libor: what happened and where are we going? - m.acc.com · 2017 - arrc recommended replacing libor...

TRANSCRIPT

1

LIBOR: What happened and where are we going?

NEIL T. BLOOMFIELD

ZACHARY J. KING

ROBERT I. KENNY

JAMES (JIM) A. BLAIR, III

2

What is LIBOR

LIBOR submitters are asked the following question:

At what rate could you borrow funds, were you to do so by asking for and then

accepting interbank offers in a reasonable market size just prior to 11 am London

time?

Reported for a series of terms from overnight to 1 year.

USD, EUR, GBP, JPY, CHF

Based on professional judgment, not transactions

3

What is LIBOR used for?

Amount in

Billions

0

50

100

150

200

250

Interest rate swaps Exchange-traded interest rate futures

and options

Forward rate agreements Syndicated loans Floating rate notes

Data from the Financial Times on July 27, 2017

LIBOR in Financial Instruments

4

Why Did People Lie?

Improve trading performance

Personal gain

Avoid scrutiny during the financial crisis

5

Traders Behaving Badly

Aggressive Traders

“We have another big fixing tom[orrow] and with the market move I was

hoping we could set [certain] Libors as high as possible.”

“cld you do me a favour would you mind moving you 6m libor up a bit today, i

have a gigantic fix”

“you're going to help me, promise me?????”

Receptive Submitters

“Hi morning mate! Do you have any special requests for the libor?

“Done, for you big boy.”

“if you aint cheating, you aint trying.”

6

The Spider’s Network

Tom

Hayes

Broker

Broker

Broker

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Submitter

Request for

false rates

False

suggested rates Bank

Trader

Bank

Trader

7

Avoiding a Self Fulfilling Prophecy

LIBOR is a reflection of the submitter’s cost of funds.

High cost of funds in the financial crisis means financial difficulties.

During the financial crisis Barclays’ management ordered the

submitters to provide rates that were lower than its cost of funds to

alleviate concerns about Barclays’ financial health.

Barclays employees’ attempted to alert the BBA and FSA

Guidance from BOE interpreted as an instruction to lie.

8

Settlements

9

LIBOR Replacement/Phase-Out Timeline

August 2012 - Wheatley Review - Chancellor of the Exchequer (UK).

February 2013 - G20 asks Financial Stability Board (FSB) (an international

organization) to review.

July 2013 - IOSCO set forth a basic framework at request of FSB.

July 2014 - FSB made further recommendations.

November 2014 - Federal Reserve (US) convened the Alternative Rates

Reference Committee (ARRC) to propose alternatives to LIBOR.

Note that while the ARRC is a United States effort, other jurisdictions

undertook similar reviews and reforms with some level of coordination.

10

LIBOR Replacement/Phase-Out Timeline

Andrew Bailey – statement of the FCA:

FCA will not compel panel banks to make

LIBOR submissions after end of 2021.

Unclear when or if LIBOR will actually be phased out.

Benchmark that exists side-by-side with LIBOR or wholly replace LIBOR?

11

Alternative Reference Rates Committee

ARRC goals for alternative reference rates:

Based on actual transactions

Comply with the IOSCO Principles of Financial Benchmarks

Adoption plan that will result in widespread use of ARRC benchmarks

Account for the potential disappearance of LIBOR, which was not originally

contemplated

12

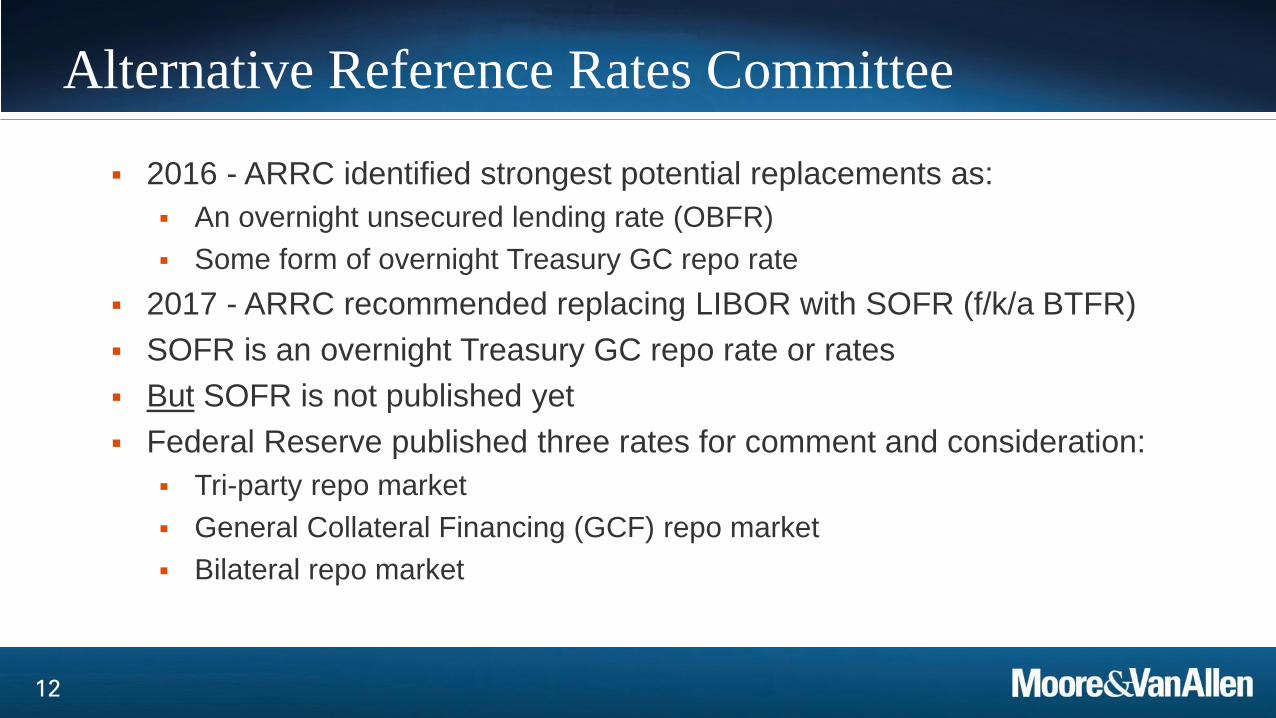

Alternative Reference Rates Committee

2016 - ARRC identified strongest potential replacements as:

An overnight unsecured lending rate (OBFR)

Some form of overnight Treasury GC repo rate

2017 - ARRC recommended replacing LIBOR with SOFR (f/k/a BTFR)

SOFR is an overnight Treasury GC repo rate or rates

But SOFR is not published yet

Federal Reserve published three rates for comment and consideration:

Tri-party repo market

General Collateral Financing (GCF) repo market

Bilateral repo market

13

Issues with LIBOR Phase-Out

Basis Risk – the new rate and LIBOR will not be priced the same.

Replacement rates may vary and administration could be difficult.

Timing – will the industry be able to pull off a “uniform switch” to a new

rate?

May lead to need for new credit agreement and swap documentation.

If the replacement is SOFR, it depends on an overnight rate – how to

price longer tenors?

14

Practical Implications if LIBOR is Discontinued

Potential Increase in Borrowing Costs

Most credit agreements for syndicated credit facilities

switch to using the “Prime Rate” with a reduced spread

Difference as of October 30, 2017*

One-Month LIBOR 1.24%

Prime Rate 4.25% *Money Rates Section of The Wall Street Journal, October 30, 2017

15

Practical Implications (Cont.)

DISCONTINUANCE NOT ANTICIPATED

Lending Example:

Interest shall accrue on the outstanding principal balance of this Note at a variable rate of

interest, adjusted monthly, equal to the LIBOR Rate (as hereinafter defined) plus 3.00% per

annum (the "Interest Rate"). The “LIBOR Rate" for the calculation of interest payable with

any payment shall mean the one-month London Interbank Offered Rate (LIBOR) as

published in the Wall Street Journal on the 1st day of the month preceding the applicable

Payment Date (or, if The Wall Street Journal is not published that day, then on the next day

on which The Wall Street Journal is published)

16

Practical Implications (Interest Rate Swaps)

Swap Floating Rate Language:

“USD-LIBOR-BBA” means that the rate for a Reset Date will be the rate for deposits in U.S.

Dollars for a period of the Designated Maturity which appears on the Reuters Screen

LIBOR01 Page as of 11:00 a.m., London time, on the day that is two London Banking Days

preceding that Reset Date. If such rate does not appear on the Reuters Screen LIBOR01

Page, the rate for that Reset Date will be determined as if the parties had specified “USD-

LIBOR-Reference Banks” as the applicable Floating Rate Option.

17

Lender and ISDA Response

Lenders Updating Forms:

Interest shall accrue on the outstanding principal balance of this Note at a variable rate of

interest, adjusted monthly, equal to the LIBOR Rate (as hereinafter defined) plus 3.00% per

annum (the "Interest Rate"). The “LIBOR Rate" for the calculation of interest payable with

any payment shall mean the one-month London Interbank Offered Rate (LIBOR) (or a

comparable or successor rate which is selected by the Lender) as published in the Wall

Street Journal on the 1st day of the month preceding the applicable Payment Date (or, if The

Wall Street Journal is not published that day, then on the next day on which The Wall Street

Journal is published)

International Swaps and Derivatives Association (ISDA) working on fallback language for

Swaps.

18

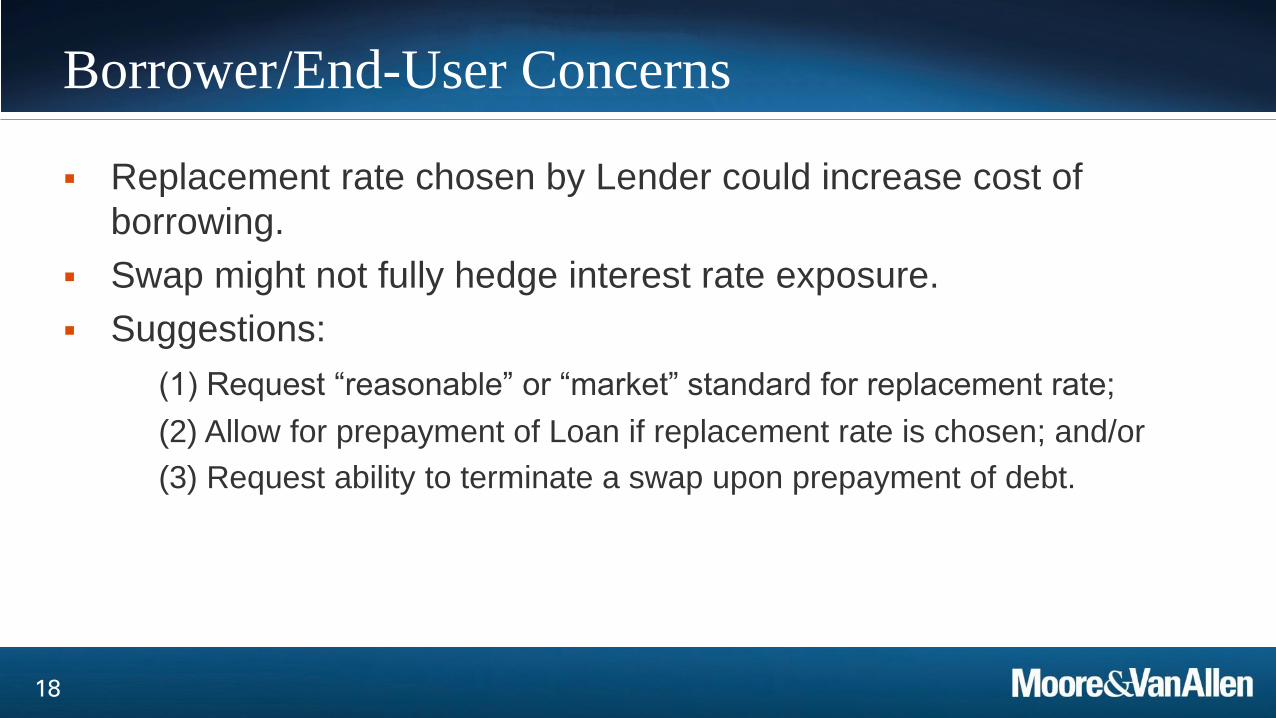

Borrower/End-User Concerns

Replacement rate chosen by Lender could increase cost of

borrowing.

Swap might not fully hedge interest rate exposure.

Suggestions:

(1) Request “reasonable” or “market” standard for replacement rate;

(2) Allow for prepayment of Loan if replacement rate is chosen; and/or

(3) Request ability to terminate a swap upon prepayment of debt.

19

NEIL T. BLOOMFIELD

Neil T. Bloomfield is a member of Moore & Van Allen’s Litigation Team. He specializes in responding to

government investigations, advising on regulatory requirements, and complex commercial litigation.

Mr. Bloomfield regularly represents clients in inquiries by Federal (e.g. CFTC, DOJ, OCC, FRB, SEC, IRS, and

various U.S. Attorney's offices), State (e.g. the North Carolina Attorney General and other state Attorneys General,

and the North Carolina Department of Revenue) and international authorities (e.g. U.K. Financial Conduct

Authority, European Commission, Monetary Authority of Singapore, and Hong Kong Monetary Authority). In

addition to these inquiries, he regularly conducts internal investigations for matters ranging from compliance with

internal policies to alleged violations of federal and state laws and regulations. Mr. Bloomfield takes a holistic

approach to investigations starting with uncovering the issues and defending the company under investigation, but

then moving past the immediate issues to enhance compliance policies and procedures and monitoring and

testing to make sure that any issues that are identified are not repeated across the enterprise.

Mr. Bloomfield also assists clients in responding to a variety of regulatory requirements including Comprehensive

Capital Analysis and Review (“CCAR”) for ongoing regulatory investigations and potential legal exposure for

events that may occur but have not yet impacted the company; Recovery and Resolution Planning and related

training for boards of directors; Risk Data Aggregation and Reporting Requirements; and Sarbanes-Oxley

whistleblower programs. As part of this practice, Mr. Bloomfield provides assistance in designing or enhancing

programs to comply with applicable regulations, legal opinions on regulatory compliance, drafting policies to

promote regulatory compliance, and preparing materials and training to promote internal initiatives and achieve

regulatory compliance.

20

ROBERT I. KENNY

Robert I. Kenny is a member of Moore & Van Allen PLLC and is part of the firm’s Financial

Services team.

Mr. Kenny started the derivatives practice at MVA and is the firm’s primary representative to

the International Swaps and Derivatives Association (ISDA) of which MVA is an associate

member. In addition to his derivatives work Mr. Kenny also represents lenders and borrowers

in equipment finance transactions with respect to aircraft, rolling stock, and other assets and

is named among Best Lawyers in America for Equipment Finance Law, 2007-2017.

21

ZACHARY J. KING

Zachary J. King is a counsel in the Financial Services Department of Moore & Van Allen PLLC.

Mr. King’s focus is on all manner of derivatives regulation and transactions. Mr. King has represented dealers,

brokers, exchanges, asset managers, and end-users on several issues related to the Commodity Exchange Act

and CFTC Regulations. Mr. King’s broad experience in the derivatives space includes in-house representation, as

well as time with the CFTC and the Washington, DC offices of WilmerHale.

Highlights of Mr. King’s experience include:

Registration of swap execution facility and creation of related policies and procedures

Negotiation of derivatives trading platform agreements

Registration of swap dealer, multiple introducing brokers and multiple commodity trading

advisors/commodity pool operators, and creation of related policies and procedures

Advise end-users such as airlines and energy companies regarding potential litigation and enforcement

actions in connection with position limits, market manipulation and trade practice violations

Create document retention policies and procedures for CFTC registrants

Advise clients on thresholds for swap dealer and major swap participant registration

22

JAMES (JIM) A. BLAIR, III

James (Jim) A. Blair, III is the General Counsel of WCM Global Wealth, LLC.

Jim, a native Texan, obtained his Bachelor of Arts (History) from the University

of Texas at Austin in 1987. He then attended Dallas Theological Seminary in

Dallas, Texas, and finished his post-graduate education in New York, obtaining

his Juris Doctor Degree from the Syracuse University College of Law in 1993.

After law school, Jim and his wife moved to South Carolina where he practiced

business and commercial law before becoming General Counsel for WCM

Global Wealth, LLC in 2015. Jim and his family live in Charleston, S.C.