listing in hong kong: what you need to know · davis polk & wardwell llp listing in hong kong:...

TRANSCRIPT

Davis Polk & Wardwell LLP

Listing in Hong Kong: What You Need to Know

Attorney Advertising. Prior results do not guarantee a similar outcome.

Presented byBonnie Chan

June 2012

A. Hong Kong as a Global IPO Market

2

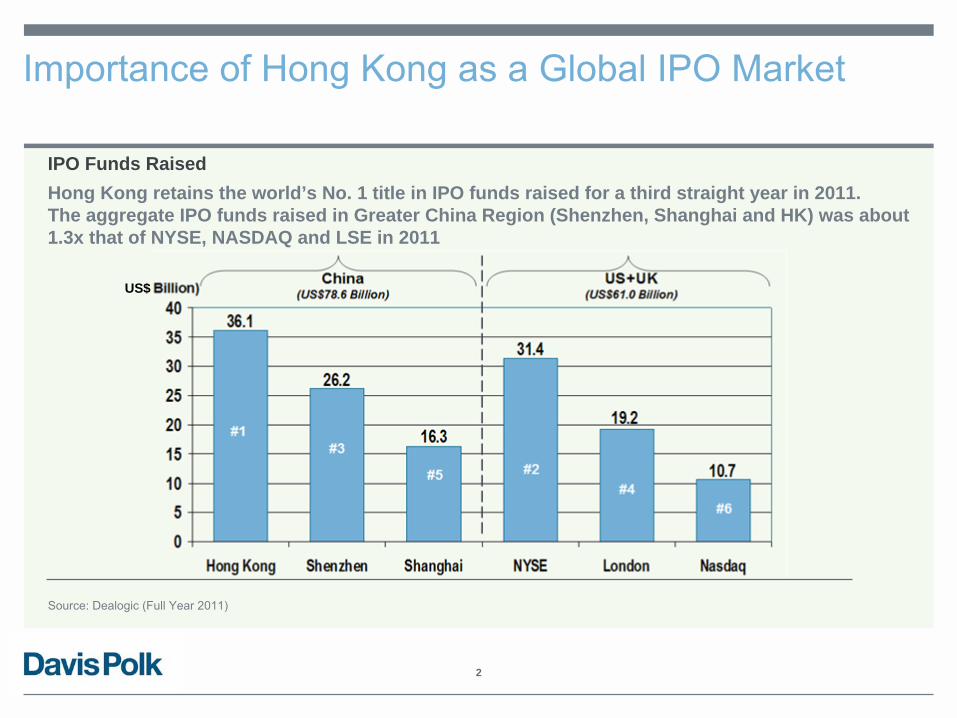

Importance of Hong Kong as a Global IPO Market

IPO Funds RaisedHong Kong retains the world’s No. 1 title in IPO funds raised for a third straight year in 2011.The aggregate IPO funds raised in Greater China Region (Shenzhen, Shanghai and HK) was about 1.3x that of NYSE, NASDAQ and LSE in 2011

US$

Source: Dealogic (Full Year 2011)

3

Total Funds Raised on HKEx

2009 – 2011 Total Funds Raised($US billions)

58Applications approved but not yet listed – As of 31 Dec 2011

93

Applications under review –

As of 31 Dec 2011

210New applications accepted – Jan - Dec 2011

IPO Pipeline

12Transfers from GEM to Main Board

98Companies newly listed (incl. 8 GEM listings)

Jan - Dec 2011New Listings

43%

52%

39%

57%

48%

61%

2009 2010 2011IPO Follow-On

83

113

61

Total

4

Foreign Issuers Listing in HK since 2010

B. The Basics of a Hong Kong Listing

6

What Are the Rules for a Hong Kong Listing?

Hong Kong Listing Rules

Companies Ordinance

Securities and Futures Ordinance

Laws of place where the business is carried on and/or company is incorporated

7

Track Record Requirement: The Three Tests

Profits Test Market Cap/Revenue Test

• Profits of HK$50m in the last three years (with HK$20m in the most recent year and aggregate of HK$30m in the two preceding years)

• Market cap at least HK$200m

Market Cap/Revenue/Cashflow Test

• Market cap at least HK$4bn

• Revenue at least HK$500m for most recent audited FY

• Market cap at least HK$2bn

• Revenue at least HK$500m for most recent audited FY

• Positive cashflow from operating activities of at least HK$100m in aggregate for past 3FY

C. Key Structuring Issues

9

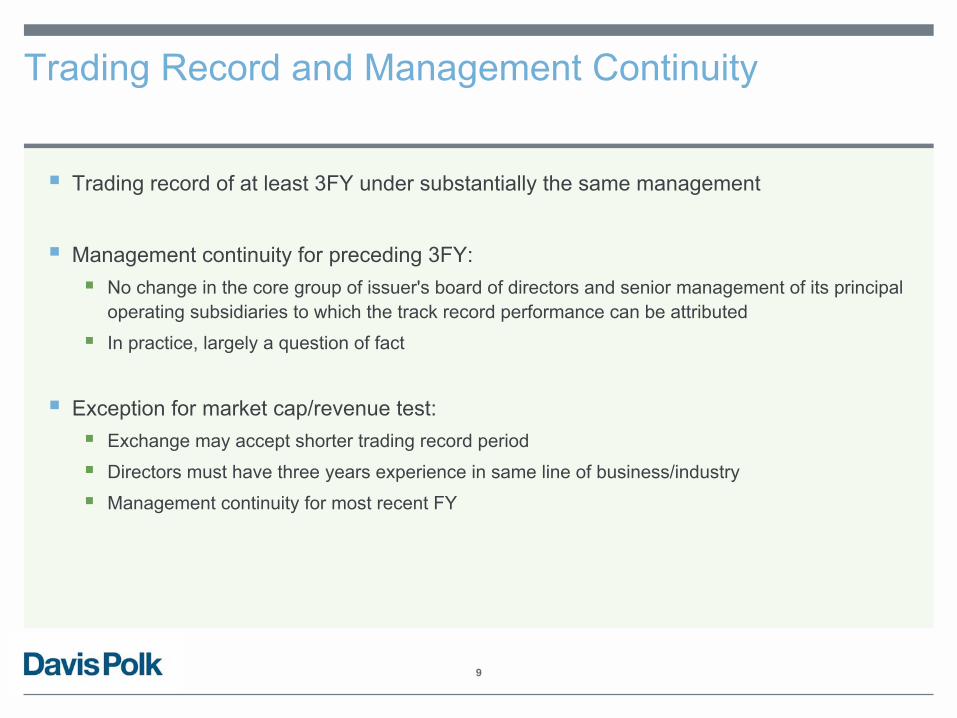

Trading Record and Management Continuity

Trading record of at least 3FY under substantially the same management

Management continuity for preceding 3FY: No change in the core group of issuer's board of directors and senior management of its principal

operating subsidiaries to which the track record performance can be attributed

In practice, largely a question of fact

Exception for market cap/revenue test: Exchange may accept shorter trading record period

Directors must have three years experience in same line of business/industry

Management continuity for most recent FY

10

Ownership Continuity and Control

Ownership continuity and control for most recent FY: Means beneficial ownership and control by the controlling shareholder, and if none, by the single

largest shareholder

Typically, at least 30% of the company has not changed hands during FY3

Take into account: Any formal and informal relationships amongst the shareholders and the nature of such

relationship, whether social, family or otherwise

Arrangement between members of the group (shareholders, management agreements) to understand how "management and control" is consolidated (e.g., actual voting patterns, documentation of historical records of arrangements at the relevant time)

Size of the group, the duration for which each member of the group was a shareholder, and the change (including frequency and size) of shareholdings within the group

11

Special Exceptions

Shorter trading record possible for: Mineral companies

Newly formed project companies to construct infrastructure projects "Infrastructure project" includes construction of "roads, bridges, tunnels, railways, mass transit systems,

water and sewage systems, power plants, telecommunications systems, seaports and airports"

Additional conditions, e.g.:

Long-term concession (at least 15 years) from government

Proceeds used to finance construction (not to repay indebtedness)

Exceptional circumstances with a trading record of at least two years “if desirable in the interests of the issuer and investors”

12

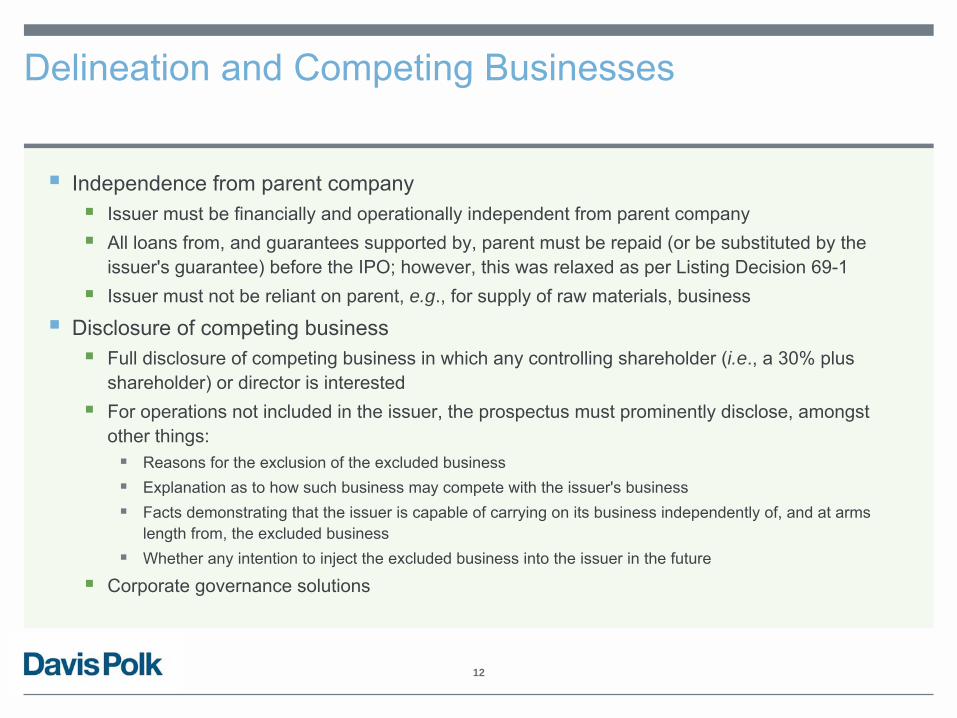

Delineation and Competing Businesses

Independence from parent company Issuer must be financially and operationally independent from parent company All loans from, and guarantees supported by, parent must be repaid (or be substituted by the

issuer's guarantee) before the IPO; however, this was relaxed as per Listing Decision 69-1 Issuer must not be reliant on parent, e.g., for supply of raw materials, business

Disclosure of competing business Full disclosure of competing business in which any controlling shareholder (i.e., a 30% plus

shareholder) or director is interested For operations not included in the issuer, the prospectus must prominently disclose, amongst

other things: Reasons for the exclusion of the excluded business Explanation as to how such business may compete with the issuer's business Facts demonstrating that the issuer is capable of carrying on its business independently of, and at arms

length from, the excluded business Whether any intention to inject the excluded business into the issuer in the future

Corporate governance solutions

13

Public Float

Public float at least 25% of issuer's total issued share capital If issuer has more than one class of shares (e.g., A+H): Public float on all markets at least 25%; but The class of securities being listed on HKSE (e.g., H shares) must not be less than 15% of the total issued share

capital, with an expected market capitalization of not less than HK$50m at time of listing

Top three public shareholders cannot beneficially own more than 50% of shares in public hands “Public” excludes connected person, shareholder who was financed by connected person or who is

accustomed to take instruction from him regarding the shares Public float waivers: Lower public float floor of between 15% to 25% may be granted if market capitalization of the issuer exceeds

HK$10bn SEHK will usually require an offering size of US$1 bn as well Additional waivers available in special cases (e.g., ABC) Further relaxation contemplated under Combined Consultation in 2008; however consultation conclusions not yet

published

D. Primary and Secondary Listings in Hong Kong

15

Primary vs. Secondary

The same listing eligibility requirements apply regardless of primary or secondary listings i.e., secondary listing does not mean lower qualifications

Concessions may be granted for continuing obligations, if primary listing venue / home corporate law has equal protections for public shareholders Listing preparation takes approximately the same amount of time

Cost estimate HKEx fees for secondary listing significantly cheaper (25% of primary, subject to HKEx discretion

to increase the fee if most of the trading takes place in HK)

Typically no significant saving of professionals costs as detailed advice, structuring and negotiations are required for obtaining waivers of HKEx continuing obligations

Where company has dual listings, level of ongoing HK compliance cost depends on regulatory waivers obtained and divergence of requirements between the listing venues

Broadly the same procedures for voluntary withdrawal of listing

16

Secondary Listings in Hong Kong

For introductions: no offer of securities in HK at the time of listing → no liquidity in such securities in the HK market → no existing mechanism for reasonable pricing for trading in the HK market

Special liquidity arrangements are required Company must engage one or more “designated dealer(s)” The designated dealer(s) will be allowed to carry out a number of actions to provide liquidity and facilitate market

price discovery – e.g., short sales on the HK market, borrowing shares from existing holders, purchases on the overseas market

Designated dealer(s) will be engaged for the duration of the designated period (typically two months), as agreed with HKEx

To provide more transparency: daily disclosure on HKEx for a period (e.g., three days) before HK listing of closing prices on the overseas markets where the securities are already listed

Listing with an Offering Listing by Introduction

Listing accompanied by fund-raising in HK (e.g., SBI Holdings)

Existing broad shareholder base, no need for additional capital raising at time of HK listing (e.g.,Vale)

17

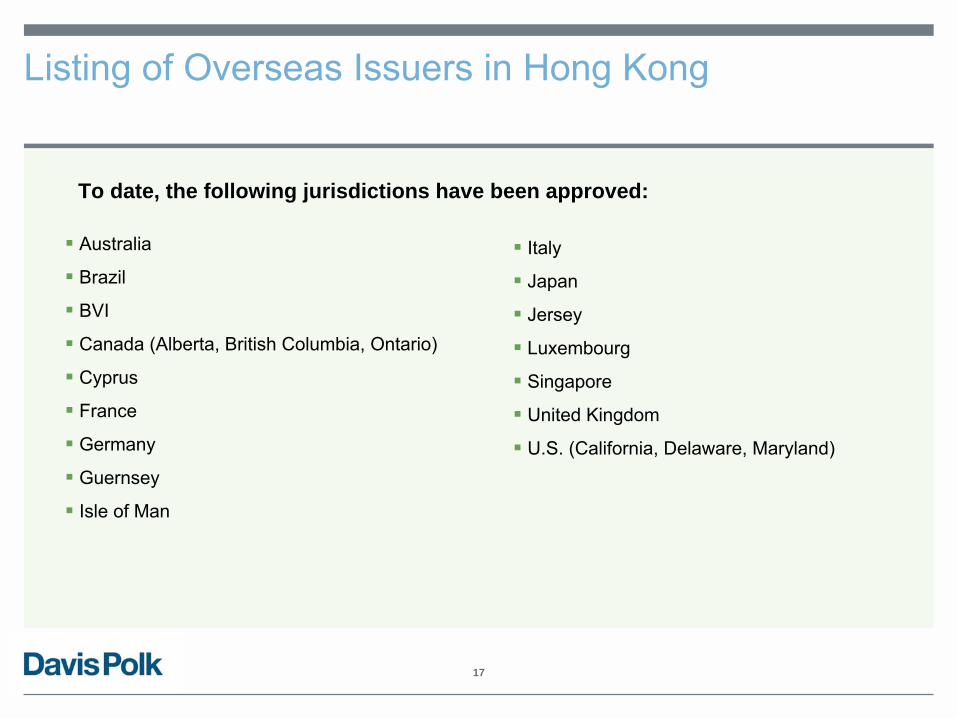

Listing of Overseas Issuers in Hong Kong

To date, the following jurisdictions have been approved:

Australia

Brazil

BVI

Canada (Alberta, British Columbia, Ontario)

Cyprus

France

Germany

Guernsey

Isle of Man

Italy

Japan

Jersey

Luxembourg

Singapore

United Kingdom

U.S. (California, Delaware, Maryland)

E. Timeline of a Hong Kong Listing

19

The Listing Application Process

A1 Filing(25 clear days)

Form A1ProspectusListing feeSponsors’ undertakingSponsors’ independence

statementWaiver applications

15-day documents

Profit forecastCashflow forecast

4-day documents

Post-hearing documentsFinal form documentsSponsors due

diligence declarationExpert’s consentsTranslator’s certificateSponsors’ certificate

on translator

Listing approvalListing Committee Hearing

Hearing proof prospectusSponsors working capital

letterCSRC approval (for H share)New listing particularsFinancial ratios

HKEx Comments

20

After the Hearing

Day 1Public offer

opensat 9am

Day 4Public offer

closesat 12 noon

Day 10Closing at 8am

and Listingat 10am

Day 5Pricing, sign International Underwriting

Agreement and print Final Offering

Circular

Day 8Announce

results

Day 9Post share

certificates and refund

cheques

Days 6-7Balloting

andAllocation

Listing Committee letter(Friday)

Week 1 Monday:Publish research and start blackout period and pre-marketing

Week 2 Thur-Fri:Bulk print and register Hong Kong prospectus

Week 2 Monday:Post WPIP and start roadshow

Week 3 Mon-Wed:Hong Kong public offer (see below)

Week 3 Thur-Fri:Pricing(see below)

Week 4:Closing and listing(see below)

End of public offer + 30 days:Exercise greenshoe and end of stabilization period

Week 1 Friday:Print red-herring and submit WPIP