member service representative

TRANSCRIPT

General Responsibilities and Requirements

Member Service Representative

04/29/2021

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

2

Table of Contents Section 1: General Member Service Requirements ......................................... 9

Member Services Responsibilities .................................................................. 9 Profile ..................................................................................................... 9 Favorable Service Techniques .................................................................... 9 Initial Contact/Greeting the member ......................................................... 10 Cut Off All Other Work Interruptions ......................................................... 10 Interview ............................................................................................... 10

Products and Services ................................................................................ 11 Fee Schedule ............................................................................................ 12

Account Fees.......................................................................................... 12 Other Service Fees.................................................................................. 12 Safe Deposit Box Fees ............................................................................. 13 Bill Pay Fees .......................................................................................... 13

Section 2: Regulations .............................................................................. 14

Office of Foreign Assets Control Policy .......................................................... 14 Member Service Representatives .............................................................. 14 What to do with the Verafin information provided ....................................... 14

Securities Transfer Agents Medallion Program – (STAMP) ............................... 16 Purpose ................................................................................................. 16 Procedures............................................................................................. 16 Authorized Signers .................................................................................. 16

Customer Identification Policy (CIP) ............................................................. 18 CIP Procedures ....................................................................................... 19 Coverage ............................................................................................... 19

Collection of Information from Individuals .................................................... 20 Information Required .............................................................................. 20 Verification of the Identity of Individuals ................................................... 20 Person Not Present (New and Existing Member) ......................................... 21 Record Retention .................................................................................... 22

Checking Government Lists ........................................................................ 23 Verifying Member’s Identity by Phone .......................................................... 24

Guidelines.............................................................................................. 24 Membership Eligibility Verification ................................................................ 25

Underserved Area ................................................................................... 25 Sponsorship ........................................................................................... 25 Joint Spouses ......................................................................................... 25 Ineligible Membership ............................................................................. 25

Harland eFunds/ChexSystems ..................................................................... 26 IF HARLAND EFUNDS IS DOWN, CALL CHEXSYSTEMS (1-800-328-5120), OUR

MERCHANT CODE IS #20023105. ................................................................ 26

Membership Guidelines ................................................................................. 30

Forms of Ownership/Definitions ................................................................... 30 Minor Accounts/Parent Opening Account for Children ..................................... 30 Opening a New Membership ........................................................................ 31

Forms Required ...................................................................................... 31 Terminal Transactions ............................................................................. 31 Accounts Opened or Changed-Person Not Present ....................................... 32

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

3

Completion of Signature Cards .................................................................... 33 Forms Required ...................................................................................... 33 Procedure .............................................................................................. 33

Audit/Maintenance of Signature Cards .......................................................... 34 Guidelines.............................................................................................. 34 Forms Required ...................................................................................... 34 Audit Procedure ...................................................................................... 34

Account Changes/Change of Ownership ........................................................ 36 Guidelines.............................................................................................. 36 Name Change ........................................................................................ 36 Addition of Joint Owner ........................................................................... 36 Deletion of Joint Owner ........................................................................... 36 Payable on Death Change ........................................................................ 36

Decedents Accounts ................................................................................... 37 Forms Required ...................................................................................... 37

Decedent's - Loans and Visa ....................................................................... 39 Forms Required ...................................................................................... 39 Procedures............................................................................................. 39 Visa Accounts ......................................................................................... 39 VISA Department Responsibilities ............................................................. 40

Account Numbers\Types ............................................................................. 41 Member Account Number ......................................................................... 41 Accounts ............................................................................................... 41 Account Table ........................................................................................ 42

Social Security Representative Payee Accounts ............................................. 43 Forms Required ...................................................................................... 43 XP2 Procedures ...................................................................................... 43 Completing the Account Card ................................................................... 44

New Primary Savings Accounts.................................................................... 46 Scope.................................................................................................... 46 Joint Accounts ........................................................................................ 46 Dividends .............................................................................................. 46

Closing a Primary Savings Account .............................................................. 47 Guidelines.............................................................................................. 47 Procedure for Closing Membership ............................................................ 47

Re-Joining After Closure ............................................................................. 50 Closing an Account (Not Primary Savings) .................................................... 51

Guidelines.............................................................................................. 51 Procedure .............................................................................................. 51 Verify: ................................................................................................... 52

Christmas Club Accounts /Vacation Club ....................................................... 53 Guidelines.............................................................................................. 53 Term ..................................................................................................... 53 Dividend Rates ....................................................................................... 53 Penalties ............................................................................................... 53 Loans .................................................................................................... 53 Insurance .............................................................................................. 53 Account Numbers ................................................................................... 53 Forms Required ...................................................................................... 54 XP2 Transaction ..................................................................................... 54 Procedure to Open .................................................................................. 54

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

4

Opening a New Certificate .......................................................................... 55 Guidelines.............................................................................................. 55 Transaction ............................................................................................ 55

CD Dividend Rate Match ............................................................................. 56 Guidelines.............................................................................................. 56

Bump Up Certificates ................................................................................. 57 Guidelines.............................................................................................. 57 Procedure to Increase Dividend Rate ......................................................... 57

Dividend Calculations ................................................................................. 58 How to Compute Dividends on Certificates ................................................. 58

Traditional Individual Retirement Plan (IRA) ................................................. 59 Overview/General Information ................................................................. 59 Contributions ......................................................................................... 59 Distributions .......................................................................................... 60

Roth Individual Retirement Plan (IRA) .......................................................... 61 Overview/General Information ................................................................. 61 Contributions ......................................................................................... 61 Distributions .......................................................................................... 62

Coverdell ESA (Education Savings Account) .................................................. 63 Overview ............................................................................................... 63 Contributions ......................................................................................... 63 Distributions .......................................................................................... 63

IRA Share Account..................................................................................... 64 Forms Required ...................................................................................... 64 XP2 Transaction ..................................................................................... 64 Procedures............................................................................................. 64

IRA Plan-To-Plan Transfers ......................................................................... 65 Guidelines.............................................................................................. 65 Custodian/Trustee to Custodian/Trustee .................................................... 65 Distribution and Redeposit (Rollover) ........................................................ 65 Forms Required ...................................................................................... 65

IRA Rollovers ............................................................................................ 67 Guidelines.............................................................................................. 67 Form ..................................................................................................... 67 Procedure .............................................................................................. 68 Rollover (In) .......................................................................................... 68 Rollover (Out) ........................................................................................ 68

New Checking Accounts.............................................................................. 69 Guidelines.............................................................................................. 69 Forms Required ...................................................................................... 69 Procedure .............................................................................................. 70

Debit Cards for Minors ............................................................................... 71 Guidelines.............................................................................................. 71

Segue Student Checking Account ................................................................ 72 Eligibility ............................................................................................... 72 Procedure .............................................................................................. 72

Money Market Accounts .............................................................................. 74 Guidelines.............................................................................................. 74 Forms Required ...................................................................................... 74 Procedure .............................................................................................. 75

Overdraft Protection .................................................................................. 76

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

5

Guidelines.............................................................................................. 76 Courtesy Pay Policy ................................................................................... 77

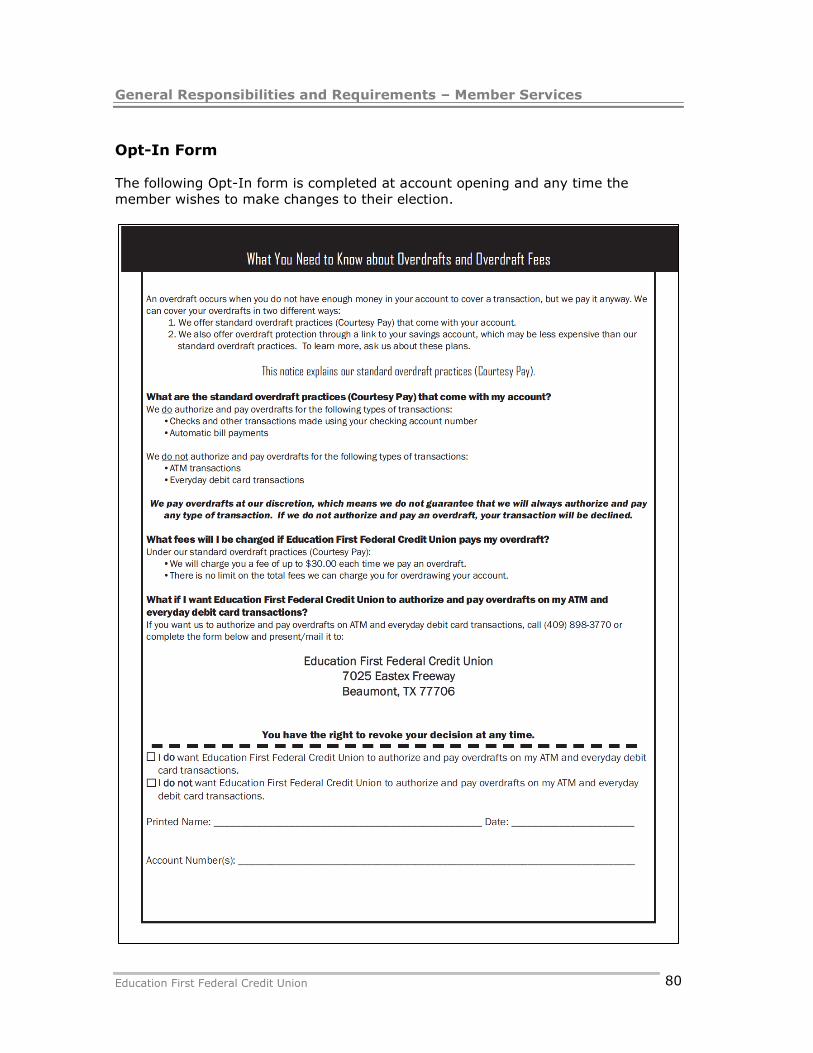

New Account Procedures ......................................................................... 77 Courtesy Pay Limit Suspension ................................................................. 79 Ineligible or Member Declined Accounts ..................................................... 79 Re-Opening Closed Accounts .................................................................... 79 Opt-In Form ........................................................................................... 80 Opt-In Maintenance ................................................................................ 81

Overdrawn Accounts/Accounts Showing Abuse .............................................. 82 Guidelines.............................................................................................. 82

Accepting & Processing Check Orders ........................................................... 83 Guidelines.............................................................................................. 83 Operation Begins .................................................................................... 83 Procedures............................................................................................. 83 Member File Information ......................................................................... 84

Check Printing Errors ................................................................................. 85 Guidelines.............................................................................................. 85 Procedure .............................................................................................. 85

Check Order Billing Errors........................................................................... 86 Guidelines.............................................................................................. 86 Procedures............................................................................................. 86

Check Orders Lost In the Mail ..................................................................... 87 Guidelines.............................................................................................. 87

Shredding Checks ...................................................................................... 88 Guidelines.............................................................................................. 88 Log Required .......................................................................................... 88 Procedure .............................................................................................. 88

Temporary Checks ..................................................................................... 89 Guidelines.............................................................................................. 89 Procedure .............................................................................................. 89 Printing Temporary Checks ...................................................................... 89

Checking Account Statements ..................................................................... 92 Notification of Errors/Questions On Monthly Statements .............................. 92 Member Responsibilities .......................................................................... 92 Credit Union Responsibilities .................................................................... 92

Checking Account Dividends ....................................................................... 94 Formula for Calculating Dividend (Example) ............................................... 94

Verification of Check Funds ......................................................................... 95 Guidelines.............................................................................................. 95

Stop Payments & Unauthorized or Authorization Revoked ACH Debits ............. 96 Guidelines.............................................................................................. 96 Forms Required ...................................................................................... 96 XP2 Transaction for Checks ...................................................................... 96 XP2 Transaction for ACH .......................................................................... 96

Check Copy Requests ................................................................................. 99 Guidelines.............................................................................................. 99 Member Services Platform Transaction ...................................................... 99 Procedure .............................................................................................. 99 Procedures for share drafts cashed at the Credit Union. ............................. 100 Total eReceipts ..................................................................................... 100 Nautilus ............................................................................................... 100

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

6

Check Encoding Errors ............................................................................. 101 Procedure ............................................................................................ 101

Check Paid Twice on Account .................................................................... 102 Procedure ............................................................................................ 102

ATM Disputes .......................................................................................... 103 Guidelines............................................................................................ 103 Forms Required .................................................................................... 103 Procedure if Machine Error ..................................................................... 103 Procedure if Fraud/Theft ........................................................................ 103

Power of Attorney (POA) .......................................................................... 104 Forms Required .................................................................................... 104 Policies ................................................................................................ 104 Procedures........................................................................................... 105

Forgery of Maker's Signature (Drafts) ........................................................ 106 Guidelines............................................................................................ 106 Forms Required .................................................................................... 106 Procedure ............................................................................................ 106 Proceed as follows: ............................................................................... 107

Forgery of Endorsement (Draft) ................................................................ 108 Guidelines............................................................................................ 108 Forms Required .................................................................................... 108 Procedures........................................................................................... 108

VISA Card Disputes ................................................................................. 110 Guidelines............................................................................................ 110 Forms Required: ................................................................................... 110 Fraud: ................................................................................................. 111

VISA Check Card – Debit .......................................................................... 111 Forms Required: ................................................................................... 111

VISA - Out of Town Notices ...................................................................... 112 Procedures: ......................................................................................... 112

WireXchange .......................................................................................... 113 Guidelines............................................................................................ 113 Information Gathered ............................................................................ 113 Entering a Wire .................................................................................... 113 Verifying a Wire .................................................................................... 116 Release an Outgoing Wire ...................................................................... 117

Western Union Wires ............................................................................... 118 Western Union & Wire Xchange Stopped .................................................... 119

Forms Required .................................................................................... 119 Procedure ............................................................................................ 119

Direct Deposit Authorizations/Miscellaneous................................................ 120 Guidelines............................................................................................ 120 Forms ................................................................................................. 120 Procedure ............................................................................................ 120

Payroll Allocations ................................................................................... 121 Guidelines............................................................................................ 121 Forms Required .................................................................................... 121 XP2 Transaction ................................................................................... 121 Procedure ............................................................................................ 122

Automatic Transfers ................................................................................. 123 Guidelines............................................................................................ 123

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

7

Forms Required .................................................................................... 123 Operation Begins .................................................................................. 123

Safe Deposit Boxes .................................................................................. 124 TTT - Cross Member Transfer Enrollment .................................................... 125

Forms Required .................................................................................... 125 XP2 Transaction ................................................................................... 125 Procedure ............................................................................................ 125

Request for Payoff on Loan ....................................................................... 126 Forms Required .................................................................................... 126 Procedure ............................................................................................ 126

Skip-a-Payment/Extension ....................................................................... 127 Forms Required .................................................................................... 128 Procedure ............................................................................................ 128

How to Re-Amortize a Loan ...................................................................... 129 Sending Documents with EchoSign (Adobe Sign) ......................................... 130

Procedure ............................................................................................ 130

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

8

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

9

Section 1: General Member Service Requirements

Member Services Responsibilities

The Member Services Department provides and processes a wide range of services for

members and provides support to the branch system. These include:

− Maintain the integrity of all members’ records in a confidential manner.

− Open new accounts for Savings, Checking, IRAs, Money Market, and

Certificates.

− Cross-sell additional services to provide the member with a complete package

to meet their financial needs.

− Order checks.

− Review and research member problems and adjust accounts as required.

− Process stop-payment orders.

− Retrieve copies of paid checks and statements at member's request.

− Process wire transfer request.

− Issue debit cards.

− Help with Online Banking.

Profile

The following list provides a profile of services offered to members by the Member

Services Department:

− Orient members to the credit union as their full-service financial institution

and inform them of the multiple benefits of doing business with the credit

union.

− Open all types of new accounts.

− Inform members of our low interest loans.

− Provide quality service to members.

Favorable Service Techniques

First impressions are long lasting. Therefore, all credit union personnel must:

− Assist the members in a professional and courteous manner, commencing with

the first initial contact; and

− Follow through to help the member feel assured that the "right" financial

institution has been chosen, and

− Provide confidence that the credit union offers the products and services that

meet their needs either now, or in the future.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

10

Initial Contact/Greeting the member

The following is a list of suggestions, which are beneficial when establishing a positive

and productive rapport with the member.

− Stand up, when possible.

− Establish eye contact.

− Smile.

− Introduce yourself.

− Ask if you can help. Listen to the member before assuming what service is

needed.

If the member wishes to open an account, thank them for choosing EFFCU.

Make the member feel at home (small courtesies make the difference-offer a seat).

Cut Off All Other Work Interruptions

Try to arrange for someone to back you up when you are opening an account. If you

are interrupted, don't forget, the member is still the most important person; excuse

yourself and make the interruption as short as possible.

Use member's name as often as possible. Remember that 75% of face-to-face

communication is non-verbal (i.e. gestures, posture, appearance, tone, etc.).

− Maintain a neat, orderly well-organized desk, giving the member ample room

to complete and/or sign the appropriate documents.

Interview

− Tactfully find out why the member is there. Be a good listener.

− Example: “Is this your FIRST account at a credit union”? Perhaps this

member is new to the community and the credit union; in which case, several

services may be needed.

− Perhaps this member was unhappy with a credit union and is moving the

account. If so, find out what went wrong and try to avoid making the mistake

yourself.

− Perhaps this member already has an account with EFFCU and is opening an

additional account.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

11

Products and Services

157BSavings/Checking Products

Regular Savings

Prime Reward (no longer offering)

Christmas Club

Vacation Club

Checking

Segue Student Checking

Money Market

Traditional IRA

Roth IRA

Educational IRA

Certificates 158B

159BAdditional Services

Direct Deposits (Automated Clearing House - ACH)

Payroll Allocations

Automatic Transfers

Online Banking

Touch Tone Teller

Check Orders

Stop Payments

Notary Services

Signature Guarantee

Automated Teller Machine Service (ATM's)

Wire Transfers (Bank to Bank and Western Union)

Visa Gift Cards

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

12

Fee Schedule

Account Fees

Overdraft Transfer Fee $5.00 per transfer

Non-Sufficient Funds – “NSF Fee” $30.00 per item

Paid by overdraft fee $30.00 per item

Return Item Fee $5.00 per item

Stop Payment Fee $30.00 per item (check or pre-authorized electronic debit)

Check Printing Fee Prices vary depending on style

Temporary Checks $3.00 per page (12)

Returned item drawn on Members’ account at

another institution (NSF) Fee

$30.00 per item

Inactive Account Fee

$5 per month, if no activity for 12 months, and/or balance under $100 and no other services

Other Service Fees

Account Research/Reconciliation Fee $15.00 per hour

Statement Copy Fee (includes account print out) $3.00 per statement

Returned Statement/Mail Fee $5.00 per statement/mail

Deposited Item Return Fee $5.00 per item

Wire Transfer Fee $15.00 per item

Cashier’s Check Fee $5.00

Money Order Fee $2.00 each

Legal Process Fee $25.00 per service

Telephone Transfer Fee* $1.00 per transfer

Copy of Paid Check Fee $2.00 per check

Plastic Card Replacement Fee $10.00 per card

ATM Transaction Fee $1.00 per transaction (excludes CU PASS Network ATMs)

Account Balance Inquiry $1.00 per inquiry

Check Cashing Fee $5.00 per check (excludes Active Checking Account or Current Loans)

Dormant Account Fee $25 per account

Inactive Account Fee

$5 per month, no activity for 12 months, under $100, and no other services

Collection Items $15.00 per item

Photocopy Service* $.50 per page

Administrative Fee (closure of primary savings within 180 days of opening) $15.00

ACH/Card Origination Payments

No charge online; $5 over the phone ACH/Debit card; $10 over the phone credit card

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

13

Safe Deposit Box Fees

Box Sizes: Annual Fee:

3 X 5 $20.00

5 X 5 $25.00

3 X 10 $25.00

5 X 10 $40.00

10 X 10 $60.00

Key Deposit $10.00

Key Replacement $55.00

Drilling Fee $100.00

Bill Pay Fees

Account to Account – to another institution $2.95

Same Day Bill Payment $9.95

Overnight check – check sent overnight $14.95

Pop Money:

Send Money Fee: $1.00 - $249.00 $0.50

$250.00 - $999.00 $0.75

$1,000.00 and above $1.50

Request Money Fee: $1.00 - $249.00 $0.50

$250.00 - $999.00 $0.75

$1,000.00 and above $1.50

Stop Payment $20

e-Greetings $0.25

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

14

Section 2: Regulations

Office of Foreign Assets Control Policy

The Office of Foreign Asset Control of the Department of the Treasury administers and

oversees a series of laws that impose economic sanctions against hostile targets to

further U.S. foreign policy and national security objectives. OFAC is responsible for

promulgating, developing, and administering the sanctions for the Treasury. NCUA is

responsible for determining that credit unions comply with OFAC regulations. OFAC

laws and regulations promote national and international security by requiring asset

freezing of; oppressive governments, international terrorists, narcotic traffickers, and

other specially designated persons.

Note: If additional OFAC information is needed, contact your supervisor and/or

compliance for further instruction.

Member Service Representatives

1 Upon opening a new account with Education First Federal Credit Union all

names of the potential member, joint owners and payable on death

beneficiaries are checked against the OFAC database using Verafin.

2 Each transaction that involves a person or entity that is not a current

member is individually checked against OFAC SDN list. This includes wires

sent to non-members as well.

What to do with the Verafin information provided

If there is a match anywhere from 90% - 100% compliance must be contacted to

determine how to proceed with the transaction. E-mail

[email protected] or call Rachel Gilmore or Amanda Lowe.

Beginning at the Home page

1 Click Internet Links

2 Click Verafin

3 Sign in

4 Enter individuals name and address. If available use social security number

as well.

5 Click Search (see screen shots on next page)

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

15

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

16

Securities Transfer Agents Medallion Program – (STAMP)

Purpose

The Securities Transfer Agents Medallion Program is a signature guarantee program

endorsed by the Securities Transfer Association (STA) and recognized by securities

industry participants in the US and Canada.

For over one hundred years, Issuers of Securities and Transfer Agents have relied upon

the signature guarantee process for the transfer of securities. This process, codified in

the Uniform Commercial Code (UCC), makes the Transfer Agent liable for improper

securities registration. To register or re-register a security, the Transfer Agent or Issuer

relies upon the warranties made by a Medallion Guarantor when placing a Medallion

Guarantee Stamp on a security, namely, that the signature is genuine, the signer is an

appropriate person to endorse, and the signer had the legal capacity to sign.

Education First Federal Credit Union provides signature guarantees as a service to

members or joint owners (only).

The Credit Union guarantees to the issuer of the securities or its transfer agent that the

registered owner’s signature, or that of an agent authorized to act for the owner on the

security or transfer form, is genuine.

Procedures

The member must sign the security in front of a Credit Union employee authorized to

provide signature guarantees. The employee must witness the actual signing. Valid

identification is required such as:

− Driver’s License

− Identification Card

− Military Identification or

− Passport

Signature guarantee logs and stamp are kept in the vault at the Rosedale and Lamar

offices. At the Administration office, the log and stamp are kept in a locked area.

Note: If authorized staff is not available to perform this service for the member at the

Rosedale or Lamar Branches, we can find the appropriate person in the Administration

Office for the member.

Authorized Signers

The authorized signers are as follows:

Christine Sliva, Gilesha Serf (Admin)

Joanna Alfaro, Laura Landry (Laurel)

Carrie Hulsey (Lamar)

Aisha Diop, Cristal Godina (Rosedale)

Jared Mason (Jasper)

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

17

163BBond Coverage

Education First Federal Credit Union is required to carry bond coverage for losses

resulting from guaranteeing a signature to sell, transfer, surrender, or exchange

securities. Bond is up to $500,000.00.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

18

Customer Identification Policy (CIP)

Education First Federal Credit Union has adopted this policy to comply with the

requirements of the USA Patriot Act and its implementing regulations to establish the

identity of individuals and entities opening accounts at the credit union.

Education First Federal Credit Union’s Member and Customer Identification Program

(CIP) consist of this board approved policy as well as procedures established by

management that at a minimum include:

− Verifying the identity of any member or customer seeking to open an account.

− Maintaining records of the information used to verify identity, using either un-

expired government-issued documents or non-documentary verification

methods; and

− Determining whether the customer appears on any government list provided

to the credit union by federal agencies, when these federal lists are issued.

In formulating and maintaining appropriate procedures, management will take into

consideration the types of accounts offered, the method of establishing accounts, and

the credit union’s field of membership to determine what level of risk the credit union

feels it has in opening accounts. Procedures will establish what documents and non-

documentary information are to be relied upon to verify identity.

For purposes of CIP, accounts include all formal account relationships established,

whether established as share, share draft, certificate, or other savings account, as well

as loan account relationships. New members and customers establishing any type of

account on or after October 1, 2003 will be subject to CIP procedures.

The term customer includes non-member joint owners, non-member co-borrowers or

any other individual or entity (business, corporation, trust, partnership) establishing a

formal account relationship with Education First Federal Credit Union who will not be a

member.

Prior to opening any account every new member or customer is required to provide a:

− Name,

− Date of birth,

− Address, and

− Identification number

The Credit Union will maintain this information for five years after the account is closed.

Reasonable steps will be taken to verify this information through documentary or non-

documentary verification methods as required by the Treasury Department’s CIP

regulations. The verification methods accepted are specified in Education First Federal

Credit Union’s CIP procedures, and the description of documents reviewed and the

verification method used will be maintained for five years after the description is

recorded.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

19

Additional verification will be required for individuals whose true identity cannot be

verified using the standard verification methods. An account will not be opened if

verification of an individual’s identity cannot be verified.

The Bank Secrecy Act officer is responsible for maintaining ongoing compliance with the

PATRIOT Act requirements and its implementing regulation. Appropriate staff will be

adequately trained on BSA and CIP requirements.

An annual audit of CIP compliance will be conducted by the credit union’s internal

auditor.

Before opening an account, potential members and new customers will be advised of

the credit union’s CIP program through the appropriate notice as specified in the

implementing procedures.

Education First Federal Credit Union believes that it has a reasonable basis to assume

that members and customers of record as of October 1, 2003 are known to the credit

union. If events occur that raise questions as to whether the credit union knows the

true identity of a person, the credit union will seek to verify the person’s identity, as

called for in the CIP procedures.

CIP Procedures

This program is designed to assure Education First Federal Credit Union’s compliance

with the USA Patriot Act and the implementing regulatory requirements of the U.S.

Treasury Department and the National Credit Union Administration to assist in

preventing and tracking money laundering and terrorism financing activities. These

procedures implement the policy adopted by Education First Federal Credit Union’s

board of directors. The credit union will take reasonable and practical steps to verify

the identity of people who open accounts with the credit union.

Coverage

These CIP procedures will apply after October 1, 2003 to anyone establishing a formal

relationship with Education First Federal Credit Union to provide services, or engage in

other financial transactions that include share, share draft, certificate, or other accounts,

as well as loan account relationships.

The term customer as used in this program refers to anyone establishing an account

relationship with Education First Federal Credit Union, including members, non-member

joint owners, non-member co-borrowers or any other individual or entity (business,

corporation, trust, partnership) establishing a formal account relationship with the credit

union.

The term customer also refers to the individual who opens an account for a minor lacking

legal capacity or for an entity that is not a legal person, such as an office bowling league,

the annual picnic fund, etc.

If events occur that raise questions about the true identity of an existing member or

customer, the credit union will follow these procedures to verify that person’s identity.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

20

Collection of Information from Individuals

Information Required

Education First Federal Credit Union requires the following information to be provided

by each individual member or customer before opening an account with the credit union:

− Name

− Residential or business street address, plus a mailing address if different than

the residential or business street address

− Army Post Office (APO) or Fleet Post Office (FPO) box number for members of

the military; residential or business street address of relative or another

contact individual

− Date of birth

− Identification number, which will be a Social Security number for U.S. citizens.

For non-U.S. persons, a W-8Ben form is required (using #000-00-0004) or a

Social Security/tax identification number; passport number and country of

issuance; alien identification card number.

Verification of the Identity of Individuals

Accounts Opened in Person

Education First Federal Credit Union verifies the identity of a new member or a customer

appearing at the credit union by examining the following unexpired documents that look

authentic. Two forms of ID are required when opening accounts. One of which must be

from the primary list; the second form can be from either list:

Primary Identification Secondary Identification − Driver’s licenses - Social Security card

− Passports - Student ID card

− State identification card or - Employer Photo badge

− US Government identification - National or local credit or debit card

− Texas Concealed Handgun License - Birth certificate

When opening a new membership, if the person’s address on the ID is incorrect it is

okay to obtain the new address from the member. The member is not required to

bring in proof of their new address before the account is opened.

Identification number, place of issuance and Identification used will be recorded on the

signature card and scanned into XP2 Images.

If the document presented for purposes of identification is not one the staff is familiar

with, it is brought to their immediate supervisor for review and/or approval.

In addition to documents, we will use other methods to verify identity such as reports

from ChexSystems through Harland eFunds. If a situation arises where staff has a

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

21

concern about being able to verify the identity of the person, the Member Support

Center Manager, Branch Manager, Assistant Branch Manager, Executive Vice President

or President is to be notified for advice on how to handle the situation.

Application for TIN Is In Process

Education First Federal Credit Union will not open an account for an individual awaiting

a Social Security number/individual taxpayer identification number (ITIN).

Joint Account Holders of Credit Cards

The Credit Union will obtain information from Experian Credit Reporting Agency about

any joint account holder on a credit card account who is not currently a member of

EFFCU before extending credit to the non-member joint accountholder.

Person Not Present (New and Existing Member)

An account opened by mail, internet, in-direct lending or payroll deduction requires the

following:

− Name

− Social security or tax identification number

− Physical address

− Date of birth

− Eligibility; and

− Copy of acceptable photo identification.

EFFCU verifies the identity of a new member or a customer who remotely opens an

account at the credit union by the following non-documentary methods. Methods used

in all cases:

− Name

− Physical address

− Social security/tax identification number

− Date of birth, and

− Copy of acceptable photo identification

Other acceptable steps the credit union may take to verify identity may include:

− Use of a verification service

− Use employment information or

− Use a student identification card

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

22

Accounts Opened Prior To Verification

Education First Federal Credit Union does not open any accounts before the verification

procedure is completed.

Discrepancies with Information Provided

The credit union seeks to resolve any substantive discrepancies discovered when

verifying the identifying information obtained from a person, and will record the

description and results of any measures used to resolve those discrepancies176B

Record Retention

Information Collected

Information required from the individual and business accountholders (name, date of

birth, address, identification number and any other information collected under these

procedures) is retained for five years after the account is closed. The information is

retained on the Account Card, Account Authorization Card and in our computer system.

If requested by a federal government agency, the information will be retrieved by our

Research Department.

Verification Descriptions

Records on the descriptions of any document (including type of documents,

identification number, place of issuance and, if any, date of issuance and expiration),

descriptions of non-documentary methods used, and descriptions of any resolution of

substantive discrepancies found when verifying an identity will be retained for five years

after the account is opened.

This information will be retained on the membership application, account change card

and in our data processing system. If requested by a federal government agency the

information will be retrieved by our Research Department.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

23

Checking Government Lists [Reserved: yet to be announced by Treasury]

Procedures need to be developed once the Treasury Department issues any information

on any designated CIP lists, which are in addition to the credit union’s current

responsibilities for checking names against the OFAC lists and the FinCEN requests.

CIP Notice

New members and customers will be notified about the credit union’s CIP policy by:

lobby notice, notice posted:

− On the website

− Orally, and

− On the account agreement.

Annual Audit

Education First Federal Credit Union has an annual audit conducted by its internal

auditor to determine whether the requirements of the customer identification program

are being met.

Training

The credit union’s service staffs, Tellers, Member Service, Lending Service and Member

Support Center Representatives, are required to participate in regular Bank Secrecy Act

training, including customer identification program requirements and procedures. The

lending staff’s responsibilities for non-member/co-borrowers is to make sure that

person’s identify is established before a loan is granted. Evidence of participation will

be retained for audit purposes.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

24

Verifying Member’s Identity by Phone

Guidelines

Members make several requests by phone. All information, concerning the member's

account, must be handled in a confidential manner. It is imperative members are

properly identified via telephone. Since the member cannot be seen, rely on your

listening skills to help pick up any indication of fraud.

Operation Begins

When phone call is received.

Member Services Platform Transaction

Access Membership Summary page

Procedure

1. Obtain the following information from the caller when verifying identity:

a. Member number and the name of the individual

b. Current address and phone number

c. Social Security Number

d. Date of Birth

e. Driver’s License Number

f. Last known deposit or transaction

g. Current loan(s) with the credit union

h. Name(s) of additional signers on the account

i. For those with access to home banking reset, you may log in and ask

up to 3 of the challenge/response questions available

2. A and b are required. Any combination of c through i must be verified to

continue with the request. Change it up; do not always ask the same for

each phone call.

3. If the caller cannot give this information, do not go any further.

4. If fraud is suspected, place a detailed contact on the account and contact a

manager. (See contact management procedures)

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

25

Membership Eligibility Verification

Anyone who lives, works, worships or attends school in the six county areas of Jefferson,

Orange, Hardin, Newton, Jasper and Tyler can join Education First FCU, along with the

employees and retirees of the East Chambers and High Island Independent School

Districts.

A family member(s) of any EFFCU member (i.e., spouse, children, parents, brothers,

sisters, grandparents and grandchildren) is eligible for membership.

Underserved Area

The reference to “the underserved area” includes the ENTIRE county. This allows ANY

person within the six counties to become a member of Education First FCU.

Sponsorship

A sponsorship letter of introduction is required under most circumstances from the

individual sponsoring their immediate family member.

If the sponsor is present there is no letter required.

If family members can be positively identified, there will be no letter needed.

If the family member who wishes to join can give you the primary owner’s

present address and date of birth this would be sufficient for identification,

therefore not requiring a sponsor letter.

If there is a doubt about family membership or marriage then a birth certificate

or marriage license may be required.

Joint Spouses

A spouse who is currently a joint owner on an account may open another account under

that primary number.

The joint owner may obtain signature cards that have been typed with all the

information to take to the primary owner and return.

When these cards are returned to the credit union, all signatures are verified.

Ineligible Membership

If it is found at any time after the account is opened that someone was not actually

eligible for membership, the account may be closed immediately. An explanation letter

is sent to the individual accompanied by a check for the total of funds in the account.

When the account is closed the address is placed on hold to prevent a statement from

being processed on that account. See XP2 Address Procedures.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

26

Harland eFunds/ChexSystems

Potential members must pass the Harland eFunds check, which pulls ChexSystems

history, to join the credit union. All signing owners on an account must pass the

ChexSystems risk assessment.

Depending on the information reported, you may grant or deny the opening of the

membership. If you deny membership, print/give an Adverse Action letter. If you are

unsure whether or not to approve the membership, get with an available supervisor. If

the member wants to verify or refute a debt, they need to contact the reporting agency.

If the debt is paid, the member is allowed to provide proof of payment.

IF HARLAND EFUNDS IS DOWN, CALL CHEXSYSTEMS (1-800-328-5120), OUR MERCHANT CODE IS #20023105.

If ChexSystems is “recommending decline” get with a supervisor to interpret the codes.

Depending on what is being reported, we may need to decline membership.

If the member already has a savings account established, go to the Individual Level,

Custom Data screen and choose “ChexSystems Declined” in the Declined Checking

Reason field. Add a contact to the account under the category Product Notes as to

why we declined the checking account.

ChexSystems also checks:

Social Security Number Validity – SSN Validation Message could be:

- Impossible Number

- Invalid Number – Not yet issued

- Number Inactivated Due To Report of Death

-

A “Please Call” response is generated when a consumer has issued a written statement

to ChexSystems disputing or clarifying information on their consumer record. Call

immediately to receive the additional information about the potential member’s

situation.

Decline Recommendations are based on:

- Fraud closure reported on the consumer within the last five years.

- Abuse closures reported on the consumer within the last five years.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

27

Review Conditions will exist due to:

- Consumer ID Theft Alert – The consumer has requested an Identity Theft Alert

be placed at ChexSystems.

- Consumer Security Freeze Alert – The consumer has placed a freeze on their

consumer report.

- Driver’s License Information – The driver’s license format review rule evaluates

the alphanumeric combination of the driver’s license, State ID, and Military ID

number for all 50 states, U.S. Territories and Military Bases. It does not verify

the validity of the number.

- Warm Address – Examples of warm addresses include hotels, penitentiaries,

mailbox drop sites, etc.

- Invalid Telephone Number – The input telephone number is invalid when the

exchange/prefix is not found in that area code. This rule does not evaluate

whether or not the actual telephone number has been issued.

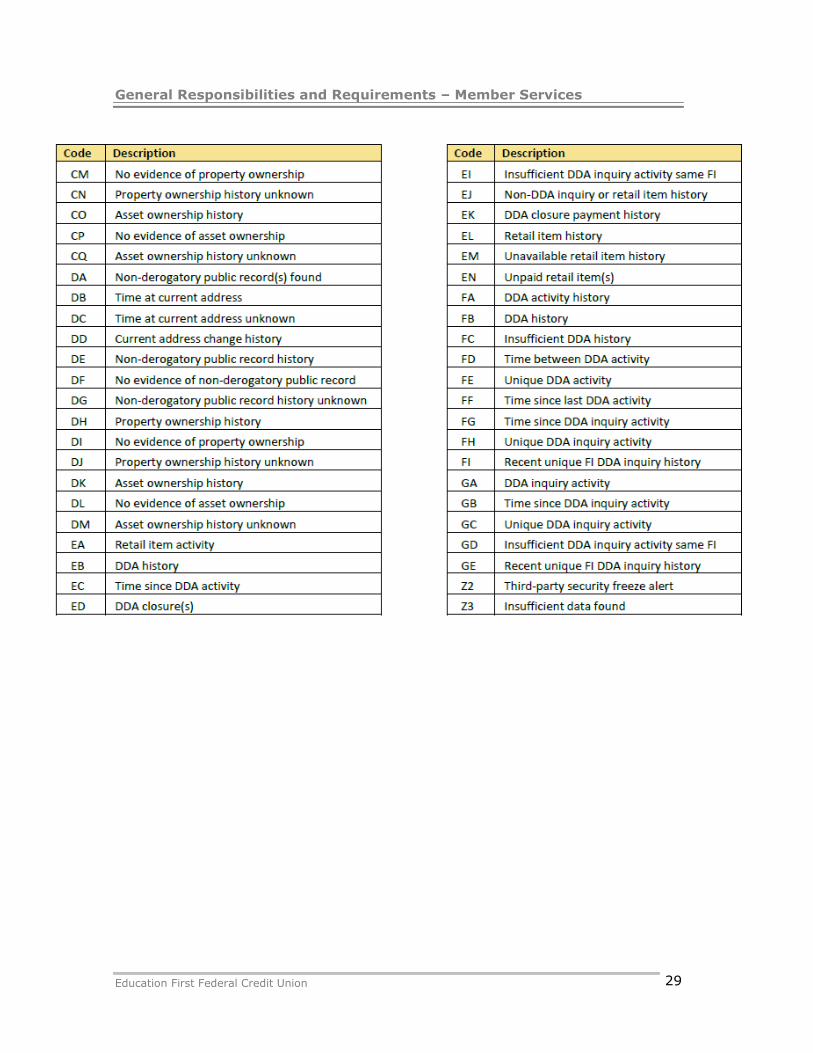

See Detailed Reason Codes on next two pages.

*DDA = Demand Deposit Account

*FI – Financial Institution

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

28

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

29

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

30

Membership Guidelines

Forms of Ownership/Definitions

The following information defines the various forms of account ownership available:

Individual Ownership Single and complete control of funds

Joint Ownership Two or more persons sharing equal ownership of the

funds on deposit, regardless of their net contribution, with a possible right of survivorship. The first named on the account is the primary member.

Individual Retirement Accounts

EFFCU acts as trustee for a member who owns an IRA. IRA is specific to the primary member account.

Social Security Rep. Payee Accounts

The primary member on the account is the beneficiary of funds with a designated representative payee controlling those funds on the beneficiary’s behalf—designated by the Social Security

Administration. The rep. payee does not own the account but manages it on the beneficiary’s behalf.

Minor Accounts/Parent Opening Account for Children

A parent may open an account for their children without them being present as long as

the child’s social security number is listed on that account and they are under the age

of 18.

If they are 16 or 17 years, the parent will be required to take the signature cards to

the child for their signature before the account can be opened.

Identification is not mandatory for children not signing on the account.

If the child is young and the parent signs for them, the child is not able to withdraw

from the account. When the child is old enough to sign on his/her own, the signature

card can be updated and driver’s license or state ID will need to be verified.

A parent is required as joint owner on an account until the child reaches the age of 18.

The CIP policy will apply for anyone 18 years of age or older.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

31

Opening a New Membership

Forms Required

Valid photo identification card along with secondary ID

Account Card

Membership and Account Agreement

Truth-in-Savings Disclosure and Agreement

Schedule of Rates & Fee Service Charges

Transaction Receipt

Terminal Transactions

Verify with OFAC (Verafin)

Verify with Harland eFund

XP2 Enroll Member or Lending 360 New Membership

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

32

Accounts Opened or Changed-Person Not Present

Note: On an existing membership, do not make any changes to the account in XP2

until account documents reflecting those changes have been received.

If the member is not able to open a new membership or make changes to an

existing membership in person:

1 Membership eligibility will be verified in the same manner as if the member

had enrolled by coming into the building. (See Collection of Information

from Individuals: Person Not Present.)

2 Before the account is established, send required disclosures via email, fax,

or mail—dependent on the member’s preferences.

3 The Account Card and Account Change Card require “wet” signatures

meaning the member must physically sign the documents if they are being

sent (via email, fax, or mail) for signing and send them back to the credit

union (via email, fax, or mail) for signature verification and to complete

account opening/changes. We must receive signed documents and

opening deposit within 30 days of paperwork being sent.

a. Create documents in L360 or IMM (depending on the membership

type) and save the documents to your computer.

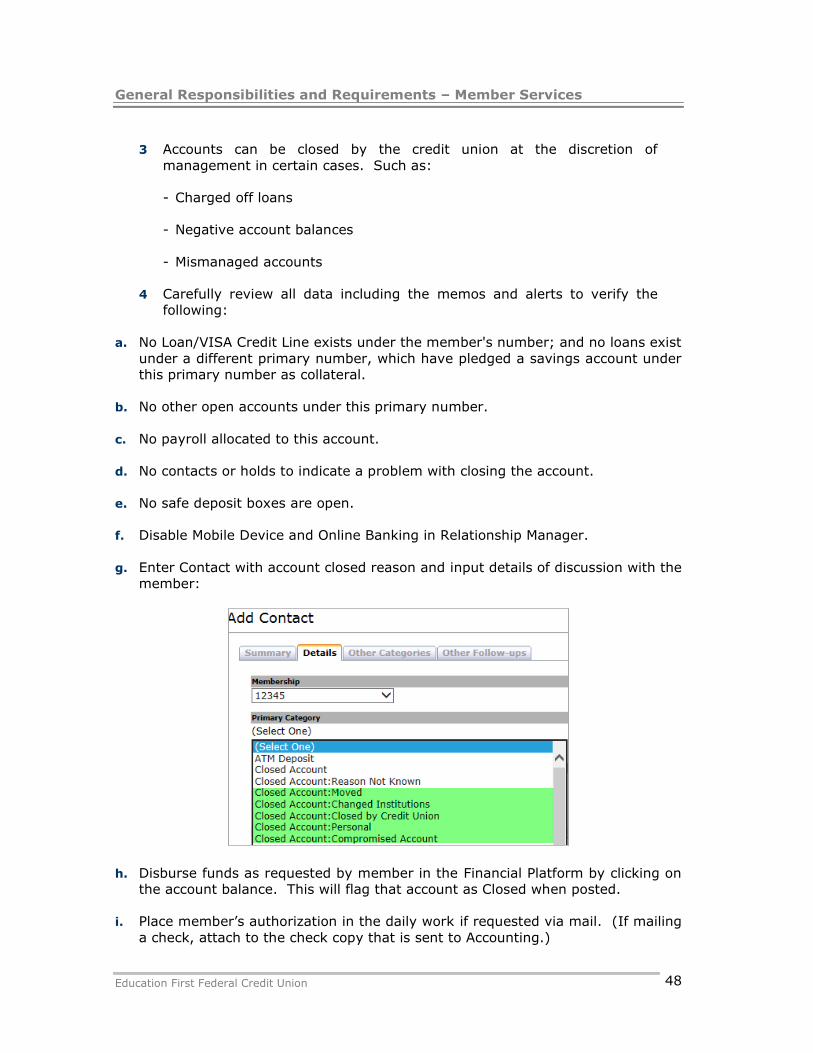

b. For New Membership: Add the red alert “No activity allowed see

membership services” to the account as well as a Contact

explaining the reason and how best to reach the member.

c. Send documents to the member via EchoSign. The member will

print, sign, and return them. (See EchoSign instructions.) After

each follow up, add a Contact to the account explaining the

interaction with the member.

1. Follow up with the member that documents have been received

immediately after sending. Offer to assist them in completing

the forms either over the phone or with a video chat. (Video

chat only if your schedule allows it.)

2. Follow up after 3 days if documents have not been returned—

answer questions/offer assistance.

3. Follow up after 10 days if documents have not been returned.

4. Mail Account Opening/Account Change Termination Letter

(found on the Intranet: Quick Links: Policies & Forms) to the

member if documents have not been received in 30 days.

4 After the account has been established, send a welcome letter, receipt,

member account identification card, and any other documents pertinent to

the membership via email, fax, or mail—dependent on the member’s

preferences.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

33

Completion of Signature Cards

The Account Card Form is a multi-purpose signature form and application/agreement

that serves to identify members by their signature. They agree to the terms and

conditions set by the credit union for the account. A Line Card, for quick signature

verification, is also completed and scanned into XP2 images. An Account Card form

must be on file for every account opened.

The Account Card Form is used for two purposes:

− To open all account types requested by the members.

− To update account type/ownership as requested by the members.

Forms Required

Account Card or Account Change Card

Line Card

Procedure

Review all signature forms for completeness and legibility. The following data must be

verified:

1 Primary owner's information completed and signed in the appropriate

spaces. Appropriate Social Security number or primary identification

number must be provided.

2 Harland E-fund verification numbers are recorded on the signature form to

indicate CIP is followed.

Note: If a credit card is used as secondary ID, do not record or copy any credit

card numbers. Record credit card type only. (i.e. VISA, MASTERCARD…)

3 The joint owner's section is completed, including: Social Security number,

date of birth, signature and valid identification.

4 If the member does not have a Social Security number, a W-8 Certificate

is completed and signed.

5 If the member selects Payable on Death Beneficiary (under Account

Ownership Information), the relationship information is provided on the

P.O.D Beneficiaries section. Enter name and identifying information (see

example). OFAC search must be run on beneficiary.

Example: Daughter DOB 12-31-1942 or Fiancé SS 123-45-6789

6 Verify that the data base system reflects accordingly, date and initial card.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

34

Audit/Maintenance of Signature Cards

Guidelines

For each new account opened, the appropriate signature form must be completed with

the correct date.

− Completed forms are to be imaged and maintained at the Administrative Office

on the Nautilus System.

− A line card for quick signature verification is also completed. (Refer to the

previous section "Completion of Signature Cards.")

− Review of signature forms for new accounts may be delegated by the Branch

Manager but are the primary focus of the Quality Assurance department.

− The designated supervisors will review new account reports daily and ensure

that associated signature forms are completed.

− The Branch Manager will communicate daily to ensure that all forms are

checked for accuracy and that the Customer Identification Policy is faithfully

followed.

− In the event a signature form is incomplete or missing, it will be held in the

pending file until a properly completed form is received. The member has 30

days to submit a completed signature form.

Forms Required

Account Card or Account Change Card

Line Card

Audit Procedure

1 Compare all personal information on the Account Card/Account Change

Card to XP2.

2 Compare all new accounts forms to the Savings Report/RPT301B-New

Accounts in Nautilus. This report is produced daily and is printed by

Assistant Branch Manager and/or the Branch Manager.

3 Verify completion of the member’s signature and withholding option under

the IRS Code 3406 (a) (1) (c). With one signature, the member agrees to

the membership, account agreement and indicates withholding status. If

the form is incomplete or missing, a corrected form is sent out allowing

the member 30 days to respond. After 20 days a reminder letter is sent

out. The account will be closed if a signed signature card is not received

after 30 days.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

35

4 Insure that the Customer Identification Program (CIP) has been followed

faithfully.

5 A pending file is created for Account Cards/Account Change Cards with

errors until a corrected form is received. The pending file is reviewed daily

by the Branch Manager to ensure all forms are completed and returned in

a timely fashion.

6 All signature cards are either archived in Nautilus or are sent to Quality

Assurance and imaged on the Nautilus System.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

36

Account Changes/Change of Ownership

Guidelines

For all types of ownership changes it is necessary to obtain an Account Change Card

and a line card for signature verification. The Account Change card reflecting any

changes must be signed and returned before changes are made in XP2.

Updated account documents must be received within 30 days of the change

request. If signed documents are not returned within 30 days, all changes are

voided/reversed.

Name Change

When a surname change is required for a primary member,

- Obtain new social security card or receipt of change from Social Security

Administration. ***Required***

- If new driver’s license is available, scan in XP2 for identification purposes.

- Complete Account Change Card with the new legal name, information and

signature. Verify the member's previous surname in XP2. Update the primary

name in XP2.

When a Joint Owner changes their name, either a driver’s license or a social security

card is acceptable proof.

Addition of Joint Owner

A member may add a joint owner at any time. Obtain an Account Change Card. Have

both the member and the joint owner(s) sign where indicated. Also have joint owner(s)

show proper identification, and run through Verafin and Harland eFunds. Only the

primary member can authorize the addition of a joint owner.

Deletion of Joint Owner

An Account Change Card must be obtained with the signature of the member along with

any other joint signers that are still on the account. If a joint owner requests to be

deleted from an account he/she must sign the “Revocation of Joint Share Account

Agreement” form. An Account Change Form must be mailed to primary member along

with letter explaining request for update of signature card.

Payable on Death Change

To change or appoint a Payable On Death beneficiary, the primary owner and any

joint owner of the account must complete the Account Ownership Selection on the

Account Change Form. (For changes of IRA's, refer to IRA/Trust Services Section.)

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

37

Decedents Accounts

Due to the complexity of handling the closure of a deceased member account,

Accounting Department staff must be notified before any action is taken. They will

provide procedures on what documentation is needed and how to close the account.

Forms Required

Certified copy of Death Certificate Letters of Administration, Letters Testamentary (if there is no joint owner).

190BProcedures

Upon notification of the death of a member, proceed as follows:

1 Notify Accounting Department.

2 Remove limit from Line of Credit and Credit Card.

3 Joint owner or beneficiary:

a. Advise of status of the account and options available.

b. Ask for any needed information or documents.

c. Advise of loans and possible credit life.

4 Handle account according to written instructions from joint owner or

beneficiary.

5 If it is an "Individual Account":

d. Call Accounting for approval to release funds, if balance of account is $100.00 or

less and there are no conflicting claims.

e. If the balance is over $100.00, we must have Letters of administration or

Letters Testamentary, before releasing funds.

6 If there are loans, share accounts cannot be closed until loans are paid off

7 Accounts without loans can be processed and closed once the required

documents, including death certificate, written instructions for

disbursement and proper identification are received from the joint owner,

beneficiary, or administrator.

Before giving anyone information about a deceased members’ account, you must make

sure that the person can receive that information legally. Upon notification of a

deceased member, the MSR will verify if the person asking for the information is a signer

on the account.

Never agree that the supposed deceased member has an account until the person has

presented a death certificate and documents showing they are over the estate. If the

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

38

person is not a signer on the account all you can tell them is that they are not a signer

on the account.

Speak with the Accounting Department before releasing any information on a deceased

member’s account. No deposits/transactions are to be made to a deceased members

account without approval from the Accounting Department.

In regards to a missing person, if someone is claiming a member is missing and is

inquiring about the account; verify if the person asking for the information is a signer

on the account before releasing any information. The MSR will only be able to release

information if the person has a Durable Power of Attorney over the missing person

(approved by Gary Coker, C.U. attorney), or if the credit union is served with a court

order. Be compassionate to the family, legally, however, we cannot release any

information about the account or even confirm if the person has an account with the

credit union now or in the past.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

39

Decedent's - Loans and Visa

Upon notification of the death of a member/borrower, review the death claims procedure

as shown in the previous section, "Decedents Accounts," then proceed as follows:

Forms Required

Certified copy of Death Certificate

Letters of Administration, Letters of Testamentary (if applicable).

Procedures

The Record Retention Department - Main Office will:

1 Notify Accounting

2 Pull signature forms/card and line cards.

3 Alpha inquiry and search for multiple accounts.

4 Loan With Insurance Coverage

- Notify Accounting Department.

5 Loan Without Insurance Coverage

- Notify the Loan Department.

6 Notification of Loan Payoff

- Notify Loan Department.

Visa Accounts

1 Deceased Member - Individual (1) Card

a. Notify Credit Card Department

b. Request card from informant or survivor.

2 Deceased Member - Joint Applicant (2) Cards

a. Notify Credit Card Department

b. Advise survivor that due to the death of the primary cardholder, the

limits have been removed and no further charges can be honored.

Request that cards be returned to the Credit Union, and complete an

application for a VISA credit card if survivor is or would like to be a

member.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union

40

VISA Department Responsibilities

1 Upon receipt of status change request, VISA will status the account.

2 Enter in appropriate Warning Bulletin.

3 Upon confirmation that the account is in the Warning Bulletin, VISA will

change VISA cross-reference number on our system to prevent any further

activity on the account or the possibility of the card being reissued.

Standard collection procedures will be followed on VISA balances, when necessary.

General Responsibilities and Requirements – Member Services

Education First Federal Credit Union