mayor bing's restructuring plan progress report march 2013

TRANSCRIPT

Nuffield College A Gwilym Gibbon Centre for Public Policy

Working Paper

All aboard the Constitutional Express? Where is the Scotland Bill taking the UK?

Professor J. D. Gallagher CB FRSE

Nuffield College, Oxford September 2015

RECOMMENDATIONS CONTAINED IN THIS PAPER Sharing a Union – the Constitutional Provisions of the Bill Clause 1 should not be amended, as some have argued, to remove the words “recognised as” before “permanent”, as would weaken rather then strengthen the protection afforded to devolution. It would be better if the Convention that the Parliament’s powers are not amended without its consent were stated in the Clause 2 of the Bill as well. Parliament should consider whether to constrain the power to alter the devolved electoral system so that it cannot be used to introduce a wholly majoritarian electoral system into a single chamber parliament. Sharing Taxes -The Fiscal Provisions of the Bill It will not be enough to see the new fiscal framework simply as a private agreement between two governments on adjustments to the Barnett formula. It is much more than that, and needs to be exposed for debate for its effect on the whole UK during the passage of this Bill. It now makes no sense to wait another 4 years before the Scotland Bill powers can be exercised. Since the administrative machinery for tax collection is mostly in place, this could come into effect in 2017 or 2018. The government's proposals for a double majority vote on income tax are unworkable, and they could render England and perhaps the whole UK ungovernable in some circumstances. No UK government without an English majority could accept them, and so they do not solve the West Lothian question. Nor do they work in practice in the absence of an rUK spending programme to match an rUK tax decision. The government's approach has been partisan rather than constitutional, and the “English Votes” plans need further consideration. Sharing Welfare - the Benefits Provisions of the Bill The Bill should be amended to place it beyond doubt that top up payments will create new Scottish entitlements, and are not “discretionary" in the sense that the social fund is. The Bill must be amended to make it clear that the Scottish Parliament is able to meet needs not covered by reserved benefits at all, but the UK Parliament cannot be prevented from meeting them on a UK basis as a result. The issue of so-called “veto” powers should be dealt with by amending the Bill to make it much more explicit that welfare, unlike other policy areas, is now effectively a partially shared competence. In consequence the Bill should impose duties of cooperation on both governments, to remove any sense, however

misplaced, that Scottish welfare choices are constrained by UK political decisions. The Scotland Bill and the UK’s Territorial Constitution The challenge set by the Scotland Bill is to develop the UK’s territorial constitution to reflect the reality of devolution, to broaden it, notably to deal with England, and in some way to codify it. The principles of the new territorial constitution have to explain both why and how the UK is a union. The UK is an association of nations which come together to form a political, economic and social union so as to provide security and opportunity for its people, by pooling and sharing resources. Political union is a means for defence and security; economic union provides opportunity and economic stability; social union is a form of mutual solidarity, sharing resources to guarantee basic social rights and protections. So the principles might include:

• The UK is a single international personality, economically integrated, but each of the constituent parts of the union has continuing separate recognition.

• The smaller nations in the union, Scotland, Wales and Northern Ireland, have special protection, because they might otherwise be constantly outvoted. That recognition takes the form of legislatures and executives with independent legitimacy, derived not solely from devolved UK powers, but from the assent of their populations.

• The powers available to the devolved bodies are sufficiently wide for each

to take a different political course from England if their voters wish, and are willing to cover the costs.

• Some key aspects of welfare are guaranteed across the whole UK, so that

the devolved administrations can add to but not subtract from them.

• The territorial constitution also has a fiscal aspect. Resources are shared across the UK so the same key aspects of welfare can be guaranteed to all citizens. So at least 50% of the resources of the devolved bodies should come from shared national taxation, but the devolved nations bear the economic risk on their own resources for the remainder.

• England is the dominant partner of the union. England's Parliament and

government are the UK's Parliament and government, but safeguards are needed against the unlikely risk that legislative change could be forced on England against the wishes of its representatives, without undermining the legitimacy of all MPs or the UK government

• Decentralisation within England should be constitutionally required. It

follows similar principles to devolution in the UK:

o Power may be decentralised asymmetrically to different cities, regions or other areas;

o power should only be decentralised if there are effective administrative structures and democratic accountability;

o decentralised executive power should always be accompanied by fiscal responsibility.

• There are institutions at the centre of the UK, working for all the nations, and charged with the responsibility of maintaining and developing the union and its constitution.

Whatever process takes constitutional reform forward should start with the two connected issues of territorial reform and House of Lords reform.

Executive summary This paper reviews the Scotland Bill currently before Parliament, in the context of both the politics of Scotland and the constitution of the United Kingdom. It proposes amendments to the Bill, and argues, additionally, that the Bill throws up major issues which make urgent the long overdue revision and codification of the UK's territorial constitution. It is no longer sustainable to see devolution as an untidy footnote in how the UK is run. Instead the UK needs a comprehensive statement of its territorial constitution, and the paper suggests some of the principles which should underlie it, and the options for taking it forward. The Scotland Bill emerged from the Scottish referendum campaign, and the Smith Commission1 set up to deliver on the promises of more devolution made before the vote. Despite losing the referendum, the SNP are now dominant in Scottish politics. The Bill is on a demanding timetable, and it would be easy for it to be driven by immediate political needs. But the referendum is now behind us, and absent a major change in circumstances and despite the enthusiasm of new SNP MPs, another is not on the cards. The Bill should be seen in a wider context, and the first section of this paper argues that context is the long-term Scotland-UK relationship. That relationship defines the nature of the UK as a union, which has always held in tension separate Scottish institutions and commitment to the UK. By the end of the 20th century those institutions were democratically accountable. That changes their nature, and means they need different powers, notably the fiscal powers which were lacking in 1999. The second section of the paper welcomes the constitutional provisions of the Scotland Bill, which make clear that the Scottish Parliament is a permanent part of the UK constitutional furniture, and that it has primacy within its own competence by giving statutory expression to the so-called Sewel Convention. Together with giving the Scottish Parliament power over its own composition, these make it much more like a sub-state legislature in federal country, and represent a key building block in what should become the UK's territorial constitution. The big gap in devolution in 1999 was the lack of tax powers. The UK has always had centralised taxation, sensible in the absence of political decentralisation, but inappropriate, and internationally unprecedented, for devolved government. This gap was recognised as long ago as 2008 by the Calman Commission2, but the new tax powers it recommended arrive only in 2016. The Scotland Bill takes these markedly further, with the virtually complete devolution of income tax and the assignment of half of VAT. This will give the Scottish Parliament very significant tax powers –around 40% of taxes will flow to Holyrood– and its powers will stand comparison with the most decentralised countries in the world. Since the present Scottish government will probably refuse to use the 2016 powers to change anything, these further powers should be introduced swiftly, in 2017 or 2018. But complete devolution of income tax throws up problems for the rest of the UK. The existing fiscal framework, based on pre-devolution administrative arrangements, is no longer suitable. Simply adjusting it will not do, as, in the absence of an English or ‘rest of the

1 Smith, 2014 2 Calman, 2008, 2009

UK’ spending programme, it is not clear how voters there can be assured that increases in their income tax do not flow to support spending in Scotland. Even more challenging, the government's plans for English votes include a proposed a “double majority” for UK income tax, which could in some circumstances render England ungovernable. The most radical part of the Bill, however, relates to welfare. Social security has always been reserved, and entitlements the same throughout the United Kingdom. As section 4 of the paper explains, this social union was one of the strongest arguments for Scotland's remaining in the United Kingdom. But an equally strong argument can be made for allowing Scotland, if it wishes and is willing to pay for it, to offer a more generous welfare package, including benefits as well as services. The provisions of the Bill which deal with this have been developed very hurriedly, and need more work. The list of benefits to be devolved was a negotiated political deal, rather than principled allocation. The Bill as drafted fails to meet its objective. The Scottish government can supplement reserved benefits, and has power to meet needs which the UK benefit system fails to meet: unfortunately, these are only allowed to be “short-term". This is a misplaced attempt to ensure that social security remains reserved, and should be amended. More substantively, the Bill needs to be amended to recognise that, as a result, welfare becomes something of a shared responsibility between the two governments, unlike the clear division between most reserved and devolved subjects. Accordingly, duties of cooperation should be imposed, not least to remove any suspicion (however misplaced) that the Scottish welfare capacity is constrained by UK political decisions. These are major changes, and ministers are right to say that they will make the Scottish Parliament perhaps the most powerful substate legislature in the world. Indeed there is a sense in which the Scotland Bill takes devolution back to its roots, the Scottish commitment to devolution was formed under a Conservative UK government, with the Labour Party saying to Scots that devolution would ensure that in future they could do something about such policies. It is to the credit of the present Conservative administration that they are willing to facilitate this. This is obviously also a political project, in that it means the SNP Scottish government will have the powers to change those UK policies which formed much of the basis of their argument for independence. They have however shown, so far, no inclination to increase taxes to help the poorest in the country. But as section 5 of the paper discusses, such major devolution to Scotland (and perhaps potentially Wales and Northern Ireland too) creates problems for the coherence of the UK. The most obvious are those thrown up by the complete devolution of income tax - what about English spending, and what about English votes? These are very specific questions but they merely make explicit the challenge which devolution has always been to the UK's idea of itself as a unitary state, based on a half understood notion of parliamentary sovereignty. The paper argues that the time has come to address this issue head-on, rather than fudge it, or see it is purely a technical challenge in the adjustment of the Barnett formula. Instead it is time to develop and write down the elements of the UK's territorial constitution. Section 5 explains why this is now necessary, and suggests what the key principles of a territorial constitution might be. They have to cover the nature of the UK as a union,

the fiscal arrangements which underpin that union, and for the first time make explicit the position of England as the dominant partner of the union, which shares a Parliament and government with the whole UK. Safeguards are needed to deal with the unlikely risk that England could have legislative change forced on it by the rest of the UK, and there must be provision for internal decentralisation in England on the same, asymmetric, principles as for the UK as a whole. Developing such a territorial constitution is a major undertaking, but should be seen as part of wider constitutional reform. A complete rewrite, from first principles, of whole UK constitution is unnecessary and unachievable, but the paper argues that the territorial constitution should be connected to the role and function of the Second Chamber of Parliament. Constitutional reform has to start somewhere; territorial issues and Lords reform are both urgent.

1: Introduction - The Context of a Constitutional Process The Scotland Bill has been launched into an extraordinarily complex context. It is an immediate reaction to remarkable events, perhaps even fundamental changes, in Scottish politics. But it must also be seen in the context of the changing constitution of the UK as a whole. A legislative process operating to a very demanding timetable may be driven by the political exigencies of the day, the promises made in the Smith Commission, and the remarkable success of the SNP in the general election. But the key to making sense of what should be done lies in a clear long term understanding Scotland's place in the UK3. Scotland and the UK It has become trite to call the United Kingdom a union state. The Treaty and Acts of Parliament which joined Scotland to England (and Wales) were the Treaty and Acts of ‘union’: legally, the ‘union of the kingdoms’ would have been dissolved if Scotland voted to leave the UK. A union state is one not just formed by the coming together of previous states, but also retaining some of the pre-union institutions. This description is not merely an interesting historical curiosity but has political, legal, and ultimately constitutional consequences today. The most striking of these was that the UK acknowledged in the independence referendum that the Scottish people could freely choose to leave. This has been largely taken for granted, but it acknowledges that Scottish membership of the United Kingdom is voluntary and that the sovereign entity making the choice is the Scottish people. (Ironically, a nationalist demand has long been that the Scottish people should become sovereign; we find they have been sovereign all along.) The UK is a union of different nations forming a multinational state. The constitutional provisions of the Scotland Bill, which are discussed in section 2 of this paper, attempt to give a more explicit recognition to this reality. The other consequence was the preservation and development of separate Scottish institutions. The 1707 treaty was not the ‘incorporating union’ which the English had hoped for (and some thought they had achieved). The Scots negotiators were in a weak but not powerless position, and secured things that mattered to them. At a time when religion mattered more than any other issue, the union ensured two separate national churches: Anglican and Erastian in England, Calvinist and proto-democratic in Scotland. This mattered to the whole population as, while only the elite had a voice in the pre-1707 Scottish Parliament, almost everyone had some place in the church. The domestic powers of the 18th century state consisted largely of the courts and the legal system, and these too were left unchanged by the union. As time went on, the powers of the state became wider, and more domestic institutions were created – for everything from education to building harbours. These new Scottish boards, commissions or government departments were not, in a pre-democratic age, democratically accountable to Scots.

3 See Gallagher, 2014 for a fuller explanation of this.

So when Mr Ron Davies, briefly Secretary of State for Wales and talking about the tortured development of the Welsh settlement, called devolution “a process not an event" he was right, and perhaps more right than he realised. The emergence of Scottish political devolution at the end of the 20th century has to be seen in the context of the three centuries before. Its prehistory included a century's gradual building up of the administrative structures of government alongside Scotland's separate church, law and education systems. So the Scottish Parliament of 1999 inherited a well-developed government operation, with powers from Agriculture to Zoo licensing. But these were the powers of a spending department of government, and the major gap, compared with sub-state governments worldwide, was taxation. Apart from local tax (about 15% of the budget) the Scottish Parliament’s spending was wholly financed by UK grant. The tax powers that did exist were either not used (variation of income tax) or used to keep taxes low (council tax freeze). Centralised taxation is a virtue in the absence of political decentralisation: but is a structural weakness for any elected decentralised government. That is why the Scotland Bill, like the Scotland Act of 2012 and the Calman Commission which preceded it, is substantially about tax devolution, analysed in detail in section 3 of this paper. Similarly the growth of government in the 20th century centralised cash welfare payments as well as taxation. There were and are good reasons for this; but when the principal political argument of the time is the extent of the generosity of the welfare state it is a reasonable question to ask to what extent this can be territorially variable across nations within the UK. That is why the Scotland Bill has substantial, if hastily constructed, welfare provisions. Their strengths and weaknesses are discussed in section 4. The political drivers of change The immediate drivers of change have been political events, not the proprieties of constitutional design. It was the shock of nationalist success in 1974, fuelled by the slogan “It's Scotland's oil", that reminded Labour of its forgotten home rule roots. It was the Thatcher government of 1979 that convinced Labour that devolution was the “settled will of the Scottish people”. It was the election of a nationalist devolved government in 2007 that led to the Calman Commission and so to the Scotland Act 2012; and the referendum campaign of 2014/15 led to the Smith Commission and very directly to the present Bill. These political developments too must be seen in the context of Scotland's long term UK relationship. It is a myth that Scottish nationalism is a 20th-century reversion to the late mediaeval, pre-union, Scottish state: one encouraged by Nationalist references, nowadays less evident, to Robert the Bruce and William Wallace, with a confusing admixture of Bonnie Prince Charlie. The truth is that, with their separate institutions, many Scots have long been culturally, ecclesiastically, or legally nationalist, none of which was seen as inconsistent with maintaining a union with England 4 . It is entirely possible to see political devolution as the next logical consequence, providing democratic oversight and accountability, and hence

4 Kidd, 2008

legitimacy, to Scottish domestic institutions. Historically, even the SNP itself, a merger of two different parties over 60 years ago, has been ambivalent about the question of separate statehood as opposed to home rule, or political devolution. It will be interesting to see how the SNP, now hegemonic in Scottish politics, but having to face to the reality of a referendum defeat, now addresses this ambiguity. One year on from the referendum, it is beginning to become easier to get the extraordinary political events of 2014 and 2015 in perspective. An independence referendum was not an opportunity which fell into the SNP's hands: instead it was an unintended consequence of their political tactics. Promising a referendum separated support for independence from voting SNP in the Scottish election: voters did not have to commit to separation to express dissatisfaction with the other political parties. And it told committed supporters that there was a route to separate state, in the expectation that it would be blocked, as previously, by the UK parties. In those circumstances a vote of nearly 45%, compared to long-term support for independence in the opinion polls seldom exceeding 35%, was a big achievement. The result however was as much down to the economic and political circumstances in which the referendum was held, as of the presentation of the case for independence. It came after the longest economic downturn in living memory, sparked by the financial crisis of 2008. Public spending and welfare benefits were being cut markedly. The legitimacy of traditional political institutions was also compromised by scandal and cynicism. So the fresh start of a new state may be have been attractive to many not previously committed to nationalism. The economic drivers of the result are clear: there was a very strong correlation between poverty and Yes voting. The three areas which returned a majority for independence inherited some of the worst of Scotland's post-industrial problems. Some of the strongest No votes were in well-off areas, including e.g. Aberdeenshire, which had returned SNP MPs for decades. Certainly the relentless positivity of the independence campaign, built intellectually on what one Scottish political scientist describes as devolution’s “debilitating oppositional grievance culture masquerading as radicalism"5, was a really a case against the status quo, rather than a campaign for a specific vision of independence. Voters could project onto an independent Scotland whatever they wanted to see there. Nevertheless the referendum campaign changed Scottish politics. Over a million and a half Scots, for whatever reason, rejected the state they belong to. Nationalism had that most elusive of political qualities, momentum. This was the highly charged context of the Smith negotiations. The extraordinarily short timetable promised during the campaign was hung round two very Scottish dates: St Andrew's Day and Burns Night. The content was built on the unionist parties’ different devolution commissions6, and the so-called “Vow” also made during the campaign, promising both more powers and key reservations, including the sanctity of the Barnett formula. Smith went further than many expected, notably on welfare, but there was no incentive for the SNP to accept a package: they participated in Smith, gained some concessions, but denounced it before it was published as inadequate.

5 Mitchell, 2014 6 Scottish Labour Party, 2015; Scottish Conservatives, 2015; Scottish Liberal Democrats, 2012

The most striking effect of the referendum, however, was in the general election six months later. 45% of the vote loses a referendum, but it sweeps the board in a first past the post election, and 50% even more so. As a result, Scotland is now represented by MPs committed to something a majority of its population rejected only a year ago. But the election result left the SNP not the kingmakers they hoped to be, but Westminster’s third party, condemned to opposition. There is little evidence to suggest this result represented “buyer’s remorse" amongst the Scottish electorate. Fewer people voted SNP than voted Yes (turnout was lower), and voters could express support for the SNP at Westminster secure in the knowledge that it would not lead to independence (off the agenda “for a generation") just as they had been able to at Holyrood because of the referendum promise. So threats by SNP MPs that the absence of further concessions on the Scotland Bill would cause them to demand a second referendum can be treated as empty. The UK as a territorial state The Scotland Bill, like other changes to devolution, has been driven by Scottish politics. It is not much of an exaggeration to say that is true of most territorial change in Britain. (Northern Ireland marches to a different tune.) Wales has its own issues and agenda, but its half-hearted Yes to devolution in 1997 might have been a No had its referendum not followed Scotland’s. The additional powers for the Welsh Assembly now on the table follow the approach of the Calman Commission and the Scotland Act 2012. But the UK has never consciously looked at itself, still less designed itself, as a territorial state, as federal countries naturally do. Instead, devolution to Scotland and Wales (still more in Northern Ireland) was seen as an essentially peripheral activity. It did not change the underlying nature of the UK, expressed in a half-understood notion of parliamentary sovereignty. Westminster spawned three new legislatures, but itself sailed on virtually unchanged. The UK government even retained the territorial departments for Scotland and Wales whose business had been transferred to Edinburgh and Cardiff. Under the pressure of events, this is changing. Some of the change is driven by devolution. In recent years, England, the silent if dominant partner in the union, has come to see itself as a political entity more distinct from the UK and Britain7. The Conservative Party won the election by emphasising the risk that the government of England might be determined by Scottish MPs. Other plates are shifting too. Established institutions no longer command the authority they once claimed. The mandate of the House of Commons is based on an electoral system design for two parties, but operating in a multi-party world. Its reputation has been tarnished by scandals, trivial in themselves, but politically significant. The nature of the House of Lords remains under constant challenge. The simplistic notion of parliamentary sovereignty has also been undermined in more substantial ways: sovereignty is pooled within the EU, with its own authoritative legal order; and, whether under domestic administrative law or the European convention on human rights, politically charged cases which the courts would have shied away from 50 years ago are now routinely regarded as justiciable.

7 See Kenny, 2014

The Scotland Bill should bring some of these issues to a head. The scale of power now being devolved makes it imperative that there is a commonly understood territorial allocation of powers, responsibilities, and resources across the UK. This understanding has to include England as a political and constitutional entity: today England isn't even a legal jurisdiction. The complete devolution of income tax throws up major problems not properly addressed in the government's plans. The first is the full detail of the fiscal framework in which these new powers will operate, not so much as it affects Scotland but as it affects England. The second is the question of English votes, where the plans announced by the government signally fail to address the major question arising from the Scotland Bill. Devolution can no longer be a series of ad hoc responses to the latest electoral achievement of the SNP, but needs to be part of a settled territorial constitution for the UK as a whole, of which Scotland has decided to remain part. What that constitution should be, how it might be constructed, and the options for relating it to other aspects of the UK's changing constitution are discussed in section 5.

2: Sharing a Union - The Constitutional Provisions of the Scotland Bill The constitutional provisions of the Scotland Bill are nevertheless to be welcomed. Two of the most significant provisions are declaratory: but what they declare is important, the permanence of the Scottish Parliament and its primacy in its own competence. The Bill also gives the Parliament control over its own composition, subject to a super-majority rule. This is all consistent with a proper understanding of the nature the United Kingdom. The permanence of the Scottish Parliament Devolution is irreversible. That is the political reality, and it would take a radical and profound transformation of Scotland's view of itself and its political institutions for that to change. But the legal form of devolution is an (apparently ordinary) Act of the United Kingdom Parliament. In the absence of a codified set of constitutional laws, different in kind from “ordinary" legislation, that is to say a fully written constitution, an ordinary Act of Parliament was the only vehicle by which the Scottish Parliament could be created. But it is subject to the theoretical (and largely specious) criticism that what Parliament created by one Act it could abolish or diminish by another. The sovereignty of the UK Parliament, often expressed by saying one Parliament cannot bind a future one, apparently makes the Scottish Parliament contingent on Westminster’s whim. This is to misunderstand the reality of parliamentary sovereignty. It is less a claim of absolute power than what the legal theorist Hart calls a “rule of recognition": a way of identifying which laws are good laws, in the sense that they will be enforced by a court in the jurisdiction8. So laws properly passed by Westminster will be recognised as legally enforceable. But reality constrains the notion of sovereignty. The UK Parliament gave up all jurisdiction over (for example) Canada when it repatriated the Canadian constitution in the 1980s. Parliamentary sovereignty does not mean it could unilaterally choose to re-assert it. Devolution was not the creation of an independent state, but it did create an institution which was a lot more than an ordinary public body and the reality is that it handed over power in a way which is similarly irreversible. But this reality has no statutory expression. On the face of the statute book, there is no indication that the Scottish Parliament is different in kind and nature from the Northern Lighthouse Board. (The courts of course understand the difference well: the Supreme Court judgment in the Axa case9 shows this clearly.) That was why the Labour Party devolution commission recommended declaratory legislation to put it far as possible beyond doubt that the Scottish Parliament was a permanent feature of the UK’s constitution. This was accepted by Smith and is now clause 1 of the Bill. It is sometimes objected that declaratory legislation is unnecessary and potentially confusing: legislation should create rights and obligations, rather than stating things to

8 Hart, 1961 9 Axa General Insurance Ltd & Ors v Lord Advocate & Ors (Scotland) [2011] UKSC 46

be true. But declaratory legislation is appropriate in the constitutional sphere, especially in the absence of a codified constitution. It is precedented in the case of Northern Ireland, whose status as part of the UK, subject to a vote of the population, was declared in legislation as long ago as 1973.The particular wording of the clause has attracted some comment: rather than simply declare the Scottish Parliament to be permanent, the clause says that it is “recognised" as permanent. This drafting has attractions. It implies that the permanence of the Parliament has sources other than the statute passed by Westminster. This of course is true: the reality is that the Parliament is entrenched in the constitution by the referendum vote of the Scottish people in 1997. Clause 1 should not be amended, as some have argued, to remove the words “recognised as”: before “permanent” as that would weaken rather then strengthen the protection afforded to devolution. A footnote to the drafting of the clause is that it declares not just the Scottish Parliament permanent but the Scottish government too. This was at the insistence of the present SNP government, displaying an untypical lack of self-confidence. Since the government is a creature of the Parliament the declaration is hardly necessary, but does no harm. Its only real effect is to entrench the Westminster model of a division between Parliament and government further into the Scottish devolution settlement. The Sewel Convention In a federal constitution powers will be allocated to the different levels of government. Some may be shared, but each level of government will have legislative and executive powers which are its alone. Devolution works differently: executive power is firmly separated, but legislative power formally overlaps. The Scotland Act 1998 means an area not reserved is devolved: and ministerial powers in relation to a devolved matter are removed from UK ministers and reside with the Scottish government. By contrast, and again as a consequence of the doctrine of parliamentary sovereignty, Parliament at Westminster retains the capacity to legislate on devolved matters. Indeed the Scotland Act 1998 explicitly declares this to be so. In reality the exercise of this power is constrained by the operation of what has become known as the Sewel Convention: Parliament does not legislate on devolved matters without the consent of the devolved legislature. This proposition was enunciated by the Minister promoting the Scotland Act in the House of Lords (the now disgraced Lord Sewel) on the basis that the government hoped that a constitutional Convention would develop on this basis. In practice, a Convention has developed 10. Parliament at Westminster, under the guidance of successive governments, has been scrupulous in not passing legislation on devolved matters unless the Scottish Parliament was content. A great deal of legislation on devolved matters has in fact been enacted at Westminster, but always with devovled consent. This has been of great practical value: some legislation inevitably touches on both reserved and devolved matters, and coordinated changes can be made in a single piece of legislation. A practice once denounced by

10 This Convention is codified in the Memorandum of Understanding between governments, and was to be called the Legislative Consent Convention. The name Sewel has stuck, however.

nationalists in opposition is now routinely, and sensibly, used by them. Well-established intergovernmental arrangements involve the devolved administration in the preparation of such legislation, and the Scottish Parliament has developed procedures for scrutinising and debating it. But here again, statute is silent, except to assert the opposite applies: section 28 (7) of the Scotland Act 1998 explicitly confirms that the power of the UK Parliament to legislate for Scotland is not affected by that Act. Of course it must not be affected in relation to reserved matters, but the reality is that Westminster has ceded legislative authority on devolved issues to Holyrood. That is the effect of the Sewel Convention. Clause 2 of the Scotland Bill gives this statutory recognition. Here again the wording chosen is interesting: rather than constrain the powers of Parliament the clause “recognises” that they are constrained, in this case by Convention. As in clause 1, this is an appropriate recognition that there is more to the position of the Scottish Parliament than the black letter law of the Scotland Act. The Scotland Bill is silent on one aspect of the Sewel Convention which may require further consideration. It has become accepted as part of the operation of that Convention that legislation to amend the powers of the Scottish Parliament also requires that Parliament's consent. Changes to the Parliament's powers can be made by Order in Council under the Scotland Act 1998, and such Orders require the agreement of both the UK and Scottish Parliaments. By analogy it has been accepted since 1999 that primary legislation which changes the powers of the Parliament requires its consent also. This is of course analogous to the provision about the permanence of the Parliament. Reducing its powers without its consent would be inconsistent with the constitutional status of the institution. It would be better if the Convention that the Parliament’s powers are not amended without its consent were stated in the Clause 2 of the Bill as well. The electoral system and composition of the Scottish Parliament The Scottish Parliament was created in 1999 with a mixture of constituency and regional list MSPs. This was a political deal made in the Scottish Constitutional Convention before 1997. It was justified as creating a partly proportional system, so that a single chamber parliament could not be dominated by one party elected on first past the post only. The list system is not wholly proportional and has not always produced coalition or minority government as expected: 45% of the votes gained the SNP a substantial overall majority in 2011. The Scotland Bill now proposes to “repatriate" this aspect of the Scottish constitution by giving the Parliament power over its own electoral system and composition. No constraints are placed upon what electoral system might be used, nor on the number of constituencies, or size of the Parliament. Sensibly, however, the Bill introduces a super-majority rule, so that this constitutional legislation cannot be passed without the support of two-thirds of MSPs. It may however be worth considering whether, given that the Scottish Parliament will remain a single chamber legislature, the clause should rule out a Parliament based solely on first past the post. Parliament should consider whether to constrain the power to alter the devolved electoral system so that it cannot be used to introduce a wholly majoritarian electoral system into a single chamber parliament.

The right constitutional direction Broadly speaking, these provisions move the Scottish Parliament in the right constitutional direction. They make it more like a legislature in a federal system whose status is set out clearly in a written constitution. The Parliament is and is seen to be permanent. It is and is seen to be pre-eminent in its own legislative domain, just as the Scottish government is pre-eminent in its executive domain already. It has control over its own composition and electoral procedure, but in a way which is constrained as such constitutional changes are often constrained. Two amendments should be considered. First, should the wider application of the Sewel Convention to legislation amending the powers of the Parliament not also be given statutory expression? And second, should the possibility of a Parliament elected only on first past the post system be ruled out? This aspect of the Scotland Bill moves Scotland's territorial constitution on in a helpful and constructive way. But it does not do the same for the territorial constitution of the UK as a whole. That is discussed later in this paper.

3: Sharing Taxes - the Fiscal Provisions of the Scotland Bill The clauses of the Scotland Bill dealing with taxes are predictable. The major structural problem of devolution, as identified by Calman, was the absence of fiscal power and accountability, and Calman's remedy in the Scotland Act 2012 comes into effect substantially in just over 6 months time. After the referendum there was scope to go further down this road, and this is what the clauses provide for. The issues which this part of the Bill raises are mostly about what is not in it, rather than what is. Devolved and assigned taxes in the Bill: income tax The major change in the Bill is the virtually complete devolution of income tax. Although Smith claimed this meant income tax would remain a shared tax as in the Calman model, this is stretching the description. The extent of sharing is idiosyncratic, and the UK government will no longer readily have recourse to the income tax base in Scotland to raise revenue. As in Calman, income tax on savings and dividends remains reserved, for largely practical reasons. Most such taxpayers are bank account holders receiving interest, often small sums, and the administrative burden of allocating this to one or other jurisdiction would be disproportionate. The UK will retain the definition of income, so the same things will be taxable, or able to be set against tax, across the whole country: this matters for pensions tax relief, for example. It will also retain control of the personal allowance, the starting point for income tax. This emerged from politics at the time of Smith: the Conservatives and Liberal Democrats saw the increased personal allowance as a coalition political achievement to preserve. As the Scottish government will be able to set the bands and rates of income tax (and so can set a zero rated band), they will effectively be able to increase but not decrease the starting point for income tax. But the big decisions about income tax taken annually –the rates of tax, and the number and boundaries of the bands of income to which these rates apply– will be the Scottish administration’s. This substantially increases the range of choices open to a Scottish government, and the consequent risks. Complete devolution of income tax is unusual internationally. In most federal countries, national, state and often local governments levy taxes on income11. Income is one of the largest and most buoyant sources of revenue, and the tax is very perceptible to taxpayers, making government directly accountable in a way which indirect taxes do not. It can be argued that there is another UK tax on income, employee national insurance contribution: but this is less perceptible, and because of its regressive structure more like a charge than a tax. Central governments worldwide turn to income tax in times of difficulty. For example it was centralised during the Second World War in both Australia and Canada; more recently it was to the top rates of income tax that the UK government turned to produce extra revenue after the financial crisis. In a veiled reference to income tax, Smith noted that there was nothing to stop the UK levying any tax it wanted; so in

11 The asymmetric tax regimes in the Basque country and Catalonia in Spain do however hand over complete responsibility for income tax to the sub-state government.

principle the UK could legislate in future to levy a supplementary income tax for reserved UK purposes in time of emergency or great need12. Additionally there may be scope to develop the salience of employee national insurance contributions further, as in effect a UK income tax. Minor Taxes The Bill also devolves two minor taxes: air passenger duty and aggregates levy. Both were recommended by Calman, but for different reasons not taken forward. There has clearly been concern from airport interests in the North of England about the risk of tax competition from Scottish airports undermining their position. This might be possible, but it would be an unwise Scottish government which entered into a tax-cutting competition on air travel with the UK. The duty is already geographically variable, and it would cost the UK little to reduce it further in northern airports only. VAT Assignment Provision is also made to assign to the Scottish budget half of the yield of value added tax in Scotland, 10 percentage points. Under European law, VAT cannot be devolved and this approach, recommended in the Conservative party’s devolution commission, was seen as a (second best) way of increasing the “own resources" proportion of the Scottish Parliament’s budget. Assignment of revenues is seen in some federal states, notably Germany, but it was rejected by Calman as importing risk into the Scottish budget without giving the Scottish government tools to manage that risk by changing the tax rate13. Assigning VAT certainly links the budget of the Scottish Parliament more firmly to the Scottish economy's success, and less to so-called “vertical fiscal transfers" from the UK government, under Barnett. But that means more risk. Apart from risk, the main issue is how this yield is to be calculated. It is currently estimated by the Scottish government for the GERS publication, but proxy measures are used. The key idea of value added tax is that tax is charged on outputs, such as sales, but the tax payable is offset by the value added tax paid on inputs, such as materials. In a large business, these transactions might well take place in different parts of the UK. Getting the amount of the tax exactly right in the first place matters less than ensuring that whatever proxies are used move in line with relative movements and the Scottish and UK economies. This will be an important part of the so-called “fiscal framework" for the new legislation, discussed below. The overall effect of the tax provisions It cannot be gainsaid that this degree of tax devolution and assignment under the Scotland Bill substantially addresses the main structural problem of devolution discussed in section 1 of this paper: the Scottish Parliament will have big tax powers.

12 The same effect could be achieved indirectly and rather opaquely by increasing expenditure on reserved issues, at the expense of rUK comparable programs, which could then be supported by increased rUK income tax, and would require Scotland to increase its income tax or reduce spending. 13 Calman’s one foray into tax assignment, of a share of income tax on savings and dividends, was rejected by the government of the time, and not revived by Smith.)

UK ministers are not wrong to say it is as a result one of the most powerful sub-state parliaments in the world. Fiscal decentralisation can be measured in two dimensions: the proportion of spending and the proportion of taxation which belong to the devolved administration. (As in McLean, Gallagher and Lodge, 2014, figure 4.1). Under Smith, Scotland will stand comparison with the most decentralised systems in the world, with around 40% of tax devolved or assigned, and over 60% of public expenditure devolved. (The precise percentages vary from year to year as the mix of taxes and spending change.) On the face of it this is not quite as devolved a Canadian province, but more than a Swiss Canton. As has been pointed out the extent of tax devolution varies in detail. But so does the extent of earmarking, or hypothecation, of fiscal transfers from central government: in Canada, for example, they are partially earmarked for health provision. In the US, fiscal transfers to states are invariably heavily conditional. In Scotland no strings at all are attached. So on any reasonable view the Smith package produces one of the most decentralised systems in the world. There is no magic number for the proportion of the devolved expenditure which should be met by devolved taxation, but one criticism of the Smith process is that its aim was to find a bundle of taxes which made that number as big as possible, rather than to get to the right number. There are good reasons of principle for having a mixture of “own resources" and “shared resources" from UK funding. It cannot be all “own resources”, nor should it simply be an allocation of national resources shared out by central government. Funding solely through “own resources” creates two problems, of principle and of economic management, discussed below under “full fiscal autonomy”. Conversely, funding only through national allocations removes from sub-state governments both accountability and the fiscal incentives to promote economic growth. The balance depends how much difference in living conditions is regarded as tolerable across the state. The USA is willing to tolerate a lot. Australia much less. Canada is in the middle. The UK is edging towards Canada, at least so far as Scotland is concerned. It would however be desirable for the UK to have a principled view on this, as it is a key aspect of the fiscal part of the territorial constitution which the country needs. The alternatives: fiscal autonomy, further tax devolution Although it would be entirely possible to rest for a period on the level of tax devolution in the Scotland Act 2012, most criticism of the Scotland Bill has been from SNP members saying it does not go far enough. The policy of the SNP appears to be full fiscal autonomy, though it is not clear that this is an immediate or concrete proposition. The idea is that Scotland should be responsible for raising all of its own taxes, and should make a fiscal transfer to the UK government to cover common services such as defence. This is wrong in principle for any part of a country, and would be catastrophic for Scotland in practice. It is wrong in principle as it would mean that the public services available in a particular part of the country depended solely on the taxable resources available there. So a rich area could have generous public services, and a poor area poor ones. But their needs might well be exactly the opposite. The second is a problem of economic management. An area with economic problems would find its

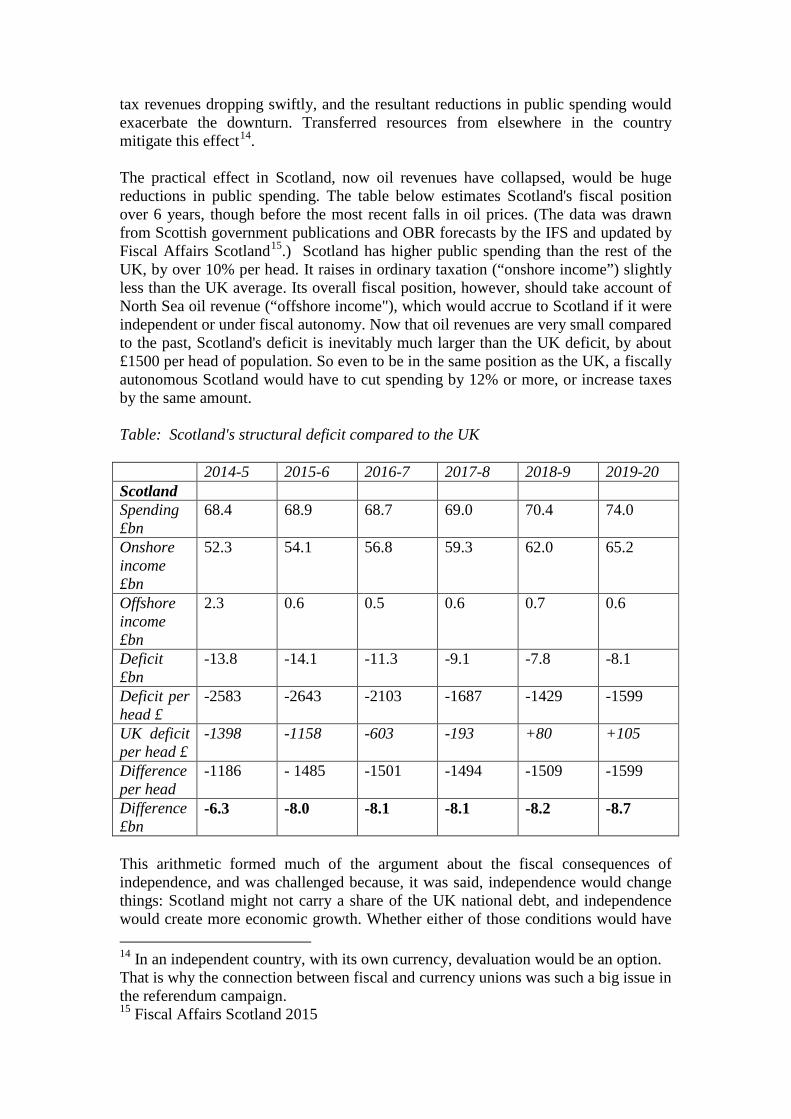

tax revenues dropping swiftly, and the resultant reductions in public spending would exacerbate the downturn. Transferred resources from elsewhere in the country mitigate this effect14. The practical effect in Scotland, now oil revenues have collapsed, would be huge reductions in public spending. The table below estimates Scotland's fiscal position over 6 years, though before the most recent falls in oil prices. (The data was drawn from Scottish government publications and OBR forecasts by the IFS and updated by Fiscal Affairs Scotland15.) Scotland has higher public spending than the rest of the UK, by over 10% per head. It raises in ordinary taxation (“onshore income”) slightly less than the UK average. Its overall fiscal position, however, should take account of North Sea oil revenue (“offshore income"), which would accrue to Scotland if it were independent or under fiscal autonomy. Now that oil revenues are very small compared to the past, Scotland's deficit is inevitably much larger than the UK deficit, by about £1500 per head of population. So even to be in the same position as the UK, a fiscally autonomous Scotland would have to cut spending by 12% or more, or increase taxes by the same amount. Table: Scotland's structural deficit compared to the UK 2014-5 2015-6 2016-7 2017-8 2018-9 2019-20 Scotland Spending £bn

68.4 68.9 68.7 69.0 70.4 74.0

Onshore income £bn

52.3 54.1 56.8 59.3 62.0 65.2

Offshore income £bn

2.3 0.6 0.5 0.6 0.7 0.6

Deficit £bn

-13.8 -14.1 -11.3 -9.1 -7.8 -8.1

Deficit per head £

-2583 -2643 -2103 -1687 -1429 -1599

UK deficit per head £

-1398 -1158 -603 -193 +80 +105

Difference per head

-1186 - 1485 -1501 -1494 -1509 -1599

Difference £bn

-6.3 -8.0 -8.1 -8.1 -8.2 -8.7

This arithmetic formed much of the argument about the fiscal consequences of independence, and was challenged because, it was said, independence would change things: Scotland might not carry a share of the UK national debt, and independence would create more economic growth. Whether either of those conditions would have 14 In an independent country, with its own currency, devaluation would be an option. That is why the connection between fiscal and currency unions was such a big issue in the referendum campaign. 15 Fiscal Affairs Scotland 2015

applied under independence is distinctly arguable: but they certainly do not both pertain under fiscal autonomy. It will be the inexorability of this arithmetic which has blunted the SNP's enthusiasm for full fiscal autonomy, but the Scottish government seek, as a down payment, devolution of employers national insurance contributions and corporation tax (notably, not oil revenues). There is a strong argument against devolving employer's national insurance contributions. Equivalent taxes are not devolved even in the most decentralised systems, including under so-called full fiscal autonomy in the Basque country. That is because they are in the nature of insurance payments, creating an entitlement to contributory welfare benefits, which will remain reserved. The case of corporation tax is not so clear-cut. The UK government has made proposals to devolve it to Northern Ireland, which faces very direct competition from the low corporation tax rates in the Republic. The problem is of course tax “stealing", when one place sets low tax rates and companies use accounting devices to locate profits there, even if the economic activity is really elsewhere. The scheme which the UK government has devised is said to avoid the risk that profits will be artificially relocated to Northern Ireland from elsewhere in the UK. But this plan has not been put into practice, because it is connected with other issues in Northern Ireland. If it is ever implemented, and if the scheme is successful in avoiding tax stealing, there may be a case for income tax devolution to Scotland and Wales also. Wales’ case is the stronger, as it is in greater need of an additional instrument of regional economic development.16 Unanswered questions: the fiscal framework The phrase “fiscal framework" means the set of decisions which will have to be taken consequent on tax and welfare devolution. The Barnett formula remains at the heart of the system for setting the Scottish budget, as promised in the referendum campaign. So one (over) simple way of looking at this framework is as a series of deductions from and a series of additions to the grant which would otherwise be paid under Barnett. The deductions are to take account of the stream of tax revenue accruing to the devolved administration; the additions take account of the new welfare responsibilities for which Barnett may not be apt. Calculating the initial deduction to the made for the new tax income is in principle straightforward: it should equal the first year's revenue. The formula which is then used to update this should ensure that the risks to the revenue stream are properly allocated. This is the only substance of the much hyped “no detriment" principle. If the UK, for example, takes a policy decision which affects the revenue stream (changing the definition of income, changing the personal allowance), then it should bear the consequences of that for grant. But the economic risks from population or income growth should be transferred to the Scottish government. This issue has already been dealt under the Scotland Act 2012, for income tax and two minor taxes, so it should be relatively easy to extend: indexing to the comparable growth in the

16 Of course the devolved administrations already have power to support business by reducing the business rate. In Scotland it has been increased every year since 2007.

English income tax base is an obvious solution. The fiscal framework for new welfare responsibilities is not well precedented. Previous transfers of responsibility (e.g. for railways) have involved moving departmental expenditure from a UK to a Scottish budget (and hence the remainder to comparable rUK budgets) so that the Barnett formula can readily be applied. Welfare expenditure does not sit within departmental expenditure limits set in three-year cycles, but is rather “annually managed”, as the expenditure is demand driven. That puts it outside the boundary of the Barnett formula. Perhaps a variant of Barnett could be applied, but it might be that a form of indexation to projected levels of spending on comparable English benefits could be devised. At present, these issues are locked in private negotiations between the two governments. This is understandable. There are, despite political differences, good working relations and financial issues are normally hammered out in private ministerial discussions. The risk with this approach, however, is that a deal will be done behind closed doors and then presented as a fait accompli. The fiscal framework for the Scotland Bill needs to be seen as rather more than a series of technical adjustments to the Barnett formula to be done in a private deal between governments. The complete devolution of income tax in particular means that a more strategic look at the way in which tax and spending is managed territorially in the UK is necessary. Income tax is to become a Scottish tax. The inevitable consequence is that income tax becomes an England, Wales and Northern Ireland tax also. Scottish income tax will be used to fund Scottish devolved spending only. Changes in Scotland's income tax will result only in changes in Scottish devolved spending. It follows that changes in UK income tax should result only in changes in UK spending. If the people of England, say, are asked to pay more income tax, they may ask whether this is going to provide additional services, devolved or reserved, in Scotland. It is not easy to see how this can be achieved. Since 1999 council tax and non-domestic rates have been completely devolved. Both can be directly linked to territorial spending, as both support local government expenditure. So changes in them can be linked to changes in spending in England or Wales. (Council tax is completely insulated from the Barnett formula. Nondomestic rates really should be17.) But this doesn't work for income tax, which doesn't just support council spending. A deduction from Barnett indexed to rUK income tax may insulate Scottish devolved spending from changes in English income tax, but not reserved spending. In the absence of an English or rUK spending budget, it is not clear whether or how this can be fully achieved or shown. It will not be enough to see the fiscal framework simply as a private agreement on adjustments to the Barnett formula between two governments. It is much more than that, and needs to be exposed for debate for its effect on the whole UK during the passage of this Bill.

17 The way in which the Treasury have dealt with it in the Barnett calculation as done that to be unexpectedly advantageous to Scotland, according to the IFS, to the tune of £600 million a year (IFS 2014).

Voting on income tax This unsolved problem in the fiscal framework is connected to the other big issue thrown up by the Scotland Bill. If income tax is devolved, should Scottish MPs voted on it for the rest of the UK? This is the West Lothian question, this time with real teeth. The Bill is silent on this, but the government has not been18. Their proposals for “English votes" would apply to income tax as well as ordinary legislation. It is for a so-called double majority. Both English (or for income tax English, Welsh and Northern Irish) MPs and all MPs have to support a measure for it to pass. An earlier paper in this series 19 identified the flaws in this approach. The major structural problem is that, as income tax is renewed on an annual basis, both groups of MPs would have to vote in favour of it each year. So a subset of MPs could hold the government to ransom over its budget; income tax makes up a quarter of revenue. The second flaw relates to the fiscal framework. If there were to be a purely English (or rUK) vote on income tax there would have to be a similar vote on English (rUK) spending. Otherwise MPs would be taking tax decisions but having no responsibility for the spending consequences. But the is no such spending programme or budget. As ministers have said, all MPs vote on the estimates. But if all MPs vote on the estimates, they are making spending decisions without having control over the revenue. This is at best a muddle. In fact the Smith Commission asserted that the devolution of income tax should not affect the rights of MPs to vote on the budget: rightly. The interconnected nature of the UK territorial finances means that the government’s spending decisions and its taxing decisions have to be considered as a package. (If all MPs decide total spending, and all non-devolved taxes, they are by subtraction, ignoring borrowing, also deciding the amount to the raised by the UK in taxes which are devolved.) This muddle needs to be sorted out, but given the complete devolution of income tax there is no obvious way to do so, short of creating an English budget, government and Parliament, which would be the end of the UK. The government's proposals for a double majority vote on income tax are unworkable, and they could render England and perhaps the whole UK ungovernable in some circumstances. No UK government without an English majority could accept them, and so they do not solve the West Lothian question. Nor do they work in practice in the absence of an rUK spending programme to match an rUK tax decision. The government's approach has been partisan rather than constitutional, and the English Votes plans need further consideration.

18 Cabinet Office, 2015 19 Gallagher, 2015

4: Sharing Welfare - the Benefits Provisions of the Scotland Bill The Scotland Bill extends the competence of the Scottish Parliament and government into welfare in new and unexpected ways. These provisions are the most radical parts of the Bill, but they emerged straight from the Smith process, with little previous research, analysis or debate. They deserve more careful scrutiny than they are getting. A welfare state? One of the arguments made for Scotland’s remaining in the United Kingdom was that the UK was a social union, a single welfare state across which risks were pooled and shared. Thus old-age pensions, or unemployment benefit, did not depend on whether Scotland alone could afford them, but rather whether the entire UK could. So the risks of demography, or asymmetric economic shocks, are not borne by Scotland alone. This is common in federal countries: social security is almost invariably a federal rather than a state or provincial function, and there are good reasons why. The federal level is able to command more resources, and spread risk more widely. So the devolution settlement for Scotland (and Wales, but not Northern Ireland20) has always excluded pensions and other forms of social security. In part this is historical accident. Devolved powers were built on the powers of administrative devolution, and these never included social security. But in part it is principled: redistributive welfare was seen as a function of the UK government, alongside redistributive taxation. Distributive welfare, on the other hand, the provision of services like health and education, was seen as suitable for devolution. To the extent that cash payments are part of an insurance system, this is easy to justify by the size of the insurance pool: the more risk is shared, the more certain the level of payouts will be. In administrative terms, uniform benefit payouts across the territory are consistent with a central administrative system: whereas the operation and management of services inevitably has to be tailored to local circumstances and requires at least their administration to be decentralised. The Calman Commission did its best to make sense of this, seeing the social union as part of the glue which held the UK together: membership of the UK guaranteed certain minimum social provision, such as old-age pensions. Calman suggested there should also be agreed underlying principles for distributive welfare as well as uniform redistributive welfare: despite devolution, for example, there might be a common UK guarantee of healthcare free at the point of need. No UK government pursued that idea, as no SNP administration would agree to UK principles in relation to health or education, almost whatever those principles were. Calman did recommend however that the social fund (various discretionary payments to benefit recipients) be devolved and this has now been put into effect. It suggested that there should be scope for a variation in Housing and Council Tax Benefits, but these suggestions were rejected. Today, as part of the UK government's changes to local government finance, Council Tax Benefit has already been devolved as well. Now however the Scotland Bill will

20 NI welfare devolution has historical roots, going back to before 1923; but it is largely formal as the UK government covers only the cost of benefits paid at UK levels.

devolve a number of social security benefits, to introduce a power of top up, and widen the power of discretionary payments markedly. Where these ideas come from These plans have their roots in two of the three devolution commissions set up by the main UK parties in the run-up to the referendum. Mainly they concentrated on tax, but all had something to say about social security. The Labour Party emphasised the benefits of the social union, but recommended devolving Housing Benefit and Attendance Allowance, as both were cash benefits closely linked to support provided directly in the form of housing or personal care. The Conservative Party made no firm recommendations; they thought there “was a case for" devolving Housing Benefit and Attendance Allowance, and for the idea of a general power of top up. In the hurried negotiations of the Smith Commission, the bundle of devolved powers increased markedly, on no obviously principled basis. This was carried forward into the draft legislation produced by ministers before the general election, and, somewhat adjusted, is now in the Bill before Parliament. These proposals have not, therefore, been subject to the level of preparatory scrutiny or consideration that would be normal in constitutional legislation. Questions of principle It is understandable that nationalist ministers will seek as many powers as they can get, but the UK government, and pro-union parties, need to be clear about the basis of principle on which powers are devolved or reserved. If Scotland is to remain in the UK, it must continue to share economic and demographic risks. If it does not do so, it will be carrying risks which it would find challenging to manage even as an independent state, but without such additional powers as independence would offer. (Scotland is not Greece: but if the EU were a social union, then Greek old-age pensions would not be being slashed because the Greek economy is struggling.) On the other hand, it is entirely justifiable to argue that the purpose of devolution is to give Scotland the scope to operate a different social model from the rest of the UK if that is what people in Scotland want, and welfare benefits are clearly a big part of that model. There are in principle two different ways in which this might be done. Significant benefits applying to large numbers of people might be devolved, so that through a combination of devolved services and benefit choices the Scottish social offering could be more, or less, generous than the UK standard. That is the model of devolution for services, so that, at least in principle, Scotland could decide to move to a private, insurance-based system of health care spending less public money, or alternatively choose to spend more on the NHS. If a benefit, say Housing Benefit, were completely devolved, the same range of options would be open. Alternatively, there is the approach of regarding UK welfare as a basic entitlement, but giving the Scottish government the power to supplement it, but not to reduce it. The first of these approaches give Scotland more flexibility (benefits can be higher or lower) but the second insulates it more successfully from asymmetric economic risk. (If demand for benefits goes up because of economic or demographic circumstances, most of that risk is borne by the UK, and only the effect on the Scottish top up cost is borne by the Scottish government.)

This distinction seems to have escaped Smith completely: they cheerfully went for both approaches at the same time. A list of benefits, almost none of which had been discussed in advance of the Commission's work, was chosen for a complete devolution. A general top power was introduced, together with the power to make discretionary payments, and to set the housing element of universal credit and to determine the frequency of universal credit payments. (The last two deal with current political challenges in the social security field: the ‘bedroom tax’ and the move to monthly benefit payment.) Individual benefits to be devolved The list of devolved the benefits to be devolved completely was negotiated around the Smith table. It comprises Disability Benefits, Carers’ Benefits, Industrial Injury Benefits, Maternity Benefits, Funeral Benefits and cold weather payments. The individual benefits appear to have been chosen for devolution on the principle that the Department of Work and Pensions was unwilling to die in a ditch to keep them. They are however very important to many individuals, notably Disability Living Allowance and its successor Personal Independence Payments, and Attendance Allowance, which many older people receive. It is possible to see some connection between devolved responsibilities for social work services for disabled and elderly people and some of these benefits. One risk has however been avoided. Demand for these benefits is not closely related to the economic cycle (they are determined by the personal circumstances of individuals rather than the state of the economy) so devolving them does not appear to import cyclical risk into the Scottish budget. If this list is taken as given, then the main issue which arises relates not to the legislation itself, but to its financial consequences. The total annual bill for the benefits to be devolved is put at £2.5 billion, but the UK government's planned reductions in welfare spending will affect that, potentially substantially, and that planned reduction will have to be carried across into the resources transferred to the Scottish government, under way in which the resource transfer is updated. (Otherwise, the Scottish government will be able to sustain the present more generous levels of benefit, but the price would be paid by UK not Scottish taxpayers.) At the moment the Barnett formula has this effect: if the UK makes reductions in comparable service spending, Scottish devolved funding is reduced per capita. In principle Barnett or something like it might be applied to spending on each individual benefit. But it may be simpler to index the amount transferred on day one to UK spend on the same or analogous benefits. As with tax, the key is to agree in principle which risks are borne by which government. The policy risk of more or less generous benefits should be borne by those making the policy decision. The Scottish government should also take the risk of relatively less or greater demand for these benefits in future (otherwise it has an incentive to widen eligibility, at the expense of the rest of the UK). The top up approach The Smith negotiations produced, not quite out of nowhere, a general power from the Scottish government to top up UK benefits. The Conservative Party’s Strathclyde Commission suggested that there “might be a case” for this, but no detailed work been

done on the idea by either the UK or Scottish governments beforehand. The relevant clause in the Scotland Bill confers on the Scottish Parliament legislative authority to provide for supplements to reserved benefits. This appears to apply to every reserved benefit, from the old-age pension to tax credits (which are technically speaking a benefit) and universal credit. (Given that, it is not immediately clear why the Scottish government also need power to set the housing element of universal credit.) The Bill also widens the powers under which the Scottish government operates the social fund, to make “discretionary payments" to any classes of person, whether or not they are getting a reserved benefit. This is achieved by giving the Scottish Parliament the power to legislate in this area, and with that will come the power for Scottish ministers to take executive action in pursuit of the legislation. The drafting is necessarily somewhat convoluted: benefits payments in general remain a reserved area, but legislating to provide for top ups to reserved benefits becomes an exception to that reservation. This is the approach that was taken in the Scotland Act 2012 to make the operation of the social fund an exception to the general reservation of benefits. Any executive powers to make payments under top up legislation would then fall to the Scottish government, but it seems likely that they would want to negotiate with the UK government to make the payments on their behalf. This could be done by an agency agreement under the existing powers in the Scotland Act 1998. The UK government is however under no obligation to administer any top up, and the Scottish government could choose to administer it themselves, or via local authorities. Tax credits are something of an exception. Employers pay them out alongside wages, and it seems likely that the devolved legislation could require them to administer a Scottish tax credit top up, but HMRC could not be compelled to play their part in the top up system unless they agreed to do so, again presumably as a “government department" with whom the Scottish government could make an agency agreement. The detail of the provisions Acts of Parliament do not have casual readers: but if there were any, they might be puzzled why the welfare provisions take the shape they do. The clauses devolving individual benefits are relatively straightforward. Relatively, because they too have to proceed by making exceptions to the generally reserved matter of social security. This will create an area which the Scottish Parliament can legislate (say for example for for maternity benefits) making this aspect of Scottish devolution rather more like the conferred powers model in the present Welsh legislation. The Scottish government appear to have reservations about whether the capacity of the Scottish Parliament to legislate is constrained merely to amending rather than replacing the devolved benefits. There seems little substance to that worry, as the example of the Welsh conferred powers model (for all its disadvantages) shows: legislation which relates to a devolved matter will be within the powers of the Parliament, and, e.g., maternity benefits will by virtue of this Bill be a devolved matter. (The Supreme Court case dealing with agricultural wages in Wales makes this clear21.)

21 Agricultural Sector (Wales) Bill [2014] UKSC 43

The clause dealing with top up powers is more puzzling. The sidenote refers to them as “discretionary" and “top up". But the clause itself uses neither word. Instead it has a quite elaborate definition of what a top-up might be for someone getting a reserved benefit. The use of the word “discretionary" is significant, and misleading. If the Scottish Parliament legislates to create a scheme of top ups for, say, jobseekers allowance, this will not be “discretionary" in the sense in which social security legislation uses that word. It will be a new, Scottish, entitlement. In DWP-speak “discretionary" means something other than an entitlement, as in the social fund. The Bill should be amended to place it beyond doubt that top up payments will create new Scottish entitlements, and are not “discretionary" in the sense that the social fund is. A separate clause deals with Scottish schemes of discretionary payments. This extends the existing devolution of the social fund in quite wide ways. Wide, but not wide enough. In essence, the first main clause gives the Scottish Parliament power to top up existing UK benefits. This clause gives a Scottish Parliament the power to legislate not according to existing benefits, but according to need: by classes of people rather than classes of benefit. Unfortunately, it is then constrained by requiring the need to be “short-term". (Other constraints on this have been sensibly dropped by the UK government.) That is intended to preserve the general social security reservation, which is right in principle. Otherwise, it might be argued, since the Scottish Parliament has the power to legislate to make payments in respect of any need at all, it has complete power over social security, and the UK Parliament will be unable to legislate to create new benefits for Scotland. That of course cannot be right: but constraining the payments to meet only short-term fails meet the objective of the legislation, and of course provides another opportunity for manufactured grievance. In effect the legislation is saying that the Scottish Parliament cannot legislate to meet needs not otherwise met because at some future date Parliament at Westminster might want to legislate in that area, and would be prevented from doing so as the matter was devolved. This is in part simply a technical challenge for parliamentary counsel. The policy objective is reasonably clear: the Bill must be amended to make it clear that the Scottish Parliament is able to meet needs not covered by reserved benefits at all, but the UK Parliament cannot be prevented from meeting them on a UK basis as a result. But it shows how in this area, unlike other devolved matters, we are looking at both legislatures and executives which will have some concurrent power over the same area. It might, for example, be that the Scottish Parliament would have power to legislate to meet any need not met by a reserved benefit, at present or in future. In the event then that the Scottish Parliament has legislated on some matter for Scotland and future Westminster legislation seeks to meet the same need on a UK basis, then agreement would have to be made so that the UK could legislate and meet these bills for Scotland. What this means for devolution It's clear that the strategic purpose of this part of the Bill is to put the Scottish Parliament and government in the place that, if they are willing to pay for it, they can have a more generous social security system than the UK provision. The politics of