liner shipping economics - harbour agency · pdf fileliner shipping economics j.o. jansson...

TRANSCRIPT

Liner Shipping Economics

Liner Shipping Economics J.O. Jansson Swedish Road and Traffic Research Institute Linkoping

and

D. Shneerson Department of Economics University of Haifa

London New York CHAPMAN AND HALL

First published in 1987 by Chapman and Hall Ltd 11 New Fetter Lane, London EC4P4EE Published in the USA by Chapman and Hall 29 West 35th Street, New York NYlO001

© 1987 J.O. Jansson and D. Shneerson

Softcover reprint of the hardcover 1st edition 1987

All rights reserved. No part of this book may be reprinted, or reproduced or utilized in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any iriformation storage and retrieval system, without permission in writing from the publisher.

British Library Cataloguing in Publication Data

Jansson, Jan Owen Liner shipping economics. I. Shipping 2. Ocean liners I. Title II. Shneerson, Dan 387.5'1 HE593

ISBN-13: 978-94-010-7914-3

Library of Congress Cataloging in Publication Data

Jansson, Jan Owen. Liner shipping economics.

Bibliography: p. Includes index. l. Shipping. 2. Shipping-Rates. 3. Shipping conferences.

I. Shneerson, Dan. II. Title. HE582.J36 1987 387.5'1 86-20718

ISBN-13: 978-94-010-7914-3 DOl: 10.1007/978-94-009-3147-3

e-ISBN-13: 978-94-009-3147-3

Contents

Preface ix

PART I THE LINER SHIPPING INDUSTRY 1

1 Characteristics of demand and supply of liner shipping 3 1.1 An aggregate picture of seaborne trade and the world fleet

tonnage 3 1.2 The development of the shares of the world fleet: developed

countries, flags of convenience and developing countries 7 1.3 Liner shipping, shipping for hire and 'own shipping' 15 1.4 The relative size of the liner shipping industry 22 1.5 Recent development in general cargo shipping 22 1.6 Geographical aspects of liner shipping 30

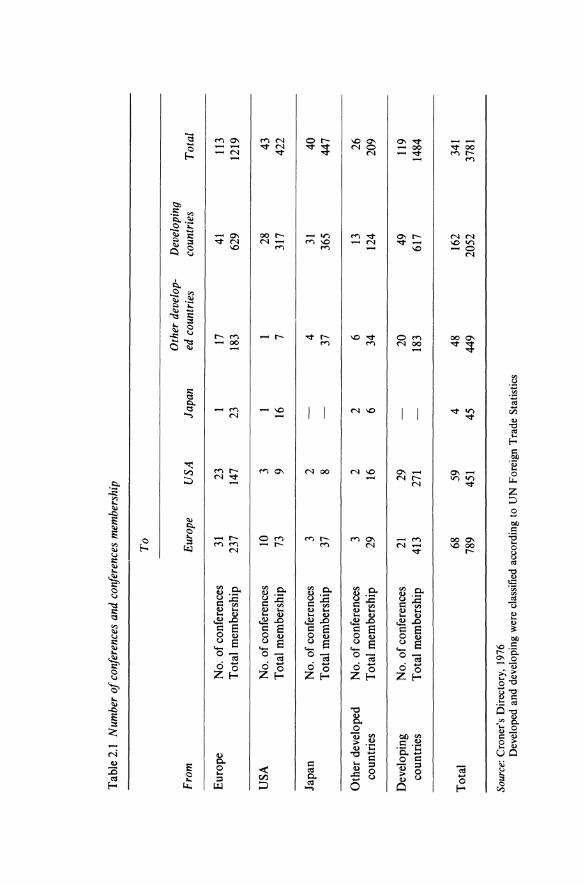

2 Market organization: the conference system 35 2.l The scope of the conference system 35 2.2 Conference organization and main activities 35 2.3 Why conferences? 42 2.4 Concluding remarks 47

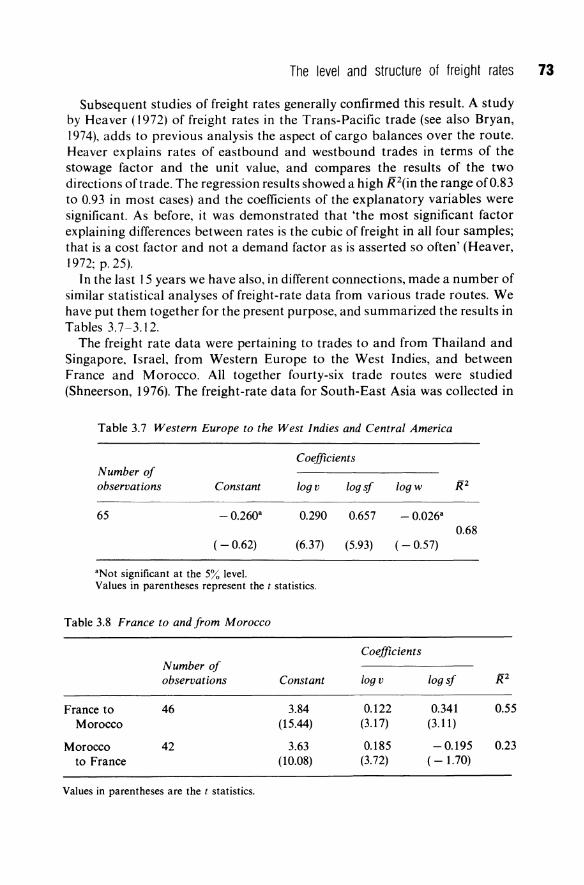

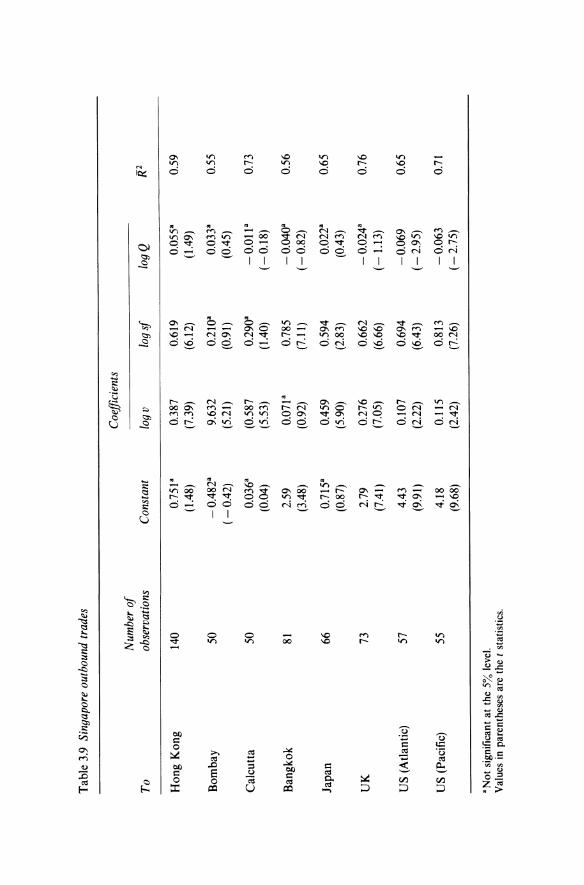

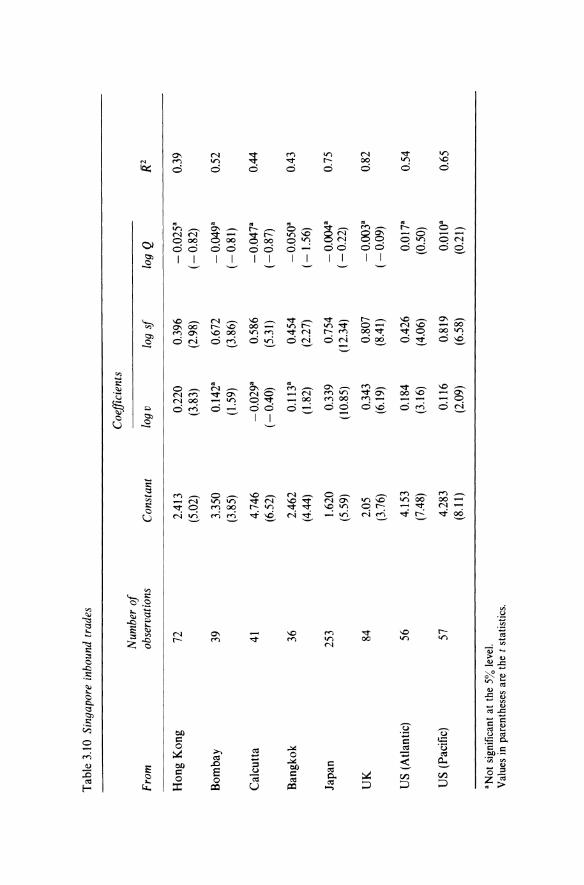

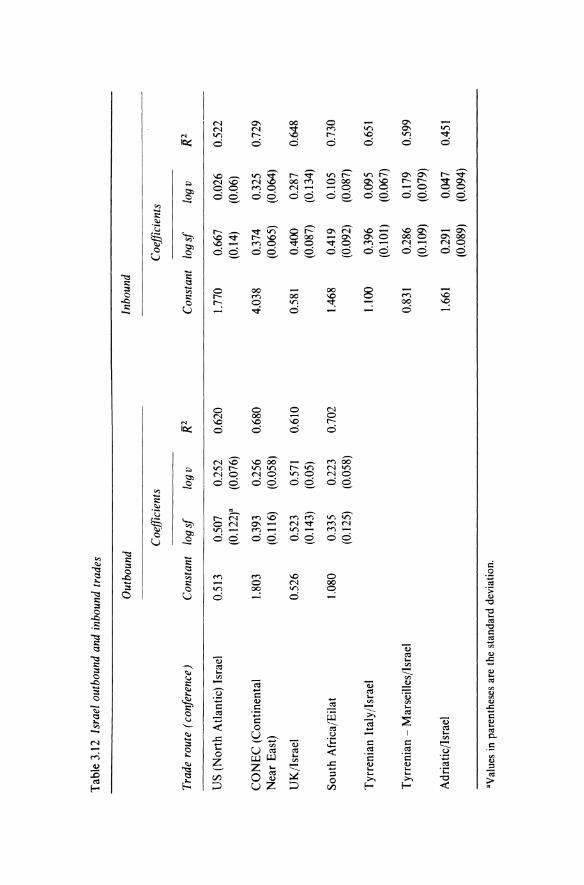

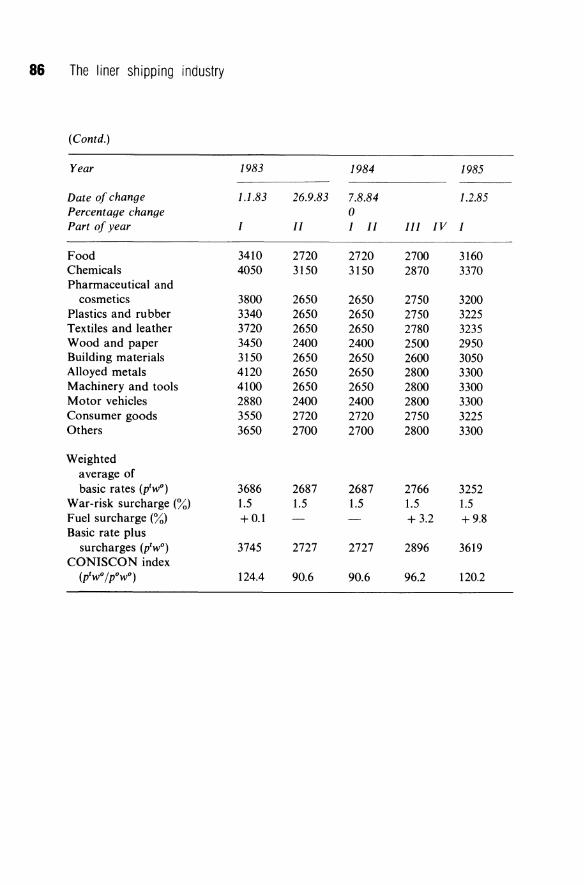

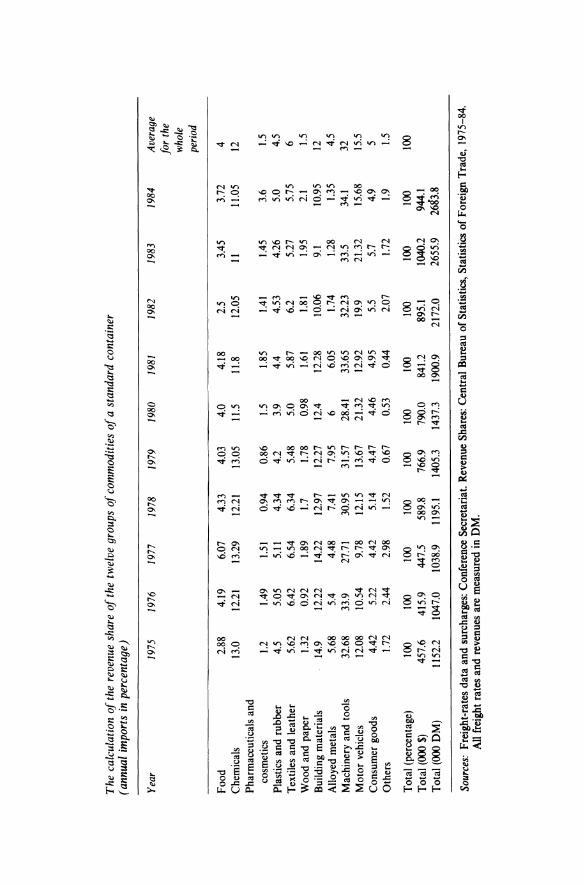

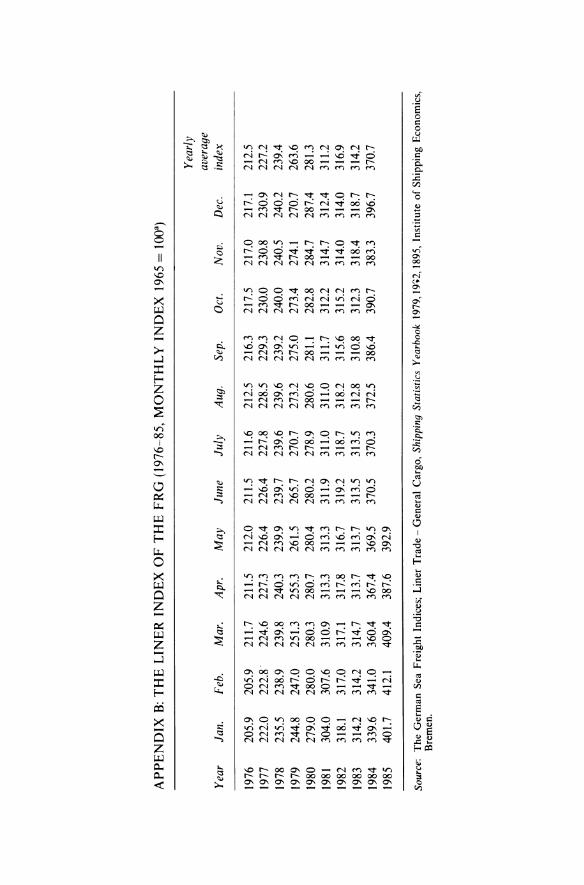

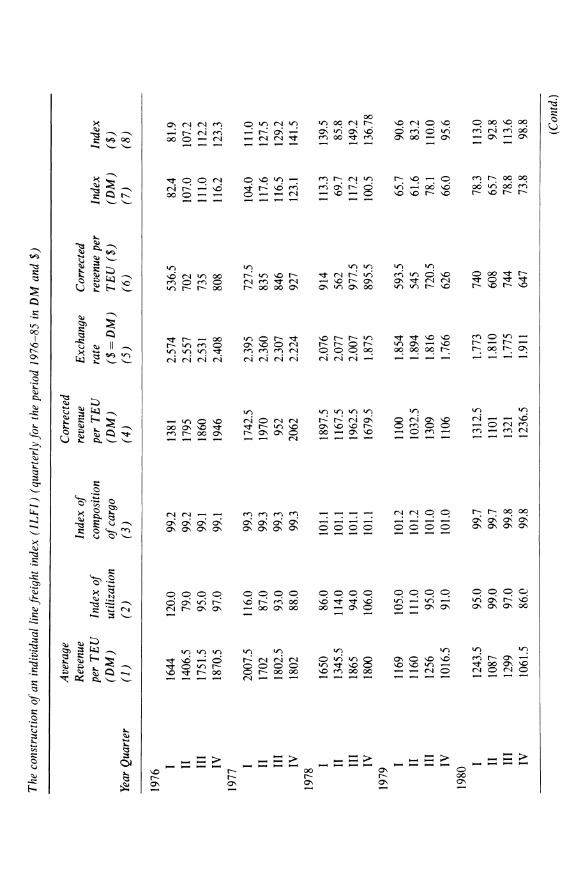

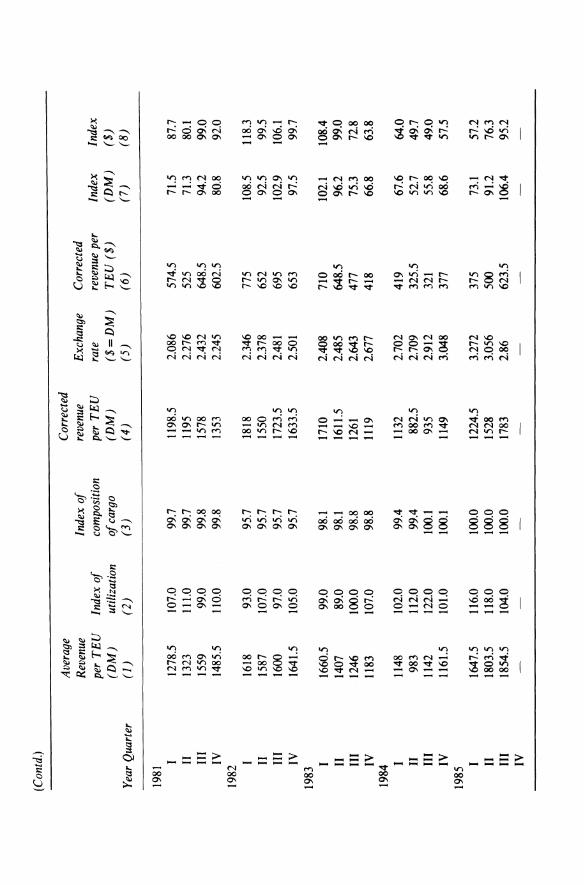

3 The level and structure of freight rates 49 3.1 The general level of freight rates 49 3.2 The structure of freight rates 66 Appendix A: The construction of the CON/SCaN index (1975-85) 84 Appendix B: The liner index of the FRG (1976-85) 88 Appendix C: The construction of an individual line freight rate index 89

4 The art of charging what the traffic can bear 94 4.1 The main form of price discrimination in liner shipping 94 4.2 The role of commodity value for shipping demand elasticity 95 4.3 The role of competition from other sources of goods supply for

shipping demand elasticity 100 4.4 Competition from 'outsiders' and other modes of transport 107 4.5 Summary and conclusions 107

PART II LINER SERVICE OPTIMIZATION 111

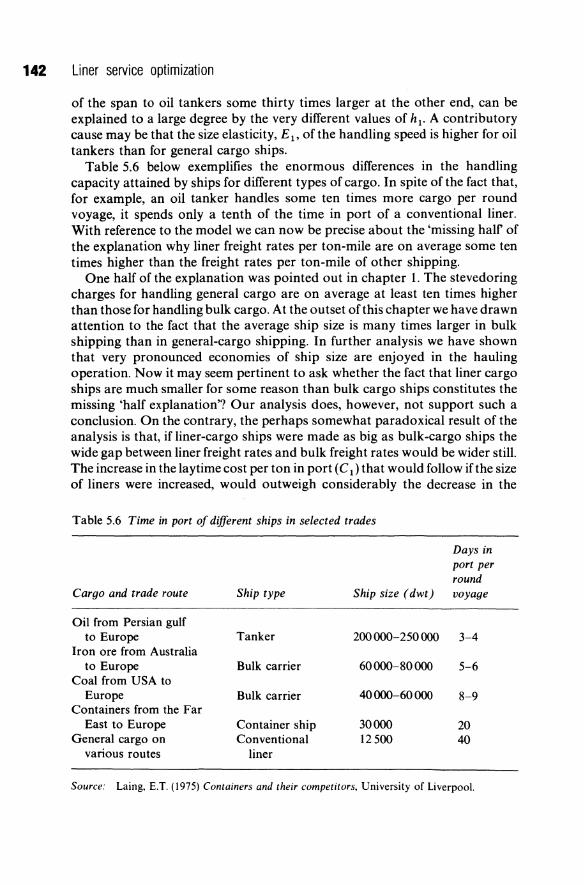

5 Ship size and shipping costs 113 5.1 Sizes of ships of different categories: The statistical picture 113

vi Contents

5.2 Plant-size economies in general 5.3 The three ship capacities 5.4 The model 5.5 Estimation of ship size elasticities of handling and hauling

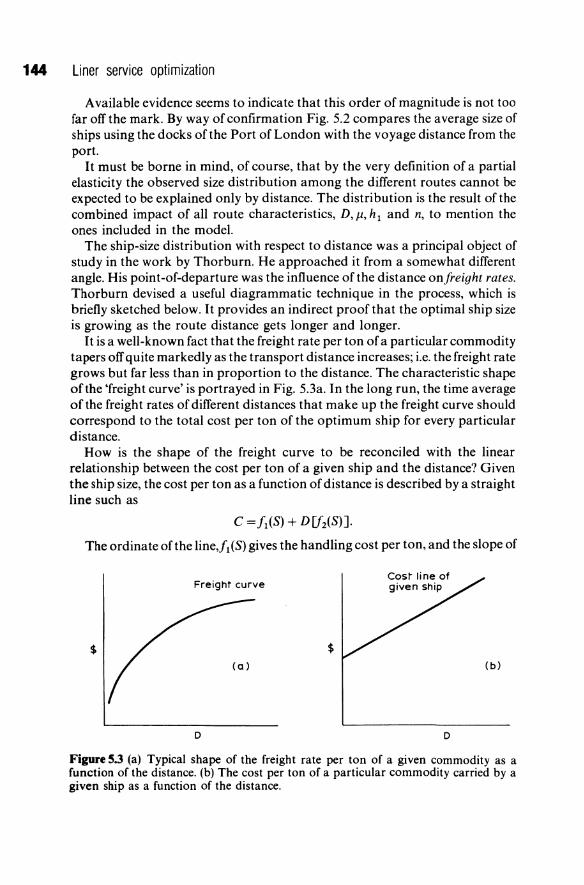

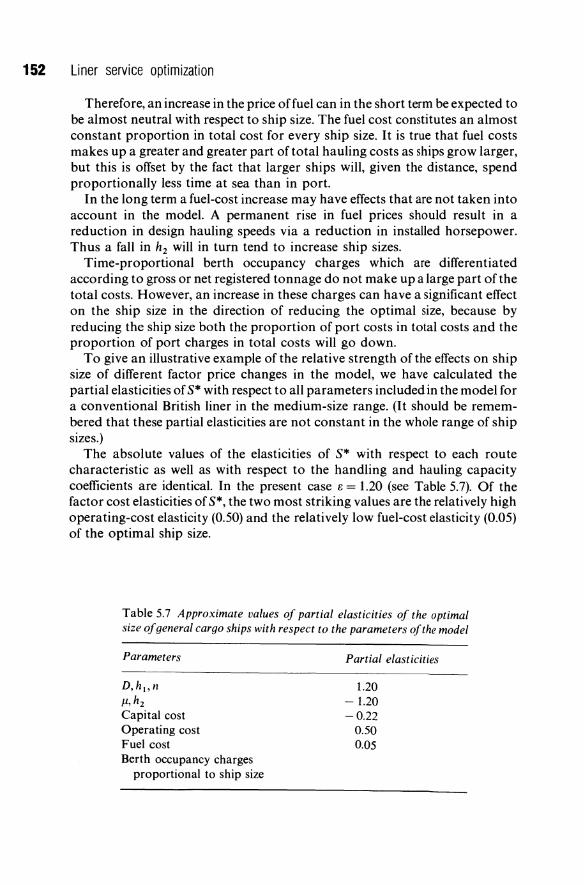

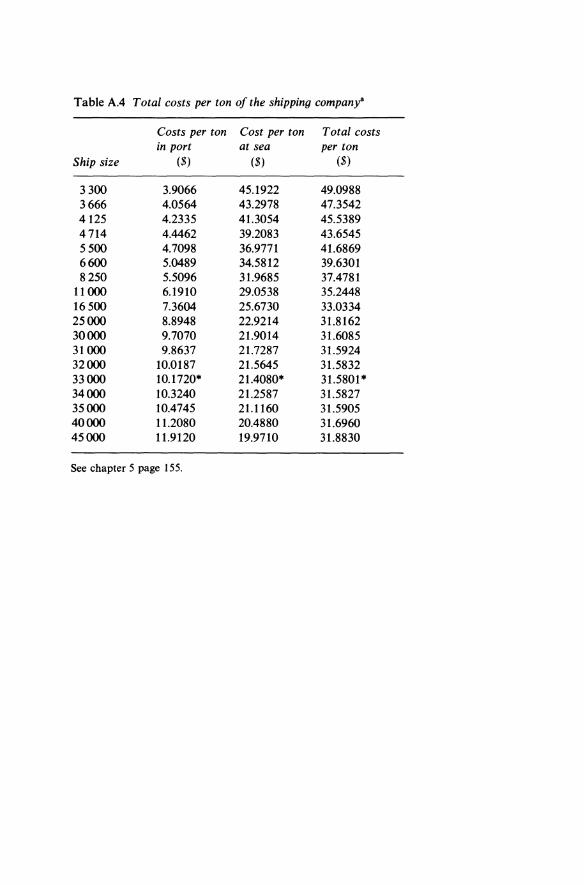

capacities and factor costs 5.6 Economies of size at sea - diseconomies of size in port 5.7 Optimal ship size 5.8 Analysis of the effect on optimal ship size of parameter changes

in the model 5.9 The optimal size of a palletized reefer ship: A case study 5.10 Towards a model of ship size growth

6 Multi-port calling versus trans-shipment 6.1 The general problem: Feeder-transport cost minimization in a

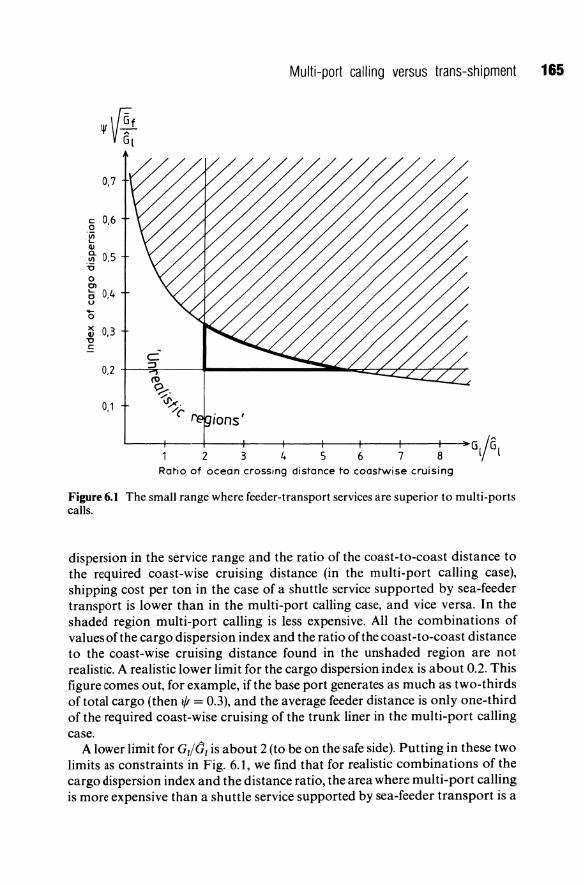

given service range 6.2 The specific problem: The potential of sea-feeder transport 6.3 The very large container carriers and feeder services

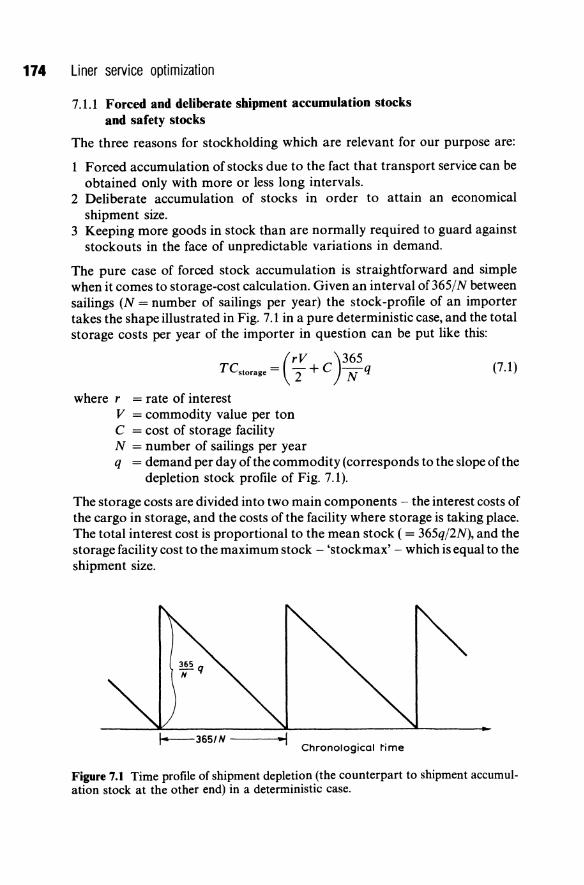

7 Shippers' costs of sailings infrequency and transit time 7.1 Storage costs 7.2 Costs of sailings infrequency and transit time for goods which are

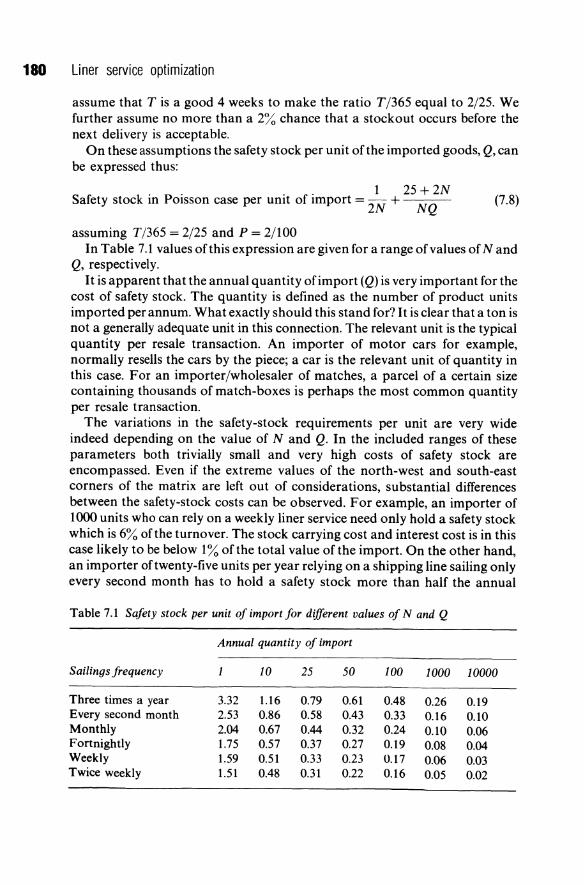

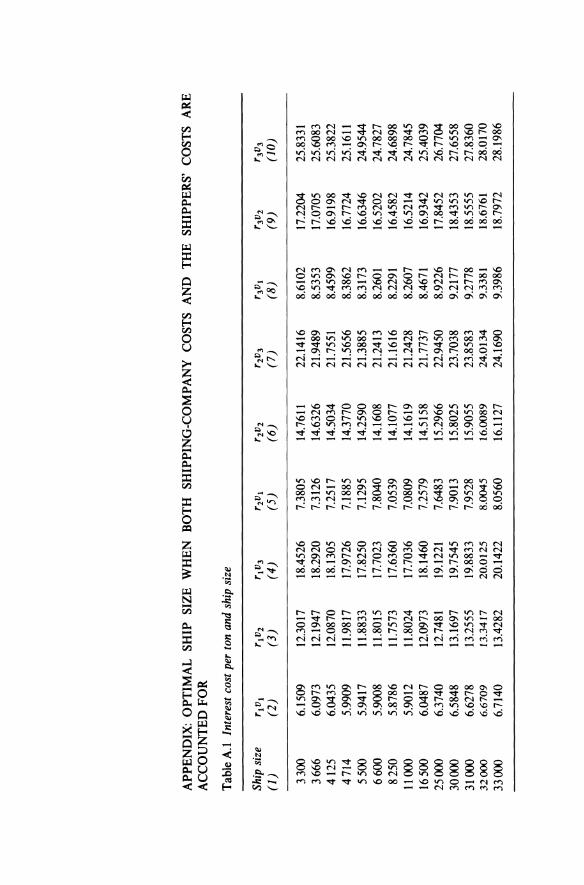

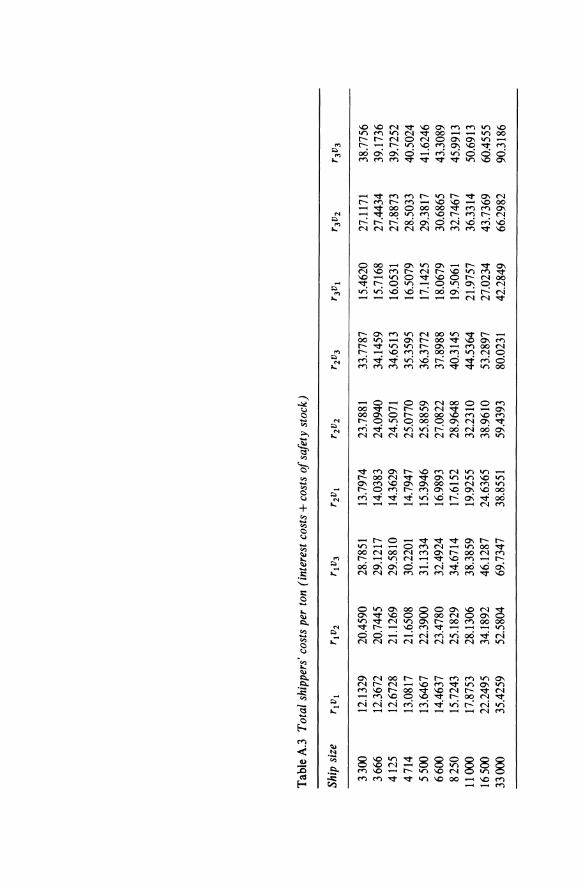

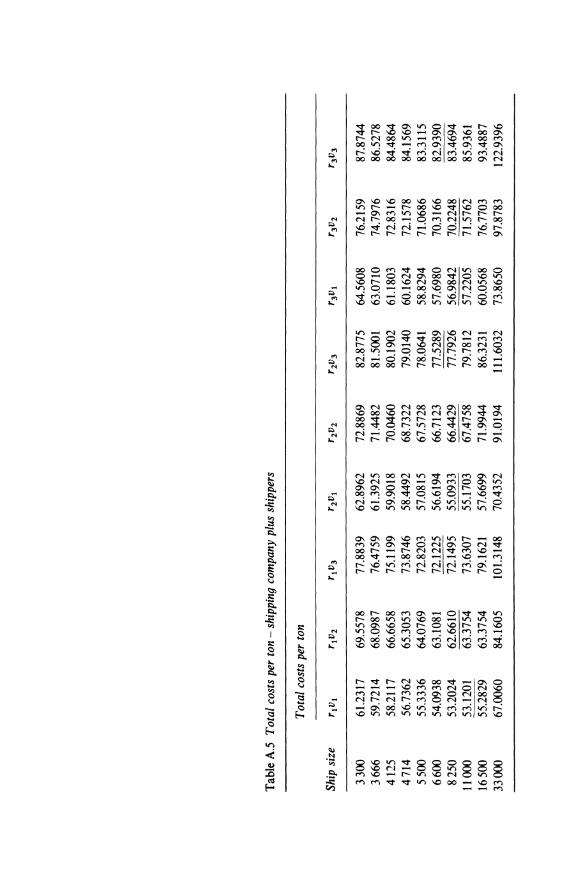

not stored by importers 7.3 Loss of value of perishable goods 7.4 How important are shippers' costs? Appendix: Optimal ship size when both shipping company

costs and the shippers' costs are accounted for

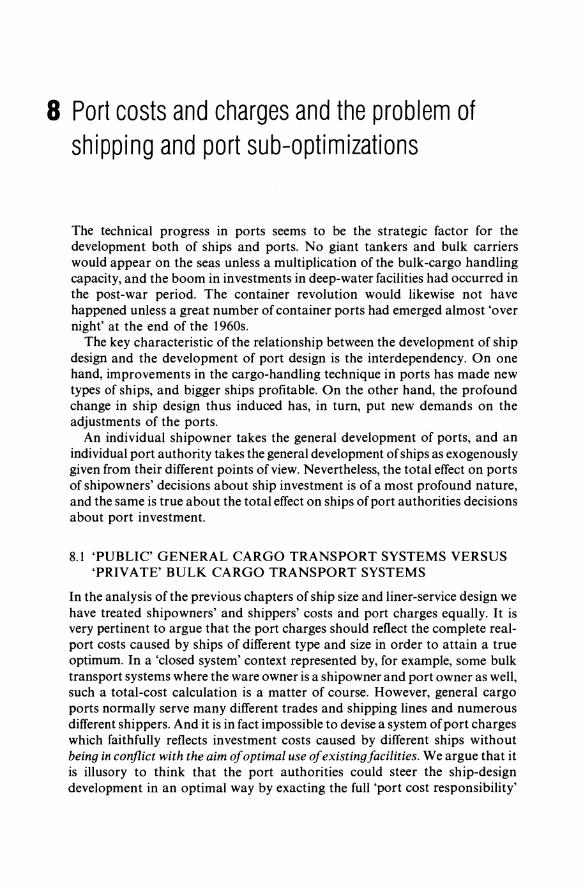

8 Port costs and charges and the problem of shipping and port sub-optimizations

8.1 'Public' general cargo transport systems versus 'private' bulk cargo transport systems

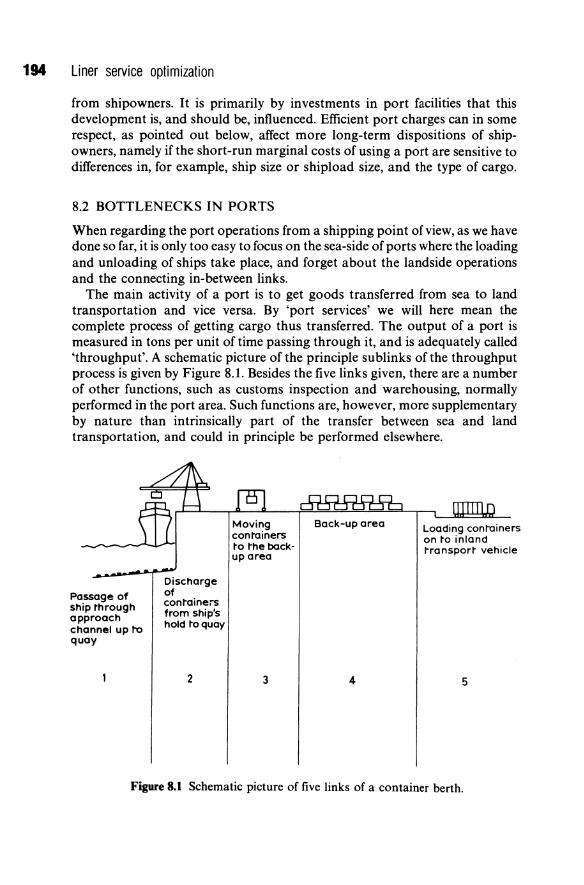

8.2 Bottlenecks in ports 8.3 Port charges as a means of coordinating shipping and port

operations

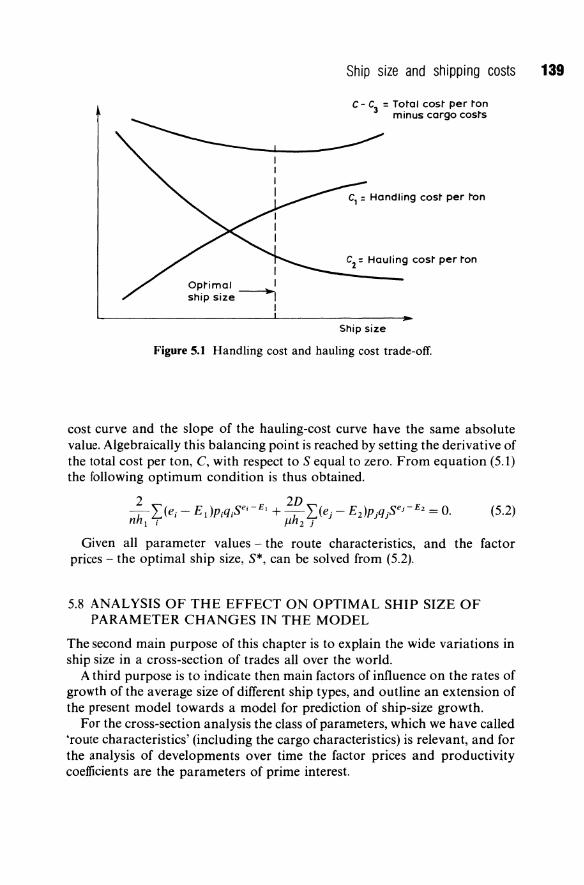

9 A cost minimization model of a liner trade 9.1 A liner trade model - purpose, scope and assumption 9.2 Total producer and user costs 9.3 Optimal ship size, multi-port diversion, and frequency of sailings 9.4 The minimum total cost per ton

PART III ECONOMIC EVALUATION OF THE CONFERENCE SYSTEM

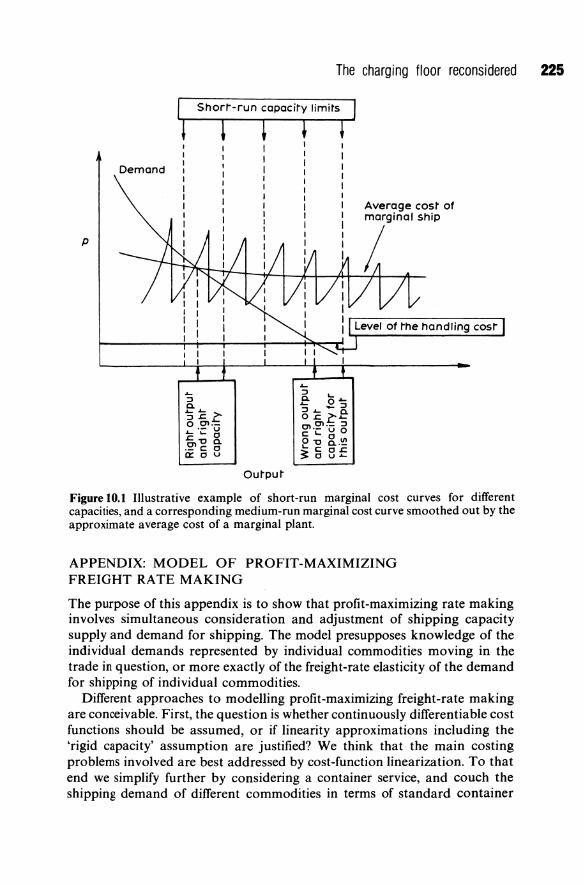

10 The charging floor reconsidered 10.1 Economies of scale?

115 117 117

123 135 138

139 147 149

157

157 157 171

173 173

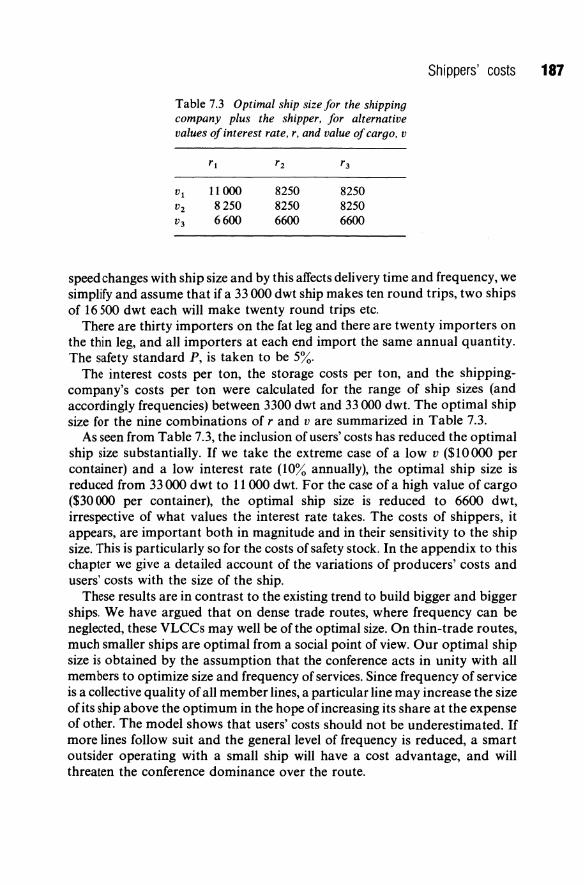

183 183 184

188

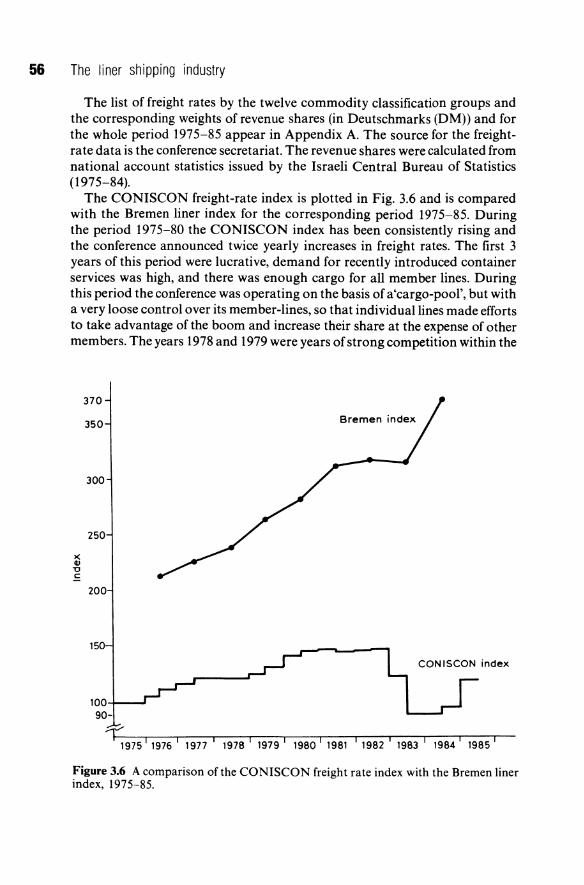

193

193 194

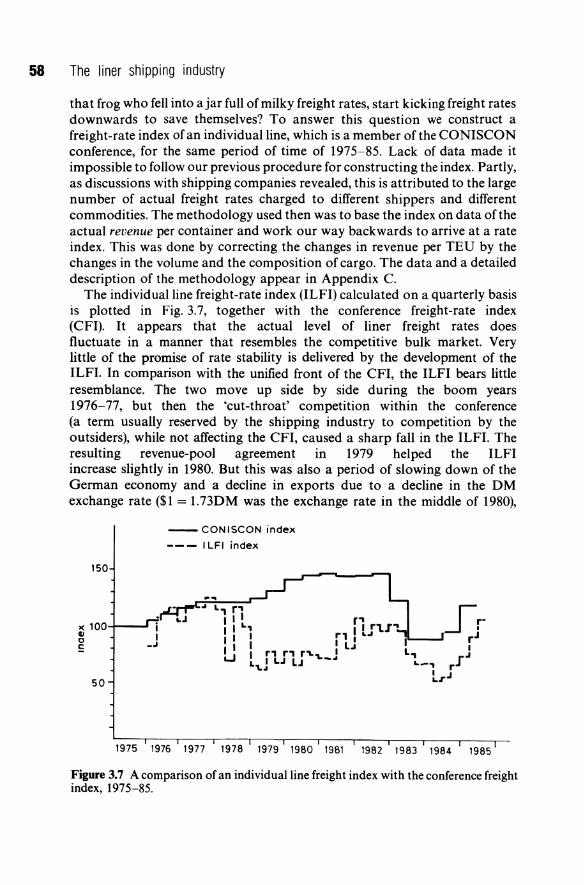

200

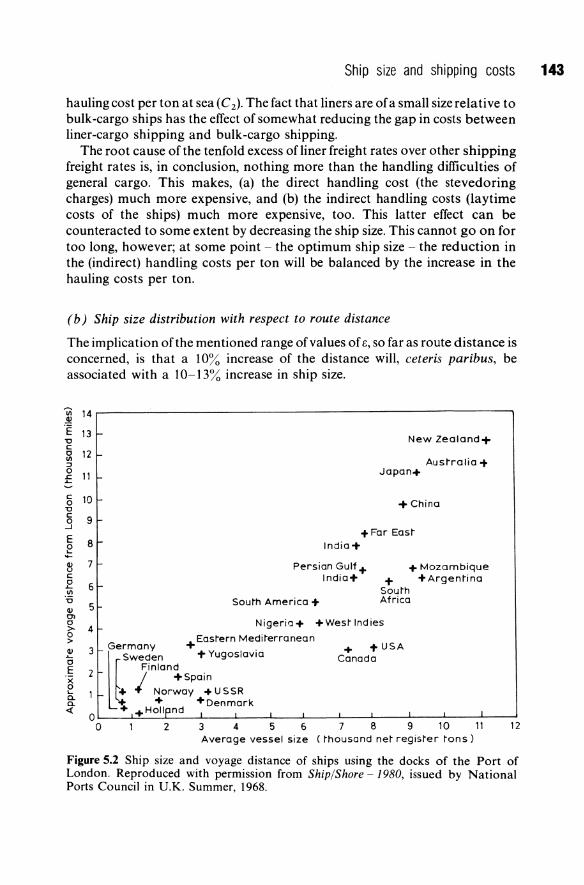

205 205 207 211 213

217

219 219

Contents vii

10.2 Common cost and factor indivisibility 223 Appendix: Model of profit-maximizing freight rate making 225

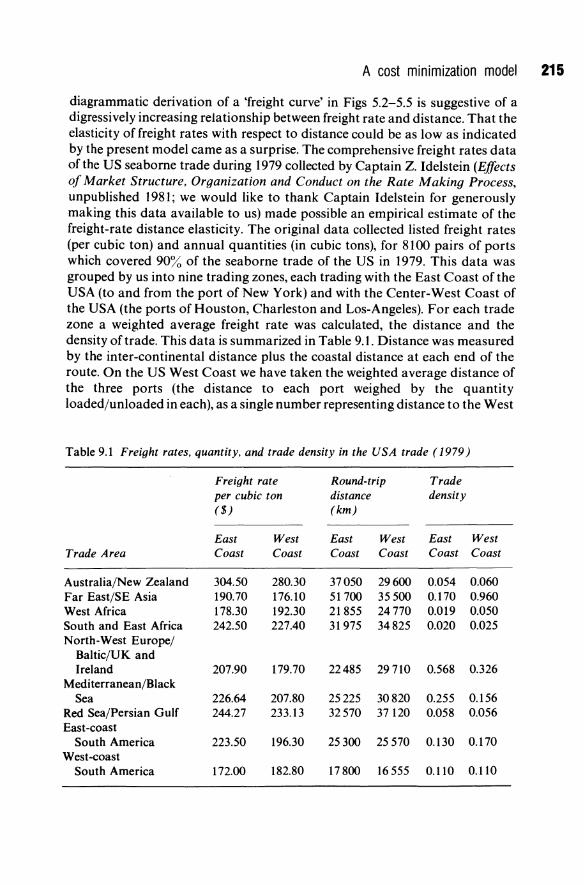

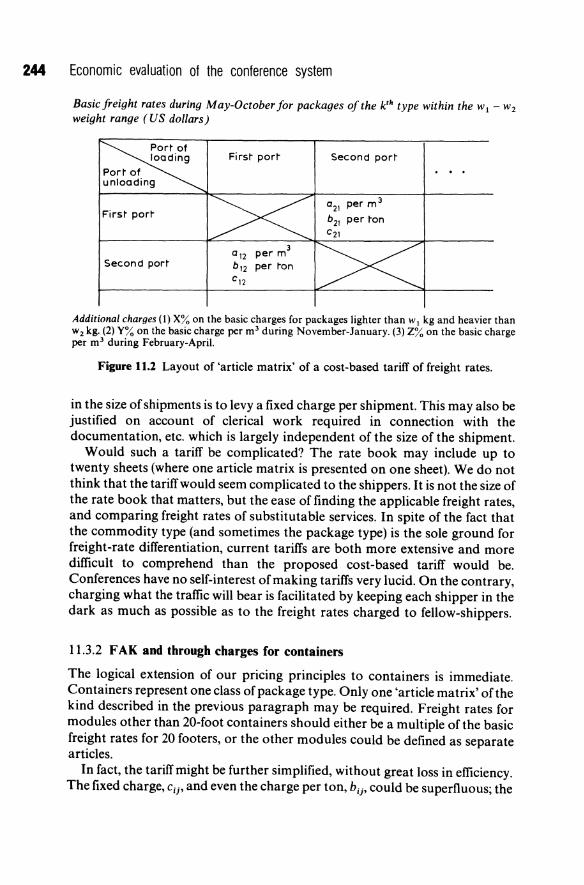

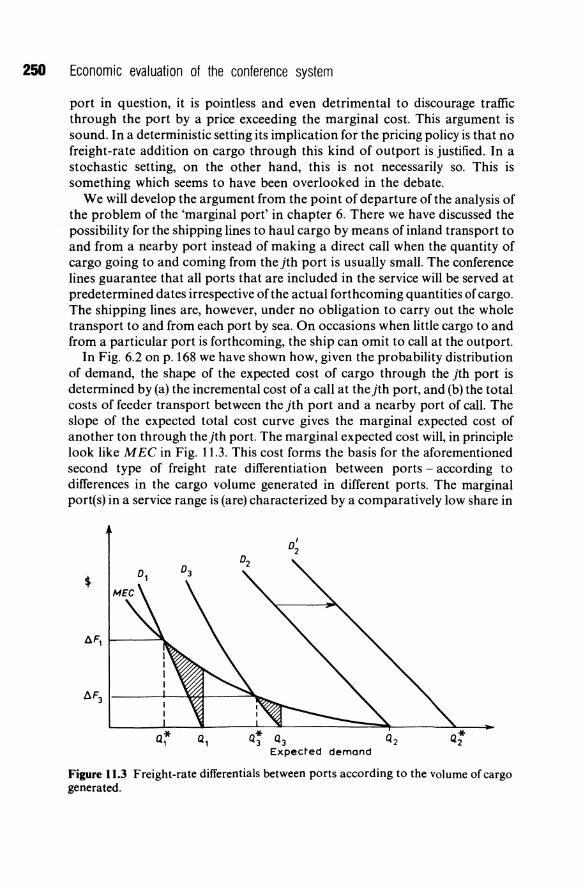

11 The freight rate structure is out of line with the marginal cost structure 238

11.1 Principles of marginal cost-based tariffs 238 11.2 Cross-subsidization between commodities 239 11.3 Excessive averaging of freight rates: Some suggestions for

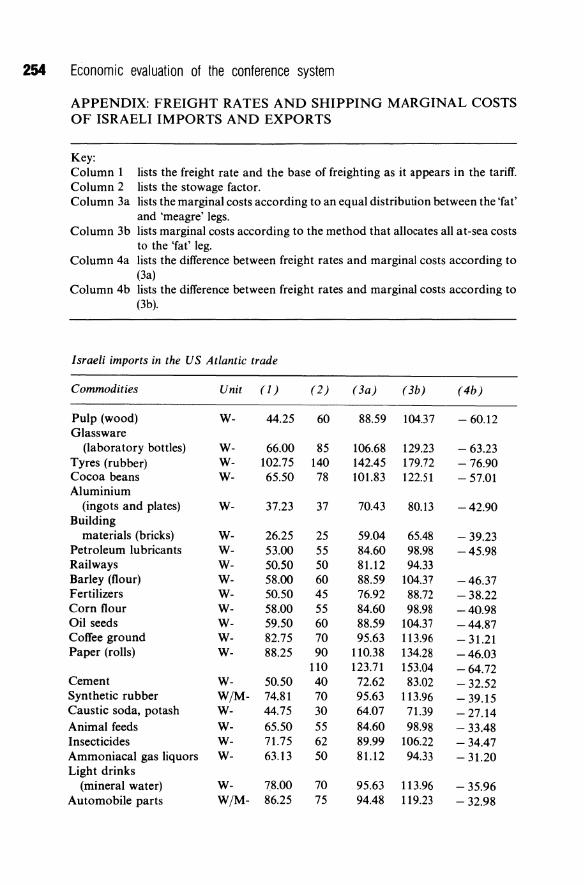

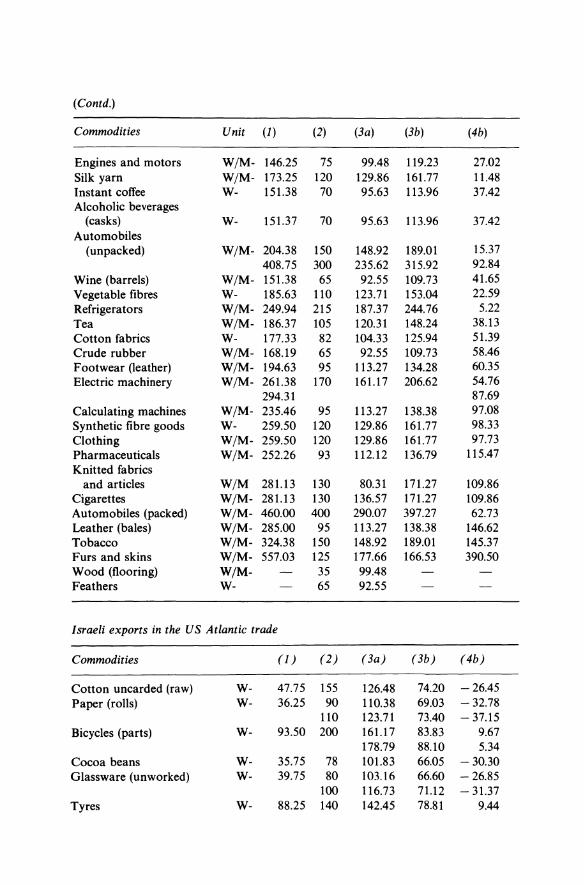

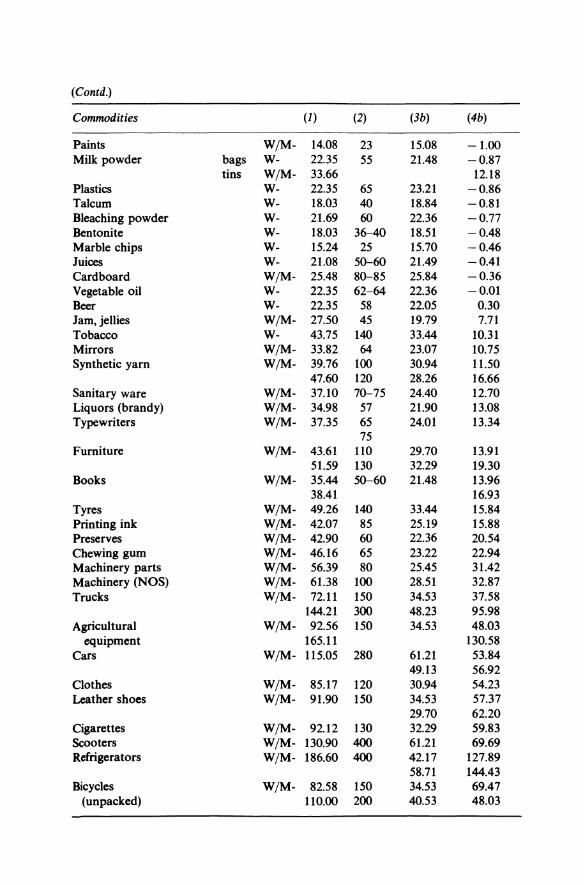

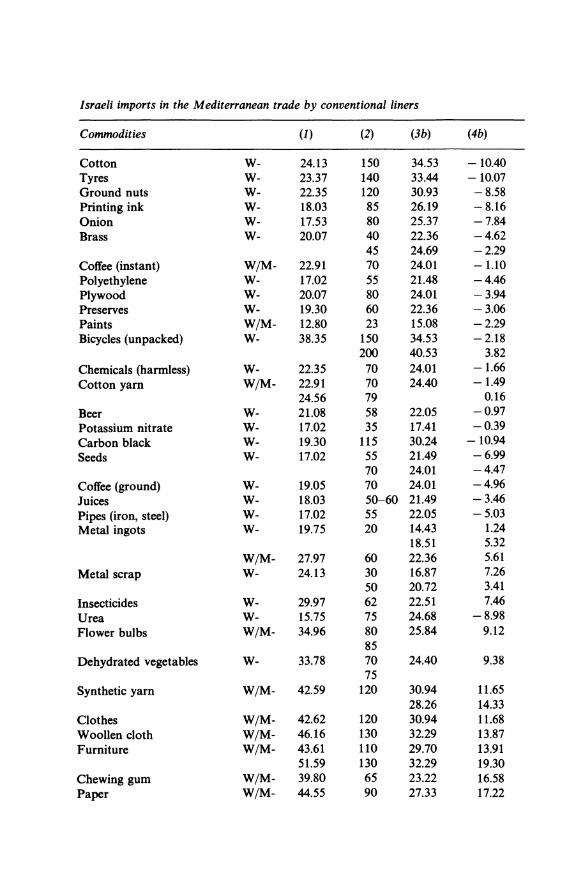

reforming the tariff construction 242 11.4 Further aspects of a cost-based freight rate structure 247 Appendix: Freight rates and shipping marginal costs

of Israeli imports and exports 254

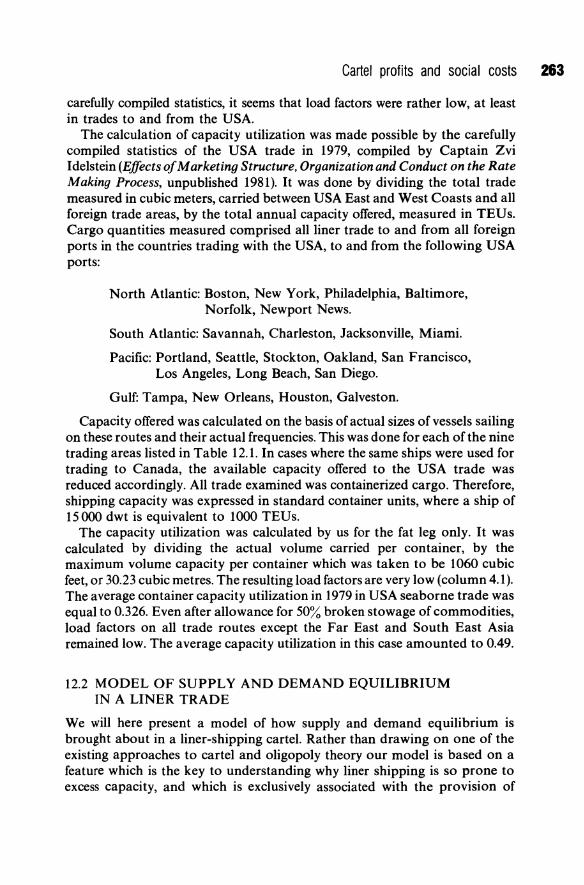

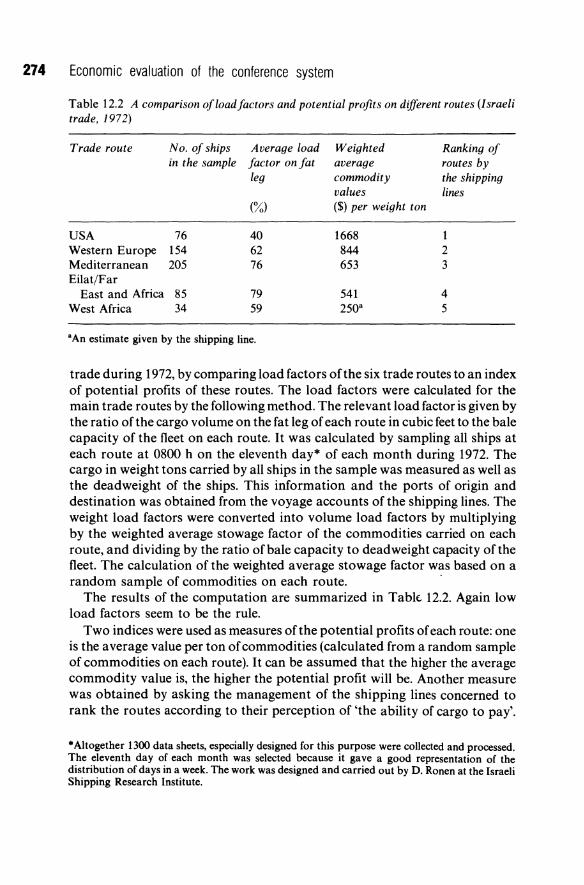

12 Potential cartel profits become social costs 264 12.1 Empirical evidence of low load factors in liner shipping 264 12.2 Model of supply and demand equilibrium in a liner trade 265 12.3 Some evidence of a negative relationship between the load factor

and the profit potential 273 12.4 Excessive service competition 275

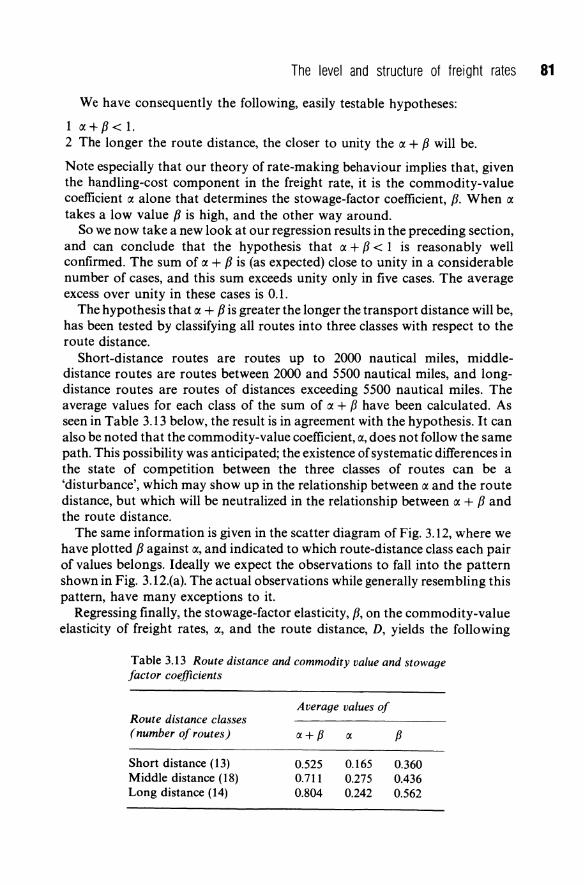

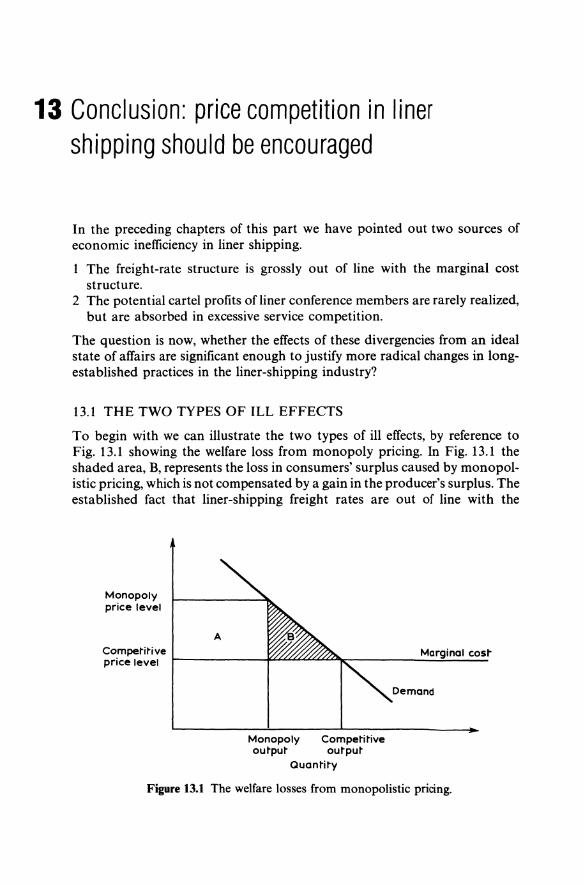

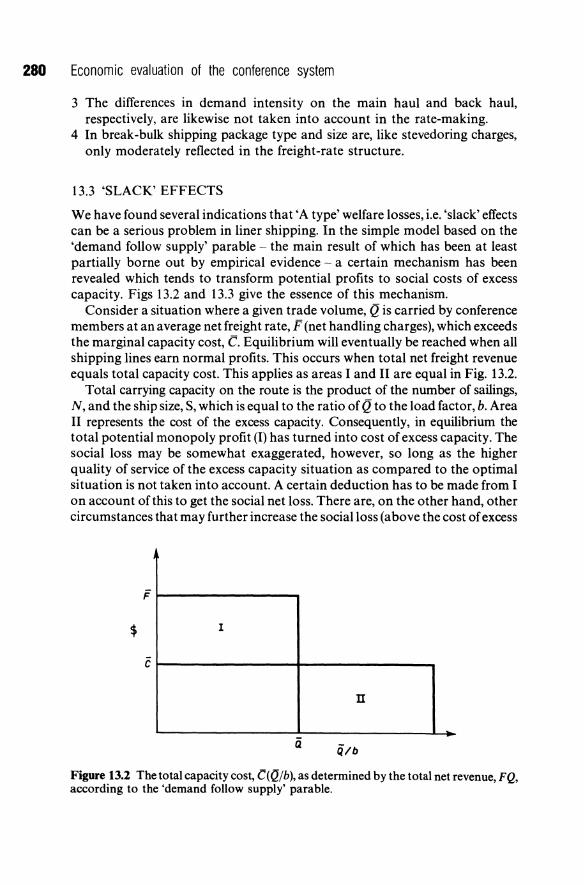

13 Conclusion: price competition in liner shipping should be encouraged

13.1 The two types of ill effects 13.2 Allocative inefficiency effects 13.3 'Slack' effects 13.4 Encourage price competition and service coordination 13.5 Recent attempts of reforming liner conference practices 13.6 Problems of regulating international liner shipping 13.7 Hopes for the future

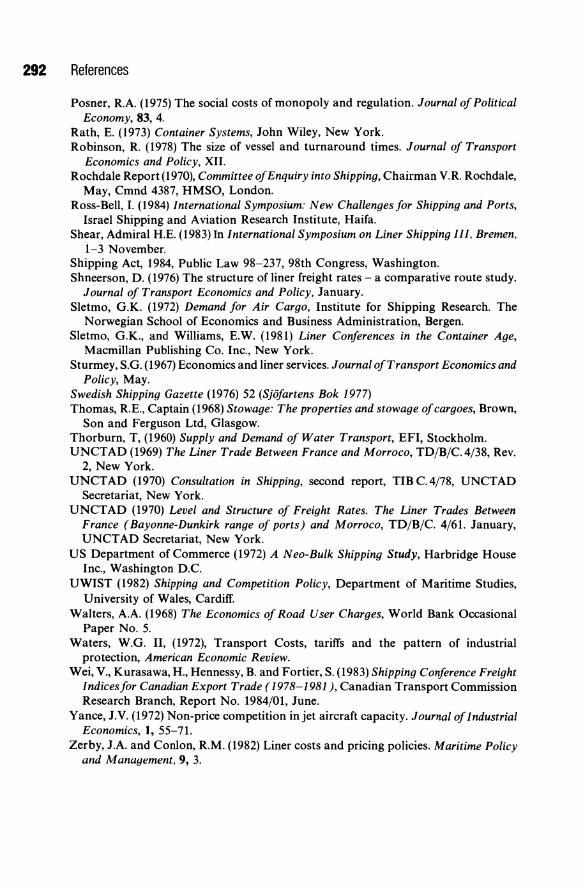

References

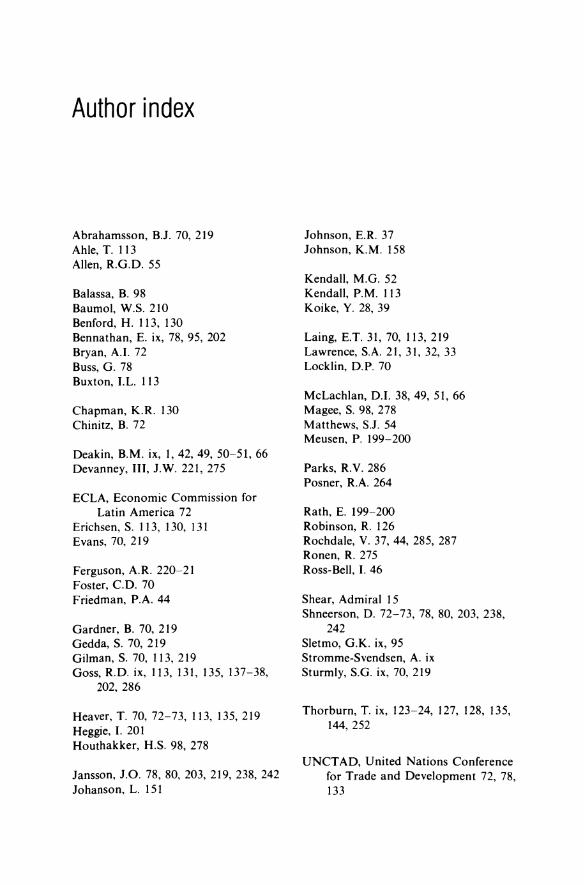

Author index

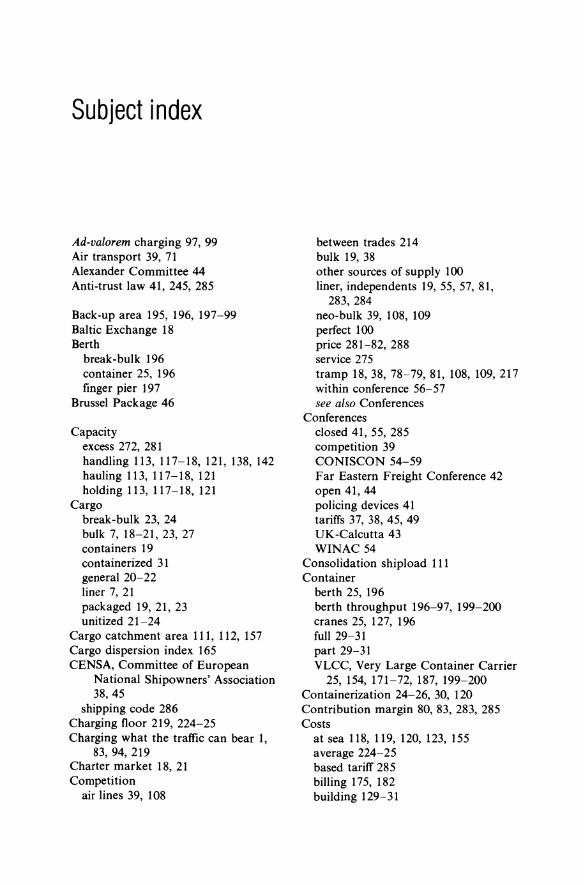

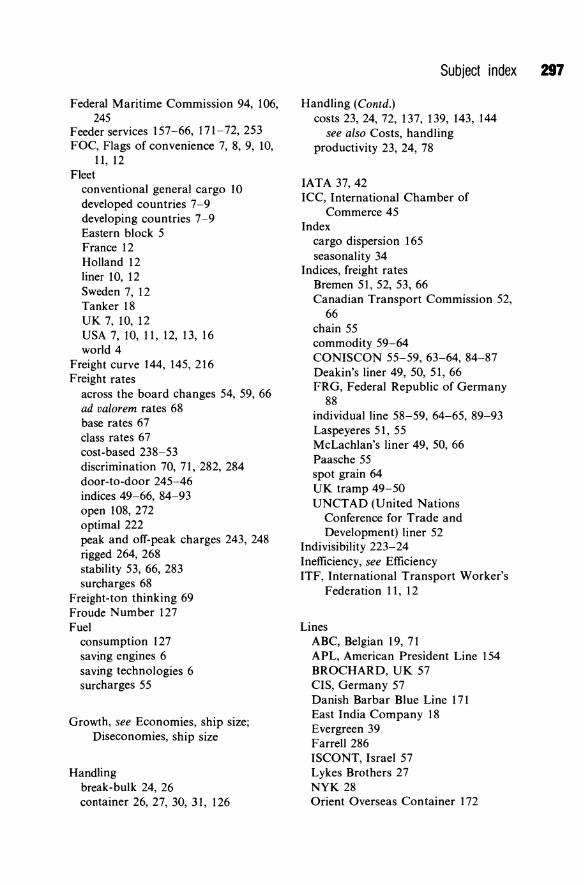

Subject index

276 276 277 280 281 285 286 287

289

293

295

Preface

The importance of international liner shipping needs little emphasizing. A large majority of international trade moves by sea, and the liner shipping share in total freight revenue exceeds one-half. Notwithstanding, people in general know surprisingly little about the basic facts of the liner shipping industry, and, in particular, about the economics ofliner shipping. Perhaps because it is an international industry, where shipping lines flying many different flags participate, it has tended to fall in between national accounts of domestic industries. Even transport economists have, generally speaking, treated liner shipping rather 'stepmotherly'; besides the work of Bennathan and Walters (1969), a relatively small group of specialized maritime economists, including A. Stromme-Svendsen, T. Thorburn, S. Sturmey, R. Goss, and B.M. Deakin, have in the post-war period made important contributions to the subject, but so far no coherent and reasonably comprehensive treatise of liner shipping economics has appeared. The first purpose of the present volume is therefore obvious: to provide just that.

The book is divided in three parts: Part I The liner shipping industry; Part II Liner service optimization; Part III Economic evaluation of the conference system. Needless to say, all three parts concur to fulfill the first purpose of providing a complete book of liner shipping economics. In Part II a more or less separate, second, purpose has been to develop analytical tools for liner service optimization.

Thereby we use different approaches. First we develop general models of, for example, ship-size optimization, the choice between multi-port calling and trans-shipment, etc. so far as it is fruitful to generalize. Then the general principles derived are illustrated by case studies or practical examples, which hopefully serve the double purpose of (i) conveying to the reader something of the reality of seaborne freight transport, as well as (ii) demonstrating the usefulness of sound theoretical underpinning of empirical studies of liner shipping operations.

A third purpose is to make substantial contribution to the long controversy over the omnipresent price cartels in liner shipping known as liner conferences. This is a very complex and difficult issue, especially in the present period of thorough structural change in liner shipping both technologically and organizationally, which could be sufficient for a whole book - the most recent example is Sletmo and Williams (1981). The present discussion of this longstanding issue is a natural continuation of the general economic analysis of the liner shipping industry in Parts I and II. The main stumbling block is, and has always been, misleading conceptions of the pricing-relevant marginal cost of scheduled transport services. A good century of administered liner freight rates

x Preface

has left costing principles in liner shipping lagging. We suggest various improvements in this field, but realize that the only certain way of exposing costing deficiencies is by freer pricing. Encouragement of price competition does not necessarily mean that all liner conferences have to be dissolved, but rather a change of object ofthe conferences from price fixing to coordination of sailings (schedules), ports of call and feeder services.

Writing this book, we have accumulated debts to many people, not the least to our families. Going back to where it started, our interest in the subject was awakened by working with Professors Thorburn, Walters, and Bannathan; later, contacts with friendly people from the shipping and port industries have been an invaluable factor of production. Informants are too many to mention individually, however, Nachum Gonzarsky of Zim Lines read chapters 1 and 2 and made valuable comments, for which we are grateful, and Y osi Sela of Zim assisted in the construction of the liner freight-rate indices. Shlomit ErgonKarlin devoted a lot of her time to the empirical work of chapters 1,5 and 9 and helped in the organization of the whole manuscript, which we gratefully acknowledge.

Many thanks to the EI-Yam Chair for Shipping and Ports which has generously financed the project in the final stages.

Haifa. October 1985 Jan Owen Jansson Dan Shneerson

PART THE LINER SHIPPING INDUSTRY ONE

In this part we describe the liner shipping industry from different points of view. In chapter 1 we take up some important characteristics of demand and supply of liner shipping including the types of cargo, ships, and trade routes involved. In chapter 2 the very specific market organization is described.

Practically all international liner shipping is organized as routespecific price cartels known as liner conferences. The conference system has existed for more than a century, and naturally has been subject to much discussion, but comparatively little regulatory action. We give a short historical background (see also Deakin, 1973), and outline recent tendencies in national as well as international shipping policy.

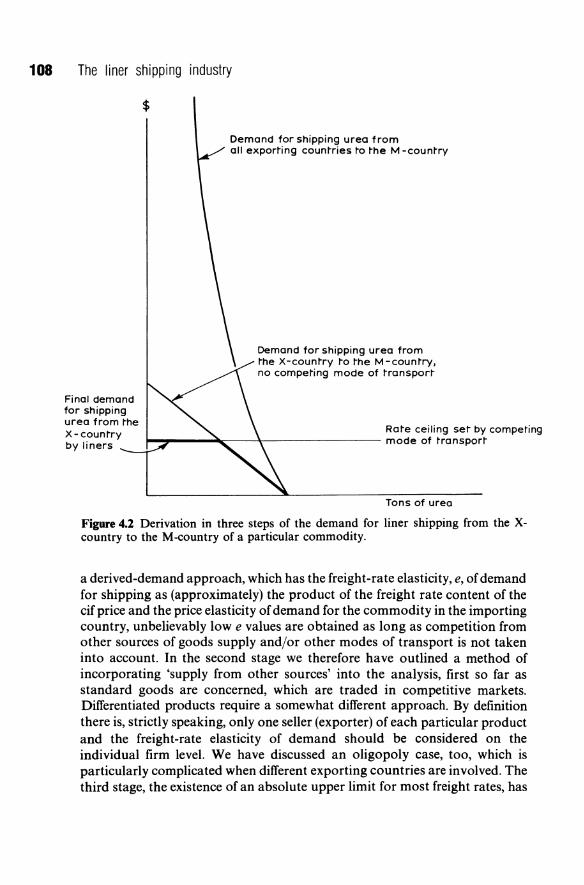

In chapters 3 and 4 the intriguing matter of freight rate making in liner shipping is dealt with. In chapter 3 the existing level and structure of freight rates are surveyed, and a hypothesis of ratemaking behaviour - charging what the traffic can bear over and above the direct handling costs - is tested statistically. Chapter 4 develops some ideas of improving the state of the art of freight rate making by combining derived-demand theory with the relevant facts of liner shipping markets.

1 Characteristics of demand and supply of liner shipping

The pattern of seaborne trade and shipping is determined by a multitude of factors, economic, geographic and political. In this chapter we have selected some factors of general importance as well as some factors of specific importance for the purpose of this book. The chapter starts by an aggregate picture, in which the liner shipping sector will gradually be identified from different points of view.

A short historical background is given and the current tendencies of the development of liner shipping are pointed out. The statistical data presented are compiled from the standard sources of currently published shipping statistics, if no other source is given. *

1.1 AN AGGREGATE PICTURE OF SEABORNE TRADE AND THE WORLD FLEET TONNAGE

Nations trade in order to increase their wealth. The role of international transport is to bridge the spatial separation of trading countries. Shipping is by far the most important mode of transport of international trade. In terms of weight something like 90% of all international trade moves by sea, and so far as long-distance trade is concerned virtually all is seaborne. Due to the fact that the average transport distance is much longer in international than in intranational trade, the total transport work in ton-miles performed by shipping dominates over the transport work made by all other modes of freight transport. According to one estimate (Swedish Shipping Gazette) the total ton-miles by sea are more than twice the total ton-miles by road, railway, and air, put together.

In a historic perspective the most striking feature of the development of international trade and shipping is the enormous upsurge in seaborne trade that has occurred in the post-war period. Today the total international trade in tons is about seven times greater than in 1950. This corresponds to a rate of growth per annum of 8%. In the first half of this century - during which two world wars and the great depression have occurred - the average rate of growth of international trade was only about 1% per annum. In the last

*The standard sources of shipping and seaborne trade statistics are: Lloyd's Register of Shipping; Fearnley and Eger's Chartering Co. Ltd; H. P. Drewry (Shipping Consultants) Ltd.

4 The liner shipping industry

decades of the nineteenth century the growth rate was more impressiveabout 4% per annum.

The unit of measurement of the volume of production or supply in shipping is all important. The number of tons (measured in weight) of cargo carried or of capacity offered is not satisfactory, and for two reasons: (i) tons should be weighted by the distance travelled; the number of ton-miles is therefore a superior measure, and (ii) in practically all liner trades volume rather than weight determines the constraint to the carrying capacity; therefore, the number of cubic ton-miles (measured in cubic meters) is a superior measure to the number of weight ton-miles. An example of the importance of distance is the fact that between the end of the 1940s and the middle of the 1970s the annual rate of growth in total ton-miles (in weight) by sea was as high as 12% compared with 8% in tons. The average transport distance has been rising. The rapid economic growth of Japan, the expansion of oil exports from the Persian Gulf to the distant markets of USA and Europe, and the opening of new sources of minerals in Africa, Australia and Brazil, are the main explanation of this observation. An example of the importance of measuring in cubic meters is the liner trade between USA and the Far East. During the years 1980-82 westbound weight tonnage (exports from USA) was 26% higher than eastbound tonnage (see Table 1.4). When measured in volume, the imbalance is reversed. Capacity utilization on the eastbound leg was greater than 90% during that period compared to a utilization of less than 60% on the westbound leg, when the two are measured by the volume of cargo. *

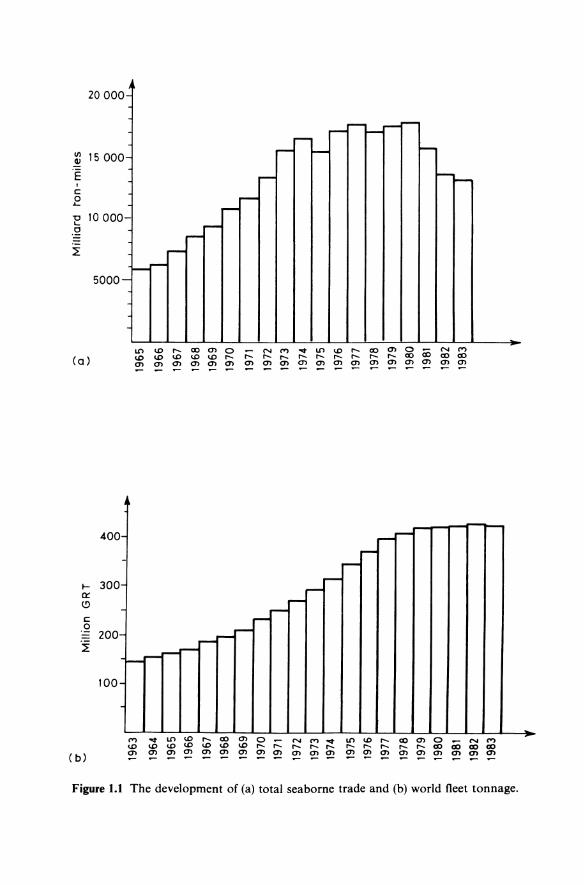

As mentioned, between the end of the 1940s and the middle of the 1970s the annual rate of growth in total seaborne trade measured in ton-miles was a good 12%. The world fleet (aggregated for all types of ships) developed in line with this tremendous rate of growth. Shipping and shipbuilding have been two of the most pronounced growth industries in the post-war period up to 1974. The development of shipping output measured in (weight) ton-miles and shipping capacity in gross revenue ton (GRT). which is a volumetric unit of measurement, is depicted in Fig. 1.1.

The last decade (middle 1970s to middle 1980s) has been characterized by ups and downs in trade during the first half of the decade, and a sharp fall in trade during its second half. It may seem as a puzzle, but during a period of decline in world trade, the world fleet has shown a rise. Between 1977 and 1982, seaborne trade has dropped from 17.5 to 13.2 million ton-miles - a fall of 25%. During the same period, the world fleet has grown from 394 to 425 million GRT - an increase of 8%. The rise in productivity in ports, and the rise in the share of container ships in this total, means that the effective carrying capacity of the fleet has increased even faster. The inevitable outcome for most shipping activities was a fall in the utilization of the world fleet, and a drop in freight

·Information disclosed by shipping lines operating on this route.

"!j

~.

; -;... >-l

::r

(l>

0-

(l>

<:

(l

> 0- '0 3 (l

>

::l ... o ...,

~

~ o §:

'" (l> ~ r:T

o ... ::l

(l>

... ... ~ 0-

(l>

~

::l

0- ~

~ o ... 0::

::>

8 ... ... o ::l

::l

~ ~

0" 19

19

19

19

19

196

196

197

197

197

197

197

I i I I I

197

197

197

1978

19

79

1980

1981

19

82

1983

o o

I I I Mill

ion

G

RT

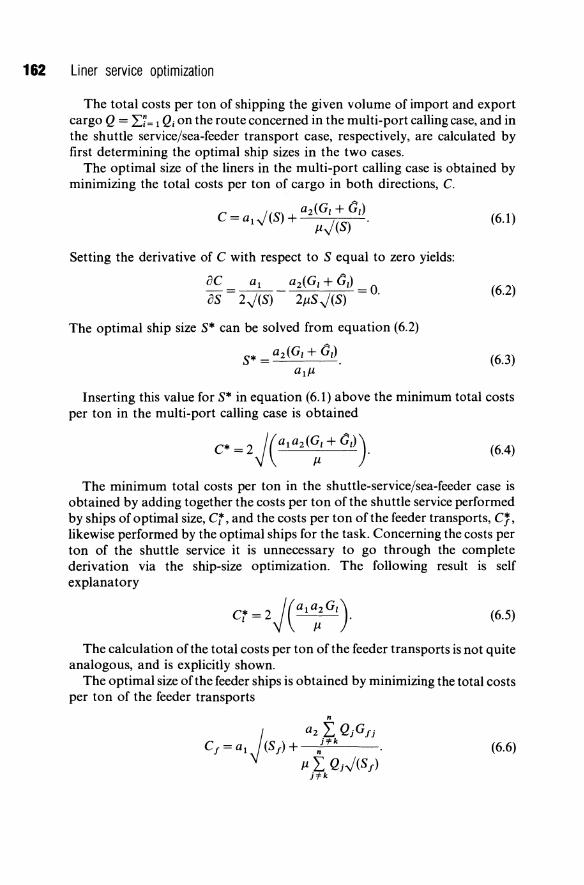

I I N o o I I I I I

w

o o I I J I

I

.". o l I I

o 196

196

196

196

196

197

197

197

197

197

197

197

197

1978

19

7 19

80

198

1982

19

83 I

lJ1 o o o

I I Mill

iard

to

n -

mile

s

I I I o o o o

I I

I I J

- <.n o o

I I I J 1 J I I J

N o o o

6 The liner shipping industry

rates. The recession that started at the beginning of the 1980s, has plunged still deeper and is likely to stick until the end of the decade.

What explains the lack of response of supply to the fall in demand and the continuous increase in shipping capacity in spite ofthe drop in total ton-miles? We suggest two explanations, one technological and the other institutional. The last ten years were a period of rapid technological development which was triggered by the rise in fuel costs.

The most important technological innovation has been the development of fuel-saving engines. New diesel engines equipped with computers that coordinate the diesel-fuel characteristics with the timing of ignition, save up to 20 tons of fuel out of 66 tons of daily fuel consumption of a middle-size container ship - approximately 30% savings. In 1984 there were about 300 orders for Sulzer's RTA newly developed engine and 250 for the MANB& WL-M C engine.

The fuel-saving operation is not limited to the efficient engine. It has been widely recognized, for instance, that the ship's propeller, in its present form, is quite an obsolete concept. Much progress has been made in experiments with new ideas, like that of Bremer Vulkan, which decreases fuel consumptionly 10%. The new propeller arrangement consists of a conventional four-blade propeller fitted with a second nine-blade reaction propeller. This second propeller, mounted behind the conventional one and not being connected to the engine, turns independently. The inner part of the reaction propeller is curved; it acts as a turbine, the nine blades being driven by the outflow of the four-blade unit. This produces a moment of rotation, which is converted into thrust, which can be used to attain higher speed or to reduce the actual power required from the main engine, thereby reducing fuel consumption.

Hull design and hull cleaning also have had an effect on fuel saving. In 1984 Japanese yards were building twenty bulk carriers for Sanko with a bulbous open stern that reduces friction and improves flow to the propeller and thereby reduces power requirements up to 4%. The inventors of the bulbous open stern maintain that it can be applied to any type of ship. Sandblasting and selfpolishing coatings have also proved to be efficient fuel-saving techniques.

There have been other innovations, for example, the 'Racal-DeccaNavigator' which incorporates in one system practically all the existing navigational instruments, and the Swedish fuel-economizer (Sal-Fe), which keeps watch on the vessel's long-term performance, including fuel quality.

Ships in this era of rapid technological changes have a much shorter life than before. At the beginning ofthe century, ships 50 or 60 years old were still sailing the seas. The Liberty ships were still in operation 30 years after the Second World War. Today, a 15-year-old container ship is considered obsolete. The life-span of a container ship is taken today to be 12 years.

Some institutional factors acted to increase the tendency for more ship building. First, governments protecting employment interests continued to

Characteristics of demand and supply 7

subsidize shipyards. Second, international intervention - in the form of the UNCT AD formula for sharing trade (see chapter 2), have triggered a development of national fleets by the developing countries. The high level of new shipbuilding orders in 1981 and 1982 will prolong the excess capacity, and may present shipping during the rest of the 1980s with the least favourable business environment the industry has known since the Second Warld War.

1.2 THE DEVELOPMENT OF THE SHARES OF THE WORLD FLEET: DEVELOPED COUNTRIES, FLAGS OF CONVENIENCE AND DEVELOPING COUNTRIES

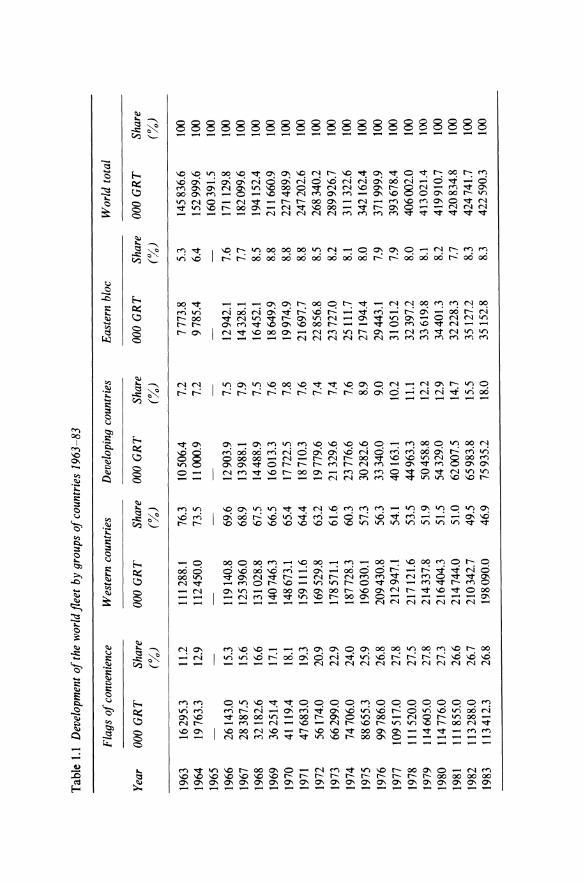

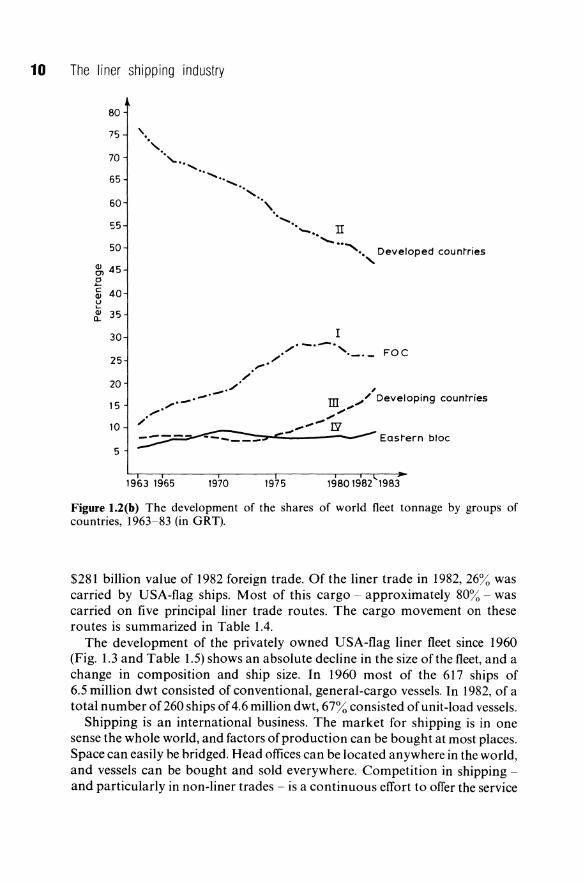

This description of the development of the world fleet concentrates on the changes in its composition by flag in the last twenty years. With the help of Table 1.1 and Fig. 1.2 we see that the fleet of the traditional maritime countries has nearly doubled during the period, while both the flags of convenience* category and the fleet of developing countries has shown a sevenfold increase. These different rates of growth mean that the shares of these groups of countries have changed substantially during the period. Most notable is the decline in the share of developed countries which has gone down by approximately 30%. Flags of convenience have increased their share from 11 % to 28% between 1963 and 1977, but show a slight decline since then. The fleet of developing countries has increased its share from 7% to 18% at an accelerating rate. The Eastern bloc has maintained a fairly constant share throughout the period of approximately 8%.

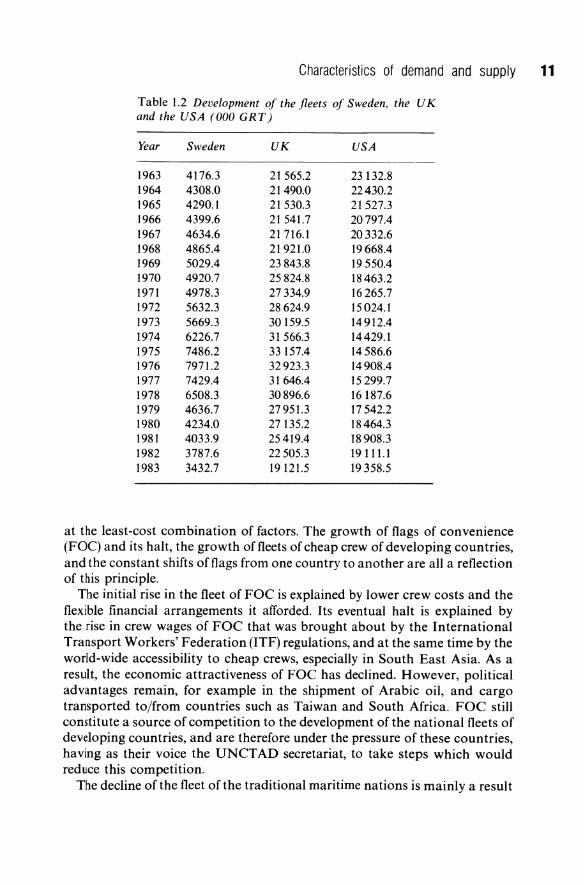

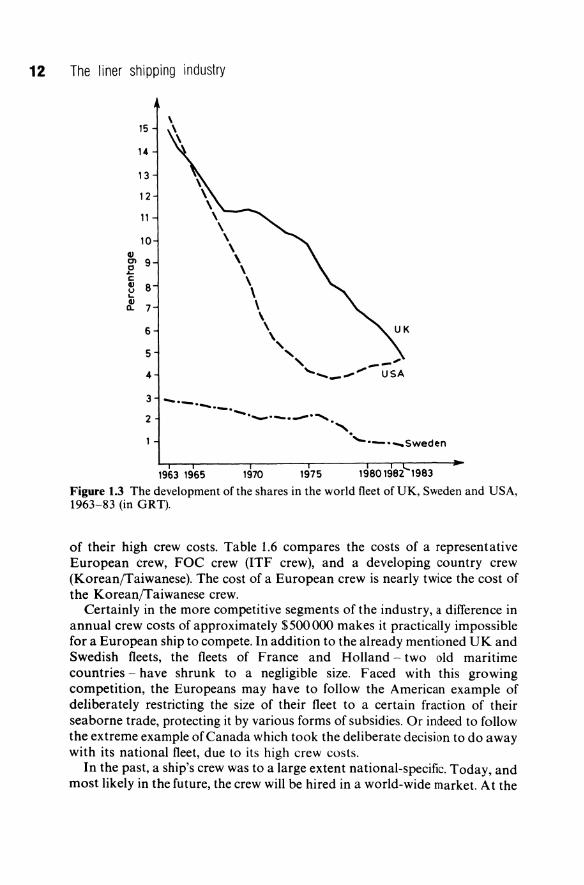

The development of two traditional maritime nations - the UK and Sweden - and that of the USA is shown in Table 1.2 and Fig. 1.3. In 1983 the size of the British fleet was less than that in 1963, and its share has declined from 15% to 5.5%. The share of the USA has dropped from 19.1 % in 1960 to 4.6% - a decline of almost four times. Similarly, the size of the fleet under the Swedish flag has declined during the period, and its share has gone down from 3% to 1%.

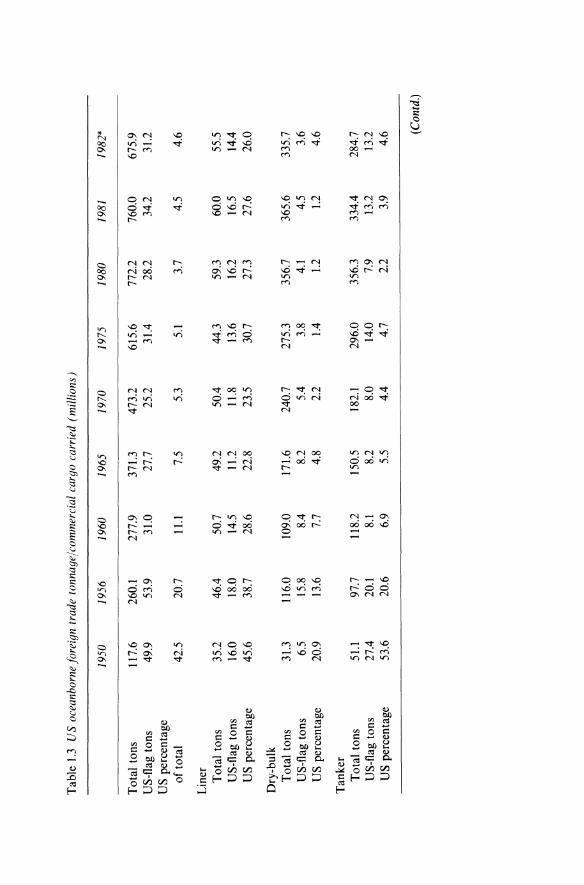

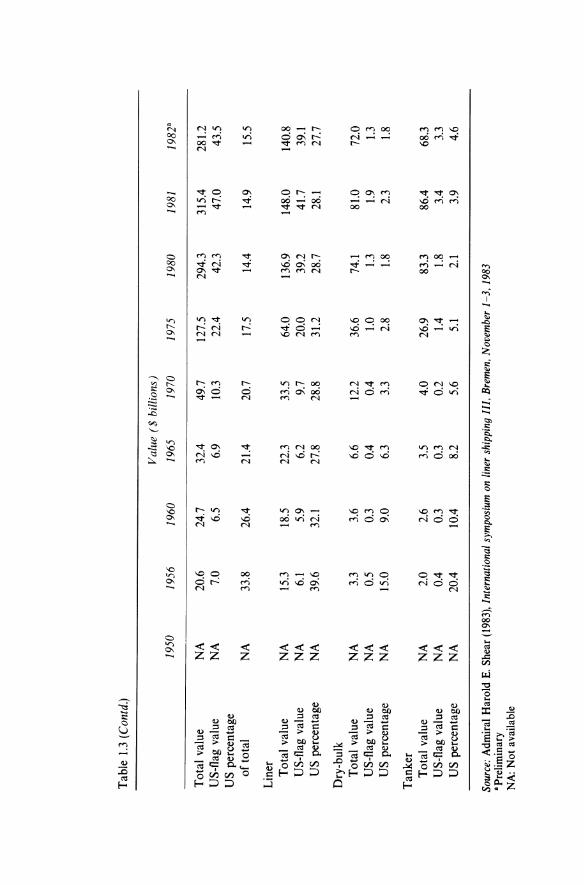

Of the developed countries the share of the USA-flag carriage of seaborne foreign trade to/from the USA has been strikingly low - below 5% - since 1975. Table 1.3 summarizes the development of this trade since 1950. Of a total of 676 million tons handled in 1982, non-liner dry-bulk shipments accounted for half this tonnage, tanker cargo represented 42%, and liner cargo constituted the remaining 8%. Thus, the 55.5 million tons of liner cargo were but a small fraction of the total trade, but they represented half of the

* A flag of convenience is characterized by the following features: (i) The country of registry allows ownership and control of vessels by non-citizens. (ii) Taxes on the income from the ships are not levied locally or are low. (iii) Manning of ships by non-nationals is freely permitted. (iv) There is little control and few regulations by the government over the shipping. Countries affording 'flags of convenience', or 'open registry flags', are Liberia, Panama, Cyprus and Somalia. Of these only Liberia and Panama have a substantial open-registry fleet.

Tab

le 1

.1

Dev

elop

men

t o

f the

wor

ld fl

eet

by g

roup

s o

f cou

ntri

es 1

963-

83

Fla

gs o

f con

veni

ence

W

este

rn c

ount

ries

D

evel

opin

g co

untr

ies

Eas

tern

blo

c W

orld

tot

al

Year

00

0 G

RT

Sh

are

000

GR

T

Shar

e 00

0 G

RT

Sh

are

000

GR

T

Shar

e 00

0 G

RT

Sh

are

(%)

(%)

(%)

(%)

(%)

1963

16

295.

3 11

.2

1112

88.1

76

.3

10 5

06.4

7.

2 77

73.8

5.

3 14

5836

.6

100

1964

19

763.

3 12

.9

1124

50.0

73

.5

1100

0.9

7.2

9785

.4

6.4

1529

99.6

10

0

1965

16

0391

.5

100

1966

26

143.

0 15

.3

1191

40.8

69

.6

1290

3.9

7.5

1294

2.1

7.6

1711

29.8

10

0

1967

28

387.

5 15

.6

1253

96.0

68

.9

13 9

88.1

7.

9 14

328.

1 7.

7 18

2099

.6

100

1968

32

182.

6 16

.6

1310

28.8

67

.5

1448

8.9

7.5

1645

2.1

8.5

1941

52.4

10

0

1969

36

251.

4 17

.1

1407

46.3

66

.5

1601

3.3

7.6

1864

9.9

8.8

2116

60.9

10

0

1970

41

119.

4 18

.1

1486

73.1

65

.4

1772

2.5

7.8

1997

4.9

8.8

2274

89.9

10

0

1971

47

683.

0 19

.3

1591

11.6

64

.4

1871

0.3

7.6

2169

7.7

8.8

2472

02.6

10

0

1972

56

174.

0 20

.9

1695

29.8

63

.2

1977

9.6

7.4

2285

6.8

8.5

2683

40.2

10

0

1973

66

299.

0 22

.9

1785

71.1

61

.6

2132

9.6

7.4

2372

7.0

8.2

2899

26.7

10

0

1974

74

706.

0 24

.0

1877

28.3

60

.3

2377

6.6

7.6

2511

1.7

8.1

3113

22.6

10

0

1975

88

655.

3 25

.9

1960

30.1

57

.3

3028

2.6

8.9

2719

4.4

8.0

3421

62.4

10

0

1976

99

786.

0 26

.8

2094

30.8

56

.3

3334

0.0

9.0

2944

3.1

7.9

3719

99.9

10

0

1977

10

9517

.0

27.8

21

2947

.1

54.1

40

163.

1 10

.2

3105

1.2

7.9

3936

78.4

10

0

1978

11

1520

.0

27.5

21

7121

.6

53.5

44

963.

3 11

.1

3239

7.2

8.0

4060

02.0

10

0

1979

11

4605

.0

27.8

21

4337

.8

51.9

50

458.

8 12

.2

3361

9.8

8.1

413

021.

4 10

0

1980

11

4776

.0

27.3

21

6404

.3

51.5

54

329.

0 12

.9

3440

1.3

8.2

4199

10.7

10

0

1981

11

1855

.0

26.6

21

4744

.0

51.0

62

007.

5 14

.7

3222

8.3

7.7

4208

34.8

10

0

1982

11

3288

.0

26.7

21

0342

.7

49.5

65

983.

8 15

.5

3512

7.2

8.3

4247

41.7

10

0

1983

11

3412

.3

26.8

19

8090

.0

46.9

75

935.

2 18

.0

3515

2.8

8.3

4225

90.3

10

0

..... a:: (!)

0 0 0 0 0 0

450

400

350

300

250

200

150

100

50

. /' ..... ..--.

/" ./ ..

./. ./

World I"ol"al

n. ."",. .. ~ ......... I.· --,.Developed countries

.. /.. "

/'

/

I _.-·-·_·-FOC ".

.// ", m /- Developing countries

./ ."

." " ." /'" lY .-' _ --""" Easl"ern bloc • ..-_fIIIII' ,<~

", . .".,. ----~ --..., ~-

1963 1965 1970 1975 19801982 1983

Figure 1.2(a) Development of the world fleet (000 GRT), by groups of countries.

10 The liner shipping industry

BO

75

70

65

60

55

50

~ 45 E ;; 40 ~ .f. 35

30

25

20

15

10

5

'. " """. ..............

.. , .. , ..

- .... ---

1963 1965 1970

'\. ".

'_" II "- ..

I

........ Developed countries ,

Foe

, ill ~/ Developing countries

"" .... "" _ ....... - IY

Eastern bloc

1975 19BO 19B2 19B3

Figure 1.2(b) The development of the shares of world fleet tonnage by groups of countries, 1963-83 (in GRT).

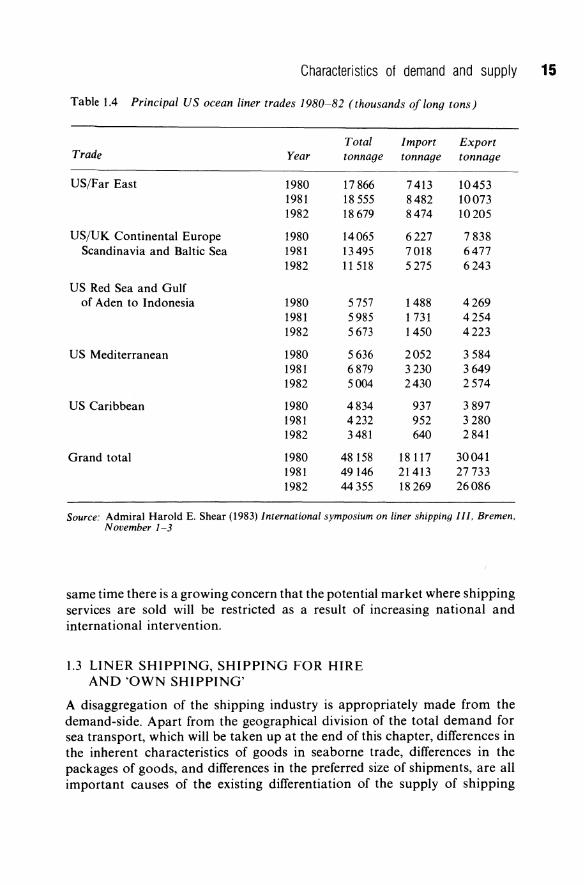

$281 billion value of 1982 foreign trade. Of the liner trade in 1982, 26% was carried by USA-flag ships. Most of this cargo - approximately 80% - was carried on five principal liner trade routes. The cargo movement on these routes is summarized in Table 1.4.

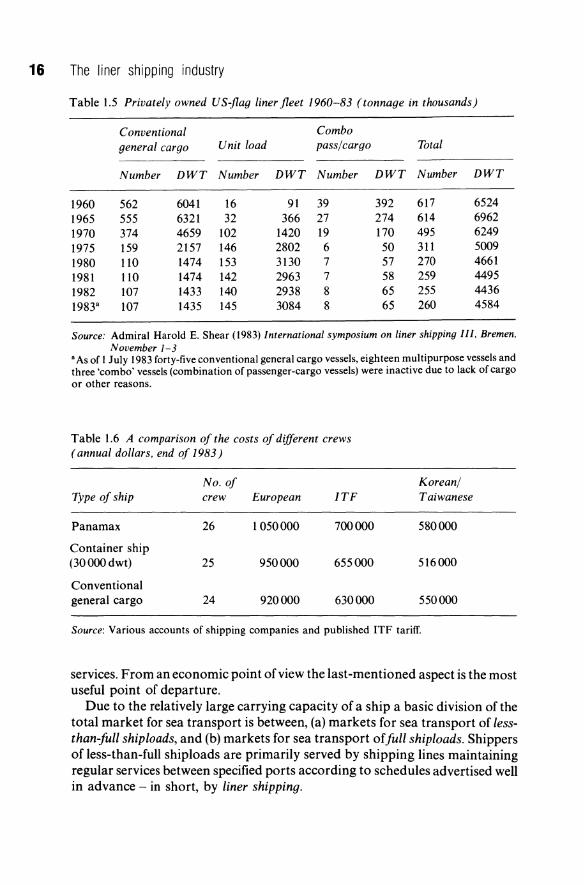

The development of the privately owned USA-flag liner fleet since 1960 (Fig. 1.3 and Table 1.5) shows an absolute decline in the size of the fleet, and a change in composition and ship size. In 1960 most of the 617 ships of 6.5 million dwt consisted of conventional, general-cargo vessels. In 1982, of a total number of260 ships of 4.6 million dwt, 67% consisted of unit-load vessels.

Shipping is an international business. The market for shipping is in one sense the whole world, and factors of production can be bought at most places. Space can easily he bridged. Head offices can be located anywhere in the world, and vessels can be bought and sold everywhere. Competition in shipping -and particularly in non-liner trades - is a continuous effort to offer the service

Characteristics of demand and supply

Table 1.2 Development oj the fleets oj Sweden, the UK and the USA (000 GRT)

Year Sweden UK USA

1963 4176.3 21565.2 23132.8 1964 4308.0 21490.0 22430.2 1965 4290.1 21530.3 21527.3 1966 4399.6 21541.7 20797.4 1967 4634.6 21716.1 20332.6 1968 4865.4 21921.0 19668.4 1969 5029.4 23843.8 19550.4 1970 4920.7 25824.8 18463.2 1971 4978.3 27334.9 16265.7 1972 5632.3 28624.9 15024.1 1973 5669.3 30159.5 14912.4 1974 6226.7 31566.3 14429.1 1975 7486.2 33157.4 14586.6 1976 7971.2 32923.3 14908.4 1977 7429.4 31646.4 15299.7 1978 6508.3 30896.6 16187.6 1979 4636.7 27951.3 17542.2 1980 4234.0 27135.2 18464.3 1981 4033.9 25419.4 18908.3 1982 3787.6 22505.3 19111.1 1983 3432.7 19121.5 19358.5

at the least-cost combination of factors. The growth of flags of convenience (FOC) and its halt, the growth of fleets of cheap crew of developing countries, and the constant shifts of flags from one country to another are all a reflection of this principle.

The initial rise in the fleet of FOC is explained by lower crew costs and the flexible financial arrangements it afforded. Its eventual halt is explained by the rise in crew wages of FOC that was brought about by the International Transport Workers' Federation (ITF) regulations, and at the same time by the world-wide accessibility to cheap crews, especially in South East Asia. As a result, the economic attractiveness of FOC has declined. However, political advantages remain, for example in the shipment of Arabic oil, and cargo transported to/from countries such as Taiwan and South Africa. FOC still constitute a source of competition to the development of the national fleets of developing countries, and are therefore under the pressure of these countries, having as their voice the UNCT AD secretariat, to take steps which would reduce this competition.

The decline of the fleet of the traditional maritime nations is mainly a result

11

12 The liner shipping industry

15

14

13 \

12 \ \

11 \ \ \ 10 \

GI \ 0'1 9 0 \ ..... c: \ cu 8 u \ ... cu \ 0- 7

\ 6 \

\ , 5 .... , -' 4 "- ,,- USA --" 2

3 ...... _ ....... _. -._.-._ ........ "

''-'-'_Sweden

1963 1965 1970 1975 19801982 1983

Figure 1.3 The development of the shares in the world fleet of UK, Sweden and USA, 1963-83 (in GRT).

of their high crew costs. Table 1.6 compares the costs of a representative European crew, FOC crew (ITF crew), and a developing country crew (Korean/Taiwanese). The cost of a European crew is nearly twice the cost of the Korean/Taiwanese crew.

Certainly in the more competitive segments of the industry, a difference in annual crew costs of approximately $500000 makes it practically impossible for a European ship to compete. In addition to the already mentioned UK and Swedish fleets, the fleets of France and Holland - two old maritime countries - have shrunk to a negligible size. Faced with this growing competition, the Europeans may have to follow the American example of deliberately restricting the size of their fleet to a certain fraction of their seaborne trade, protecting it by various forms of subsidies. Or indeed to follow the extreme example of Canada which took the deliberate decision to do away with its national fleet, due to its high crew costs.

In the past, a ship's crew was to a large extent national-specific. Today, and most likely in the future, the crew will be hired in a world-wide market. At the

Tab

le 1

.3

US

ocea

nbor

ne[o

reig

n tr

ade

tonn

age/

com

mer

cial

car

go c

arri

ed (

mil

lion

s)

1950

19

56

1960

19

65

1970

19

75

1980

19

81

1982

"

Tot

al t

ons

117.

6 26

0.1

277.

9 37

1.3

473.

2 61

5.6

772.

2 76

0.0

675.

9 U

S-f

lag

tons

49

.9

53.9

31

.0

27.7

25

.2

31.4

28

.2

34.2

31

.2

US

per

cent

age

of

tota

l 42

.5

20.7

11

.1

7.5

5.3

5.1

3.7

4.5

4.6

Lin

er

Tot

al t

ons

35.2

46

.4

50.7

49

.2

50.4

44

.3

59.3

60

.0

55.5

U

S-f

lag

tons

16

.0

18.0

14

.5

11.2

11

.8

13.6

16

.2

16.5

14

.4

US

per

cent

age

45.6

38

.7

28.6

22

.8

23.5

30

.7

27.3

27

.6

26.0

Dry

-bul

k T

otal

ton

s 31

.3

116.

0 10

9.0

171.

6 24

0.7

275.

3 35

6.7

365.

6 33

5.7

US

-fla

g to

ns

6.5

15.8

8.

4 8.

2 5.

4 3.

8 4.

1 4.

5 3.

6 U

S p

erce

ntag

e 20

.9

13.6

7.

7 4.

8 2.

2 1.

4 1.

2 1.

2 4.

6

Tan

ker

T

otal

ton

s 51

.1

97.7

11

8.2

150.

5 18

2.1

296.

0 35

6.3

334.

4 28

4.7

US

-fla

g to

ns

27.4

20

.1

8.1

8.2

8.0

14.0

7.

9 13

.2

13.2

US

per

cent

age

53.6

20

.6

6.9

5.5

4.4

4.7

2.2

3.9

4.6 (C

ontd

.)

Tab

le 1

.3 (

Con

td.)

Val

ue (

$ b

illi

ons)

1950

19

56

1960

19

65

1970

19

75

1980

19

81

1982

"

Tot

al v

alue

N

A

20.6

24

.7

32.4

49

.7

127.

5 29

4.3

315.

4 28

1.2

US-

flag

valu

e N

A

7.0

6.5

6.9

10.3

22

.4

42.3

47

.0

43.5

U

S pe

rcen

tage

of

tota

l N

A

33.8

26

.4

21.4

20

.7

17.5

14

.4

14.9

15

.5

Lin

er

Tot

al v

alue

N

A

15.3

18

.5

22.3

33

.5

64.0

13

6.9

148.

0 14

0.8

US-

flag

valu

e N

A

6.1

5.9

6.2

9.7

20.0

39

.2

41.7

39

.1

US

perc

enta

ge

NA

39

.6

32.1

27

.8

28.8

31

.2

28.7

28

.1

27.7

Dry

-bul

k T

otal

val

ue

NA

3.

3 3.

6 6.

6 12

.2

36.6

74

.1

81.0

72

.0

US-

flag

valu

e N

A

0.5

0.3

0.4

0.4

1.0

1.3

1.9

1.3

US

perc

enta

ge

NA

15

.0

9.0

6.3

3.3

2.8

1.8

2.3

1.8

Tan

ker

Tot

al v

alue

N

A

2.0

2.6

3.5

4.0

26.9

83

.3

86.4

68

.3

US-

flag

valu

e N

A

0.4

0.3

0.3

0.2

1.4

1.8

3.4

3.3

US

perc

enta

ge

NA

20

.4

10.4

8.

2 5.

6 5.

1 2.

1 3.

9 4.

6

Sour

ce:

Adm

iral

Har

old

E. S

hear

(198

3), I

nter

natio

nal

sym

posi

um o

n lin

er s

hipp

ing

III.

Bre

men

, N

ovem

ber

1-3.

198

3 • P

relim

inar

y N

A:

Not

ava

ilabl

e

Characteristics of demand and supply

Table 1.4 Principal US ocean liner trades 1980-82 (thousands of long tons)

Total Import Export Trade Year tonnage tonnage tonnage

US/Far East 1980 17866 7413 10453 1981 18555 8482 10073 1982 18679 8474 10205

US/UK Continental Europe 1980 14065 6227 7838 Scandinavia and Baltic Sea 1981 13495 7018 6477

1982 11 518 5275 6243

US Red Sea and Gulf of Aden to Indonesia 1980 5757 1488 4269

1981 5985 1731 4254 1982 5673 1450 4223

US Mediterranean 1980 5636 2052 3584 1981 6879 3230 3649 1982 5004 2430 2574

US Caribbean 1980 4834 937 3897 1981 4232 952 3280 1982 3481 640 2841

Grand total 1980 48158 18117 30041 1981 49146 21413 27733 1982 44355 18269 26086

Source: Admiral Harold E. Shear (1983) International symposium on liner shipping III, Bremen, November 1-3

same time there is a growing concern that the potential market where shipping services are sold will be restricted as a result of increasing national and international intervention.

1.3 LINER SHIPPING, SHIPPING FOR HIRE AND 'OWN SHIPPING'

A disaggregation of the shipping industry is appropriately made from the demand-side. Apart from the geographical division of the total demand for sea transport, which will be taken up at the end of this chapter, differences in the inherent characteristics of goods in seaborne trade, differences in the packages of goods, and differences in the preferred size of shipments, are all important causes of the existing differentiation of the supply of shipping

15

16 The liner shipping industry

Table 1.5 Privately owned US-flag liner fleet 1960-83 (tonnage in thousands)

Conventional Combo

general cargo Unit load pass/cargo Total

Number DWT Number DWT Number DWT Number DWT

1960 562 6041 16 91 39 392 617 6524 1965 555 6321 32 366 27 274 614 6962 1970 374 4659 102 1420 19 170 495 6249 1975 159 2157 146 2802 6 50 311 5009 1980 110 1474 153 3130 7 57 270 4661 1981 110 1474 142 2963 7 58 259 4495 1982 107 1433 140 2938 8 65 255 4436 1983" 107 1435 145 3084 8 65 260 4584

Source: Admiral Harold E. Shear (1983) International symposium on liner shipping III, Bremen, November /-3

"As of I July 1983 forty-five conventional general cargo vessels, eighteen multipurpose vessels and three 'combo' vessels (combination of passenger-cargo vessels) were inactive due to lack of cargo or other reasons.

Table 1.6 A comparison of the costs of different crews (annual dol/ars, end of 1983)

No. of Korean/ Type of ship crew European ITF Taiwanese

Panamax 26 1050000 700000 580000

Container ship (30000dwt) 25 950000 655000 516000

Conventional general cargo 24 920000 630000 550000

Source: Various accounts of shipping companies and published ITF tariff.

services. From an economic point of view the last-mentioned aspect is the most useful point of departure.

Due to the relatively large carrying capacity of a ship a basic division of the total market for sea transport is between, (a) markets for sea transport of lessthan-full shiploads, and (b) markets for sea transport offull shiploads. Shippers of less-than-full shiploads are primarily served by shipping lines maintaining regular services between specified ports according to schedules advertised well in advance - in short, by liner shipping.

Fin

al

m a

nufac~ured

go

od

s, fru

i~,

vege~ables a

nd

fr

oze

n m

ea

l"

Inte

rme

dia

l"e

g

oo

ds

Pro

cess

ed

m

al"

eri

al

Ra

w m

ate

ria

l

Typ

e o

f g

oo

ds

Ca

rl"o

ns

Bo

xe

s

Cra

l"e

s

Un

pa

cke

d b

ig

art

icle

s (

e.g

ca

rs)

Ba

gs

Dru

ms

Ba

les,

ro

lls

e~c.

Typ

e o

f p

ack

ag

e

DE

MA

ND

Sm

all

ship

me

nl"

s a

t sh

orl

"er

or

I •

I lo

ng

er

inte

rva

ls

Me

diu

m-s

ize

sh

ipm

en

l"s

Fu

ll sh

iplo

ad

s _I

o

nce

or

tWic

e

a ye

ar

Lin

er

ship

pin

g

Sh

ipp

ing

fo

r h

ire

Sh

ipp

ing

un

de

r yo

ur

ow

n

Fu

ll sh

iplo

ad

s H

sl

"eam

('o

wn

m

an

y h

me

s

ship

pin

g ')

a

ye

ar

Siz

e a

nd

an

nu

al

nu

mb

er o

f shipmen~

Typ

e o

f sh

ipp

ing

se

rvic

e

SU

PP

LY

Figu

re 1

.4 S

hipp

ing

dem

and

and

supp

ly a

spec

ts.

Bre

ak-b

ulk

ca

rgo

sh

ips

('co

nve

nh

on

al

line

rs>

)

Bre

ak-b

ulk

ca

rgo

sh

ip

wit

h o

ne

or

mo

re ref

rige

ra~e

d h

old

s

Sp

eci

aliz

ed

'u

nit

lo

ad

' ca

rrie

rs

All-

pu

rpo

se

~ramp s

hip

s

Sp

eci

aliz

ed

d

ry-b

ulk

ca

rrie

rs a

nd

o

il I"

an

kers

Typ

e o

f sh

ip

18 The liner shipping industry

Shippers of full shiploads rely on the ship charter market. They can either enter a long-term charter agreement which may have a duration of6 months to 20 years and more, or they may enter a single-voyage charter agreement, and make use of the spot charter market. Full shiploads make possible 'shipping for hire' transactions - either short or long term.

The development of telecommunication has greatly facilitated the continuous matching of shipping capacity and potential shiploads, which is a prerequisite for the working of a voyage charter market. However, the Baltic Exchange in London, the most important auction market for tramp-ship charters, originated in the 18th century.

We think it is instructive to speak about 'own shipping' (an abbreviation of our own making) as the third main type of shipping services (see Fig. 1.4). Historically 'own shipping' has the oldest origin at least so far as deep-sea shipping is concerned. As the term suggests, merchant shipping used to be conducted by big merchants and trading firms like the East India Company, which had more or less monopolized each particular trade. They owned the ships which carried their goods, and there was not much room for special shipping companies. As international trade grew, however, new demands for shipping arose.

The general technological progress made possible specialization in shipping. The two catalysts for the emergence of liner shipping and voyage charter shipping, were respectively the introduction of steamships during the second half of the nineteenth century which made possible regular shipping services according to schedule, and the development of telecommunication. With these developments 'own shipping' tonnage was offered for the general use by the big trading companies, and shipping lines were thus formed. Today 'own shipping' is confined to specialized shipping activity, especially in the -bulk-shipping market. About one-half of the world tanker fleet is owned or long-time chartered by the oil companies. In the dry-bulk market about 30% of the tonnage is owned by industrial companies.

1.3.1 Shipping activities and ship types

We distinguish three main types of shipping activities: 'liner services', 'shipping for hire', and 'own shipping'. In the past all three activities were served by ships of an 'all-purpose' type. Shipping-for-hire services had mostly been carried out by the so-called 'tramps'. The traditional tramp used to be an all-purpose ship. The idea behind such a ship was to maximize the chances of getting a cargo in any port of the world. The tramp would go to a port wherever and whenever sufficient cargo was available to fill the ship. The ships employed in liner shipping were, like the tramps, exclusively all-purpose ships. The important difference was that liners were designed to carry miscellaneous packaged cargo. That meant in the first place that the liners were equipped with two or

Characteristics of demand and supply 19

more decks. They were also usually faster than the tramps, which is a reflection of the higher average value of time of packaged cargo.

The similarity of the ship types meant that they were all, at least potentially, in competition with each other. Although the main space in the lower holds of a typical all-purpose tramp was intended for loose cargo or big lots of robust packaged cargo, it could also stow small packaged cargo on the single shelter deck. This also meant that conversions of tramps into liners and liners into tramps were not too involved. It was not unusual that an original liner ended its days as a tramp. Or, that a shipping line would occasionally charter a suitable tramp ship for one or more sailings.

The potential savings of specialization and tailor-made ships, have embraced all types of shipping activities. The traditional all-purpose tramp has practically disappeared from the seas. Shipping-for-hire services are nowadays carried out by specialized bulk carriers designed to take one or two types of cargo (e.g. ore and oil, carried by Ore-Bulk-Oil (OBO) ships). Similarly own shipping is nowadays performed by specialized ships. The main point of owning ships for a large goods producer/exporter is that a high degree of cost-reducing specialization of the ships' design can be ventured. The tendency to specialization has also influenced the design of liners. The disadvantages of handling very heterogeneous articles have been mitigated by introducing standard 'unit loads'. Special ships go with each particular type of unit load. Containers and container ships are the dominant and most well-known examples of this development. In 1985 approximately 60% of the liner cargo was carried by the general category of container ships, while the remaining 40% by the non-container category, called 'conventional liners'.

An outcome of the tendency to specialization is that competition between the different types of shipping activities has greatly declined. In particular, the traditional competition between the liner and the all-purpose tramp belongs to the past.

In the future, some competition between the liners and tramp will remain, and will take two forms. First, there are bulk ships that are designed to take both bulk and general cargo or containers. These are few in number and do not constitute a severe threat to the liner trade. One example is the Belgian ABC line, which has been operating six specially designed vessels which can carry both bulk and containers on the Australia-Europe and USA trade routes. The other form of competition is simply that with the general increase in the volume of international trade, the borderline between general cargo and bulk will gradually shift. Some commodities that were potential liner cargo (such as sugar and rice) will become minor bulk, moving in quantities that are sufficient to fill a ship.

Yet, the main source of competition in the liner shipping industry is the liners themselves - either by the independents operating outside the conferences, or by member lines operating within the conferences.

20 The liner shipping industry

A summary of the main ship types and their association with the type of shipping activity is given below:

Tankers

Bulk shipping ~ Gas carriers -----======- Dry bulk OBOs

__________ Full container

~Part container _________ Unit load vessels ~ Roro

L· h" ---------- Palletized mer s Ippmg

~ Conventionailine"

____ Tankers

Own shipping Gas carriers

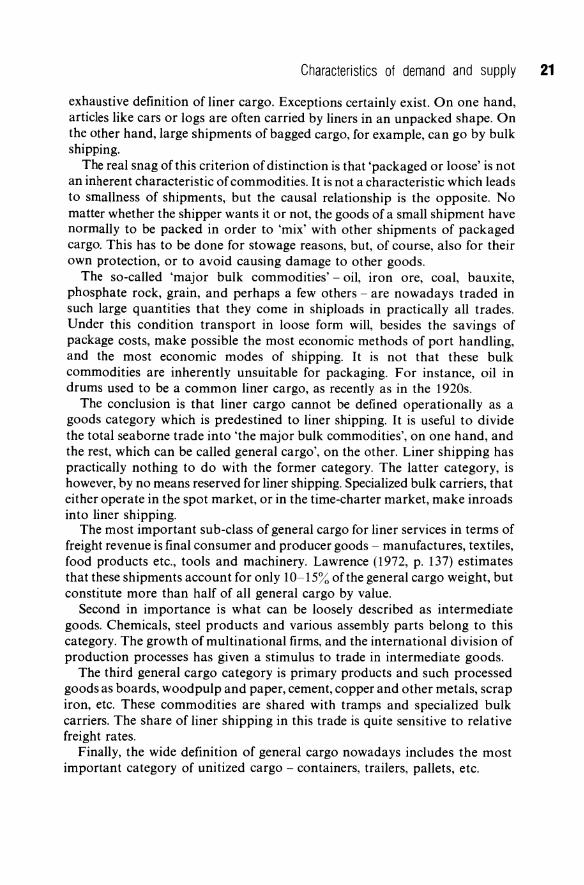

----Dry bulk

Note: The shipping terms of the different types are discussed in the subsequent sections of the book. The term 'unit load' is chosen by us as the most appropriate to describe all the ship types of the given four sub-categories, although a common term used for them all in the industry is container ships 'unit load' is normally associated with the specific form of ships for palletized cargo.

1.3.2 The wide definition of general cargo

The crucial aspect of liner cargo is that the shipments are each rather small. Shipment smallness is in the first place associated with these two kinds of commodities.

'Odd' commodities - in the sense that the annual quantity traded is very small - will necessarily move in small lots.

2 High-value commodities will, even if the annual quantity traded is substantial, normally move in small lots because the storage costs will otherwise be too high.

Both these characteristics - 'oddity' and high-value - are possessed by highly processed goods. Many other commodities than highly processed goods are, however, carried by liners.

Another way of distinguishing liner cargo from bulk cargo is by the presence or absence of packages. It is true that 'packaged cargo' is rather close to an

Characteristics of demand and supply 21

exhaustive definition of liner cargo. Exceptions certainly exist. On one hand, articles like cars or logs are often carried by liners in an unpacked shape. On the other hand, large shipments of bagged cargo, for example, can go by bulk shipping.

The real snag of this criterion of distinction is that 'packaged or loose' is not an inherent characteristic of commodities. It is not a characteristic which leads to smallness of shipments, but the causal relationship is the opposite. No matter whether the shipper wants it or not, the goods of a small shipment have normally to be packed in order to 'mix' with other shipments of packaged cargo. This has to be done for stowage reasons, but, of course, also for their own protection, or to avoid causing damage to other goods.

The so-called 'major bulk commodities' - oil, iron ore, coal, bauxite, phosphate rock, grain, and perhaps a few others - are nowadays traded in such large quantities that they come in shiploads in practically all trades. Under this condition transport in loose form will, besides the savings of package costs, make possible the most economic methods of port handling, and the most economic modes of shipping. It is not that these bulk commodities are inherently unsuitable for packaging. For instance, oil in drums used to be a common liner cargo, as recently as in the 1920s.

The conclusion is that liner cargo cannot be defined operationally as a goods category which is predestined to liner shipping. It is useful to divide the total seaborne trade into 'the major bulk commodities', on one hand, and the rest, which can be called general cargo', on the other. Liner shipping has practically nothing to do with the former category. The latter category, is however, by no means reserved for liner shipping. Specialized bulk carriers, that either operate in the spot market, or in the time-charter market, make inroads into liner shipping.

The most important sub-class of general cargo for liner services in terms of freight revenue is final consumer and producer goods - manufactures, textiles, food products etc., tools and machinery. Lawrence (1972, p. 137) estimates that these shipments account for only 10-15% of the general cargo weight, but constitute more than half of all general cargo by value.

Second in importance is what can be loosely described as intermediate goods. Chemicals, steel products and various assembly parts belong to this category. The growth of multinational firms, and the international division of production processes has given a stimulus to trade in intermediate goods.

The third general cargo category is primary products and such processed goods as boards, wood pulp and paper, cement, copper and other metals, scrap iron, etc. These commodities are shared with tramps and specialized bulk carriers. The share of liner shipping in this trade is quite sensitive to relative freight rates.

Finally, the wide definition of general cargo nowadays includes the most important category of unitized cargo - containers, trailers, pallets, etc.

22 The liner shipping industry

1.4 THE RELATIVE SIZE OF THE LINER SHIPPING INDUSTRY

It is remarkable that there exists no published records of the total turnover, value added, or some other measure of the size in economic terms of the liner shipping industry. The main reason for this is probably that liner shipping companies, unless forced to do so, do not bother to report this kind of data. However, estimates of total liner shipping turnover have from time to time been produced on an ad hoc basis. There seems to be a reasonable consensus about the relative importance of liner shipping: total resource costs of liner shipping are about the same as the resource costs of all other branches of shipping put together. For example, in the Rochdale report it was estimated that 'the gross revenue ofthe liner trades amounts to perhaps about one half of the total revenue of the shipping industry' (HMSO, 1970).

In terms of cargo tons, ton-miles, or fleet tonnage the relative size of the liner shipping sector appears much smaller. But neither can this be shown with accurate figures, due to lack of data. * Total ton-miles of general cargo (which is perhaps twice that of liner cargo) and total tonnage of ships for general cargo, can be given and related to the totals of all shipping. From the previously mentioned sources of shipping and seaborne trade statistics, we have extracted these round figures:

Total ton-miles of general cargo: Total dwt of ships for general cargo: Total GRT of ships for general cargo: Total freight revenue of general cargo:

One-fifth of total ton-miles of all seaborne trade One-fifth of total dwt of world fleet One-quarter of total GRT of world fleet Two-thirds of total freight revenue

1.5 RECENT DEVELOPMENT IN GENERAL CARGO SHIPPING

The fact that barely 10% of total seaborne ton-miles is produced by liners while about 50% of total freight revenue is earned in the liner shipping sector means that the average liner freight rate per ton-mile is almost ten times the average freight rate per ton-mile of all other shipping. Why is this so? This question will be fully answered in Part II, where a thorough shipping engineering economy analysis is made. A full answer requires a model which takes into account all important interrelationships between ship design variables and shipping costs.

Part of the answer is, however, very straightforward, and can be given

* An attempt to account for the liner trade between sixty pairs of countries was made by the American consulting company WAF A jointly with Mennelitics. They publish a 5-year forecast of the main commodities moving on these trades, which is updated every 6 months.

Characteristics of demand and supply 23

already at this stage. The stevedoring charges for handling heterogeneous packaged cargo are in general at least ten times higher than the stevedoring charges for handling homogeneous bulk cargo. In view of the fact that total stevedoring charges make up a good half of the total freight cost of break-bulk cargo in, for example, the North Atlantic trades and the North Pacific trades, * the relatively high direct handling (loading and unloading) costs can be said to provide half the explanation of the wide difference between liner freight rates and other shipping freight rates.

For break-bulk cargo it is generally true that the 'journey' from quay to hold and back of a shipment is more expensive than the journey across an ocean. If, in addition, the cost of ship's lay time is included, as it should be, the cost of the loading and unloading, will typically constitute two-thirds or even more of the total freight cost. In view of this rather lopsided cost structure it is not surprising that something radical had to be done about the break-bulk handling costs. The general answer to the soaring costs of stevedoring was unitization of cargo.

1.5.1 Unitization of break-bulk cargo

Break-bulk cargo handling is very labour-intensive. To minimize the lay time a big conventional liner can employ as many as ten gangs of stevedoring labour at a time, which can mean that some one hundred men are engaged in cargo handling simultaneously. (The gang size varies fairly widely from port to port.) The productivity per man-hour is very variable depending on a number of factors: the handling equipment, the type of article being handled, etc. In the port of Stockholm the round figure of 1 ton per man-hour was used as a standard in the 1950s and 1960s. Much higher figures were not reported anywhere in the ports of the world during the late 1960s and the beginning of the 1970s. Table 1.7 indicates that the productivity per gang-hour was typically less than 25 tons, and was on average in a range which corresponds to a figure somewhat above 1 ton per man-hour.

Unitization made an increase in break-bulk handling productivity possible. In 1985 the average productivity in ports of developed countries varied between 200 and 300 tons per gang shift. Given a size of a gang of ten stevedores and 8-hour shifts, 250 tons per gang-shift implies a productivity of 3 tons per man-hour: a three-fold increase over handling productivity in the 1960s.

The level of wages of longshoremen in American ports was such that the stevedoring charges for loading or unloading break-bulk cargo were in the range of $10-20 per ton at the beginning of the 1970s. The stevedoring charges

*In liner trad~sDetween deVeloping countries the proportion of total stevedoring charges in the total freight costs is much less - typically in the range of 20-30% - due to the much lower docklabour wage rate. If chronically congested ports are included in the service, the proportion of stevedoring charges is still less because the lay time cost of ships becomes very dominating.

24 The liner shipping industry

Table 1.7 Break-bulk loading and unloading capacity

Port

Antwerp and Rotterdam Bremen and Hamburg Gothenburg New York Chicago Long Beach and San Francisco Karachi Valparaiso La Valletta

Tons per gang-hour

18-25 14-22 12-20 12-18 12-20 10-15 6-22

10-18 12-15

Sources: A Battelle report pertaining to 1970 and the UNCTAD report Berth Throughput (United Nations, New York, 1973) pertaining to 1971 and 1972.

of West Europe ports were also very high, although not as high as their American counterparts. The European level of break-bulk handling costs was about half the American level.

The container made its first appearance in the 1950s, and in the latter half of the 1960s the breakthrough occurred. One used to speak about the container revolution. This is an adequate expression, which, however, should not obscure the fact that a development had been under way for some time, and can be described as a transition stage between manual break-bulk cargo handling and the container system.

One important innovation which anticipated containerization was the putting together of small-size packages to large units by pre-slinging and palletization for better utilization of crane capacity. This required equipment for lifting and carrying those units which no longer could be handled manually in ship holds and on the quay apron. The forklift truck was the most important answer to this demand.

The increase in package unit size was not without its problems. Given the conventional gear for cargo handling, the bigger units increased the risk of damage and the danger of the work. Furthermore, at least in the past, as cargo had to be lying in the open for rather long periods without protection, unpredictability of rain became an awkward problem (in the temperate zones).

The container was the logical continuation of the trend towards bigger units; it was an answer to several demands. From the handling-of-cargo point of view, by standardization of container dimensions* expensive tailor-made

·Until recently standard container dimensions were 20 x 8 x 8 feet, and 40 x 8 x 8 feet for a large one. Today a standard container has more height and is of dimensions of 20 x 8 x 8.5 feet, and 40 x 8 x 8.5 or 40 x 8 x 9.5 feet respectively. Some shipping lines are using non

standardized containers. Sea-Land still has boxes of dimensions 35 x 8 x 8 feet in use, but these are gradually being removed from operation, and American President Line (APL) are currently using 45 x 8 x 9.5 feet containers, which are not officially approved by the International Container Organization (lCO).

Characteristics of demand and supply 25

container cranes of very-high capacity could achieve sufficiently high degree of capacity utilization to be profitable. The weight per crane was raised to meet the container weight. Cranes of capacity between 30 and 45 tons were designed (container cranes of capacity of less than 30 tons are not in use, and today all new designs lift no less than 35 tons). Thanks to this and by eliminating the need for stowing the cargo in the ship's hold, the continuous work of the crane was not impeded by that notorious bottleneck.

At a container berth, where, as is usual, two container cranes are used simultaneously, fifty to sixty containers an hour can be loaded and/or unloaded, and, which is most significant, the operation does not require more than about ten men, induding the crane-operators. The productivity per manhour in this case is approximately 70 tons. Thanks to the containerization the potential man-hour productivity has risen (conservatively calculated) fifty times!

The new generation of container ships - the very large container carrier (VLCC) - of 3000 to 4400 TEUs (twenty foot equivalent units) may require more than the standard two cranes per berth, and are often supplemented by cranes of other berths. At Port Newark for example, 900-foot container ships are worked by four and sometimes by six container cranes. It should be recalled that while working, container cranes must normally have a space of a hold width between them, due to the dense container traffic on the quay.

However, bearing in mind that the lay time of ships has also been drastically reduced by cargo unitization - in the aforementioned illustrative example the handling performance per ship-hour is about 100 tons in the break-bulk case and about 700 tons in the container case - this question presents itself; Why have not all liner services already been containerized? There are three main reasons why break-bulk cargo handling still prevails in most trades.

All cargo cannot, or is not very suitable to put in a container box. 2 The tremendous labour-saving potential is somewhat of an optical illusion.

The stowage and unstowage of break-bulk cargo in the ship's hold is eliminated, but reappears to some extent in the stuffing and stripping of containers, which are second packages, so to speak.

3 The containers themselves, the container cranes, and the container ships are relatively expensive equipment.

Ofthe three the unsuitability of cargo is the most important one. In addition to the fact that some cargo is not fit to be stowed in a container, there are types of cargo that cannot be mixed within a container (raisins and coffee is an example).

Where the containerization has been carried out, a reduction in freight rates has not occurred; the cost of the capital which has been substituted for labour is very substantial. The hope is that the containerization will halt the trend of soaring freight rates, and not that it will really turn this trend downwards.

For containerization to be really labour-saving it is required that the

26 The liner shipping industry

containers are stuffed already at the premises of the shippers, and are not stripped until the containers have reached their final destinations. In these circumstances the containerization does not only save labour for loading and unloading of ships, but also eliminates the need for expensive break-bulk cargo handling at the landside of the ports, and at inland re-Ioading depots.

In developing countries the potential for door-to-door container transports has so far not seemed very great, depending among other things on the underdeveloped inland transport infrastructure; the stevedoring costs have not yet reached the critical level, where a switch from labour-intensive breakbulk cargo handling to the very capital-intensive container system is justified unless significant inland transport and handling cost savings can be achieved in addition.

A reservation to this observation is that the development of container trade does not depend only on the cost savings achieved at one end of the route. In the trade between developing and developed countries, a developing country may start container services to meet demands set by the developed country, although this development would not be justified by the cost savings of the developing country. Dar es Salaam in Tanzania and Mombasa in Kenya are examples of ports with container-service developments which aim at integrating the trade of these countries with that of the developed nations. The most captive non-containerized trade will consequently be trade between the developing countries.

Container lift-on/lift-off is the most common handling technique. Containers can also be rolled on and off, if the ship is equipped with stern-, bow- or side-ports. In that case the bogies have to be left attached to the containers in order to achieve really speedy handling, which means that the space utilization of the ship's hold cannot be as high as when the containers are stacked on each other. Two great advantages of the roll-on/roll-offtechnique are, on the other hand, (i) that the expensive container cranes are not required, and (ii) that great flexibility as to the combination of different units - containers, trailers, trucks, cars etc. - is obtained. The roll-on/roll-off technique is a development of traditional ferry services. It is predominant on short sea routes, but in the last few years roll-on/roll-off ships have spread into deep-sea trades, particularly into trades including large shipment of motor cars.

On the dense routes of the international trade, fully cellular container ships can be employed. On thin routes, the volume of cargo and the lack of port facilities may encourage the use of mix-ships. Where ports do not have liftonjIift-off container cranes, roll-on/roll-off (RoRo) ships are often being used. There are two methods of handling cargo in a RoRo ship, both requiring little port investment. According to one, any cargo - containerized or otherwise -is put on a chassis, which is connected to a tractor, which carries the load out ofthe ship and the port. Alternatively, the cargo may be put on a 'slave chassis' which is much lower and will be used only in the port area. By the other

Characteristics of demand and supply 27

method - the 'Stow-Ro' technique -large forklifts take the containers up and down the ramp and stow them in/out of the holds ofthe RoRo ship. Such ships are currently in widespread use in the thin trades, and are also used in some dense routes, e.g. the North Atlantic route.

A third unit-load system is represented by the barge-carrying vessels, which have appeared recently. As distinguished from the traditional tug towing a number or barges, the barges (lighters) are carried aboard the mother ship. The so-called lighter aboard (LASH) ships, to which a great deal of attention has been paid, can carry some seventy barges each of 850 tons holding capacity. LASH ships were built during the 1970s. There are fewabout thirty - ships of this kind operating in the mid-1980s.

There is a newer version of the LASH, which is called SEABEE, where the barges are designed according to modular dimensions of containers. LASH ships can also carry containers but are not specifically designed to do so, with the result that some idle space will remain. SEABEEs and LASHs have been operating in a number of different trades and particularly on routes between developing and developed countries. Prudential line and Lykes Brothers line, for example, operate these types of ships in the East African trade. SEABEEs and LASHs are big and expensive vessels. The penetration of container ships to many trades including those of developing countries, has lowered their attractiveness. In the mid-1980s there is no new construction of LASH and SEABEE ships.

1.5.2 Composition of the fleet of general cargo ships, and current tendencies

A decade ago, a very topical question in the shipping world was, how quick, and how far the penetration of containerization will be in liner shipping? Will something be left for conventional liners, or will this ship type be as completely replaced by unit-load carriers in the next decade, as horses were by tractors two or three decades ago? Two developments are relevant to consider: the development of the total general cargo sector, and the development of the modal split in this sector.

The most expansive part of seaborne trade in the post-war period has been the sector represented by the major bulk commodities - especially oil, coal, iron ore and grain. (So far as the oil trade is concerned the expansion came to an abrupt halt in 1975.) The general-cargo sector has been growing steadily but not at quite the same pace. In the 1970s the annual rate of growth has been a good 5%.

The total tonnage of ships for general cargo has been growing much slower in the 1970s than the general-cargo trade in ton-miles. The average rate of growth of this tonnage was only 2%. The explanation for the disparity of the trade and tonnage growth rates is two-fold.

28 The liner shipping industry

The productivity in terms of ton-miles performed per ton of deadweight has been increasing.

2 Specialized bulk carriers have made inroads into the general cargo trade.

The source of the productivity increase is easily pinpointed. During the 1970s the share of unit-load carriers of the total fleet of ships for general cargo has been steadily growing. Under otherwise equal conditions the carrying capacity in ton-miles of a container ship, or a RoRo ship is about three times greater than the carrying capacity of a conventional liner of the same tonnage. (This is probably a conservative estimate. Koike (1983), ofNYK lines, argued that 'the transport efficiency of container ships is believed to be at a level six (6) times that of conventional vessels'.) This is explained by higher speed at sea, and, above all, considerably shorter turn-around times in port of unit-load carriers.

It should, however, be remembered that the price of a container ship (including the containers) per dwt is not far from three times that of a conventional liner. The fact that the total deadweight of ships for general cargo has been slow-growing does not mean that investments in new ships have been slow.

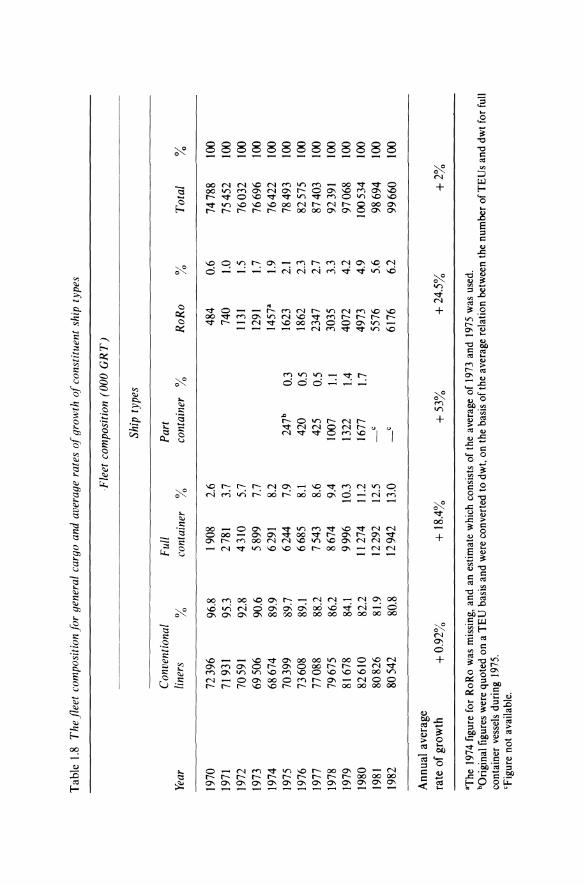

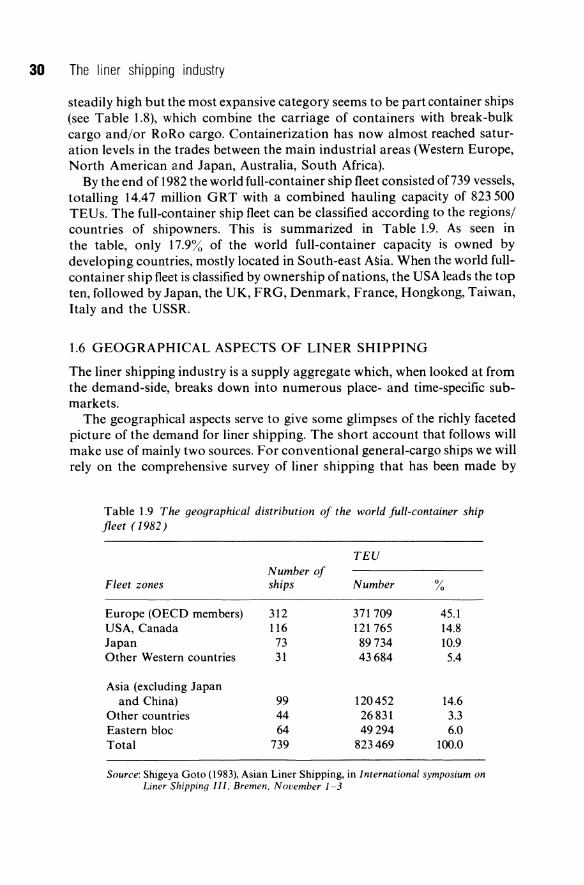

Table 1.8 below gives the composition of the general cargo fleet and the average annual rate of growth of its constituent ship types between 1970 and 1982. By the end of the period all unit-load ships measured in GRTconstituted approximately one-quarter of the total GRT of conventional liners. Bearing in mind that the productivity per GRT of unit-load ship is approximately three times greater, the liner fleet composition in terms of carrying capacity is approximately 40% unit-load ships and 60% conventional liners. Quite another matter is how the total liner cargo is divided between conventional liners and unit load carriers. The old ships do not disappear automatically as they lose business. However, Koike (1983) estimated that out of a total liner cargo trade of 1369.3 billion ton-miles, 561.3 billion ton-miles was container trade, approximately 41 % of the world liner cargo.

Lawrence (1972; p. 141) estimated that the proportion ofliner cargo carried by container ship would rise from 12% in 1970 to 35-40% by 1975 and 50-60% by 1980. This estimate seems belatedly to have come true, if the carryings of all unit-load ships are taken into account.

By the middle of 1980s it appears that the question raised a decade ago has been answered. Containerization has become the dominant form of liner shipping. By 1985 unpublished accounts of shipping lines estimate the container share in the total trade - full and part load - to be around 60%. In conjunction with the tendency to integrate land and sea transport, it can be predicted that all containerizable cargo will eventually 'go containers', with the trade between developing countries being the last to join. As to shipbuilding the rate of growth of container ship and RoRo ship investments is

Tab

le 1

.8

Th

e fl

eet

com

posi

tion

for

gen

eral

car

go a

nd a

vera

ge r

ates

of g

row

th o

f con

stit

uent

shi

p ty

pes

,Fle

et c

ompo

siti

on (

00

0 G

RT

)

Ship

typ

es

Con

vent

iona

l F

ull

Par

t Ye

ar

line

rs

%

cont

aine

r %

co

ntai

ner

%

Ro

Ro

%

T

ota

l %

1970

72

396

96.8

19

08

2.6

484

0.6

7478

8 10

0 19

71

7193

1 95

.3

2781

3.

7 74

0 1.

0 75

452

100

1972

70

591

92.8

43

10

5.7

1131

1.

5 76

032