may untapped export 2017 potential of pakistan · untapped export potential of pakistan may 2017....

TRANSCRIPT

THE LAHORE CHAMBEROF COMMERCE & INDUSTRY

w w w . l c c i . c o m

Untapped Export Untapped Export Potential of PakistanPotential of Pakistan

Untapped Export Potential of Pakistan

MAY

2017

Quaid-e-Azam Muhammad Ali JinnahFounder of Pakistan

1

Mamnoon HussainPresident of Pakistan

2

Muhammad Nawaz SharifPrime Minister of Pakistan

3

Mohammad Ishaq Dar Federal Minister for Finance

4

Khurram Dastgir KhanCommerce Minister of Pakistan

5

Muhammad Shahbaz SharifChief Minister of Punjab

6

Abdul BasitPresident

The Lahore Chamber of Commerce & Industry

7

Amjad Ali JawaSenior Vice President, LCCI

Muhammad Nasir HameedVice President, LCCI

8

FOREWORD

Pakistan's economy is back on the path of recovery ever since Prime Minister Nawaz Sharif's Government

took over in May 2013. The environment in which the economy is opera�ng may not be ideal but it

remains pre�y much conducive for growth. Cost of capital is at its historic low as infla�on remains low,

investment is increasing, public development spending is rising, energy shortages for the industry have

considerably been reduced as is indicated by a pick-up in large-scale manufacturing (LSM) and the country

is expected to have surplus power once the new genera�on plants being set up under the $57bn China

Pakistan Economic Corridor (CPEC) come on line over the next couple of years.

There is evidence that the investors' confidence has improved on the back of macroeconomic stability

and improved security condi�ons in the wake of the military's opera�on against militants as reflected by

capacity expansion plans of a number of industries. Foreign direct investment (FDI), especially from China

under the Corridor ini�a�ve and from elsewhere in construc�on-allied, power, automobile and food

industries, is also showing signs of improvement. Turkish and European investors have recently acquired

Pakistani food and white goods companies. Several industries like cement, steel, beverages, and

automobiles are inves�ng in capacity expansion.

Indeed, the present recovery is primarily a�ributable to macroeconomic reforms that have helped the

government control fiscal deficit at a manageable level and stabilize external sector. Yet the modest

economic recovery seen in the recent years remains fragile. The gross domes�c product (GDP) grew by

4.7 per cent last financial year and is targeted to increase by 5.0 per cent this year. But this is not enough to

create new jobs in the economy to accommodate around two million people entering the job market

every year.

Growth is driven mainly by domes�c consump�on, which contributed over 7.0 per cent to GDP last fiscal

year. Investment is surging but remains low, constraining GDP growth. The budget deficit has significantly

come down but risks remain as much of the economy con�nues to operate from the shadows and the tax-

to-GDP rate of 11 per cent is one of the lowest in the world. Coupled with rising development spending

and security related expenditure, the decline in revenue collec�on has led fiscal deficit to widen by 0.7 per

cent of GDP in the first half of the ongoing financial year compared with the last year. Going forward,

lower-than-expected growth in tax revenues could undermine the government's efforts to keep the fiscal

deficit at the targeted level and at the same �me increase the development spending, according to the

State Bank of Pakistan (SBP).

More important, the external sector, which is stable for now, is fast coming under strain because its

recovery is mainly based on debt-crea�ng capital inflows rather than on exports. The SBP, for example,

9

has in its report on the country's State of the Economy for the first half of 2016/2017 admi�ed to the fact

that the current account deficit has almost doubled from a year earlier because of delayed realiza�on of

Coali�on Support Fund (CSF) from the United States, decline in the exports and a surge in the imports.

“From the external sector stability standpoint, such increase in the current account deficit does not bode

well, par�cularly in view of the bo�oming out of global commodity prices, especially oil prices, along with

some shi�s in the interna�onal capital markets due to rise in the US interest rates,” the bank had stated in

the report.

No doubt the surge in imports is mainly concentrated in the growth-inducing capital goods for power,

tex�le, construc�on sectors, etc., and fuel and metals as pointed out by the SBP. It is but natural for

current account deficit to rise in a growing economy. But we need to contain this although the external

inflows in the country have been sufficient to finance the current account deficit so far, and the current

SBP foreign exchange reserves are enough to pay the import bill of more than five months.

The challenges facing the external account need to be addressed to sustain the present macroeconomic

stability and move towards low infla�on-high growth balance. In addi�on to boos�ng private foreign

investment and contain imports to keep the overall import bill manageable, Pakistan must boost its

exports by improving the industry's compe��veness in the world markets. In par�cular, there is a need to

further reduce cost of doing business, enhance produc�vity, and remove structural impediments in the

export sector, as pointed out by the SBP. Unless we are able to diversify our exports and markets, we will

con�nue to be dependent on foreign debt to pay our import bill. The situa�on may worsen going forward

as the workers' remi�ances are showing signs of stagna�on at best and decline at the worst.

Pakistan has a lot of poten�al for becoming the manufacturing hub and export powerhouse. It is

strategically located with half of its 200 million people under the age of 30. With almost 2.0 million people

joining the labour force every year, we should devise policies to take advantage of this demographic

dividend as the workforce ages in China and other East Asian countries. The Lahore Chamber of

Commerce and Industry (LCCI) has always tried its best to bring home to the country's policymakers that

Pakistan could become a prosperous country and export powerhouse if a right set of policies is

implemented to help the manufacturing industry. This report is also another step in this direc�on. We

hope that the government will incorporate our sugges�ons in its budget for the next financial year to

exploit the country's economic poten�al for its people.

The report comprises three parts: a) an overview of the economy; b) Pakistan's export performance; and

c) proposals to boost the country's exports. We are hopeful that the proposals given in this report can help

Pakistan put its economy on a more sustainable growth path and achieve its true export poten�al.

(ABDUL BASIT)

President, Lahore Chamber of Commerce and Industry

May 2017

10

OVERVIEW OF THE ECONOMY

11

PART-I

OVERVIEW OF THE ECONOMY

Macroeconomy has stabilized under the PML-N Government. Ever since the Pakistan Muslim League-

Nawaz returned to power in May 2013, Pakistan's macroeconomic condi�ons have significantly improved

with the assistance of a three-year $6.7 billion loan under the Extended Fund Facility (EFF) programme of

the Interna�onal Monetary Fund (IMF), substan�al development assistance from other mul�lateral

lenders, rise in remi�ances, low global oil prices, debt raised from the interna�onal bond markets, surge

in private and official capital inflows under the $57 billion CPEC ini�a�ve and financial and economic

reforms undertaken to restructure the economy.

Fig 1: Global Oil Price since June 2013, Source: Bloomberg

Country 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

USA 1,735.87 1,771.19 2,068.67 2,334.47 2,186.24 2,467.65 2,702.7 2,524 U.K. 605.59 876.38 1,199.67 1,521.10 1,946.01 2,180.23 2,376.2 2,579 Saudi Arabia 1,559.56 1,917.66 2,670.07 3,687.00 4,104.73 4,729.43 5,630.4 5,968 U.A.E. 1,688.59 2,038.52 2,597.74 28,48.86 2,750.17 3,109.52 4,231.8 4,365 Other GCC Countries 1,202.65 1,237.86 1,306.18 1,495.00 1,607.88 1,860.03 2,173.0 2,422 EU Countries 247.66 252.21 354.76 364.79 357.37 431.85 364.1 417 Other Countries 771.51 812.08 1003.88 935.40 969.26 1,059.00 1,241.7 1194 Total 7,811.43 8,905.90 11,200.97 13,186.62 13,921.66 15837.71 18,719.8 19,916 Source: SBP.

Table 1: Country Wise Workers’ Remittances US$ Million

12

Emerging from a near-crisis in 2013, the authori�es have substan�ally reduced the near-term

vulnerabili�es. Helped by suppor�ve policies, low oil prices and strong remi�ances, the budget deficit

and infla�on have declined while foreign exchange stock has strengthened. The near-term economic

outlook is broadly favorable although structural bo�lenecks s�ll impede higher poten�al growth, the IMF

said in its various staff reports over the last one and a half year.

The stock market is booming, foreign exchange reserves are at their historic peak, Foreign Direct

Investment (FDI) has started to slightly pick up as energy and transport projects get under way under the

CPEC project, infla�on remains under control on low global oil, food and commodity prices. Twin deficits –

current account and fiscal – have substan�ally come down. Energy availability for the industry has

improved with the induc�on of new power genera�on capacity and import of LNG.

The overall domes�c economic ac�vi�es gained further momentum in the last three and a half years with

the improvement in the energy and security situa�on in the country. The GDP has grown at an average

annual rate of 4.3 per cent since the induc�on of the PML-N government, jumping to 4.7 per cent during

the financial year 2015/2016. It was the highest growth rate the country has achieved since 2007. The

growth achieved under the present government is much higher given the state of the economy it had

inherited from its predecessor.

Fig 2: Pakistan’s Stock Market movement since June 2013, Source Bloomberg

13

Present GDP growth rate is much be�er than the one under the previous government: The economy grew at an average annualized rate of under 3.0 per cent under the previous government of

the PPP between 2008 and 2013. The macroeconomic situa�on had already started to deteriorate long

before the PPP took over power in March 2008 in the a�ermath of a popular an�-Pervez Musharraf

movement launched by lawyers to protest the removal of Chief Jus�ce I�ikhar Mohammad Chaudhry,

massive increase in terrorist a�acks across the country and the murder of former Prime Minister Benazir

Bhu�o in a gun-and-bomb a�ack during an elec�on rally in Rawalpindi.

In the first four months of the financial year 2008/2009, the economic condi�ons started deteriora�ng

fast owing to adverse security developments, large exogenous price shocks as global oil and food prices

shot through the roof and the world found itself in the midst of a severe financial turmoil. The failure of

the then government to take appropriate measures and policy inac�on led the country's stock markets to

collapse, infla�on to skyrocket, fiscal deficit to balloon, foreign exchange reserves to deplete to a

dangerously low level and current account deficit to widen substan�ally. The country verged on

bankruptcy before the IMF agreed to provide $11.6 billion loan to calm the markets and restore investors'

confidence in the country's economy. The economy achieved a rela�ve stability a�er the announcement

of the agreement with the IMF, but the government's failure to implement structural and tax reforms kept

growth subdued despite an increase in the workers' remi�ances and exports on the back of higher global

commodity prices.

Table 2: Comparison of Macroeconomic Indicators

2013-14

2015-16

GDP Growth

4.05%

4.71%

Infla�on

8.6%

2.9%

Current Account Deficit (As% of GDP)

1.3

1.1

Fiscal Deficit (As % of GDP)

8.2

4.3

FDI (net) (US$ Million) 1,700

1,921

Manufacturing Sector Growth Rate

5.6%

5.0%

Source: State Bank of Pakistan

14

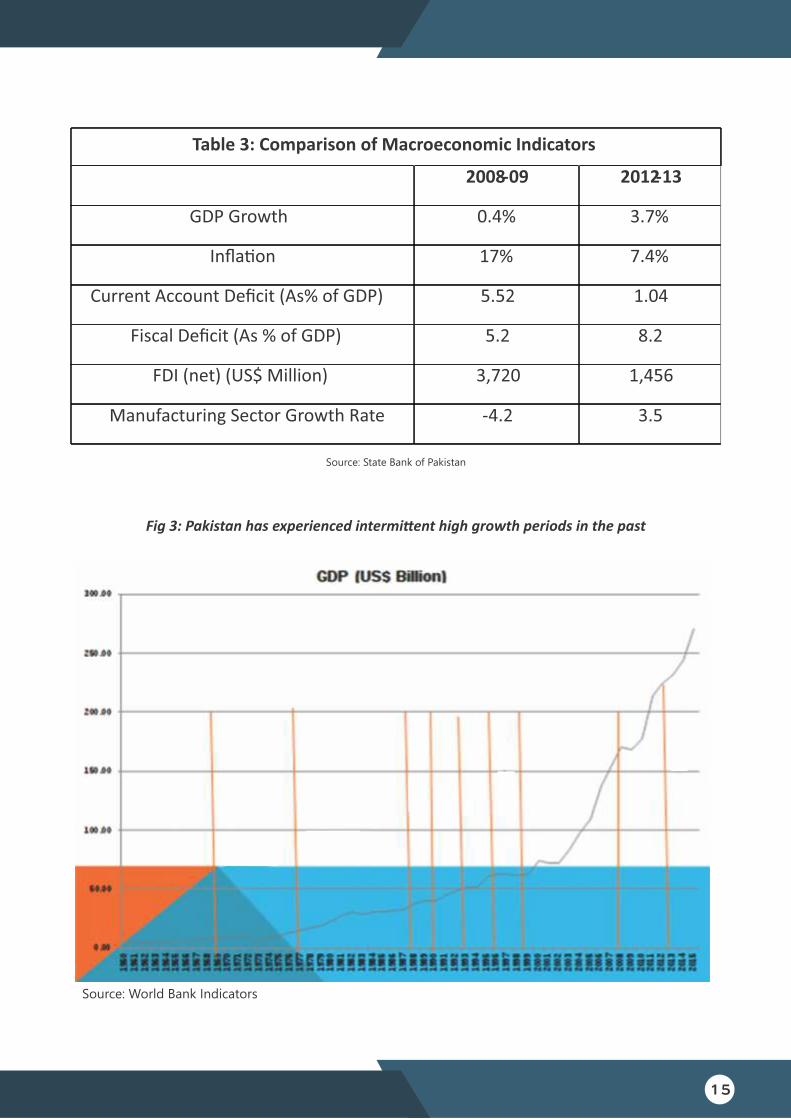

Table 3: Comparison of Macroeconomic Indicators

2008-09 2012-13

GDP Growth 0.4% 3.7%

Infla�on 17% 7.4%

Current Account Deficit (As% of GDP) 5.52 1.04

Fiscal Deficit (As % of GDP) 5.2 8.2

FDI (net) (US$ Million) 3,720 1,456

Manufacturing Sector Growth Rate -4.2 3.5

Source: State Bank of Pakistan

Source: World Bank Indicators

Fig 3: Pakistan has experienced intermi�ent high growth periods in the past

15

Pakistan's economy has grown at a fairly impressive rate of 6.0 per cent per annum through the first four

decades of the na�on's existence, according to Dr. Ishrat Hussain, the former SBP Governor. In spite of

rapid popula�on growth during this period, the country's per capita income doubled, infla�on remained

low and poverty declined from 46 per cent down to 18 per cent in the late 1980s. This strong economic

performance was maintained through several wars and successive civilian and military governments un�l

the decade of 1990s, now remembered as the lost decade.

In the 1990s, the economic growth plummeted to between 3.0 per cent and 4.0 per cent, poverty rose to

33 per cent, infla�on was in double digits and the foreign debt grew to nearly the en�re GDP of Pakistan.

In 1999 Pakistan's total public debt as percentage of GDP was the highest in South Asia – 99.3 per cent of

its GDP and 629 per cent of its revenue receipts compared with Sri Lanka (91.1 per cent and 528.3 per

cent, respec�vely, in 1998) and India (47.2 per cent and 384.9 per cent, respec�vely, in 1998). Internal

debt of Pakistan in 1999 was 45.6 per cent of GDP and 289.1 per cent of its revenue receipts compared

with Sri Lanka (45.7 per cent and 264.8 per cent, respec�vely, in 1998) and India (44 per cent and 358.4

per cent, respec�vely, in 1998).

A�er an economically stagnant decade, Pakistan was able to fuel growth and to double the size of its

economy in the 2000s on the back of generous loans from mul�lateral lenders like the IMF), the World

Bank, the Asian Development Bank (ADB), etc. The country also received massive financial assistance

from the United States and other Western countries as it joined the global war on terror following fateful

a�acks on the soil of the US on September 11, 2001.

Shortly, Pakistan became one of the four fastest growing economies in the Asian region with its growth

averaging 7.0 per cent per year for most of this period. As a result of strong economic growth, Pakistan

succeeded in halving poverty and crea�ng almost 13 million jobs. The country's debt burden was halved

and foreign exchange reserves rose to a comfortable posi�on, and, thus, propping the exchange rate and

restoring investors' confidence.

Pakistan's economy witnessed a major transforma�on in the 2000s. The country's real GDP increased

from $60 billion to $170 billion, with per capita income rising from under $500 to over $1000 during 2000

and 2007. The investment to GDP ra�o peaked to above 20 per cent and volume of interna�onal trade

increased from $20 billion to nearly $60 billion. The improved macroeconomic performance enabled

Pakistan to re-enter the interna�onal capital markets in the mid-2000s. Large capital inflows financed the

current account deficit and contributed to an increase in gross official reserves to $14.3 billion at end-June

2007. Buoyant output growth, low infla�on, and the government's social policies contributed to a

reduc�on in poverty and improvement in many social indicators.

FDI jumped to $5 billion in 2007 and the workers' remi�ances shot up to a new level from less than a

16

billion in 2000 as foreign governments slapped strict restric�ons on hundi and hawala – informal money

transfer business – transac�ons to eliminate money laundering and plug sources of funding for terrorist

organiza�ons. Riding on high growth trajectory, the government ended the IMF Programme prematurely.

But several studies have established that foreign capital inflows – whether in the form of assistance or

grants, loans, or private investment – have played a major role in maintaining macroeconomic stability

and spurring growth rate in Pakistan since 1950s because of very low domes�c savings and investment

rates, as well as small size of exports. These show that inflow and ou�low of a few hundred millions of

dollars un�l late 1990s could boost or pull down the economic growth rate and decrease or increase

poverty and vulnerability. Li�le wonder then that successive governments have looked outward for

assistance, loans and grants as a short-cut for pushing growth at home instead of taking the long road of

encouraging domes�c savings and investments.

Source: Economic Survey of Pakistan (2015-16)

Fig 4: Na�onal Saving (as % of GDP)

17

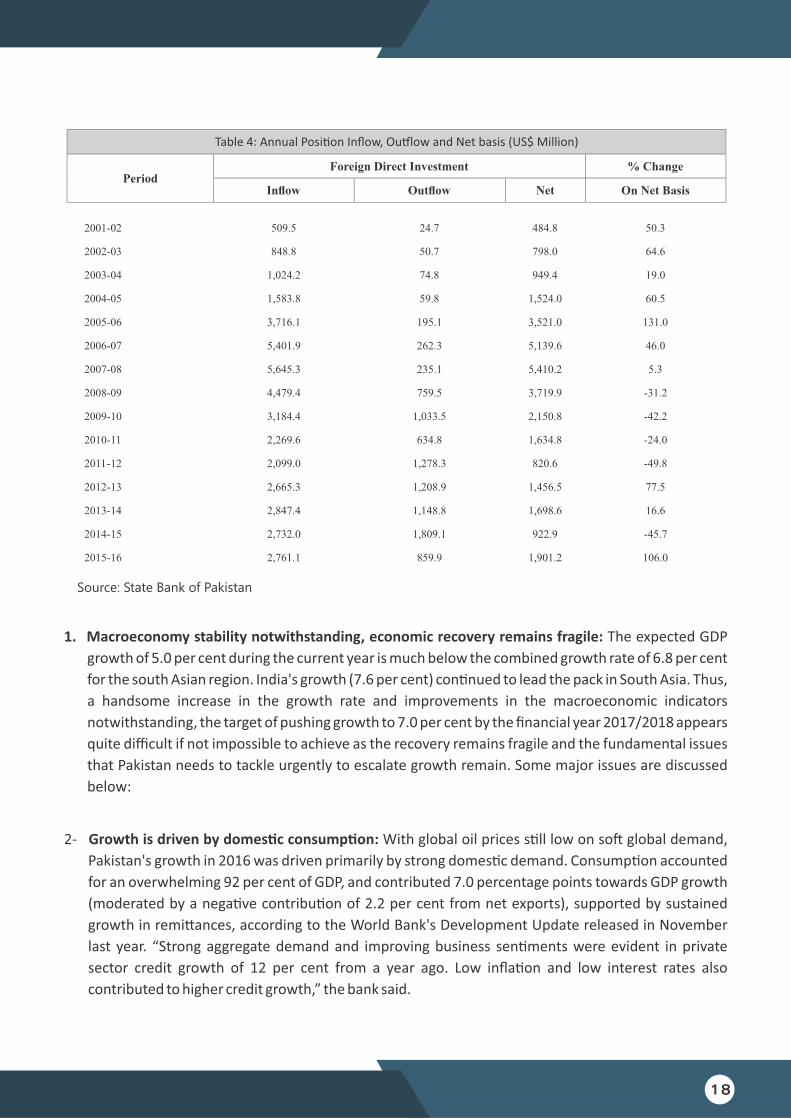

1. Macroeconomy stability notwithstanding, economic recovery remains fragile: The expected GDP

growth of 5.0 per cent during the current year is much below the combined growth rate of 6.8 per cent

for the south Asian region. India's growth (7.6 per cent) con�nued to lead the pack in South Asia. Thus,

a handsome increase in the growth rate and improvements in the macroeconomic indicators

notwithstanding, the target of pushing growth to 7.0 per cent by the financial year 2017/2018 appears

quite difficult if not impossible to achieve as the recovery remains fragile and the fundamental issues

that Pakistan needs to tackle urgently to escalate growth remain. Some major issues are discussed

below:

2- Growth is driven by domes�c consump�on: With global oil prices s�ll low on so� global demand,

Pakistan's growth in 2016 was driven primarily by strong domes�c demand. Consump�on accounted

for an overwhelming 92 per cent of GDP, and contributed 7.0 percentage points towards GDP growth

(moderated by a nega�ve contribu�on of 2.2 per cent from net exports), supported by sustained

growth in remi�ances, according to the World Bank's Development Update released in November

last year. “Strong aggregate demand and improving business sen�ments were evident in private

sector credit growth of 12 per cent from a year ago. Low infla�on and low interest rates also

contributed to higher credit growth,” the bank said.

Table 4: Annual Posi�on Inflow, Ou�low and Net basis (US$ Million)

Period

Foreign Direct Investment

% Change

Inflow

Outflow

Net

On Net Basis

2001-02

509.5

24.7

484.8

50.3

2002-03

848.8

50.7

798.0

64.6

2003-04

1,024.2

74.8

949.4

19.0

2004-05

1,583.8

59.8

1,524.0

60.5

2005-06 3,716.1 195.1 3,521.0 131.0

2006-07 5,401.9 262.3 5,139.6 46.0

2007-08 5,645.3 235.1 5,410.2 5.3

2008-09

4,479.4

759.5

3,719.9

-31.2

2009-10

3,184.4

1,033.5

2,150.8

-42.2

2010-11

2,269.6

634.8

1,634.8

-24.0

2011-12

2,099.0

1,278.3

820.6

-49.8

2012-13

2,665.3

1,208.9

1,456.5

77.5

2013-14

2,847.4

1,148.8

1,698.6

16.6

2014-15 2,732.0 1,809.1 922.9 -45.7

2015-16 2,761.1 859.9 1,901.2 106.0

Source: State Bank of Pakistan

18

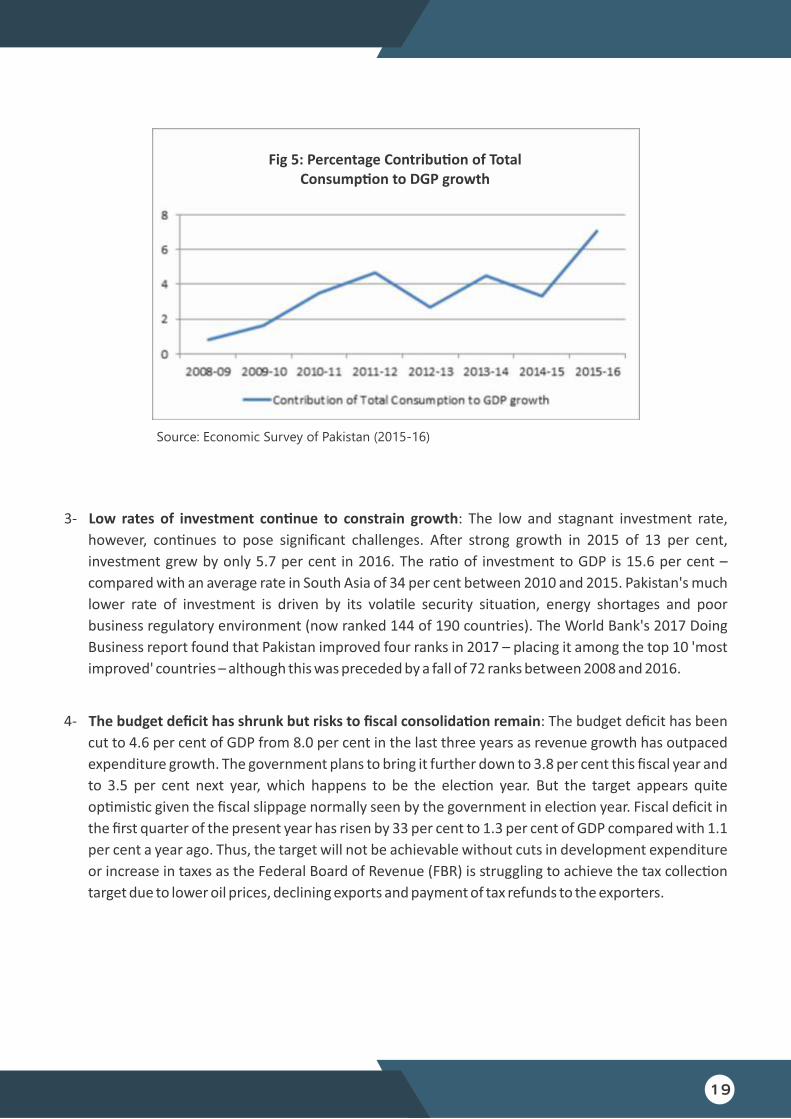

3- Low rates of investment con�nue to constrain growth: The low and stagnant investment rate,

however, con�nues to pose significant challenges. A�er strong growth in 2015 of 13 per cent,

investment grew by only 5.7 per cent in 2016. The ra�o of investment to GDP is 15.6 per cent –

compared with an average rate in South Asia of 34 per cent between 2010 and 2015. Pakistan's much

lower rate of investment is driven by its vola�le security situa�on, energy shortages and poor

business regulatory environment (now ranked 144 of 190 countries). The World Bank's 2017 Doing

Business report found that Pakistan improved four ranks in 2017 – placing it among the top 10 'most

improved' countries – although this was preceded by a fall of 72 ranks between 2008 and 2016.

4- The budget deficit has shrunk but risks to fiscal consolida�on remain: The budget deficit has been

cut to 4.6 per cent of GDP from 8.0 per cent in the last three years as revenue growth has outpaced

expenditure growth. The government plans to bring it further down to 3.8 per cent this fiscal year and

to 3.5 per cent next year, which happens to be the elec�on year. But the target appears quite

op�mis�c given the fiscal slippage normally seen by the government in elec�on year. Fiscal deficit in

the first quarter of the present year has risen by 33 per cent to 1.3 per cent of GDP compared with 1.1

per cent a year ago. Thus, the target will not be achievable without cuts in development expenditure

or increase in taxes as the Federal Board of Revenue (FBR) is struggling to achieve the tax collec�on

target due to lower oil prices, declining exports and payment of tax refunds to the exporters.

Source: Economic Survey of Pakistan (2015-16)

Fig 5: Percentage Contribu�on of TotalConsump�on to DGP growth

19

5- Exports fall: In spite of a decent recovery in economic growth rate, Pakistan's exports con�nue to

decline underlining low export compe��veness. Pakistan's share in global trade also dropped further

in 2016. The country's exports have dropped to $22 billion in three years to the end-June 2016 from

$25.1 billion at end-June 2013. The decline in exports means the country will have to rely more on

foreign capital flows going forward unless the trend is reversed as reflected by a net addi�on of $17

billion to the foreign debt stock since the government came to power.

Source: Economic Survey of Pakistan (2015-16)

Fig 6: Fiscal Deficit (as % of GDP)

20

Table 5: Pakistan’s Export Performance (US$ Thousand)

Code Product label Exported

value in 2012

Exported value in

2013

Exported value in

2014

Exported value in

2015

'TOTAL All products

24,613,676.00

25,120,883.00

24,722,182.00

22,089,018.00

'52 Co�on

5,225,694.00

5,333,784.00

4,731,369.00

4,040,271.00

'63

Other made-up tex�le ar�cles; sets; worn clothing and worn tex�le ar�cles; rags

3,285,353.00

3,685,485.00

3,906,465.00

3,759,721.00

'61 Ar�cles of apparel and clothing accessories, kni�ed or crocheted

2,006,290.00

2,105,321.00

2,402,619.00

2,359,608.00

'62

Ar�cles of apparel and clothing accessories, not kni�ed or crocheted

1,694,386.00

1,854,926.00

1,984,656.00

2,127,462.00

'10 Cereals

2,060,801.00

2,181,045.00

2,211,315.00

1,942,267.00

'42

Ar�cles of leather; saddlery and harness; travel goods, handbags and similar containers; ar�cles ...

673,815.00

743,538.00

742,028.00

687,621.00

'25

Salt; sulphur; earths and stone; plastering materials, lime and cement

714,069.00

722,822.00

694,237.00

507,567.00

'41 Raw hides and skins (other than furskins) and leather

457,395.00

529,698.00

547,508.00

425,085.00

'08 Edible fruit and nuts; peel of citrus fruit or melons

347,796.00

434,229.00

424,832.00

415,332.00

'90

Op�cal, photographic, cinematographic, measuring, checking, precision, medical or surgical ...

319,109.00

348,075.00

364,565.00

369,205.00

'17 Sugars and sugar confec�onery

253,535.00

633,568.00

439,338.00

358,000.00

'11 Products of the milling industry; malt; starches; inulin; wheat gluten

263,190.00

227,190.00

212,144.00

336,018.00

'03 Fish and crustaceans, molluscs and other aqua�c invertebrates

292,205.00

333,130.00

355,625.00

328,733.00

'22 Beverages, spirits and vinegar

172,771.00

364,159.00

352,272.00

310,032.00

'55 Man-made staple fibres

449,180.00

418,173.00

417,658.00

302,343.00

'39 Plas�cs and ar�cles thereof

520,985.00

449,789.00

361,431.00

284,130.00

'27

Mineral fuels, mineral oils and products of their dis�lla�on; bituminous substances; mineral ...

330,676.00

526,781.00

647,584.00

265,131.00

'02 Meat and edible meat offal

209,402.00

212,595.00

215,723.00

263,743.00

21

6- Foreign exchange reserves remain high and balance-of-payment situa�on is stable for now: A major

risk to economic stability emanates from weaknesses of the country's external sector. No doubt that

2016 marked the third straight year in which Pakistan's external account was in surplus. “While the

current account deficit widened over last year, it was comfortably financed by the surplus in the

financial account. A doubling in net FDI, as well as IMF disbursements and the government's external

borrowings, all contributed to the financial account surplus. The country's foreign exchange reserves

increased by $4.4 billion in 2016 to $23.1 billion. Apart from ensuring stability in foreign exchange

market, these reserves provided import coverage of over seven months.” The SBP concedes that the

balance-of-payment stability is debt-based as the country's trade deficit is widening, remi�ances

stagna�ng and FDI drying up. Growth in non-oil imports par�cularly of heavy machinery for power

and construc�on sectors and industrial raw materials (mainly steel and raw co�on) has also offset the

posi�ve impact of low global oil prices and current account deficit is growing wider. Given that these

non-oil imports were essen�al to grow economic ac�vity, they also contained the drop in overall

imports to only 2.3 per cent to above $40 billion in 2016. This small reduc�on in overall imports was

insufficient to outweigh the 8.8 per cent decline in exports, which fell to $22 billion. The current

account deficit widened to $3.3 billion in 2016 from $2.7 billion in 2015. Trade balance on the other

hand grew to $18.4 billion from $17.2 billion as export dropped to $22 billion from $24.1 billion. The

remi�ances remained a key offse�ng factor within the current account, and the country's reliance on

these flows has increased appreciably since 2012 as exports fall and FDI shrinks. Even in 2016, the

modest growth of 6.4 per cent in remi�ances was enough to offset 93.9 per cent of the trade deficit

(both in goods and services). Hence, the need for boos�ng exports through diversifica�on of products

and markets for cu�ng trade gap and reducing reliance on workers' remi�ances cannot be

overstated.

Source: Economic Survey of Pakistan (2015-16)

Fig 7: Current Account Deficit (US $ Million)

22

Source: Economic Survey of Pakistan (2015-16)

Fig 8: Trade Account Deficit (US$ Million)

23

Pakistan's Export Performance

24

PART-II

Pakistan's Export Performance

Exports are vital for a developing economy: Exports are a vital component of a country's GDP. They have

a direct impact on economic growth, crea�on of employment and balance of payments. Pakistan has

always been vulnerable to downfalls in its balance of payments which destabilizes its macroeconomic

outlook. The Economist Intelligence Unit has given Pakistan's 'Foreign Trade and Payments Risks' a score

of 75 out of 100 (100 = riskiest). In comparison, India has a score of 50 while Bangladesh has a score of 57.

There are many examples where countries like China, Malaysia, Bangladesh, India, South Korea, Thailand,

Vietnam (and the list goes on and on) have achieved higher level of economic growth and prosperity by

pursuing export-led growth strategy. While other na�ons have formulated target policies to boost and

diversify their exports for rapid economic development, Pakistan has lagged far behind in this area.

The importance of export-led growth policies becomes even more impera�ve for a country like Pakistan,

which has been running high current account deficits for decades and is extremely reliant on foreign

private and official capital inflows to pay for its import bill and create jobs to absorb millions entering the

job market every year. It is for this reason that both the mul�lateral donors and the SBP have for long been

underscoring the need for formula�ng and implemen�ng clear-cut policies for diversifying and increasing

exports. The SBP has par�cularly stressed the impact of falling exports on the country's current account in

its recent reports. “In order to ensure adequate financing for imports of capital goods and raw material,

there is a need to enhance export revenues, which have contracted for the second year in a row.”

Unless Pakistan significantly boosts its exports, it is headed for a major balance of payments crisis as

reducing import bill is near impossible because of highly inelas�c composi�on of imports like fuel, capital

goods, etc. It therefore is impera�ve that it moves to create comfortable surpluses of manufactured

goods and value-added products, which would allow it room to address other major issues facing the

economy.

25

Pakistan's export performance has remained dismal compared with its regional peers: Pakistan has

been able to more than double its exports, which peaked from $11.93 billion in 2003 to $25.2 billion in

2014 before declining to $22 billion in 2016. It is interes�ng to note that the en�re growth in exports over

these years has been posted in the conven�onal products and commodi�es – tex�les, rice, leather and

leather products, sports goods, surgical instruments, sugar and molasses, fish, and so on and so forth. It

means that Pakistan has failed to diversify its exports at all. Nor has it been able to increase the share of

value addi�on to our exis�ng exports.

Similarly, the markets where the country's exports are headed every year remain the same. Thus,

Pakistan's exports con�nue to be constrained by lack of diversifica�on of products and markets, as well as

lower levels of value-addi�on. As a consequence, Pakistan's share in the world exports has declined to 1.5

per cent in 2015 from 1.8 per cent in 2003.

Source: Economic Survey of Pakistan (2015-16)

Source: ITC World Trade Map

Fig 9: Exports as % of GDP

Table 6:

26

Pakistan's lacklustre export performance means that its compe�tors are star�ng to catch up or go past it.

Compared with Pakistan, for example, Bangladesh has massively boosted its exports from $6.4 billion in

2003 to $36 billion in 2015. Like our exports, Bangladesh's exports have a very narrow base – mostly

tex�le garments – and limited markets. Yet, while Pakistan's tex�le exports are stagnant at $12-13 billion

despite it being the 4th largest producer of co�on, Bangladesh has grown its tex�le-based exports to

more than $33 billion over the years and plans to push them to $50 billion by 2020 to overtake China

through massive value-addi�on. It is in spite that it does not grow co�on at all. They have done so by

implemen�ng investment and industrial policies and se�ng defini�ve targets for themselves. Indeed, the

concessional du�es offered by the European Union and the United States for Bangladesh's tex�les and

government subsidies have helped its tex�le makers grow their exports much faster than Pakistan, the

level of value addi�on its industry has achieved is a major contributor to the export growth. India also has

achieved remarkable export growth over the same period, growing its exports from $59.30 billion to a

whopping $264 billion. Also, Indian exports are more diversified and carry higher levels of value addi�on.

Why Pakistan failed to grow its exports: There are many reasons for the recent declining trend in the

export sector. Broadly speaking, the factors responsible for the lackluster performance of the export

sector include: lack of an effec�ve industrial/export policy, liberal import policy and free trade

agreements, high cost of doing business, narrow base of exports and limited market access, etc.

1- Lack of Effec�ve Industrial Policy: Prolonged stagna�on in the manufacturing sector, and a consistent

decline in investment in Greenfield projects, capacity expansion and technology replacement have led

many to conclude that Pakistan could be on the verge of 'premature de-industrializa�on'.

Manufacturing — especially Large Scale Manufacturing (LSM) that cons�tutes almost 80 per cent of

the manufacturing sector output and contributes 11.7 per cent to GDP, which plays a crucial role in the

Source: ITC World Trade Map

Fig 10: Percentage Change in Exports (%)

27

economic growth of a country by helping it absorb most of the urban labour and a�ain higher income

levels, has been in trouble for quite a long �me. The country's decision to abandon its proac�ve

industrial policy around 1990 and start a process of trade and economic liberaliza�on at the behest of

interna�onal financial ins�tu�ons is a major reason for this state of affairs.

2- Impact of trade liberaliza�on and free trade agreements: Pakistan's decision to liberalize its

interna�onal trade regime without encouraging export-oriented manufacturing is another reason for

declining export performance. By abandoning ac�ve industrial policy, Pakistan seems to have lost the

benefits of an economic focus on the development of the manufacturing sector and its lackadaisical

a�empts at trade liberaliza�on were not enough to start the process of export-oriented

manufacturing and economic growth.

In fact, Pakistan is fast turning into a consumer economy. The conclusion of Free Trade Agreements

(FTAs) with its trading partners has not so far helped it a�ract investments in export-oriented

industries, diversify exports and create jobs. Actually, the FTAs have heavily subsidized imports from

countries like China and export jobs. With the influx of cheaper goods from China and elsewhere no

new investment is taking place. Local manufacturers aren't only facing intense compe��on in export

markets, but also losing their domes�c market because they just cannot compete with the rivals.

Table 7: Pakistan’s Trade Balance (US$ Million)

Year of FTA Signing 2015

Trade Balance with

Malaysia

-1,076 (Year 2007) -725

Trade Balance with China -2,408 (Year 2006) -9,084

Trade Balance with Sri

Lanka

95 (Year 2005) 188

Source: ITC World Trade Map

28

3- Cost of doing business: The consistent erosion in the country's exports is a major indicator of

decreasing compe��veness because of rising cost of doing business, primarily on account of energy

shortages and high prices, especially in Punjab. While the government has reduced energy shortages

for the industry in the last three years by induc�ng Liquefied natural gas (LNG) into the system of gas

companies, the costs remain way higher than the regional average. The industry in Pakistan, especially

in Punjab where the export-oriented industry is using expensive LNG, is paying over $0.11 per unit of

electricity compared with $0.085 in China, $0.07 in Vietnam and $0.09 in India. Low labour

produc�vity and efficiency and difficul�es in star�ng a business further add to the cost of doing

business. A Pakistan Business Council (PBC) study shows that the cost disparity between Pakistan and

Bangladesh is 1.3 to 2.7 �mes. Li�le wonder then Pakistan is losing its garments markets to

Bangladeshi and Vietnamese companies.

Source: World Bank

Fig. 11

29

4- Narrow export base, low value-addi�on and limited markets: Pakistan's exports con�nue to revolve

mostly around a single crop – co�on (as tex�les cons�tute 55 percent of the na�on's total exports), low

value-added merchandise like leather and agriculture commodi�es like rice. Li�le effort has been

made to diversify exports to meet the changing global economy and consumer demand and trends.

Narrow export base means our exporters will be constrained to sell their goods in the same tradi�onal

markets with demand for those products and quality. Thus, Europe, America and, in the recent years,

China remain Pakistan's major markets with chunk of exports des�ned for these des�na�ons. The

increase in product base would help in bring down the product concentra�on index. To capture a large

share in the world trade, Pakistan has to make a strategic shi� in the composi�on of its exports and

encourage value-addi�on for be�er prices and for capturing greater share even in the exis�ng

markets.

Source: World Bank

Fig. 12

30

Table 8: Major Export Markets of Pakistan

31

Proposals to Enhance Exports

32

PART-III

Proposals to Enhance Exports

If Pakistan wants to tackle its fragile balance of payments posi�on on a sustainable basis, develop capacity

to absorb exogenous price shocks like sudden increase in essen�al imports as oil, create jobs and reduce

its reliance on foreign debt, it has no op�on but to rapidly increase its exports.

Prime Minister Nawaz Sharif has recently announced an 18-month Rs180 billion “Trade Enhancement

Incen�ves” to arrest the declining exports in five major export-oriented industries, including tex�les and

clothing sector, which have already been granted zero-rated status. The subsidy package is expected to

first plug further drop in exports of these sectors before boos�ng export growth by up to $2 billion.

While the ini�a�ve must be welcome as it provides immediate relief to the exis�ng exporters and

expor�ng sectors, it does not address the deep-rooted issues hampering exports like erosion in export

compe��veness, high cost of energy, low labour produc�vity, diversifica�on of exports and markets, etc.

Even the SBP has repeatedly urged for taking “concrete steps to enhance compe��veness and ease of

doing business; promote investments in Research & Development (R&D) and innova�on, and a culture of

entrepreneurship; ins�tute a vigorous legal system to protect intellectual property rights; and improve

the quality of labour, etc. In addi�on, given the mul�tude of regional and even intercon�nental trade

pacts that are under process or deliberated upon, Pakistan ought to improve its trade compe��veness, as

FTAs signed among other countries could put Pakistan in a disadvantageous posi�on. The structural issues

afflic�ng the export industry also need to be addressed. Pakistani exporters need to keep pace with

changing consumer preferences in their key markets, and adjust their product mix accordingly; the tex�le

sector in par�cular should start focusing on synthe�c fiber-based ones that are in demand in the US.

Moreover, the small and medium enterprise (SME) sector, which has a major share in producing electrical

products like fans, light bulbs and surgical equipment etc., con�nues to largely operate on the fringes; its

share in export financing is minimal.”

Pakistan has a lot of economic poten�al. The country is located at the crossroads of South Asia, Central

Asia, China and the Middle East and is, thus, at the center of a very large regional market with a vast

popula�on, diverse resources, and untapped poten�al for trade. The country's growing working-age

popula�on offers the country with a poten�al demographic dividend but also with the cri�cal challenge

to create jobs. But we need to formulate an effec�ve export-oriented strategy that addresses industry's

compe��veness issues, encourage value-addi�on, and diversify markets and products before this

poten�al can be realized.

33

1- A new strategic trade policy framework needs to be formulated... The government has shown

encouraging signs recently to boost exports. These include par�al se�lement of the refunds of

exporters, restora�on of zero-ra�ng tax regime for five major export sectors: tex�les, carpets, leather,

surgical and sports goods, and the Rs180 billion trade enhancement ini�a�ve. While these measures

will support exports in the near to medium term, we require a long-term integrated industrial and

trade (import and export) strategy that encourages investment in manufacturing for producing export

surpluses, encourages value-addi�on, resolves long-standing issues like compe�veness and

produc�vity to boost our exports, and reduces our reliance on foreign loans and aid.

It is �me to formulate a coherent strategic trade policy with a long-term aim of realizing the country's true

export poten�al and create jobs for the millions entering the market every year. The present Strategic

Trade Policy Framework (STPF) 2015/2018 is not a strategy at all. At best it's merely a documented jo�ed

down by the bureaucrats with li�le knowledge and insight about how the global markets func�on, or how

exports can be increased.

While this so-called framework sets a target for boos�ng the country's exports over a three-year �me

framework, it doesn't explain as to how the government is going to achieve it. Li�le wonder that the

exports declined 8.9 per cent in the first year of the STPF and the government had to put together 18-

month Rs180 billion package early this year to arrest further decline.

2- The new export policy should involve input from all stakeholders: A new export strategy should not

just spell out export target set at whim. No policy framework can deliver the desired results without

incorpora�ng in it the input from all the stakeholders in trade: all relevant ministries including

commerce, industry, tex�les, agriculture, planning, labour, finance, etc. all the provincial

governments and their relevant departments; and last but not least the business community

represen�ng different sectors. The involvement of all the stakeholders will allocate clear-cut

responsibili�es for each stakeholder and hold them accountable for their ac�ons or lack of them.

3- Economic, industrial, agriculture and tax policies should be updated to achieve the STPF targets:

The framework must lay out a well-defined long-term roadmap to achieve whatever targets are set by

the stakeholders a�er consulta�on. It means that the country's industrial, agriculture, labour, fiscal

and tax policies are updated and tweaked to align them with the STPF targets. No link should be le�

missing to ensure smooth implementa�on of the policy framework and achieve the desired outcome.

4- Import policy should be dovetailed into export policy: No export strategy can succeed without

dovetailing import policy into it. An export policy looking in one direc�on and an import policy into

another will keep working at cross purposes and pulling each other down. By making its import

policies subservient to its export strategy, for example, Bangladesh has successfully created a vibrant,

34

export-oriented garment sector and millions of jobs although it does not grow co�on. Similarly,

Malaysia, Vietnam and Thailand have two-fi�h of their exports based on imported raw materials. In

contrast, the import content used in exports is less than 10 per cent in case of Pakistan.

This also calls for a review of FTAs and PTAs Pakistan has signed with different countries. The primary

objec�ve of any such bilateral agreement should be to create jobs at home, encourage value-addi�on,

boost industrial output, and enhance export. In Pakistan's case, however, such agreements have proven

detrimental for the domes�c industry and tax revenues and failed to increase exports. It is es�mated that

the free and preferen�al trade agreements signed by Islamabad so far have resulted in subsidizing the

industries of the partner countries to the extent of $30 billion to $40 billion.

Such arrangement with China, for instance, has resulted in an influx of cheap imports at the cost of local

industry's compe��veness and jobs, and caused a major dent into the government tax revenues. On the

other hand Pakistan has not been able to increase its exports to China because Beijing now offers more

concessional access to countries like Thailand than it does to Islamabad.

5- Trade policy framework should stop smuggling and discourage under-invoicing: Preven�on of

smuggling and influx of under invoiced goods into the country should be an important part of the new

strategic trade policy to secure local industry and promote exports. Large-scale smuggling via

Afghanistan and rampant under-invoicing in case of imports from China and Dubai has injured the

domes�c industry and undermined its ability to produce for export markets. The business community

has long been raising its concerns on the threats posed by the menace of smuggling and under-

invoicing. The menace isn't hur�ng the industry alone it is also causing enormous tax revenue loss to

the government.

6- Trade policy framework should enhance compe��veness of the domes�c industry: The declining

exports clearly show that Pakistan is becoming more and more uncompe��ve in the world markets

because of a number of factors: high cost of energy, uncertain supply of power and gas, low labour

produc�vity, lack of technology up-grada�on, security condi�ons, absence of R&D facili�es, etc. The

trade policy needs to address these issues effec�vely and urgently in order to push exports.

7- Development of export clusters for technology-intensive products: Cluster development can be of

great help in broadening the export base. Most firms in high and medium technology sectors are

rela�vely small. Due to their limited resources and high cost of produc�on, these enterprises find it

difficult to exploit market opportuni�es. The government should develop common export cluster

facili�es for firms producing technology-intensive products as cluster development enables the SMEs

in the medium/high technology sectors to complement each other's resources and exper�se.

35

8- Focus on technology exports: As the role of technology is increasing in the world trade, Pakistan will

have to make concerted efforts to boost technologically based industrial produc�on through

induc�on of medium/hi-tech industries in export categories. There is especially a need to focus on

medium technology products like chemical and pharmaceu�cal products and engineering goods,

which have shown nega�ve export growth of 13 percent and 20.7 percent, respec�vely, in 2015/2016

compared with the previous year.

9- Increase access to trade finance: According to the Global Enabling Trade Report 2014, Pakistan ranks

88 in the availability of trade finance. To make sufficient funds readily available as financial

assistance/credit for exporters, especially the smaller ones, it will be a good idea to establish a

separate bank –Exim Bank – for this purpose. The bank should provide export finances/loans/credit

on so� terms along with other services to exporters for rapid growth of exports. The domes�c credit

to the private sector is around 15 percent of the GDP in Pakistan as compared to around 50 percent in

India and over 100 per cent in the developed countries like Singapore, New Zealand and China.

10- Encourage value-addi�on: Pakistan's exports are constrained not only by lack of diversifica�on but

also low value addi�on. Pakistan's tex�le and clothing exports, for example, which form above 55 per

cent of its total exports, mainly comprise yarn and grey fabric and low end garments. This calls for

need to link export incen�ves with the value addi�on, discouraging lower value addi�on and

rewarding higher value addi�on. By expor�ng commodi�es and semi-finished items, we are actually

crea�ng compe��on for our exports from countries such as Bangladesh and Vietnam.

11- Diversify markets: Pakistan has so far done li�le to enter and increase its presence in new markets.

There is a dire need to diversity the exports in terms of markets as about 60 percent of Pakistan's

exports go to 10 countries: the USA, China, UAE, Afghanistan, the UK, Germany, France, Bangladesh,

Italy and Spain. The US has largest share of 17 per cent followed by European countries 22 per cent in

total exports of Pakistan. There is an ample poten�al of increasing exports to the other world markets,

where Pakistan is an under achiever – South America, Africa, Central Asian Republics (CARs) and

Russia where the combined share of Pakistan's exports is less than 10 per cent of its total exports.

Apart from looking for new markets, Pakistan's exports have enormous poten�al and space to increase

their penetra�on into the exis�ng markets. Pakistan's exports to the EU, for example, represent almost 37

per cent of the country's total exports but form just 0.14 per cent of the EU's world imports of $5.2 trillion.

Compared with Pakistan, which increased its exports to the EU from $4.6 billion in 2006 to $7.3 billion,

Bangladesh has improved its exports from $7.6 billion to $19.84 billion or 0.38 per cent of the block's

world exports in the same period. The grant of GSP+ status allowing Pakistan's 70 per cent exports to

enter the EU at preferen�al rates and 20 per cent at zero tariffs offers a big opportunity to increase our

penetra�on in its market. Such preferen�al market access needs to be nego�ated with the US as well.

36

Pakistan also needs to tap the trade poten�al of the south Asian region with a view to diversifying its

export markets. At present, Pakistan remains least integrated country in the region. While poli�cal

disputes are holding Islamabad from boos�ng trade with India, it could easily enhance its trade �es with

the other regional countries just as India has done over the last few years.

12- Diversify exports: The new export strategy must focus on the diversifica�on of products and

des�na�ons, and include the export of services. Tex�les, the mainstay of Pakistan's exports,

represent just 6 percent of the world trade, which shows the need for encouraging other industries,

especially halal meat and food industry and engineering goods manufacturing industry, to enter the

export markets. The strategy should be based on incen�ves to encourage product diversifica�on and

reduce dependence on tradi�onal exports like co�on, tex�les and clothing, leather and rice that

contribute more than 60 percent to the na�on's total exports. Increase in product base would also

help in bringing down the product concentra�on index. To capture a large share in the world trade,

Pakistan has to make a strategic shi� in the composi�on of its exports which entails promo�ng

exports of medium/high technology products whose share in the world trade is increasing and

reducing the share of exports with low technology content. There is also a great scope of increasing

the exports of services sector.

37

Sectors with Export Poten�al

Halal Food: Halal food is one of the fastest growing markets in the world with a share of more than 15

percent in the world trade. The size of the market is es�mated to be around $300 billion with Pakistan

having a negligible share in the world trade despite being one of the largest Muslim countries and

enormous poten�al to produce and export halal food, including meat and poultry products. In fact, the

halal food market is dominated by non-Muslim countries like China, Brazil, etc.

If encouraged, Pakistani companies dealing in poultry and poultry products alone can boost their exports

to $8-10 billion in a ma�er of five years as demand for halal poultry and poultry products is growing in the

Middle East as well as in Europe and America as their Muslim popula�ons increase.

In order to encourage poultry exports, the government should help the industry bring down the cost of its

locally produced poultry and its products to allow it compete in the interna�onal markets.

At present, the poultry sector pays huge import du�es and taxes on various inputs, components, etc.

required for poultry produc�on. For example, import duty on grandparent stock is 17 percent, on

vaccines/medicines 18 percent, on poultry feed ingredients up to 22 percent, and chicken food

ingredients up to 62 percent. These taxes are passed on to exportable poultry products whether these are

imported directly by producers and/or by the third party (vendors), significantly raising their costs and

making them more expensive than the rivals in the foreign markets. In addi�on, the producers pay 17

percent sales tax on their electricity/energy bills.

All these taxes - including sales tax - imposed on the import of different inputs at different stages and paid

by various producers and vendors are ul�mately passed on to the exporters.

As producers are unable to claim these taxes these costs add to inputs as duty drawback. Therefore, it is

proposed that the government should allow duty drawback on exportable products like chicken hatching

eggs (for broiler and parent stock), chicken table eggs, poultry/ca�le feed, chicken meat and prepared

chicken finished products (fully and semi cooked).

In addi�on to duty drawback, the government must also consider allowing freight subsidy on export of

halal poultry meat and its products like other poultry expor�ng na�ons. It is proposed that 50 percent

freight subsidy on the air and sea freight cost will go a long way in boos�ng our exports.

Engineering Goods: The share of Pakistan's engineering industry in overall global exports has remained

stagnant at around 4 percent over the past 10 years, though engineering goods cons�tute more than 60

38

percent of the world trade. But for nominal growth, Pakistan's engineering export proceeds are abysmally

low.

The demand for domes�c engineering goods accounted for 37 percent of the total import bill in 2015-16.

The same year, earnings from export proceeds of engineering goods declined by 15pc, from $1.05 billion

to $899 million.

Currently, the government's focus is on promo�ng tradi�onal export sectors. With a focus on

moderniza�on and technology up grada�on, export poten�al of engineering products stands at $10

billion by 2026-27

The domes�c engineering industry currently caters to 25-30 percent of the local demand, while the rest of

the demand is being met through imports. This is because of the fact that the engineering industry mostly

operates in the unorganized sector. Small workshops manufacture small items using conven�onal

methods and machines.

To produce import subs�tutes and create export surpluses, successive governments had given tax

incen�ves on import of plant, machinery, equipment and inputs for engineering goods manufacturing

through SROs over the last 10 years. In the absence of technology up-grada�on and plant moderniza�on,

the engineering industry is generally characterized by low produc�vity, high cost of output, small volumes

and non-compe��veness.

The industry produces limited export surpluses of be�er quality products. The top 15 products cons�tute

more than 98 percent of the total engineering exports. The major share comes from surgical instruments

and apparatus, followed by ar�cles of iron and steel, machinery components, tool, implements, cutlery,

copper, etc. Exports are also limited to few markets like Afghanistan, Bangladesh, Egypt, Syria, South

America, Africa and the US. The Government can take several steps like declaring small scale manufacturing as export houses,

conduc�ng market surveys and collec�ng informa�on, alloca�on of maximum amount out of LTFF

investment for exporters, engineering industry venture capital fund management companies, risk and

insurance coverage, export refinance scheme of heavy equipment exports, waiver of federal excise duty

on technology acquisi�on, common facility centers, tes�ng laboratories and standard cer�fica�ons. It is

also recommended that business support centers be established, energy efficiency audits and extensive

training and development of human resource take place.

Pharmaceu�cal Industry: The pharmaceu�cal Industry has tremendous export poten�al but the industry

has not been able to realize that poten�al. The pharmaceu�cal exports of Pakistan are around US$ 200

million. The main hurdle in the enhancement of pharmaceu�cal exports to developed countries is the

cer�fica�ons i.e. US Food and Drug Administra�on (USFDA), UK's Medicines and Healthcare Products

Regulatory Agency (MHRA). It is worth men�oning that around 500 companies in India are

USFDA/MHRA/WHO approved. These cer�fica�ons are very expensive but if the Government of Pakistan

39

hires consultants to help large pharmaceu�cal Industries to get these cer�fica�ons, the Industry can earn

considerable foreign exchange.

India is one of the largest exporters of generic medicine and has been the supplier of 20% of global export

volume. The pharmaceu�cal exports of India are around US$ 11.2 billion and are expected to touch US$

$100 billion by 2025. The Pharmaceu�cal Export Promo�on Council (PHARMEXCIL) was established in

2004 by the Ministry of Commerce and Industry, Government of India, to promote pharmaceu�cal

exports. The Indian pharmaceu�cal industry is expected to touch US$ 55 billion by 2020.

Furniture industry: Pakistan's furniture industry has a negligible presence in the $250 billion world

furniture trade because of supply chain obstacles: obsolete technology, unskilled workers, unavailability

of cheaper raw materials, shortage of furniture designers, vanishing tradi�onal Shisham (Indian

Rosewood) resource, etc. Pakistan's furniture exports remain very small in spite of demand for its carved

Chinio� furniture by Pakistanis living in the West and the Middle East. In the modern furniture segment

Pakistan stands nowhere in the world market.

But now Pakistan is losing its advantage even in the tradi�onal carved solid wood furniture segment

owing to unavailability of Shisham and disappearing skills and lack of technology. Thus, the country's

furniture exports have declined from $18 million in 2007 to $6 million during 2016. Compared with its

rivals, Pakistan's furniture industry remains an essen�ally fragmented, tradi�onal co�age opera�on with

small workshops spread in Lahore, Karachi, Gujrat, Faisalabad, and Peshawar.

Major problems faced by the furniture industry include unsustainable wood resource handling that has

resulted in its shortage and higher prices, lack of technology for wood seasoning, sta�c designs, lack of

produc�on innova�ons, unskilled workforce, substandard finishing and packaging, etc.

In the world market Pakistan competes with countries like China, India, Vietnam and Malaysia with

facili�es to supply huge orders. China and Vietnam in par�cular are concentra�ng their industries into

larger bases and reaping the benefits of mass produc�on to the extent possible. If Pakistan wants to

move from the small co�age industry status into SME networking culture, it will be have to adopt

new technology, update skills of workers and improve designing. The best way for Pakistan to enter the

world market is to start manufacturing modern furniture using new raw materials used by its compe�tors.

According to Furniture makers, the furniture export could reach half a billion dollars in few years if the

government supports them in improving skilled labour, ini�ate courses in furniture designing, provide

manufacturers access to subsidized credit for acquiring new technologies and raw materials including

solid wood, etc.

40