liability insurers as corporate monitors · international rel’iera qf law und economics (19901,...

TRANSCRIPT

International Rel’iera qf Law und Economics (19901, 10(115-129)

LIABILITY INSURERS AS CORPORATE MONITORS

CLIFFORD G. HOLDERNESS

Wallace E. Carroll School of Management, Boston College, Chestnut Hill, MA, 02167-3808, USA

1. INTRODUCTION

Corporate directors and officers are being personally sued with increasing fre- quency for a broad array of alleged offenses, ranging from breach of the common- law duty of loyalty to shareholders, to violations of federal securities laws, to “looting” the corporate treasury, to violations of federal security laws, to even the “failure to exercise reasonable care in the selection of a depository bank.“’ According to one report, such suits increased fourfold from 1984 to 1985 alone.2 Although this rate of increase has apparently moderated, the liability of corporate officials remains controversial.3

Most public corporations have responded by purchasing directors’ and officers’ liability insurance (“liability insurance”), which covers the expenses of individual directors and officers as well as the corporation’s expenses incurred under in- demnification agreements. Proponents of liability insurance point out that it re- duces the cost of compensating risk-averse directors and officers and encourages

I have benefited from the comments of James Brickley, Jeffrey Coles, Frank Easterbrook, Victor Goldberg, Michael Jensen, Fred McChesney, Roberta Romano, Dennis Sheehan, Clifford Smith, Jerold Zimmerman, and two anonymous referees. This research has been supported by the Managerial Economics Research Center at the University of Rochester, N.Y.

’ Wull Street Journal, July 22, 1976, p. I.

‘Romano, “What Went Wrong With Directors’ and Officers’ Liability Insurance,” Uni- versity ofCincinnuti La~l Review 69 (1988). The one systematic survey in this area reports that payments (excluding legal fees) under liability insurance policies increased from an average of $340,018 in 1980 to $880,800 in 1984. Wyatt Survey, 1985 Wyatt Directors’ and Officers’ Liubility Insurunce. Moreover, between 1974 and 1984, the percentage of surveyed firms with suits filed against their directors increased from 7% to 18%. Id.

‘Because over the past decade few statutes were passed or Supreme Court decisions handed down expanding directors’ liability, some have argued that the increased exposure reflects a willingness of courts to hold directors liable for actions that were previously protected by the business judgment rule. See Romano, supru note 2. The most widely reported case of director liability is Slflit/l v. Van Gorkom, in which the Delaware Supreme Court pierced the business judgment rule and imposed liability in excess of $20 million on the outside directors of Trans Union Corporation because they accepted a merger at a price the court deemed to be less than the “intrinsic value” of the firm. Smith v. Vun Gorkom, 488 A.2d 858 (Del. 1985). The case was eventually settled out of court for $23.5 million. Business Week, March 18. 1985, p. 56.

0 1990 Butterworth-Heinemann

116 Liubility insurers as corporute monitors

them to take appropriate business risks. 4 Critics, on the other hand, argue that liability insurance largely nullifies the disciplining potential of litigation, causing directors and officers to be less attentive to their duties to shareholders. As a result, there are calls for limitations on liability insurance, either voluntarily or through legislation.’

This debate has centered almost exclusively on the risk-shifting function and moral hazards of liability insurance. Another important effect of such insurance- its role in monitoring the board of directors and top managerial teams-has gone unrecognized. Insurance companies monitor their customers’ directors and top managers in a number of ways. When it decides whether to issue a policy, the insurer investigates the firm’s past actions, occasionally requires changes in the board, and sets conditions for directors and officers to observe. When allegations of misconduct arise, the insurer through its defense efforts can serve as an in- dependent external investigator of not only the accused official but the entire board and top managerial team. Liability insurance also promotes internal mon- itoring by making it easier to recruit outside directors whose relative independence of management is likely to make them more effective representatives of share- holders. Although these monitoring services may not have originated as such and may be provided jointly with the risk-shifting and litigation functions of the in- surance, they provide distinct benefits for some firms which help explain the prevalence of liability insurance. These monitoring benefits are the focus of this paper.

Section 2 provides an overview of indemnification and liability insurance. Sec- tion 3 discusses how insurance companies monitor the directors and officers of client firms. Section 4 tests the hypothesis that liability insurance provides external monitoring of the board and top managerial team and shows that some major empirical regularities that are consistent with the hypothesis would be difficult to understand if the insurance only shifted risks. Concluding observations are offered in section 5.

2. AN OVERVIEW OF INDEMNIFICATION AND LIABILITY INSURANCE

Directors and officers in most corporations are reimbursed for business-related legal fees and judgments.6 Indeed, most states require that corporations reimburse

‘Many directors claim that liability insurance is imperative. As Walter Wriston, former chief executive of Citicorp and director of nine companies, remarked, “I don’t know of anybody who would join a board without [liability] insurance.” Wull Street Jownml, July 10, 1985, p. 1. See also Lester Korn, “Directors are Getting Harder to Find,” Fortune, April 29. 1985.

5See, for example, Farrell, “If Directors Are Doing Their Job, They Don’t Need Insur- ance,” Business Week, September 8, 1986.

6The Conference Board reports that 99% of the firms it surveyed indemnified directors and officers, with 94% accomplishing this through bylaws or articles of incorporation, 4% relying on state laws that mandate indemnification, and 1% using “informal understandings.” Conference Board, Corporate Directorship Pructices: Compensation 68-69 (1977). See also J. Bishop, The Law of Corporute QfjTcers and Directors, Ch. 6 (1981).

CLIFFORD G. HOLDERNESS 117

their officials for losses in lawsuits in which the officials are vindicated.’ Firms typically supplement this protection through indemnification agreements in their bylaws or articles of incorporation.

Many firms also purchase a group liability insurance policy, which typically has two parts. The first reimburses the corporation for any expenses and payments incurred under its indemnification obligations; the second reimburses individual directors and officers when they are not indemnified by the corporation. Both parts carry deductibles, which vary from $5,000 for individuals to more than $2 million for large corporations. The exclusions and conditions of liability insurance are similar to those for other types of insurance. For example, liability insurance does not cover obvious conflicts of interest, willful misconduct, or acts the accused should have known were illegal. Beyond the general dictates of insurance law, there are few legal constraints on the corporate purchase of liability insurance.x

Although indemnification and liabililty insurance often cover the same occur- rences, liability insurance provides broader coverage in some instances. In par- ticular, insurance has somewhat broader coverage for suits by, or in the right of, the corporation, including derivative suits.’ The statutory requirement that the

‘Every state has a statute permitting indemnification that falls into one of two categories: statutues (notably Delaware’s) that allow broad indemnification, and those (notably Cali- fornia’s) that restrict certain aspects of indemnification. although the right to indemnify remains broad. These statutes were apparently a response to the uncertainty under the common law of the grounds for indemnification. See, e.g., NW. York Dock Co. v. Mc- Collom, 173 Misc. 106, I6 N.Y.S. 2d 844 (1939) (court invalidated indemnification payment to directors who had successfully defended themselves in a derivative suit because there was insufficient evidence that the corporation had benefited from the directors’ successful defense).

XSee Osterle, “Limits on a Corporation’s Protection of Its Directors and Officers from Personal Liability,” Wisconsin La~3 Reviewer 513, 549-55. A notable exception is New York’s requirement that shareholders be notified when a firm purchases liability insurance.

‘See e.g., Loomis, “Naked Came the Insurance Buyer,” Fortune, June IO, 1984, p. 72. This difference in coverage, however, is often not that great. First, many states allow firms to supplement the protections of indemnification and insurance with employment contracts. In addition, several states, notably Delaware, have statutes that explicitly allow firms to broaden their indemnification. “The indemnification provided by this section shall not be deemed exclusive of any other rights to which those indemnified may be entitled under any by-law, agreement. vote of stockholders or disinterested directors or otherwise .” Del. Code Ann. Tit. $8, 145(f). Although there is little case law interpreting this nonex- clusivity provision, it appears that firms can broaden their indemnification significantly, perhaps to include indemnification for directors adjudged liable to the firm itself. The National Steel Corporation, a Delaware corporation, for example. specifically extends indemnification “to judgments in favor of the Corporation or amounts paid in settlement to the Corporation.” Quoted in Bishop, supra note 6, App. 58. In a case decided under a now repealed Delaware statute that contained a nonexclusivity clause similar to the current provision, the Third Circuit suggested that a corporation could expand indemnification to cover costs incurred in defending a derivative suit regardless of whether such indemnifi- cation would be permissible under other provisions of the indemnification statute. Mooney v. Willys-Overland Motors, Inc., 204 F.2d 888 (3d Cir. 1953). More recently. the Delaware Supreme Court reaffirmed the right of corporations to expand their indemnification. Hihhrrt v. Holl~~wod Park, Inc., 457 A.2d 339, 344 (Del. 1983) (“The corporation can also grant indemmfication beyond those provided by the statute.“) Other states likewise permit liberal indemnification in suits by, or in the right of, the corporation. Montana, for instance, allows a corporation to indemnify directors and officers “in connection with the defense. com- promise or settlement of any action, suit. or proceeding. .” Mont. R~I’. Codes Ann. #35- l-108 (15). Even in states having restrictive indemnification statutues. firms are usually

118 Liability insurers us corporute monitors

board approve all indemnification payments leads to further differences in the effective coverage of indemnification and liability insurance. When the entire board is sued, there are no untainted directors to vote on indemnification; when several directors are sued, it may be impossible to raise a quorum to vote on indemnification.“’ Finally, when the value of a firm’s equity is small, the avail- ability of funds for indemnification is uncertain. If bankruptcy occurs, additional uncertainty arises over a trustee in bankruptcy, often a stranger to the board, who must decide whether circumstances warrant or funds allow for indemnifi- cation.” In all of these situations, even if a firm indemnifies its directors and officers, liability insurance shifts risks and thus reduces the cost to the firm of compensating risk-averse directors and officers.”

3. MONITORING OF THE BOARD AND TOP MANAGERIAL TEAM WITH LIABILITY INSURANCE

Monitoring services provided by the insurance convey distinct benefits to both the insurer and the client company’s shareholders. They reduce the insurer’s exposure, and they encourage directors and officers to act in the shareholders’ interests. Moreover, these services, which supplement other monitoring efforts, will be provided even if insurance shifts no risk beyond what is shifted by indem- nification, because the policies reimburse companies for their indemnification payments.

3.1 Monitoring by the insurance company before a policy is issued

The insurance company’s monitoring begins even before it issues a policy, when it investigates a potential client company for factors that are likely to increase its exposure, such as a dominant chief executive officer, unattentive directors, or the absence of an audit subcommittee composed of outside directors.” Further- more, liability applications require that a firm supply detailed information to be used in establishing premiums. For example, CNA Insurance Company requires that an applicant supply information on its dividend policy and acquisition plans

required to indemnify directors when they have been successful in suits brought on behalf of the corporation. In addition, under most of these statutes, firms can under certain circumstances indemnify directors who have been held liable to the firm. California is probably the most important state having a restrictive indemnification statute. Under Cal- ifornia’s statute a court has the power to permit indemnification of a director or officer who has been adjudged liable to the corporation. Cal. Corp. Code $317(c). “‘Such suits are common because the board typically acts as a unit. Indeed. directors are often precluded by law from acting individually or even in a group apart from the rest of the board. See H. Henn & J. Alexander, Hnndbook of the Luw ofCorporutions und Other Business Enterprises 208. “Indeed, trustees occasionally bring lawsuits against directors, alleging that their mis- management contributed to the firm’s financial difficulties. ‘*When individuals are risk-averse, by definition the incremental salary they demand as compensation for possible litigation will exceed the expected costs of that litigation. Li- ability insurance shifts risks from individual directors and officers to shareholders of the insurance company, who will charge a lower price for risk-bearing because they own divisible claims and can therefore diversify the risks through the capital markets. See Arrow, “The Role of Securities in the Optimal Allocation of Risk-Bearing,” 31 Review of Economic Studies 91 (1964). 13See Prncticing Luw Institute, Directors’ und Ojficers’ Liability 1986, at 640-55; Daenzler, “Why Directors and Officers Buy D&O Insurance,” The Weekly Undetw~riter, Feb. 17, 1968, Cover Note; Oesterle, supru note 8. at 256.

CLIFFORDG. HOLDERNESS 119

and the stock ownership of its board. I4 Sometimes the issuance of a policy is predicated on the company’s implementing specific organizational changes, in particular the addition of outside directors or the establishment of an audit sub- committee. In other instances, a policy is not issued or premiums are increased unless the firm alters specific practices to reduce the insurer’s exposure.

3.2 Monitoring through policy coverage and conditions

Once a policy is issued, monitoring occurs through the coverage and conditions of the policy. For example, several years ago the standard liability policy was changed to exclude claims arising from resistance to takeoversls and from targeted share repurchases (“greenmail”).‘h This change caused “some takeover special- ists [to] say that a lack of insurance coverage could, among other things, make corporate directors and officers more responsive to shareholders’ interests when responding to takeover bids.“r7 Interestingly, academic studies suggest that firm value typically declines with managerial resistance to takeover attempts and with the payment of greenmail. I8 Because insurance polices can be modified only with the consent of the insurer (who bears the consequences if any change triggers liability), as opposed to indemnifications which often can be changed unilaterally by the board, liability insurance reduces the board’s ability to increase its pro- tection opportunistically.

Liability insurance also facilitates internal monitoring. The standard liability policy augments directors’ incentives to monitor each other, because the failure of one of them to reveal material facts when applying for insurance can result in loss of coverage for all directors. I9 Liability insurance is also viewed as instru- mental in recruiting outside directors. 2o This is relevant for monitoring purposes because outside directors “act as arbiters in disagreements among internal man- agers and carry out tasks involving agency problems between internal managers and residual claimants.“2’ In addition, without the protection of insurance there are likely to be fewer wealthy outside directors. Such a self-selection would occur

14Pructicing Law Institute, sicpra note 13, at 479-81.

“See Wall Street Journal, January 13, 1987; January 20, 1986. Other insurers, such as Chubb, do not exclude coverage for takeover attempts but consider the possibility of a hostile takeover before deciding to issue a policy. Id. lhSee Forbes, “Greenmail-The Backlash,” December 2, 1985.

” Wull Street Journal, January 20, 1986. “See Dann and DeAngelo, ‘Corporate Financial Policy and Corporate Control, A Study of Defensive Adjustments in Assets and Ownership Structure,” 20 Journal of Finuncial Economics 87 (1988) for evidence on firm value and managerial resistance to takeover attempts. See Mikkelson and Ruback, “An Empirical Analysis of the lnterfirm Equity Investment Process,” 14 Journal of Financial Economics 523 (1985) for evidence on stock- price reactions to targeted repurchases.

“In Shapiro v. American Home Assur. Co., 584 F.Supp. 1245 (D. Mass. 1984), Judge Keeton held that a material misrepresentation by one director in an application for liability insurance voided coverage for all directors, even those who made no misrepresentations or had no knowledge of the misrepresentation.

“‘Some have attributed the decline in the incidence of outside directors in part to the threat of increased personal liability. See, for example. Business Week, September 8, 1986, pp. 56-61; Wull Street Journal, June 2, 1986, p. 19.

‘I Fama & Jensen, “Separation of Ownership and Control,” 26 Journal of Law & Economics 301, 313-15 (1983). The available empirical evidence is consistent with a monitoring role for outside directors. See Weisbach, “Outside Directors and CEO Turnover,” 20 Journul of Financiul Economics 43 I (1988).

120 Liability insurers as corporate monitors

if directors were held liable because poorer individuals would find personal bank- ruptcy a more attractive option than would wealthier individuals. This would further weaken internal monitoring, because some monitoring skills are likely to be correlated with financial wealth. For instance, those who have been successful in business may be skillful in selecting and monitoring top management.22

Finally, denial or loss of liability coverage can convey valuable information to directors, shareholders, and the capital markets, which in turn can trigger other, complementary control devices. This apparently was what happened when Control Data Corporation lost its liability insurance and two outside directors resigned; shortly thereafter the chief executive also resigned, reportedly because he lacked board support. The new chief executive then began restructuring the corporation.*’ Although it would be an overstatement to attribute these events solely to the loss of liability coverage, that apparently had an influence.

3.3 Monitoring by the insurance company during litigation

Directors and officers are sometimes monitored through legal actions brought against them personally. 24 Most such actions are brought by shareholders in de- rivative suits through which they seek remedies for violations of the directors’ and officers’ fiduciary duty to the firm, including the expropriation of corporate assets, clear and undisclosed conficts of interest, and gross mismangement.25 Suits are also brought for other purposes by third parties, including government agencies or suppliers, but nonetheless reveal information about directors and officers that is valuable to shareholders.

The probability of litigation against directors and officers appears to be partly a function of their corporate decisions. The Wyatt Survey reports that the prob- ability of suit increases with a vigorous acquisition policy, resistance to takeover attempts, the number of subsidiaries “and the degree of their control by the parent,” equity issues, dividend decreases, and the profitability of the corpora- tion.2h These events often affect stock prices significantly and are therefore among the management decisions that shareholders want monitored.

Two conditions, however, are necessary for monitoring to be effective when suit is brought against directors and officers. First, the allegations must be in- vestigated to ascertain whether they are true. Second, those findings must be conveyed to individuals who can take the appropriate remedial action. Analyzed below are several non-mutually exclusive options a firm has to satisfy these two conditions. A key finding is that the insurance company’s litigation services can be instrumental in satisfying the conditions for effective monitoring.

Judicial Investigation: One reason litigation, particularly derivative litigation, is brought is to have an independent third party investigate the accused director. But it is not inevitable that the judge hearing the case will conduct an investigation

“This is a role traditionally played by outside directors. See Richard Vancil, Passing the Baton: Managing the Process of CEO Succession, Harvard Business School Press, Cam- bridge, MA, (1987).

*‘Fortune, January 20, 1986, p. Il. Fortune, February 3, 1986, p. I I. ?“For a discussion of the monitoring role of litigation, see, for example, Levmore, “Mon- itors and Free Riders in Commercial and Corporate Settings,” 92 Yale Law Journal 49, 64-65 ( 1982).

*SThe 1979 Wyatt Survey reports that 40% of the claims against directors and officers are brought by stockholders. Wyatt Company, The 1979 Directors und Officers Liability and Fiduciary Liability Survey, 6 (1979).

‘hWyatt Survey, supra note 25, at 47-48.

CLIFFORD G. HOLDERNESS 121

that shareholders value. Most prominently, the judge will not consider the evi- dence if, as is typical, the case is settled before trial.” When he does consider the evidence, he may issue an erroneous interpretation or fail to discuss infor- mation relevant to stockholders (perhaps by deciding the case on narrow grounds)? Finally, even when he does issue an accurate and relevant opinion, he may not do so until years after the complaint is filed. If the accusations are true, this can delay remedial action. If the accusations are false, their mere existence can reduce the effectiveness of the accused and perhaps the entire board.

internal Investigation: A judicial investigation may be supplemented by an internal investigation conducted by the board. Indeed, this is virtually a foregone conclusion with indemnification, because by law the board must approve all in- demnification payments. Internal investigations, however, can lack independence because legally as well as in practice the board acts as a team. In fact, when the entire board is sued-which is not uncommon because of its collective decision- making process-an independent internal investigation is not feasible. Even if the entire board is not sued, a main responsibility of directors is to monitor each other. Consequently, if allegations against some directors are true, the other directors may also have failed in their obligations to shareholders. In addition, under some circumstances nondefendant directors are jointly liable for judgments against fellow directors. Other, even more obvious, conflicts of interest arise when one director sues the rest of the board.

Special Counsel Investigation: One way to augment the independence of in- ternal investigations is for a subcommittee of directors who are not tainted by the allegations to appoint a special outside counsel who has high standing in the community and no previous contact with the firm (often a retired judge or prom- inent attorney) to investigate the charges. This option is unavailable, of course, when the entire board is sued. Although the special counsel’s reputation and lack of previous contact can provide independence that may be wanting in board investigations, some limitations remain. Because the special counsel is customarily chosen after the allegations have been raised, the unaccused directors, especially if they fear they could ultimately be implicated, may choose a sympathetic person or one who is unlikely to investigate the allegations vigorously.2’ Moreover, a special counsel, like a judge, bears few of the wealth effects of his investigation, which reduces his incentives to investigate the accusations thoroughly.

Insurance Company Investigation: Irrespective of any investigations by a judge, the board, or a special counsel, the insurance company is likely to investigate allegations against a director or an officer, if for no other reason than to ascertain whether the policy is triggered. Liability policies typically exclude claims involving dishonesty or obvious illegality, but these are among the transgressions share- holders will most want independently investigated. Before this exclusion can be invoked, however, the insurance company’s “own investigation of the relevant facts pertaining to a claim [must] afford reasonable grounds . . . that such an

‘7Most suits against directors are settled before judgment. See Jones, “An Empirical Examination of the Resolution of Shareholder Derivative and Class Action Lawsuits,” 60 Boston University Law Review 547 (1980); Conard, “A Behavioral Analysis of Directors’ Liability for Negligence,” Duke Law Journal 895, 900-01 (1972).

‘XMoreover, the judge could have a recognized bias that might induce “forum shopping.” 2yThis is a frequent criticism of the increasing use of outside counsel to investigate alleged corporate wrongdoings. See, for example, Laurie Cohen, “Firms Faulted for ‘Independent’ Inquiries,” Wall Street Journal, June 140, 1989. p. Bl.

122 Liability insurers as corporate monitors

exclusion . . . does apply.“30 Moreover, because such exclusions are “subject to reversal by a judgment or other final determination in a legal proceeding,“” the insurer will often investigate the accused, explain to the client firm why its cov- erage is tentative, and continue to participate in the defense.32 Thus by purchasing liability insurance, a firm receives from the insurer potential investigations of its directors and officers for a wide array of offenses, including breach of fiduciary obligations and illegal acts.

When the allegations advance to litigation, legal counsel for the accused director or officer must be retained. In policies containing a “duty to defend,“‘j this choice is made directly by the insurance company, and the opportunity arises to have the defense contribute to the monitoring. There are (as noted by a corporate attorney) advantages in combining these efforts:

An undertaking to complete and publish a factual report of the extent of alleged misconduct [of the accused director], although expensive and time consuming and onerous in some instances, is nothing more than the finalization in a formal way of the work that a lawyer would do to assess what it is that he is faced with in the litigation. If someone is going to conduct an investigation, it is probably better for counsel employed by the corporation, with its own perspective to do it, especially as this offers some hope of protecting the work product and the information developed and utilizing it affirmatively rather than negatively.j4

Several factors suggest a fiduciary relationship that would provide the firm with access to at least some investigations by the insurance company’s attorney. Firms typically purchase a group policy to cover all directors. This was a key factor in Judge Keeton’s decision in Shapiro v. American Home Assurance Company that the liability policy in question was properly construed as a single contract, not as a series of separate contracts between the insurer and each director.js Although the issue of a fiduciary relation was not raised in Shapiro and evidently has not yet been litigated, the concept of a single contract negotiated and purchased by the corporation is consistent with such a relationship between the corporation and the insurer’s attorney. Two revisions to the standard liability policy further support this relationship. Policies now stipulate that the firm is an insured, and

“‘See Lydando No. 1, Directors and Ofjcers Liability Insurance and Reimbursement ,for Directors’ and Of$cers’ Liability Insurance, Clause 4(C). [Following convention in this area, when discussing the specifics of liability insurance policies, this paper will reference the standard Lloyd’s directors’ and officers’ liability policy, “Lydando No. 1.” This policy is similar to policies issued by other insurance companies. A specimen copy of Lydando No. 1 can be found in Bishop supra note 6, Appendix C; Hinsey, “The New Lloyd’s Policy Form for Directors and Officers Liability Insurance-An Analysis,” 33 BUS. Lutz,. 1961 (1978); Practicing Law Institute, Liability yfcorporate OJficers and Directors 287-98 (1980) (this source contains specimen copies of liability policies from other insurance companies as well).]

“Id.

‘?See Hinsey. supru note 30, at 1970-71.

“The other type of policy is a “defense expense, ” in which the insurance company reim- burses the accused’s expenses. See Practicing Law Institute, supru note 13 at 620.

“Klein. “Conduct of Directors When Litigation Is Commenced Against Management,” 31 Business Law 1355, 1361 (1976).

=584 F.Supp. 1253.

CLIFF~RDG. HOLDERNESS 123

that “investigative expenses” will be reimbursed. 36 It is thus understandable that “some insurers believe that the corporation is really the only party at risk.“37

Those implicated by damaging information revealed by an investigation often attempt to suppress it. If they succeed, the probability that the problem will be remedied decreases, and deterrence of future malfeasance is weakened. Several factors reduce the probability that an insurance company will suppress infor- mation, whether obtained during the application process, when coverage for a given claim is being reviewed, or during trial preparation. Unlike a special counsel, an insurance company is chosen before allegations have been made. Unlike in- ternal investigators, an insurance company is independent of the client firm and its directors. Moreover, an insurance company will typically bear more of the wealth effects of its monitoring efforts than will a judge or special counsel. When there are quasi-specific rents with specific clients, an insurance company is hurt financially when its suppression of information is revealed to the market, because some clients are likely to switch to insurers that show more independence.3x In light of its perpetual existence, an insurance company’s suppression of information will affect its cash flows over an infinite horizon. All of these factors benefit stockholders of client firms by adding independence to the monitoring of their boards and top managerial teams.

Any firm, whether it carries liability insurance or relies on indemnification, can use the options described above to monitor its board and top managers. Further, none of the options or combinations thereof is likely to yield the largest benefits for all firms. Nevertheless, an insurance company, because of its experience with corporate litigation, its investigation of the firm before issuing a policy and when deciding whether a claim is covered, its independence and reputation, the pos- sibility of the firm’s gaining access to some of its defense attorney’s findings, and the wealth effects it bears, can be a valuable monitor of corporate directors and officers.

4. TESTING THE MONITORING HYPOTHESIS

This section tests the hypothesis that liability insurance provides external mon- itoring of corporate boards and managers. A practical problem in testing this hypothesis is that liability insurance has several effects that are not inconsistent with monitoring. Accordingly, once it has been established that a given empirical regularity is consistent with monitoring, it is difficult to rule out all reasonable alternative explanations. Throughout this section, however, I do consider the most conspicuous alternative hypothesis, that liability insurance only shifts risks.

‘hLydando No. 1, supru note 30, Clause 6(d).

“Gawel. Jain, & Agnello, “Directors and Officers Indemnification Insurance: What Is Being Offered?” 39 Journal of the American Society of CLU 92 (1985).

“See DeAngelo, “Auditor Independence, ‘Low Balling,’ and Disclosure Regulation,” 3 Journal ofAccounting and Economics 113 (1981). This revelation could come in a number of ways: during a lawsuit; from companies switching insurance companies in a systematic way: from disgruntled employees of either the firm or the insurance company; from security analysts reviewing a particular company.

124 Liability insurers as corporate monitors

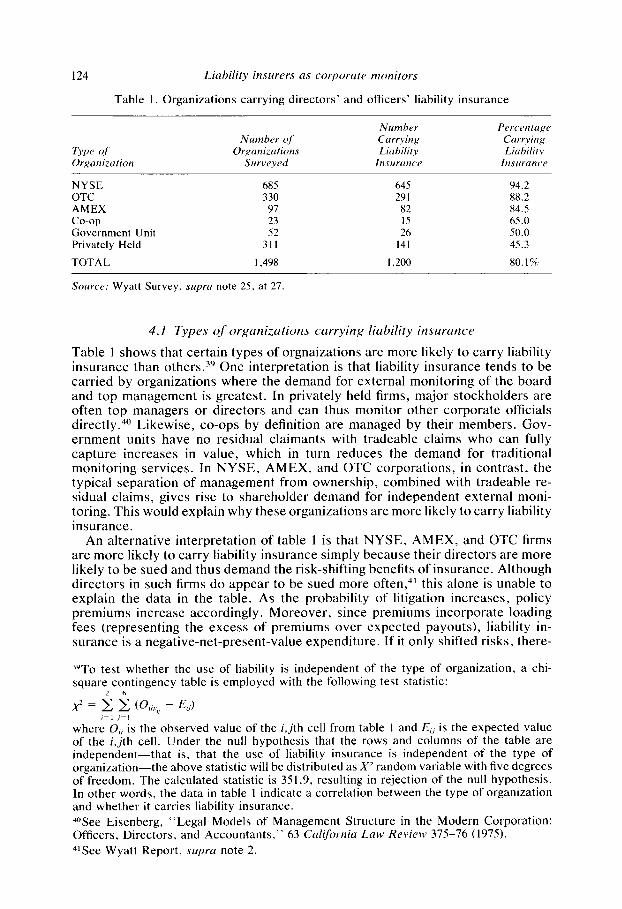

Table 1. Organizations carrying directors’ and officers’ liability insurance

Type of Organization

Number of Organizations

Surveyed

NYSE 685 645 94.2 OTC 330 291 88.2 AMEX 97 82 84.5 co-op 23 15 65.0 Government Unit 52 26 50.0 Privately Held 311 141 45.3

TOTAL 1,498 1,200 80.1%

Source: Wyatt Survey, supru note 25, at 27

4.1 Types of organizations carrying liability insurance

Table 1 shows that certain types of orgnaizations are more likely to carry liability insurance than others.3Y One interpretation is that liability insurance tends to be carried by organizations where the demand for external monitoring of the board and top management is greatest. In privately held firms, major stockholders are often top managers or directors and can thus monitor other corporate officials directly. 40 Likewise co-ops by definition are managed by their members. Gov- ernment units have’no residual claimants with tradeable claims who can fully capture increases in value, which in turn reduces the demand for traditional monitoring services. In NYSE, AMEX, and OTC corporations, in contrast, the typical separation of management from ownership, combined with tradeable re- sidual claims, gives rise to shareholder demand for independent external moni- toring. This would explain why these organizations are more likely to carry liability insurance.

An alternative interpretation of table 1 is that NYSE, AMEX, and OTC firms are more likely to carry liability insurance simply because their directors are more likely to be sued and thus demand the risk-shifting benefits of insurance. Although directors in such firms do appear to be sued more often,4’ this alone is unable to explain the data in the table. As the probability of litigation increases, policy premiums increase accordingly. Moreover, since premiums incorporate loading fees (representing the excess of premiums over expected payouts), liability in- surance is a negative-net-present-value expenditure. If it only shifted risks, there-

“To test whether the use of liability is independent of the type of organization, a chi- square contingency table is employed with the following test statistic:

Z h

X2 = C C CO,,,, - E(j)

where 0, is the observed value of the i,jth cell from table 1 and E,, is the expected value of the i,jth cell. Under the null hypothesis that the rows and columns of the table are independent--that is, that the use of liability insurance is independent of the type of organization--the above statistic will be distributed as X’ random variable with five degrees of freedom. The calculated statistic is 351.9, resulting in rejection of the null hypothesis. In other words, the data in table 1 indicate a correlation between the type of organization and whether it carries liability insurance.

4oSee Eisenberg, “Legal Models of Management Structure in the Modern Corporation: Officers, Directors, and Accountants,” 63 California Law Review 375-76 (1975).

41See Wyatt Report, supra note 2.

CLIFFORDG. HOLDERNESS 125

fore, NYSE-listed firms should be the least likely-not the most likely-to carry insurance, because many are large and incorporated in Delaware, which has a liberal indemnification statute. These firms are better able to shift risks with indemnification and thus avoid an insurer’s loading fees.4’

Additional evidence consistent with the monitoring proposition but inconsistent with the alternative risk-shifting hypothesis comes from the practices of liability insurers. All five of the nine insurance companies responding to my inquiries stated that they protect their directors and officers with policies purchased from other companies. Because these companies are large, indemnification should shift most of their risks of litigation. The value of specialized litigation services likewise fails to explain this regularity because the five companies presumably provide these services to clients and therefore possess the necessary skills. The one benefit the five insurance companies realize by purchasing liability insurance from other companies is independent external monitoring of their directors and officers.

4.2 Prevulence of group policies

Although 80% of publicly held corporations provide group liability policies for their directors, only 4% to 23% provide group policies for other types of insurance such as life and health.4’ Group insurance is normally explained by economies of scale in contracting or as a means to reduce adverse selection.44 Neither seems to explain the predominance of group over individual liability policies.45 The size of the typical board would not seem to offer the corporation substantial admin- istrative savings in contracting for a single policy. Moreover, such savings are unlikely to be greater for liability policies than for other types of insurance.

“‘Although some provisions of the tax code encourage corporations to purchase insurance [see Mayers & Smith, “On the Corporate Demand for Insurance,” Jo~lrnal oJ’Bu.sine.s.s 55, 289-91 (1982)], in general tax obligations will be invariant with how a director is protected from potential liability. Therefore, tax considerations do not explain the data in table I. Any increment in directors’ fees to compensate for expected litigation is, of course, deductible by the firm and taxable to the individual receiving it. The individual, in turn, can deduct litigation costs or damages (with the exception of fines, which are never de- ductible) that stem from corporate responsibilities. See Union Investment Company, CCH, Dec. 20, 134,21 TC 659 (1954), acq. 1954-2 CB 6: Mooney, The Indemnification Dilemma- Tax Problems in Protecting the Corporate Officer and Director from Liability, Tux 498 (August, 1972). Insurance premiums are deductible either by the firm (if it purchases the policy) or by individual directors (if they purchased the policy) on the grounds of being an ordinary business expense. See Rev. Rul. 69-491, 1969-2 CB 22: Note, “Liabililty Insurance for Corporate Executives,” 80 Harvurd LNM’ Review, 644-48, (1967). Finally, the firm can deduct attorneys’ fees and other indemnification payments, again on the grounds of their being an ordinary and necessary business expense. See Bishop, suprcr note 6, Ch. IO, 5, 9. The individual must report these payments as income but can simul- taneously deduct attorneys’ fees and damages. Mooney, sy.m at 504. Because the indem- nification payments will typically equal the defendant’s costs. the two will cancel and the director’s taxes will be unaffected.

“‘A 1983 survey of the compensation policies of more than 600 publicly held corporations found that 82% of manufacturing companies provide liability insurance for their directors. The equivalent figures for other types of insurance are: life 16%, accidental death and dismemberment 23%, medical 6%. and dental 4%. The figures are nonmanufacturing com- panies are: liability 81%, life 12%, accidental death and dismemberment 16% medical 7%, and dental 4%. Edwin S. Mauk & James A. Giardina. Organization & Compensation of Boards of Directors 33 (1984).

j4See, for example, Mayers and Smith suprcr note 42. at 284.

“‘See Wyatt Report, supra note 2.

126 Liuhility ins44rers as corporcrte monitors

Potentially more substantial savings could be realized when directors simulta- neously serve on a number of boards. To establish a premium in these cases, an insurer would have to investigate each company of which the applicant is a di- rector. If this were a major cause of the prevalence of group liability policies, one would expect to observe fewer group policies as the incidence of multiple direc- torships declines. Although there has been a decline in multiple directorships over the past ten years, there has not been a corresponding decline in the use of group policies.4”

Adverse selection, the other factor normally used to explain group insurance, is unlikely to be a greater problem with liability insurance than with, say, health insurance. Indeed, adverse selection is often cited as a reason why firms provide group health insurance. Yet firms provide group liability more often than they provide group health. Consider also life insurance, which primarily, if not exclu- sively, involves risk-shifting. Presumably directors choose to purchase life in- surance based on their individual preferences. If risk-shifting were the only effect of liability insurance, one would predict a pattern of individual versus group policies similar to that for life insurance. Instead, 80% of corporations provide group liability coverage, but only 16% provide group life insurance.

The predominance of group liability policies, while inconsistent with a pure risk-shifting function, is consistent with a monitoring role for liability insurance. As discussed earlier, when a company purchases a group policy, the insurance company’s fiduciary obligations generally run to the company and not to the individual directors and officers. Thus, for example, when an insurance company refuses coverage under an existing policy because of a director’s dishonesty, it will establish the grounds for its refusal by investigating and documenting the dishonest behavior. If an individual had purchased the policy, the company would have been denied access to the results of this investigation. In addition, with a group policy containing a duty to defend by the insurance company, the company gains access to some of the defense attorney’s investigations. If an individual purchases the policy, the company is denied access to these investigations as well. Thus only by purchasing a group policy can a company obtain investigations of its directors and officers by the insurance company.

4.3 Liability coverage for directors only

Internal investigations of directors potentially lack independence because the board is in effect investigating itself. This problem is less severe with investigations of lower-level employees. For example, theft by a bank teller usually does not imply that the directors of the bank were at fault, nor are the directors (who must authorize any indemnification) jointly liable for judgments against lower-level employees. The availability of relatively independent investigations supervised by the board reduces the value to the firm of the insurance company’s external investigatory services. Consistent with this view of an insurer’s monitoring role, even though lower-level employees are occasionally sued, they are almost uni- versally protected by indemnification alone, whereas directors typically are pro- tected by liability insurance. 47 If liability insurance only shifted risks, this differ- ence in protection would not be observed if the risk preferences of lower-level employees and directors are similar.

470sterle, supra note 8, at 13.

CLIFFORD G. HOLDERNESS

4.4 Event studies of liability insurunce

127

The results of a recent event study support the proposition that liability insurance entails monitoring of boards of directors and top managerial teams.4x Professors Bhagat, Brickley, and Coles wrote to every firm incorporated in New York and listed on either the New York or American Stock Exchange requesting the date when the first public notice that the firm had purchased liability insurance was mailed to stockholders.49 They received 1 I responses classified as “clean” be- cause the information on insurance was contained in proxy statements or other communications that contained no other unusual information about the firms, and 14 additional responses classified as “contaminated” because the communications contained unusual information about the firms.

Using two announcement periods-the month the communication was mailed and that month and the following month-Bhagat, Brickley, and Coles measure stock-price changes for both the clean portfolio of I1 firms and the full portfolio of 25 firms. The studies using the one-month event period yield stock-price re- actions that are positive but only marginally significant.5” Event studies for both portfolios using the two-month announcement period, however, yield stock-price increases that are significant at the 5% level.5’

Although, as the authors note, these findings must be interpreted with caution because of the small sample sizes and because of difficulties in identifying precisely when the information on liability insurance was released, the results are consistent with the proposition that liability insurance involves monitoring services. Because all 25 firms in the study were incorporated in New York, where indemnification is mandatory, it is likely that indemnification agreements were in place when the firms purchased insurance. Moreover, because all of the firms are listed on either the New York or American Stock Exchange, their size should have made indem- nification agreements credible, and their ownership most likely was diffuse. Con- sequently, the stock-price increases could in part reflect the market’s estimation of the value of the external monitoring provided with liability insurance.

4.5 Summary: The evidence und the monitoring hypothesis

Although individual pieces of the data reported above are consistent with several plausible effects of liability insurance, the totality of the evidence supports a monitoring role for insurance companies. Moreover, some of the data would be difficult to understand if liability insurance only shifted risks. For example, it would be difficult to understand why NYSE-listed firms are more likely to carry insurance than privately held firms, and why firms purchase group policies for liability purposes while directors individually insure their lives and health. These empirical regularities, on the other hand, are consistent with the hypothesis that the insurance company provides external monitoring of directors and officers.

4XBhagat, Brickley, and Coles, “Managerial Indemnification and Liability Insurance: The Effect on Shareholder Wealth,” forthcoming, Journul of Risk wd Insurancc~.

“‘They limited their requests to firms incorporated in New York because New York law is unique in requiring that shareholders be notified when a firm purchases liability insurance. NPW York Business Corporute Law $727(d).

>“For the clean portfolio the abnormal return for month 0 is 2.89%. p-value = I I ; for the full portfolio the abnormal return for month 0 is 2.27%, p-value = .19. See Bhagat, Brickley, & Coles, supra note 48 at 19.

c’ For the clean portfolio the two month return is 6.23%. p-value = .02; for the full portfolio the two month return is 4.89%, p-value = .05. Id.

128 Liubility insurers as corporate monitors

5. CONCLUSION

Liability insurance contributes both directly and indirectly to the monitoring of a firm’s board of directors and top managerial team. Although monitoring is not the only effect of liability insurance, it has gone unrecognized as previous analyses have stressed risk shifting and moral hazards.52

When deciding whether to issue a liability policy, the insurance company mon- itors the board and top management by investigating their past actions, by oc- casionally requiring changes in the board, and through the conditions and coverage of the policy itself. When allegations of misconduct arise, the insurance company can through its litigation efforts serve as an independent external investigator of not only the accused official but the entire board and top managerial team. Thus when a director or an officer is protected by insurance purchased by the firm, he is, in effect, agreeing in the eventuality of suit to be investigated by an independent third party-the insurance company. Liability insurance also encourages internal monitoring by making it easier to recruit outside directors, who are usually more effective monitors for shareholders than inside directors. The hypothesis that liability insurance plays a role in the monitoring of directors and officers is con- sistent with the available empirical evidence on the types of organizations that carry the insurance, the prevalence of group over individual policies, the fact that the policies typically cover directors and officers only, and event studies identi- fying stock-price increases associated with initial announcements of liability in- surance purchases.

Such monitoring services will often be valued by shareholders. The insurance company will generally have a comparative advantage in providing these services because they are produced jointly with defense and litigation services. Moreover, the insurance company’s very independence will enable it to conduct a thorough investigation and convey its findings to the decision-makers within the firm who can take remedial action. The insurance company has a dual incentive to provide these monitoring services: they reduce its exposure and they enable it to charge higher premiums.

The analysis in this paper of the monitoring role of liability insurance links two bodies of research. The first concerns the corporate purchase of insurance. Al- though risk-aversion motivates most insurance purchases by individuals, it is unlikely to motivate corporate insurance purchases because shareholders can eliminate insurable risks through diversification. A firm, however, must pay load- ing fees with insurance that represent the excess of premium payments over expected payouts. Corporate insurance would represent a negative-net-present- value project and would thus be unlikely to survive to the extent it does,s3 unless it provided non-risk-shifting benefits. Several such benefits have been identified: lower expected bankruptcy costs, specialized litigation services, the bonding of a firm’s investment decisions, and the monitoring of contract compliance.54 The

5’Dean Clark, for example, writes: “From the point of view of the corporation, the ad- vantages of D&O insurance are twofold. First, the corporation will obtain protection against having to pay out as indemnification more than it considers prudent in any given year. Second, the insurance may enable the corporation to obtain better directors and officers.” Robert Charles Clark, Corporate Law 673-674 (1986).

‘jMayers and Smith, supra note 42 report that corporations spend more on insurance premiums than they pay out in dividends.

54For instance, as a condition of obtaining insurance, ski areas must have their lifts inspected by the insurance company’s safety experts at least once a year. Ski Magazine, March 1986, at 12. Boiler insurance is likewise predicated on periodic inspections by the insurance company. Goldberg, “Tort Liability for Negligent Inspection by Insurers,” 2 Research Law and Economics 65 (1980).

CLIFFORD G. HOLDERNESS 129

external monitoring of boards of directors and top managerial teams is another benefit that helps explain why many risk-neutral corporations purchase insurance.

The second body of research addresses the agency problems between share- holders of diffusely held corporations and their directors. The issue arises: what, sort of a hostile control transaction, encourages directors to act in the share- holders’ best interest. Research has stressed the effects on directors’ reputations, direct monitoring by owners of large-percentage blocks of stock, and incentive compensation. Because the board of directors is in theory the shareholder’s mon- itor of managment, for some firms liability insurance provides a partial answer to the question, Who monitors the monitor?