life sciences industry overview boot camp - … sciences industry overview boot camp ... onesource,...

TRANSCRIPT

Life Sciences Industry Overview

Boot Camp

Phyllis Feeney – Bristol-Myers Squibb Company Mike Lombardo / Mike Makovec / Matt Riviello –

Deloitte & Touche LLP

March 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means

of this presentation, rendering accounting, business, financial, investment, legal,

tax, or other professional advice or services. This presentation is not a substitute

for such professional advice or services, nor should it be used as a basis for any

decision or action that may affect your business. Before making any decision or

taking any action that may affect your business, you should consult a qualified

professional advisor. Deloitte shall not be responsible for any loss sustained by

any person who relies on this presentation.

Disclaimer

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Agenda

Workshop Leaders’ Welcome and Opening Remarks - Matt Riviello

Gross To Net Principles - Mike Makovec

• Estimation Process

• Hot Topics

• Sales Returns and Other Considerations

Break

Government Programs Landscape and Overview – Phyllis Feeney

• Overview of Government Programs

• Discount and Rebate Overview

Basic Revenue Principles – Mike Lombardo

• Product Launch Considerations

• Collaborations / Multi Element Arrangements

• Licensing Arrangements / SEC Comment Letter Trends

Concluding Comments

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Introduction of Speakers

• Matt Riviello – Deloitte & Touche LLP Partner

• Phyllis Feeney – Executive Director, Pricing & Reimbursement (Bristol-Myers Squibb Company)

• Mike Lombardo – Deloitte & Touche LLP Senior Manager

• Mike Makovec – Deloitte & Touche LLP Senior Manager

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Polling Question: Life Sciences Industry Trends

By show of Hands, let’s see what the make-up of our room is today. Please raise

your hand as I call out the type of organization / services firm you may be with?

A – Branded Pharmaceutical Manufacturer

B – Generic Pharmaceutical Manufacturer

C – Biotechnology Entity

D – Medical Device Manufacturer

E – Services Organizations (CROs / CMOs)

F – Professional Services Firm (Auditor, Consultant, etc.)

G - Other

©2005 Firm Name/Legal Entity

Life

Sciences

Industry

Description:

Pharmaceutical companies

• develop “small molecule” compounds to treat infections, cardiovascular conditions,

gastrointestinal/metabolism, inflammatory diseases, women’s health care, and other

chronic and acute conditions.

Biotechnology companies • develop “large molecule” compounds derived from living organisms. Focus therapeutic

areas include oncology, autoimmune disorders, and infectious diseases.

Medical Device companies • develop products including diagnostic equipment, cardiovascular stents, orthopedic

products, implantables, and monitoring devices. The five major therapeutic categories

include: cardiology, diagnostic imaging, orthopedics, invitro diagnostics, and vascular

diseases.

Service companies include contract research organizations (CROs), contract

manufacturing organizations (CMOs) and drug wholesale distributors.

– The CRO market is highly fragmented, consisting of more than 1,000 companies with

revenues ranging from $1 million to $1 billion. Large portion of CRO’s revenues is

derived from outsourcing of clinical trials.

– CMO’s offer a range of services including primary production, physical processing,

clinical lots manufacturing, and formulation development.

– The drug wholesale distribution segment is highly consolidated in the U.S. with

three companies contributing 90-95% of the U.S. third-party distribution market.

Life Sciences Industry Snapshot

Sources: OneSource, S&P Industry Reports, Datamonitor Reports Copyright © 2015 Deloitte Development LLC. All rights reserved.

©2005 Firm Name/Legal Entity

7

Commercialization

Development

7

Pharmaceutical Product Life Cycle P

re-D

isc

ove

ry:

Ta

rge

t

Ide

nti

fic

ati

on

& V

ali

da

tio

n

Research

Discovery

Find Drug

Candidate

Pre-

Clinical

Animal

Testing

Phase III

Test large

group for

safety

and

efficacy

Phase I

Test

small

group of

healthy

humans

Phase II

Test

small

group

with

disease

FDA

Review

Regulatory

review for

approval

Post-Marketing

Surveillance

Phase IV clinical

trials to monitor

adverse reactions,

drug safety and

clinical testing for

new indications

IND

Su

bm

itte

d

ND

A S

ub

mit

ted

Dru

g L

au

nc

he

d

Pilot-Scale

Manufacturing

Large Scale Clinical

Trial Manufacturing Full-Scale Commercial Manufacturing

The complex drug development process typically spans 10-15 years from research to approval. The

high risk and likelihood of failure during the R&D process drives companies to focus on drugs that

will deliver the greatest return on investment.

For every 5,000-10,000 compounds discovered, 250 enter pre-clinical trials. Of those 250, only

5 move into Phase I, II, and III trials. Of those 5, only1 drug will receive FDA approval. One FDA-Approved

Drug

• On average, it takes 15 years to bring a drug from clinical trials to commercial use.

• The average cost of developing a drug is nearly $900 million.

• Only 3 out of 10 drugs reaching the market generate enough revenue to recover the average development costs.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

©2005 Firm Name/Legal Entity

CDC

EPA

The Regulatory Landscape

FDA

SEC

OIG

FTC

CMS

HIPAA GLP

GMP

PDMA

Part 11

Kickbacks False Claims

SOX 404

FCPA

ePedigree

Privacy

GCP Gov Price

Reporting

IT Security

Pharmaceutical

Company Commercial

Operations are subject

to numerous external

regulators and

regulations

DDMAC

Copyright © 2015 Deloitte Development LLC. All rights reserved.

HCR

©2005 Firm Name/Legal Entity

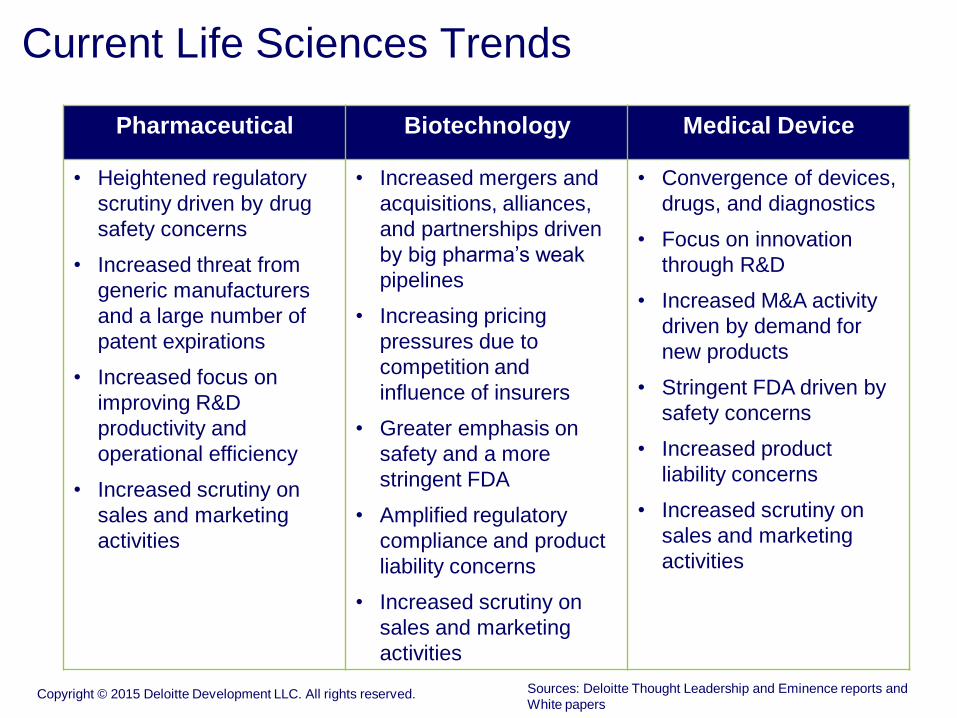

Current Life Sciences Trends

Pharmaceutical Biotechnology Medical Device

• Heightened regulatory

scrutiny driven by drug

safety concerns

• Increased threat from

generic manufacturers

and a large number of

patent expirations

• Increased focus on

improving R&D

productivity and

operational efficiency

• Increased scrutiny on

sales and marketing

activities

• Increased mergers and

acquisitions, alliances,

and partnerships driven

by big pharma’s weak

pipelines

• Increasing pricing

pressures due to

competition and

influence of insurers

• Greater emphasis on

safety and a more

stringent FDA

• Amplified regulatory

compliance and product

liability concerns

• Increased scrutiny on

sales and marketing

activities

• Convergence of devices,

drugs, and diagnostics

• Focus on innovation

through R&D

• Increased M&A activity

driven by demand for

new products

• Stringent FDA driven by

safety concerns

• Increased product

liability concerns

• Increased scrutiny on

sales and marketing

activities

Sources: Deloitte Thought Leadership and Eminence reports and

White papers Copyright © 2015 Deloitte Development LLC. All rights reserved.

©2005 Firm Name/Legal Entity

Current Life Sciences –Growth Drivers

Pharmaceutical Biotechnology Medical Device

• Aging population

• Increased life

expectancy

• Increasing healthcare

expenditures as a

percentage of GDP in

emerging and developed

markets

• Rising incidence of

chronic and acute

diseases

• Technological innovation

• Product innovation

• International expansion

• Aging population

• Higher incidence of

chronic diseases

• Scientific and

technological advances

• Aging population

• Higher incidence of

chronic diseases

• High level of private

equity funding

Sources: Deloitte Thought Leadership and Eminence reports and

White papers Copyright © 2015 Deloitte Development LLC. All rights reserved.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Polling Question: Life Sciences Industry Trends

What Keeps Life Sciences Executives Up at Night within your

Organization?

A – Supply Chain challenges

B – Increasing scrutiny by the FDA

C – Expansion of market share and market penetration

D – Capitalizing on emerging markets

E – All of the Above

©2005 Firm Name/Legal Entity

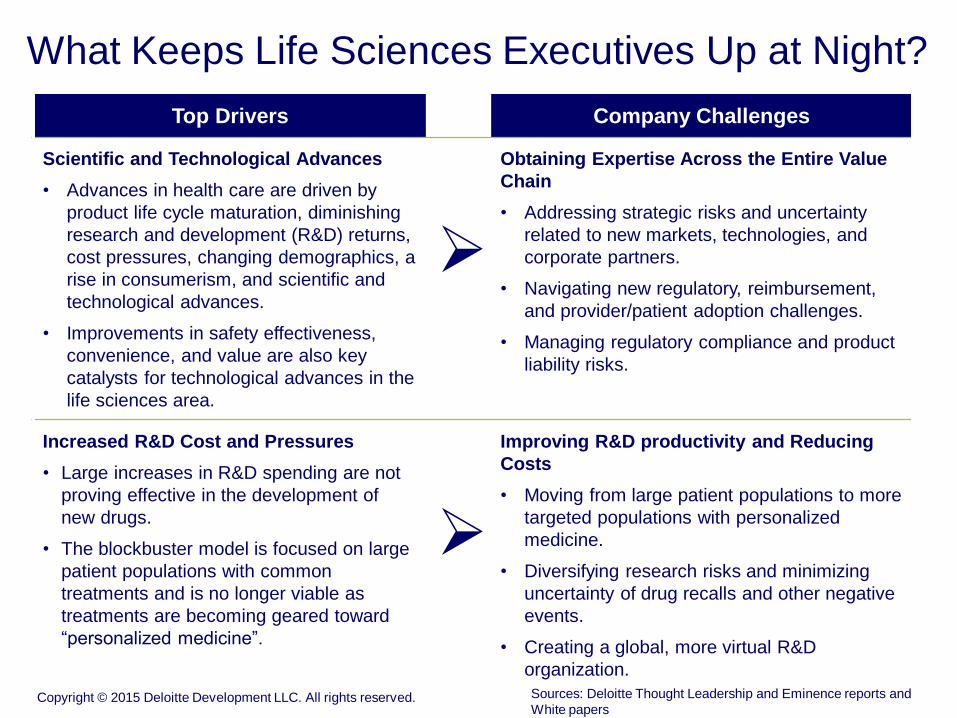

What Keeps Life Sciences Executives Up at Night?

Top Drivers Company Challenges

Scientific and Technological Advances

• Advances in health care are driven by

product life cycle maturation, diminishing

research and development (R&D) returns,

cost pressures, changing demographics, a

rise in consumerism, and scientific and

technological advances.

• Improvements in safety effectiveness,

convenience, and value are also key

catalysts for technological advances in the

life sciences area.

Obtaining Expertise Across the Entire Value

Chain

• Addressing strategic risks and uncertainty

related to new markets, technologies, and

corporate partners.

• Navigating new regulatory, reimbursement,

and provider/patient adoption challenges.

• Managing regulatory compliance and product

liability risks.

Increased R&D Cost and Pressures

• Large increases in R&D spending are not

proving effective in the development of

new drugs.

• The blockbuster model is focused on large

patient populations with common

treatments and is no longer viable as

treatments are becoming geared toward

“personalized medicine”.

Improving R&D productivity and Reducing

Costs

• Moving from large patient populations to more

targeted populations with personalized

medicine.

• Diversifying research risks and minimizing

uncertainty of drug recalls and other negative

events.

• Creating a global, more virtual R&D

organization.

Sources: Deloitte Thought Leadership and Eminence reports and

White papers Copyright © 2015 Deloitte Development LLC. All rights reserved.

©2005 Firm Name/Legal Entity

What Keeps Life Sciences Executives Up at Night?

Top Drivers Company Challenges

Increased Competition and Pricing

Pressures

• Rising global competitive forces are

spurring innovation and forcing life science

companies to be able to create successful

strategic collaborations and alliances.

• Benefits of collaboration include increased

access to: 1) marketing and distribution

channels, 2) R&D, 3) manufacturing, 4)

regulatory expertise, and 5) new markets.

Managing Complex Business Functions and

Stakeholders

• Partnering effectively with firms that have

different expectations, operating models, and

cultures.

• Companies need agile research and

development, sales, and marketing

organizations to partner and execute.

Rising Influence of Emerging Markets

• The role of emerging markets as

developers and consumers across the life

science sector is projected to significantly

grow in the next decade.

• Life science companies estimate 25% of

their revenues to come from emerging

markets by 2015.

Selecting the Right Investment Expansion

Strategy

• Critical success capabilities include an

effective regulatory strategy, M&A experience,

alliances, outsourcing, R&D, product

discovery, manufacturing, and sales and

marketing.

Sources: Deloitte Thought Leadership and Eminence reports and

White papers Copyright © 2015 Deloitte Development LLC. All rights reserved.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – How do the dollars break down

National Health Expenditure Accounts (“NHEA”)

• Official estimates of total health care spending in the United

States

• Provides U.S. expenditures for spending including health

care goods and services, net cost of health insurance,

government administration, etc.

Sources: Centers for Medicare & Medicaid Services

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – How do the dollars break down

• U.S. health care spending growth:

Spending grew 3.6% in 2013

Reaching and estimated $2.9 trillion

Estimated to be approximately $9,255 per person

Health care spending – approximately 17.4% of Gross

Domestic Product

Note – (2013 – latest available statistics from CMS)

Sources: Centers for Medicare & Medicaid Services

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – How do the dollars break down

Sources: Centers for Medicare & Medicaid Services

Break down of Health Insurance spending:

• Private Health Insurance accounted for 33%

• Medicare accounted for 20%

• Medicaid accounted for 15%

• VA, DOD, CHIP for 4%

• Out of Pocket spending for 12%

• Remainder from various programs

Note – the sum of the pieces may not equal 100% due to rounding

Health Insurance

72%

Out of Pocket 12%

Other Third Party Payers /

Programs 8%

Investment 6%

Government Public Health

Activities 3%

Calendar Year 2013

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Polling Question: Life Sciences Industry Trends

Where did the largest amount of health care spending go in

2013?

A – Prescription Drugs

B – Government Administration

C – Physicians and Clinics

D – Hospital Care

E – Investment

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – How do the dollars break down

Hospital Care 32%

Physicians and Clinics

20%

Other 14%

Prescription Drugs 9%

Dental and Other Services

7%

Government Administration

7%

Investment 6%

Nursing Care and CCRAs

5%

Calendar Year 2013

Sources: Centers for Medicare & Medicaid Services

How does Other Spending break down?

• Other Health, Residential, and Personal Care – 5%

• Durables & Other Non-Durables – 3%

• Government Public Health Activities – 3%

• Home Health Care – 3%

Note – the sum of the pieces may not equal 100% due to rounding

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Where is Spending Projected to Go in 2013 and beyond?

• Health care spending – projected to grow at an average

rate of 5.7% from 2013 to 2023

• Faster spending and growth in 2014 driven by:

• Improving economic conditions

• Affordable Care Act coverage expansions

• Aging population

Sources: Centers for Medicare & Medicaid Services

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Other Market Trends

• Focus shifting to biologics and genomics = advances in

treatments that use the body’s own defenses to attack

disease

• Industry and analysts anticipate that Oncology and auto-

immune disorders to have larger potential for growth

• More precise treatment through better diagnostic tools

• Specialty and biologics expected to lead in industry profits

• M&A activity reaching all time highs

Sources: Deloitte Thought Leadership and Eminence reports and

White papers

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Other Market Trends

• M&A Activity in Life Sciences

• Global YTD value of deals was $600 billion for July 2014

compared to $200 billion for July 2013

• One way forward to respond to changing landscape of the

life sciences industry

Sources: Deloitte Thought Leadership and Eminence reports and

White papers

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Other Market Trends

• Driving Factors of M&A Activity in Life Sciences

• Financial Pressures

• Decreased reimbursement

• Expiration of patents

• Diversification of portfolios

• Changing demographic trends – aging population

• Tax considerations due to global environment and looking

for ways to restructure that allow for efficient use of

foreign capital

Sources: Deloitte Thought Leadership and Eminence reports and

White papers

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Other Market Trends

• Types of Transactions expected in the coming years

• Collaboration Agreements

• Licensing Agreements

• Mergers & Acquisitions

• Joint Ventures

Sources: Deloitte Thought Leadership and Eminence reports and

White papers

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Life Sciences Industry – Other Market Trends

©2005 Firm Name/Legal Entity

Questions?

In recognition of completing the Industry Boot Camp on March 16, 2015

at the 11th Annual CBI Pharmaceutical/Biotech Accounting

and Reporting Congress

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Matt Riviello: AERS Partner

Office: 215-405-7774

Mike Lombardo: AERS Senior Manager

Office: 973-602-6860

Mike Makovec: AERS Senior Manager

Office: 973-602-5071

Deloitte Presenter Contact Information