market access analysis to identify …trade.ec.europa.eu/doclib/docs/2005/may/tradoc_123220.pdf1...

TRANSCRIPT

1

MARKET ACCESS ANALYSISTO IDENTIFY BARRIERS

IN CHINA AND IN RUSSIA AFFECTINGTHE EU TEXTILES INDUSTRY

Final Report

Franklin DEHOUSSE /Katelyne GHEMAR /Tsonka IOTSOVA

CENTRE D’ETUDES ECONOMIQUES ET INSTITUTIONNELLES - C.E.E.I.

Brussels – 10/04/2000

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 2

MARKET ACCESS ANALYSISTO IDENTIFY BARRIERS

IN CHINA AND IN RUSSIA AFFECTINGTHE EU TEXTILES INDUSTRY

Final Report

Franklin DEHOUSSE / Katelyne GHEMAR / Tsonka IOTSOVA

This Report was prepared with financial assistance from the Commission of theEuropean Communities. The views expressed herein are those of the Consultant, and

do not representany official view of the Commission

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 3

TABLE OF CONTENTS

EXECUTIVE SUMMARY

PART 1:

TRADE AND INVESTMENT BARRIERS IDENTIFIED BY THE EU TEXTILESINDUSTRY

PART 2:

CHINA

PART 3:

RUSSIA

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 4

EXECUTIVE SUMMARY

Objectives

Russian and Chinese markets have been investigated to map out trade obstaclesmet by Community exporters. These barriers hamper Community exports of textilesand clothing products and/or supplies of raw materials (CN Chapters 50 – 63). Thestudy aims to fulfil three objectives: (1) to identify trade obstacles implemented bythese countries; (2) to evaluate the impact such barriers have on EU exports, (3) toassess the compatibility of these restrictions under the terms of international orbilateral agreements.

Work Methodology

In the first phase, the consultant collected information from the EU textiles industry(individual companies, National associations, EURATEX) and Commission servicesin order to identify the most damaging restrictions. In the second phase, moredetailed research was carried out in both countries (missions to China and Russia).In the third phase, a detailed analysis was made on the identified restrictions.

A mission was conducted in China from 29 November to 10 December 1999. Amission to Russia took place from 24 January to 30 January 2000. These missionsaimed at meeting both National administrations and third countries operators(importers and other contacts). After the missions, a legal analysis was conductedon the measures identified as most damaging by the industry.

The main findings

Three fundamental comments must be made:

• EU exporters suffer in both markets from a total lack of transparency of importand export rules, which affects differently their trade flows with China and Russia.

• EU exporters face a large variety of trade restrictions in both markets. Some ofthese measures are of horizontal nature (local taxes for Joint Ventures,implementation of customs duties, customs procedures) while others arespecifically applicable to textiles and clothing (labelling, certification, quotas fortextile products, export restrictions).

• The impact of these measures is much more stringent in China than in Russiawhere exports have much developed, despite the implementation of several traderestrictions.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 5

1. The lack of transparency affects the EU productsbefore and after clearance

The lack of transparency is by far the main obstacle encountered byEU textile and clothing companies in China and Russia. This affectseach step to be followed by the EU producer before shipping thegoods, by the forwarder agent and the Third country importer duringclearance, and the distributor during the retail.

1.1. Before clearance

• the nature of documents for clearance: this can change from one day to another,without prior notification to the EU exporter or the importer.

• the pre-shipment inspections to be conducted, including certification inspections• the exact requirements to be affixed on the labels: in both countries regulations

have set up drastic requirements, which would completely hamper exports if fullyimplemented by Customs Authorities.

• the compliance of requirements concerning certification of products is unclear inparticular in Russia where there are many different certification schemes.Products benefit or suffer from a complete “case by case” approach.

• the exact amount of import duties to be paid: EU companies have often littleinformation on the real level of total import duties charged on their products andthe problems occurring during clearance.

• the nature of products subject to quotas, and therefore to import licence: InChina, the exact positions for which quotas are implemented, their quantitativelevel and the criteria on which the import licenses could be delivered are nottransparent.

1.2. During clearance

• Customs Authorities require constantly new documents. Suddenly new types ofimport authorisations are required for a specific product (China) or importdocuments are requested in specific format (Russia). These practices delayexports and constitute strong disincentives for EU exporters.

• The implementation of minimum or reference prices for certain products is alsoseen as uncertain and blackmail by certain EU exporters. This involves moreparticularly imports of fabrics in Russia. However, valuation remains a strongconcern for China.

• There are physical checks on imported goods concerning the productcomposition, the compliance of labelling and certification rules.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 6

1.3. After clearance

• Controls conducted on imported goods are often reported to be stringent incertain cases: This is for instance the case for labels and certificates in Russia.

• Distribution schemes are not transparent neither in Russia nor in China, wheremany restrictions remain and will hamper potential exports of clothing products.

2. There are both horizontal and specific restrictions

2.1. In China, more trade barriers were identified

• China implements a large variety of trade restrictions affecting either (1) theimport of textile products, (2) the processing of textile products by EU companiesand their distribution on the domestic market or (3) the export of some rawmaterials. Some barriers are of horizontal nature, the rest being specificallyapplied for textiles.

a) Horizontal measures

These measures also affect EU exports or investments in other industrial sectors.

• Changes in customs rules: in particular affecting inward processing rules, whileimporters are classified among different categories.

• Export performance rates for Joint Ventures (JV): it is alleged that different exportperformance levels are implemented.

• Local taxes: EU–Chinese JV and EU companies are required to pay anincreasing number and amount of local taxes, which are alleged not be chargedequally on local producers.

• Distribution rules still hamper the development of independent shops selling EUoutlets.

• State trading affects in particular the supply and the costs of raw materials for EUsilk producers and the distribution of EU products imported into China. Despiterecent changes, it is still problematic for EU producers.

b) Measures affecting textiles

• Import quotas are enforced on about 50 tariff lines. The delivery process ofimport license hampers dramatically (1) direct imports of EU products, (2) EUcompanies having realised huge investment to produce and distribute on thedomestic market with imported raw materials subject to quotas. The quotaimplementation is considered by far by various EU producers as the main tradebarrier.

• Labelling rules: contain strict requirements. However, their implementation is notreported to be damaging EU exports but could constitute a serious obstacle iffully implemented by Chinese Authorities.

• Export restrictions: are still felt discriminatory by EU silk producers.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 7

2.2. In Russia, priorities are certification, customs rules and tariffs

a) Horizontal measures

• Changes in Customs rules: this affects the implementation of customs duties(specific duties), the nature of import documents, the implementation of minimumimport prices (affecting other sectors).

• Rules on distribution: they impede EU producers to distribute themselves theirproducts.

b) Measures affecting textiles

• Tariffs and specific duties: their level is too high and complaints focus on thenon-transparency of the dual calculation system.

• Certification: is felt to be a strong disincentive for some EU exporters, inparticular SME, which will export little quantities and are not used to certificationschemes. However, it has to be stressed that EU companies got used to theircertification schemes over the years under the current system and therefore fearany changes, which could affect the precarious equilibrium they might have foundon that issue with their customers and with Russian Authorities.

• New rules for certification could be soon implemented: The 1999 766 Decree isnot yet implemented. It concerns a limited number of textile products for which aDeclaration of conformity could be made. These rules are presented as animprovement by the Russian authorities. However, EU operators fear theirimplementation for several reasons. For instance, a Foreigner cannot do theDeclaration. Another inconvenient for EU operator is the need to register thedeclaration in a Gosstandart accredited body.

• Transparency: The main problem affecting namely the certification of textileproducts in Russia is the lack of transparency. The implementation rules areoften not made public immediately and EU operators face difficulties to obtain therelevant information.

3. The impact of trade measures affects more severely exports to China

• The trade restrictions in China aim at protecting the domestic industry from EUexports of quality products. Restrictions affecting JV aim at hindering them todistribute their products on the domestic market, and, in certain cases toconstrain them to use Chinese raw materials instead of imported inputs.Changing clearance procedures also target specific products (e.g. requirement ofan import authorisation on synthetic fabrics). This affects and restricts EU tradeflows. This also explains why EU exports to China remain rather limited whereasChina has become our first supplier in textile and clothing products.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 8

• Conversely, exports of EU products to Russia have constantly increased over theyears and are recovering after the 1998 crisis. Trade balance in textile andclothing products remain largely positive. Therefore, import measures applied fortextile products are more felt by EU operators as an illustration of the Russiantrading system, than as a voluntary protectionist policy. This explains why the EUindustry itself is sometimes reluctant to criticise openly the import regime and inparticular the certification system. Big EU exporting companies got used to it andfear a new regulatory system, which would allow more corruption, lesstransparency, and new problems that will hinder their exports.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 9

PART 1

TRADE AND INVESTMENT BARRIERSIDENTIFIED BY THE EU TEXTILES INDUSTRY

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 10

TABLE OF CONTENTS

§1. ORGANISATION OF RESEARCH

1.1. The objectives of the study

1.2. The questionnaire to the EU textiles industry

1.3. The meetings with the textiles EU industry

1.4. The Preliminary Report

1.5. The missions to China and Russia

1.6. The legal analysis

§2. RESULTS OF CONSULTATIONS WITH THE EU TEXTILESINDUSTRIES

2.1. The problems identified for China

2.2. The problems identified for Russia

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 11

PART 1: TRADE AND INVESTMENT BARRIERS IDENTIFIED BY THEEU TEXTILES INDUSTRY

§ 1. ORGANISATION OF RESEARCH

1.1. The objectives of the study

• CEEI research methodology has been adapted to the objectives of the study. Thefirst objective is to identify obstacles implemented by China and Russia. Thesecond objective is to evaluate the impact of such barriers on EU exports oftextile products and EU supply of raw materials. The third objective is to assessthe compatibility of these restrictions under the terms of internationalagreements.

• According to these objectives, in cooperation with the Commission, the first stageof the research was focused on drafting and distributing a standard questionnaireto EU operators, developing geographical files and organising meetings with EUoperators in order to gather precise data on identified barriers. During the secondstage, field missions were organised in China and Russia. The third stage wasdevoted to legal analysis and drafting of the Final Report.

1.2. The questionnaire to the EU textiles industry

• The first task carried out by the consultant was the identification of trade barriersto the EU industry in countries under review and the evaluation of these barriersimpact on producers. For this purpose, a questionnaire was drafted in co-operation with EURATEX and the Commission and sent to EURATEX Membersand individual companies which had already mentioned having difficulties toexport to these markets (1998-1999 CEEI Textile Market Access Study 1).

• The questionnaires aimed at giving a preliminary overview of problems (barriers)encountered by European operators when exporting their products or importingtheir raw materials. The Industry was invited to give its comments on the barriersit is encountering and the impact barriers have on their individual business.

• The questionnaire presented a selection of barriers with practical examples.Operators were also invited to define the scope of problems encountered (traderestrictions, administrative problems, additional costs).

1 "Market Access Study to identify trade barriers affecting the EU textiles industry in certain thirdcountry markets" Final Report: 23 March 1999.EC site: (http: //www.europa.eu.int/comm/trade/mk_access/legis.htm).

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 12

• Operators were requested to indicate the possible effects of identified barriers ontheir own situation (additional costs, markets and production losses…). Thequestionnaire was meant to be a starting point followed up by interviews.

1.3. The meetings with the EU textiles industry

1.3.1. The meetings with textile companies

• CEEI attended meetings with EU companies who had returned completedquestionnaires in order to obtain more details on barriers, which had beensignalled. Some other companies preferred having a meeting with the consultantinstead of completing the questionnaire.

• These meetings were organised with management representatives and, in certaincases, with persons in charge of customs procedures. These conversations werefruitful because they pointed out specific and practical cases of problemsencountered by the companies:

- When preparing the import documentation (certification, products compositionissues);

- When having invested in the countries under review, problems encountered bythe local staff with Third countries Authorities;

- Additional costs caused by the implementation of technical barriers or requestedinspections (pre-shipment, certification, labelling issues);The meetings were organised with companies of different textile sub-sectors(carpets, fabrics, and apparel).

1.3.2. The meetings with textile associations

• Co-operation with EURATEX was followed on a continuous basis. Contactsdeveloped with EURATEX representatives enabled the consultant to be providedwith:

- Basic information on the main problems registered by this associationet European level;

- Information on persons and companies of the textile and apparelindustry to be contacted.

• The consultant received full support from EURATEX during the research. Inaddition, meetings were organised with the most motivated and representativeIndustry associations. These associations know their export oriented members(those who answered questionnaires). They can also gather operators fromdifferent sub-sectors of the textiles industry. They distributed the questionnairesto the most oriented export companies.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 13

1. The first mission was organised by the Finnish Textiles and Clothing Association(28 October – 1 November 1999). This mission mainly focused on the problemsof access to the Russian market. The association organised various meetingsand visits to Finnish companies exporting to Russia and having developed aninteresting export practice to this market.

2. Two missions took place in Milan (11 November and 22 November 1999) in orderto meet the Representatives of the Italian Industry (Federtessile, AssociationSerica Italiana) and individual companies which have developed their exports toor have made investments in China.

3. Contacts organised with the support of French Knitting Association. .

4. Contacts were also taken with the German Knitting association.

5. Several contacts were developed with the European Carpet Association (ECA)and the Belgium Textile Association (FEBELTEX).

6. These meetings gave CEEI more precise information on trade practices andbarriers. There were successful and gave the opportunity of further contacts withenterprises and their agents or customers. This helped the consultant to organiseinterviews in the countries under review.

1.3.3. Meetings with Commission services

• The consultant arranged several meetings with various Commission officials inthe different services concerned by the study:

- Meetings with DG Trade, Textile Unit and Market Access Unit- Meetings with DG Enterprises representatives (textiles and TBT)- Meetings with EC Delegations in China and Russia.

1.4. The Preliminary Report

• The Preliminary report was delivered to the Commission services on 3 January2000. This report summarised the results of the research phase with the EUtextiles industry (questionnaires, meetings, personal interviews). It alsopresented the main outcomes of the mission conducted in China.

1.5. The missions to China and Russia

• CEEI missions were organised as follows:

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 14

1. The first mission took place from 29 November to 10 December 1999 to Chinaand Hongkong.

2. The second mission took place in Moscow and St Petersburg from 24 January to2 February 2000.

• During these missions, the consultant has conducted interviews with thecompetent national authorities (commerce, industry, customs) and some privatesector representatives (importers, distribution, forwarders, Customs agents). Theobjective was to get a more precise idea on the implementation of barriersidentified by the industry and to gather the legal and administrative informationnecessary to the constitution of the legal files.

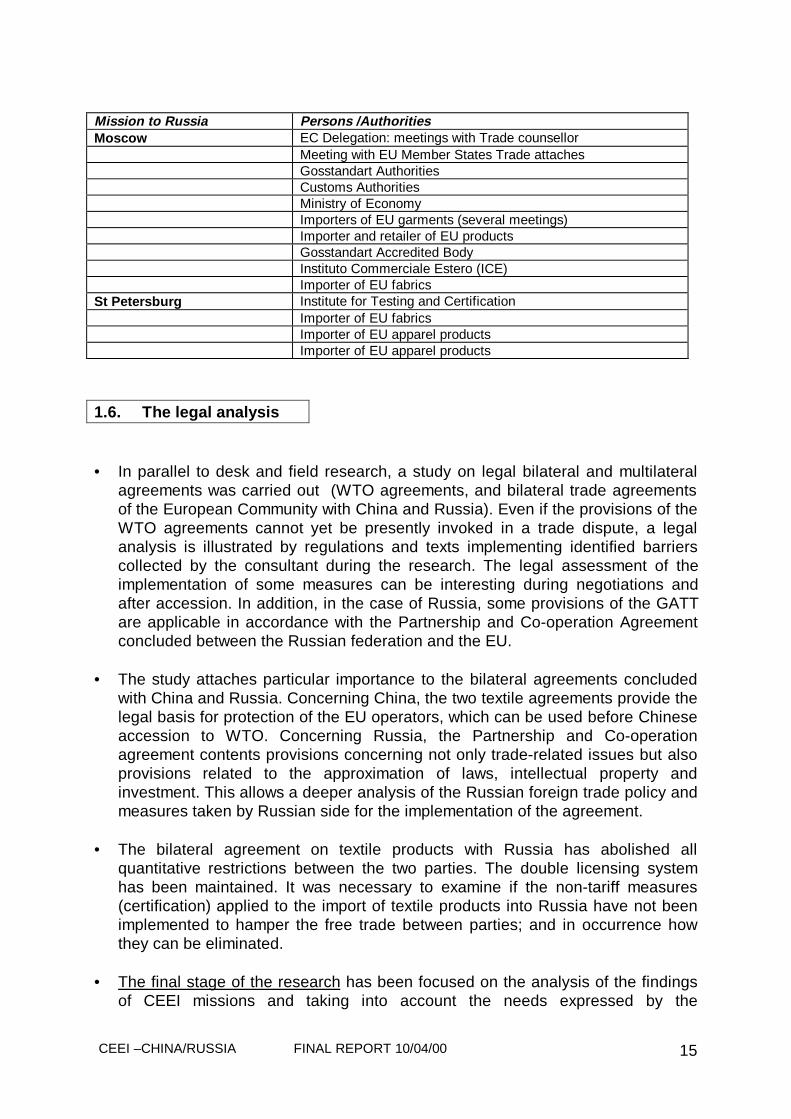

• Entities and persons interviewed during these missions are as follows:

Mission to China Persons /AuthoritiesHong-Kong EC Delegation: meetings with Head of Delegation, Trade counsellors.

PEE French Embassy: meetings with Head of Post, trade counsellorsPEE French Embassy: meetings with several agents and importers ofFrench productsEC Delegation/Spanish Chamber of Commerce: meeting with importers

Shanghai EU/Chinese JVEU/Chinese JVPEE French Embassy: Trade counsellorImporter of EU fabrics, agent of EU companyForwarder importing inputs for EU companiesVisit to Department stores

Beijing EC Delegation: meetings with Trade counsellor and Trade adviserMOFTECCustoms AuthoritiesChina National Import Export Corporation (CNSIEC)EU/Chinese JV importing textiles and ClothingChinese Import export cpy importing EU fabricsEU Forwarder AgentDebriefing Meeting with EU Member StatesSIQ (State agency for commodity inspections)

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 15

Mission to Russia Persons /AuthoritiesMoscow EC Delegation: meetings with Trade counsellor

Meeting with EU Member States Trade attachesGosstandart AuthoritiesCustoms AuthoritiesMinistry of EconomyImporters of EU garments (several meetings)Importer and retailer of EU productsGosstandart Accredited BodyInstituto Commerciale Estero (ICE)Importer of EU fabrics

St Petersburg Institute for Testing and CertificationImporter of EU fabricsImporter of EU apparel productsImporter of EU apparel products

1.6. The legal analysis

• In parallel to desk and field research, a study on legal bilateral and multilateralagreements was carried out (WTO agreements, and bilateral trade agreementsof the European Community with China and Russia). Even if the provisions of theWTO agreements cannot yet be presently invoked in a trade dispute, a legalanalysis is illustrated by regulations and texts implementing identified barrierscollected by the consultant during the research. The legal assessment of theimplementation of some measures can be interesting during negotiations andafter accession. In addition, in the case of Russia, some provisions of the GATTare applicable in accordance with the Partnership and Co-operation Agreementconcluded between the Russian federation and the EU.

• The study attaches particular importance to the bilateral agreements concludedwith China and Russia. Concerning China, the two textile agreements provide thelegal basis for protection of the EU operators, which can be used before Chineseaccession to WTO. Concerning Russia, the Partnership and Co-operationagreement contents provisions concerning not only trade-related issues but alsoprovisions related to the approximation of laws, intellectual property andinvestment. This allows a deeper analysis of the Russian foreign trade policy andmeasures taken by Russian side for the implementation of the agreement.

• The bilateral agreement on textile products with Russia has abolished allquantitative restrictions between the two parties. The double licensing systemhas been maintained. It was necessary to examine if the non-tariff measures(certification) applied to the import of textile products into Russia have not beenimplemented to hamper the free trade between parties; and in occurrence howthey can be eliminated.

• The final stage of the research has been focused on the analysis of the findingsof CEEI missions and taking into account the needs expressed by the

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 16

Commission and the EU industry. The objective is to constitute detailed files onboth countries, each identified restriction has been assessed as follows in part II(China) and part III (Russia) of the present Report:

(1) explanation of the measures based on legal texts and description given bythird country authorities (referred as "Measures");

(2) implementation of the measures in the third country, based on interviewsconducted with importers, agents of EU products and customs agents(referred as "Implementation");

(3) a legal comment on its compatibility under the present internationalagreements (referred as "Legality").

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 17

§2. RESULTS OF CONSULTATIONS WITHTHE EU TEXTILES INDUSTRIES

• Consultations with the EU textile industries started with the distribution of thequestionnaire to EURATEX national and sector associations and individualcompanies. In addition, interviews with EU companies have been conducted. Atthe end of the first stage, CEEI compiled a short list of identified barriers on thebasis of the information provided in returned questionnaires and interviews.

• This Chapter gives a preliminary overview on barriers currently identified by EUoperators in questionnaires, meetings and personal interviews. Some generalcomments can be made:

• According to both EU exporters and importers of EU products in both markets,trade flows are hampered by a constant insecurity on the identity ofrequirements for clearance affecting the shipments to be imported. Thesechange drastically from one day to another. This lack of transparency on theimport conditions (documents, taxes) discourages many EU exporters as well astheir customers.

• As expected, there is a huge gap between theory and practice : the theoreticallegal requirements for import and practice may differ significantly. However, andparadoxically, some of these discrepancies enable sometimes imports to takeplace. Generally, in both countries, the mere level of customs duties is by itselfthe main trade barrier in direct flows. This report insists on some importrequirements and explains the implementation schemes as described ininterviews with EU exporters and importers of EU products.

2.1. The problems identified for China

• EU operators identified China as a country with important restrictions hamperingeither the import of finished products (textiles and clothing) or the export of someraw materials (silk). China is a problematic market where EU exporters areencountering increased difficulties They reported a large variety of trade barriers:

• Customs duties and additional import taxes are allegedly the most importantobstacle to EU direct exports of apparel and of textile fabrics. In addition to thecustoms duties, EU operators also indicated various additional import taxes,which raise the level of total import duties (namely a consumer tax and an importsurcharge, and a registration fee).

• Customs formalities are complex, cumbersome, heavy and costly. They arementioned as a major difficulty encountered by some EU operators and theirclients (in OPT schemes). Various problems were reported:

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 18

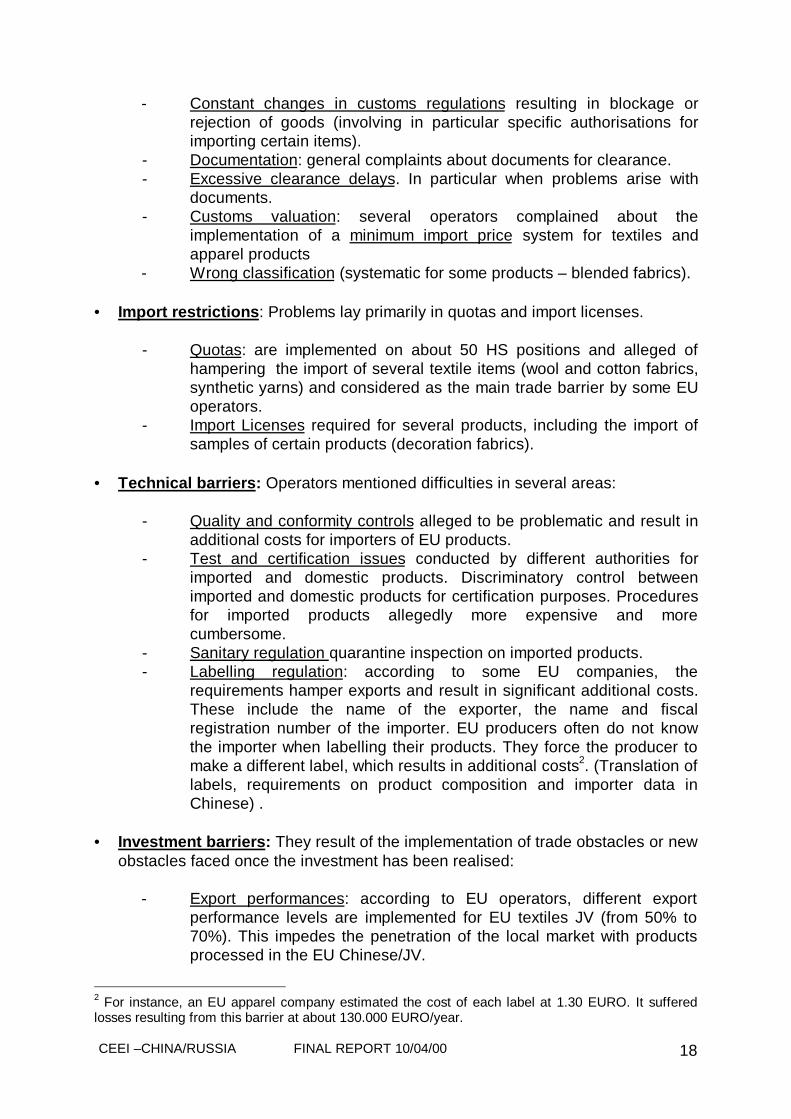

- Constant changes in customs regulations resulting in blockage orrejection of goods (involving in particular specific authorisations forimporting certain items).

- Documentation: general complaints about documents for clearance.- Excessive clearance delays. In particular when problems arise with

documents.- Customs valuation: several operators complained about the

implementation of a minimum import price system for textiles andapparel products

- Wrong classification (systematic for some products – blended fabrics).

• Import restrictions : Problems lay primarily in quotas and import licenses.

- Quotas: are implemented on about 50 HS positions and alleged ofhampering the import of several textile items (wool and cotton fabrics,synthetic yarns) and considered as the main trade barrier by some EUoperators.

- Import Licenses required for several products, including the import ofsamples of certain products (decoration fabrics).

• Technical barriers: Operators mentioned difficulties in several areas:

- Quality and conformity controls alleged to be problematic and result inadditional costs for importers of EU products.

- Test and certification issues conducted by different authorities forimported and domestic products. Discriminatory control betweenimported and domestic products for certification purposes. Proceduresfor imported products allegedly more expensive and morecumbersome.

- Sanitary regulation quarantine inspection on imported products.- Labelling regulation: according to some EU companies, the

requirements hamper exports and result in significant additional costs.These include the name of the exporter, the name and fiscalregistration number of the importer. EU producers often do not knowthe importer when labelling their products. They force the producer tomake a different label, which results in additional costs2. (Translation oflabels, requirements on product composition and importer data inChinese) .

• Investment barriers: They result of the implementation of trade obstacles or newobstacles faced once the investment has been realised:

- Export performances: according to EU operators, different exportperformance levels are implemented for EU textiles JV (from 50% to70%). This impedes the penetration of the local market with productsprocessed in the EU Chinese/JV.

2 For instance, an EU apparel company estimated the cost of each label at 1.30 EURO. It sufferedlosses resulting from this barrier at about 130.000 EURO/year.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 19

Quotas: on the remaining percentage for which distribution and saleson the local market are authorised, JV can be subject to the quotassystem for the import of their inputs, which in practice hinders stronglythe sales on the local market.

- Local taxes: EU/Chinese JV or EU companies are requested to pay anincreasing number and amount of local taxes. EU companies claim thatthese taxes are not perceived on an equal way to domestic producers.These taxes (including the difficulty to recover the VAT for otherservices and items than the raw materials) can amount 10% the JVCompany turnover.

- Credit restrictions combined with import guarantees discourageimporters from buying EU products. EU exporters complain about thenon-convertibility of the Chinese currency, which makes transactionsinsecure for small and medium size enterprises.

• Export restrictions: these affect in particular the export of the silk raw materials(raw silk and thrown silk yarn):

- Export licence fee: estimated to be 1 – 3%.- Other export fees: non-total VAT refund (-2%), inspection fees (2%).- Double price system for raw silk different prices applied to raw silk

materials exported to EU weavers and to Chinese textile and apparelindustry.

• Other problems mentioned , notably new rules for OPT (significant financialguarantee). Credit restrictions (difficulties in obtaining credit) and absence ofprotection of intellectual property rights were also indicated as highlyproblematic.

2.2. The problems identified for Russia

• Trade barriers – tariff barriers, import taxes, customs formalities, certification,sanitary regulations and labeling - in conjunction with the difficulties to cope withthe local authorities and the endemic corruption make normal exports to Russiadifficult and in some cases almost impossible.

• Even if current trade flows demonstrate positive trade balance in textileproducts in 1998 and in 1999, after the crisis; EU exporters complained aboutseveral restrictions.

• Customs duties and additional import taxes are considered by various EUindustry operators as the most important obstacle to EU exports of textiles andclothing products. EU products are alleged to be affected by import dutiesbetween 15% and 60% of CIF value. Complexity of the dual system of calculation

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 20

of import duties is often criticised. The system of minimum duty/kg (specific duty)renders the transparency of the calculation method rather difficult for EUexporters.

All questionnaires and interviews emphasise the lack of information. They alsounderline the unpredictability of the final duties charged by Customs authorities.In addition to VAT (about 20%), other import duties are allegedly collected byCustoms: files fees, clearance duties, additional VAT and fees for importerregistration are levied, but their amount and existence are variable according tothe EU operators.

Some operators estimated the total impact of import duties 30% - 70% of theproduction value. The uncertainty concerning the exact amount of all taxesprevent a lot of EU companies from seeking business opportunities in Russia,despite the enormous perspectives offered by this market. This situationgenerates insecurity and considerably harms business. Operators must oftenresort to under-evaluation and under-billing of their products

• Customs formalities In addition to endemic corruption, theft and constanthassle, operators reported many difficulties with Russian Customs. Formalitiesare complex, cumbersome, heavy and costly. Given the peculiarity of customsprocedures in Russia, they are conducted exclusively by Russian importers andtheir brokers. This explains why the EU industry has little information on theseprocedures. Various problems were reported:

- Documents and formalities are complex and numerous, most documents arewritten in Russian and have to be filled in also in Russian.

- Clearance delays are excessive and depend to a large extent of the blackpayment given to some customs officials. Problems related to the customvaluation occur in connection with the implementation of a minimum importprice by Customs authorities that are competent to determine the value ofimported products. The existence of minimum import prices prevents sales ofcertain items and stocks to Russia.

- Wrong classification of the products seems occasional, but a number ofoperators declared that it is a way to oblige them to pay higher customsduties.

- Several operators have also mentioned problems with the determination ofthe origin of the products and the use of the rules of origin.

- Pre-shipment inspection: the goods are sometimes subject to a pre-shipmentinspection. It delays exports and the additional costs are estimated between1000 and 2200 EURO.

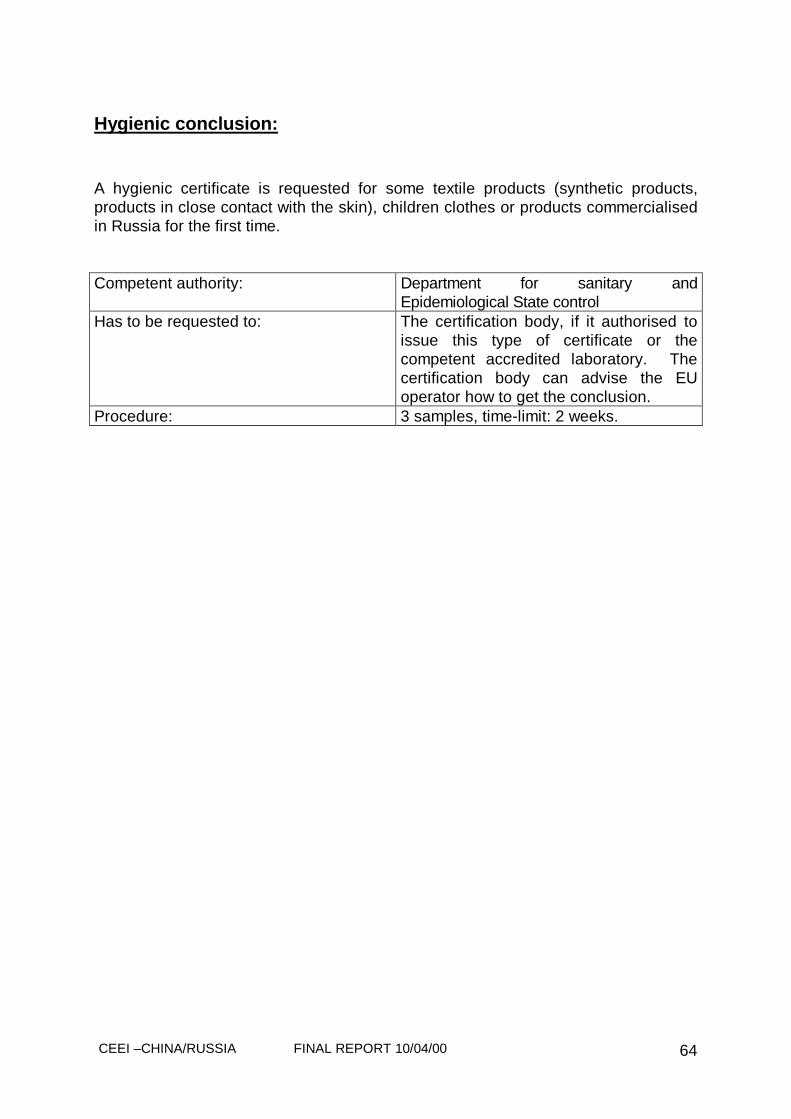

• Certification (GOSSTANDART Certificate and Hygienic Conclusion)

Non transparency: these procedures are reported to be excessively complex,burdensome and costly. Each EU company follows its ("via crucis") scheme forcertification. Different implementation schemes among Member Statescompanies reflect the non-transparency in the rules as in their implementation by

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 21

Russian authorities. Procedures for imported products are allegedly moreexpensive and more cumbersome than for domestic products.

Costs of the procedure are also reported to be excessive.

Non rationality of the process: under current rules, the EU producer can obtainthe production certificate for duration of three years. Once obtained, thiscertificate remains valid for 3 years, even if the EU producer changes the originor the quality of the item processed (e.g. fabrics). However, if the importer or theexporters wants a "shipment certificate", he is obliged to request it for everyshipment.

Controls: EU operators are allegedly subject to controls much more often thanlocal producers. In general, EU companies denounced the discrimination intreatment between European products and Russian products.

Restrictive rules of GOSSTANDARD regulations, which require a new certificateif the percentage of used materials has changed in a non-significant way. Anumber of companies find the rules of Russian certification very complicate andover prescriptive. The high costs of the certification prohibit the company to selltheir stock from other border countries, because it would be too expensive andtoo long to get a new certificate for a small quantity.

Delays for obtaining a certificate: it can last two weeks to several months.

The validity period of the certificate varies according to the nature and thecomplexity of the product. Some EU operators had obtained a certificate for aduration of three years, while others were requested to get a certificate for everyshipment for the same type of product.

Absence of equitable judicial recourse: the GOSTSTANDARD (regulatory body)is competent in case of disputes or conflicts between participants in thecertification procedure. EU Operators fear partiality if a legal dispute arises.

However, according to other EU exporters (FIN, DE), the certification procedurehad recently improved (EU companies get used to the procedures, increasingnumber of entities in charge of the verification, creation of a co-financed EU-Russian institute of certification in St Petersburg…).

Sanitary regulations: The legislation concerning the hygiene conclusion isunclear for the EU companies. They reported having supported importantadditional costs (e.g. between 6000 and 10 000FF, a loss of about 50,000-DM foranother operator). This combined with particularly unpredictable customsclearing deadlines is of great concern for producers exporting large numbers ofarticles.

Other problems mentioned:

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 22

• Labelling regulation result in significant additional costs for EU companies whoaffix the labels already in the country of shipment. Requirements concerning theidentity of the importer and of the person responsible of the packaging or thenumber of certificate of conformity are considered excessive. However, this is nota practice followed in all Member States companies. These specific requirementsforce the producer to make a different label, which results in additional costs3.(Translation of labels, requirements on product composition and importer data inRussian)

• Investment barriers: Companies willing to invest in Russia face many difficulties.The Federation Law on investment is very strict and they also should respectdifferent regional laws and negotiate with local authorities for preferentialtreatment.

• Advance payments (FIN) are prohibited under Russian Law.

• Protection of drawings and models: Even if Russia has adopted an advancedlegislation on protection of drawing and models, the EU industry and theircustomers claim that it is not implemented. The EU operators are worrying aboutthe increasing number of illegal copies of their production.

• Cost of export licenses for OPT: Finnish operators complained about theexcessive extra costs of getting export licences for products re-exported to theEU as processed products under the OPT scheme (about 1000 DM/category ofproducts and item.

Impact of trade barriers on EU exports

• The impact of all measures implemented by Russia increase the price of theproducts sometimes by more than 50%. Nevertheless, the most importantproblem is not only the advantage granted to local production, but theimplementation of import rules. Various companies work with Russia only withterms - delivery "ex factory" and cash payment. For a large number ofcompanies, this is the easier way to penetrate the Russian market without havingto go trough all administrative prescriptions and customs formalities.

• Russian clients are often small companies without the necessary organisation tocreate a distribution system covering the whole country. EU operators are obligedto deal with a large number of intermediaries for small quantities of products.

3 For example, an EU apparel company estimated the cost of each label at 1.30 EURO. It sufferedlosses resulting from this barrier at about 130.000 EURO/year.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 23

PART 2

CHINA

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 24

TABLE OF CONTENTS

§1. GENERAL CONDITIONS OF IMPORT OF EU TEXTILESAND CLOTHING PRODUCTS

1.1. Trade flows

1.2. Problems identified by EU companies

§2. IMPORT DUTIES

2.1. Measures

2.2. Implementation

2.3. Legality

§3. IMPORT QUOTAS

3.1. Measures

3.2. Implementation

3.3. Legality

§4. CLEARANCE PROCEDURES

4.1. Measures

4.2. Implementation

4.3. Legality

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 25

§5. TECHNICAL BARRIERS

5.1. Measures

5.2. Implementation

5.3. Legality

§6. RESTRICTIONS AFFECTING EU JV

6.1. Measures

6.2. Legality

§7. EXPORT RESTRICTIONS

7.1. Measures

7.2. Implementation

7.3. Legality

§8. OTHER RESTRICTIONS

8.1. Measures

8.2. Legality

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 26

§ 1. GENERAL CONDITIONS OF IMPORT OF EU TEXTILES ANDCLOTHING PRODUCTS

1.1. Trade flows

• Trade in textile and clothing products between China and the EU is regulated bytwo bilateral agreements on trade in textile products covering textile products andsilk products4. Under these agreements, exports of textile and clothing productsfrom China are limited to the quantities provided in the Agreements.

• The EU is China's first export market and China remains its main supplier oftextile and clothing products. In 1998, imports of Chinese textile and clothingproducts into the EU reached 6 995 Mio Euro (1 642 Mio for textiles and 5 353Mio for clothing). China remaining the first EU supplier in clothing products invalue terms. It is also the forth supplier of textiles after Turkey, India and USA.The imports from Hong Kong reached 2 680 Mio Euro (60 Mio for textiles and 2620 for clothing). Together China and Hong Kong represent 16,7% of EU importsof textile products5.

• Conversely, the level of EU exports of textiles and clothing products to Chinaremains modest. In 1998, exports of textile products to China reached only 252Mio Euro (216 Mio for textiles and 36 for clothing). China is the 31st export marketfor EU. The trade balance is largely negative. Exports to Hong Kong amounted to1 199 Mio Euro for the same period (716 for textiles and 483 for clothing). Theexports to China and Hong Kong amount only 4,2% of the total EU exports oftextile and clothing products.

• According to importers, the high level of tariffs explains that an important part ofEU products is reportedly still exported through Hong-Kong (about 60%). Theproducts are imported smoothly and quickly at 0% in Hong-Kong and thenexported to the Popular Republic of China.

• The volume of trade concerned by direct traffic remains consequently limited. Itcovers mainly IPT operations. EU fabrics are imported duty free into China,processed into apparel products under subcontracting activities. They are re-exported to the EU or to other export markets. IPT schemes are still veryattractive due to low wages.

4The Agreements with China are: the Agreement on trade in textile products between the Communityand China – MFA (modified 20 November 1998-OJEC 1999 L12/27) and the Agreement between theEC and China concerning the products non covered by the MFA (signed in 1995). They were modifiedby the Agreement signed by Exchange of Letters between the EC and the Republic of China (OJEC1999, L 345).5 Eurostat trade data for 1998. See also: PR China: textile and clothing sector and its export potential,OETH, 1999, p. 90.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 27

1.2. Problems identified by EU companies

• As explained above (see Part 1), the main trade obstacles are:

- the high level of customs duties- the implementation of import quotas- some restrictions affecting Joint Ventures- the export measures hampering the access to raw materials

• These measures are treated below, together with other problems identified duringthe mission conducted by CEEI in China (26 November – 10 December 1999).

§2. IMPORT DUTIES

2.1. Measures

Customs duties remain too high

• Level of applied tariffs is still rather high despite the 1999 reduction. They rangefrom 0% to 41%: yarn about 12%, fabrics 14 - 34 % and apparel 25 - 35%. Tariffsare applied ad valorem. Peaks concern in particular woven synthetic fabrics(36%), carpets (30%) raw and carded wool (41%).

• A system of tariff quotas, called "in quota interim duty rate" was enforced on 1st

January 1999. It is applied to a limited number of products by Customsauthorities. For textiles, it only covers raw wool and wool tops, for which importquantitative limits have already been fixed. These products can therefore beimported (in direct trade for internal consumption) at 1% or 3%6 (instead 41%) inthe limits of the quantitative restriction (quota) existing for this product. Customsauthorities were quite reluctant to talk about this system.

VAT is the only official import tax additional to the Customs duty

• It was confirmed during the mission that VAT (17%) is the only official import taxcharged by Customs authorities at the moment of clearance. It is collected on thefollowing result: CIF value + Customs duties. Importers complained that there isdiscrimination among domestic and imported products (for which VAT is onlycharged on the value of the local product).

6 Can be imported at 1%: HS 51011100, 51011900, 51011200, 51012100, 51012900, 51013000,51031010. Can be imported at 3% : HS 51051000, 51052100, 51052900.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 28

2.2. Implementation

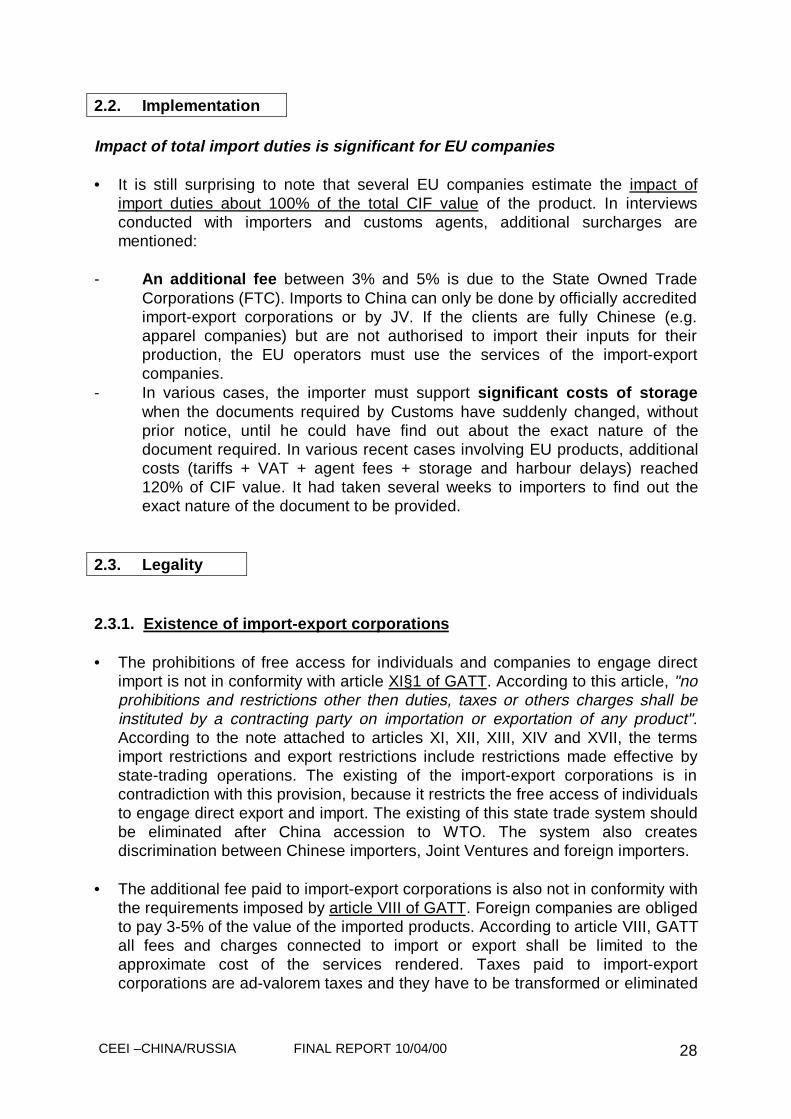

Impact of total import duties is significant for EU companies

• It is still surprising to note that several EU companies estimate the impact ofimport duties about 100% of the total CIF value of the product. In interviewsconducted with importers and customs agents, additional surcharges arementioned:

- An additional fee between 3% and 5% is due to the State Owned TradeCorporations (FTC). Imports to China can only be done by officially accreditedimport-export corporations or by JV. If the clients are fully Chinese (e.g.apparel companies) but are not authorised to import their inputs for theirproduction, the EU operators must use the services of the import-exportcompanies.

- In various cases, the importer must support significant costs of storagewhen the documents required by Customs have suddenly changed, withoutprior notice, until he could have find out about the exact nature of thedocument required. In various recent cases involving EU products, additionalcosts (tariffs + VAT + agent fees + storage and harbour delays) reached120% of CIF value. It had taken several weeks to importers to find out theexact nature of the document to be provided.

2.3. Legality

2.3.1. Existence of import-export corporations

• The prohibitions of free access for individuals and companies to engage directimport is not in conformity with article XI§1 of GATT. According to this article, "noprohibitions and restrictions other then duties, taxes or others charges shall beinstituted by a contracting party on importation or exportation of any product".According to the note attached to articles XI, XII, XIII, XIV and XVII, the termsimport restrictions and export restrictions include restrictions made effective bystate-trading operations. The existing of the import-export corporations is incontradiction with this provision, because it restricts the free access of individualsto engage direct export and import. The existing of this state trade system shouldbe eliminated after China accession to WTO. The system also createsdiscrimination between Chinese importers, Joint Ventures and foreign importers.

• The additional fee paid to import-export corporations is also not in conformity withthe requirements imposed by article VIII of GATT. Foreign companies are obligedto pay 3-5% of the value of the imported products. According to article VIII, GATTall fees and charges connected to import or export shall be limited to theapproximate cost of the services rendered. Taxes paid to import-exportcorporations are ad-valorem taxes and they have to be transformed or eliminated

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 29

even if the transitional period requested by China for the elimination of theimport-export corporation is accepted.

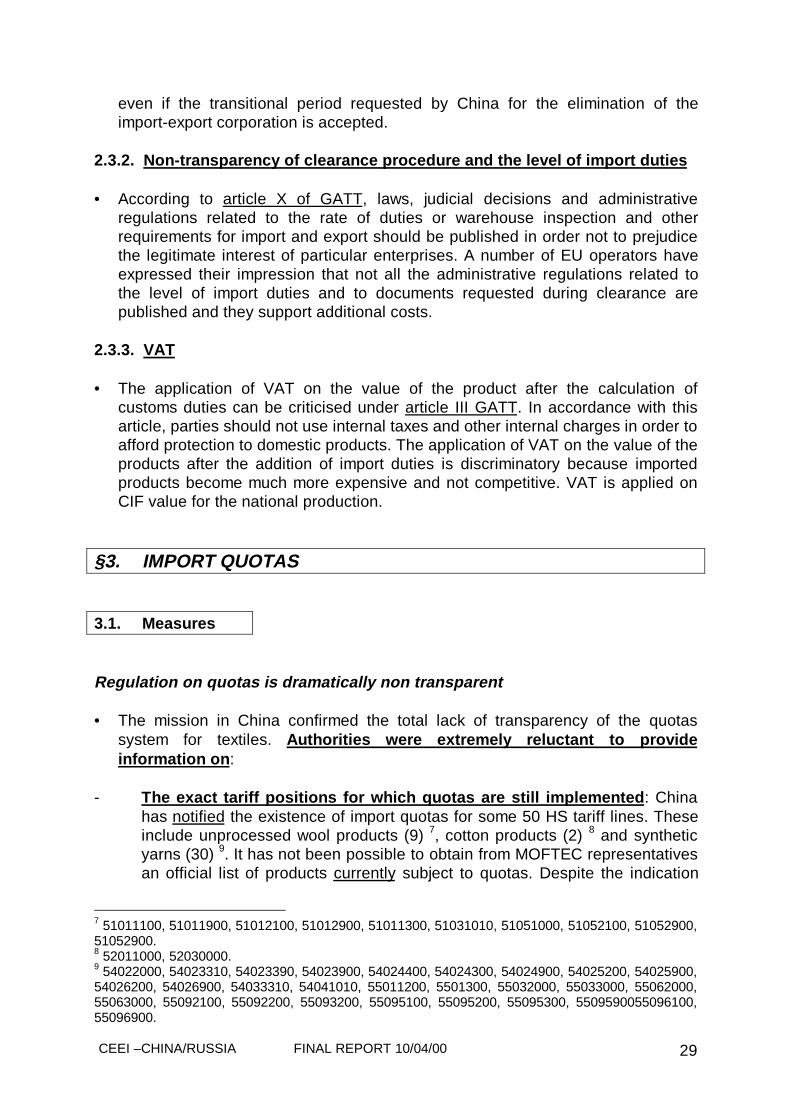

2.3.2. Non-transparency of clearance procedure and the level of import duties

• According to article X of GATT, laws, judicial decisions and administrativeregulations related to the rate of duties or warehouse inspection and otherrequirements for import and export should be published in order not to prejudicethe legitimate interest of particular enterprises. A number of EU operators haveexpressed their impression that not all the administrative regulations related tothe level of import duties and to documents requested during clearance arepublished and they support additional costs.

2.3.3. VAT

• The application of VAT on the value of the product after the calculation ofcustoms duties can be criticised under article III GATT. In accordance with thisarticle, parties should not use internal taxes and other internal charges in order toafford protection to domestic products. The application of VAT on the value of theproducts after the addition of import duties is discriminatory because importedproducts become much more expensive and not competitive. VAT is applied onCIF value for the national production.

§3. IMPORT QUOTAS

3.1. Measures

Regulation on quotas is dramatically non transparent

• The mission in China confirmed the total lack of transparency of the quotassystem for textiles. Authorities were extremely reluctant to provideinformation on :

- The exact tariff positions for which quotas are still implemented : Chinahas notified the existence of import quotas for some 50 HS tariff lines. Theseinclude unprocessed wool products (9) 7, cotton products (2) 8 and syntheticyarns (30) 9. It has not been possible to obtain from MOFTEC representativesan official list of products currently subject to quotas. Despite the indication

7 51011100, 51011900, 51012100, 51012900, 51011300, 51031010, 51051000, 51052100, 51052900,51052900.8 52011000, 52030000.9 54022000, 54023310, 54023390, 54023900, 54024400, 54024300, 54024900, 54025200, 54025900,54026200, 54026900, 54033310, 54041010, 55011200, 5501300, 55032000, 55033000, 55062000,55063000, 55092100, 55092200, 55093200, 55095100, 55095200, 55095300, 5509590055096100,55096900.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 30

given that the list has made public to the European Commission, the MemberStates Embassies and the EC Delegation have no or very little informationabout these quotas. According to importers, quotas are not implemented forsome items, such as cotton fabrics. Quotas would be implemented for rawwool, combed wool, synthetic fibres, polyester yarns, and polyacrilic fibres.

Customs authorities use an internal document (tariff code "blue book") listingfor each tariff position the applicable import authorisations, licences orrestrictions. This internal document is not made public by customs authorities(not published) but, it can be consulted, in certain cases, at the request ofimporters. According to various sources, it indicates the positions for whichCustoms Authorities are entitled to request import licenses (and thereforepossibly subject to quotas). These tariff lines mainly correspond to theproducts already notified with some differences 10.However, it was reported that some tariff positions do not appear in theCustoms list: (51052900, 51052900, 54024400, 54024300 54023900,54024900; 54025200, 54026900, 54041010, 55011200, 55096100), whileother positions are allegedly included in the Customs list: (54023990,54024200, 54024300, 54024990, 54025990, 54026990, 54041000,55012000, 55021000, 55093100, 55096200). This increase the existingconfusion on the identity of quotas currently implemented.

- The quantitative level of quotas : is not known and made public by Chineseauthorities. Levels are fixed yearly by the State Planning Commission onbasis of proposals made by MOFTEC and the domestic industry.

- The criteria on which import licences are delivered : various EU exportersand EU JV complained about the non-transparency of the licence issuingsystem. If some importers can be provided with a sufficient number oflicenses, EU JV claim they are discriminated compared to domestic producersand also with other foreign non-EU JV producing the same items (whichreceive more licenses).

3.2. Implementation

Implementation of Quotas is a significant trade and investment barrier

(1) Quotas hamper the development of EU direct exports on the products forwhich they are implemented.

(2) The implementation itself restricts the import of the products under licenseand forces the importer to use Chinese input.

(3) Quotas restrict the production process of EU JV and impede them to distributetheir products on the local market.

10 51011100, 51011900, 51012100, 51012900, 51011300, 51031010, 51051000, 51052100, ,.520100, 520300. 54022000, 54023310, 54023390, 54023990; 54024200, 54024300; 54024990,54025990, 54026200, 54026990, 54033310, 54041000, 55012000, 55013000, 55021000, 55032000,55033000, 55062000, 55063000, 55092100, 55092200, 55093100, 55093200, 55095100, 55095200,55095300, 55095900, 55096200, 55096900.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 31

(1) Restriction of direct EU exports : there is a limited development of exportsfor some products subject to Chinese import quotas (e.g. woollen fabrics).

(2) Implementation is aimed at protecting Chinese items : a very goodillustration is the implementation of the import quota for raw wool and wooltops. Chinese and EU JV desiring to produce wool yarns with EU wool topsfor the domestic industry have to request an import license to MOFTEC or touse Chinese wool tops. Chinese – EU Joint ventures producing wool topshave to either use Chinese raw wool or to request import license to importtheir usual quality of raw wool.

The State Planning Commission fixes the quota for wool at the beginning ofthe year. The quantities are then communicated to MOFTEC, which deliversthe import licenses. The quota is divided into two (or three) parts. The firstpart is attributed at the beginning of the year. Nobody knows when theremaining quantities will be attributed. This provokes speculations on theprice of the local raw materials. In 1999, Chinese authorities waited until theend of auction sales of Chinese raw wool (July) to distribute the second partof the import quota. Increased competition among foreign investors forced tolook for Chinese wool. This also increased very much the price of thisdomestic commodity, which became above 20% more expensive thanAustralian wool (of better quality). In addition, the late allocation of theremaining quota (December 1999) renders in practice the import almostimpossible (time duration for product purchase and transport to the mill inChina often last too long (2 months). In the case of wool, the Australian woolis sold on auctions after beginning of the year. All companies were forced torush into wool purchases in January 2000 and to build up stocks, which resultin additional costs.

(3) Quotas implementation impedes distribution of EU JV products for localmarket : when EU JV have difficulties to buy local raw materials (at expensiveprices and for a non suitable quality) and do not get enough import licensesfor their production for local market, they are forced to produce for export.They can therefore import raw wool or wool tops free of quotas and importduties. However, they fail in their objective to penetrate the local market(which has motivated their investment into China). In addition, they mightencounter other difficulties with the import regime for processing goods(Inward processing Trade as explained below).

3.3. Legality

• The EU operators complain about the non-transparent management of quotasand import licences, which aims to protect national production. This situation is incontradiction with article X of GATT. This provision requires that "all laws,regulations and decisions on requirements, restrictions or prohibitions on imports

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 32

and exports should be published in order to enable governments and traders tobecome acquainted with them".

• Moreover, according to article 11 of EC-China Agreement on textile products,China should encourage and facilitate the importation on its market of textileproducts listed in annexes I and II of the Agreement, originating in theCommunity. For this, "China should take measures to reduce the disequilibrium inits textile trade with the Community". Current situation where EU joint venturesface difficulties to receive import licences for products listed in the annexesbecause of the non-transparency of Chinese legislation is in contradiction withthis provision.

• Where quotas and quantitative restrictions are still implemented under GATT,they should be managed according to article XIII (non-discriminatoryadministration of quantitative restrictions). After elimination of quotas, Chinecould try to implement a number of non-tariffs trade barriers (technical regulation,labelling) in order to maintain the protection of domestic production actuallyguaranteed by import quotas and licences.

§4. CLEARANCE PROCEDURES

4.1. Measures

• According to Chinese Customs Law, the documents required for clearance are asfollows:

- Commercial invoice,- Packing list- Bill of lading- Contract- And in certain cases certificate of origin.

4.2. Implementation

The main problems arise with the import authorisation

• The import documentation in itself is not a significant problem for EU operators.However, sometimes the authorities are very slow to make a full check of thedocumentation. Therefore, this creates delays and losses for the producers.

• The problems lay primarily in the presentation of the appropriate importauthorisation (import license or other type of authorisation). In practice, theimporter has to request the Customs, for each import, IF he is entitled (or not) toimport. For some textile items, an import license is required (mentioned in the

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 33

Customs code as "1"). Import license is normally required when the product issubject to quotas. However, EU exporters complained also about import licencesrequired even for sample hanger. For other specific products, which areconsidered as "sensitive products", another type of import document can beasked by Customs under specific instructions of Central Power. Some textileproducts (such as polyester fabrics) are reportedly considered as being underspecial commodity restriction in 1999. Importers are requested to undergospecific registration, which means to ask for a new special import authorisation.

Customs denied still implementing a minimum import price system for textiles

• Several operators mentioned that Customs are applying a minimum importprice system for textiles. When the price declared on the invoice is below thereference value (regularly updated by them), they charge a penalty, which canexceed the difference between the import duties charged on the declared valueand those calculated on the basis of the minimum import price. This wasconfirmed by importers and EU agents interviewed in Shanghai, Beijing andHong-Kong. However, the Customs authorities denied the implementation of suchminimum import price. They insisted firmly that they fully respect the WTOAgreement of customs valuation.

In some cases, Customs create additional problems

• Various cases of difficulties during the clearance process are reported. Forinstance, in January 2000, Chinese Authorities have tried to stop import of rawsilk in order to control the price of this commodity. Customs Authorities madeproblems with sanitary and hygiene certificates blocking during three months theimport of products originating in China, which had been already exported inEurope and reshipped to China.

4.3. Legality

4.3.1. Transparency of the customs clearance

• Transparency of documents and procedures for Customs clearance is requiredby article X of the GATT. After accession, China should apply this provision andadopt clear rules concerning documentation and inspections for customsclearance.

4.3.2. Customs valuation

• If confirmed, the application of secret minimum import prices probably goesagainst article VII of GATT and the Agreement on customs valuation. Accordingto these provisions, the value of the product for customs proposes should not bebased on the value of merchandises of national origin but should be determinedin accordance with the rules provided in article VII of GATT or the Agreement of

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 34

Customs valuation. The value of the products for customs clearance cannot bebased on arbitrary or fictitious values. Rules and practices used by customs toascertain value of the products for customs proposes should be given sufficientpublicity to enable traders to estimate this value. According to EU operators,China implements secret minimum import prices for some imported textileproducts in order to protect domestic production and this practice is verydamageable for EU exporters. Minimum import prices should be eliminated byChina before accession to WTO.

§5. TECHNICAL BARRIERS

5.1. Measures

• Under Chinese Law, commodity inspections have to be carried out on textile andclothing domestic and imported products. Raw materials (raw silk and raw silkyarns) are also to be inspected before exports.

• The main legal texts implementing these commodity inspections for textile andclothing products are:The Law of the People's Republic of China on Import and Export CommodityInspection of 1989: this Law was enforced on 1 August 1989. It establishes theprinciples of Commodity inspection and that the State Administration forCommodity shall adjust and publish a list of Import Export Commodities subject toinspection (art. 4).Regulation for the Implementation of the Law of the People's Republic of Chinaon Import and Export Commodity Inspection. It was enforced in 1992. It describesthe rules for implementation of Import and Export Commodities Inspections byChinese Authorities11.

•5.2. Implementation

Technical barriers are less damaging in practice than expected

• EU operators mainly complained about the implementation of certification rulesand labelling rules. However, the interviews with importers revealed that:

- Commodity inspections, certification procedures and sanitary controlsare not specifically considered by importers as a problem as such. However,EU operators reported difficulties in their implementation. Under the Law onInspection of imported goods of 27 February 1999, these controls are carried,out randomly by SIC (Sanitary Quarantine Inspection Bureau). Complaintsfocus on the discretionary power of Chinese Authorities, which render controls

11 Laws and regulations for entry-exit inspection and quarantine of the people's republic of China,1999.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 35

burdensome and time consuming.

- Labelling : according to SIC and Customs, there are no specific requirementsfor textiles. SIC does not verify the conformity of labelling requirements.Customs are entitled to do it. However, it seems that these controls are notconducted by Customs. This means that the required label (with importer dataetc…) can be affixed in practice at a later stage, when the product isdistributed.

5.3. Legality

• Two different authorities are competent in China for conformity assessment. Thefirst one (State Administration of Import and Export commodity inspection) isconducting controls for imported and exported goods. The second one (Chinesebureau of technical supervision) is responsible for inspection on domesticproducts. Accordingly, there are two sets of regulations applied to domestic andimported products. A large number of imported products can be subject tomandatory inspection. Even, if the procedure is not extremely burdensome for EUoperators, some discrimination between products is not excluded.

• This situation is not in conformity with article III of GATT and article 5 of TBTAgreement. These provisions require that internal regulations and in particularlyrules for conformity assessment (article 5 TBT Agreement) are not applied toimported products under conditions less favourable then those granted tosuppliers of products of national origin. Conformity assessment should not beused in order to protect domestic production. The existence of two differentregulations for imported and domestic products renders difficult the overallappreciation of conditions for conformity assessment and may be used as adiscriminatory instrument. Even if differences in conformity assessment are notpresently considered as damageable by the EU operators, the system couldlegally be implemented in a stricter way to compensate elimination of quotas andimport licensing system. In any case, the justification of different rules forChinese and imported products cannot be accepted under the exceptions ofGATT and TBT Agreement and should be eliminated before accession.

§6. RESTRICTIONS AFFECTING EU JV

6.1. Measures

• Only a few EU Textiles and Apparel companies have realised significantinvestments in China. Two types of problems must be underlined. First EUcompanies often encounter difficulties linked to the provisions (or lack of explicitprovisions) in their JV contract protecting their rights. Second, specific

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 36

restrictions exist hampering the distribution on the local market.

Conditions of establishment are often not clearly defined in JV contracts

• It is understandable that information on the conditions of negotiation of JVcontracts is not easy to obtain from the EU companies. However, it turns out thatmost difficulties encountered by EU JV in China arose from the lack oftransparency of trade conditions agreed with Chinese Authorities and partnersduring the negotiations of the JV contract. Some commitments made by ChineseAuthorities are apparently not explicitly drafted in these contracts.

For example, in some cases, the commitments made by Chinese authorities todeliver export or import licenses were not written in the contracts. Afterwards, JVencountered difficulties to be provided with licences and had no legal recourseagainst the Authorities. For instance, notwithstanding the MOFTEC originalguarantee, it happened that Chinese Authorities stopped delivering exportlicences to a European partner given its refusal to accept trade conditions notagreed in the initial contract. In other cases, the EU Joint Venture have obtainedto distribute a fixed percentage of their production on the local market but werenever provided with the corresponding import licences (see infra).

Joint Ventures and EU companies are facing increasing restrictions:

• These companies were facing increasing trade barriers hampering theirpenetration into the local market. Their investment was mainly driven by theobjective to get a better access to the local market. However, these companiesare limited by at least three types of obstacles:

- Export performance requirements : JV and EU companies have to export aminimum part of their production. This percentage is agreed in their JVcontract with Chinese authorities. It can be from 50% to 95% (95% ineconomic zones). This constitutes a serious trade obstacle and cannot bechanged.

- Quotas : as above explained, the implementation of quotas strongly reducesthe possibility to distribute on local market the products processed in JV withimported inputs. It happened that these companies were granted with importlicences covering only 3 – 10% of their production, while they were expectingto distribute at least 30% of their production on the local market. Quotaimplementation damages therefore investments made by EU companies,provoking, in certain cases, production losses and temporary closings of themills.

- Local taxes and VAT : Joint Ventures companies are complaining about theincreasing burden of local taxes charged by local authorities (increasing everyyear). These are for instance educational tax, real estate tax, anti-flood tax,and food fund; help farmer fund, various stamps and fees, withholding andbusiness tax. The refundable VAT is calculated with a complicated formula,integrating parameters, such as export ratio and local sales. EU companies

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 37

allege they can only recuperate, while exporting their products, some 90-95%of VAT paid during the production process, when domestic competitors canrefund VAT by 100%. According to some companies interviewed, the overallpercentage of non-refundable VAT and local taxes can reach about 10% ofannual turnover of the company.

6.2. Legality

6.2.1. Export performance requirements

• Chinese authorities export performance requirements for Joint Ventures are incontradiction with the WTO Agreement on trade-related investment measures.According to the illustrative list of the Agreement, restrictions on the exportationsor sale for exports are inconsistent with article XI §1of GATT. The transitionalarrangements authorised by article 5 of the Agreement for the initial members ofGATT and countries acceding before the expiration of all transitional periods arealready not applicable. China will thus be obliged to abolish trade-relatedinvestment measures in contradiction with the provisions of the Agreement beforeaccession.

6.2.2. VAT refund and other taxes

• Discrimination concerning VAT refunds goes against the national treatmentprinciple established by article III of the GATT. This article specifically envisagesthe question of taxes.

§7. EXPORT RESTRICTIONS

EU industry against State agencies monopoly position for raw silk purchase

• EU operators complain about the violation of the «national treatment clause»contained in the bilateral Agreement between China and the EU and giving to theCommunity industry purchase conditions identical to these of the Chineseindustry. According to their arguments, the production and the purchase of rawmaterials are strictly regulated and can only be operated through State exportcorporations. Therefore, EU producers have no direct access to Chineseproducers (e.g. reeling mills) and must deal with an Import/Export corporation.

Recent modifications in the licensing system are not sufficient for EU industry

• Until January 2000, China National Silk Import and Export Corporation (CNSIEC)kept the exclusivity of Export Licenses. Since beginning 2000, MOFTEC wasgranted with the export licenses delivering. It recently entitled approximately 40

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 38

traders to get the right to make the exports. This means that the total amount ofquotas can be split among these 40 traders, selected by local Chambers ofcommerce.

• A significant part of the EU silk industry is distrustful regarding these new rules.The industry considers that they do not fulfil the expectation of elimination ofmonopoly position for raw silk purchase. EU operators will in fact continue todepend on licences, which are given to traders entitled by local authorities. Thecontrol on the export of silk materials will therefore not disappear. Export freedomobjective will consequently not been achieved.

• The Industry insisted on the fact that they need total export freedom in orderto be able to get their supplies directly from Chinese reeling mills, withoutany surcharge from Chinese Customs .

Double price system is still a key concern

• In addition, EU operators complain about the double price system applied toproducts sold to Chinese producers and to foreign producers (prices about 30%more expensive). In the case of silk products, Chinese farmers can sell a minorpart of their production directly to textile Chinese reeling mills. These cannot sellraw silk directly to EU operators (producers/traders), which have to buy thoughState agencies. This can raise considerably the price of exported productscompared to internal price for raw silk used by domestic producers. If for instancethe reeling mill sell raw silk 15 USD/kg to the domestic producer, the sameproduct will be charged with 2 USD internal taxes (17 USD). On this amount, theImport/export Corporation will charge 20%. Before export to Europe, the value ofthe product is then 21 USD, compared with 15 USD for the domestic market .

• Even if, for the moment, the double price system is less relevant, for conjuncturalreasons, it is feared that the export licence system may always give thepossibility to raise big differences in domestic and international prices for silk.

Improvement of raw silk quality is perceived as an essential issue

• The EU does not import cocoons from China but raw silk and raw thrown silkyarns. Silk reeling industry is a labour intensive industry. The interest of the EUindustry is therefore in practice more concentrated on the purchase of raw silk.About 3000 tons of raw silk are imported yearly in the EU, from which 2,500directly in Italy, 300 tons in France the remaining 200 tons in the other MemberStates. However, increasing number of EU operators left the raw silk Chinesemarket. There were mainly two reasons: (1) the structural quality problems - toomany defects appearing in the fabrics scarves processing in the EU - and (2)the conjunctural shortage of the highest raw silk grades (4 A, 5 A) required byhigh quality EU producers. This explains, for example, why over the recent yearsEU (e.g. French) silk operators have increased their purchases of silk to Braziluntil 50%. However, Brazilian silk is more expensive and some operators alsoencounter other difficulties with this market.

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 39

• EU silk operators would therefore welcome an improvement of the Chinese rawsilk processing, even through a cooperation framework with the EU. However, forthe EU industry, this cooperation should respect strict conditions. For someinterlocutors, the removal of the export restrictions and the State tradingmonopoly for silk is a pre-requisite. For others, which also agree with theimportance of removal of export restrictions, a Partnership would have to promotesilk as high quality commodity. According to them, this could be achieved forinstance through a system of withholding tax in China. A Partnership could alsoimprove the quality of the raw silk produced in China. However, this would needboth the support of the Industry representatives in the EU and a financialassistance regarding these projects.

• During the mission in China, Representatives of CNSIEC underlined their interestfor any project aiming at improving the quality control and the production processin reeling mills. Some co-operation project has already started with Japanesepartners for specific silk items (silk for kimonos).

7.1. Measures

Export licenses are needed for various raw materials items

• For some textile items, which are not subject to quotas under bilateral Agreementwith the EU (raw silk, silk fabrics), an export license is needed. The Chinese orEuropean JV producer must ask for the export licence, either directly toMOFTEC. (for JV) or via CNSIEC (for domestic producers). The Central Authority(State Planning Commission) establishes annually the maximum quantity to beexported. MOFTEC determines the quantities to be allocated for each applicant.

Raw materials subject to export taxes

• Silk products are subject to export taxes under Chinese Law. The number andthe levels of these export taxes have been reduced according to ChineseAuthorities (see implementation).

7.2. Implementation

Difficulties to obtain export licenses lay in the non-transparency of the system

• It was reported that EU/Chinese JV have encountered difficulties to get theirexport licenses for exporting silk materials and thrown yarns. It is difficult to dealwith the different Authorities in charge of issuing the export licenses in order toobtain the quantities needed. It is also problematical to know if the Chineseproducers have met difficulties to get the licenses.

Number and level of export taxes have been reduced

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 40

• There is a discrepancy of opinion between Chinese authorities which pretendthat there is no fee for export licenses, except minor and administrative fees, andEU operators which identified various surcharges hampering raw silk and silkyarns exports and increase significantly the value of the products.

• According to Chinese authorities (CNIESC), export license is free of charge.Export licenses cannot be sold from an exporter to another exporter (licensesnominative). However, there are two small and minor fees:

Administrative fee: this RMB 50 fee covers administrative fee for the exportlicense delivering (covering fill in of license and postal mail).Silk stabilisation fee: It is 8000 RMB/ton. It is aimed at feeding the silkdevelopment risk fund since 1st March 1997. It is levied only on the export ofraw silk.

• According to EU operators, export license "duty" varies between 1 – 5%.according to the market conditions. In addition, the quarantine inspection feecharged by CCIB (Chinese Commodity Inspection Bureau – about 2%) alsoaffects the price of the exported product. The MOFTEC surcharge of 4%, whichwas previously charged, is not currently applied (but apparently not abolished).

• VAT refund: is 5% only for cocoons, 13% for raw silk and 15% for silk thrown silkyarns and is total (17%) for silk apparel. For EU operators, which buy raw silk orsilk yarns, there is therefore a difference in price compared to Chinesecompetitors.

7.3. Legality

• According to article 12 of the Agreement between EC and China, concerningnon-MFA products, China must ensure that the supply to the Community industryof raw materials exists at conditions not less favourable than to Chinese domesticusers. The requirement of export licences, export duties and administrative feesis not in conformance with the Agreement. According to the Protocol about theimplementation of article 12 of the Agreement, if products of raw materials aresubject to specific practices (such as licences, fiscal, customs and others), theconditions for the Community users must not become less favourable than for theusers in China. This concerns among other things actual access and prices.China must also abstain from any such measures, practices and policies that mayresult in double pricing. The export licences introduced by China are automaticbut the administrative burden can be very important because of the non-transparency of the system. The export taxes, non refund of total amount of VATand administrative duties increase the price of the raw materials and the result isthat they are not supplied at the same conditions to EU producers than toChinese domestic users. Conditions for EU producers are obviously notably lessfavourable and the situation is a breach to EC-China Agreement. According toEU producers they suffer at present from a 50% price difference comparing toChinese producers. The situation is subject to regular review under the

CEEI –CHINA/RUSSIA FINAL REPORT 10/04/00 41

Agreement and the problem may be solved if the EC requires abolishment ofexport licences and duties.

§ 8. OTHER RESTRICTIONS

8.1. Measures

New import rules for processing trade are a new subject of concern

• Both importers of EU products and EU exporters have expressed their strongconcern about the new rules implemented since October 1999 for inwardprocessing trade (IPT), also referred as “Export processing trade”. According toimporters, these rules are being implemented only in some entry points: