march 2007 presentation to: regarding an evaluation of

TRANSCRIPT

March 2007

Presentation to:Presentation to:

Regarding an Evaluation ofRegarding an Evaluation of

Table of Contents

1. Executive Summary

2. GSN Business Plan Review

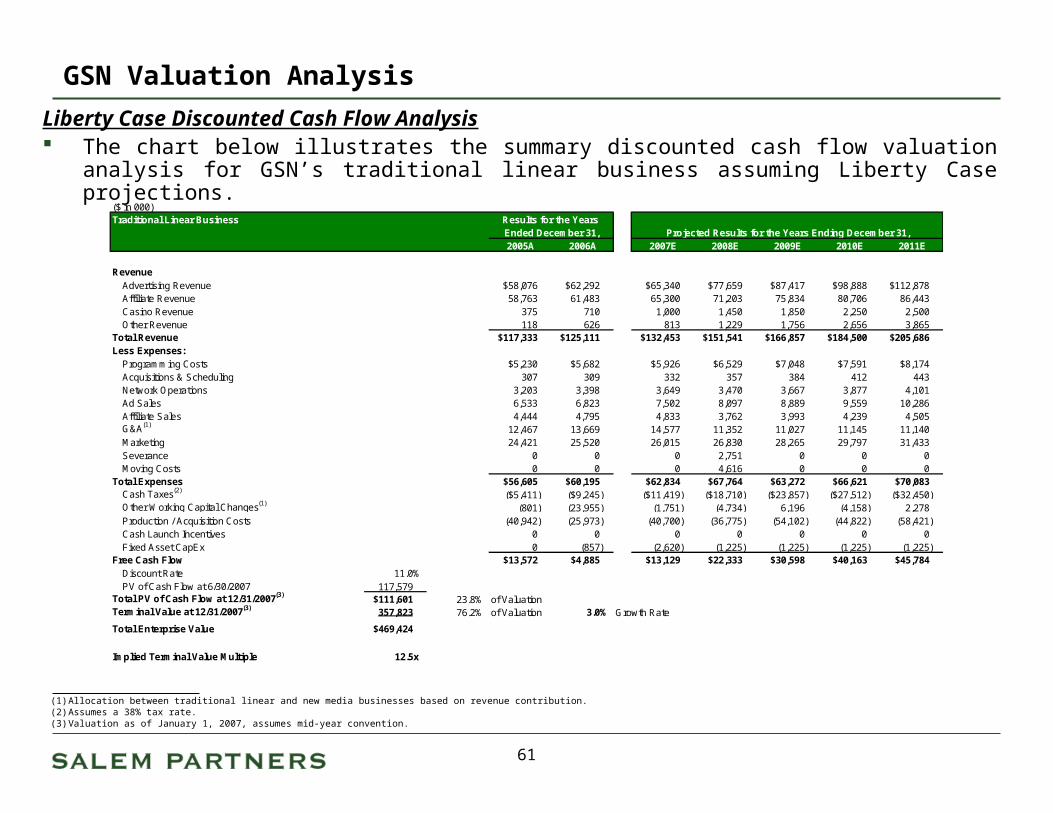

3. Discussion of Liberty Case

4. Discussion of SPE Case

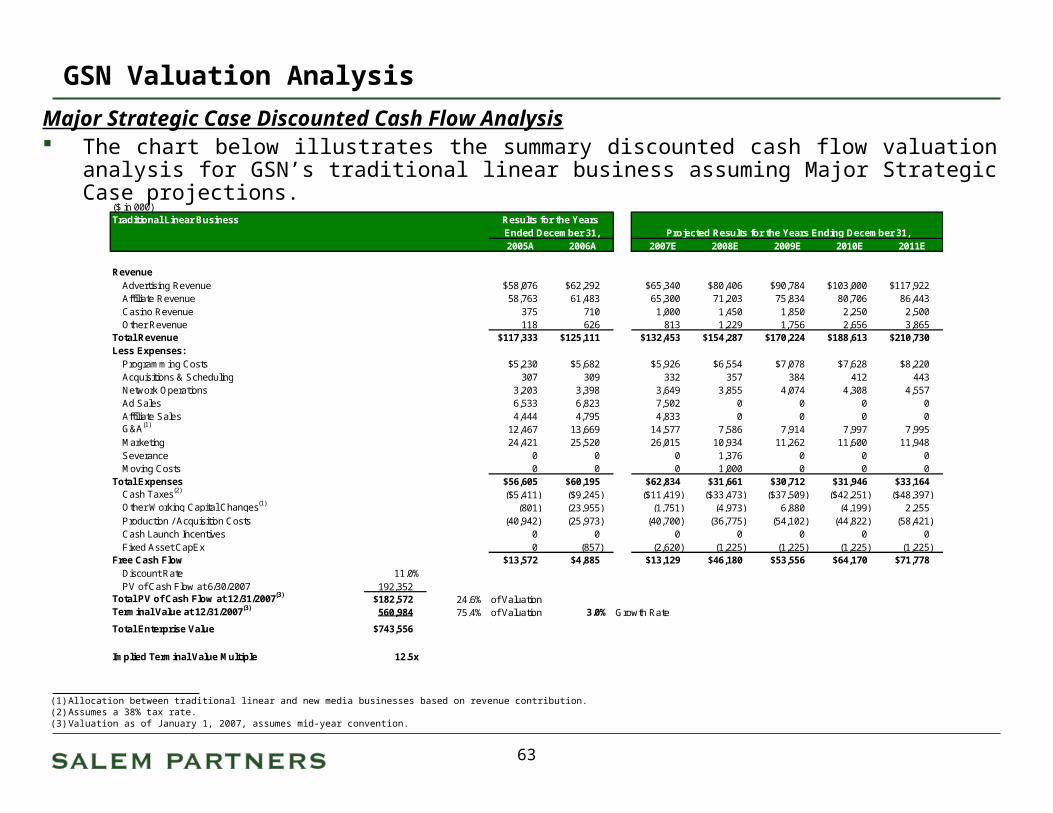

5. Discussion of Major Strategic Case

6. GSN Valuation Analysis

Exhibits

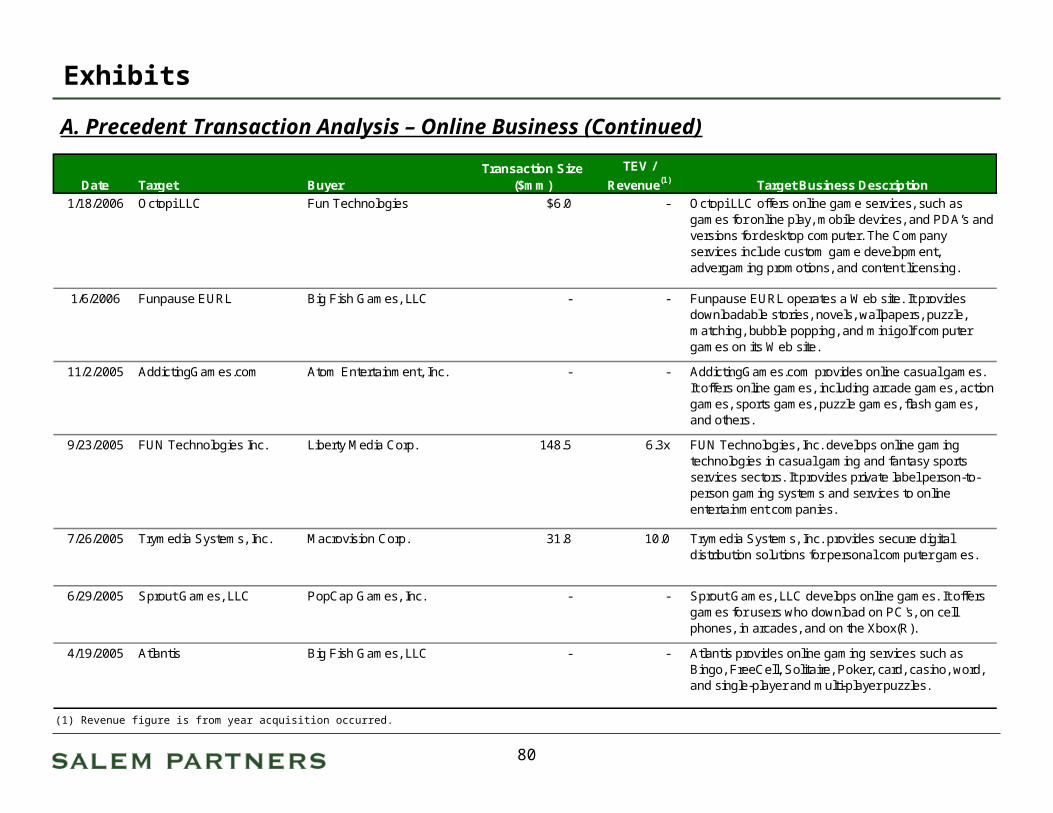

A. Precedent Transaction Analysis – Casual Games

B. Precedent Transaction Analysis – International Cable Networks

C. Overview of Fun Technologies

D. Alternative WACC Analysis

Executive SummaryExecutive Summary

Executive Summary

Introduction Salem Partners LLC is pleased to present to Sony Pictures Entertainment (“SPE”) a valuation

of Game Show Network, LLC (“GSN” or the “Company”).

Salem Partners was engaged by SPE to render the following services:

a) Review certain due diligence materials, including documentation supplied by the Company regarding its financial history, affiliate contracts, programming commitments and advertisers.

b) Evaluate the Company’s financial plan.

c) Estimate the value of revenue growth or cost savings opportunities that might arise in connection with a merger of GSN into Liberty Media Corporation (“Liberty”).

d) Provide estimates of value for GSN on a standalone basis as well as under Liberty ownership.

SPE Management has also verbally requested that we focus particular attention on GSN’s new businesses related to digital media and audience participation-based linear programming.

In order to compare the value of GSN in an acquisition by Liberty to that in an acquisition by SPE, we have also taken into account potential cost savings, synergies and risk to affiliate status under SPE’s ownership. Cost savings opportunities have been provided by SPE Management.

1

Executive Summary

Introduction (Continued) Salem Partners has also analyzed two other scenarios.

The first reflects the value implied if GSN achieved the financial performance projected by Management.

The second reflects the potential value achievable in a sale to a major cable network owner such as Viacom, Time Warner, Fox, Comcast, NBC/Universal, or Scripps (“Major Strategics”).

2

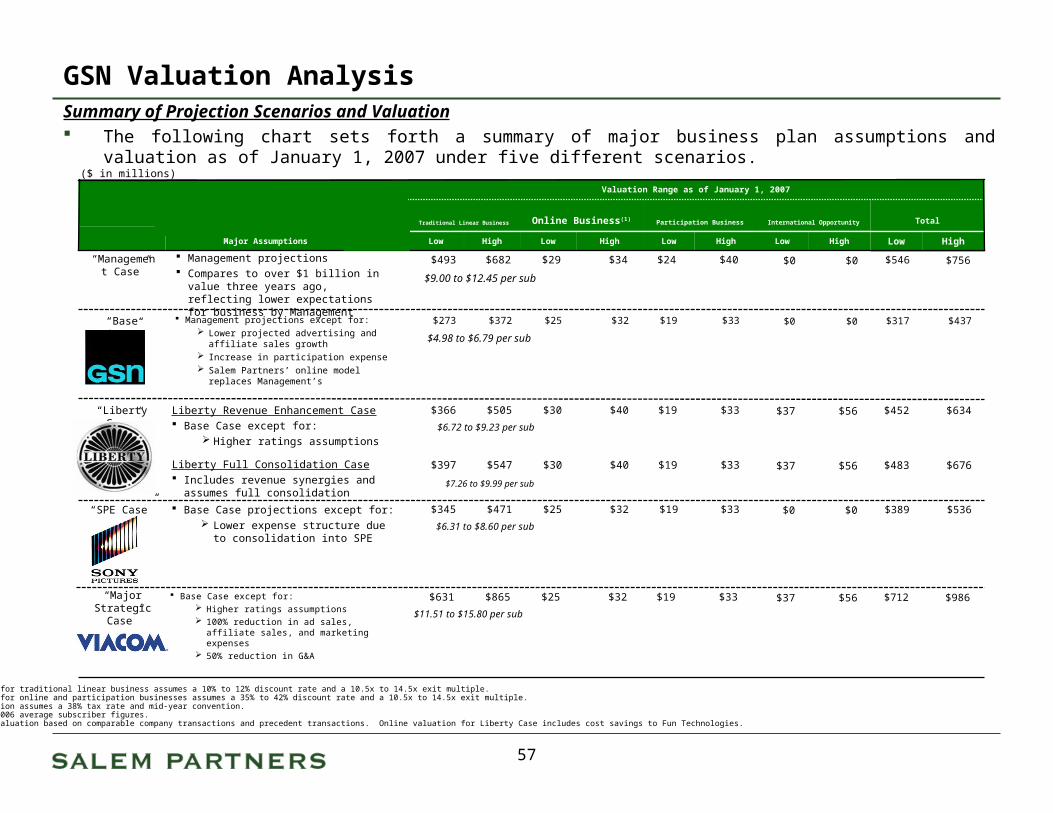

Executive SummarySummary of Projection Scenarios and Valuation The following chart sets forth a summary of major business plan assumptions and valuation as of January 1, 2007

under five different scenarios.

Note: Range for traditional linear business assumes a 10% to 12% discount rate and a 10.5x to 14.5x exit multiple. Note: Range for online and participation businesses assumes a 35% to 42% discount rate and a 10.5x to 14.5x exit multiple. Note: Valuation assumes a 38% tax rate and mid-year convention.Note: Uses 2006 average subscriber figures.(1) Online valuation based on comparable company transactions and precedent transactions. Online valuation for Liberty Case includes cost savings to Fun Technologies.

“Liberty Case”

“Management Case”

Base Case except for: Higher ratings assumptions 100% reduction in ad sales, affiliate

sales, and marketing expenses 50% reduction in G&A

($ in millions)

Valuation Range as of January 1, 2007

Participation BusinessOnline Business(1)Traditional Linear Business

Base Case projections except for: Lower expense structure due to

consolidation into SPE

“SPE Case”

$33$19$40$30$505$366Liberty Revenue Enhancement Case Base Case except for:

Higher ratings assumptions

Liberty Full Consolidation Case Includes revenue synergies and assumes full

consolidation

$33$19$32$25$372$273 Management projections except for: Lower projected advertising and affiliate

sales growth Increase in participation expense Salem Partners’ online model replaces

Management’s

“Base Case”

HighLowHighLowHighLowMajor Assumptions

International Opportunity

$56$37

$0$0

HighLow

Total

$634$452

$437$317

HighLow

$33$19$40$30$547$397 $56$37 $676$483

$4.98 to $6.79 per sub

$6.72 to $9.23 per sub

$7.26 to $9.99 per sub

$33$19$32$25$471$345 $0$0 $536$389

$6.31 to $8.60 per sub

“Major Strategic

Case”

$33$19$32$25$865$631 $56$37 $986$712

$11.51 to $15.80 per sub

$40$24$34$29$682$493 $0$0 $756$546

$9.00 to $12.45 per sub

Management projections Compares to over $1 billion in value three

years ago, reflecting lower expectations for business by Management

3

Executive Summary

Valuation Methodology We have been instructed to value GSN objectively.

Valuation is intended for internal SPE use and was not prepared as a negotiating tool for use with Liberty.

Salem Partners would be pleased to revise and reconsider our analysis in connection with SPE’s negotiation with Liberty.

Traditional Linear Business Salem Partners has relied primarily on a discounted cash flow analysis to value GSN’s linear

channel. This methodology is consistent with the approach utilized by potential buyers in recent

cable channel acquisitions. Per subscriber values have been computed from DCF valuation to provide context and

assess overall reasonableness. However, the dearth of comparable recent transactions and the substantial recent change in the business environment causes a valuation based primarily on per subscriber values to be less reliable.

GSN’s current position on the subscriber and revenue growth curve makes an analysis based on cash flow multiples unreliable.

4

Executive Summary

Valuation Methodology (Continued)

Online Business GSN's online business is valued through an analysis of comparable publicly traded

companies and precedent transactions, together with a discounted cash flow analysis. Synergies from a combination with Fun Technologies is valued on a discounted cash flow

basis utilizing a range of discount rates of 35% to 42% for consistency.

Participations GSN’s participations business is valued on a discounted cash flow basis utilizing a range of

discount rates of 35% to 42% to reflect higher risk and expected returns of the business.

International Opportunity The value of the international opportunity was derived by analyzing the values implied by

analyzing comparable public companies and precedent transactions to arrive at a range of potential values that could be created internationally by GSN. The valuation ranges relevant to each ownership case have been discounted back to the

present assuming a 5-year time frame in which such businesses could be built.

5

Executive Summary

GSN Business Plan Review – Base Case versus Management Case

Item Revision made

Comment

Traditional Linear Network Affiliate Revenue Lowered

Company has projected increases in subscribers and license fees. Given distribution environment, subscriber fee growth reduced to a CAGR of 3.0% rather than the 6.6% CAGR GSN Management is projecting.

Advertising Revenue Lowered Company has projected increases in CPMs, ratings and subscribers. Given historical ratings performance and likelihood of increasingly weak channel positioning as a standalone channel, we have estimated ratings to stay flat rather than increase at the 11.0% CAGR GSN Management is projecting.

Online Business Lowered Company has projected that 20% of unique visitors subscribe at $4.85 per month, which is an increase from 0.46% and 1% of uniques in 2006 and 2007E, respectively. We have revised the subscription percentage to grow to 10% in 2011. Further, we believe Management’s expectations of non-GSN viewer visitors is conservative compared to other similar business plans. On balance, the reduction in subscriber growth, along with a reduction in download conversion and video viewings, lowers financial results. Valuation is based on venture capital expected rates of return, comparable company analysis and precedent M&A transactions.

Participation Business Increased expense

Company has projected an 89% increase in participation revenue over the next five years. However, the Company has not projected prize money to grow proportionately with the participation rate and revenue. Salem Partners has projected prize money per winner to increase 45% over the next five years. Management projected this variable to increase 20% over the next five years. This adjusts the prize money CAGR up to 89%, in line with revenue projections. Valuation is based on venture capital expected rates of return to reflect higher business risk.

Cost Structure No change Management’s projected expense items appeared to be reasonable considering historical costs and industry analysis of other channels.

6

Executive Summary

Overview of Revenue Enhancement Opportunities and Cost Savings The following chart presents a more detailed review of the potential revenue enhancement opportunities

and cost savings for GSN under 100% Liberty ownership, 100% SPE ownership and under the ownership of a major strategic.

Liberty Case SPE Case Major Strategic Case

Advertising Revenue Increase/Decrease

19% increase in 2008 (35% increase in national ad revenue) due to cross promotional opportunity of Liberty channels.

9% increase in 2009-2011 due to ratings impact of security of channel positioning.

Few revenue enhancement opportunities identified.

Possibility of revenue decrease due to ratings impact of weakening channel positioning.

23% increase in 2008 (45% increase in national ad revenue) due to cross promotional opportunity of Major Strategic channels.

9% increase in 2009-2011 due to ratings impact of security of channel positioning.

Affiliate Revenue Increase/Decrease

Consistent with Base Case. Consistent with Base Case. Consistent with Base Case.

International Network Opportunity

Utilize Chellomedia and Liberty Global to expand GSN internationally.

None, as instructed by SPE Management.

Leverage other international assets to roll out GSN internationally.

Cost Savings/Increases In Liberty Revenue and Cost Savings Case: 25% decrease in G&A. 50% headcount reduction in finance. 100% headcount reduction in HR. 20% decrease in affiliate sales cost. 50% cost reduction in facilities. 10% cost reduction in network operations. Severance costs equal to 50% of 2008

salaries. Moving costs incurred of $1 million. Lease breakage equal to one year’s rent.

Significant due to consolidation within SPE Los Angeles operation.

10% decrease in marketing. 61% decrease in ad sales cost. 25% decrease in G&A. Severance costs equal to 50% of annual

salaries of terminated employees. Moving costs incurred of $1 million for

incidentals.

100% decrease in marketing with the exception of media spending.

100% decrease in ad sales cost. 100% decrease in affiliate sales cost. 50% decrease in G&A. Severance costs equal to 50% of

annual salaries of terminated employees.

Moving costs incurred of $1 million for incidentals.

Increase in FUN Technologies value

Liberty can use FUN as a skill game tracking stock and drive valuation increase through a contractual arrangement with FUN.

Zero Zero

7

Notes: Queer Eye for the Straight Guy premiered on Bravo in July 2003 (T+8).

Notes: Beach Patrol: Miami Beach premiered on Court TV in July 06 (T+2).

Notes: 'Til Death Do Us Part premiered on Court TV in April 06 (T-1).

Notes: Las Vegas Law premiered on Court TV in February 06 (T-3).

Notes: The Chapelle Show premiered on Comedy Central in November 03 (T+7).

Notes: Each data point represents one month.

Executive Summary

Potential Ratings Increase due to Liberty Acquisition The chart below illustrates the ratings increase that occurred when Bravo, Comedy Central and Court TV

were acquired by NBC, MTV Networks and Time Warner, respectively. These transactions represent recent consolidations of formerly independent channels into major

media companies. We believe that cross promotion was a primary driver of the ratings increases.

Ratings Increase Due to Acquisition

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

T-9 T-8 T-7 T-6 T-5 T-4 T-3 T-2 T-1 0 T+1 T+2 T+3 T+4 T+5 T+6 T+7 T+8 T+9 T+10 T+11 T+12 T+13 T+14 T+15 T+16 T+17 T+18 T+19 T+20

Bravo Comedy Central Court TV

Acquisition Date

0.75

0.46

0.30

24

-Ho

ur

Nie

lse

n R

ati

ng

s

8

Executive Summary

Other Transactional Considerations We believe SPE should consider a number of other issues in preparation for negotiations with

Liberty and in making its ultimate buy/sell/hold decision.

Almost every major GSN affiliation agreement is either expired or will expire in 2007. We believe this factor presents significant risk to the business plan if the current

ownership of the Company is maintained or if SPE acquires 100% of the Company. We believe GSN’s affiliate status will be more stable under Liberty ownership due to

Liberty’s significant stake in DirecTV.

Liberty has shown in the past the willingness to utilize distribution leverage in mergers and acquisitions negotiations. Liberty or its predecessors have threatened the affiliate status of networks, even those in

which it maintains significant ownership, to force other owners of that business to sell their stake at a lower price.

9

Executive Summary

Other Transactional Considerations (Continued) From our conversations with GSN Management, we believe Liberty is enthusiastic about the

prospects for GSN and GSN.com to become large and dominant platforms for cash skill games. Certain value from cash skill games is included in the linear channel valuation. Identifying the incremental value Liberty might attribute to the opportunity has proven to

be difficult.

Although we have projected significant revenue enhancement opportunities for GSN under 100% Liberty ownership, such opportunities would have even greater potential if Liberty purchased Rainbow Media Holdings, which is rumored to be a possibility.

As reflected in the Major Strategic Case, we believe it is possible that the highest value for GSN would be in a sale of 100% of the Company to a party other than either SPE or Liberty. In a sale to Liberty, SPE should propose receiving a premium comparable to such a

scenario.

10

Executive Summary

Other Transactional Considerations (Continued) Liberty Management has communicated to the market that it intends to consolidate its holdings in an effort

to become more of an operating company and effect a simpler organizational structure. We believe an additional source of value for Liberty in a transaction involving GSN is the potential

transaction’s indication to the marketplace that the consolidation plan is viable. Liberty has not been able to consolidate 100% ownership of partially-owned subsidiary in quite some

time. Such an event could cause an increase in Liberty’s stock price that is disproportionate to the intrinsic

value created by its ownership of 100% of the Company.

Research Company Date Research Analyst Commentary

Bear Sterns 11/6/06 Robert S. Peck “With more than adequate liquidity on its balance sheet, outside share repurchases, we think it is likely the company could pursue strategic acquisitions to achieve synergistic leverage with its existing commerce platforms. We continue to remain bullish on the LINTA story while looking for further clarity on usage of liquidity/acquisitions.”

Citigroup 10/5/06 Jason Bazinet “We think Liberty will further exchange its passive stakes in other media companies (Time Warner, CBS, and Viacom) for assets that fit strategically with DIRECTV, allowing Liberty to emerge as a vertically integrated media company. Even though Liberty may acquire DIRECTV at $20 per share (its intrinsic value is $18), we find the savings from avoided taxes and a lower conglomerate discount would result in a share price of $101.”

Bear Stearns 8/9/06 Robert S. Peck “The shares are trading at a 23% discount to the net asset value, primarily reflecting the risks inherent in the complex capital structure, in our opinion. As the segment continues to deliver significant free cash flows and there is additional visibility into integration of recently acquired businesses (Provide Commerce & BUYSEASONS, Inc.), the use of cash for acquisitions (that could drive further growth) or for share repurchases (await for quarterly updates from Management on this front), as well as clarity on the potential tax liabilities, we think there is significant scope for multiple expansion.”

Jefferies 8/9/06 Robert G. Routh “As far as growth is concerned, Management said it plans to grow LINTA both organically as well as through strategic acquisitions and equity shrink as mentioned above. Dr. Malone also noted on the call that although now LINTA gets little value for them, eventually he would like LINTA to own and control both Expedia and InterActiveCorp, two entities now controlled by Barry Diller. He mentioned that long term these are strategic operations for LINTA and that the one year anniversary of the split off of Expedia from IACI is coming up, causing Morris Trust limitations to be ending and allowing for an aggressive restructuring of both companies, something he sees as happening in the not too distant future….we like the story, the stock’s visibility and cash flow generating capability.”

Jefferies 8/9/06 Robert G. Routh “We continue to think that the opportunity to combine QVC with HSN makes sense, and would simplify the overall company, which would reduce the holding company and tracking stock discount currently ascribed to the shares.”

11

Executive Summary

Information Reviewed/Collected In connection with this assignment, Salem Partners has reviewed:

Summaries of affiliation agreements between MSOs and satellite service providers and GSN.

Historical and projected subscriber information for GSN. Historical and projected license fee information for GSN. Historical and projected ratings information for GSN. Historical and projected financial information for GSN from 2003 through 2011. Schedule of programming commitments. Summary of top 10 advertisers. FUN Technologies and Game Trust agreements with GSN. Wall Street and industry research regarding long term advertising and affiliate revenue

growth rates. Industry research on online CPMs and unique visitor long term growth rates. Unique visitors of comparable online websites. Participation rates of comparable networks with participation revenue. Publicly available financial information regarding precedent change of control

transactions of US and international cable networks and online gaming companies. Ratings data for previously acquired networks. Publicly available financial information regarding publicly-traded US and international

cable network companies and online gaming sites.

12

Executive Summary

Information Reviewed/Collected (Continued) In addition, Salem Partners has conducted numerous due diligence sessions with GSN

Management to confirm information provided and assess the reasonableness of the GSN plan.

We have conducted discussions with numerous cable and cable network industry executives to assess certain qualitative elements of both the market environment for cable networks overall and that of independent cable channels in particular.

We have conducted discussions with numerous analysts and online gaming company executives to analyze and construct a plan for GSN.com that we believe reflects market expectations of similar opportunities.

We have conducted discussions with several international cable executives in order to analyze the opportunities for GSN outside of the United States.

We have compiled and analyzed available market data and projections for the cable network industry.

13

Executive Summary

Qualifications

This Report is subject in all respects to the following qualifications: This Report is intended only to provide a potential valuation of GSN, as defined herein, and expresses

no opinion as to the ability of GSN to fund any of its current obligations or to the solvency of GSN. This Report may only be used in connection with the matter of SPE, as defined in the engagement

letter dated February 14, 2007 (the “Engagement Letter”). This Report may not be summarized, excerpted from or otherwise used, made available to any other

third parties, other than to SPE, or publicly referred to, without the prior written approval of Salem Partners.

In arriving at the valuation presented in this Report, Salem Partners has not conducted a physical inspection of the properties and facilities of GSN and has not made, obtained or assumed any independent evaluations or appraisals of any such properties and facilities or of the assets or liabilities of GSN and have not assumed any responsibility or obligation to do so.

Salem Partners has taken into account our assessment of general economic, market and financial conditions and our experience in similar transactions, as well as our experience in valuation in general. The report necessarily is based upon conditions as they exist and can only be evaluated on the date hereof.

In arriving at a valuation, we have not considered the value that SPE, its shareholders or creditors may be able to obtain in a liquidation of GSN. The analysis of GSN as presented herein represents only the “fair market value” of a 100% ownership and controlling interest in GSN. The term “fair market value” as used herein, is defined as the amount at which the aggregate asset would change hands between a willing buyer and a willing seller, each having reasonable knowledge of all relevant facts, neither being under any compulsion to act, with equity to both. The projected cash flows also do not take into account any impact on the value of GSN due to the success of SPE’s or Liberty’s other activities.

14

Executive Summary

Qualifications (Continued) In our preparation of the Report, Salem Partners has relied upon the accuracy and completeness of

the financial and other information supplied to or otherwise used by it, has further relied upon the assurances of Management of the Company that they are not aware of any facts or circumstances that would make such information inaccurate or misleading, and shall not be obligated to attempt independently to verify, or undertake any obligation to verify, such information.

We express no opinion as to the value of GSN going forward. Developments subsequent to the date of this Report may affect the value of GSN and we do not have any obligation to update, revise or reaffirm this Report.

Salem Partners has reviewed unaudited financial information from SPE regarding GSN, and does not make any assumptions regarding the potential results of an audit.

Salem Partners shall be entitled to assume, and shall not be obligated to attempt independently to verify, or undertake any obligation to verify, that forecasts and projections supplied to it by the Management of SPE or GSN represent the best current judgments of such parties as to the future revenues to be received from and expenses associated with operation of GSN, and shall be entitled to assume that such forecasts and projections have been reasonably prepared based on such current judgment; provided, however, this reliance by Salem Partners does not eliminate its obligations under the Engagement to perform any and all tasks required to provide the Report. The Company will promptly notify Salem Partners if it learns of any material inaccuracy or misstatement in, or material omission from, any information provided to Salem Partners.

As compensation for its services rendered pursuant to this Report, Salem Partners has been or will be paid a cash fee and will be indemnified against certain liabilities that may arise as a result of its engagement and this Report. Salem Partners has not received any other compensation for investment banking services from the SPE, Liberty or GSN in the past five years.

15

GSN Business Plan ReviewGSN Business Plan Review

GSN Business Plan Review

Financial Overview The chart below sets forth historical and projected financial results for GSN as provided by

GSN Management (the “Management Case”).

($ in 000)For the Years Ended December 31, Projected for the Years Ending December 31,

2001A 2002A 2003A 2004A 2005A 2006A 2007E 2008E 2009E 2010E 2011E

RevenueAd Revenue (Net) $25,626 $33,518 $43,851 $49,742 $58,076 $62,292 $68,207 $78,189 $90,719 $106,364 $126,536Affiliate Revenue 33,711 39,800 44,576 53,066 58,763 61,483 66,994 74,312 82,901 91,943 102,445Participation Revenue 0 0 0 0 0 711 11,149 14,669 19,734 26,781 36,111Online Revenue 0 0 0 0 229 801 4,036 9,638 20,182 36,416 60,231Casino Revenue 0 0 0 0 375 710 1,000 1,450 1,850 2,250 2,500Other Revenue 8 27 31 34 118 626 811 1,224 1,741 2,625 3,796

Total Gross Revenue $59,345 $73,345 $88,458 $102,842 $117,561 $126,623 $152,197 $179,481 $217,128 $266,379 $331,619Launch Support Amort (22,008) (20,031) (12,813) (15,287) (14,449) (11,634) (6,865) (172) 0 0 0Online Revenue Share 0 0 0 0 (77) (296) (1,739) (3,721) (8,163) (14,953) (24,940)

Total Net Revenue $37,337 $53,314 $75,645 $87,555 $103,035 $114,693 $143,592 $175,588 $208,964 $251,426 $306,679

Operating CostsProgramming $21,368 $16,979 $26,713 $33,749 $39,393 $36,909 $41,247 $43,866 $50,903 $56,432 $62,009Participation Expense 0 0 0 0 0 859 8,432 9,041 9,937 11,074 12,489Network Operations 2,566 4,233 4,458 3,412 3,203 3,398 3,649 3,855 4,074 4,308 4,557Online/Interactive 714 2,795 4,050 4,370 5,295 6,375 8,748 9,109 9,640 10,478 10,751Marketing 5,018 15,670 14,157 26,421 24,421 25,520 26,015 27,377 28,828 30,377 32,031Ad Sales 4,692 5,410 6,084 6,012 6,533 6,823 7,509 8,104 8,938 9,652 10,425Affiliate Sales 3,298 5,953 4,947 3,220 4,444 4,795 4,837 4,711 5,009 5,327 5,671Gen & Admin 16,273 13,189 14,608 12,041 12,483 13,801 16,009 17,181 18,715 19,948 21,269

Total Operating Costs $53,929 $64,229 $75,017 $89,225 $95,772 $98,479 $116,446 $123,243 $136,045 $147,596 $159,201

EBITDA ($16,592) ($10,915) $628 ($1,670) $7,263 $16,214 $27,147 $52,345 $72,920 $103,830 $147,478

Other Inc/(Exp) (756) (872) (1,104) (1,116) (237) (215) 32 60 453 661 969

Net Income ($17,348) ($11,787) ($476) ($2,786) $7,026 $15,998 $27,178 $52,405 $73,373 $104,492 $148,447

16

GSN Business Plan Review

Financial Overview (Continued) The chart below sets forth our Base Case assumptions for GSN.

($ in 000)For the Years Ended December 31, Projected for the Years Ending December 31,

2001A 2002A 2003A 2004A 2005A 2006A 2007E 2008E 2009E 2010E 2011E

RevenueAd Revenue (Net) $25,626 $33,518 $43,851 $49,742 $58,076 $62,292 $65,340 $71,114 $77,619 $84,853 $93,249Affiliate Revenue 33,711 39,800 44,576 53,066 58,763 61,483 65,300 71,203 75,834 80,706 86,443Participation Revenue 0 0 0 0 0 711 11,149 14,669 19,734 26,781 36,111Online Revenue 0 0 0 0 229 801 3,132 9,163 18,403 32,634 55,680Casino Revenue 0 0 0 0 375 710 1,000 1,450 1,850 2,250 2,500Other Revenue 8 27 31 34 118 626 813 1,229 1,756 2,656 3,865

Total Gross Revenue $59,345 $73,345 $88,458 $102,842 $117,561 $126,623 $146,734 $168,827 $195,196 $229,880 $277,848Launch Support Amort (22,008) (20,031) (12,813) (15,287) (14,449) (11,634) (6,865) (172) 0 0 0Online Revenue Share 0 0 0 0 (77) (296) (1,261) (3,397) (7,085) (12,796) (22,221)

Total Net Revenue $37,337 $53,314 $75,645 $87,555 $103,035 $114,693 $138,608 $165,258 $188,111 $217,084 $255,627

Operating CostsProgramming $21,368 $16,979 $26,713 $33,749 $39,393 $36,909 $41,205 $43,775 $50,722 $56,137 $61,565Participation Expense 0 0 0 0 0 859 8,599 9,483 10,818 12,641 15,107Network Operations 2,566 4,233 4,458 3,412 3,203 3,398 3,649 3,855 4,074 4,308 4,557Online/Interactive 714 2,795 4,050 4,370 5,295 6,375 8,748 9,109 9,640 10,478 10,751Marketing 5,018 15,670 14,157 26,421 24,421 25,520 26,015 27,377 28,828 30,377 32,031Ad Sales 4,692 5,410 6,084 6,012 6,533 6,823 7,502 8,097 8,931 9,644 10,417Affiliate Sales 3,298 5,953 4,947 3,220 4,444 4,795 4,833 4,703 4,991 5,299 5,631Gen & Admin 16,273 13,189 14,608 12,041 12,483 13,801 16,009 17,181 18,715 19,948 21,269

Total Operating Costs $53,929 $64,229 $75,017 $89,225 $95,772 $98,479 $116,560 $123,579 $136,720 $148,833 $161,329

EBITDA ($16,592) ($10,915) $628 ($1,670) $7,263 $16,214 $22,048 $41,680 $51,392 $68,251 $94,298

Other Inc/(Exp) (756) (872) (1,104) (1,116) (237) (215) 32 60 453 661 969

Net Income ($17,348) ($11,787) ($476) ($2,786) $7,026 $15,998 $22,080 $41,740 $51,845 $68,913 $95,267

17

GSN Business Plan Review

Financial Overview – Management Case versus Base Case The chart below sets forth the differences between Management’s projected financial results

and the Base Case assumptions for GSN.

($ in 000)For the Years Ended December 31, Projected for the Years Ending December 31,

2001A 2002A 2003A 2004A 2005A 2006A 2007E 2008E 2009E 2010E 2011E

RevenueAd Revenue (Net) $0 $0 $0 $0 $0 $0 ($2,867) ($7,075) ($13,101) ($21,511) ($33,287)Affiliate Revenue 0 0 0 0 0 0 (1,694) (3,109) (7,067) (11,237) (16,002)Participation Revenue 0 0 0 0 0 0 0 0 0 0 0Online Revenue 0 0 0 0 0 0 (904) (474) (1,779) (3,782) (4,551)Casino Revenue 0 0 0 0 0 0 0 0 0 0 0Other Revenue 0 0 0 0 0 0 2 5 15 32 69

Total Gross Revenue $0 $0 $0 $0 $0 $0 ($5,463) ($10,654) ($21,931) ($36,499) ($53,771)Launch Support Amort 0 0 0 0 0 0 0 0 0 0 0Online Revenue Share 0 0 0 0 0 0 479 324 1,078 2,157 2,719

Total Net Revenue $0 $0 $0 $0 $0 $0 ($4,984) ($10,329) ($20,853) ($34,342) ($51,052)

Operating CostsProgramming $0 $0 $0 $0 $0 $0 ($41) ($92) ($182) ($295) ($444)Participation Expense 0 0 0 0 0 0 167 442 882 1,567 2,618Network Operations 0 0 0 0 0 0 0 0 0 0 0Online/Interactive 0 0 0 0 0 0 0 0 0 0 0Marketing 0 0 0 0 0 0 0 0 0 0 0Ad Sales 0 0 0 0 0 0 (7) (7) (7) (7) (7)Affiliate Sales 0 0 0 0 0 0 (4) (8) (18) (28) (40)Gen & Admin 0 0 0 0 0 0 0 0 0 0 0Severance 0 0 0 0 0 0 0 0 0 0 0Moving Costs 0 0 0 0 0 0 0 0 0 0 0

Total Operating Costs $0 $0 $0 $0 $0 $0 $114 $336 $675 $1,237 $2,127

EBITDA $0 $0 $0 $0 $0 $0 ($5,098) ($10,665) ($21,528) ($35,579) ($53,179)

Other Inc/(Exp) 0 0 0 0 0 0 0 0 0 0 0

Net Income $0 $0 $0 $0 $0 $0 ($5,098) ($10,665) ($21,528) ($35,579) ($53,179)

18

GSN Business Plan Review

Assumptions The chart below illustrates the 5 year CAGR assumptions Salem Partners used to derive its

valuation of GSN compared to the assumptions GSN Management used to derive its long range plan.

5 Year CAGR AssumptionsManagement

Case Base Case

Affiliate RevenueSubscriber Growth 3.9% 3.9%License Fee/Subscriber Growth 6.6 3.0

Total Affiliate Revenue Growth 10.8% 7.1%

Advertising Revenue% Sold Growth 2.4% 2.4%Ratings Growth 11.0 0.0CPM Growth 5.5 5.5VPVH Growth 5.0 5.0

Total Advertising Revenue Growth 15.2% 8.3%

Online RevenueMonthly Uniques - GSN TV Viewers Growth 38.1% 38.1%Monthly Uniques - Non GSN TV Viewers (1)

77.8 73.2Total Monthly Uniques Growth 46.0 54.0Banner Ad CPM Growth 17.6 17.6Video Ad CPM Growth 5.0 5.0% Visits Watching Videos(1)

49.5 10.0Videos Watched Per Visit(1)

31.6 10.0% Uniques Subscribing 112.5 85.3Subscription Growth 219.6 193.9% Download Games(1)

31.6 18.3Total Online Revenue Growth 137.2% 133.5%

Participation RevenueAverage Rating per Airing Growth 10.0% 10.0%Total Participants Growth 68.1 68.1Entries per Participant Growth 8.7 8.7Net Revenue per Entry Growth 3.2 3.2

Total Participation Revenue Growth 119.4% 119.4%

Participation ExpenseWinner/On Air % 0.0% 0.0%Money Per Winner 20.0 45.0Total Prize Money 70.4 89.4

Total Participation Expense Growth 70.8% 77.4%(1) Represents a 4 year CAGR from 2007 through 2011.

19

GSN Business Plan Review

Introduction Salem Partners has conducted a detailed review of GSN’s 2007 budget as well as its long

range plan.

The objective of the review is to assess the reasonableness of the revenue and expense assumptions utilized in the Company’s cash flow projections and suggest potential modifications to the projections for use as our Base Case for valuation purposes.

In general, the Base Case differs from the Management Case in the following areas: Subscriber fee growth. Advertising sales growth, primarily as driven by ratings increases. Participation and online components of the business.

– Very little data has been provided to support either business model.– While we believe the online opportunity is of the order of magnitude reflected in

Management’s plan, we do not believe the business model provided to us reflected our, or Management’s, view of how the business will develop.

20

GSN Business Plan Review

Advertising Revenue

Cable networks as a group have continued to take audience from broadcast networks, surpassing broadcast networks in April 2002.

This positive effect has been mitigated somewhat by the proliferation of networks over the previous ten years as well as competition from non-television entertainment options. Average ratings growth for the cable networks industry of 5.9% annually over the past 10

years.

Growth in ratings combined with CPM growth in the mid-single digits has resulted in advertising growth for the industry group overall of 17.3% annually over the past 9 years.

In 2006, advertising revenue growth for the cable industry slowed to 14.8%. Industry sources indicate that the significant share growth of cable networks advertising

has slowed significantly.

21

GSN Business Plan Review

Advertising Revenue GSN Management projects 9% growth in gross advertising revenue in fiscal 2007 and a 15% CAGR from

fiscal 2006 through fiscal 2011.

The following chart compares GSN’s projected advertising growth with that of several other network groups and for the cable network industry overall. Information supplied regarding GSN reflects a blend of national spot advertising, infomercial and

direct response advertising.

Projected Advertising Revenue Growth Rate2006 2007 L-T Growth Rate

GSN(1)7.7% 9.2% 15.2%

Hallmark Channel(2)13.3 16.5 NA

Viacom Cable Networks(3)7.5 6.9 6.7%

Disney Cable Networks(4)7.5 15.2 10.6

Time Warner Networks(3)6.0 6.7 7.0

Discovery Networks(4)2.0 5.8 5.9

News Corp. Networks(4)11.1 8.0 7.2

Cable Network Industry(2)14.8 13.8 12.7

(1) Long term growth rate is from 2006 through 2011.(2) Long term growth rate for overall industry is from 2006 through 2010, source is Kagan Research.(3) Long term growth rate is from 2006 through 2010, source is Wall Street consensus estimates.(4) Long term growth rate is from 2006 through 2008, source is Wall Street consensus estimates.

22

GSN Business Plan ReviewNational Spot Revenue Discussion GSN has a relatively low level of national spot sales, with approximately $27 million generated on a gross basis in 2006.

GSN Management projects 27% growth in national spot sales in fiscal 2007 and a 29% CAGR from fiscal 2006 through fiscal 2011.

Over the long term projection period (five years), revenue is expected to increase almost four times. The growth in national spot revenue at GSN is projected to be driven by three primary factors:

Growth in ratings Growth in viewers per viewing household Growth in CMPs

Ratings GSN Management expects to grow ratings an average of 11% over the next five years, to an average household rating

of 0.545. The following charts set forth the ratings of the top 20 highest rated cable networks in 2005: a 0.545 rating would

establish GSN in that list, a potentially unrealistic assumption for a standalone niche channel.

2005 Average 24-Hour Rating by Cable Network

Source: Kagan research and Nielsen Source: Kagan research and Nielsen

Average 24-Hour Rating by Cable Network Five Year2000 2001 2002 2003 2004 2005 CAGR

Nickelodeon 1.53 1.39 1.16 1.52 1.64 1.70 2.1%TNT 0.87 0.88 0.93 1.13 1.18 1.23 7.2Cartoon 1.11 1.13 1.13 1.14 1.13 1.18 1.2Disney Channel 0.00 0.80 0.83 1.13 1.13 1.15 NALifetime 1.11 1.23 1.22 1.14 1.00 1.00 (2.1)Fox News 0.00 0.55 0.70 1.00 0.88 0.93 NATBS 1.14 1.05 0.95 0.90 0.85 0.85 (5.7)USA 0.89 0.80 0.85 0.83 0.86 0.77 (2.9)ESPN 0.69 0.60 0.68 0.75 0.77 0.73 1.1Hallmark 0.00 0.30 0.26 0.44 0.58 0.71 NAMTV 0.57 0.50 0.52 0.56 0.58 0.64 2.3Spike TV 0.41 0.46 0.44 0.45 0.47 0.61 8.3ABC Family 0.52 0.53 0.51 0.46 0.57 0.59 2.6FX Network 0.53 0.50 0.53 0.52 0.57 0.58 1.8History Channel 0.57 0.53 0.48 0.52 0.58 0.58 0.3TV Land 0.46 0.43 0.46 0.48 0.49 0.58 4.7A&E 0.91 0.81 0.66 0.61 0.60 0.56 (9.3)Court TV 0.34 0.35 0.41 0.40 0.54 0.53 9.3CNN 0.63 0.85 0.55 0.68 0.48 0.53 (3.4)Discovery 0.65 0.63 0.57 0.53 0.52 0.51 (4.7)GSN 0.33 0.31 0.27 0.28 0.25 0.31 (1.2)Total 13.26 14.63 14.11 15.47 15.67 16.27 4.2%

1.70

1.231.18 1.15

1.000.93

0.850.77 0.73 0.71

0.64 0.61 0.59 0.58 0.58 0.58 0.56 0.55 0.53 0.53 0.51

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Nic

kelo

deon

TN

T

Car

toon

Dis

ney

Cha

nnel

Life

time

Fox

New

s

TB

S

US

A

ES

PN

Hal

lmar

k

MT

V

Spi

ke T

V

AB

C F

amily

FX

Net

wor

k

His

tory

Cha

nnel

TV

Lan

d

A&

E

2011

GS

N P

roje

ctio

n

Cou

rt T

V

CN

N

Dis

cove

ry

2005

Ave

rag

e 24

Hr.

Rat

ing

23

GSN Business Plan Review

National Spot Revenue Discussion (Continued) In addition, we believe that the continued

proliferation of entertainment product, including cable networks, that compete for consumers’ share may lead to more difficulty in establishing higher ratings without a significant hit show. Historical ratings have been flat for the past

three years as outlined by the graph on the right.

CPM GSN Management expects CPMs to grow at an

average rate of 5% over the next five years to an average rate of $5.66.

We believe this assumption reflects market expectations for the growth of cable network CPMs overall.

The table to the right sets forth the CPMs of comparable, independently operated networks.

Source: Kagan research and the Cabletelevision Advertising Bureau

2005 CPM Target Demographics

Style $6.44 W18-49

Food 5.13 W18-49, W25-54

Lifetime 4.33 A18-49, A25-54, W18-49, W25-54

GSN 4.23 A25-54, W25-54

A&E 3.95 A18-49, A25-34, A25-54, M18-49, W18-49

E! 3.72 A18-49

History Channel 3.45 A18-49, A25-54, M18-49, M25-54, M35-49, W25-54

Weather Channel 3.43 A18-54

MSNBC 3.34 A25-54, M25-54, W25-54

Hallmark Channel 2.48 A18-49, A25-54, W18-49, W25-54

Historical GSN Total Day Ratings

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

12/2

7/99

-03/

26/0

0

06/2

6/00

-10/

01/0

0

01/0

1/01

-04/

01/0

1

07/0

2/01

-09/

30/0

1

12/3

1/01

-03/

31/0

2

07/0

1/02

-09/

29/0

2

12/3

0/02

-03/

30/0

3

06/3

0/03

-09/

28/0

3

12/2

9/03

-03/

28/0

4

06/2

8/04

-09/

26/0

4

12/2

7/04

-03/

27/0

5

06/2

7/05

-09/

25/0

5

12/2

6/05

-03/

26/0

6

06/2

6/06

-09/

24/0

6

01/0

1/07

-02/

25/0

7

24

GSN Business Plan Review

Comparison to Hallmark Channel We believe that there is validity to the assumption that advertising revenue per subscriber

increases as the number of subscribers of a cable network grows.

Hallmark Channel’s growth from approximately 47 million subscribers to approximately 75 million subscribers can be used to analyze the appropriateness of GSN advertising projections as it grows from 55 million subscribers to a projected 68 million subscribers by the end of 2011.

($ in 000)Hallmark Channel For the Years Ended December 31, 4 Year

2002A 2003A 2004A 2005A 2006A CAGR

Total Advertising Revenue(1)$40,991 $76,153 $104,481 $143,780 $172,950 43.3%

Average Subscribers 46,800 53,100 61,700 69,100 74,600 12.4Average 24 Hour Ratings 0.26 0.44 0.58 0.71 0.76 31.0Revenue per Subscriber

per Ratings Point $0.22 $0.63 $0.98 $1.47 $1.75 67.1%

Total Programming Cost $50,600 $66,200 $85,700 $122,300 $130,900 26.8%

Total Marketing Cost $34,004 $16,619 $16,477 $24,160 $16,021 (17.2%)

GSN(2) For the Years Ending December 31, 4 Year2007E 2008E 2009E 2010E 2011E CAGR

Net Advertising Revenue(1)$68,207 $78,189 $90,719 $106,364 $126,536 16.7%

Average Subscribers 56,325 58,790 61,290 63,636 66,353 4.2Average 24 Hour Ratings 0.36 0.40 0.44 0.49 0.55 11.0Revenue per Subscriber

per Ratings Point $0.43 $0.53 $0.65 $0.82 $1.04 24.4%Total Programming Cost(3)

$41,247 $43,866 $50,903 $56,432 $62,009 10.7%

Total Marketing Cost $26,015 $27,377 $28,828 $30,377 $32,031 5.3%

(1) Represents net advertising revenue.(2) Represents GSN Management Case.(3) Represents programming expense, programming amortization, acquisitions and scheduling and new media and short form.

25

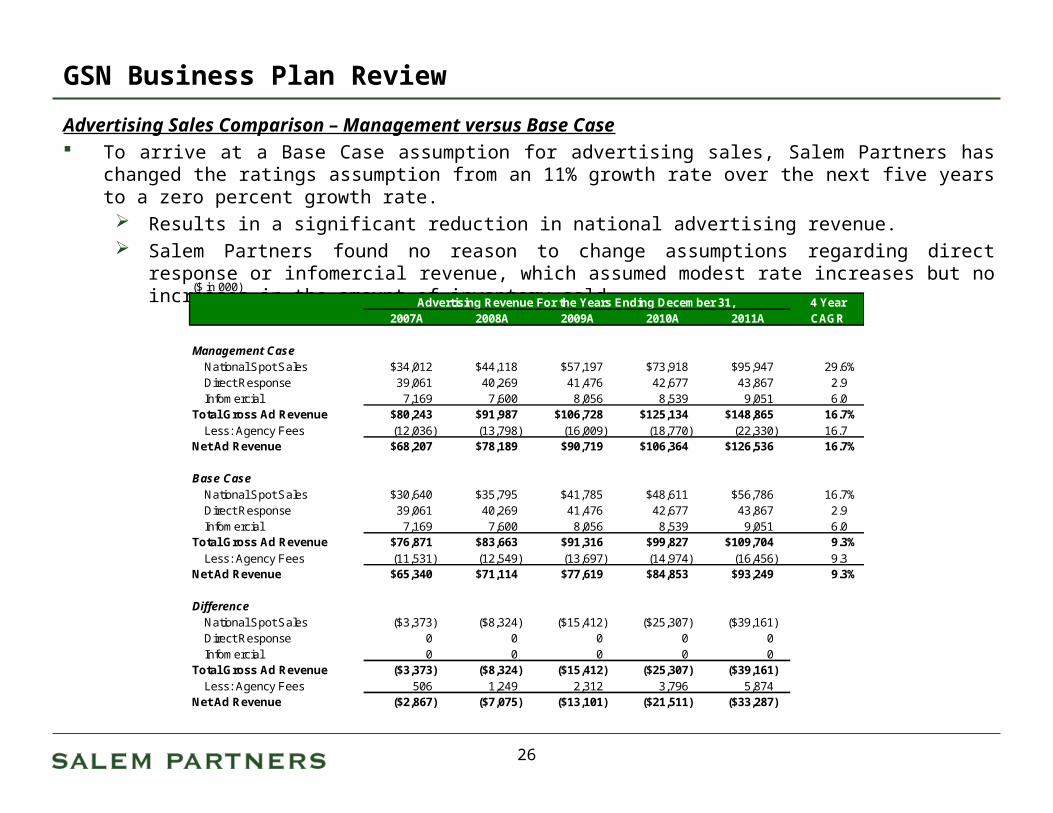

GSN Business Plan Review

Advertising Sales Comparison – Management versus Base Case To arrive at a Base Case assumption for advertising sales, Salem Partners has changed the ratings

assumption from an 11% growth rate over the next five years to a zero percent growth rate. Results in a significant reduction in national advertising revenue. Salem Partners found no reason to change assumptions regarding direct response or infomercial

revenue, which assumed modest rate increases but no increases in the amount of inventory sold.

($ in 000)Advertising Revenue For the Years Ending December 31, 4 Year

2007A 2008A 2009A 2010A 2011A CAGR

Management CaseNational Spot Sales $34,012 $44,118 $57,197 $73,918 $95,947 29.6%Direct Response 39,061 40,269 41,476 42,677 43,867 2.9Infomercial 7,169 7,600 8,056 8,539 9,051 6.0

Total Gross Ad Revenue $80,243 $91,987 $106,728 $125,134 $148,865 16.7%Less: Agency Fees (12,036) (13,798) (16,009) (18,770) (22,330) 16.7

Net Ad Revenue $68,207 $78,189 $90,719 $106,364 $126,536 16.7%

Base CaseNational Spot Sales $30,640 $35,795 $41,785 $48,611 $56,786 16.7%Direct Response 39,061 40,269 41,476 42,677 43,867 2.9Infomercial 7,169 7,600 8,056 8,539 9,051 6.0

Total Gross Ad Revenue $76,871 $83,663 $91,316 $99,827 $109,704 9.3%Less: Agency Fees (11,531) (12,549) (13,697) (14,974) (16,456) 9.3

Net Ad Revenue $65,340 $71,114 $77,619 $84,853 $93,249 9.3%

DifferenceNational Spot Sales ($3,373) ($8,324) ($15,412) ($25,307) ($39,161)Direct Response 0 0 0 0 0Infomercial 0 0 0 0 0

Total Gross Ad Revenue ($3,373) ($8,324) ($15,412) ($25,307) ($39,161)Less: Agency Fees 506 1,249 2,312 3,796 5,874

Net Ad Revenue ($2,867) ($7,075) ($13,101) ($21,511) ($33,287)

26

GSN Business Plan Review

Affiliate Revenue Over the last several years the distribution environment has grown increasingly difficult for cable

networks, particularly independent networks that lack the benefit of critical mass of popularity with viewers.

The difficulties in the market have resulted from several factors:

Continued consolidation of distributors (MSOs), further increasing their negotiating leverage when establishing affiliation fee levels,

Increased focus by MSOs on services other than linear video programming, such as high speed data and telephony, limiting bandwidth available for growing networks, and

Increased focus on reducing the growth of programming costs.

These trends have resulted in: Longer and sometimes more acrimonious negotiations between networks and distributors, and A noticeable reduction in the rate of growth in subscriber fees.

The chart on the following page outlines GSN’s current affiliation agreements. Most of GSN’s agreements have either expired or will expire this year. The status of these agreements presents significant risk to the business plan.

27

GSN Business Plan Review

MSO Total GSN Subs Current Term Current Rates Status of Contract Discussions

DirectTV 14,031,000 Expired on 1/31/07

$0.0775 Did not exercise option to extend term through 1/31/09. Do not want to lock in specific tier but would discuss carriage in terms of penetration.

Comcast 13,962,000 Expires on 5/1/07

$0.08 Comcast contact is on maternity leave until April/May. Will start negotiations when she returns.

Echostar 7,840,000 Expires on 3/31/11

MFN Recently concluded long-term affiliation agreement with Echostar for AT120 carriage.

Time Warner 5,596,000 Expires on 12/31/07

$0.095 (digital), $0.08 (expanded basic)

Prepared to begin contract renewal discussions in the upcoming weeks.

Charter 3,892,000 Expired on 12/31/06

TBD (Charter proposed $0.13, GSN proposed $0.14)

Have been exchanging proposals since last fall. GSN to send counter proposal. Significant reduction in per subscriber fees will be implemented.

NCTC 2,550,000 Expires on 12/31/08

$0.20 in 2007, $0.22 in 2008

Agreement recently rolled over for an additional two years, ending in 2008.

Cablevision 2,300,000 Expired on 1/31/05

TBD (still receiving 2005 rate of $0.11)

In negotiations.

Cox 1,898,000 Expires on 1/31/07

$0.22 Contract discussions to begin in summer 2007.

28

GSN Business Plan Review

Affiliate Revenue GSN generated approximately $64 million of affiliate fees on a gross basis in 2006.

GSN Management projects 7% growth in affiliate fee revenue in fiscal 2007 and a 10% CAGR from fiscal 2006 through fiscal 2011.

Salem Partners has had conversations with a number of professionals in the cable networks industry and has conducted other research. These conversations generally indicate that cable network affiliate discussions can be divided into

three tiers when determining growth rates agreed in the current round of affiliate contracts. Tier 1: High-single digit to low- to mid-teen growth rates Tier 2: Low- to mid-single digit growth rates Tier 3: Flat to decreasing growth rates

We believe GSN would be considered a Tier 2 cable network. The following chart compares GSN’s projected affiliate fee growth with that of several other network groups

and for the cable network industry overall.Projected Affiliate Revenue Growth Rate

2006 2007 L-T Growth Rate

GSN(1)5.9% 6.5% 9.7%

Hallmark Channel(2)13.0 19.5 NA

Viacom Cable Networks(3)9.5 6.4 6.0

Disney Cable Networks(3)10.9 9.0 7.7

Time Warner Networks(3)5.9 6.2 7.7

Discovery Networks(4)16.9 10.0 8.9

News Corp. Networks(4)20.9 17.0 16.0

Cable Network Industry(5)9.5 7.8 7.6

(1) Long term growth rate is from 2006 through 2011.(2) Source is Kagan Research.(3) Long term growth rate is from 2006 through 2010, source is Wall Street consensus estimates.(4) Long term growth rate is from 2006 through 2008, source is Wall Street consensus estimates.(5) Long term growth rate for overall industry is from 2006 through 2010, source is Wachovia Securities research.

29

GSN Business Plan Review

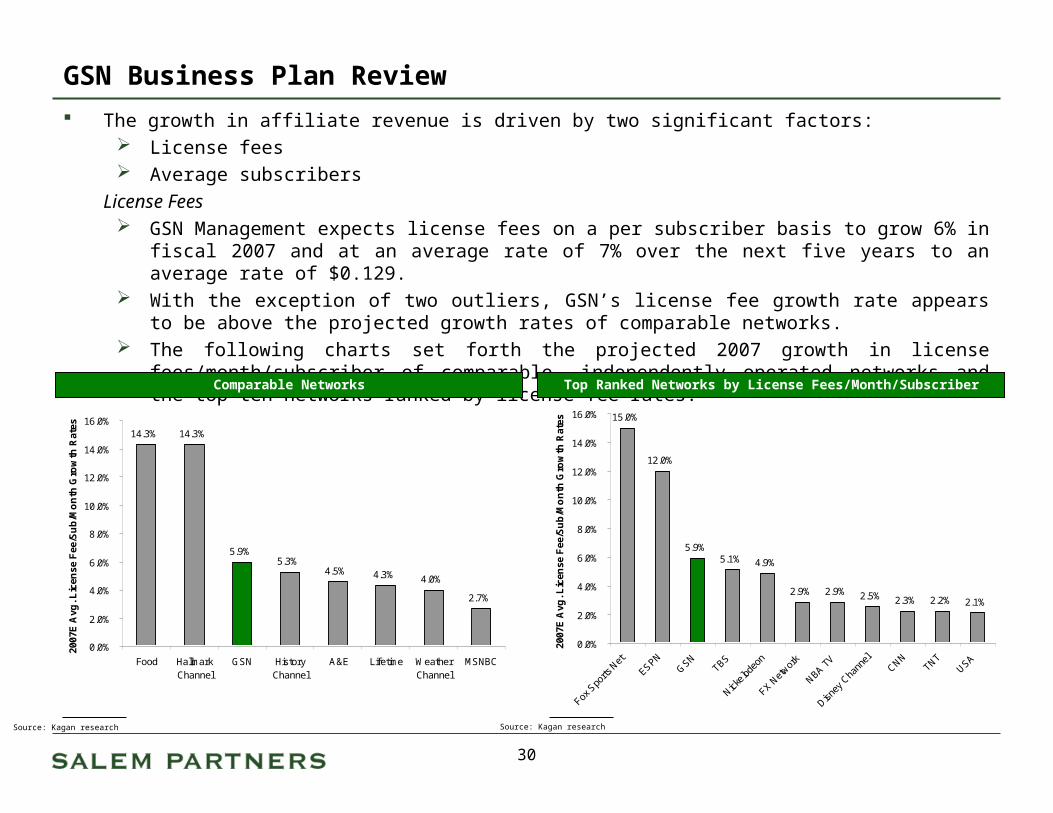

The growth in affiliate revenue is driven by two significant factors: License fees Average subscribers

License Fees GSN Management expects license fees on a per subscriber basis to grow 6% in fiscal 2007 and at

an average rate of 7% over the next five years to an average rate of $0.129. With the exception of two outliers, GSN’s license fee growth rate appears to be above the projected

growth rates of comparable networks. The following charts set forth the projected 2007 growth in license fees/month/subscriber of

comparable, independently operated networks and the top ten networks ranked by license fee rates.

Source: Kagan research

Comparable Networks Top Ranked Networks by License Fees/Month/Subscriber

Source: Kagan research

15.0%

12.0%

5.9%5.1% 4.9%

2.9% 2.9% 2.5% 2.3% 2.2% 2.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Fox S

ports

Net

ESPNG

SNTBS

Nickelod

eon

FX Net

work

NBA TV

Disney

Cha

nnel

CNNTNT

USA

2007

E A

vg. L

icen

se F

ee/S

ub

/Mo

nth

Gro

wth

Rat

es

14.3% 14.3%

5.9%5.3%

4.5% 4.3% 4.0%

2.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Food HallmarkChannel

GSN HistoryChannel

A&E Lifetime WeatherChannel

MSNBC

2007

E A

vg. L

icen

se F

ee/S

ub

/Mo

nth

Gro

wth

Rat

es

30

GSN Business Plan Review

Average Subscribers GSN Management expects average subscribers to grow 3% in fiscal 2007 and at an average rate of

4% over the next five years to 68 million subscribers. GSN’s subscriber growth rate assumptions appear to be in line with the growth rates of similar

networks within the industry. The following charts set forth the 2007 growth in average subscribers of comparable, independently

operated networks.

Source: Kagan research

Comparable Networks

5.9%

3.7%3.5% 3.4%

2.8%

1.9%1.6%

1.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

HallmarkChannel

MSNBC Food WeatherChannel

GSN Lifetime HistoryChannel

A&E

2007

E A

vera

ge

Su

bsc

rib

er G

row

th R

ates

31

GSN Business Plan Review

Affiliate Revenue Comparison – Management versus Base Case To arrive at a Base Case assumption for affiliate revenue, Salem Partners has changed the subscriber fee

growth rate assumption from approximately 7% to 3% from 2006 to 2011. We believe there is further downside exposure to affiliate subscriber fees.

($ in 000)Affiliate Revenue For the Years Ending December 31, 4 Year

2007A 2008A 2009A 2010A 2011A CAGR

Management CaseAverage Subscribers 56,325 58,790 61,290 63,636 66,353 4.2%Average Subscriber Fee/Month $0.10 $0.11 $0.11 $0.12 $0.13 6.7

Total Subscriber Revenue $66,994 $74,312 $82,901 $91,943 $102,445 11.2%

Base CaseAverage Subscribers 56,325 58,790 61,290 63,636 66,353 4.2%Average Subscriber Fee/Month $0.10 $0.10 $0.10 $0.11 $0.11 3.0

Total Subscriber Revenue $65,300 $71,203 $75,834 $80,706 $86,443 7.3%

DifferenceAverage Subscribers 0 0 0 0 0Average Subscriber Fee/Month ($0.00) ($0.00) ($0.01) ($0.01) ($0.02)

Total Subscriber Revenue ($1,694) ($3,109) ($7,067) ($11,237) ($16,002)

32

50.0%

30.0%

15.0%12.0% 11.0%

4.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Pro Sieben Media(1) Top Chef (Bravo) Flavor of Love (VH1) Last Comic Standing(NBC)

GSN 2011 Projection GSN Historical

Par

ticip

atio

n R

ate

GSN Business Plan Review

Participation Business GSN’s programming allows viewers to participate in its game shows through phone and SMS entries. GSN Management projects participation revenue to grow to approximately $7 million in fiscal 2007, or

482%, with a long term average growth rate of 89% through fiscal 2011. A significant driver of participation revenue is the participation rate.

GSN’s current participation rate is 4% and is projected to grow to 11% over the course of the projection period.

Amounts charged per phone or SMS entry is projected to remain flat through fiscal 2011. The volume of participation-based programming is also projected to grow significantly over the period, from

6 hours per week currently to 16 hours per week in 2011. Below is a graph of other programs’ participation rates when inclusive of an audience participation

component.Participation Rates

(1) Pro Sieben Media owns 9Live in Germany and other gaming networks with interactive programming.

33

GSN Business Plan Review

Participation Business Currently, participants can only participate via SMS entries. However, in 2007 GSN will begin to offer the ability to phone into the game show.

Expected to be 50% of volume by 2011. Phone capability enables GSN to access its older skewing demographic, which typically

does not use SMS technology. GSN Management admits that participation is a new business model for the network and for this

country. $1.2 million gross revenue generated in 2006. $30.1 million gross revenue projected in 2011. We believe this revenue and cash flow stream is speculative. Early results from Playmania are interesting, but do not support the anticipated growth in that

segment of the business. We have reflected the speculative nature of the participation segment of the business in the

discount rate applied to the projections in the discounted cash flow analysis. Management has projected an 89% increase in participation revenue over the next five years.

However, the Company has not projected prize money to grow proportionately with the participation rate and revenue.

Salem Partners has projected the money per winner to grow by 45% each year, reaching $509 by 2011, while Management projected this to grow by 20% each year.

This adjustment brings the prize money CAGR up to 89%, in line with revenue projections.

34

GSN Business Plan Review

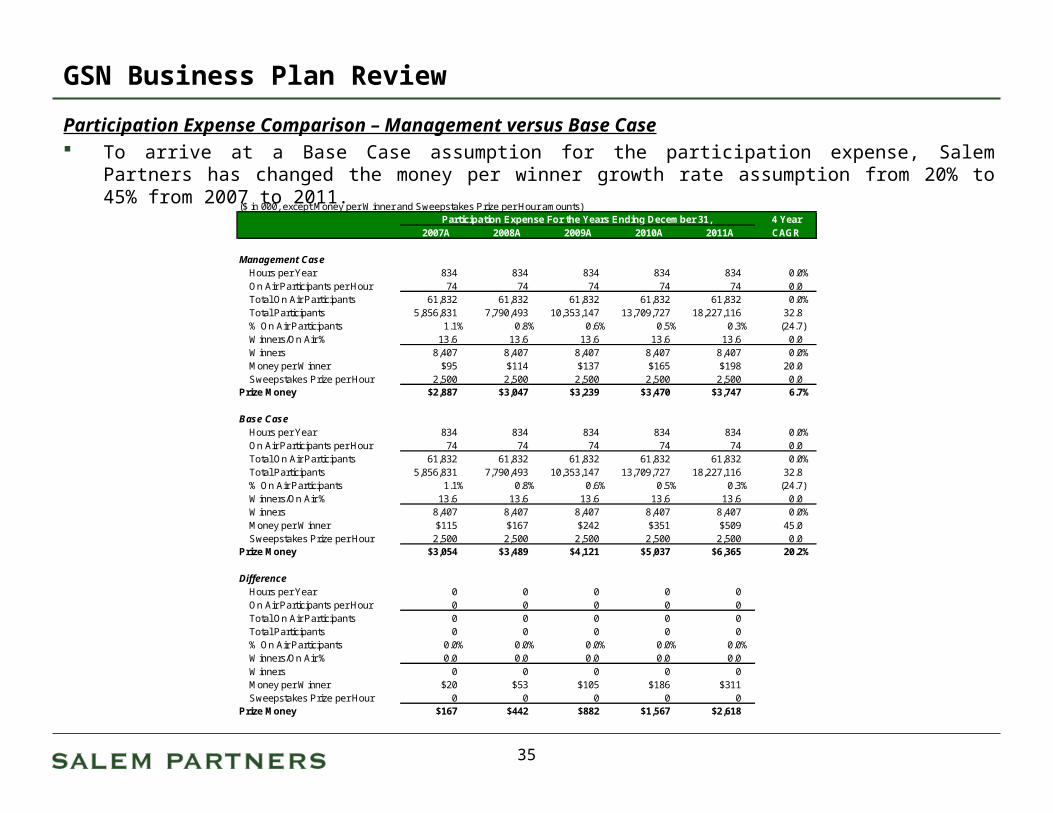

Participation Expense Comparison – Management versus Base Case To arrive at a Base Case assumption for the participation expense, Salem Partners has changed the

money per winner growth rate assumption from 20% to 45% from 2007 to 2011.

($ in 000, except Money per Winner and Sweepstakes Prize per Hour amounts)Participation Expense For the Years Ending December 31, 4 Year

2007A 2008A 2009A 2010A 2011A CAGR

Management CaseHours per Year 834 834 834 834 834 0.0%On Air Participants per Hour 74 74 74 74 74 0.0Total On Air Participants 61,832 61,832 61,832 61,832 61,832 0.0%Total Participants 5,856,831 7,790,493 10,353,147 13,709,727 18,227,116 32.8% On Air Participants 1.1% 0.8% 0.6% 0.5% 0.3% (24.7)Winners/On Air % 13.6 13.6 13.6 13.6 13.6 0.0Winners 8,407 8,407 8,407 8,407 8,407 0.0%Money per Winner $95 $114 $137 $165 $198 20.0Sweepstakes Prize per Hour 2,500 2,500 2,500 2,500 2,500 0.0

Prize Money $2,887 $3,047 $3,239 $3,470 $3,747 6.7%

Base CaseHours per Year 834 834 834 834 834 0.0%On Air Participants per Hour 74 74 74 74 74 0.0Total On Air Participants 61,832 61,832 61,832 61,832 61,832 0.0%Total Participants 5,856,831 7,790,493 10,353,147 13,709,727 18,227,116 32.8% On Air Participants 1.1% 0.8% 0.6% 0.5% 0.3% (24.7)Winners/On Air % 13.6 13.6 13.6 13.6 13.6 0.0Winners 8,407 8,407 8,407 8,407 8,407 0.0%Money per Winner $115 $167 $242 $351 $509 45.0Sweepstakes Prize per Hour 2,500 2,500 2,500 2,500 2,500 0.0

Prize Money $3,054 $3,489 $4,121 $5,037 $6,365 20.2%

DifferenceHours per Year 0 0 0 0 0On Air Participants per Hour 0 0 0 0 0Total On Air Participants 0 0 0 0 0Total Participants 0 0 0 0 0% On Air Participants 0.0% 0.0% 0.0% 0.0% 0.0%Winners/On Air % 0.0 0.0 0.0 0.0 0.0Winners 0 0 0 0 0Money per Winner $20 $53 $105 $186 $311Sweepstakes Prize per Hour 0 0 0 0 0

Prize Money $167 $442 $882 $1,567 $2,618

35

21.6

7.05.9 5.5

4.9

2.7 2.51.9

0.7 0.6

0.0

5.0

10.0

15.0

20.0

25.0

Yahoo

!Gam

es

Real A

rcad

e

Shock

Wav

e

Min

iclip

Addict

ingG

ames

.com

Big F

ish

Fun T

echno

logies

iWin

Wild

Tan

gent

GSN

2006

Ave

rage

Mon

thly

Uni

ques

(m

m)

2.6%

(19.5%)4.8% 62.2%

65.6%

56.6% NA28.2%

623.4% (6.3%)

GSN Business Plan Review

Online Business• GSN’s online revenue is $801K in fiscal 2006 and is projected to grow 137% on average

through fiscal 2011 to approximately $60 million. Total monthly uniques is a significant driver of online revenue and it is projected to

increase 46% each year through fiscal 2011. The charts below compare GSN’s 2006 average monthly uniques with that of other

network websites and online gaming websites.Average Monthly Uniques – Cable Networks Average Monthly Uniques – Online Gaming Websites

Source: ComscoreNote: Percentages represent YOY January 2007 growth ratesSource: Public filings

10.0

7.0

4.0 4.0

2.0 2.0 2.0

0.7 0.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FoodN

etwor

kM

TVVH1

HGTV

Comed

y Cen

tral

BETDIY

Life

time

GSN

2006

Ave

rage

Mon

thly

Uni

ques

(m

m)

36

GSN Business Plan Review

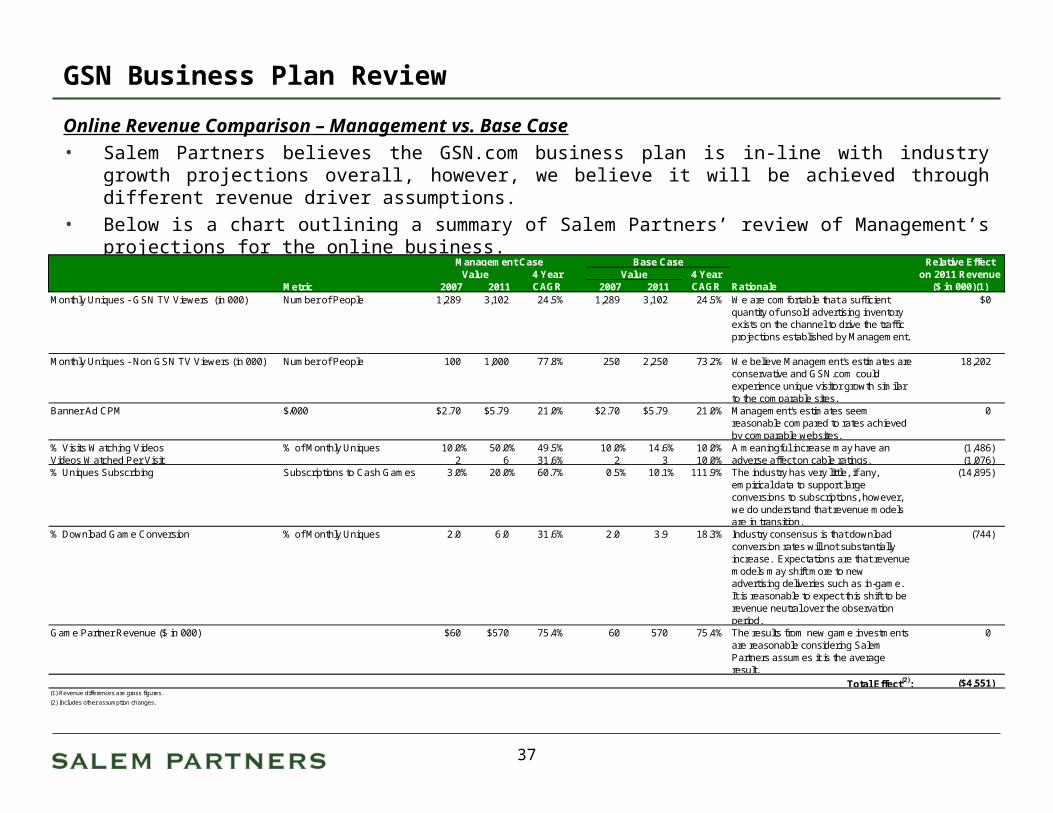

Online Revenue Comparison – Management vs. Base Case

• Salem Partners believes the GSN.com business plan is in-line with industry growth projections overall, however, we believe it will be achieved through different revenue driver assumptions.

• Below is a chart outlining a summary of Salem Partners’ review of Management’s projections for the online business.

Management Case Base Case Relative EffectValue 4 Year Value 4 Year on 2011 Revenue

Metric 2007 2011 CAGR 2007 2011 CAGR Rationale ($ in 000)(1)Monthly Uniques - GSN TV Viewers (in 000) Number of People 1,289 3,102 24.5% 1,289 3,102 24.5% We are comfortable that a sufficient

quantity of unsold advertising inventory exists on the channel to drive the traffic projections established by Management.

$0

Monthly Uniques - Non GSN TV Viewers (in 000) Number of People 100 1,000 77.8% 250 2,250 73.2% We believe Management's estimates are conservative and GSN.com could experience unique visitor growth similar to the comparable sites.

18,202

Banner Ad CPM $/000 $2.70 $5.79 21.0% $2.70 $5.79 21.0% Management's estimates seem reasonable compared to rates achieved by comparable websites.

0

% Visits Watching Videos % of Monthly Uniques 10.0% 50.0% 49.5% 10.0% 14.6% 10.0% (1,486)Videos Watched Per Visit 2 6 31.6% 2 3 10.0% (1,076)% Uniques Subscribing Subscriptions to Cash Games 3.0% 20.0% 60.7% 0.5% 10.1% 111.9% The industry has very little, if any,

empirical data to support large conversions to subscriptions, however, we do understand that revenue models are in transition.

(14,895)

% Download Game Conversion % of Monthly Uniques 2.0 6.0 31.6% 2.0 3.9 18.3% Industry consensus is that download conversion rates will not substantially increase. Expectations are that revenue models may shift more to new advertising deliveries such as in-game. It is reasonable to expect this shift to be revenue neutral over the observation period.

(744)

Game Partner Revenue ($ in 000) $60 $570 75.4% 60 570 75.4% The results from new game investments are reasonable considering Salem Partners assumes it is the average result.

0

Total Effect(2): ($4,551)(1) Revenue differences are gross figures.

(2) Includes other assumption changes.

A meaningful increase may have an adverse affect on cable ratings.

37

GSN Business Plan Review

Online Comparison – Management versus Base Case• Below is a chart comparing the revenue of GSN.com in the Management Case to revenue of

GSN.com in the Base Case.

($ in 000)Online Revenue For the Years Ending December 31, 4 Year

2007A 2008A 2009A 2010A 2011A CAGR

Management CaseTotal Online Gaming Revenue $3,517 $8,210 $17,507 $31,667 $52,427 96.5%Total Online Content Revenue 519 1,428 2,675 4,749 7,804 96.9%

Total Gross Online Revenue $4,036 $9,638 $20,182 $36,416 $60,231 96.5%

Revenue Shares (1,739) (3,721) (8,163) (14,953) (24,940) 94.6Total Net Online Revenue $2,297 $5,916 $12,019 $21,464 $35,291 98.0%

Base CaseTotal Online Gaming Revenue $2,560 $7,627 $15,540 $27,753 $47,855 107.9%Total Online Content Revenue 572 1,536 2,863 4,881 7,825 92.3%

Total Gross Online Revenue $3,132 $9,163 $18,403 $32,634 $55,680 105.3%

Revenue Shares (1,261) (3,397) (7,085) (12,796) (22,221) 104.9Total Net Online Revenue $1,871 $5,766 $11,318 $19,838 $33,459 105.6%

DifferenceTotal Online Gaming Revenue ($957) ($583) ($1,967) ($3,914) ($4,572)Total Online Content Revenue 53 109 188 132 21

Total Gross Online Revenue ($904) ($474) ($1,779) ($3,782) ($4,551)

Revenue Shares 479 324 1,078 2,157 2,719Total Net Online Revenue ($425) ($150) ($701) ($1,625) ($1,832)

38

Discussion of Liberty CaseDiscussion of Liberty Case

Discussion of Liberty Case

Overview Salem Partners believes potential incremental value to Liberty of owning 100% of GSN lies in

six general areas.

Comments

Advertising Revenue Enhancement Due to Ratings Increase

Analysis of precedent cable networks transactions indicates a significant near-term increase in ratings, which Salem Partners attributes primarily to cross promotion.

We believe modest ratings growth under Liberty ownership will be possible over the projection term due to the ability of Liberty to cause increased stability in channel positioning.

Affiliate Revenue Enhancement

No change.

Cost Savings Opportunities

We believe the cost savings opportunities under Liberty ownership are not as great as originally anticipated by SPE and will only be realized upon a full consolidation of GSN into Liberty operations. Primary savings opportunities are in network operations and G&A. Ad sales, marketing and affiliates sales were also considered.

International Network Opportunities

Discussions with international cable network executives have indicated that Liberty has significant power to launch channels internationally. Given the strong appeal of game show programming internationally, this concept would seem to be a natural part of the strategy.

Opportunity with FUN Technologies

Liberty can use Fun as a skill game tracking stock and may drive a valuation increase through a contractual arrangement with Fun or an outright contribution of GSN.com’s business.

Value Enhancement Opportunity with Other Liberty Entities Considered But Not Included

DirecTV (other than ability to leverage distribution for better GSN channel placement). OpenTV Starz/Encore (shared programming considered but not included). QVC (joint programming considered but not included).

39

Discussion of Liberty Case

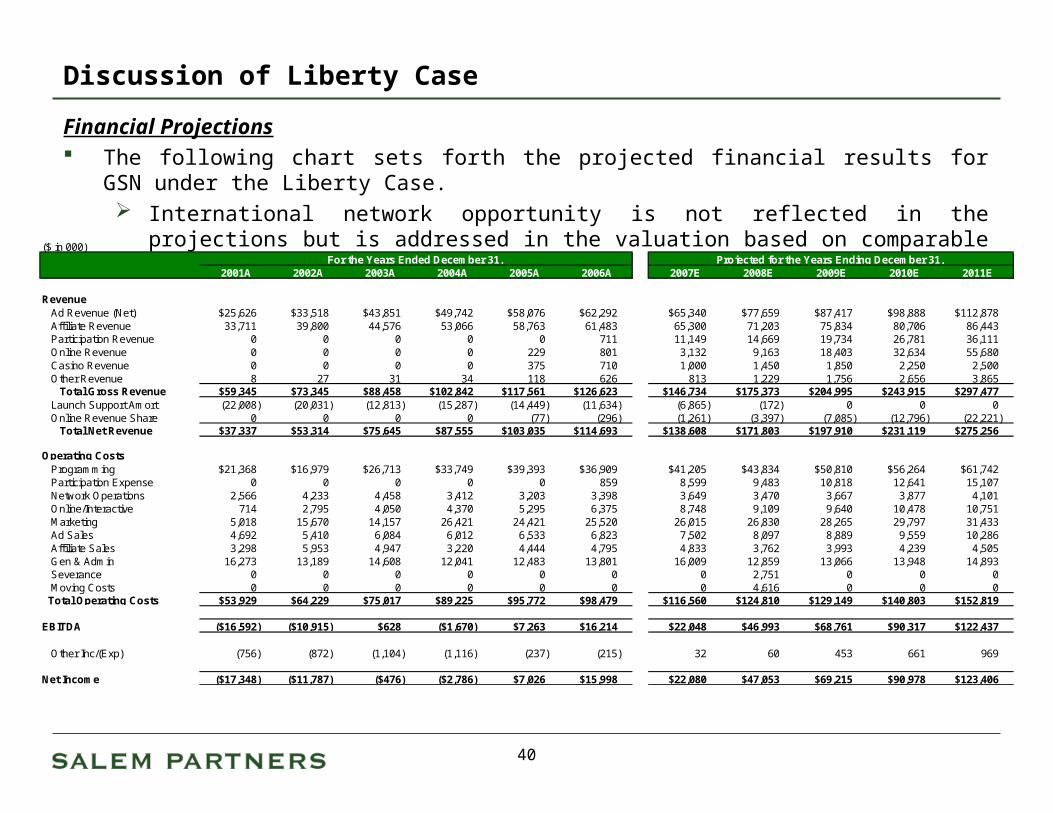

Financial Projections The following chart sets forth the projected financial results for GSN under the Liberty Case.

International network opportunity is not reflected in the projections but is addressed in the valuation based on comparable transactions.

($ in 000)For the Years Ended December 31, Projected for the Years Ending December 31,

2001A 2002A 2003A 2004A 2005A 2006A 2007E 2008E 2009E 2010E 2011E

RevenueAd Revenue (Net) $25,626 $33,518 $43,851 $49,742 $58,076 $62,292 $65,340 $77,659 $87,417 $98,888 $112,878Affiliate Revenue 33,711 39,800 44,576 53,066 58,763 61,483 65,300 71,203 75,834 80,706 86,443Participation Revenue 0 0 0 0 0 711 11,149 14,669 19,734 26,781 36,111Online Revenue 0 0 0 0 229 801 3,132 9,163 18,403 32,634 55,680Casino Revenue 0 0 0 0 375 710 1,000 1,450 1,850 2,250 2,500Other Revenue 8 27 31 34 118 626 813 1,229 1,756 2,656 3,865

Total Gross Revenue $59,345 $73,345 $88,458 $102,842 $117,561 $126,623 $146,734 $175,373 $204,995 $243,915 $297,477Launch Support Amort (22,008) (20,031) (12,813) (15,287) (14,449) (11,634) (6,865) (172) 0 0 0Online Revenue Share 0 0 0 0 (77) (296) (1,261) (3,397) (7,085) (12,796) (22,221)

Total Net Revenue $37,337 $53,314 $75,645 $87,555 $103,035 $114,693 $138,608 $171,803 $197,910 $231,119 $275,256

Operating CostsProgramming $21,368 $16,979 $26,713 $33,749 $39,393 $36,909 $41,205 $43,834 $50,810 $56,264 $61,742Participation Expense 0 0 0 0 0 859 8,599 9,483 10,818 12,641 15,107Network Operations 2,566 4,233 4,458 3,412 3,203 3,398 3,649 3,470 3,667 3,877 4,101Online/Interactive 714 2,795 4,050 4,370 5,295 6,375 8,748 9,109 9,640 10,478 10,751Marketing 5,018 15,670 14,157 26,421 24,421 25,520 26,015 26,830 28,265 29,797 31,433Ad Sales 4,692 5,410 6,084 6,012 6,533 6,823 7,502 8,097 8,889 9,559 10,286Affiliate Sales 3,298 5,953 4,947 3,220 4,444 4,795 4,833 3,762 3,993 4,239 4,505Gen & Admin 16,273 13,189 14,608 12,041 12,483 13,801 16,009 12,859 13,066 13,948 14,893Severance 0 0 0 0 0 0 0 2,751 0 0 0Moving Costs 0 0 0 0 0 0 0 4,616 0 0 0

Total Operating Costs $53,929 $64,229 $75,017 $89,225 $95,772 $98,479 $116,560 $124,810 $129,149 $140,803 $152,819

EBITDA ($16,592) ($10,915) $628 ($1,670) $7,263 $16,214 $22,048 $46,993 $68,761 $90,317 $122,437

Other Inc/(Exp) (756) (872) (1,104) (1,116) (237) (215) 32 60 453 661 969

Net Income ($17,348) ($11,787) ($476) ($2,786) $7,026 $15,998 $22,080 $47,053 $69,215 $90,978 $123,406

40

Discussion of Liberty Case

Financial Projections – Liberty Case versus Base Case The following chart highlights the changes from the Base Case to arrive to the Liberty Case.

($ in 000)For the Years Ended December 31, Projected for the Years Ending December 31,

2001A 2002A 2003A 2004A 2005A 2006A 2007E 2008E 2009E 2010E 2011E

RevenueAd Revenue (Net) $0 $0 $0 $0 $0 $0 $0 $6,545 $9,799 $14,035 $19,629Affiliate Revenue 0 0 0 0 0 0 0 0 0 0 0Participation Revenue 0 0 0 0 0 0 0 0 0 0 0Online Revenue 0 0 0 0 0 0 0 0 0 0 0Casino Revenue 0 0 0 0 0 0 0 0 0 0 0Other Revenue 0 0 0 0 0 0 0 0 0 0 0

Total Gross Revenue $0 $0 $0 $0 $0 $0 $0 $6,545 $9,799 $14,035 $19,629Launch Support Amort 0 0 0 0 0 0 0 0 0 0 0Online Revenue Share 0 0 0 0 0 0 0 0 0 0 0

Total Net Revenue $0 $0 $0 $0 $0 $0 $0 $6,545 $9,799 $14,035 $19,629

Operating CostsProgramming $0 $0 $0 $0 $0 $0 $0 $59 $88 $126 $177Participation Expense 0 0 0 0 0 0 0 0 0 0 0Network Operations 0 0 0 0 0 0 0 (386) (407) (431) (456)Online/Interactive 0 0 0 0 0 0 0 0 0 0 0Marketing 0 0 0 0 0 0 0 (547) (563) (580) (597)Ad Sales 0 0 0 0 0 0 0 0 (42) (85) (131)Affiliate Sales 0 0 0 0 0 0 0 (941) (998) (1,060) (1,126)Gen & Admin 0 0 0 0 0 0 0 (4,322) (5,649) (6,000) (6,376)Severance 0 0 0 0 0 0 0 2,751 0 0 0Moving Costs 0 0 0 0 0 0 0 4,616 0 0 0

Total Operating Costs $0 $0 $0 $0 $0 $0 $0 $1,232 ($7,571) ($8,030) ($8,510)

EBITDA $0 $0 $0 $0 $0 $0 $0 $5,314 $17,370 $22,065 $28,139

Other Inc/(Exp) 0 0 0 0 0 0 0 0 0 0 0

Net Income $0 $0 $0 $0 $0 $0 $0 $5,314 $17,370 $22,065 $28,139

41

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

T-9 T-8 T-7 T-6 T-5 T-4 T-3 T-2 T-1 0 T+1 T+2 T+3 T+4 T+5 T+6 T+7 T+8 T+9 T+10 T+11 T+12 T+13 T+14 T+15 T+16 T+17 T+18 T+19 T+20

Bravo Comedy Central Court TV

Acquisition Date

0.75

0.46

0.30

Notes: Queer Eye for the Straight Guy premiered on Bravo in July 2003 (T+8).

Notes: Beach Patrol: Miami Beach premiered on Court TV in July 06 (T+2).

Notes: 'Til Death Do Us Part premiered on Court TV in April 06 (T-1).

Notes: Las Vegas Law premiered on Court TV in February 06 (T-3).

Notes: The Chapelle Show premiered on Comedy Central in November 03 (T+7).

Notes: Each data point represents one month.

Discussion of Liberty Case

Ratings Increase due to Liberty Acquisition The chart below illustrates the ratings increase that occurred when Bravo, Comedy Central and Court TV

were acquired by NBC, MTV Networks and Time Warner, respectively. These transactions represent recent consolidations of formerly independent channels into major

media companies. We believe that cross promotion was a primary driver of the ratings increases.

Ratings Increase Due to Acquisition

24

-Ho

ur

Nie

lse

n R

ati

ng

s

42

Discussion of Liberty Case

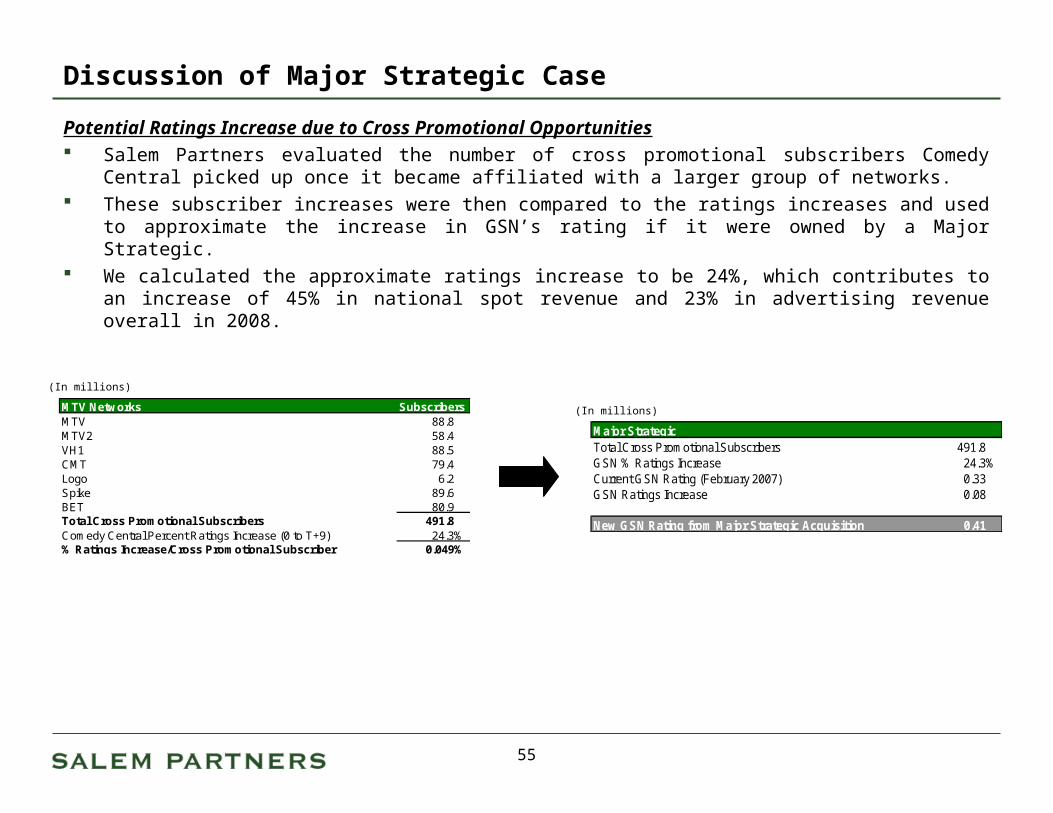

Potential Ratings Increase due to Cross Promotional Opportunities Salem Partners evaluated the number of cross promotional subscribers Bravo, Comedy Central and Court

TV picked up once it became affiliated with a larger group of networks. These subscriber increases were then compared to the ratings increases and used to approximate the

increase in GSN’s rating if it were owned by Liberty. We calculated the approximate ratings increase to be 16%, which contributes to an increase of 35% in

national spot revenue and 19% in advertising revenue overall in 2008. This analysis would demonstrate a much larger potential impact if it included the Rainbow channels.(In millions)

(In millions)

Liberty Media Networks SubscribersQVC 88.0Total Cross Promotional Subscribers 88.0GSN % Ratings Increase 15.7%Current GSN Rating (February 2007) 0.33GSN Ratings Increase 0.05

New GSN Rating from Liberty Acquisition 0.38

MTV Networks SubscribersMTV 88.8MTV2 58.4VH1 88.5CMT 79.4Logo 6.2Spike 89.6BET 80.9Total Cross Promotional Subscribers 491.8Comedy Central Percent Ratings Increase (0 to T+9) 24.3%% Ratings Increase/Cross Promotional Subscriber 0.049%

NBC Networks SubscribersMSNBC 85.1NBC 110.3USA 89.7Total Cross Promotional Subscribers 285.1Bravo Percent Ratings Increase (0 to T+9) 76.5%% Ratings Increase/Cross Promotional Subscriber 0.268%

Time Warner SubscribersTBS 89.5TNT 89.8Turner Classic Movies 71.5CNN 89.9Total Cross Promotional Subscribers 340.7Court TV Ratings Increase (0 to T+9) 74.4%% Ratings Increase/Cross Promotional Subscriber 0.218%

Average % Ratings Increase/Cross Promotional Subscriber 0.179%

43

Discussion of Liberty Case

Potential Ratings Increase Due to Enhanced Channel Stability We believe that Liberty will be able to utilize its influence as a major distributor of cable programming to cause

greater stability in GSN’s channel positioning, leading to a higher possibility of organic ratings growth going forward. Liberty will have direct influence over DirecTV. Liberty should be able to utilize the threat of retaliation to keep cable MSOs from altering GSN’s channel

positioning. An analysis of GSN’s ratings history in two different markets highlights the difficulties in maintaining or growing

ratings when channel positioning is changed by an MSO or satellite provider. The chart below highlights GSN’s historical ratings in two markets where Comcast is the cable provider.

Comcast Sacramento carries GSN on expanded basic and has been on the same channel for many years. Comcast Baltimore use to carry GSN on expanded basic, but was migrated to digital by Comcast in

September 2006. GSN’s rating went from a 0.23 to a 0.08 when it was migrated.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Jan-

04

Mar

-04

May

-04

Jul-0

4

Sep-0

4

Nov-0

4

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep-0

5

Nov-0

5

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-0

6

Nov-0

6

Rat

ing

Sacramento Baltimore

0.65

0.08

Local Market GSN Ratings

Notes: Ratings data is based against total cable subs in the DMA, not against GSN’s universe. No single MSO owns all the cable subs in a DMA. While some may dominate a DMA, other smaller MSO/systems exist and impact ratings, therefore, some ratings impact may be muted by other systems.

GSN is migrated from expanded basic to digital.

44

Discussion of Liberty Case

Cost Savings Opportunities Salem Partners has performed an analysis of the potential cost savings due to consolidation

of GSN into Liberty’s operations.

We believe that cost savings opportunities exist but will be realized only if Liberty fully consolidates. Rather than speculate about whether Liberty would make such a decision and the timing

of when such a move might occur, we have quantified the opportunity but have valued the Liberty Case with and without such cost savings.

One-time costs to move are estimated at $7.4 million, including 50% of total annual payroll (six months) of assumed severance, one year of rent from lease breakage and $1 million of moving costs.

45

Discussion of Liberty Case

Cost Savings Opportunities (Continued) The following chart highlights a summary of our cost savings analysis

($ in 000)

Projected 2008 Expense

Assumed Percentage Reduction

Pro Forma 2008 Expense Comment

Production and Programming Costs(1) $62,367 0.1% $62,425 Although Liberty subsidiaries, Overture Films and Starz Encore have programming operations in Los Angeles, GSN's programming operator will have to operate on a standalone basis due to its unique nature. Small increase in music royalties projected due to higher ad revenue.

Network Operations 3,855 (10.0%) 3,470 Some savings due to headcount eliminations.Marketing 27,377 (2.0%) 26,830 We have assumed a 5% reduction in the cost of

purchased media ($10.6 million in 2007) to reflect greater buying power of Liberty. Impact is small due to the uncertain timing of GSN media buys, leading to a relative inability to coordinate purchases with other Liberty operators.

Advertising Sales 8,097 0.0% 8,097 Liberty's consolidated operations do not appear to include a strong advertising sales capability.

Affiliate Sales 4,703 (20.0%) 3,762 With QVC incorporating a different MSO compensation model and Starz/Encore being a consumer subscription sale as opposed to a MSO-driven sale, savings in this area may not be as much as would initially appear. GSN's affiliate relations process will be unique among Liberty's current bouquet of channels.

G&A 17,181 (25.0%) 12,882 In a full consolidation, significant savings opportunities would exist in the areas of finance, human resources and facilities.

(1) Represents programming, programming amortization, acquisitions and scheduling, new media & short form, participation expense and online/interactive.

46

Discussion of Liberty Case

International Network Opportunity In our survey of international cable network executives, we received the following comments

regarding the potential for Liberty to launch international channels.

“[Liberty] has the ability, at least in some territories, to launch channels. Whether they have the desire is something else.”

“It is possible to launch new international channels, but much more difficult than it used to be. You need either a brand or other channel or distribution leverage. Liberty has that.”

– International cable network executive response to the question, “Does Liberty have the clout internationally to launch new networks?”

– International cable network executive response to the question, “How difficult is it to launch new international networks? Can Liberty do it?”

47

Discussion of Liberty Case

Impact on FUN Technologies The potential incremental value of GSN.com to Liberty is suggested in the chart below. Salem Partners has assumed that Liberty can reduce website costs and G&A by 80% if Liberty and Fun

entered into a contractual relationship whereby Fun manages the entirety of GSN.com.($ in 000)

OpEx Reduction For the Years Ending December 31, Discounted Cash Flow Sensitivity Analysis - Cost Savings to Fun Technologies2007E 2008E 2009E 2010E 2011E

Website Cost 6/30/2007 6/30/2008 6/30/2009 6/30/2010 6/30/2011Website Buildout 0 $160 $160 $400 $160Additional Hosting Costs 0 210 221 232 243

Total Website Cost Savings $0 $370 $381 $632 $403

G&ASalaries $0 $1,126 $1,182 $1,241 $1,303Bonuses 0 113 118 124 130Benefits 0 136 143 150 158Legal Fees 0 168 176 185 194Consultants 0 42 44 46 49Recruitment fees 0 0 0 0 0Research (Comscore) 0 63 66 69 73Traffic Software 0 168 176 185 194Other 0 84 88 93 97Rent 0 161 169 178 187

Total G&A $0 $2,061 $2,164 $2,272 $2,385Cash Taxes(1)

0 (783) (822) (863) (906)

Total Cost Savings $0 $1,278 $1,341 $1,409 $1,479Discount Rate 38.5%PV of 80% of Certain OpEx Reduction at 6/30/2007(2)

2,552PV of 80% of Certain OpEx Reduction at 12/31/2007 $2,168Terminal Value 4,269 12.5x MulipleTotal Value of Cost Savings $6,437(1) Assumes a 38% tax rate.

(2) Assumes mid-year convention.

Discounted Cash Flow Sensitivity Analysis - Cost Savings to Fun Technologies

Total DCF ValuationPresent Value of Terminal Total Present Value Assuming Implied Perpetuity Cash Flow

Projection Period Assuming Terminal Multiple Terminal Multiple Growth RatesCash Flow 10.5x 12.5x 14.5x 10.5x 12.5x 14.5x 10.5x 12.5x 14.5x

35.0% $2,322 $4,024 $4,790 $5,557 $6,346 $7,112 $7,879 25.5% 27.0% 28.1%38.5 2,168 3,586 4,269 4,952 5,754 6,437 7,120 29.0 30.5 31.642.0 2,029 3,205 3,816 4,426 5,235 5,845 6,456 32.5 34.0 35.1

48

Discussion of Liberty Case

Liberty annotated stock price analysis Salem Partners analyzed the catalysts for significant stock price movement of Liberty’s common stock in

order to determine whether there is precedent for an expected increase in Liberty’s stock upon an acquisition of GSN. While no precedent is obvious, we still believe an announcement would indicate further proof of