medical technology investing...the current climate

Upload: inflection-point-executive-coaching-consulting-for-medtech-biopharma-and-healthcare-services

Post on 14-Jan-2017

286 views

TRANSCRIPT

Venture Healthcare – Industry Update

S V B - P h oen ix C on feren ce

P h oen ix M ed icalD evice C on feren ce

O ctober2 0 1 5

Jon N orris- jn orris@ svb.com 2

Manage West Coast Healthcare Relationshipsfor SVB across the SVB Platform, including

Fund of Funds (Investment as LP)

Direct Equity (Co-Investments and Rights to Invest)

Commercial Bank (Venture/Mezzanine Debt, Asset-based Debt,New Fundings)

Equity Financing Strategy for Early Stage and Venture-BackedCompanies

Industry Thought Leadership

Jon Norris: Managing Director, SVB Capital

Jonathan NorrisManaging Director,HealthcareSilicon Valley Bank

Mobile [email protected]: @jonnysvb

Publications

Trends in Healthcare Investments and Exits (2015)

A Year of Dazzling Returns: 2014 Healthcare Investmentsand Exits (2015)

Trends in Healthcare Investments and Exits (2014)

Strong Momentum in Healthcare (2013)

First Mover Advantage (2012)

Continued Rebound (2012)

Trends in M&A (2011)

Bringing Home the Bacon (2010)

3Jon N orris- jn orris@ svb.com 3

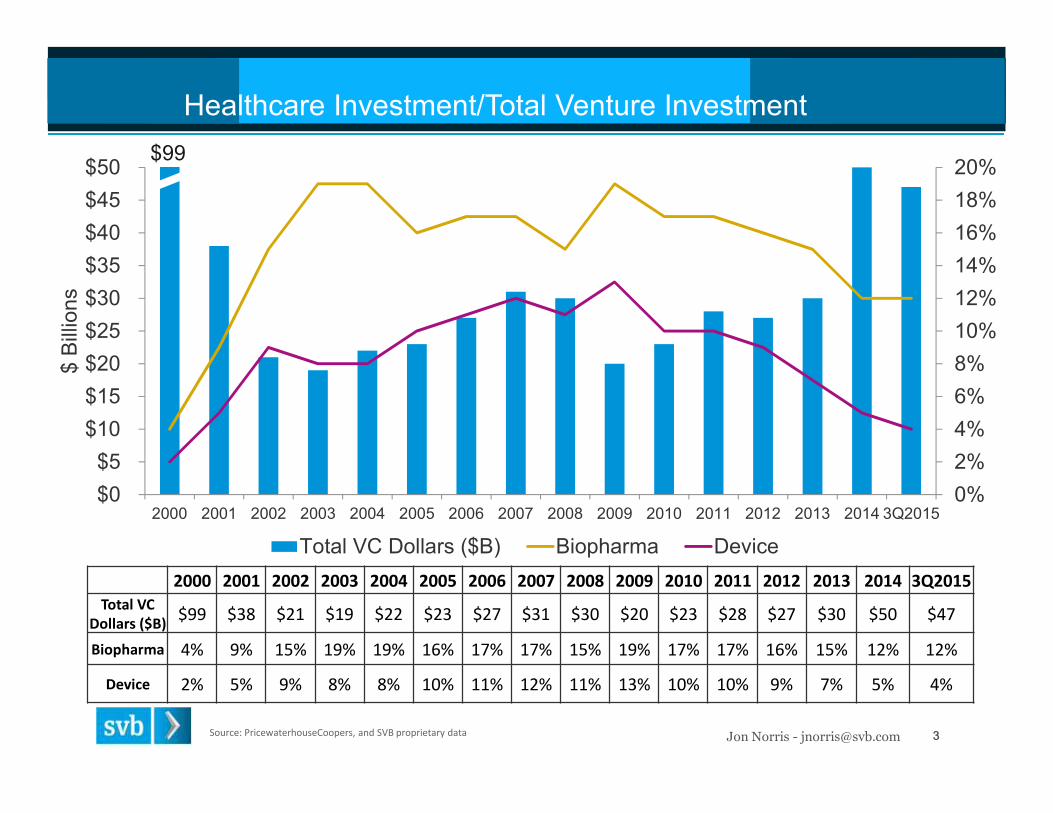

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015Total VC

Dollars ($B)$99 $38 $21 $19 $22 $23 $27 $31 $30 $20 $23 $28 $27 $30 $50 $47

Biopharma 4% 9% 15% 19% 19% 16% 17% 17% 15% 19% 17% 17% 16% 15% 12% 12%

Device 2% 5% 9% 8% 8% 10% 11% 12% 11% 13% 10% 10% 9% 7% 5% 4%

Healthcare Investment/Total Venture Investment

Source: PricewaterhouseCoopers, and SVB proprietary data

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

$B

illio

ns

Total VC Dollars ($B) Biopharma Device

$99

4Jon N orris- jn orris@ svb.com 4

Historical Trend Data for Device 2000-3Q2015

3Q2015

Source: PricewaterhouseCoopers, NVCA, Thomson Reuters

5Jon N orris- jn orris@ svb.com 5

Device Investment Into Venture - Consistency since 2009

Year Device $ Invested Dollars as % of Total VC

2007 $3.7 Billion 12%

2008 $3.6 Billion 11%

2009 $2.6 Billion 13%

2010 $2.5 Billion 10%

2011 $2.9 Billion 10%

2012 $2.6 Billion 9%

2013 $2.1 Billion 7%

2014 $2.6 Billion 5%

1H2015 $1.3 Billion (stable) 4%

*3Q2015 Device $ Invested: $821M (includes $200M given to Mevion Medical, led by two Chinese investors)

6Jon N orris- jn orris@ svb.com 6

0%

100%

200%

300%

400%

500%

0

1

2

3

4

5

6

7

8

9

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$B

illi

on

s

Gap in Funding HC $ Fundraised HC $ Invested % Capital Flow Ratio

Source: PricewaterhouseCoopers, Thompson Reuters, and SVB proprietary data

US Healthcare: Venture Dollars Invested and Raised

Jon N orris- jn orris@ svb.com 7

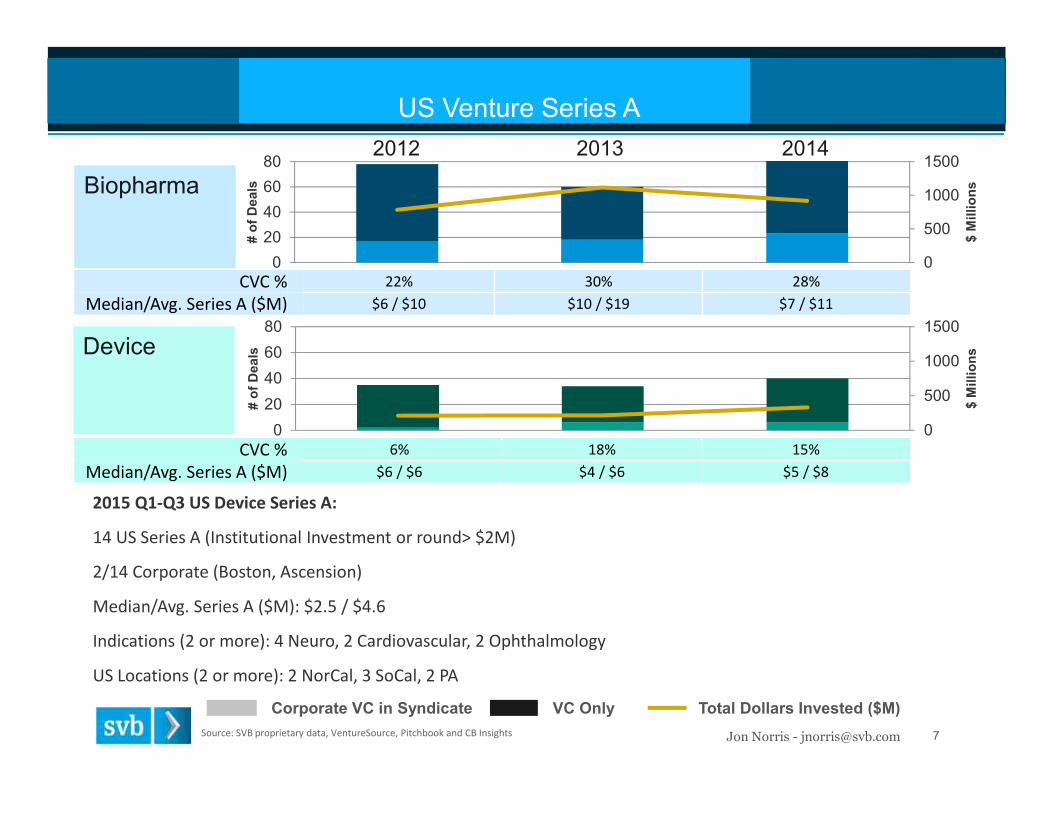

2015 Q1-Q3 US Device Series A:

14 US Series A (Institutional Investment or round> $2M)

2/14 Corporate (Boston, Ascension)

Median/Avg. Series A ($M): $2.5 / $4.6

Indications (2 or more): 4 Neuro, 2 Cardiovascular, 2 Ophthalmology

US Locations (2 or more): 2 NorCal, 3 SoCal, 2 PA

0

500

1000

1500

0

20

40

60

80

$M

illio

ns

#o

fD

eals

0

500

1000

1500

0

20

40

60

80

$M

illio

ns

#o

fD

eals

US Venture Series A

Source: SVB proprietary data, VentureSource, Pitchbook and CB Insights

Device

Biopharma

CVC % 6% 18% 15%

Median/Avg. Series A ($M) $6 / $6 $4 / $6 $5 / $8

CVC % 22% 30% 28%

Median/Avg. Series A ($M) $6 / $10 $10 / $19 $7 / $11

2012 2013 2014

Total Dollars Invested ($M)VC OnlyCorporate VC in Syndicate

Jon N orris- jn orris@ svb.com 8

0

4

8

12

16

20

24

#o

fD

ea

ls

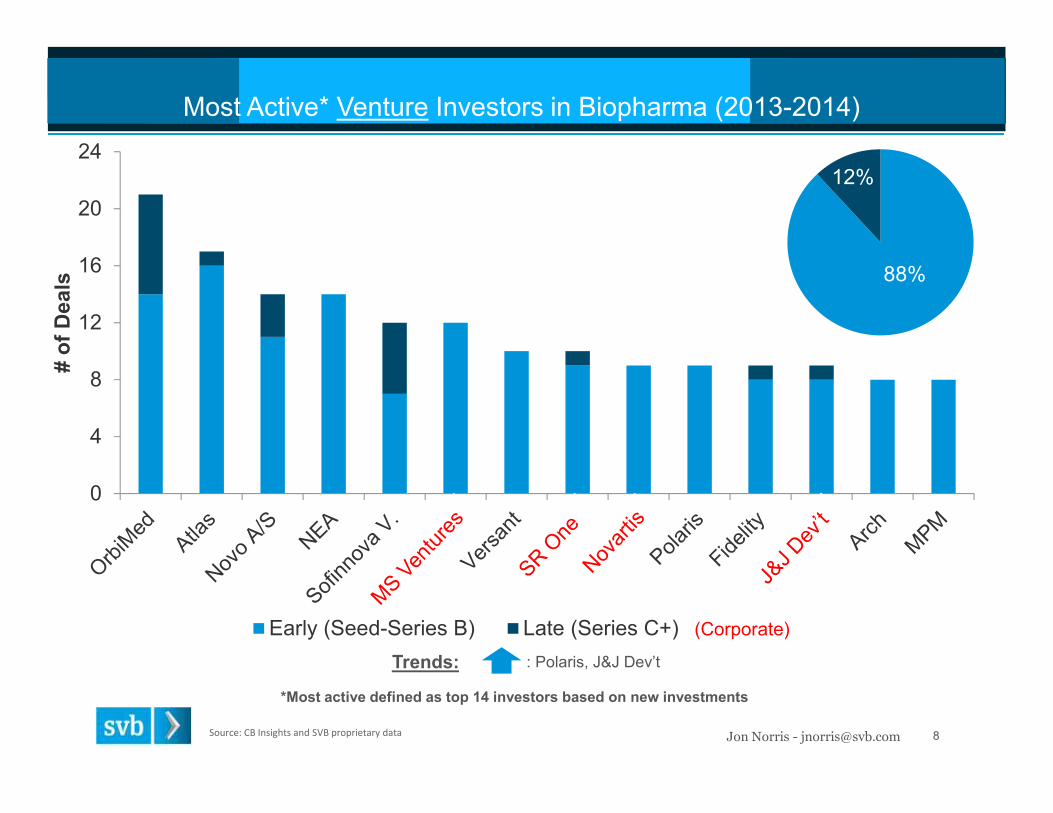

Early (Seed-Series B) Late (Series C+)

*Most active defined as top 14 investors based on new investments

Most Active* Venture Investors in Biopharma (2013-2014)

(Corporate)

Source: CB Insights and SVB proprietary data

12%

88%

: Polaris, J&J Dev’tTrends:

Jon N orris- jn orris@ svb.com 9

0

1

2

3

4

5

6

7

8

9

10

Early (Seed-Series B) Late (Series C+)

64%

36%

Most Active* Venture Investors in Device (2013-2014)

(Corporate)

Source: CB Insights and SVB proprietary data

: Sofinnova P., Sightline, Kearny, BioStar, Emergent, LightstoneTrends:

*Most active defined as top 13 investors based on new investments

#o

fD

ea

ls

Jon N orris- jn orris@ svb.com 10

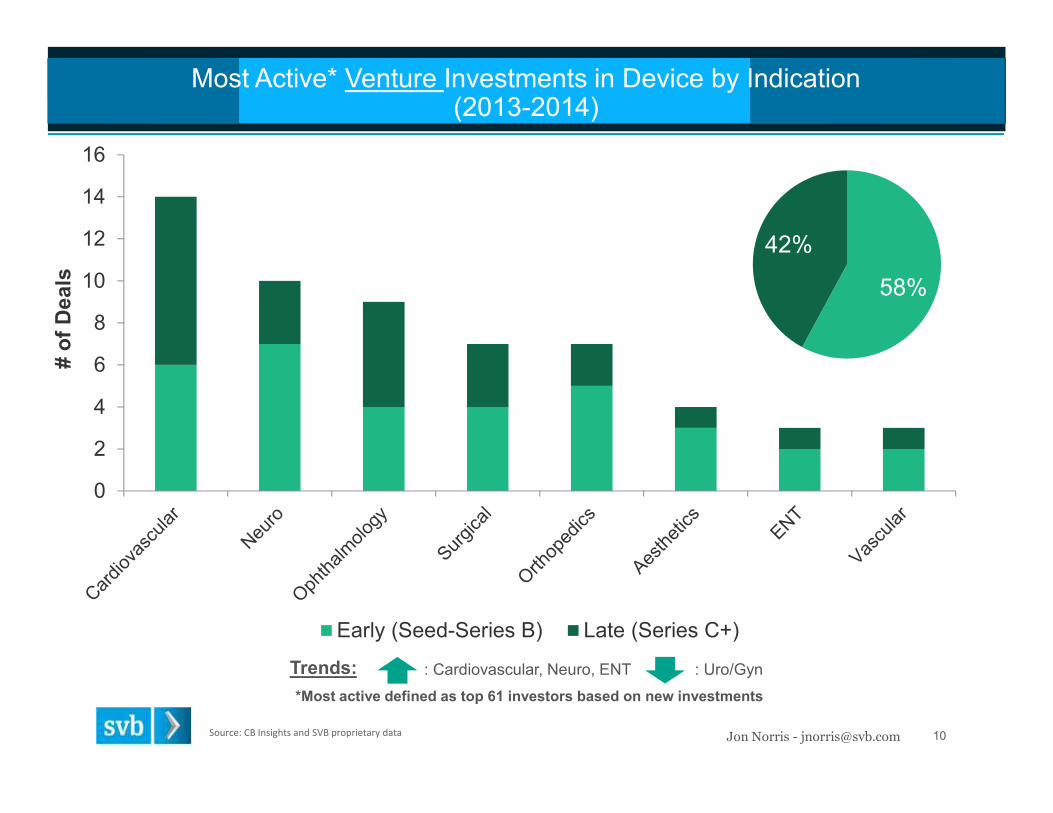

0

2

4

6

8

10

12

14

16

Early (Seed-Series B) Late (Series C+)

*Most active defined as top 61 investors based on new investments

Most Active* Venture Investments in Device by Indication(2013-2014)

: Cardiovascular, Neuro, ENT : Uro/GynTrends:

58%

42%

Source: CB Insights and SVB proprietary data

#o

fD

ea

ls

Jon N orris- jn orris@ svb.com 11

Most Active* Venture Investments in Device by Location (2013-2014)

*Most active defined as top 61 investors based on new investments (duplicate investments removed)

Source: CB Insights and SVB proprietary data

Northern CA,32

Southern CA,11

OUS, 9

MN, 5

WA, 3

MA, 3

2

1

1

1

1

1

1

1

OUS Countries

Ireland

Canada

India

Finland

China

UnitedKingdomFrance

Germany

12Jon N orris- jn orris@ svb.com 12

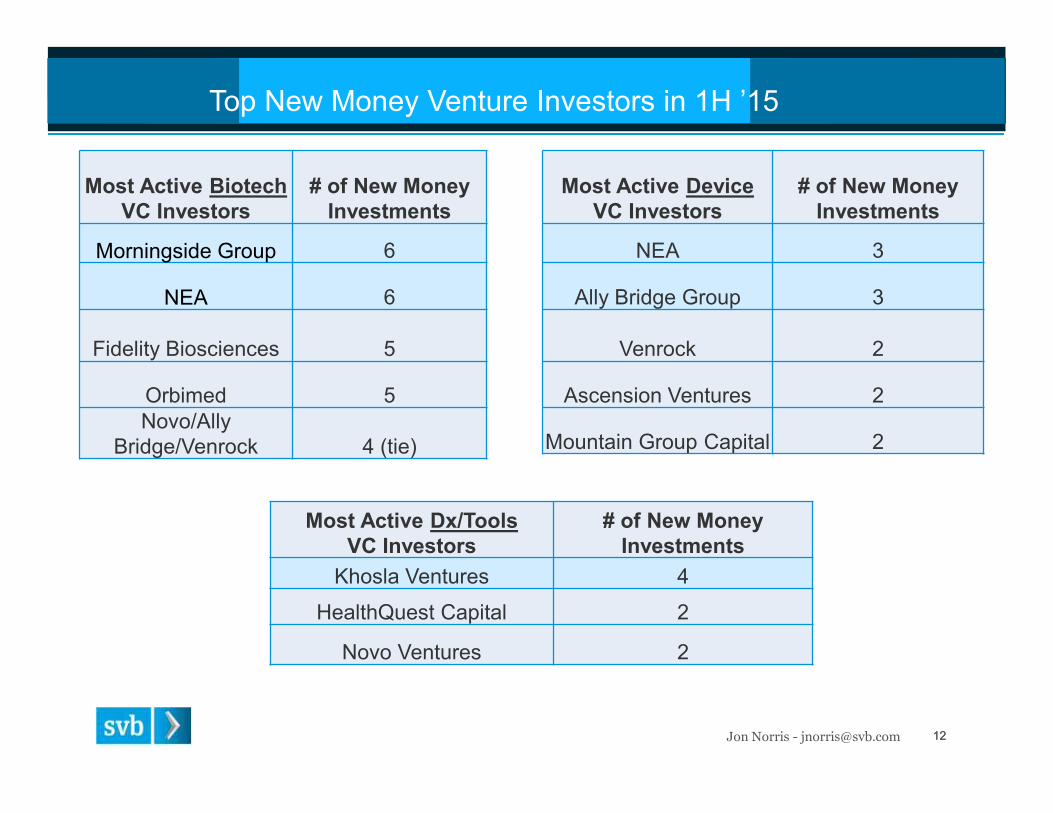

Top New Money Venture Investors in 1H ’15

Most Active BiotechVC Investors

# of New MoneyInvestments

Morningside Group 6

NEA 6

Fidelity Biosciences 5

Orbimed 5Novo/Ally

Bridge/Venrock 4 (tie)

Most Active DeviceVC Investors

# of New MoneyInvestments

NEA 3

Ally Bridge Group 3

Venrock 2

Ascension Ventures 2

Mountain Group Capital 2

Most Active Dx/ToolsVC Investors

# of New MoneyInvestments

Khosla Ventures 4

HealthQuest Capital 2

Novo Ventures 2

13Jon N orris- jn orris@ svb.com 13

Q3 ‘15 Device Update

Q3 ‘15 Device Update:4 Deals raising more than $100M rounds in Q3

Top deal in first half was only $57M.6/10 Deals w/ Cross Over participation, versus 3/10 in Q2.

Not your typical BioPharma crossovers like RA and Rock Springs –examples include Longwood, Third Point, Seneca and Woodford.

5/10 Deals included Corporate Venture, way up over previous years and upover Q2 (2/10)

One deal with Boston, and a few with JJDC, but includes less knownplayers like Sino, Santen, Intersect Partners, Healthcor, and Hoya.

Endavor Vision did three new deals in Q3 (Reshape, Gynesonics, andCeQur).

Swiss based firm that raised over $100M+ Medtech fund in late 2014Final Take away:

New $ moving in to the sector – be prepared for lots of China interestin 2016 (really, we mean it this time!)

Jon N orris- jn orris@ svb.com 14

0

5

10

15

20

25

#o

fD

eals

Biopharma Medical Device Tools/Dx

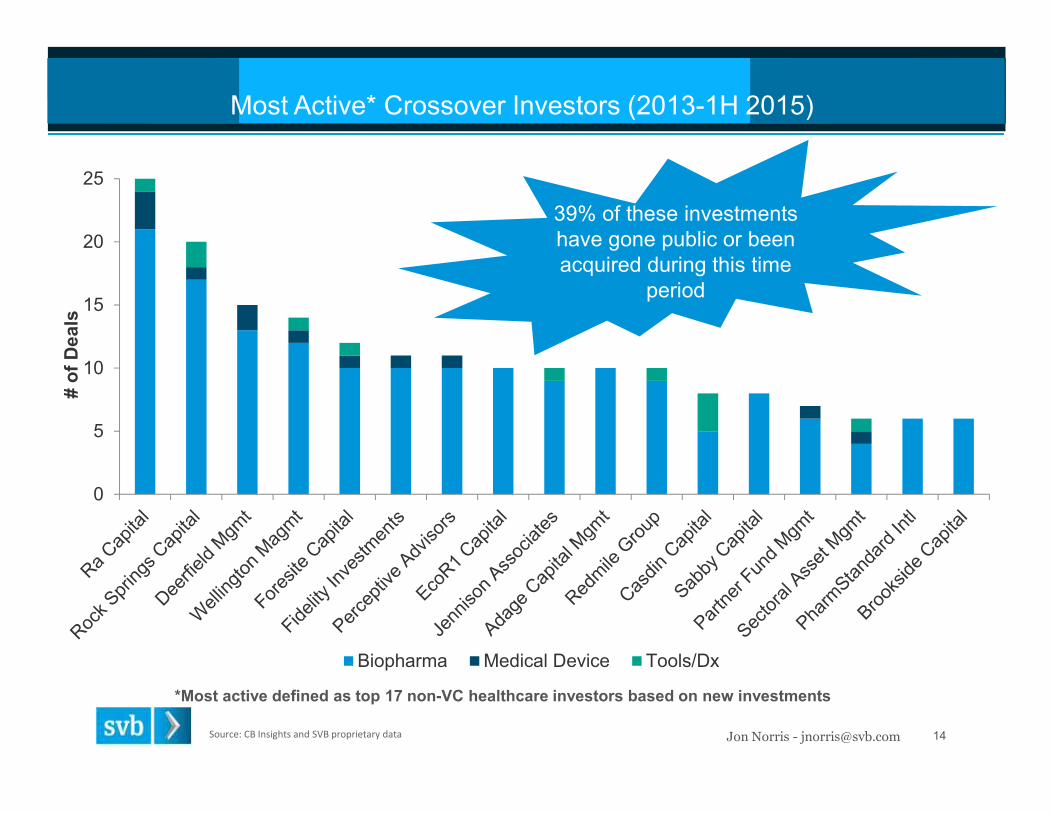

Most Active* Crossover Investors (2013-1H 2015)

Source: CB Insights and SVB proprietary data

*Most active defined as top 17 non-VC healthcare investors based on new investments

39% of these investmentshave gone public or beenacquired during this time

period

15Jon N orris- jn orris@ svb.com 15

Device Pre Money Valuations in Private Device Companies2012 – 3Q2015

Jon N orris- jn orris@ svb.com 16

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

#o

fB

igE

xit

s

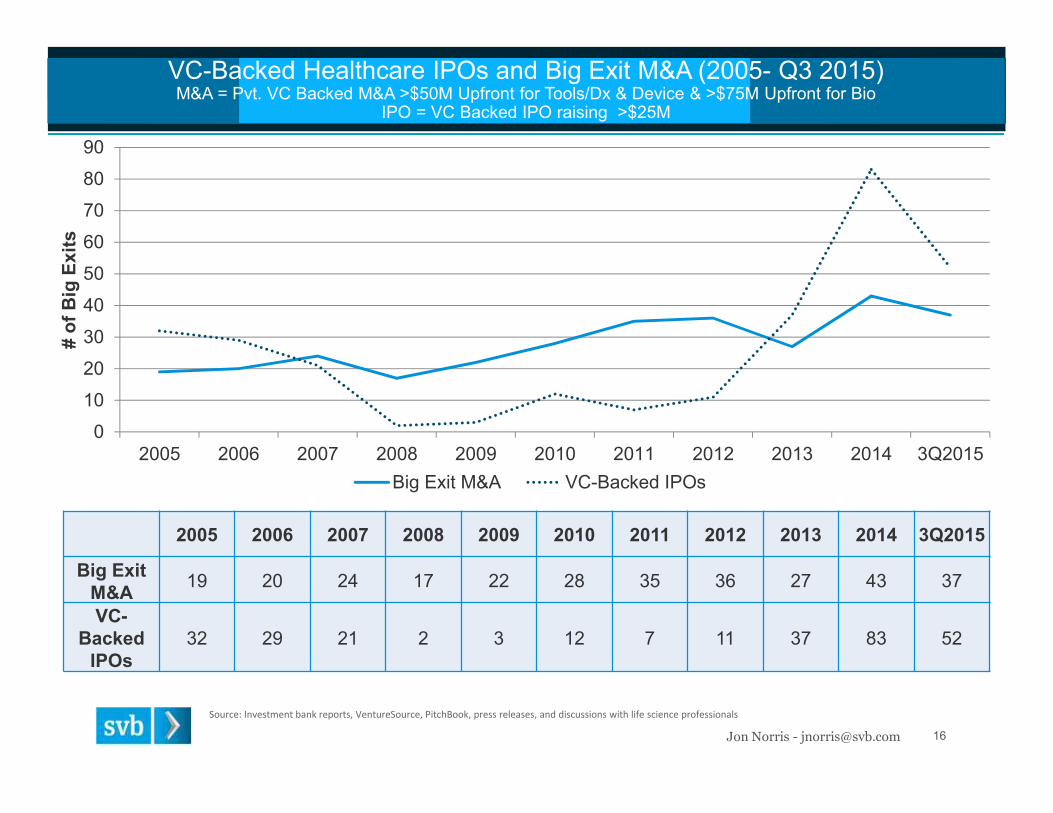

Big Exit M&A VC-Backed IPOs

VC-Backed Healthcare IPOs and Big Exit M&A (2005- Q3 2015)M&A = Pvt. VC Backed M&A >$50M Upfront for Tools/Dx & Device & >$75M Upfront for Bio

IPO = VC Backed IPO raising >$25M

Source: Investment bank reports, VentureSource, PitchBook, press releases, and discussions with life science professionals

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

Big ExitM&A

19 20 24 17 22 28 35 36 27 43 37

VC-Backed

IPOs32 29 21 2 3 12 7 11 37 83 52

Jon N orris- jn orris@ svb.com 17

0

2

4

6

8

10

12

14

16

18

20

22

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

To

tal

Va

lue

($B

illi

on

s)

Big Exit Upfront Payments Big Exit Milestones to be Earned Pre-Money IPO Value

*Potential distribution calculated as 75% of Upfront Payments, 25% of Milestones, and 75% of Pre-Money IPO Value

Potential Distributions* From VC-Backed IPOs and M&A (2005 – Q3 2015)

Source: Investment bank reports, VentureSource, press releases, CB Insights, and discussions with life science professionals

2015: Projected numbers outpace 2013and approach last year’s record returns

Jon N orris- jn orris@ svb.com 18

VC Backed Device Exits by Quarter 2013 – Q32015

• Device IPOs: 4/7 IPOs in 1H’15 had <$11M Rev in Previous 12 months

• Q3: 9 M&A, with 5/9 companies Non-Approved; 3 CE Mark Only

Source: CB Insights, press releases, and SVB proprietary data

Q1 Q2 Q3 Q4 Total

2013 IPO 0 0 0 2 2

M&A 1 2 6 2 11

2014 IPO 1 5 1 3 10

M&A 2 9 5 2 18

2015 IPO 3 4 3 10

M&A 0 4 9 13

Jon N orris- jn orris@ svb.com 19

VC-Backed Device Exits by Stage (2009 – 3Q2015)

Source: Press releases, CB Insights, and SVB proprietary data

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 3Q2015

#o

fB

igE

xit

s

Non-Approved CE Mark U.S. Commercial

Represents number of IPOs

Represents Big Exit M&A

1 1

2

1

2

1 2 7

1 2 8

Jon N orris- jn orris@ svb.com 20Source: Press releases, CB Insights, and SVB proprietary data

VC-Backed Device Exits by Indication 2014- Q32015

0

1

2

3

4

5

6

7

8

9

10

#o

fC

om

pan

ies

Non-Approved CE Mark U.S. Commercial

Represents number of IPOs

Represents Big Exit M&A

1 1

1

1

1

2 3

2

1

1 1

Jon N orris- jn orris@ svb.com 21

0

200

400

600

0

4

8

12

16

20

Deal

Siz

e($

M)

0

200

400

600

0

4

8

12

16

20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Deal

Siz

e($

M)

VC-Backed Big Exit M&A

Biopharma

Device

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

#ofB

igE

xits

Upfront $: Median ($M) 66 132 89 150 323 160 130 95 130 180

Total Deal $: Median 101 150 121 250 405 200 155 195 220 185

Upfront $: Median ($M) 230 410 346 200 200 158 208 155 200 225

Total Deal $: Median 230 435 346 285 403 380 407 350 440 413

Avg. Upfront ($M)Avg. Total Deal Value ($M)# of Structured Deals

Source: Investment bank reports, press releases, anddiscussions with life science professionals

#ofB

igE

xits

2015 Q1-Q3 Device Big Exit M&A:

Deals (Structured/Unstructured): 14 (8/6)

Upfront Median/Avg. ($M): $163 / $199

Total Deal Median/Avg. ($M): $227 / $272

Jon N orris- jn orris@ svb.com 22

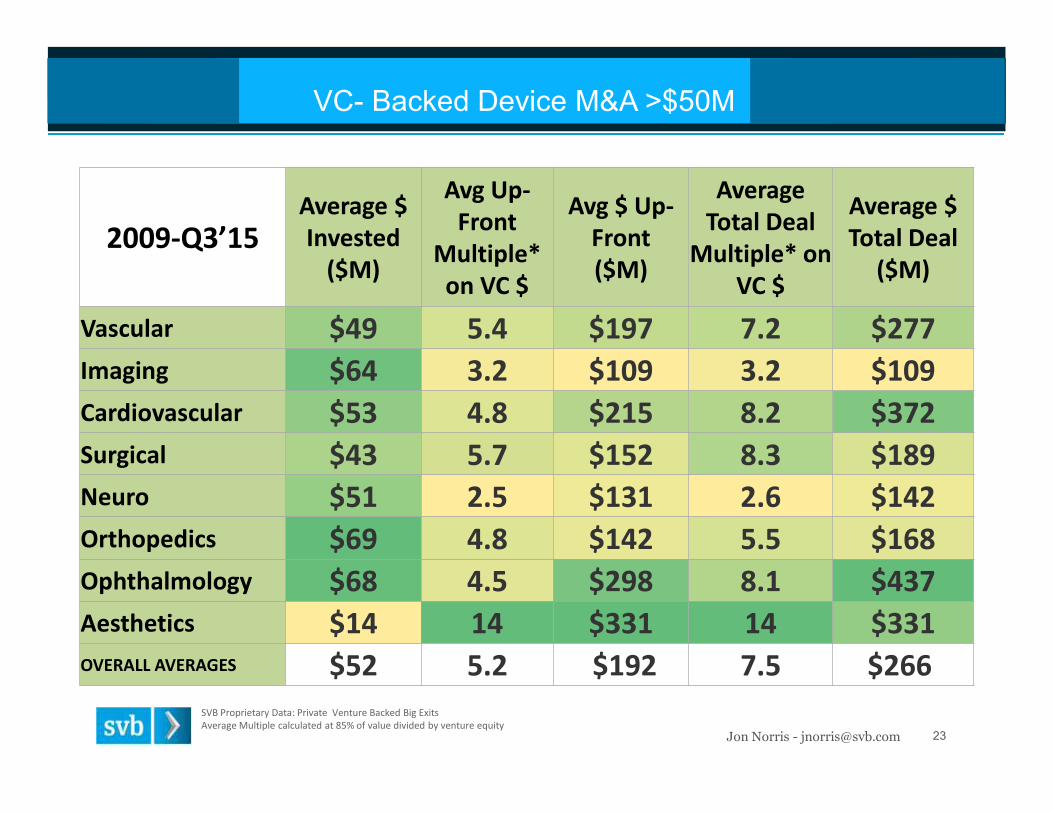

VC- Backed Device M&A >$50M

SVB Proprietary Data: Private Venture Backed Big ExitsAverage Multiple calculated at 85% of value divided by venture equity

2009-Q3’15Number of

ExitsStage:

Dev/CE/USAverage Years

to Exit

Vascular 18 1/6/11 7

Imaging 6 0/0/6 10

Cardiovascular 22 7/8/7 6.6

Surgical 16 1/2/13 7.7

Neuro 4 2/2/0 5

Orthopedics 7 0/0/7 7.3

Ophthalmology 6 1/2/3 6.7

Aesthetics 4 0/0/4 4.8

OVERALL AVERAGES 7.0

Jon N orris- jn orris@ svb.com 23

VC- Backed Device M&A >$50M

SVB Proprietary Data: Private Venture Backed Big ExitsAverage Multiple calculated at 85% of value divided by venture equity

2009-Q3’15Average $Invested

($M)

Avg Up-Front

Multiple*on VC $

Avg $ Up-Front($M)

AverageTotal Deal

Multiple* onVC $

Average $Total Deal

($M)

Vascular $49 5.4 $197 7.2 $277

Imaging $64 3.2 $109 3.2 $109

Cardiovascular $53 4.8 $215 8.2 $372

Surgical $43 5.7 $152 8.3 $189

Neuro $51 2.5 $131 2.6 $142

Orthopedics $69 4.8 $142 5.5 $168

Ophthalmology $68 4.5 $298 8.1 $437

Aesthetics $14 14 $331 14 $331OVERALL AVERAGES $52 5.2 $192 7.5 $266

Jon N orris- jn orris@ svb.com 24

Top Acquirers – VC Backed M&A (2009-Q32015)

Acquirer Car

dio

vasc

ula

r

Vas

cula

r

Surg

ical

Ne

uro

Op

hth

alm

olo

gy

Ort

ho

ped

ics

Oth

er

Re

spir

ato

ry

Uro

/Gyn

ENT

Met

abo

lic

SUM

Medtronic (Covidien) 6 6 10 2 0 0 0 1 1 0 0 26

Boston Scientific 5 1 0 1 0 0 1 1 1 0 0 10

Abbott 3 1 0 0 2 0 0 0 0 0 0 6

CR Bard 1 2 2 0 0 0 0 0 0 0 0 5

Stryker 0 1 0 0 0 3 0 0 0 0 0 4

Johnson & Johnson 0 1 0 0 0 0 0 0 0 1 1 3

St. Jude 2 0 0 1 0 0 0 0 0 0 0 3

Allergan 0 0 0 0 2 0 1 0 0 0 0 3

TOTAL 17 12 12 4 4 3 2 2 2 1 1

Jon N orris- jn orris@ svb.com 25

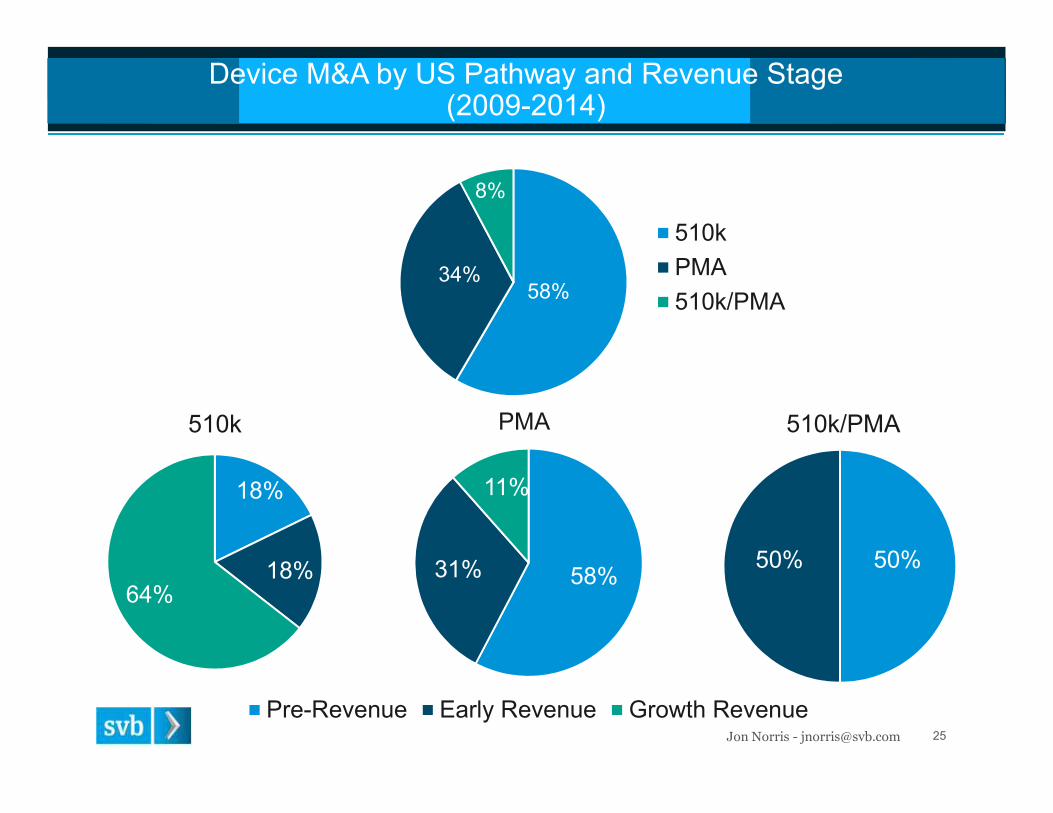

Device M&A by US Pathway and Revenue Stage(2009-2014)

50%50%

510k/PMA

18%

18%64%

510k

58%31%

11%

PMA

Pre-Revenue Early Revenue Growth Revenue

58%34%

8%

510k

PMA

510k/PMA

Jon N orris- jn orris@ svb.com 26

Device M&A: Analysis by US Pathway(2009-2014)

N = 45 N = 26 N = 6

510k PMA 510k/PMAMedian Time to Exit (Years) 6.5 6.8 6.2

Median $ Invested (MMs) $33.0 $62.0 $43.0

Median Up-Front $ Value (MMs) $120.0 $193.0 $85.0

Median Total Deal $ Value (MMs) $132.0 $325.0 $120.0

Median Upfront Multiple 3.68x 2.62x 2.35xMedian Total Multiple 3.76x 5.60x 2.73x

Jon N orris- jn orris@ svb.com 27

Device M&A: Values by Revenue Stage(2009-2014)

510k n = 8 n = 8 n = 29

MMs Pre-Revenue Early Revenue Growth Revenue

Median Up-Front $ Value $83.0 $90.0 $135.0

Median Total Deal $ Value $100.0 $110.0 $150.0

Median Time to Exit (Years) 3.4 7.0 6.8

PMA n = 15 n = 8 n = 3

MMs Pre-Revenue Early Revenue Growth Revenue

Median Up-Front $ Value $193.0 $188.0 $230.0

Median Total Deal $ Value $325.0 $393.0 $255.0

Median Time to Exit (Years) 5.3 8.8 11.1

Thank you!!!

28S V B - P h oen ix C on feren ce

Medical Device Market Update

October 2015 CONFIDENTIAL

Average Revenue

Multiple (2) 5.81x 4.03x 3.76x 2.85x 4.53x 3.41x 3.85x 3.99x 4.19x 3.38x

Average Deal Value

(Excl. Mega Deals) (3) $216 $1,124 $1,193 $462 $370 $792 $630 $368 $517 $902

$6

$45

$37

$11$14

$28

$20

$11$14 $22

$38

$5

$19

$9

$73

$47

$19

$87

30

40

31

23

38

35

3129

27

24

0

10

20

30

40

50

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Excluding Mega Mergers, Average Transaction Sizes are at Their Highest Levels Since 2008

Med

ical

Dev

ice

M&

AV

olu

me

(1)

Dea

lV

olu

me

($b

n)

Trends in M&A Volume

Representsmega-deals

________________________Source: Wall Street research, Company filings and FactSet.Note: Transaction values include earnouts as disclosed. Valtech Cardio excludes earnouts (~$560mm incremental value at time of announcement).(1) Historical statistics through 2012 per Wall Street research report dated 12/22/14. 2013 through 2015 per FactSet, Company filings and Wall Street research.(2) Historical statistics through 2014 per Wall Street research report dated 12/22/14. 2015 per FactSet, Company filings and Wall Street research.(3) Excludes Guidant, Synthes, Bausch & Lomb (take private and sale), Biomet (take private and sale), Covidien and CareFusion.

#o

fD

eals

2015 YTD:

Dentsply / Sirona

St. Jude / Thoratec

Hill-Rom / Welch Allyn

Cardinal / J&J Cordis

Greatbatch / Lake Region

Boston Scientific / EndoAMS

Cyberonics / Sorin

Straumann / Neodent

Medtronic / Twelve

XIO Group / Lumenis

Edwards / CardiaQ

Heartware/ ValtechCardio

Integra / TEI

Allergan / AqueSys

Medtronic / RF Surgical

Abbott / Tendyne

St. Jude / SpinalModulation

Steris / General Econopak

Medtronic /Medina

Atricure / nContact

Medtronic / Aptus

Medtronic / Lazarus

TransEnterix / SOFARRobotics

Medtronic / CardioInsight

1

NA NA NA NA NA 4.70x NA NA NA NA NA NA NA NA2015 EV/Rev:

$929

$458$400

$300$250 $235

$175 $175 $150$110 $100 $100 $99 $93

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

4.38x 6.86x ~3.00x 2.49x ~2.15x 3.30x 1.60x 1.66x 5.75x 4.50x2015 EV/Rev:

$5,560

$3,400

$2,050$1,944 $1,730 $1,650

$1,400

$510 $478 $312

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

________________________Source: Press Releases and Wall Street Research(1) Includes potential earnouts.(2) Excludes potential earnouts.

2015 Transactions To Date

Twelve SOFARRobotics

Lat

erS

tag

e/

Co

mm

erci

al

Dea

lV

alu

e($

mm

)

Mean: $1,903mm

Mean: $256mm

(1)

(1)

(1)

(2)

(2)

(2) (2)

(2) (2)

Dea

lV

alu

e($

mm

)

Ear

lyS

tag

e

2

Selected Pre-PMA Medical Device Precedent Transactions

________________________Source: Company website, filings, Wall Street research, and FactSet as of 10/16/15.(1) Future payments tied to regulatory milestones were undisclosed.(2) Represents approximate values assuming the pre-announcement Heartware closing price of $81.81 to imply upfront and future earn-out payments.(3) Abbott acquired the remainder of the equity of Tendyne that it did not own for $225mm, or a transaction value of $250mm plus milestone payments.

DateAnnounced

Acquiror TargetTarget Public

vs. PrivateCE Mark Upfront Value

PotentialEarnout

TotalConsideration

Earnout as a % ofTotal

10/04/15 AtriCure nContact Private $99 $50 $149 33.6%

09/03/15 Allergan AqueSys Private 300 NA 300 NA

09/01/15 Heartware Valtech Cardio Private 360 569 929 61.2%

08/25/15 Medtronic Twelve Private 408 50 458 10.9%

07/30/15 Abbott Tendyne Private 250 NA 250 NA

07/10/15 Edwards Lifesciences CardiAQ Valve Technologies Private 350 50 400 12.5%

08/19/13 St. Jude Medical Endosense Private 171 161 332 48.5%

07/15/13 Abbott OptiMedica Private 250 150 400 37.5%

06/07/13 St. Jude Medical Spinal Modulation Private 40 300 340 88.2%

11/08/12 Boston Scientific Vessix Vascular Private 125 300 425 70.6%

10/08/12 Boston Scientific Rhythmia Medical Private 90 175 265 66.0%

03/09/12 Boston Scientific Cameron Health Private 150 1200 1350 88.9%

12/20/11 Bard Lutonix Private 225 100 325 30.8%

01/19/11 Boston Scientific Atritech Private 100 275 375 73.3%

11/22/10 Medtronic Ardian Private 800 NA 800 NA

11/19/10 Boston Scientific Sadra Medical Private 193 193 386 50.0%

09/03/10 St. Jude Medical CardioMEMS Private 60 375 435 86.2%

07/07/10 Alcon LenSx Lasers Private 362 383 745 51.4%

09/10/09 Abbott Labs Evalve Private 356 90 446 20.2%

09/02/09 Abbott Labs Visiogen Private 400 0 400 0.0%

06/02/09 ev3 Chestnut Medical Private 75 75 150 50.0%

02/23/09 Medtronic CoreValve Private 700 150 850 17.6%

02/23/09 Medtronic Ventor Private 325 0 325 0.0%

02/13/09 Thoratec Heartware (terminated) Public 282 0 282 0.0%

01/12/09 Medtronic Ablation Frontiers Private 225 NA 225 NA

12/22/08 St. Jude Medical MediGuide Private 300 0 300 0.0%

09/25/08 Medtronic CryoCath Public 378 0 378 0.0%

06/16/08 Medicis Liposonix Private 150 150 300 50.0%

Mean $275 $206 $451 40%

Median 250 150 378 48%

(1)

(2)

(1)(3)

3

Top 50 Device Companies – Then vs. NowCompany MV ($mm)

1 Medtronic $60,0372 Boston Scientific 29,6963 Alcon 24,6364 Guidant 23,1225 Zimmer 19,6696 Stryker 19,4217 St. Jude Medical 15,0438 Becton Dickinson 14,3669 Synthes Inc 12,879

10 Biomet Inc. 10,96411 C. R. Bard 6,69712 Varian Medical 5,77413 Kinetic Concepts 5,22114 DENTSPLY 4,53015 Hillenbrand 3,44516 Bausch & Lomb 3,43217 Cytyc 3,08018 Edwards Lifesciences 2,45219 Cooper Companies 2,31220 Inamed 2,27121 Teleflex 2,10022 Respironics 1,92623 ResMed 1,74424 STERIS 1,64125 Advanced Medical Optics 1,52526 Sybron Dental 1,41127 Intuitive Surgical 1,37028 Mentor 1,36729 Arrow 1,36230 Integra LifeSciences 1,07831 Kyphon 1,06532 Given Imaging 99433 Wright Medical 96534 Haemonetics 93735 CONMED 82436 Adv. Neuromodulation Systems 80337 Laserscope 78938 Symmetry Medical 698

39 Syneron Medical (1) 692

40 ArthroCare 68641 Align Technology 65442 IntraLase 629

43 Orthofix (1) 614

44 Analogic 61345 Datascope 587

46 SurModics (1) 573

47 Foxhollow Technologies 54748 Aspect Medical Systems 51049 Thoratec 50450 Cyberonics 495

10Y

ears

Ag

o(1

2/31

/04

)

To

day

________________________Source: Market values per FactSet as of 12/31/04 and 10/16/15. Note: Excludes Abbott, Johnson & Johnson and Baxter. Except for LivaNova, excludes announcedpending acquisitions. (1) Publicly traded today but not the public Top 50 medical device companies.

• Of the Top 50 standalone U.S. device companies U.S.

ten years ago, 24 (48%) have been acquired or taken

private

• Mid-cap companies that were sub-$10bn then

were slightly more vulnerable with 20 (50%)

out of 40 acquired or taken private

• P/E multiples for the remaining constituents have

compressed by >20% since their peak

• Over 50% of Today’s Top 50 constituents are new

entrants of the list

• Some IPOs / spin-off’s have been introduced

then acquired within the 10 year cycle (e.g.,

Covidien, AGA Medical, Tornier)

• Six were recent IPOs (Glaukos, Nevro, LDR,

K2M, Inogen, Penumbra)

Shaded companies since acquired / taken private ornew Top 50 entrants

Company MV ($mm)1 Medtronic $104,7632 Stryker 37,6673 Becton Dickinson 29,3434 Boston Scientific 22,9415 Zimmer 20,0406 St. Jude Medical 19,1597 Intuitive Surgical 17,3008 Edwards Lifesciences 16,2659 C. R. Bard 14,481

10 Dentsply 7,92211 ResMed 7,89012 Varian Medical Systems 7,60913 Cooper Companies 7,01714 Dexcom 6,66915 Sirona Dental 5,76916 Teleflex 5,37517 Align Technology 4,85718 Abiomed 4,25019 Steris 4,00320 LivaNova 3,36821 Hill-Rom Holdings 3,01522 NuVasive 2,42723 Cantel Medical 2,36524 Globus Medical 2,21125 Integra LifeSciences 2,20726 Wright Medical 2,16727 Masimo 2,09128 ICU Medical 1,77529 Insulet 1,75930 Haemonetics 1,64531 OSI Systems 1,63932 Natus Medical 1,46233 Penumbra 1,46034 Greatbatch 1,39635 CONMED 1,37336 Halyard Health 1,34037 Nevro 1,23938 Merit Medical 1,06739 Analogic 1,06540 NxStage 1,00241 Endologix 94242 Conformis 91443 Inogen 87744 K2M 77845 Heartware 76446 LDR 76447 Cynosure 74048 Glaukos 73349 AtriCure 62150 Vascular Solutions, Inc. 594

4

$1,986

$7,028

$5,242

$1,311

$860

$1,849$2,085

$1,074$1,323

$1,838

$2,648

13

25

29

8 7

18

10

7

14

19

21

0

5

10

15

20

25

30

35

$0

$2,000

$4,000

$6,000

$8,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015YTD

IPOs FOs Converts No. of Offerings

The Equity Issuance Market Remains Active

________________________Source: Wall Street research, Company filings and FactSet as of 10/16/15.Note: Excludes deals below $25mm. Current market capitalization per FactSet. If over-allotment period still open, deals assume over-allotment fully exercised.

Dea

lV

olu

me

($m

m)

Nu

mb

ero

fO

ffering

s

• Positive equity marketenvironment and recoveredvaluations allowed issuers to tapthe market

• Strongest new issuance market since 2007

• 18 IPOs (excluding Biomet), 19 Follow-ons and 3 Converts since 2014

• Investor receptivenessexpected to continue

• Several IPOs in thepipeline / on the road

1 2 3

5

Pricing Date Issuer Deal ValuePerform. vsRussell2000

09/18/15 $75.9 (71.3%)

08/13/15 92.0 (30.6%)

08/04/15 231.5 1.1%

07/08/15 117.0 (11.1%)

06/30/15 16.0 (54.8%)

06/11/15 57.5 (15.8%)

06/02/15 103.0 (15.2%)

06/02/15 276.0 (6.5%)

05/28/15 41.8 (12.8%)

02/26/15 69.4 (26.6%)

02/02/15 130.4 0.3%

01/29/15 86.8 (33.2%)

10/29/14 51.9 95.8%

05/14/14 111.9 2.2%

04/16/14 48.0 (71.7%)

04/14/14 56.4 (76.5%)

02/24/14 98.7 5.9%

02/13/14 94.1 (9.8%)

01/24/14 86.3 (56.7%)

11/20/13 90.0 (57.7%)

11/07/13 67.3 136.7%

11/06/13 161.0 49.1%

10/29/13 46.9 (34.4%)

05/09/13 130.0 9.2%

04/25/13 98.3 (61.6%)

Mean $96.9 (16.3%)Median 88.4 (15.5%)

02/13/15 $632.5 (11.4%)

06/04/14 201.0 (15.1%)

05/28/14 230.0 (51.6%)

12/05/13 86.0 (24.1%)

02/07/13 115.0 (3.7%)

Mean $252.9 (21.2%)Median 201.0 (15.1%)

________________________Source: Wall Street research, Company filings and FactSet as of 10/16/15.Note: Excludes deals below $25mm. Current market capitalization per FactSet. If over-allotment period still open,deals assume over-allotment fully exercised. Filed IPOs assume maximum size and launched IPOs assumemidpoint of range.(1) Zimmer acquired Biomet for $13.4bn on 04/24/14.(2) Valeant acquired Bausch & Lomb for $8.7bn on 05/27/13.

Init

ialP

ub

lic

Off

erin

gs

Sin

ce20

13

Las

t25

Fo

llo

w-O

nO

ffer

ing

sL

ast

5C

on

vert

ible

Deb

tO

ffer

ing

s

Medical Device’s Equity Issuance ActivityPricing Date Issuer Deal Value

Current MarketValue ($mm)

Perform. vsRussell2000

Filed [$1,000.0] NA NA

09/17/15 138.0 $1,460 37.6%

06/30/15 155.3 914 43.0%

06/24/15 124.2 826 36.6%

06/12/15 55.2 173 16.5%

06/04/15 109.5 286 (15.9%)

01/29/15 65.0 200 28.3%

01/28/15 41.7 72 (44.9%)

01/28/15 90.0 340 8.0%

11/18/14 36.2 283 (55.4%)

11/05/14 144.9 1,239 147.2%

10/28/14 86.3 104 (62.7%)

07/23/14 63.3 547 77.2%

05/07/14 147.4 778 20.7%

Acquired (1) [100.0] NA NA

04/25/14 55.0 60 (69.8%)

04/15/14 89.7 119 (55.6%)

03/19/14 80.5 165 (43.2%)

02/27/14 84.2 496 15.4%

02/13/14 72.2 877 180.7%

11/13/13 138.0 247 (49.7%)

10/08/13 86.3 764 66.5%

Acquired (2) [100.0] NA NA

Mean $90.8 $447 12.8%Median 36.2 286 15.4%

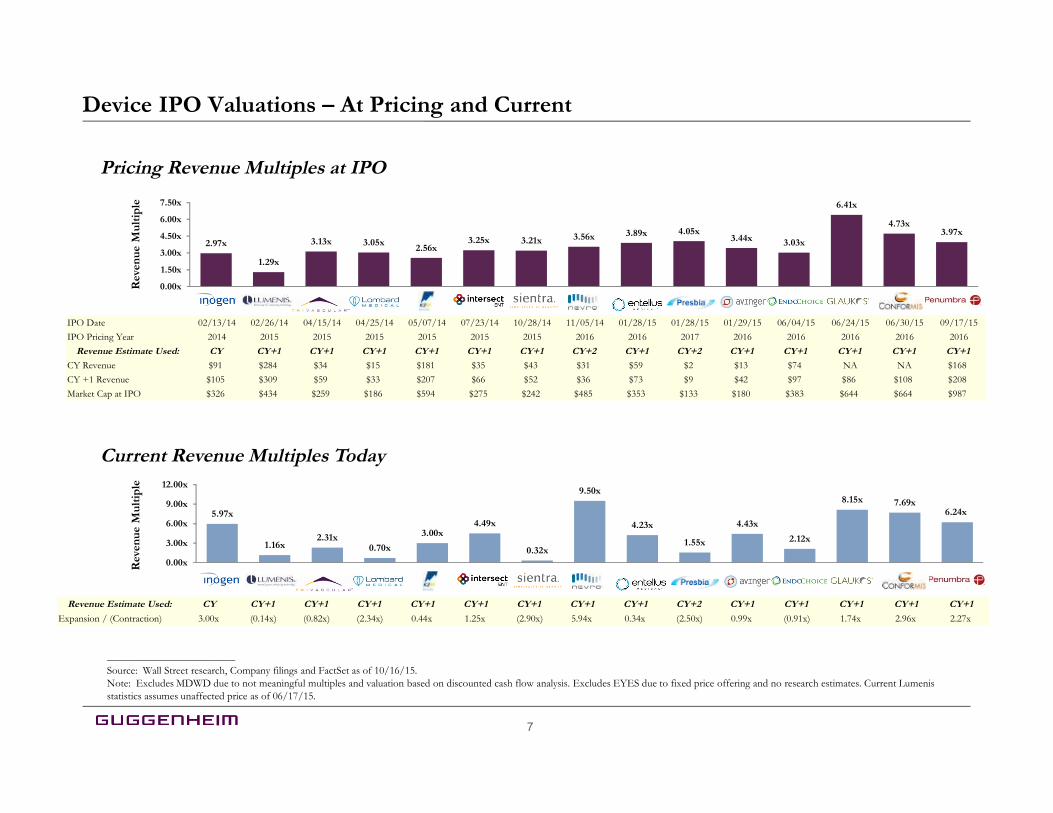

6

Revenue Estimate Used: CY CY+1 CY+1 CY+1 CY+1 CY+1 CY+1 CY+1 CY+1 CY+2 CY+1 CY+1 CY+1 CY+1 CY+1

Expansion / (Contraction) 3.00x (0.14x) (0.82x) (2.34x) 0.44x 1.25x (2.90x) 5.94x 0.34x (2.50x) 0.99x (0.91x) 1.74x 2.96x 2.27x

5.97x

1.16x2.31x

0.70x

3.00x4.49x

0.32x

9.50x

4.23x

1.55x

4.43x

2.12x

8.15x 7.69x6.24x

0.00x

3.00x

6.00x

9.00x

12.00x

IPO Date 02/13/14 02/26/14 04/15/14 04/25/14 05/07/14 07/23/14 10/28/14 11/05/14 01/28/15 01/28/15 01/29/15 06/04/15 06/24/15 06/30/15 09/17/15

IPO Pricing Year 2014 2015 2015 2015 2015 2015 2015 2016 2016 2017 2016 2016 2016 2016 2016

Revenue Estimate Used: CY CY+1 CY+1 CY+1 CY+1 CY+1 CY+1 CY+2 CY+1 CY+2 CY+1 CY+1 CY+1 CY+1 CY+1

CY Revenue $91 $284 $34 $15 $181 $35 $43 $31 $59 $2 $13 $74 NA NA $168

CY +1 Revenue $105 $309 $59 $33 $207 $66 $52 $36 $73 $9 $42 $97 $86 $108 $208

Market Cap at IPO $326 $434 $259 $186 $594 $275 $242 $485 $353 $133 $180 $383 $644 $664 $987

2.97x

1.29x

3.13x 3.05x2.56x

3.25x 3.21x 3.56x 3.89x 4.05x3.44x 3.03x

6.41x

4.73x3.97x

0.00x

1.50x

3.00x

4.50x

6.00x

7.50x

INGN LMNS TRIV EVAR KTWO XENT SIEN NVRO ENTL LENS AVGR GI GKOS CFMS PEN

Device IPO Valuations – At Pricing and Current

________________________Source: Wall Street research, Company filings and FactSet as of 10/16/15.Note: Excludes MDWD due to not meaningful multiples and valuation based on discounted cash flow analysis. Excludes EYES due to fixed price offering and no research estimates. Current Lumenisstatistics assumes unaffected price as of 06/17/15.

Pricing Revenue Multiples at IPO

Rev

enu

eM

ult

iple

Rev

enu

eM

ult

iple

Current Revenue Multiples Today

7