merger and acquisition.......book

DESCRIPTION

It states about mergers and acquisitionTRANSCRIPT

Chapter :-1

Introduction

[1]

1. INTRODUCTION

We have been learning about the companies coming together to from another

company and companies taking over the existing companies to expand their

business. With recession taking toll of many Indian business and the feelings of

insecurity surging over our businessmen, it is not surprising when we hear about the

immense numbers of corporate restructuring taking place, especially in the last

couple of years. Several companies have been taken over and several have

undergone internal restructuring, whereas certain companies in the same field

of business have found it beneficial to merge together into one company.

All our daily newspapers are filled with cases of mergers, acquisitions, spin-offs,

tender offers, & other forms of corporate restructuring. Thus important issues

both for business decision and public policy formulation have been raised. No

firm is regarded safe from a takeover possibility. On the more positives idea Mergers

& Acquisitions may be critical for the healthy expansion and growth of the firm.

Successful entry into new product and geographical markets may require Mergers &

Acquisitions at some stage in the firm’s development. Successful competition in

international markets may depend on capabilities obtained in a timely and efficient

fashion through Mergers and Acquisitions.

To opt for a merger or not is a complex affair, especially in terms of the technicalities

involved. We have discussed almost all factors that the management may have to

look into before going for merger.

[2]

Considerable amount of brainstorming would be required by the managements to reach a conclusion. E.g. A due diligence report would clearly identify the status of the company in respect of the financial position along with the net worth and pending legal matters and details about various contingent liabilities.

Decision has to be taken after having discussed the pros & cons of the proposed

merger & the impact of the same on the business, administrative costs benefits,

addition to shareholder’s value, tax implications including stamp duty and last but

not the least also on the employees of the Transferor or Transferee Company.

[3]

Objective of study:-

The objectives of this project were mainly to study the merger and acquisition,

customer relation, their profit making techniques of company, but there are some

more and they are -

The main purpose of our study is to render a better understanding of the concept “merger and acquisition”

To understand the planning and management of merger and acquisition. To understanding the process of merger and evaluating process of

merger. To understanding the what are the benefit to company after adopting

merger and acquisition concept.

[4]

Scope of study:-

As merger is a combination of two or more co‘s into an existing co or a new co. Acquired co. transfer its assets, liabilities and shares to the acquiring company for cash or exchange of shares. Need for Merger and Acquisition arises because in general, a merger can facilitate the ability of two or more competitors to exercise market power interdependently, through an explicit agreement or arrangement, or through other forms of behaviour that permits firms implicitly to coordinate their conduct. It will be found to be likely to prevent or lessen competition substantially when the parties to the merger would like to be in a position to exercise a materially greater degree of market power in a substantial part of a market for two years or more, than if the merger did not proceed in whole or in part. In short, a company can achieve its growth objective by:

Expanding its existing markets

Entering in new markets

A company can expand internally or externally. If internally there is a problem due to lack of resources and managerial skill it can to the same externally through mergers and acquisitions. This helps a company to grow at a faster pace in a convinent and inexpensive way. Combination of companies may result in more than the average profitability due to reduction in cost and effective utilization of resources.

[5]

Research methodology:-

Secondary data

The mechanism involved in secondary data collection, mainly borrowing through adequate journal (related to merger and acquisition), web portals, books, white papers.

This research has been conducted with the help of secondary data as follow : Different websites like Google , yahoo etc This data was gathered through the company’s websites, its corporate

intranet , adidas and reebok annual report. Also, various text books on financial management like Khan & Jain,

Prasanna Chandra were consulted to equip ourselves with the topic.

[6]

Chapter no:-2

Review of Literature

[7]

Review of Literature:-

American Tower Corporation looks at mergers and acquisitions to boost presence in India

October 2, 2014 | Danish Khan , ET Bureau

NEW DELHI: American Tower Corporation (ATC) is betting on the need for more telecom towers in India as the country's data consumption surges and 4G is adopted widely even as the Boston- based company looks at mergers and acquisitions to grow its presence, its top official in the region said. Telecom operators such as Bharti-Airtel, Vodafone India and Idea Cellular are focusing on upgrading their existing sites to support growing.

India's M&A deal stands at $32.6 billion during January-August: Grant Thornton

September 18, 2014 | PTI

NEW DELHI: The month of August saw overall private equity deal activity worth $1.6 billion, taking the year-to-date value of transactions in the country to $32.6 billion, indicating this year will end with much better number in terms of mergers and acquisitions. According to assurance, tax and advisory firm Grant Thornton, the overall deal sentiment in India has remained consistently high from second quarter of 2014.

Competition Commission of India eases merger and acquisition rules

May 12, 2011

NEW DELHI: India's competition regulator on Wednesday announced the regulations for mergers and acquisitions, diluting several of its earlier proposals to address industry concerns that the competition law was intrusive and burdensome. The new rules exempt a host of transactions from the scrutiny of the Competition Commission of India (CCI) and seek much lower merger notification fees than proposed earlier. "We have exempted routine merger and acquisition.

[8]

Chapter no:3

Theoretical aspects of project

[9]

WHAT IS MERGER ?

Merger is defined as combination of two or more companies into a single company

where one survive and the others lose their corporate existence. The survivor

acquires all the assets as well as liabilities of the merged company or companies.

Merger is a combination of two or more companies into one company.

In India, we call mergers as amalgamations, in legal parlance. The acquiring

company, (also referred to as the amalgamated company or the merged company)

acquires the assets and the liabilities of the target company (or amalgamating

company). Typically, shareholders of the amalgamating company get shares of the

amalgamated company in exchange for their existing shares in the target company.

Merger may involve absorption or consolidation.

A MERGER happens when two firms, often about same size, agree to go forward

as a new single company rather than remain separately owned & operated by

pooling all their resources together, to create a sustainable competitive

advantage. For example , both Daimler-Benz & Chrysler ceased to exist when two

firms merged, and a new company ’Daimler-Chrysler’ was created.

Generally, he surviving company is the buyer, which retains its identify, and the

extinguished company is the seller. Merger is also defined as amalgamation. Merger

is the fusion of two or more existing companies. All assets, liabilities and the stock

stand transferred to transferee company in consideration of payment in the form

of:

Equity shares in the transferee company,

Debentures in the transferee company,

Cash, or

A mix of the above modes

[10]

WHAT IS ACQUISITION?

Acquisition in general sense is acquiring the ownership in the property. In the

context of business combinations, an acquisition is the purchase by one

company of a controlling interest in the share capital of another existing

company. When a Company takes over another one & clearly becomes the

new owner, the purchase is called ‘ACQUISITION’. Unlike mergers,

acquisitions can sometimes be unfriendly. i.e., when a firm tries to takeover

another by adopting hostile measures.

Acquisition is nothing but takeover, is the buying one company by another company. An acquisition or takeover is the purchase of one business or company by another company or other business entity. Such purchase may be of 100%, or nearly 100%, of the assets or ownership equity of the acquired entity. Consolidation occurs when two companies combine together to form a new enterprise altogether, and neither of the previous companies remains independently. Acquisitions are divided into "private" and "public" acquisitions, depending on whether the acquire or merging company (also termed a target ) is or is not listed on a public stock market . An additional dimension or categorization consists of whether an acquisition is friendly or hostile .

[11]

Methods of Acquisition:

An acquisition may be affected by:-

a) Agreement with the persons holding majority interest in the company

management like members of the board or major shareholders

commanding majority of voting power;

b) Purchase of shares in open market;

c) To make takeover offer to the general body of shareholders;

d) Purchase of new shares by private treaty;

e) Acquisition of share capital through the following forms of considerations viz.

Means of cash, issuance of loan capital, or insurance of share capital.

[12]

Merger process:-

Defining the corporate strategy

Implementation the corporate strategy

Target identification

Valuation of merger

Merger implementation

Post-merger integration

1) Defining the Corporate Strategy: A firm needs to first clearly define its

corporate strategy- what business the firm is currently ? What business it

intends to be in ? How does it wish to grow, and be known as?

2) Implementing the Corporate Strategy: Next, the firm should define a route

or roadmap to implement its corporate strategy - whether it intends to use

mergers or joint ventures/strategic alliances, or internal development as a

strategy for its growth/diversification plan.

3) Target Identification: If the firm finds it attractive to pursue the M&A route,

sufficient effort should be devoted to identification of the right kind of a target

firm to merge/acquire. The parameters for identification should include the

[13]

financial considerations, business strengths and weakness, the specific

resources, etc.

4) Valuation of the Merger: Then, a financial valuation of the merger should

begin. The specific cost and the premium that the firm would like to pay for

acquiring share/management control of the target firm would again depend on

the projected synergies that the merger is likely to bring about.

5) Merger Implementation: The tax, regulatory, and market issues dominate the

next stage of the merger process – the merger implementation. In this stage,

when the merger is begin implemented, depending on the local laws,

conditions, and shareholder prederences, the merger could happen through a

stock swap, a cash offer, or any other method.

6) Post – Merger Integration: The final stage called the post – merger

integration includes activities like asset stripping (selling off those assets in the

target company that are not likely to add value to the merged/acquired firm);

efforts at improving the operating efficiency and setting up managerial systems

at the acquired firm.

[14]

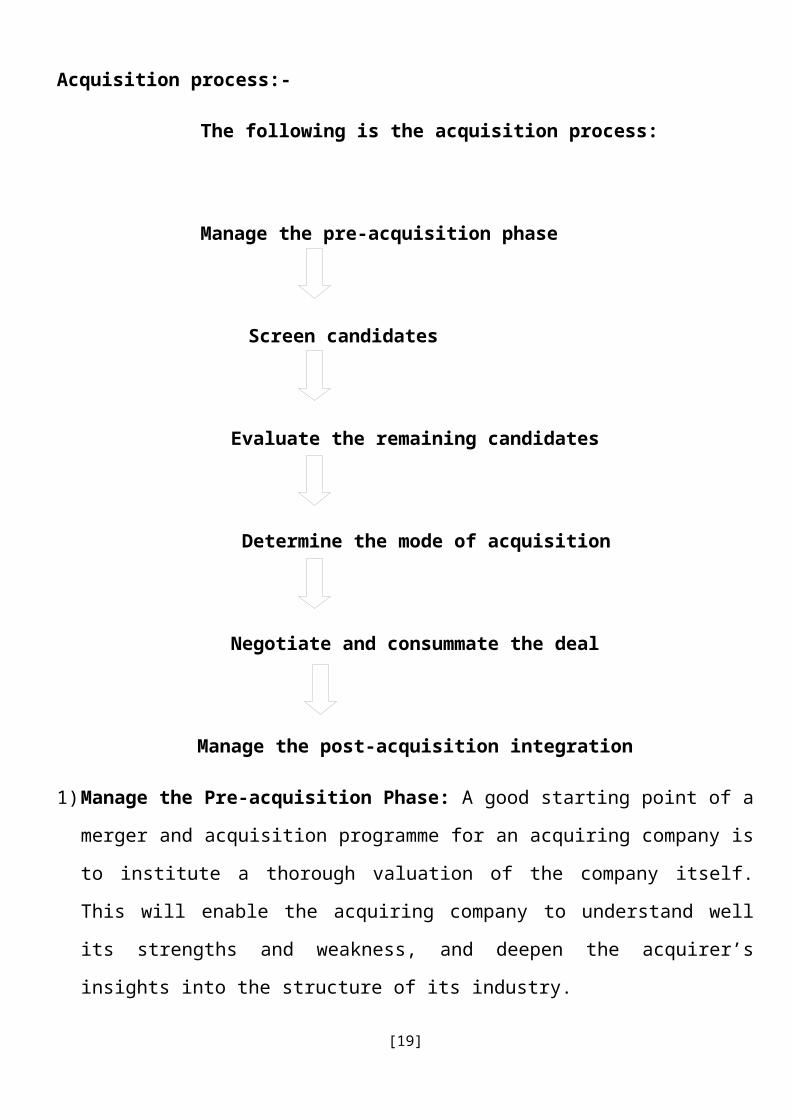

Acquisition process:-

The following is the acquisition process:

Manage the pre-acquisition phase

Screen candidates

Evaluate the remaining candidates

Determine the mode of acquisition

Negotiate and consummate the deal

Manage the post-acquisition integration

1) Manage the Pre-acquisition Phase: A good starting point of a merger and

acquisition programme for an acquiring company is to institute a thorough

valuation of the company itself. This will enable the acquiring company to

understand well its strengths and weakness, and deepen the acquirer’s insights

into the structure of its industry.

2) Screen Candidates: The ideas generated in the brainstorming sessions and the

suggestions received from various quarters will have to be filtered. Screening criteria

that make sense for the acquiring company’s perspective need to be used.

3) Evaluation the Remaining Candidates: The screening criteria applied in step 2 will

narrow down the list of candidates to a fairly small number. Each of them should be

[15]

examined thoroughly. A comprehensive evaluation must cover in great detail the

following aspects: operations, plant facilities, distribution network, sales, personnel, and

finances. Special attention should be paid to the quality of management.

4) Determine the Mode of Acquisition: The three major modes of acquisition are merger,

purchase of assets, and takeover. In addition, one may look at leasing a facility or

entering into a management contract.

5) Negotiate and Consummate the Deal: for successful negotiation, the acquiring firm

should know how valuable the acquisition candidate is to the firm, to the present owner,

and to other potential acquirers.

6) Manage the Post-acquisition Integration: Generally after the acquisition the new

controlling group tends to be much more ambitious and is inclined to assume a higher

degree of risk.

[16]

Takeover:

A ‘takeover’ is acquisition and both the terms are used inter changeably. Takeover

differs from merger in approach to business combinations i.e. The process of

takeover, transaction involved in takeover, determination of share exchange or cash

price and the fulfillment of goals of combination all are different in takeovers than in

mergers. For example, process of takeover is unilateral and the offer or

company decides about the maximum price.

Time taken in completion of transaction is less in takeover than in mergers, top

management of the offer company being more co-operative.

Kinds of takeovers:

Negotiated or Friendly Takeover

The existing management of a company decides to give away the control of the

company to another group on terms and conditions mutually agreed upon by both

the parties.

Open market or Hostile Takeover

A group acquires shares of a company from the open market in order to take

control of the company

Bail-out Takeover

When a financially sick company is taken over by a profit earning company in

order to bail out the form ,it is called a bail-out takeover.

[17]

Hostile Takeover Strategies:-

Tender Offer

General offer made publicly and directly to a firm’s shareholders to buy their stock

at a price well above the current market price.

Street Sweep

The acquirer accumulates large amounts of the stocks in the target company

before making the open offer

Bear Hug

The acquirer tries to put pressure on the management of the target firm by

threatening to make an open offer

Strategic Alliance

An acquirer offers a partnership rather than a buyout of the target firm.

Brand Power

The acquiring firm enters into an alliance with other powerful brands to

displace the competitor’s brand.

Issues in takeover:-

Economic Issues

Legal Issues

Public Policy Issues

Powers of financial institutions

Proxy wars

[18]

Effects of Takeovers:-

Effects on the Acquirer Company

Effects on the Target company

Effects on the Shareholders of the Target Company

Effects on the Shareholders of Acquiring Company

[19]

PURPOSE OF THE MERGER AND ACQUISITION

The purpose for an offer or company for acquiring another company shall be

reflected in the corporate objectives. It has to decide the specific objectives to be

achieved through acquisition. The basic purpose of merger or business combination

is to achieve faster growth of the corporate business. Faster growth may be had

through product improvement and competitive position. Other possible purposes for

acquisition are short listed below: -

(1) Procurement of supplies:

To safeguard the source of supplies of raw materials or intermediary product;

To obtain economies of purchase in the form of discount,

savings in transportation costs, overhead costs in buying department, etc.;

To share the benefits of suppliers economies by standardizing the materials.

(2) Revamping production facilities:

To achieve economies of scale by amalgamating production facilities through

more intensive utilization of plant and resources;

To standardize product specifications, improvement of quality of product,

expanding Market and aiming at consumers satisfaction through strengthening

after sale Services;

To obtain improved production technology and know-how from the offered

company

To reduce cost, improve quality and produce competitive products to retain

and Improve market share.

(3) Market expansion and strategy:

[20]

To eliminate competition and protect existing market;

To obtain a new market outlets in possession of the offeree;

To obtain new product for diversification or substitution of existing products

and to enhance the product range;

Strengthening retain outlets and sale the goods to rationalize distribution;

To reduce advertising cost and improve public image of the company;

Strategic control of patents and copyrights.

(4) Financial strength:

To improve liquidity and have direct access to cash resource;

To dispose of surplus and outdated assets for cash out of combined

enterprise;

To enhance gearing capacity, Bank of Rajasthan row on better strength and

the greater assets backing;

To avail tax benefits;

To improve EPS (Earning per Share).

(5) General gains:

To improve its own image and attract superior managerial talents to manage

its affairs;

To offer better satisfaction to consumers or users of the product.

(6) Own developmental plans:

The purpose of acquisition is backed by the offer or company’s own developmental

plans.

A company thinks in terms of acquiring the other company only when it has

arrived at its own development plan to expand its operation having examined its

own internal strength where it might not have any problem of taxation, accounting,

valuation, etc. but might feel resource constraints with limitations of funds and lack

of skill managerial personnel’s. It has to aim at suitable combination where it could [21]

have opportunities to supplement its funds by issuance of securities, secure

additional financial facilities, eliminate competition and strengthen its market

position.

(7) Strategic purpose:

The Acquire Company view the merger to achieve strategic objectives through

alternative type of combinations which may be horizontal, vertical, product

expansion, market extensional or other specified unrelated Objectives depending

upon the corporate strategies.

Thus, various types of combinations distinct with each other in nature are adopted to

pursue this objective of horizontal combination.

(8) Corporate friendliness:

Although it is rare but it is true that business houses exhibit degrees of co-operative

spirit despite competitiveness in providing rescues to each other from hostile

takeovers and cultivate situations of colla Bank of Rajasthan nations sharing

goodwill combinations. He combining corporate aim at circular combinations by

pursuing the objective.

(9) Desired level of integration:

Mergers and acquisitions are pursued to obtain the desired level of integration

between the two combining business houses. Such integration could be operational

or financial. This gives birth to conglomerate combinations. The purpose and the

requirements of the offer or company go a long way in selecting a suitable partner

for merger or acquisition in business combinations.

[22]

TYPES OF MERGERS

Merger or acquisition depends upon the purpose of the offer or company it wants to

achieve. Based on the offer or’s objective profile, combination could be vertical,

horizontal, circular and conglomeratic as precisely described below with reference to

the purpose in view of the offer or company.

(A) Vertical combination:

A company would like to takeover another company or seek its merger with that

company to expand espousing backward integration to assimilate the resources of

supply and forward integration towards market outlets. The acquiring company

through merger of another unit attempts on reduction of inventories of raw material

and finished goods, implements its production plans as per the objectives and

economizes on working capital investments. In other words, in vertical combinations,

the merging undertaking would be either a supplier or a buyer using its product as

intermediary material for final production.

The following main benefits accrue from the vertical combination to the acquirer

company i.e.

1. It gains a strong position because of imperfect market of the intermediary

products, scarcity of resources and purchased products;

2. Has control over products specifications.

(B) Horizontal combination:

It is a merger of two competing firms which are at the same stage of industrial

process. The acquiring firm belongs to the same industry as the target company.

The mail purpose of such mergers is to obtain economies of scale in production by

eliminating duplication of facilities and the operations and broadening the product

line, reduction in investment in working capital, elimination in competition

concentration in product, reduction in advertising costs, increase in market segments

and exercise better control on market.[23]

(C) Circular combination:

Companies producing distinct products seek amalgamation to share common

distribution and research facilities to obtain economies by elimination of cost on

duplication and promoting market enlargement. The acquiring company obtains

benefits in the form of economies of resource sharing and diversification.

(D) Conglomerate combination:

It is amalgamation of two companies engaged in unrelated industries like DCM

and Modi Industries. The basic purpose of such amalgamations remains utilization of

financial resources and enlarges debt capacity through re-organizing their financial

structure so as to service the shareholders by increased leveraging and EPS,

lowering average cost of capital and thereby raising present worth of the outstanding

shares.

[24]

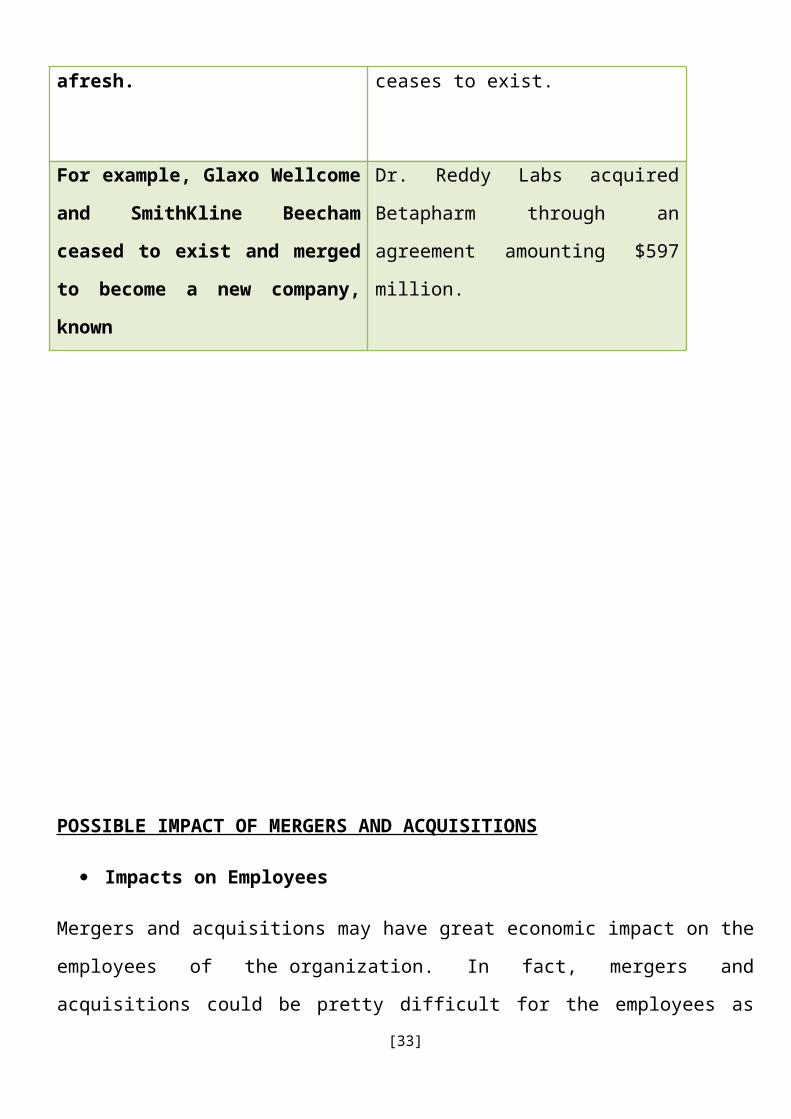

DIFFERENCE BETWEEN MERGERS AND AQUISITION

Merger Acquisition

The case when two companies

(often of same size) decide to

move forward as a single new

company instead of operating

business separately.

The case when one company takes

over another and establishes itself

as the new owner of the business.

The stock of both the companies

are surrendered while new stock

are issued afresh.

The buyer company “swallows” the

business of the target company,

which ceases to exist.

For example, Glaxo Wellcome and

SmithKline Beecham ceased to

exist and merged to become a

new company, known

Dr. Reddy Labs acquired Betapharm

through an agreement amounting

$597 million.

[25]

POSSIBLE IMPACT OF MERGERS AND ACQUISITIONS

Impacts on Employees

Mergers and acquisitions may have great economic impact on the employees of

the organization. In fact, mergers and acquisitions could be pretty difficult for the

employees as there could always be the possibility of layoffs after any merger or

acquisition. If the merged company is pretty sufficient in terms of business

capabilities, it doesn't need the same amount of employees that it previously had to

do the same amount of business. Due to the changes in the operating environment

and business procedures, employees may also suffer from emotional and physical

problems.

Impact on Management

The percentage of job loss may be higher in the management level than the general

employees. The reason behind this is the corporate culture clash. Due to change

in corporate culture of the organization, many managerial level professionals, on

behalf of their superiors, need to implement the corporate policies that they might

not agree with. It involves high level of stress.

Impact on Shareholders

Impact of mergers and acquisitions also include some economic impact on the

shareholders. If it is a purchase, the shareholders of the acquired company get

highly benefited from the acquisition as the acquiring company pays a hefty amount

for the acquisition. On the other hand, the shareholders of the acquiring company

suffer some losses after the acquisition due to the acquisition premium and

augmented debt load.

Impact on Competition

[26]

Mergers and acquisitions have different impact as far as market competitions are

concerned. Different industry has different level of competitions after the mergers

and acquisitions. For example, the competition in the financial services industry is

relatively constant. On the other hand, change of powers can also be observed

among the market players.

[27]

ADVANTAGES OF MERGERS

Mergers and takeovers are permanent form of combinations which vest in

management complete control and provide centralized administration which are not

available in combination of holding company and its partly owned subsidiary.

Shareholders in the selling company gain from the merger and takeovers as the

premium offered to induce acceptance of the merger or takeover offers much more

price than the book value of shares. Shareholders in the buying company gain in the

long run with the growth of the company not only due to synergy but also due to

“boots trapping earnings”.

Mergers and acquisitions are caused with the support of shareholders, manager’s ad

promoters of the combing companies. The factors, which motivate the shareholders

and managers to lend support to these combinations and the resultant

consequences they have to bear, are briefly noted below based on the

research work by various scholars globally.

(1) From the standpoint of shareholders

Investment made by shareholders in the companies should enhance in value. The

sale of shares from one company’s shareholders to another and holding investment

in shares should give rise to greater values i.e. The opportunity gains in alternative

investments. Shareholders may gain from merger in different ways viz. From the

gains and achievements of the company i.e. through

(a)Realization of monopoly profits;

(b)Economies of scales;

(c)Diversification of product line;

(d)Acquisition of human assets and other resources not available otherwise;

( e ) Better investment opportunity in combinations

[28]

One or more features would generally be available in each merger where

shareholders may have attraction and favor merger.

(2)From the standpoint of managers

Managers are concerned with improving operations of the company, managing the

affairs of the company effectively for all round gains and growth of the company

which will provide them better deals in raising their status, perks and fringe benefits.

Mergers where all these things are the guaranteed outcome get support from the

managers. At the same time, where managers have fear of displacement at the

hands of new management in amalgamated company and also resultant

depreciation from the merger then support from them becomes difficult.

(3) Promoter’s gains

Mergers do offer to company promoters the advantage of increasing the size of their

company and the financial structure and strength. They can convert a closely held

and private limited company into a public company without contributing much wealth

and without losing control.

4) Benefits to general public

Impact of mergers on general public could be viewed as aspect of benefits and costs

to:

(a) Consumers

The economic gains realized from mergers are passed on to consumers in the form

of lower prices and better quality of the product which directly raise their standard of

living and quality of life. The balance of benefits in favour of consumers will depend

upon the fact whether or not the mergers increase or decrease competitive

economic and productive activity which directly affects the degree of welfare of the

[29]

consumers through changes in price level, quality of products, after sales service,

etc.

(b) Workers community

The merger or acquisition of a company by a conglomerate or other acquiring

company may have the effect on both the sides of increasing the welfare in the form

of purchasing power and other miseries of life. Two sides of the impact as discussed

by the researchers and academicians are:

First, mergers with cash payment to shareholders provide opportunities for them to

invest this money in other companies which will generate further employment and

growth to uplift of the economy in general. Secondly, any restrictions placed on such

mergers will decrease the growth and investment activity with corresponding

decrease in employment.

Both workers and communities will suffer on lessening job Opportunities, preventing

the distribution of benefits resulting from diversification of production activity.

(c) General public

Mergers result into centralized concentrate of power. Economic power is to be

understood as the ability to control prices and industries output as

monopolists. Such monopolists affect social and political environment to till

everything in their favour to maintain their power ad expand their business empire.

These advances result into economic exploitation.

But in a free economy a monopolist does not stay for a longer period as other

companies enter into the field to reap the benefits of higher prices set in by the

monopolist. Every merger of two or more companies has to be viewed from different

angles in the business practices which protects the interest of the shareholders in

the merging company and also serves the national purpose to add to the welfare of

the employees, consumers and does not create hindrance in administration of the

Government polices..

[30]

REGULATIONS OF MERGER AND ACQUISTIONS

Mergers and acquisitions are regulated under various laws in India. The objective of

the laws is to make these deals transparent and protect the interest of all

shareholders. They are regulated through the provisions of:-

The Companies Act, 1956

The Act lays down the legal procedures for mergers or acquisitions:-

Permission for merger :- Two or more companies can amalgamate only when

the amalgamation is permitted under their memorandum of association. Also,

the acquiring company should have the permission in its object clause to carry

on the business of the acquired company. In the absence of these provisions

in the memorandum of association, it is necessary to seek the permission of

the shareholders, board of directors and the Company Law Board before

affecting the merger.

Information to the stock exchange : - The acquiring and the acquired companies

should inform the stock exchanges (where they are listed) about the merger.

Approval of board of directors: - The board of directors of the individual companies

should approve the draft proposal for amalgamation and authorize the

managements of the companies to further pursue the proposal.

Application in the High Court: - An application for approving the draft

amalgamation proposal duly approved by the board of directors of the

individual companies should be made to the High Court.

[31]

Shareholders' and creators' meetings: - The individual companies should hold

separate meetings of their shareholders and creditors for approving

the amalgamation scheme. At least, 75 percent of shareholders and creditors

in separate meeting, voting in person or by proxy, must accord their approval

to the scheme.

Sanction by the High Court: - After the approval of the shareholders

and creditors, on the petitions of the companies, the High Court will pass an

order, sanctioning the amalgamation scheme after it is satisfied that the

scheme is fair and reasonable. The date of the court's hearing will be

published in two newspapers, and also, the regional director of the Company

Law Board will be intimated.

Filing of the Court order: After the Court order, its certified true copies will be

filed with the Registrar of Companies.

Transfer of assets and liabilities : - The assets and liabilities of the acquired

company will be transferred to the acquiring company in accordance with the

approved scheme, with effect from the specified date.

Payment by cash or securities :- As per the proposal, the acquiring company

will exchange shares and debentures and/or cash for the shares and

debentures of the acquired company. These securities will be listed on

the stock exchange.

[32]

The Competition Act, 2002

The Act regulates the various forms of business combinations through Competition.

Under the Act, no person or enterprise shall enter into a combination, in the form of

an acquisition, merger or amalgamation, which causes or is likely to cause an

appreciable adverse effect on competition in the relevant market and such a

combination shall be void. Enterprises intending to enter into a combination may

give notice to the Commission, but this notification is voluntary. But, all combinations

do not call for scrutiny unless the resulting combination exceeds the thresh old limits

in terms of assets or turnover as specified by the Competition Commission of India.

The Commission while regulating a 'combination' shall consider the following

factors:-

• Actual and potential competition through imports;

• Extent of entry barriers into the market;

• Level of combination in the market;

• Degree of countervailing power in the market;

• Possibility of the combination to significantly and substantially increase prices or

profits;

• Extent of effective competition likely to sustain in a market;

• Availability of substitutes before and after the combination;

• Market share of the parties to the combination individually and as a combination;

• Possibility of the combination to remove the vigorous and effective competitor

or competition in the market;

[33]

• Nature and extent of vertical integration in the market;

• Nature and extent of innovation;

• Whether the benefits of the combinations outweigh the adverse impact of the

combination.

Thus, the Competition Act does not seek to eliminate combinations and only aims

to eliminate their harmful effects.

[34]

PROCEDURE OF MERGERS & ACQUISITIONS

Public announcement:

To make a public announcement an acquirer shall follow the following procedure:

1. Appointment of merchant banker :

The acquirer shall appoint a merchant banker registered as category – I with SEBI to

advise him on the acquisition and to make a public announcement of offer on his

behalf.

2. Use of media for announcement :

Public announcement shall be made at least in one national English daily one Hindi

daily a done regional language daily newspaper of that place where the shares of

that company are listed and traded.

3. Timings of announcement:

Public announcement should be made within four days of finalization of negotiations

or entering into any agreement or memorandum of understanding to acquire the

shares or the voting rights.

4 Contents of announcement:

Public announcement of offer is mandatory as required under the SEBI

Regulations.

[35]

(1)Paid up share capital of the target company, the number of fully paid up

and partially paid up shares.

( 2 ) Total number and percentage of shares proposed to be acquired from public

subject to minimum as specified in the sub-regulation (1) of Regulation 21 that is:

a) The public offer of minimum 20% of voting capital of the company to the

shareholders;

b) The public offer by a raider shall not be less than 10% but more than 51%

of shares of voting rights. Additional shares can be had @ 2% of voting rights in any

year.

(3)The minimum offer price for each fully paid up or partly paid up share;

( 4 ) Mode of payment of consideration;

(5) The identity of the acquirer and in case the acquirer is a company, the identity of

the promoters and, or the persons having control over such company and the group,

if any, to which the company belong;

( 6 ) The existing holding, if any, of the acquirer in the shares of the target company,

including holding of persons acting in concert with him;

(7) Salient features of the agreement, if any, such as the date, the name of the

seller, the price at which the shares are being acquired, the manner of payment of

the consideration and the number and percentage of shares in respect of which the

acquirer had entered into the agreement to acquire the shares or the consideration,

monetary or otherwise, for the acquisition of control over the target company, as the

case may be;

[36]

(8)The highest and the average paid by the acquirer or persons acting in concert

with him for acquisition, if any, of shares of the target company made by

him during the twelve month period prior to the date of the public announcement;

( 9 ) Objects and purpose of the acquisition of the shares and the future plans of the

acquirer for the target company, including disclosers whether the acquirer proposes

to dispose of or otherwise encumber any assets of the target company:

Provided that where the future plans are set out, the public announcement

shall also set out how the acquirers propose to implement such future plans;

(10)The ‘specified date’ as mentioned in regulation 19;

(11)The date by which individual letters of offer would be posted to each of the

shareholders;

(12)The date of opening and closure of the offer and the manner in which and the

date by which the acceptance or rejection of the offer would be communicated to the

shareholders;

(13)The date by which the payment of consideration would be made for the shares

in respect of which the offer has been accepted;

(14) Disclosure to the effect that firm arrangement for financial resources required to

implement the offer is already in place; including the details regarding the sources

of the funds whether domestic i.e. from banks, financial institutions, or otherwise

or foreign i.e. from Non-resident Indians or otherwise;

[37]

(15)Provision for acceptance of the offer by person who own the shares but are not

the registered holders of such shares;

(16)Statutory approvals required to obtained for the purpose of acquiring the

shares under the Companies Act, 1956, the Monopolies and Restrictive Trade

Practices Act, 1973, and/or any other applicable laws;

(17)Approvals of banks or financial institutions required, if any;

( 1 8 ) Whether the offer is subject to a minimum level of acceptances from the

shareholders; and

(19)Such other information as is essential fort the shareholders to make an informed

design in regard to the offer.

[38]

WHY MERGERS FAIL?

It's no secret that plenty of mergers don't work. Those who advocate mergers will

argue that the merger will cut costs or boost revenues by more than enough to

justify the price premium. It can sound so simple: just combine computer systems,

merge a few departments, use sheer size to force down the price of supplies and the

merged giant should be more profitable than its parts. In theory, 1+1 = 2 sounds

great, but in practice, things can go awry.

Historical trends show that roughly two thirds of big mergers will disappoint on their

own terms, which means they will lose value on the stock market. The motivations

that drive mergers can be flawed and efficiencies from economies of scale may

prove elusive. In many cases, the problems associated with trying to make merged

companies work are all too concrete.

Below example show the, how would be implication came in banking

sector:

4.3 FINANCIAL IMPLICATIONS OF BANKING M&A

These indicators include measures of financial performance:

asset and liability composition

capital structure

liquidity

risk exposure

profitability

financial innovation and efficiency

As dependent variable, we measure change of performance as the difference

between the merged banks two-year average return on equity (ROE ) after the

[39]

acquisition and the weighted average of the ROE of the merging banks two years

before the acquisition.

COST OF MERGERS AND ACQUISITIONS

Costs of mergers and acquisitions are an important and integral part of mergers and acquisitions process. Before going for any merger or acquisition, both the companies calculate the costs of mergers and acquisitions to find out the viability and profitability of the deal. Based on the calculation, they decide whether they should go with the deal or not.

In mergers and acquisitions, both the companies may have different theories about

the worth of the target company. The seller tries to project the value of the company

high, whereas buyer will try to seal the deal at a lower price. There are a number

of legitimate methods for valuation of companies.

5.1 REASONS FOR MERGERS AND ACQUISITIONS

Capacity

Economies of Scale

Accessing technology or skills

Tax reasons

Growth with External Efforts

Deregulation

Technology

New Products/Services

Over Capacity

Customer Base

Merger of Weak Bank

[40]

Chapter no:- 4

PROCEDURE FOR BANK MERGER

[41]

PROCEDURE FOR BANK MERGER

The procedure for merger either voluntary or otherwise is outlined in

the respective state statutes/the Banking regulation Act. The Registrars, being

the authorize vested with the responsibility of administering the Acts,

will be ensuring that the due process prescribed in the Statues has been

compiled with before they seek the approval of the RBI.

They would also be ensuring compliance with the statutory procedures for

notifying the amalgamation after obtaining the sanction of the RBI.

Before deciding on the merger, the authorized officials of the acquiring

bank and the merging bank sit together and discuss the procedural modalities

and financial terms. After the conclusion of the discussions, a scheme is

prepared incorporating therein the all the details of both the banks and the

area terms and conditions.

Once the scheme is finalized, it is tabled in the meeting of Board of directors of

respective banks. The board discusses the scheme thread bare

and accords its approval if the proposal is found to be financially viable

and beneficial in long run.

After the Board approval of the merger proposal, an extra ordinary general

meeting of the shareholders of the respective banks is convened to discuss

the proposal and seek their approval.

[42]

After the board approval of the merger proposal, a registered valuer is

appointed to valuate both the banks. The value valuates the banks on the

basis of its share capital, market capital, assets and liabilities, its reach

and anticipated growth and sends its report to the respective banks.

Once the valuation is accepted by the respective banks, they send the

proposal along with all relevant documents such as Board approval,

shareholders approval, valuation report etc. to Reserve Bank of India and

other regulatory bodies such Security and Exchange Board of India(SEBI) for

their approval.

After obtaining approvals from all the concerned institutions, authorized

officials of both the banks sit together and discuss and finalize share allocation

proportion by the acquiring bank to the shareholders of the merging

bank (SWAP ratio)

After completion of the above procedures, a merger and acquisition agreement

is signed by the bank.

[43]

Chapter no :-5

GUIDELINES ON MERGERS & ACQUISITIONS OF

BANKS

[44]

GUIDELINES ON MERGERS & ACQUISITIONS OF BANKS

With a view to facilitating consolidation and emergence of strong

entities and providing an avenue for non disruptive exit of weak/unviable

entities in the banking sector, it has been decided to frame guidelines to

encourage merger/amalgamation in the sector.

Although the Banking Regulation Act, 1949 (AACS) does not empower

Reserve Bank to formulate a scheme with regard to

merger and amalgamation of banks, the State Governments have incorporated

in their respective Acts a provision for obtaining prior sanction in writing, of RBI

for an order, inter alia, for sanctioning a scheme of amalgamation or

reconstruction.

[45]

The request for merger can emanate from banks registered under the same

State Act or from banks registered under the Multi State Co-operative

Societies Act (Central Act) for takeover of a bank/s registered under State

Act. While the State Acts specifically provide for merger of co-operative

societies registered under them, the position with regard to take over of a co-

operative bank registered under the State Act by a co-operative bank

registered under the CENTRAL

Although there are no specific provisions in the State Acts or the Central Act

for the merger of a co-operative society under the State Acts with that under

the Central Act, it is felt that ,if

Allconcerned including administrators of the concerned Acts are agreeable to

order merger/amalgamation, RBI may consider proposals on merits leaving

the question of compliance with relevant statutes to the administrators of the

Acts. In other words, Reserve Bank will confine its examination only to

financial aspects and to the interests of depositors as well as the stability

of the financial system while considering such proposals.

[46]

Chapter no: 4Data analysis of merger and acquisition of

some company

[47]

British Salt Acquisition-20thDecember 2010

Background:-

All soda ash manufacturers have ownership of their key raw material –tronaor salt deposits

This was the case for Brunner Mond (BM) until 1991 when it was divested from ICI –the salt deposits are now owned by Ineos

This highly unusual position has been made tenable by the existence of a 25 year contract made as part of the divestment

It has been recognized for some time that BM needs to restore the umbilical to its key raw material

The existing contract with Ineos is set to expire in 2016

Due to the consolidated nature of salt (Brine) industry, BM is at a disadvantage to negotiate a similar long term contract with Ineos

In case of contract renewal with Ineos, it is expected that BM’s sourcing cost for brine would increase substantially

British Salt is the only other producer of Brine in UK

British Salt (BS)British Salt, established in the 1920s is located in Middlewich, UK

Products from BS stable are:Brine

Un-dried vacuum salt

Pure dried vacuum salt

Compact vacuum saltBS currently produces 390 ktesof vacuum salt per year and is the leader in UK evaporated salt market

[48]

Salt reserves of BS can serve UK requirement for up to ~50 years

BS has developed long standing relationships with leading companies in food, Industrial and Chemicals sectors in UK

It’s customer relationship with key customers extends up to 30 years

In the recent years, BS has successfully developed gas storage opportunities from brine cavities

UK evaporated salt market share 2009 by volume

import ineos

British salt

Strategic benefits from acquisition

Provides secure, cost-effective brine supply

Maintains and enhances BM’s low cost position within Europe

Generates substantial and consistent cash flows from the highly profitable and non- cyclical vacuum salt business

Generates additional cash flows from operational synergies between British salt and BM

Unique opportunity to generate large cash flows from gas storage business

Acquisition details

British Salt has been valued at £93 m (approx. 6x EBITDA)

[49]

BM to have 100% equity ownership of BS

The deal is entirely debt financed on a non- recourse basis to Tata Chemicals

Financial ImpactImpact on BM UK

Maintenance of sourcing costs at current levels which would not have been possible without this deal

Increased EBITDA of £15m per year from vacuum salt business

Synergies between BM and British Salt to result in EBITDA improvement of £2m per year

Increased cash of £45m from lease of cavities for gas storage after 5 years

BS’s defined benefit pension in small surplus on FRS17 basis and closed to future accrual

Impact on TCL

Post- acquisition, TCL comfortably placed in view of existing debt covenants on a consolidated basis

Adidas acquired to Reebok

Adidas company profile:-

Founded in 1926

World leader in soccer shoes

#2 behind Nike worldwide - #4 in the US

Three acquisitions before Reebok:

Company Sports Incorporation in 1993

Salomon in 1997

Arc'Teryxin 2002

Culture of control, engineering, and production

[50]

Reebok company profile:-

Founded in 1895

First athletic shoe for woman

#2 in US - #4 in Europe

Strong sales growth from 2002-2004

Unique portfolio of long term league licenses

Creative marketing-driven culture

INDUSTRY OVERVIEW

One of the most competitive industries.

Over 75% of the industry controlled by branded items.

Large players – supplier power and access to shelf space.

Small players – anticipating a fashion trend.

Private label a threat.

US FOOTWEAR MARKET

[51]

ACQUISITION BACKGROUND

Goal: increase share in the U.S. market + better compete with Nike

Stock prices improved the day of announcement

Reebok sales down in fourth quarter of 2005

Deal closed on January 2006

Price: $3.52 billion

SWOT ANALYSIS

STRENGTH

Adidas is strong in Europe, Reebok is strong in US, & Asia

Complementary licenses and contracts

Reduced costs for retailers

Reebok is extremely strong in Women’s wear

WEAKNESSES

Many overlapping products

Two HQ’s that will be hard to integrate

Two very strong, distinct corporate cultures

OPPORTUNITIES

Leverage combined R&D strengths & budgets

Bring Reebok’s women’s wear to Europe

Reduce costs to retailers by larger distribution networks

Ability for better reaction to global trends

[52]

THREATS

Competition between brands employees

Cannibalization of sales

Realization of revenue growth synergies

Adidas may treat Reebok as a second tier brand

SYNERGIES

Geographies and Categories

Idea sharing across markets and geographies

Capitalize on Reebok's skills and know how to accelerate Adidas position in North America

Benefit from Adidas expertise in Europe and Reebok's in Asia

Combine expertise in branded and licensed athletic apparel

Consumer & Demographics

Ability to identify sport/style trends

Better product and category prioritization

More products and more price points

Continue brand developments into new segments

Benefit from Reebok's expertise in Women's segment

Capitalize from Reebok's skills in sport lifestyle and leisure

Technology

Enhance profile as technology leader and innovation leader

Bigger combined R&D spend

More products to capitalize on R&D spending

New technology developments and awareness across brands

Applications

[53]

Materials

Licenses, Events and Teams

Transfer of skills and know-how

Management of exclusive agreements

Relationship with teams and athletes

More active events calendar

ACTUAL ACQUISITION STATISTICS

Adidas paid $3.527 billion for Reebok

Adidas paid $59.00 per share for all of Reebok’s shares

Adidas paid a 34.2% premium which was still accretive to the P/E ratio

Based on our model Adidas could have paid between $53.91 & $66.85

INTEGRATION ISSUES

Research & Development

Combined to share both costs and technology

Reduced employees and raised efficiencies

Brand Imaging to Reebok as Premium Shoe

New “Pay-as-You-go” system reduces retailer sales on Reebok

Customize shoes through a website

Increase Prices

Reduce manufacturing of Classic Styles

Geographies and Product Lines

Increased international presence and product lines (i.e. shoes & apparel)

[54]

Licenses, Events and Teams

Very similar strategy for both brands but Adidas gets Reebok NBA contract

Contd……

Management /Structure Changes

New Brand CEO’s and Reebok CEO to Advisor

Head Quarters to Remain

Integration planning team comprised of employees from both

Employee Care and Retention

Mixed employee benefits

HR resources to all employees

Distribution Centers and Back Operations

Combined many Distribution Centers and Back Operations

Reebok switched from a “Bulk Pre-Order” system to “Pay-as-You-go”

Consolidate Suppliers

POST INTEGRATION RESULTS

Management/Structure Changes

Successful through speed, efficiency and cooperation

Employee Care

Handled as well as could be expected

Distribution Centers

Mixed Emotions in short term, spent money to become efficient

Taking longer than anticipated

R&D

Successful at reaching companies goals on new products & efficiency

[55]

Brand Imaging

Continue to face uphill battle and challenge

Success is still possible in long term

Geographies and Product Lines

Expansion into new countries has partially offset loses in mature markets

New product lines and strategies have produced mixed results

Licenses, Events and Teams

With little change no success or failure has been noticed

DID MERGER WORK???

“Our focus this year will be on getting Reebok back onto a growth track. It's going to take time, but we're moving in the right direction.”

- Herbert Hainer, Adidas Chief Executive in 2007

Gross margins dropped 3.6% in 2007.

Sales and order back log of Reebok declined.

The whole group still made money.

WHAT WENT WRONG??

Misperception among Retail Partners about the future of Reebok’s brand strategy

Questions about the German – American Corporate Culture.

Underestimation of competition from Nike.

WHAT HAPPENING NOW??

[56]

In 2008, Adidas put in an extra $50 million to bring back Reebok on

track.Started realizing some of the synergies in late 2008 but on a lower scale than estimated.

CONCLUSION

One of the most common reasons for mergers and acquisitions is the belief that

"synergies" exist, allowing the two companies to work more efficiently together than

either would separately. Such synergies may result from the firms' combined ability

to exploit economies of scale, eliminate duplicated functions, share managerial

expertise, and raise larger amounts of capital. Another reason for banks to

move towards merger is that they are motivated by a desire for greater market

power.

The 'human factor' is a major cause of difficulty in making the integration between

two companies work successfully. If the transition is carried out without sensitivity

towards the employees who may suffer as result of it, and without awareness of

the vast differences that may exist between corporate cultures, the result is a

stressed, unhappy and uncooperative workforce - and consequently a drop in

productivity Decision to carry out a merger or acquisition should consider not only

the legal and financial implications, but also the human consequences - the effect of

the deal upon the two companies' managers and employee

Almost 60 -70% mergers and acquisitions and the reason for the failure is cultural

differences, flawed intentions, and sometimes decisions are taken without properly

analysis the future of the merger.

[57]

Recommendation:-

The conclusion shows that the merger and acquisition is becoming more important

in day to day life from the point of view of the loss running business and for those

entrepreneur who wants to expand their business by selling a unit or buy

purchasing a unit or the entire empire. Regular increase in competition has made

merger and acquisition a necessity. Some Companies depend on the risk and return

and give tips to their companies to make flexibility in the market.

[58]

WIBLOGRAPHY

www.investopedia.com

www.business.mapsofindia.com

www.bloomberg.com

www.legalserviceindia.com

www.slideboom.com

www.papercamp.com

www.moneycontrol.com

[59]