managing commercial lines pricing levels in a loss cost environment lisa hays ohio casualty group

TRANSCRIPT

Managing Commercial Lines Pricing Levels in a Loss Cost Environment

Lisa HaysOhio Casualty Group

Today’s Challenge

Accurate measurement of pricing changes over time for a book of business Impact on planned vs. actual results

Production PlanLoss Ratio Plan

Impact on Rate-level indications (onlevel factors)

Why is this so difficult?

Blame the Underwriters

The implemented rate change may not be equal to the filed or intended rate change.

Underwriters have many tools at their disposal Access to multiple companies Schedule rating

Must track change in total price level - base rate changes and other rating factors.

How are pricing changes tracked today?

Cash-to-cash renewal reports Policies that renew are matched up to their

expiring terms and premiums are compared PRO - simple to calculate PRO - necessary data should be readily

available PRO - over entire book of business it should

provide an adequate measure of the rate plus exposure change for a book

How are pricing changes tracked today?

Cash-to-cash renewal reports (cont.) PRO - easy for the underwriters to

understand and to implement CON - on individual policies or small

segments, significant exposure changes will distort the results

CON - Only renewal business that is retained is evaluated. Omits new business and lost renewals.

How are pricing changes tracked today?

Exposure-adjusted renewal reports Similar to cash-to-cash reports except

that expiring rates are multiplied by renewing exposures before being compared to renewing premium

New Business - somewhat hit-and-miss Monitor change in company usage,

discretionary credits, etc.

Percent of Loss Cost (PoLC)

Definition - the PoLC is the ratio of the collected premium to the underlying bureau loss cost dollars. Loss Cost Dollars = Loss Costs * Exposures

Which rating factors are included in the calculation of the underlying loss costs?

Potential Factors to include in Loss Costs

Increased Limits Factor Deductible Factor? Experience Mod? Package ModX Loss Cost Multiplier (LCM)X Schedule Rating FactorX Company-specific deviations

Potential Factors to include in Loss Costs

ILFs and deductible factors should always be considered part of the loss costs - they objectively quantify expected losses.

Obviously judgmental factors such as schedule rating should not be included in the underlying loss costs.

Potential Factors to include in Loss Costs

Package mods If you use rating bureau factors “as is”

they should be included in loss costs. If you filed a significant deviation from

the rating bureau, the revised mods (or the difference between filed and suggested) should be tracked as a deviation to loss costs and monitored.

Potential Factors to include in Loss Costs

Experience mod - Although experience rating plans are considered to be objective, in practice there are situations where the use of schedule credit or company placement may double-count a risk characteristic underlying the mod.

I prefer to track it as part of the PoLC statistic, but retain ability to exclude it for ad hoc analysis.

Potential Factors to include in Loss Costs

General Rule of Thumb: If the rating factor is specifically tied to the level of coverage that you are providing (such as ILFs) it should be included in the loss cost.

If the rating factor results from the pricing actuary’s or the field underwriter’s judgement, it should be captured in PoLC.

Percent of Loss Cost (PoLC)

The general formula for the PoLC when all rating factors are multiplicative is:

PoLC = Collected Written Premium ΣLoss Costs * Exposures

= Σ Loss Costs * Exposures * LCM * OTHR * PKG * SRP * EXPERΣ Loss Costs * Exposures

The LCM includes the company deviation.

Indexed PoLC

Ideally, to facilitate comparisons through time, the PoLC is calculated by comparing the collected written premium for a given year to loss cost dollars calculated from a base year.

The calculation is simple assuming: Loss Costs from the Base Year are accessible You are able to re-rate current exposures

with the Base Year loss costs.

Indexed PoLC

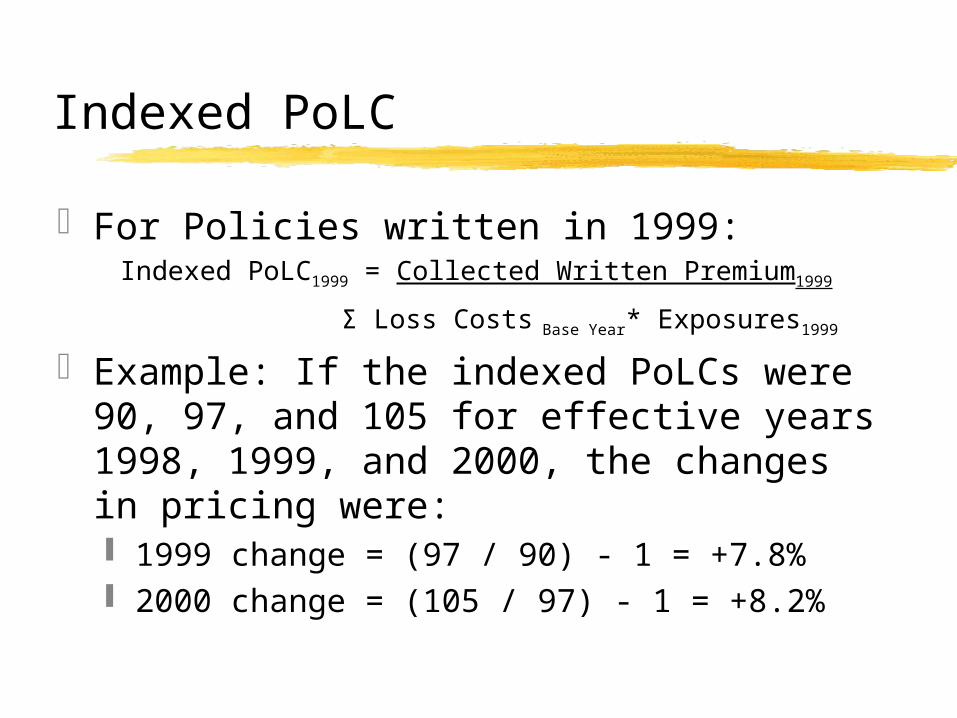

For Policies written in 1999:Indexed PoLC1999 = Collected Written Premium1999

Σ Loss Costs Base Year* Exposures1999

Example: If the indexed PoLCs were 90, 97, and 105 for effective years 1998, 1999, and 2000, the changes in pricing were: 1999 change = (97 / 90) - 1 = +7.8% 2000 change = (105 / 97) - 1 = +8.2%

Indexed PoLC

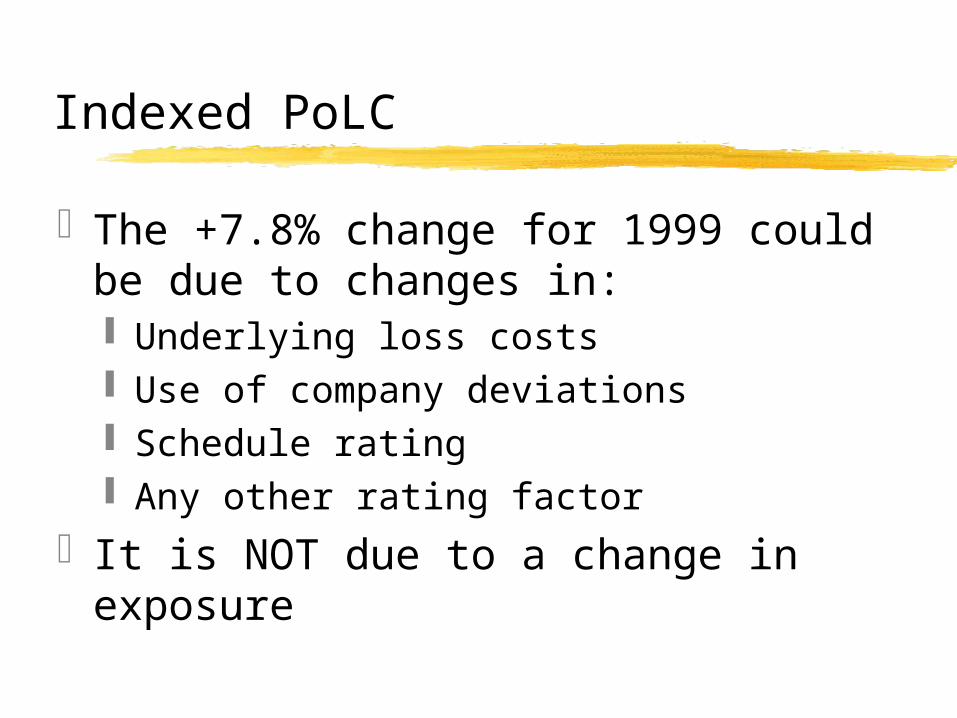

The +7.8% change for 1999 could be due to changes in: Underlying loss costs Use of company deviations Schedule rating Any other rating factor

It is NOT due to a change in exposure

Calculation of Components

Please refer to this section of the paper for a detailed example for Commercial Auto of how to calculate the contribution from each factor to the overall PoLC.

The example also demonstrates how to handle rating variables that are additive.

Workers’ CompensationCase Study (Exhibits 2 and 3)

Using PoLC to manage pricing levels Correlate the PoLC levels with loss

experience Compute loss ratio and frequency

relativities across PoLC ranges Use these relativities to distribute the

overall rate indication Perform further analysis on ranges that

deviate significantly from average.

Workers’ CompensationCase Study (Exhibits 2 and 3)

This case study assumes that the underlying loss cost inadequacy or redundancy is the same across states and industry segments.

If you disagree with this assumption you should make appropriate adjustments or perform the analysis at a lower level of detail.

Setting Goals and Monitoring Results

Exhibit 4 shows sample monitoring reports that can be produced to track PoLC.

New vs. Renewal business should be monitored separately.

In this example, no pricing improvement for new business in 2000 compared to total in 1999. Renewals increased by 6.7% relative to loss costs.

Setting Goals and Monitoring Results

Assuming the sample report in Exhibit 4 is not using indexed loss costs, what should the 2001 PoLC goal be to achieve a rate increase of 20% if we file a loss cost change of +5% effective on 1/1/2001?

88.2% * (1.20 / 1.05) = 100.8%

Setting Goals and Monitoring Results

The goal of 100.8% could apply to both new and renewal business.

If you target significant price changes on your renewal book for selected PoLC ranges, policy retention across ranges may not be uniform.

In this case, a renewal price increase report may be a better monitoring tool.

Setting Goals and Monitoring Results

Exhibit 5 – based on the Experience Mod and the policy’s PoLC, develop a Target Renewal Price Change for each policy.

Include an additional amount for the overall expected exposure change if you use a cash-to-cash renewal increase report.

For all policies that renew, compare the actual renewal price change to the target.

Setting Goals and Monitoring Results

Again, this report will be useful at a countrywide or state level, but can be distorted at the underwriter or agency level if exposure changes are significantly different than the projected average.

Every attempt should be made to produce exposure-adjusted renewal reports for detailed reporting.

Caveats

The case studies and examples in the paper assume that the underlying loss costs are inadequate or redundant by the same percentage amount across states industry groups effective years

If this is not so, you need to adjust for mix shift over time.

Summary

PoLC is a useful tool Un-indexed it measures the change in

usage of company tiers, schedule credit/debit, etc. over time.

Indexed also incorporates impact of underlying loss cost changes.

Can be correlated with loss experience to develop targeted pricing strategies.