longer-term global oil supply volumes and composition · pira energy group longer-term global oil...

TRANSCRIPT

PIRA Energy Group

Longer-Term Global Oil Supply Volumes And Composition

Bill FullerSenior Director, International Oil

Annual Retainer Client SeminarNew York City: October 10-11, 2013

Overview and Non-OPEC Supplies

Call-on-OPEC Crude Continues to Grow in LongTerm But Non-OPEC Covers Most of Demand Growth

0.0

0.5

1.0

1.5

2.0

'00-'05 '05-'10 '10-'15 '15-'20 '20-'25 '25-'30

Total Non-OPEC Call on OPEC Crude Supply Growth Demand Growth

Non-OPEC Growth includes increasing amounts of higher cost non-conventionals

Annual Growths, MMB/D

World Oil Non-OPEC Supply Forecast Overview

Medium Term (to 2017):Non-OPEC Growth 2013 – 2017 Averages 1.4 MMB/D

– U.S. and Canada have strongest growth– Growth is relatively stable over the years thru 2017

Longer Term (to 2030):Non-OPEC Growth declines slightly to average 1.0 MMB/D / Year 2020-2030

– U.S. and Canada remain in lead group which becomes more broad based as Brazil, Mexico, FSU, China and OPEC NGL’s grow

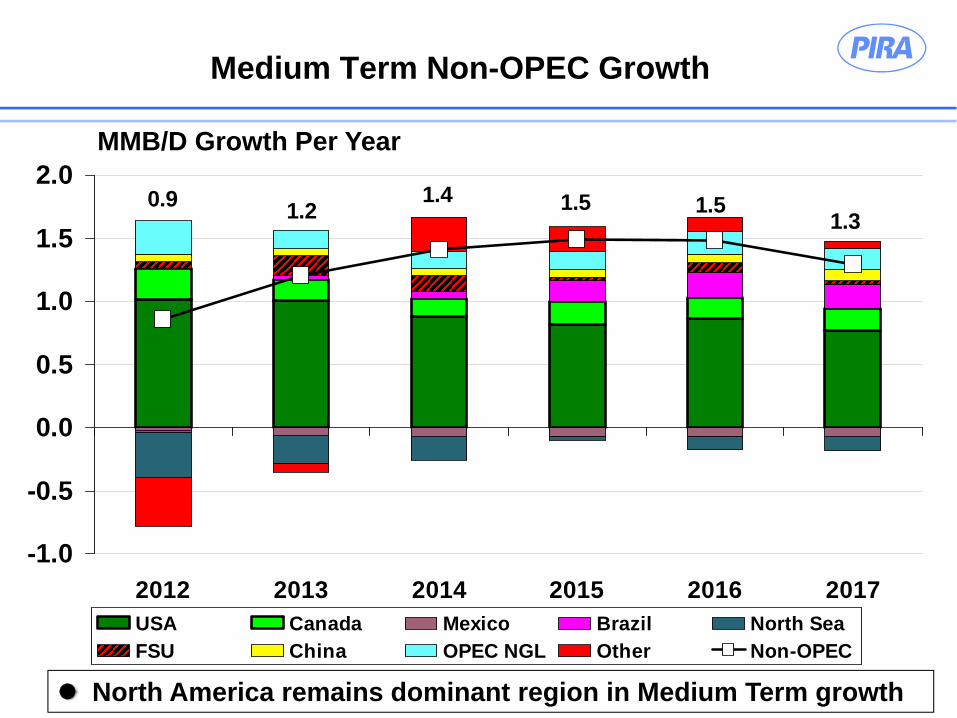

Medium Term Non-OPEC Growth

1.30.9 1.2 1.51.51.4

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2012 2013 2014 2015 2016 2017USA Canada Mexico Brazil North SeaFSU China OPEC NGL Other Non-OPEC

MMB/D Growth Per Year

North America remains dominant region in Medium Term growth

Medium Term Non-OPEC Growth Components

Development of Shale Liquids; especially strong in U.S.

Also growing in Canada; slow beginning outside North America

Canada: Bitumen projects are economic at forecast price

Brazil: Development of already discovered sub salt fields

Kazakhstan: Start up of giant Kashagan field

OPEC NGL/Condensate: Recovery of liquids from associated

gas from crude expansion projects and from non-associated gas

projects

Long Term Non-OPEC GrowthContinues Strong But Less U.S. Centric

1.0

1.1

0.7 1.0

1.31.1

-0.5

0.0

0.5

1.0

1.5

'00-'05 '05-'10 '10-'15 '15-'20 '20-'25 '25-'30

USA Canada Mexico Brazil North SeaFSU China OPEC NGL Other Non-OPEC

MMB/D Growth Per Year

Factors Leading to Continued StrongNon-OPEC Production In the Long Term

Perceptions of evolution of oil market prices

“Easy” oil (i.e., low cost oil) used up

– Next increment of world resource base more expensive, supporting higher

oil prices

Higher oil price supports new higher cost projects

Technological advances; as spurred on by higher prices

Shale liquids; Oil Sands; Ultra-deep water; Sub-salt imaging

Investment climate good in countries at forefront of technology

Huge resource base for Shale liquids and Canadian oil sands

Increasing Natural Gas production provides associated liquids

High ratio oil to gas prices provides incentives for liquids recovery

Russian tax/duty incentives to develop new frontiers; ESPO pipeline

U.S. Shale Play Operators Improvising to ReapCost and Volume Improvements

More wells per rig» Cutting single well spud-to-spud times» Pad drilling (Multiple wells from one pad) reduces time to move rigs to

new locations

More wells per acre» Earlier 640 acre spacing being tested to reduction to 320 or 160» Some loss in single well recovery, but overall higher recovery

Initial production (IP) rates improving from longer laterals and higher horsepower fracing

Expanding into new areas / counties within formations» More activity now in Northern end of Niobrara shale

Developing deeper layers of existing shale plays» Bakken: Three Forks Benches 2-4; Permian Basin: Wolfcamp / Cline

U.S. Shale Crude Peaks at Over 6 MMB/DAbout 2025 – Peak Growth Year is 2013

0

1

2

3

4

5

6

7

2005 2010 2015 2020 2025 2030

MMB/D

Bakken Eagle FordPermian Basin Others

-0.2-0.10.00.10.20.30.40.50.60.70.8

'05-'10 '10-'15 '15-'20 '20-'25 '25-'30

MMB/D

Bakken Eagle FordPermian Basin Others

Lower 48 Onshore Crude Production Ex Shale CrudeGrows to 2020 Due To Resurgence in Permian Basin

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015 2020 2025 2030

Lower48 Onshore ex Shale L48 ex Shale ex Permian

MMB/D

1998/99 Oil Price Collapse (Asian Financial Crisis)

2009 Price Fall (Global Recession)

L48 Onshore ex Shale Crude

Resurgence of Permian Basin Non-Shale Crude

Non-Shale Non-Permian Production

Crude Growth in Permian Basin Mainly from ShalesBut Non-Shale Crude Remains Larger Component

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2005 2010 2015 2020 2025 2030TX Permian Non-Shale NM Permian Non-ShaleTX Permian Shale Crude NM Permian Shale Crude

MMB/D

Total Non-Shale

Growth in Non-Shale crude reflects growth in rigs drilling vertically

U.S. Gulf of Mexico Forecast AssumesBacklog of New Fields Begin Production

0.0

0.5

1.0

1.5

2.0

2.5

1995 2000 2005 2010 2015 2020 2025 2030

Fields Started Before 2013 Identified New Unidentified New

MMB/D

Unidentified “New”

(Post-2013) Production

Decline rates of “Older” production (Pre-2013) estimated at ~16%/Yr

Macondo spill April 2010 led to increased regulations

Identified Named Fields

Cost escalation and storm loss dented output in 2000’s decade

New GOM output highs reflect:Higher oil prices since 2010Good resource potentialTechnological advancesGood fiscal environmentLack cheaper alternatives

Alaska Production Expected to Grow After 2025

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1990 1995 2000 2005 2010 2015 2020 2025 2030

Cook Inlet Existing North Slope New Named FieldsNew NPR-A New Central New Ugnu HeavyFederal Offshore Shale Crude ANWR

MMB/D

U.S. NGL Production Almost Doubles by 2030With Large Growth in Ethane

0

1

2

3

4

5

6

2010 2015 2020 2025 2030

Barnett Marcellus/UticaEagle Ford Anadarko/OtherPermian Bakken/RockiesOther Shales Non-Shale

0

1

2

3

4

5

6

2010 2015 2020 2025 2030Pentanes+ ButanesPropane Ethane

By Source By GradeMMB/D MMB/D

U.S. Total Oil Supply Growth Remains Strong in Medium Term then Tapers off Long Term

02468

101214161820

1990 2000 2010 2020 2030

MMB/D

Shale Crude Shale NGL Non-Shale Crude On.Non-Shale Crude Off. Non-Shale NGL BiofuelsOther Liquids Refinery Gain

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

95-0

0

00-0

5

05-1

0

10-1

5

15-2

0

20-2

5

25-3

0

MMB/DProduction Growth

Canadian Total Crude Growth is Mainly Oil SandsAnd Remains Strong Both Medium Term and Long Term

0

1

2

3

4

5

6

7

1990 2000 2010 2020 2030

Heavy Light/MediumAtlantic SyntheticBitumen Condensate

Production

-50

0

50

100

150

200

250

'95-

'00

'00-

'05

'05-

'10

'10-

'15

'15-

'20

'20-

'25

'25-

'30

Heavy Light/MediumAtlantic SyntheticBitumen Condensate

Growth / YearMMB/D MB/D

Light Includes Shale Crude

Canada Oil Sands Projects –Breakevens and Forecast Volume Discounts

CAPEX($Cdn/bbl

of capacity, Cdn$2010)

Economic Threshold(WTI US$

equivalent/bbl, US$2010)

1 - Mining, Extraction and Upgrading

$85,000-$105,000

$85-$95

2 - Mining and Extraction Only (No upgrading)

$60,000-$75,000

$65-$75

3 - Steam-assisted Gravity Drainage (SAGD)/Cyclic Steam Stimulation (CSS)

$25,000-$40,000

$50-$60

Includes an after-tax rate of return of 10 to 15%.

Source: Canada National Energy Board (NEB) Nov2011

Canada Risked Shale / Tight Oil Resource Base -Estimated Ultimately Recoverable Reserves (EUR)

0

2

4

6

8

10

12 Bn Bbls, Crude & CondensateTotal Canada Crude &

Condensate EUR 68 Bn Bbls

Canada Shale Crude Production

0100200300400500600700800900

1000

2005 2010 2015 2020 2025 2030

MB/D

Bakken VikingCardium MontneyDuvernay Other ProducingNew Probable New Possible

-100

10203040506070

'00-

'05

'05-

'10

'10-

'15

'15-

'20

'20-

'25

'25-

'30

MB/D

Bakken VikingCardium MontneyDuvernay Other ProducingNew Probable New Possible

Production Growth

FSU Crude Production Gains Result fromKashagan Field in Kazakhstan and Shale Crude In Russia

0

2

4

6

8

10

12

14

16

1990 2000 2010 2020 2030

Russia KazakhstanAzerbaijan Other FSUShale Crude

MMB/D MMB/D Growth

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

95-0

0

00-0

5

05-1

0

10-1

5

15-2

0

20-2

5

25-3

0

Russia KazakhstanAzerbaijan Other FSUTotal

Shale Crude

Production

China Crude Oil Production is Expected to Grow Faster After 2020 Due to Shale Crude

0

1

2

3

4

5

6

1990 2000 2010 2020 2030Daqing ShengliChangqing YanchangXinjiang Other OnshoreOffshore Shale Crude

MMB/D

-50

0

50

100

150

200

'00-

'05

'05-

'10

'10-

'15

'15-

'20

'20-

'25

'25-

'30

Daqing ShengliChangqing YanchangXinjiang Other OnshoreOffshore Shale Crude

MB/DProduction Growth

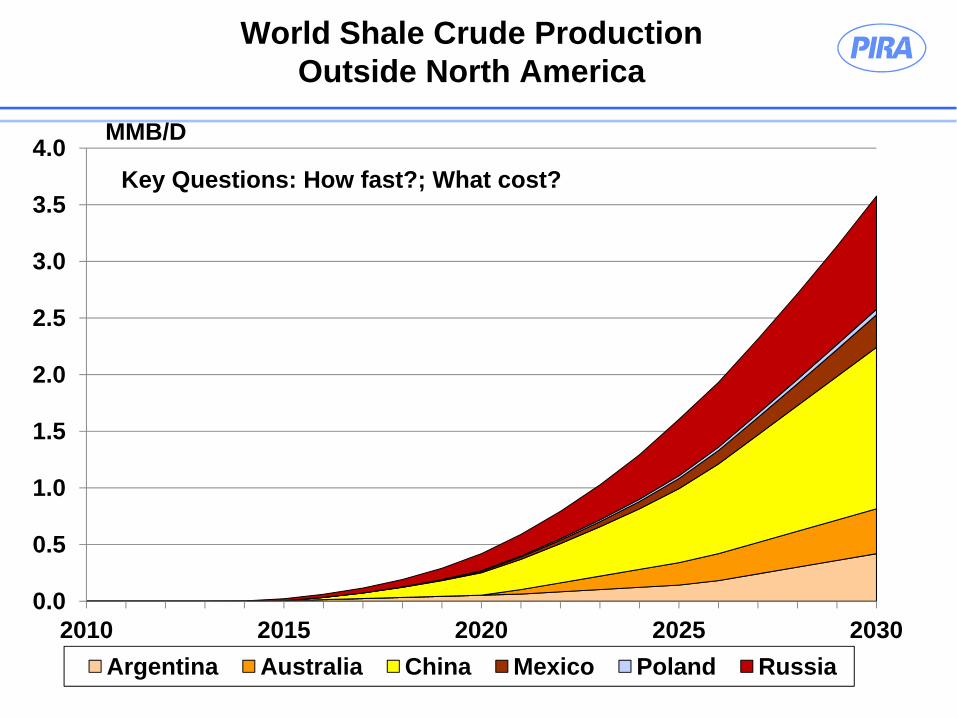

World Shale Crude Production Outside North America

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2010 2015 2020 2025 2030Argentina Australia China Mexico Poland Russia

MMB/D

Key Questions: How fast?; What cost?

Argentina Vaca Muerta Shale

History / EventsYPF discovery well drilled Nov 2010; drilled 51 wells Jun12-Jul13Ryder Scott assessed ~22 Bn BblsOE Feb12 in part of Vaca MuertaYPF reported production for Jul13 of ~12 MBoe/D (crude ~8 MB/D)Argentina Ministry has not reported increased “Vacas Muertas” production; PIRA has not included YPF’s reported production in our data pending confirmation from Ministry

YPF / Chevron AgreementYPF and Chevron sign $1.24 billion agreement Jul13 to invest in developing a portion of the Vaca Muerta

Pilot program of 100 wellsFull development program ~1500 wellsTarget production in 5 years of 50 MB/D oil and 3 million cm/d gas

PIRA ForecastCurrently assuming Argentina shale crude production starts 2015

Production gradually climbs to 200 MB/D 2030

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020 2025 2030

MMB/D

Shale Crude Shale NGL Onshore CrudeOffShore Crude Canada Oil Sands Non-Shale NGLBiofuels Other Liquids Refinery Gain

31 MMB/D

Consolidated Long Range Supply

Shale Crude

35

Strong Initial Growth Rate for Light SweetLessens in Longer Term

Production

0102030405060708090

100

1990 2000 2010 2020 2030Lt Sweet Lt SourMed Sweet Med SourHvy Sweet Hvy SourShale Crude

MMB/D MMB/D

-0.5

0.0

0.5

1.0

1.5

2.0

'00 -'05

'05 -'10

'10 -'15

'15 -'20

'20 -'25

'25 -'30

Lt Sweet Lt SourMed Sweet Med SourHvy Sweet Hvy SourTotal Growth

Growth

PIRA Energy Group

Longer-Term Global Oil Supply Volumes And Composition

Dr. James MasonSenior Analyst, Global Oil

Annual Retainer Client SeminarNew York City: October 10-11, 2013

World Shale Resource Assessment

PIRA’s World Shale Oil Database:58 Countries; 89 Petroleum Basins; 180 Shale Plays

PIRA’s List of Prospective Shale Oil Plays Identified from Analyses of World Petroleum Sedimentary Basins

Many Shale Formations Were Formed by Marine Sediments Rich in Organic Matter

Bakken

AnadarkoWoodford

Marcellus

PermianWoodford

Example: U.S. Bakken, Marcellus, and Woodford Shale FormationsFormed from Marine Sediments 400 Million Years Ago

Most of U.S. Under Water

Geology of Petroleum Sedimentary Basins

Organic Sediments Settle to Floor of Bowl Shaped Basins

With Burial Depth Organic Sediments Compact Into Shale Layers

Example: Williston Basin and the Bakken Shale Formation

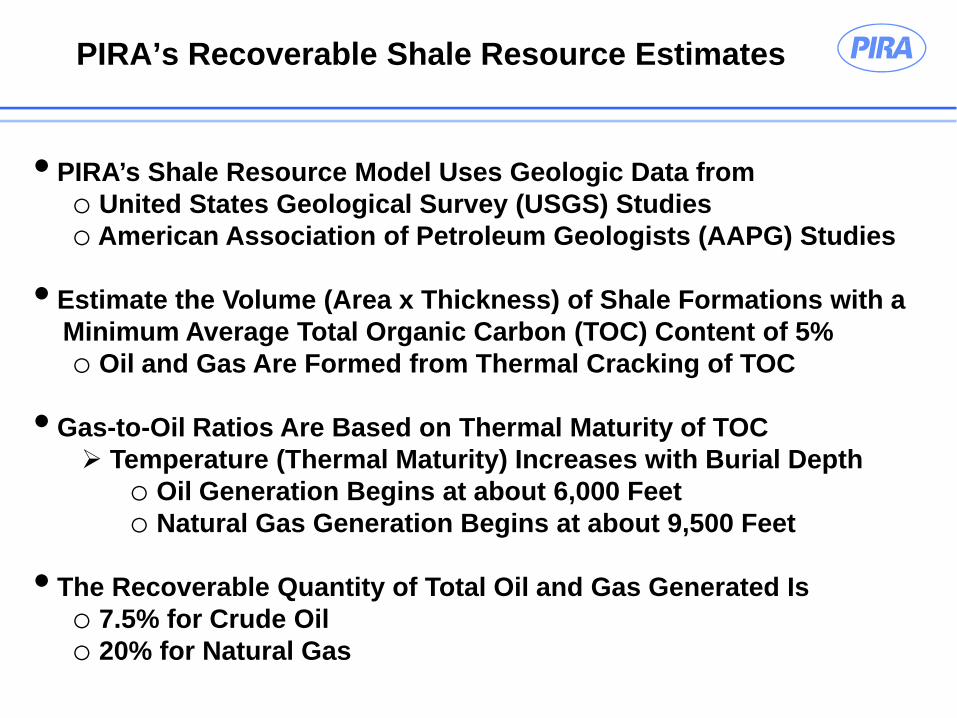

PIRA’s Recoverable Shale Resource Estimates

• PIRA’s Shale Resource Model Uses Geologic Data fromo United States Geological Survey (USGS) Studieso American Association of Petroleum Geologists (AAPG) Studies

• Estimate the Volume (Area x Thickness) of Shale Formations with aMinimum Average Total Organic Carbon (TOC) Content of 5%o Oil and Gas Are Formed from Thermal Cracking of TOC

• Gas-to-Oil Ratios Are Based on Thermal Maturity of TOCTemperature (Thermal Maturity) Increases with Burial Depth

o Oil Generation Begins at about 6,000 Feeto Natural Gas Generation Begins at about 9,500 Feet

• The Recoverable Quantity of Total Oil and Gas Generated Is o 7.5% for Crude Oilo 20% for Natural Gas

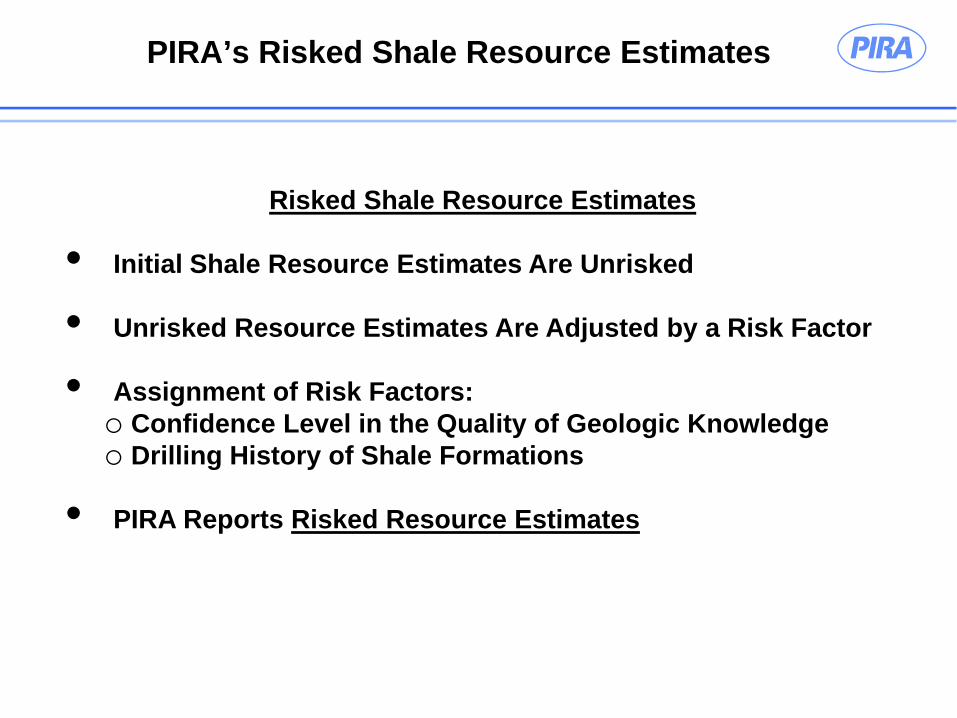

PIRA’s Risked Shale Resource Estimates

Risked Shale Resource Estimates

• Initial Shale Resource Estimates Are Unrisked

• Unrisked Resource Estimates Are Adjusted by a Risk Factor

• Assignment of Risk Factors:o Confidence Level in the Quality of Geologic Knowledgeo Drilling History of Shale Formations

• PIRA Reports Risked Resource Estimates

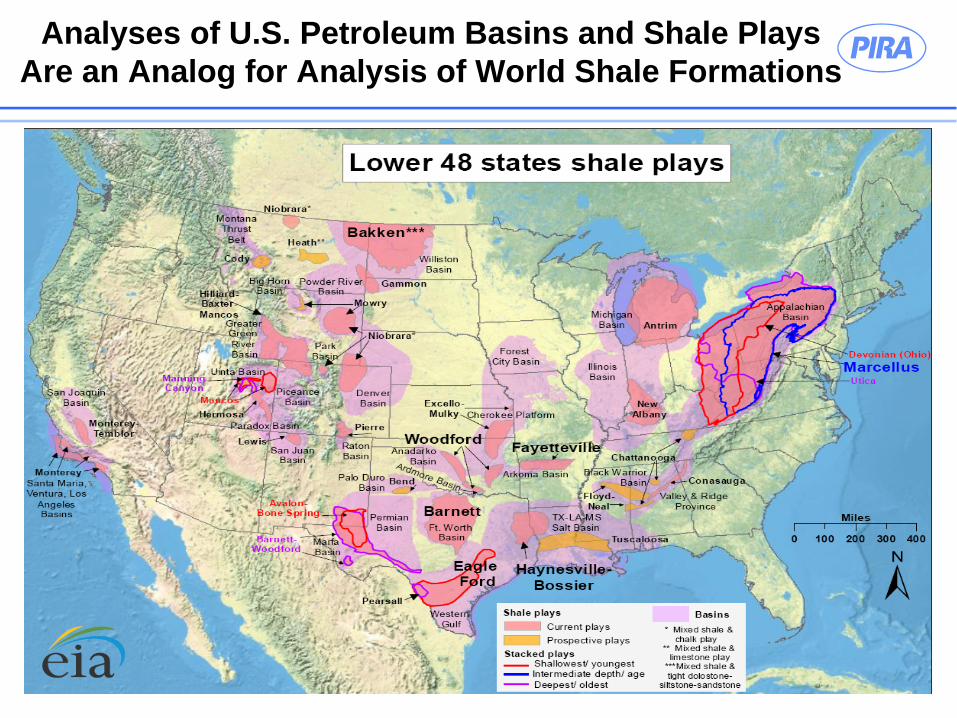

Analyses of U.S. Petroleum Basins and Shale Plays Are an Analog for Analysis of World Shale Formations

U.S. Shale Play Characteristics Are an Analog for Evaluation of World Shale Oil Plays

Geology of Bazhenov Shale Formation Is Similar to Bakken Shale Formationo Mineral Content (Brittleness) o Water Contento Natural Fracture Networks

Bazhenov Shale Has Above Average TOC Content (> 5%)

Highly Prospective Shale Oil Play.

Bazhenov Shale, West Siberia, Russia Compared with U.S. Shale Plays

BazhenovShale (Aqua)

West Siberian Basin

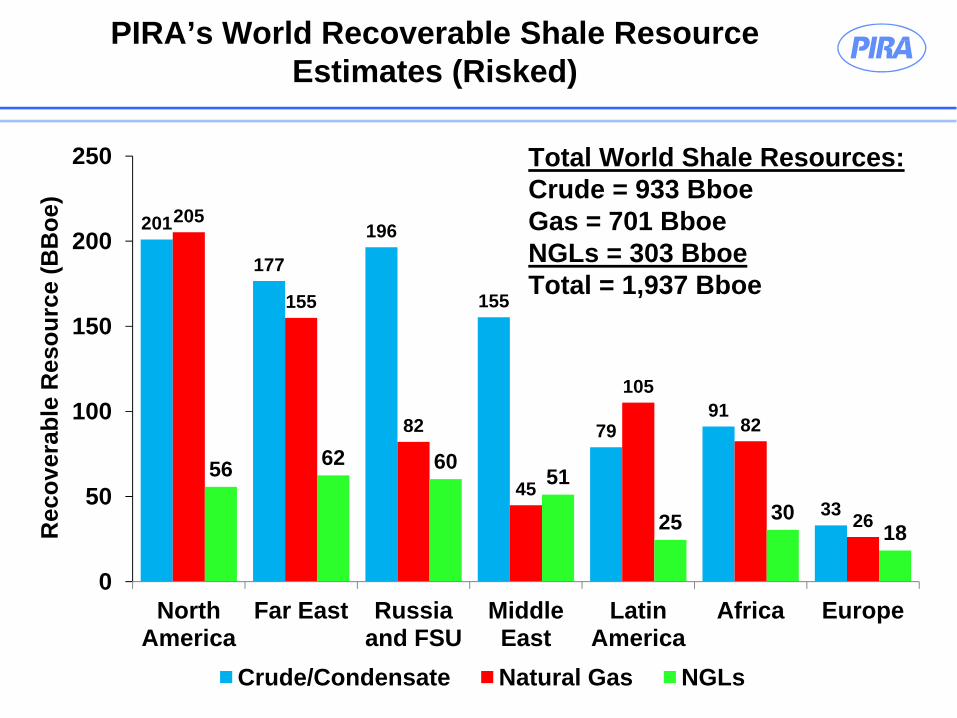

PIRA’s World Recoverable Shale Resource Estimates (Risked)

201

177

196

155

7991

33

205

155

82

45

105

82

26

56 62 6051

25 3018

0

50

100

150

200

250

North America

Far East Russia and FSU

Middle East

Latin America

Africa Europe

Rec

over

able

Res

ourc

e (B

Boe

)

Crude/Condensate Natural Gas NGLs

Total World Shale Resources:Crude = 933 BboeGas = 701 BboeNGLs = 303 BboeTotal = 1,937 Bboe

0%20%40%60%80%

100%

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Ado

ptio

n

Classic Innovation-Adoption S-Curve

WolfcampMarcellus

Eagle FordBakken

Barnett

• U.S. Adoption of Horizontal, Hydraulic Fracturing (HHF) Well Technology for Shale Production Took Over Ten Years toDemonstrate First Economic Success (Barnett)

• Requires Application of Sophisticated and Costly TechnologyApplied by Experienced HHF Drilling & Completion Companies

• World Shale Development Is Not Expected to Occur Rapidly

Cracking the Code:Adoption of Horizontal, Hydraulic Fracturing (HHF)

Countries with Advanced Shale Oil Exploration Programs

• Russiao Russian E&P Companies Are Drilling > 400 HHF Wells o Russian Drilling Companies Order $9 bn of High-Spec Drilling

Rigs That Are Capable of Drilling Shale HHF Wellso Russian E&P Companies Are Forming JV’s with Foreign E&P

Companies to Gain Knowledge about Shale Drilling and Fracking

• Chinao Demonstration Projects for Shale HHF Drilling in 19 Zoneso Focus on Multi-Well Pad Drilling to Minimize Well Footprinto Foreign Companies Are Signing Production Sharing Contracts

• Argentinao YPF Drilling ~ 100 Shale HHF Exploratory Wells in Vaca Muertao YPF Finalized $1.2 bn Joint Venture with Chevron

Countries with Initial Shale Oil Exploration Programs

• Australiao Large Shale Oil Potential but Shale Oil Formations Are Located

in Remote and Unexplored Petroleum Basins

• Colombiao Good Initial HHF Well Flow Rates in Eastern Cordillera Basin’s

La Luna Shale

• Polando Shale Oil Wells Being Drilled in Eastern Poland – Horizontal

Fracking Pending

• United Kingdomo First Exploratory Shale Oil Well Being Drilled in Southern

England

• Other Countries:o Romania, Mexico, South Africa, Ukraine, Turkey, Lithuania,

Brazil, Kuwait, Saudi Arabia, and Germany

Shale Recoverable Resource Estimates (Risked)for Countries with Nearest Term Potential

143

89 7047

10 7 4

59

27112

24

5

73

47

21

35

16 3

0

50

100

150

200

250

300

Russia Australia China Argentina Colombia Mexico UK

Estim

ated

Ulti

mat

e R

ecov

ery

(Bbo

e)

Crude/Condensate Natural Gas and Casinghead Gas NGLs

PIRA Energy Group

Longer-Term Global Oil Supply Volumes And Composition

Glenn SchwartzSenior Analyst, Emissions and Clean Energy

Annual Retainer Client SeminarNew York City: October 10-11, 2013

International Fracking Regulation Discussion

Overview

Key drivers for global shale oil productionCan the U.S. boom be reproduced?

Key Policy Developments in major shale resource

potential countries in past year.

China

Russia

Argentina

Conditions for Successful Shale Oil Development

U.S. EU Russia China Argentina MidEast

Geology

Private sector rights/Access X X X X

Flexible Environ. Regime X

Attractive Fiscal Regime X X X X

Water Access X X

Technology/Labor

Robust Service Providers

Room for Innovative Players X X

Capital X

Takeaway Infrastructure

Limited Conventional Oil X X

Land Rights – Another Key Difference

Land rights. U.S. is fairly unique in that subsurface mineral rights belong to private landowners. Elsewhere, owned by the State» Pros: only need one large negotiated production sharing contract (PSC)

with Energy Minister.» Cons: Public opinion becomes much more important as citizens see

same problems, but less direct benefit. – Political decisions move more slowly than private ones.

» China – less of an issue – gov’t option to relocate landowners.– BUT overlapping land use rights an issue.

» Russia – less of an issue – biggest shale deposits in sparsely populated areas.

» Argentina – Emerging issue. Local population (especially indigenous people) already instituting law suits, local bans.

Role of Foreign Investment

Some local deficiencies can be offset with foreign investment» Skilled labor, technology, know-how all exist in U.S.

– Producers and/or service companies» Money/investment is needed.» A good portion of drilling rig growth must come from foreign sources.» Technology acquisition a driver of China’s investment in U.S. shale

development.Tax Incentives being used to stimulate foreign investment.Difficulties» Importing expertise increases cost of shale development.» Risk-adjusted profitability must be high enough to draw investment

and expertise from North America» Shale industry requires flexibility on the part of operators.

Russia

Previous tax structure thought to be unworkable to justify developing increased costs associated with shale production.

Tax Incentives passed by the Duma in July (effective Sep 1, 2013). Producers get degrees of exemption from the Mineral Extraction Tax (MET).» Coefficient changes and becomes more favorable depending on degree

of difficulty of oil extraction. Taking into account depth, permeability, etc.

» Siberia’s Bazhenov formation (which contains huge shale oil reserves) as well as several other unconventional plays are 100% exempt for a period of 15 years.

New structure helps mitigate investment risks and compensates for significant capital expenditure associated with shale oil development.

Argentina

In July, Pres. Kirchner issued a Presidential Decree to incentivize foreign investment in oil and nat gas exploration.

That decree grants:» All companies that invest > $1B over 5 years gain the ability to export

20% of their crude and nat gas production after the 5th year without paying export duties.

» Freedom to access the foreign currency market at real market value.» The ability to keep earnings in foreign exchange outside Argentina

(other companies are required to repatriate their earnings).» Guaranteed international prices for crude sold on the local market

when obliged to sell locally to meet local demand.

China

Auction Leasing Policy Struggling to Find Success» First two auctions (June 2012, Jan 2013) of shale leasing rights

limited to state-owned companies. » Issue:

– PetroChina, Sinopec etc. reluctant to bear the risk or expense for uncertain returns; Have already experienced hefty exploration costs for low output in pilot drilling. Current/ongoing conventional projects far more attractive.

– Smaller companies offer entrepreneurial spirit, but lack skills, resources. (Many 2nd auction winners had no ties whatsoever to oil/gas industry)

» Third Auction planned – will they change criteria to encourage bids by companies with the relevant technology and experience in drilling for oil and gas?

Drilling has commenced, but chances of hitting FYP targets are remote.

Elsewhere

Europe – EU currently. has no regs, studies on whether to require Environmental Impact Assessments (EIA) ongoing. Right now, entirely regulated at members-state level.» France – moratorium. but pressure to lift mounting?» UK – government published proposals for a new tax regime designed to

incentivize the shale gas industry.» Poland – Recent law exempts drilling of up to 5,000 meters if it is away

from dwellings and drinking water from EIA.

Australia» Currently producing shale gas, but not oil. » Northern Territory’s “use it or lose it” policy to stimulate development.» Attempts at moratorium by Greens in Parliament, but voted down.

Conclusions

U.S. above-ground conditions will be difficult to duplicate elsewhere.

Foreign development will be slower, less efficient, and more costly.

But policy steps have been taken and will likely support production given the enormous potential.

PIRA Energy Group

Longer-Term Global Oil Supply Volumes And Composition

Miriam LevyDirector, Political Risk

Annual Retainer Client SeminarNew York City: October 10-11, 2013

Implications For and From OPEC

OPEC Crude Requirement Grows in the Longer Term, But Remains Flat for the Next Several Years

0

20

40

60

80

100

120

1995 2000 2005 2010 2015 2020 2025 2030Non-OPEC Conventional Non-OPEC UnconventionalOPEC Other OPEC CrudeNon-OPEC Shale Liquids

Global Liquids Supply (MMB/D)

30

15

313031

35

28

Potentially Difficult Period Ahead for OPECAnd for Saudi in Particular

0

5

10

15

20

25

30

35

40

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Saudi Kuwait/UAE Iran Iraq Other

OPEC Crude Production (MMB/D)

(500)(400)(300)(200)(100)

0 100 200 300 400 500 600

'00-'05 '05-'10 '10-'15 '15-'20 '20-'25 '25-'30

Latin America

W. Africa

Other MENA

Libya

Iraq

Iran

Kuwait/UAE

Saudi Arabia

Net Growth

0.3 0.2 0.1 0.3 0.3 0.3

5-Year Average Annual Capacity Growth (MMB/D)

Post-2015, Annual OPEC Capacity Growth Of 0.3 MMB/D Contributes to Flat Call on Saudi

…But OPEC Capacity Growth Is Not Assured:Capacity Has Declined 1.5 MMB/D Since 2008

OPEC Production

OPEC Spare

0

5

10

15

20

25

30

35

40MMB/D

OPEC Capacity

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Feb-08 Forecast Current Forecast

Forecast OPEC Capacity in 2020 (MMB/D)

Excluding Iraq, Down 4.6 MMB/D

Forecast 2020 Non-Saudi OPEC Capacity Is Down 3.6 MMB/D from Forecast Five Years Ago

0

500

1,000

1,500

2,000

2,500

3,000

Major OPEC Supply Losses (MMBbl)

* Disruptions limited to two years cumulative impact on capacity.

Iran 1951/54*Suez 195657

Iraq Gaps 1997/03Nigeria Unrest 1999/00Kuwait Fire 2002/03Ven Strike 2002/03*Iraq War 2003*Nigeria Violence 2007/08Libya Civil War 2011Iran Sanctions 2012/13Libya Protests 2013

Iraq 1966/671967 WarNigeria 1967/68Libya 1970/71Algeria 19711973 Embargo

Iran Rev. 1978/79Iran/Iraq 1980*Iraq/Syria 1982/83*

Gulf War 1990/91*

OPEC Supply Capacity Disruptions:Unpredictable But Certain… And More Frequent?

Impact of Disruptions Often Lasts Well Beyond Immediate Production Losses

02468

Iran (MMB/D)

01234

Iraq (MMB/D)

01234

Libya (MMB/D)

01234

Venezuela (MMB/D)

Iran (MMB/D) Iraq (MMB/D)

Libya (MMB/D) Venezuela (MMB/D)

In Reference Case, Disruptions Diminish Over Time And Planned Future Capacity Growth Is Discounted

Current disruptions will slowly recede over timeIranLibyaNigeria

Planned capacity growth is discounted, especially in countries at high risk for disruptions

VenezuelaIraq

Potential for surprise to upside if situations improve faster than expected

Could create strategic dilemma for OPEC, especially Saudi Arabia

Iran Sanctions Cause Production Losses and Capacity Declines Through 2020

2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8 4.0 Downside

Sanctions prove difficult to evade and/or unwindDamage to reservoirs from forced shut-ins worse than anticipatedPolitical climate prevents foreign investment even if sanctions liftedMilitary action

UpsideQuick, effective deal allows removal of sanctions and quick return of oil to marketSanctions easier to evade over time even without explicit removal

Iran Production and Sanctions Impact (MMB/D)

Production

Crude not sold as a result of

sanctions

Risks to Iranian Production Outlook

Libyan Production Returns Gradually as Political Disputes Continue, Particularly in Eastern Libya

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0

Libya Production and Disruptions (MMB/D)

Production

Civil War and Protests

Risks to Libyan Production Outlook

DownsideCurrent political protests devolve into civil war Cutting off oil sales becomes status quo in political negotiationsCentral power vacuum allows extremists to further establish themselves and destabilize country

UncertainEastern Libya attempts to sell oil independently

UpsideFaster resolution of protests and renewed efforts to create stable, democratic, central government

Theft in Nigeria Continues to Damage Infrastructure, But Some Stolen Crude Sold on Black Market

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Nigeria Production and Disruptions (MMB/D)

Production

Black Market Crude Sales

Risks to Nigerian Outlook

DisruptionsDownside

Theft worsens, causing more prolonged pipeline closures and field shut-insResurgence of MEND militant group prior to or after 2015 Nigerian presidential electionPetroleum Industry Bill (PIB) never passes, foreign investment wanes

UpsideCorruption and theft reduced or eradicatedPIB passes with favorable terms for foreign investment

Difficult Economic and Political Dynamics in Venezuela Could Limit Pace of Orinoco Development

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Venezuela Production and Disruptions (MMB/D)

Conventional

Losses from Upgrader

Maintenance

Risks to Venezuelan Outlook

Blended Extra Hvy

Syncrude

DownsideAcceleration of conventional decline rates and increased upgradermaintenanceCurrent economic difficulties become a full-blown crisis, reducing or deterring foreign investmentPolitical crisis prior to or during 2018 Presidential election

UpsideNext administration (2018 or earlier) pursues more open economic policies

0

2

4

6

8

10

12

14

16

2012 2013 2014 2015 2016 2017 2018 2019 2020Rumaila West Qurna-1 Kurdish Fields MajnoonWest Qurna-2 Kirkuk & Other NOC Zubair HalfayaMissan Gharaf Other South Fields PIRA Forecast

Planned Capacity Additions vs. PIRA Forecast (MMB/D)

In Iraq, PIRA Forecast Calls for Less Than 20% Of the Planned Capacity Additions by 2020

Field Operator

Prior Target

(MMB/D)

New Target

(MMB/D)TargetYear

Recent Output

(MMB/D) Recent Delays

Rumaila BP 2.85 2.10* 2016 1.33

West Qurna 1 XOM 2.83 1.80* 2016 0.45

Majnoon Shell 1.80 1.20* 2017 0.20175 MB/D restart target delayed from end-2012 to 4Q13

West Qurna 2 Lukoil 1.80 1.20 2017 0.00 Startup in Feb/Mar-

14, not 4Q13Zubair Eni 1.13 0.85 2016 0.32

Badra Gazprom, et al. 0.17

60 MB/D startup target delayed from Aug-13 to 2Q14

*Reported targets from ongoing negotiations between government and operators. Official targets remain unchanged.

Iraq Already Slipping from Original Contract Timelines And Reducing Production Plateaus

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Saudi Production (MMB/D) OPEC Strategy Implications

OPEC dilemma: market share vs. price?

Higher non-OPEC productionIncreased OPEC capacitySlower demand growth

Unique Saudi position: Can absorb lower price with higher volumes, but…

… Other OPEC members will experience revenue loss,… Budget requirements are growing

Shale could help set limits on price

Reduced Call on OPEC Could Create Difficult Strategic Choices for OPEC and Saudi

Saudi Arabia Requires Higher Oil Prices To Balance Its Budget

0

50

100

150

200

250

3% Annual Spending Growth (2013 Budget)8% Annual Spending Growth14% Annual Spending Growth (5-yr avg)

Breakeven Price (Nominal $/Bbl Brent)

0

20

40

60

80

100

120

140

2007 2009 2011 2012 2013

Oil Price Requirements for Key Exporters Have Almost Doubled Since 2007

Required Breakeven Oil Prices ($/Bbl Brent)

0

20

40

60

80

100

120

140

160

180

Reference Case (Nominal)Reference Case (2012$)

Forecast Brent Price ($/Bbl)

Price-Responsiveness of Shale Production Likely to Help Manage Long-Term Price Trends