management and regulation of hospital costs

TRANSCRIPT

Management and Regulation of Hospital

Costs

Why do hospital cost more than others?

How do managers control costs?

- Managers control hospital costs through the budget process.

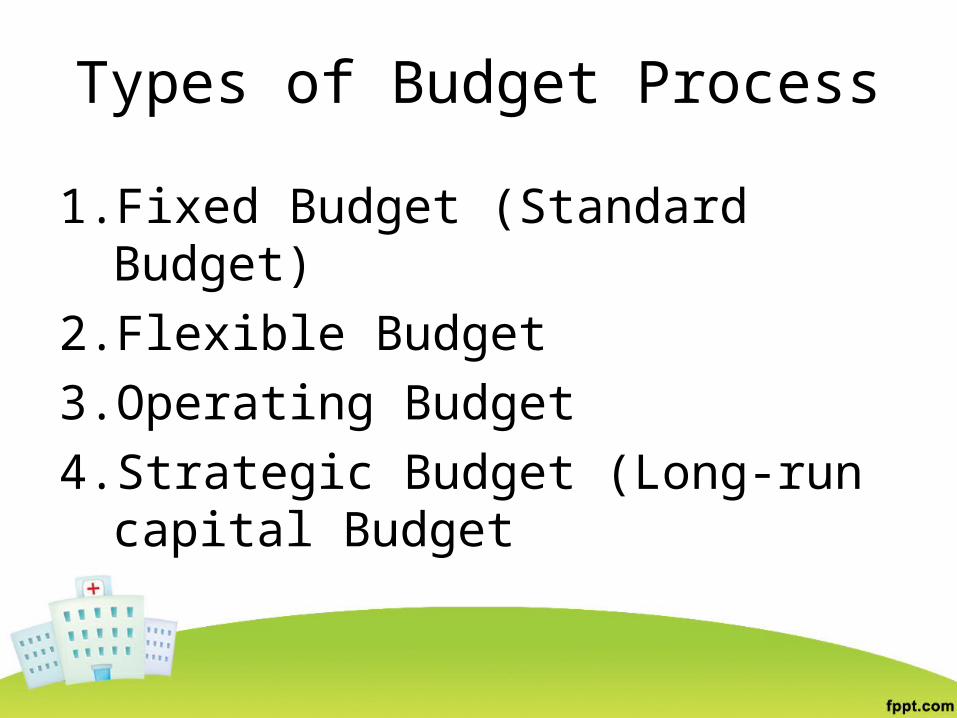

Types of Budget Process

1. Fixed Budget (Standard Budget)2. Flexible Budget3. Operating Budget4. Strategic Budget (Long-run capital

Budget

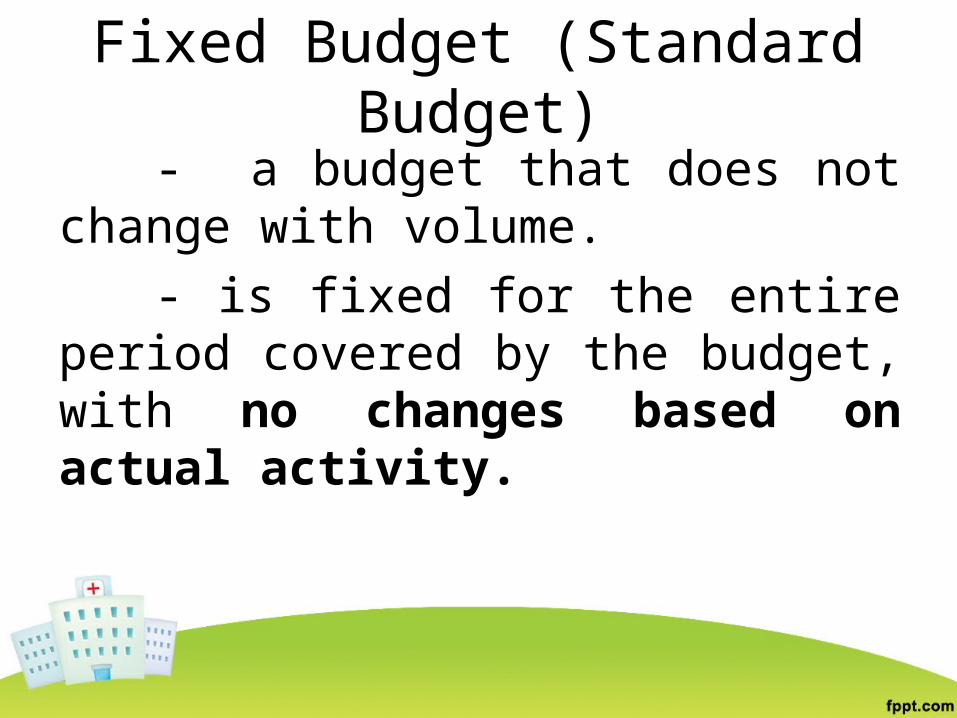

Fixed Budget (Standard Budget)- a budget that does not change

with volume.- is fixed for the entire period

covered by the budget, with no changes based on actual activity.

Flexible Budget

- A budget that change in volume.-is financial plan of estimated

revenues and expenses based on the current actual amount of output.

Operating Budget

- A hospital or medical group practice creates an operating budget that projects all anticipated expenses for the next year.

Strategic Budget (Long-run capital Budget)

- A budget that focuses on trends in the number of patients and capital renovations and expansions.

How Organizations Deal with Change.

1. Intermediate-run changes – changes occur during the next two to five years

2. Known short-run variations – dealt with by making limited changes in the number of staff scheduled.

3. Known long-run change – such as declining trend in admissions due to the closure of a local manufacturing plant, calls for a permanent reduction in capacity.

4. Random short-run fluctuations – are dealt with primarily by building in some excess reserve capacity, making the staff work faster or slower, and allocating less immediate tasks to the slower days.5. Unforeseen long-run changes – provide the test of the organization’s ability to control costs.

Cost per day in the hospital varies for many reasons:

1. Differences in quality and type of services offered2. Cost shifting to pay for research and teaching3. Severity of patient illness4. Prices of labor and other inputs5. Differences in production efficiency.

Some of common mistakes made in accounting for the true costs of

medical care.

1. Provider costs misallocated (displaced in time, overhead, or wrong department)

2. Patient costs not counted (wait time, transportation, family care)

3. Emotional costs not counted (pride, fear, pain, lack of respect)

Hospitals are Multiproduct Firms

- Hospitals are complex institutions, providing many types of care; thus, comparisons of cost per day or per case may not be very meaningful indicators of how efficiently a hospital is producing care.

Technology- Has tended to increase total spending

in health care because generous insurance payments and costs reimbursement have given little incentive to develop cost – reducing techniques or to give up a little quality for large reduction in cost.

- An increase in capability to improve health often makes more spending worthwhile.

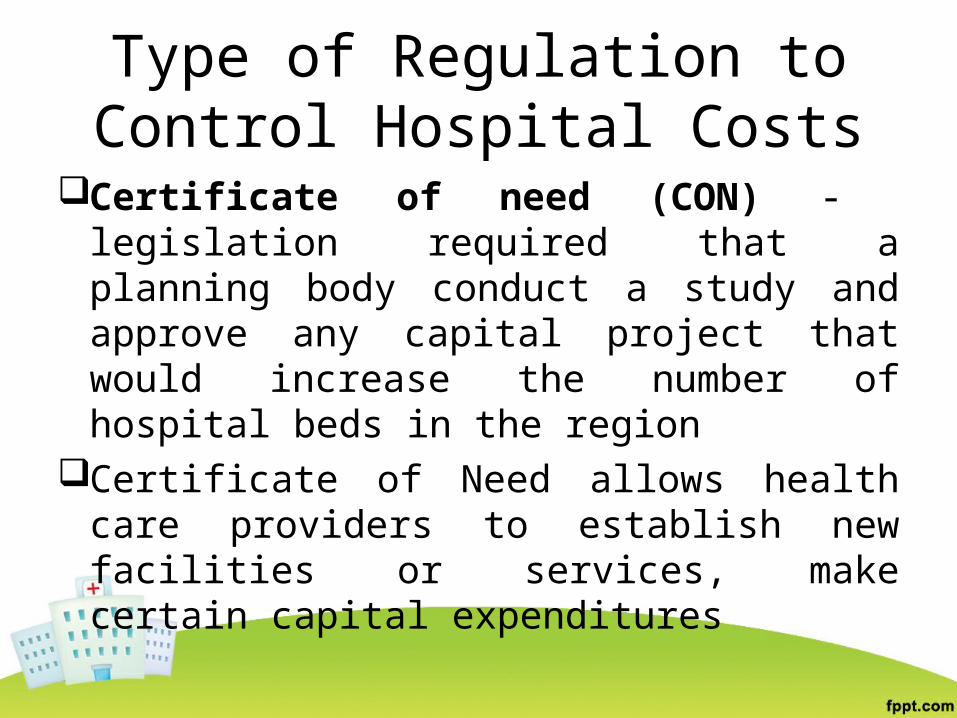

Type of Regulation to Control Hospital Costs

Certificate of need (CON) - legislation required that a planning body conduct a study and approve any capital project that would increase the number of hospital beds in the region

Certificate of Need allows health care providers to establish new facilities or services, make certain capital expenditures

Utilization review (UR) – a process to eliminate unnecessary surgery and other services by having a panel of doctors and nurses in a professional standards review organization (PSRO) review patients chart to find cases of inappropriate care.

Utilization review(UR) is a safeguard against unnecessary and inappropriate medical care.

Professional standards review organization (PSRO) - an organization established to monitor health care services paid for through Medicare, Medicaid, and Maternal and Child Health programs to assure that services provided are medically necessary, meet professional standards, and are provided in the most economic medically appropriate health care agency or institution.

Budgetary review – was much more labor – intensive process involving the line-by-line examination of spending plans.

Administered prices (DRGs, PPS, BBA)DRGs (Diagnostically related groups)– used for

setting federally administered prices per discharge covering the entire patient stay.

PPS (Prospective payment system)- is a method of reimbursement in which Medicare payment is made based on a predetermined, fixed amount.

BBA (Balanced Budget Act of 1997)- it directly reduced Medicare payments to physicians, hospitals and hoe – health agencies by reducing the hospital update factor .

Thank you for listening