metro boston office… · with construction freezes in boston and cambridge still in play and...

TRANSCRIPT

303 CONGRESS STREET | BOSTON, MA 02210 | 617.457.3400 | HUNNEMANRE.COM

METRO BOSTON OFFICE MARKET REPORT

FIRST QUARTER | 2020

2 | METRO BOSTON OFFICE | Q1 2020

GREATER BOSTON OFFICE MARKET OVERVIEW

Over the last eleven years, The Greater Boston Area (GBA) has exhibited the longest economic

expansion since the Post World War II Era and has emerged as an international business hub and a

world leader in technology and the life sciences. Similarly, the GBA’s office market has run parallel,

helping provide the region with the largest construction boom since the same time period which has

allowed for the adoption of a significantly more diverse industry base now more than ever before.

However, while the GBA does provide a buffer against global forces that hinder this growth through

the economic backbones of healthcare and education, the metro is still subject to the universal

headwinds brought on by unseen circumstances such the COVID-19 pandemic which is currently

sweeping the country.

Having performed steadily during this quarter, the Greater Boston office market started off 2020

similar to the past three years with a slowdown in leasing activity compared to the prior quarter.

With many year-end decisions being made last quarter to help the GBA achieve one of its largest

years in recent history as it relates to the velocity of leasing and absorption, not nearly as many

transactions were left to execute and the uncertainty surrounding the global pandemic has only

minimized decision-making further. For now, most developers, tenants, and landlords alike are

hitting the pause button on decisions that are allowed to be pushed off until more economic clarity

is found on both local and national scale. That being said, the market has not come to a halt and

many of the cylinders that are needed to ensure solid fundamentals moving forward are still firing.

Most importantly, a significant supply injection is underway to help alleviate historically high office

rents and provide tenants with an wider array of options as the GBA evolves. Just over 2 million

square feet of new supply has kicked off this quarter across the metro and while mainly concentrated

in the Urban Market, the Route 128 Market is transforming into a destination-market. Historically a

relief valve for Boston and Cambridge, Route 128 is becoming a top choice for tenants considering a

move to recently built Class A space or unique product such as Brick and Beam which has become

limited. With over 11 million square feet in the construction pipeline, over 50% is already preleased,

most of which will deliver in 2021.

Average asking rents were static this quarter with the exception of select pockets such as Watertown

and Somerville which are being squeezed by overspill from the Cambridge market and a lack of

options on the northern and southern portions of the Route 128 Market. 2019 marketed the largest

annual increase in average asking rent throughout the region over the last decade and with leasing

activity down this quarter, limited pressure has been placed on rates over the last three months.

Moreover, net absorption remained flat this quarter with significant space give-backs along Route

495 and in Boston, limiting market growth. However, between Cambridge and the Route 128

submarket, occupancy gains were enough to put the market into positive territory with just under

500,000 square feet of net absorption taking place.

Looking ahead, limited pressure on urban market rents is expected to persist in the short-term

with construction freezes in Boston and Cambridge still in play and tenants hesitant to make

immediate decisions if they are able to. Furthermore, tenant build-outs are anticipated to be less

popular through the remainder of the year with more companies expected to be agile with time-to-

occupancy projects. This is expected to bode well for landlords who have built-out spec suites and

can capture tenants in a tighter window. Conversely, tenants who are able to renew and extend their

current leases in the short term are expected to do so to defer real estate decisions at the moment.

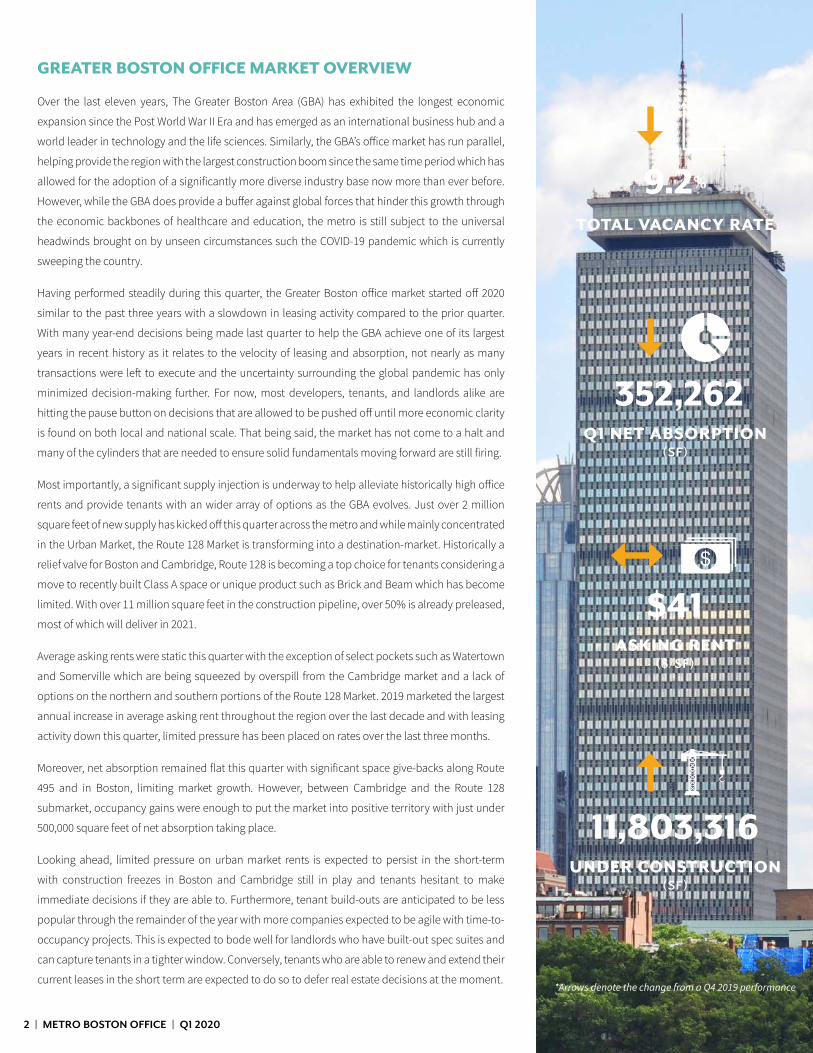

9.2%

TOTAL VACANCY RATE

352,262Q1 NET ABSORPTION

(SF)

$41 ASKING RENT

($/SF)

11,803,316UNDER CONSTRUCTION

(SF)

*Arrows denote the change from a Q4 2019 performance

3 | METRO BOSTON OFFICE | Q1 2020

BOSTON OFFICE

• While a significant portion of the active requirements in Boston have

paused, a plethora of tenants are still expected to be on the hunt for space

with companies such as the Cambridge Innovation Center, Hill Holiday,

and Eaton Vance still exploring new options with an emphasis on new

construction; which has been in play for most users looking for above

50,000 square feet since existing blocks in this size range are still limited

throughout the City.

• Asking rents have reached peak levels for 2020 considering a significant

slowdown in leasing activity is taking place. Landlords have yet to raise

asking rents in most cases as they anticipate the market uncertainty to

persist over the next quarter at minimum. With a significant amount of trades

taking place over the last five years, rents have been underwritten to climb

and while that is still very possible over the next several years, shorter term

lease renewals and extensions are in considerations to pacify uncertainty

on the short-term horizon. This will potentially allow landlords to get higher

rates, sooner rather than later, if demand levels similar to 2019 reignite.

• With negative absorption taking place in Boston this quarter, vacancy

ticket upward to 6.2% but remains well below the 10-year average of 8.5%.

While vacancy is expected to increase further this year due to recent job

losses which have mainly been concentrated in Boston, similar to past

market corrections, the expectation is that more sublease space is going

to be put back on the market than in the last few quarters.

• Already having undergone scrutiny in 2019 through investment models

made public by WeWork, coworking occupancy is expected to bounce

back if operators can weather the storm. Coworking platforms such

as WeWork, Industrious, and landlord-run flex office operations made

up a substantial amount of absorption over the last two years and

while most are struggling right now due to economic uncertainty and

the unwillingness for employees work in close quarters due to social

distancing practices, the flexible term solutions they provide may be

something users can lean on if the market corrects.

TOTAL VACANCY

QUARTERLY NET ABSORPTION

GROSS ASKING RENTS

$0

$20

$40

$60

$80

$100

$/SF

BAC

K B

AY

FIN

AN

CIA

L D

ISTR

ICT

SEA

PORT

CH

ARL

ESTO

WN

MID

TOW

N

NO

RTH

STA

TIO

N

ASKING RENT RANGE WEIGHTED AVERAGE

0%

12%

10%

8%

6%

4%

2%

2013 2014 2015 2016 2017 2018 2019 2020

0

-600

-400

-200

200

400

600

800

1,000

1,200

SQU

AR

E FE

ET(t

hous

and

s)

2013 2014 2015 2016 2017 2018 2019 2020

CLASS A CLASS B

TOTAL VACANCYRATE

Q1 NET ABSORPTION(SF)

ASKING RENT($/SF)

UNDER CONSTRUCTION(SF)

6.2% (502,334) $61 6,170,832

*Asking rent ranges denote the highest and lowest rents on gross basis

4 | METRO BOSTON OFFICE | Q1 2020

CAMBRIDGE & INNER SUBURBS OFFICE

• The office market in Cambridge remains on solid footing with the

exception of new supply which continues to play catch-up to the rest of

the submarket. With virtually no space options in Mid and East Cambridge,

tenants are being faced to look outside the market. Specifically, these

include parts of the western and northern suburbs, as well as crossing over

the Charles to Boston where an urban employee base can still be tapped

in full potential and access to the redline is maintained. Major projects at

Cambridge Crossing and in Kendall Square will bring more supply to the

market next year but much more will need to be built to counteract the lab

market which is accounting for the brunt of leasing and new supply on the

horizon. Of the 2 million square feet of office construction taking place,

almost 80% is already preleased.

• Similar to most markets, asking rents have remained in line with the

previous quarter. East Cambridge saw a slight uptick in asking rents and is

expected to draw more demand due to the unique position the submarket

is currently in from activity surrounding the life science sector. Most users

in this sector need lab space but the majority of the operations relies on

office space for administrative and sale operations. As the global dynamic

surrounding the life sciences is put under the microscope through the

COVID-19 pandemic, East Cambridge could become a ground-zero for

further therapies beyond what is just being explored by only several

companies at the moment such as Moderna. As the largest biotech hub

in the world, Cambridge is positioned to capture a large wave of demand

as collaboration between innovative companies become even more

essential and important to ramp up quickly in a short timeframe.

• Approximately 350,000 square feet of net absorption registered in Cambridge

this quarter, most of which was driven by the delivery of 222 Jacobs Street,

Philips new North American headquarter, where they are accompanied by

Thrive Early Detection and Cerevel Therapeutics. On the other side of the

equation, office space in West Cambridge continues to be affected by the

lab market with just over 300,000 square feet of space vacated in the last

twelve months in order to make way for more lab product. While some tech

companies such as Hubspot are starting to retract in size in East and Central

Cambridge to find rent relief in the GBA’s most expensive submarket.

TOTAL VACANCY

QUARTERLY NET ABSORPTION

GROSS ASKING RENTS

$50

$60

$70

$80

$90

$100

$110

$/SF

EAST

CA

MBR

IDG

E

MID

CA

MBR

IDG

E

WES

T C

AM

BRID

GE

ASKING RENT RANGE

0%

10%

8%

6%

4%

2%

2013 2014 2015 2016 2017 2018 2019 2020

0

-200

200

400

600

800

1,000

SQU

AR

E FE

ET(t

hous

and

s)

2013 2014 2015 2016 2017 2018 2019 2020

CLASS A CLASS B

TOTAL VACANCYRATE

Q1 NET ABSORPTION(SF)

ASKING RENT($/SF)

UNDER CONSTRUCTION(SF)

2.6% 353,196 $57-105 2,017,300

5 | METRO BOSTON OFFICE | Q1 2020

SUBURBAN OFFICE

• Driven primarily by an active Route 128 corridor, the suburban office

market carried the GBA posting the most positive absorption in Q1. This

absorption was mainly credited to expansions from existing tenants and

new tenants to the market, relocating to escape the high prices closer to

Boston. Most of the +/-450,000 square feet of the office space absorbed

went to several of the new construction projects along Route 128 West. The

North submarket of 128, the tightest of the submarkets, saw an additional

224,000 square feet of positive absorption through a healthy volume of

small to mid-size lease transactions. The size of those transactions was

do in most part to the dearth of large block space options for Tenant’s in

that the submarket.

• Several new construction projects totaling +/-1,000,000 square feet of Class

A space commenced this quarter throughout the suburbs with the majority

in the 128 West submarket. In addition, new construction projects with

expected delivery in Q2 2021 have broken ground in the Inner Burbs and

Quincy. Unlike much of the new construction in the CBD, many of these

new suburban projects were designed with “flexibility of use” in mind, with

the goal of attracting both office users and lab/biotech Tenants. These

new facilities are designed with larger floor plates, more floor-by-floor clear

heights to accommodate sophisticated infrastructure and on-site parking

not typically available to lab tenants. The suburbs provide lab and biotech

Tenants a dramatic cost savings in contrast to the expensive lab “hot bed”

areas of Cambridge and Watertown, priced accordingly due to their proximity

to Boston, the universities and hospitals and talent pool. Lab and biotech

users currently represent a significant amount of the active requirements in

the suburbs and have absorbed much of the new construction to date.

• With the exception of inner suburban pockets like Watertown and

Somerville, asking rents have remained motionless with Class B asking

rents ticking downward slightly. Watertown in particular is seeing the most

pressure on rents through a three-pronged market dynamic where overspill

from Cambridge, demand from the western suburbs and an encroaching

lab market is putting upward pressure on rates as tenants try to find what

value is left in a city that has almost no office space left.

TOTAL VACANCY

QUARTERLY NET ABSORPTION

GROSS ASKING RENTS

$0

$10

$20

$30

$40

$50

$/SF

INN

ER S

UBU

RBS

ROU

TE 12

8 N

ORT

H

ROU

TE 12

8 N

ORT

HW

EST

ROU

TE 12

8 W

EST

ROU

TE 12

8 SO

UTH

FRA

MIN

GH

AM

/NA

TICK

ROU

TE 4

95 N

ORT

HEA

ST

ROU

TE 4

95 N

ORT

H

ROU

TE 4

95 W

EST

ROU

TE 9

5 SO

UTH

ASKING RENT RANGE WEIGHTED AVERAGE

0%

25%

20%

15%

10%

5%

2013 2014 2015 2016 2017 2018 2019 2020

ROUTE 128 ROUTE 495

0

-800

-400

-600

-200

200

400

600

800

1,000

SQU

AR

E FE

ET(t

hous

and

s)

2013 2014 2015 2016 2017 2018 2019 2020

CLASS A CLASS B

TOTAL VACANCYRATE

Q1 NET ABSORPTION(SF)

ASKING RENT($/SF)

UNDER CONSTRUCTION(SF)

12.4% 501,400 $27 3,615,184

6 | METRO BOSTON OFFICE | Q1 2020

NOTABLE TRANSACTIONS

260 FRANKLIN STREETA BOSTON

60 STATE STREETBOSTON

1 RESSEARCH DRIVEWESTBOROUGH

4 TECHNOLOGY DRIVE PEABODY

Company Acadian Asset Management Company Pioneer Investment Company Company Park Palace Technologies Company Converge

Size 108,000 SF Size 99,000 SF Size 84,000 SF Size 77,000 SF

Submarket Financial District Submarket Financial District Submarket Route 495 West Submarket Route 128 North

ONE FINANCIAL CENTER BOSTON

125 HIGH STREETBOSTON

200 CLARENDON STREETBOSTON

25 UPTON DRIVE WILMINGTON

Company Brown Rudnick Company GID Company TA Associates Company Eckert & Ziegler Radiopharma

Size 57,000 SF Size 47,000 SF Size 47,000 SF Size 40,000 SF

Submarket Financial District Submarket Financial District Submarket Back Bay Submarket Route 128 North

10-20 CHANNEL STREET BOSTON

205 LOWELL ST WILMINGTON

275 GROVE STREETNEWTON

99 HIGH STREETBOSTON

Company United Way Company AeroVironment Company Paypal Company True Motion

Size 40,000 SF Size 40,000 SF Size 37,000 SF Size 27,000 SF

Submarket Seaport Submarket Route 128 West Submarket Route 128 West Submarket Financial District

7 | METRO BOSTON OFFICE | Q1 2020

URBAN BOSTON

STATUS ON THE HORIZON FILED CITY APPROVED READY TO GO UNDERWAY

Total 6,285,630 6,285,630 3,003,500 3,028,000 4,856,980

Available 5,861,230 5,861,230 3,003,500 2,468,000 2,405,627

Leased 0 0 0 560,000 2,451,353

% Leased 0% 0% 0% 18% 50%

DELIVERY YEAR 20' 21' 22' 23' 24'+

Total 903,000 1,923,353 1,018,627 1,012,000 11,252,130

Available 338,000 547,000 1,018,627 502,000 10,267,730

Leased 565,000 1,376,353 0 510,000 560,000

% Leased 63% 72% 0% 50% 5%

CAMBRIDGE

STATUS ON THE HORIZON FILED CITY APPROVED READY TO GO UNDERWAY

Total 400,000 400,000 150,000 985,000 3,411,023

Available 400,000 400,000 150,000 985,000 558,247

Leased 0 0 0 0 2,852,776

% Leased 0% 0% 0% 0% 84%

DELIVERY YEAR 20' 21' 22' 23' 24'+

Total 3,532,023 0 0 0 0

Available 679,247 864,000 0 150,000 400,000

Leased 2,852,776 0 0 0 0

% Leased 81% N/A N/A N/A N/A

INNER RING

STATUS ON THE HORIZON FILED CITY APPROVED READY TO GO UNDERWAY

Total 4,654,400 4,654,400 2,411,350 2,642,965 1,752,789

Available 4,654,400 4,654,400 2,231,350 2,367,965 1,301,317

Leased 0 0 0 275,000 451,472

% Leased N/A N/A 0% 10% 26%

DELIVERY YEAR 20' 21' 22' 23' 24'+

Total 1,062,433 0 0 0 0

Available 610,961 1,374,321 211,000 0 9,593,750

Leased 451,472 0 275,000 0 0

% Leased 42% N/A N/A N/A N/A

128 BELT

STATUS ON THE HORIZON FILED CITY APPROVED READY TO GO UNDERWAY

Total 1,040,000 1,040,000 962,000 1,059,000 1,081,510

Available 1,040,000 1,040,000 962,000 889,000 739,510

Leased 0 0 0 0 342,000

% Leased 0% 0% 0% 0% 32%

DELIVERY YEAR 20' 21' 22' 23' 24'+

Total 513,890 0 0 0 0

Available 171,890 647,620 0 0 3,186,000

Leased 342,000 0 0 0 0

% Leased 67% N/A N/A N/A N/A

GREATER BOSTON DEVELOPMENT PIPELINEOFFICE & LAB SPACE

8 | METRO BOSTON OFFICE | Q1 2020

OFFICE RECAP

TOTAL INVENTORY SF

UNDER CONSTRUCTION

"DIRECT VACANT"

SUBLEASE VACANT

"TOTAL VACANT SF"

"TOTAL VACANCY

RATE"

Q1 NET ABSORPTION

12-MONTH NET ABSORPTION

AVERAGE ASKING RENT

Total Market 221,560,837 11,803,316 18,210,996 2,075,533 20,286,529 9.2% 352,262 1,898,827 $41

Urban Market 100,496,295 8,188,132 4,506,865 814,667 5,321,532 5.3% (149,138) 1,345,790 N/A

Boston 74,811,544 6,170,832 4,191,542 463,180 4,654,722 6.2% (502,334) 589,234 $61

Back Bay 15,150,560 0 324,365 64,196 388,561 2.6% (45,179) 341,234 $77

Financial District 36,974,655 1,942,038 2,162,184 248,339 2,410,523 6.5% (273,683) 3,344 $62

Seaport 11,619,790 1,980,400 1,310,086 77,983 1,388,069 11.9% (20,717) 222,952 $60

Charlestown 2,487,985 109,000 83,229 6,785 90,014 3.6% (55,014) (45,485) $49

Fenway 2,027,769 275,645 34,868 16,940 51,808 2.6% (48,608) (48,608) N/A

Midtown 2,287,595 235,000 112,170 23,184 135,354 5.9% (38,030) (44,852) $56

North Station 3,040,190 1,628,749 159,400 24,259 183,659 6.0% (27,510) 144,899 $58

South Station 1,223,000 0 5,240 1,494 6,734 0.6% 6,407 15,750 N/A

Cambridge 25,684,751 2,017,300 315,323 351,487 666,810 2.6% 353,196 756,556

East 15,208,585 1,714,423 141,391 146,986 288,377 1.9% 340,706 764,758 N/A

Mid 7,572,444 302,877 67,769 46,761 114,530 1.5% 2,729 (17,211) N/A

West 2,903,722 0 106,163 157,740 263,903 9.1% 9,761 9,009 $58

Suburban Market 121,064,542 3,615,184 13,704,131 1,260,866 14,964,997 12.4% 501,400 553,037 $27

Route 128 83,833,504 3,405,184 7,068,194 901,338 7,969,532 9.5% 714,922 812,663 $32

Inner Suburbs 6,234,607 1,816,155 427,509 12,433 439,942 7.1% 99,025 103,808 $36

North 14,721,514 364,031 1,021,874 83,167 1,105,041 7.5% 109,736 121,029 $25

Northwest 15,742,255 210,700 1,136,151 76,929 1,213,080 7.7% (16,486) (22,665) $35

West 25,933,011 507,620 1,952,313 534,469 2,486,782 9.6% 448,514 492,109 $38

South 16,413,238 347,276 1,904,206 123,732 2,027,938 12.4% 78,045 101,283 $28

Framingham/Natick 4,788,879 159,402 626,141 70,608 696,749 14.5% (3,912) 17,099 $27

Route 495 37,231,038 210,000 6,635,937 359,528 6,995,465 18.8% (213,522) (259,626) $20

Northeast 7,836,084 0 1,387,436 17,438 1,404,874 17.9% (91,867) (128,225) $19

North 13,802,627 60,000 2,920,648 179,804 3,100,452 22.5% (175,228) (32,080) $20

West 11,973,397 150,000 2,038,607 162,286 2,200,893 18.4% 44,285 (115,650) $21

South 3,618,930 0 289,246 0 289,246 8.0% 9,288 16,329 $19

9 | METRO BOSTON OFFICE | Q1 2020303 CONGRESS STREET | BOSTON, MA 02210 | 617.457.3400 | HUNNEMANRE.COM

METHODOLOGY

Source: Co-Star, Hunneman. Prepared: March 2020.

Disclaimer: The above data is from sources deemed to be generally reliable, but no warranty is made as to the accuracy of the data nor its usefulness for any particular purpose.

Average Rental Rates are asking rents on direct space. Vacant space includes both direct and sublease space.

TUCKER WHITE Director of Research

978.828.5141 [email protected]

JAMES FIFTALSenior Research Analyst

HEATHER CHAPMANGraphics Manager