maybank ib research - xinhua08.comupload.xinhua08.com/2011/1024/1319433749190.pdf · maybank ib...

TRANSCRIPT

Initiating Coverage 24 October 2011

Maybank IB Research PP16832/01/2012 (029059)

Sugar is what keeps the body going

Steady eddy. MSM Malaysia Holdings (“MSM”) is Malaysia’s leading

sugar refinery and distributor. We believe it is well positioned to exploit

Malaysia’s insatiable demand for sugar due to its scale, superior

product quality and cost efficiency. We initiate with a HOLD, with a

target price of RM4.85/share based on DDM.

Stable growth, low risk, and cash cow. Sugar consumption is directly

correlated to population growth and diet, and it has grown by 4.1%

CAGR for the past 20 years. MSM is a staunch disciple of the cost plus

approach business model, which is low risk in nature. It has achieved

efficiency gains and reduced unit costs, evident in its widening profit

margin. Virtually debt free, and generates significant free cash flow, we

think this is a stellar inflation beating, defensive stock.

Three-pronged growth strategy. (1) Organic growth – boost volumes

on higher utilisation rate, efficiency enhancements and facility

expansion; (2) grow the export business by focusing on product quality

complimented with competitive bidding; and (3) strategic acquisition of

a third party. Furthermore, MSM is extracting structural fixed cost

reductions from the synergies of business consolidation.

The FELDA connection. FELDA is the de facto master of Malaysian

agriculture, with a full fledge infrastructure and logistics chain across

the world. Its political clout is substantial, and this may be beneficial for

MSM’s trade negotiations and raw sugar procurement.

Upcoming raw sugar contract expiry to impact sentiment.

Domestic raw sugar is purchased on a 3-year long term contract. The

current price of 17.5 US cents/lb expires at the end of the year; MSM is

certain to pay higher prices as the current sugar prices are hovering

around 27.0 US cents/lb. The ability for MSM to raise its selling price is

a concern as domestic sugar is a price controlled item.

DDM, peer comparison suggests RM4.75-4.83/share. Based on

DDM, MSM is worth RM4.83/share, and RM4.75/share based on 10x

2012 PER – which is the average long-term PER for sugar refineries.

MSM is highly cash generative, with an expected cashflow yield of

12.3%, 10.6% and 9.6% in 2011-13F respectively, and it can fund its

capex requirements in 2012-13 entirely from its retained earnings.

MSM: Summary earnings table

FYE Dec (RM m) 2009A 2010A 2011E 2012E 2013E

Revenue 1,643.6 2,168.6 2,138.3 2,159.1 2,202.3

EBITDA 305.6 387.1 458.3 504.8 545.4

Reported Net Profit 237.3 232.9 283.2 324.9 354.7

Recurring Net Profit 228.5 253.4 303.7 334.1 354.7

Recurring Basic EPS (Sen) 32.5 36.0 43.2 47.5 50.5

DPS - net (Sen) 27.3 26.8 17.2 19.8 21.6

PER 15.4 13.8 11.6 10.5 9.9

EV/EBITDA (x) 11.4 9.4 8.1 7.1 6.5

Dividend Yield - net (%) 5.5 5.4 3.5 4.0 4.3 Net Gearing (%) cash 9.2 12.9 5.7 2.0

ROE (%) 45.2% 24.7% 19.0% 19.7% 19.7% Consensus (RM m) n.a. n.a. 273.1 293.8 320.5

Source: Maybank-IB

MSM Malaysia Holdings Hold (new)

Share price: RM5.00 Target price: RM4.85 (new)

Wong Chew Hann, CA [email protected] (603) 2297 8692 Chai Li Shin [email protected] (603) 2297 8684

Description: Leading sugar refiner and distributor in Malaysia. Information: Ticker: MSM MK Shares Issued (m): 703.0 Market Cap (RM m): 3,514.9 3-mth Avg Daily Volume (m): 1.65 KLCI: 1,438.83 Major Shareholders: % Felda Group 54.0 Koperasi Permodalan Felda 20.0 EPF 6.3

Price Performance: 52-week High/Low RM6.1/RM3.5

1-mth 3-mth 6-mth 1-yr YTD 0.6 - - - -

Price Chart (RM5)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jun-11 Jul-11 Aug-11 Aug-11 Sep-11 Oct-11

MSM MK Equity

Description: Leading sugar refiner and distributor in

MSM Malaysia Holdings Berhad

Page 2 of 21

Table of contents

Page

Investment summary 3

Introduction 4

Sugar is what keeps the body going 6

Competitive Advantages 7

How does MSM stack up against Tradewinds 9

Key Risks 10

What if GOM opens up the market and removes subsidies? 12

Valuation 13

Earnings forecast 14

Sensitivity analysis 15

Financials 16

Appendix

I. Sugar refining process chart 19

MSM Malaysia Holdings Berhad

Page 3 of 21

Investment Summary

Introduction. MSM Malaysia Holdings Berhad is Malaysia’s leading

sugar refiner and distributor. It has two production facilities, in

Seberang Prai and Perlis. It operates under a regulated environment,

as sugar is a control item and only two players have the license to

operate in Malaysia. It thrives under the duopolistic environment and is

making positive inroads for its export markets.

Opportunities. The demand for sugar has been growing steadily at 20-

year CAGR of 4.0%, driven by population growth and increased sugar

consumption as part of the common diet. The annual sugar

consumption per capita in Malaysia is currently 48kg and it is expected

to rise going forward owing to the population’s sweet tooth tendencies.

Strengths. MSM’s key attractions are: (1) geographically well situated

infrastructure combined with a comprehensive logistic chain across the

country; (2) having large scale, vertically integrated manufacturing

facilities; and (3) secures attractively priced raw sugar on a long-term

contractual basis. These factors are proven beneficial as MSM’s cash

cost is among the globally most competitive.

Risks. MSM has no pricing power for domestic sugar, as any price

increase requires the Government of Malaysia’s (GOM) approval.

Therefore, it runs the risk of losing out in the event there is a fierce

upsurge in global raw sugar prices as it may not be able to recoup the

cost increase in the interim period that the GOM decides to raise

prices. Secondly, the GOM provides a subsidy for domestic sugar

(currently RM0.20/kg) and this is revised periodically.

Managing risks. MSM’s business model is relatively low risk; it

practices a cost plus approach for its domestic business and a back-to-

back transaction (buys raw sugar and sells refined sugar

simultaneously) for its export markets. In addition, its cost leadership,

strategically located facilities (lowers transportation and distribution

costs), and strong balance sheet should enable it to navigate the down-

cycles better relative to its peers.

What if the industry is liberised? MSM receives direct subsidy for

domestic sugar (RM0.20/kg). We think natural gas and electricity tariffs

are unsustainably low, and will be revised. Assuming these subsidies

are removed, the cost will rise by RM0.22/kg, we estimate, which is

10% higher from current selling price (RM2.30/kg). We expect per

capita consumption growth rate to ease somewhat but will not decline

(based on historical evidence). We think the removal of subsidies is not

a concern, provided that MSM is granted the freedom to price its

products accordingly.

Valuation. We believe the company is worth between RM4.75-4.83 per

share, using DDM valuation metric and PER comparison against global

peers. MSM, at the current share price of RM5.00, appears fairly

valued relative to the peer group’s long-term average PER of 10x, and

hence we advocate a HOLD call on the stock.

MSM Malaysia Holdings Berhad

Page 4 of 21

Introduction

Malayan Sugar Manufacturing Company Ltd. was incorporated in

1959 with the mission to reduce Malaysia’s dependence on imported

refined sugar. It was a private funding initiative by the Kuok Brothers

Sdn Bhd (later injected to PPB Group), Mitsui & Co and Nissin Sugar

Manufacturing. Prai (Penang) was chosen as the production site due to

its strategic geographical attributes.

Kilang Gula Felda Perlis Sdn. Bhd. (“KGFP”) was incorporated in

1971 as part of the national effort to diversify agricultural products and

bring development in the rural areas. KGFP was a 50:50 JV comprised

of the FELDA Group and PPB Group (Kuok Brothers), with its principal

business in the cultivation of a sugar plantation in Chuping, Perlis

(5,698 ha), sugar cane milling and refining raw sugar, also in Perlis.

FELDA takes all. In January 2010, FELDA bought out PPB Group’s

entire sugar business in Malaysia for RM1,335m and the combined

entity is now called MSM Malaysia Holdings Berhad (“MSM”). FELDA’s

intention was to gain a leading role in the industry. KGFP (on a

standalone basis) was the smallest player in the industry with 8.3%

market share, its growth prospects were limited and it faced a bleak

future due to its size and limited customer profile. With the acquisition,

MSM quickly rose to become the dominant sugar company in Malaysia.

Happy marriage. Post merger, management of both companies were

integrated, with MSM head (Mr. Chua Say Sin) taking the helm and

KGFP head (Mr. Amri Sahari) claiming the deputy CEO role. The day-

to-day business operations remain largely unchanged, and some

overlapping functions and duplications were removed from the system.

Among the synergies achieved are better pricing for raw materials and

products sold due to joint procurement and marketing efforts.

Simple business model. MSM’s business model is as follows:

procures raw sugar and sells refined sugar for a refining margin. The

domestic sugar operates in a cost plus business structure. For exported

sugar, the raw sugar procurement and refined sugar sales are done

back-to-back, thus eliminating inventory holding risk and securing

profits. MSM’s motivation is to continually achieve superior production

cost to expand profit margins and stay ahead of its competitors.

Domestic focused, with a zing for exports. The domestic market is

MSM’s primary market (and it will always be). Export market (local

export + export) is dynamic and hard to predict. “Local export” refers to

sale of refined sugar to manufacturing facilities in Malaysia which

subsequently export their finished products. In 2008, exports

constituted 13% of revenue; it then fell to 8% in 2009 and recovered to

16% in 2010. The management indicated that the export market is one

of the key sector earmarked for growth in the future.

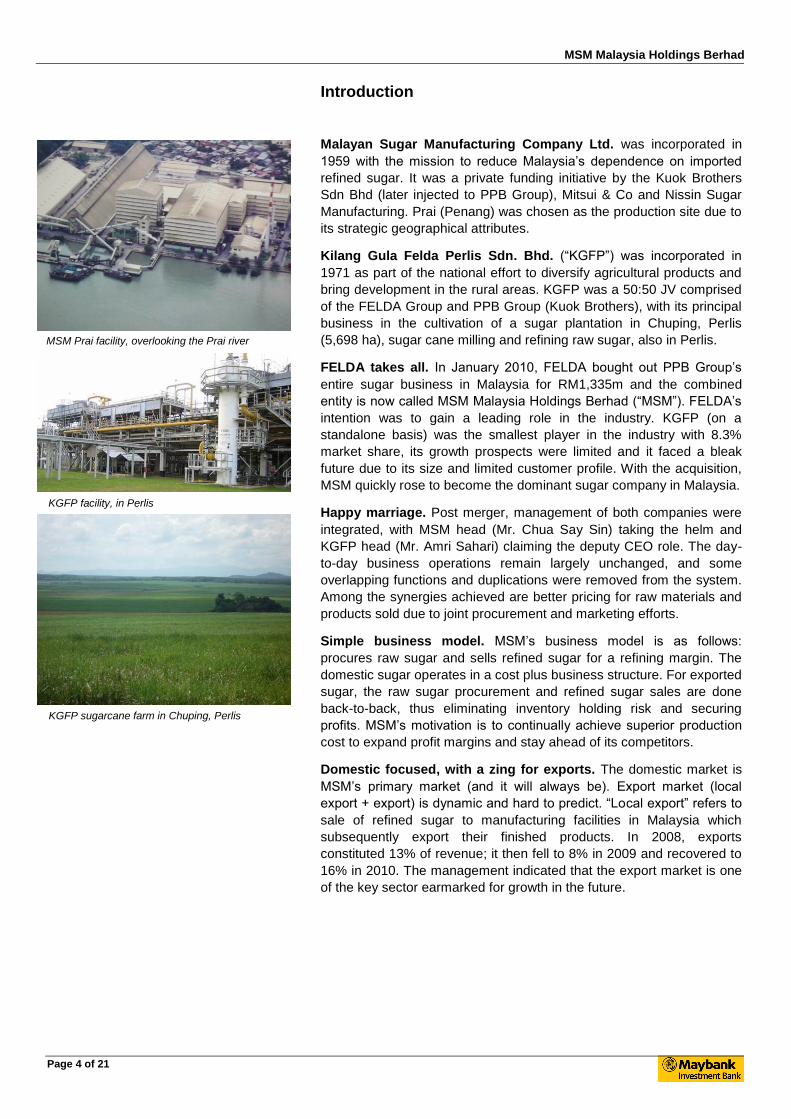

MSM Prai facility, overlooking the Prai river

KGFP facility, in Perlis

KGFP sugarcane farm in Chuping, Perlis

MSM Malaysia Holdings Berhad

Page 5 of 21

Revenue category Volume by category

86%

91%

84%

2%

2%

4%

11%

6%

12%

1% 1% 1%

75%

80%

85%

90%

95%

100%

2008 2009 2010

Domestic Local Export Export Molasses

-

200

400

600

800

1,000

2008 2009 2010

Domestic Local Export Export Molasses'000 mt

Sources: Company, Maybank IB Sources: Company, Maybank IB

Market leader. The sugar industry in Malaysia is a duopoly, and MSM

is the leader with roughly a 57% market share. MSM has been gaining

market share at the expense of its competitor, Tradewinds. We believe

MSM will continue to expand its market share due to its superior

infrastructure and available spare capacity.

Malaysia sugar industry market share

56.5% 57.0% 56.9% 56.9% 57.2% 57.6%

43.5% 43.0% 43.1% 43.1% 42.8% 42.4%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011F 2012F 2013F

Tradewinds MSM Group

Sources: Company, Tradewinds, Maybank-IB

MSM Malaysia Holdings Berhad

Page 6 of 21

Sugar is what keeps the body going

Sugar is a staple food for humans. While oil is the energy that drives

world economy, sugar is the energy that drives people. There is a direct

relationship between the rising population growth and rising living

standards versus sugar consumption – the average sugar consumption

relative to population growth in Malaysia for the past 25 years is 1.49

times. This is higher than the world’s correlation of 1.35 times.

Malaysia sugar consumption versus population growth World sugar consumption versus population growth

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1975 1980 1985 1990 1995 2000 2005 2010

Sugar consumption growth Population growth

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1975 1980 1985 1990 1995 2000 2005 2010

Sugar consumption growth Population growth

Sources: USDA, United Nations, Maybank IB Sources: USDA, United Nations, Maybank IB

Plenty of room to grow. Malaysia’s projected sugar consumption is

expected to grow by CAGR 4.2% over the next five years. This is

higher than the global average projection of 2.0%-2.5% p.a..

Malaysians have a sweet tooth; its per capita consumption in 2009 was

48kg, well above the global average of 31kg, and ranked the 22nd

highest in the world.

Malaysia sugar consumption projected growth

1,400

1,500

1,600

1,700

1,800

1,900

2011F 2012F 2013F 2014F 2015F 2016F

'000 mt

Source: Frost & Sullivan

Tremendous barriers to entry. The barriers to entry into the industry

are: (1) license and permit requirement from the GOM; (2) capital

intensity – at least RM100m to build a production facility and RM200m

working capital; (3) must have a comprehensive distribution network.

Competition is further complicated by the fact that domestic refined

sugar products are price-controlled. The element of competition is

primarily on the basis of product offerings, product quality, the ability to

meet timely delivery requirements and overall customer service.

Average sugar / population = 1.35

Average sugar / population = 1.49

CAGR 4.19%

MSM Malaysia Holdings Berhad

Page 7 of 21

MSM’s competitive advantages

Geographically well situated. MSM’s facilities are located: (1) next to

ports and sugar cane field – minimize feedstock distribution cost, (2)

near to customers in the industrial zone areas – lowers transportation

cost, (3) next to railway line and major highways – reduces

transportation time and provide just-in-time delivery; and (4) it has an

effective logistics infrastructure; which includes a range of storage,

packaging and distribution network across the country.

These attributes enables MSM to service its customers’ requirements

and provide a timely delivery of products. These are structural cost

advantages that cannot be easily replicated by others.

MSM facilities

Source: Company

Big scale operations with high utilization rate. MSM enjoys a high

level of operational and cost efficiency due to: (1) big scale refinery that

operates all year round; (2) benefits of state-of-the art equipments and

technology; and (3) high capacity utilization rate. Economies of scale

and high utilization rate are the key variable that determines

competitive unit cost of production. MSM possesses both these traits

as seen by the graphs overleaf; its refinery is among the largest in the

world and its utilization rate is around the 90%.

The biggest sugar refinery in the world is the Al-Khaleej in Dubai with a

capacity of 1,800k mt/year followed by MSM’s Prai and Central

Malaysian Sugar (belongs to Tradewind). Note that these three

refineries are raw sugar refineries (raw sugar → refined sugar). The

other sugar refineries in the list are smaller because they are integrated

sugar refineries (cane → raw sugar → refined sugar).

Critical requirements for a cost efficient sugar refinery in Malaysia

1. Next to port with a dry bulk terminal to

enable economical raw sugar imports 2. Next to the railway line for bulk

distribution 3. Close to major highway for ease of

transportation 4. Access to reliable energy source

(natural gas) for process heating

Sites that meets the criteria:

1. Penang

2. Port Klang

3. Johor Bahru

MSM Malaysia Holdings Berhad

Page 8 of 21

Sugarcane is harvested once a year. Therefore the refinery’s capacity

is designed to facilitate the expected annual crop harvest; it will be very

busy during harvest season and remain idle during off-season. A raw

sugar refinery on the other hand is able to function all year round as it

imports all its feedstock from Northern and Southern hemisphere, and

is not subjected to the changing of seasons.

Selected Asian sugar refinery capacity per annum MSM plant utilisation rate

1,821

960

600500 500

400

208150

0

500

1,000

1,500

2,000

Al Khaleej (Dubai)

MSM (Malaysia)

Central Sugar

(Malaysia)

Victoria (Australia)

Mitr Phol (Thailand)

PT Angels (Indonesia)

Victorias (Philippines)

KGFP (Malaysia)

'000 mt

74%77%

85%87%

90%

94%

60%

70%

80%

90%

100%

2008 2009 2010 2011F 2012F 2013F

Utilisation

Sources: Respective companies’ website, www.sugartech.com Sources: Company, Maybank-IB

Long-term supply contract. Approximately 49% of MSM’s imported

raw sugar is under a long-term supply contract (normally three years)

with various countries. This is beneficial to help secure a consistent

supply of raw sugar at fixed prices, and provides the forward visibility to

execute business effectively.

This forward procurement practice has been very beneficial to MSM as

it was able to procure raw sugar lower than the market price at 17.5 US

cents/lbs (9.8%-36.4% lower) as depicted in the graph below. The

current long-term contract is expiring at the end of this year, and all

parties (GOM, Malaysian sugar industry) are in the midst of securing

the next round of raw sugar procurement. (refer to Key Risk on page 10

for further commentary)

MSM’s raw sugar price versus World Sugar No. 11 price

10

15

20

25

30

35

2008 2009 2010 1Q-2011

US cents / lb MSM Price World Price (ICE)

Sources: Company, Bloomberg, Maybank-IB

14.9% discount

9.8% discount

10.0% discount

36.4% discount

MSM’s Prai refinery is Asia’s second largest refinery by capacity

Biggest sugar refinery in the world

MSM Malaysia Holdings Berhad

Page 9 of 21

How does MSM stack up against Tradewinds

Tradewinds is MSM’s competitor in Malaysia. It is a diversified

agriculture commodity group with interests in palm oil, rice, and sugar.

Its sugar division composes of Gula Padang Terap (Kedah) and Central

Sugars Refinery (Shah Alam).

No clear winner. The table below shows the financial performance

comparison between MSM and Tradewinds for 2008-10. There is no

clear winner between the two, as the performance gap is marginal.

MSM had historically outperformed Tradewinds in 2008-09. However,

Tradewinds was the winner in 2010 as depicted by the following KPIs:

(1) EBIT margin of 16.4% – a 0.5 ppt outperformance; and (2) unit cost

of RM1.90/kg – 2.1% lower.

It may be the simple fact that Tradewinds managed to purchase its raw

sugar at a lower price in 2010 as compared to MSM, and thus explains

its better unit cost performance. But we are unable to verify this due to

limited disclosure.

Summary of MSM and Tradewinds’ sugar division financial information

Tradewinds Sugar MSM

FYE December 2008 2009 2010 2008 2009 2010

Revenue inclusive of subsidies (RM m) 862.2 1,263.3 1,661.4 1,154.2 1,643.6 2,168.6

Total cost (RM m) (784.2) (1,121.6) (1,389.7) (982.3) (1,365.6) (1,824.7)

EBIT (RM m) 78.1 141.7 271.7 171.9 278.0 343.9

Volume produced (‘000 mt) 636,000 642,000 731,882 825,659 852,368 944,703

Total realized price of sugar (RM/kg) 1.36 1.97 2.27 1.40 1.93 2.30

Unit cost of production (RM/kg) 1.23 1.75 1.90 1.19 1.60 1.94

Unit margin (RM/kg) 0.12 0.22 0.37 0.21 0.33 0.36

EBIT % 9.1% 11.2% 16.4% 14.9% 16.9% 15.9%

Sources: Company, Tradewinds (sugar division only), Maybank IB

MSM will be the undisputed cost leader. We believe MSM’s unit cost

– excluding raw sugar, will reduce by 4%-6% in the next 2-3 years.

MSM plans to spend RM220m of Capex over the next two years to

expand, modernize and enhance operational efficiency (refer page 15:

Capex heavy for next two years).

We believe these efforts will greatly boost productivity and cost

efficiency. This will ensure MSM reclaim its cost leadership position and

stay ahead of the competitors.

MSM Malaysia Holdings Berhad

Page 10 of 21

Key risks

No pricing power. Freedom of pricing is where the complication lies as

sugar product prices are controlled by the GOM. Pursuant to the Price

Controls Act 1946, the Malaysian government has historically set price

ceilings for refined white sugar products, taking into account various

factors. The GOM does revise the ceiling price accordingly, but there is

always a lag between the implementation date and input cost rise –

especially when raw sugar exhibits extreme volatility (as the case now).

In January 2009, the GOM provided subsidy for domestic refined sugar

to keep prices low with the intention to curtail excessive food inflation.

The level of subsidy is revised periodically depending on market

dynamics. The current subsidy amount for domestic refined sugar is

RM0.20/kg (last revised on 10 May 2011). Note that exported sugar

and industrial customers do not qualify for this subsidy, and therefore

the weighted average subsidy is lower than RM0.20/kg.

MSM’s ASP and subsidies received

1.40 1.411.79

2.23

0.00

0.52

0.51

0.10

0.00

0.50

1.00

1.50

2.00

2.50

2008 2009 2010 2011F

RM / kg Subsidy ASP

Sources: Company, Maybank-IB

MSM unit profit margin

FYE December 2008 2009 2010 1Q-2011 2Q-2011

Core net income (RM’000) 123,649 228,485 253,399 88,747 50,848

Refined sugar produce (mt) 825,659 852,368 944,703 216,201 245,593

Core net income margin (RM/kg) 0.15 0.27 0.27 0.41 0.21

Average subsidy received No subsidy RM0.52/kg RM0.51/kg RM0.23/kg RM0.23/kg

Sources: Company, Maybank-IB

Subsidy mechanism. The subsidy is being handled by the Finance

Ministry, and is revised actively. The sugar players have provided

their annual budgets, and the GOM has ascertained an acceptable

level of margin for every refined sugar produced. Detail of the

methodology is private and management is tight lipped about it.

1.40

1.93

2.30 2.33

Realisation price

MSM Malaysia Holdings Berhad

Page 11 of 21

Raw sugar volatility. Raw sugar is a commodity, and is subject to

extreme price volatility due to a multitude of factors such as: (1) world

supply-demand dynamics; (2) weather conditions that may affect

positively or negatively for sugar cane harvest; (3) outbreak of pest and

diseases that may impact crops; and (4) artificial demand pent-up by

financial speculators.

The graph below shows the price movement of raw sugar for the past

decade. The average price for the period is 11.8 US cents/lb, the

lowest was 4.9 US cents/lb back in 2000, and the highest was 35.2 US

cents/lb recorded on 2 February 2011. The current spot price – at time

of print, hovers around 27.0 US cents/lb and the future price

showcases a backwardation in prices to around 22-23 US cents/lb.

World sugar price Sugar futures prices

-

5

10

15

20

25

30

35

40

45

2000 2001 2002 2003 2004 2004 2005 2006 2007 2008 2009 2010

USD cents /pound

20.0

21.0

22.0

23.0

24.0

25.0

26.0

27.0

28.0

Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14

US cents / lb

Sources: Bloomberg, Maybank-IB Sources: Bloomberg, Maybank-IB

Long-term contract expiry a concern. The current long-term

procurement contract for raw sugar is expiring by the end of 2011. The

current raw sugar price of 27.0 US cents/lb is significantly higher than

the previous rate of 17.5 US cents/lb (+57% higher). Refined sugar

prices have to increase by RM0.65/kg (+28% price hike) in order to fully

recoup the cost increase of roughly RM300m in 2012. This represents

98% of 2012’s net profits. It is therefore imperative that the GOM allows

MSM to price up the selling price as quickly as possible.

We think the government will be swift to raise prices. We think that

domestic sugar price will be raised on 1 Jan 2012 without any

hesitation by the government. This assumption is based on the

government’s consistent track record of raising sugar prices as per the

PEMANDU schedule of reducing subsidies on a six month rolling basis.

The last time domestic sugar price was raised was on 10 May 2011

and there were no objections by the rakyat.

Forex volatility. MSM’s revenue stream is majority in RM with roughly

88% exposure in 2010. MSM’s cost however, are majority USD (±88%)

as raw sugar price is quoted in USD and the majority of its capex is

also denominated in USD. It appears that MSM is at an advantage from

a stronger Ringgit against the USD. However, we have seen that when

US dollar weakens, it results in higher commodity prices which may

offset the impact of a stronger Ringgit.

World sugar supply deficit of 1.7 mmt due to draughts

World sugar supply deficit of 8.9 mmt due to draughts

Financial speculators

unwound positions

The sugar future exhibits a backwardation in price. The new LTC could potentially be locked in at 21-22 US cents/lbs

MSM Malaysia Holdings Berhad

Page 12 of 21

What if GOM opens the market and remove subsidies?

We simulate the scenario in the event the GOM liberates the industry

and (a) allow for another player to open a sugar refinery, (b) remove all

subsidies (refined sugar, natural gas, electricity), and (c) allow imports

of refined sugar with no import duties or tariffs imposed. In our opinion,

if this scenario materializes, the GOM will also allow freedom of pricing

and remove the price ceiling mechanism.

a. New player will find it difficult to compete. As explained in page

7, there are three suitable locations in Penisular Malaysia to build a

cost efficient sugar refinery: Penang, Port Klang and Johor Bahru.

We understand that Penang and Johor is full and does not have any

spare real estate. This leaves Port Klang as the only possible site.

Secondly, cost efficient refinery alone is not sufficient as it also

needs to compete on the basis of product offerings, product quality

(and consistency), the ability to meet timely delivery requirements

and overall customer service. A newcomer with no prior reputation

will find it difficult to penetrate the market as it takes time to

establish reputation and develop a good track record.

b. No subsidy, no problem. MSM receives RM0.20/kg of subsidy for

domestic sugar. We believe that the current “cheap” natural gas and

electricity tariff enjoyed by Malaysians are not sustainable and will

have to be revised upwards at some point of time. We estimate the

removal of the subsidies will add RM0.22/kg of cost. This represents

10% of the current selling price of RM2.30/kg. Put in another

perspective, each Malaysian will have to pay RM10.10 more per

year (on per capita consumption of 48kg) – hardly an encumbrance.

Competitive cost. The graph below shows the unit cash cost of

refining sugar from raw sugar for selected companies across the world.

MSM’s cost base of 28.6 US cents/lb is among the lowest and this

leads us to believe that MSM will be able to defend for itself in the

event the markets are opened up to international players.

Selected sugar refiner’s cash cost of refined sugar (2010)

28.6 28.3

31.7 32.3

39.4

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

40.0

MSM (Malaysia) Tradewinds

(Malaysia)

Khon Kaen

(Thailand)

Maryborough

(Australia)

Huletts (South

Africa)

US cent/lb

Sources: Company, respective Companies’ annual reports, Maybank-IB

MSM Malaysia Holdings Berhad

Page 13 of 21

Valuation

It’s all about the dividends. We believe MSM is valued between

RM4.83 and RM4.75 per share based on dividend discount model

(DDM) and comparative peer group PER valuation respectively. The

key attraction for this stock is its dividends, given its cash generative

prowess and modest capex requirements. Therefore, we favour the

DDM model. We use the peer group comparative PER as a secondary

method to cross check the valuation relative to the earnings cycle.

DDM methodology

Our DDM model uses dividend forecast for 2012 with cost of equity

(Ke) of 10.5%, beta (β) of 0.9x and a perpetual growth rate of 4.0%. We

use a payout ratio of 50% for FY2011-13; this is the minimum

guaranteed by the management. We derive an intrinsic value of

RM4.83/share. Should the payout ratio be revised upwards, it will

positively impact on valuations and our target price. We show our

estimated equity value for various payout ratios; with 50% as the base

case and 80% as the ceiling level.

Valuation matrix relative to dividend payout ratio

Payout ratio 50% 60% 70% 75% 80%

Target price (RM/share) 4.83 5.26 5.68 5.89 6.10

Source: Maybank-IB

Peer comparison PER

The graphs below shows the historical PER of seven global listed sugar

refineries. Filtering out the 2009 global financial crisis impact, the group

trading band is between 5x-15x with a mean of 9.5x. Assuming we use

the mid range of the trading band of 10.0x, we derive a fair value of

RM4.75/share. We think this is a fair multiple given that the industry is

at a mature stage and volumes are growing at a modest rate.

Selected sugar refiners combined PER

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011

(x)

Name of sugar refinery in the list = Maryborough Sugar, Delta Sugar, Roxas, Rogers

Sugars, Imperial Sugar, Uttam SugarMills

Sources: Company, respective Companies’ annual reports, Bloomberg, Maybank-IB

+1 sd = 12.4x

-1 sd = 6.6x

Mean = 9.5x

MSM Malaysia Holdings Berhad

Page 14 of 21

Earnings forecasts

Key Assumptions, FY10-13F

FYE December 2010A 2011F 2012F 2013F

Sugar demand growth (%) 10.8% (3.0%) 4.0% 4.0%

Average selling price (RM/kg) 1.79 2.10 2.10 2.10

Average subsidy (RM/kg) 0.51 0.23 0.23 0.23

Total realized sugar price (RM/kg) 2.30 2.33 2.33 2.33

Average raw sugar price (US cents/lb) 20.24 19.24 19.24 19.38

Dry bulk handysize (USD/day) 16,403 11,000 11,000 11,000

RM:US$ 3.22 2.99 2.88 2.88

Sources: Company, Maybank-IB

Little forward visibility, for now. Sugar dynamics are very volatile

and difficult to predict. Historically, global supply-demand balance

exerts the most influence on raw sugar price. Therefore, the key

assumptions listed above are subject to frequent changes depending

on the sugar supply-demand dynamics and commodity markets

volatility.

FY2011 result expectation

Our in-built assumptions. We assume volume shrinkage of 3.0%,

which is consistent to the volume reductions seen in the 1H2011 of

4.2% contraction. This is due to the discontinuation of subsidies to the

local-export industry, namely condensed milk producers. The cost

advantage is no longer visible and we conclude that this business will

be permanently lost. We believe the GOM will maintain both the sugar

selling price and sugar subsidy. We are imputing a constant raw sugar

price of 19 US cents/lb for the moment, pending news of the new long-

term contract rate by the GOM. We assume cash tax rate of 25%.

1H2011 reported net profit was RM139.6m (+11.3% YoY) on the back

of a 1.8% YoY turnover contraction due to 4.2% lower volumes. MSM

however enjoyed higher ASPs (+2.4% YoY) thanks the higher ceiling

price allowed by the government as well as expanding margins for the

export business. 1H PATAMI margins expanded by 1.5 pppt and met

46% of our full-year forecast.

● FY2012 and beyond

Sustained volume growth. We forecast an annual volume growth of

4.0% for 2012-13. This will raise capacity utilization to 90% in 2012. We

are imputing a constant total realized sugar price of RM2.33/kg, we

expect subsidy to reduce but the GOM to allow the industry to raise

sugar price accordingly. We maintain raw sugar price of 19 US cents/lb

for the moment, pending news of the new long-term contract rate by the

GOM. We assume cash tax rate of 25%.

Margin set to expand. Management guides that unit operating cost will

reduce stemming from plant modernization and higher energy efficient

process. We also think that MSM will enjoy greater economies of scale

as per the capacity expansion plans explained overleaf.

Definition of core net income:

Reported net income

+ forex translation (gain) / loss

+ non cash item FRS139 (gain) / loss

+ once-off events (gain) / loss

Core net income

MSM Malaysia Holdings Berhad

Page 15 of 21

Capex heavy for next two years. MSM is embarking on a capacity

expansion and facility modernization program and will be incurring

RM220m in the next two years. In addition, management is also

considering a strategic acquisition of a foreign sugar refinery for

approximately RM100m – this may take 2-3 years to materialise.

Capex profile

0

50

100

150

200

2008 2009 2010 2011F 2012F 2013F

Capacity Expansion Equipment and parts replacements Other RM million

52

64

18

64

184

114

Sources: Company, Maybank-IB

Sensitivity Analysis

Sensitivity analysis on core net income

RM million unless otherwise stated 2011F 2012F 2013F

1% change in volume 3.9 4.4 4.8

Impact on core net income 1.0% 1.0% 1.0%

1% change in raw sugar 12.6 12.7 12.9

Impact on core net income 3.2% 2.9% 2.7%

1% change in product price 22.5 23.4 24.3

Impact on core net income 5.8% 5.3% 5.1%

10% change in ship charter rates 19.6 19.7 20.5

Impact on core net income 5.0% 4.5% 4.3%

Source: Maybank IB

MSM Malaysia Holdings Berhad

Page 16 of 21

Financials

Robust profit margin. MSM’s EBIT margin for the past three years is

consistently among the best against the peer group. Another attribute is

MSM’s EBIT margin is the least volatile, a clear testimony to its world

class operations.

Selected companies’ EBIT margins

Company names 2008A 2009A 2010A

Maryborough sugar factory (Australia) n/a 1.6% 7.3%

Uttam Sugar Mills (India) n/a 18.5% 2.7%

Roxas Holdings (Philippines) 9.9% 6.1% 9.3%

Rogers Sugar (Canada) 13.6% 10.8% 9.8%

Padiberas Nasional (Malaysia) n/a 7.0% 7.5%

Average 11.7% 8.8% 7.3%

MSM 14.9% 16.9% 15.9%

Sources: Company, Bloomberg, Maybank-IB

Strong balance sheet. MSM’s is sitting in a net cash position of 9%

(as of 30 June 2011). This compares favorably against its peer average

of 27-517%.

Selected companies net debt / equity ratio (gearing)

MSM Mary-

borough Uttam Roxas

Padi-

beras

Rogers

Sugar

Imperial

Sugar

(9%) 27% 517% 138% 87% 75% 10%

Sources: Company, Bloomberg, Maybank-IB

Good working capital management. MSM’s average inventory

turnover of 84 days is on par with its global peers of 30-120 days. This

is respectable given that MSM imports 99% of its raw sugar whereas

some of the other companies benefit from being situated in close

vicinity to a sugar cane plantation. More importantly, MSM has been

successful in reducing its inventory turnover days consistently for the

past three years whereas others have not.

Selected companies’ inventory turnover days

Company names 2008A 2009A 2010A

Maryborough sugar factory (Australia) n/a 35.3 120.6

Delta Sugar (Egypt) 106.6 53.3 53.3

Roxas Holdings (Philippines) 81.0 98.9 110.2

Rogers Sugar (Canada) 55.7 50.5 30.9

Imperial Sugar (USA) 61.6 78.4 45.6

Padiberas Nasional 54.2 61.9 67.2

Average 71.8 63.1 71.3

MSM 131.7 96.2 84.2

Sources: Company, Bloomberg, Maybank-IB

MSM Malaysia Holdings Berhad

Page 17 of 21

Cash flush underscores huge dividend potential. MSM can finance

its capex requirements in 2012-13 via retained earnings, with no

necessity to raise debt or new equity. This means MSM’s dividend

paying capabilities are enormous, with a total cash flow yield (total cash

flow less dividend payments and less new equity issuance) of 12.3%,

10.6% and 9.6% for 2011-13F. Given its ample cash surplus projection

for 2011-13F based on its committed payout ratio of 50%, there is

scope for MSM to surprise positively on dividends.

MSM total cashflow yields

RM’000 unless otherwise stated 2011F 2012F 2013F

Total cashflow (pre dividend & new equity) 338,225 289,739 262,771

Dividend (assuming 50% payout) (161,427) (185,191) (202,198)

Cash surplus / (deficit) 176,797 104,548 60,572

Dividend yield at RM4.47/share 5.9% 6.8% 7.4%

Total cashflow yield at RM4.47/share 12.3% 10.6% 9.6%

Upside potential 6.4 ppt 3.8 ppt 2.2 ppt

Sources: Company, Maybank-IB

MSM Malaysia Holdings Berhad

Page 18 of 21

Financial statements

INCOME STATEMENT (RM m) BALANCE SHEET (RM m)

FY Dec 2010A 2011F 2012F 2013F FY Dec 2010A 2011F 2012F 2013F

Revenue 2,168.6 2,138.3 2,159.1 2,202.3 Net Fixed Assets 462.1 633.4 682.9 773.2

EBITDA 387.1 458.3 504.8 545.4 Other LT Assets 659.9 749.5 746.2 742.9

Depreciation & Amortisation (43.3) (45.1) (50.9) (63.9) Cash & ST Invts 87.1 263.8 368.4 428.9

EBIT 343.9 413.2 453.9 481.5 Other Current Assets 579.4 554.9 552.7 557.7

Net int (exp)/ Inc (8.6) (8.3) (8.4) (8.5) Total Assets 1,788.6 2,201.6 2,350.1 2,502.7

Associates & JV 0.0 0.0 0.0 0.0

Exceptional gain/ (loss) 0.0 0.0 0.0 0.0 ST Debt 217.0 467.0 467.0 467.0

Pretax profit 305.7 377.7 433.2 472.9 Other Current Liab 51.4 55.8 55.3 55.4

Tax (72.9) (94.4) (108.3) (118.2) LT Debt 0.0 0.0 0.0 0.0

Minority interest 0.0 0.0 0.0 0.0 Other LT Liab 111.6 105.7 105.7 105.7

Net profit 232.9 283.2 324.9 354.7 Shareholders Equity 1,408.5 1,573.2 1,722.2 1,874.7

Core Net profit 253.4 303.7 334.1 354.7 Minority Interest 0.0 0.0 0.0 0.0

Total Cap. & Liab 1,788.6 2,201.6 2,350.1 2,502.7

Sales Gth (%) 31.9% (1.4%) 1.0% 2.0%

hEBITDA Gth (%) 26.7% 18.4% 10.1% 8.0% Share Capital (m) 703.0 703.0 703.0 703.0

EBIT Gth (%) 23.7% 20.2% 9.8% 6.1% Gross Debt/(Cash) 217.0 467.0 467.0 467.0

Net profit Gth (%) (1.9%) 21.6% 14.7% 9.2% Net Debt/(Cash) 129.9 203.2 98.6 38.1

Effective Tax Rate (%) 23.8% 25.0% 25.0% 25.0% Working Capital 398.1 296.0 398.8 464.3

CASH FLOW (RM m) RATES & RATIOS

FY Dec 2010A 2011F 2012F 2013F FY Dec 2010A 2011F 2012F 2013F

Net Profit 232.9 283.2 324.9 354.7 EBITDA Margin (%) 17.9% 21.4% 23.4% 24.8%

Dep. & amort (43.3) (45.1) (50.9) (63.9) EBIT Margin (%) 15.9% 19.3% 21.0% 21.9%

Chg. In wkg cap (105.2) 22.5 1.8 (4.9) Net Profit Margin (%) 10.7% 13.2% 15.0% 16.1%

Other ope. CF (45.2) (4.5) (18.3) (28.9) Core Net Profit Margin (%) 11.7% 14.2% 15.5% 16.1%

Operating CF 134.3 354.6 367.6 393.3 ROE (%) 24.7% 19.0% 19.7% 19.7%

Net capex (25.2) (64.0) (97.1) (150.9) ROA (%) 17.6% 14.2% 14.3% 14.6%

Disposal/(purchase) 0.0 0.0 0.0 0.0 Dividend Cover (x) 1.1 0.6 0.6 0.6

Others 3.5 3.1 5.7 7.1 Interest Cover (x) 40.1 49.8 54.2 56.4

Investment CF (21.7) (60.9) (91.3) (143.9) Debtors Turn (days) 36.4 36.4 36.4 36.4

Net chg in debt 80.5 (384.7) 21.8 21.8 Creditors Turn (days) (7.2) (7.2) (7.2) (7.2)

Chg in other LT liab. (257.2) 267.8 (193.6) (210.7) Inventory Turn (days) 67.6 67.6 67.6 67.6

Oth. Financing CF 0.0 0.0 0.0 0.0 Current Ratio (x) 2.5 1.6 1.8 1.9

Financing cash flow (176.7) (116.9) (171.8) (188.9) Quick Ratio (x) 1.3 1.0 1.2 1.3

Net cash flow (64.1) 176.8 104.5 60.6 Net Debt/Equity (X) 0.1 0.1 0.1 0.0

Capex to Debt (%) (11.6%) (13.7%) (20.8%) (32.3%)

N.Cash/(Debt)PS (sen) 18.5 28.9 14.0 5.4

Opg CFPS (sen) 19.1 50.4 52.3 56.0

Free CFPS (sen) 15.5 41.3 38.5 34.5

Sources: Company, Maybank-IB

MSM Malaysia Holdings Berhad

Page 19 of 21

Appendix I: Sugar refining process chart

Source: Company

MSM Malaysia Holdings Berhad

Page 20 of 21

Source: Company

MSM Malaysia Holdings Berhad

Page 21 of 21

Definition of Ratings

Maybank Investment Bank Research uses the following rating system:

BUY Total return is expected to be above 10% in the next 12 months

HOLD Total return is expected to be between -5% to 10% in the next 12 months

SELL Total return is expected to be below -5% in the next 12 months

Applicability of Ratings The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not carry investment ratings as we do not actively follow developments in these companies.

Some common terms abbreviated in this report (where they appear): Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings

BV = Book Value FV = Fair Value PEG = PE Ratio To Growth

CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio

Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter

CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset

DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On Equity DPS = Dividend Per Share

NTA = Net Tangible Asset ROSF = Return On Shareholders’ Funds

EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital

EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year

EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date

EV = Enterprise Value PBT = Profit Before Tax

Disclaimer

This report is for information purposes only and under no circumstances is it to be considered or intended as an offer to sell or a solicitation of an offer to buy the securities referred to herein. Investors should note that income from such securities, if any, may fluctuate and that each security’s price or value may rise or fall. Opinions or recommendations contained herein are in form of technical ratings and fundamental ratings. Technical ratings may differ from fundamental ratings as technical valuations apply different methodologies and are purely based on price and volume-related information extracted from Bursa Malaysia Securities Berhad in the equity analysis. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. This report is not intended to provide personal investment advice and does not take into account the specific investment objectives, the financial situation and the particular needs of persons who may receive or read this report. Investors should therefore seek financial, legal and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently verified by Maybank Investment Bank Bhd and consequently no representation is made as to the accuracy or completeness of this report by Maybank Investment Bank Bhd and it should not be relied upon as such. Accordingly, no liability can be accepted for any direct, indirect or consequential losses or damages that may arise from the use or reliance of this report. Maybank Investment Bank Bhd, its affiliates and related companies and their officers, directors, associates, connected parties and/or employees may from time to time have positions or be materially interested in the securities referred to herein and may further act as market maker or may have assumed an underwriting commitment or deal with such securities and may also perform or seek to perform investment banking services, advisory and other services for or relating to those companies. Any information, opinions or recommendations contained herein are subject to change at any time, without prior notice.

This report may contain forward looking statements which are often but not always identified by the use of words such as “anticipate”, “believe”, “estimate”, “intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”, “should”, “could” or “might” occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions made and information currently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on these forward-looking statements. Maybank Investment Bank Bhd expressly disclaims any obligation to update or revise any such forward looking statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

This report is prepared for the use of Maybank Investment Bank Bhd's clients and may not be reproduced, altered in any way, transmitted to, copied or distributed to any other party in whole or in part in any form or manner without the prior express written consent of Maybank Investment Bank Bhd and Maybank Investment Bank Bhd accepts no liability whatsoever for the actions of third parties in this respect.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Published / Printed by

Maybank Investment Bank Berhad (15938-H)

(A Participating Organisation of Bursa Malaysia Securities Berhad) 33rd Floor, Menara Maybank, 100 Jalan Tun Perak, 50050 Kuala Lumpur

Tel: (603) 2059 1888; Fax: (603) 2078 4194 Stockbroking Business:

Level 8, Tower C, Dataran Maybank, No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888; Fax: (603) 2282 5136

http://www.maybank-ib.com