market structure, fragmentation, and market quality paul bennett li wei new york stock exchange...

TRANSCRIPT

Market Structure, Fragmentation, and Market Quality

Paul BennettLi Wei

New York Stock Exchange

December, 2005

2

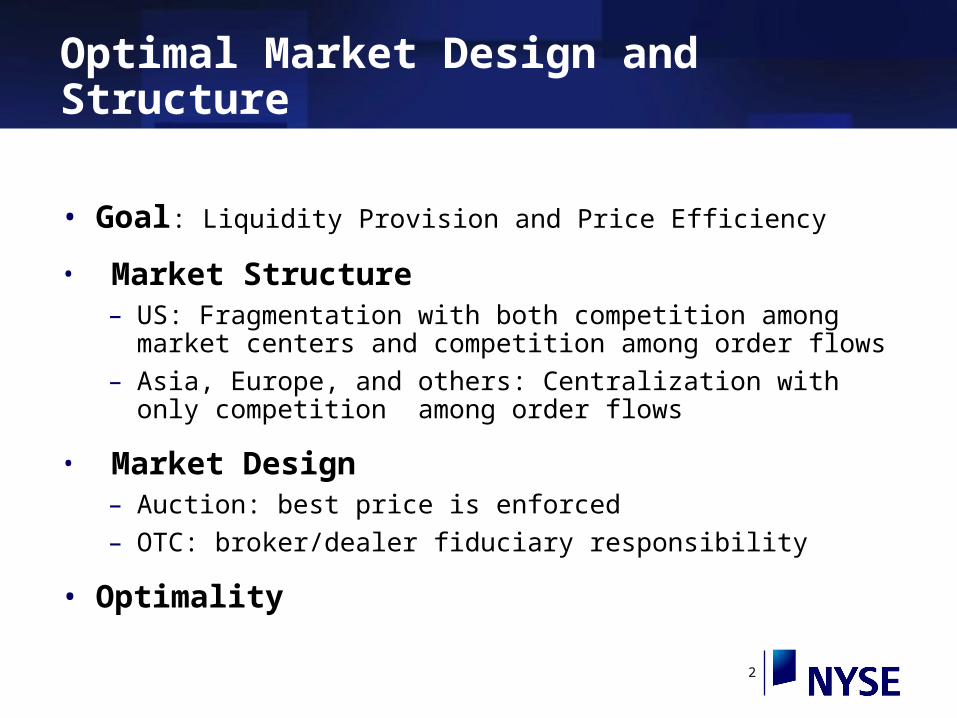

Optimal Market Design and Structure

• Goal: Liquidity Provision and Price Efficiency

• Market Structure– US: Fragmentation with both competition among market centers

and competition among order flows

– Asia, Europe, and others: Centralization with only competition among order flows

• Market Design– Auction: best price is enforced

– OTC: broker/dealer fiduciary responsibility

• Optimality

3

NYSE vs NASDAQ Difference Fundamental difference between the NYSE and NASDAQ Today

• Pre – NASDAQ Reform

• Pre – Decimal

• Post – Decimal– Decimalization Has Driven the Transaction Cost Down

– New Technology of Order Routing Increases Competition

• NYSE vs NASDAQ Difference– Difference in spread is narrowing

– Fragmentation

4

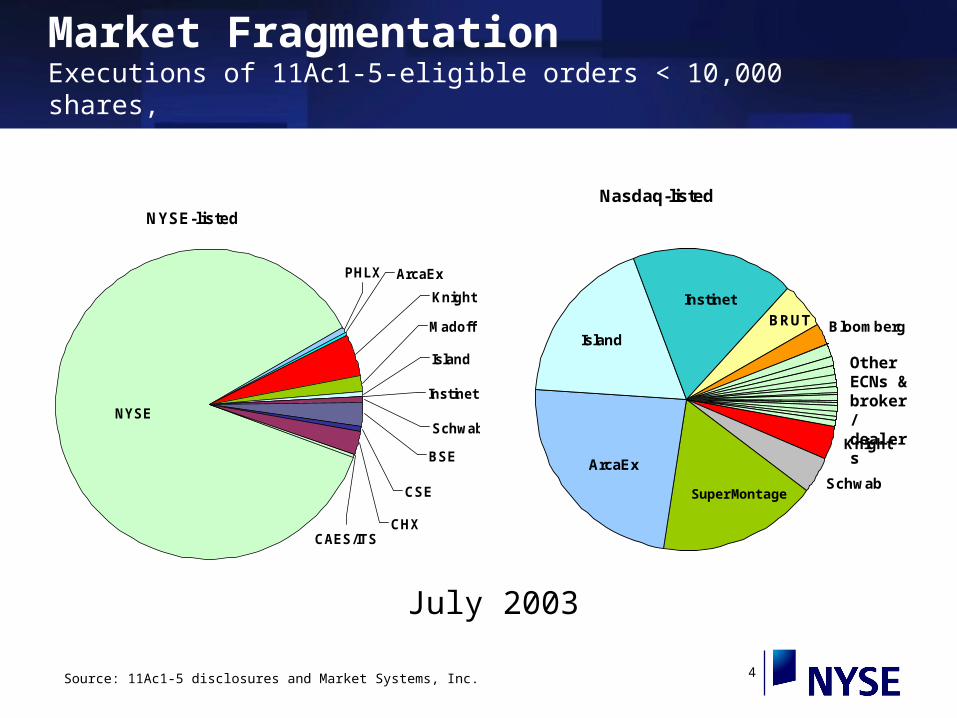

NYSE-listed

NYSE

CHXCAES/ITS

Madoff

Knight

ArcaExPHLX

Instinet

Island

CSE

BSE

Schwab

Market FragmentationExecutions of 11Ac1-5-eligible orders < 10,000 shares,

Source: 11Ac1-5 disclosures and Market Systems, Inc.

Nasdaq-listed

BloombergBRUT

Knight

SchwabArcaEx

Island

Instinet

Other ECNs & broker/ dealers

SuperMontage

July 2003

5

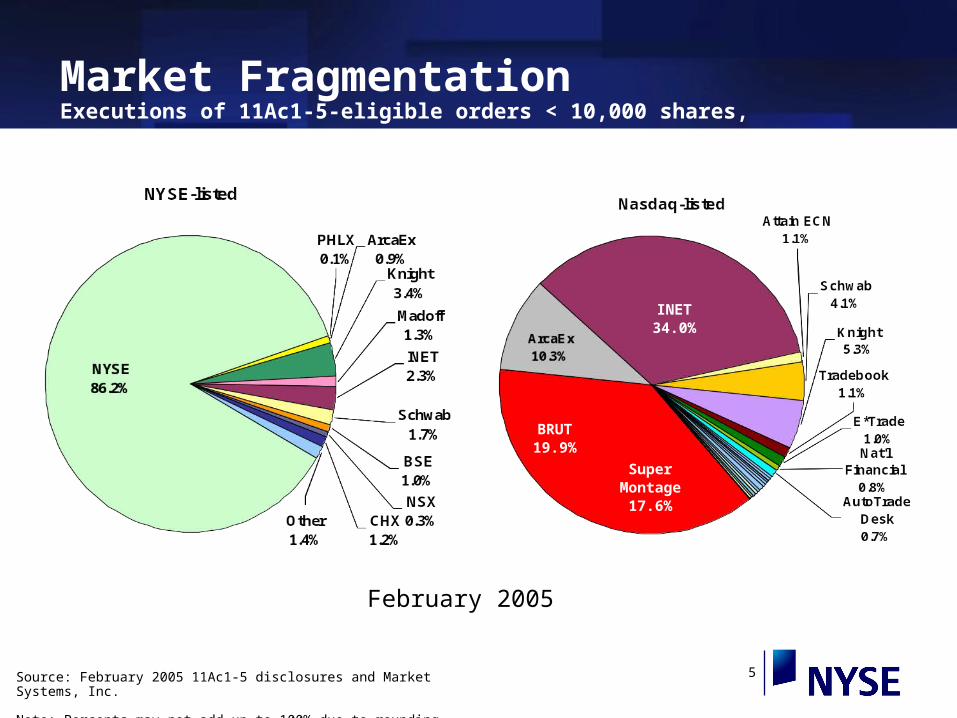

Market FragmentationExecutions of 11Ac1-5-eligible orders < 10,000 shares,

Source: February 2005 11Ac1-5 disclosures and Market Systems, Inc. Note: Percents may not add up to 100% due to rounding.

February 2005

SuperMontage

17.6%

BRUT19.9%

INET34.0%

6

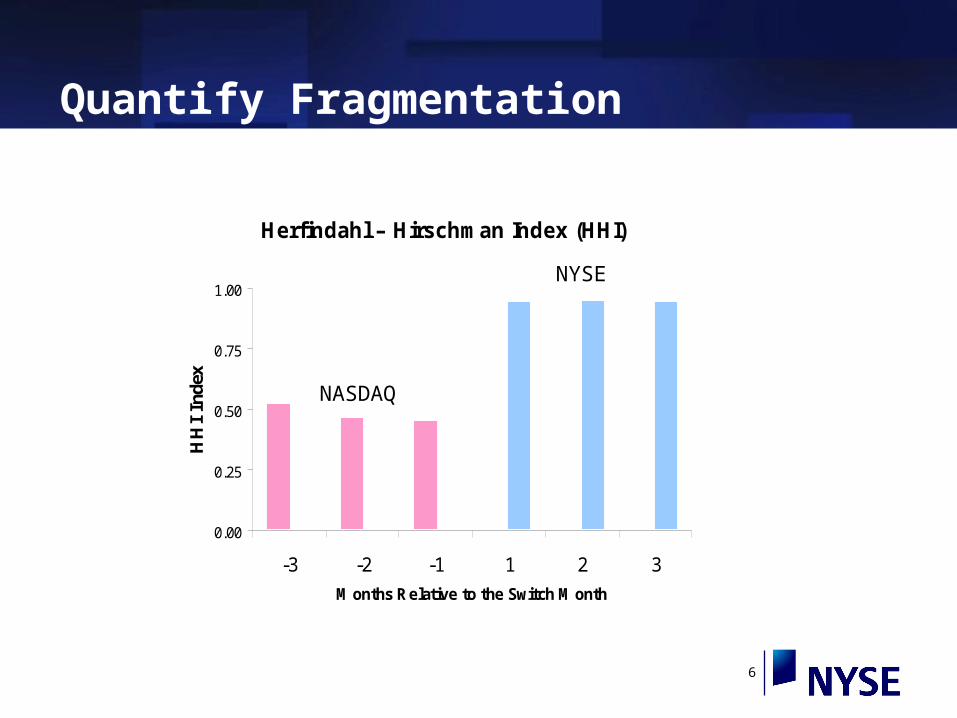

Quantify Fragmentation

Herfindahl – Hirschman Index (HHI)

0.00

0.25

0.50

0.75

1.00

-3 -2 -1 1 2 3

Months Re lative to the Switch Month

HH

I In

dex

NASDAQ

NYSE

7

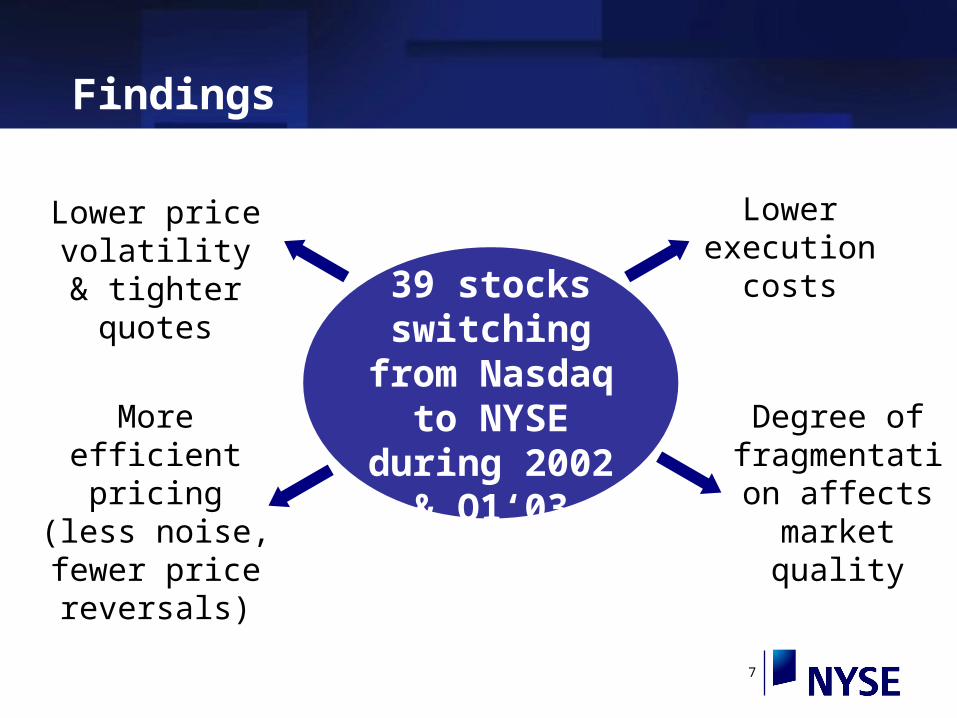

Findings

39 stocks switching from

Nasdaq to NYSE during 2002 & Q1‘03

Lower price volatility &

tighter quotes

More efficient pricing (less noise, fewer

price reversals)

Lower execution

costs

Degree offragmentation affects market

quality

8

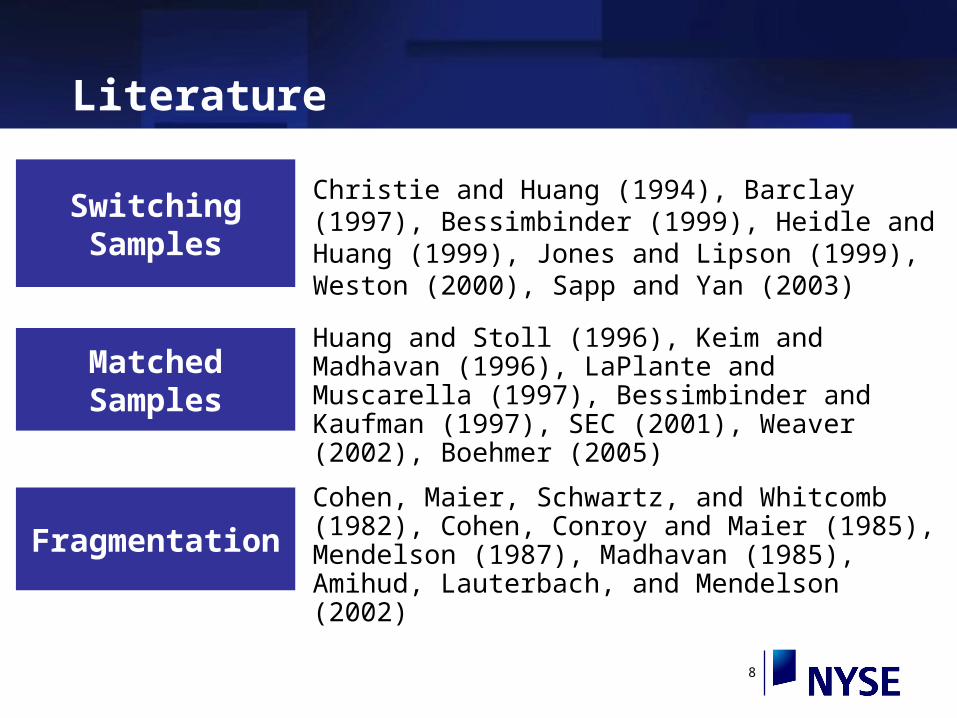

Literature

Switching Samples

Matched Samples

Christie and Huang (1994), Barclay (1997), Bessimbinder (1999), Heidle and Huang (1999), Jones and Lipson (1999), Weston (2000), Sapp and Yan (2003)

Huang and Stoll (1996), Keim and Madhavan (1996), LaPlante and Muscarella (1997), Bessimbinder and Kaufman (1997), SEC (2001), Weaver (2002), Boehmer (2005)

Fragmentation

Cohen, Maier, Schwartz, and Whitcomb (1982), Cohen, Conroy and Maier (1985), Mendelson (1987), Madhavan (1985), Amihud, Lauterbach, and Mendelson (2002)

9

Sample and Data

Sample• 39 companies switching from

Nasdaq to the NYSE from Jan ‘02 through Mar ‘03

Data• Trades and Quotes• SEC 11Ac1-5 Reports

Window• 60 trading days before and after for

trades and quotes.• 3 months before and after for the

Dash-5 data

10

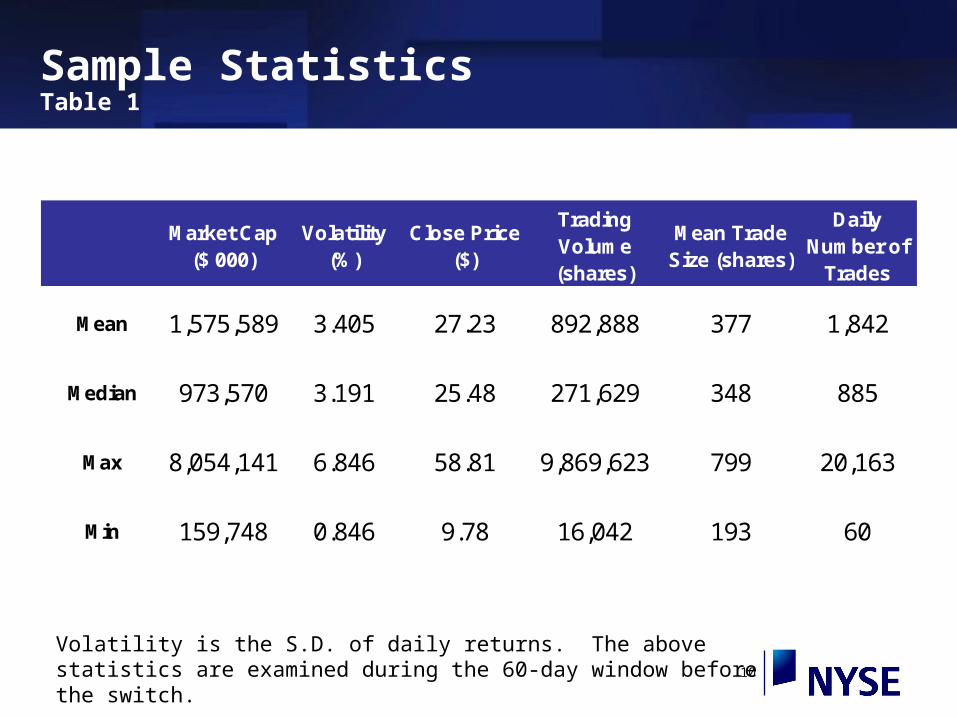

Sample StatisticsTable 1

Market Cap ($ 000)

Volatility (%)

Close Price ($)

Trading Volume (shares)

Mean Trade Size (shares)

Daily Number of

Trades

Mean 1,575,589 3.405 27.23 892,888 377 1,842

Median 973,570 3.191 25.48 271,629 348 885

Max 8,054,141 6.846 58.81 9,869,623 799 20,163

Min 159,748 0.846 9.78 16,042 193 60

Volatility is the S.D. of daily returns. The above statistics are examined during the 60-day window before the switch.

11

Voluntary Order Flow MigrationFigure 1

0

20

40

60

80

100

-60 -50 -40 -30 -20 -10 0 10 20 30 40 50

Trading Days Relative to the Switch

NASDAQ SuperMontage + ECNs + Dealers

NYSE

Regionals + ECNs

12

Market Quality

• Volatility

• Price Efficiency

• Quoted Spread: pre-trade

• Effective Spread: post-trade

• Realized Spread: competition of supplying liquidity

• Execution Speed

13

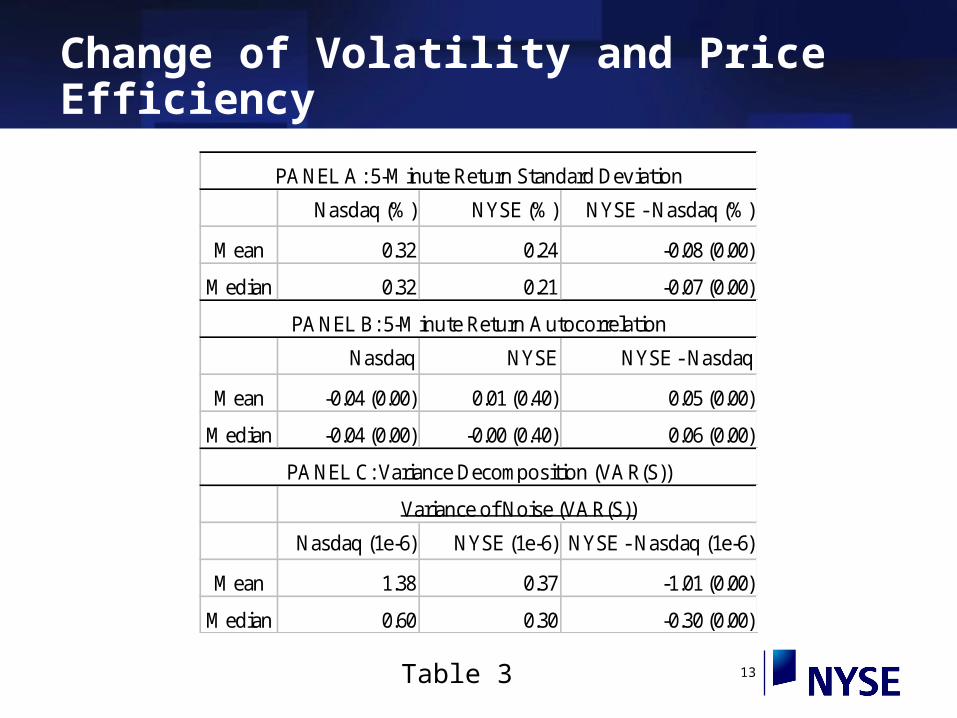

Change of Volatility and Price Efficiency

Nasdaq (%) NYSE (%) NYSE - Nasdaq (%)

Mean 0.32 0.24 -0.08 (0.00)

Median 0.32 0.21 -0.07 (0.00)

Nasdaq NYSE NYSE - Nasdaq

Mean -0.04 (0.00) 0.01 (0.40) 0.05 (0.00)

Median -0.04 (0.00) -0.00 (0.40) 0.06 (0.00)

Nasdaq (1e-6) NYSE (1e-6) NYSE - Nasdaq (1e-6)

Mean 1.38 0.37 -1.01 (0.00)

Median 0.60 0.30 -0.30 (0.00)

PANEL A: 5-Minute Return Standard Deviation

PANEL B: 5-Minute Return Autocorrelation

PANEL C: Variance Decomposition (VAR(S))

Variance of Noise (VAR(S))

Table 3

14

Variance DecompositionHasbrouck (1993)

S is measured at a trade-by-trade basis. P is computed as natural log.

Pt = mt + st , where mt is the efficient price

Magnitude of Pricing Error

Nasdaq NYSE Nasdaq - NYSE

VAR(S) 1.384 *10-6 0.374*10-6 1.010 *10-6

(0.000)

STD (S) 0.1176 cents 0.0611 cents 0.057(0.000)

15

Change of VolatilityFigure 1

Daily 5-Minute Interval Price Range(High - Low)

0

2

4

6

8

10

12

-60

-52

-44

-36

-28

-20

-12 -4 4 12 20 28 36 44 52

Event Window

Pri

ce R

ang

e ($

0.01

)

Nasdaq = 8.3 c

NYSE = 4.0 c

16

Intraday VolatilityFigure 2

Intraday 5-Minute Interval Price Range (High- Low)

0

5

10

15

20

25

30

1 9 17 25 33 41 49 57 65 73

Intraday Interval

Pri

ce R

ang

e ($

0.01

)

Nasdaq

NYSE

17

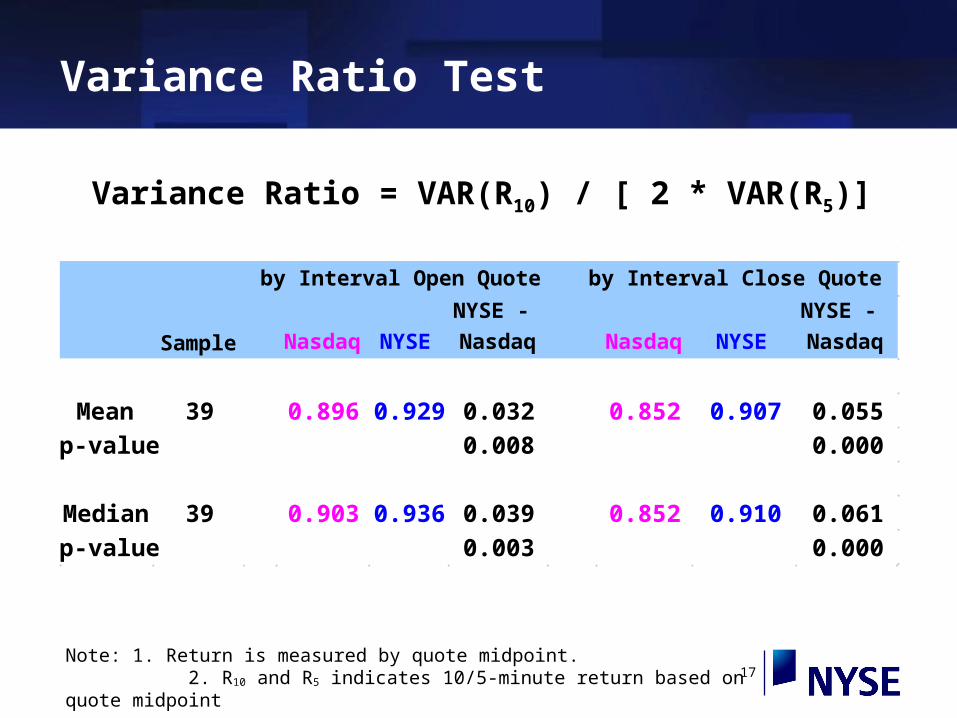

Variance Ratio Test

Variance Ratio = VAR(R10) / [ 2 * VAR(R5)]

Note: 1. Return is measured by quote midpoint. 2. R10 and R5 indicates 10/5-minute return based on quote midpoint

Sample Nasdaq NYSE

NYSE -

Nasdaq Nasdaq NYSE

NYSE -

Nasdaq

Mean 39 0.896 0.929 0.032 0.852 0.907 0.055

p-value 0.008 0.000

Median 39 0.903 0.936 0.039 0.852 0.910 0.061

p-value 0.003 0.000

by Interval Open Quote by Interval Close Quote

18

Effective SpreadsTable 2

• SEC 11Ac1 – 5 Reports

• Difference between transaction price to quote midpoint at order arrival time (x2)

• Caveats– Accuracy (idiosyncratic errors)– Order types– Cancellation rates– Time measurements for effective spreads

19

Change of Spreads

NASDAQ NYSE NYSE-Nasdaq NASDAQ NYSE NYSE-Nasdaq

Mean 9.19 5.94 -3.25 (0.00) 37.13 27.33 -9.80 (0.01)

Median 7.63 5.84 -1.71 (0.00) 31.57 23.37 -4.90 (0.00)

NASDAQ NYSE NYSE-Nasdaq NASDAQ NYSE NYSE-Nasdaq

Mean 8.50 5.57 -2.93 (0.00) 34.03 25.30 -8.72 (0.00)

Median 6.51 5.02 -1.12 (0.00) 28.34 23.13 -3.10 (0.00)

NASDAQ NYSE NYSE-Nasdaq NASDAQ NYSE NYSE-Nasdaq

Mean 4.51 -0.42 -4.93 (0.01) 16.66 -0.51 -17.18 (0.00)

Median 1.75 -0.23 -2.01 (0.00) 6.21 -0.01 -6.50 (0.00)

Panel A: Quoted Spread

Quoted Spread ($0.01) Quoted Spread Relative to Price (bp)

Panel B: Effective Spread

Effective Spread (ES) ($0.01) Effective Spread Relative to Price (bp)

Panel C: Realized Spread

Realized Spread (RS) ($0.01) Realized Spread Relative to Price (bp)

Table 4

20

Daily NBBO Spread between Nasdaq and NYSE

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

-60 -50 -40 -30 -20 -10 0 10 20 30 40 50

Event Window

NB

BO

Sp

read

($0

.01) Nasdaq = 9.2 c

NYSE = 5.7 c

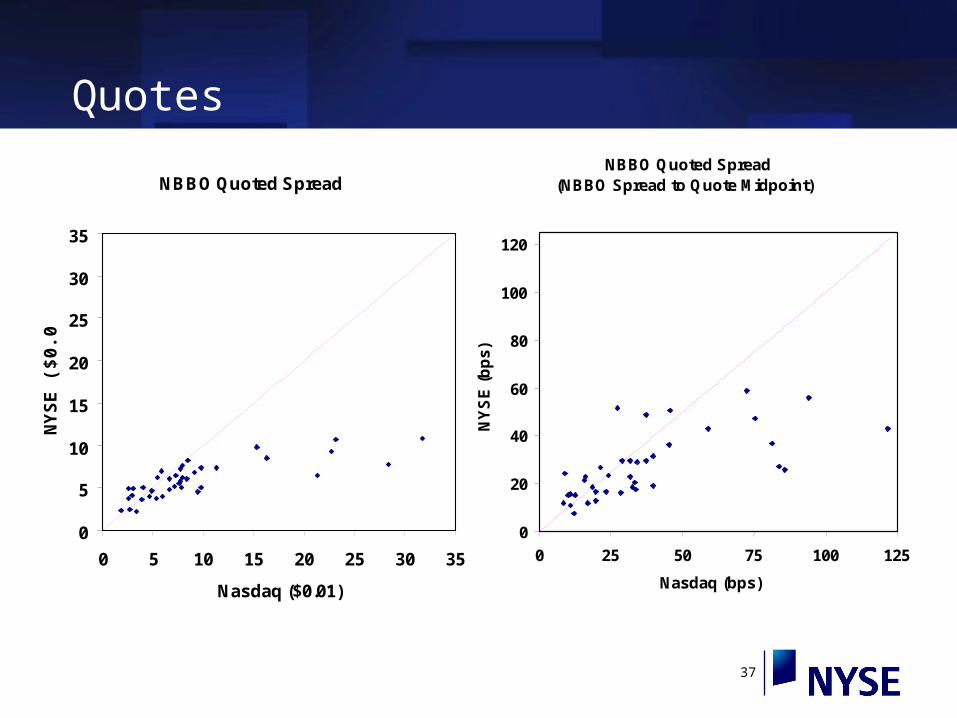

QuotesFigure 3

21

Intraday QuoteFigure 4

Intraday NNBO Quoted Spread

0

0.05

0.1

0.15

0.2

0.25

1 12 23 34 45 56 67 78

Intraday 5-Minute Interval

NB

BO

Sp

read

($0.

01)

Nasdaq

NYSE

22

Effective SpreadsFigure 5

0246

81012

Eff

ecti

ve S

pre

ad

($0.

01)

-3 -2 -1 1 2 3

Months Relative to Switch

Share-weighted Monthly Effective Spread

Nasdaq NYSE

23

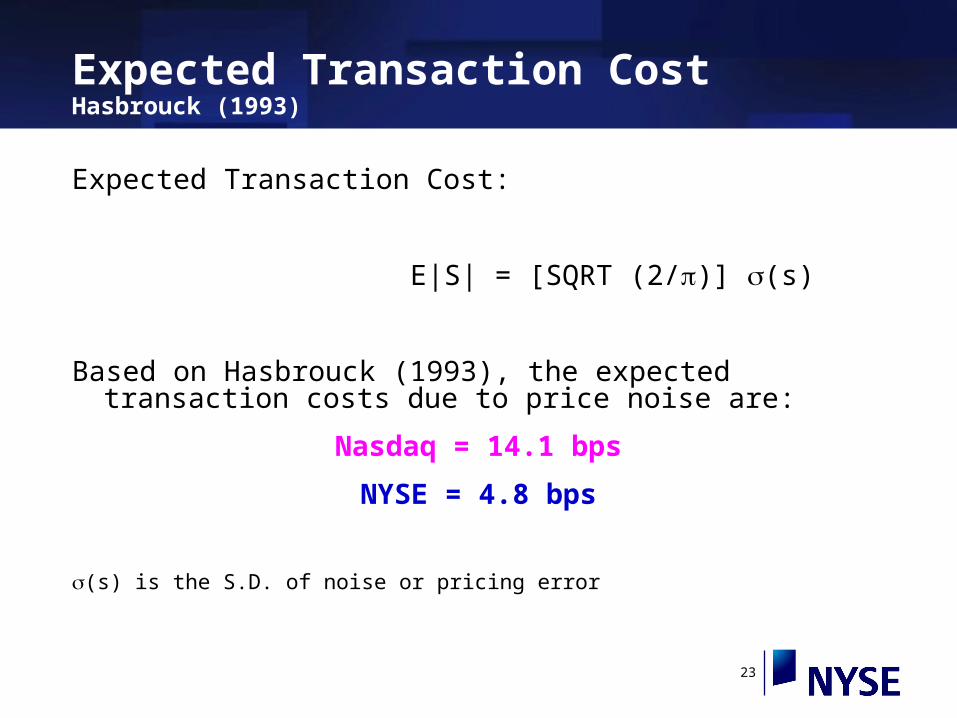

Expected Transaction CostHasbrouck (1993)

Expected Transaction Cost:

E|S| = [SQRT (2/)] (s)

Based on Hasbrouck (1993), the expected transaction costs due to price noise are:

Nasdaq = 14.1 bps

NYSE = 4.8 bps

(s) is the S.D. of noise or pricing error

24

Selection Bias

• Simple Comparison– 39 transferring stock

– 660 Nasdaq NYSE-eligible stocks

• Matching Sample – Select 39 Nasdaq “sister” stocks

– Mcap, volume, volatility, price

• Heckman (1997) 2-Stage Probit Model– 660 firms in the first stage probit regression

25

Simple Comparison

• Variables– Market Cap + Daily Trading Volume + Price

– Daily High-Low Price Range & Daily Return Volatility

– Share Outstanding,

– Daily Close-to-Close Return,

– Registered Market Maker Count

– Distance

– SIC Exchange Industry Concentration Index by mcap

• Compare medians

26

Matching Sample

• 39 non-switching Nasdaq sisters – Match: MCAP, Trading Volume, Return Volatility,

Price

– 2001 matching period

• Replicate analysis on sisters

• Sisters: No significant changes between the 60-day pre-switch and post-switch periods.

27

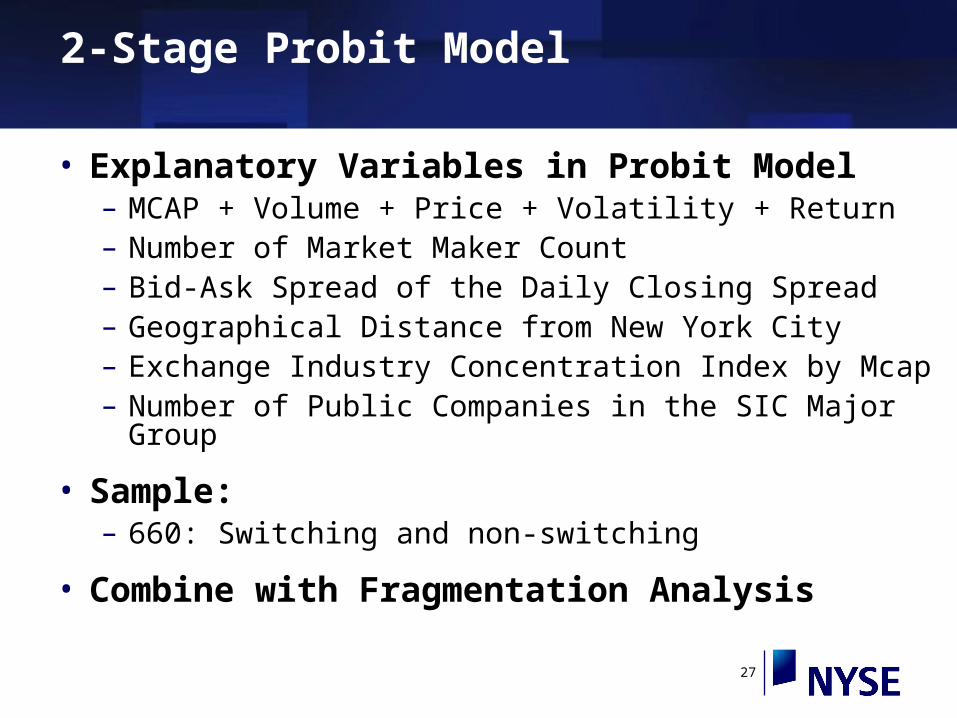

2-Stage Probit Model

• Explanatory Variables in Probit Model– MCAP + Volume + Price + Volatility + Return– Number of Market Maker Count– Bid-Ask Spread of the Daily Closing Spread– Geographical Distance from New York City– Exchange Industry Concentration Index by Mcap– Number of Public Companies in the SIC Major Group

• Sample: – 660: Switching and non-switching

• Combine with Fragmentation Analysis

28

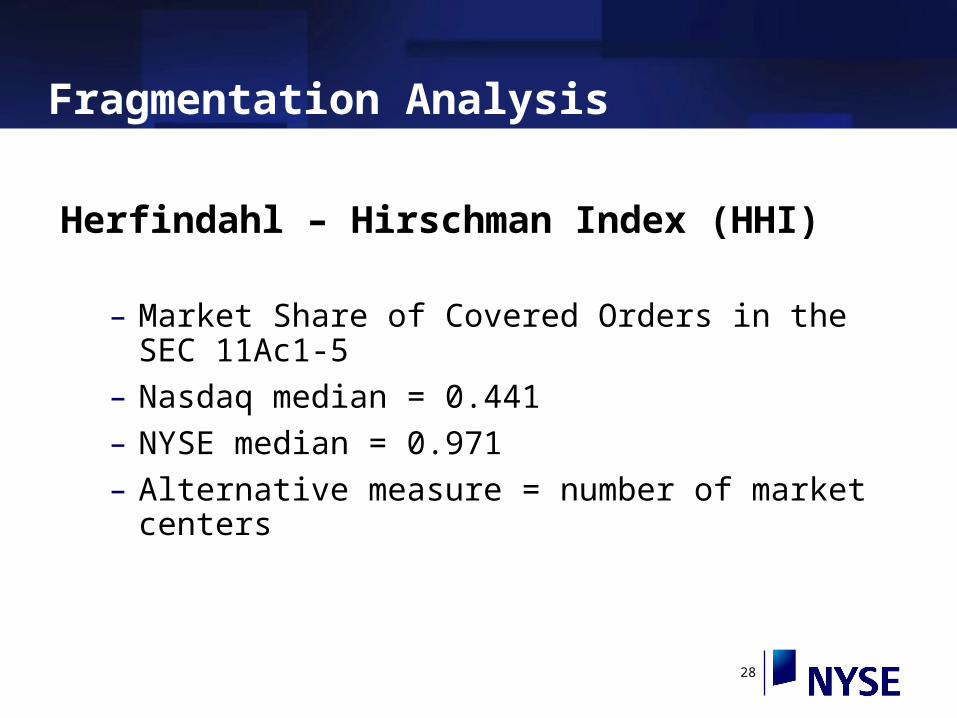

Fragmentation Analysis

Herfindahl – Hirschman Index (HHI)

– Market Share of Covered Orders in the SEC 11Ac1-5

– Nasdaq median = 0.441

– NYSE median = 0.971

– Alternative measure = number of market centers

29

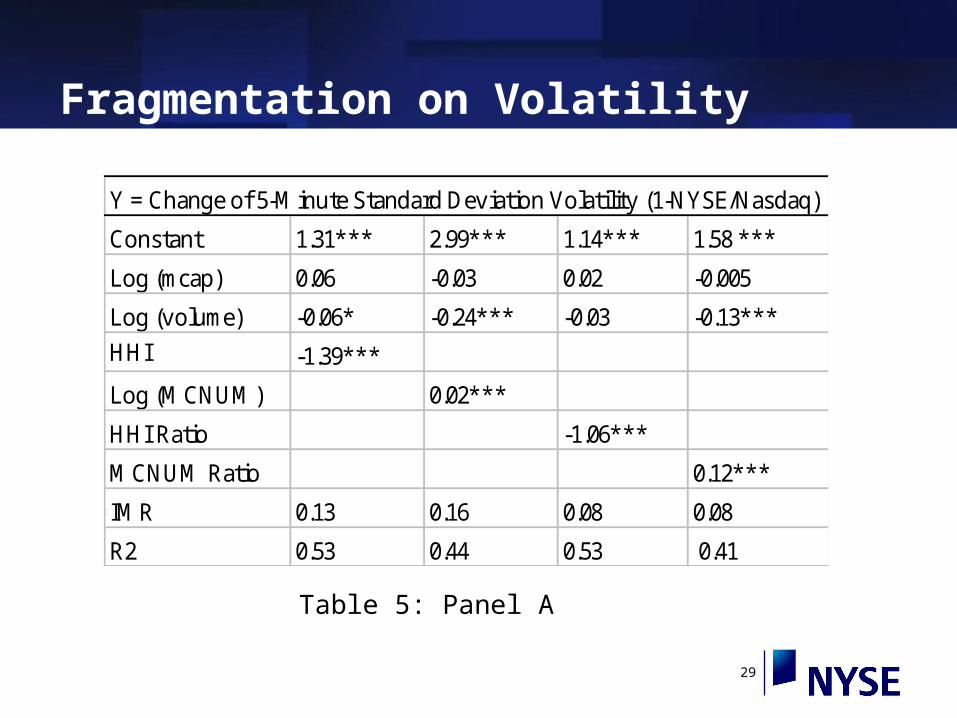

Fragmentation on Volatility

Y = Change of 5-Minute Standard Deviation Volatility (1-NYSE/Nasdaq)

Constant 1.31*** 2.99*** 1.14*** 1.58 ***

Log (mcap) 0.06 -0.03 0.02 -0.005

Log (volume) -0.06* -0.24*** -0.03 -0.13***

HHI -1.39***

Log (MCNUM) 0.02***

HHI Ratio -1.06***

MCNUM Ratio 0.12***

IMR 0.13 0.16 0.08 0.08

R2 0.53 0.44 0.53 0.41

Table 5: Panel A

30

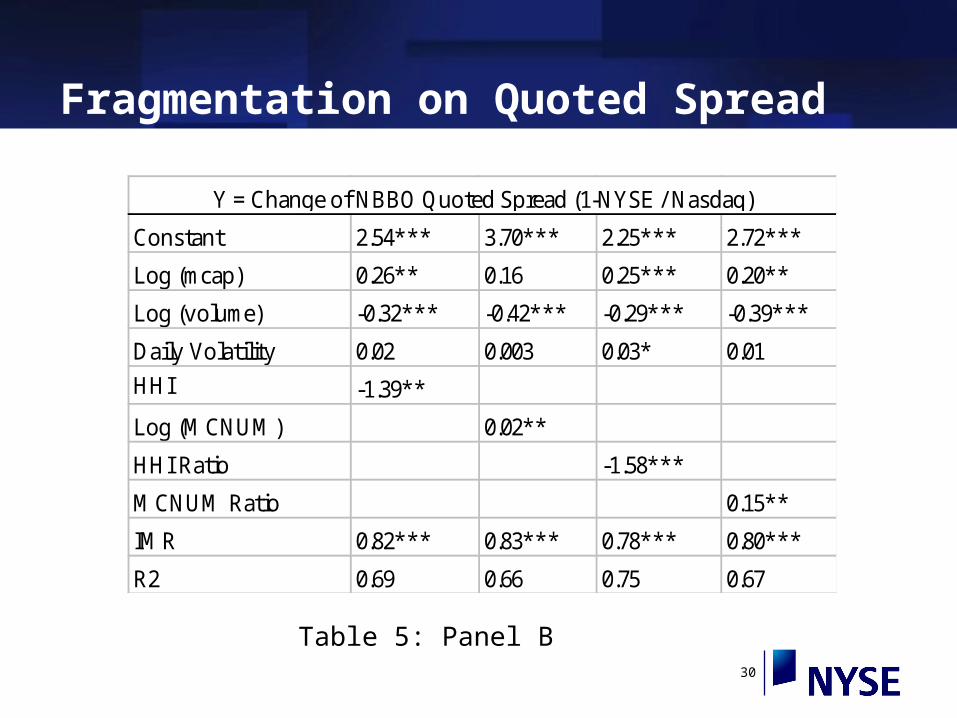

Fragmentation on Quoted Spread

Constant 2.54*** 3.70*** 2.25*** 2.72***

Log (mcap) 0.26** 0.16 0.25*** 0.20**

Log (volume) -0.32*** -0.42*** -0.29*** -0.39***

Daily Volatility 0.02 0.003 0.03* 0.01

HHI -1.39**

Log (MCNUM) 0.02**

HHI Ratio -1.58***

MCNUM Ratio 0.15**

IMR 0.82*** 0.83*** 0.78*** 0.80***

R2 0.69 0.66 0.75 0.67

Y = Change of NBBO Quoted Spread (1-NYSE / Nasdaq)

Table 5: Panel B

31

Fragmentation on Effective Spread

Constant 1.59*** 2.82*** 1.38*** 1.64***

Log (mcap) 0.04 0.002 0.05 0.04

Log (volume) -0.12*** -0.26*** -0.10*** -0.19***

Daily Volatility 0.02 0.01 0.02 0.01

HHI -0.72*

Log (MCNUM) 0.02**

HHI Ratio -0.97**

MCNUM Ratio 0.16**

IMR 0.13 0.21 0.11 0.15

R2 0.41 0.43 0.45 0.42

Y = Change of Effective Spread (1-NYSE / Nasdaq)

Table 5: Panel C

32

Conclusions

• NYSE provides better liquidity provision and price efficiency.

• Order Flow Fragmentation Affects Market Quality

• Competition among market centers does not dominate the benefits of order flow consolidation

• Market fragmentation is particular detrimental for less liquid securities.

33

34

Market Capitalization

0

2,000

4,000

6,000

8,000

10,000

1 6 11 16 21 26 31 36

Company in Order of Their Transfer Date

MC

AP

($M

illi

on

)

Market Capitalization

Regions Financial Co.5/3/02$8 Billion

Concord EFS Co.11/7/02$7.3 Billion

II

35

Daily and 5-Minute Volatility

Daily Volatility (S.T. of Daily Close-to-Close Return)

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

0.000 1.000 2.000 3.000 4.000 5.000 6.000 7.000 8.000

Nasdaq (%)

NY

SE

(%)

5-Minute Volatility(S.T. of 5-Minute Return)

0.000

0.200

0.400

0.600

0.800

1.000

0.000 0.200 0.400 0.600 0.800 1.000

Nasdaq (%)

NY

SE

(%

)

36

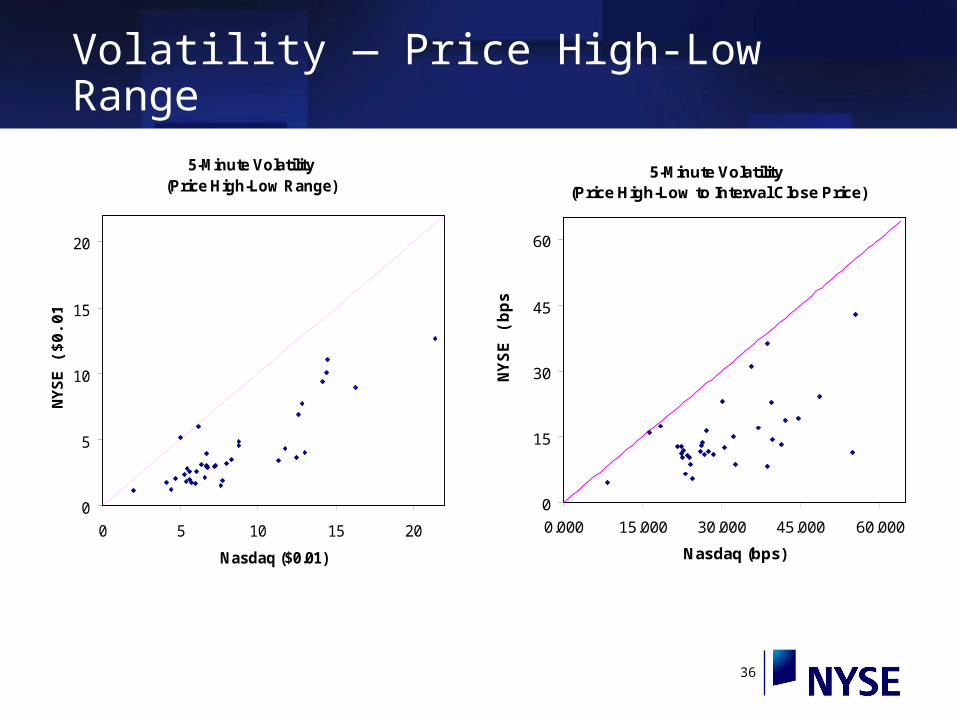

Volatility — Price High-Low Range

5-Minute Volatility (Price High-Low to Interval Close Price)

0

15

30

45

60

0.000 15.000 30.000 45.000 60.000

Nasdaq (bps)

NY

SE

(b

ps

)

5-Minute Volatility(Price High-Low Range)

0

5

10

15

20

0 5 10 15 20

Nasdaq ($0.01)

NY

SE

($0.

01)

37

Quotes

NBBO Quoted Spread

0

5

10

15

20

25

30

35

0 5 10 15 20 25 30 35

Nasdaq ($0.01)

NY

SE

($

0.0

1)

NBBO Quoted Spread (NBBO Spread to Quote Midpoint)

0

20

40

60

80

100

120

0 25 50 75 100 125

Nasdaq (bps)

NY

SE

(b

ps)