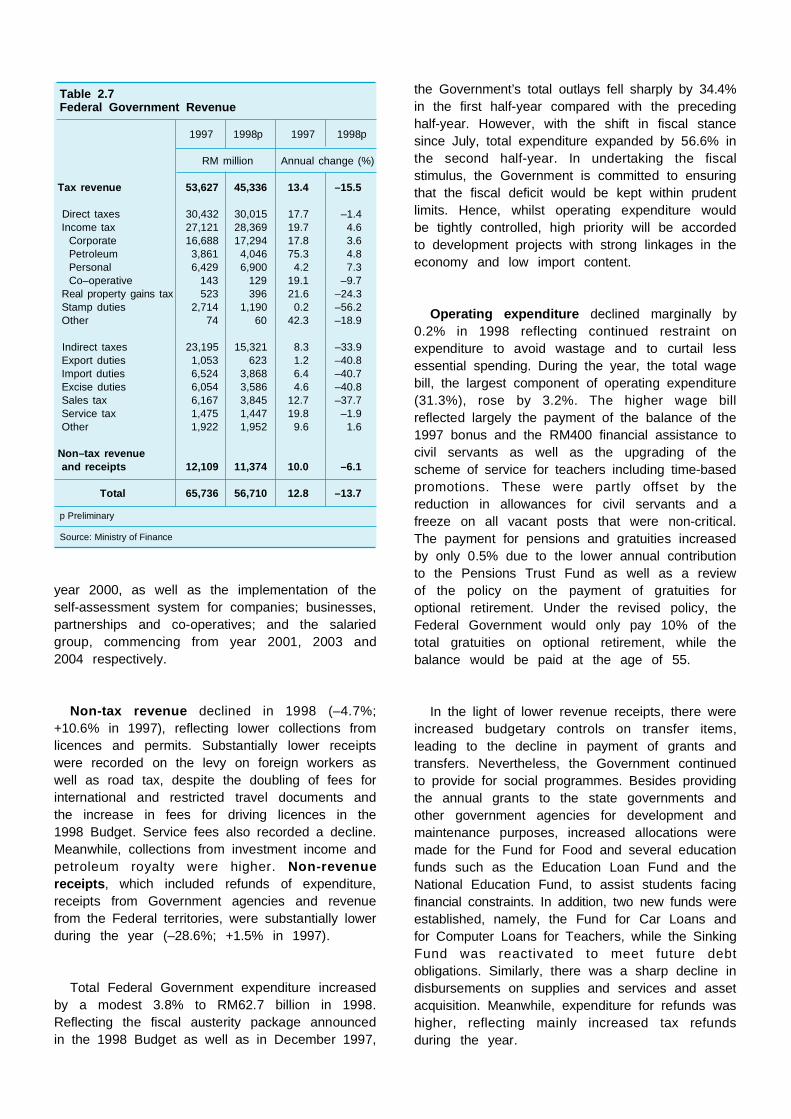

The financial position of the Federal Governmentwas less favourable in 1998 in the face of asubstantial decline in revenue as well as theimplementation of the fiscal stimulus package sinceJuly. The overall fiscal position reverted to a deficitof RM5 billion or –1.9% of GNP from a surplusof RM6.6 billion or 2.5% of GNP in 1997. This isthe first overall deficit since 1992. The currentaccount continued to remain in surplus, albeitsmaller, at RM12.1 billion or 4.6% of GNP (RM21billion or 8.1% of GNP in 1997).

In 1998, Federal revenue fell by 13.7% toRM56.7 billion or 21.6% of GNP, reflecting thecontraction in economic activity and weak domesticdemand. This decline also reflected the reductionin tax rates as well as several tax concessionsprovided in the 1998 Budget to promote productivity-driven growth and reduce the cost of doing

business. Revenue foregone from lower taxes wasestimated at about RM1.3 bill ion in 1998.Meanwhile, the marked decline in petroleum pricescoupled with the reduction in the rate of petroleumincome tax and export duty also affected receiptsfrom petroleum income tax, exports, imports andexcise duties which together with PETRONASdividends accounted for about one-fifth of totalrevenue (–5.1% to RM11.8 billion). In aggregate,revenue decline was recorded across the broadcategories of direct taxes (–RM417 million), indirecttaxes (–RM7.9 billion) and non-tax revenue andreceipts (–RM735 million).

For the first time since 1988, tax revenue fellby 15.5% to account for a lower share of 80% ofthe total Federal revenue. As a result, the ratio oftax receipts to GNP declined to 17.3% (20.5% in1997). Revenue from indirect taxes declinedsignificantly (–33.9%), thereby reducing its share to

Table 2.6Federal Government Finance

1997 1998p 1999r

RM million

Revenue 65,736 56,710 50,332Operating expenditure 44,665 44,584 47,220

Current surplus 21,071 12,126 3,112(% of GNP) 8.1 4.6 1.2

Development expenditure 14,445 17,128 19,202Gross development

expenditure 15,750 18,103 20,202Less Loan recoveries 1,305 975 1,000

Overall balance 6,626 –5,002 –16,090(% of GNP) 2.5 –1.9 –6.0

Sources of financing 1

Net domestic borrowing –2,048 11,040 –Gross borrowing 3,000 17,990 –Less Repayment 5,048 6,950 –

Net foreign borrowing –1,681 1,819 –Gross borrowing 462 4,001 –Less Repayment 2,143 2,182 –

Special receipts 91 1 –

Realisable assets 2 andadjustments –2,988 –7,858 –

Total –6,626 5,002 –

1Data for 1999 are not given.

2Includes changes in Government's Trust Fund balances. An increase in theaccumulated realisable assets is indicated by a minus (–) sign.

p Preliminaryr Revised

Source: Ministry of Finance

27% of total revenue. Reflecting the contraction indomestic demand and lower petroleum prices,almost all major categories of indirect taxes recordeddouble-digit declines. Receipts from import andexcise duties registered sizeable declines of 40.7%and 40.8% respectively. Lower collection of theseduties were apparent across the whole spectrum ofgoods, in particular, duties on motor vehicles andspare parts; petrol and petroleum products; electricalappliances and machinery. The poor performanceof import duties also reflected the sharp decelerationin import growth. The lower private sector spendingaffected sales tax collections (–37.7%), with lowerreceipts in all sub-sectors, especially transportequipment (including passenger, commercial and bus

vehicles). Meanwhile, the decline in the collectionof service tax was marginal (–1.9%) as wideningthe scope of the service tax in the 1998 Budgetto include services provided by employmentagencies, limousine and management services had,to some extent, offset the lower collection particularlyfrom professional services. The reduction in theexport duty on petroleum from 20% to 10% aswell as the lower crude oil prices also contributedto the lower collection from export duties. However,the decline was moderated somewhat by higherexport volume of crude petroleum.

Revenue from direct taxes recorded a lowerdecline (–1.4%) than receipts from indirect taxesand, hence increased its share of total revenue(53%; 46% in 1997). This was largely becauseincome tax collections were mainly based on theprevious year’s earnings which were still experiencingstrong growth in the first-half of 1997. Nevertheless,the rescheduling of some tax payments due tocorporate cashflow problems as well as the provisionof several tax concessions and incentives in the1998 Budget to enhance productivity and boostexports had moderated income tax collections. Thesefiscal measures included the two percentage pointreduction in corporate and petroleum income tax,and tax incentives to boost exports, promoteresearch and development, human resourcedevelopment and tax rebate for the purchase ofpersonal computers. On the whole, the higherreceipts from personal (+7.3%), petroleum (+4.8%)and corporate (+3.6%) income taxes were morethan offset by lower revenue collection from stampduties (–56.2%) and real property gains tax (–24.3%).The decline in these two taxes reflected lower pricesand volume of transactions in both the stock andproperty markets.

The sustained high level of income tax collectionduring the year was partly due to the increasednumber of taxpayers (+151,930 in 1998). It alsoreflected to some extent the success of the InlandRevenue Board (IRB) in widening the tax baseand its concerted efforts to strengthen the efficiencyof the tax collection machinery, improve complianceand ensure enforcement. Further measures wereintroduced in the 1999 Budget to increase theefficiency and responsiveness in the collection ofincome tax and to ensure that the cashflow of theGovernment reflects the current performance. Thisincluded the change in the tax assessmentbased on income received in the current yearinstead of the previous year basis, beginning from

-6-4-202468

101214

-6-4-202468101214

Net foreign borrowing

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

RM billion

Graph 2.7Federal Government Finance

1992 1993 1994 1995 1996 1997 1998

Development expenditure

Current revenue

Operating expenditure

-2-10123456789

10

-2-1012345678910

RM billion

Net domestic borrowing

1992 1993 1994 1995 1996 1997 1998

1992 1993 1994 1995 1996 1997 1998

Market loansGovernment securities Investment issues

-5

-4

-3

-2

-1

0

1

2

-5

-4

-3

-2

-1

0

1

2

Market loans

Other loans

1992 1993 1994 1995 1996 1997 1998

Total net borrowing

Overall deficit/surplus

year 2000, as well as the implementation of theself-assessment system for companies; businesses,partnerships and co-operatives; and the salariedgroup, commencing from year 2001, 2003 and2004 respectively.

Non-tax revenue declined in 1998 (–4.7%;+10.6% in 1997), reflecting lower collections fromlicences and permits. Substantially lower receiptswere recorded on the levy on foreign workers aswell as road tax, despite the doubling of fees forinternational and restricted travel documents andthe increase in fees for driving licences in the1998 Budget. Service fees also recorded a decline.Meanwhile, collections from investment income andpetroleum royalty were higher. Non-revenuereceipts, which included refunds of expenditure,receipts from Government agencies and revenuefrom the Federal territories, were substantially lowerduring the year (–28.6%; +1.5% in 1997).

Total Federal Government expenditure increasedby a modest 3.8% to RM62.7 billion in 1998.Reflecting the fiscal austerity package announcedin the 1998 Budget as well as in December 1997,