malaysia - listed companykpj.listedcompany.com/misc/analyst/kpj_maybank_20111130.pdf · malaysia 17...

TRANSCRIPT

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Malaysia

17 October 2011

PP16832/01/2012 (029059)

Initiating Coverage 30 November 2011

PP16832/01/2012 (029059)

KPJ Healthcare Niche specialist with regional dreams

Initiate coverage with BUY and target price of RM5.10. KPJ is well-

positioned to benefit from the fast-growing healthcare sector in

Malaysia. This sector has been identified as one of the 12 key pillars in

the country‟s Economic Transformation Programme and is expected to

contribute USD10.4b to the Gross National Income by 2020. As a

defensive play, KPJ also offers limited revenue downside given its

domestic dominance and a wide array of positive demand factors.

Entrenched market leader. KPJ operates 20 private hospitals in

Malaysia, the largest network among local private hospital operators,

and has a 19% share of total private hospital beds. As the leader of the

domestic market, it stands to reap the greatest benefits from the rising

healthcare needs of the local population.

Limited revenue downside. The ever-growing demand for private

healthcare services in Malaysia limits the downside risk to revenue for

KPJ. This relatively inelastic demand is underpinned by structural

factors such as the increased number of elderly people, growing

population, higher per capita income and strain on public-sector

healthcare system.

New hospitals, new foreign patients. KPJ plans to add 1-2 hospitals

each year in its efforts to expand its hospital network. By end-2013,

KPJ could have added up to five new hospitals, and expanded its bed

capacity by up to 35%. We also expect the company to compete more

aggressively for foreign patients in the medical tourism sector. Its

education business could also serve as another thrust for growth.

Cheapest valuation, highest dividend yield. KPJ is the cheapest

hospital stock vis-à-vis its regional peers, trading at FY12F PER of

18.1x vs the peer average of 22.3x. Nevertheless, it offers the highest

yield at 2.4% net. We expect revenue growth of 13-18% over FY11-13

as its hospital network expands and it becomes a bigger player in

medical tourism. Corresponding net profit would grow by 8-19% over

the same period. Initiate coverage with BUY and TP of RM5.10, based

on 22x PER on FY12F fully diluted EPS, pegged to peer average.

KPJ Healthcare Bhd– Summary Earnings Table Source: Company, Kim Eng

FYE Dec (RM m) FY2009 FY2010 FY2011F FY2012F FY2013F Revenue 1,456.4 1,654.6 1,867.0 2,118.7 2,495.9 EBITDA 186.9 203.0 241.8 302.6 366.0 Recurring Net Profit 110.9 118.9 128.7 153.2 180.2 Recurring Basic EPS (Sen) 21.7 22.6 21.9 26.1 30.7 Recurring Diluted EPS (Sen) 21.7 20.3 19.5 23.2 27.3 EPS growth (%) 29.5% 4.3% -2.8% 19.0% 17.7% Net DPS (Sen) 7.5 11.3 10.0 11.3 13.2 PER (x) - diluted 19.3 20.6 21.4 18.0 15.3 EV/EBITDA (x) 14.0 12.9 10.8 8.6 7.1 Net Div Yield (%) 1.8% 2.7% 2.4% 2.7% 3.2% P/BV (x) 3.4 3.0 2.9 2.5 2.2 Net Gearing (%) 35.6% 26.3% 16.9% 19.7% 16.5% ROE (%) 18.3% 17.0% 15.8% 16.7% 17.2% ROA (%) 8.4% 7.8% 7.4% 8.0% 8.3% Consensus Net Profit (RM m) n.a. n.a. 128.6 157.0 177.0

Buy (new)

Share price: RM4.18 Target price: RM5.10 (new)

Yeak Chee Keong, CFA [email protected] (65) 6433 5730 Wong Chew Hann, CA [email protected] (603) 2297 8686

Stock Information

Description: The largest private hospital operator in Malaysia. It also runs 2 hospitals in Indonesia.

Ticker: KPJ MK Shares Issued (m): 580.6 Market Cap (RM m): 2,426.8

3-mth Avg Daily Volume (m): 0.89 KLCI: 1,444.72 Free float (%): 23.0

Major Shareholders: % Johor Corp 41.0 EPF 13.4 Nomura Asset Management 8.7

Skim Amanah Saham 8.7 Kumpulan Waqaf 8.0

Key Indicators

ROE – annualised (%) 14.5% Net cash (RM m): (187.1)

NTA/shr (RM): 1.64 Interest cover (x): 8.7

Historical Chart

0.0

1.0

2.0

3.0

4.0

5.0

Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11

KPJ MK Equity

Performance:

52-week High/Low RM4.72/RM3.67

1-mth 3-mth 6-mth 1-yr YTD

Absolute (%) (1.2) (9.1) 9.7 12.7 12.4

Relative (%) 6.3 6.6 26.5 27.6 28.1

30 November 2011 Page 2 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Investment merits

Premium valuation set to lift. Healthcare operators in Asia command

a premium valuation as the region‟s growing population and increasing

affluence fuel the need for healthcare services. There also exists a

scarcity premium by virtue of the limited number of such listed stocks.

Khazanah Nasional, Malaysia‟s sovereign wealth fund which privatised

Singapore‟s Parkway Holdings, is planning to relist its healthcare unit,

Integrated Healthcare, in the next 1-3 years. If this eventuates, it could

stir up further interest and the valuations of healthcare operator stocks

would be primed for a lift.

Stable base for scaling up foreign patient market. KPJ‟s niche has

been in the domestic private sector, owning the largest network of

community hospitals. It has thus been shielded from the more volatile

medical tourism market. With this stable and established base in the

domestic market, we believe the time is ripe for the company to move to

a higher plane and play a bigger, if not more aggressive role in medical

tourism.

Asset-light structure a boon to ROE. KPJ‟s modus operandi involves

selling its hospital assets to Al-„Aqar REIT and leasing back the

buildings for its operations. This allows the company to maintain an

asset-light structure, which, in turn, enhances its ROE. The proceeds

from the disposals also provide a stream of cash to enable continued

investment and expansion of its hospital network without straining its

balance sheet.

Good risk-reward proposition; initiate with BUY and target price of

RM5.10. The defensive nature of hospital stocks makes them attractive

investments in the current volatile equity market. In our view, KPJ offers

an appealing risk-return proposition premised on its stable earnings

from a strong domestic market focus and growth opportunities in the

medical tourism arena. The stock currently trades at the lowest FY12F

PER of 18.1x among regional peers and yet offers the highest gross

dividend yield of 3.2% (2.4% net). We initiate coverage with a BUY

recommendation and target price of RM5.10.

30 November 2011 Page 3 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Cheapest hospital stock by far

Premium valuation for Asian healthcare stocks. In Asia, long-term

positive structural factors pointing to an increasing demand for quality

healthcare have enabled the region‟s healthcare stocks to enjoy

premium valuations. Stocks of hospital operators offer one of the purest

plays on such a theme. Recent M&A activities saw hospital stocks

(Parkway Holdings and Thomson Medical) being acquired at 23-32x

PERs, reaffirming their premium valuation. At the same time, such

stocks should also command a scarcity premium. Parkway Pantai,

formed by a merger of Singapore‟s Parkway Holdings and Malaysia‟s

Pantai Group, is seeking a possible relisting under its parent, Integrated

Healthcare, and this could spark more interest in the sector, thereby

lifting valuation.

Moving to a higher plane. A study of the valuations of regional

hospital stocks over the past five years shows that KPJ has been

trading at much lower PERs compared with its peers. Although the

valuation gap is closing over the past two years, its PER is still trailing

behind its peers. We guess the reason for the discount is its domestic

market focus, while other hospital stocks offer the potential to benefit

from medical tourism. But KPJ now has a strong domestic base, which

it can leverage to grow its foreign patient volume more aggressively.

We believe this will push the company to compete on a higher plane. In

our opinion, KPJ offers one of the most attractive risk-reward

propositions.

Figure 1: Regional hospital stocks – historical PER at a glance

Source: Bloomberg

30 November 2011 Page 4 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Healthcare in Malaysia

A two-tier system. Malaysia operates a two-tier health system, split

between the public and private sectors. Public healthcare is provided

and managed by the Ministry of Health (MOH) and funded by the tax

system. It is also heavily subsidised by the government and is used by

the majority of its 28m population. The private system, on the other

hand, is user-charged and demand is mainly driven by the more affluent

who seek shorter waiting time as well as a higher quality of care and

service. The private sector is beginning to play a more important role in

alleviating the strain on the public system.

Private versus public sector. In terms of the number of hospital beds,

the private sector accounted for about 26% of the 50,087 licensed

hospital beds in Malaysia last year. Admissions-wise, the private

hospitals recorded about 29% of total hospital admissions. However, a

disproportionate split became apparent in the distribution of resources,

as evidenced by human resource allocation and hospital expenditure.

About 45% of doctors were employed in the private sector in 2008

despite the sector having only 22% of total hospital beds. Expenditure

in the private sector also exceeded that in the public sector by about

10%.

Figure 2: Distribution of resources, 2008 Figure 3: Distribution of beds

Source: Ministry of Health, Malaysia Source: Ministry of Health, Malaysia

Large burden on government. Government expenditure on healthcare

in Malaysia comprised 44% of the total national health expenditure in

2008. The figure seemed reasonable vis-à-vis other countries.

However, if the social security portion of the expenditure were

excluded, the healthcare burden on the Malaysian government would

appear to be rather high at 43%, compared to less than 20% for upper-

middle income and above nations. In fact, in the latter, a large part of

the government spending on healthcare is funded by social security

schemes, which Malaysia currently lacks. Hence, the large burden on

government spending. We understand that the government is seeking

to address this asymmetry by encouraging growth in the private sector.

Room for more healthcare spending. According to data from the

Ministry of Health, total national health expenditure in 2008 formed

about 4.8% of total GDP (WHO measured it at 4.3%). Though this

figure might be higher than some of its neighbouring countries, it was

significantly below that of the more developed nations. The US, for

example, spends about 15% of its GDP on healthcare while the global

average is about 8% in 2008. This suggests that Malaysia has room to

raise its healthcare expenditure.

30 November 2011 Page 5 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Figure 4: Worldwide healthcare expenditure as a % of GDP, 2008

Source: World Health Organisation

Table 1: Health expenditure data Health expenditure ratios Per capita health expenditures

General government expenditure on

health as % of total expenditure on

health

Social security expenditure on health as % of

general government expenditure on

health

General government expenditure on health (excl. social security)

as % of total expenditure on health

Private expenditure on health as % of

total expenditure on

health

General government expenditure

on health as % of total

government expenditure

Per capita total expenditure on

health (PPP int. $)

Per capita government

expenditure on health

(PPP int. $)

Member states 2000 2008 2000 2008 2000 2008 2000 2008 2000 2008 2000 2008 2000 2008

Malaysia 52.4 44.1 0.6 0.8 51.8 43.3 47.6 55.9 6.2 6.9 67 156 159 274

Singapore 44.9 34.1 4.8 13.2 40.1 20.9 55.1 65.9 6.2 7.8 291 479 421 625

India 27.5 32.4 16.9 17.2 10.6 15.2 72.5 67.6 3.9 4.4 69 122 19 40

Indonesia 36.6 54.4 6.2 12.3 30.4 42.1 63.4 45.6 4.5 6.2 47 91 17 49

Thailand 56.1 74.3 9.4 9.0 46.7 65.3 43.9 25.7 9.9 14.2 165 328 92 244

US 43.2 47.8 33.5 27.8 9.7 20.0 56.8 52.2 17.1 18.7 4 703 7 164 2 032 3 426

Range of values

Minimum 3.0 6.5 0 0 3.0 6.5 0.4 0.3 1.2 0.7 9 18 <1 2

Median 57.6 60.9 1.6 3.1 56.0 57.8 42.5 39.2 9.8 11.5 274 442 141 259

Maximum 99.6 99.7 100 98.5 -0.4 1.2 97.0 93.5 21.7 26.1 4 703 7 164 2 785 5 028

Income group

Low income 37.1 40.5 4.6 11.5 32.5 29.0 62.9 59.5 7.7 8.9 37 74 14 30

Lower middle income 37.1 45.4 36.0 44.4 1.1 1.0 62.9 54.6 7.1 7.8 95 197 35 88

Upper middle income 54.0 57.2 41.3 41.5 12.7 15.7 47.1 42.9 9.0 9.9 438 830 236 479

High income 59.3 62.2 46.3 42.3 13.0 19.9 40.4 36.4 15.3 16.7 2 740 4 246 1 626 2 589

Global 56.4 60.5 44.9 42.2 11.5 18.3 43.5 38.4 13.3 13.9 566 899 320 524

Source: World Health Organisation (PPP int. $) = Purchasing Power Parity International $

30 November 2011 Page 6 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Bigger role for private sector

Public system experiencing strain. While Malaysia‟s public

healthcare system has progressed over the years, the rising demand

for healthcare services has put a strain on it. Long waiting times and

high bed occupancy rates are some of the problems plaguing the

system. As a result, middle-income earners who have the means are

increasingly turning to private healthcare. This presents opportunities

for private healthcare operators to step up its role in alleviating the

stress on the public healthcare system.

Regular checks on service and cost. To ensure quality service and

rein in medical costs, the government regularly monitors the private

sector. The regulatory environment is strengthened by the passage of

the Private Healthcare Facilities and Services Act 1998. A key

regulation is the zoning regulation limit, which requires a general 20km

distance between private hospitals unless one is a centre of excellence.

A centre of excellence focuses on a specialised field of medicine. The

Act helps to curb competition while promoting a more even distribution

of private hospitals in the country. The Act also involves a doctors‟ fee

schedule, which caps the maximum amount of fees that doctors can

charge, thereby controlling medical costs.

Government lending support

Figure 5: GNI contribution from Heathcare National Key Economic Area

Source: PEMANDU, a unit of Malaysia’s Prime Minister’s Department

Ultimate vision for healthcare sector. The Malaysian government

launched the Economic Transformation Programme (ETP) on 25

October 2010 in a bid to transform the country into a high-income

economy by 2020. Healthcare is one of the 12 National Key Economic

Areas (NKEAs) identified as a driver of economic activity. The ETP

would identify private sector opportunities to reframe health as an

economic commodity as well as a social right. The ultimate vision is to

have the healthcare sector contribute an incremental GNI impact of

RM35.3b in 2020 with an additional 181,000 jobs by the same year.

One of the strategic opportunities identified in the Healthcare NKEA is

health travel or medical tourism.

30 November 2011 Page 7 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Next goal: international medical tourism

An emerging player in medical tourism. Travelling abroad for

medical treatment is a rapidly growing phenomenon in recent years.

The high cost of medical procedures in many developed countries,

coupled with rising medical standards in Asia, has attracted patients to

come to the region. This trend is also emerging as a lucrative business

proposition as affluence and mobility increases in Asia. In Malaysia,

medical tourism grew at a steady rate of 38% pa from 2003 to 2008 but

suffered a contraction in 2009. Last year, the market was estimated at

RM350m, still relatively small compared with that in countries like

Singapore, Thailand and India who were the forerunners. However,

Malaysia has its plans to gain a slice of the pie.

Attracting 1.9m health tourists by 2020. The Malaysian government

has set up the Malaysia Healthcare Travel Council (MHTC) in

December 2009 to spearhead efforts to market the country as a

preferred healthcare destination. The target is to attract 1.9m health

tourists by 2020, from about 400,000 last year, with planned investment

of RM335m in infrastructure and human capital.

Table 2: Cost comparison of selected medical procedures

Procedure (US$) US India Thailand Singapore Malaysia

Heart bypass 130,000+ 10,000 11,000 18,500 9,000 Heart valve

replacement 160,000 9,000 10,000 12,500 9,000

Angioplasty 57,000 11,000 13,000 13,000 11,000 Hip replacement 43,000 9,000 12,000 12,000 10,000

Hysterectomy 20,000 3,000 4,500 6,000 3,000 Knee replacement 40,000 8,500 10,000 13,000 8,000 Spinal fusion 62,000 5,500 7,000 9,000 6,000

Source: Patients beyond borders © 2008 by Josef Woodman

Accreditation required to be competitive. The Joint Commission

International (JCI) accreditation is arguably the gold standard for

international credentialling. Although individual countries have their own

accreditation systems, such as the Malaysian Society for Quality in

Health (MSQH) in Malaysia, possessing a JCI accreditation will find

favour with more international tourists. We understand that two of KPJ‟s

hospitals are in the process of seeking the JCI accreditation. However,

most of its hospitals already have the MSQH accreditation.

Hospitals appointed for health tourism. The MHTC has appointed

several hospitals (Table 3) to participate in attracting foreign patients to

the country. 11 of KPJ‟s current portfolio of 20 hospitals are in the

MHTC list. Hospitals owned by Parkway Pantai, Columbia, Prince Court

and Sime Darby all have the JCI accreditation.

30 November 2011 Page 8 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Table 3: Cost comparison of selected medica procedures

Private hospital No. of

beds

Quality certification*

1 Assunta Hospital, Selangor 344 ISO, MSQH

2 Columbia Asia Hospital, Bukit Rimau, Selangor 84

3 Gleneagles Hospital Kuala Lumpur, Wilayah Persekutuan - Kuala Lumpur 330 JCI, ISO, MSQH

4 Gleneagles Medical Centre, Pulau Pinang 227 MSQH

5 Hospital Fatimah, Perak 223 ISO, MSQH

6 HSC Medical Center, Wilayah Persekutuan - Kuala Lumpur 7

7 Island Hospital, Pulau Pinang 7

8 KPJ Ampang Puteri Specialist Hospital, Selangor 230 ISO

9 KPJ Damansara Specialist Hospital, Selangor 250 MSQH

10 KPJ Ipoh Specialist Hospital, Perak 260 ISO, MSQH

11 KPJ Johor Specialist Hospital, Johor 206 ISO, MSQH

12 KPJ Kajang Specialist Hospital, Selangor 118

13 KPJ Penang Specialist Hospital, Pulau Pinang 236

14 KPJ Selangor Specialist Hospital, Selangor 173 MSQH

15 Lam Wah Ee Hospital, Pulau Pinang 422 ISO, MSQH

16 LohGuanLye Specialists Centre, Pulau Pinang 265 ISO, MSQH

17 Mahkota Medical Centre, Melaka 365 ISO, MSQH

18 Mawar Renal Medical Centre, Negeri Sembilan 78

19 Mount Miriam Cancer Hospital, Pulau Pinang 40 ISO

20 National Heart Institute (IJN), Wilayah Persekutuan - Kuala Lumpur 270 JCI, ISO, MSQH

21 NCI Cancer Hospital, Negeri Sembilan 0 ISO

22 Normah Medical Specialist Centre, Sarawak 130 MSQH

23 Pantai Hospital Ayer Keroh, Melaka 250

24 Pantai Hospital Ipoh, Perak 121

25 Pantai Hospital Kuala Lumpur, Wilayah Persekutuan - Kuala Lumpur 332 JCI

26 Pantai Hospital Penang, Pulau Pinang 180 ISO, MSQH

27 Penang Adventist Hospital, Pulau Pinang 216 JCI, MSQH

28 Prince Court Medical Centre, Wilayah Persekutuan - Kuala Lumpur 300 JCI, MSQH

29 Puteri Specialist Hospital, Johor 102

30 Putra Specialist Hospital, Melaka 225 ISO

31 Sabah Medical Centre, Sabah 95

32 Sentosa Medical Centre, Wilayah Persekutuan - Kuala Lumpur 135 ISO

33 Sime Darby Medical Centre Subang Jaya, Selangor 393 JCI, ISO, MSQH

34 Sunway Medical Centre, Selangor 240 ISO, MSQH

35 Taman Desa Medical Centre, Wilayah Persekutuan - Kuala Lumpur 128

36 Tawakal Hospital, Wilayah Persekutuan - Kuala Lumpur 158 ISO, MSQH

37 Timberland Medical Centre, Sarawak 72

38 Tropicana Medical Centre, Selangor 70 ISO

39 Tun Hussein Onn National Eye Hospital (THONEH), Selangor 46

40 Tung Shin Hospital, Wilayah Persekutuan - Kuala Lumpur 247 ISO

41 UM Specialist Centre, Wilayah Persekutuan - Kuala Lumpur 60

Private healthcare facilities in Malaysia are required to be licensed under the Private Healthcare Facilities and Services Act 1998. Joint Commission International (JCI) and Malaysian Society for Quality in Health (MSQH) are two accreditations that many of the private hospitals

have. Both are recognised members of the International Accreditation Federation Council (IAFC), a body under the umbrella of the International Society for Quality Healthcare (ISQuA). These accreditations ensure a minimum level of quality. Source: Association of Private Hospitals

30 November 2011 Page 9 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Positive structural factors

Population growth and demographic shift. Malaysia‟s total

population stood at about 28.3m in 2010, having grown at an annual

rate of 2.0% in the past decade. Longer life spans also resulted in a

larger number of people aged 65 and above. As at last year, they

accounted for about 4.7% of the total population and are still growing.

This demographic shift will underpin the factors fuelling the ever-

increasing need for healthcare services.

Rising national income. In the meantime, Malaysians are getting

wealthier as income levels rise in tandem with the country‟s progress.

Better education, longer life span and a desire for a better lifestyle also

make them more willing to spend on healthcare. As evidence, per

capita expenditure on health has increased along with higher income

levels over the years.

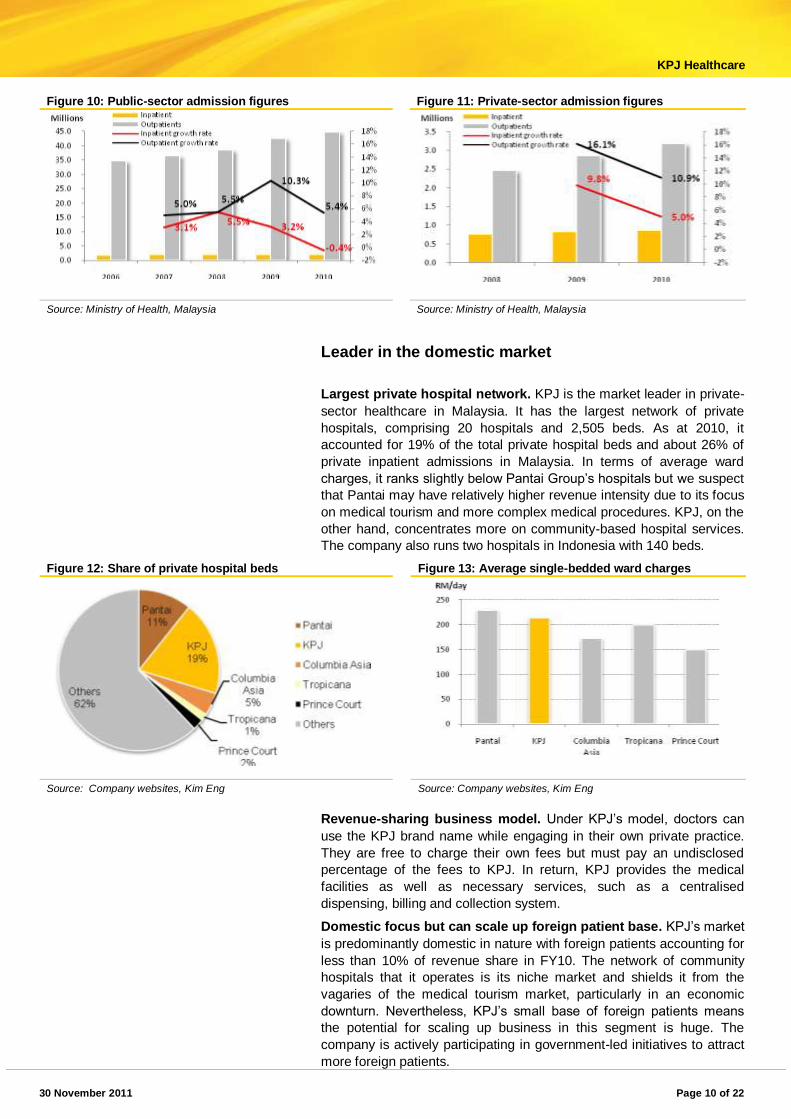

Admission rates on the rise. Rising admission figures from data

released by the MOH support our notion. Inpatients and outpatients are

growing in both the public and private sectors. However, the statistics

also show that admission figures in the private sector are growing at a

much higher rate than in the public sector.

Figure 6: Population growth Figure 17: Ageing population

Source: Department of Statistics, Malaysia Source: Ministry of Health, Malaysia

Figure 8: Rising GNI per capita Figure 9: Rising per capita expenditure on health

Source: World Health Organisation Source: World Health Organisation

30 November 2011 Page 10 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Figure 10: Public-sector admission figures Figure 11: Private-sector admission figures

Source: Ministry of Health, Malaysia Source: Ministry of Health, Malaysia

Leader in the domestic market

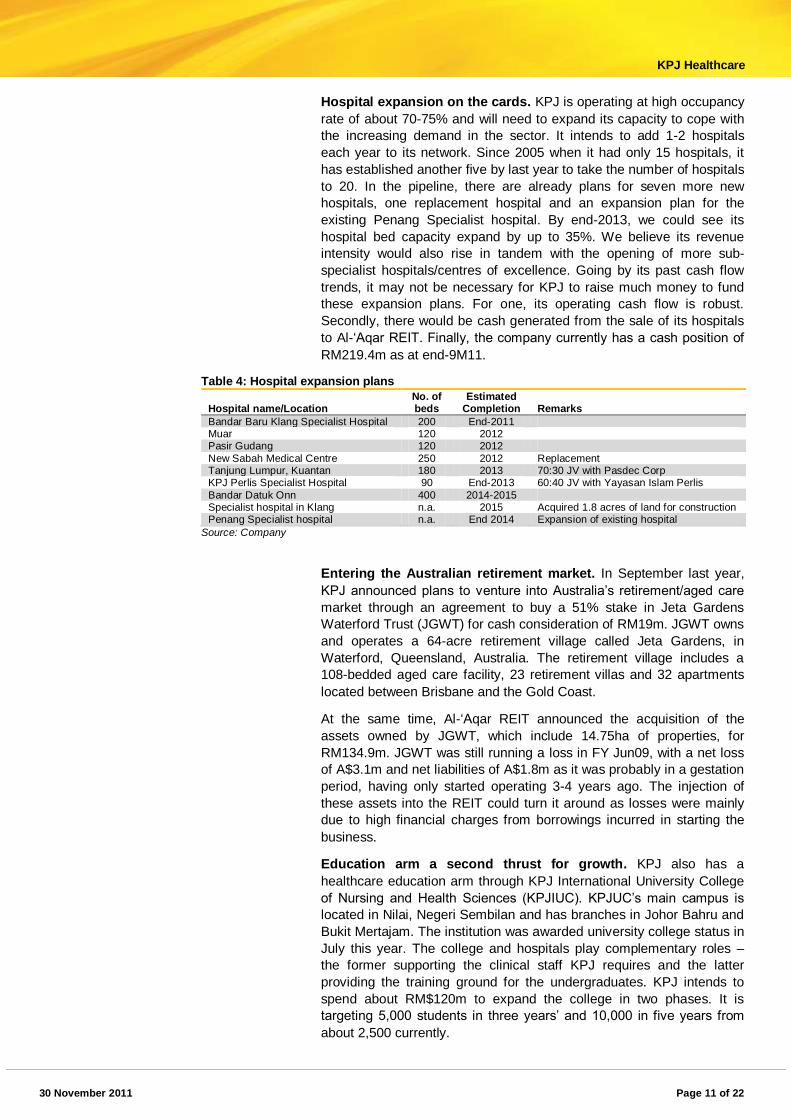

Largest private hospital network. KPJ is the market leader in private-

sector healthcare in Malaysia. It has the largest network of private

hospitals, comprising 20 hospitals and 2,505 beds. As at 2010, it

accounted for 19% of the total private hospital beds and about 26% of

private inpatient admissions in Malaysia. In terms of average ward

charges, it ranks slightly below Pantai Group‟s hospitals but we suspect

that Pantai may have relatively higher revenue intensity due to its focus

on medical tourism and more complex medical procedures. KPJ, on the

other hand, concentrates more on community-based hospital services.

The company also runs two hospitals in Indonesia with 140 beds.

Figure 12: Share of private hospital beds Figure 13: Average single-bedded ward charges

Source: Company websites, Kim Eng Source: Company websites, Kim Eng

Revenue-sharing business model. Under KPJ‟s model, doctors can

use the KPJ brand name while engaging in their own private practice.

They are free to charge their own fees but must pay an undisclosed

percentage of the fees to KPJ. In return, KPJ provides the medical

facilities as well as necessary services, such as a centralised

dispensing, billing and collection system.

Domestic focus but can scale up foreign patient base. KPJ‟s market

is predominantly domestic in nature with foreign patients accounting for

less than 10% of revenue share in FY10. The network of community

hospitals that it operates is its niche market and shields it from the

vagaries of the medical tourism market, particularly in an economic

downturn. Nevertheless, KPJ‟s small base of foreign patients means

the potential for scaling up business in this segment is huge. The

company is actively participating in government-led initiatives to attract

more foreign patients.

30 November 2011 Page 11 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Hospital expansion on the cards. KPJ is operating at high occupancy

rate of about 70-75% and will need to expand its capacity to cope with

the increasing demand in the sector. It intends to add 1-2 hospitals

each year to its network. Since 2005 when it had only 15 hospitals, it

has established another five by last year to take the number of hospitals

to 20. In the pipeline, there are already plans for seven more new

hospitals, one replacement hospital and an expansion plan for the

existing Penang Specialist hospital. By end-2013, we could see its

hospital bed capacity expand by up to 35%. We believe its revenue

intensity would also rise in tandem with the opening of more sub-

specialist hospitals/centres of excellence. Going by its past cash flow

trends, it may not be necessary for KPJ to raise much money to fund

these expansion plans. For one, its operating cash flow is robust.

Secondly, there would be cash generated from the sale of its hospitals

to Al-„Aqar REIT. Finally, the company currently has a cash position of

RM219.4m as at end-9M11.

Table 4: Hospital expansion plans

Hospital name/Location No. of beds

Estimated Completion Remarks

Bandar Baru Klang Specialist Hospital 200 End-2011 Muar 120 2012 Pasir Gudang 120 2012

New Sabah Medical Centre 250 2012 Replacement Tanjung Lumpur, Kuantan 180 2013 70:30 JV with Pasdec Corp KPJ Perlis Specialist Hospital 90 End-2013 60:40 JV with Yayasan Islam Perlis

Bandar Datuk Onn 400 2014-2015 Specialist hospital in Klang n.a. 2015 Acquired 1.8 acres of land for construction Penang Specialist hospital n.a. End 2014 Expansion of existing hospital

Source: Company

Entering the Australian retirement market. In September last year,

KPJ announced plans to venture into Australia‟s retirement/aged care

market through an agreement to buy a 51% stake in Jeta Gardens

Waterford Trust (JGWT) for cash consideration of RM19m. JGWT owns

and operates a 64-acre retirement village called Jeta Gardens, in

Waterford, Queensland, Australia. The retirement village includes a

108-bedded aged care facility, 23 retirement villas and 32 apartments

located between Brisbane and the Gold Coast.

At the same time, Al-„Aqar REIT announced the acquisition of the

assets owned by JGWT, which include 14.75ha of properties, for

RM134.9m. JGWT was still running a loss in FY Jun09, with a net loss

of A$3.1m and net liabilities of A$1.8m as it was probably in a gestation

period, having only started operating 3-4 years ago. The injection of

these assets into the REIT could turn it around as losses were mainly

due to high financial charges from borrowings incurred in starting the

business.

Education arm a second thrust for growth. KPJ also has a

healthcare education arm through KPJ International University College

of Nursing and Health Sciences (KPJIUC). KPJUC‟s main campus is

located in Nilai, Negeri Sembilan and has branches in Johor Bahru and

Bukit Mertajam. The institution was awarded university college status in

July this year. The college and hospitals play complementary roles –

the former supporting the clinical staff KPJ requires and the latter

providing the training ground for the undergraduates. KPJ intends to

spend about RM$120m to expand the college in two phases. It is

targeting 5,000 students in three years‟ and 10,000 in five years from

about 2,500 currently.

30 November 2011 Page 12 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Risks

Competition from other hospitals. KPJ faces competition from other

hospitals with established networks. Its two largest rivals are Pantai

Group and Columbia Asia. There are also many other small players in

the market. It would also face more competition from regional players

as it begins to compete for foreign patients.

Liberalisation of the healthcare sector. Healthcare is one of the three

services sector (the others being education and professional services)

which is heading towards liberalization to raise its overall

competitiveness. Some of the recommendations announced in the

government‟s Strategic Reform Initiatives in July 2011 are the removal

of restrictions to foreign equity participation in setting up specialised

private hospitals if they meet a minimum number of beds and the

relaxation of entry restrictions for foreign specialists such as doctors

and dentists.

Shortage of healthcare professionals. Malaysia faces a shortage of

doctors and nurses. Expanding the capacity of a hospital or building

new ones would require a corresponding increase in the number of

doctors and nurses to operate it. In the event that KPJ fails to engage

such professionals to support its expansion plans, it may not be able to

achieve optimal operation. Conversely, if it fails to retain such

professionals and an exodus occurs, its operations would also be

affected.

Price pressure by insurance companies. The insurance industry in

Malaysia has grown bigger and more established. This has enhanced

its bargaining power in negotiations for more discounts for medical

procedures and treatments. This development could negatively affect

pricing.

Delay in expansion plans. We expect KPJ to pursue its expansion

plans to continue to grow its hospital network, which would in turn lead

to an overall increase in patient volume and revenue. Any delay in

expansion would retard the pace of growth that we have assumed. Cost

overrun for building new hospitals poses further risk.

30 November 2011 Page 13 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Financials

Double-digit revenue growth. KPJ reports its revenue under four

major segments as illustrated in Figure 19. Last year, the bulk of the

revenue came from Malaysia with less than 1% from Indonesia. Over

FY06-10, revenue grew by strong double-digit CAGR of 19% as patient

volume swelled on hospital network expansion and increase in revenue

intensity. Future base revenue growth would be driven by the

expansion of hospital network via acquisitions or building new hospitals,

thereby increasing revenue intensity and foreign patient numbers.

Figure 14: Revenue and profit history Figure 15: FY10 segmental revenue, (RM’000)

Source: Company Source: Company

Figure 16: Patient volume growth Figure 17: Margin trends

Source: Company Source: Company

Figure 18: COGS breakdown for FY10

Source: Company

30 November 2011 Page 14 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Stable margins and cost trends. Gross margins have been stable at

29-30% over the past five years with net profit margins trending up from

4.9% in FY06 to 7.2% in FY10 due mainly to lower net interest

expense. Going forward, we expect gross margins to remain stable at

the 30-31% level. Medical consultants‟ fees and material cost are the 2

major cost components, making up about 75% of total COGS. KPJ has

managed to keep these cost increases in tandem with revenue growth,

thereby maintaining its gross margins and we expect that it would

continue to do so going forward.

Cash flows. KPJ has generated increasingly strong operating cash

flows in tandem with the growth in revenue. The investment cash flows

mainly reflect its acquisition of hospitals, facilities as well as proceeds

from the disposal of its hospital assets to Al-„Aqar REIT. Going forward,

KPJ intends to continue to expand its hospital network by acquiring or

building 1-2 hospitals a year. We estimate that this would require about

RM150-200m capex per year. In addition, it has capital commitments of

RM19m for the acquisition of Jeta Gardens, RM120m for its university

expansion and we forecast it would need about RM35m yearly for

maintenance capex. However, the sale of more hospital assets to Al-

„Aqar REIT would generate about RM83.3m of positive cash flow for

KPJ.

Table 5: Future investing cash inflows/(outflows)

Purpose (RM m) 2011 2012 2013 2014

Jeta Gardens (19) - - -

University Expansion (10) (30) (30) (30)

Hospital Expansion Plans (150) (150) (150) (150)

Sale of hospitals to REIT 83.3

Purchase of land in Klang (23.8)

Maintenance capex (35) (35) (35) (35)

(130.7) (238.8) (215) (215)

Source: Kim Eng estimates

Figure 19: Historical cash flows Figure 20: Improving gearing

Source: Company Source: Company

Table 6: Working capital efficiency

FY06 FY07 FY08 FY09 FY10

Inventory days 6.9 11.5 11.5 10.5 11.3 Receivable days 28.8 46.9 50.2 55.0 59.8

Payable days 53.8 89.7 90.6 87.4 90.2

Cash conversion cycle (18.1) (31.2) (28.8) (21.9) (19.1)

Source: Company, Kim Eng

30 November 2011 Page 15 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Favourable working capital cycle and improving gearing. With short

inventory days and long payable days, KPJ‟s cash conversion cycle is

favourable at about negative 20-30 days. Gearing has also improved

with net gearing decreasing from 0.63x as at end-FY06 to 0.20x as at

end-9M11. Other than strong cash flows from its business, the disposal

of its assets to Al-„Aqar REIT contributed to the improved gearing. Our

cash flow projections derive a strengthening gearing level. We expect

net gearing to reduce further to 0.17x by end-FY13.

REIT injection. KPJ makes it a point to dispose of its hospital assets to

Al-„Aqar REIT, resulting in a lean balance sheet structure which

enhances its ROE. The Al-„Aqar KPJ REIT is the world‟s first Islamic

healthcare REIT and was established on 27 June 2006 to invest in

Syariah acceptable properties. It was listed on the Main Board of Bursa

Malaysia on 10 August 2006. KPJ injects its hospital assets into the

REIT in order to maintain an asset-light structure. To date, it has

injected three tranches of assets into the REIT. A fourth tranche

consisting of three properties at a sale price of RM139m is in progress.

KPJ is expected to receive 56.6m units of Al-„Aqar REIT as part of the

consideration for the sale, which it intends to distribute in specie or sell

in the open market to maintain its stake in the REIT at below 50%. KPJ

currently has a 49% stake in the REIT and by keeping it below 50%, its

assets and debts will be accounted for off-balance sheet.

Table 7: Assets disposed to Al-‘Aqar REIT

Asset Book value

(RM m) Sale price

(RM m) Status

1st tranche KPJ Ampang Puteri Specialist Hospital 87.8 481 Completed

17 Aug 2006

KPJ Damansara Specialist Hospital 88.6

KPJ Johor Specialist Hospital 68.6

KPJ Ipoh Specialist Hospital 44.3

Puteri Specialist Hospital 35.0

KPJ Selangor Specialist Hospital 46.3

2nd tranche KPJ Perdana Specialist Hospital 36.3 170 Completed

17 Mar 2008

Kuantan Specialist Hospital 15.6

KPJ Kajang Specialist Hospital 38.5

Kedah Medical Centre, Alor Star 44.8

Sentosa Medical Centre 22.5

3rd tranche KPJ Seremban Specialist Hospital 45.9 292 Completed 6 July 2010

Taiping Medical Centre 2.8

Damai Specialist Hospital 13.1

Bukit Mertajam Specialist Hospital 10.3

KPJ Penang Specialist Hospital 21.7

Tawakal Hospital Existing Building 36.0

KPJ Tawakal Specialist Hospital 62.1

KPJ International University College 26.0

4th tranche Bandar Baru Klang Specialist Hospital 38.0 139 In progress

Kluang Utama Specialist Hospital 3.2

RS Bumi Serpong Damai, Jakarta (completed) 47.3

Source: Company

Table 8: Dupont analysis

FY06 FY07 FY08 FY09 FY10

Net margin 4.9% 6.7% 6.8% 7.6% 7.2% Total asset turnover 1.5 1.0 1.0 1.1 1.1 ROA 7.4% 6.4% 6.9% 8.4% 7.8%

Financial leverage 2.5 2.4 2.3 2.2 2.2 ROE 18.5% 15.6% 15.7% 18.3% 17.0%

Source: Company

Dilutive warrants. KPJ completed a share split exercise on 15 January

2010 whereby each share was split into two shares. There was also a

bonus issue of 105.5m new shares and 131.9m free warrants. The

warrants have an exercise price of RM1.70 per share and are dilutive,

being in-the-money. There were 80.8m warrants outstanding as at end-

September this year.

30 November 2011 Page 16 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Dividend payout. KPJ does not have a fixed dividend policy but based

on historical trends, it has paid out between 28-68% of its net profits as

dividends over FY06-10. It would also make additional payouts in

specie, in the form of shares in Al‟Aqar REIT which it receives as part

consideration for sale of its hospital assets to the REIT. In FY08 for

example, it paid out dividend in specie of 23 REIT units per 100 KPJ

shares.

Revenue model and assumptions We forecast KPJ‟s revenue to grow by 13-18% over FY11F-14F,

buoyed by total patient growth of 9-15% in the same period. We expect

revenue growth to be driven by increased patient load from the addition

of more hospitals to its network, as well as higher foreign patient

volume as it actively participates in the medical tourism scene.

Revenue intensity should also go up gradually from general healthcare

cost increases and higher-quality earnings from the foreign patient

portion.

Table 9: Model assumptions

FY05 FY06 FY07 FY08 FY09 FY10 FY11F FY12F FY13F

Revenue (RM m)

Hospital income 239.2 306.5 403.9 476.6 531.3 638.2 731.7 805.6 977.3

Consultation income 212.0 260.6 338.5 394.7 444.7 490.0 544.3 634.4 738.8

Sale of pharmaceutical,

medical & surgical pdt 198.2 250.9 345.7 376.0 462.8 507.4 571.0 657.0 756.4

Other hospital income 10.3 14.0 20.0 20.0 17.6 19.0 20.1 21.7 23.5

Clinic rental 8.5 8.1 12.0 12.1 12.3 10.5 10.8 11.6 12.6

Others 1.8 5.9 8.0 7.9 5.3 8.5 9.3 10.1 10.9

Total 659.6 832.0 1,108.0 1,267.3 1,456.4 1,654.6 1,867.0 2,118.7 2,495.9

Growth (%)

26% 33% 14% 15% 14% 13% 13% 18%

Operating assumptions

Malaysia

No. of hospitals 15 17 17 19 19 20 20 23 25

No. of licensed beds 1,724 2369 2369 2455 2455 2505 2505 3100 3370

Indonesia

No. of hospitals 1 1 1 1 1 2 2 2 2

No. of licensed beds 80 80 80 80 80 140 140 140 140

Outpatients (‟000) 1,163 1,556 1,734 1,956 1,979 2,232 2,422 2,778 3,192

Inpatients (‟000) 118 158 179 196 207 226 248 278 326

Total patients ('000) 1,280 1,715 1,913 2,153 2,186 2,458 2,670 3,056 3,518

Growth (%) 34% 12% 13% 2% 12% 9% 14% 15%

Source: Company, Kim Eng estimates

Accordingly, based on our model assumptions, we derive net profit

growth of between 8-19% over FY11-13F. KPJ reported its 9M11

results on 29 November 2011 with net profit of RM92.2m, which makes

up about 72% of our FY11F forecast, and validating our growth

expectation for the year.

30 November 2011 Page 17 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Valuation and recommendation

We initiate coverage on KPJ with a BUY recommendation and target

price of RM5.10 based on 22x PER on fully-diluted FY12F earnings.

This valuation is hardly expensive considering that some of its peers

are trading as high as 29x PER. At its current price, KPJ is the

cheapest hospital stock in the region in terms of PER valuation, trading

at 18.1x FY12F PER compared with the peer average of 22.3x. It also

offers the highest gross dividend yield of 3.2% (2.4% net yield) and one

of the highest ROEs among its peers. With a stable domestic earnings

base, we see limited downside to KPJ‟s earnings. Moreover, structural

demand factors would provide further support and present vast

opportunities for growth in areas such as medical tourism.

Table 10: Peer comparison

Mkt cap

Rating TP Price PER (x) P/S P/B ROE NPM Net D/E

Yld

Company

(lcl b) (lcl) (lcl) Hist Curr Fwd (x) (x) (%) (%) (%) (%)

Raffles Medical Group SGD 1.1 BUY 2.73 2.15 24.9 24.2 21.2 4.3 3.6 16.9 18.9 (29.5) 1.6

Healthway Medical Corp SGD 0.2 NR n.a. 0.08 38.1 - - 2.0 0.8 1.7 3.3 9.1 0.0

Apollo Hospitals Enterprise Rs 80.5 NR n.a. 612.50 41.3 33.5 29.2 2.9 4.0 10.4 7.1 37.8 0.6

Fortis Healthcare India Rs 46.4 NR n.a. 114.50 35.4 - - 3.0 1.4 4.8 8.4 26.2 0.0

Bangkok Dusit Medical Bt 115.5 NR n.a. 74.75 26.6 27.5 23.5 3.2 3.8 15.4 9.7 39.7 1.1

Bumrungrad Hospital Bt 33.3 NR n.a. 45.75 21.5 22.4 19.5 3.0 5.2 21.8 12.8 14.9 2.1

KPJ Healthcare RM 2.4 BUY 5.10 4.18 20.6 21.3 18.1 1.3 2.9 17.0 7.2 24.0 3.2

Average

29.8 25.8 22.3 2.8 3.1 12.6 9.6 17.5 1.2

Average excl. KPJ

31.3 26.9 23.3 3.1 3.1 11.8 10.0 16.4 0.9

Source: Bloomberg, Kim Eng

30 November 2011 Page 18 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Company profile

Overview. KPJ Healthcare Berhad is the largest private hospital

operator in Malaysia, operating 20 hospitals and licensed for 2,505

beds. It also runs two hospitals in Indonesia with a total of 140 beds.

KPJ maintains an asset-light structure by selling its hospital buildings to

Al-‟Aqar REIT and then leasing them back. It owns a 49% stake in the

REIT. Johor Corporation, a government-linked corporation of the Johor

state and one of Malaysia‟s leading conglomerates, is the parent

company of KPJ and holds a 41% interest in it. KPJ was listed on the

Main Board of Bursa Malaysia, then known as the Kuala Lumpur Stock

Exchange, on 29 November 1994 and remains the only listed hospital

group on Bursa.

Table 11: KPJ’ s hospital network

No. of licensed beds No. of licensed beds

Malaysia Johor

Negeri Sembilan KPJ Johor Specialist Hospital 200 KPJ Seremban Specialist Hospital 130

Puteri Specialist Hospital 146

Kluang Utama Specialist Hospital 40 Perak

KPJ Ipoh Specialist Hospital 250

Kuala Lumpur/Selangor

Taiping Medical Centre 46

KPJ Ampang Puteri Specialist Hospital 217 KPJ Damansara Specialist Hospital 158 Penang

KPJ Selangor Specialist Hospital 169 KPJ Penang Specialist Hospital 236

KPJ Kajang Specialist Hospital 110 KPJ Tawakal Specialist Hospital 147 Pahang

Sentosa Medical Centre 135 Kuantan Specialist Hospital 72

Kelantan

Sarawak

KPJ Perdana Specialist Hospital 83 Kuching Specialist Hospital 80

Sibu Specialist Medical Centre 50

Kedah

Kedah Medical Centre, Alor Star 98 Sabah

Damai Specialist Hospital 43

Sabah Medical Centre 95

Total Malaysia 2,505

Indonesia RS Medika Permata Hijau, Jakarta 60

RS Bumi Serpong Damai, Jakarta 80

Total Indonesia 140

Total no. of beds 2,645

Source: Company

30 November 2011 Page 19 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

Figure 31: Corporate structure

Source: Company

Key management

Datin Paduka Siti Sa’diah Sheikh Bakir, Managing Director. Datin

Paduka has been the managing director of KPJ since March 1993. She

graduated with a Bachelor of Economics from the University of Malaya

and holds an MBA from Henley Management College, University of

Reading, London. She is also the chairman of various hospitals and

companies in the KPJ Group and sits as a director for various other

companies in Malaysia. She has served as an independent non-

executive director of Bursa Malaysia since 2004 and the president of

the Malaysian Society for Quality in Health (MSQH) since 1997.

Mohd Sahir Rahmat, Chief Financial Officer. Previously the group

general manager, Mr Mohd took over the role of chief financial officer

from Lee Swee Hee on 4 July 2011. He holds an MBA from Henley

Management College, London, and has served as the executive

director of Johor Specialist Hospital and Puteri Specialist Hospital.

Amiruddin Abdul Satar, Chief Operating Officer. Mr Amiruddin is an

accountant by profession and holds an MBA from Henley Business

School, University of Reading, London. He is also an executive director

of KPJ, having spent more than 15 years with the group and

contributing in areas of hospital operations, finance, strategic planning

and investment decisions.

30 November 2011 Page 20 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

INCOME STATEMENT (RM m) BALANCE SHEET (RM m)

FY Dec FY2010 FY2011F FY2012F FY2013F FY Dec FY2010 FY2011F FY2012F FY2013F

Revenue 1,654.6 1,867.0 2,118.7 2,495.9 Fixed Assets 1,024.6 1,193.1 1,374.8 1,513.6

EBITDA 203.0 241.8 302.6 366.0 Other LT Assets 0.0 0.0 0.0 0.0

Depreciation & Amortisation 59.0 69.7 87.2 106.6 Cash/ST Investments 197.1 240.5 248.4 317.1

Operating Profit (EBIT) 144.0 172.1 215.4 259.4 Other Current Assets 458.4 362.8 411.5 484.6

Interest (Exp)/Inc (6.4) (9.5) (12.0) (13.5) Total Assets 1,680.0 1,796.4 2,034.7 2,315.3

Associates 30.4 22.8 30.1 30.4

One-offs 0.0 0.0 0.0 0.0 ST Debt 362.7 128.5 147.1 166.8

Pre-Tax Profit 168.0 185.5 233.5 276.3 Other Current Liabilities 362.2 386.4 428.3 492.4

Tax (41.7) (43.4) (62.0) (72.1) LT Debt 36.7 257.1 294.1 333.6

Minority Intereset (7.3) (13.4) (18.3) (23.9) Other LT Liabilities 55.0 55.6 57.7 60.7

Net Profit 118.9 128.7 153.2 180.2 Minority Interest 94.7 112.0 127.1 149.8

Recurring Net Profit 118.9 128.7 153.2 180.2 Shareholders' Equity 768.6 856.8 980.4 1,112.1

Total Liabilities-Capital 1,680.0 1,796.4 2,034.7 2,315.3

Revenue Growth (%) 13.6% 12.8% 13.5% 17.8%

EBITDA Growth (%) 8.6% 19.1% 25.1% 21.0% Share Capital (m) 280.0 289.3 289.3 289.3

EBIT Growth (%) 2.5% 19.5% 25.2% 20.4% Gross Debt/(Cash) 399.4 385.6 441.2 500.4

Net Profit Growth (%) 7.2% 8.3% 19.0% 17.7% Net Debt/(Cash) 202.3 145.0 192.8 183.3

Recurring Net Profit Growth (%) 7.2% 8.3% 19.0% 17.7% Working Capital (69.4) 88.5 84.5 142.5

Tax Rate (%) 24.1% 22.7% 25.8% 25.3%

CASH FLOW (RM m) RATES & RATIOS

FY Dec FY2010 FY2011F FY2012F FY2013F FY Dec FY2010 FY2011F FY2012F FY2013F

Profit before taxation 168.0 185.5 233.5 276.3 EBITDA Margin % 12.3% 13.0% 14.3% 14.7% Depreciation 59.0 69.7 87.2 106.6 Op. Profit Margin % 8.7% 9.2% 10.2% 10.4% Net interest receipts/(payments) 6.4 9.5 12.0 13.5 Net Profit Margin % 7.2% 6.9% 7.2% 7.2% Working capital change 31.2 2.9 (7.3) (9.7) ROE % 17.0% 15.8% 16.7% 17.2% Cash tax paid (37.1) (43.3) (62.5) (72.9) ROA % 7.8% 7.4% 8.0% 8.3% Others (incl'd exceptional items) (13.3) (17.2) (19.3) (22.0) Net Margin Ex. El % 7.2% 6.9% 7.2% 7.2% Cash flow from operations (32.2) (16.0) (39.1) (30.6) Dividend Cover (x) 2.0 2.2 2.3 2.3 Capex 182.0 191.1 204.5 261.2 Interest Cover (x) 10.6 10.0 11.2 11.8 Disposal/(purchase) (227.5) (214.0) (238.8) (215.0) Asset Turnover (x) 1.0 1.0 1.0 1.1 Others 64.7 83.3 0.0 0.0 Asset/Debt (x) 4.2 4.7 4.6 4.6 Cash flow from investing (36.6) 50.8 34.4 35.8 Debtors Turn (days) 59.8 59.2 56.4 55.5 Debt raised/(repaid) (199.5) (80.0) (204.4) (179.2) Creditors Turn (days) 90.2 88.1 84.9 83.3 Equity raised/(repaid) 30.6 (13.8) 55.6 59.3 Inventory Turn (days) 11.3 11.8 11.3 11.1 Dividends (paid) 54.9 9.4 0.0 0.0 Net Gearing % 26% 17% 20% 16% Interest payments (26.5) (63.3) (47.9) (72.5) Debt/ EBITDA (x) 2.0 1.6 1.5 1.4 Others 0.0 0.0 0.0 0.0 Debt/ Market Cap (x) 0.17 0.16 0.18 0.21 Cash flow from financing 59.0 (67.7) 7.7 (13.3)

Change in cash 41.6 43.4 7.8 68.8

Source: Company, Kim Eng

30 November 2011 Page 21 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

APPENDIX 1

Definition of Ratings

Maybank Investment Bank Research uses the following rating system:

BUY Total return is expected to be above 10% in the next 12 months

HOLD Total return is expected to be between -5% to 10% in the next 12 months

SELL Total return is expected to be below -5% in the next 12 months

Applicability of Ratings

The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are

only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not

carry investment ratings as we do not actively follow developments in these companies.

Some common terms abbreviated in this report (where they appear):

Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings

BV = Book Value FV = Fair Value PEG = PE Ratio To Growth

CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio

Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter

CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset

DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On Equity DPS = Dividend Per Share

NTA = Net Tangible Asset ROSF = Return On Shareholders‟ Funds

EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital

EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year

EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date

EV = Enterprise Value PBT = Profit Before Tax

Disclaimer

This report is for information purposes only and under no circumstances is it to be considered or intended as an offer to sel l or a solicitation

of an offer to buy the securities referred to herein. Investors should note that income from such securi ties, if any, may fluctuate and that each

security‟s price or value may rise or fall. Opinions or recommendations contained herein are in form of technical ratings and fundamental

ratings. Technical ratings may differ from fundamental ratings as technical valuations apply different methodologies and are purely based on

price and volume-related information extracted from Bursa Malaysia Securities Berhad in the equity analysis.Accordingly, investors may

receive back less than originally invested. Past performance is not necessarily a guide to future performance. This report is not intended to

provide personal investment advice and does not take into account the specific investment objectives, the financial situation and the

particular needs of persons who may receive or read this report. Investors should therefore seek financial, legal and other advice regarding

the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently

verified by Maybank Investment Bank Berhad and consequently no representation is made as to the accuracy or completeness of this report

by Maybank Investment Bank Berhad and it should not be relied upon as such. Accordingly, no liability can be accepted for any direct,

indirect or consequential losses or damages that may arise from the use or reliance of this report. Maybank Investment Bank Berhad, its

affiliates and related companies and their officers, directors, associates, connected parties and/or employees may from time to time have

positions or be materially interested in the securities referred to herein and may further act as market maker or may have assumed an

underwriting commitment or deal with such securities and may also perform or seek to perform investment banking services, advisory and

other services for or relating to those companies. Any information, opinions or recommendations contained herein are subject to change at

any time, without prior notice.

This report may contain forward looking statements which are often but not always identified by the use of words such as “ant icipate”,

“believe”, “estimate”, “intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”,

“should”, “could” or “might” occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions

made and information currently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ

materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on thes e forward-

looking statements. Maybank Investment Bank Berhad expressly disclaims any obligation to update or revise any such forward looking

statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrenc e of unanticipated

events.

This report is prepared for the use of Maybank Investment Bank Berhad's clients and may not be reproduced, altered in any way, transmitted

to, copied or distributed to any other party in whole or in part in any form or manner without the prior express written consent of Maybank

Investment Bank Berhad and Maybank Investment Bank Berhad accepts no liability whatsoever for the actions of third parties in this respect.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any

locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

30 November 2011 Page 22 of 22

KPJ Healthcare 17 October 2011

Page 1 of 2

APPENDIX 1

Additional Disclaimer (for purpose of distribution in Singapore)

This report has been produced as of the date hereof and the information herein maybe subject to change. Kim Eng Research Pte Ltd

("KERPL") in Singapore has no obligation to update such information for any recipient. Recipients of this report are to contact KERPL in

Singapore in respect of any matters arising from, or in connection with, this report. If the recipient of this report is not an accredited investor,

expert investor or institutional investor (as defined under Section 4A of the Singapore Securities and Futures Act), KERPL shall be legally

liable for the contents of this report, with such liability being limited to the extent (if any) as permitted by law.

As of 30 November 2011, KERPL does not have an interest in the said company/companies.

Additional Disclaimer (for purpose of distribution in the United States)

This research report prepared by Maybank Investment Bank Berhad is distributed in the United States (“US”) to Major US Institutional

Investors (as defined in Rule 15a-6 under the Securities Exchange Act of 1934, as amended) only by Kim Eng Securities USA, a broker-

dealer registered in the US (registered under Section 15 of the Securities Exchange Act of 1934, as amended).

All responsibility for the distribution of this report by Kim Eng Securities USA in the US shall be borne by Kim Eng. All resulting transactions

by a US person or entity should be effected through a registered broker-dealer in the US.

This report is for distribution only under such circumstances as may be permitted by applicable law. The securities described herein may not

be eligible for sale in all jurisdictions or to certain categories of investors. This report is not directed at you if Kim Eng Securities is prohibited

or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it

that Kim Eng Securities is permitted to provide research material concerning investments to you under relevant legislation and regulations.

Without prejudice to the foregoing, the reader is to note that additional disclaimers, warnings or qualifications may apply i f the reader is

receiving or accessing this report in or from other than Malaysia.

As of 30 November 2011, Maybank Investment Bank Berhad and the covering analyst does not have any interest in in any companies

recommended in this Market themes report.

Analyst Certification:

The views expressed in this research report accurately reflect the analyst's personal views about any and all of the subject securities or

issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations

or views expressed in the report.

Additional Disclaimer (for purpose of distribution in the United Kingdom)

This document is being distributed by Kim Eng Securities Limited, which is authorised and regulated by the Financial Services Authority and

is for Informational Purposes only.This document is not intended for distribution to anyone defined as a Retail Client under the Financial

Services and Markets Act 2000 within the UK. Any inclusion of a third party link is for the recipients convenience only, and that the firm does

not take any responsibility for its comments or accuracy, and that access to such links is at the individuals own risk. Nothing in this report

should be considered as constituting legal, accounting or tax advice, and that for accurate guidance recipients should consult with their own

independent tax advisers.

Published / Printed by

Maybank Investment Bank Berhad (15938-H)

(A Participating Organisation of Bursa Malaysia Securities Berhad) 33rd Floor, Menara Maybank, 100 Jalan Tun Perak, 50050 Kuala Lumpur

Tel: (603) 2059 1888; Fax: (603) 2078 4194 Stockbroking Business:

Level 8, Tower C, Dataran Maybank, No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888; Fax: (603) 2282 5136

http://www.maybank-ib.com