libby ch 13

TRANSCRIPT

Chapter 13 Statement of Cash FlowsChapter 13 Statement of Cash Flowsread pp. 658-662, 665-666,677-680read pp. 658-662, 665-666,677-680

* Classification of Cash Flows as operating, investing, & financing

* Identify the basic differences between the indirect & direct methods for reporting operating cash flows

* Preparing the operating activities cash flow using the indirect method

* Significant non-cash financing & investing activities * Ratios

13-5

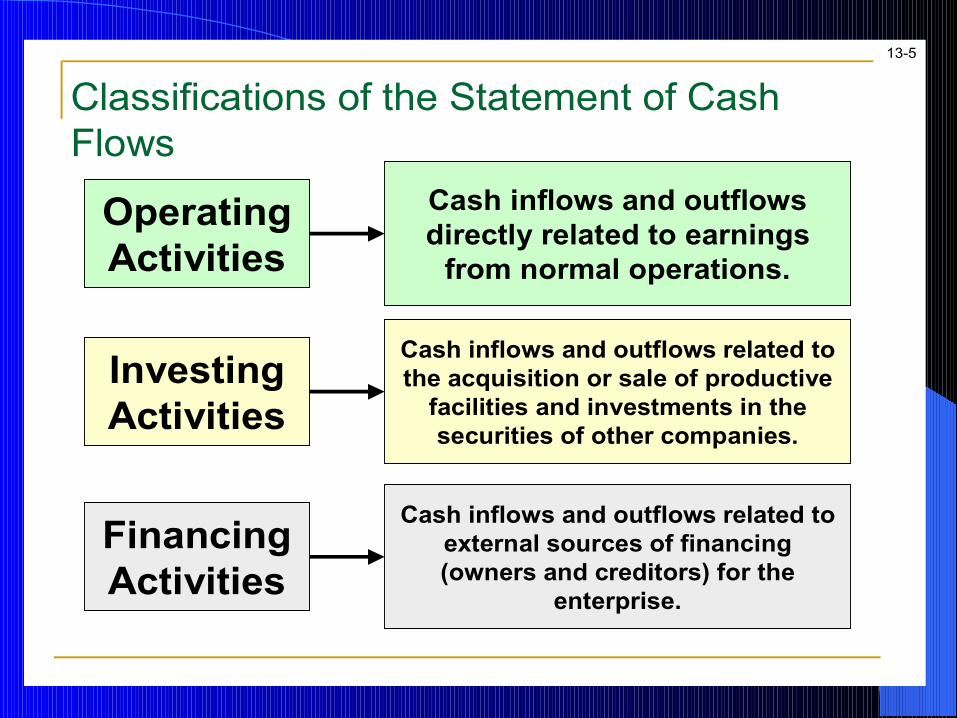

Classifications of the Statement of Cash Flows

Operating Activities

Cash inflows and outflows directly related to earnings

from normal operations.

Investing Activities

Cash inflows and outflows related to the acquisition or sale of productive

facilities and investments in the securities of other companies.

Financing Activities

Cash inflows and outflows related to external sources of financing (owners and creditors) for the

enterprise.

13-6

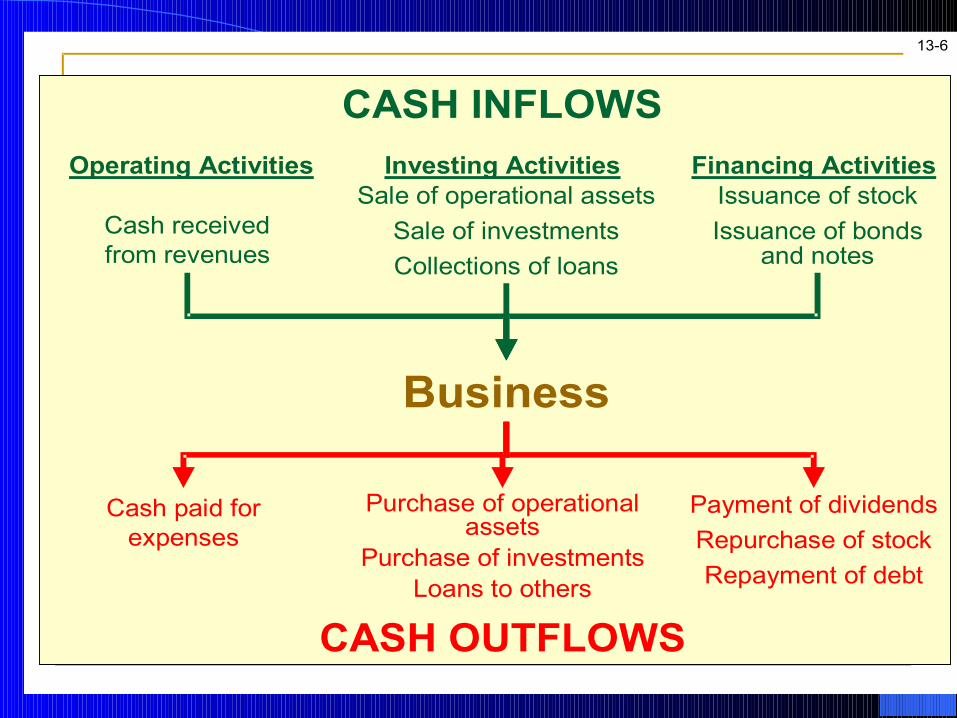

Investing ActivitiesOperating Activities Financing ActivitiesSale of operational assets

Sale of investments

Collections of loans

Cash received from revenues

Issuance of stock

Issuance of bonds and notes

CASH INFLOWS

Business

CASH OUTFLOWS

Purchase of operational assets

Purchase of investmentsLoans to others

Cash paid for expenses

Payment of dividends

Repurchase of stock

Repayment of debt

13-7

Cash Flows from Operating Activities

Cash Flows from

Operating Activities

Cash Flows from

Operating Activities

InflowsCash received from: Customers Dividends and interest on

investments

InflowsCash received from: Customers Dividends and interest on

investments

+

OutflowsCash paid for: Purchase of goods for resale

and services (electricity, etc.) Salaries and wages Income taxes Interest on liabilities

OutflowsCash paid for: Purchase of goods for resale

and services (electricity, etc.) Salaries and wages Income taxes Interest on liabilities

_

13-8

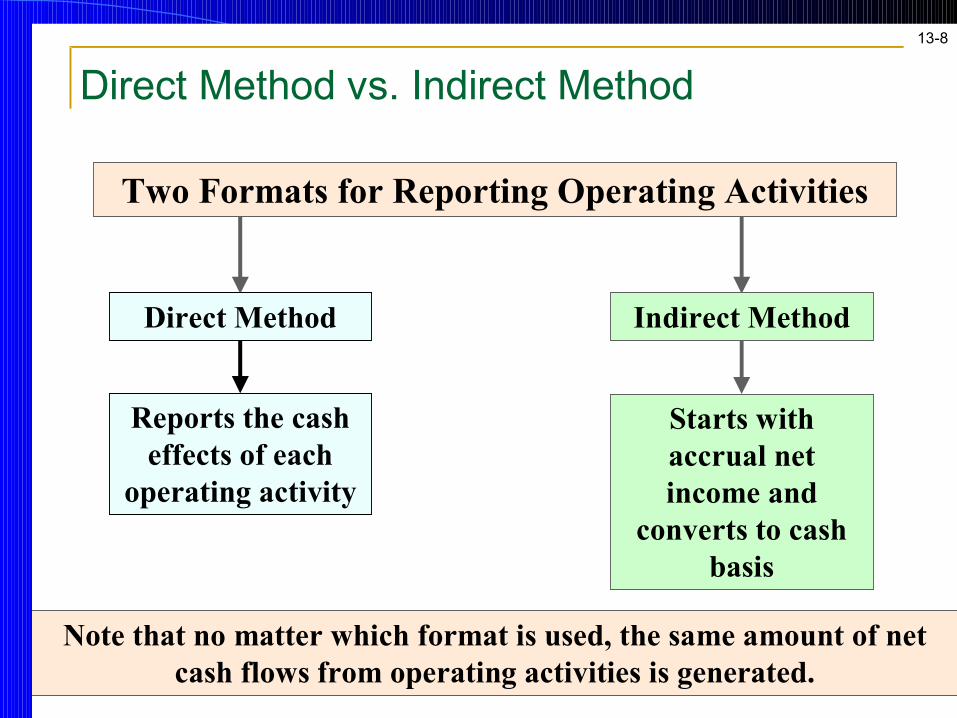

Direct Method vs. Indirect Method

Two Formats for Reporting Operating Activities

Reports the cash effects of each

operating activity

Direct Method

Starts with accrual net income and

converts to cash basis

Indirect Method

Note that no matter which format is used, the same amount of netcash flows from operating activities is generated.

13-11

(in thousands) Three months ended(unaudited) March 27, 2004Cash flows from operating activities: Net income 1,271$ Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 2,543 Changes in assets and liabilities: Accounts receivable 861

Inventory (577)Prepaid expense (322)Accounts payable (52)Accrued expenses (954)

Net cash provided by operating activities 2,770Cash flows for investing activities: Purchases of property, plant and equipment (2,373) Purchase of short-term investments (4,627) Net cash provided by investing activities (7,000) Cash flows from financing activities: Purchase of treasury stock (4,409) Proceeds from issuance of stock 5,593 Net cash used in financing activities 1,184 Net increase (decrease) in cash & cash equivalents (3,046) Cash & cash equivalents at beginning of period 27,792 Cash & cash equivalents at end of period 24,746$

CONSOLIDATED STATEMENT OF CASH FLOWSTHE BOSTON BEER COMPANY, INC.

Boston Beer uses the indirect

method.

Boston Beer uses the indirect

method.

The indirect method is used by 98.3% of

companies.

The indirect method is used by 98.3% of

companies.

This ending cash balance should agree with the balance sheet.

This ending cash balance should agree with the balance sheet.

13-16

Reporting Cash Flows from Operating Activities—Indirect Method

Net Income

Net Income

Cash Flows from Operating

Activities -Indirect Method

Cash Flows from Operating

Activities -Indirect Method

+/- Changes in current assets and current

liabilities.

+/- Changes in current assets and current

liabilities.

+ Losses and - Gains

+ Losses and - Gains

+ Noncash expenses such as depreciation and

amortization.

+ Noncash expenses such as depreciation and

amortization.

The indirect method adjusts net income by eliminating noncash items.

The indirect method adjusts net income by eliminating noncash items.

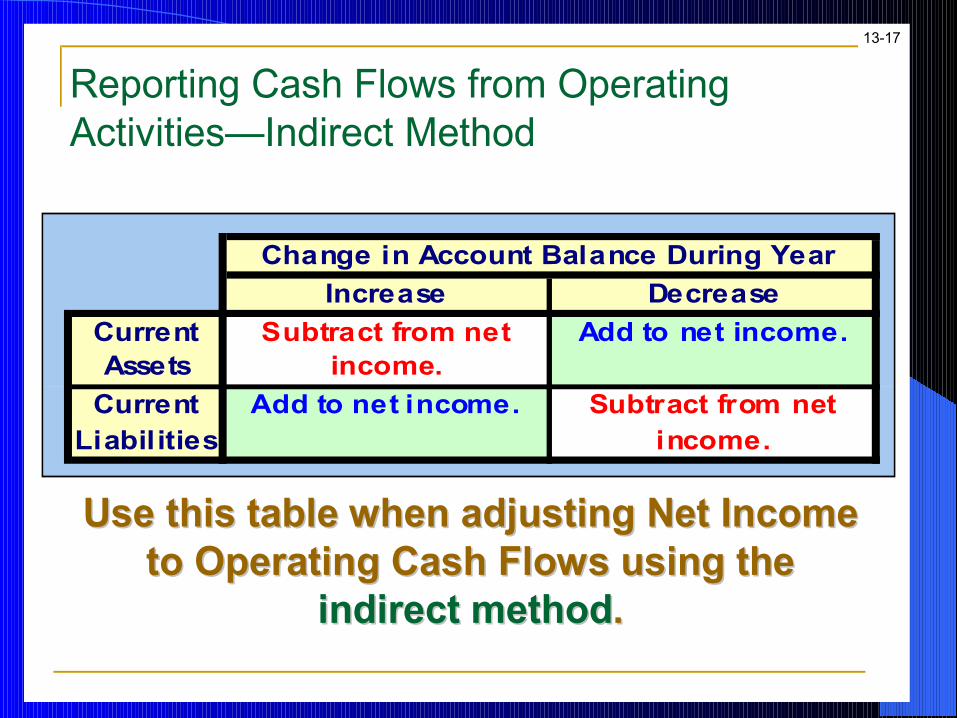

13-17

Use this table when adjusting Net Income Use this table when adjusting Net Income to Operating Cash Flows using the to Operating Cash Flows using the

indirect methodindirect method..

Change in Account Balance During Year

Increase Decrease

Current Subtract from net Add to net income.Assets income.

Current Add to net income. Subtract from netLiabilities income.

Reporting Cash Flows from Operating Activities—Indirect Method

13-18

Reporting Cash Flows from Operating Activities—Indirect Method

Use the following financial statements for

The Boston Beer Company and prepare the Statement of Cash Flows for the quarter ended on March 27,

2004.

Use the following financial statements for

The Boston Beer Company and prepare the Statement of Cash Flows for the quarter ended on March 27,

2004.

13-19

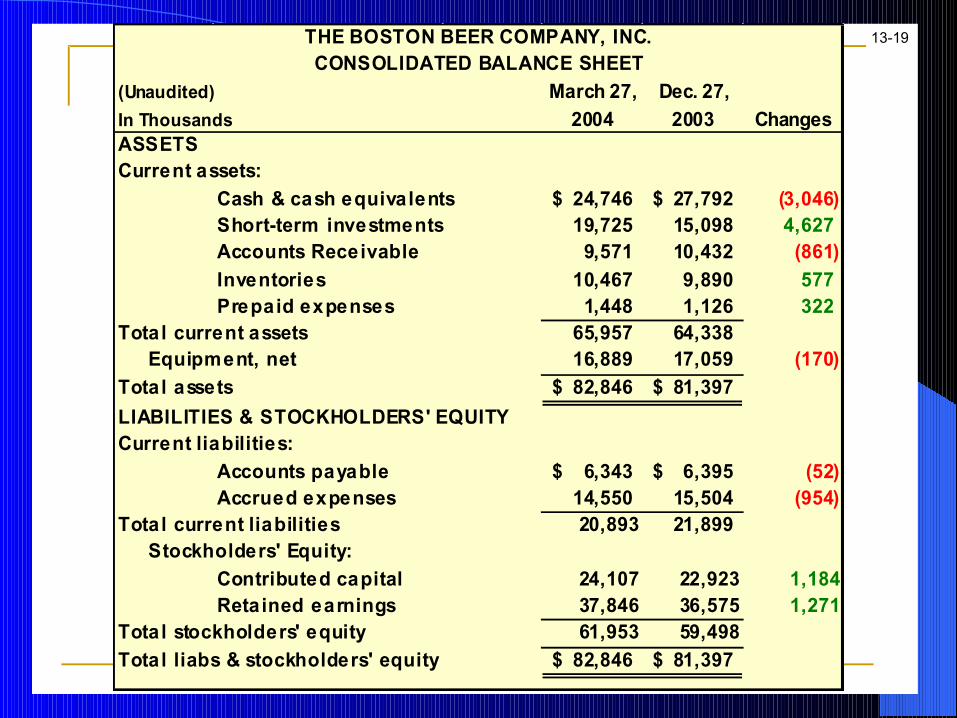

(Unaudited) March 27, Dec. 27,

In Thousands 2004 2003 ChangesASSETSCurrent assets:

Cash & cash equivalents 24,746$ 27,792$ (3,046) Short-term investments 19,725 15,098 4,627 Accounts Receivable 9,571 10,432 (861)

Inventories 10,467 9,890 577 Prepaid expenses 1,448 1,126 322

Total current assets 65,957 64,338 Equipment, net 16,889 17,059 (170)

Total assets 82,846$ 81,397$

LIABILITIES & STOCKHOLDERS' EQUITYCurrent liabilities:

Accounts payable 6,343$ 6,395$ (52)Accrued expenses 14,550 15,504 (954)

Total current liabilities 20,893 21,899 Stockholders' Equity:

Contributed capital 24,107 22,923 1,184Retained earnings 37,846 36,575 1,271

Total stockholders' equity 61,953 59,498

Total liabs & stockholders' equity 82,846$ 81,397$

THE BOSTON BEER COMPANY, INC.CONSOLIDATED BALANCE SHEET

13-20

(Unaudited) Three months endedIn Thousands March 27, 2004 Net sales 44,655$

Cost of sales 18,073 Gross profit 26,582Operating expenses:Selling, general and administrative 22,188

Depreciation and amortization 2,543 Total operating expenses 24,731Operating income 1,851

Interest income 192Income before provision for income taxes 2,043Provision for income taxes 772Net income $1,271

THE BOSTON BEER COMPANY, INC.CONSOLIDATED STATEMENT OF INCOME

The Statement of Cash Flows will begin with Boston Beer’s Net income from the

Income Statement.

The Statement of Cash Flows will begin with Boston Beer’s Net income from the

Income Statement.

13-21

(Unaudited) Three months endedIn thousands March 27, 2004Cash flows from operating activities: Net income 1,271$ Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 2,543 Changes in assets and liabilities: Accounts receivable decrease 861

Inventory increase (577)Prepaid expense increase (322)Accounts payable decrease (52)Accrued expenses decrease (954)

Net cash provided by operating activities 2,770$

CONSOLIDATED STATEMENT OF CASH FLOWSTHE BOSTON BEER COMPANY, INC.

Step 1Adjust net income for

depreciation and amortization expense.

Step 1Adjust net income for

depreciation and amortization expense.

13-22

(Unaudited) Three months endedIn thousands March 27, 2004Cash flows from operating activities: Net income 1,271$ Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 2,543 Changes in assets and liabilities: Accounts receivable decrease 861

Inventory increase (577)Prepaid expense increase (322)Accounts payable decrease (52)Accrued expenses decrease (954)

Net cash provided by operating activities 2,770$

CONSOLIDATED STATEMENT OF CASH FLOWSTHE BOSTON BEER COMPANY, INC.

(Remember, we showed the comparative balance sheets a few slides earlier.)

Step 2Adjust net income for changes in current assets and current

liabilities.

Step 2Adjust net income for changes in current assets and current

liabilities.

The Indirect Approach :The Indirect Approach :(Operating Activities Section)(Operating Activities Section)

13-23

(Unaudited) Three months endedIn thousands March 27, 2004Cash flows from operating activities: Net income 1,271$ Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 2,543 Changes in assets and liabilities: Accounts receivable decrease 861

Inventory increase (577)Prepaid expense increase (322)Accounts payable decrease (52)Accrued expenses decrease (954)

Net cash provided by operating activities 2,770$

CONSOLIDATED STATEMENT OF CASH FLOWSTHE BOSTON BEER COMPANY, INC.

Change in Account Balance During Year

Increase Decrease

Current Subtract from net Add to net income.Assets income.

Current Add to net income. Subtract from netLiabilities income.

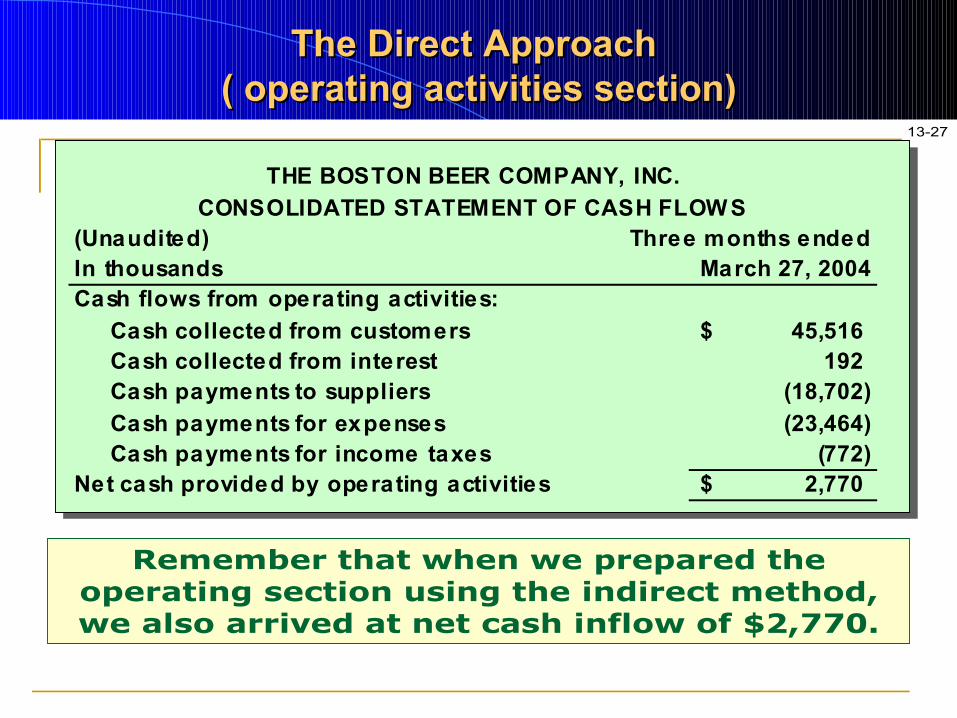

The Direct Approach The Direct Approach ( operating activities section)( operating activities section)

13-27

(Unaudited) Three months endedIn thousands March 27, 2004Cash flows from operating activities:

Cash collected from customers 45,516$ Cash collected from interest 192 Cash payments to suppliers (18,702)

Cash payments for expenses (23,464) Cash payments for income taxes (772)Net cash provided by operating activities 2,770$

CONSOLIDATED STATEMENT OF CASH FLOW S

THE BOSTON BEER COMPANY, INC.

Remember that when we prepared the operating section using the indirect method, we also arrived at net cash inflow of $2,770.

13-9

Cash Flows from

Investing Activities

Cash Flows from

Investing Activities

+

Cash Flows from Investing Activities

InflowsCash received from: Sale or disposal of property,

plant and equipment Sale or maturity of investments

in securities

InflowsCash received from: Sale or disposal of property,

plant and equipment Sale or maturity of investments

in securities

_Outflows

Cash paid for: Purchase of property, plant and

equipment Purchase of investments in

securities

OutflowsCash paid for: Purchase of property, plant and

equipment Purchase of investments in

securities

13-10

Cash Flows from

Financing Activities

Cash Flows from

Financing Activities

+

_

Cash Flows from Financing Activities

InflowsCash received from: Borrowings on notes,

mortgages, bonds, etc. from creditors

Issuing stock to owners

InflowsCash received from: Borrowings on notes,

mortgages, bonds, etc. from creditors

Issuing stock to owners

OutflowsCash paid for: Repayment of principal to

creditors (excluding interest, which is an operating activity)

Repurchasing stock from owners

Dividends to owners

OutflowsCash paid for: Repayment of principal to

creditors (excluding interest, which is an operating activity)

Repurchasing stock from owners

Dividends to owners

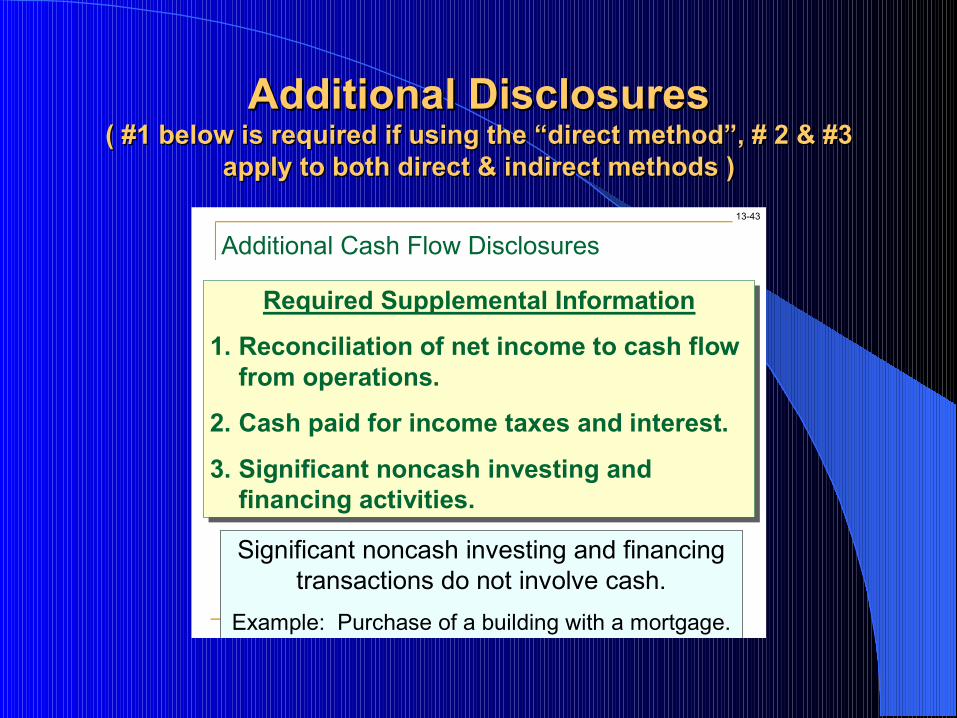

Additional DisclosuresAdditional Disclosures( #1 below is required if using the “direct method”, # 2 & #3 ( #1 below is required if using the “direct method”, # 2 & #3

apply to both direct & indirect methods )apply to both direct & indirect methods )

13-43

Required Supplemental Information

1. Reconciliation of net income to cash flow from operations.

2. Cash paid for income taxes and interest.

3. Significant noncash investing and financing activities.

Required Supplemental Information

1. Reconciliation of net income to cash flow from operations.

2. Cash paid for income taxes and interest.

3. Significant noncash investing and financing activities.

Additional Cash Flow Disclosures

Significant noncash investing and financing transactions do not involve cash.

Example: Purchase of a building with a mortgage.

Free Cash FlowFree Cash Flow13-37

In general, this measures a firm’s ability to pursue long-term investment

opportunities.

Free Cash Flow

Cash Flow from Operating Activities Cash Flow from Operating Activities –– Dividends Dividends ––Capital ExpendituresCapital Expenditures

Quality of Income ratioQuality of Income ratio13-30

Quality of Income Ratio

In general, this ratio measures the portion of income that was generated in cash. All other things equal, a higher quality of

income ratio indicates greater ability to finance operating and other cash needs from

operating cash inflows.

Cash Flow from Operating ActivitiesNet Income

Quality of Income Ratio

=

Capital Acquisition RatioCapital Acquisition Ratio13-36

In general, this ratio reflects the portion of purchases of property, plant and equipment financed from operating

activities. A high ratio indicates less need for outside financing for current

and future expansions.

Capital Acquisition Ratio

Cash Flow from Operating ActivitiesCash Paid for Property, Plant,

and Equipment

Capital Acquisition

Ratio=

End of Chapter MC AnswersEnd of Chapter MC Answers

1. b) 2. d) 3. d) 4. a) 5. a) 6. b) 7. d) 8. a) 9. d) 10. c)

Homework Manager AssignmentHomework Manager Assignment

E13-3 E13-7 E13-14 E13-15 E13-17