mining strategies for the future - trench & sykes - nov 2015 - centre for exploration targeting...

TRANSCRIPT

MINING SECTOR STRATEGIES FOR

THE FUTURE – PREPARING FOR

THE NEXT BOOM

Allan Trench1234

John P. Sykes235

[1] Department of Mineral & Energy Economics, Curtin University, Australia

[2] Centre for Exploration Targeting, Curtin University, Australia

[3] Centre for Exploration Targeting, The University of Western Australia

[4] CRU Group

[5] Greenfields Research

Wrays Resources Innovation Group Seminar,

Perth, Australia, 2 November 2015

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Some Takeaway Messages….

Mining Sector Strategies for the Future – Preparing for the Next Boom

‘Strategies for the future’ means far more than automation and technology….

Few resources companies stand out on strategy or capability…..

Doing something different can be a winner…. aside from picking the ‘next big thing’

on the Periodic Table

‘Low-cost’ is likely to still be the dominant strategy in 100 years time….

Niche mining business opportunities are all around us – even now….

Corporate strategy, even in commodity industries, is very far from boring…

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Let’s start with a truism…

Source: Trench & Sykes; Picture Source:

bigalmanack.com

Mining Sector Strategies for the Future – Preparing for the Next Boom

Everyone turns their attention to

innovations at asset and company

level when times are tough…

….Then go back to ‘business as usual’

at the first opportunity when things

pick up.

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

..and with a proposed takeaway…

Picture Source:

bigalmanack.com

Mining Sector Strategies for the Future – Preparing for the Next Boom

Opportunities are everywhere…

we just don’t easily see them

….There are however processes and

precedents as to how to find them

“We don’t like their sound and

guitar music is on the way out”

Decca

Records

1962

“Who the hell wants to hear actors talk?””

H.M.

Warner

1927

Harvard

Professor

1940

“The television will never achieve popularity;

it takes place in a semi-darkened room and

demands continuous attention””

Allied

Commander

WWI

“This is good sport, but for the military,

the aeroplane is useless””

..so spot the next generation of these…

..next generation concepts do not need

to be rocket science…

Bet Exploration.Com

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Like “BetExploration.com” ?

Old strategy

• Few winning holes

• Infrequent shareholder

returns

• “Expert”-based drill

programme assessment

• Lack of drilling buying

power

‘Blue ocean’ strategy

• Every drill program a winner

• Frequent shareholder “wins”

locked-in

• Crowd-based drill outcome

betting/probabilities

• Significant drilling buying

power Source: Trench & Sykes, 2015 (Re-inventing exploration, MiningNewsPremium.net)

.. Beware a solution looking for a

problem…

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Effective minerals sector strategy requires:

• A knowledge of your industry (and beyond)

• A knowledge of your own company!

• An understanding of the effectiveness of generic (and

other) strategies

• And a way of acquiring and updating this information

quickly and cheaply

• Consideration of views on the future (e.g. scenarios)

0 10 20 30 40 50 60 70 80 90 100

AL

CU

NI

ZN

FE

LRMC = 100 Ave qtly price (Q3) 2015

Source: CRU: LRMC = Long-Run-Marginal-Cost www.crugroup.com

A knowledge of your industry; Prices

Source: CRU

Big bets are made, big

risks taken often ending

in tears

Risks are avoided, small

bets are made

“Irrational exuberance” • Excessive optimism

• Inability to see the downturn

• Major projects launched

• Acquisition activity

• Rising tide floats all boats

“Irrational depression” • Excessive pessimism

• Inability to see the upturn

• Cost cutting, divestment, small

expansions & debottlenecking

• Develop future options

• We find out who is swimming naked.

A knowledge of your industry; Cycles

CRU CONSULTING Data: CRU

Rio Tinto’s mines occupy mainly

1st quartile positions on the global

cost curve

Port of

Dampier

Cape

Lambert

Port

Pannawonica (155Mt)

Nammuldi (73Mt)

Brockman 2 (15Mt)

Brockman 4 (381Mt)

Mt Tom Price (23Mt)

Marandoo (181Mt)

Paraburdoo (6Mt)

Channar (24Mt)

Eastern Range (40Mt)

West Angelas (150Mt)

Hope Downs (77Mt)

Yandicoogina (297Mt)

Western Turner Syncline

(257Mt)

Rio Tinto mining operations

Vale’s mines occupy mainly 1st and

2nd quartile positions on the global

cost curve

Tubarao

Port

Itaguai

Port Guaiba

Island

Terminal

Madeira

Port

Southern

System

(2,080Mt)

Midwestern

System

(660Mt)

Southeastern

System

(2,110Mt)

Northern

System

(4,796Mt)

VALE mining operations

Global iron ore business cost curve, all products($/t, Nominal, 2015) Global iron ore business cost curve, all products($/t, Nominal, 2015)

A knowledge of your industry; Costs

DISTINCTIVE CAPABILITY* YOUR REASONING /

PROOF / FACT-BASE

Your answer here...

Your answer here...

Your answer here...

Your answer here...

Your answer here...

Your answer here...

* A Distinctive Capability originates from a skill, or set of skills, that are superior to those of our peers

[NOT a physical asset or cash balance]

WHAT DO YOU CONSIDER THE THREE FOREMOST DISTINCTIVE CAPABILITIES* THAT

SET YOUR COMPANY APART FROM OTHERS?

A knowledge of your own company!

Does company XXX have a strategic advantage over peer companies?

(YES or NO)

If YES, allocate100% of the root cause of the advantage across the following

three categories:

Our Distinctive Capabilities... Financial strengths of XXXX... Our mine and/or exploration assets..

? ? ?

e.g. - skills

- people

- systems

e.g. - strong balance sheet

- strong cash flows

e.g. - mines

- projects

- exploration upside

?

WHAT DO YOU CONSIDER THE CURRENT STRATEGIC ADVANTAGES, IF ANY,

THAT WILL FACILITATE PROFITABLE GROWTH?

Mining companies most often choose which of these strategies?

A: Low Cost B: Differentiation C: Focus

A knowledge of generic strategies

• Lowest cost equals highest margin

• Position of strategic strength averts price competition & allows

exploration of new opportunities

• ‘Only one firm wins’

Low Cost

Strategy

• Differentiated products &/or services equals highest margin

• Competitive position is protected via continuous innovation of product

& service attributes

• ‘Many winners’

Differentiation

Strategy

• Market segmentation approach eg. by niche or geography

• Experience effects in target market segment can create barriers to

entry for competitors

• ‘Many winners’

Focus

Strategy

Sources: Porter (1985), Trench& Judge (2002)

Note the danger of getting ‘stuck in the middle’

Generic Approach Attributes

Most strategies will remain generic

Source: “The Red Queen Effect” From Kauffmann 1995, McKinsey Quarterly: quoting Lewis Carroll

Price

Quantity

Kryptonite Cash Costs 2013

Kryptonite Cash Costs 2016

"You have to run faster and faster just to stay in

the same place!"

BE CAREFUL: COST & PRODUCTIVITY IMPROVEMENTS ARE NO

GUARANTEE OF GREATER MARGINS OVER TIME

Some things never change – like the

cost leadership strategy…

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

..and strategy effectiveness?…

Mining Sector Strategies for the Future – Preparing for the Next Boom

Source: Arvidson (2014)

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Effective minerals sector strategy requires:

• A knowledge of your industry (and beyond)

• A knowledge of your own company!

• An understanding of the effectiveness of

generic (and other) strategies

• And a way of acquiring and updating this

information quickly and cheaply

• Consideration of views on the future (e.g.

scenarios)…

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

..what about the ‘next big thing’ strategy

Source: Google images

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

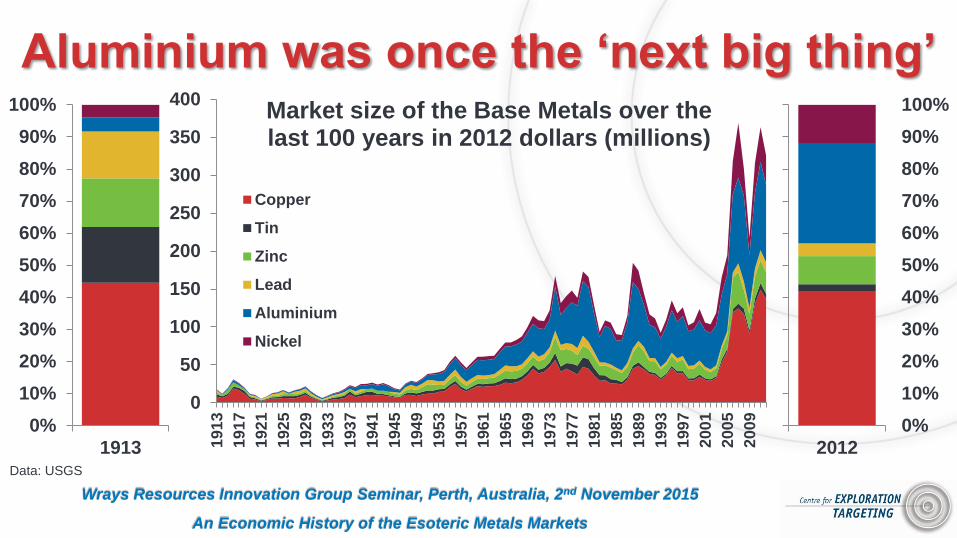

Aluminium was once the ‘next big thing’

0

50

100

150

200

250

300

350

400

191

3

191

7

192

1

192

5

192

9

193

3

193

7

194

1

194

5

194

9

195

3

195

7

196

1

196

5

196

9

197

3

197

7

198

1

198

5

198

9

199

3

199

7

200

1

200

5

200

9

Market size of the Base Metals over the last 100 years in 2012 dollars (millions)

Copper

Tin

Zinc

Lead

Aluminium

Nickel

An Economic History of the Esoteric Metals Markets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1913

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Data: USGS

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

However a lot needs to fall into place

An Economic History of the Esoteric Metals Markets

Images: sandatlas.org; earlham.edu; tempraturedetectors.com & shutterstock

ABUNDANCE

CONCENTRATION

8.2%

Factors in place prior to 20th century

MINING

PROCESSING

DEMAND

Solved in late 19th & early 20th century

Source: Sykes et al., 2015, in press

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

And not all metals hold the potential R

an

k

Critical Metal

Dis

co

ve

ry

Su

pp

ly

De

ma

nd

Total

1 Antimony 1 2 1 4

2 Barium 1 2 0.5 3.5

- Germanium 1 1 1.5 3.5

- Indium 1 1 1.5 3.5

- Tellurium 1 1 1.5 3.5

Mining Sector Strategies for the Future – Preparing for the Next Boom R

an

k

Critical Metal

Dis

co

ve

ry

Su

pp

ly

De

ma

nd

Total

44 Holmium (REE) 0 0 1 1

- Lutetium (REE) 0 0 1 1

- Terbium (REE) 0 0 1 1

- Thulium (REE) 0 0 1 1

- Tantalum 0 0 1 1

Source: Sykes et al., 2015, in press

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Automation is not a strategy – so we

Won’t Mention Driverless Trucks

Sources: Rio Tinto, FT, ABC, Courtesy Dr Carla Boehl (2015)

Mining Sector Strategies for the Future – Preparing for the Next Boom

Again!

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

So no need for NASA urine technology!

Sources: Google Images, NASA

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Strategies for the future requires an

entrepreneurial mindset

Source: bigalmanack.com

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Some strategies for the future will

require an entrepreneurial mindset

Source:http://www.cleanlink.com/productwatch/details/Urinal-Fly-Target—741

Urinals at Amsterdam Schiphol Airport

Mining Sector Strategies for the Future – Preparing for the Next Boom

Urinal Fly Target - The Urinal Fly Target Sticker

is an inexpensive, easy way to improve restroom

cleanliness. The product acts as a target,

reducing splashes on the floor by up to 80

percent. With a long life and installation ease, the

flies are available in 20 per pack.

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Strategies for the future requires a

process to see what is in plain sight

Mining Sector Strategies for the Future – Preparing for the Next Boom

1. Think through what makes a very

successful company in another

industry so special? Is it a

renegade?

2. Carefully document the elements of

its strategic approach

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Source: Trench 2002 ‘Make Your Firm a Business Renegade;

Trench (2006) Resources Companies Should ‘dare to be Different’

Mining Sector Strategies for the Future – Preparing for the Next Boom

3. Think how similar approach to

business might be ‘translated’ back to

the world of mining and exploration

4. Determine whether the equivalent

strategic space is already occupied in

exploration and mining. If not ask why

not?

Strategies for the future requires a

process to see what is in plain sight

-50

-40

-30

-20

-10

0

10

20

30

40

Total Returns to Shareholders (1986-2003) Per Cent (US$ Real Rate of Return)

Source: NM Rothschild & Sons (2003), A Trench analysis

Renegades occupy the first four places……and are nowhere else to be seen!!

Franco Nevada 34% First global mining royalty company

Barrick 28% Financial management/M&A

Sons of Gwalia 18% Miner in the third cost quartile

Delta 17% A mining company that didn’t mine

Sometimes doing things differently

pays off…Historical Mining Examples

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Typical life-of-mine risk & value profile

Mining Sector Strategies for the Future – Preparing for the Next Boom

Concept Exploration Discovery Economics Development Mining

Value

Time

MINING

High Risk – High Potential Lowered risk Full Value

Speculation Orphan Period

Speculators Leave

Institutional

Investment

EXPLORATION DEVELOPMENT

Uncertainty driven Risk driven

Source: Cook

(2010)

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Aside Generic Strategies – What are

successful Mining Sector Strategies?

Mining Sector Strategies for the Future – Preparing for the Next Boom

1. Best-in-Class Mine Operator

Source: Bill Gates; Rio Tinto

Which of the following mainstream gold companies are the

‘best’ best-in-class operator?

AngloGold Newmont

Barrick Newcrest

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Aside Generic Strategies – What are

successful Mining Sector Strategies?

Mining Sector Strategies for the Future – Preparing for the Next Boom

2. Faster and Under-Budget Project

Developer

Which of the following mainstream resources companies is a

‘best in class’ project developer?

Glencore BHP Billiton

South32 MetalsX

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Developers need to manage technical &

corporate risk profile R

isk

Change in risk type through the mine project development stage

Corporate

Risk

Technical

Risk

Sources: Modified from Trench et al., (2014); Trench & Packey (2012)

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

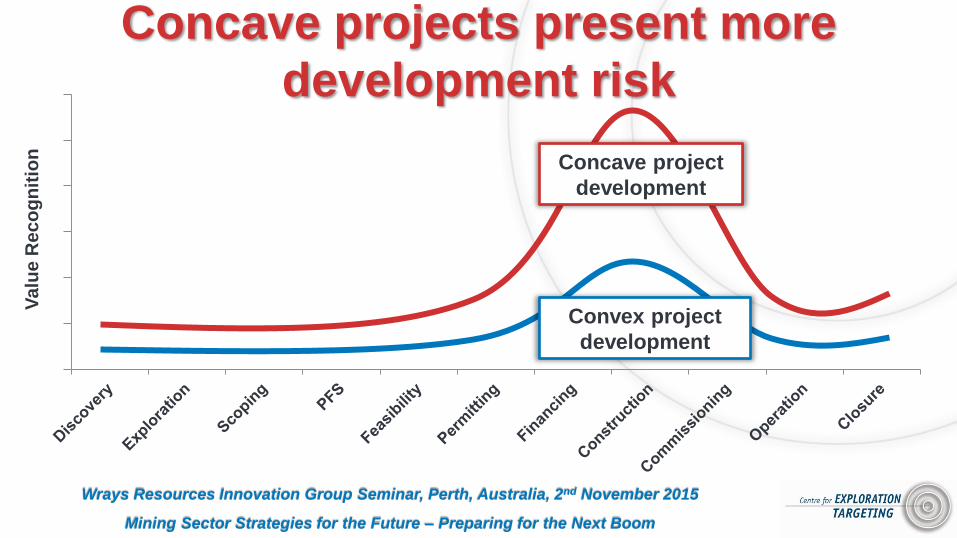

Concave projects present more

development risk

Mining Sector Strategies for the Future – Preparing for the Next Boom

Va

lue

Re

co

gn

itio

n

Convex project

development

Concave project

development

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Aside Generic Strategies – What are

successful Mining Sector Strategies?

Mining Sector Strategies for the Future – Preparing for the Next Boom

3. Perennial Discoverer of New Mines – The ‘Great Explorer’ Strategy

Which of the following is a great explorer?

Sub-Economic Resources NL BHP Billiton

Mark Creasy-Mark Bennett Rio Tinto

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Great explorers must find the orebodies of

the future…which look like?

Mining Sector Strategies for the Future – Preparing for the Next Boom

Source: Sykes & Trench (2014)

Based on: Sykes and Trench (2014)

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Discovery impact is dependent on

commodity type

Mining Sector Strategies for the Future – Preparing for the Next Boom

Va

lue

Re

co

gn

itio

n

Convex minerals: • Gold,

• Diamonds

• Tin

• Copper

• Nickel sulphide

• Hematite DSO

• Oil

Concave minerals: • Nickel laterite

• Vanadium

• Rare earths

• Graphite

• Magnetite

• Gas

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Aside Generic Strategies – What are

successful Mining Sector Strategies?

Mining Sector Strategies for the Future – Preparing for the Next Boom

3. Partner of Choice - The Great Socioeconomic Miner

Geographical (Country) Risk

Re

so

urc

e

Nationalis

m

La

nd

Acce

ss

La

nd

Cla

ims

Re

d T

ap

e

Gre

en

Ta

pe

Co

rru

ptio

n

Civ

il U

nre

st

Infr

astr

uctu

re

So

cia

l U

nre

st

Na

tura

l D

isa

ste

rs

La

bo

ur

Re

latio

ns

Source: Trench et al., (2014)

Which of the following is an asset owner of choice (great

socioeconomic miner)?

Oceanagold Vale

First Quantum Anglo American

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Sources: Trench et al., (2014); Wilson et al., (2014); Multilateral Investment Guarantee Agency

(2013); Schwab et al., (2013); World Bank (2013); Transparency International (2013)

Great Socioeconomic Miner……Country Risk information

exists at high-level but is founded upon perception bias

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Ris

k

Change in risk type through the mine project development stage

Corporate Risk Technical Risk Sources: Modified from Trench et al., (2014); Trench & Packey (2012)

Non-Technical Risk:

Commodity Price?

Lo

wer

Pri

ces

Hig

he

r Pric

es

Mining Sector Strategies for the Future – Preparing for the Next Boom

Understanding ‘composite risk’

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Ris

k

Change in risk type through the mine project development stage

Sources: Modified from Trench et al., (2014); Trench & Packey (2012)

Non-Technical Risk:

NIMBYism?

Corporate Risk Technical Risk

Mining Sector Strategies for the Future – Preparing for the Next Boom

Understanding ‘composite risk’

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Ris

k

Change in risk type through the mine project development stage

Sources: Modified from Trench et al., (2014); Trench & Packey (2012)

Non-Technical Risk:

Political Risk? Elections

Unsupportive party elected

Unsupportive

party

unelected Risk

increases as

project

advances

Corporate Risk Technical Risk

Mining Sector Strategies for the Future – Preparing for the Next Boom

Understanding ‘composite risk’

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

But what about industry scenarios?

Mining Sector Strategies for the Future – Preparing for the Next Boom

Incre

ase

d D

ecre

ase

d

PROSPECT AVAILABILITY

Increased

Decreased

CRUSADES COUNTING HOUSE

PEASANTS’ REVOLT UNDER SEIGE E

CO

NO

MIC

MA

RG

INS

Source: Sykes (2015)

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Developing scenario-based strategy for

mining and exploration

• Centre for Exploration Targeting

“Future of Exploration” Scenarios

– Dec 2015: CET Students Trial Workshop

– Feb/Mar 2016: Perth-wide Students Trial

Workshop

– Jun/Jul 2016: International Expert Workshop

Contact: Allan or John to get involved!

Mining Sector Strategies for the Future – Preparing for the Next Boom

Wrays Resources Innovation Group Seminar, Perth, Australia, 2nd November 2015

Thank you to the organisers – Wrays -

and to all of you for coming along today [email protected]

Mining Sector Strategies for the Future – Preparing for the Next Boom