market outlook 130412

TRANSCRIPT

8/2/2019 Market Outlook 130412

http://slidepdf.com/reader/full/market-outlook-130412 1/4

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539 1

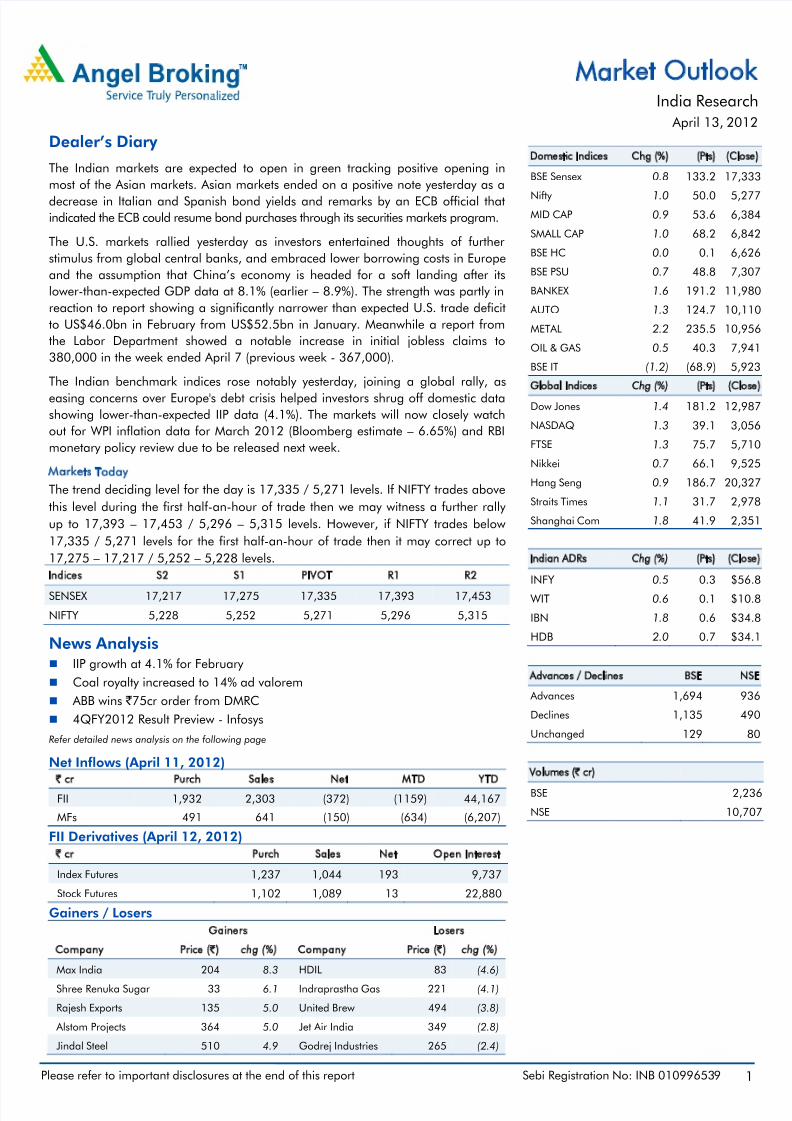

Market OutlookIndia Research

April 13, 2012

Dealer’s Diary

The Indian markets are expected to open in green tracking positive opening in

most of the Asian markets. Asian markets ended on a positive note yesterday as a

decrease in Italian and Spanish bond yields and remarks by an ECB official thatindicated the ECB could resume bond purchases through its securities markets program.

The U.S. markets rallied yesterday as investors entertained thoughts of further

stimulus from global central banks, and embraced lower borrowing costs in Europe

and the assumption that China’s economy is headed for a soft landing after its

lower-than-expected GDP data at 8.1% (earlier – 8.9%). The strength was partly in

reaction to report showing a significantly narrower than expected U.S. trade deficit

to US$46.0bn in February from US$52.5bn in January. Meanwhile a report from

the Labor Department showed a notable increase in initial jobless claims to

380,000 in the week ended April 7 (previous week - 367,000).

The Indian benchmark indices rose notably yesterday, joining a global rally, as

easing concerns over Europe's debt crisis helped investors shrug off domestic datashowing lower-than-expected IIP data (4.1%). The markets will now closely watch

out for WPI inflation data for March 2012 (Bloomberg estimate – 6.65%) and RBI

monetary policy review due to be released next week.

Markets Today

The trend deciding level for the day is 17,335 / 5,271 levels. If NIFTY trades above

this level during the first half-an-hour of trade then we may witness a further rally

up to 17,393 – 17,453 / 5,296 – 5,315 levels. However, if NIFTY trades below

17,335 / 5,271 levels for the first half-an-hour of trade then it may correct up to

17,275 – 17,217 / 5,252 – 5,228 levels.

Indices S2 S1 PIVOT R1 R2

SENSEX 17,217 17,275 17,335 17,393 17,453

NIFTY 5,228 5,252 5,271 5,296 5,315

News Analysis IIP growth at 4.1% for February

Coal royalty increased to 14% ad valorem

ABB wins ` 75cr order from DMRC

4QFY2012 Result Preview - Infosys

Refer detailed news analysis on the following page

Net Inflows (April 11, 2012)

` cr Purch Sales Net MTD YTD

FII 1,932 2,303 (372) (1159) 44,167

MFs 491 641 (150) (634) (6,207)

FII Derivatives (April 12, 2012)

` cr Purch Sales Net Open Interest

Index Futures 1,237 1,044 193 9,737

Stock Futures 1,102 1,089 13 22,880

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Max India 204 8.3 HDIL 83 (4.6)

Shree Renuka Sugar 33 6.1 Indraprastha Gas 221 (4.1)

Rajesh Exports 135 5.0 United Brew 494 (3.8)

Alstom Projects 364 5.0 Jet Air India 349 (2.8)

Jindal Steel 510 4.9 Godrej Industries 265 (2.4)

Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex 0.8 133.2 17,333

Nifty 1.0 50.0 5,277MID CAP 0.9 53.6 6,384

SMALL CAP 1.0 68.2 6,842

BSE HC 0.0 0.1 6,626

BSE PSU 0.7 48.8 7,307

BANKEX 1.6 191.2 11,980

AUTO 1.3 124.7 10,110

METAL 2.2 235.5 10,956

OIL & GAS 0.5 40.3 7,941

BSE IT (1.2) (68.9) 5,923

Global Indices Chg (%) (Pts) (Close)

Dow Jones 1.4 181.2 12,987

NASDAQ 1.3 39.1 3,056

FTSE 1.3 75.7 5,710

Nikkei 0.7 66.1 9,525

Hang Seng 0.9 186.7 20,327

Straits Times 1.1 31.7 2,978

Shanghai Com 1.8 41.9 2,351

Indian ADRs Chg (%) (Pts) (Close)

INFY 0.5 0.3 $56.8

WIT 0.6 0.1 $10.8

IBN 1.8 0.6 $34.8

HDB 2.0 0.7 $34.1

Advances / Declines BSE NSE

Advances 1,694 936

Declines 1,135 490

Unchanged 129 80

Volumes (` cr)

BSE 2,236

NSE 10,707

8/2/2019 Market Outlook 130412

http://slidepdf.com/reader/full/market-outlook-130412 2/4

Market Outlook | India Research

April 13, 2012 2

IIP growth at 4.1% for February

The industrial production (IIP) growth was sluggish for the month of February,

registering a growth of 4.1% yoy, which was well below the Bloomberg consensus

estimates of 6.7% yoy. January IIP figures were significantly downwardly revised to

1.1% yoy from 6.8% yoy. The 12-month rolling industrial production growth,

which has been on a declining trend since November 2010 (9.9%), slipped

further to 4.5% yoy.

The 8.5% manufacturing growth for January was downwardly revised to 1.4%

yoy. For February too, the manufacturing index growth was modest at 4.0% yoy.

However, on the positive side, 18 out of 22 industry groups in the manufacturing

sector registered above zero growth during February 2012.

Mining activity recorded expansion for the first time in 7 months, growing by 2.1%

yoy. However, the growth can be partly attributed to the low base effect (6.4%mom contraction in mining activity in February 2011). Growth in electricity

production which had moderated down to 3.2% yoy in January 2012, revived in

February 2012, growing by 8.0% yoy.

As per use-based data, growth was primarily contributed by 10.6% yoy growth in

capital goods sector (low base effect created due to 10.2% mom contraction in

capital goods index in February 2011) and 7.5% yoy growth in basic goods

index.

Coal royalty increased to 14% ad valorem

India's Cabinet has announced to increase royalty on coal to ad valorem 14%

based on its pit-head price. Currently royalty on coal is charged at the rate of 5%

plus fixed charge which range from ` 55-130/tonne depending on the coal grade.

For Coal India, the royalty is borne by it's customers and hence there will be no

impact on its financials. Hence, we retain our estimates on Coal India and

maintain our Neutral stance. However, this move will increase coal costs for steel,

aluminium and sponge iron companies by 4-10% depending on the grade of

coal purchased by them. Since steel and aluminium players sell their products at

a price based on global benchmarks, the additional royalty costs will have to be

absorbed by them thus affecting their margins slightly.

ABB wins ` 75cr order from DMRC

ABB has announced it has won an order worth ` 75cr from Delhi Metro Rail

Corporation (DMRC). ABB is required to complete the power infrastructure for

stage 1 of the east west corridor of Jaipur Mass Rapid Transport System (MRTS).

The project scope includes electrification of overhead lines, provision of auxiliary

substations and supply of SCADA solution. The new order contributes

insignificantly to ABB’s order book (less than 1% of order book, which stands at

` 9,129cr). We maintain our Sell recommendation on the stock with a target

price of `503.

8/2/2019 Market Outlook 130412

http://slidepdf.com/reader/full/market-outlook-130412 3/4

Market Outlook | India Research

April 13, 2012 3

Result Preview

Infosys

Infosys is slated to announce its 4QFY2012 results. We expect the company to

post merely 0.3% qoq growth in USD revenue to US$1811mn on the back of qoq

flat volume growth. In rupee terms, revenue is expected to come in at ` 9,100cr,

down 2.1% qoq due to qoq ~1.2% INR appreciation against USD. EBITDA

margin is expected to decline by 59bp qoq to 33.1%. PAT for the quarter is

expected to come in at ` 2,310cr.

Key points to watch out for are a) USD revenue growth guidance for FY2013,

the upper end of which should exceed Nasscom’s guidance of 11-14%, else it will

be negative for the stock and b) management’s commentary on the macro picture

and scenario in decision making by clients. We maintain our Buy rating on the

stock with a target price of `3,348.

Quarterly Bloomberg Brokers’ Consensus Estimates

Infosys Ltd – Consolidated (13/04/2012)

Particulars (` cr) 4QFY12E 4QFY11 yoy (%) 3QFY12 qoq (%)

Net sales 9,186 7,250 27 9,298 (1)

Net profit 2,309 1,818 27 2,372 (3)

Economic and Political News

FDI in airlines: Cabinet to decide in a few weeks

Government approves Public Procurement Bill

Government approves Air India financial restructuring

IIP data to have bearing on monetary policy: Pranab Mukherjee

Corporate News

Cabinet approves Neyveli's proposed JV for power project

Jet Airways delays airport payments

NBCC looks at overseas opportunities for expansion Suzlon Energy bags order to supply turbines to U.K.'s Renerco

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Results Calendar

13/04/2012 Infosys

16/04/2012 Crisil, MindTree

18/04/2012 HDFC Bank, HCL Tech, Infotech Enterprises

19/04/2012 Hind Zinc, Ambuja Cements, ACC, IndusInd Bank

20/04/2012 Cairn India, FAG Bearings

8/2/2019 Market Outlook 130412

http://slidepdf.com/reader/full/market-outlook-130412 4/4

Market Outlook | India Research

April 13, 2012 4

Source: Economic Times, Business Standard, Business Line, Financial Express, MintResearch Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investmentdecision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or inthe past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.