making sense of the building, construction and property market in the vuca* environment (*volatile,...

TRANSCRIPT

1 © BMI-BRSCU© BMI-BRSCU

TowardsMaking sense of the Building-, Construction- and Property-Industry

In the

VUCA ENVIRONMENT

Dr. Llewellyn B. LewisSF April 2013

THE STRATEGIC FORUMA place of assembly

for strategic conversations

THE STRATEGIC FORUMwww.strategicforum.co.za

BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

Reg. No. 2002/105109/23

•

BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCH

STRATEGY CONSULTING

UNIT cc

•

BMI•

BMI•

BMI•

BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCHSTRATEGY CONSULTINGUNIT cc

Reg. No. 2002/105109/23

•

BMI

Studium Ad Prosperandum

Voluntas in Conveniendum

BUILDING RESEARCH

STRATEGY CONSULTING

UNIT cc

•

BMI•

BMI•

BMI•

BMI•

BMI•

BMI•

2

Across every sector of society, decision makers are struggling with the complexity and velocity of change in an increasingly interdependent

world.

The context for decision-making has evolved,

and in many cases has been altered in revolutionary ways. In the decade ahead, our lives will be more intensely shaped by

transformative forces, including economic, environmental, geopolitical, societal and technological seismic shifts.

The signals are already apparent with the

rebalancing of the global economy, the presence of over seven billion people and the societal and environmental challenges linked

to both.

The resulting complexity threatens to overwhelm countries, companies, cultures and communities.

Klaus SchwabFounder and Executive ChairmanWorld Economic Forum

THE VUCA ENVIRONMENTwww.strategicforum.co.za

3

Central Bank Governor Gill Marcus

The aftermath of the global financial crisis of 2008

has years to run, according to Reserve Bank

governor Gill Marcus.

Referring to the recession in Europe and its

impact on the rest of the world, she said: “The depth of the crisis is so profound that, even if nothing gets worse, it’s going to take a very long time to come out of it.”

And she noted: “We’re not yet in a situation where nothing gets worse. I only hope that in

seven year’s time we can say we are okay.” (Business Report: 23 April 2013)

THE VUCA ENVIRONMENTwww.strategicforum.co.za

4

THE VUCA ENVIRONMENTwww.strategicforum.co.za

The VUCA environment.

The transition to the new normal is a sea change for the global economy. The full impact will take years, if not decades, to become clear.

In the meantime, the world will face much greater uncertainty, as conflicting views of the world play out on a day-to-day basis. As a result, companies need to plan for a VUCA environment during the transition that is now underway.

Volatility, Uncertainty, Complexity and Ambiguity will be the order of the day.

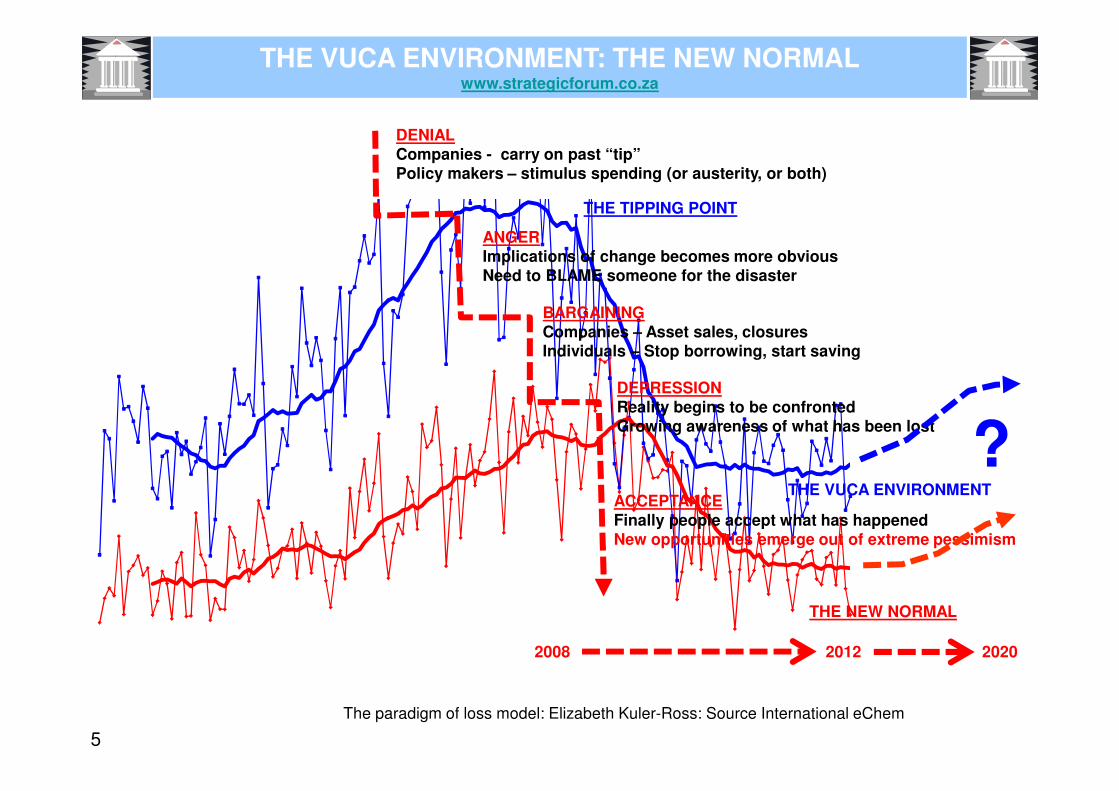

5

DENIALCompanies - carry on past “tip”Policy makers – stimulus spending (or austerity, or both)

ANGERImplications of change becomes more obviousNeed to BLAME someone for the disaster

BARGAININGCompanies – Asset sales, closuresIndividuals – Stop borrowing, start saving

DEPRESSIONReality begins to be confrontedGrowing awareness of what has been lost

ACCEPTANCEFinally people accept what has happenedNew opportunities emerge out of extreme pessimism

THE NEW NORMAL

The paradigm of loss model: Elizabeth Kuler-Ross: Source International eChem

THE TIPPING POINT

THE VUCA ENVIRONMENT

2008 2012 2020

?

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

6

The New Normal values . . . And Strategic implicationsUnilever is an excellent example of a company that already lives by New Normal values. But the application of these

values needs to constantly evolve, as this extract from the Guardian’s Sustainable Living blog illustrates:

In November 2010 Unilever announced its Sustainable Living Plan, which sets out its sustainability commitments

and targets for the next decade. This plan is not just central to the company’s business strategy but, in the words of CEO

Paul Polman, is a “new business model”. It aims to decouple business growth from environmental impact, so that

while the company increases in size it will reduce its total environmental footprint across the value chain.

“Growth at any cost is not viable,” said Polman. “We have to develop new ways of doing business which increase the positive social benefits arising from Unilever’s activities, while reducing our environmental impacts. We want to be sustainable in every sense of the word.”

Unilever’s plan has three distinctive features: It covers social and economic, as well as environmental challenges.

All Unilever’s products and brands are included, not just a few. It also covers the company’s entire value chain, from sourcing raw materials to consumer use of its products and their disposal. With

thousands of products that are used 2 billion times a day in more than 280 countries, this represents a massive undertaking.

The company has also set itself some stretching targets. By 2020 it aims to help more than a billion people take action to improve their health and wellbeing, halve the environmental footprint of its products, source 100% of its agricultural raw materials sustainably, and link more than half a million smallholder farmers and small-scale distributors to its supply chain.

Halving the greenhouse gas footprint of Unilever products across their life cycle by 2020 represents an equally

big challenge. Only 5% of these impacts come from manufacturing and transport. By far, the largest contribution comes from consumer use which accounts for 68% of the total, most of it caused by people showering, washing their hair and

doing laundry. To achieve its goal Unilever will have to provide consumers with more products that use less water.

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

7

Looking over the edge of a cliff (November 2012)

With the Marikana tragedy ushering in a period of industrial turmoil

which, aggravated by the lack of service delivery, can escalate into afull-blown South African version of the Arab Spring, we haverevised the probability yet again.

While we are keeping Premier League at 50%, we now have

amended the chances of a peaceful versus violent, anarchicdecline from 40:10 to 50:50 and therefore accord the Second

Division and Failed State scenarios each a 25% probability.(www.mindofafox.com

Clem Sunter

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

8

Looking over the edge of a cliffSince writing the column about South Africa looking over the edge of a cliff,

we have had plenty of responses from: "you should have said teeteringon the edge" to: "anywhere but South Africa if you're thinking of

investing in the continent of Africa.“

Nevertheless, the two comments we want to respond to are from

respected members of the political and business establishments. Neither

said it to us face to face; we read about their opinion in the media. Thefirst stated that there was no crisis and there was no cliff, basicallydismissing the idea of a 25% probability on a "Failed State". The

second one said that South Africa has always lurched from one extreme to

another, but we have always managed to right the ship and survive. Havea glass of nice red South African wine and think more hopefully about the

future!

We put the cat among the pigeons precisely because we believe thechances of a real crisis have risen dramatically (though we still give a50% probability to South Africa staying in the "Premier League").(www.mindofafox.com)

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

9

50%

25% 25%

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

10

Matamela Cyril

Ramaphosa was elected

as Deputy President of the African National

Congress at the ANC

National Conference in

Mangaung in December 2012.

Cyril is a flagBy Clem Sunter, originally published on News24.com on 28 November 2012

When I was told earlier this week that Cyril

Ramaphosa might be nominated as Jacob Zuma's

deputy and there might be a chance that the deputy position could be changed into that of Prime

Minister, something went ping in my mind. This

could signal a major shift in ANC strategy. Zumawould become the equivalent of non-executive chairman of the country with Cyril as CEO.

Cyril's nomination to a key ANC position would be a

very positive flag and would make the conference in December a much more important affair for the

immediate future of the country. Overnight, it would transform foreign perceptions of South Africa being on a downward slide to nowhere.Instead, people might even talk of a second miracle being close at hand - the one that has to take place in the economic sphere.

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

11

LegendAlert

WarningModerate

SustainableNo Information / Dependent Territory

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

12

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

13

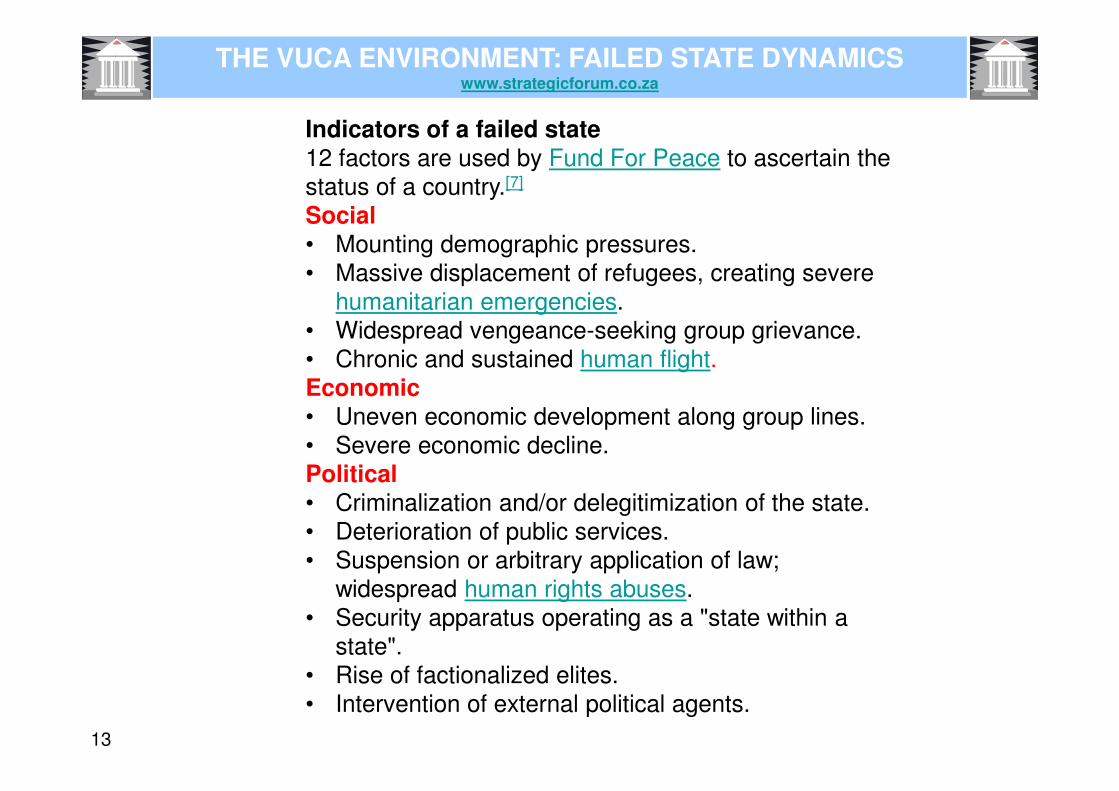

Indicators of a failed state12 factors are used by Fund For Peace to ascertain the status of a country.[7]

Social• Mounting demographic pressures.

• Massive displacement of refugees, creating severe

humanitarian emergencies.• Widespread vengeance-seeking group grievance.• Chronic and sustained human flight.

Economic• Uneven economic development along group lines.• Severe economic decline.Political• Criminalization and/or delegitimization of the state.• Deterioration of public services.

• Suspension or arbitrary application of law;

widespread human rights abuses.

• Security apparatus operating as a "state within a state".

• Rise of factionalized elites.• Intervention of external political agents.

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

14

There are some disquieting signs. State failure occurs along a continuum: dysfunctional institutions, popular protests (such as the regular service delivery

protests), illegal and often violent strikes and the evident growing alienation of young, urban blacks, who face a lifetime of unemployment.

There are other danger signals of threats to key institutions: cadre deployment, which has already played havoc with the efficient running of the government in all spheres; the weakness of parliamentary oversight; and the reluctance to answer

probing parliamentary questions. The list of manifestations of a reluctance to heed

the constitutional requirement of transparency is long.

The quest for hegemonic control of all the levers of power has gone far. Increasingly, independent sources of information will be shackled, with

consequences for the freedom of the press. Obstreperous civil society organisations will feel the heat — remember: a strong civil society is one of the best guarantors of a democratic political system. Our democratic institutions

have survived, but longer-term threats are apparent. Endemic corruption is having a corrosive effect. Whether Planning Minister Trevor Manuel’s stirring calls

for public servants to mend their ways will have any effect is debatable. (David Welsh, retired Professor of Political Science; Paul Hoffman, Director, Institute for Accountability in Southern Africa; Business Day, 7 March 2013)

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

15

While it is true that the complex of factors that lead to the failed state mutate into a vicious cycle, there is nothing inevitable about failure. But strong corrective

measures are required and those require strong leadership, which is precisely what we lack. The ANC is faction-ridden and its alliance with the South African

Communist Party and Congress of South African Trade Unions makes it difficult to

take decisive steps.

Many African nationalist parties begin to fragment after 20-25 years in office. The period of fragmentation is also a time of huge danger to democratic

institutions, as threatened politicians flail about in search of scapegoats and other

imagined causes.

Of the 10 countries least likely to fail, only three come from the English-speaking

world — New Zealand, Canada and Australia. South Africa at present ranks a lowly 66 and falling, but stands well away from the tail-enders, Somalia, South Sudan, the Democratic Republic of Congo and Pakistan, to name a

few.(David Welsh, retired Professor of Political Science; Paul Hoffman, Director,

Institute for Accountability in Southern Africa; Business Day, 7 March 2013)

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

16

There are four social indicators.

Demographic pressures, such as those created by disputes over the ownership

and occupancy of land, redistribution of land and environmental issues, such as access to water and food, count. So, too, the presence of refugees in the border

and urban areas of South Africa is considered, as are internal migrations. The internal displacement of people who live in squalor in informal settlements for long periods is regarded as a symptom of failure. A 'legacy of vengeance-seeking

group grievances', such as those harboured by locals against foreigners

(xenophobic attacks) and locals against Afrikaner farmers (farm murders), as well as nationalistic political rhetoric ('the land was stolen from us') feature.

Flight from the country under scrutiny, by its intellectuals and its middle class, is the last of the social factors. The shrinking size of the 'white' population and its

own demographic profile bear testimony to this factor.

(David Welsh, retired Professor of Political Science; Paul Hoffman, Director,

Institute for Accountability in Southern Africa; Business Day, 7 March 2013)

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

17

Then there are economic factors that are regarded as relevant —a high Gini co-efficient such as South Africa’s and disparity in the development of

groups. In short, high levels of inequality contribute to failure. Education levels and the state of the education system are vital to economic

success and are considered, together with the rate of economic decline of the country being assessed. Poverty, unemployment and inequality nurture failure while prosperity, full

employment and the achievement of equality in a sustainable fashion through

proper education and long-term job creation are the conditions for success.

Measures such as the infant mortality rate, gross national product, per-capita

income, devaluation of the currency, commodity prices, foreign investment, the size of the drug trade and, of course, the prevalence of corruption are relevant to

economic health.

There are six political indicators that bear mention:

the delegitimisation or criminalisation of the state; the progressive deterioration of

public services; the widespread violation of human rights; the security apparatus as a 'state within a state'; the rise of factionalised elites; and intervention of other

states and external factors.(David Welsh, retired Professor of Political Science; Paul Hoffman, Director, Institute for Accountability in Southern Africa; Business Day, 7 March 2013)

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

18

Overall, our picture is not a pretty one, and Sunter’s scenario-planning prognostication appears chillingly accurate.

The legitimacy of the state depends on the wholehearted embrace of its value

system as reflected in the constitutional dispensation in place.

Our constitution is sound, but it is constantly being undermined or hollowed out by the tenets of the 'national democratic revolution', which is being pursued by

those in the ANC who do not genuinely subscribe to the National Development

Plan embraced by the ANC in Mangaung.

Without genuine fealty to constitutionalism, our slide down the ratings is likely to continue.(David Welsh, retired Professor of Political Science; Paul

Hoffman, Director, Institute for Accountability in Southern Africa; Business Day, 7 March 2013)

THE VUCA ENVIRONMENT: FAILED STATE DYNAMICSwww.strategicforum.co.za

19

“WHATEVER you do, don’t employ or house anyone,"

said local farmers when Don Rush, a foreign industrialist,

bought his farm. "If you do, they won’t work and you’llnever get rid of them. Unions will torment you. You’ll

fund extra benefits. You’ll waste time and money in

the Commission for Conciliation, Mediation andArbitration. They’ll take some of your land. It’s a

nightmare.“

This, he explained, was why he would not give full-time

jobs or housing to workers encountered during a hike up

the escarpment. "Elsewhere," he said, "we co-operate

with workers. Here, we avoid them. Elsewhere, wethink about how to motivate and keep them; we

arrange medical, savings, housing, training and

pension schemes, even scholarships for their kids.Here we minimise employment.“ (Business Day, 6

March 2013)

Leon Louw,Executive Director of the Free Market Foundation.

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

20

Minister in the Presidency Trevor Manuel(Picture: Beeld)

It is time for government to take

responsibility for its actions, Minister in the Presidency Trevor Manuel said on

Wednesday.

"We [government] should no longer say

it's apartheid's fault," Manuel told

reporters at the government leadership summit in Pretoria.

"We should get up every morning and recognise we have responsibility. There

is no longer the Botha regime looking

over our shoulder, we are responsible

ourselves."

Manuel: Time to stop blaming apartheid

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

21

ZUMA: A mistake to stop blaming apartheid

Zuma said it was impossible to see complete change in just 20 years. The damage done by apartheid would be with the country for some time, he said.

"To suggest we cannot blame apartheid for what is

happening in our country now, I think is a mistake to

say the least.

"We don't need to indicate what it is apartheid did. The

fact that the country is two in one, you go to any city

there is a beautiful part and squatters on the other

side, this is not the making of democracy and we can't stop blaming those who caused it," said Zuma.

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

22

Presidency denies Zuma-Manuel clash over legacy of apartheid

"Stating that the apartheid legacy and impact still exist and will

linger on for a long time does not mean that the

president is saying that public servants should

use it to excuse laziness

and incompetence," spokesman Mac Maharajsaid in a statement. "The

point President Zuma

made is that it is impossible to reverse the

legacy of apartheid in only 20 years."

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

23

When Ramphele launched Agang earlier this year she said she intended to contest

the national elections next year.

She said South Africans she had been talking to were conscious that changing the

country would take time.

"People are resonating with Agang."

She said she was looking forward to the parliamentary process of getting to the

bottom of how the country got to this point.

Most people complained about housing, health and education.

"People feel they have been lied to about

what to expect," Ramphele said.

"They tell stories which are very sad."

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

24 © BMI-BRSCU

Available on Amazon.com

“This economic crisis

doesn’t represent the

cycle, it represents a

reset. It’s an emotional,

raw, social, economic

reset.” (General Electric

CEO Jeffrey Immelt)

“People who understand

that, will prosper; those

who don’t will be left

behind.”

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

25 © BMI-BRSCU

�The bubble was so big in the 1920s, that after it popped during the Great Depression, it would take 22 years for non-residential construction investment to regain its precrash peak and 24 years for real spending on residential construction to recover to its pre-crisis highs.

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

26 © BMI-BRSCU

Stage 1Hubris bornOf success

Stage 2Undisciplined

Pursuit of More

Stage 3Denial of Risk

and Peril

Stage 4Grasping for

Salvation

Stage 5Recovery and

Renewal

WELL FOUNDED HOPE

?

What will it take?

(Source: Based on Collins: How the Mighty Fall: 2009)

New mortgage loans and readvances by

THE NEW NORMAL ?

THE VUCA ENVIRONMENT: THE NEW NORMALwww.strategicforum.co.za

27 ©27© BMI-BRSCU

� It appears that the limits to growth have been

reached and the Industry is once again on the

cusp of change and standing on the burning platform. � It is a time of discomfort with a real danger of

strategic drift. It means gradual demise for the

industry or quantum change back to its potential

growth rate.

� It is the time to challenge old mindsets,

assumptions and established industry recipesand to expose paradigm blind spots. Only then

can reinvention and the required growth be achieved.

THE VUCA ENVIRONMENTwww.strategicforum.co.za

28

THE VUCA ENVIRONMENT: THE NDPwww.strategicforum.co.za

29

THE VUCA ENVIRONMENT: THE NDPwww.strategicforum.co.za

30

In the past 18 months the South African economy continued to function significantly below full capacity, although in a number of areas bottlenecks visibly inhibited economic progress. The National Planning Commission released a vision statement and development plan for the country in November 2011, targeting the elimination of poverty and reduction of inequality by 2030 through appropriate changes, hard work, leadership and unity. Having identified the key developmental challenges facing the country and its people, the commission developed a plan focusing on

– the creation of jobs; – improving South Africa’s infrastructure; – appropriate transition to a low-carbon economy; – an inclusive and integrated rural economy; – reversing the spatial effects of apartheid; – improving the quality of education, training and innovation; – providing quality healthcare for all; – social protection; – building safer communities; – reforming the public service to build a capable state; – eliminating corruption; and – transforming society and uniting the country.

Addressing the infrastructure bottlenecks was recognised as of particular importance. In 2011, to ensure timeous and effective implementation in this area, Cabinet created the Presidential Infrastructure Co-ordinating Commission, chaired by the President and including half the members of Cabinet, the nine provincial premiers, and the mayors of the metropolitan areas. The President underlined the need for speeding up the capital programmes of the public sector in his State of the Nation address to Parliament early in 2012, when he unveiled the government’s infrastructure development programme. (SARB, Annual Economic Report: 2012)

THE VUCA ENVIRONMENT: THE NDPwww.strategicforum.co.za

31

Thami Mazwai, resident executive, Wits Business School,and also consults on small business and enterprise development.

In our February Newsletter we focus on the vexed question of Infrastructure spend.

This has become a burning issue of National importance, to the extent that Thami Mazwai (Resident Executive at the

Wits Business School) called for a national day of prayer to rid SA of the anger that, arguably, is the cause of the violence that regularly shocks SA. But, says Mazwai, it

should not only be about the anger, it must also be about the

offerings in the Presidential Infrastructure Coordination Commission.

He goes on to state that the national infrastructure rollout

programme, worth a wopping R4 Trillion, can create viable

and vibrant businesses in black communities. This will reduce the anger; people will feel their areas are a priority on the

agenda.

The BMI-BRSCU Strategic Forum has consistently

maintained that the Infrastructure programme, coupled with Affordable and RDP housing could usher in the next economic miracle in SA.

THE VUCA ENVIRONMENT: THE NDPwww.strategicforum.co.za

32

(Source: WEF: Global Risks 2013: Eighth Edition)

THE VUCA ENVIRONMENT: THE NDPwww.strategicforum.co.za

33 © BMI-BRSCU

BMI Est Q4 REV % Change GFCF BMI FC % Change MAT FC (DEC) % Change GFCF MAT FC BMI FC % Change GFCF MAT FC

PRIVATE RESIDENTIAL 2010 2011 2011 2011 2012 2012 2012 MAT FC 2012 Q4 2012 2013 2013 2013

- Dwelling-houses < 80 m2 1 835 2 297 25.15% 2 337 1.72% 2 337 1.72% 2 517 7.70%

- Dwelling-houses > 80 m2 12 323 13 372 8.51% 14 576 9.00% 14 576 9.00% 14 628 0.35%

- Townhouses & Flats 5 646 4 845 -14.18% 5 852 20.77% 5 852 20.77% 5 127 -12.37%

- Other (Incl. hotels & casinos) 1 209 863 -28.59% 305 -64.65% 305 -64.65% 944 209.30%

- Additions & alterations 7 392 7 871 6.48% 6 867 -12.75% 6 867 -12.75% 8 242 20.01%

TOTAL PRIVATE RESIDENTIAL 28 405 29 248 2.97% 29 937 2.35% 29 937 2.35% 31 457 5.08%

PUBLIC RESIDENTIAL

- Affordable Housing 18 028 25 316 40.43% 25 949 2.50% 25 949 2.50% 25 490 -1.77%

- General Government 3 762 2 940 -21.85% 4 210 43.20% 4 210 8.30% 3 643 -13.47%

- Public corporations 35 70 100.00% 117 67.14% 117 -60.97% 38 -67.83%

- Private Business Enterprises 8 460 7 882 -6.83% 9 039 14.69% 9 039 17.38% 9 378 3.74%

TOTAL PUBLIC RESIDENTIAL 30 284 36 208 19.56% 39 315 8.58% 39 315 8.58% 38 548 -1.95%

TOTAL RESIDENTIAL (Incl AH) 58 690 65 456 11.53% 69 252 5.80% 69 252 5.80% 70 005 1.09%

TOTAL GFCF RES (Excludes AH) 40 662 40 140 -1.28% 40 140 43 303 7.88% 43 303 7.88% 43 303 44 515 2.80% 44 515

PRIVATE NON-RESIDENTIAL

- Offices 3 623 2 352 -35.09% 3 150 33.97% 3 150 33.97% 2 285 -27.48%

- Shops 3 342 3 319 -0.69% 2 790 -15.93% 2 790 -15.93% 2 792 0.07%

- Industrial & warehouse 3 686 3 140 -14.81% 4 714 50.12% 4 714 50.12% 3 427 -27.30%

- Other 926 1 269 37.07% 1 060 -16.44% 1 060 -16.44% 1 142 7.73%

- Additions & Alterations 3 866 3 601 -6.84% 3 315 -7.96% 3 315 -7.96% 3 046 -8.10%

TOTAL PRIVATE NON-RESIDENTIAL 15 443 13 681 -11.41% 15 029 9.86% 15 029 9.86% 12 692 -15.55%

PUBLIC NON-RESIDENTIAL

- General Government 10 000 12 157 21.57% 15 094 24.16% 15 094 23.02% 14 896 -1.31%

- Public Corporations 3 785 5 617 48.40% 6 033 7.41% 6 033 -37.41% 3 497 -42.03%

- Private Business Enterprises 25 976 29 496 13.55% 28 773 -2.45% 28 773 6.16% 35 800 24.42%

TOTAL PUBLIC NON-RESIDENTIAL 39 761 47 270 18.88% 49 900 5.56% 49 900 5.56% 54 193 8.60%

TOTAL GFCF NON RESIDENTIAL 55 204 60 951 10.41% 60 951 64 929 6.53% 64 929 6.53% 64 929 66 885 3.01% 66 885

TOTAL GFCF RES AND NON RES 95 866 101 091 5.45% 101 091 108 232 7.06% 108 232 7.06% 111 401 2.93%

- Unrecorded Res Additions and Alterations 28 664 28 117 -1.91% 26 629 -5.29% 26 629 -5.29% 25 931 -2.62%

- Unrecorded Non Res Additions and Alterations 4 119 4 046 -1.79% 3 532 -12.69% 3 532 -12.69% 3 246 -8.10%

TOTAL UNRECORDED ADD'S & ALT'S 32 783 32 163 -1.89% 30 161 -6.22% 30 161 -6.22% 29 177 -3.26%

TOTAL INVESTMENT IN BUILDING 146 677 158 570 8.11% 164 342 3.64% 164 342 3.64% 166 068 1.05%

BC as % of Total Investment in Building 29.89% 27.07% 27.36% 27.36% 26.58%

Private Sector as % of Total Investment in Building 52.25% 47.36% 45.71% 45.71% 44.15%

CONSTRUCTION

47 909 59 078 23.31% 68 022 15.14% 68 022 5.00% 72 608 6.74%

85 436 91 483 7.08% 90 912 -0.62% 90 912 4.00% 88 975 -2.13%

24 891 25 817 3.72% 26 838 3.95% 26 838 6.25% 28 833 7.43%

TOTAL INVESTMENT IN CONSTRUCTION 158 236 176 378 11.47% 176 378 185 772 5.33% 185 772 5.00% 185 772 190 416 2.50% 190 416

TOTAL INV IN BLDNG AND CONSTR 304 913 334 948 9.85% 350 114 4.53% 350 114 4.53% 294 004 356 484 1.82% 301 817

TOTAL GFCF CONSTRUCTION 158 236 185 772 185 772 185 772 190 416

TOTAL GFCF BLDNG AND CONSTR 304 913 350 114 350 114 350 114 356 484 356 484

* Res GFCF excludes Affordable Housing 47.34% 46.94%

* Non Res GFCF includes Public Sector 52.66% 53.06%

** Stats SA

*** StatsSA and BMI-BRSCU Workings

Source: BMI-BRSCU

SHORTTERM OUTLOOK FOR THE BUILDING & CONSTR INDUSTRY: 2012: R*MILLION (CURRENT VALUE)

- General government

- Public corporations

- Private Business Enterprises

34

(R MILLION) (R MILLION)Listed Property (Market Cap) Formal Empl in Bldng & Constr

Mortgage Advances Land included

Urban Housing Backlog

Mortgages Outstanding

Land included

Inv in Affordable Housing Investment in Building

4.64% 29.70%

Government Budget Gross Fixed Capital Formation

29.75% 18.47%

33.57%

Transfer Duty Investment in Construction

13.58

Gross Domestic Product

R 41 351 249 025 R 164 342

R 1 637 879

Average Annual Housing Need (units)

R 2 995 530R 891 199 R 553 313

R 3 870 R 1 206 460 R 185 772

(Copyright) BMI-BRSCU

2 819 535

R 253 461

R 1 064 971

Investment in Infrastructure (3 years)

(R MILLION)

R 5 082 588R 210 997

THE ROLE OF BUILDING, CONSTRUCTION AND PROPERTY IN THE ECONOMY: 2012

Residential Property (Units*Millilon)

Non Res Property (m2*million)

342

427 162

www.strategicforum.co.za

35

(R MILLION) (R MILLION)Listed Property (Market Cap) Formal Empl in Bldng & Constr

Mortgage Advances Land included

Urban Housing Backlog

Mortgages Outstanding

Land included

Inv in Affordable Housing Investment in Building

4.64% 29.70%

Government Budget Gross Fixed Capital Formation

29.75% 18.47%

33.57%

Transfer Duty Investment in Construction

13.58

Gross Domestic Product

R 41 351 249 025 R 164 342

R 1 637 879

Average Annual Housing Need (units)

R 2 995 530R 891 199 R 553 313

R 3 870 R 1 206 460 R 185 772

(Copyright) BMI-BRSCU

2 819 535

R 253 461

R 1 064 971

Investment in Infrastructure (3 years)

(R MILLION)

R 5 082 588R 210 997

THE ROLE OF BUILDING, CONSTRUCTION AND PROPERTY IN THE ECONOMY: 2012

Residential Property (Units*Millilon)

Non Res Property (m2*million)

342

427 162

www.strategicforum.co.za

“Public Investments or joint Private-

Public Investments that yielded even moderate real returns (say 5%

- 6%) would increase activity, cut

unemployment, generate more tax returns and mean lower long-term

debt.” (Joe Stiglitz: Freefall: 2010)

“Investing in infrastructure is an

engine for long-term economic growth, increasing GDP,

employment, household income, and exports,” the engineer’s society

said in its report. “The reverse is

also true -- without investing, infrastructure can become a drag

on the economy.” (Pres Obama:

Bloomberg.com: 19 March 2013)

36

(R MILLION) (R MILLION)Listed Property (Market Cap) Formal Empl in Bldng & Constr

Mortgage Advances Land included

Urban Housing Backlog

Mortgages Outstanding

Land included

Inv in Affordable Housing Investment in Building

4.64% 29.70%

Government Budget Gross Fixed Capital Formation

29.75% 18.47%

33.57%

Transfer Duty Investment in Construction

13.58

Gross Domestic Product

R 41 351 249 025 R 164 342

R 1 637 879

Average Annual Housing Need (units)

R 2 995 530R 891 199 R 553 313

R 3 870 R 1 206 460 R 185 772

(Copyright) BMI-BRSCU

2 819 535

R 253 461

R 1 064 971

Investment in Infrastructure (3 years)

(R MILLION)

R 5 082 588R 210 997

THE ROLE OF BUILDING, CONSTRUCTION AND PROPERTY IN THE ECONOMY: 2012

Residential Property (Units*Millilon)

Non Res Property (m2*million)

342

427 162

www.strategicforum.co.za

“Unless the Housing Market recovers, the Economy will

not recover.” (Warren Buffet, CNN,

4 October 2011)

It is estimated that for every R1 spent on infrastructure, R1.40 is added to a country’s gross domestic product.PPP’s are the ideal vehicle for funding the gaps in infrastructure in Africa. (Deloittes research, May 2011)

The UK Government plan to promote building. “It clearly has

recognised the need to boost house building, both to address

the housing crisis and to create jobs.” (Business Day, 22 November 2011)

37

-80%-70%-60%-50%-40%-30%-20%-10%0%10%20%30%40%50%60%70%80%90%100%110%120%130%

Go

ld b

oo

m

SA

SO

L I

I

SA

SO

L I

II

Au

ste

rity

pa

cka

ge

Ru

bic

on

sp

ee

ch

De

bt sta

nd

still

Eco

no

mic

re

cove

ry

Ma

nde

la's

re

lea

se

De

mo

cra

tic E

lectio

n

Tra

nsitio

n t

o D

em

ocra

cy

Cu

rren

cy c

olla

pse

Wo

rld

Tra

de

Ce

ntr

e

BN

G H

ou

sin

g P

rog

ram

me

Su

b P

rim

e C

risis

(N

CA

)

23

8 1

47

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Y/Y

Pe

rce

na

tag

e C

ha

ng

e

Defining Events

R M

illi

on

s (

Cu

rren

t V

alu

e)

Total Mortgage Loans and Readvances: 1979-2012 (Current Values) (Source: SARB, BMI-BRSCU Workings)

R233 Billion taken out of the system

in two years!

© BMI-BRSCU© BMI-BRSCU

The 2004 EARLY WARNINGS OF CHANGE had no impact on Industry Strategy.How did the Industry respond to the 2007 Sub-prime Crisis?

TOTAL MORTGAGE LOANS & RE-ADVANCES: 1979-2012www.strategicforum.co.za

38

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 00019

93/0

1

19

93/0

8

19

94/0

3

19

94/1

0

19

95/0

5

19

95/1

2

19

96/0

7

19

97/0

2

19

97/0

9

19

98/0

4

19

98/1

1

19

99/0

6

20

00/0

1

20

00/0

8

20

01/0

3

20

01/1

0

20

02/0

5

20

02/1

2

20

03/0

7

20

04/0

2

20

04/0

9

20

05/0

4

20

05/1

1

20

06/0

6

20

07/0

1

20

07/0

8

20

08/0

3

20

08/1

0

20

09/0

5

20

09/1

2

20

10/'0

7

20

11/'0

2

20

11/'0

9

20

12/'0

4

20

12/'1

1

R M

illi

on

s (

Cu

rre

nt

Va

lue

)

Total gross new mortgage loans and re-advances by Month: 1993- 2012 (December)(Source: SARB: KBP 2127M, BMI-BRSCU Workings)

Total gross new mortgage loans and re-advances 12 per. Mov. Avg. (Total gross new mortgage loans and re-advances )

2007= (2000)*548.4%

2012= (2000)*314,9%

2012= (2007)*57.4%

© BMI-BRSCU

www.strategicforum.co.za

The reduction in new mortgage advances following the introduction of the NCA in 2007 was very effective . . .

How did the Building Industry respond?

39

238147

235856

255510

259590

257484

257353

282204

300141

301592

441410

208488

0

100 000

200 000

300 000

400 000

500 000

600 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

R M

illi

on

s (

Cu

rre

nt a

nd

Co

ns

tan

t 2

01

2

Va

lue

s)

Total Mortgage Advances: 2002 - 2012 (Current Values)The Strategic Forum Scenarios: 2013-2020 (Constant 2012 Value)

(Source: SARB, BMI-BRSCU Workings)

High Road New York Scenario: 2012-2020

Higher Middle Road London Scenario: 2012-2020

Lower Middle Road Sao Paolo Scenario: 2012-2020

Low Road Harari Scenario: 2012-2020

Sao Paolo Scenario:2012-2020

Sao Paolo Scenariois Current

Most likely future

© BMI-BRSCU© BMI-BRSCU

R233 Billion decline in

only 2 years!

Under the Upper Middle Road it could take a

decade to get back to the 2007 level

www.strategicforum.co.za

40

“. . . . the market for new housing would be

affected by trends on the macro-economicfront, the state of household finances,consumer confidence and propertymarket- related factors.

“These factors will be reflected in new housingdemand and supply conditions, market activity,transaction volumes, price levels and the

demand for mortgage finance”.(Jacques du Toit, Bus. Report 22 April 2013)

www.strategicforum.co.za

41

STRUCTURAL SHIFT IN FINANCE: UNINTENDED CONSEQUENCES ? • Banks grow unsecured lending ahead of Home loans and asset

finance because unsecured lending is more profitable;• New regulations discourage banks from taking on long-term loans

like 20 year loans;• Global financiers believe this lowers one form of risk in the balance

sheets of banks, but asset finance, whether for homes or cars, is a healthier form of borrowing for consumers, because assets are usually productive;

• Unsecured lending is too easily used to finance consumption rather than anything that may offer a future return;

• What does worry is the declining prominence of mortgage lending. It will make home ownership more difficult and hurt fixed investment spending;

• That could have social and economic consequences as serious as the micro loan debacle of a decade ago. (Stuart Theobald, Business Day 16 July 2012)

www.strategicforum.co.za

42 © BMI-BRSCU

A recent survey of 8 000 Britons aged 20 to 45 found that more than three-quarters who don’t own property would like to, but 64% believe their chance of doing so is nil. (The Independent, 31 May 2011)

In South Africa some 80% own their homes, but home ownership is under serious threat.

www.strategicforum.co.za

43 © BMI-BRSCU

THE SA LIQUIDITY CYCLETHE REAL ECONOMY LAGS ABOUT 9 MONTHS BEHIND THE LIQUIDITY CYCLE

(Based on the Barings Liquidity Model : The Economist : 19 Nov. 1994)

��

��

��

��

��

��

��

��

CASHCASH

COINCIDE WITH ECONOMICUPSWING

COINCIDE WITH ECONOMICUPSWING

COINCIDE WITH ECONOMICDOWNSWING

COINCIDE WITH ECONOMICDOWNSWING

BONDSPROPERTYBONDSPROPERTY

EQUITIESPROPERTYEQUITIESPROPERTY

COMMODITIESCOMMODITIES

EQUITIESEQUITIES

BONDSBONDS

��

��

��

��

��

��

��

INVESTMENT CLIMATE

44

Equities (2) SA Listed Property (1) Bonds (3) Cash (4)

MTD 3.23% 0.99% 0.07% 0.43%

QTD 3.23% 0.99% 0.07% 0.43%

2012 23.68% 31.00% 13.73% 5.55%

0%

5%

10%

15%

20%

25%

30%

35%

Re

turn

%

RETURNS ON SA LISTED PROPERTY ASSET CLASSES: 31 FEB 2013

(Source: Catalyst Fund Managers; BMI-BRSCU Workings)

1. SA Listed Property Index2. All Share Index3. All Bond Index4. Cash

INVESTMENT CLIMATE

The traditional drivers for total

property returns remain intact.

The current income yield plus

prospect of income growth will

drive the total return over the

long term. (Catalyst Fund

Managers, Listed Property

Report, February 2013)

45

In 2011 economic agents exhibited preference for cash and deposits, as well as

fixed-interest securities relative to other financial instruments. Although such preference does

not reveal much about its demand- or supply-side origin, it shows the evolution of risk tolerance among agents. Credit extension was third in the rank as a preferred financial

instrument, in line with stricter lending criteria and a fragile demand for mortgage

funds. The latter’s persistence could hamper economic activity. (Source: SARB, Quarterly Bulletin, June 2012)

INVESTMENT CLIMATE

46 © BMI-BRSCU© BMI-BRSCU

There can be no return to high levels of employment and growth without finding a way of harnessing finance’s creative energies to allocate resources

and risk so effectively that it spurs and speeds economic growth.

We must never forget that credit, and the need for securitisation too, is at the heart of a modern financial system. (Gordon Brown: 2010: 109)

There is a compelling need for wide Stakeholder collaboration to address common problems.

INVESTMENT CLIMATE

47

-20%

-10%

0%

10%

20%

30%

40%

50%

Dem

ocra

tic E

lect

ion

Tra

nsiti

on to

De

mocr

acy

Curr

ency

Co

llapse

World

Tra

de

Ce

ntr

e

BN

G H

ousin

g P

rog

ram

me

Sub

Pri

me C

risi

s (N

CA

)

Socce

r W

orld C

up

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

19

93

/01

19

94

/01

19

95

/01

19

96

/01

19

97

/01

19

98

/01

19

99

/01

20

00

/01

20

01

/01

20

02

/01

20

03

/01

20

04

/01

20

05

/01

20

06

/01

20

07

/01

20

08

/01

20

09

/01

20

10

/'01

20

11

/'01

20

12

/'01

CU

M Q

/Q (

PR

EV

IOU

S Y

EA

R)

% C

HA

NG

E

Defining Events

R M

ILL

ION

S (

CU

RR

EN

T V

AL

UE

S)

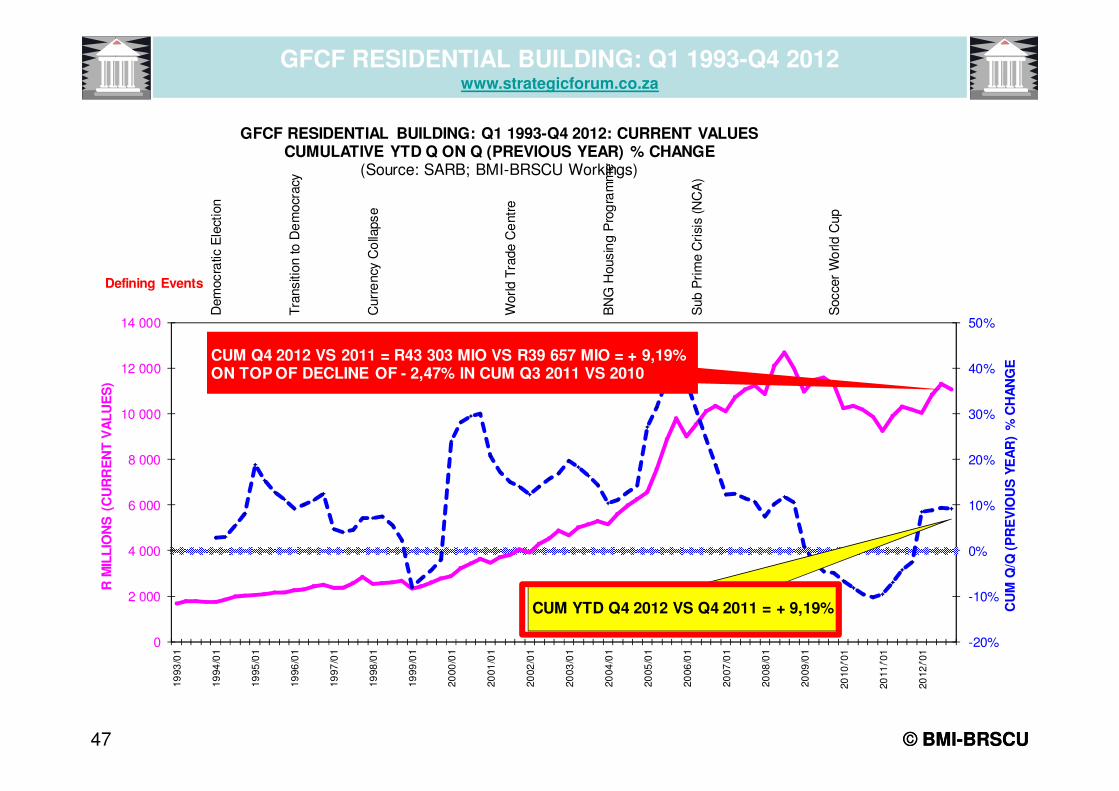

GFCF RESIDENTIAL BUILDING: Q1 1993-Q4 2012: CURRENT VALUESCUMULATIVE YTD Q ON Q (PREVIOUS YEAR) % CHANGE

(Source: SARB; BMI-BRSCU Workings)

CUM YTD Q4 2012 VS Q4 2011 = + 9,19%

CUM Q4 2012 VS 2011 = R43 303 MIO VS R39 657 MIO = + 9,19%ON TOP OF DECLINE OF - 2,47% IN CUM Q3 2011 VS 2010

© BMI-BRSCU© BMI-BRSCU

GFCF RESIDENTIAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

48

CumRes/Q

CUM Q/Q GFCF RESIDENTIAL 2012 10 043 20 891 32 223 43 303

CUM GFCF RESIDENTIAL 2013 10 318 21 342 32 866 44 515

CUM Q/Q % CHANGE 2013 VS 2012 2.74% 2.16% 2.00% 2.80%

CUM Q/Q % CHANGE 2012 VS 2011 8.51% 8.94% 9.30% 9.19%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

Cu

m Q

/Q P

erc

en

tag

e C

han

ge

R M

illio

ns

CUM Q/Q GFCF RESIDENTIAL 2013 VS 2012 (FC)(Source: SARB, BMI-BRSCU Workings)

MAT FORECAST

ACTUAL

GFCF RESIDENTIAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

49 © BMI-BRSCU© BMI-BRSCU

RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

4 000 000

4 500 000

5 000 000

5 500 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

R*1000 (Current Values)

BPP & BC Total Residential: 1993-2013 by month: R*1000 (Current Values) (Feb)(Source: StatsSA; BMI-BRSCU: BC Total RSA by Month and Type of Building1993-2008: TOTAL RES BC&BPP R)

BC TOTAL RESIDENTIAL: R*1000 BPP TOTAL RESIDENTIAL: R*1000

12 per. Mov. Avg. (BC TOTAL RESIDENTIAL: R*1000) 12 per. Mov. Avg. (BPP TOTAL RESIDENTIAL: R*1000)

50 © BMI-BRSCU© BMI-BRSCU

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cum Y/Y % Change: BPP & BC: Total Residential (Incl A&A): 1993-2013: R*1000 (Current Values) (Feb)

(Source: StatsSA; BMI-BRSCU: BC by Month and Type of Building: % CUM BC BY SEGM & MNTH: Chart 51(14))

% CUM BC BY SEGM& MNTH % CUM BPP BY SEGM& MNTH

12 per. Mov. Avg. (% CUM BC BY SEGM& MNTH) 12 per. Mov. Avg. (% CUM BPP BY SEGM& MNTH)

RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

51

Jan Feb March April May June July August Sept Oct Nov Dec

Res Total: YTD FC 2013: R*Mio 2142904 5101565 7667103 9962373 12554293 15124543 17978745 20779228 23545647 26443695 29612281 32257834

Res Total: YTD Actual 2012: R*Mio 1735721 4112309 6817332 8995254 11305286 13687835 16360216 19175476 21664074 24245294 27422358 29936556

Res Total: YTD FC 2013 vs 2012: % 23.46% 24.06% 12.46% 10.75% 11.05% 10.50% 9.89% 8.36% 8.69% 9.07% 7.99% 7.75%

0%

5%

10%

15%

20%

25%

30%

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

Pe

rcen

tag

e D

iffe

ren

ce:

YT

D F

C 2013

vs

201

2

R*1

00

0RESIDENTIAL TOTAL (INCL A&A): BC: YTD FC 2013 VS 2012 BY MONTH (FEB)

(Source: StatsSA, BMI-BRSCU Workings)

YTD FORECASTCUM ACTUAL

RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

52

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Dem

ocra

tic E

lect

ion

Tra

nsiti

on to

De

mocr

acy

Curr

ency

Co

llapse

World

Tra

de

Ce

ntr

e

BN

G H

ousin

g P

rog

ram

me

Sub

Pri

me C

risi

s

Socce

r W

orld C

up

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

19

93

/01

19

94

/01

19

95

/01

19

96

/01

19

97

/01

19

98

/01

19

99

/01

20

00

/01

20

01

/01

20

02

/01

20

03

/01

20

04

/01

20

05

/01

20

06

/01

20

07

/01

20

08

/01

20

09

/01

20

10

/'01

20

11

/'01

20

12

/'01

CU

M Y

TD

Q/Q

% C

HA

NG

E

Defining Events

R M

ILL

ION

S (

CU

RR

EN

T V

AL

UE

S)

GFCF NON RESIDENTIAL BUILDING: Q1 1993-Q4 2012: CURRENT VALUESCUMULATIVE YTD Q TO Q (PREVIOUS YEAR) PERCENTAGE CHANGE

(Source: SARB; BMI-BRSCU Workings)

CUM YTD Q4 2012 VS 2011 = + 8,70%

2012 VS 2011 = R64 929 MIO VS R59 735 Mio = + 8,70%ON TOP OF GROWTH OF + 8,21% IN 2011 VS 2010

© BMI-BRSCU© BMI-BRSCU

GFCF NON RESIDENTIAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

53

2012/'01 2012/'02 2012/'03 2012/'04

CUM GFCF NON RES BUILDING 2012 16 426 32 682 48 451 64 929

CUM GFCF NON RES BUILDING 2013 16246 32522 49113 66885

CUM Q/Q % CHANGE 2013 VS 2012 -1.10% -0.49% 1.37% 3.01%

CUM Q/Q % CHANGE 2012 VS 2011 10.01% 10.35% 9.53% 8.70%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Cu

m Q

/Q P

erc

en

tag

e C

han

ge

R M

illio

ns

CUM Q/Q GFCF NON RESIDENTIAL BUILDING 2013 VS 2012(Source: SARB, BMI-BRSCU Workings)

MAT FORECASTACTUAL

GFCF NON RESIDENTIAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

54 © BMI-BRSCU© BMI-BRSCU

NON RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

R*1000 (Current Values)

BPP & BC Total Non Residential: 1993-2013 by month: R*1000 (Current Values) (Feb)(Source: StatsSA; BMI-BRSCU: BC Total RSA by Month and Type of Building1993-2008: TOTAL NR BC&BPP R)

BC TOTAL NON RESIDENTIAL: R*1000 BPP TOTAL NON RESIDENTIAL: R*1000

12 per. Mov. Avg. (BC TOTAL NON RESIDENTIAL: R*1000) 12 per. Mov. Avg. (BPP TOTAL NON RESIDENTIAL: R*1000)

55 © BMI-BRSCU© BMI-BRSCU

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cum Y/Y % Change: BPP & BC: Total Non Residential (Incl A&A): 1993-2013: R*1000 (Current Values)(Feb)

(Source: StatsSA; BMI-BRSCU)

% CUM BC BY SEGM& MNTH % CUM BPP BY SEGM& MNTH

12 per. Mov. Avg. (% CUM BC BY SEGM& MNTH) 12 per. Mov. Avg. (% CUM BPP BY SEGM& MNTH)

NON RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

56

Jan Feb March April May June July August Sept Oct Nov Dec

NR Total:YTD FC 2013: R*Mio 679926 2576781 3698681 4745999 5858404 6895140 8005261 9045416 10230923 11386344 12624949 13630148

NR Total: YTD Actual 2012: R*Mio 839485 2043989 3223310 5267683 6742569 7682250 8539546 9661691 11500685 12283201 14040375 15029402

NR Total: YTD FC 2013 vs 2012: % -19.01% 26.07% 14.75% -9.90% -13.11% -10.25% -6.26% -6.38% -11.04% -7.30% -10.08% -9.31%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

16000000

Pe

rce

nta

ge

Dif

fere

nce

: Y

TD

FC

201

3 v

s 2

01

2

R*1

000

NON RES TOTAL (INCL A&A): BC: YTD FC 2013 VERSUS 2012 BY MONTH (FEB) (Source: StatsSA, BMI-BRSCU Workings)

YTD FORECASTCUM ACTUAL

NON RESIDENTIAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

57

Dem

ocra

tic E

lect

ion

Tra

nsiti

on to

De

mocr

acy

Curr

ency

Co

llapse

World

Tra

de

Ce

ntr

e

BN

G H

ousin

g P

rog

ram

me

Sub

Pri

me C

risi

s (N

CA

)

Socce

r W

orld C

up

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

5 000

10 000

15 000

20 000

25 000

30 000

19

93

/01

19

94

/01

19

95

/01

19

96

/01

19

97

/01

19

98

/01

19

99

/01

20

00

/01

20

01

/01

20

02

/01

20

03

/01

20

04

/01

20

05

/01

20

06

/01

20

07

/01

20

08

/01

20

09

/01

20

10

/'01

20

11

/'01

20

12

/'01

Defining events

Cu

m Y

TD

Q/Q

Perc

en

tag

e C

han

ge

R M

illio

ns (

Cu

rren

t V

alu

e)

GFCF Total Building by Quarter: Q1 1993 - Q4 2012: Current ValuesCumulative YTD Q/Q (Previous Year) % Change

(Source: SARB; BMI-BRSCU Workings)

CUM YTD Q4 2012 VS 2011 = + 8,89%

2012 VS 2011 = R108 232 MIO VS R99 392 MIO = + 8,89%ON TOP OF DECLINE OF - 0,02% IN 2011 VS 2010

© BMI-BRSCU© BMI-BRSCU

GFCF TOTAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

58

CumGFCF Q1

CumGFCF Q2

CumGFCF Q3

CumGFCF Q4

CUM Q/Q GFCF TOTAL BUILDING 2012 26 469 53 573 80 674 108 232

CUM GFCF TOTAL BUILDING 2013 26 564 53 865 81 979 111 401

CUM Q/Q % CHANGE 2013 VS 2012 0.36% 0.54% 1.62% 2.93%

CUM Q/Q % CHANGE 2012 VS 2011 9.44% 9.80% 9.44% 8.89%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

0

20 000

40 000

60 000

80 000

100 000

120 000

Cu

m Q

/Q P

erc

en

tag

e C

ha

ng

e

R M

illio

ns

CUM Q/Q GFCF TOTAL BUILDING 2013 VS 2012 (FC)(Source: SARB, BMI-BRSCU Workings)

MAT FORECAST

ACTUAL

GFCF TOTAL BUILDING: Q1 1993-Q4 2012www.strategicforum.co.za

59 © BMI-BRSCU© BMI-BRSCU

TOTAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

10 000 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

R*1000 (Current Values)

BPP & BC Total Building: 1993-2013 by month: R*1000 (Current Values) (Feb)(Source: StatsSA; BMI-BRSCU: BC Total RSA by Month and Type of Building1993-2008: TOTAL BLDNG BC&BPP R)

BC TOTAL BUILDING: R*1000 BPP TOTAL BUILDING: R*1000

12 per. Mov. Avg. (BC TOTAL BUILDING: R*1000) 12 per. Mov. Avg. (BPP TOTAL BUILDING: R*1000)

60 © BMI-BRSCU© BMI-BRSCU

-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cum Y/Y % Ch: BPP and BC: Total Building (Incl A&A): 1993-2013: R*1000 (Current Values) (Feb) (Source: StatsSA; BMI-BRSCU)

% CUM BC BY SEGM& MNTH % CUM BPP BY SEGM& MNTH

12 per. Mov. Avg. (% CUM BC BY SEGM& MNTH) 12 per. Mov. Avg. (% CUM BPP BY SEGM& MNTH)

TOTAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

61

Jan FebMarc

hApril May June July Aug Sept Oct Nov Dec

Res & NR Total: YTD FC 2013 2822830 7678346 11365784 14708371 18412697 22019683 25984006 29824644 33776569 37830038 42237230 45887983

Res & NR Total: YTD Actual 2012 2575206 6156298 10040642 14262937 18047855 21370085 24899762 28837167 33164759 36528495 41462733 44965958

Res & NR Total: % Difference YTD FC 2013 vs 2012 9.62% 24.72% 13.20% 3.12% 2.02% 3.04% 4.35% 3.42% 1.84% 3.56% 1.87% 2.05%

0%

5%

10%

15%

20%

25%

30%

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

45000000

50000000

R*1

000

RES & NON RES TOTAL (INCL A&A): BC: YTD FC 2013 VERSUS 2012 BY MONTH (FEB)(Source: StatsSA, BMI-BRSCU: Buildings Completed Total RSA; Chart BC57)

% D

iffe

ren

ce:

YT

D

Actu

al

2012 v

s Y

TD

Fo

recast

2013

CUM ACTUAL YTD FORECAST

TOTAL BPP & BC: 1994-2013 (FEB)www.strategicforum.co.za

62

THE INDUSTRY DASHBOARD: BPP & BC, CEMENT AND LUMBER SALES: 2010, 2011 & 2012

-40%

-30%

-20%

-10%

0%

10%

20%

Perc

en

tag

e

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Total Res BC Cum YTD % Change (m2) 9.85% 14.94% 7.38% 6.90% 7.00% 6.81% 7.25% 6.48% 7.54% 8.03% 7.08% 6.59%

Total Non Res BC Cum YTD % Change (m2) -30.93% 4.49% 3.21% -13.76%-18.44%-16.12%-12.06%-11.78%-15.08%-11.20%-13.21%-12.37%

Total BC Cum YTD % Change (m2) -3.17% 11.56% 6.12% -0.05% -1.75% -0.81% 1.10% 0.78% 0.26% 2.02% 0.72% 0.72%

Domestic Cement Sales (Tonnes) 2.45% 2.83% 1.40% 1.81% 2.26% 2.75% 4.05% 5.41% 6.90% 10.49% 11.39% 11.98%

Local Building Lumber Sales (m3) -0.75% -2.62% -6.22% -4.75% -3.75% -3.13% -2.71% -2.33% -2.08% -1.84% -1.65% -1.56%

Total Residential BPP (m2) 14.75% 11.39% -6.79% -4.93% -3.39% -5.95% -5.84% -4.03% -3.40% -0.60% 0.16% -0.07%

Total Non Residential BPP (m2) -33.37%-13.28%-17.16% -2.20% 0.09% 3.38% 4.33% 4.85% 1.64% -0.99% 2.14% 1.51%

Total Building BPP (m2) -3.83% 2.96% -9.87% -4.15% -2.37% -3.25% -2.97% -1.51% -1.91% -0.72% 0.76% 0.42%

Cumulative YTD Buildings Completed (BC), Domestic Cement Sales and Local Building Lumber Sales: % Change by Sector: January - Dec 2013

(Source: StatsSA; BMI-BRSCU Workings)

CUM ACTUAL

BMI-BRSCU Estimate of Cement Sales

Publication of Cement Statistics stopped on 3 April

2012 by Competition Commission. PPC withdrew

from providing statistics and C&CI disbanded and the

last statisices were provided on 3rd April 2013.

No further statistics will be provided.

63

-1 000 000

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Total Building: BC: 1993-2013: Net Building in the Pipeline (NBIP): by Month: R*1000 (Current Values) (Feb)

(Source: StatsSA, BMI-BRSCU: BC Total RSA by Month and Type of Building: NBIP (BPP-BC): Chart 81(14))

Total Building NBIP (BPP-BC) Total Building BC 12 per. Mov. Avg. (Total Building NBIP (BPP-BC)) 12 per. Mov. Avg. (Total Building BC)

© BMI-BRSCU© BMI-BRSCU

NET BUILDING IN THE PIPELINE: 1993-2013 (FEB)www.strategicforum.co.za

Total BC Trend-break occurred in mid 2006.

Recovery is on the way.

64

NET BUILDING IN THE PIPELINE: 1993-2013 (FEB)www.strategicforum.co.za

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

2 000 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Total Residential: 1993-2013: BC, Net Building in the Pipeline (NBIP): by month: 1993-2012: m2 (Feb)

(Source: StatsSA, BMI-BRSCU: BC Total RSA by Month and Type of Building: NBIP (BPP-BC): Chart 77(14))

Total Residential NBIP

Total Residential BC

Total Residential BPP

12 per. Mov. Avg. (Total Residential NBIP)

12 per. Mov. Avg. (Total Residential BC)

12 per. Mov. Avg. (Total Residential BPP)

NBIP = 70.4%*BC

NBIP = 45.5%*BC

NBIP = 42,10%*BC

65 © BMI-BRSCU© BMI-BRSCU

NET BUILDING IN THE PIPELINE: 1993-2013 (FEB)www.strategicforum.co.za

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

500 000

550 000

600 000

650 000

700 000

750 000

800 000

850 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Total Non Residential: 1993-2013: BC, Net Building in the Pipeline (NBIP): by Month: m2 (Feb)

(Source: StatsSA, BMI-BRSCU: BC Total RSA by Month and Type of Building: NBIP (BPP-BC): Chart 79(14))

NBIP Total Non Residential

BC Total Non Residential

BPP Total Non Residential

12 per. Mov. Avg. (NBIP Total Non Residential)

12 per. Mov. Avg. (BC Total Non Residential)

12 per. Mov. Avg. (BPP Total Non Residential)

NBIP = 76.4%*BC

NBIP = 42.8%*BC

NBIP = 45,13%*BC

66 © BMI-BRSCU© BMI-BRSCU

NET BUILDING IN THE PIPELINE: 1993-2013 (FEB)www.strategicforum.co.za

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

2 000 000

2 200 000

2 400 000

2 600 000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Total Building: BC: 1993-2013: Net Building in the Pipeline (NBIP): by Month: m2 (Feb)

(Source: StatsSA, BMI-BRSCU: BC Total RSA by Month and Type of Building: NBIP (BPP-BC): Chart 80(14))

Total Building NBIP (BPP-BC)

Total Building BC

Total Building BPP

12 per. Mov. Avg. (Total Building NBIP (BPP-BC))

12 per. Mov. Avg. (Total Building BC)

12 per. Mov. Avg. (Total Building BPP)

NBIP = 71.8%*BC

NBIP = 44%*BC

NBIP = 42.5%*BC

67 © BMI-BRSCU© BMI-BRSCU

% DIFFERENCE IN CUM Y/Y BC : ACTUAL 2012 VS 2011: DECwww.strategicforum.co.za

2.5

5%

-0.4

7%

1.5

6%

1.0

2%

1.0

6% 8.9

2%

20

.00

%

10

.89

% 20

.74

%

-69

.60

%

-64

.65

%

7.8

4%

21

.15

%

33

.97

%

-14

.38

%

-15

.93

%

42

.02

%

48

.25

%

-18

.70

%

-16

.66

%

15

.61

%

-16

.75

%

-12

.72

%

-20

.80

%

-7.9

6%

-11

.23

%

4.5

7%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

No

m2

R'0

00

No

m2

R'0

00

No

m2

R'0

00

m2

R'0

00

R'0

00

m2

R'0

00

m2

R'0

00

m2

R'0

00

m2

R'0

00

R'0

00

m2

R'0

00

m2

R'0

00

R'0

00

R'0

00

Dwellings <80m2

Dwellings >80m2

Flats and TH Other Total Office &Banking

Shopping Ind&WH Other Total A&ADwellings

A&A Other A&ATotalTotal

% Difference in Cumulative Y/Y BC: Cum Actual 2012 vs 2011 by Segment: Total RSA(Source: StatsSA, BMI-BRSCU: Buildings Completed Total RSA; Chart BC60)

68

0

903

2 805

1 105

45

1 467

10 026

1 627

45

3 493

21 516

463

499

1 128

201

549

2 853

1 140

5 438

12 272

5 688

754

40 231

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

PRIVATE RESIDENTIAL

Dwelling-houses < 80 m2

Dwelling-houses > 80 m2

Townhouses & Flats

Other (Incl. hotels & casinos)

Additions & alterations

PUBLIC RESIDENTIAL

Affordable Housing

Gene ral Government

Public corporations

Private Business Enterprises

TOTAL RESIDENTIAL

PRIVATE NON-RESIDENTIAL

Offices

Shops

Industrial & warehouse

Other

Additions & Alterations

PUBLIC NON-RESIDENTIAL

Gene ral Government

Public corporations

Private Business Enterprises

TOTAL NON RESIDENTIAL

Unrecorded Res Adds and Alts

Unrecorded Non Res Adds and Alts

GRAND TOTAL

INVESTMENT IN BUILDING BY SECTOR AND BY SEGMENT: 2012: M2*1000(TOTAL = 40 067 M2*1000)

(Source: SARB, StatsSA, MFA, BMI-BRSCU Workings)

© BMI-BRSCU© BMI-BRSCU

CURRENT REALITY OF INVESTMENT IN BUILDINGBY SECTOR AND SEGMENT: 2012

69 © BMI-BRSCU© BMI-BRSCU

THE ROLE OF AFFORDABLE HOUSING IN BUILDING: 2013-2020www.strategicforum.co.za

203588

193615

217348

252834

271219

220204

248850

226216

185225

214979

218381

214518

202930

198978

201962

206002

211152

217486

224011

203 5

88

193 6

15

217 3

48

252 8

34

271 2

19

220 2

04

248 8

50

226 2

16

185 2

25

214 9

79

218 3

81

251 1

38

288 8

09

332 1

30 381 9

50

410 5

96

441 3

91

474 4

95

498 2

20

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

0

100 000

200 000

300 000

400 000

500 000

600 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

AN

NU

AL

HO

US

ING

BA

KL

OG

(U

NIT

S)

AN

NU

AL

HO

US

ING

DE

LIV

ER

Y (

UN

ITS

)

AFFORDABLE HOUSING DELIVERY AND BACKLOG: 2002-2012LOWER MIDDLE ROAD SOYUZ AND HIGH ROAD COLUMBUS SCENARIO: 2013-2020

(Source: StatsSA and BMI-BRSCU Workings)

70 © BMI-BRSCU© BMI-BRSCU

THE ROLE OF AFFORDABLE HOUSING IN BUILDING: 2013-2020www.strategicforum.co.za

203588

193615

217348

252834

271219

220204

248850

226216

185225

214979

218381

214518

202930

198978

201962

206002

211152

217486

224011

203 5

88

193 6

15

217 3

48

252 8

34

271 2

19

220 2

04

248 8

50

226 2

16

185 2

25

214 9

79

218 3

81

251 1

38

288 8

09

332 1

30 381 9

50

410 5

96

441 3

91

474 4

95

498 2

20

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

0

100 000

200 000

300 000

400 000

500 000

600 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

AN

NU

AL

HO

US

ING

BA

KL

OG

(U

NIT

S)

AN

NU

AL

HO

US

ING

DE

LIV

ER

Y (

UN

ITS

)

AFFORDABLE HOUSING DELIVERY AND BACKLOG: 2002-2012LOWER MIDDLE ROAD SOYUZ AND HIGH ROAD COLUMBUS SCENARIO: 2013-2020

(Source: StatsSA and BMI-BRSCU Workings)

If 3,08 Million houses are built in next 8 years

Backlog reduced to I,32 million by 2020.

The target must be the eradication of all

slums, or informal settlements, by 2025. For

this to happen, some 500 000 new units a year must become available.

71

28 8

14

32 5

32

33 9

17

37 7

73

47 0

42

60 0

20

72 9

69

86 0

85

100 7

72

101 3

07

95 8

66

99 3

92

108 2

32

111 4

01

115 1

23

118 3

79

119 7

04

126 3

08

133 8

87

139 8

47

135 6

99

0

50 000

100 000

150 000

200 000

250 000

300 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

R M

ILL

ION

S (

CU

RR

EN

T A

ND

CO

NS

TA

NT

20

12

VA

LU

ES

)TOTAL INVESTMENT IN BUILDING: 2000-2012 (CURRENT VALUES)

THE STRATEGIC FORUM SCENARIOS: 2013-2020 (CONSTANT 2012 VALUE)(Source: SARB, StatsSA, MFA, BMI-BRSCU Workings)

TOTAL BUILDINGS : 2000-2007: LOWER MIDDLE ROAD SOYUZ SCENARIO: 2008-2015

TOTAL BUILDINGS HIGH ROAD COLUMBUS SCENARIO

TOTAL BUILDINGS LOW ROAD CHALLENGER SCENARIO

TOTAL BUILDINGS HIGHER MIDDLE ROAD APOLLO SCENARIO

CURRENT MOST LIKELY SCENARIOBETWEEN LOWER MIDDLE AND LOW

ROAD SCENARIOSHigh Road 10%

Upper Middle Road 20%

Lower Middle Road 40%

Low Road 30%

© BMI-BRSCU© BMI-BRSCU

www.strategicforum.co.za

72

28

814

32 5

32

33 9

17

37

773

47

042

60 0

20

72 9

69

86

085

10

0 7

72

10

1 3

07

95

866

99 3

92

10

8 2

32

11

1 4

01

115

123

118 3

79

11

9 7

04

126

308

133 8

87

13

9 8

47

135

699

0

50 000

100 000

150 000

200 000

250 000

300 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

R M

ILL

ION

S (

CU

RR

EN

T A

ND

CO

NS

TA

NT

20

12

VA

LU

ES

)TOTAL INVESTMENT IN BUILDING: 2000-2012 (CURRENT VALUES)

THE STRATEGIC FORUM SCENARIOS: 2013-2020 (CONSTANT 2012 VALUE)(Source: SARB, StatsSA, MFA, BMI-BRSCU Workings)

TOTAL BUILDINGS : 2000-2007: LOWER MIDDLE ROAD SOYUZ SCENARIO: 2008-2015

TOTAL BUILDINGS HIGH ROAD COLUMBUS SCENARIO

TOTAL BUILDINGS LOW ROAD CHALLENGER SCENARIO

TOTAL BUILDINGS HIGHER MIDDLE ROAD APOLLO SCENARIO

CURRENT MOST LIKELY SCENARIOBETWEEN LOWER MIDDLE AND LOW

ROAD SCENARIOS

High Road 10%

Upper Middle Road 20%

Lower Middle Road 40%

Low Road 30%

© BMI-BRSCU© BMI-BRSCU

www.strategicforum.co.za

The difference between “high road” and “lower middle road” could be R560 Billion and 940 000 jobs over the 8 years to 2020.

73

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dem

ocra

tic E

lect

ion

Tra

nsiti

on to

De

mocr

acy

Curr

ency

Co

llapse

World

Tra

de

Ce

ntr

e

BN

G H

ousin

g P

rog

ram

me

Sub

Pri

me C

risi

s

Socce

r W

orld C

up

0

10 000

20 000

30 000

40 000

50 000

60 000

19

93

/01

19

94

/01

19

95

/01

19

96

/01

19

97

/01

19

98

/01

19

99

/01

20

00

/01

20

01

/01

20

02

/01

20

03

/01

20

04

/01

20

05

/01

20

06

/01

20

07

/01

20

08

/01

20

09

/01

20

10

/'01

20

11

/'01

20

12

/'01

CU

M Y

TD

Q/Q

% C

HA

NG

E

Defining Events

R M

ILL

ION

S (

CU

RR

EN

T V

AL

UE

S)

GFCF CONSTRUCTION: Q1 1993-Q4 2012: CURRENT VALUESCUMULATIVE YTD Q TO Q (PREVIOUS YEAR) PERCENTAGE CHANGE

(Source: SARB; BMI-BRSCU Workings)

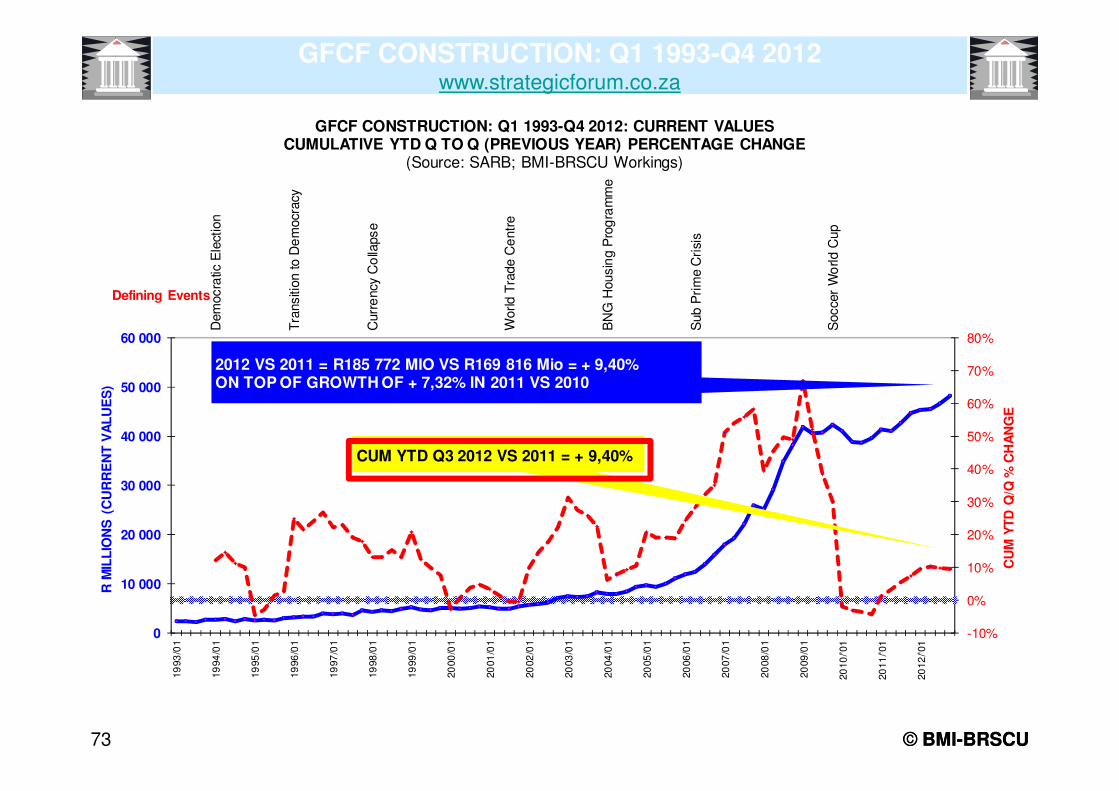

CUM YTD Q3 2012 VS 2011 = + 9,40%

2012 VS 2011 = R185 772 MIO VS R169 816 Mio = + 9,40%ON TOP OF GROWTH OF + 7,32% IN 2011 VS 2010

© BMI-BRSCU© BMI-BRSCU

GFCF CONSTRUCTION: Q1 1993-Q4 2012www.strategicforum.co.za

74

2012/'01 2012/'02 2012/'03 2012/'04

CUM GFCF CONSTRUCTION 2012 45 393 90 913 137 498 185 772

CUM GFCF CONSTRUCTION 2013 45 409 91 104 138 903 190 416

CUM Q/Q % CHANGE GFCF CONSTR 2013VS 2012

0.04% 0.21% 1.02% 2.50%

CUM Q/Q % CHANGE GFCF CONSTR 2012VS 2011

9.51% 10.19% 9.86% 9.40%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

200 000

Cu

m Q

/Q P

erc

en

tag

e C

han

ge

R M

illio

ns

CUM Q/Q GFCF CONSTRUCTION: 2013 VS 2012 (FC) (Source: SARB, BMI-BRSCU Workings)

MAT FORECASTACTUAL

© BMI-BRSCU© BMI-BRSCU

GFCF CONSTRUCTION: Q1 1993-Q4 2012www.strategicforum.co.za

75 © BMI-BRSCU© BMI-BRSCU

SCENARIOS FOR CONSTRUCTION: 2013-2020www.strategicforum.co.za

19 0

29

23 0

22

30 6

63

35 1

15

40 7

39

53 1

24 80 8

79

127 3

02 161 5

95

158 2

36

169 8

16

185 7

72

190 4

16

199 9

37

213 9

33

216 0

72

226 8

76

238 2

19

245 3

66

250 2

73

0

50 000

100 000

150 000

200 000