iv. monetary developments - national bank of ethiopia 21 q2/financial... · · 2009-08-25iv....

TRANSCRIPT

IV. MONETARY DEVELOPMENTS

During the second quarter of 2005/06, ensuring price and exchange rate stability as well as maintaining conducive macroeconomic environment for economic growth, continued to be the focal policy of the National Bank of Ethiopia (NBE). It also continued to use both direct and indirect monetary policy instruments to achieve its stated objectives.

4.1. Money Supply and Credit

At the close of the second quarter of 2005/06, domestic liquidity as measured by broad money (M2), reached Birr 42.1 billion,

reflecting quarterly and annual growth rates of 0.6 and 17.3 percent, respectively. The marginal quarterly expansion in broad money supply came largely due to a rise of 12.2 percent in credit to non-government sectors, which was sufficient enough to absorb the drop in net foreign assets (NFA) of the banking system by 6.1 percent. Similarly, the year-on-year basis increase in broad money was attributable to the expansion in domestic credit by 34.7 percent, which offset the 9.0 percent draw down in net foreign assets. Claims on the non-government sector indicated a significant annual rise of 41.9 percent, owing to increase in disbursement of new loans and purchases of corporate bonds by CBE

Table IV. 1 : Factors Influencing Broad Money(In Millions of Birr

Particulars 2004/05 2005/06 Percentage ChangeQtr. II Qtr. I Qtr. II

(Dec. 04) (Sept. 05) (Dec. 05) C/A C/BA B C

1. External Assets (net) 13,590.5 13,179.7 12,371.1 -9.0 -6.12. Domestic Credit 34,343.4 43,711.8 46,246.1 34.7 5.8 . Claims on Central Gov't (net) 19,076.5 24,482.4 24,665.2 29.3 0.7 . Claims on Non-Central Gov't 15,266.8 19,229.4 21,580.9 41.4 12.2 . Financial Institutions 53.7 0.0 0.0 . Others 15,213.1 19,229.4 21,580.9 41.9 12.23. Other Items (net) 12,051.9 15,058.3 16,518.3 37.1 9.74. Broad Money (M2) 35,882.0 41,833.2 42,098.9 17.3 0.6

Source: National Bank of Ethiopia

Looking at the components of broad money, M1 (the sum of currency outside banks and net demand deposits) reached Birr 21.2

billion, indicating a marginal fall of 0.9 percent as a result of a 2.3 percent decline in demand deposits which outstripped the slight rise of 0.7 percent in currency outside banks. The draw-down in demand deposits was attributed to the seasonality of business activities related to the harvesting season that begins in December when more cash is needed to undertake transactions. On the other hand, quasi-money (the sum of time and savings deposits) surged by 2.3 percent during the same period. Year-on-year basis, both M1

and quasi money surged by 13.6 percent and 21.3 percent, respectively.

Table IV.2 : Components of Broad Money

(In Millions of Birr)Particulars 2004/05 2005/06 Percentage Change

Qtr. II Qtr. I Qtr. II(Dec. 04) (Sept. 05) (Dec. 05) C/A C/B

A B C 1. Narrow Money Supply 18,662.9 21,406.7 21,205.8 13.6 -0.9 . Currency outside banks 8,274.5 9,552.7 9,623.3 16.3 0.7 . Demand Deposits (net) 10,388.4 11,854.0 11,582.5 11.5 -2.32. Quasi-Money 17,219.1 20,426.5 20,893.1 21.3 2.3 . Savings Deposits 15,849.0 18,711.9 19,122.9 20.7 2.2 . Time Deposits 1,370.2 1,714.6 1,770.2 29.2 3.23. Broad Money Supply 35,882.0 41,833.2 42,098.9 17.3 0.6

Source: National Bank of Ethiopia

4.2 Developments in Reserve Money and Monetary Ratios

At the end of the second quarter of 2005/06, reserve money (the sum of currency in circulation and deposits of commercial banks at the National Bank of Ethiopia), reached Birr 24.2 billion indicating a slight quarterly decline of about 1.5 percent and an annual increase of 6.9 percent. The fall in commercial banks' reserve at the National Bank of Ethiopia (NBE) was the main factor for the quarterly drop in reserve money.

Table IV. 3 : Monetary Aggregates and Ratios (In millions of Birr unless otherwise indicated)

2004/05 2005/06 Qtr. II Qtr. I Qtr. II Percentage Change

(Dec. 04) (Sept. 05) (Dec. 05)Particulars A B C C/A C/B

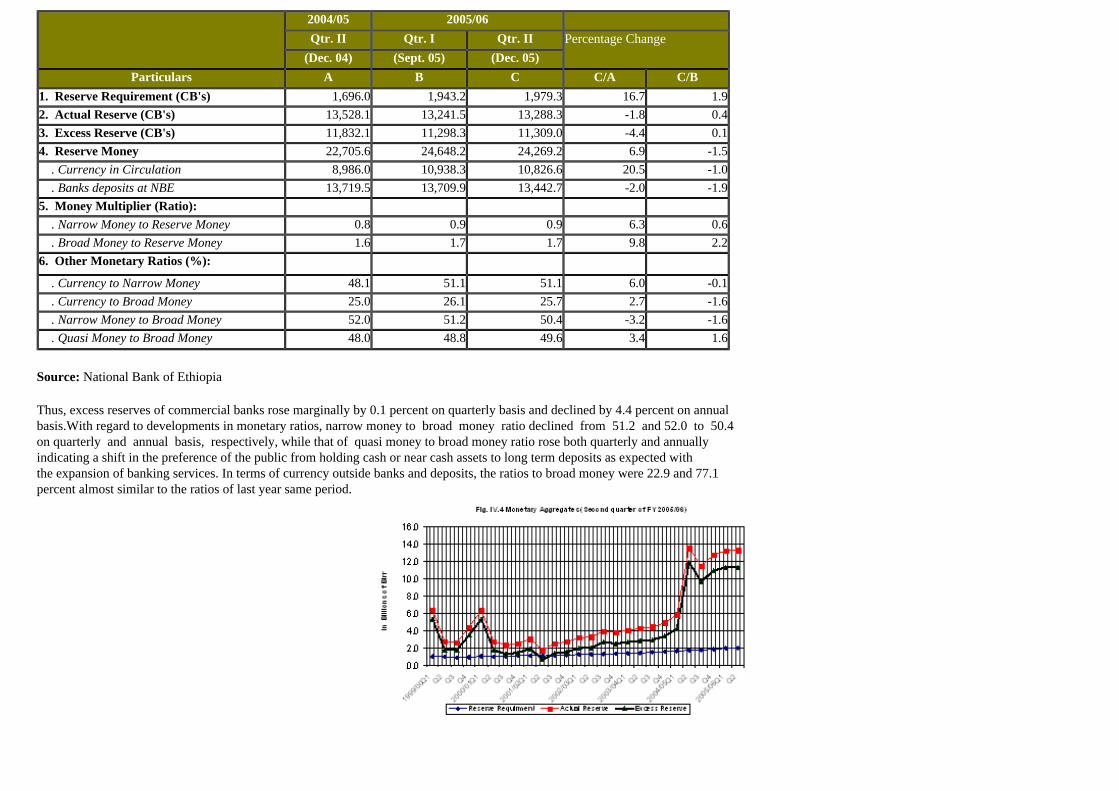

1. Reserve Requirement (CB's) 1,696.0 1,943.2 1,979.3 16.7 1.92. Actual Reserve (CB's) 13,528.1 13,241.5 13,288.3 -1.8 0.43. Excess Reserve (CB's) 11,832.1 11,298.3 11,309.0 -4.4 0.14. Reserve Money 22,705.6 24,648.2 24,269.2 6.9 -1.5 . Currency in Circulation 8,986.0 10,938.3 10,826.6 20.5 -1.0 . Banks deposits at NBE 13,719.5 13,709.9 13,442.7 -2.0 -1.95. Money Multiplier (Ratio): . Narrow Money to Reserve Money 0.8 0.9 0.9 6.3 0.6 . Broad Money to Reserve Money 1.6 1.7 1.7 9.8 2.26. Other Monetary Ratios (%):

. Currency to Narrow Money 48.1 51.1 51.1 6.0 -0.1 . Currency to Broad Money 25.0 26.1 25.7 2.7 -1.6 . Narrow Money to Broad Money 52.0 51.2 50.4 -3.2 -1.6 . Quasi Money to Broad Money 48.0 48.8 49.6 3.4 1.6

Source: National Bank of Ethiopia

Thus, excess reserves of commercial banks rose marginally by 0.1 percent on quarterly basis and declined by 4.4 percent on annual basis.With regard to developments in monetary ratios, narrow money to broad money ratio declined from 51.2 and 52.0 to 50.4 on quarterly and annual basis, respectively, while that of quasi money to broad money ratio rose both quarterly and annually indicating a shift in the preference of the public from holding cash or near cash assets to long term deposits as expected with the expansion of banking services. In terms of currency outside banks and deposits, the ratios to broad money were 22.9 and 77.1 percent almost similar to the ratios of last year same period.

4.3 Interest Rate Developments

There were no substantial changes in the interest rate structure of commercial banks during the second quarter of 2005/06. Average savings deposit rate remained at the preceding quarter level of 3.08 percent while the weighted demand deposit rate slightly declined to 0.05 percent from 0.06 percent during the preceding quarter. Average interest rate on time deposits also went down and reached 3.73 percent in contrast to 3.74 percent a quarter earlier. On the other hand, average lending rate was 10.5 percent, remaining unchanged since March 2003. Considering the 7.2 percent average annual core (non-food) inflation registered during December 2005, deposit interest rates, weighted average yields on T-bills and government bond yields all were negative in real terms. Average real cost of borrowing (real lending rate), however, was positive (3.3 percent). The National bank of Ethiopia, after analyzing the situation has decided not to change the nominal interest rate.

Table IV.4: Interest Rate Structure of Commercial Banks(Percent per Annum)

Particulars 2004 2005

Mar. June Sep. Dec. Mar. June Sep. Dec. 1.Saving Deposit Rates ● Minimum 3 3 3 3 3 3 3 3● Maximum 3.15 3.15 3.15 3.15 3.15 3.15 3.15 3.15Average Saving Rate 3.08 3.08 3.08 3.08 3.08 3.08 3.08 3.082.Time Deposit Rates (Weighted) ● Up to 1 year 3.39 3.4 3.36 3.38 3.452 3.47 3.49 3.48● 1 – 2 years 3.63 3.64 3.6 3.64 3.69 3.71 3.74 3.73● Over 2 years 3.83 3.84 3.81 3.86 3.92 3.94 3.99 3.99Average Time Dep. Rate 3.62 3.62 3.59 3.63 3.69 3.71 3.74 3.733. Weighted Demand Deposit Rate 0.04 0.05 0.04 0.02 0.05 0.05 0.06 0.05

4. Lending Rate ● Minimum 7 7 7 7 7 7 7 7● Maximum 14 14 14 14 14 14 14 14Average Lending Rate 10.5 10.5 10.5 10.5 10.5 10.5 10.5 10.55. Weighted Ave. T-bills Rate 0.69 0.53 0.23 0.12 0.07 0.05 0.04 0.046. Inter-bank Rates - 7.5 - - - - - - 7. Average Bond Yield* 3.78 3.78 3.78 3.71 4 4 4 4Source: Commercial Banks and National Bank of Ethiopia NB: *Shows average bond yield on outstanding government bonds

4.4 Activities of the Banking System

4.4.1. Resource Mobilization

A) Deposit Mobilization

Deposit liabilities of the banking system reached Birr 41.6 billion at the end of second quarter of 2005/06, reflecting quarterly and annual growth rates of 2.2 and 21.4 percent, respectively.

Component wise, all types of deposit tended to increase. Demand deposits at Birr 20 billion accounted for 48.1 percent of the total deposits. They surged by 2.2 percent over the previous quarter and by 22.4 percent vis-à-vis the same quarter of last fiscal year. Savings deposit with 46.0 percent share in total deposits reached Birr 19.1 billion, indicating quarterly and annual growth rates of 2.2 and 20.7 percent, respectively. Similarly, time deposits of Birr 2.45 billion constituted 5.9 percent of the total deposits and surged by 2.5 percent and 18.9 percent vis-à-vis the previous quarter and the same quarter of the preceding year, respectively.

The share of Commercial Bank of Ethiopia (CBE) in total deposits of the banking system stood at 68.4 percent while private banks altogether accounted for 27.5 percent, indicating increases in their market share of 24.1 percent a year earlier. The

remaining balance constituted deposit liabilities of the two other public banks, i.e. Construction & Business Bank (CBB) and Development Bank of Ethiopia (DBE).

B) Collection of Loans

During the second quarter of 2005/06, collection of loans by the banking system totaled Birr 2,040.4 million, reflecting a quarterly slowdown of 12.9 percent. This was attributed to the 33.1 percent decline in collection by public owned banks that offsets the 12.9 percent rise in collection of private banks. Sector wise, domestic and international trade sub-sectors accounted for Birr 1,163.8 (57.0 percent) of the loan settlement followed by industry with Birr 276.4 million (13.5 percent). In terms of collecting banks, CBE collected Birr 744.0 million (37.0 percent) of the total loan repayments. Meanwhile, private banks jointly collected Birr 1,160.1 million (57.6 percent) reflecting 12.9 percent growth rate vis-à-vis its share of 43.8 percent during the preceding quarter. Construction & Business Bank and Development Bank of Ethiopia together collected the remaining 6.8 percent.

C) Borrowing

At the end of December 2005, outstanding borrowings of the banking system (CBB and DBE) reached Birr 1,786.2 million, reflecting a quarterly decline of 5.6 percent and an annual increase of 22.4 percent. About 82.1 percent of the outstanding borrowing was mobilized from domestic sources and the balance from external sources. Development Bank of Ethiopia constituted 93.8 percent of the outstanding borrowing and the balance was taken up by Construction & Business Bank.

Table IV 5. Outstanding Borrowing by Source

(In Million of Birr)

Banks 2004/05 2005/06Quarter II Quarter I Quarter II

Internal External Total Internal External Total Internal External TotalDBE 1019.3 284.3 1303.6 1426.8 345.5 1772.3 1355.4 319.9 1675.3CBB 155.4 0 155.4 119.1 0 119.1 110.9 0 110.9Grand Total 1174.7 284.3 1459 1545.9 345.5 1891.4 1466.3 319.9 1786.2

Table IV 6 : Stock of Deposits Mobilized by the Banking System as at end of December 31, 2005

(In Millions of Birr)

Types of Deposit 2004/05 2005/06 % ChangeQuarter II % Share Quarter I % Share Quarter II % Share

(A) (B) (C) C/B C/A

Demand Deposit 16,337.1 47.7 19,585.4 48.1 20,006.2 48.1 2.2 22.4

Saving Deposit 15,851.3 46.3 18,709.5 46.0 19,125.7 46.0 2.2 20.7

Time Deposit 2,060.4 6.0 2,390.9 5.6 2,450.0 5.9 2.5 18.9

Total 34,248.8 40,685.8 41,584.7 2.2 21.4

Table IV 7: Summary of Resource Mobilization & Disbursement of the Banking System During the Second Quarter of 2005/06 ended on 31, December 2005 Birr

Particulars Total Public Banks Total Private Banks Grand Total

(1) (2) (3) =(1)+(2)

Qtr. I Qtr. II % Change Qtr. I Qtr. II % Change Qtr. I Qtr. II % Change

1.Deposits (net change) 917.0 467.0 (49.1) 1,253.4 429.4 (65.7) 2,170.4 896.4 (58.7)

-Demand 159.7 372.7 133.4 506.3 48.4 (90.4) 666.0 421.1 (36.8)

-Saving 778.0 70.9 (90.9) 620.1 345.3 (44.3) 1,398.1 416.2 (70.2)

-Time (20.7) 23.4 (212.9) 127.0 35.7 (71.9) 106.3 59.1 (44.4)

2. Borrowing (net change) 124.8 (105.2) (184.2) - - - 124.8 -105.2 (184.2)

-Local 63.6 (79.6) (225.0) - - - 63.6 -79.6 (225.0)

-Foreign 61.2 (25.6) (141.8) - - - 61.2 -25.6 (141.8)

3. Collection of Loans 1,316.3 880.3 (33.1) 1,027.2 1,160.1 12.9 2,343.5 2,040.4 (12.9)

4. Total Resources Mobilized (1+2+3) 2,358.2 1,242.2 (47.3) 2,280.6 1,589.5 (30.3) 4,638.7 2,831.7 (39.0)

5. Disbursement 909.5 1,631.8 79.4 1,326.7 1,969.9 48.5 2,236.1 3,601.7 61.1

6. Change in Liquidity (4-5) 1,448.7 (389.6) (126.9) 953.9 (380.4) (139.9) 2,402.6 -770.0 (132.0)

Memorandum Item:

A. Outstanding Credit 21,060.5 27,332.9 29.8 8,825.9 9,591.6 8.7 29,886.4 36,924.4 23.5

B. Outstanding Inter bank Lending 340.2 278.5 (18.1) - - - 305.0 278.5 (8.7)

4.4.2 Disbursement of Fresh Loans

The banking system disbursed a total of Birr 3,601.7 million fresh loans to the various sectors of the economy during the second quarter of 2005/06. This was 61.1 and 37.4 percent higher than the amount disbursed during the preceding quarter and same quarter of 2004/05, respectively. The private sector, received Birr 3,544.7 million (or 98.4 percent) of the total new loans disbursed during the quarter. In terms of economic sectors, fresh loans disbursed to international and domestic trade amounted to Birr 1,756.2 million (48.8 percent of total disbursement). Meanwhile, Birr 952.2 million (26.4 percent) was disbursed to agriculture, the dominant sector of the economy.

4.4.3 Outstanding Credit

The stock of outstanding credit of the banking system reached Birr 36.9 billion at the end of the second quarter of 2005/06, indicating a quarterly and annual increase of 23.5 and 39.7 percent, respectively. Of the total outstanding loans, claims on the private sector accounted for 58.2 percent while claims on government 32.0 percent. In terms of economic sectors, industry took 16.2 percent and international trade 12.4 percent. Other major recipient sectors include domestic trade, agriculture and transport & communication.

Table IV 8: Summary of Loans and Advances by Banks and Receiving Sectors during October- December 2005 (in Million Birr)

Borrowing Sector

Total Public Banks Total Private Banks Grand Total Private & Public Banks

(1) (2) (3) =(1+2)

Disbursed Collected O/S Disbursed Collected O/S Disbursed Collected O/S

Central Government * 11,212.9 - - 589.0 - - 11,801.9

Agriculture 863.1 96.9 3,069.0 89.1 15.4 343.1 952.2 112.2 3,412.1

Industry 80.9 128.0 4,290.2 215.6 148.3 1,674.7 296.5 276.4 5,964.9

Domestic Trade 212.8 128.9 976.9 626.1 286.3 2,170.5 838.8 415.3 3,147.4

International Trade 286.6 327.2 2,058.0 630.8 421.4 2,535.2 917.3 748.6 4,593.2

Export 89.4 66.7 504.9 395.1 199.4 962.1 484.5 266.1 1,467.0

Imports 197.1 260.5 1,553.1 235.7 221.9 1,655.8 432.8 482.4 3,208.9

Hotels and Tourism 9.0 14.9 341.8 6.7 4.3 39.7 15.7 19.1 381.5

Transport & Communication 37.8 16.8 403.8 132.0 88.4 632.5 169.8 105.2 1,036.3

Housing & Construction 95.1 66.5 1,523.7 170.6 84.4 1,119.0 265.6 150.9 2,642.7

Mines, Power & Water Resources - - 30.5 - - - - - 30.5

Others 15.4 45.2 3,093.3 85.7 99.7 373.3 101.0 144.9 3,466.6 Personal 31.2 22.6 54.3 13.5 11.9 32.0 44.7 34.5 86.3 Inter-Bank Lending - 33.4 278.5 - - - - 33.4 278.5 Total 1,631.8 880.3 27,332.9 1,969.9 1,160.1 9,591.5 3,601.7 2,040.4 36,924.4

*Refers to government bonds and Treasury bills holdings

Table IV. 9 Breakdown of Loans & Advances of the Banking System by Clients,

for the Second Quarter of 2005/06 ended December 2005.

(In Millions of Birr)

Particulars Disbursement Collection Outstanding

1. Public Banks 1,631.8 880.3 27,332.9

Central Government* - - 11,212.9 State Enterprises 57.0 91.7 3,319.2 Cooperatives 895.8 125.1 1,764.5

Private Enterprises 679.0 630.1 10,757.8 Inter-bank Lending - 33.4 278.5 2. Private Banks 1,969.9 1,160.1 9,591.5 Central Government* - - 589.0

State Enterprises - 1.0 19.9

Cooperatives 76.2 5.6 110.8

Private Enterprises 1,893.7 1,153.5 8,871.8

Inter-bank Lending - - -

3.Grand Total 3,601.7 2,040.4 36,924.4 Note: *Refers to government bonds and Treasury bills holdings

4.5 Financial Activities of the National Bank of Ethiopia

National Bank of Ethiopia’s claims on the central government in the form of direct advance and bonds reached Birr 28.2 billion at he end of the second quarter of 2005/06, indicating quarterly and annual growth rates of 13.3 and 9.1 percent, respectively. Meanwhile, NBE’s deposit liabilities to the government and domestic financial institutions reached Birr 18.7 billion showing a

0.6 percent quarterly marginal decline and an annual increase of 1.8 percent.

Table IV.10: Financial Activities of the National Bank of Ethiopia During the Second Quarter of 2005/06(In Millions of Birr)

Particulars

2004/05 2005/06 % ChangeQtr.II Qtr.I Qtr.II

A B C C/A C/B1.Loans and Advances 22,779.9 24,842.2 28,151.1 9.1 13.3 1.1. To Central Government 22,726.2 24,842.2 28,151.1 9.3 13.3 - Direct Advance 12,638.0 16,427.1 18,111.0 30.0 10.3 - Bonds 10,088.2 10,040.1 10,040.1 (0.5) - 1.2.To Development Bank of Ethiopia

53.7 - - (100.0) -

2.Deposit Liabilities 18,453.8 18,781.6 18,671.6 1.8 (0.6) 2.1. Government 4,629.9 4,836.2 5,058.6 4.5 4.6 2.2. Financial Institutions 13,823.9 13,945.4 13,613.0 0.9 (2.4) O/W: -Banks 13,785.6 13,915.2 13,582.7 0.9 (2.4) -Insurance companies 38.3 30.2 30.3 (21.1) 0.3

4.

4.6 Developments in Financial Markets

a) Treasury Bills Market

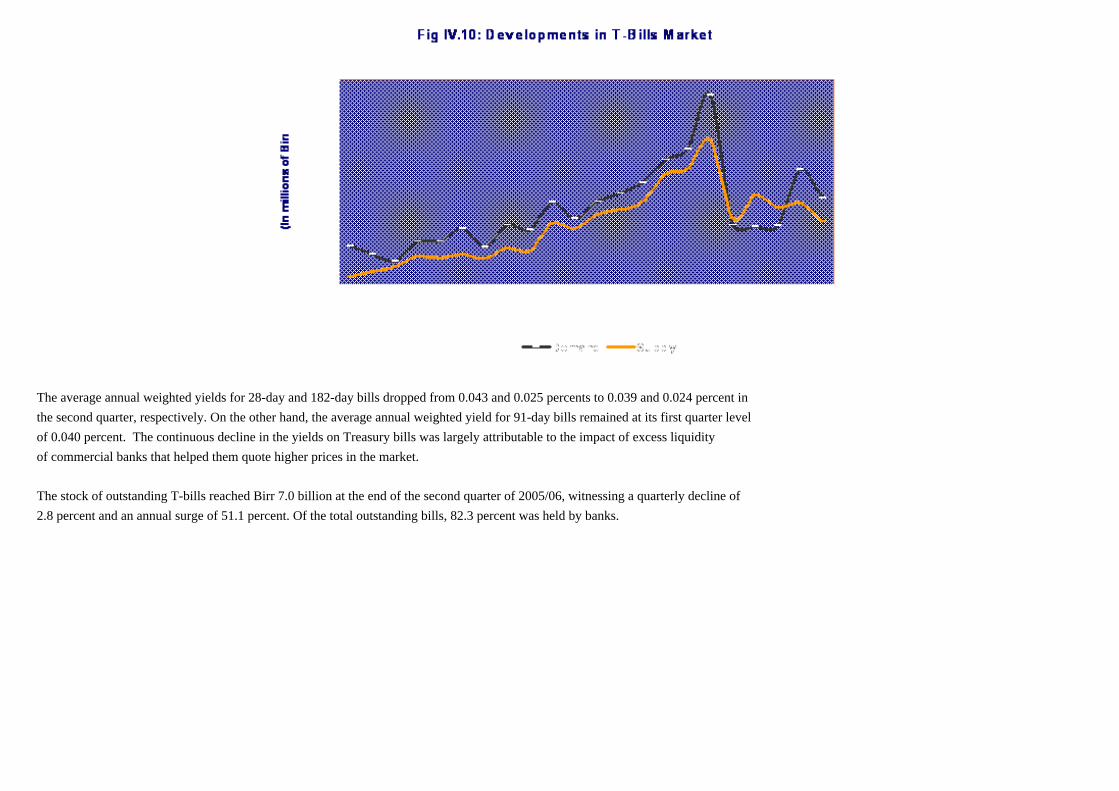

During the second quarter of 2005/06, Treasury bills worth of Birr 8.6 billion were offered in the fortnightly auction market. This was 21.7 percent lower than the amount offered during the preceding quarter and 40.8 percent higher than the amount supplied during the same quarter of 2004/05. On the other hand, T-bills worth of Birr 11.6 billion were demanded in the market, of which, about 73.5 percent was satisfied. In coherent with the movements of amount supplied, demand for treasury bills dropped by 24.5 percent on quarterly but increased by 39.6 percent on annual basis.

The average annual weighted yields for 28-day and 182-day bills dropped from 0.043 and 0.025 percents to 0.039 and 0.024 percent in the second quarter, respectively. On the other hand, the average annual weighted yield for 91-day bills remained at its first quarter level of 0.040 percent. The continuous decline in the yields on Treasury bills was largely attributable to the impact of excess liquidity of commercial banks that helped them quote higher prices in the market.

The stock of outstanding T-bills reached Birr 7.0 billion at the end of the second quarter of 2005/06, witnessing a quarterly decline of 2.8 percent and an annual surge of 51.1 percent. Of the total outstanding bills, 82.3 percent was held by banks.

Table IV 11: Results of Treasury Bills Auction

Particulars 2004/05 2005/06 % Change

Qtr.II Qtr.I Qtr.II

A B C C/A C/B

Number of Bidders 50 59 45 -10.00 -23.73

Private 37 34 32 -13.51 -5.88

Public 13 25 13 0.00 -48.00

Number of Bids Accepted 55 72 45 -18.18 -37.50 Private 36 35 32 -11.11 -8.57

Public 19 37 13 -31.58 -64.86

Amount Demanded (Mn.Birr)

8,861.50 15,414.50 11,642.50 31.38 -24.47

28-day bill 5,017.00 9,624.50 7,676.50 53.01 -20.24

91-day bill 2,414.50 3,074.00 2,515.00 4.16 -18.18

182-day bill 1,430.00 2,716.00 1,451.00 1.47 -46.58

Amount Supplied (Mn.Birr) 6,082.00 10,925.50 8,560.50 40.75 -21.65

28-day bill 3,441.00 6,514.50 5,314.50 54.45 -18.42

91-day bill 1,600.00 2,405.50 2,205.00 37.81 -8.34

182-day bill 1,041.00 2,006.00 1,041.00 0.00 -48.11

Amount Sold (Mn.Birr) 5,884.00 10,925.50 8,560.50 45.49 -21.65

Banks 5,071.00 10,075.50 8,015.50 58.07 -20.45

Non-Banks 813.00 850.00 545.00 -32.96 -35.88

Average Weighted Price for Successful bids(Birr)

28-day bill 99.98 99.997 99.997 0.02 0.00 91-day bill 99.95 99.989 99.989 0.04 0.00 182-day bill 99.96 99.987 99.988 0.03 0.00

Average Weighted Yield for Successful bids (%)

28-day bill 0.3 0.043 0.039 -86.98 -9.18 91-day bill 0.21 0.044 0.044 -79.02 0.14 182-day bill 0.1 0.025 0.024 -75.97 -3.86

Outstanding bills at the end of Period (Mn.Br.)

4,649.50 7,223.50 7,023.50 51.06 -2.77

Banks 3,711.00 6,003.50 5,778.50 55.71 -3.75

Non-Banks 938.5 1,220.00 1,245.00 32.66 2.05

b) Inter- Bank Money Market

No inter-bank money market was held during the quarter under review as virtually all commercial banks carried excess reserve. Since its introduction some five years ago merely thirteen transactions involving Birr 186.7 million were conducted among few commercial banks with an interest rate ranging between 7 and 11 percent. The maturity period of these loans widely ranged from overnight to 5 years.

No. Borrower

Lender

Amount Borrowed (In Mn.Br.)

Interest rate charged (%)

Transaction Date Maturity Period

1 Nib International Bank Awash International Bank 7.0 11 16/11/00 Overnight

2 Wegagen Bank CBE 10.0 8 03/01/01 5 years

3 Nib Int.l Bank ,, 10.0 8 31/03/01 3 months

4 Wegagen Bank ,, 10.0 8 22/03/01 1 year

5 Nib Int. ,, 3.6 8 31/05/01 6 months

6 Nib Int. Bank ,, 3.7 8 31/06/01 6 months

7 Nib Int. Bank ,, 0.8 8 30/11/01 6 months

8 Nib Int. Bank Bank of Abyssinia 29.0 7 31/12/02 3.5 months

9 Nib Int. Bank ,, 19.0 7 31/01/03 3.5 months

10 Nib Int. Bank ,, 20.3 7 28/02/03 3.5 months

11 Nib Int. Bank ,, 28.3 7 31/03/03 3.5 months

12 Nib Int. Bank CBE 25.0 7.5 07/07/03 5.2 month

13 Nib Int. Bank Bank of Abyssinia 20.0 7.5 26/03/05 Over draft

Total/Average 186.7 7.8

B) Collection of Loans

During the first quarter of 2005/06, loan collection by the banking system reached Birr 2,342.9 million, reflecting a quarterly increase of 19.5 percent. International trade accounted for 33.5 percent of the loan repayment followed by domestic trade (19.6 percent). In terms of collecting banks, CBE claimed 48.3 percent while all the six private banks jointly collected 43.8 percent, and Construction & Business Bank and Development Bank of Ethiopia, together, 7.9 percent.

C) Borrowing

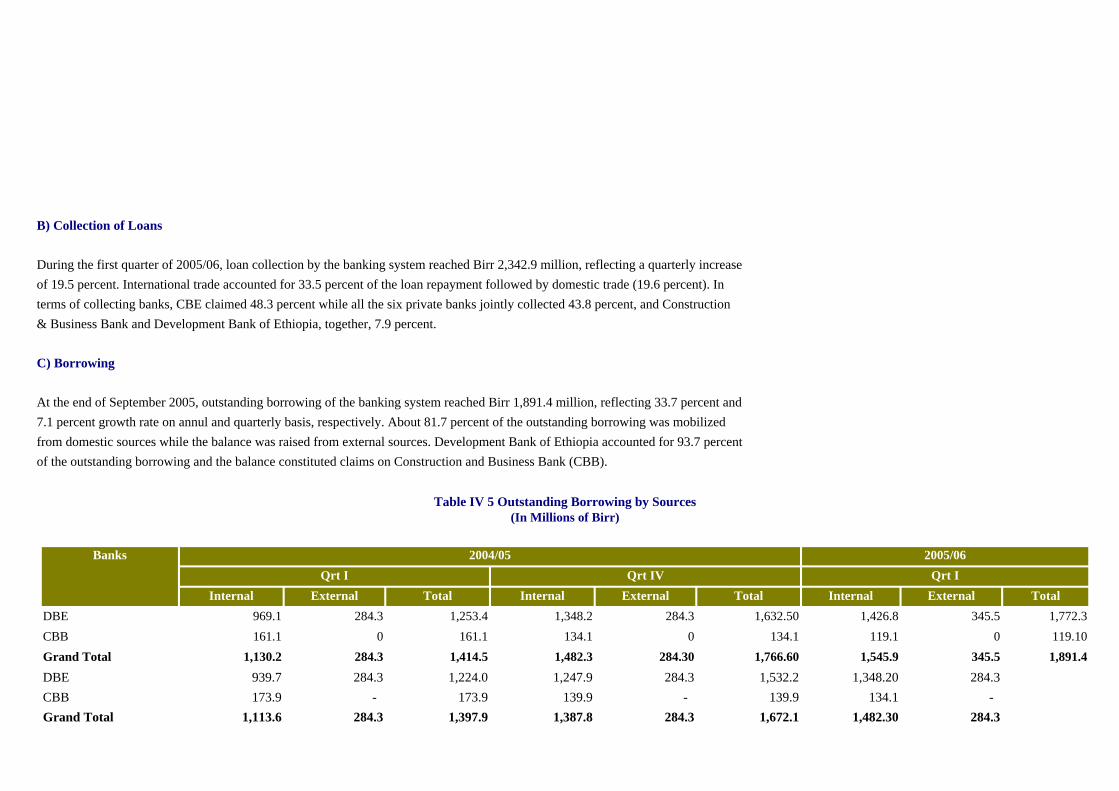

At the end of September 2005, outstanding borrowing of the banking system reached Birr 1,891.4 million, reflecting 33.7 percent and 7.1 percent growth rate on annul and quarterly basis, respectively. About 81.7 percent of the outstanding borrowing was mobilized from domestic sources while the balance was raised from external sources. Development Bank of Ethiopia accounted for 93.7 percent of the outstanding borrowing and the balance constituted claims on Construction and Business Bank (CBB).

Table IV 5 Outstanding Borrowing by Sources (In Millions of Birr)

Banks 2004/05 2005/06Qrt I Qrt IV Qrt I

Internal External Total Internal External Total Internal External TotalDBE 969.1 284.3 1,253.4 1,348.2 284.3 1,632.50 1,426.8 345.5 1,772.3CBB 161.1 0 161.1 134.1 0 134.1 119.1 0 119.10Grand Total 1,130.2 284.3 1,414.5 1,482.3 284.30 1,766.60 1,545.9 345.5 1,891.4DBE 939.7 284.3 1,224.0 1,247.9 284.3 1,532.2 1,348.20 284.3CBB 173.9 - 173.9 139.9 - 139.9 134.1 - Grand Total 1,113.6 284.3 1,397.9 1,387.8 284.3 1,672.1 1,482.30 284.3

Table IV 6: Summary of Resource Mobilization & Disbursement of the Banking System

(In Millions of Birr)

Particulars Total Public Banks Total Private Banks Grand Total

(1) (2) (3) =(1)+(2)Qtr. IV Qtr. I % Change Qtr. IV Qtr. I % Change Qtr. IV Qtr.I % Change

1.Deposits (net change) 1,236.2 918.4 (25.7) 673.7 1,253.4 86.1 1,909.9 2,171.8 13.7 -Demand 540.6 164.7 (69.5) 189.2 506.3 167.6 729.8 671.0 (8.1)-Saving 686.9 778.0 13.3 370.1 620.1 67.5 1,057.0 1,398.1 32.3 -Time 8.7 (24.3) (378.8) 114.4 127.0 11.0 123.1 102.7 (16.6)

2. Borrowing (net change) 94.5 518.7 448.9 - - - 94.5 518.7 448.9-Local 94.5 457.7 384.3 - - - 94.5 457.7 384.3

-Foreign 0 61 0.0 - - - - 61 0.0 3. Collection of Loans 859.2 1,026.6 19.5 1,100.8 1316.3 19.6 1,960.00 2,342.9 19.5 4. Total Resources Mobilized (1+2+3) 2,189.90 2,463.70 12.5 1,774.5 2,569.7 44.8 3,964.40 5,033.4 27.0 5. Disbursement 852.9 909.5 6.6 1,129.3 1,315.0 16.4 1,982.30 2,224.5 12.2

6. Change in Liquidity (4-5) 1,337.00 1,120.8 -16.2 645.2 1,254.7 94.5 1,982.10 2,375.5 19.8Memorandum Item:

A. Outstanding Credit 21,494.5 22,000.5 2.0 7,609.9 8,825.9 16 29,104.4 30,826.4 5.9 B. Inter-bank Lending 340.2 305 -10.4 - - - 340.2 305 -10.4

Source: Commercial Banks

Table IV 6: Quarterly Changes in Deposits as at end of March 31, 2005

(In Millions of Birr)

Types of Deposit 2004/05 2005/06 % Change

Quarter IV Quarter I

Demand Deposit 18,919.4 19,585.4 3.5

Saving Deposit 17,311.4 18,709.5 8.1

Time Deposit 2,284.6 2,390.9 4.7

Total 38,515.4 40,685.8 5.6

Source: Commercial banks

4.4.2 Disbursement of Fresh Loans

The banking system granted a total of Birr 2,224.8 million new loans to the different sectors of the economy during the first quarter of 2005/06. This was 12.2 percent higher than the amount disbursed during the previous quarter but 4.1 percent lower than that of the corresponding quarter of 2004/05. The private sector (including cooperatives) received about 94.2 percent of the total new loans disbursed during the quarter. By economic sectors, the largest share (24.1 percent) was channeled to international trade, followed by agriculture (22.2 percent) and domestic trade (20.5 percent).

4.4.3 Outstanding Credit

The stock of outstanding credit (including inter-bank lending and claims on the central government) stood at Birr 30.8 billion at the end of the first quarter of 2005/06, indicating a quarterly increase of 5.9 percent and an annual decline of 9.3 percent. Of the total outstanding loans, claims on the private sector (including cooperatives) were 59.9 percent, claims on central government 27.4 percent and public enterprises nearly 11.3 percent. In terms of economic sectors, industry took 18.8 percent, while international trade accounted for 12.7 percent. The residual constituted claims on other sectors such as transport and communication, hotels, tourism, power and mining.

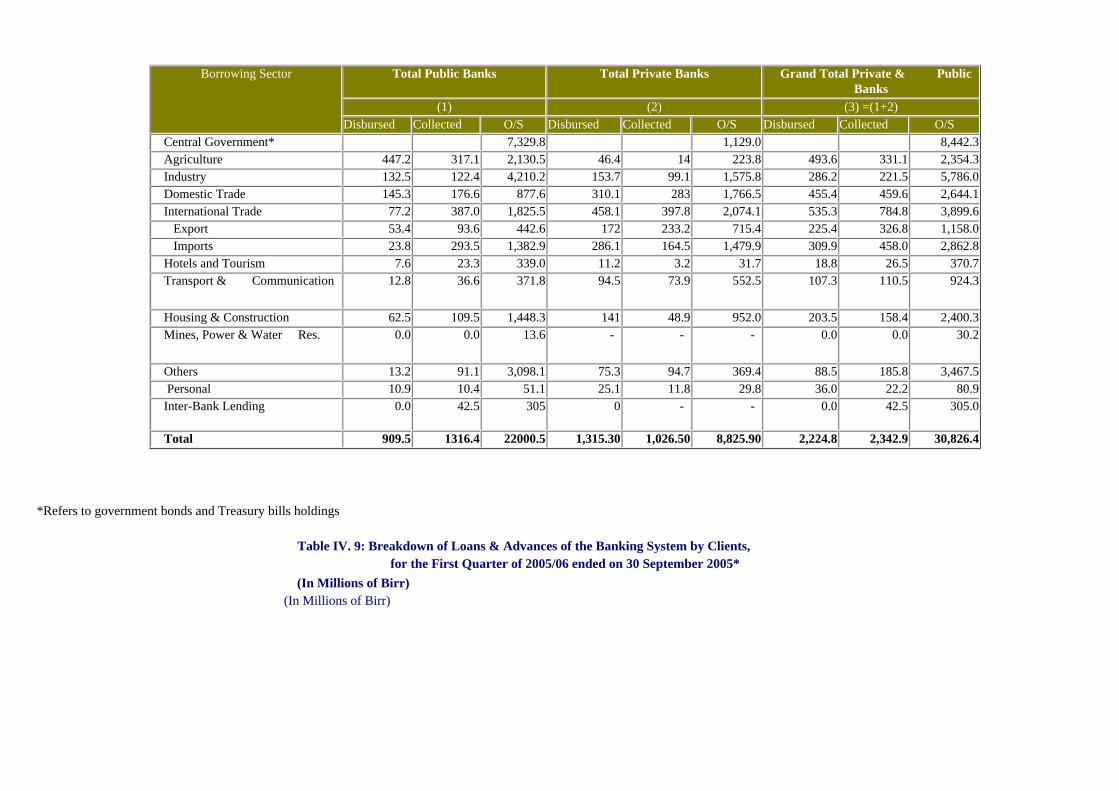

Table IV 8: Summary of Loans and Advances by Banks and Receiving Sectors during July- September 2005* (In Millions of Birr)

Borrowing Sector

Total Public Banks Total Private Banks Grand Total Private & Public Banks

(1) (2) (3) =(1+2)Disbursed Collected O/S Disbursed Collected O/S Disbursed Collected O/S

Central Government* 7,329.8 1,129.0 8,442.3 Agriculture 447.2 317.1 2,130.5 46.4 14 223.8 493.6 331.1 2,354.3 Industry 132.5 122.4 4,210.2 153.7 99.1 1,575.8 286.2 221.5 5,786.0 Domestic Trade 145.3 176.6 877.6 310.1 283 1,766.5 455.4 459.6 2,644.1 International Trade 77.2 387.0 1,825.5 458.1 397.8 2,074.1 535.3 784.8 3,899.6 Export 53.4 93.6 442.6 172 233.2 715.4 225.4 326.8 1,158.0 Imports 23.8 293.5 1,382.9 286.1 164.5 1,479.9 309.9 458.0 2,862.8 Hotels and Tourism 7.6 23.3 339.0 11.2 3.2 31.7 18.8 26.5 370.7 Transport & Communication 12.8 36.6 371.8 94.5 73.9 552.5 107.3 110.5 924.3

Housing & Construction 62.5 109.5 1,448.3 141 48.9 952.0 203.5 158.4 2,400.3 Mines, Power & Water Res. 0.0 0.0 13.6 - - - 0.0 0.0 30.2

Others 13.2 91.1 3,098.1 75.3 94.7 369.4 88.5 185.8 3,467.5 Personal 10.9 10.4 51.1 25.1 11.8 29.8 36.0 22.2 80.9 Inter-Bank Lending 0.0 42.5 305 0 - - 0.0 42.5 305.0

Total 909.5 1316.4 22000.5 1,315.30 1,026.50 8,825.90 2,224.8 2,342.9 30,826.4

*Refers to government bonds and Treasury bills holdings

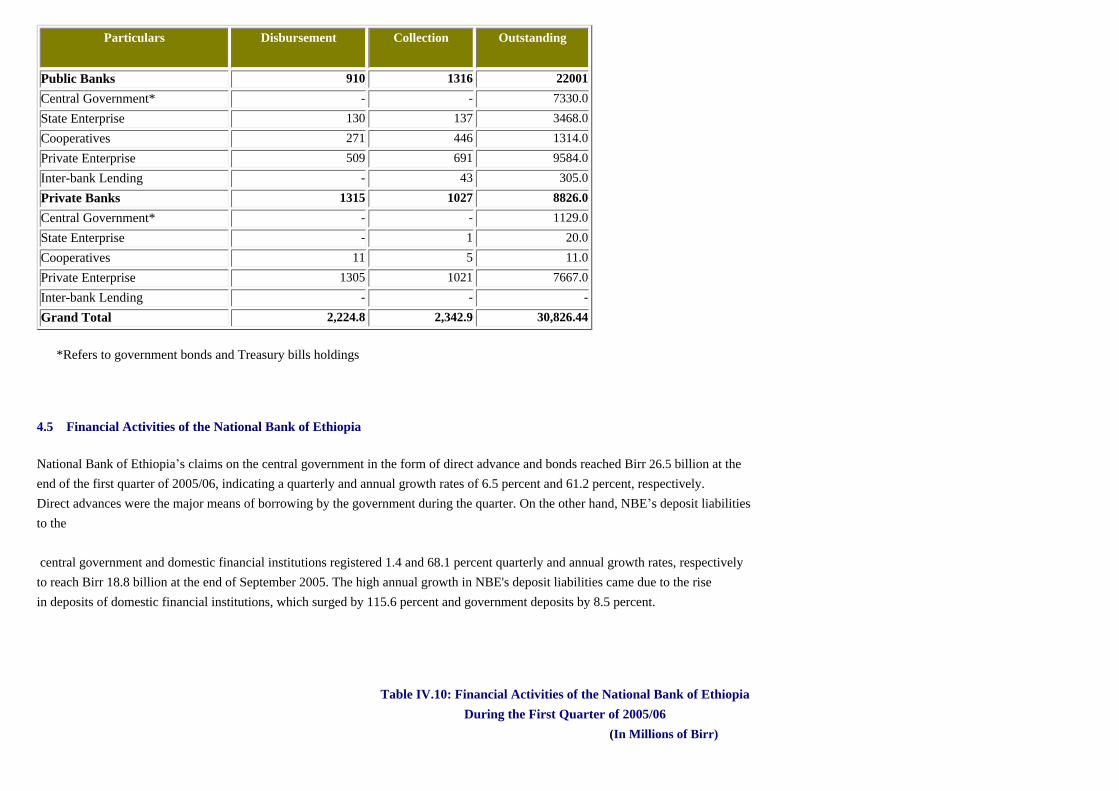

Table IV. 9: Breakdown of Loans & Advances of the Banking System by Clients, for the First Quarter of 2005/06 ended on 30 September 2005*

(In Millions of Birr) (In Millions of Birr)

Particulars Disbursement Collection Outstanding

Public Banks 910 1316 22001Central Government* - - 7330.0State Enterprise 130 137 3468.0Cooperatives 271 446 1314.0Private Enterprise 509 691 9584.0Inter-bank Lending - 43 305.0Private Banks 1315 1027 8826.0Central Government* - - 1129.0State Enterprise - 1 20.0Cooperatives 11 5 11.0Private Enterprise 1305 1021 7667.0Inter-bank Lending - - - Grand Total 2,224.8 2,342.9 30,826.44

*Refers to government bonds and Treasury bills holdings

4.5 Financial Activities of the National Bank of Ethiopia

National Bank of Ethiopia’s claims on the central government in the form of direct advance and bonds reached Birr 26.5 billion at the end of the first quarter of 2005/06, indicating a quarterly and annual growth rates of 6.5 percent and 61.2 percent, respectively. Direct advances were the major means of borrowing by the government during the quarter. On the other hand, NBE’s deposit liabilities to the

central government and domestic financial institutions registered 1.4 and 68.1 percent quarterly and annual growth rates, respectively to reach Birr 18.8 billion at the end of September 2005. The high annual growth in NBE's deposit liabilities came due to the rise in deposits of domestic financial institutions, which surged by 115.6 percent and government deposits by 8.5 percent.

Table IV.10: Financial Activities of the National Bank of Ethiopia During the First Quarter of 2005/06

(In Millions of Birr)

Particulars 2004/05 2005/06 % ChangeQtr.I Qtr.IV Qtr.I

A B C C/A C/B1.Loans and Advances 15,406.9 24,842.2 26,467.2 61.2 6.5

1.1. To Central Government 15,353.2 24,842.2 26,467.2 61.8 6.5 Direct Advance 5,265.0 14,754.0 16,427.1 180.2 11.3 Bonds 10,088.2 10,088.2 10,040.1 - (0.5) 1.2.To Development Bank of Ethiopia

53.7 - - (100.0) -

2.Deposit Liabilities 11,022.2 18,527.6 18,781.6 68.1 1.4 2.1. Government 4,888.5 5,302.2 4,836.2 8.5 (8.8) 2.2. Financial Institutions 6,133.7 13,225.4 13,945.4 115.6 5.4 O/W:

-Banks 6,104.6 13,195.2 13,915.2 116.2 5.5 -Insurance companies 29.1 30.2 30.2 3.8 -

4.6 Developments in Financial Markets

a) Treasury Bills Market

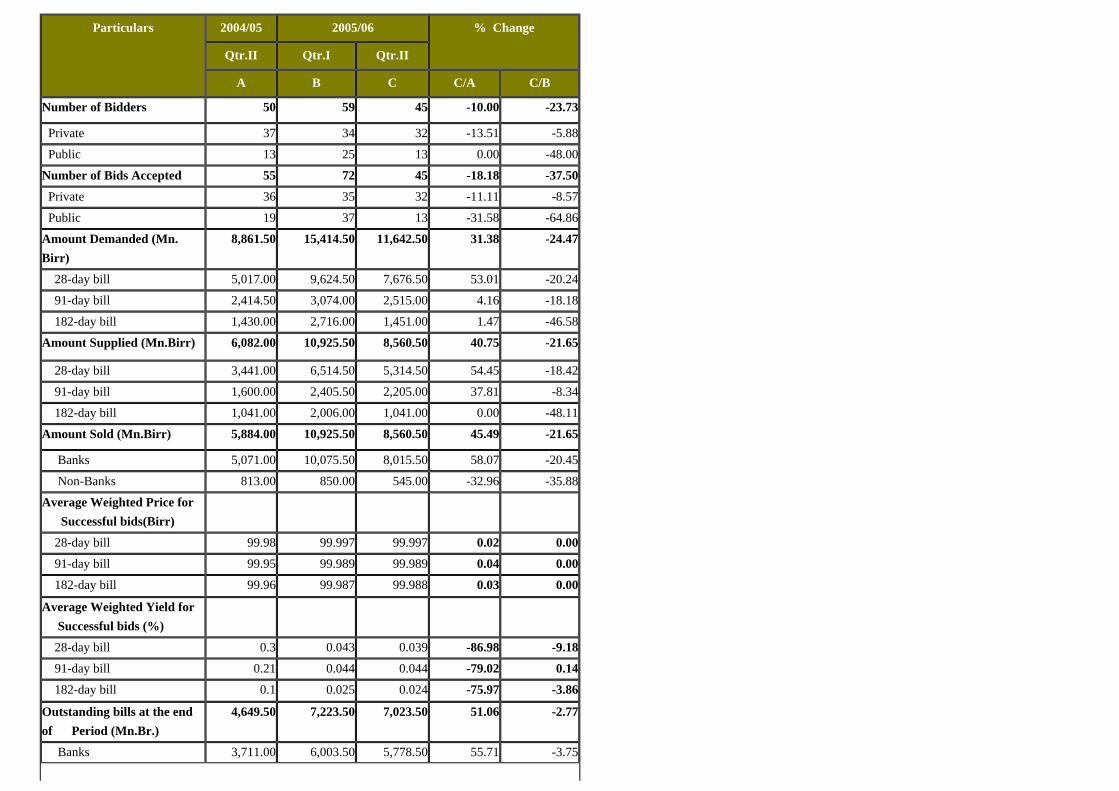

) Treasury Bills Market

During the first quarter of 2005/06, Treasury bills worth of Birr 10.9 billion were floated in the fortnightly auction market. This was 37.7 percent higher than the amount offered during the preceding quarter and 43.8 percent lower compared to the amount supplied a year earlier. On the other hand, T-bills worth of Birr 15.4 billion were demanded in the market, of which, about 70.9 percent was satisfied. The total quarterly demand for Treasury bills increased by 47.7 percent but it fell by 39.6 percent on annual basis.

The average annual weighted yield for 28-day bills plummeted from 0.065 percent in the preceding quarter to 0.043 percent and that of 91-day bills from 0.048 to 0.040 percent during the review quarter. The average annual weighted yield for 182-day bills also declined significantly from 0.043 percent to 0.025 percent in the same period.

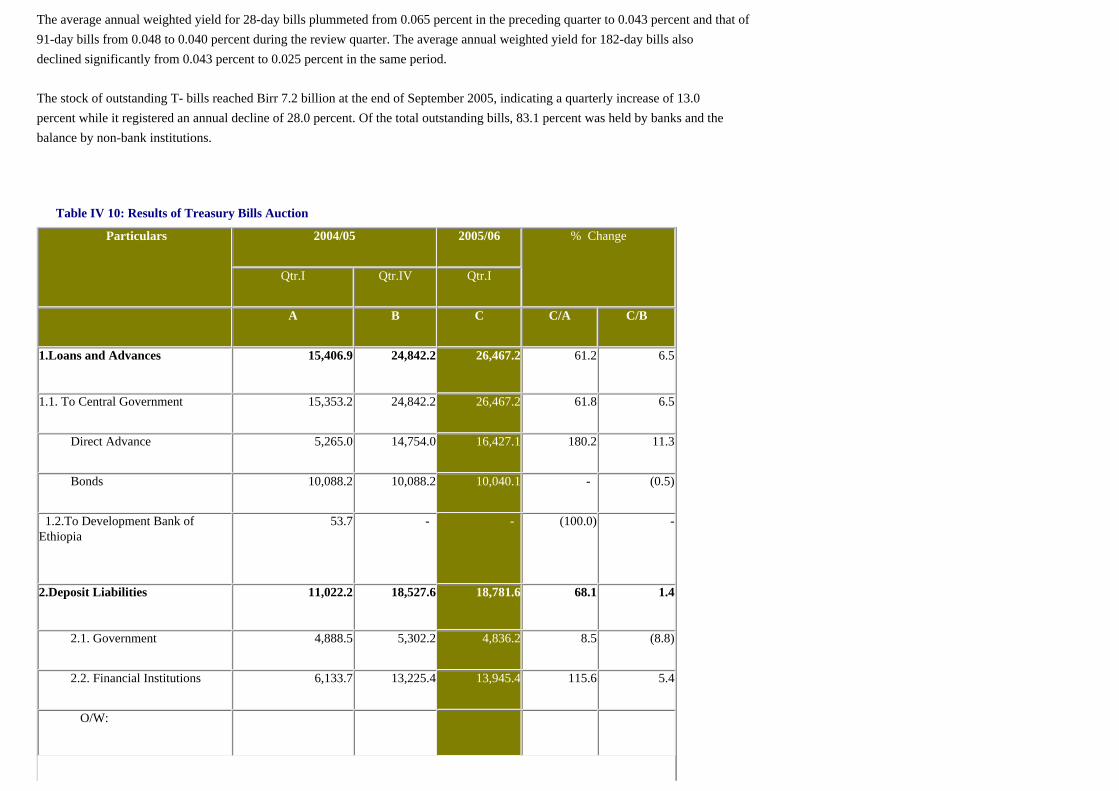

The stock of outstanding T- bills reached Birr 7.2 billion at the end of September 2005, indicating a quarterly increase of 13.0 percent while it registered an annual decline of 28.0 percent. Of the total outstanding bills, 83.1 percent was held by banks and the balance by non-bank institutions.

Table IV 10: Results of Treasury Bills Auction

Particulars 2004/05 2005/06 % Change

Qtr.I Qtr.IV Qtr.I

A B C C/A C/B

1.Loans and Advances 15,406.9 24,842.2 26,467.2 61.2 6.5

1.1. To Central Government 15,353.2 24,842.2 26,467.2 61.8 6.5

Direct Advance 5,265.0 14,754.0 16,427.1 180.2 11.3

Bonds 10,088.2 10,088.2 10,040.1 - (0.5)

1.2.To Development Bank of Ethiopia

53.7 - - (100.0) -

2.Deposit Liabilities 11,022.2 18,527.6 18,781.6 68.1 1.4

2.1. Government 4,888.5 5,302.2 4,836.2 8.5 (8.8)

2.2. Financial Institutions 6,133.7 13,225.4 13,945.4 115.6 5.4

O/W:

-Banks 6,104.6 13,195.2 13,915.2 116.2 5.5

-Insurance companies 29.1 30.2 30.2 3.8 -

Table IV. 11: Inter-bank Money Market Transactions

Particulars 2004/05 2005/06 % Change

Qtr.I Qtr.IV Qtr.I

A B C C/A C/B

Number of Bidders 78 48 59 -24.36 22.92

Number of Bids Accepted 135 56 72 -46.67 28.57

Amount Demanded (Mn.Birr) 25,507.0 10,437.2 15,414.5 -39.6 47.7

28-day bill 12,705.0 6,643.0 9,624.5 -24.3 44.9

91-day bill 9,678.0 2,285.0 3,074.0 -68.2 34.5

182-day bill 3,124.0 1,509.2 2,716.0 -13.1 80.0

Amount Supplied (Mn.Birr) 19,440.0 7,932.0 10,925.5 -43.8 37.7

28-day bill 10,787.0 4,686.0 6,514.5 -39.6 39.0

91-day bill 6,847.0 2,205.0 2,405.5 -64.9 9.1

182-day bill 1,806.0 1,041.0 2,006.0 11.1 92.7

Amount Sold (Mn.Birr)

19,440.0 7,932.0 10,925.5 -43.8 37.7

Banks 18,791.0 7,282.0 10,075.5 -46.4 38.4

Non-Banks 649.0 650.0 850.0 31.0 30.8

Average Successful bids (Birr)

Weighted Price for

28-day bill 99.973 99.995 99.997 0.024 0.002

91-day bill 99.924 99.988 99.989 0.065 0.001

182-day bill 99.948 99.983 99.987 0.039 0.004

Average Weighted Yield for

Successful bids (%)

28-day bill 0.346 0.065 0.043 -87.56 -33.9

91-day bill 0.304 0.048 0.044 -85.5 -8.3

182-day bill 0.105 0.034 0.025 -76.2 -26.5

Outstanding bills at the end

of Period (Mn.Br.) 10,038.0 6,395.0 7,223.5 -28.0 13.0

Banks 8,856.0 4,995.0 6,003.5 -32.2 20.2

Non-Banks 1,182.0 1,400.0 1,220.0 3.2 -12.9

b) Inter- Bank Money Market

No inter-bank money market transaction was effected during the fourth quarter of 2004/05 as virtually all banks carried excess reserve. Since its introduction some five years ago up until July 2003, merely twelve transactions involving Birr 166.7 million were held among few commercial banks with an interest rate ranging between 7 and 11 percent. The maturity period of these loans widely ranged from overnight to 5 years.

Table IV. 12: Inter-bank Money Market Transactions

No Borrower Lender Amount Interest Date of Maturity

Borrowed Rate Transaction Period

(In Mn. Br.) (%)

1 Nib Int. Bank Awash Int.Bank 7 11 16/11/00 Overnight

2 Wegagen Bank Commercial Bank of Eth.

10 8 3/01/01 5 years

3 Nib Int. Bank ,, 10 8 31/03/01 3 months

4 Wegagen Bank ,, 10 8 22/03/01 1 year

5 Nib Int. Bank ,, 3.6 8 31/05/01 6 months

6 Nib Int. Bank ,, 3.7 8 30/06/01 6 months

7 Nib Int. Bank ,, 0.8 8 30/11/01 6 months

8 Nib Int. Bank Bank of Abyssinia 29.0 7 31/12/02 3.5 months

9 Nib Int. Bank Bank of Abyssinia 19.0 7 31/01/03 3.5 months

10 Nib Int. Bank Bank of Abyssinia 20.3 7 28/02/03 3.5 months

11 Nib Int. Bank Bank of Abyssinia 29.0 7 31/03/03 5.2 months

12 Nib Int. Bank Commercial Bank of Eth.

25.0 7.5 07/07/03 5.2 month

13 Nib Int. Bank Bank of Abyssinia 20.0 7.5 26/3/05 Over draft

Total/Average - 187.4 7.8

Source: Commercial Banks