mahesh bhupati group (pdf)

TRANSCRIPT

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 1 ~

ABSTRACT

Economic globalization is an unavoidable trend. Financial liberalization to integrate into the international

financial community is an aspect of globalization. Many Middle-East countries had begun this process with

a view to attract capital for economic development. The unexpected onset of the recent global financial

crisis made these countries reassess the state of their financial systems as well as the pace and the

sequence of financial liberalization. Due to its geographical location and increasing economic

interdependence, Middle-East countries could not avoid the impact of the global financial crisis. This study

looks at assessment of the strategic planning among Middle-East financial institutions is facing and

identifies the impact of financial crisis in Middle-East countries. Practical solutions for overcoming the global

financial crisis are outlined.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 2 ~

SCOPE OF THE STUDY

Financial institutions in the Middle East are being urged to implement strategic planning fast as a means to

combat the global slump and ensure survival in the face of intense regional competition. This study can be

divided in three categories. First it focus on the strategic planning among the middle east countries, second

the impact of the global financial crisis over the middle east financial institutions and the last part is the

strategies that followed to overcome the impact of the crisis. The impact has been classified in few sectors

to differentiate the problems that the countries facing in all terms. According to the impact mentioned, the

steps to overcome to impacts are determined. After that, there are a brief discussion about the impact of

the global financial crisis to the Middle East countries and the findings/strategies on how to overcome the

impact of the global financial crisis to the Middle East financial institutions. As there are some risk taken to

overcome the impact of the global financial crisis to the Middle East countries, so it cause for some

disadvantages for the countries.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 3 ~

OBJECTIVE OF THE STUDY

This paper intends to study about the strategic planning among Middle-East financial institutions is facing

and overcoming the impact of global financial crisis.

� The first section of the study will analyze the impact of the global financial crisis towards Middle

East financial institutions.

� The second section of the study will present about the strategic planning used among the Middle

East financial institutions.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 4 ~

INTRODUCTION

I.) Impact of the global financial crisis in Middle east financial institutions

Global financial crisis give a variety impact to the Middle East financial institutions. Around in the 10th

century the Middle east economic was economically advanced region of the world and it will be measured

by standard of living, technology, agricultural productivity and others. This scenario has been changed in

2007 and the early part of 2008, rising oil prices lined the coffers of major exporters like Saudi Arabia, the

United Arab Emirates, Iran, Kuwait, and Iraq. The first impact of global financial crisis is reduces of oil

prices and global liquidity shortages. Basically, most of the GCC country faces with decline in oil prices and

production, as well as by liquidity shortages in global financial markets. The direct impact from U.S.

subprime assets, however, was limited, given a relatively low direct exposure of GCC commercial banks to

these assets. Oil market developments affected government finances and external positions directly, but

they also had an indirect impact on banking and corporate liquidity and funding costs as speculative capital

inflows reversed and investor confidence in the GCC declined. This will together with global liquidity

shortages, course a sudden fall in asset prices and weakened financial systems’ balance sheets, prompting

governments’ intervention in the financial sector.

The second impact was Pressures on bank funding and liquidity led to tight credit conditions. The

turnaround of speculative short-term inflows linked to exchange rate speculation, combined with global

deleveraging and widening emerging market spreads, resulted in significant liquidity pressures and

increased funding costs. Commercial banks drew down their reserves with central banks, and short-term

interest rates spiked sharply, although temporarily. Timely response by the authorities, including through

the infusion of liquidity and deposit guarantees, helped stabilize interest rates and liquidity conditions.

Next is Changes in the fund investment strategies. Due to the global financial crisis in Middle East

financial institutions the investors have been change their investment strategies. In the other hand, some

funds are opting for more conservative strategies, such as SAMA (Saudi Arabian Monetary Agency), the

Saudi Sovereign Wealth Fund Institute. Those countries are traditionally focused on financial markets in

Europe and the U.S. are turning their attentions towards other markets - in Arab countries and emerging

ones, as well as towards direct investments. For example, in 10 January 2009 the Abu Dhabi Investment

Company announced to create four investment funds in the Middle East and North Africa.

Last but not least were repercussions for stock markets and the Arab financial system. The huge

losses recorded by both supreme wealth funds and private Arab capital in financial markets in the United

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 5 ~

Kingdom and the United States meant that the stock market crash in September 2008 affected the majority

of the Middle Eastern stock markets. After the bankruptcy of Lehman Brothers was announced, on

September 15th 2008, the Saudi Arabian stock market fell by 6.5%, Doha 7%, Kuwait 3% and Abu Dhabi

4.35%.Certain markets, such as Kuwait, had to close for a number of days to avoid outbreaks of panic.

Over the last year, falls in these Gulf stock markets have followed a parallel path to those in Europe and

North America and are strongly linked.

II.) Lessons learn from the global financial crisis towards middle east financial

institutions

Now let us see what are the lessons did Middle East countries learns from the global financial crisis? First

for the political leadership the lessons are Lack of regulation is as bad as over-regulation. Although they

believe governments should not regulate free market choices, they also believe investors should regulate to

protect investors against conflict of interests and negligence by investment bankers. Regulations should

also ensure full transparency and disclosures and should effectively penalize violators. To be more specific,

investment banking firms who knowingly sold investments to their clients and later betted against them

without informing the same clients; those who invested in fraudulent funds without proper due diligence on

behalf of their clients; and rating agencies that miss-rated subprime junk derivatives as grade A assets.

Second was Insanity is defined as doing the same thing and expecting different results. Hiring the

same people who got us into the economic recession in the first place or hiring those who did not foresee

the financial crisis to design the recovery policies is not the right solution. Most of the economic advisors

did not see the crisis until it was too late and some of them participated in the policies that led to the crisis

in the first place.

Third was the country pay a big price not only for their wrong economic policies, but also for wrong

foreign policies. Countries that allow foreign lobbies, special interest groups or extreme nationalist

movements to dominate their foreign policies by becoming active participants in international conflicts will

end up creating more enemies and wasting their valuable resources in defending their own security.

Countries that try to spread their ideologies by force, be it religion, socialism, capitalism, democracy or

something else, will be overwhelmed by the human and economic cost of conflicts. Those countries will lag

behind other countries that are focusing on developing their economies and advancing their interests via

global partnerships and trade.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 6 ~

As an overall the lesson should be strengthen strategic thinking by place more emphasis on

scenario planning, trends analysis and client/ market listening. Institute strategic planning cycle make the

process more regular and important inside the organization. Make a stronger connection to resource

allocation by ensure that strategic plans allocate resources and connect to budgets. Increase leadership

engagement: more visibility and direct involvement in the strategic planning process by senior leaders.

Improve strategic action: enhance operational execution through better change and performance

management as well as overall communications.

III.) Define strategic planning

Strategic planning is an organization's process of defining its strategy,or direction, and making decisions on

allocating its resources to pursue this strategy. In order to determine the direction of the organization, it is

necessary to understand its current position and the possible avenues through which it can pursue a

particular course of action. Generally, strategic planning deals with at least one of three key questions.

"What do we do”? , For whom do we do it?" "How do we excel?”. The linkage between global financial crisis

and Middle East are institutions that used strategic planning to make critical decisions were better able to

pursue growth opportunities during the crisis. Institutions that relied on strategic planning during the crisis

are more confident about their prospects for near-term growth. Institutions employing a regular strategic

planning process and cycle were more prepared for the economic crisis. Institutions that involve the entire

executive team in strategic planning expect revenue growth over the next 12 months.

The recovery of oil importers in MENA will depend crucially on their key markets, especially the

European Union (EU) and the GCC countries. The feeble recovery expected in the Euro zone will drag

down growth in the near term, particularly the growth of those with strong links to EU markets. Growth of oil

importers is expected to decelerate slightly to 4.5 percent in 2010.Trade is recovering, with export revenue

of oil importers expected to grow by 7.7 percent in 2010, after contracting by 13 percent in 2009.

Remittance flows are expected to grow by 1.3 percent in 2010, albeit this pace is much slower than the one

observed during the pre crisis years. The crisis has not led to any major reform reversals, except perhaps a

slowing of food and energy subsidy reforms, which have generally been very slow to progress. Some

countries have steamed ahead with the reforms started prior to the crisis. These include the financial sector

reform in Egypt and trade integration in Tunisia For the circumstances as mention above, the GCC

countries used a long-term growth planning on the recovery of the financial crisis such as formation of Gulf

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 7 ~

Cooperation Council, Steadily Increase Oil Production, and Maintain a long-term demand for oil at the

expense of alternative energies.

LITERATURE REVIEW

The world doomed to recession in the year 2008, and what are the causes of these unlikely event; well as it

is the global financial crisis that hit on the globalized world which has originated in The United States and

extended to the rest of the world in 2008 led to massive destruction of economy. According to;

Ramadhan.M and Naseeb.A 2009 in their Journal the Global Financial Crisis: Causes and Solutions; the

likely events of the crisis tend to be caused by Imbalance in World Trade, Consumption Pattern in the U.S,

Excessive deregulation of financial market, and the dominant role of the U.S dollars. The first clear sign that

the US housing bubble was bursting, the mid-2007 crisis in the sub-prime mortgage market (stemming from

the significant increase in defaults), transmitted losses to a whole set of securitized financial products such

as mortgage-backed securities (Lin, Senior Vice President and Chief Economist The World Bank; 2008).

Hence, the lack of supervision of the financial markets has caused the mortgage bubble motivated an

abruption of crisis which led to indebtedness or bankruptcy among the banks in U.S and throughout the

world. Therefore the Middle-East financial institution is not left behind in this mounting crisis.

The Impact of Global Financial Crisis to the Middle-East Countries’ Financial Institution

The impact in Middle East is said to be not impulsive, according to Kouame. A 2009, the Acting Chief

Economist for the MENA Region in an interview of Q&A of the global financial crisis and MENA he stated

that; Although financial systems in MENA countries have not been highly vulnerable to the crisis so far due

to their limited integration with global financial institutions, the impact of the global recession on the real

economy can be significant in many MENA countries. As a whole, the MENA region is projected to grow at

3.3% in 2009 down from 5.5% in 2008. This is a significant mark down. However, MENA is expected to be

less impacted by the global recession than most other developing regions, notably Eastern Europe &

Central Asia, and East Asia & Pacific. Regarding the impact of the global financial crisis, (Larbi .H 2009)

from the Quarterly Publication - The World Bank Middle East Department has clarified that one common

factor among Middle-East countries was that the initial impact of the global financial crisis on their financial

systems was muted. Habibi.N 2009 articulates that in terms of integration into global financial markets, the

Middle East falls behind all other emerging-market regions other than Africa; but although a lower level of

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 8 ~

financial integration is a disadvantage under normal circumstances, it can protect an emerging region when

the global economy sinks into a severe financial crisis. Subsequently, he also further clarifies that Middle-

East region is affected by global economic conditions through fluctuations in the oil market. The global

crisis sharply reduced the flow of foreign investment into real estate; as a result, the uptrend in real estate

prices in the Middle East, which had lasted for several years, came to an end in 2008. This development

put severe pressure on real estate construction firms and encouraged sell-offs in regional stock markets. In

turn, the end of real estate speculation sharply increased mortgage defaults, and as a result many listed

commercial banks came under financial distress. To adhere the impacts of the crisis on the Middle East

countries financial institution; the introduction of Gulf Cooperation Council (GCC) is crucial because there

are huge number of countries of Middle East is participating in the council. Meaning to say, if the crisis

affects GCC it distresses the ME-countries itself. GCC is a political and economic union of the Arab states

bordering the Persian Gulf and located on or near the Arabian Peninsula, namely Bahrain, Kuwait, Oman,

Qatar, Saudi Arabia and United Arab Emirates, Jordan and Morocco. Therefore the first massive impact

would be fall of oil prices in late 2008, leaving many oil exporters struggling under the weight of debt they

had assumed during oil's run-up. In Middle Eastern countries without major crude supplies, the crisis posed

a threat more humanitarian in nature: It challenged their abilities to pay off international debts and strained

international aid institutions. Thus in the article of Khamis .M & Senhadji.A 2010; they anticipated that the

global economic crisis took hold, the GCC countries were affected through trade and financial channels. By

the second half of 2008, GCC government finances and external positions were directly affected by the

decline in oil prices and demand. At the same time, GCC countries underwent reversals of speculative

capital inflows experienced in 2007 and early 2008. These developments tightened liquidity conditions and

affected investor confidence, and were further exacerbated by Lehman’s collapse in September 2008 and

the ensuing global liquidity shortages and deleveraging. GCC financial sector imbalances came to the fore,

especially in the United Arab Emirates (U.A.E.), Kuwait, and Bahrain, given these countries’ close linkages

with global equity and credit markets. There are several categories of impact on the financial institution of

Middle East classified in the article of (Rocha.R et al 2011); such as Impact on Regional Equity and Bond

Markets, Impact on Regional Banking Systems, and Impact on Islamic and Conventional Banks.

• Impact on Regional Equity and Bond Markets

MENA stock markets reacted to the global financial crisis with a lag in comparison to markets in high-

income and other emerging economies: as a result of high oil prices, they held up better than markets

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 9 ~

elsewhere until the third quarter of 2008. However, both the GCC and non-GCC stock markets crashed

with other stock markets around the world during the worldwide panic in the fourth quarter of 2008,

following the bankruptcy of Lehman Brothers. The fall of stock prices in the GCC was more pronounced,

reflecting the burst of the real estate bubble and the sub region’s greater openness relative to other parts of

the region. The impact of the global financial crisis on the region’s sovereign debt broadly mirrored global

trends, with a sharp spike in credit spreads as a reaction to the Lehman bankruptcy and a rapid decline as

the panic subsided.

• Impact on Regional Banking Systems

In the run-up to the financial crisis, credit growth had been on an upward trend in all three MENA

subregions. The GCC credit expansion has caused a large component of real estate lending and in some

countries increasing reliance on foreign funding; which seem to accelerate during most of 2008, in contrast

with trends in other regions. With the collapse of asset and commodity prices and the freezing of financial

markets, the crisis reached emerging economies and led to a sharp slowdown in lending in virtually all

MENA countries, especially those in the GCC. The very sharp credit slowdown in the GCC reflected not

only reduced oil inflows but also restricted access to foreign borrowing and domestic banks’ curtailing of

real estate lending. The prompt and forceful reaction by the GCC authorities included fiscal stimulus,

monetary easing, and exceptional measures to support the financial sector (Khamis and Senhadji 2010).

Apart from credit growth being affected, the Resiliency of banking sector is also being disturbed. Standard

indicators of banking system soundness and the lack of systemic consequences underscore the resiliency

of MENA banking sectors to the global financial crisis. Banking systems in GCC countries were highly

capitalized in the precrisis years, and capitalization increased further in 2009. The regional political crisis

and the unwinding of countercyclical measures will test the resiliency of emerging MENA banking sectors.

There has been significant disruption in economic activity in countries experiencing long protests and

turmoil. These disruptions will lead to reduced lending activity and deteriorating asset quality and

profitability of banks, to different degrees across countries.

• Impact on Islamic and Conventional Banks

The financing activities of Islamic banks are tied more closely to real economic activities, Islamic banks

avoided direct exposure to exotic and toxic financial derivative products and Islamic banks in general kept a

larger proportion of their assets in liquid form. As the global financial crisis turned into a global economic

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 10 ~

crisis, Islamic banks and financial institutions started to be indirectly affected. The business model of many

Islamic banks—which relied on murabaha financing and invested predominantly in the real estate sector

and in the previously growing equity markets—has been facing higher risks (Ali 2011).

Strategic Planning Among Middle East Countries to Overcome The Crisis.

Speciously, as the research by;(World Bank Regional Economic Update 2011) stated that by the end of

2010, countries in the Middle East and North Africa (MENA) had largely recovered from the global financial

crisis, and growth rates were expected to reach pre-crisis levels in 2011. Therefore, how would this be

possible without the proper strategic planning to endure the risk from the overwhelming crisis? According to

Larbi (2009), while the impact of the crisis of Middle East financial systems has been limited so far, going

forward, one cannot exclude a significant impact on the real economy. How countries’ real economies are

impacted and how they can mitigate the impact will depend in part on initial conditions. In particular, fiscal

and current account balances, as well as debt level, play an important role in shaping countries’ ability to

mitigate the impact of the crisis. According to Reinikka (2010); the impact of the 2008–09 global financial

and economic crises varied substantially among three country groupings in the Middle East and North

Africa (MENA): the Gulf Cooperation Council (GCC), developing oil exporters, and oil importers.

Henceforth, this section will identify and state the strategic planning structure that has been practiced by

the Middle East countries in order to combat the crisis.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 11 ~

1. Strategic Planning in the GCC(Gulf Cooperation Council) countries: Oil Exporting

Countries;

Formation of Gulf Cooperation Council

The Gulf Cooperation Council is known as a Cooperation Council for the Arab States of the Gulf and it was

found in 26 May 1981.The GCC was established in order to promote coordination between member states

in all fields to achieve unity. (Wikipedia) Basically, the original Council comprised the 630-million-acre

(2,500,000 km²) Persian Gulf states of the United Arab Emirates, Bahrain, Saudi Arabia, Oman, Qatar and

Kuwait. The unified economic agreement between the countries of the Gulf Cooperation Council was

signed on 11 November 1981 in Abu Dhabi. These countries are often referred to as The GCC States. The

objective of this council was to formulate similar regulations in variety of fields like economy, finance, trade,

tourism and other. Besides that, they also involve in fostering scientific and technical progress in industry,

mining, agriculture, water and others.(Sheikh Mohammad Bin Rashid Al Moktoum).Other countries in the

Middle East, in particular the countries of the Gulf Cooperation Council (GCC), are more closely tied to the

global economy and their performance is more directly affected by world economic conditions.

The GCC countries list of nations or member states is Bahrain, Kuwait, Oman, Qatar, Saudi Arabia,

and UAE. The full name is Cooperation Council for the Arab States of the Gulf (CCASG) and also referred

to as the Arab Gulf Cooperation Council (AGCC). GCC countries have a significant economic dependence

on oil export as Kuwait, Saudi Arabia, and Abu Dhabi in the UAE in particular. Qatar has a large natural gas

industry; Oman and Bahrain have much less dependence on oil. The GCC oil exporters were hardest hit

because the crisis affected them directly through two different channels: (a) a negative terms-of-trade

shock associated with the drop in oil prices; and (b) a financial shock, which destabilized overextended

domestic banks and led to the bursting of a real estate bubble (Reinikka, 2010). Eventually, as the GCC

countries comprises a large influence on the Middle East regional economy, this section will cover briefly

about the strategic plan which has been practiced by this countries to cope the impact of the crisis. The

governments of the GCC states are dealing with the consequences of the crisis in a number of strategic

plans:

a) Implement expansionary fiscal policy (Winckler, 2010):

This policy has three goals:

• To maintain the economic activity level

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 12 ~

GCC Countries Economic expansion

Qatar � The 2009-10 budgets, is expected to be the largest ever because

Qatar has intended to launch large-scale infrastructure projects

such as construction of the New Doha International Airport and

the Sidra Hospital, expansion of the Ruwais port, large-scale

road-building, expansion of drainage systems, and improvements

in educational and vocational facilities.

� Inclusively, in 2010, more than $229 billion worth of projects were

planned or under way in Qatar alone.

Oman � In year 2009 the budget spiked 10.8% higher than 2008; although

there is sharp decline in governments revenues.

Saudi Arabia � Saudi capital spending for 2009 is also projected to be 36 percent

higher than in 2008 and includes $7 billion for a railway linking

Damman and Jeddah through Riyadh.

� Reserves requirement for banks has been lowered from 13

percent to 7 percent, $2-3 billion has been injected into banks in

the form of dollar deposits, all bank deposits have been

guaranteed, and the government has allocated an additional $2.7

billion in credit to low income citizens having problems accessing

loans

According to Winckler (2010), each of the GCC countries without exception has adopted

extraordinary measures in order to restore confidence and to stabilize the financial sector, among

them, cutting interest rates, providing bank deposit guarantees, reducing requirements on bank

deposits, and introducing new credit facilities in order to strengthen bank liquidity. The Persian Gulf

governments have also injected capital into private banks to encourage them to lend more to the

private sector.

• To create new job opportunities for the national workforce

Apparently, to reduce the unemployment rate in GCC countries radical approach has been taken

such as diversifying job opportunity for the national workforce. Therefore, in the case of Saudi

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 13 ~

Arabia as example; in April 2009, the Saudi Human Resources Development Fund offered to pay

half of the first year's salary in advance for Saudis who were newly hired by private firms.

Previously, it had paid a 50 percent bonus after the completion of the employee's first year on the

job. Furthermore, the aim of the advanced payment was to tempt companies to increase the

number of employed nationals since getting credit from banks had become more difficult since the

onset of the financial crisis. Saudi authorities also strengthened the inspection regime for private

companies' adherence to the government-mandated quotas for national employees (Arab News

2010).

• To prepare for the end of the crisis.

The practice of the expansionary fiscal policy has innate good benefits. Despite considerable

damage to the GCC economies resulting from the global crisis, the situation in these countries was

and still is much more favorable than that of the rest of the world's economies. It appears that

timely responses by the GCC governments to the worldwide financial crisis brought about stability

in their economies when most other worldwide economies were still shaken by it (Iradian, 2009).

Since the second quarter of 2009, the Persian Gulf economies have gradually returned to solid

growth.

b) Steadily Increase Oil Production Capacity (Winckler,2010)

To begin with, in order to curb the situation in which the decrease in demand for oil at the start of

crisis the Middle East countries has implement to reduce the oil production at first and then

gradually increase the production later when the crisis muted. GCC countries tried to continue

demand for oil as the world's primary energy source at the expense of tracking alternative energy

sources. Increasing oil production spare capacity in order to sustain moderate prices for the long-

run was another measure adopted by many GCC members. There were two goals for this

increase:

• Stable and moderate oil prices constitute a major tool for global economic recovery

• Maintain a long-term demand for oil at the expense of alternative energies.

In mid-2009, the Saudi Arabian crude production capacity amounted to 12.5 million b/d, more than

4 million b/d above its production scale in early 2010 (see Table 1). Since the peak of oil prices in mid-

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 14 ~

2008, the Saudi authorities have consistently emphasized both their huge proven oil reserves and

spare production capacity in an effort to convince oil consumers not to switch to alternative energy

sources. The Kuwaiti government is currently acting to increase its oil production capacity to 4 million

b/d until 2020. Maintaining the level of the current global oil demand is viewed as insurance for long-

term governmental revenues, also enabling the GCC governments to maintain high expenditure levels.

Conclusively, according to Reinikka (2010) the Gulf countries are leading the regional recovery as

oil prices have rebounded, and the GCC financial sector is stabilizing. Growth in the GCC countries is

projected at 4.4 percent in 2010—a remarkable comeback. The recovery in the GCC countries is

expected to have a positive impact on other MENA countries, mainly through increased flows of

remittances and FDI.

Table 1: Oil Production in GCC States, 2000-10 (thousands of b/d)

Country 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010**

Saudi Arabia 8,404 8,031 7,634 8,410 8,897 9,353 9,112 8,651 9,261 8,250 8,240

UAE 2,368 2,276 2,082 2,248 2,344 2,378 2,540 2,504 2,681 2,413 2,414

Kuwait 2,079 1,998 1,894 2,136 2,289 2,529 2,535 2,465 2,586 2,350 2,350

Qatar 737 714 679 676 755 766 821 807 924 927 1,020

Oman 970 960 897 819 780 774 738 710 757 813 855

Bahrain* 190 190 190 240 209 187 185 180 180 180 180

Total 14,748 14,169 13,376 14,529 15,274 15,987 15,931 15,317 16,389 14,933 15,059

* Including Bahrain's share of Abu Sa'afa oilfield. ** Jan.-Mar. average. Source: EIA, International Petroleum Monthly, June 2010, table 1.1; ESCWA data.

2. Strategic Planning in the Other Developing Oil Exporting Countries:

Eventually, the developing oil exporting countries in the region are Algeria, Iran, Syria, and Yemen. As

identified in Global Economic Prospects (June 2011), these countries form a group of economies troubled

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 15 ~

by political protest and/or forms of repression on the part of authorities over a range of intensity (from most

severe in Yemen and Syria, to concealed popular dissatisfaction in Iran, and to a lesser degree in Algeria).

Furthermore, the growth for the aggregate of oil exporters immersed from 2.2 percent in 2009 to 1.4

percent in 2010. Gains across the group ranged from 1 percent in Iran to 3.3 percent in Algeria, with

Yemen an exception, as the coming online of an LNG train boosted growth to 8 percent in the year (Global

Economic Prospects, June 2011). Developing oil exporters were hurt less than GCC oil exporters as they

felt the impact of the crisis only through the oil channel (Figure 1). Hence, due to the limited integration of

their banking sectors into global financial markets, developing oil exporters felt the impact of the crisis

mostly through the negative oil price shock (WORLD BANK MENA REGION – A REGIONAL ECONOMIC

UPDATE, APRIL 2010).The financial sectors of developing oil exporters were not affected by the global

financial crisis due to the underlying government guarantees and the fact that the banking sectors in these

countries have remained isolated from global financial markets. Credit growth was much lower prior to the

crisis in the developing oil exporters than in the GCC countries, and therefore these countries experienced

only a moderate decline.

Figure1: Real GDP Growth Rates

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 16 ~

a) Steadily Increase Oil Production Capacity (Winckler,2010)

Due to the crisis; for the oil-exporting MENA countries, the slower economic growth is partly due to a

decision by OPEC to reduce its oil output by 2.2 million barrels per day (7.5% of the cartels total oil output

in December 2008), effective January 2009. Habibi (2009), state that the implementation of this decision

led to a reduction in the value of Arab oil exporters’ oil sector GDP in real terms. Outwardly, the developing

oil exporters has also practice the similar strategic planning towards the crisis whereby steadily increase

the oil production to avoid any losses. Hence, global demand for oil started growing in the fourth quarter of

2009 after falling for five consecutive quarters. The strong rebound was due to the rapid recovery in

emerging markets, most notably Asia, and improvements in global financial conditions. US demand for oil

has started growing too (WORLD BANK MENA REGION – A REGIONAL ECONOMIC UPDATE, APRIL

2010). This growth acceleration is faster than that expected for developing oil exporters, and in glaring

contrast to the slight deceleration anticipated for oil importers in 2010 as illustrated in Figure 2.

Figure 2: Expected growth rate changes relative to previous year (percentage point change)

3. Strategic Planning Among Oil Importing Countries

As opposed in the study of Reinikka (2010); the oil-importing MENA countries were hurt mostly by the

secondary effects of the crisis on trade, remittances, and foreign direct investment (FDI). Growth of

MENA’s oil importing countries decelerated from 6.8 percent in 2008 to 4.8 percent in 2009, mostly

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 17 ~

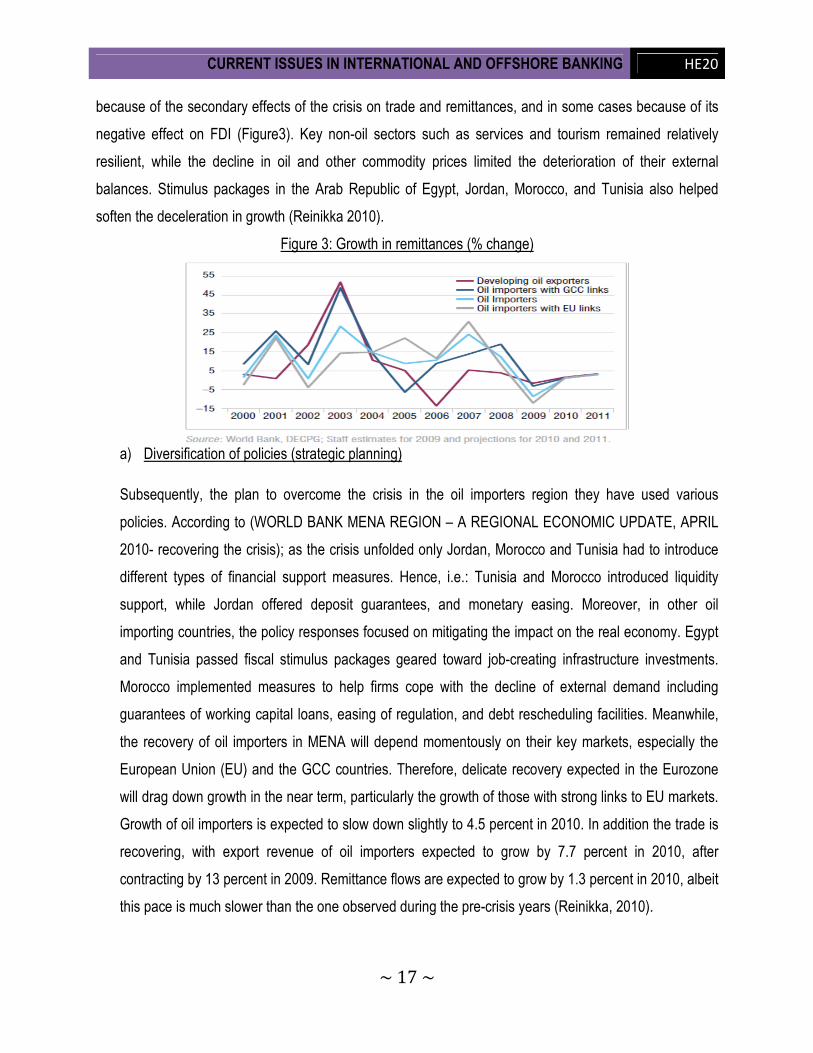

because of the secondary effects of the crisis on trade and remittances, and in some cases because of its

negative effect on FDI (Figure3). Key non-oil sectors such as services and tourism remained relatively

resilient, while the decline in oil and other commodity prices limited the deterioration of their external

balances. Stimulus packages in the Arab Republic of Egypt, Jordan, Morocco, and Tunisia also helped

soften the deceleration in growth (Reinikka 2010).

Figure 3: Growth in remittances (% change)

a) Diversification of policies (strategic planning)

Subsequently, the plan to overcome the crisis in the oil importers region they have used various

policies. According to (WORLD BANK MENA REGION – A REGIONAL ECONOMIC UPDATE, APRIL

2010- recovering the crisis); as the crisis unfolded only Jordan, Morocco and Tunisia had to introduce

different types of financial support measures. Hence, i.e.: Tunisia and Morocco introduced liquidity

support, while Jordan offered deposit guarantees, and monetary easing. Moreover, in other oil

importing countries, the policy responses focused on mitigating the impact on the real economy. Egypt

and Tunisia passed fiscal stimulus packages geared toward job-creating infrastructure investments.

Morocco implemented measures to help firms cope with the decline of external demand including

guarantees of working capital loans, easing of regulation, and debt rescheduling facilities. Meanwhile,

the recovery of oil importers in MENA will depend momentously on their key markets, especially the

European Union (EU) and the GCC countries. Therefore, delicate recovery expected in the Eurozone

will drag down growth in the near term, particularly the growth of those with strong links to EU markets.

Growth of oil importers is expected to slow down slightly to 4.5 percent in 2010. In addition the trade is

recovering, with export revenue of oil importers expected to grow by 7.7 percent in 2010, after

contracting by 13 percent in 2009. Remittance flows are expected to grow by 1.3 percent in 2010, albeit

this pace is much slower than the one observed during the pre-crisis years (Reinikka, 2010).

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 18 ~

4. Working Together Towards Recovery And Improved Crisis Resilience

Another; strategic approach of Middle East countries to combat the crisis is to cooperate with higher

authorities and accepting wide range of helping hand from other institution. Well, according the (WORLD

BANK MENA REGION – A REGIONAL ECONOMIC UPDATE, APRIL 2010- recovering the crisis); during

the past year, the World Bank Group responded actively to the economic downturn in the MENA region and

tailored this support to the needs of the countries. Consequently, in Iraq, where the fall in oil prices severely

affected public finances, the World Bank provided financial support through a development policy loan,

working closely with the International Monetary Fund. Furthermore, as in the oil importing MENA countries,

such as Egypt, Jordan, Morocco and Tunisia, the World Bank has been providing technical support through

diagnostics work as well as quick-disbursing financial support through several development policy

operations focusing on financial sector, public sector reforms, and trade integration. These operations also

help build crisis resilience for the future. In the GCC countries, the short-term response of the World Bank

Group was to step up economic and financial monitoring and engage in strategic reimbursable technical

assistance. IFC’s Global Trade Finance Program has helped businesses, especially small ones, access

trade finance, while its Global Trade Liquidity Program has helped infuse liquidity into the trade finance

market. IFC has also helped banks across the MENA region by sharing views and solutions on how to

successfully navigate the crisis, structure robust risk management systems, and train key bank staff on risk

management.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 19 ~

DISCUSSION OF THE FINDINGS

As mention earlier in literature review, the Middle East country’s can be divided into three categories .In

includes GCC countries (oil exporting), developing oil exporting countries, and oil importing countries.

Furthermore we will be discussing in detail about the strategies that have been used to overcome the

global financial crisis and do some justification. Firstly, author (Wincker, 2010) mention about the

implementation of expansionary fiscal policy. In our point of view this strategy was successful and effective

because when the Middle East countries plan to spend more, it will increase the revenue of the country. For

example in the 2009-10 budgets, is expected to be the largest ever because Qatar has intended to launch

large-scale infrastructure projects such as construction of the New Doha International Airport and the Sidra

Hospital, expansion of the Ruwais port, large-scale road-building, expansion of drainage systems, and

improvements in educational and vocational facilities. This indicates that it could be one of the portions

of gross domestic product of the country. In addition, when the revenue is increased the growth of GDP will

increase. Because, one of the policy aim is to maintain and stable the economic level. The fiscal policies

also, help the GCC, measures to help ease inter-bank lending rates and add new regulations to their stock

markets.

The other aim of this policy is to create new job opportunities for the national workforce. Based on

the Arabic News (2010), in April 2009, the Saudi Human Resources Development Fund offered to pay half

of the first year's salary in advance for Saudis who were newly hired by private firms. Previously, it had paid

a 50 percent bonus after the completion of the employee's first year on the job. Furthermore, the aim of the

advanced payment was to tempt companies to increase the number of employed nationals since getting

credit from banks had become more difficult since the onset of the financial crisis. From here what they

want to critic is to reduce the unemployment rate in GCC countries they must be offer job to their country

people. When, there is too much foreign or other country workers in GCC countries, it will lead to so much

of cash outflow for the country that will give negative impact. It also increases the unemployment rate in the

country.

After years of decline in unemployment among Gulf nationals due to the strategy of labour market

“nationalization” through citizen quotas in private sector employment, the lay-off threat reversed the trend.

Private sector employees, considered at a disadvantage relative to their peers in secured public sector

positions, held their governments responsible for securing their jobs. This situation forced governments to

diversify their policy response and introduce labour market policies. However, diverse trends converged to

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 20 ~

contain rising labour governance issues. Saudi officials issued protectionist “anti-foreign” statements,

denouncing the employment of foreigners at the expense of “unemployed national[s]” but with no practical

strings attached. Kuwait has drafted a progressive new labour law that practically equates in terms of

benefits citizens and foreigners but maintains the “sponsorship scheme.”

Meanwhile, the author (Wincker,2010) mention that, in order to curb the situation in which the

decrease in demand for oil at the start of crisis the Middle East countries has implement to reduce the oil

production at first and then gradually increase the production later when the crisis muted. This strategy is

used in GCC countries. In our point of view, this strategy will be useful to steadily increase oil production

capacity to ensure the financial resources needed to maintain the entire system. This also helps to continue

demand for oil as the world's primary energy source at the expense of pursuing alternative energy sources.

In other way, oil production was a main source of income for the GCC countries to survive.

Based on the Global Economic Prospects (June 2011), the developing oil exporting countries in the

region are Algeria, Iran, Syria, and Yemen these countries form a group of economies troubled by political

protest and/or forms of repression on the part of authorities over a range of intensity (from most severe in

Yemen and Syria, to concealed popular dissatisfaction in Iran, and to a lesser degree in Algeria).To avoid

this crisis, author suggest that, for steadily increase oil production capacity (Winckler,2010). Due to the

crisis; for the oil-exporting MENA countries, the slower economic growth is partly due to a decision by

OPEC to reduce its oil output by 2.2 million barrels per day (7.5% of the cartels total oil output in December

2008), effective January 2009.However, economic growth has been constrained by anaemic credit growth,

which has started inching higher only recently, and by the fact that the four GCC members of OPEC have

restrained output of crude oil to support oil prices, in the face of large stock overhang and rising non-OPEC

supply.

Moreover, author Reinikka (2010) identified that the oil-importing countries were hurt mostly by the

secondary effects of the crisis on trade, remittances, and foreign direct investment. To cure this crisis, the

author suggested to apply diversification policies and working together recovery and improved crisis

resilience. The policy has been used are focused on mitigating the impact on the real economy. This

strategy will be effective because by applying it, the other oil importers will know how to reduce the crisis by

getting guidance of the big authorities. In addition to easing liquidity constraints on banks and firms, so far

the response has focused on mitigating the short-term impact of the crisis on the real economy, although

some measures including tax cuts and investment expenditure would promote sustained growth. In Tunisia

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 21 ~

and Morocco, fiscal stimulus through increased current expenditures included measures to support private

consumption, in the form of public sector wage increases, and measures to help SMEs cope with the

decline of external demand, including guarantees of working capital loans, easing of regulation, and debt

rescheduling facilities. Assistance to firms, irrespective of size, was provided in Egypt through transfers

supporting exporters, industrial zones in the Delta region, and logistic areas for internal trade. Stimulus

through capital expenditure increases went into job-creating infrastructure investments in Egypt and

Tunisia. In addition, Egypt increased investments in rural and social sectors.

A range of tax measures were introduced in Egypt, including cuts in customs duties on selected

industrial inputs and capital goods, temporary suspension of the sales tax on selected capital goods,

introduction of import tariffs on steel, and imposition of anti-dumping duties on sugar to protect domestic

production. Djibouti and Lebanon registered only minor declines in growth during the same period, with

both economies growing at 5 and 8 percent, respectively, in 2009. Lebanon grew at a much faster pace

than other oil importers with GCC links, reflecting a post-conflict recovery boom aided by strength in certain

sectors – tourism and real estate – and vibrant private investment. Policy interventions in Lebanon helped

fuel the post-conflict recovery boom, but strained further the fiscal outlook. Public sector wages increased,

and a daily compensation fee was introduced for low-income public school students. Other policies were

introduced to ensure access to finance, including subsidized interest rates extended to all sectors, except

construction and trade, and strengthen macroeconomic fundamentals such as an increase in international

reserves.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 22 ~

LIMITATION OF THE STUDY

Although the study has reached its aims, there were some unavoidable limitations. First because of the

time limit, we can’t find some important information for our third strategic planning, which are oil importers

countries affected by foreign direct investment trade and remittances. An additional there was lack of

sources for that part. Second, the students’ overloaded work, to some extent, might affect the correlation

between students’ motivation in learning current issue subject because they were required to take part in

many studies at the same time. Finally, the slow network might discourage participants’ interests and

motivation in joining peer feedback activities.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 23 ~

CONCLUSION

The global economic crisis which began in the second half of 2008 impacted Middle East economies

through several transmission channels. The flow of foreign investment into the region diminished; the crude

oil market experienced a significant price correction after having reached record-high levels as of mid-2008;

international tourism to Middle Eastern destinations declined; and there was a reduction in global demand

for the region’s non-oil exports. Depending on their exposure to each of these transmission channels,

different Middle East countries were impacted differently by the crisis. Most governments are taking action

to address the vulnerabilities identified in their economies. For example, GCC countries intervened early to

support their banking systems and stock markets. They did so by easing monetary policy, securing the

banking system’s liabilities (including through deposit guarantees), and by injecting fresh capital where

necessary. Saudi Arabia, for example, has announced a substantial investment spending plan and

provided capital to Saudi Credit Bank to secure credits to low income households. Among G-20 countries,

Saudi Arabia’s fiscal stimulus package is the largest as a share of GDP. Kuwait is discussing a

stabilization package. Egypt has announced a fiscal stimulus package geared toward job-creating

infrastructure investment.

Besides that, the World Bank doing help to the global financial crisis impacted countries. The World

Bank Group is responding on a number of fronts. The World Bank group will remain close to their clients to

gain a good understanding of the crisis implications for each country. The World Bank’s knowledge

resources are being mobilized to support their client countries in efforts to monitor economic and social

development, review scenarios and policy options, design policy responses, and implement reforms in

these critical times. Middle East countries will continue to play a major role in knowledge creation and

sharing by raising the effectiveness of our analytic, advisory, and capacity enhancing services and

strengthening our adaptation and learning.

Apparently, if this global financial crisis occurs in future, we have to know what kind of the

precaution steps should be taken to avoid this crisis. Because this crisis was give a good lesson and

overview the impact that we will be face. Rather than that, government and other authorities have to play a

crucial task to make the Middle East countries economy being stable.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 24 ~

REFERENCES

Ali, S. 2011. “Islamic Banking in the MENA Region.”Background paper for this book, World Bank,

Washington, DC.

Bank, T. W. (2010). Sustaining the Recovery in Times of Uncertainty.

Creane, S., Goyal, R., Mobarak, A., & Sab, R. (2010). Measuring Financial Development in the Middle East

and North Africa: A New Database. International Monetary Fund Journals.

Habibi, N. (2009). The Impact of the Global Economic Crisis on Arab Countries:A Year-End Assessment.

Middle East Brief.

Khamis, M., & Senhadji, A. (2010). Impact of the Global Financial Crisis on the Gulf Cooperation Council

Countries and Challenges Ahead.

Khamis, M., & Senhadji, A 2010b. Impact of the Global Financial Crisis on the Gulf

Cooperation: Crisis and Challenges Ahead: An Update. Washington, DC: International Monetary

Fund

Larbi, H. (2009). The Financial Crisis: Impact on the Middle East. The World Bank Middle East Department.

Leenders, R. (2007). 'Regional Conflict Formations': Is the Middle East Next? Third World Quarterly.

Lin, J. Y. (2008). The Impact of the Financial Crisis in Devoloping Countries. The Institute of Chartered

Accountants of Sri Lanka.

Maroun, N., & Azour, J. (n.d.). One Year After The GCC Region's Post Crisis Prosspects.

Motaghi, L., Carey, K., & Gourdon, J. (January, 2011). Sustaining The Recovery and Looking Beyond.

Middle East and North Africa. (June 2011). Global Economic Prospects June 2011: RegionalAnnex.

(October 2010). chapter 2: Country and Regional Perspectives. International Monetary Fund:World

economic outlook: Recovery, Risk, and Rebalancing.

Ramadhan, M., & Naseeb, A. (2008). The Global Financial Crisis: Causes and Solution.

CURRENT ISSUES IN INTERNATIONAL AND OFFSHORE BANKING HE20

~ 25 ~

Reinikka, R. (2010). A Handbook on the Future of Economic Policy in the Developing World. In O. C.

GIUGALE, The Day After Tommorow.

Rocha, R. R., Arvai, Z., & Farazi, S. (2011). A Road Map for the Middle East and North Africa. Financial

Access and Stability.

Winckler, O. (2010). Can the GCC Weather the Economic Meltdown? MIDDLE EAST QUARTERLY

SUMMER 2010.